government pension fund global - bi.no · set exposure to currencies and duration, remove credit....

TRANSCRIPT

GOVERNMENT

PENSION FUND

GLOBALOLE CHRISTIAN BECH-MOEN

CIO ALLOCATION STRATEGIES

CME/CAPR

OSLO, 6. FEBRUARY 2018

20/02/2018

Disclaimer

2

This presentation is intended for general informational purposes only. The

views set out in this presentation are solely those of the author(s) and do not

necessarily reflect the views, position or official policy of the Government of

Norway, Norges Bank or Norges Bank Investment Management. Responsibility

for the information, views and other content set out in the presentation lies

entirely with the author(s). None of the Government of Norway, Norges Bank,

Norges Bank Investment Management or any person acting on their behalf may

be held responsible for the information, views or other content in this

presentation or for the use thereof. Reproduction of this presentation, or any

part thereof, is prohibited.

Return on portfolioUS Dollars

3

-10%

0%

10%

20%

30%

40%

12/2012 12/2013 12/2014 12/2015 12/2016 12/2017

Return on portfolio and reference indexUS Dollars

4

-10%

0%

10%

20%

30%

40%

12/2012 12/2013 12/2014 12/2015 12/2016 12/2017

Sgt

Governance model

Government Pension Act

Management mandate

and ethical guidelines

Reports.

Advice on

investment strategies

Annual white paper.

