great american food monitor - august 2017 food... · global food prices reached a two-year ......

TRANSCRIPT

WORLD FOOD PRICES ON THE RISE

VOLUME

251

AUGUST 2017

Food

DEMAND FOR DAIRY Increased demand from overseas caused dairy prices to surge

PRICES SOARING Global food prices reached a two-year high in July, driven by prices for meats, dairy, and wheat

WHEAT RISING Wheat prices surged through the summer months amid drought conditions

© 2017 Great American Group, LLC. All Rights Reserved.

In This Issue MONITOR FOODGREATAMERICAN.COMAUGUST 2017800-45-GREAT

VOLUME

251

Deals are a moving target. A constantly shifting mix of people, numbers,

and timing. We’re here to simplify this process for you. Our experts are

dedicated to tracking down and flushing out the values you need, even on

the most complex deals. So when the time comes to take your shot with

Great American, you’re always—right on the money.

Deals are a moving target. A constantly shifting mix of people, numbers,

and timing. We’re here to simplify this process for you. Our experts are

dedicated to tracking down and fl ushing out the values you need, even

on the most complex deals. So when the time comes to take your shot

with Great American, you’re always—right on the money.

© 2016 GREAT AMERICAN GROUP, LLC. ALL RIGHTS RESERVED

GREATAMERICAN.COM

0304050810101111

12121315161617

Trend Tracker

Overview

Meat

Seafood

Dairy

Sugar

Food Reference Sheet

Experience

Appraisal & Valuation Team

Fruits and Vegetables Monitor Information

Coffee

Corn About Great American Group

Wheat

Trend Tracker

NOLVS

• Meat: NOLVs increased versus the prior year due to a

favorable spread between acquisition costs for beef and

market prices.

• Seafood: NOLVs are mixed, as sales are down but

margin and prices have increased for certain categories.

Companies may focus on crabmeat, as this traditionally

carries a higher gross margin.

SALES TRENDS

• Meat: Sales increased driven by higher prices for meat

and continued demand in the market.

• Seafood: Sales declined due to the loss of contracts

with customers as well as companies focusing on

higher margins.

GROSS MARGIN

• Meat: Gross margins are mixed due to some companies

increasing prices to customers and others updating

standard costing.

• Seafood: Gross margins increased, particularly for

crabmeat, as companies are focusing on higher

margin products.

INVENTORY

• Meat: Inventory levels are mixed overall as some

companies are intentionally working down inventory

levels while some have seen increases due to higher

prices and demand.

• Seafood: Inventory levels have increased due to

seasonal factors such as the timing of the shrimp and

crab harvests.

PRICING

• Meat: Beef prices are increasing as compared to the

prior year due to increased demand. Pork prices have

increased due to lower supply, while poultry prices

are increasing due to higher demand from health-

conscious consumers.

• Seafood: Shrimp prices, while still down year-over-year,

stabilized in the past several months due to increased

volumes in the marketplace.

• Dairy: Milk prices increased year-over-year, as prices in

2016 were unusually low due to a global oversupply and a

lower amount of exports, but have been relatively stable in

recent months.

• Corn: Despite recent month-to-month increases, prices

remain down year-over-year due to favorable weather

patterns that resulted in an ample supply.

3 | MONITOR FOOD August 2017

Meat (Mainly Beef) Seafood

NOLVs Increasing Mixed

Sales Trends Increasing Decreasing

Gross Margin Mixed Increasing

Inventory Mixed Increasing

Pricing

Meat Increasing

Seafood (Mainly Shrimp) Consistent

Dairy Increasing

Corn Decreasing

While meat, dairy, and wheat prices continue to increase,

prices for other commodities, namely sugar and coffee, have

followed a downward trajectory. According to the FAO, global

sugar prices are down 26% year-over-year, as the main

producing area in Brazil remains on track to produce a record

crop. Within the U.S., sugar prices have been falling from a

slight peak experienced in February 2017 when demand was

higher. Similarly, global coffee prices have been on the decline

due to a buildup of large inventories and reduced export

volumes by Brazil.

