gst latest updates & developments 3rd october 2015 · pdf file01.10.2015 ·...

TRANSCRIPT

GST Latest Updates & Developments

3rd October 2015

Presented by Simon ChuaITS Management Sdn Bhd

1ITS Management Sdn Bhd ~ Simon Chua ©

Speaker profile

Simon Chua, CA(M), FCCA(UK), B.Sc (First Class Hons) in applied accounting, Dip in Commerce (TARC),

is a practising chartered accountant and GST tax agent licensed by Ministry of Finance, with more than 12 years of wide and diversified working experience involving in tax advisory, tax compliance and business advisory services.

He conducts in-house and public trainings to organizations in relation to tax compliance and goods and services tax. He is a member of Malaysian Institute of Accountants (MIA) and Association of Chartered Certified Accountants (ACCA).

Currently, he is ITS’ program director for GST Training & Implementation unit.

2ITS Management Sdn Bhd ~ Simon Chua ©

Course Content

Updates affecting the followings and its practical implications: Supply (incl. disbursement vs. reimbursement) Deemed supply (gift rule) Input tax credits Cross-border supply of goods Cross-border supply of services FOREX rates Bad debts adjustments Other recent developments Q&A

ITS Management Sdn Bhd ~ Simon Chua © 3

Reimbursement & Disbursement

ITS Management Sdn Bhd ~ Simon Chua © 4

Disbursement vs. reimbursement

My CusReimbursement

Disbursement

My CoMy

SupplierTax Invoice to “My Co”

Tax Invoice to “My Cus”

OPOS

TXSRTax invoice Sales RM1,000GST RM 60Total RM1,060

Example

ITS Management Sdn Bhd ~ Simon Chua © 5

Reimbursement

• Expenses incurred in the course of providing services/goods for a business

• A supply subject to GSTEntitled to an input tax claim

• Reported in GST return

• Tax invoice must be issued

• Can mark up

• Itemised the details is not required

• Control the supplier

ITS Management Sdn Bhd ~ Simon Chua © 6

Disbursement

• Payments made on behalf of related companies/customers are not a supply

• Not subject to GST

• Not entitled to an input tax claim

• Not reported in the GST returns

• Can not mark up

• Itemised the details

• Do not control the supplier

ITS Management Sdn Bhd ~ Simon Chua © 7

Deemed supplies

ITS Management Sdn Bhd ~ Simon Chua © 8

Free gift

ITS Management Sdn Bhd ~ Simon Chua © 9

Free gift rule

• Goods given free to anyone:-• Same person

• Same year

• >RM500.00

• Including employees (Individual name)& customers (Company name)

• Gift rule is applicable to goods only, services are not included except connected person

• A registered person has to accounts for GST even the input tax is not claimed (Decision 5/2015 — Item 5 )

ITS Management Sdn Bhd ~ Simon Chua © 10

Free gift rule

No deemed output tax:-• Zero rated supplies

• Exempt supplies

• Blocked input tax

• Services

• Sponsor (Decision 1/2015 — Item 2 )

• Cash/cash voucher

• Purchase from non-registered person (Decision 2/2014 – Item 4)

• Gifts worth RM500 and below

Employee benefit - Included in company policy (ie handbook)

ITS Management Sdn Bhd ~ Simon Chua © 11

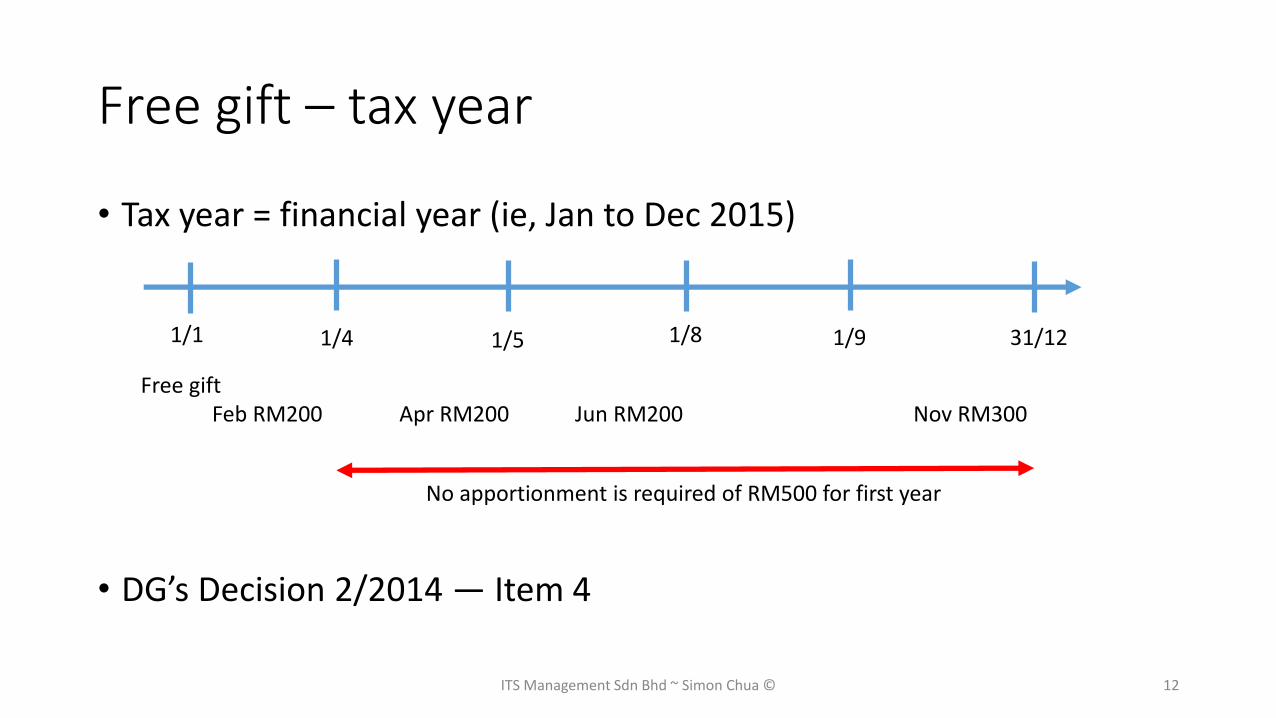

Free gift – tax year

• Tax year = financial year (ie, Jan to Dec 2015)