National budget and accounts

5

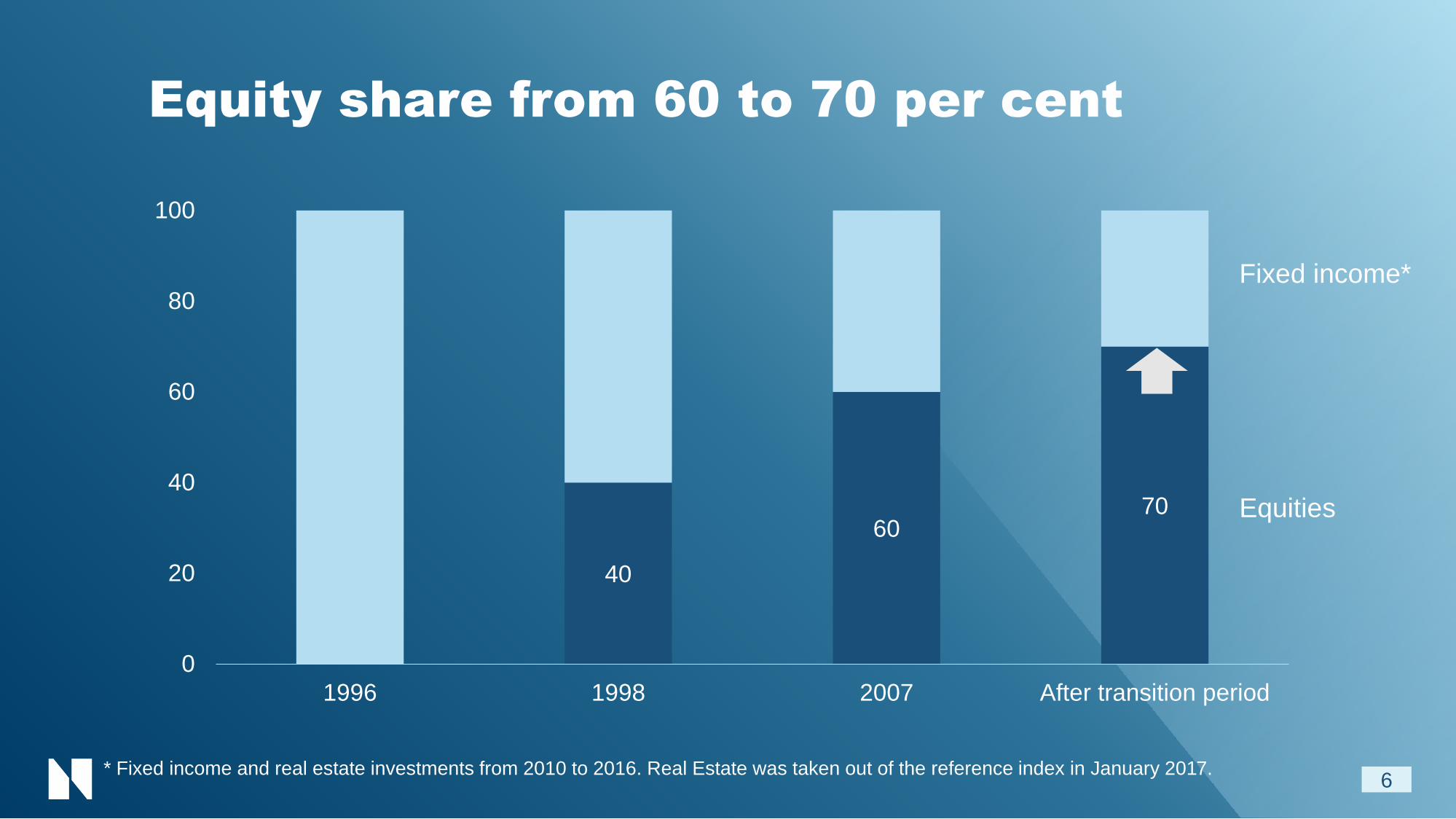

Equity share from 60 to 70 per cent

6

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Fixed income*

Equities

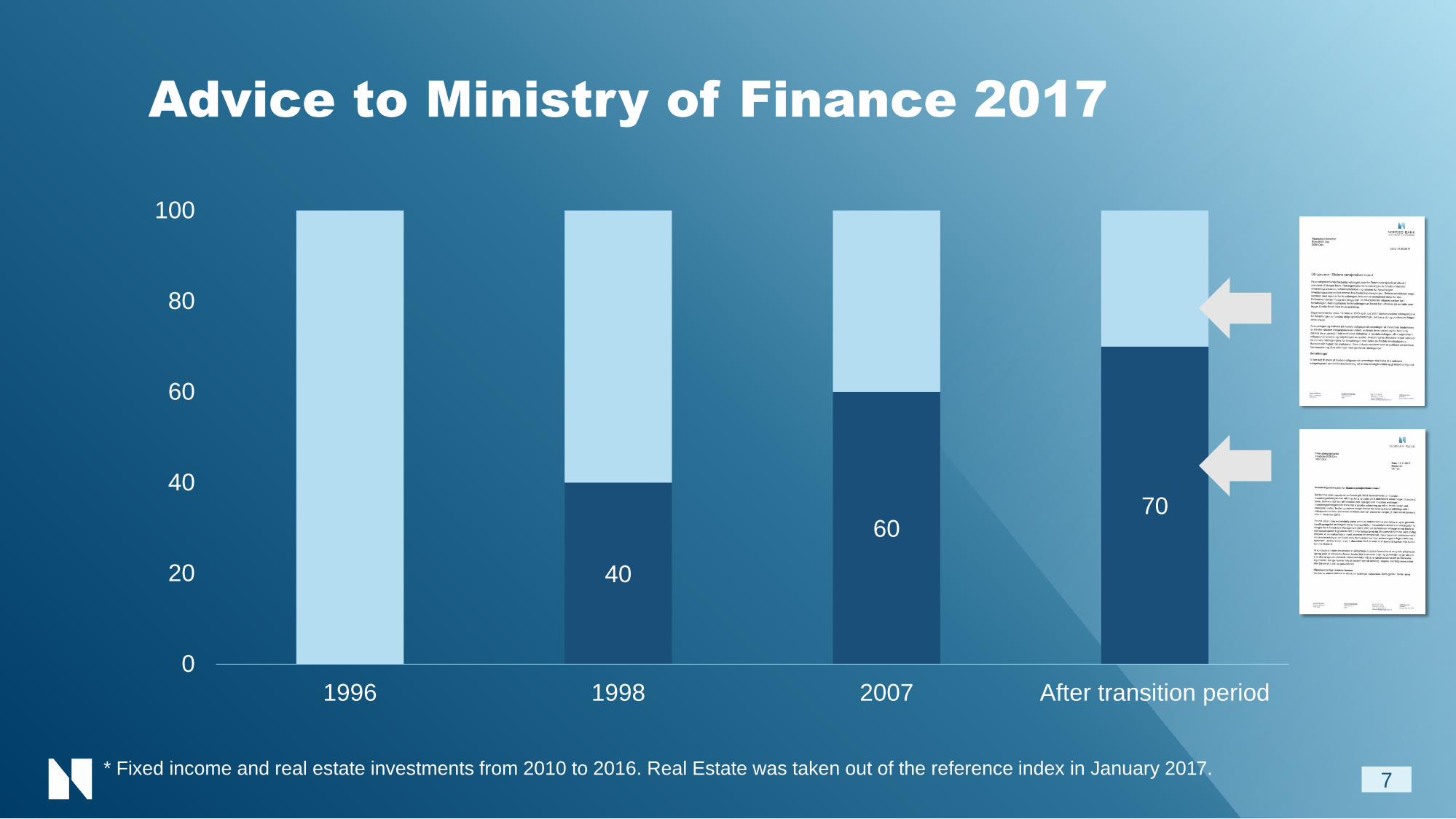

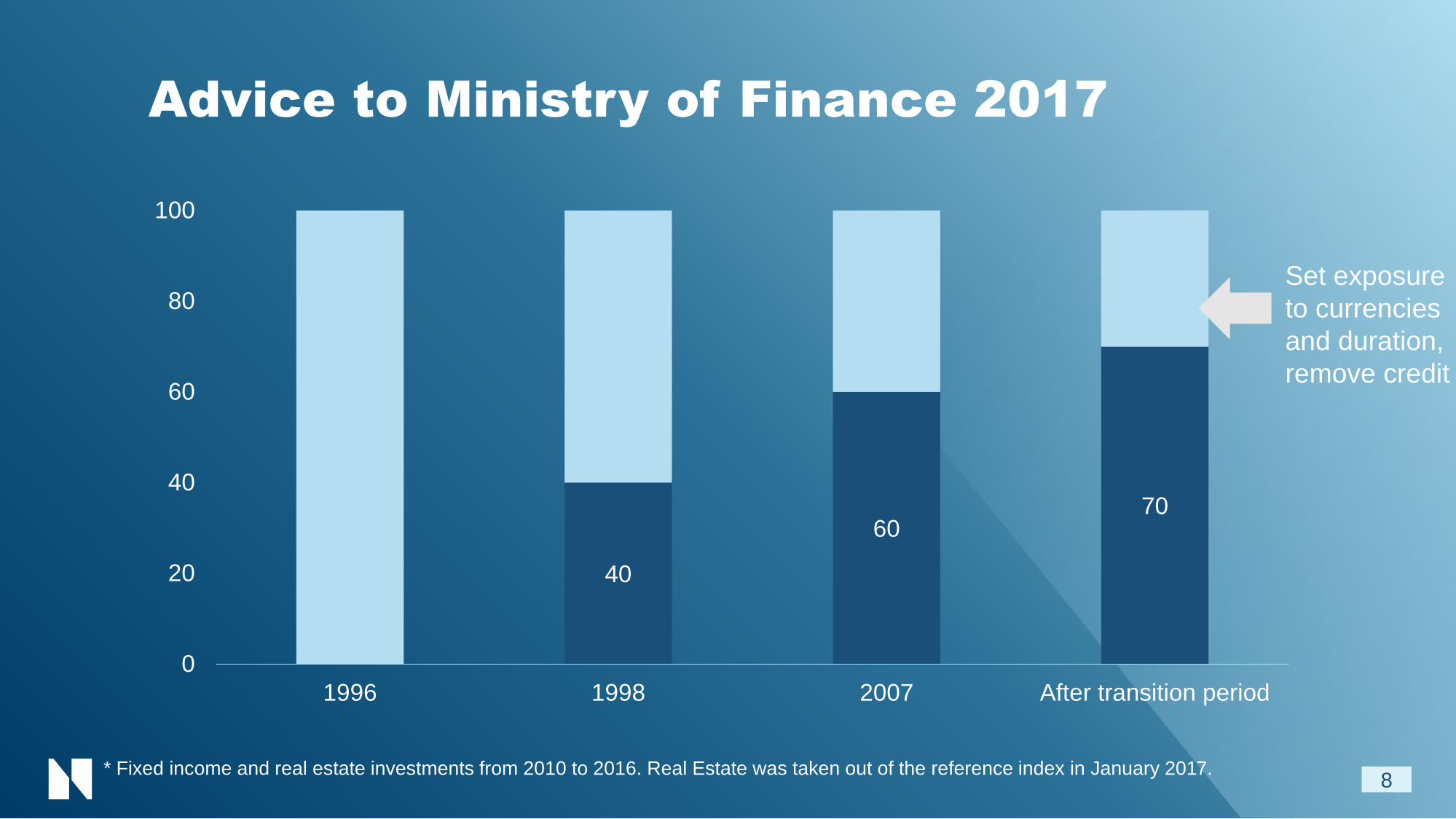

Advice to Ministry of Finance 2017

7

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Advice to Ministry of Finance 2017