One of the major current trends within the food industry is

the focus on healthier eating. According to a survey by the

research firm Label Insight, 49% of consumers have stated

that they follow a specific diet or healthy eating program.

Similarly, nearly 48% of consumers report that they consume

a larger amount of fresh (unprocessed) foods than they did

three years ago. A majority of consumers avoid specific

ingredients, such as high fructose corn syrup, artificial

sweeteners, preservatives, or artificial colors and flavors,

and regularly purchase “superfoods” such as avocado, kale,

cinnamon, green tea, or blueberries.

Gluten-free eating is also becoming increasingly popular in

today’s society due to the ingredient’s perceived effects on

the body. As a result, numerous fast-food restaurants are now

offering gluten-free options along with other healthy menu

items, such as salads, fruits, smoothies, and yogurt. The focus

on healthier eating has also resulted in higher demand for

lean protein options, such as chicken, pork, and seafood, and

lower consumption of sugar.

Overview

Worldwide food prices are on the rise, according to the latest data from the Food and Agriculture Organization (“FAO”). Prices reached a two-year high in July 2017, an increase of 2.3% from June and 10.2% above last year’s level, driven by higher costs for meats (including beef, pork, and chicken), dairy, and wheat. Year-over-year, global meat prices have risen approximately 8%, while dairy prices soared 52% above last year’s levels, bolstered by increased demand from overseas. Wheat prices have also continued to surge through the summer months, owing to drought conditions in key growing regions. In July 2017, hard red spring wheat traded 34% higher than in June 2017, its highest monthly gain since 2010.

4 | MONITOR FOOD August 2017

5 | MONITOR FOOD August 2017

Meat

BEEF

Wholesale beef prices averaged $3.24 per pound in July

2017, posting a significant decrease from the prior month,

but remained above the average of $3.12 per pound posted

in July 2016. Beef prices had increased in the first half of

2017 as demand rose in anticipation of holidays such as

Independence Day; following July 4th, prices typically decline.

Within the U.S., beef consumption per capita increased from

53.9 pounds in 2015 to 57.1 pounds in 2017.

As retail prices typically lag several months behind wholesale,

most retail beef prices rose slightly in July 2017, but remained

below the prior year, when a lack of supply had resulted in

higher overall pricing.

Retail prices for USDA ground beef averaged $3.75 per

pound in July, up from $3.68 per pound in June and were

above the prior year’s price of $3.69 per pound. Similarly,

round steak prices increased from $5.76 per pound to

$5.94 per pound year-over-year. However, sirloin decreased

from $8.52 per pound to $8.36 per pound, despite a slight

increase from June to July.

Looking ahead, retail beef prices are expected to decrease

between 1.0% and 2.0% in 2017 due to an expected increase

in production. While beef production through year-end is

lower than originally forecast, it is still predicted to exceed the

2016 level if weather and other factors remain unchanged.

Monthly Choice Beef Wholesale Value Per Pound July 2016 through July 2017 ($ per Pound)1

6 | MONITOR FOOD August 2017

Meat

PORK

Wholesale pork prices have been on the rise in recent

months, increasing on both a monthly and year-over-year

basis. In July 2017, prices climbed to an average of $1.84

per pound, up from $1.78 per pound in June 2017 and

surpassing the price of $1.64 per pound posted in July

2016, driven by lower amounts of pork in cold storage

coupled with higher consumption rates. Pork consumption

per capita increased from 49.7 pounds in 2015 to 50.8

pounds in 2017.

At the end of 2016, there were 477.2 million pounds of

pork in cold storage, representing a decrease of 8% from

the prior month and a decline of 12.5% year-over-year. This

year-end figure represented the smallest amount of frozen

pork for any month since September 2011. In particular,

pork bellies in cold storage at the end of 2016 were down

66.7% as compared to the prior year. However, pork

production rates have begun to rise, with a 4.9% increase

expected through year-end; this is likely to result in lower

prices in the months to come.

