growth potential of عﺎﻄﻘﻟا ﻲﻓ مﺎﺴﻳﻹا private education

TRANSCRIPT

الإيسام في القطاع الحكومي بالمملكة

العربية السعوديةقيــــاس فعــاليــــة وكفــــــاءة

الممـــارســــــات الحــــــــالــيـــــة

Growth Potential of Private Education in Saudi Arabia

SEP. 2018

By Strategic Gears Management Consultancy

22 2

المقدمةوالملخص التنفيذي

العودة إلى قائمة المحتويات3

Table of Content

Executive Summary ...........................................................................3

Introduction ......................................................................................... 6

Regional comparison of private education market ............... 8

Challenges facing Saudi Education Market ...............................11

Private education potential in Saudi Arabia ............................15

Conclusion ...........................................................................................18

32 3 3

المقدمةوالملخص التنفيذي

العودة إلى قائمة المحتويات3

Executive summary

44 4

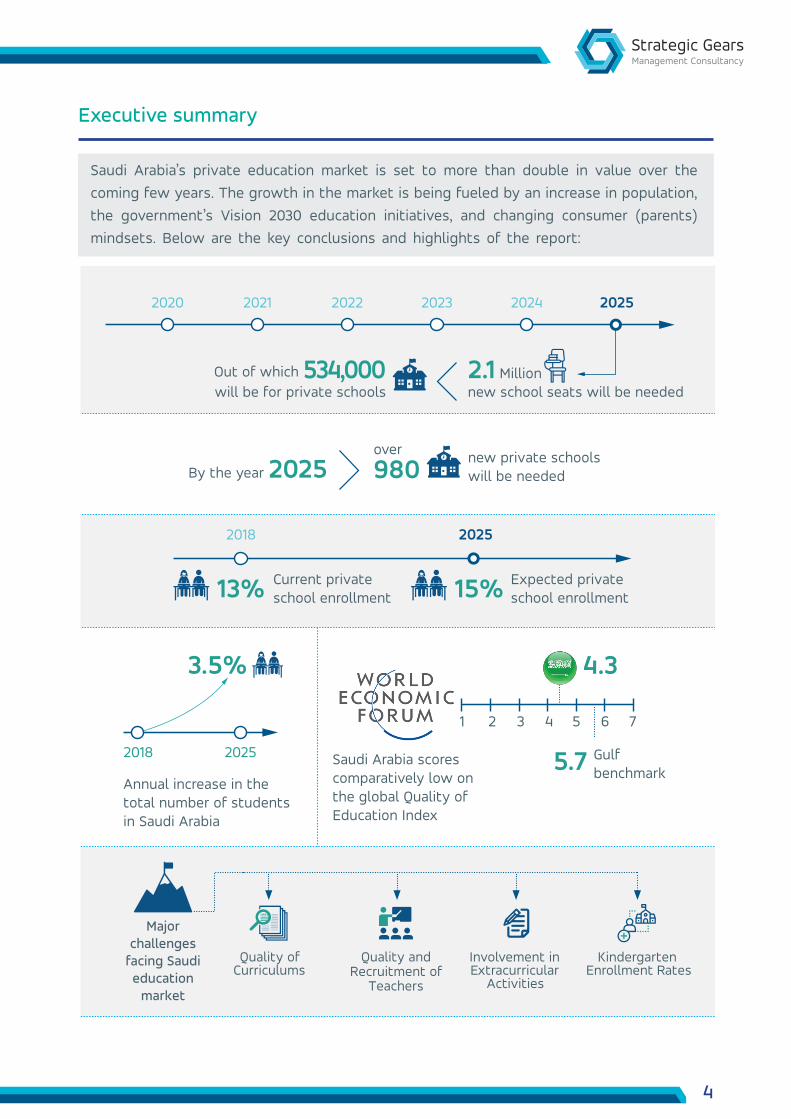

Saudi Arabia’s private education market is set to more than double in value over the coming few years. The growth in the market is being fueled by an increase in population, the government’s Vision 2030 education initiatives, and changing consumer (parents) mindsets. Below are the key conclusions and highlights of the report:

