grasim industries limited _nov2015.pdf– market leader in white cement & putty (1.4 mn. tpa)...

TRANSCRIPT

Grasim Industries Limited

A VSF and Cement Major

November 2015

2

Statements in this ‘Presentation’ describing the Company’s objectives, estimates, expectations or predictions may be ‘forward looking statements’ within

the meaning of applicable securities laws and regulations. Actual results could differ materially from those expressed or implied. Important factors that

could make a difference to the Company’s operations include global and Indian demand supply conditions, finished goods prices, feedstock availability and

prices, cyclical demand and pricing in the Company’s principal markets, changes in Government regulations, tax regimes, economic developments within

India and the countries within which the Company conducts business and other factors such as litigation and labour negotiations. The Company assumes

no responsibility to publicly amend, modify or revise any forward looking statement, on the basis of any subsequent development, information or events,

or otherwise.

Cautionary Statement

Glossary VSF : Viscose Staple Fiber, MT : Metric Ton, TPA : Tons Per Annum, YoY: Year on Year Comparison, CY : Current Year

EBITDA : Earnings before Interest, Tax, Depreciation and Amortisation,

ROAvCE : Return on Avg. Capital Employed, RONW : Return on Avg. Net Worth

3

Presentation Structure

Introduction

Financial Highlights

Capex

Our Businesses

4

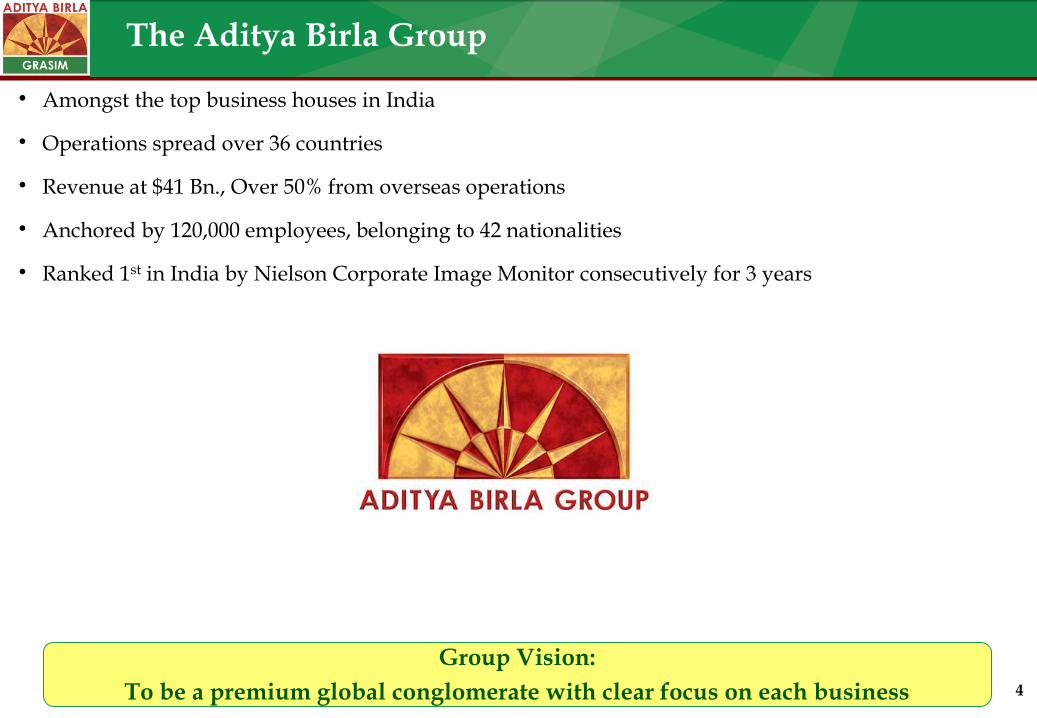

Amongst the top business houses in India

Operations spread over 36 countries

Revenue at $41 Bn., Over 50% from overseas operations

Anchored by 120,000 employees, belonging to 42 nationalities

Ranked 1st in India by Nielson Corporate Image Monitor consecutively for 3 years

The Aditya Birla Group

Group Vision:

To be a premium global conglomerate with clear focus on each business

5

The Aditya Birla Group : Leadership Across Businesses

Leading Global Player

– Hindalco – Novelis is the largest aluminum rolling company

– Largest producer of carbon black

– One of the two largest producers of VSF

– Fourth-largest producer of insulators and acrylic fibre

Leadership position in India

– VSF, Cement, Aluminium, Carbon Black, VFY, Branded Apparels, Linen, Copper,

Chlor-alkali and Insulators

– Among top three mobile telephony companies

– Among top four in Asset Management

– Among top six in Life Insurance (Private players)

6

Grasim: Market leader across Business Segments

Cement Revenue ` 244 Bn.

(US$ 4.0 Bn.)

Largest manufacturer in India

– Capacity : 67.7 Mn. TPA

– Total capacity to reach ~75 Mn. TPA on completion of ongoing Brownfield expansion projects and acquisition in process

– Market leader in White Cement & Putty (1.4 Mn. TPA) and Ready Mix Concrete

Viscose Staple Fibre

Revenue ` 66 Bn. (US$ 1.1 Bn.)

Leading Global Player

– Capacity : 498K TPA

– Grasim commands 9% Global share; ABG share 17%

– Integrated model with experience of more than six decades

Chemical Revenue ` 17 Bn.

(US$ 278 Mn.)

Largest Chlor-Alkali Manufacturer in India

– Capacity : 452K TPA

– Post merger of ABCIL, capacity to reach 804K TPA

– Portfolio of value added products – Epoxy (52K TPA) and Chlorine Derivatives (243K TPA)

7

Investment in Growth

Consolidated Financials.

