gross pay deductions cpp ei - national magazine … pay deductions other full deposit ltd pension...

TRANSCRIPT

Gross Pay

Deductions

Other

Full DepositLTD

Pension

Federal TaxCPP

EI

Net Pay

22 june 2012 REPORT ON BUSINESS june 2012 REPORT ON BUSINESS 23

b y D O u G s T E I N E r

P h O T O G r a P h s b y a N G u s r O w E m a C P h E r s O N

Sometimes they lose millions of our money.

Sometimes they make a killing.

And now the brainiacs at Canada Pension Plan Investment Board have a daring strategy* to ensure our

retirements are golden(*hope they’re right!)

Who’s going to support

you?

june 2012 REPORT ON BUSINESS 25

obody likes losing every cent they have invested in some-thing. And $288 million is a lot to lose on one investment. Especially when it’s money that Canadians are expecting to retire on.

It was early 2011 when André Bourbonnais, the head of the private investing group at Canada Pension Plan Investment Board, got the news that Citibank, EMI Group’s secured creditor, had just seized the music pub-lishing company that CPPIB had started buying an inter-est in back in 2007. But Bourbonnais wasn’t at all shocked. CPPIB had already written down the investment.

The $288 million that had gone poof represented $17 from every one of the 17 million Canadians whom Bour-bonnais was investing for. But in this game, as in so many others, it’s lose some, win some—tomorrow would be another day. Even Bourbonnais’s boss, Mark Wiseman, who is executive vice-president, investments at the Board, is phil-osophical about this sort of setback: “If we don’t lose money in investments, we’re not taking enough risk.”

And, in fact, $288 million isn’t a lot of money in Bourbonnais’s job. CPPIB made more than 30 times the EMI loss for its fiscal year ended March 31, and recorded a return of 6.6% on its funds. The place had $153 bil-lion in assets as of Dec. 31 (that number grew to $162 billion as of March 31). And by the time I forget to slip on my Depends 20 years from now, CPPIB should be tracking close to half a trillion dollars under management, according to the actuaries.

We’d better hope they make the target. As countless politicians, think tanks and news stories have warned, Canadians are not saving enough on their own for their retire-ments. To make things worse, the tradition of company-funded defined-benefit pen-sions is eroding and, come 2023, Ottawa is going to make us wait longer for the Old Age Security benefit.

It all means the other basic federal pay-out for retirees—CPP—is under pressure to perform. So then—just where has that deduction on your paycheque been going all these years?

The model for investing that money has gone through a rapid evolution, leaving the sleepy world of government bonds far behind and culminating in something the CPPIB’s managers call “risk budgeting.” All told, CPPIB has emerged as one adventure-some investor.

It’s all run by investment professionals like Wiseman and Bourbonnais, guys who,

for some mysterious reason, think it’s more rewarding to invest on behalf of the Canadian public than make far more dough on the other side of the Street. As a Bay Street professional myself, I want to know what makes these guys tick.

PPIB owes its existence to the bad old days of the early 1990s, when Ottawa was creaking with debt. The CPP obligations that the federal gov-ernment had on the books amounted to only part of the fiscal shortfall, but it was a wakeup

call nonetheless. Previously, the government thought it was enough to simply collect money from Canadians’

paycheques and invest it in federal and provincial bonds. It was a safe way to invest money, but also self-serving because it kept the money in Ottawa.

Back in 1966 when the CPP took effect, nobody really had a clue how much a national pension scheme would cost. The government made a best guess at contribution rates based on how much it was paying out. In this pay-as-you-go scheme, contribution rates were low. For the first 20 years, the CPP slice was only 3.6%.

But by 1994, Canada had suffered through one recession in 1990-91 and was heading for another slowdown. Government bonds didn’t look so good any more: Some bonds were barely selling at auction, and others had been downgraded from AAA to AA+ by Standard & Poor’s.

So just investing in bonds wouldn’t be enough. The future burden of the CPP, lumbering along with its fixed-income portfolio, stuck out like a sore thumb in each year’s parlia-mentary budget reports.

At both the federal and provincial levels, the idea bub-bled up that responsibility for investment of the funds should be taken away from the government. That way, politicians wouldn’t be on the hook for potentially poor investment performance. The CPPIB was conceived in get-rid-of-the-problem meetings beginning in 1994, and the CPPIB was founded in 1997.