• DG’s Decision 2/2014 — Item 4

1/4 1/5 1/8 1/9 31/121/1

No apportionment is required of RM500 for first year

Free gift Feb RM200 Apr RM200 Jun RM200 Nov RM300

ITS Management Sdn Bhd ~ Simon Chua © 12

Free gift

ITS Management Sdn Bhd ~ Simon Chua © 13

Connected personsAccounts for GST follows open market value

ITS Management Sdn Bhd ~ Simon Chua © 14

Disposal – with or without consideration to connected person• Transfer or disposal can be for a consideration or no consideration

• Disposal of assets below market value to connected person but accounts for GST must follows open market value

• Without consideration is treated as a supply of goods and is subject to GST depending on the open market value

• Example:• Disposal of an company assets of RM53,000 (Inclusive of GST)

• Open market value of that assets is RM106,000 (inclusive of GST)

ITS Management Sdn Bhd ~ Simon Chua © 15

Disposal of goods without consideration

• My Co carrying on a trading business disposes of its stocks of equipment to its staff for no consideration

• The disposal of the stocks of equipment is subject to GST

ITS Management Sdn Bhd ~ Simon Chua © 16

Goods for personal use

• Ah Chua carries on a sole proprietorship business of selling electronic products

• He took a stand fan for his own uses

• This transaction involves the transfer (not disposal) of company stock from the sole proprietorship business to the individual owner of the business

• This is a supply of goods subject to GST, whether or not for a consideration

ITS Management Sdn Bhd ~ Simon Chua © 17

Input tax credit

ITS Management Sdn Bhd ~ Simon Chua © 18

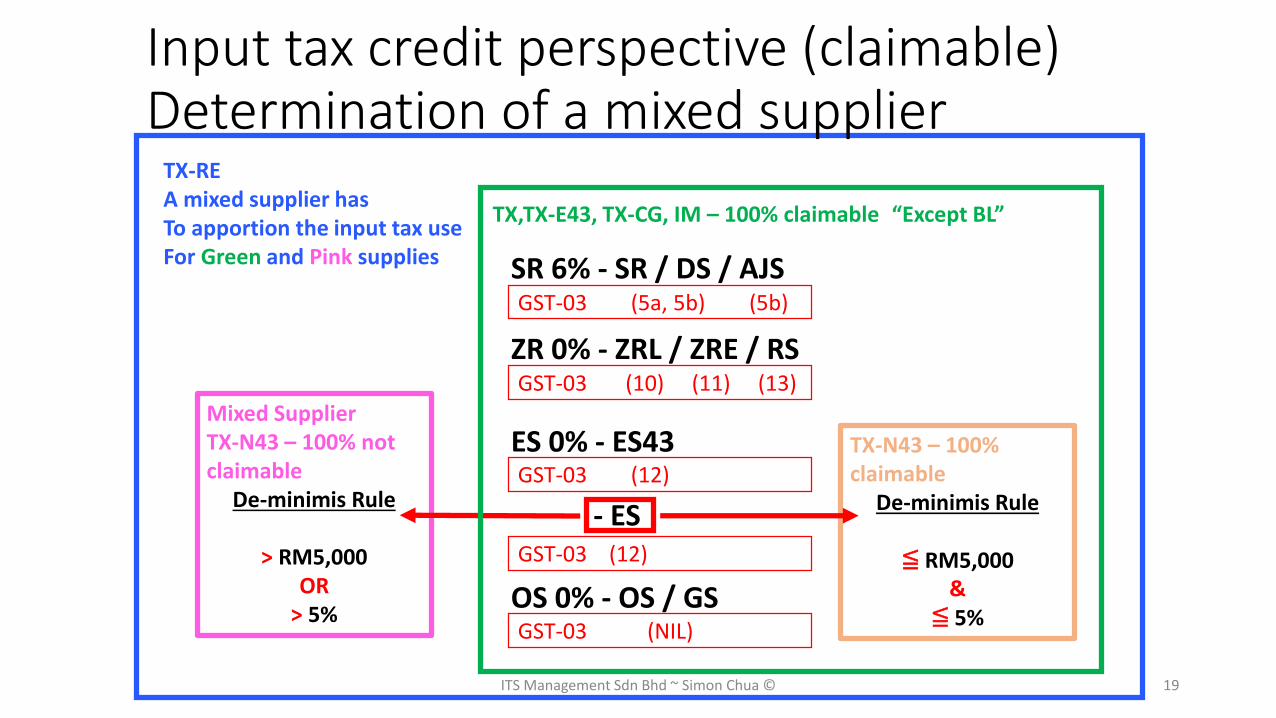

OS 0% - OS / GS

GST-03 (5a, 5b) (5b)

SR 6% - SR / DS / AJS

ZR 0% - ZRL / ZRE / RS

ES 0% - ES43

- ES

GST-03 (10) (11) (13)

GST-03 (12)

GST-03 (12)

GST-03 (NIL)

TX-N43 – 100% claimable

De-minimis Rule

≦ RM5,000&

≦ 5%

Mixed SupplierTX-N43 – 100% not claimable

De-minimis Rule

> RM5,000OR

> 5%

TX,TX-E43, TX-CG, IM – 100% claimable

TX-REA mixed supplier has To apportion the input tax use For Green and Pink supplies

Input tax credit perspective (claimable)Determination of a mixed supplier

“Except BL”

ITS Management Sdn Bhd ~ Simon Chua © 19

Exempt Supply (Income)

ES43 (Incidental financial exempt supply)

• Interest

• Interest income from staff or intercompany loans

• Realised exchange gains • If Gain > Loss = Gain – Loss = ES43

• If Loss > Gain = Loss – Gain = EP

ITS Management Sdn Bhd ~ Simon Chua © 20

Exempt Supply (Income)

ES (Non-incidental exempt supply)

• Rental of residential property

• Disposal of residential property

• Fees charged for transportation services (Bus Kilang) provided to staff by the employer

• Fees charged to staff for child care centre provided by the employer

• Free/FOC is not exempt supply income

ITS Management Sdn Bhd ~ Simon Chua © 21

De-minimis rule

• An average of RM5,000 per month of exempt supplies, and

• 5% of the total value of all supplies (taxable and exempt supplies).