– Capital Employed ` 471 Bn.

– Net Debt at ` 59 Bn. (Net surplus of ` 3.1 Bn. at standalone level)

– Net Debt / Equity : 0.18

– Net Debt / EBITDA : 0.98

H1 FY16 Return Ratio (consolidated) :

– ROAvCE : 10.0%, RONW : 8.2%

Substantial Investment made across Businesses – US$ 4 Bn. over last five years.....

.....Balance Sheet Continues to be Strong – Net worth of ~ US$ 4 Bn.

Full Benefit to flow with ramping up of capacity utilisations and expected upturn in business cycle

48.8 63.2 69.3

FY 10 FY 15 FY 16

Cement * Mn. TPA

74.8#

FY 10 FY 15

334 498

FY 10 FY 15

VSF * KTPA

50%

258 452

804

FY 10 FY 15 FY 16

Caustic * KTPA

75%

30%

Gross Fixed Asset Rs. Cr

110%

21717

45577

* Capacity

Leading Global Player Largest in India Largest in India

310%

55%

# Post acquisition of JAL’s MP assets

8

Driving Robust Volume Growth

.....and Revenue Growth

……Yielding Results

7

308 305 307

336

367

403

FY10 FY11 FY12 FY13 FY14 FY15

VSF ('000)

230 241 266 269

314

409

FY10 FY11 FY12 FY13 FY14 FY15

Caustic ('000)

39.6 41.6

44.0 43.6 44.7

48.2

FY10 FY11 FY12 FY13 FY14 FY15

Cement (Mn. Tons)

39.4

48.2 50.1 54.3

63.3 66.4

FY10 FY11 FY12 FY13 FY14 FY15

VSF

4.9 5.4 7.8

9.5 10.7

17.0

FY10 FY11 FY12 FY13 FY14 FY15

Caustic Soda

154.7 159.4

192.3

213.2 216.5

243.5

FY10 FY11 FY12 FY13 FY14 FY15

Cement

` Bn.

9

Consolidated Business Mix – H1 FY16

Net Revenue - ` 170 Bn. EBITDA - ` 30 Bn.

124.4

26.9

8.3 10.1

0.2

23.9

3.5

1.9

0.9

10

Presentation Structure

Introduction

Our Businesses

Financial Highlights

Capex

Viscose Staple Fibre (VSF)

Birla Viscose Birla Modal Birla Excel

12

58%

18%

17%

Cotton 26%

VSF 5%

Synthetic 67%

Wool 1%

Others 1%

VSF: A cellulosic fibre

5% of global fibre market

7% of global man-made fibre market

Major Global Players’ Capacity

ABG group (incl. Grasim) : 935

of which Grasim : 498

Lenzing : 992

(Austria, Indonesia & China)

Niche business where Grasim has relative cost

advantage due to backward integration and long

experience

VSF Global Industry Scenario

‘000 TPA

Global Fibre Pie (92 Mn. MT)

Source: Company estimate, Fibre Organon (for CY 2014)

Chinese Players

Lenzing

ABG Group

Grasim 9% Others 7%

VSF Business Global Market Share

13

3.5

5.5

2.7

4.8

2009 2014

VSF : Fastest Growing Fibre

22.2

26.2 25.3 24.4

8.6

21.9

2009-10 2014-15 Production Consumption

Season End Stock

17.0

24.5

12.6 15.5

2009 2014

VSF PSF Cotton (Mn. Ton)

VSF fastest growing among competing fibres

– Rising prosperity in emerging economies

– High cotton prices in China lead to substitution

Overcapacity across Fibres leading to pressure on prices

Source : ICAC, Fibre Organon, Company Estimates

Capacity Demand

CAGR -1%

14

VSF: Global Presence

• 4 VSF plants

• 1 Pulp plant

• 2 Caustic soda

plants

India

• 3 Pulp plants

JVs

Canada

• 2 VSF plants of AVB

Group Cos.

South East Asia

VSF Plant - Own

VSF Plant - JV

VSF Plant - Group Co.

Pulp Plant - Own

Pulp Plant - JV

• VSF JV

China,Hubei

• Domsjo pulp plant

JV

Sweden

15

VSF : Sustainable Competitive Strengths

Amongst the low cost producers globally

Highly integrated operations

Captive raw materials - Pulp & Caustic Soda

Five pulp manufacturing plants – India : 1, Overseas JVs : 4 (Canada : 3, Sweden : 1)

Captive power and steam

Self managed water supply resources

In-house R&D capabilities

Global brand positioning :“Birla Cellulose”

Our Integrated Business Model will continue to provide Sustainable Competitive Advantage

16

(` Bn.) 2013-14 2014-15 H1

2015-16

Capacity (‘000 Ton)* 375 434 249

Sales Volume (‘000 MT) 367 403 216

Net Revenue 47.1 49.7 26.9

EBIDTA 7.2 4.7 3.5

EBIDTA Margin 15% 9% 13%

EBIT 5.7 3.1 2.4

VSF: H1 FY16 Performance

Global Industry Scenario

Increase in global prices in H1 FY16 after prolonged decline

Rise in raw material cost and stoppage of few plants in China for environmental issues and maintenance

Business performance

Sales volume up by 16% with ramping up of Vilayat plant

Achieved 100% utilisation in Q2

Business development activities coupled with LIVA brand launch supported increase in domestic volumes