In Paul Martin’s 1998 federal budget, the CPP was moved on from pay-as-you-go financing. Ottawa jacked up contribution rates from slightly more than 6% of pay to 9.9% (subject to a maximum dollar value). The increase allowed for both the demographic bulge of boomers head-ing for retirement and the additional cash flow needed to make up for past miscalculations.

John MacNaughton, who had recently retired as the president of investment firm Nesbitt Burns, became CPPIB’s first CEO. On his watch, a portion of the cash coming in from CPP contributions was moved into the equity market in a broad-based index portfolio.

The CPPIB had to take on risk to make better returns, it was true. But in the opinion of early members of the CPPIB team, making all the equity investments in Canada would be a whole other type of risk, written into federal pension laws that allowed only a small percentage of equity port-folios to be invested internationally. That was fixed with a change of the law in 2005, and since then the fund has been able to buy anything that is legal in Canada.

Under David Denison, who has been CEO since 2005, CPPIB has proven its savvy in passive equity investments and also lately in private equity. In fact, in less than a decade, CPPIB has stepped up a league, and it’s Denison

who gets the credit for turning the fund into a respected global giant. With the possible exception of the Caisse de dépôt et placement du Québec, it has eclipsed all the other major Canadian public pension funds, some of which have been in business much longer. That league includes Teachers’ and OMERS in Ontario, PSP Investments and British Columbia Investment Management Corp.

Many major funds now share what was originally a provocative (and, we’d like to think, made-in-Canada) idea, of which CPPIB was an early adopter: Instead of paying outside fee-taking managers, practise do-it-yourself mega-investing. It’s just cheaper to do it that way. But that works for the long term only if you’re smart enough to keep up with your competition. Unfortunately, every-one else on the planet now has the same idea.

CPPIB’s quest, stated most simply, is to find long-term investments that have predictable cash flow. “Long-term” to CPPIB is decades. It doesn’t

matter if anyone at CPPIB likes music (EMI), or drives cars on toll highways (Ontario’s Highway 407), or makes video calls to Uzbekistan (Skype). They know lots of people do, and that means cash flow, and cash flow for a long, long time means sustainability. When you think that way, EMI really was a good investment idea: Sales of recordings are down, but song-publishing rights can produce consistent revenues from year to year.

Starting this July, CPPIB will have a new leader—cur-rent head of investment Mark Wiseman. There’s a reas-suring continuity here. For the last seven years, Denison and Wiseman have been a design-and-execute team as the fund has morphed and grown. “I think Denison’s legacy was that he raised the bar for other pension funds in Can-ada,” says Tim Hodgson, a former head of Goldman Sachs Canada who helped Denison and then Wiseman rise through the investment ranks. “Mark and David taught a bunch of people how fast you can move in investments. Firms like ADIA [Abu Dhabi Investment Authority] can take as long as six months to make up their mind.” CPPIB’s relative speed is a competitive advantage, Hodgson says.

Denison is all about process. Wiseman is all about events. Denison, although taciturn by nature, has made it a habit to meet every new employee in the firm per-sonally. Given the growth of the staff, what started out as one-to-ones has grown into group breakfasts. At Fidel-ity, where Denison was head of the Canadian operations, he was known as a superintelligent but control-obsessed manager. He has apparently mellowed in the Canada Pen-sion job. But the bone-thin executive still gets up at 4:30 to run 10 kilometres before he shows up for work at 7:30.

24 june 2012 REPORT ON BUSINESS

N

CCountless

warnings hold that Canadians are not saving

enough for retirement

IN LESS THAN A DECADE, CPPIB HAS STEPPED UP A LEAGUE; DAVID DENISON IS CREDITED WITH TURNING IT INTO A RESPECTED GLOBAL GIANT

26 june 2012 REPORT ON BUSINESS june 2012 REPORT ON BUSINESS 27

he design-and-execute team is now just execute. At 42, Wiseman looks too young for the job until you check his resumé. A lawyer

and Fulbright Scholar who also has an MBA, he started his career with a dream legal job—apprenticing as a law clerk for Supreme Court Jus-tice Madame Beverley McLachlin in Ottawa. Wiseman then moved to Paris with his girlfriend, Marcia Moffat, and worked on deals with storied Wall Street law firm Sullivan & Cromwell.