If the value of exempt supplies does not exceed the prescribed value and proportion as stated above, all exempt input tax shall be “treated”as attributable to “taxable supplies”.

ITS Management Sdn Bhd ~ Simon Chua © 22

Blocked input tax• Passenger car

• Buy or importation of passenger motorcar or the hiring of motor vehicle

• Repair, maintenance and refurbishment of motor vehicle

Except:

• Test drive car

• Cars used for security purposes

• Cars used in providing technical assistance

• Serve as an integral part in the running of a business (taxi or car rental)

Additional conditions:

• Motor car is registered in company name(Business name or logo printed on the car)

• Motor car is not let on hire

• No private use

• Kept at business premises, used for business trips and must not be taken home overnight

ITS Management Sdn Bhd ~ Simon Chua © 23

Blocked input tax

• Passenger carDisallowed even fulfilled all the above conditions:

• Assigned car (Director car)

• Pooled car

• Cars used in sales and marketing

• Demo or display car

(DG’s Decision 2/2014 — Item 1)

• Rental paid to hire and drive a passenger motor car

ITS Management Sdn Bhd ~ Simon Chua © 24

Blocked input tax

• Subscription fee, joining fee, membership fee, transfer fee (Recreational or sporting purposes)

• Staff insurance premiums (Foreign Workers Hospitalization and Surgical Insurance Scheme)

• Staff medical expenses incurred for the provision of all forms of medical treatment

• Family benefits including hospitality provided to the wife, husband, child, adopted child or parents of any person employed by the taxable person

• Business entertainment except existing customer and staff

ITS Management Sdn Bhd ~ Simon Chua © 25

Allowable input tax credit• Mobile phone bill not under taxable person name (DG’s Decision

2/2014 — Item 2 )

• Electricity and water bills not under taxable person name until 31/3/2016 (DG’s Decision 7/2017 — Item 1 )

• Conditions:• not a GST registered person

• tenancy agreement

• Additional clause “the input tax on the electricity and water invoices/bills can only be claimed by the tenant. However if the property ownerbecomes GST registered person, the tenant is not allowed to claim the input tax using such invoices/bills.’

ITS Management Sdn Bhd ~ Simon Chua © 26

Allowable input tax credit

• Lorry registered under another company (rental lorry)• Repair, maintenance and refurbishment of motor vehicle

• (Furtherance of business)

• Staff claim – Mr Simon Chua C/O SCMS Business Advisory Sdn Bhd

ITS Management Sdn Bhd ~ Simon Chua © 27

Supply of goods

ITS Management Sdn Bhd ~ Simon Chua © 28

Customer – transfer to goods

Goods CommentsTax

CodeFrom

LocationTo

Location

OM DA M OM DA M

Customer Bill of landing OS √ √

Bill of landing OS √ √

K1 – supplier is importer SR √ √

K1 – customer is importer (DG’s Decision 04/2015 Item 1)

OS √ √

K2 – supplier is exporter ZRE √ √ √

Local supply SR √ √

Invoice to local company & K2-supplier is exporter (DG’s decision 04/2015 Item 2)

ZRE √ √

OM – Outside Malaysia DA – Designated Areas (Labuan, Langkawi & Tioman M – MalaysiaITS Management Sdn Bhd ~ Simon Chua © 29

Supplier – transfer to goods

Goods Comments Tax CodeFrom

LocationTo

Location

OM DA M OM DA M

Supplier Bill of landing OP √ √

Supplier invoice OP (IMI/ISI) √ √ √

K1 IM √ √ √

K1 with ATS IS √ √ √

√

OM – Outside Malaysia DA – Designated Areas (Labuan, Langkawi & Tioman M – MalaysiaITS Management Sdn Bhd ~ Simon Chua © 30

Transfer to goods

• DG’s Decision 04/2015 Item 1

K1- under LBTax code “IM”

Tax code “OS”

Invoice from OS to LC Tax code “OP”

ITS Management Sdn Bhd ~ Simon Chua © 31

Transfer to goods

• DG’s decision 04/2015 Item 2

Tax code “ZRE”

Tax code “OS”

K2 – exporter is LM

ITS Management Sdn Bhd ~ Simon Chua © 32

Transfer to goods

• DG’s decision 04/2015 Item 3

Tax code “SR”

Tax code “ZRE”LA is exporter (K2)

ITS Management Sdn Bhd ~ Simon Chua © 33

Transfer to goods

• DG’s decision 04/2015 Item 4

Tax code “ZRE”K2 – under LS’s name

ITS Management Sdn Bhd ~ Simon Chua © 34

Supply of Services

ITS Management Sdn Bhd ~ Simon Chua © 35

Supply of services – Local and overseas

Location of Treatment

Supplier Services perform CustomerServices used/consumed

/BeneficiallyTax Code

Malaysia Malaysia Malaysia Malaysia SR

Malaysia Malaysia Singapore Malaysia SR

DA Malaysia Malaysia Malaysia SR

Malaysia DA DA DA SR

Malaysia Singapore Singapore Singapore ZRE

Singapore China China China OS

DA DA DA DA OS

ITS Management Sdn Bhd ~ Simon Chua © 36

Exported services that qualified for ZRE

• Supplier belongs in Malaysia

• Receiver belongs out of Malaysia

• Receiver not in Malaysia when the services are performed + not directly benefit Malaysian

• Not relate to any land situated in Malaysia

• Not relate to any goods situated in Malaysia

ITS Management Sdn Bhd ~ Simon Chua © 37

Supply of services (Imported services)

Location of Treatment

Supplier Services perform Customer Services are used or consumed

Tax Code

China Singapore Malaysia Malaysia RCP / (DS)

China Malaysia Malaysia Malaysia RCP / (DS)

Foreign supplier – Supply of services in Malaysia if the taxable supply of services made in Malaysia exceeded the threshold of RM500,000, then foreign supplier is required to be registered for GST.