Executive summary

2020

2018 2025

2018 2025

2021 2022 2023 2024 2025

13%

3.5%

2025 980

2.1 Millionnew school seats will be neededwill be for private schools

Current private school enrollment

new private schools will be needed

over

534,000

15%

4.3

5.7

Expected private school enrollment

Gulf benchmark

Saudi Arabia scores comparatively low on the global Quality of Education Index

Annual increase in the total number of students in Saudi Arabia

By the year

Major challenges

facing Saudi education

market

Quality of Curriculums

Quality and Recruitment of

Teachers

Involvement in Extracurricular

Activities

Kindergarten Enrollment Rates

1 2 3 4 5 6 7

Out of which

54 5 5

The government has set a goal to raise

to

Saudi Arabia's international test scores in mathematics and science are low and decreasing. In order to reverse this trend, national curricula must be drastically improved or more international curriculums must be adopted.

The quality of teachers in schools is still low

in 2016 10 hours18 hours

15%

14.9%

55%2016

The average number of annual professional development hours completed by teachers

The government has set a target involvement by the year 2020

by the year 2020

Only

of Saudi students were involved in extra curricular activities

Kindergarten enrollment rates remain the lowest in the GCC at

Kindergarten enrollment rates are expected to reach

13%SR

2013 2017

in the year

to reach

17% by the year 2020, far from the governments

27.2%target of

Consumer spending on education increased by 13% over the past 5 years in Saudi Arabia, indicating the growing preference given to a quality education.

66 6

Introduction

76 7 7

The Kingdom of Saudi Arabia is undergoing rapid changes in many different Industries due to its Vison 2030 initiatives. One such industry is the education sector, specifically the Private K-12 market which is set to more than double in value from $5 Billion currently to over $12 Billion by 2023.

Education plays a key role in achieving Saudi Arabia’s Vision 2030 targets. Improving the access and quality of education would create a thriving economy by enabling the population to meet growing labor market demands. Furthermore, it would create a vibrant & ambitious society who are socially responsible and able to lead a fulfilling life.

In 2016, the Saudi government developed the National Transformation Program 2020 to fulfill some of the objectives of Vision 2030. As part of the plan, the ministry of education was tasked with 8 key objectives to transform the education industry in Saudi Arabia, which in turn would strengthen the economy and provide the Saudi citizens with the key skills to become more competitive in the local and global labor market.

As it stands, there are approximately 7.7 million students in Saudi Arabia, out of which 6.7 million (87%) attend public schools and 1 million (13%) attend private schools. There are a total of 30,625 schools in Saudi Arabia, out of which 26,248 (86%) are public and 4,377 (14%) are private. Between the years 2013 and 2017, the number of private schools grew by 13%, while the number of public schools grew by 1%.

Certain factors are affecting the education landscape including the governments push for privatization, the need for overall improvement in the quality of education, and consumers growing preference for private schools that offer value for money.

In this report we focus on private education in Saudi Arabia by looking at the overall GCC private education market and Saudi Arabia’s position in it, challenges facing the Saudi education market that need to be addressed, and the size of the opportunity for the private education market.

Introduction:

88 8

Regional Comparison of Private Education Market

98 9 9

Saudi Arabia’s current private education market is valued at $5 Billion, only slightly greater than the UAE’s which is at $4.3 Billion. Given that Saudi Arabia’s population is more than 3 times larger than the UAE’s indicates the huge potential for growth. Kuwait’s market stands at $1.2 Billion followed by Oman at $1 Billion respectively. Given its small population, Bahrain’s private education market size is the smallest in the GCC at $0.4 Billion.

The UAE has the highest private school enrollment in the GCC at 74%, while in Saudi Arabia public schools dominate, leaving only 13% enrollment for private schools. The government of Saudi Arabia is aiming to push private school enrollment up to 25% by the year 2020.

When it comes to private international schools, Saudi Arabia only has 7 international schools per 1 million people, while the GCC average is 31 international schools per 1 million people. This indicates the huge potential that the Saudi private education market has, particularly for high quality schools that offer international curriculums.

Dubai and Abu Dhabi are the top two cities in the GCC with the highest number of international schools. Riyadh and Jeddah on the other hand, have a significantly lower amount of International Schools.