In 2000, Wiseman and Moffat moved back to Toronto, he to work with investment über-mensch Brent Belzberg at Belzberg’s Harrowston Corp. (Moffat now runs the mortgage business at RBC.) Belzberg, one of the most focused and best-connected private equity manag-ers in Canada, remembers Wiseman as a “force of nature,” and also highlights his obsessive focus on finding the best investments. To Belzberg, Wiseman epitomizes a famous saying of former Intel CEO Andy Grove: “Only the para-noid survive.”

Wiseman, still in his 20s at Harrowston, had already established a reputation for working brutal hours and answering all e-mails within minutes (which is still true today). He quit Harrowston after it was sold to TD Capi-tal in September, 2001. When he turned down Belzberg’s offer to help start a new investment firm, Wiseman was at loose ends. “No one was hiring after 9/11, and I thought it was over,” he says with a smile. But he didn’t have to wait long for an offer. He received a call from Jim Leech in the private equity investing group at Ontario Teachers’ Pen-sion Plan. Wiseman soon began a four-year stint there.

Wiseman potentially has almost a quarter of a century of managing the investment board before he gets his own CPP payments. He states his goal simply: “to find a group of people, and manage them to make sure that the invest-ments they make will do better than picking just anything to buy.”

When pushed to name some of the issues the Board has to deal with, all that senior managers talk about is mini-mum investment size. If each investment were as “small” as $150 million, that’s more than 1,000 investments to manage—an oversight nightmare. CPPIB’s minimum investment cutoff now is in the range of $75 million to $100 million for private equity investment. That cuts out a lot of interesting opportunities.

A related issue is the how-to and who-to and when-to of selling large-scale investments. It’s one thing to write a cheque; it’s another to convert an investment into cash. Public markets are tricky, and CPPIB will eventually get stuck with some albatrosses.

Hiring is also a special issue at CPPIB. Attempts to find great people can be a little stressful for management. A couple of times, Wiseman and his team have had people bail at the last minute after signing up to work in senior positions at the firm. Wiseman takes it all very personally. He realizes that the issues for the last-minute walk-aways have been complicated, including rigorous competition for talent from the companies the Board invests with. The big issue is the superior compensation the private sector can offer.

Yet to any normal working person, the compensation received by senior management and the investing staff at CPPIB is plenty generous. Wiseman made north of $3.1 million in fiscal 2011; yet, to prospective hires, he says, “Don’t come here looking for a fat paycheque.” He and others liken their job to a public service—and there is indeed some sacrifice involved, but only by the standards of the investment industry.

In any case, there are other attractions to working at CPPIB. Ask Eric Wetlaufer, 50, the first senior executive who is not Canadian to make the move from the heady investment world in the U.S.

“I’m an investor, full stop,” says Wetlaufer, who has been running active investing for the fund for less than a year. He came because he thought he would find the perfect world of investing. No restrictions on where to look and what to put money into. No cap-in-hand looking for money for a new fund every five years or so. Equi-ties, fixed income, commodities, short-horizon trading, strategic stakes in public companies, they’re all good. An investment job “where we are limited only by our creativ-ity” is, to him, a dream job. Then he stops himself: “Wow, that sounds a lot like Disney.”

And there’s another thing, he says: “I really like my boss.” Indeed, Tim Hodgson counts another competitive advantage in CPPIB’s ability, led principally by Wiseman and Denison, for finding and keeping investment talent for the firm.

