gst on charitable trusts, non-profit organizations and...

TRANSCRIPT

GSTonCharitableTrusts,Non-ProfitOrganizations andCo-Operative Societies

CAYashwantJ.KasarB.Com,FCA,DISA,CISA,PMP,FAIA

Feb2018

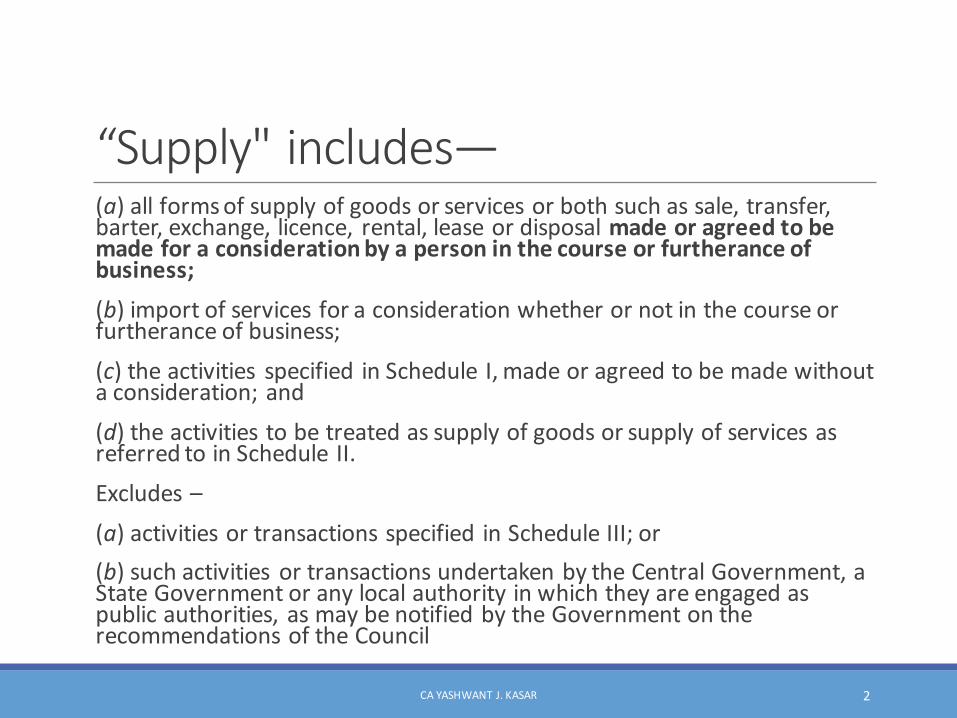

“Supply"includes—(a) allformsofsupplyofgoodsorservicesorbothsuchassale,transfer,barter,exchange,licence,rental,leaseordisposalmadeoragreedtobemadeforaconsiderationbyapersoninthecourseorfurtheranceofbusiness;(b) importofservicesforaconsiderationwhetherornotinthecourseorfurtheranceofbusiness;(c) theactivities specified inSchedule I,madeoragreedtobemadewithoutaconsideration;and(d) theactivitiestobetreatedassupplyofgoodsorsupplyofservicesasreferredtoinSchedule II.Excludes–(a) activitiesortransactionsspecified inScheduleIII;or(b) suchactivities ortransactionsundertakenbytheCentralGovernment,aStateGovernmentoranylocalauthorityinwhichtheyareengagedaspublicauthorities,asmaybenotifiedbytheGovernmentontherecommendationsoftheCouncil

CAYASHWANT J.KASAR 2

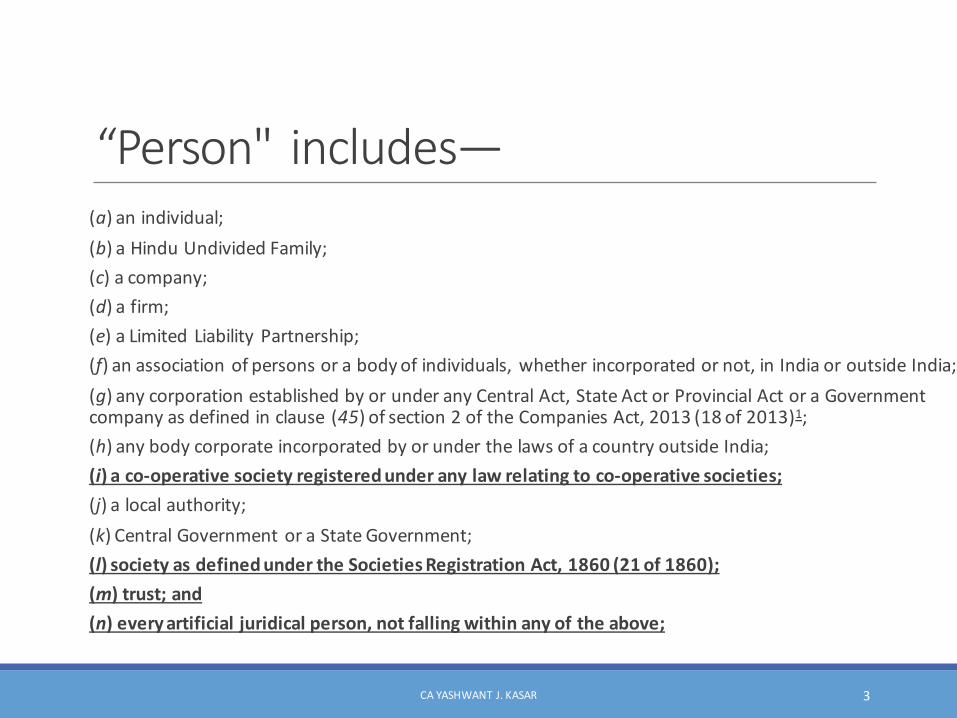

“Person" includes—(a) anindividual;(b) aHinduUndividedFamily;(c) acompany;(d) afirm;(e) aLimitedLiabilityPartnership;(f) anassociationofpersonsorabodyofindividuals,whetherincorporatedornot,inIndiaoroutsideIndia;(g) anycorporationestablishedbyorunderanyCentralAct,StateActorProvincialActoraGovernmentcompanyasdefinedinclause (45)ofsection2oftheCompaniesAct,2013(18of2013)1;(h) anybodycorporateincorporatedbyorunderthelawsofacountryoutsideIndia;(i) aco-operativesocietyregisteredunderanylawrelatingtoco-operativesocieties;(j) alocalauthority;(k) CentralGovernmentoraStateGovernment;(l) societyasdefinedundertheSocietiesRegistrationAct,1860(21of1860);(m) trust;and(n) everyartificialjuridicalperson,notfallingwithinanyoftheabove;

CAYASHWANT J.KASAR 3

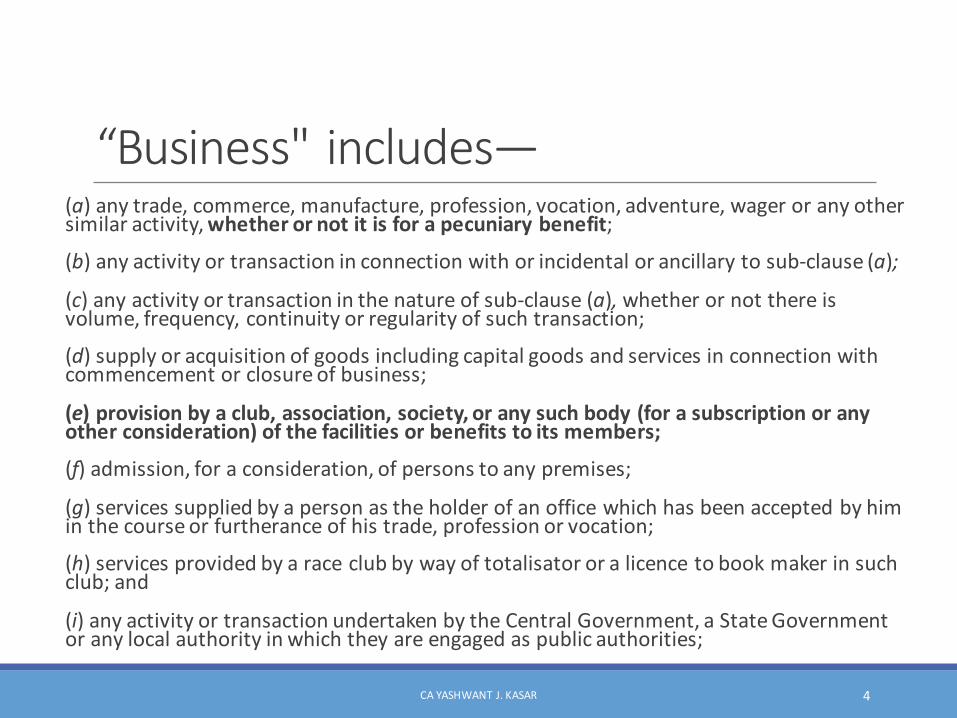

“Business" includes—(a) anytrade,commerce,manufacture,profession,vocation,adventure,wageroranyothersimilaractivity,whetherornotitisforapecuniarybenefit;