8

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Set exposure

to currencies

and duration,

remove credit

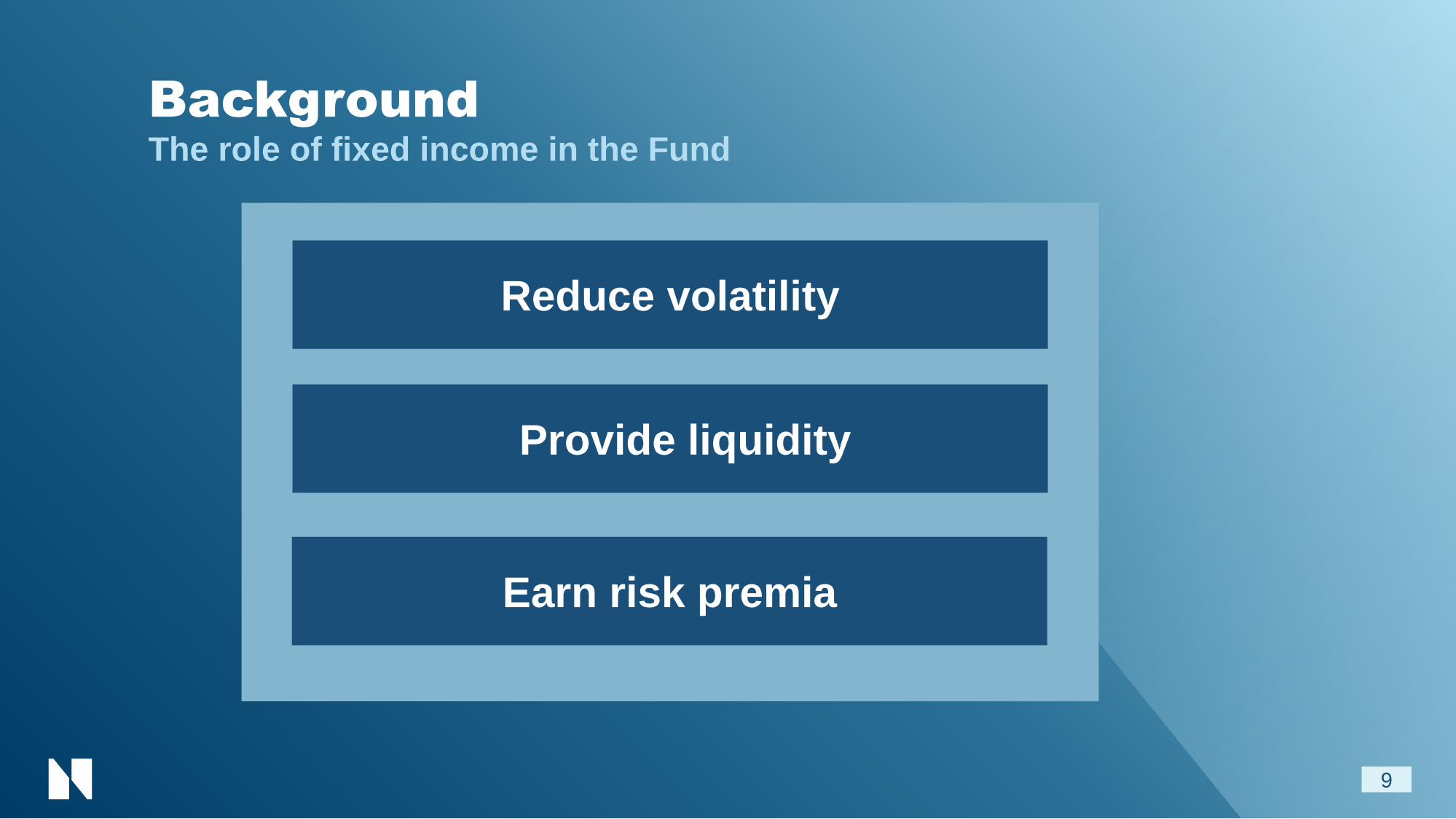

BackgroundThe role of fixed income in the Fund

9

Reduce volatility

Earn risk premia

Provide liquidity

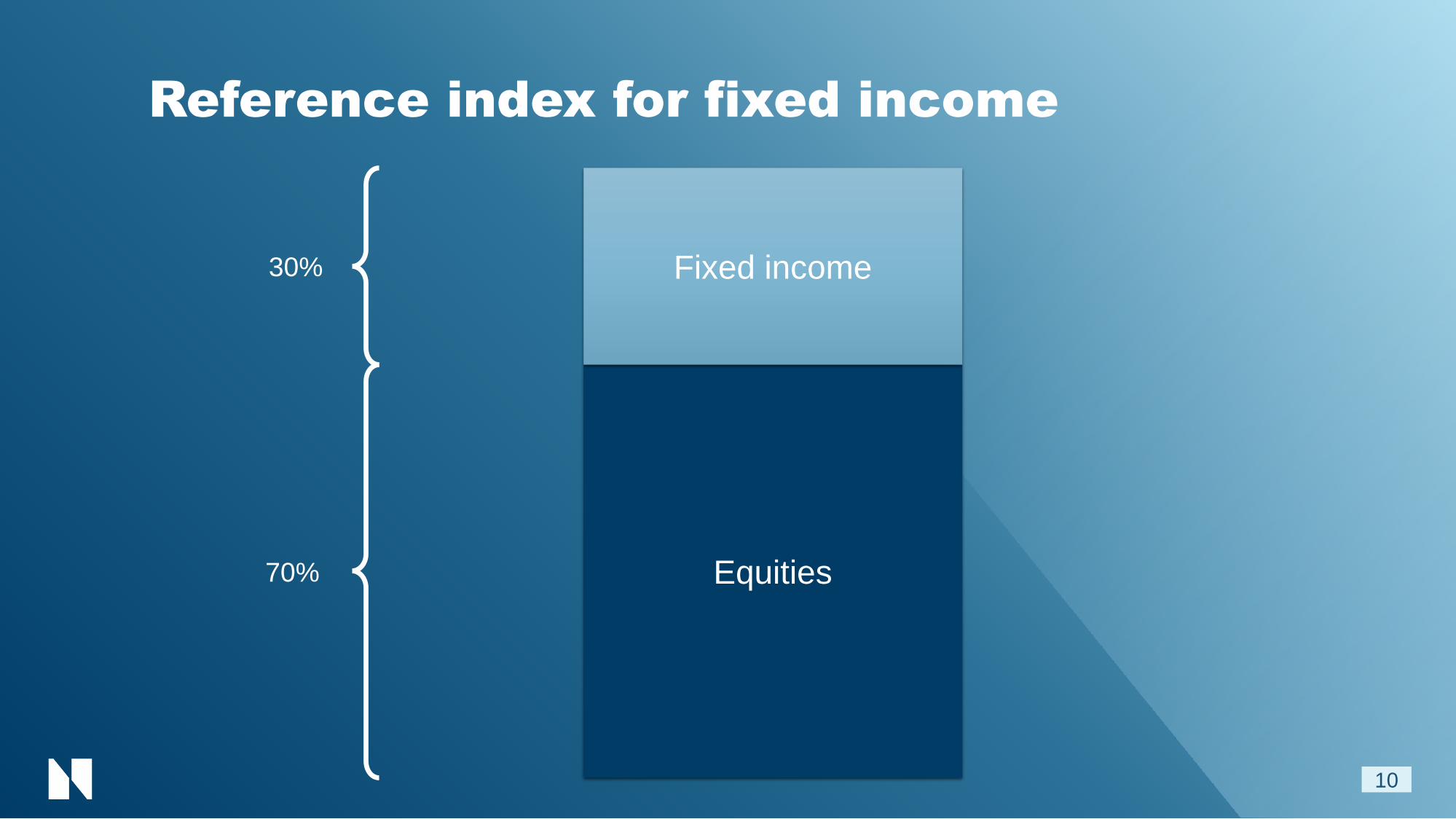

Reference index for fixed income

10

Equities

Fixed income30%

70%

Reference index for fixed income

11

Equities

Government30%

70%

Corporate30%

70%

Reference index for fixed income

12

Equities

Bloomberg GDP Govt

30%

70%

Bloomberg Index-linked

Bloomberg Credit

• Investability factors

• Selected currencies30%

70%

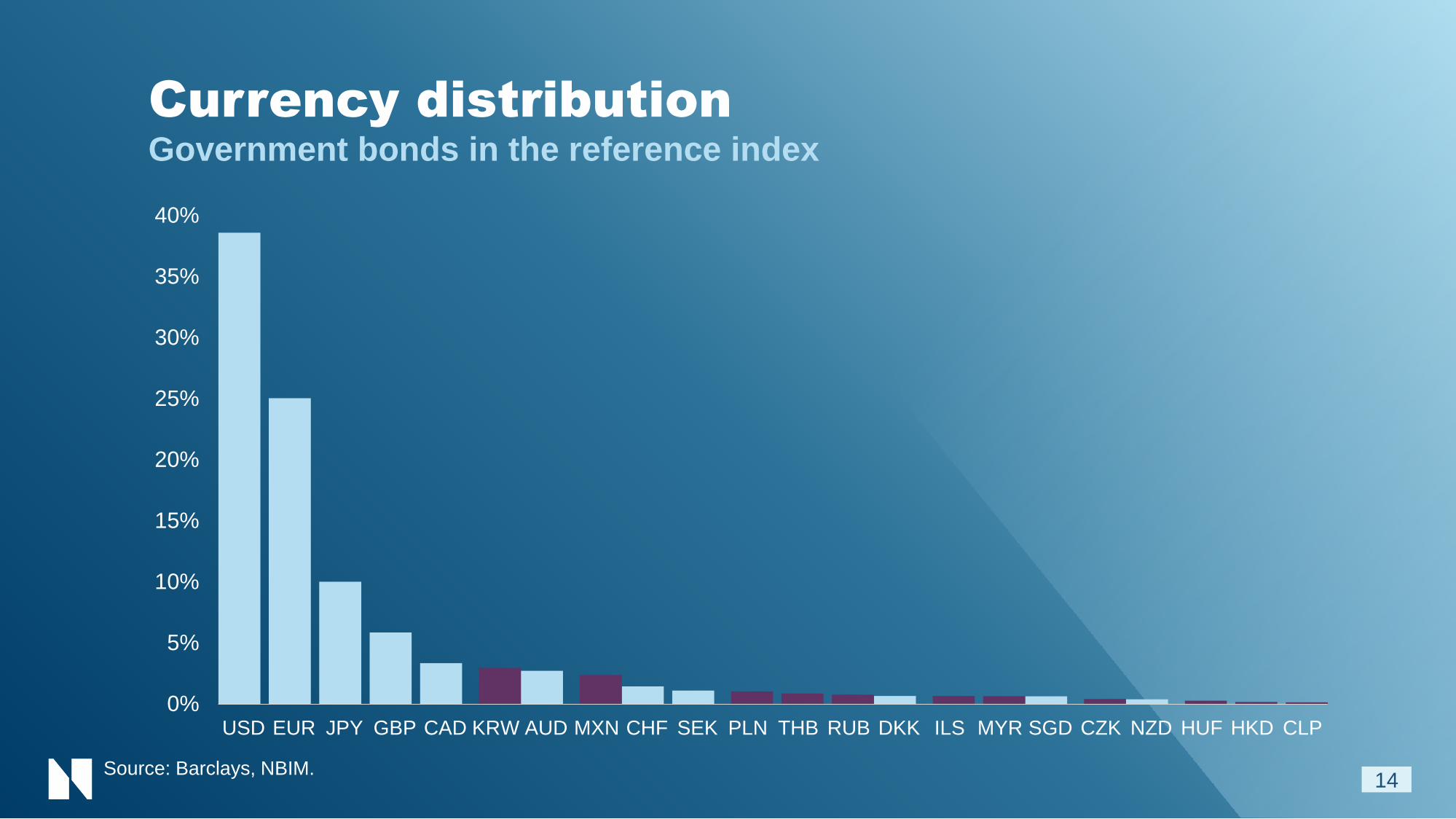

Currency distribution

13

0%

25%

50%

75%

100%

2006 2008 2010 2012 2014 2016

USD EUR GBP JPY Other

Government bonds in the reference index

Source: Barclays, NBIM.

Currency distributionGovernment bonds in the reference index

14

0%

5%

10%

15%

20%

25%

30%

35%

40%

USD EUR JPY GBP CAD KRW AUD MXN CHF SEK PLN THB RUB DKK ILS MYR SGD CZK NZD HUF HKD CLP

Source: Barclays, NBIM.