As retail prices typically lag several months behind

wholesale costs, prices at supermarkets have been mixed on

a year-over-year basis, depending on the cut. Boneless hams

were priced at $4.02 per pound in July 2017, an increase

from $3.96 per pound listed in the same month of 2016,

while bacon rose from $5.45 per pound to $5.82 per pound

year-over-year. However, pork chops decreased from $3.83

per pound to $3.42 per pound during this same period.

According to the USDA, retail pork prices are expected to be

1.0% to 2.0% lower through year-end.

POULTRY

Wholesale broiler prices have been increasing steadily

since February due to larger sizes of birds and increased

demand from health-conscious consumers. In July 2017,

USDA wholesale broiler prices averaged $0.99 per pound,

increasing from the June 2017 average of $0.98 per

pound and up considerably from July 2016’s average

of $0.76 per pound. Chicken consumption per capita

increased from 90.0 pounds in 2015 to 91.6 pounds in

2017, an all-time high.

At the retail level, year-over-year price changes have been

mixed, depending on the cut. Retail fresh whole chicken

prices in July 2017 increased from $1.44 to $1.49 per

pound year-over-year, while prices for whole turkeys

increased from $1.59 to $1.62 per pound. Chicken leg

prices decreased from $1.55 per pound to $1.42 per pound

and chicken breast prices fell two cents to $3.19 per pound.

While overall retail poultry prices are expected to increase

between 0.5% and 1.5% through year-end, the USDA

notes that such prices will remain lower than the 20-year

historical average of 2.1%.

Monthly Average Pork Wholesale Value Per Pound July 2016 through July 2017 ($ per Pound)2

7 | MONITOR FOOD August 2017

Meat

POULTRY (CONT’D)

One notable trend within the chicken segment of late has

been rising wholesale prices of chicken wings, a trend that

has negatively impacted restaurant chains such as Buffalo

Wild Wings and Chick-Fil-A. In April and May, analysts at

BMO Capital Markets reported an 11% increase in year-over-

year chicken wing prices, the largest jump since the Super

Bowl, when prices traditionally rise due to higher demand. It

remains to be seen whether this trend will continue through

the late summer and fall months.

3 Monthly Wholesale Broiler Composite July 2016 through July 2017 ($ per Pound)

8 | MONITOR FOOD August 2017

Seafood

OVERVIEW

According to market research firm IBISWorld, Inc.

(“IBISWorld”), revenue within the seafood wholesaling industry

increased at an annualized rate of 1.2% in the five years to

2017. Revenue reached $16.5 billion, with a growth rate of

1.8% expected through year-end.

The recent improvement in the industry has been the result

of overall economic growth. Per capita disposable income

has increased over the past five years, allowing consumers to

purchase more expensive protein options such as seafood.

Additionally, seafood prices decreased, allowing for greater

consumption of more expensive varieties, such as salmon

and crab.

SHRIMP

Prices have been steady to mainly flat and remain generally

lower than over the last couple of years when early mortality

syndrome hit the farmed shrimp market extremely hard.

Market prices for shrimp (No.1 shell-on headless, 26-30

count per pound, Mexican origin, New York port) fell from

an average of $12.13 per pound in May 2016 to $10.69 per

pound in May 2017. Prices have remained stable since the

end of September due to an ample supply in the market.

Imports grew 7% in June 2017 and are now 2% higher as

compared to 2016. However, the U.S. remains in third place,

with Asia purchasing over 50% of Ecuador production,

followed by Europe, at approximately 24%. With so much

demand for Ecuador shrimp overseas, offerings have

remained generally steady and somewhat disconnected from

a barely steady to weak U.S. spot market, which has resulted

in eroded margins.

Gulf of Mexico wild shrimp is a much different market than

farmed and has trended higher than the past two years due to

lower than expected harvest stocks. The highest quality wild

shrimp have higher prices year-to-date than those of the last

few years.

LOBSTER

Prices of Atlantic and New England sourced lobster were

down in July 2017, despite a lower supply than in recent

years. According to Urner Barry, the wholesale price for

1¼-pound hard shell lobsters at the end of July 2017

averaged $7.63 per pound, down from a little over $8.00 per

pound at the same time in 2016. Lobster prices historically

fluctuate in conjunction with supply and demand; if lobster

catches are high in the coming weeks, the price may drop

even further.