(b) anyactivityortransactioninconnectionwithorincidentalorancillarytosub-clause(a);

(c) anyactivityortransactioninthenatureofsub-clause(a), whetherornotthereisvolume,frequency,continuityorregularityofsuchtransaction;

(d) supplyoracquisitionofgoodsincludingcapitalgoodsandservicesinconnectionwithcommencementorclosureofbusiness;

(e) provisionbyaclub,association,society,oranysuchbody(forasubscriptionoranyotherconsideration)ofthefacilitiesorbenefitstoitsmembers;

(f) admission,foraconsideration,ofpersonstoanypremises;

(g) servicessuppliedbyapersonastheholderofanofficewhichhasbeenacceptedbyhiminthecourseorfurtheranceofhistrade,professionorvocation;

(h) servicesprovidedbyaraceclubbywayoftotalisator oralicencetobookmakerinsuchclub;and

(i) anyactivityortransactionundertakenbytheCentralGovernment,aStateGovernmentoranylocalauthorityinwhichtheyareengagedaspublicauthorities;

CAYASHWANT J.KASAR 4

CAYASHWANT J.KASAR 5

Theprovisionsrelatingtotaxationofactivitiesofcharitableinstitutionsandreligioustrustshavebeenborrowedandcarriedoverfromtheerstwhileservicetaxprovisions.

Allservicesprovidedbysuchentitiesarenotexempt.Infact,therearemanyservicesthatareprovidedbysuchentitieswhichwouldbewithintheambitofGST.

NotificationNo.12/2017-Central Tax(Rate)dated28thJune2017ExemptsservicesprovidedbyentityregisteredunderSection12AA oftheIncome-taxAct,1961bywayofcharitableactivitiesfromwholeofGSTvide entryNo.1ofthenotification,

whichspecifiesthat"servicesbyanentityregisteredunderSection12AAofIncome-taxAct,1961bywayofcharitableactivities"areexemptfromwholeoftheGST.Thusasperthisnotification,exemptionisgiventothecharitabletrusts,onlyifthefollowingconditionsaresatisfied.

a) EntitiesmustberegisteredunderSection12AAoftheIncome-taxAct,and

b) Suchservicesoractivitiesbytheentityarebywayofcharitableactivities.

CAYASHWANT J.KASAR 6

CAYASHWANT J.KASAR 7

Thus,itisessential thattheactivitiesmustconformtotheterm“CharitableActivities”which hasbeendefined inthenotificationasunder"charitableactivities"meansactivities relatingto:(i)publichealthbywayof:(A) careorcounseling of(I) terminallyillpersonsorpersonswithseverephysicalormentaldisability;(II) personsafflictedwithHIVorAIDS;(III) personsaddictedtoadependence-formingsubstancesuchasnarcoticsdrugsoralcohol;or(B) publicawarenessofpreventivehealth,familyplanningorpreventionofHIVinfection;(ii) advancementofreligion,spiritualityoryoga;(iii) advancementofeducationalprogrammesorskilldevelopmentrelatingto:(A) abandoned,orphanedorhomeless children;(B)physicallyormentallyabusedandtraumatizedpersons;(C) prisoners;or(D) personsovertheageof65yearsresidinginaruralarea;(iv) preservationofenvironmentincludingwatershed,forestsandwildlife.

CAYASHWANT J.KASAR 8

Thisnotificationmakestheexemptiontocharitabletrustsavailableforcharitableactivitiesmorespecific.

WhiletheincomefromonlythoseactivitieslistedaboveisexemptfromGST,incomefromtheactivitiesotherthanthosementionedaboveistaxable.

Thus,therecouldbemanyservicesprovidedbycharitableandreligioustrustwhicharenotconsideredascharitableactivitiesandhence,suchservicescomeundertheGSTnet.

Theindicativelistofsuchservicescouldberentingofpremisesbysuchentities,grantofsponsorshipandadvertisingrightsduringconductofevents/functionsetc.

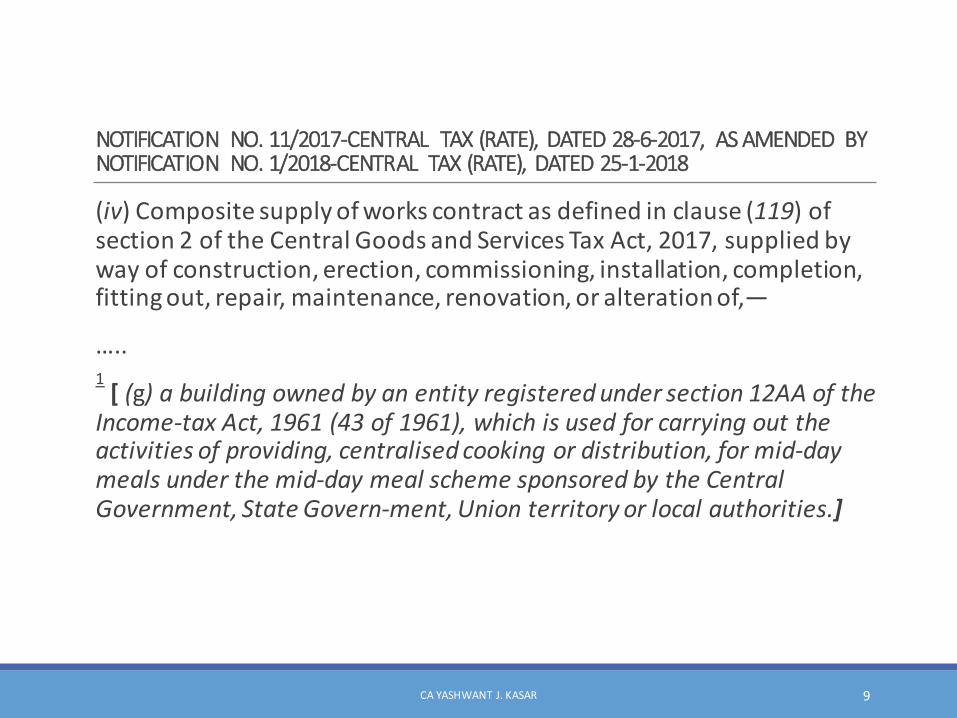

NOTIFICATION NO.11/2017-CENTRAL TAX(RATE), DATED28-6-2017, ASAMENDED BYNOTIFICATION NO.1/2018-CENTRAL TAX(RATE), DATED25-1-2018

(iv)Compositesupplyofworkscontractasdefinedinclause(119)ofsection2oftheCentralGoodsandServicesTaxAct,2017,suppliedbywayofconstruction,erection,commissioning,installation,completion,fittingout,repair,maintenance,renovation,oralterationof,—

…..1[ (g) abuildingownedbyanentityregisteredundersection12AAofthe

Income-taxAct,1961(43of1961),whichisusedforcarryingouttheactivitiesofproviding,centralised cookingordistribution,formid-daymealsunderthemid-daymealschemesponsoredbytheCentralGovernment,StateGovern-ment,Unionterritoryorlocalauthorities.]

CAYASHWANT J.KASAR 9

CharitableHealthcareTrusts

CAYASHWANT J.KASAR 10

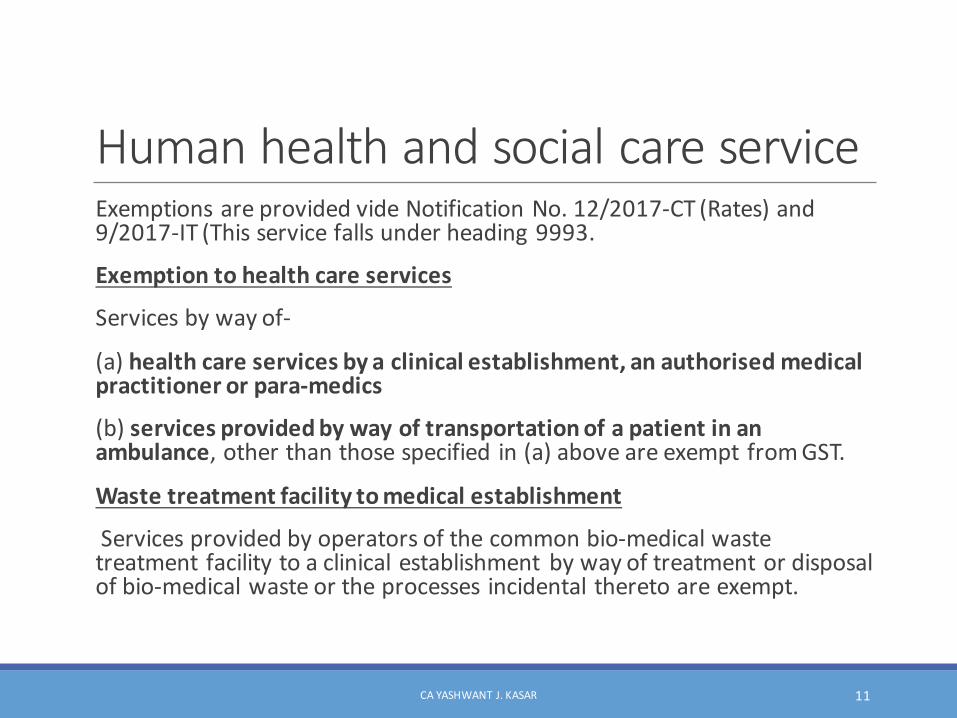

HumanhealthandsocialcareserviceExemptionsareprovidedvideNotificationNo.12/2017-CT(Rates)and9/2017-IT(Thisservicefallsunderheading9993.