ITS Management Sdn Bhd ~ Simon Chua © 38

GST Accounting and GST-03

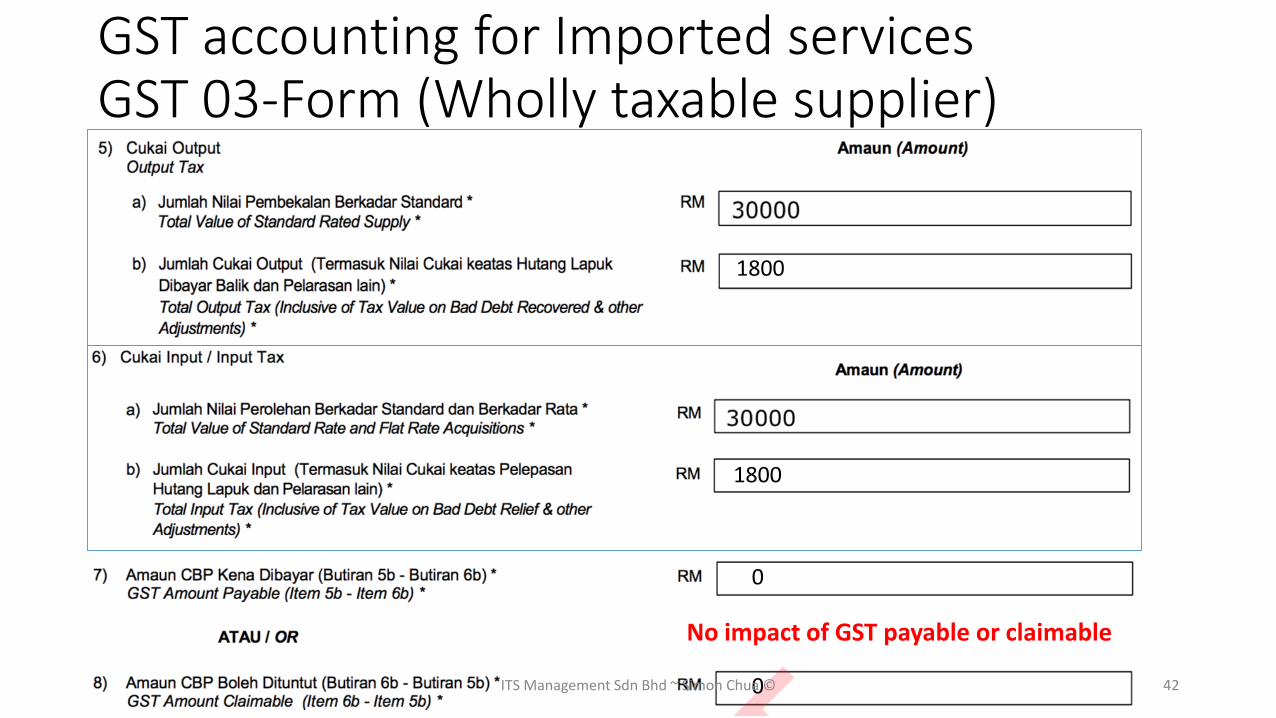

GST Accounting for Imported services

GST 03-Form (Wholly taxable supplier)

ITS Management Sdn Bhd ~ Simon Chua © 39

GST accounting for Imported services

DateGL

CodeParticulars Tax Code DR CR Form - 03

1 May XXXX Purchases / Expenses RCP 30,000 Item 6a

XXXX GST Input tax recoverable RCP 1,800 Item 6b

XXXX GST Output tax payable RCP 1,800 Item 5a

XXXX Bank / Creditor RCP 30,000 Item 5b

ITS Management Sdn Bhd ~ Simon Chua © 40

GST accounting for Imported services

DateGL

CodeParticulars Tax Code DR CR Form - 03

1 May XXXX Purchases / Expenses TX 30,000 Item 6a

XXXX GST Input tax recoverable TX 1,800 Item 6b

XXXX GST Output tax payable DS 1,800 Item 5a

XXXX Bank / Creditor DS 30,000 Item 5b

ITS Management Sdn Bhd ~ Simon Chua © 41

GST accounting for Imported services GST 03-Form (Wholly taxable supplier)

1800

1800

0

0

No impact of GST payable or claimable

ITS Management Sdn Bhd ~ Simon Chua © 42

Foreign exchange

ITS Management Sdn Bhd ~ Simon Chua © 43

Foreign exchange

• If value of supply is expressed in foreign currency, it must be converted in RM:-

• At the selling rate of exchange prevailing in Malaysia at the time when supply takes place, or

• At the rate of exchange determined by the DG in the case of import of goods

ITS Management Sdn Bhd ~ Simon Chua © 44

Foreign exchange

Exchange rates published by

• Central Banks

• Any banks registered under central of Malaysia

ITS Management Sdn Bhd ~ Simon Chua © 45

Foreign exchange

• News agencies

ITS Management Sdn Bhd ~ Simon Chua © 46

Selling rate and TOS available

• Monthly average – prior month

• Month‐end average rate

• Month-end selling rate

• Opening selling rate

• Highest rate plus (+) the lowest rate / 2 – prior month

• Hedged exchange rate

• Any other rate must be approved by DG

Used consistently at least one year

ITS Management Sdn Bhd ~ Simon Chua © 47

9/12 also can Must

ITS Management Sdn Bhd ~ Simon Chua © 48

Bad Debt ReliefCustomer, other customer, accounts receivable, other receivable

(Tax invoice and DN with SR, with GST charged (5a and 5b)

ITS Management Sdn Bhd ~ Simon Chua © 49

Bad debt relief – receivable (update)