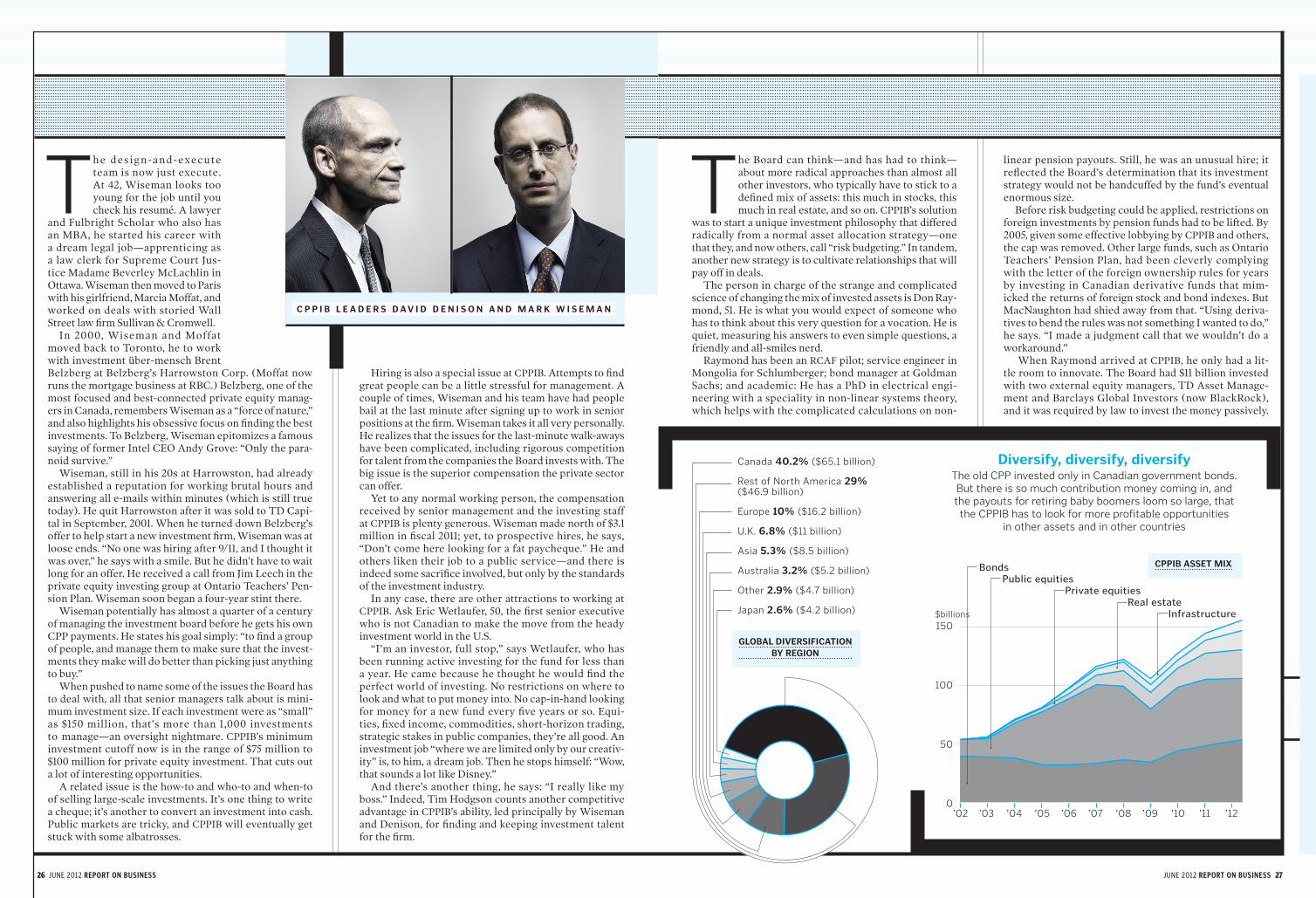

he Board can think—and has had to think—about more radical approaches than almost all other investors, who typically have to stick to a defined mix of assets: this much in stocks, this much in real estate, and so on. CPPIB’s solution

was to start a unique investment philosophy that differed radically from a normal asset allocation strategy—one that they, and now others, call “risk budgeting.” In tandem, another new strategy is to cultivate relationships that will pay off in deals.

The person in charge of the strange and complicated science of changing the mix of invested assets is Don Ray-mond, 51. He is what you would expect of someone who has to think about this very question for a vocation. He is quiet, measuring his answers to even simple questions, a friendly and all-smiles nerd.

Raymond has been an RCAF pilot; service engineer in Mongolia for Schlumberger; bond manager at Goldman Sachs; and academic: He has a PhD in electrical engi-neering with a speciality in non-linear systems theory, which helps with the complicated calculations on non-

linear pension payouts. Still, he was an unusual hire; it reflected the Board’s determination that its investment strategy would not be handcuffed by the fund’s eventual enormous size.