Exemptiontohealthcareservices

Servicesbywayof-

(a)healthcareservicesbyaclinicalestablishment,anauthorisedmedicalpractitionerorpara-medics

(b)servicesprovidedbywayoftransportationofapatientinanambulance,otherthanthosespecified in(a)aboveareexemptfromGST.

Wastetreatmentfacilitytomedicalestablishment

Servicesprovidedbyoperatorsofthecommonbio-medicalwastetreatmentfacilitytoaclinicalestablishment bywayoftreatmentordisposalofbio-medicalwasteortheprocesses incidentaltheretoareexempt.

CAYASHWANT J.KASAR 11

CAYASHWANT J.KASAR 12

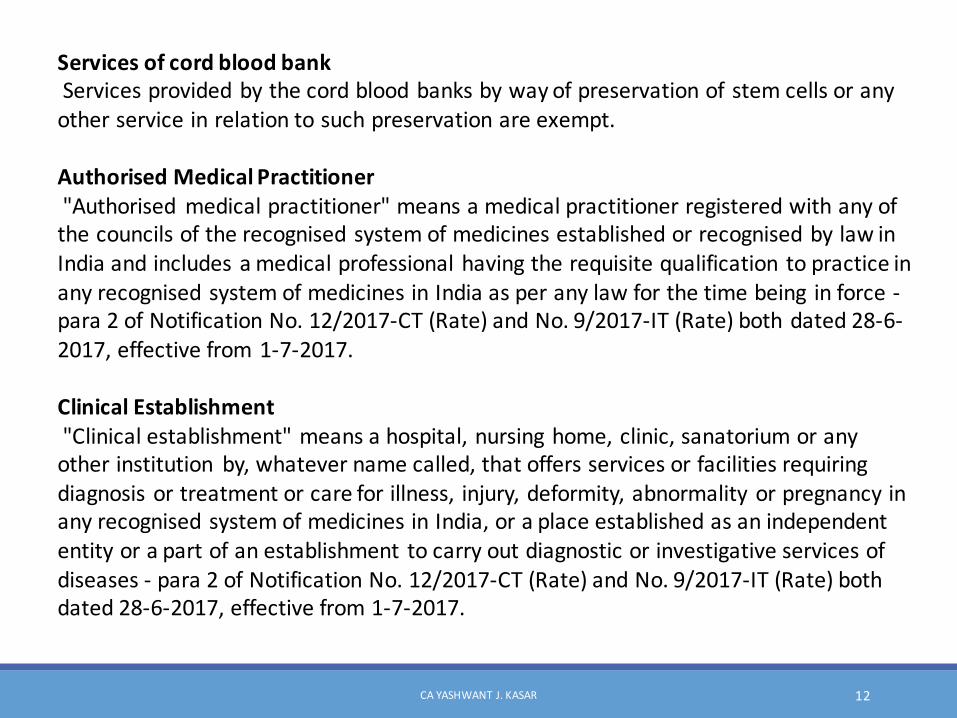

ServicesofcordbloodbankServicesprovidedbythecordbloodbanksbywayofpreservationof stemcellsoranyotherserviceinrelationtosuchpreservationareexempt.

Authorised MedicalPractitioner"Authorised medicalpractitioner"meansamedicalpractitionerregisteredwithanyofthecouncilsoftherecognised systemofmedicinesestablishedorrecognised bylawinIndiaandincludesamedicalprofessionalhavingtherequisitequalification topracticeinanyrecognised systemofmedicinesinIndiaasperanylawforthetimebeing inforce-para 2ofNotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

ClinicalEstablishment"Clinicalestablishment"meansahospital,nursinghome,clinic,sanatoriumoranyotherinstitution by,whatevernamecalled,thatoffersservicesorfacilitiesrequiringdiagnosisortreatmentorcareforillness, injury,deformity,abnormalityorpregnancyinanyrecognised systemofmedicinesinIndia,oraplaceestablishedasanindependententityorapartofanestablishment tocarryoutdiagnosticorinvestigativeservicesofdiseases- para 2ofNotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

CAYASHWANT J.KASAR 13

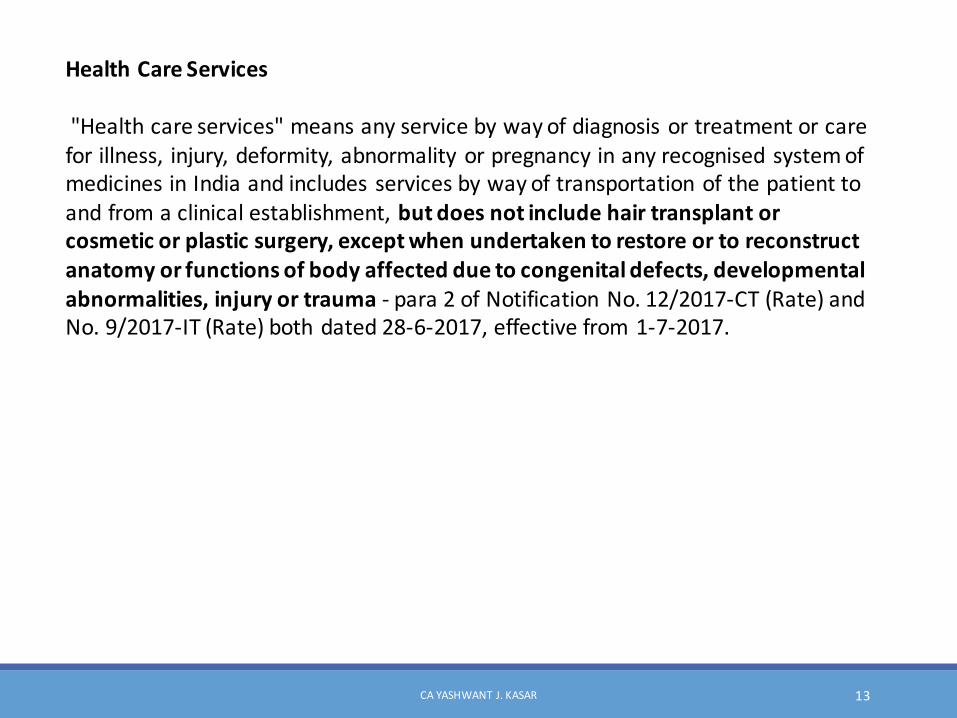

HealthCareServices

"Healthcareservices"meansanyservicebywayofdiagnosisortreatmentorcareforillness, injury,deformity,abnormalityorpregnancyinanyrecognised systemofmedicinesinIndiaandincludesservicesbywayoftransportationofthepatienttoandfromaclinicalestablishment,butdoesnotincludehairtransplantorcosmeticorplasticsurgery,exceptwhenundertakentorestoreortoreconstructanatomyorfunctionsofbodyaffectedduetocongenitaldefects,developmentalabnormalities,injuryortrauma - para 2ofNotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

CircularNo.32/06/2018-GST -Clarifications(1)Hospitalshireseniordoctors/consultants/techniciansindependently,withoutanycontractofsuchpersonswiththepatient;andpaythemconsultancycharges,withouttherebeinganyemployer-employeerelationship.WillsuchconsultancychargesbeexemptfromGST?WillrevenuetakeastandthattheyareprovidingservicestohospitalsandnottopatientsandhencemustpayGST?

- Servicesprovidedbyseniordoctors/consultants/technicianshiredbythehospitals,whetheremployeesornot,arehealthcareserviceswhichareexempt.

CAYASHWANT J.KASAR 14

CAYASHWANT J.KASAR 15

(2)Retentionmoney:Hospitalschargethepatients,say,Rs.10000/-andpaytotheconsultants/techniciansonlyRs.7500/- andkeepthebalanceforprovidingancillaryserviceswhichincludenursingcare,infrastructurefacilities,paramediccare,emergencyservices,checkingoftemperature,weight,bloodpressureetc.WillGSTbeapplicableonsuchmoneyretainedbythehospitals?

- Healthcareserviceshavebeendefinedtomeananyservicebywayofdiagnosisortreatmentorcareforillness,injury,deformity,abnormalityorpregnancyinanyrecognised systemofmedicinesinIndia[para2(zg)ofnotificationNo.12/2017- CT(Rate)].Therefore,hospitalsalsoprovidehealthcareservices.