• Panel Decision 2014 • ITEM 3: Claiming bad debt relief

If the bad debt relief is not claimed immediately after the expiry of sixth month, then the taxable person has to notify the Director General (DG) within 5 days after the expiry of sixth month on his intention to claim at a later date. (Amended on 23/3/2015)

First letter to RMCD • 5th November 2015 for monthly submission; • 5th January 2016 for quarterly submission

~~~~Refer to appendix to sample letter~~~

ITS Management Sdn Bhd ~ Simon Chua © 50

Bad debt relief – receivable

• Example 1.0• My co issued an tax invoice on April 2015 to My cus RM106,000 inclusive of

GST

• As at 31 October 2015, My co unable to recover the debt from My cus

• My co is on monthly taxable period

• My co has taken legal action on the outstanding due by My cus and fulfil the GST Act 2014’s requirement of sufficient efforts

ITS Management Sdn Bhd ~ Simon Chua © 51

Bad debt relief – receivable (Monthly submission)

April 2015(Tax Invoice/DN)

February 2016(Refund) –Payment

received

October 2015(Claim)

GST-03

5a – 100,000

5b – 6,000

GST-03

5a – NIL

5b – 6,000

GST-03

6a – NIL

6b – 6,000

GST-03

17 – NIL

18 – NIL

GST-03

17 – NIL

18 – 106,000

GST-03

17 – 106,000

18 – NILITS Management Sdn Bhd ~ Simon Chua © 52

Bad debt relief Example 1.0

Bad debt relief – Receivable (Quarterly submission)

Apr - Jun 2015(Tax Invoice/DN)

Jan to Mar 2016(Refund) –Payment

received

Oct to Dec 2015(Claim)

GST-03

5a – 300,000

5b – 18,000

GST-03

5a – NIL

5b – 18,000

GST-03

6a – NIL

6b – 18,000

GST-03

17 – NIL

18 – NIL

GST-03

17 – NIL

18 – 318,000

GST-03

17 – 318,000

18 – NILITS Management Sdn Bhd ~ Simon Chua © 53

Bad debt relief Example 2.0

Bad debt relief – receivable (Monthly submission)

ITS Management Sdn Bhd ~ Simon Chua © 54

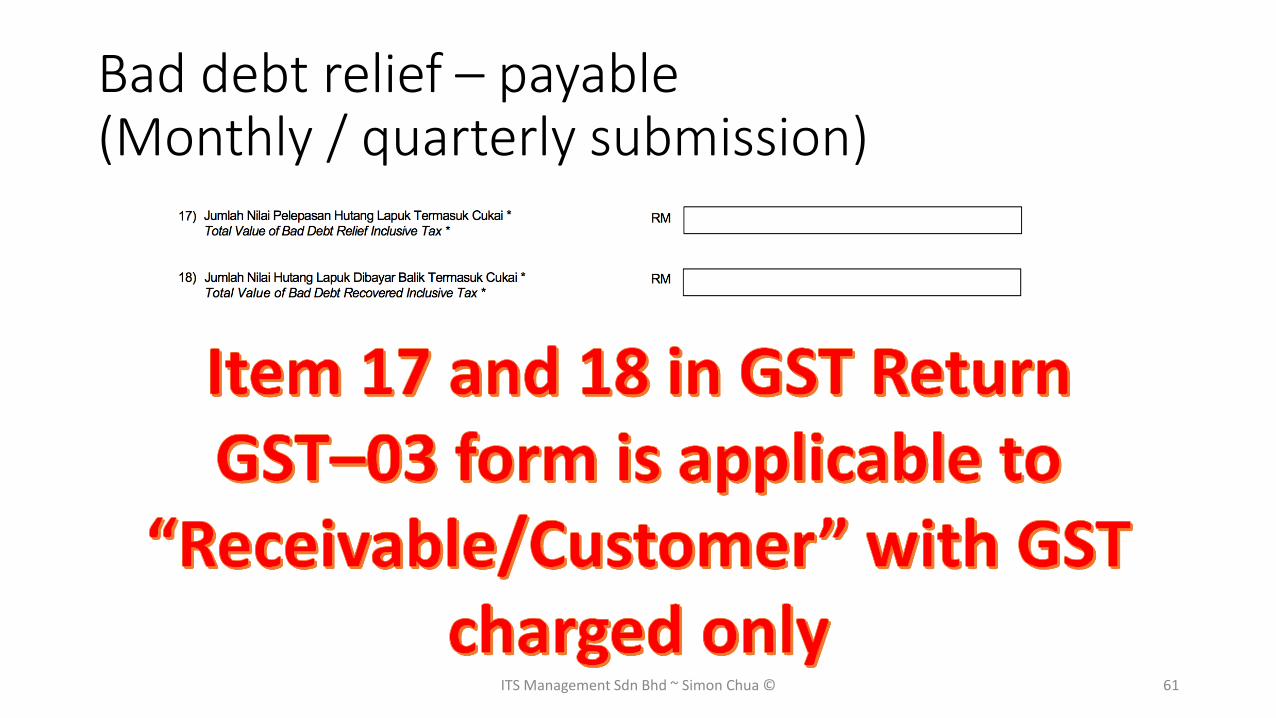

Item 17 and 18 in GST Return Form – 03 is applicable to “Receivable” onlyIn other word - Tax Invoice issued with “SR”