Standalone EBITDA increased by 51% YoY

Higher volumes

Improved margins from 9% to 13%

o Lower pulp and other input cost

o Operational efficiency gains

* Effective capacity for the period

17

Sep

- 1

5 0.7

0.9 1.1 1.3 1.5 1.7 1.9 2.1 2.3

Ap

r-1

3

Jun

-13

A

ug-

13

O

ct-1

3

Dec

-13

Fe

b-1

4

Ap

r-1

4

Jun

-14

A

ug-

14

O

ct-1

4

Dec

-14

Fe

b-1

5

Ap

r-1

5

Jun

-15

A

ug-

15

International Fibre Prices

VSF continues to hold favorable position in comparison to other

fibres

Preference for comfort fabric leading to increase in demand for high

quality cellulosic fibre

Rising population and increasing prosperity in developing

economies

Prices likely to be influenced by

Development in China - Resumption of operations of shut capacities

Competing fibre prices trend

Developments in the down stream industry

Concerted market and product development activities for demand

expansion in domestic segment

Liva brand to improve usage of VSF products

Continued focus on improving quality and share of specialty

products

VSF: Outlook

1.52

0.94

1.90

Grey VSF Cotton PSF

$/ Kg

18

Chemical

Largest Chlor-Alkali manufacturer in India

Largest producer of Epoxy Resins in India

Largest value-added product portfolio including water

treatment chemicals

19

Business Performance

Revenue up by 21%

Epoxy volumes up by 78% with product

approvals from major customers in place

Vilayat Caustic plant achieved ~96% capacity

utilisation for the period

EBITDA up by 10% at ` 1.9 bn.

Increase in volume

Healthy EBITDA margin

Chemical Business : H1 FY16 Performance

(` Bn.) 2013-14 2014-15 H1

2015-16

Capacity (000’ Ton)* 352 452 226

Sales Volume Caustic Soda (‘000 MT)

314 409 220

Net Revenue 10.7 17.0 10.1

EBIDTA 2.3 2.9 1.9

EBIDTA Margin 21% 18% 18%

EBIT 1.6 2.0 1.4

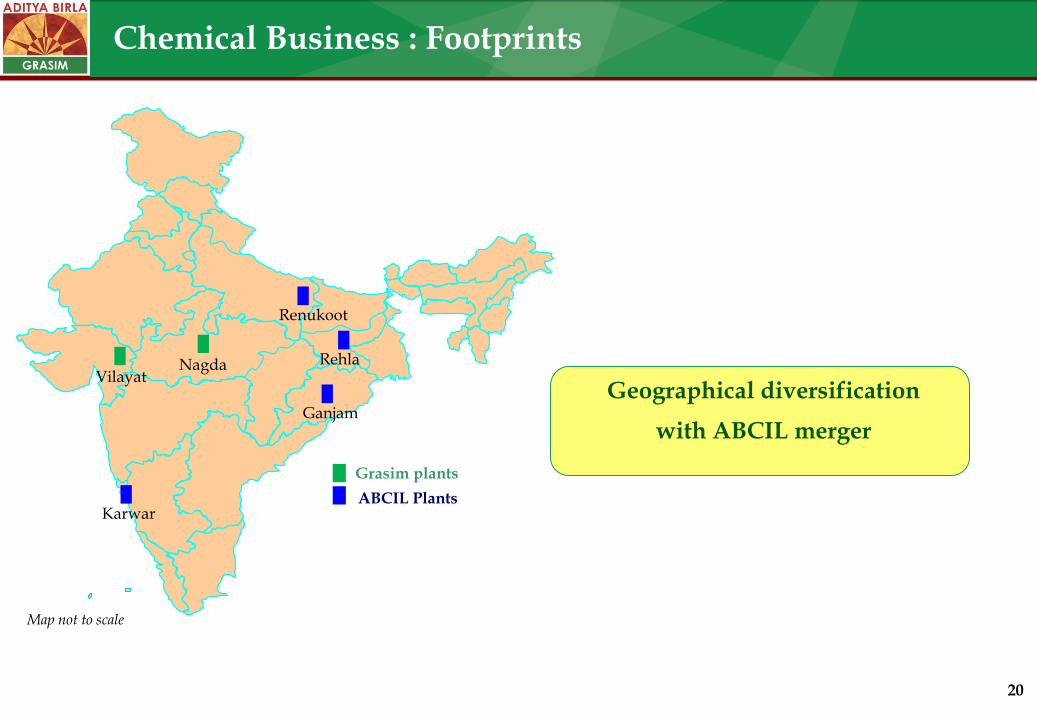

Merger of Aditya Birla Chemicals (India) Ltd. with the Company under process (w.e.f.