Theentireamountchargedbythemfromthepatientsincludingtheretentionmoneyandthefee/paymentsmadetothedoctorsetc.,istowardsthehealthcareservicesprovidedbythehospitalstothepatientsandisexempt.

CAYASHWANT J.KASAR 16

(3)Foodsuppliedtothepatients:Healthcareservicesprovidedbytheclinicalestablishmentswillincludefoodsuppliedtothepatients;butsuchfoodmaybepreparedbythecanteensrunbythehospitalsormaybeoutsourcedbytheHospitalsfromoutdoorcaterers.Whenoutsourced,thereshouldbenoambiguitythatthesuppliersshallchargetaxasapplicableandhospitalwillgetnoITC.Ifhospitalshavetheirowncanteensandpreparetheirownfood;thennoITCwillbeavailableoninputsincludingcapitalgoodsandinturniftheysupplyfoodtothedoctorsandtheirstaff;suchsupplies,evenwhennotcharged,maybesubjectedtoGST ?

- Foodsuppliedtothein-patientsasadvisedbythedoctor/nutritionistsisapartofcompositesupplyofhealthcareandnotseparatelytaxable.Othersuppliesoffoodbyahospitaltopatients(notadmitted)ortheirattendantsorvisitorsaretaxable.

CAYASHWANT J.KASAR 17

So,ifcharitabletrustsrunahospitalandappointspecialistdoctors,nursesandprovidemedicalservicestopatientsataconcessionalrate,suchservicesarenotliabletoGST.

Ifhospitalshirevisitingdoctors/specialistsandthesedeductsomemoneyfromconsultation/visitfeespayabletodoctorsandtheagreementbetweenhospitalandconsultantdoctorsissuchthatsomemoneyischargedforprovidingservicestodoctors,theremaybeGSTonsuchamountdeductedfromfeespaidtodoctors.

CharitableReligiousTrusts

CAYASHWANT J.KASAR 18

EntryNo.13ofNotification No.12/2017-Central Tax(Rate)dated28thJune,2017ProvidesthefollowingexemptiontoentitiesregisteredunderSection12AAoftheIncomeTaxAct:

Servicesbyapersonbywayof:

(a)conductofanyreligiousceremony;

(b)rentingofprecinctsofareligiousplacemeantforgeneralpublic,ownedormanagedbyanentityregisteredasacharitableorreligioustrustundersection12AA oftheIncome-taxAct,1961(hereinafterreferredtoastheIncome-taxAct)oratrustoraninstitutionregisteredundersub-clause(v)ofclause(23C)ofsection10oftheIncome-taxActorabodyoranauthoritycoveredunderclause(23BBA)ofsection10ofthesaidIncome-taxAct:

Providedthatnothingcontainedinentry(b)ofthisexemptionshallapplyto:

CAYASHWANT J.KASAR 19

CAYASHWANT J.KASAR 20

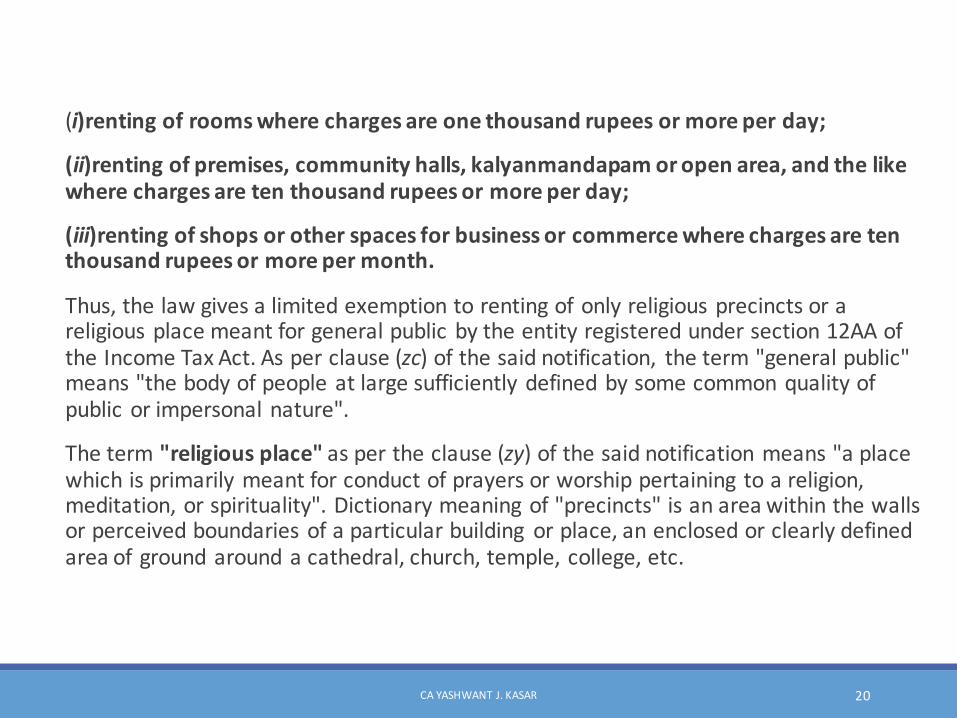

(i)rentingofroomswherechargesareonethousandrupeesormoreperday;

(ii)rentingofpremises,communityhalls,kalyanmandapam oropenarea,andthelikewherechargesaretenthousandrupeesormoreperday;

(iii)rentingofshopsorotherspacesforbusinessorcommercewherechargesaretenthousandrupeesormorepermonth.

Thus,thelawgivesalimitedexemptiontorentingofonlyreligiousprecinctsorareligiousplacemeantforgeneralpublicbytheentityregisteredundersection12AAoftheIncomeTaxAct.Asperclause(zc)ofthesaidnotification, theterm"generalpublic"means"thebodyofpeopleatlargesufficientlydefinedbysomecommonqualityofpublicorimpersonalnature".

Theterm"religiousplace"aspertheclause(zy)ofthesaidnotificationmeans"aplacewhichisprimarilymeantforconductofprayersorworshippertaining toareligion,meditation,orspirituality".Dictionarymeaningof"precincts"isanareawithinthewallsorperceivedboundariesofaparticularbuilding orplace,anenclosedorclearlydefinedareaofgroundaroundacathedral,church,temple, college,etc.

CAYASHWANT J.KASAR 21

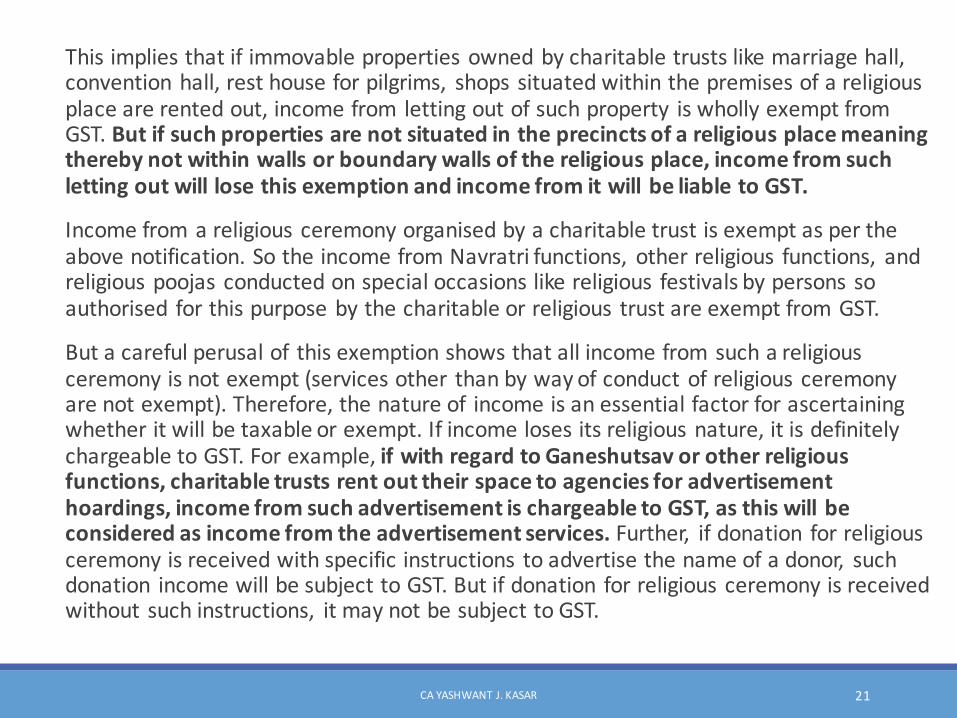

Thisimpliesthatifimmovablepropertiesownedbycharitabletrustslikemarriagehall,conventionhall,resthouseforpilgrims, shopssituatedwithinthepremisesofareligiousplacearerentedout,incomefrom lettingoutofsuchproperty iswhollyexemptfromGST.Butifsuchpropertiesarenotsituatedintheprecinctsofareligiousplacemeaningtherebynotwithinwallsorboundarywallsofthereligiousplace,incomefromsuchlettingoutwilllosethisexemptionandincomefromitwillbeliabletoGST.