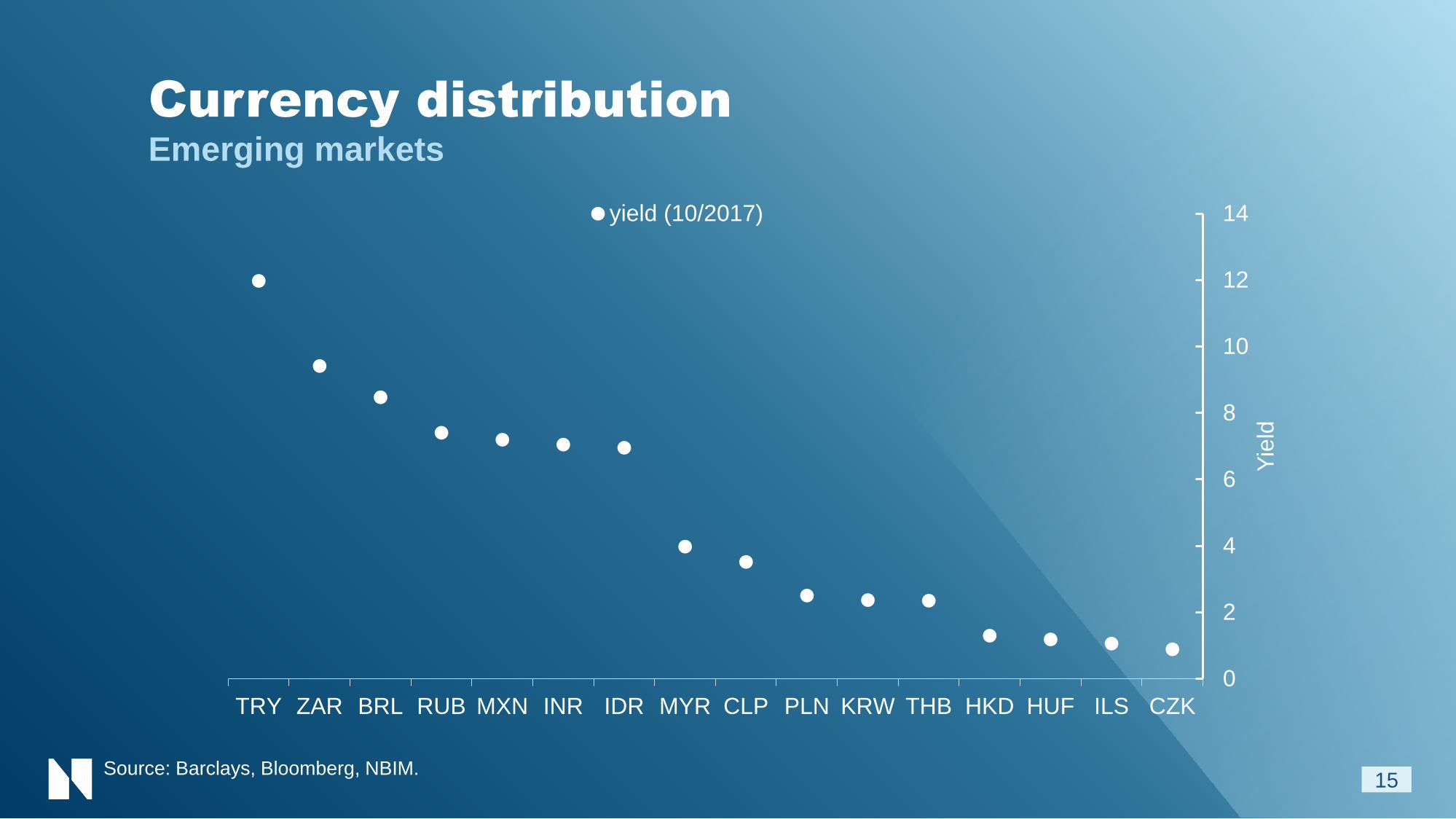

Currency distribution

TRY ZAR BRL RUB MXN INR IDR MYR CLP PLN KRW THB HKD HUF ILS CZK

0

2

4

6

8

10

12

14

Yie

ld

yield (10/2017)

Emerging markets

15Source: Barclays, Bloomberg, NBIM.

Currency distribution

0

2

4

6

8

10

12

14

0

10

20

30

40

50

60

TRY ZAR BRL RUB MXN INR IDR MYR CLP PLN KRW THB HKD HUF ILS CZK

Yie

ld

Bn

NO

K

Current Index yield (10/2017)

Emerging markets

16Source: Barclays, Bloomberg, NBIM.

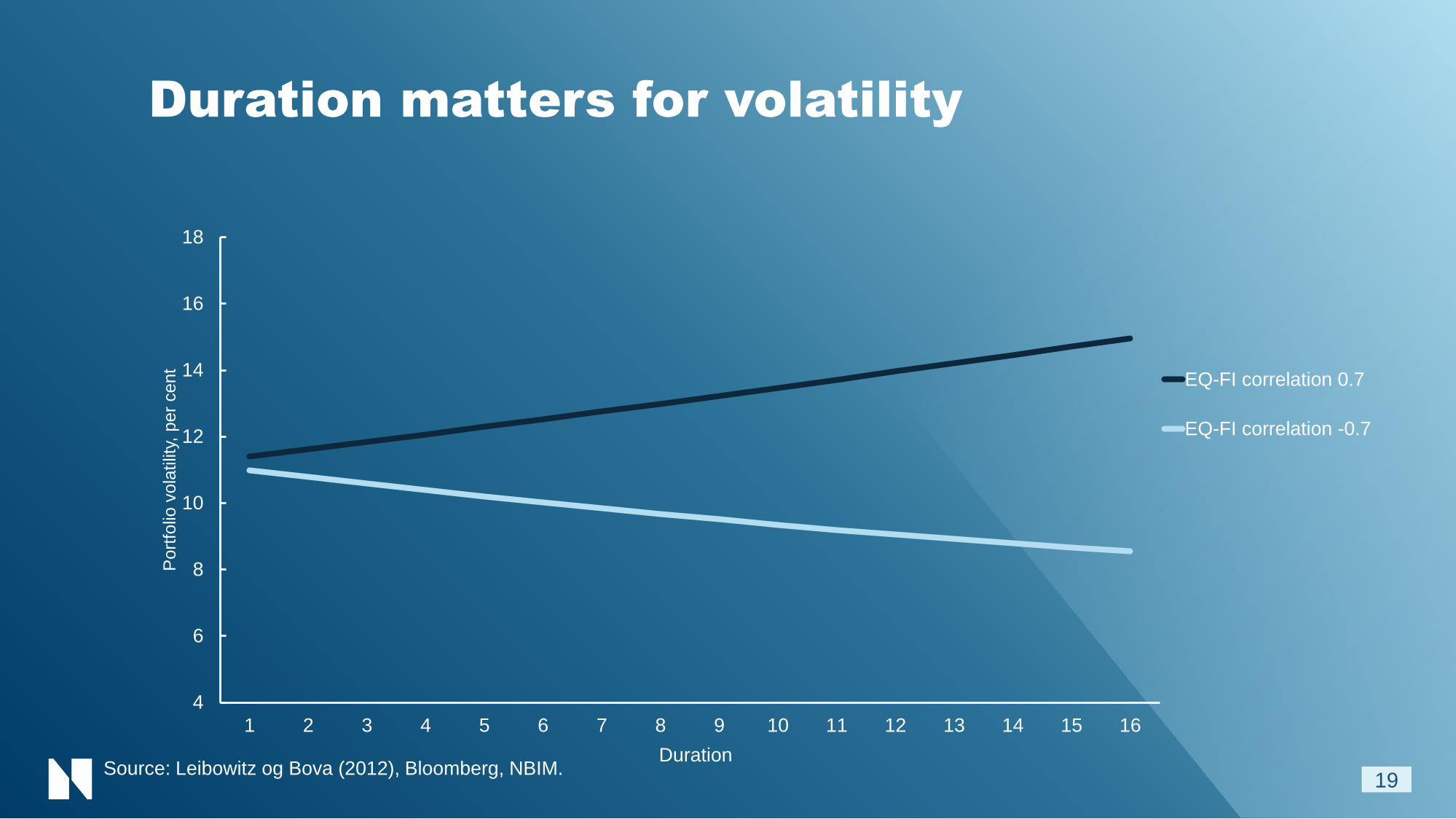

DurationBarclays Global Aggregate – Treasuries

17

4

5

6

7

8

9

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Dura

tion

Source: Barclays, Bloomberg.