1.4.2015) Caustic Soda capacity to increase from 452K TPA to 804K TPA

ABCIL completed acquisition of Odisha plant (59K TPA) from Jayshree Chemicals

* Effective capacity for the period

20

Map not to scale

Chemical Business : Footprints

Grasim plants

ABCIL Plants

Nagda

Vilayat

Karwar

Renukoot

Rehla

Geographical diversification

with ABCIL merger

Ganjam

Cement

No. 1 RMC player in India

With > 100 plants No.1 Player of White Cement

& Cement based Putty

Different Products to provide

complete Building Solutions

``q

India’s Largest Selling

Brand

22

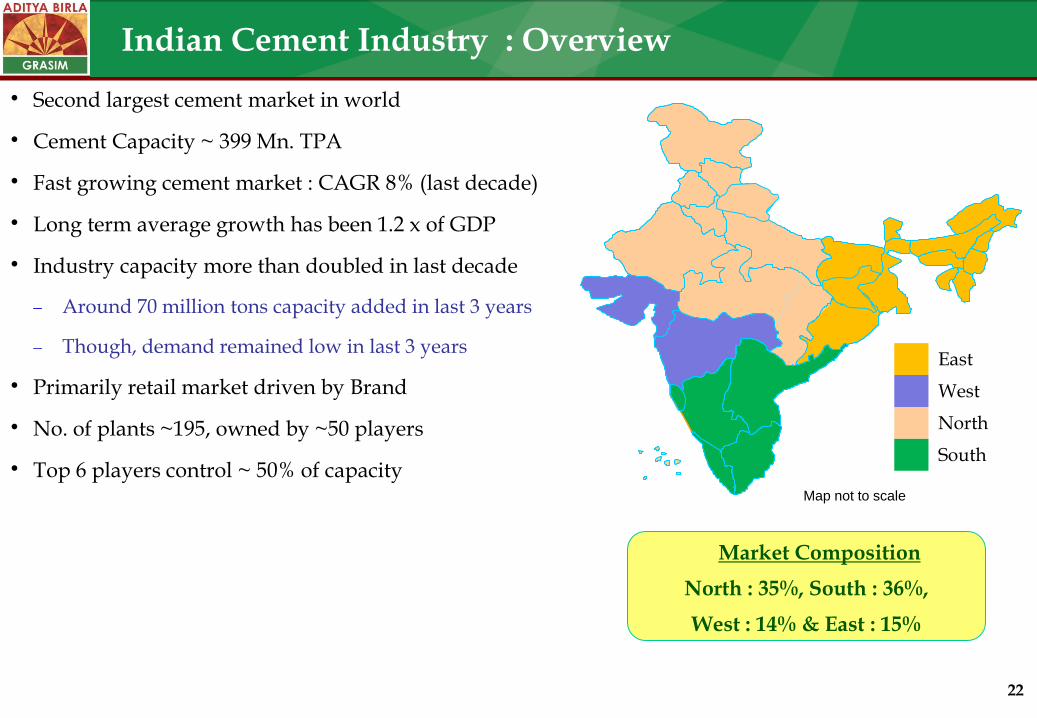

Indian Cement Industry : Overview

Second largest cement market in world

Cement Capacity ~ 399 Mn. TPA

Fast growing cement market : CAGR 8% (last decade)

Long term average growth has been 1.2 x of GDP

Industry capacity more than doubled in last decade

Around 70 million tons capacity added in last 3 years

Though, demand remained low in last 3 years

Primarily retail market driven by Brand

No. of plants ~195, owned by ~50 players

Top 6 players control ~ 50% of capacity Map not to scale

East

West

North

South

Market Composition

North : 35%, South : 36%,

West : 14% & East : 15%

23

Global Cement Capacity and Per Capita Consumption

Top Cement Producing Countries - 2014 Per Capita Consumption - 2014

________________________________________________________ Source: Cembureau ,Company Estimate

_________________________________________________________ Source: Cembureau, Company estimates, Population - IMF

India’s per capita consumption (200 kgs) is lowest among developing nations

(Brazil ~355 kgs, China ~1,780 kgs, World Average ~600 kgs)

Low per capita consumption reflects significant potential for future growth

1,780

830

600 470

355 280

200

Ch

ina

Tu

rkey

Wo

rld

Ru

ssia

Bra

zil

US

A

Ind

ia

Kgs/person

2,438

255 81 71 72 68

Ch

ina

Ind

ia

US

A

Tu

rkey

Bra

zil

Ru

ssia

Mn. Tons

24

Cement – Major Growth Drivers in India

Housing

Infrastructure

Favorable demographics with growing young population

Rising affordability - Increasing income level

Government vision of house for every family by 2022

Rapid Urbanisation (28.7% in 2005 to exceed 40% by 2030)

No. of Cities with population of 1Mn.+ to grow from 33 in 2005 to 68 in 2030

Demand from urban housing to improve with softening of interest rates

Investment projected across various Infrastructure segments

Government’s focus on building concrete highways

Western and Eastern dedicated freight corridor with investment of ~$ 13 Bn.

Metro projects in tier II cities (~$ 17 Bn.)

5 new Mega Power Projects each of 4000 MW in the Plug-and-Play mode (~$ 16 Bn.)

Target of 175,000 MW renewable energy by 2022

30% higher allocation for infrastructure (~$ 48 Bn.)

Commercial & Industrial Investments

Demand from IT / ITES

Expected revival in corporate capex

Emerging growth from resources based industries from Eastern India

25

8.5

12.1

5.7

7.1

5.2

2.6 3.5

0

2

4

6

8

10

12

14

08-09 09-10 10-11 11-12 12-13 13-14 14-15

Capacity addition pace slowing down….. Leading

towards improvement in utilisation

Setting up new Cement capacity becoming more

challenging due to

Tougher land acquisition process

Increased gestation period

Lower availability of new limestone mines

Softening of energy prices in global markets augur

well for the Cement sector

Cement Sector Outlook

Industry Capacity Trend

% Growth

Source: Company Estimates, DIPP data

Cement Demand Growth Trend

216

276 304 319

353 364 386

178 203 214

229 241 247 256

0

100

200

300

400

08-09 09-10 10-11 11-12 12-13 13-14 14-15

Capacity Production

Mn. Tons

26

Cement Business : Key Strengths

Excellent growth record

From 8 Mn. TPA in FY2000 to ~75 Mn. TPA

Grew organically as well as inorganically

Market Leadership

“UltraTech” – Premium brand, largest in India

Leadership in key consuming markets

Strong nationwide distribution network

Cost leadership

Economy of scale with large size kilns

Latest technology plants

Assured power supply thru’ captive thermal power plants meeting 80% of power requirement

Hub and Spoke model thru’ split grinding units / terminals near markets and efficient logistics