UB Shrimp, Cooked, Asian, Tail-On, White, 16-20 Count May 2016 through May 2017 ($ per Pound)4

9 | MONITOR FOOD August 2017

Seafood

SALMON

Norwegian frozen product imports are up 43% versus a year

ago, while the Chilean farmed salmon market continues to

struggle with algae bloom and other geo-political issues.

Imports from Chile have shrunk significantly over the last

two to three years, a trend that has continued. Regarding the

overall market, there have been lower than expected frozen

inventories, as there has been a higher demand for and

health-conscious incentives to buy and sell fresh salmon.

Fresh salmon sourcing from Norway and the UK are up 100%

over last year. Fresh salmon prices are extremely high all over

the world due to this trend, while the demand for salmon

sourced from Chile remains cool.

Prices for fresh fruits decreased 1.9% from May 2017 to June

2017, yet were up 1.1% as compared with 2016. Despite rising

prices for bananas, apples, and citrus fruits in June, prices for

all other fresh fruit decreased on a month-to-month basis due

primarily to elevated supplies. The USDA expects fresh fruit

prices to change between negative 0.5% and 0.5% through

year-end, with increases predicted for 2018.

Fresh vegetable prices fell 1.3% from May 2017 to June

2017, but prices remained 1.6% higher than June 2016. ERS

expects fresh vegetable prices to decrease between 0.5%

and 1.5% through year-end, as a stronger U.S. dollar, low oil

prices, and seasonal availability will place downward pressure

on retail fresh produce prices.

10 | MONITOR FOOD August 2017

Dairy

Global dairy prices have risen in 2017, as evidenced by the

FAO Dairy Price Index, which was up 52% year-over-year in

July. Within the U.S., milk prices were relatively flat from June

to July 2017, but remained elevated year-over-year. Retail milk

prices averaged $3.22 per gallon in July 2017, rising from

$3.21 in the previous month but above the July 2016 price of

$3.06 per gallon. Milk prices in 2016 were unusually low due

to a global oversupply and a lower amount of exports.

However, according to the USDA, dairy exports are expected

to increase in the coming months, particularly for products

with high skim-milk content as consumers opt for healthier,

lower fat options.

Domestic cheese inventories have been high in recent

months, resulting in a trend toward lower, or stable, prices.

American cheese prices declined from $4.37 per pound

to $4.28 per pound year-over-year, while cheddar cheese

declined from $5.18 per pound to $4.85 per pound. However,

cheese exports increased by 26.9% in May versus the prior

month; should this trend continue, it will likely reduce the

oversupply and result in higher prices. Additionally, domestic

consumption of cheese has increased within the last two

decades, with American cheese consumption up 20% and

Italian style cheeses up 40% on a per capita basis. Yogurt

consumption was up 139% during this period.

Demand for most dairy products is expected to increase as

the year progresses. As a result, the USDA expects retail dairy

product prices to rise between 0.5% and 1.0% through year-

end 2017.

5 Average Monthly Milk Retail Prices - Fresh, Whole, Fortified Per GallonJuly 2016 through July 2017

Fruits and Vegetables

11 | MONITOR FOOD August 2017

Corn

Prices for U.S. #2 yellow corn, used primarily for livestock

feed, have continued to decline, averaging $159.99 per metric

ton in June 2017, representing a decline from $162.70 per

metric ton in the prior year.

Corn prices have been falling since the historic highs reached

in 2012, when drought conditions drove prices to over

$330.00 per metric ton.

As mentioned in the prior monitor, the recent decrease in

pricing correlates to an plentiful supply of corn in the market.

According to the USDA, the total U.S. corn supply for 2017/18

is projected at 16.7 billion bushels, which is 265 million higher

than the previous forecast. Planted corn acreage is projected

at 90.9 million acres, up nearly 1.0 million. As a result,

corn prices are not expected to increase significantly in the

foreseeable future.