106,000 (Oct 2015)

106,000 (Feb 2016)

GST accounting for bad debt reliefReceivable – claim (monthly)

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 Oct XXXX GST input tax recoverable AJP/DBRC 6,000 6b

XXXX GST sales deferred tax 6,000

XXXX GST sales deferred tax clearing AJP-DBRC 106,000 17

XXXX GST sales deferred tax clearing 106,000

ITS Management Sdn Bhd ~ Simon Chua © 55

For tracking purposes only

GST accounting for bad debt reliefReceivable – refund (monthly)

DateGL

CodeParticulars Tax Code DR CR Form - 03

28 Feb XXXX GST sales deferred tax 6,000

XXXX GST output tax payable AJS/DBRR 6,000 5b

XXXX GST sales deferred tax clearing 106,000

XXXX GST sales deferred tax clearing AJS-DBRR 106,000 18

ITS Management Sdn Bhd ~ Simon Chua © 56

For tracking purposes only

GST accounting bad debt relief Receivable – actual bad debt written off

DateGL

CodeParticulars Tax Code DR CR Form - 03

28 Feb XXXX Bad debt written off OP 100,000

XXXX GST sales deferred tax OP 6,000

XXXX Receivable 106,000

ITS Management Sdn Bhd ~ Simon Chua © 57

Bad Debt ReliefSupplier, other supplier, accounts payable, other payable

(Tax invoice and DN with TX, with GST charged (6a and 6b)

ITS Management Sdn Bhd ~ Simon Chua © 58

Bad debt relief – payable(Monthly submission)

April 2015(Tax Invoice/DN)

February 2016(Claim) –Payment

made

October 2015(Refund)

GST-03

6a – 100,000

6b – 6,000

GST-03

6a – NIL

6b – 6,000

GST-03

5a – NIL

5b – 6,000

GST-03

17 – N/A

18 – N/A

GST-03

17 – N/A

18 – N/A

GST-03

17 – N/A

18 – N/AITS Management Sdn Bhd ~ Simon Chua © 59

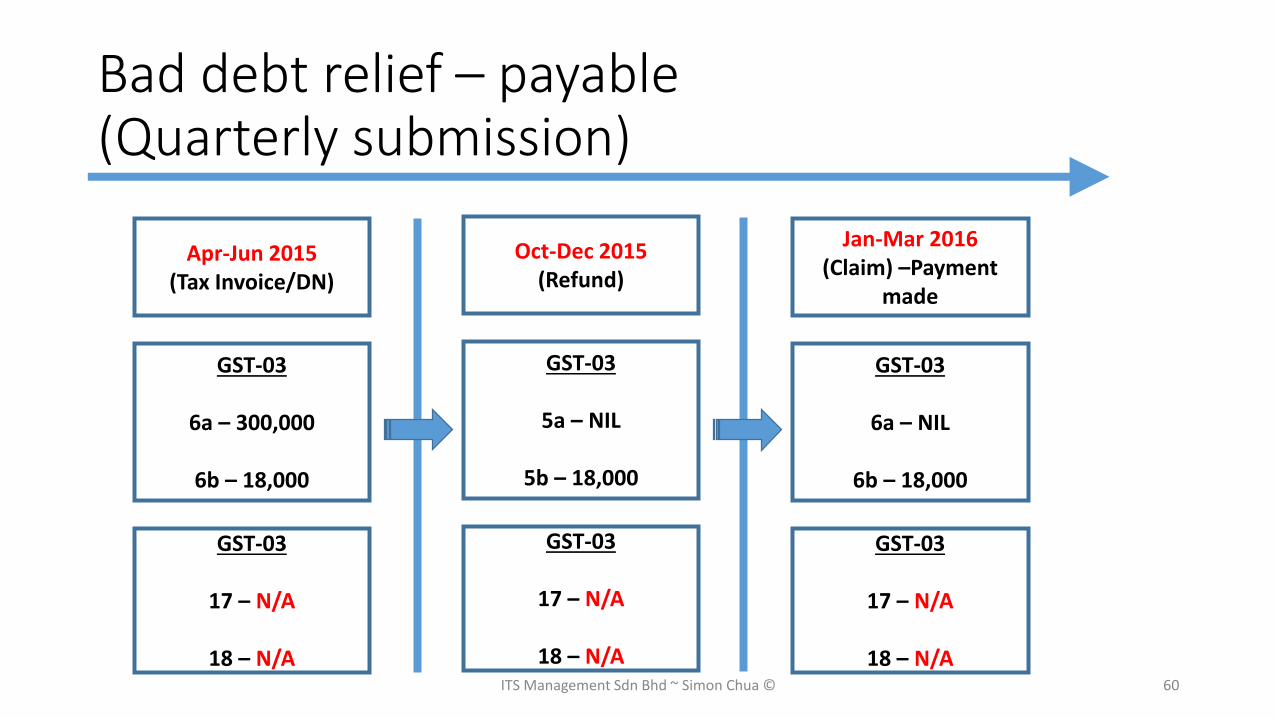

Bad debt relief – payable(Quarterly submission)

Apr-Jun 2015(Tax Invoice/DN)

Jan-Mar 2016(Claim) –Payment

made

Oct-Dec 2015(Refund)

GST-03

6a – 300,000

6b – 18,000

GST-03

6a – NIL

6b – 18,000

GST-03

5a – NIL

5b – 18,000

GST-03

17 – N/A

18 – N/A

GST-03

17 – N/A

18 – N/A

GST-03

17 – N/A