Incomefromareligiousceremonyorganisedbyacharitabletrustisexemptaspertheabovenotification.SotheincomefromNavratri functions, otherreligious functions, andreligiouspoojas conductedonspecialoccasionslikereligious festivalsbypersonssoauthorised forthispurposebythecharitableorreligious trustareexemptfromGST.

Butacarefulperusalof thisexemptionshowsthatallincomefromsuchareligiousceremonyisnotexempt(servicesother thanbywayofconductofreligiousceremonyarenotexempt).Therefore,thenatureof incomeisanessentialfactorforascertainingwhetheritwillbetaxableorexempt.Ifincomelosesitsreligiousnature,itisdefinitelychargeabletoGST.Forexample,ifwithregardtoGaneshutsav orotherreligiousfunctions,charitabletrustsrentouttheirspacetoagenciesforadvertisementhoardings,incomefromsuchadvertisementischargeabletoGST,asthiswillbeconsideredasincomefromtheadvertisementservices.Further, ifdonation forreligiousceremonyisreceivedwithspecificinstructions toadvertisethenameofadonor, suchdonation incomewillbesubjecttoGST.Butifdonation forreligiousceremonyisreceivedwithout suchinstructions, itmaynotbesubjecttoGST.

EntryNo.80ofNotification No.12/2017-Central Tax(Rate)

Similarly,entryNo.80ofNotificationNo.12/2017-CentralTax(Rate),providesthefollowingexemptiontoanentityregisteredunderSection12AA.

Servicesbywayoftrainingorcoachinginrecreationalactivitiesrelatingto:

(a)artsorculture,or

(b)sportsbycharitableentitiesregisteredundersection12AAoftheIncome-taxAct.

Thus,servicesprovidedbywayoftrainingorcoachinginrecreationalactivitiesrelatingtoartsorcultureorsportsbyacharitableentitywillbeexemptfromGST.

CAYASHWANT J.KASAR 22

CharitableEducationalTrusts

CAYASHWANT J.KASAR 23

EducationServicesThisservicefallsunderheading9992.

ThecommercialeducationissubjecttoGST@18%(CGST9%andSGST9%)orIGST18%.

VariousexemptionsarecontainedinNotificationNo.12/2017-CT(Rates)and9/2017-IT(Rates)bothdated28-6-2017,effectivefrom1-7-2017.

ServicesprovidedbyeducationinstitutionServicesuppliedbyaneducationalinstitutiontoitsstudents,facultyandstaffisexemptfromGST.

CAYASHWANT J.KASAR 24

GSTonmanagement ofeducational institutions bycharitabletrustsIftrustsarerunningschools,collegesoranyothereducationalinstitutionsspecificallyforabandoned,orphans,homelesschildren,physicallyormentallyabusedpersons,prisonersorpersonsoverageof65yearsoraboveresidinginaruralarea,suchactivitieswillbeconsideredascharitableactivitiesandincomefromsuchsupplieswillbewhollyexemptfromGST.

Meaningofthewordruralareadefinedinsaidnotificationisruralareameanstheareacomprisedinavillageasdefinedinlandrevenuerecordsexcludingtheareaunderanymunicipalcommittee,municipalcorporation,townareacommittee,cantonmentboardornotifiedareacommitteeoranyareathatmaybenotifiedasanurbanareabytheCentralGovernmentoraStateGovernment.

CAYASHWANT J.KASAR 25

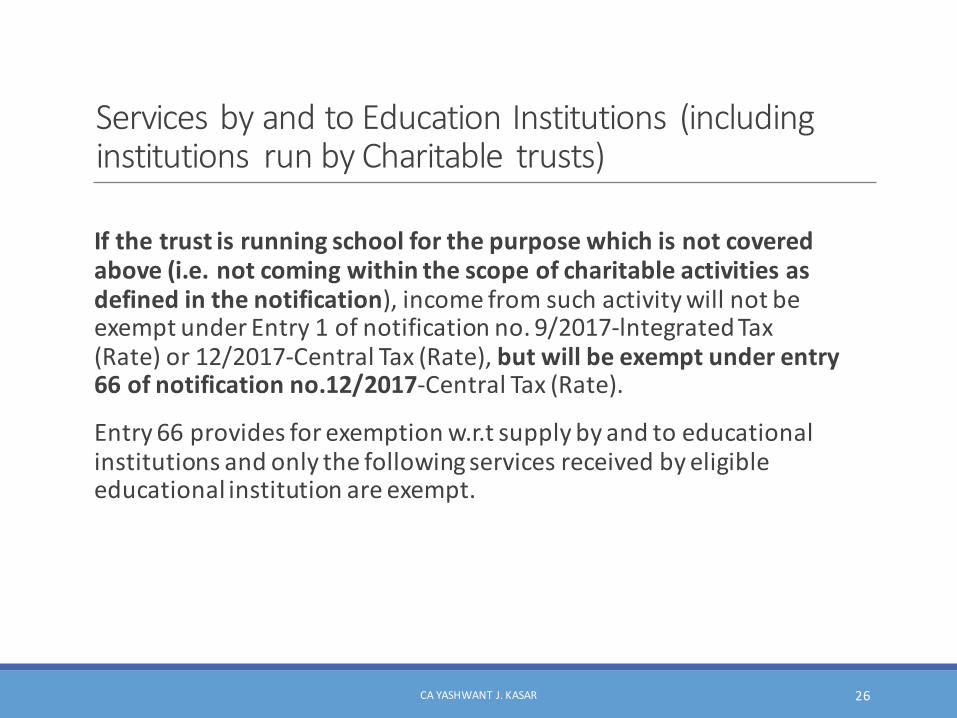

ServicesbyandtoEducationInstitutions (includinginstitutions runbyCharitable trusts)

Ifthetrustisrunningschoolforthepurposewhichisnotcoveredabove(i.e.notcomingwithinthescopeofcharitableactivitiesasdefinedinthenotification),incomefromsuchactivitywillnotbeexemptunderEntry1ofnotificationno.9/2017-lntegratedTax(Rate)or12/2017-CentralTax(Rate),butwillbeexemptunderentry66ofnotificationno.12/2017-CentralTax(Rate).

Entry66providesforexemptionw.r.t supplybyandtoeducationalinstitutionsandonlythefollowingservicesreceivedbyeligibleeducationalinstitutionareexempt.

CAYASHWANT J.KASAR 26

CAYASHWANT J.KASAR 27

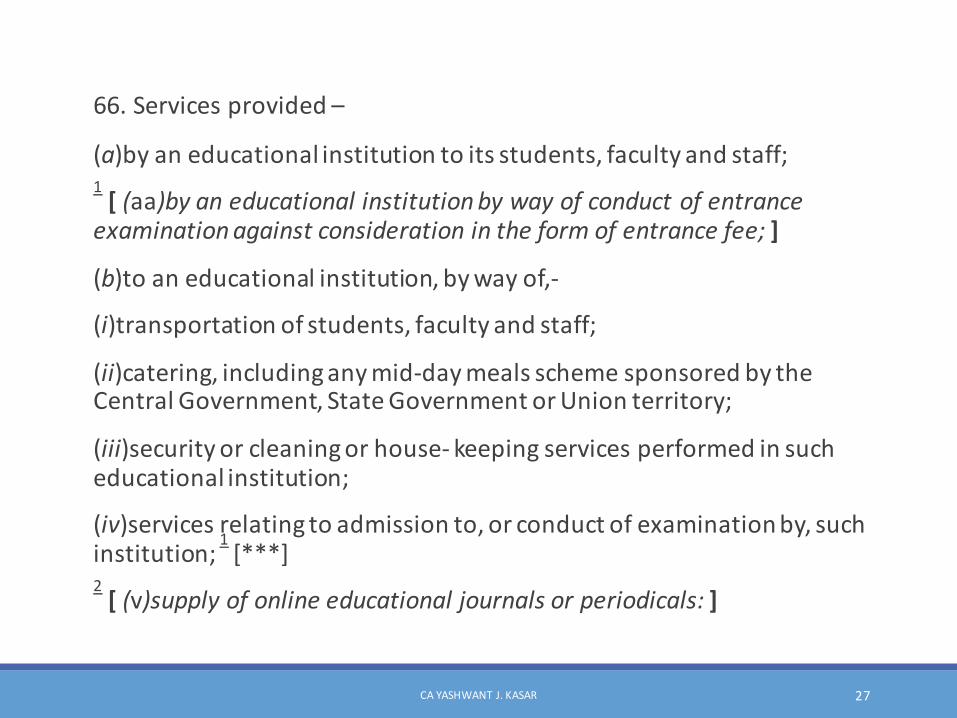

66.Servicesprovided–

(a)byaneducationalinstitutiontoitsstudents,facultyandstaff;1[ (aa)byaneducationalinstitutionbywayofconductofentrance

examinationagainstconsiderationintheformofentrancefee; ]