6 U.S. No. 2 Yellow Corn Prices June 2016 through June 2017 ($ Per Metric Ton)

Wheat

Global wheat prices have been rising amid concerns over a

major drought in key growing areas in the U.S. (particularly

in Montana and the Dakotas) and in Canada. This has had

a significant impacted on spring wheat, a high protein grain

used in artisan wheat foods such as rolls, breads, and pizza

crust. In June 2017, hard red spring wheat traded 34% higher

than the prior month, representing its highest monthly gain

since 2010.

According to a report by CNBC, wheat conditions in the U.S.

deteriorated in recent months, and do not seem likely to

improve in the coming weeks. While there are ample stocks

of wheat in storage, the harvest for this year is expected to

remain poor. This is predicted to result in higher prices in the

months to come.

12 | MONITOR FOOD August 2017

Coffee

According to the International Coffee Organization’s (“ICO”)

most recent Monthly Coffee Market Report, coffee prices

decreased in June 2017, partially due to a buildup of large

inventories and reduced export volumes by Brazil. The ICO

composite indicator fell 2.4% in June to 122.39 U.S. cents per

pound. In terms of the group indicators, all categories except

Robustas experienced declines, with Brazilian Naturals, Other

Milds, and Colombian Milds posting declines from the prior

month of 5.7%, 4.5%, and 3.5%, respectively.

However, Robustas posted an increase of 3.6% in June due to

concerns of a possible shortage in the coming months.

Overall exports of coffee in June were estimated at 10.9

million bags, representing an increase of 8.8% compared to

the same month in 2016. Exports by Brazil were down by

22.7 million bags, or 5.9%, compared to last year, continuing

a trend that has been ongoing for two years. The reduced

exports by Brazil, however, were partially offset by increases

by other origins such as Ethiopia, Colombia, Honduras, Peru,

Uganda, and Indonesia.