4

6

8

10

12

14

16

18

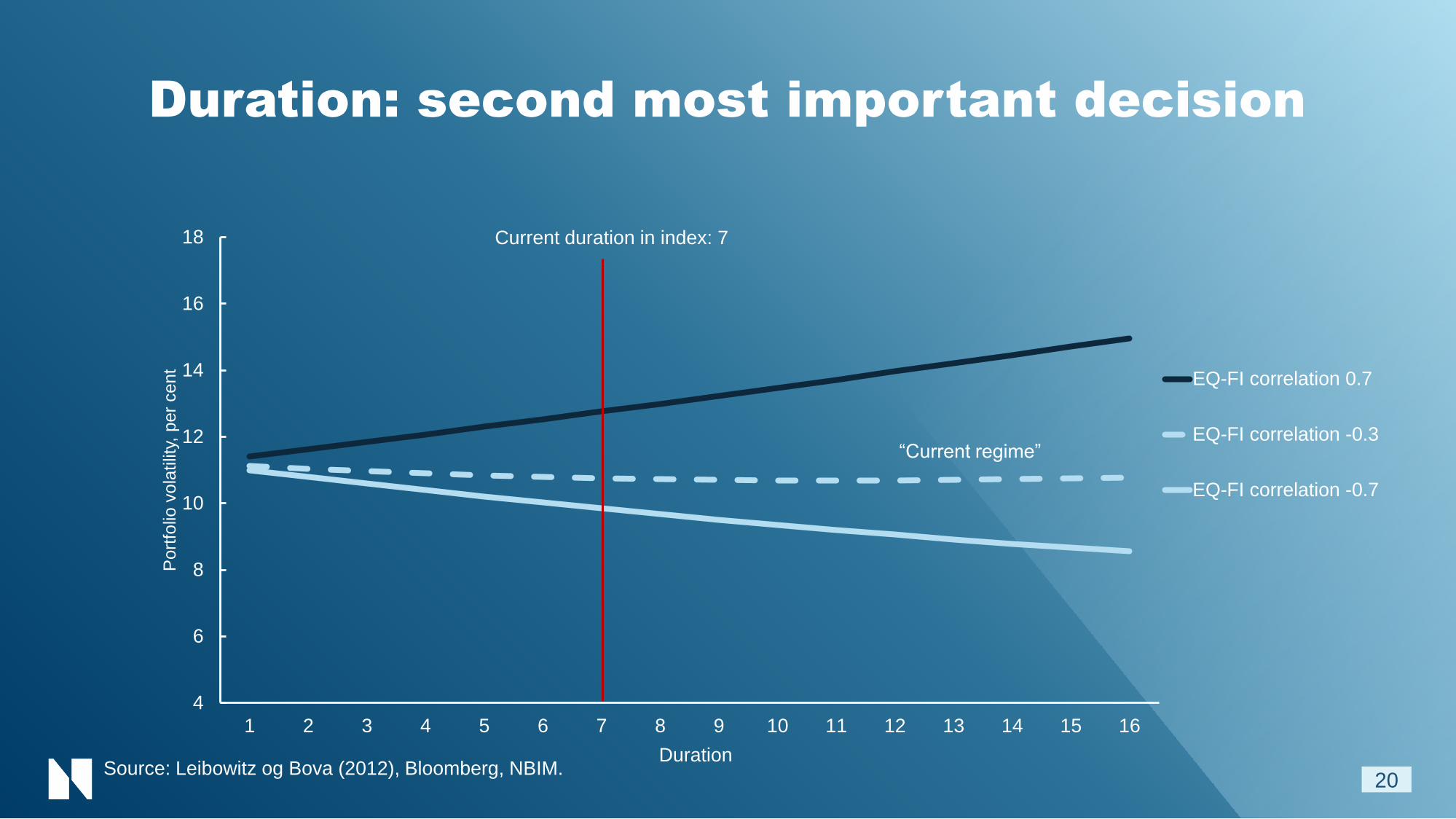

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Port

folio

vola

tilit

y, p

er

cent

EQ-FI correlation 0.7

Duration

Duration matters for volatility

18Source: Leibowitz og Bova (2012), Bloomberg, NBIM.

4

6

8

10

12

14

16

18

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Port

folio

vola

tilit

y, p

er

cent

EQ-FI correlation 0.7

EQ-FI correlation -0.7

Duration

Duration matters for volatility

19Source: Leibowitz og Bova (2012), Bloomberg, NBIM.

4

6

8

10

12

14

16

18

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Port

folio

vola

tilit

y, p

er

cent

EQ-FI correlation 0.7

EQ-FI correlation -0.3

EQ-FI correlation -0.7

Duration

Duration: second most important decision

20

Current duration in index: 7

“Current regime”

Source: Leibowitz og Bova (2012), Bloomberg, NBIM.

Credit qualityBarclays Global Aggregate – Corporates

21

8% 7%1%

28%24%

9%

42%44%

41%

22% 25%

49%

0%

20%

40%

60%

80%

100%

12/31/1999 12/31/2005 12/31/2017

Baa

A

Aa

Aaa

Source: Barclays, Bloomberg.

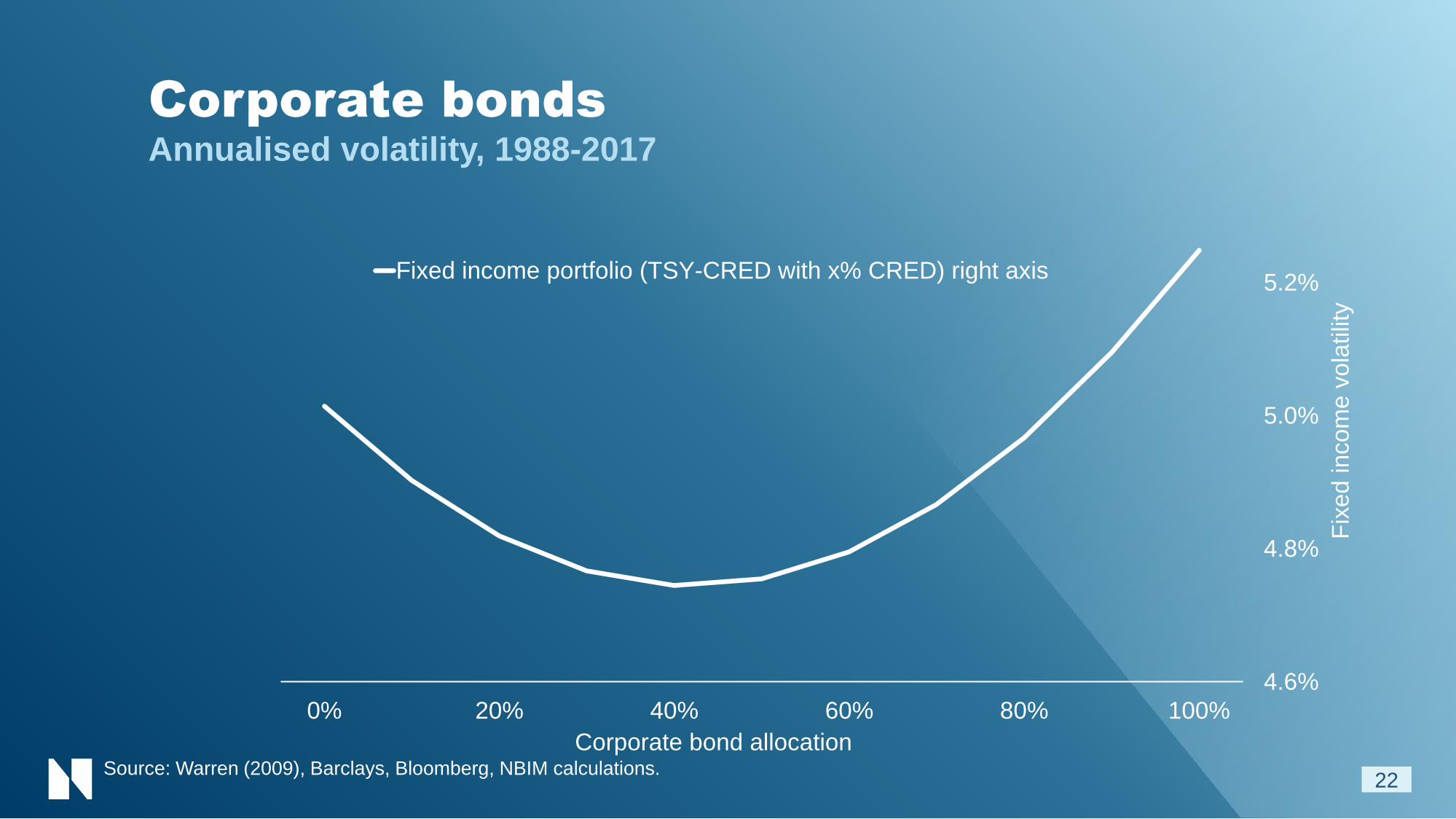

Corporate bondsAnnualised volatility, 1988-2017

22

4.6%

4.8%

5.0%

5.2%

0% 20% 40% 60% 80% 100%

Fix

ed

incom

e v

ola

tilit

y

Corporate bond allocation

Fixed income portfolio (TSY-CRED with x% CRED) right axis

Source: Warren (2009), Barclays, Bloomberg, NBIM calculations.

Corporate bondsAnnualised volatility, 1988-2017

23

4.6%

4.8%

5.0%

5.2%

10.0%

10.2%

10.4%

10.6%

0% 20% 40% 60% 80% 100%

Fix

ed

incom

e v

ola

tilit

y

Multi-asse

t vola

tilit

y

Corporate bond allocation

Multi-asset portfolio (70/30 EQ-FI with x% CRED in FI) left axis

Fixed income portfolio (TSY-CRED with x% CRED) right axis

Source: Warren (2009), Barclays, Bloomberg, NBIM calculations.

Advice to Ministry of Finance 2017

24

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Set exposure

to currencies

and duration,

remove credit

Advice to Ministry of Finance 2017

25

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Remove oil &

gas stocks

BackgroundNBIM’s strategy plan 2017 – 2019

26

Reference index for equities

27

FTSE Global All-Cap

Fixed income30%

70%• Regional factors

• Exclusions

0

2,000

4,000

6,000

8,000

10,000

2006 2017

Value of oil and gas in the ground Fund`s value

The fund makes up 2/3 of petroleum wealth

28All numbers NOK bn.