Leadership in Ready Mix Concrete and White Cement business

Strong brand with pan India presence

8.2 14.2

29.7 35.0

51.8

63.2

99-00 03-04 04-05 07-08 11-12 14-15 15-16

Capacity (Mn. Tons)

Continuous Growth in Capacity

74.8#

# Post acquisition of JAL’s MP assets

67.7

27

Hyderabad

Map not to scale

Shambhupura

Jawad

Raipur

Malkhed

Jodhpur

Reddipalayam

Bangalore

Bhatinda

Hotgi

Pipavav

Jafrabad

Magdalla Awarpur

Hirmi

Durgapur

Tadpatri

Arakonam

Ratnagiri

B Navi Mumbai

B Mangalore

Kotputli

Dadri

Panipat

Jharsuguda

Aligarh

Ginigera

Integrated Plants 12

Integrated plants under acquisition 2

Grinding units 14

Grinding Units in progress 2

White Cement Plant 1

Putty Plant 2

Bulk Terminals 6

B

Cement Business Footprint – A Pan India Player

P Katni

P

P

B Cochin

Sewagram

Wanakbori

Bela Sidhi

Dankuni

Patliputra

Jhajjar

Nagpur

Current Mix FY16 Mix

North 19.0 29% 23.9 34%

East 9.8 15% 11.4 16%

West 20.5 32% 20.5 28%

South 15.5 24% 15.5 22%

All India 64.7 100% 71.2 100%

Overseas 3.0 3.6

Total 67.7 74.8

B

B

B Pune

28

Industry Scenario

Industry off take estimated flat at ~1%

Low capacity utilisation for the sector

Positive signs on cost front with softening of petcoke costs

Raw material cost impacted with increased royalty on limestone

Business Performance

Revenue up by 5%

- Volume growth of 5% despite slowdown

Capacity utilisation for the Indian operations

at 76%

EBITDA up by 5% at ` 23.9 Bn.

- Saving in energy cost with higher usage of petcoke and decline in fuel prices

- Offset partially due to District Mineral Development levy

Cement Business : H1 FY16 Performance

(` Bn.) 2013-14 2014-15 H1

2015-16

Capacity (Mn. Ton) 57.0 63.2 33.8

Sales Volume Cement and Clinker (Mn. Tons)

44.7

48.2

24.5

Net Revenue 216.5 243.5 124.4

EBIDTA 43.6 47.8 23.9

EBIDTA Margin 20% 19% 19%

EBIT 32.2 35.7 14.4

29

Cement Business: Strategy for profitable growth

7

Capacity to increase to ~75 Mn. TPA on completion of existing projects and acquisition

Grinding unit in Bihar : 1.6 Mn. TPA

Grinding unit in Bahrain : 0.6 Mn. TPA

Acquisition of JAL’s Bela and Siddhi units : 4.9 Mn. TPA

Strengthening cost competitiveness

Investments in logistics infrastructure – grinding units, bulk terminal in Maharashtra and jetty expansion in

Gujarat

Continuous increase in use of petcoke to optimise fuel mix

Putting up waste heat recovery system for cheaper power

30

Presentation Structure

Introduction

Our Businesses

Financial Highlights

Capex

Summary

31 Q2FY15 Q2FY16 H1FY15 H1FY16

EBITDA

4.3 4.9

6.2 7.3

16.0 18.4

30.4

35.0

4.2 4.9

9.0 9.7

12.8 14.9

27.7 30.2

79.4 83.9

159.9 169.9

3.0 3.4

4.1 4.4

Net Profit Revenue

Financial Performance – Q2 / H1FY16

Q2FY15 Q2FY16 H1FY15 H1FY16

15%

Standalone

Revenue

Q2FY15 Q2FY16 H1FY15 H1FY16

Net Profit EBITDA

16%

Consolidated

Q2FY15 Q2FY16 H1FY15 H1FY16 Q2FY15 Q2FY16 H1FY15 H1FY16

Q2FY15 Q2FY16 1FY15 H1FY16

15%

Amount in ` Cr.

6%

13%

17%

17% 15%

10%

9% 6% 8%

32

Presentation Structure

Introduction

Our Businesses

Financial Highlights

Capex

33

Capex plan

# Represents residual capex of brownfield expansion projects already commissioned and Grinding unit at Bihar

Capex

(Net of CWIP as on

1-4-15)

Cash Outflow

FY16 FY17 onward

Standalone

VSF Expansion : Vilayat (120K TPA) – Residual Capex 1.6

Nagda Revamp 1.5

Normal Capex : VSF 2.6

: Chemical & Others 1.5

Standalone Capex (A) 7.2 4.3 3.0

Cement Subsidiary

Capacity expansion # 16.8

Logistic Infrastructure 6.6

RMC Business 1.2

Modernisation, Upgradation, Coal Mines and others (Incl. Land) 24.3

Cement Business Capex (B) 48.9 27.1 21.8

Capex (A + B) 56.1 31.4 24.8

34

Grey Cement

67.7 Mn. TPA

Pulp & Fibre

VSF 498K TPA

VSF JV China

Overseas

Pulp JVs

AV Terrace Bay 353K TPA (40%)

Domsjo 255K TPA (33.3%)

AV Nackawic 190K TPA (45%)

AV Cell 130K TPA (45%)

Grasim Bhiwani Textiles

18 Mn. Mtr. (100%)

UltraTech Cement (60.25%)

Grasim Group Structure

Idea Cellular (4.75%)

Birla Jingwei

70K TPA (26%)

Pulp 70K TPA

Others

Domestic

Overseas 3 Mn. TPA,

(UAE, Bangladesh, Sri Lanka)