Before risk budgeting could be applied, restrictions on foreign investments by pension funds had to be lifted. By 2005, given some effective lobbying by CPPIB and others, the cap was removed. Other large funds, such as Ontario Teachers’ Pension Plan, had been cleverly complying with the letter of the foreign ownership rules for years by investing in Canadian derivative funds that mim-icked the returns of foreign stock and bond indexes. But MacNaughton had shied away from that. “Using deriva-tives to bend the rules was not something I wanted to do,” he says. “I made a judgment call that we wouldn’t do a workaround.”

When Raymond arrived at CPPIB, he only had a lit-tle room to innovate. The Board had $11 billion invested with two external equity managers, TD Asset Manage-ment and Barclays Global Investors (now BlackRock), and it was required by law to invest the money passively.

Diversify, diversify, diversify The old CPP invested only in Canadian government bonds. But there is so much contribution money coming in, and the payouts for retiring baby boomers loom so large, that the CPPIB has to look for more profitable opportunities

in other assets and in other countries

150

100

50

0’02 ’03 ’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12

$billions

GLObaL DIvErsIFICaTION by rEGION

C P P I b L E a D E r s D av I D D E N I s O N a N D m a r k w I s E m a N

T T

Bonds Public equities Private equities Real estate Infrastructure

CPPIb assET mIX

Canada 40.2% ($65.1 billion)

Rest of North America 29% ($46.9 billion)

Europe 10% ($16.2 billion)

U.K. 6.8% ($11 billion)

Asia 5.3% ($8.5 billion)

Australia 3.2% ($5.2 billion)

Other 2.9% ($4.7 billion)

Japan 2.6% ($4.2 billion)

comes from CPPIB’s sheer heft and from not paying exter-nal managers. (The Board does outsource work that falls below its minimum-investment thresholds, to the tune of more than $500 million in management and performance fees in 2011.)

In competing with others who also have billions to invest in good ideas, CPPIB has a mantra: “We’re here, we’re steady and we are not going away.” The goal is simple—to be the first call from anybody selling anything that might be valuable for CPPIB to buy.

Much of the job of letting everybody know who CPPIB is and how much money that it has to invest was com-pleted many years ago. Now the direction is reversed. Sit-ting quietly in the Board’s 26th-floor lobby in downtown Toronto on any given weekday are salespeople from all over the world, waiting to offer their asset wares to a very hungry investor.

he job of getting excess return is really about finding unique investments. That job largely rests with Bourbonnais, who runs private investments and took the EMI hit. He personi-fies the competitive-investor cast of CPPIB in

28 june 2012 REPORT ON BUSINESS june 2012 REPORT ON BUSINESS 29

Shortly thereafter, however, these restrictions were removed, and Ray-mond moved quickly to establish internal passive management and hire external managers who could invest actively in equities and deploy currency hedging strategies for for-eign holdings.

Raymond is widely credited with coming up with two radical ideas for investing. He believed that there was no point in hiring external asset managers if they didn’t beat the CPPIB’s benchmark equity portfo-lio, mostly consisting of index-fund-type investments based on the S&P/TSX 60, S&P 500 and others. He came up with a plan to allow managers to target portions of the portfolio and substitute other investments that they figured would per-form better. The managers were only paid if they outper-formed. Few took up the challenge, but a couple did so and have consistently beat their targets.

Raymond also recommended to his board that they should adopt the novel risk-budgeting approach. Simply

put, all assets have risk, and each one behaves in a particular way. Raymond and his team’s strategy was to “bud-get” for the amount of risk each asset class had, and then focus on finding investments that would generate a higher return for taking the same amount of risk, regardless of whether the investments were in the same asset class or not.

This meant doing a massive amount of research into the behav-iour of different assets. Real estate, for example, exhibits different return characteristics based on project age and size. A new apartment building

has many of the same potential risks and rewards as the shares of a new company—it has big start-up costs, and the upside comes from the growth of revenue and profits as the buildings fill up. Old buildings or shopping malls are like bonds—start-up costs have been amortized, and they provide a steady stream of income.