Source: Ministry of Finance, NBIM

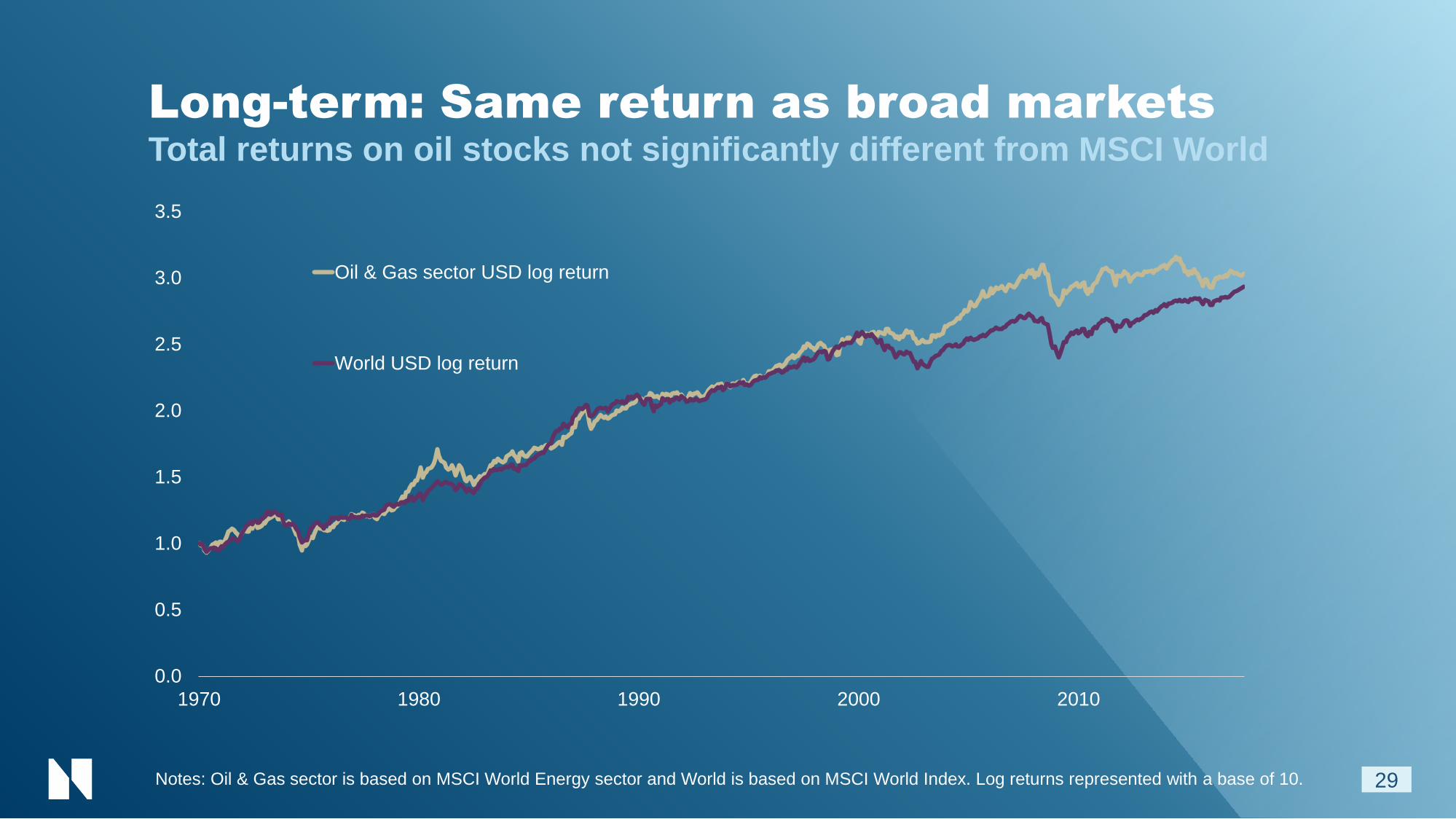

Long-term: Same return as broad marketsTotal returns on oil stocks not significantly different from MSCI World

29Notes: Oil & Gas sector is based on MSCI World Energy sector and World is based on MSCI World Index. Log returns represented with a base of 10.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1970 1980 1990 2000 2010

Oil & Gas sector USD log return

World USD log return

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1970 1980 1990 2000 2010

Oil & Gas sector USD log return

World USD log return

Oil & Gas sector relative USD returns

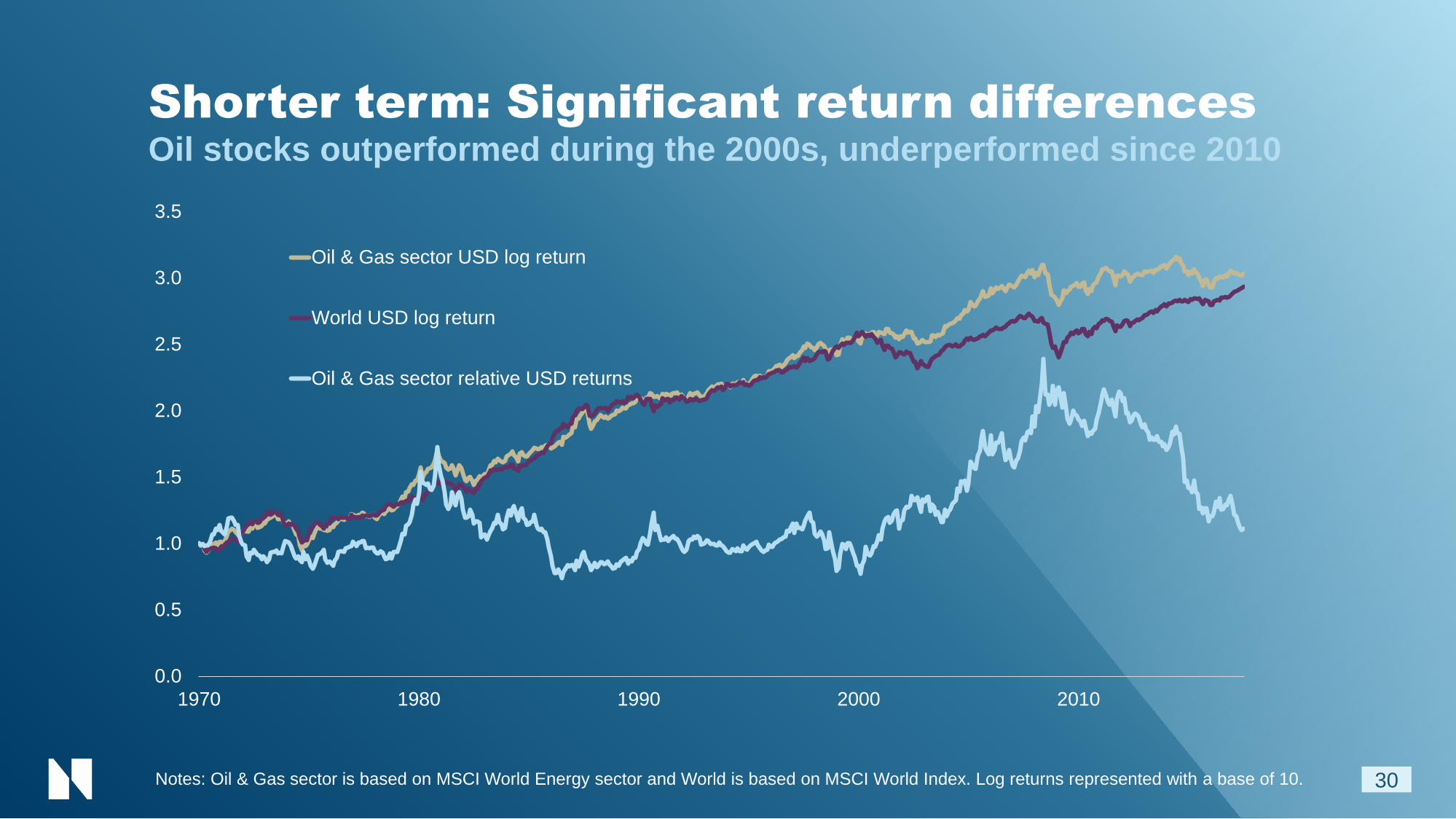

Shorter term: Significant return differencesOil stocks outperformed during the 2000s, underperformed since 2010

30Notes: Oil & Gas sector is based on MSCI World Energy sector and World is based on MSCI World Index. Log returns represented with a base of 10.

Return differentials driven by oil price… Investing in oil stocks add oil price risk

31

-40

0

40

80

120

160

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1970 1980 1990 2000 2010

Oil & Gas sector USD log return

World USD log return

Oil & Gas sector relative USD returns

Oil price (WTI, RHS)

Notes: Oil & Gas sector is based on MSCI World Energy sector and World is based on MSCI World Index. Log returns represented with a base of 10.