12 Composite Plants

14 Split Grinding Units

>100 RMC Plants

White Cement & Putty

1.4 Mn. TPA

Nagda 162K TPA

Kharach 128K TPA

Harihar 87K TPA

Vilayat 120K TPA

Nagda 270K TPA

Vilayat 182K TPA

23

Epoxy 51K TPA

Caustic 452K TPA

BCML (26%)

Chemical

Harihar

70K TPA

Standalone Subsidiary JV JV Associate

Thank You

Contacts:

Grasim Industries Limited

(Corporate Finance Division)

Aditya Birla Centre,

S.K. Ahire Marg, Worli, Mumbai - 400 030

CIN: L17124MP1947PLC000410

Sharad Agarwal +91-22-66525062 [email protected]

Shirin Sancheti +91-22-66525097 [email protected]

Grasim Industries Limited - A VSF and Cement Major

(Supplement)

37

Supplement

• Consolidated Financial Performance

• Standalone Financial Performance

• Balance Sheet - Grasim

• Balance Sheet – UltraTech (Consolidated)

• Consolidated Businesswise Performance

38

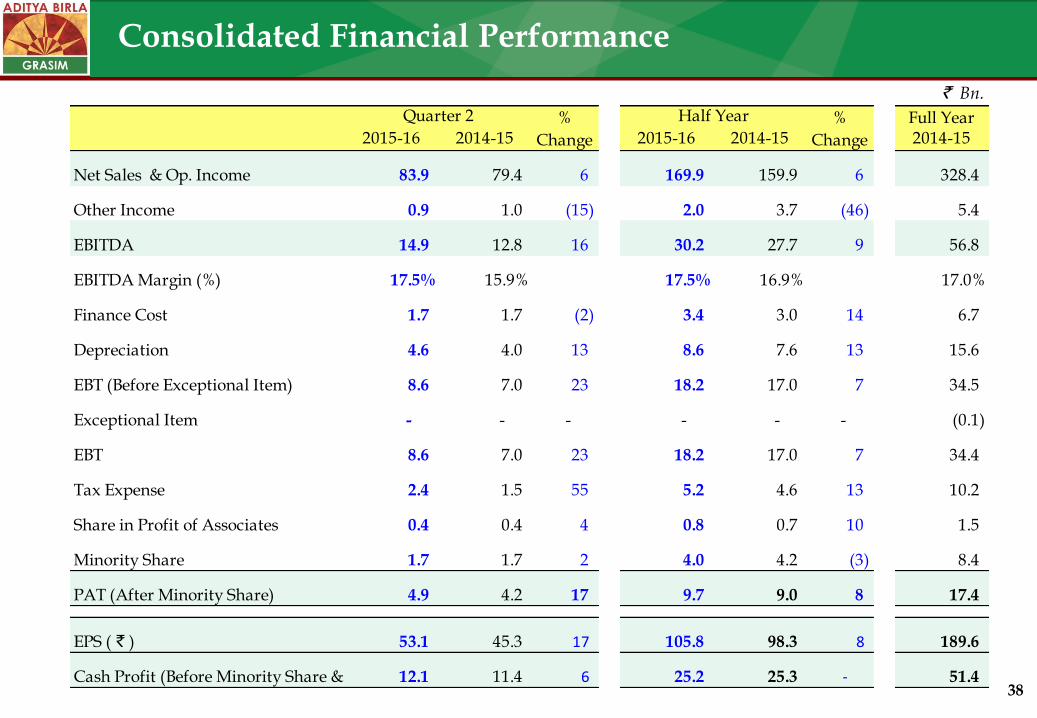

Consolidated Financial Performance

` Bn.

Full Year2015-16 2014-15 2015-16 2014-15 2014-15

Net Sales & Op. Income 83.9 79.4 6 169.9 159.9 6 328.4

Other Income 0.9 1.0 (15) 2.0 3.7 (46) 5.4

EBITDA 14.9 12.8 16 30.2 27.7 9 56.8

EBITDA Margin (%) 17.5% 15.9% 17.5% 16.9% 17.0%

Finance Cost 1.7 1.7 (2) 3.4 3.0 14 6.7

Depreciation 4.6 4.0 13 8.6 7.6 13 15.6

EBT (Before Exceptional Item) 8.6 7.0 23 18.2 17.0 7 34.5

Exceptional Item - - - - - - (0.1)

EBT 8.6 7.0 23 18.2 17.0 7 34.4

Tax Expense 2.4 1.5 55 5.2 4.6 13 10.2

Share in Profit of Associates 0.4 0.4 4 0.8 0.7 10 1.5

Minority Share 1.7 1.7 2 4.0 4.2 (3) 8.4

PAT (After Minority Share) 4.9 4.2 17 9.7 9.0 8 17.4

EPS ( ` ) 53.1 45.3 17 105.8 98.3 8 189.6

Cash Profit (Before Minority Share & EI) 12.1 11.4 6 25.2 25.3 - 51.4

Half YearQuarter 2 %

Change

%

Change

39

Full Year 2015-16 2014-15 2014-15 2013-14 2014-15

Net Sales & Op. Income 18.4 16.0 15 35.0 30.4 15 63.3

Other Income 2.1 2.1 (2) 2.3 2.7 (14) 3.5

EBIDTA 4.9 4.3 15 7.3 6.2 17 10.1

EBIDTA Margin (%) 24.0% 23.5% 19.5% 18.8% - 15.2%

Finance Cost 0.14 0.09 - 0.3 0.15 88 0.4

Depreciation 0.8 0.6 35 1.6 1.2 41 2.6

EBT (Before Exceptional Item) 3.9 3.5 11 5.4 4.9 9 7.1

Exceptional Item - - - - - - (0.3)

EBT 3.9 3.5 11 5.4 4.9 9 6.8

Tax Expense 0.5 0.5 0 0.9 0.9 9 1.6

PAT 3.4 3.0 13 4.4 4.1 10 5.3

EPS ( ` ) 36.8 32.6 13 48.3 44.1 10 57.6

Cash Profit (Excl. EI) 4.8 4.2 14 7.0 6.1 15 9.7

Scenario Actual Actual #REF!