Raymond’s idea could be tested. He asked external equity portfolio managers to target portions of the port-

folio the CPPIB already had—which would be the bench-mark—and propose alternatives. The essence of the strat-egy is telling money managers who claim that they can do better that they will only be paid if they tell the truth.

From the other side of the investing equation—sell-ers—CPPIB has a sticky sort of pitch. The size of its mar-keting literature speaks to this. The paper version of the CPPIB’s pitch deck—its spiel for potential partners—is 40% smaller than its competitors’. It’s the elevator pitch, which goes something like this: “We do our homework ahead of time, we move faster, we’ll stay far longer, and might buy everybody out at the end, and we’re nice.” Time will tell if they can keep all their promises.

To a private equity firm looking for dough, the pitch is compelling. CPPIB now has access to, and investments in, the largest private equity funds in the world. With more money than most could handle, the fund gets preference in “co-investing”—putting up money beside the PE out-fits in deals that might be too large even for the largest firms to handle.

By all accounts, CPPIB competes effectively in the mar-ket of global investing. That said, it seems short-sighted that it has only two foreign offices, in London and Hong Kong. After all, there are other giant pools of capital around the world trying to do almost exactly the same thing as CPPIB.

Even though it ranks in the pack of supersize funds globally, the Board got started a long time after some others, and it is not the largest by any stretch. The United Arab Emirates, for example, has $627 billion (U.S.) to invest. Also in the big leagues is Norway, which real-ized that it ought to save some of its North Sea oil revenues for a rainy day. It has $560 billion (U.S.) in its kitty. China, meanwhile, has a positive balance of payments so high that it invests through two funds that together have about $1 trillion (U.S.) under management.

Given the size of these pools of capi-tal, efficiency and scale of investing is a hot topic these days. Last year, two University of Toronto academics, Alex-ander Dyck and Lakasz Pomorski, tried to figure out if managing more money meant more efficiency. They looked at the efficacy of funds both large and small, both internally and externally managed, and found that larger plans outperform smaller ones by almost half a per cent annually. Half a per cent doesn’t sound like much until you man-age $160 billion. That’s $800 million a year extra for Canada’s pensioners that