18 – N/AITS Management Sdn Bhd ~ Simon Chua © 60

Bad debt relief – payable (Monthly / quarterly submission)

ITS Management Sdn Bhd ~ Simon Chua © 61

GST accounting for bad debt reliefPayable – refund (monthly)

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 Oct XXXX GST purchase deferred tax 6,000

XXXX GST output tax payable AJS/DBPC 6,000 5b

ITS Management Sdn Bhd ~ Simon Chua © 62

GST accounting for bad debt reliefPayable – claim (monthly)

DateGL

CodeParticulars Tax Code DR CR Form - 03

28 Feb XXXX GST input tax payable AJP/DBPR 6,000 6b

XXXX GST purchase deferred tax 6,000

ITS Management Sdn Bhd ~ Simon Chua © 63

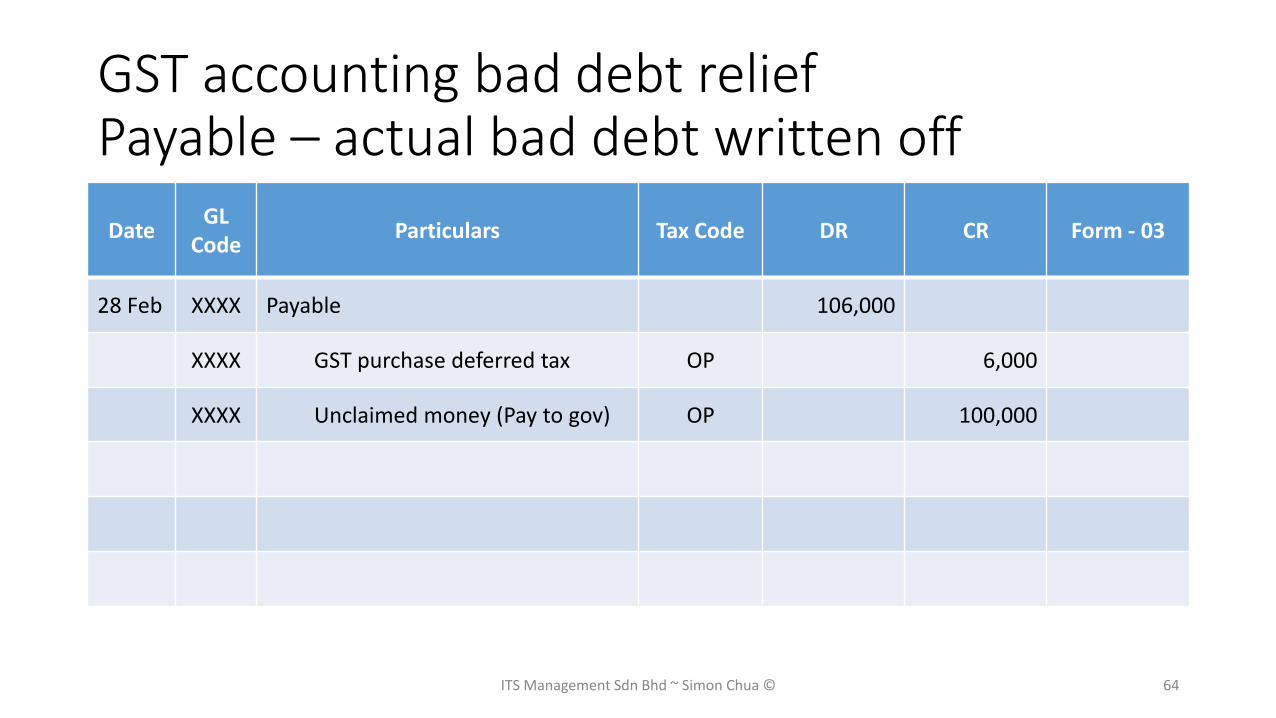

GST accounting bad debt relief Payable – actual bad debt written off

DateGL

CodeParticulars Tax Code DR CR Form - 03

28 Feb XXXX Payable 106,000

XXXX GST purchase deferred tax OP 6,000

XXXX Unclaimed money (Pay to gov) OP 100,000

ITS Management Sdn Bhd ~ Simon Chua © 64

Reimbursement & Disbursement

GST Accounting

ITS Management Sdn Bhd ~ Simon Chua © 65

GST accounting for disbursementMy Supplier tax invoice

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 May XXXX Contra OP 1,060 NIL

XXXX My Supplier / payable / Bank 1,060 NIL

ITS Management Sdn Bhd ~ Simon Chua © 66

GST accounting for disbursementClaim back from My Cus

DateGL

CodeParticulars Tax Code DR CR Form - 03

30 Jun XXXX My Cus / receivable / bank 1,060 NIL

XXXX Contra OS 1,060 NIL

ITS Management Sdn Bhd ~ Simon Chua © 67

GST accounting for reimbursementMy Supplier tax invoice

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 May XXXX Contra / expense account TX 1,000 6a

XXXX GST input tax recoverable TX 60 6b

XXXX My Supplier / payable / Bank 1,060

ITS Management Sdn Bhd ~ Simon Chua © 68

GST accounting for reimbursementClaim back from My Cus

DateGL

CodeParticulars Tax Code DR CR Form - 03

30 Jun XXXX My Cus / receivable / bank 1,060

XXXX GST output tax payable SR 60 5a