Year 2013 2012 2011

Period Sep Sep Mar

View Qtd Qtd #REF!

Value <Entity Curr Total><Entity Curr Total> #REF!

ICP [ICP TOP] [ICP TOP] #REF!

Entity GIL_IFS GIL_IFS #REF!

Custom1 TOTC1 TOTC1 #REF!

Custom2 TOTC2 TOTC2 #REF!

Custom3 TOTC3 TOTC3 #REF!

Custom4 TOTC4 TOTC4 #REF!

Full Year

2015-16 2014-15 2015-16 2014-15 2014-15

Net Sales & Op. Income 1,838.1 1,599.8 15 3,495.4 3,039.3 15 6,332.6

Other Income 206.7 211.4 (2) 228.6 266.6 (14) 348.1

PBIDT 490.5 425.4 15 728.0 621.3 17 1,013.0

PBIDT Margin (%) 24.0% 23.5% 19.5% 18.8% 15.2%

Finance Cost 13.8 9.0 53 27.5 14.6 88 39.3

Depreciation 84.1 62.4 35 162.8 115.4 41 262.5

PBT 392.6 353.9 11 537.7 491.3 9 711.2

Exceptional Item - - - - - - (26.2)

PBT (After Exceptional Item) 392.6 353.9 11 537.7 491.3 9 684.9

Tax Expense 54.4 54.5 0 93.7 86.1 9 155.0

PAT 338.2 299.4 13 444.0 405.3 10 529.9

EPS 36.8 32.6 13 48.3 44.1 10 57.6

Cash Profit 476.7 416.3 14 700.5 606.7 15 973.7

Cash Profit 476.7 416.3 14 700.5 606.7 15 973.7

Quarter 2 %

Change

%

Change

Quarter 2 %

Change

Half Year %

Change

Half Year

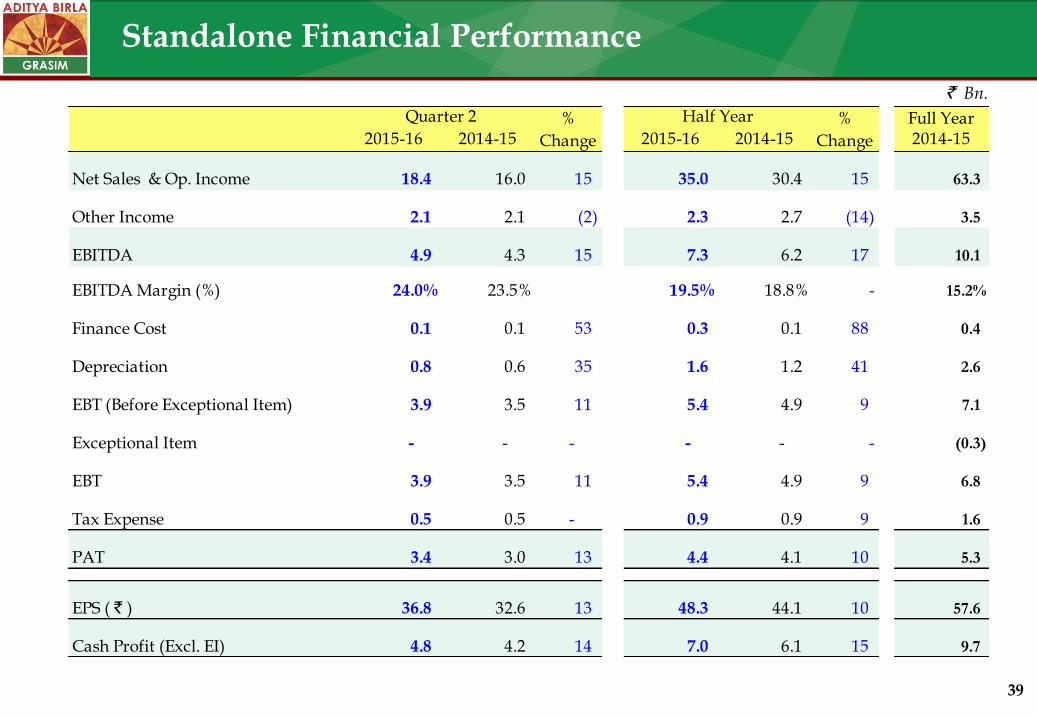

Standalone Financial Performance

` Bn.

Full Year 2015-16 2014-15 2015-16 2014-15 2014-15

Net Sales & Op. Income 18.4 16.0 15 35.0 30.4 15 63.3

Other Income 2.1 2.1 (2) 2.3 2.7 (14) 3.5

EBITDA 4.9 4.3 15 7.3 6.2 17 10.1

EBITDA Margin (%) 24.0% 23.5% 19.5% 18.8% - 15.2%

Finance Cost 0.1 0.1 53 0.3 0.1 88 0.4

Depreciation 0.8 0.6 35 1.6 1.2 41 2.6

EBT (Before Exceptional Item) 3.9 3.5 11 5.4 4.9 9 7.1

Exceptional Item - - - - - - (0.3)

EBT 3.9 3.5 11 5.4 4.9 9 6.8

Tax Expense 0.5 0.5 - 0.9 0.9 9 1.6

PAT 3.4 3.0 13 4.4 4.1 10 5.3

EPS ( ` ) 36.8 32.6 13 48.3 44.1 10 57.6

Cash Profit (Excl. EI) 4.8 4.2 14 7.0 6.1 15 9.7

Quarter 2 %

Change

%

Change

Half Year

40

Balance Sheet - Grasim

* ` Bn.