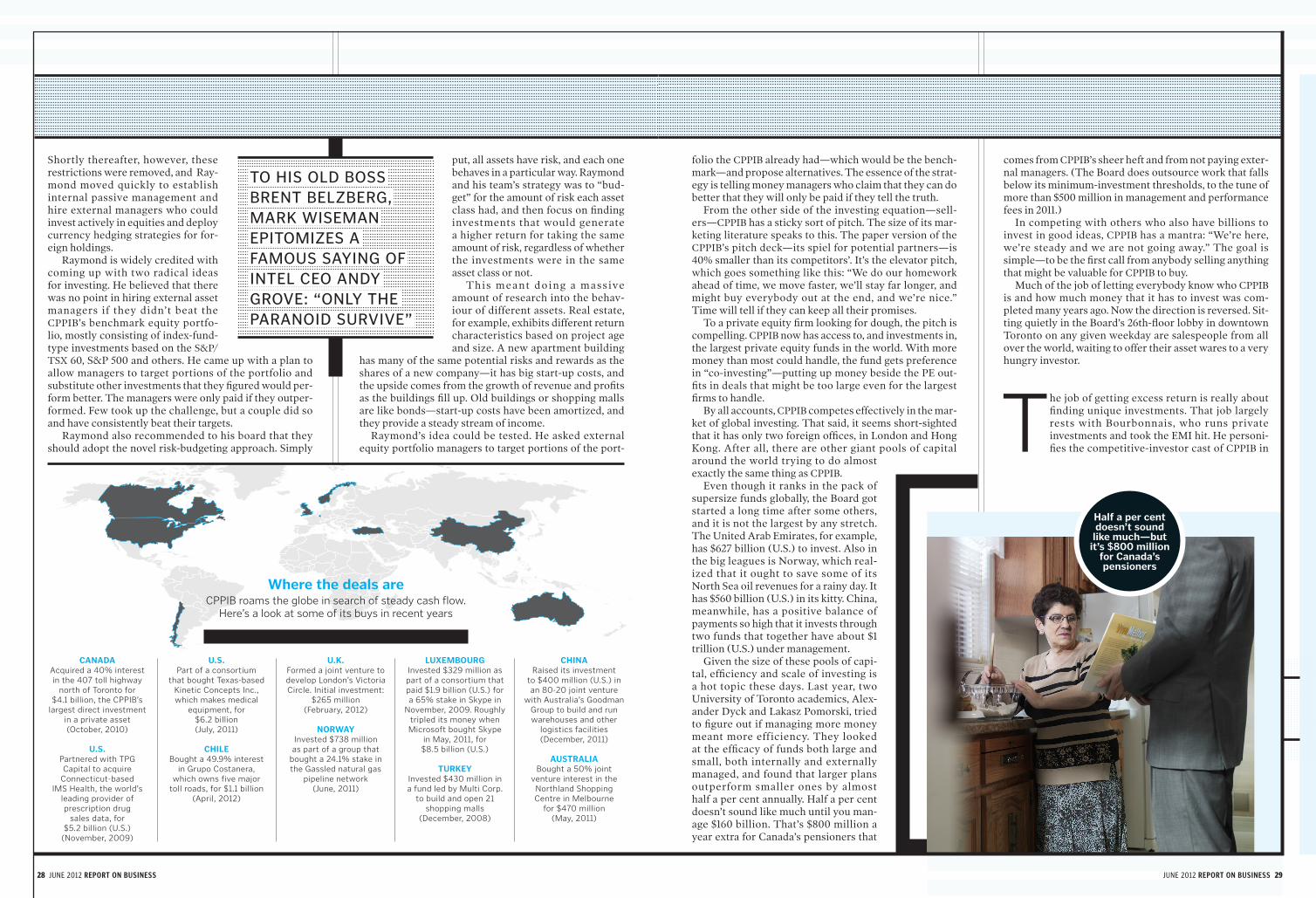

CaNaDaAcquired a 40% interest in the 407 toll highway

north of Toronto for $4.1 billion, the CPPIB’s

largest direct investment in a private asset (October, 2010)

u.s.Partnered with TPG Capital to acquire

Connecticut-based IMS Health, the world’s

leading provider of prescription drug

sales data, for $5.2 billion (U.S.)

(November, 2009)

u.s. Part of a consortium

that bought Texas-based Kinetic Concepts Inc., which makes medical

equipment, for $6.2 billion (July, 2011)

ChILE Bought a 49.9% interest

in Grupo Costanera, which owns five major

toll roads, for $1.1 billion (April, 2012)

u.k.Formed a joint venture to develop London’s Victoria Circle. Initial investment:

$265 million (February, 2012)

NOrwayInvested $738 million as part of a group that

bought a 24.1% stake in the Gassled natural gas

pipeline network (June, 2011)

LuXEmbOurGInvested $329 million as part of a consortium that paid $1.9 billion (U.S.) for a 65% stake in Skype in

November, 2009. Roughly tripled its money when Microsoft bought Skype

in May, 2011, for $8.5 billion (U.S.)

TurkEyInvested $430 million in a fund led by Multi Corp.

to build and open 21 shopping malls

(December, 2008)

ChINaRaised its investment

to $400 million (U.S.) in an 80-20 joint venture

with Australia’s Goodman Group to build and run warehouses and other

logistics facilities (December, 2011)

ausTraLIaBought a 50% joint

venture interest in the Northland Shopping Centre in Melbourne

for $470 million (May, 2011)

where the deals are CPPIB roams the globe in search of steady cash flow.

Here’s a look at some of its buys in recent years

TO HIS OLD BOSS BRENT BELZBERG, MARk WISEMAN EPITOMIZES A FAMOUS SAYING OF INTEL CEO ANDY GROVE: “ONLY THE PARANOID SURVIVE”

half a per cent doesn’t sound like much—but

it’s $800 million for Canada’s pensioners

T

30 june 2012 REPORT ON BUSINESS

2012. He flies his own plane for sport. It’s a Cirrus SR20, a plane that comes with its own parachute so it can coast to the ground if the engine conks out. That’s a little like having a hedge on adventure.

The confidence is quiet in Bour-bonnais, but firm. When asked if he gets mad when he hears about a large potential investment that CPPIB wasn’t informed of, he responds, “I’m pissed, but it doesn’t happen very often.” He has more than 100 people who not only follow investments, but who have models for assets not yet for sale. They also track competitor investors and their abilities to stay with their assets over the long term.