Sugar

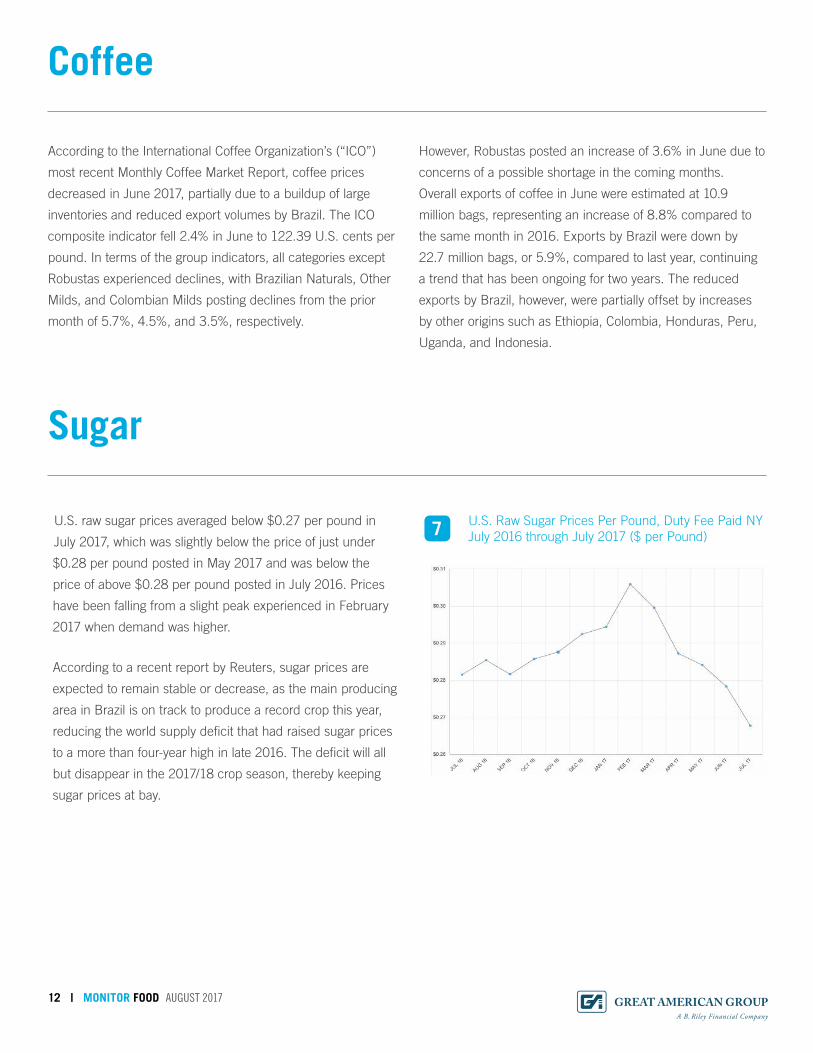

U.S. raw sugar prices averaged below $0.27 per pound in

July 2017, which was slightly below the price of just under

$0.28 per pound posted in May 2017 and was below the

price of above $0.28 per pound posted in July 2016. Prices

have been falling from a slight peak experienced in February

2017 when demand was higher.

According to a recent report by Reuters, sugar prices are

expected to remain stable or decrease, as the main producing

area in Brazil is on track to produce a record crop this year,

reducing the world supply deficit that had raised sugar prices

to a more than four-year high in late 2016. The deficit will all

but disappear in the 2017/18 crop season, thereby keeping

sugar prices at bay.

U.S. Raw Sugar Prices Per Pound, Duty Fee Paid NYJuly 2016 through July 2017 ($ per Pound)7

Food Reference Sheet

13 | MONITOR FOOD August 2017

USDA CHOICE BEEF VALUES, PRICE SPREAD, AND ALL-FRESH RETAIL VALUE DOLLARS PER POUND OF RETAIL EQUIVALENT

July 2017 June 2017 July 2016

Retail Value $6.100 $6.207 $6.090

Wholesale Value $3.247 $3.736 $3.120

Net Farm Value $2.585 $2.901 $2.550

Wholesale to Retail Spread $2.853 $2.471 $2.970

Farm to Wholesale Spread $0.662 $0.835 $0.570

Total Spread $3.515 $3.306 $3.540

All-Fresh Beef Retail Value $5.833 $5.795 $5.775

USDA PORK VALUES AND SPREADSDOLLARS PER POUND OF RETAIL EQUIVALENT

July 2017 June 2017 July 2016

Retail Value $3.833 $3.756 $3.781

Wholesale Value $1.843 $1.784 $1.635

Net Farm Value $1.138 $1.056 $0.981

Wholesale to Retail Spread $1.990 $1.972 $2.146

Farm to Wholesale Spread $0.705 $0.728 $0.654

Total Spread $2.695 $2.700 $2.800

USDA RETAIL PRICES FOR POULTRY CUTS DOLLARS PER POUND OF RETAIL EQUIVALENT

July 2017 June 2017 July 2016

Retail Broiler Composite $1.863 $1.868 $1.899

Wholesale Broiler Composite $0.991 $0.982 $0.757

Wholesale to Retail Broiler Spread $0.872 $0.886 $1.142

Chicken, Fresh, Whole $1.496 $1.497 $1.445

Chicken, Legs, Bone-In $1.418 $1.436 $1.547

Chicken, Boneless Breast $3.189 $3.215 $3.210

Turkey, Frozen, Whole $1.622 $1.576 $1.586

Food Reference Sheet

14 | MONITOR FOOD August 2017

USDA RETAIL PRICES FOR DAIRY PRODUCTS

July 2017 June 2017 July 2016

Milk, fresh, whole, fortified($/gallon)

$3.219 $3.213 $3.062

American processed cheese ($/pound)

$4.282 $4.306 $4.373

Cheddar cheese, natural ($/pound) $4.851 $4.797 $5.184

COFFEE: ICO INDICATORS AND FUTURES PRICES (NEW YORK MARKET)

June 2017 May 2017 June 2016

ICO Composite $1.2726 $1.2239 $1.3298

Columbian Milds $1.5251 $1.4612 $1.6446

Other Mild Arabicas $1.4966 $1.4322 $1.7176

Brazilian Natural Arabicas $1.2919 $1.2371 $1.4476

Robustas $1.0494 $1.0195 $0.9082

15 | MONITOR FOOD August 2017

GA has worked with and appraised many large and well-

known companies within the food service industries. While

our clients remain confidential, they have included meat

processors and distributors, seafood distributors, leading fresh

and processed fruit and vegetable distributors, and specialty

and prepared food distributors servicing restaurants, retailers,

food service companies, and wholesalers across the U.S. GA

has appraised companies such as the following:

• One of the nation’s largest independent canning and

frozen food companies and one of the world’s largest

producers of fresh and packaged fruits and vegetables.