…also longer term10-year returns relative to equity market vs. 10-year change in real oil price

32

-10%

0%

10%

20%

-5%

0%

5%

10%

15%

1979 1984 1989 1994 1999 2004 2009 2014

Oil & gas sector - Equity market Oil price (rhs)

Equity market refers to MSCI World, Oil & Gas to MSCI World Energy sector, Oil price refers to spot WTI price deflated using the U.S. CPI for all urban

consumers, all series are measured in USD

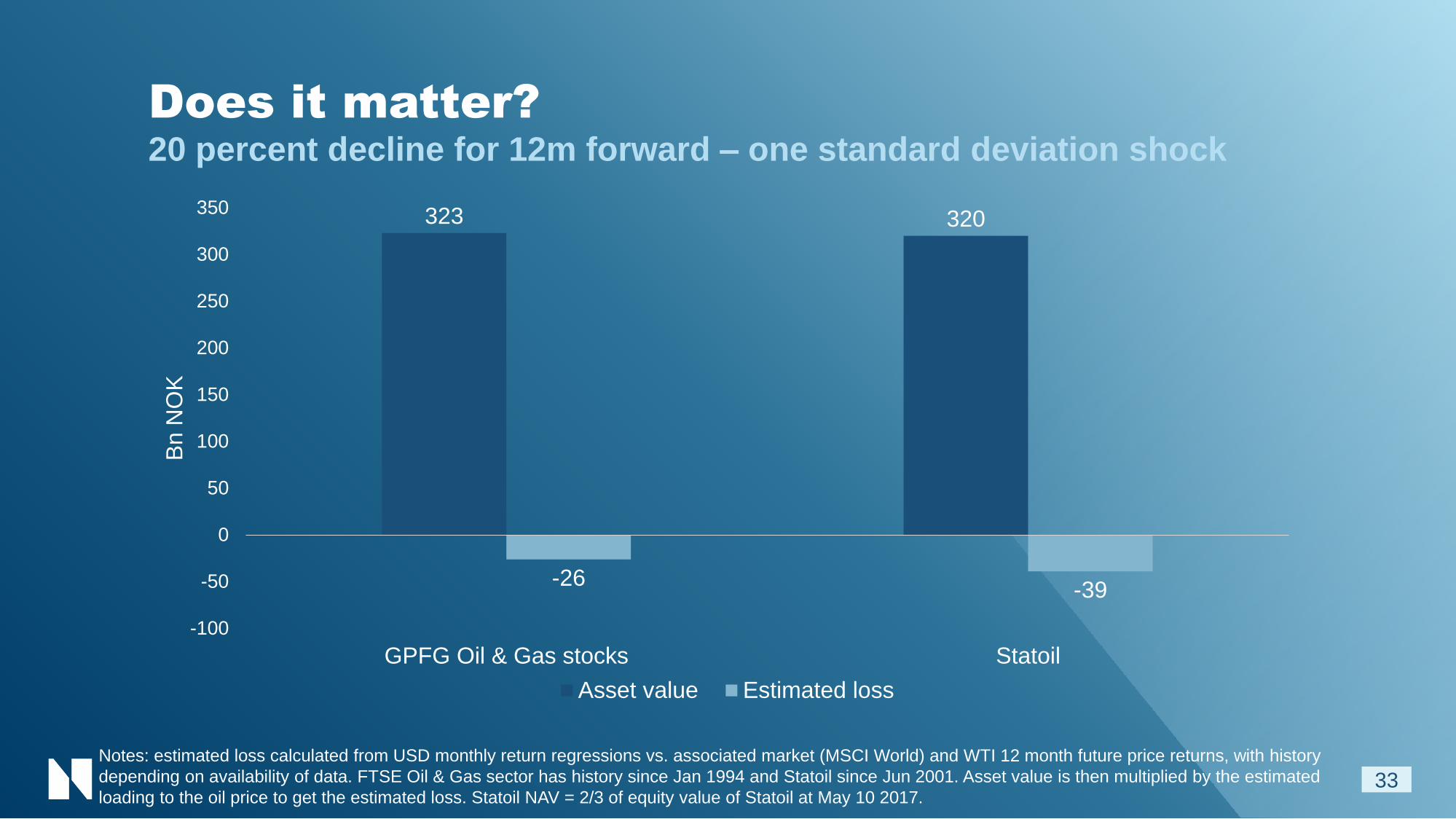

Does it matter?20 percent decline for 12m forward – one standard deviation shock

33

323 320

-26-39

-100

-50

0

50

100

150

200

250

300

350

GPFG Oil & Gas stocks Statoil

Bn N

OK

Asset value Estimated loss

Notes: estimated loss calculated from USD monthly return regressions vs. associated market (MSCI World) and WTI 12 month future price returns, with history

depending on availability of data. FTSE Oil & Gas sector has history since Jan 1994 and Statoil since Jun 2001. Asset value is then multiplied by the estimated

loading to the oil price to get the estimated loss. Statoil NAV = 2/3 of equity value of Statoil at May 10 2017.

Advice to Ministry of Finance 2017

34

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

Remove oil &

gas stocks

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Forthcoming advice to Ministry of Finance