(b)toaneducationalinstitution,bywayof,-

(i)transportationofstudents,facultyandstaff;

(ii)catering,includinganymid-daymealsschemesponsoredbytheCentralGovernment,StateGovernmentorUnionterritory;

(iii)securityorcleaningorhouse- keepingservicesperformedinsucheducationalinstitution;

(iv)servicesrelatingtoadmissionto,orconductofexaminationby,suchinstitution;

1[***]

2[ (v)supplyofonlineeducationaljournalsorperiodicals: ]

CAYASHWANT J.KASAR 28

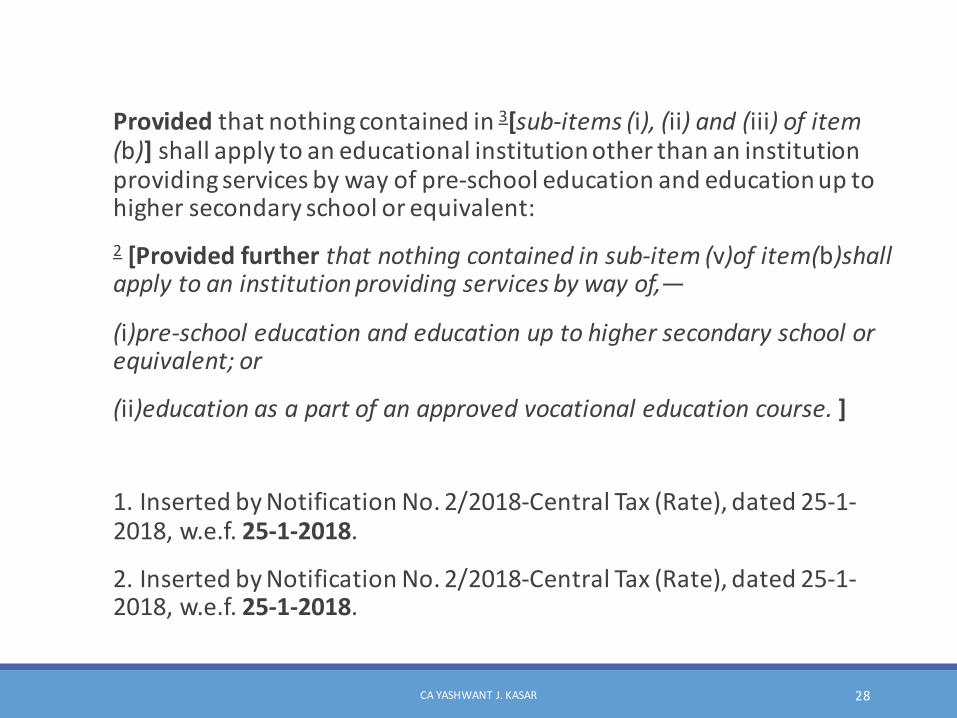

Provided thatnothingcontainedin 3[sub-items(i),(ii)and(iii)ofitem(b)] shallapplytoaneducationalinstitutionotherthananinstitutionprovidingservicesbywayofpre-schooleducationandeducationuptohighersecondaryschoolorequivalent:2 [Providedfurther thatnothingcontainedinsub-item (v)ofitem(b)shallapplytoaninstitutionprovidingservicesbywayof,—

(i)pre-schooleducationandeducationuptohighersecondaryschoolorequivalent;or

(ii)educationasapartofanapprovedvocationaleducationcourse. ]

1. InsertedbyNotificationNo.2/2018-CentralTax(Rate),dated25-1-2018,w.e.f. 25-1-2018.

2. InsertedbyNotificationNo.2/2018-CentralTax(Rate),dated25-1-2018,w.e.f. 25-1-2018.

CircularNo.32/06/2018-GST -ClarificationsIshostelaccommodationprovidedbyTruststostudentscoveredwithinthedefinitionofCharitableActivitiesandthus,exemptunderSl.No.1ofnotificationNo.12/2017-CT(Rate)?

Hostelaccommodationservicesdonotfallwithintheambitofcharitableactivitiesasdefinedinpara2(r)ofnotificationNo.12/2017-CT(Rate).However,servicesbyahotel,inn,guesthouse,cluborcampsite,bywhatevernamecalled,forresidentialorlodgingpurposes,havingdeclaredtariffofaunitofaccommodationbelowonethousandrupeesperdayorequivalentareexempt.Thus,accommodationserviceinhostelsincludingbyTrustshavingdeclaredtariffbelowonethousandrupeesperdayisexempt.[Sl.No.14ofnotificationNo.12/2017-CT(Rate)refers]

CAYASHWANT J.KASAR 29

CAYASHWANT J.KASAR 30

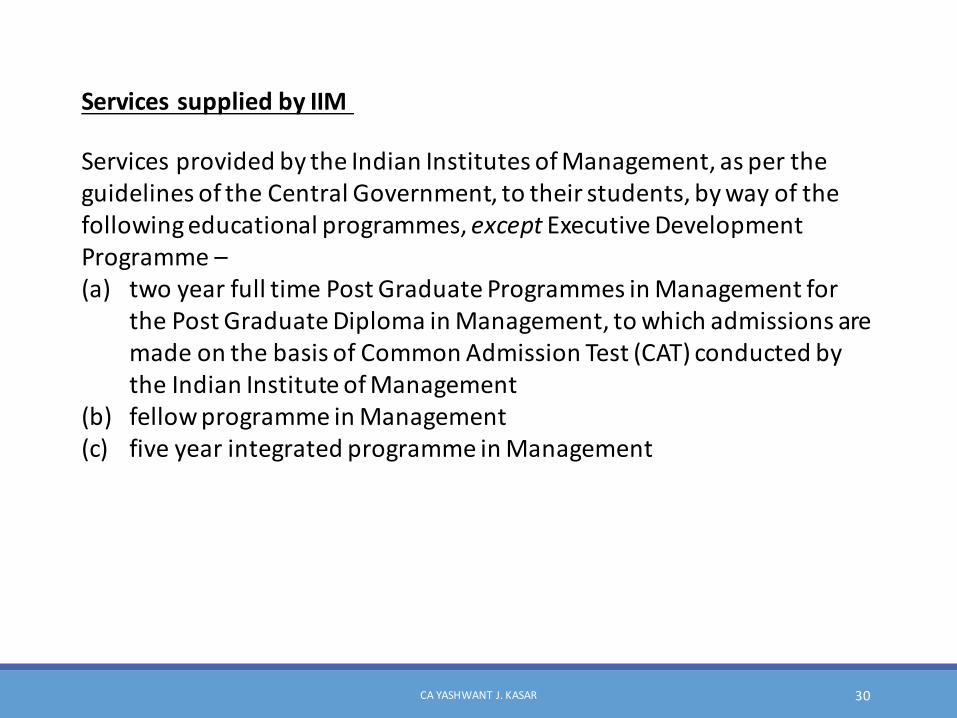

ServicessuppliedbyIIM

ServicesprovidedbytheIndianInstitutesofManagement,aspertheguidelinesoftheCentralGovernment,totheirstudents,bywayofthefollowingeducationalprogrammes, except ExecutiveDevelopmentProgramme–(a) twoyearfulltimePostGraduateProgrammesinManagementfor

thePostGraduateDiplomainManagement,towhichadmissionsaremadeonthebasisofCommonAdmissionTest(CAT)conductedbytheIndianInstituteofManagement

(b) fellowprogrammeinManagement(c) fiveyearintegratedprogrammeinManagement

CAYASHWANT J.KASAR 31

ServicessuppliedbyNationalSkillDevelopmentCorporation(NSDC)

Servicesprovided by- (a)theNationalSkillDevelopmentCorporationsetupbytheGovernmentofIndia(b)aSectorSkillCouncilapprovedbytheNationalSkillDevelopmentCorporation (c)anassessmentagencyapprovedbytheSectorSkillCouncilortheNationalSkillDevelopmentCorporation (d)atrainingpartnerapprovedbytheNationalSkillDevelopmentCorporationortheSectorSkillCouncil,inrelationtofollowing areexempt(i)theNationalSkillDevelopmentProgrammeimplemented bytheNationalSkillDevelopmentCorporation;or(ii)avocationalskilldevelopmentcourseunder theNationalSkillCertificationandMonetaryRewardScheme;or(iii)anyotherSchemeimplementedbytheNationalSkillDevelopment - NotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

CAYASHWANT J.KASAR 32

ServicesofassessmentbodiesunderNSDCServicesofassessingbodiesempanelledcentrallybytheDirectorateGeneralofTraining,MinistryofSkillDevelopmentandEntrepreneurship bywayofassessmentsunder theSkillDevelopment InitiativeSchemeareexempt.

ServicesunderDeen Dayal Upadhyaya YojanaServicesprovidedbytrainingproviders (Projectimplementationagencies)underDeen Dayal Upadhyaya Grameen Kaushalya Yojana implementedbytheMinistryofRuralDevelopment, GovernmentofIndiabywayofoffering skillorvocationaltrainingcoursescertifiedbytheNationalCouncilforVocationalTrainingareexempt.