According to Wiseman, CPPIB was “very underwa-ter” on some investments at one point during the credit crisis in 2009. But while the market value of its portfo-lio was way down, it wasn’t under pressure to sell near the bottom to raise cash—the way many mutual funds, hedge funds and pension fund managers were, because their clients were bailing on them. And the CPPIB still had money—more than half a billion a month—coming in from contributions.

It was a huge structural advantage. The investment team realized that there could be assets for sale from other investors who were forced to sell. Speed at deci-sion-making, advance preparation and the ability baked into the fund based on risk budgeting—and not a percent-age allocation to certain asset classes—turned CPPIB into one of the few games in town (that would be the global town) for making investments.

When the market turned bad, funds that had allocation maximums for certain asset classes were forced to sell. CPPIB stepped in, for instance, when CalPERS, the fund that invests the retirement assets for employees of the State of California, had too much money in private equity investments compared to its equity holdings. Since 2008, CPPIB has scooped up $3.6 billion in such investments from 19 parties.

More daring, perhaps, was the investment in the Cana-dian asset-backed commercial paper market. Some of the paper was bank-backed, some not—and the latter type went all pear-shaped and no-bid ugly in the fall of 2007, contaminating the bank-backed stuff in investors’ minds as well. Canadian banks, and other large funds, had all been active in the now-frozen market. CPPIB stepped in and bought nearly all the bank-issued asset-backed paper available in the industry, or nearly 40% of the market, at a large discount. The paper was later sold for a large profit as the market stabilized.

Another substantial investment that the Board made during this time was in the 407 toll highway north of

Toronto. The highway was originally funded by the province and then leased in 1999 to a consortium that included a subsidiary of Spanish construction colossus Ferrovial, Montreal-based SNC-Lavalin and, later, Macquarie Infrastructure Group from Australia. But by 2009, both Ferrovial and Mac-quarie had run into issues with their investors thanks to the recession, and became motivated sellers.

The private investment team had its eyes on the asset because it was in the CPPIB’s sweet spot. The 407 can charge as much as it likes, and there is no prospect of new competition.

The fund was looking to pick up the Macquarie piece, and had an agreement to buy part of the Ferrovial stake in place. But then SNC-Lavalin tried to step in front by exercising its right of first refusal on the Ferrovial stake; SNC-Lavalin planned to flip its interest into a public vehi-cle in 2010 at a price roughly 25% higher than CPPIB was bidding.

That almost scuppered the deal. Fortunately, the mar-ket realized that large assets can’t be bought at a discount by one investor, and sold at a premium at the same time by another, and the SNC IPO ended up dead in the water. CPPIB got its piece: 40% of the highway at a cost of $4 bil-lion. It has since syndicated part of the stake, reducing its share to 29%.

As we’ve seen, the team doesn’t spend a lot of time look-ing around for smaller deals. They leave that to outside managers. On the other hand, one thing CPPIB does look for is the ability to top up existing investments. It makes sense: no more work and better returns, if the investment is performing well.

More money will flow into the fund if Ottawa acts on the idea of forcing Canadians to save more for their retirements by simply raising contributions. Wiseman confirms the fund is prepared. I’m in, but can they handle a trillion dollars under management? That kind of kitty could be a possibility.

And what happens if the CPPIB team turn out to be the worst investors the world has ever seen, and lose most or all of the money? Notwithstanding all of the checks and balances in place, Wiseman cracks a smile and says, “If they raise the amount taken off your paycheque by 50%, in less than five years we’re right back where we are now.”

When he puts it that way, it sounds a little like all this investing is a bit of a high-paid make-work project for a bunch of people. But more likely, as long as we’re all invest-ing, driving our cars on toll highways, making long-dis-tance calls on our laptops and listening to Coldplay on our iPods, what CPPIB is really doing is quite simple: making sure we’re all ready for when our earning days are over.

ONTARIO’S 407 TOLL HIGHWAY IS IN CPPIB’S SWEET SPOT: THE 407 CAN CHARGE AS MUCH AS IT LIkES, AND THERE IS NO PROSPECT OF NEW COMPETITION