• Processors of both conventional and organic frozen

vegetables, and manufacturers and distributors of frozen

and canned vegetable and fruit products.

• A major dairy marketing cooperative that offers cheese,

butter, non-fat dry milk, aseptic, and other dairy products.

• A producer of cheese and dairy powders, grated hard

Italian cheeses, dairy concentrates, seasonings, and

similar products for the foodservice industry.

• A leading manufacturer of private label soft drinks,

including juice, carbonated soft drinks, sport drinks, and

other beverages.

• A manufacturer and distributor of desserts, sour cream

products, and dips.

• A processor and distributor of milk and other dairy

products such as cultured yogurt, sour cream, cream,

cream cheese, and ice cream.

• A seafood distributor maintaining its own chain of

restaurants, offering a wide variety of frozen seafood items

including lobster, crab, and scallops.

• Multiple importers and distributors of fresh and frozen

seafood products to large national food wholesalers.

• Leading portion-controlled beef, pork, lamb, and poultry

cutting operations designated for the casual dining and

quick serve restaurant segments.

• A distributor of sweeteners, non-dairy creamers, croutons,

crunchy toppings, stuffing, breadcrumbs/cracker meals,

foodservice stuffing mixes, snacks, and snack mixes.

• A producer and distributor of ice cream and related

frozen goods.

• Vertically-integrated producers of high-quality coffees for

the restaurant and supermarket industries.

• A producer and distributor of various fruit juices, as well

as vitamin-enriched water and cocktail mixers.

• Producers and distributors of desserts, such as

frozen cheesecakes, gourmet cakes, mini desserts,

and brownies.

• A processor, packager, and distributor of nuts such as

pecans, cashews, almonds, and peanuts.

• An importer, producer, and bottler of olive oils, vinegars,

and specialty foods.

• Distributors of specialty food products, including pasta,

sauces, marinades, and fine artisan cheeses.

• A processor and distributor of snack and specialty foods,

such as roasted nuts and seeds, snack mixes, sesame

sticks, candies, and dried fruit.

GA has been involved in the liquidation of several food

processing and distribution companies, including South

Pacific Specialties, LLC; Metropolitan Foods; BSB, Inc.;

New Sam Woo Trading; Markel Johnson; and Gulf Shrimp

Company, as well as food processing, storage, and distribution

equipment for companies such as Winn Dixie, Maui

Pineapple Company, Humboldt Creamery, Loeb Equipment,

and Webvan. Food processing, storage, and distribution

equipment liquidated by GA included blow molding lines,

bagging machines, bottle conveyors, milk separators and

pasteurizers, filling lines, pizza manufacturing lines, vacuum

sealers, freezers and coolers, stainless steel tanks, liquid lines,

and frozen and refrigerated box trucks.