TrainingprogrammeswhereexpenditurebornebyCentralGovernment -Servicesprovided totheCentralGovernment, StateGovernment, UnionterritoryadministrationunderanytrainingprogrammeforwhichtotalexpenditureisbornebytheCentralGovernment, StateGovernment, Unionterritoryadministrationareexempt.

Definitions relevantinrespectofeducationservices"Approved vocationaleducationcourse"means,-(i)acourserunbyanindustrial traininginstituteoranindustrial trainingcentreaffiliatedtotheNationalCouncilforVocationalTrainingorStateCouncilforVocationalTrainingofferingcoursesindesignatedtradesnotified under theApprenticesAct,1961or(ii)aModularEmployableSkillCourse,approvedbytheNationalCouncilofVocationalTraining, runbyaperson registeredwiththeDirectorateGeneralofTraining,MinistryofSkillDevelopmentandEntrepreneurship - para 2ofNotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

EducationalInstitution

"Educationalinstitution"meansaninstitutionproviding servicesbywayof- (i)pre-schooleducationandeducationuptohigher secondaryschoolorequivalent(ii)educationasapartofacurriculumforobtainingaqualificationrecognisedbyanylawforthetimebeing inforce(iii)educationasapartofanapprovedvocationaleducationcourse- para 2ofNotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

CAYASHWANT J.KASAR 33

CAYASHWANT J.KASAR 34

GSTonOnlineEducationalServices?

OtherServices

CAYASHWANT J.KASAR 35

GSTonservices providedtocharitabletrustsServicesprovidedtocharitabletrustsarenotoutofambitofGST.AllservicesotherthanthosespecificallyexemptedprovidedtocharitabletrustswillbesubjecttoGST.

CAYASHWANT J.KASAR 36

GSTonsupplyofgoodsbyCharitable TrustsThereisnoexemptionforsupplyofgoodsbycharitabletrusts.ThusanygoodssuppliedbysuchcharitabletrustsforconsiderationshallbeliabletoGST.Forinstance,saleofgoodsshallbechargeabletoGST.

CAYASHWANT J.KASAR 37

ImportofServicesAlsoaspertheentryno.10ofNotificationno.9/2017-lntegratedTax(Rate)dated28.06.2017,ifcharitabletrustsregisteredunderSection12AAofIncome-taxActreceivesanyservicesfromproviderofserviceslocatedinnon-taxableterritory,forcharitablepurposes,suchservicesreceivedarenotchargeabletoGSTunderthereversechargemechanism.

CAYASHWANT J.KASAR 38

GSTonarranging yogaandmeditationcampbycharitabletrustsCharitabletrustsorganiseyogacampsorotherfitnesscampsandtheygenerallyarenotfreeforparticipants,astrustschargesomeamountfromtheparticipantsinthenameofaccommodationorparticipation.Iftrustsarearrangingresidentialornon-residentialyogacampsbyreceivingdonationorotherchargesfromtheparticipants,thesewillnotbeconsideredcharitableactivities(asitisdifferentfromadvancementofreligion,spiritualityoryoga).

Sincedonationisreceivedforparticipation,itwillbeconsideredcommercialactivityanditwilldefinitelybecoveredundertheGST.Similarly,ifcharitabletrustsorganisefitnesscampsinreiki,aerobics,etc.,andreceivedonationfromparticipants,suchincomethatcomesunderhealthandfitnessservicesandwillalsobetaxable.

CAYASHWANT J.KASAR 39

GSTonrunning ofpublic libraries bycharitable trusts

NoGSTwillbeapplicableifcharitabletrustsarerunningpubliclibrariesandlendbooks,otherpublicationsorknowledge-enhancingcontent/materialfromtheirlibraries.ThisactivityisspecificallyexcludedbywayofentryNo.50ofNotificationNo.12/2017- CentralTaxRate(andisapplicableforeveryone,includingcharitabletrusts);whichmeansservicesbyprivatelibrariesarenotexempt.Thus,ifdonorsofpubliclibraryremainopentoallandifitcaterstoeducational,informationalandrecreationalneedsofitsusersandfinanceforsuchlibrariescanbeprovidedfromdonation,subscription,fromspecialfundcreatedforthispurposeorfromcombinationofallsuchsources,itwillbecalledpubliclibraryandnoGSTwillbeapplicableonsuchservices.

CAYASHWANT J.KASAR 40

Co-OperativeBanks&CreditSocieties

CAYASHWANT J.KASAR 41

CAYASHWANT J.KASAR 42

Banking servicesfallunderheading9971.

ThemainservicesuppliedbyBanks isofcoursepaymentofinteresttodepositors.

IsInterestsubjecttoGST?“Goods"meanseverykindofmovablepropertyotherthanmoneyandsecurities butincludesactionableclaim,growingcrops,grassandthingsattachedtoorformingpartofthelandwhichareagreedtobeseveredbeforesupplyorunderacontractofsupply;

“Services"meansanythingotherthangoods,moneyandsecurities butincludesactivitiesrelatingtotheuseofmoney oritsconversionbycashorbyanyothermode,fromoneform,currencyordenomination,toanotherform,currencyordenominationforwhichaseparateconsiderationischarged;

CAYASHWANT J.KASAR 43

CAYASHWANT J.KASAR 44

Servicesbywayof— (a)extendingdeposits,loansoradvancesinsofarastheconsiderationisrepresentedbywayofinterestordiscount(otherthaninterestinvolvedincreditcardservices)isexemptfromGST- NotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

"Interest"meansinterestpayableinanymannerinrespectofanymoneysborrowedordebtincurred(includingadeposit,claimorothersimilarrightorobligation)butdoesnotincludeanyservicefeeorotherchargeinrespectofthemoneysborrowedordebtincurredorinrespectofanycreditfacilitywhichhasnotbeenutilized.

Saleorpurchaseofforeignexchangeamong banks ordealersisexempt

Serviceof interse saleorpurchaseofforeigncurrencyamongst banks orauthorizeddealersofforeignexchangeoramongst banks andsuchdealersisexempt- NotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

CAYASHWANT J.KASAR 45

ExemptiontoGSTon bank chargesforcashlesstransactionsupto Rs2,000

Servicesbyanacquiring bank,toanypersoninrelationtosettlement ofanamountupto twothousandrupees inasingletransactiontransactedthroughcreditcard,debitcard,chargecardorotherpaymentcardservice.

"Acquiring bank"meansany banking company,financial institutionincludingnon-banking financialcompanyoranyotherperson,whomakesthepaymenttoanypersonwhoacceptssuchcard- NotificationNo.12/2017-CT(Rate)andNo.9/2017-IT(Rate)bothdated28-6-2017,effectivefrom1-7-2017.

Bank,FI,NBFCliabletopayGSTunderreversechargeinrespectofservicesreceivedfromrecoveryagent

Incaseofservicessuppliedbyarecoveryagenttoa banking companyorafinancialinstitution oranon-bankingfinancial company,therecipientofservicei.e. banking companyorafinancial institutionoranon-bankingfinancial company,locatedinthetaxableterritoryNotification isliabletopayGSTunderreversecharge- No.13/2017-CT(Rates)and10/2017-IT(Rates)bothdated28-6-2017,effectivefrom1-7-2017.