Source: Saudi MoE; UAE MoE; Kuwait Central Statistical Bureau; Bahrain MoE; World Bank

Source: International Schools ConsultancySource: SG Analysis; International Schools Consultancy; World bank

Regional Comparison of Private Education Market:

74

26

UAE

35

65

Kuwait

32

68

Bahrain

23

77

Oman

13

87

KSA

Figure 1: Private vs. Public School Enrollment (%)

Private Public

120

100

80

60

40

20

0

!

!

!

!

!

!

!

!

!

7

31

35

30

25

20

15

10

5

0

Saudi Arabia GCC Average

Figure 2: Number of International Schools (Per 1 Million People)

281

Dubai

151

Abu Dhabi

83

Riyadh

82

Jeddah

Figure 3: Number of International Schools in various cities

1010 10

It is important to note that while the GDP per capita for both Saudi And UAE has dropped over the past 5 years, consumer expenditure on education for Saudi Arabia has risen by 13% over the same period and has decreased for the UAE by 18%.

Case Study: United Arab Emirates vs. Saudi Arabia

9.3 Million

UAE Saudi Arabia

8.1 Million (88% of total)

$4.3 Billion

$7 Billion

$4,600

-British-IB

32.3 Million12 Million (37% of total)

$5 Billion

$12 Billion

$4,400

-Saudi-American

Expat PopulationTotal Population

Current Private education market value

Expected 2023 market value

Prevalent Education Systems

Average tuition fee per year (Private schools)

Figure 4: Consumer Expenditure on Education (USD Per Household)

5,000

4,000

3,000

2,000

1,000

02013 2014 2015 2016 2017

UAE Saudi ARabia

Source: Euromonitor

UAE and Saudi Arabia have completely opposite education markets. Due to its high expatriate population and higher income levels, the UAE has an oversupply of International Schools that offer premium level quality. Because of this, the major challenge facing the UAE education market is student retention, as tuition prices have reached an unsustainable level. As a result, the UAE government has recently halted an increase in tuition prices.

Saudi Arabia on the other hand has a low amount international schools, since much of the expatriate population is of a low income level and Saudi citizens weren’t allowed to attend international schools until a few years back. When compared to the UAE, Saudi Arabia’s education market faces more fundamental challenges such as the quality of curriculums and teachers which needs to be addressed first if the country aims to build a thriving knowledge based economy.

1110 11 11

Challenges facing Saudi Education market

1212 12

Challenges Facing Saudi Education Market:

Saudi Arabia’s education sector faces challenges on many fronts including quality of education, quality and recruitment of teachers, involvement in extra curricular activities and kindergarten enrollment. These challenges must be addressed in order to reach the ambitious targets set by the government to reach high international standards in education. Below are the highlights of each challenge:

1.Quality of Education

One of the aims of Saudi Arabia’s Vision 2030 program is to build a thriving economy and a fundamental part of that is to improve the access and quality of education.

Due to outdated curriculums and low quality of teachers, Saudi Arabia generally ranks low on global education rankings. According to the World Economic Forum, Saudi Arabia’s overall quality of education scores 4.3 (Out of 7) on the global index scale, significantly lower than the GCC benchmark of 5.7 and even farther away from the International benchmark of 6.1.

*TIMMS = Trends in International Math and Science Study TIMMS is conducted by the International Association for the Evaluation of Educational Achievement

International test scores for Saudi Arabia in math and science (TIMMS)* dropped significantly between 2011 and 2015. 4th grade and 8th grade math scores dropped by 7%, while 4th and 8th grade science scores dropped by 10%. In order to improve the scores, significant efforts must be made in either upgrading the national curriculum or adopting more international curricula.