Experience

16 | MONITOR FOOD August 2017

Appraisal & Valuation Team

Daniel J. Williams

Managing Director

New York Region

(908) 251-3580

Kristi Faherty

Managing Director

(781) 429-4060

Chad P. Yutka, ASA

Managing Director, CAVS Group Head

(312) 909-6078

Jason Gomes

Associate Project Manager

(781) 429-4082

Michael Petruski

Executive Vice President

(818) 884-3737

BUSINESS DEVELOPMENT

OPERATIONS

Bill Soncini

Senior Vice President

Midwest Region

(773) 495-4534

David Seiden

Executive Vice President

Southeast Region

(404) 808-8153

Drew Jakubek

Managing Director

Southwest Region

(214) 455-7081

Jennie Kim

Vice President

Western Region

(818) 974-0602

Ryan Mulcunry

Executive Vice President

Northeast Region, Canada & Europe

(857) 231-1711

Monitor Information

The Food Monitor relates information covering most

commodity food products, including industry trends, market

pricing, and their relation to the valuation process. GA

internally tracks recovery ranges for beef, pork, poultry,

dairy products, seafood, coffee, sugar, corn, and fruits and

vegetables in all price points, but we are mindful to adhere

to your request for a simple reference document. Should

you need any further information or wish to discuss recovery

ranges for a particular segment, please feel free to contact

your GA Business Development Officer.

The information contained herein is based on a composite

of GA’s industry expertise, contact with industry personnel,

industry publications, liquidation and appraisal experience,

and data compiled from a variety of well-respected sources

believed to be reliable. GA does not make any representation

or warranty, expressed or implied, as to the accuracy or

completeness of the information contained in this issue.

Neither GA nor any of its representatives shall be liable

for use of any of the information in this issue or any errors

therein or omissions therefrom.

Great American Group is a leading provider of asset

disposition solutions and valuation and appraisal services to

a wide range of retail, wholesale, and industrial clients, as

well as lenders, capital providers, private equity investors,

and professional services firms. In addition to the Food

Monitor, GA also provides clients with industry

expertise in the form of monitors for the paper and

packaging, metals, chemicals and plastics, and building

products sectors, among many others. For more information,

please visit www.greatamerican.com.

Great American Group, LLC is a wholly owned subsidiary

of B. Riley Financial, Inc. (NASDAQ: RILY), a diversified

provider of collaborative financial and business advisory

services through several subsidiaries, including: B. Riley &

Co. LLC, a leading investment bank and a FINRA & SIPC

member, which provides corporate finance, research, and

sales & trading to corporate, institutional, and high net worth

individual clients; Great American Group, LLC; B. Riley

Capital Management, LLC, an SEC registered Investment

Advisor, which includes B. Riley Asset Management, a

provider of investment products to institutional and high net

worth investors, and B. Riley Wealth Management (formerly

MK Capital Advisors), a multi-family office practice and

wealth management firm focused on the needs of ultrahigh

net worth individuals and families; and Great American

Capital Partners, a provider of senior secured loans and

second lien secured loan facilities to middle market public

and private U.S. companies.

B. Riley Financial, Inc. is headquartered in Los Angeles

with offices in major financial markets throughout the

United States and Europe. For more information on B. Riley

Financial, Inc., please visit www.brileyfin.com.

About Great American Group

MONITOR FOOD GREATAMERICAN.COMAUGUST 2017800-45-GREAT

VOLUME

251LOS ANGELES (HQ)21255 Burbank Blvd.Suite 400Woodland Hills, CA 91367T 818.884.3737F 818.884.2976

CHARLOTTE, NC15720 Brixham Hill Ave.Suite 300Charlotte, NC 28277T 704.227.7161F 704.227.7171

ATLANTA1200 Abernathy Rd.Suite 1700Atlanta, GA 30328T 770.551.8115

WILTON, CT73 Old Ridgefield Road Suite 6Wilton, CT 06897T 203.663.5101

NEW YORKGraybar Building420 Lexington AvenueSuite 3001New York, NY 10170T 917.464.1521

MILWAUKEE10850 West Park PlaceSuite 970Milwaukee, WI 53224T 414.831.2850

BOSTON300 First AvenueSuite 201Needham, MA 02494T 781.444.1400F 781.444.1401

GERMANYPrinzregentenstr 18Fifth Floor 80538 Munchen, Germany

DALLAS17304 Preston Rd.Suite 720Dallas, TX 75252T 972.996.5630 F 972.996.5639

CHICAGO10 South LaSalle St.Suite 2170Chicago, IL 60603T 312.777.7950F 312.777.7948

AUSTRALIALevel 29, Chifley Tower 2 Chifley SquareSydney, NSW 2000 Australia

17 | MONITOR FOOD August 2017