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

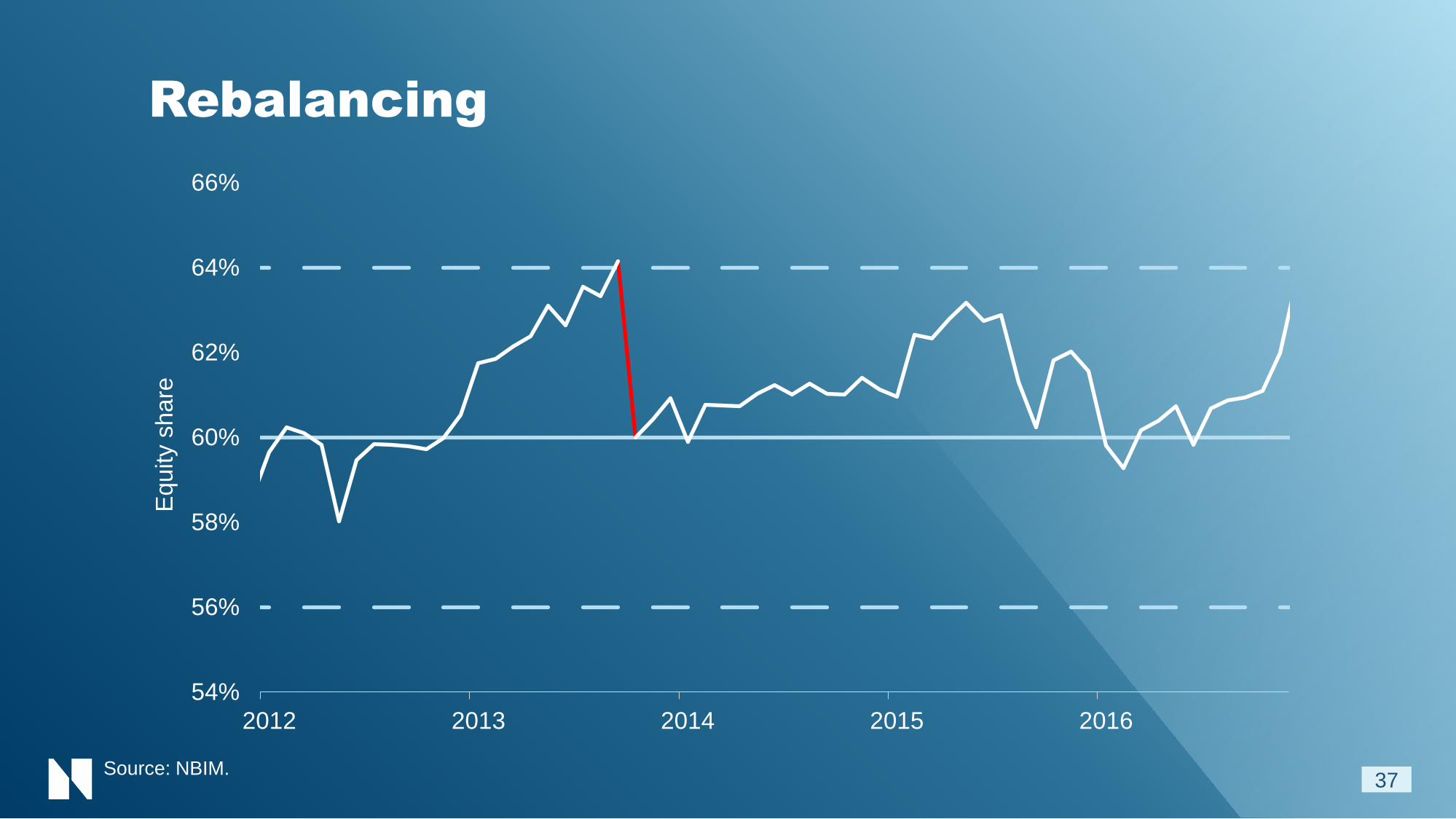

Rebalancing

35* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Rebalancing

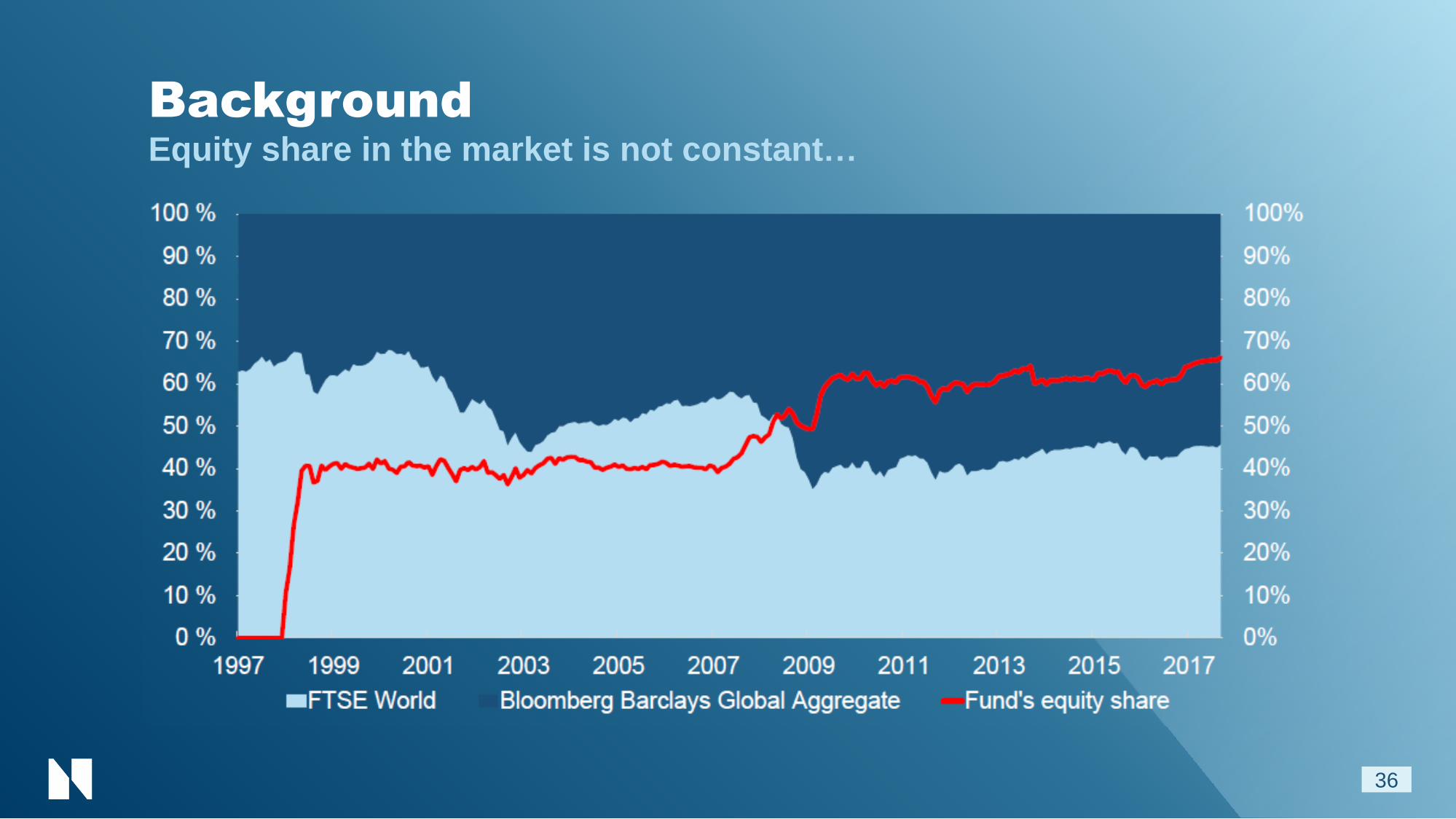

BackgroundEquity share in the market is not constant…

36

Rebalancing

37

54%

56%

58%

60%

62%

64%

66%

2012 2013 2014 2015 2016

Equ

ity s

ha

re

Source: NBIM.

Summary

38

40

6070

0

20

40

60

80

100

1996 1998 2007 After transition period

* Fixed income and real estate investments from 2010 to 2016. Real Estate was taken out of the reference index in January 2017.

Remove oil &

gas stocks

Set exposure

to currencies

and duration,

remove creditRebalancing

Reference indexAs just described

39

Equities

Fixed income

Reference portfolioUniverse expansion, improved rules, systematic exposures, requirements

40

Equities

Fixed income

Investing in Real EstateWe need to sell assets to finance new investments

41

Equities

Real estate

Fixed income

Equities

Fixed income

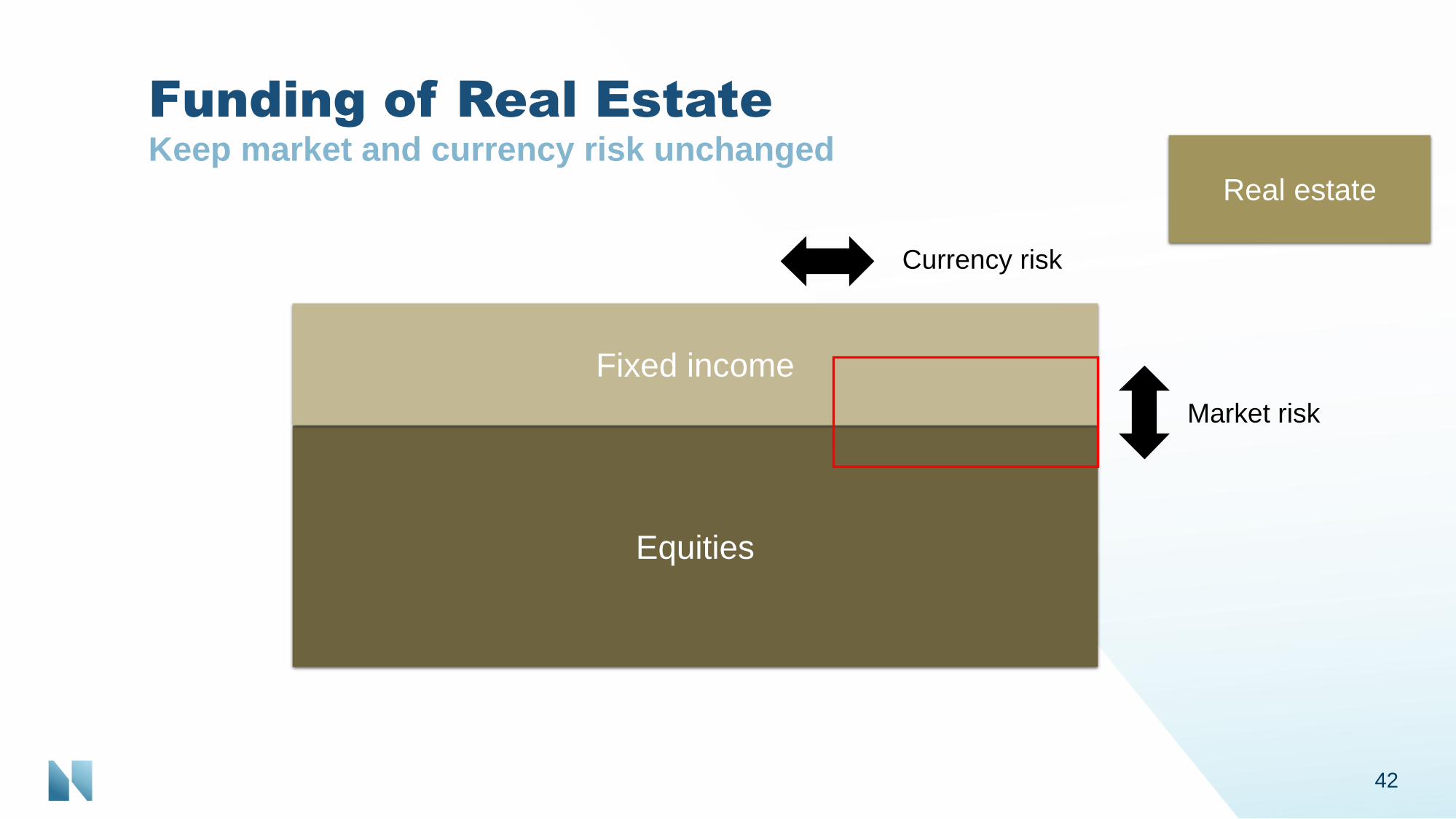

Funding of Real EstateKeep market and currency risk unchanged

42

Market risk

Currency risk

Real estate

Example: funding of Regent’s Street

43

Equities

Fixed income

Real estate

Equities

Fixed income

Real Estate returnWe report the return on the investments versus the funding

44

Equities

Fixed income

Real estate

Return on portfolio and reference indexUS Dollars

45

-10%

0%

10%

20%

30%

40%

12/2012 12/2013 12/2014 12/2015 12/2016 12/2017

Discussion Notes 2017Background for reference index advice

46

Summary

47

Advice

• Equity share

• Currency composition, duration, credit and petroleum wealth

• Rebalancing

Implementation

• Reference portfolio

• Real Estate funding