4,3

5,76,1

7

6

5

4

3

2

1

0

Saudi Arabia GCC Benchmark Int. Benchmark

Figure 5: Quality of Education Scores (World Economic Forum-2017)

Scale of 1-7 (With 7 being best)

Figure 6: 4th Grade Math Figure 7: 8th Grade Math

0 200 400 600 800 0 200 400 600 800

Int. Benchmark

Regional Benchmark

Saudi Arabia(2015)

Saudi Arabia(2011)

Int. Benchmark

Regional Benchmark

Saudi Arabia(2015)

Saudi Arabia(2011)&

&!"#$٪&"#'()

Figure 8: 4th Grade Science Figure 9: 8th Grade Science

0 200 400 600 800 0 200 400 600 800

Int. Benchmark

Regional Benchmark

Saudi Arabia(2015)

Saudi Arabia(2011)

Int. Benchmark

Regional Benchmark

Saudi Arabia(2015)

Saudi Arabia(2011)&

& *('٪+(٪

Mathematics

Science

1312 13 13

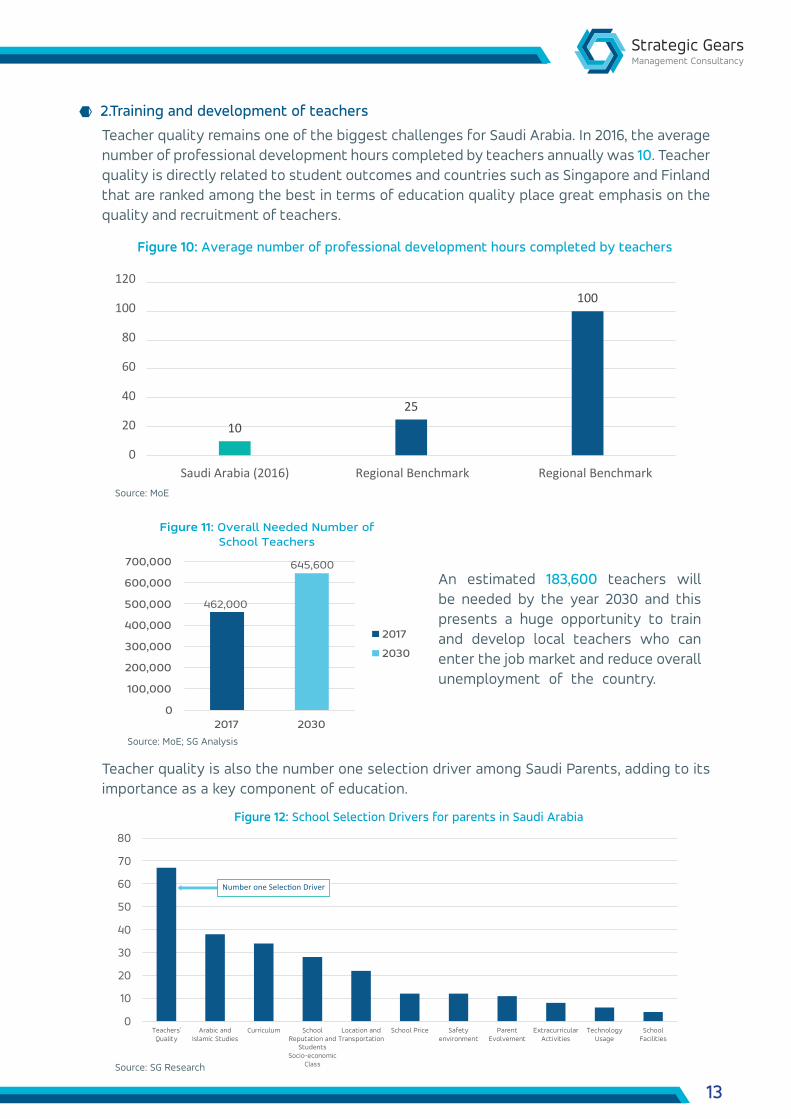

2.Training and development of teachers

Teacher quality remains one of the biggest challenges for Saudi Arabia. In 2016, the average number of professional development hours completed by teachers annually was 10. Teacher quality is directly related to student outcomes and countries such as Singapore and Finland that are ranked among the best in terms of education quality place great emphasis on the quality and recruitment of teachers.

Teacher quality is also the number one selection driver among Saudi Parents, adding to its importance as a key component of education.

An estimated 183,600 teachers will be needed by the year 2030 and this presents a huge opportunity to train and develop local teachers who can enter the job market and reduce overall unemployment of the country.