XXXX Contra / expense account SR 1,000 5b

ITS Management Sdn Bhd ~ Simon Chua © 69

More detail suggestion answer refer to appendix

Free gift

GST Accounting

ITS Management Sdn Bhd ~ Simon Chua © 70

GST accounting free gift1st Scenario (account GST separately for OTP)

DateGL

CodeParticulars Tax Code DR CR Form - 03

30 Nov XXXX Free gift expense / GST expense 42

XXXX GST gift clearing account 700

XXXX GST output tax payable DS 42 5a

XXXX GST gift clearing account DS 700 5b

ITS Management Sdn Bhd ~ Simon Chua © 71

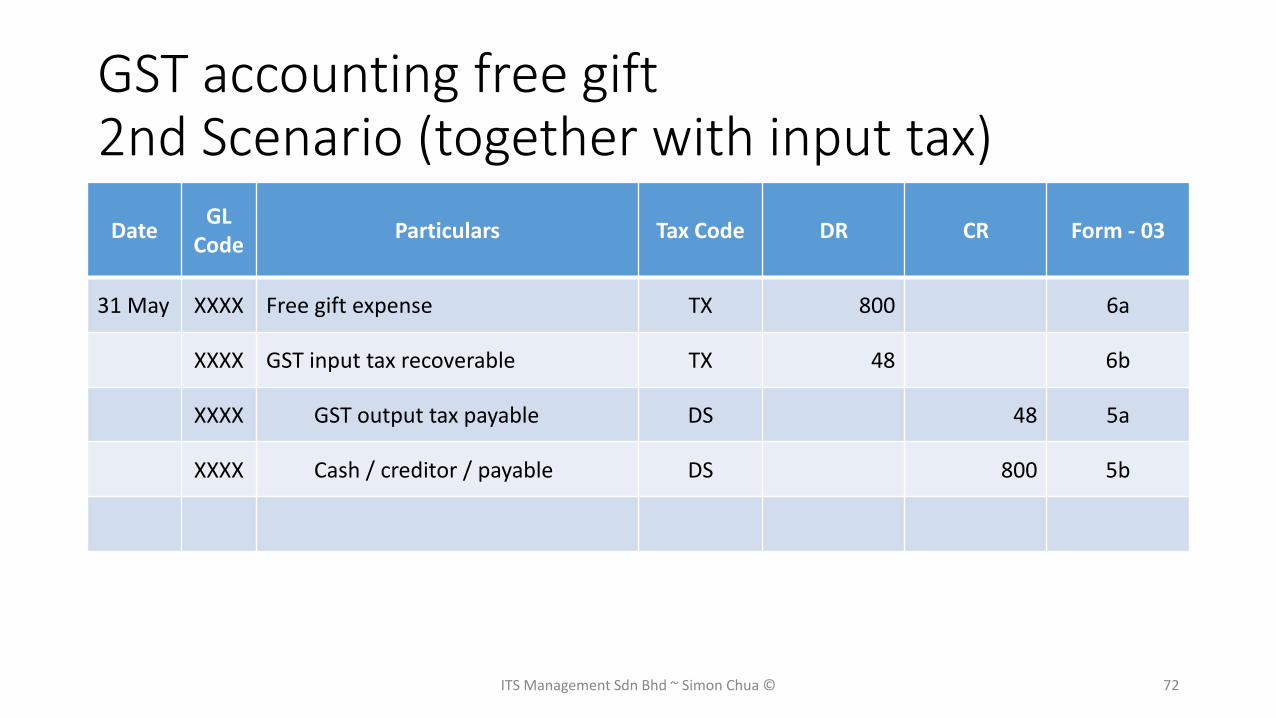

GST accounting free gift2nd Scenario (together with input tax)

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 May XXXX Free gift expense TX 800 6a

XXXX GST input tax recoverable TX 48 6b

XXXX GST output tax payable DS 48 5a

XXXX Cash / creditor / payable DS 800 5b

ITS Management Sdn Bhd ~ Simon Chua © 72

Connected personsAccounts for GST follows open market value

GST Accounting

ITS Management Sdn Bhd ~ Simon Chua © 73

GST accounting on deemed supplyConnected person – Issue a tax invoice

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 May XXXX Bank / other receivable 53,000

XXXX GST Output tax payables SR 3,000 5b

XXXX Disposal of fixed assets SR 50,000 5a

ITS Management Sdn Bhd ~ Simon Chua © 74

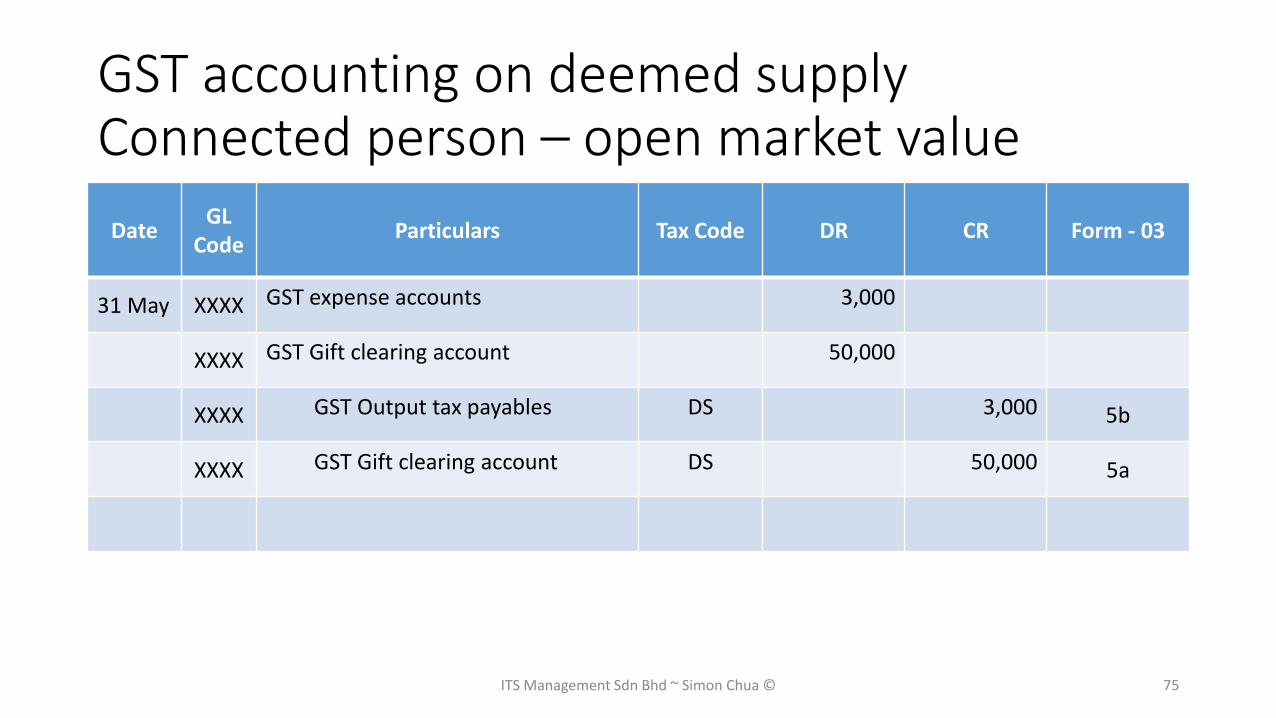

GST accounting on deemed supplyConnected person – open market value

DateGL

CodeParticulars Tax Code DR CR Form - 03

31 May XXXX GST expense accounts 3,000

XXXX GST Gift clearing account 50,000

XXXX GST Output tax payables DS 3,000 5b

XXXX GST Gift clearing account DS 50,000 5a

ITS Management Sdn Bhd ~ Simon Chua © 75

ITS Management Sdn Bhd ~ Simon Chua © 76

For Choosing ITS Management Sdn Bhd

As Your Training Provider

If you have questions or require further assistance later, please email to

Email Subject: “Attn: Trainer’s Name”

Other inquiries, please email to

[email protected] Management Sdn Bhd ~ Simon Chua © 77