30th Sep'15 31st Mar'15 EQUITY & LIABILITIES 30th Sep'15 31st Mar'15

116.3 111.8 Net Worth 241.6 231.4

- - Minority Interest 79.9 76.8

10.1 11.2 Borrowings 112.6 119.3

7.1 6.2 Deferred Tax Liability (Net) 36.9 34.1

13.7 14.5 Liabilities & Provisions 79.9 78.7

147.2 143.7 SOURCES OF FUNDS 550.9 540.3

ASSETS

51.6 51.9 Net Fixed Assets 293.2 285.5

5.6 5.2 Capital WIP & Advances 34.2 35.1

- - Goodwill on Consolidation 33.5 32.8

Investments

26.4 26.4 Cement Subsidiary - -

13.2 11.0 Liquid Investments 53.6 57.9

16.2 16.2 Other Investments 16.8 14.7

34.2 33.0 Current Assets, Loans & Advances 119.6 114.3

147.2 143.7 APPLICATION OF FUNDS 550.9 540.3

(3.1) 0.2 Net Debt 58.9 61.4

- - Net Debt : Equity 0.18 0.20

- 0.02 Net Debt : EBIDTA 0.98 1.08

Standalone Consolidated

41

Balance Sheet – UltraTech (Consolidated)

* ` Bn.

EQUITY & LIABILITIES 30th Sep'15 31st Mar'15

Net Worth 200.8 190.4

Minority Interest 0.1 0.2

Borrowings 93.2 98.3

Deferred Tax Liability (Net) 29.7 27.9

Liabilities & Provisions 63 63.8

SOURCES OF FUNDS 386.9 380.5

ASSETS

Net Fixed Assets 230.8 222.9

Capital WIP & Advances 27.6 29.0

Goodwill on Consolidation 11.0 10.5

Investments

Liquid Investments 39.8 46.3

Other Investments 0.2 0.2

Current Assets, Loans & Advances 77.5 71.6

APPLICATION OF FUNDS 386.9 380.5

Net Debt 53.3 52.0

Net Debt : Equity 0.27 0.27

Net Debt : EBITDA 1.12 1.09

42

Viscose Staple Fibre : Summary (Standalone)

* Operational capacity during the period

Full Year

2015-16 2014-15 2015-16 2014-15 2014-15

Capacity* K TPA 125 108 15 249 202 23 434

Production K MT 121 101 20 215 191 13 408

Sales Volumes K MT 114 101 13 216 187 16 403

Net Revenue ` Bn. 14.4 12.7 13 26.9 23.6 14 49.7

EBITDA ` Bn. 2.1 1.5 40 3.5 2.3 51 4.7

EBITDA Margin % 14.6% 11.8% -- 12.9% 9.7% -- 9.3%

EBIT ` Bn. 1.6 1.1 37 2.4 1.7 45 3.1

Capital Employed (Incl. CWIP) ` Bn. 51.9 52.3 (1) 51.9 52.3 (1) 52.8

ROAvCE (Excl. CWIP) % 13.1% 12.5% -- 10.0% 9.1% -- 7.5%

Quarter 2 %

Change

Half Year %

Change

43

Full Year

2015-16 2014-15 2015-16 2014-15 2014-15

Capacity K TPA 113 113 - 226 226 - 453

Production K MT 113 102 12 213 202 6 412

Sales Volumes K MT 118 98 20 220 196 12 409

Net Revenue ` Bn. 5.2 4.2 26 10.1 8.3 21 17.0

EBITDA ` Bn. 0.9 0.8 17 1.9 1.7 10 2.9

EBITD Margin % 17.7% 18.9% -- 18.4% 20.4% -- 18.0%

EBIT ` Bn. 0.7 0.6 - 1.4 1.22 12 2.0

Capital Employed (Incl. CWIP) ` Bn. 19.8 19.5 2 19.8 19.5 2 19.2

ROAvCE (Excl. CWIP) % 14.4% 12.2% -- 14.7% 13.4% -- 10.9%

Half YearQuarter 2 %

Change

%

Change

Chemical : Summary

44

Cement : Summary

Includes captive consumption for RMC

$$ Includes captive consumption for value added products

Full Year

2015-16 2014-15 2015-16 2014-15 2014-15

Grey Cement

Capacity Mn. TPA 16.90 15.45 9 33.80 30.85 10 63.15

Production Mn. MT 11.45 10.91 5 24.30 22.95 6 46.71

Cement Sales Volumes $ Mn. MT 11.44 10.92 5 24.31 23.09 5 47.09

Clinker Sales Volumes Mn. MT 0.07 0.25 (72) 0.15 0.51 (71) 1.08

White Cement & Putty

Sales Volumes $$ Lac MT 3.22 2.99 8 5.89 5.56 6 12.24

Net Revenue ` Bn. 60.1 57.7 4 124.4 118.0 5 243.4

EBITDA ` Bn. 11.0 9.9 12 23.9 22.8 5 47.8

EBITD Margin % 18.2% 17.0% -- 19.0% 18.9% -- 19.3%

EBIT ` Bn. 7.5 6.7 13 14.4 14.2 1 35.7

Capital Employed (Incl. CWIP) ` Bn. 342.9 327.4 5 342.9 327.4 5 346.8

ROAvCE (Excl. CWIP) % 9.6% 9.2% -- 9.1% 10.3% -- 12.4%

Half Year %

Change

Quarter 2 %

Change