Source: MoE; SG Analysis

10

25

100120

100

80

60

40

20

0Saudi Arabia (2016) Regional Benchmark Regional Benchmark

Figure 10: Average number of professional development hours completed by teachers

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2017 2030

2017

2030

Figure 11: Overall Needed Number of School Teachers

462,000

645,600

&

&

&

&

&

&

&

&

&

&0

10

20

30

40

50

60

70

80

Teachers'Quality

Arabic andIslamic Studies

Curriculum SchoolReputation and

StudentsSocio-economic

Class

Location andTransportation

School Price Safetyenvironment

ParentEvolvement

ExtracurricularActivities

TechnologyUsage

SchoolFacilities

Number one Selection Driver

Figure 12: School Selection Drivers for parents in Saudi Arabia

Source: MoE

Source: SG Research

1414 14

100

80

60

40

20

02016 2017

79 81

13 13.9 14.9 15.9 17

2018 2019 2020

Figure 14: % of Kindergarten Enrollment among Saudi Population Aged 3-6

Regional Benchmark Int. Benchmark Saudi Arabia

3.Extra-Curriculars Involvement

4. Kindergarten enrollment rates

Only 15% of Saudi students were involved in extracurricular activities in 2016. Extracurricular activities are one of the key selection drivers for parents and schools that offer strong programs can quickly differentiate themselves in the market.

Kindergarten enrollment in KSA is currently among the lowest in the GCC with only 13.9 % of the Saudi population enrolled in KG. Current estimates indicate that by the year 2020 about 17% of the Saudi population aged 3-6 will be attending KG, still significantly lower than the regional benchmark which is at 79%.

15

60 57

Saudi Arabia (2016) Regional Benchmark Int. Benchmark

80

60

40

20

0

Figure 13: Percentage of Saudi students involved in Extra Curriculars

Source: MoE

Source: Gastat; MoE; SG Analysis

To improve current education levels and tackle various challenges, the Saudi Ministry of Education has laid out an ambitious plan, as part of the National Transformation Program 2020, to reform the quality of education in Saudi Arabia with the help of the private sector. Some of the objectives of the plan include:

1) Improve the quality of education by upgrading curricula and teaching methods to improve math & science scores by 21% and reading scores by 7% by 2020.

2) Improve recruitment, training, and development of teachers by increasing the number of annual professional development hours from 10 in 2016 to 18 in 2020.

3) Improve students’ values and core skills by increasing involvement in extra curricular activities from 15% in 2016 to 55% by 2020

4) Provide education services to all student levels by increasing kindergarten enrollment from 13% in 2016 to 27.2% by 2020

Government Interventions:

1514 15 15

Private Education Potential in Saudi Arabia

1616 16

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Private

Public

Figure 16: Private vs Public Enrollment in Saudi Arabia

Target

11

89 88 88 87 87 86 86 85 85 8575

12 12 13 13

2020

87

13 14 14 15 15 1525

The past few years have seen an increase in the number of private schools as well as private school enrollment and it is expected to increase much further. This growth is being caused by 2 major factors including an increase in student population and an increasingly greater preference for private education.

Based on the public and private enrollment growth rate over the past 3 years, private enrollment is expected to reach 15% by the year 2025. Out of the 2.1 Million new seats that will be needed by 2025, over 534,000 should be provided by private schools. Given that the average private school size is 540 students, over 980 new private schools will be needed by the year 2025.

Reaching 15% private enrollment however is much lower than the governments target of 25% private enrollment by the year 2020. In order to reach the government’s target of 25% private enrollment, over 2,000 new private schools will be needed by the year 2020 to accommodate for over 1 million new private school students.

Private Education Potential in Saudi Arabia:

Enrollment Growth and Shift Toward Private Schools:

Student Population Growth:

Based on the average growth rate over the past three years, the total number of students in Saudi Arabia is expected to increase by 3.5% annually during the period 2018 to 2025. This indicates an additional 2.1 million seats (Public + Private) will be needed in the next 7 years to accommodate for new students.

12,000

10,000

8,000

6,000

4,000

2,000

02015 2016 2017 2018 2019 2020 2021 2022

3.5%

2023 2024 2025

Figure 15: : Student Population Growth in Saudi Arabia

7,450 7,277 7,530 7,792 8,064 8,347 8,641 8,946 9,263 9,592 9934

Source: MoE; SG Analysis

Source: MoE; SG Analysis

1716 17 17

The number of public schools in Saudi Arabia has increased by 1% over the previous 5 years. However, the number of private schools has increased by 13% in the same period, indicating a much greater demand for private schools.

Also, class sizes in private national schools have remained mostly steady at around 23-25 students per class while those in private international schools have more than doubled in a period of 4 years between 2012 – 2016 showcasing the increasing demand for such services.

Source: MoE; SG Analysis

Source: MoE; SG Analysis

!

!

!

!

!

!

!

!

!2+'.&%N!=#2F!+>!@8(8/6-1!

0

5,000

10,000

15,000

20,000

25,000

30,000

2013 2014 2015 2016 2017

Public Private

1%

13%

Figure 17: Increase in Public and Private Schools in Saudi Arabia

0

5

10

15

20

25

30

2012 2013 2014 2015 2016

Private National Schools Private International Schools

Figure 18: Increase in Class Sizes

Num

ber O

f Stu

dent

s Pe

r Cla

ssro

om

1818 18

Conclusion

1918 19 19

Conclusion:

Saudi Arabia’s private education market is set to more than double in value over the coming few years. The growth in the market is being fueled by an increase in population, government education initiatives, and changing consumer mindsets.

There are many fundamental challenges facing the education sector in Saudi Arabia, including quality of curriculums, teacher recruitment, and kindergarten enrollment to name a few. Such challenges, coupled with the governments vision and serious initiatives all indicate the big potential for current and new private schools, especially ones that can address the most important selection drivers and pass the nationalization requirements.

With the right entry strategy and school offerings, private education investors will be welcomed by a growing demand all while contributing to the governments Vision 2030 initiatives.

2020 20 132

About Strategic Gears:

Strategic Gears is a Management Consultancy based in Saudi Arabia, with presence in Riyadh and Jeddah, serving clients across the country. Strategic Gears' clients include the biggest public and private sector organizations, includ-ing a number of ministries, authorities, financial

institutions, and companies.

The company utilizes its top notch local consul-tants, and global network of experts to offer strategic solutions in the fields of public policy, analytics, product development, and strategic marketing, and have a proven track record with

multiple clients in each.

Disclaimer of Liability:Unless otherwise stated, all information contained in this document (the “Publication”) shall not be reproduced, in whole or in part, without the specific written permission of Strategic Gears. Strategic Gears makes its best effort to ensure that the content in the Publication is accurate and up to date at all times. Strategic Gears makes no warranty, representation or undertaking whether expressed or implied, nor does it assume any legal liability, whether direct or indirect, or responsibility for the accuracy, completeness, or usefulness of any information that is contained in the Publication. It is not the intention of the Publication to be used or deemed as recommendation, option or advice for any action (s) that may take place in future.

www.strategicgears.com

2120 21 21132

About Strategic Gears:

Strategic Gears is a Management Consultancy based in Saudi Arabia, with presence in Riyadh and Jeddah, serving clients across the country. Strategic Gears' clients include the biggest public and private sector organizations, includ-ing a number of ministries, authorities, financial

institutions, and companies.

The company utilizes its top notch local consul-tants, and global network of experts to offer strategic solutions in the fields of public policy, analytics, product development, and strategic marketing, and have a proven track record with

multiple clients in each.

Disclaimer of Liability:Unless otherwise stated, all information contained in this document (the “Publication”) shall not be reproduced, in whole or in part, without the specific written permission of Strategic Gears. Strategic Gears makes its best effort to ensure that the content in the Publication is accurate and up to date at all times. Strategic Gears makes no warranty, representation or undertaking whether expressed or implied, nor does it assume any legal liability, whether direct or indirect, or responsibility for the accuracy, completeness, or usefulness of any information that is contained in the Publication. It is not the intention of the Publication to be used or deemed as recommendation, option or advice for any action (s) that may take place in future.

www.strategicgears.comwww.strategicgears.com