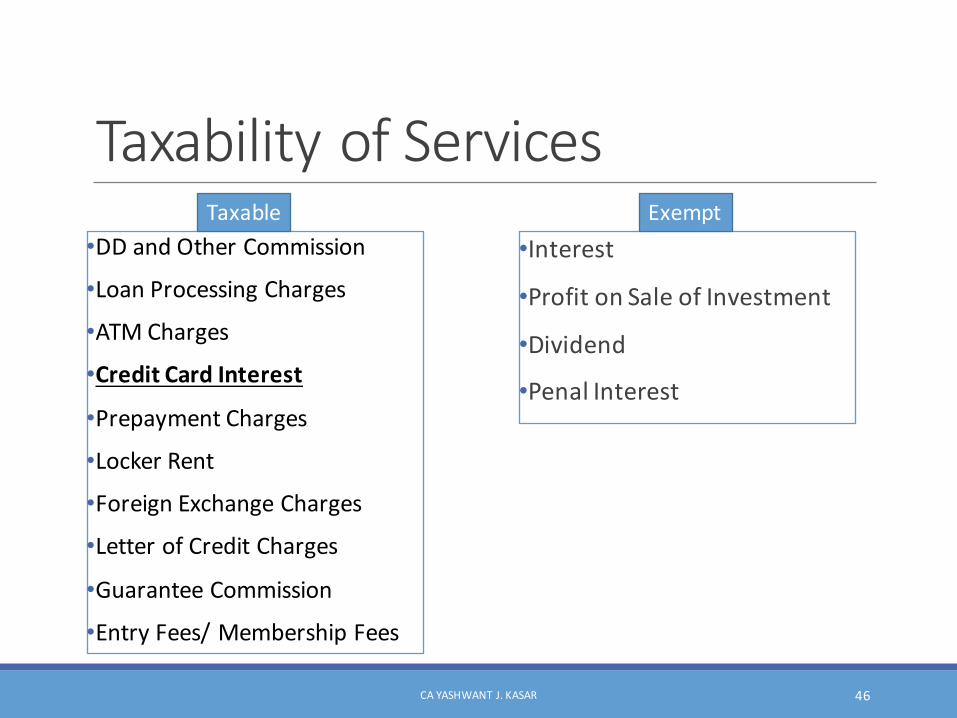

TaxabilityofServices•DDandOtherCommission

•LoanProcessingCharges•ATMCharges

•CreditCardInterest

•PrepaymentCharges

•LockerRent•ForeignExchangeCharges•LetterofCreditCharges

•GuaranteeCommission

•EntryFees/MembershipFees

CAYASHWANT J.KASAR 46

•Interest

•ProfitonSaleofInvestment

•Dividend

•PenalInterest

Taxable Exempt

Banking andotherfinancial serviceswithinIndiaTheplaceofsupplyof bankingandotherfinancialservicesincludingstockbrokingservicestoanypersonshallbethelocationoftherecipientofservicesontherecordsofthesupplierofservices- section12(12)ofIGSTAct.

However,ifthelocationoftherecipientofservicesis not ontherecordsofthesupplierofservices,theplaceofsupplyshallbelocationofthesupplierofservices.

CAYASHWANT J.KASAR 47

Servicessuppliedby BankstoaccountholdersoutsideIndiaIncaseofservicessuppliedbya banking company,orafinancialinstitution,oranon-banking financialcompany,toaccountholders,theplaceofsupplyshallbethelocationofthesupplierofservice- section13(8)(a)ofIGSTAct.Really,thisprovisionisappliesonlytoIndian bank orFinancial Institution,asaforeign bank canneverbe banking companyorFinancial Institutionasdefined"Account"meansanaccountbearinginteresttothedepositor,andincludesanon-residentexternalaccountandanon-residentordinaryaccount-Explanation (a)tosection13(8)ofIGSTAct."Banking company"hasthemeaningassignedtoitinclause(a)ofsection45AoftheReserve Bank ofIndiaAct,1934- Explanation (b)tosection13(8)ofIGSTAct.[Thus,aforeign Bank providingservicefromoutside Indiacannotbe'banking company'.Hence,generalprovisionofplaceofsupplyofservicewillapplyi.e.locationofrecipientofservicewillbeplaceofsupplyofservice].

CAYASHWANT J.KASAR 48

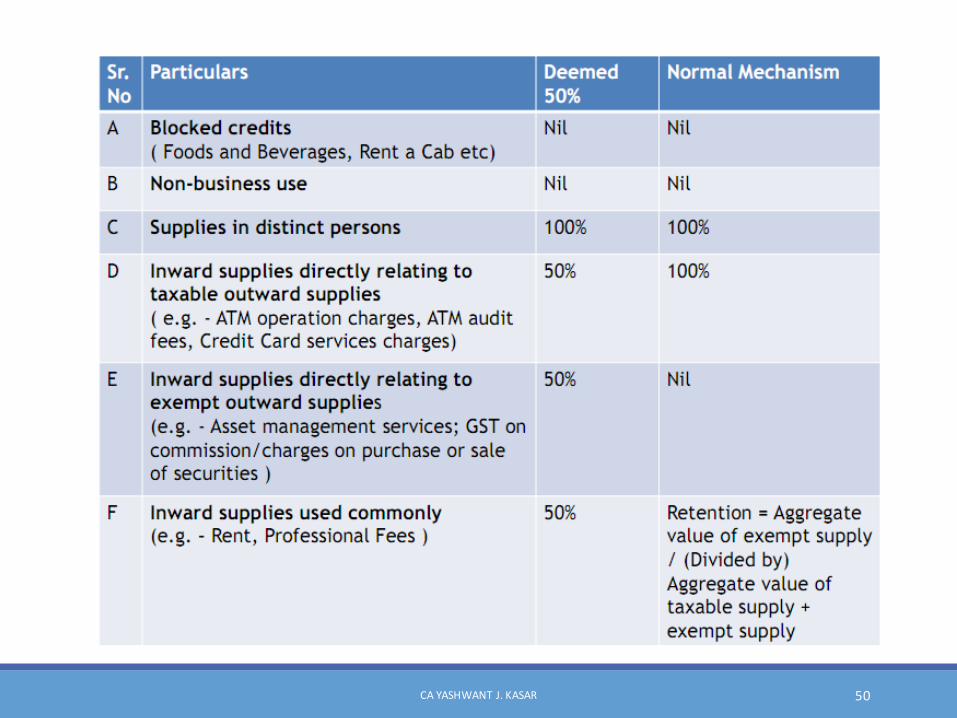

ITC:Special provisions inrespect of Banks,FIandNBFCA banking companyorafinancialinstitution includinganon-banking financialcompany,engagedinsupplyingservicesbywayofacceptingdeposits,extending loansoradvancesshallhavetheoptiontoeithercomplywiththeprovisionsofsection17(2)ofCGSTAct,or availof,everymonth,anamountequaltofiftypercentoftheeligibleinputtaxcreditoninputs,capitalgoodsandinputservicesinthatmonth- section17(4)ofCGSTAct.Theoptiononceexercisedshallnotbewithdrawnduringtheremainingpartofthefinancialyear- first proviso tosection17(4)ofCGSTAct.The50%restrictionshallnotapplytothetaxpaidonsuppliesmadebyoneregisteredpersontoanotherregisteredpersonhavingsamePANnumber-second proviso tosection17(4)ofCGSTAct.Thisprovisionapplieswhen Bank/FI/NBFCinoneStateprovidesservices(orsuppliesgoods)toitsownbranchinanotherState.Inmostofthecases, Bank,FIorNBFCmayfinditeasyandprofitabletoavail50%ofinputtaxcreditinsteadofavailinginputtaxcreditonproportionatebasisaspersection17(2)ofCGSTAct.

CAYASHWANT J.KASAR 49

CAYASHWANT J.KASAR 50

CAYASHWANT J.KASAR 51

Timelimitforissuingtaxinvoiceforservices

Theinvoiceincaseoftaxablesupplyofservices,shallbeissuedwithinaperiodofthirtydaysfromthedateofsupplyofservice- Rule47ofCGSTandSGSTRules,2017.

Ifthesupplierofservicesisaninsurerora banking companyorafinancialinstitution,orNBFC,invoicecanbeissuedwithinfortyfivedaysfromthedateofsupplyofservice- first proviso toRule47ofCGSTandSGSTRules,2017.

Relaxationstoinsurance, Bank,FI,telecomoperatorandNBFCinissuinginvoiceforownbranch/divisioninotherStates

Aspersection25(5)ofCGSTandSGSTAct,ifaperson(withsinglePAN)hasestablishmentsindifferentStates,herequiresGSTregistrationineachState.SuchestablishmentsindifferentStatesaretreatedas'distinctpersons'forpurposeofCGSTandSGSTAct.

TheestablishmentinoneStatemaysupplyservicetoestablishmentinanotherState.Thisisparticularlyinsectorslike banking,insurance,NBFC,FinancialInstitutionsandtelecom.Insuchcases,theymaybegivenrelaxationbyGovernmentonissueofinvoiceeitherwhenthesupplierrecordsthesameinhisbooksoronquarterlybasis-secondprovisotoRule47ofCGSTandSGSTRules,2017.

Sofar,suchnotificationhasnotbeenissued.

Suchinter-StateinvoicesandtransfersarerequiredasGSTisadestinationbasedtaxandtaxistobepaidwheretheservicesorgoodsarefinallyconsumed.

CAYASHWANT J.KASAR 52

TaxInvoicesissuedby Bank,FI,NBFCandinsurancecompany

TaxInvoiceissuedby Bank,FI,NBFCandinsurermaybecalledbyanyothername.Itcanbemadeavailablephysicallyorelectronically.Itmaynothaveserialnumberandaddressofrecipient.However,itshouldhaveotherdetailsasspecifiedinrule46ofCGSTandSGSTRules - Rule44(2)ofCGSTandSGSTRules,2017.

ThisrelaxationshallalsoapplytoBillofSupply,ReceiptVoucher,RefundVoucher,PaymentVoucher,DebitNote,CreditNoteandRevisedInvoice.

InvoiceofISDof banking,FIorNBFC - WheretheInputServiceDistributorisanofficeofa bankingcompanyorafinancialinstitutionorNBFC,ataxinvoiceshallincludeanydocumentinlieuthereof,bywhatevernamecalled,whetherornotseriallynumberedbutcontainingtheinformationasprescribedabove- proviso toRule54(1)ofCGSTandSGSTRules,2017.

Co-OperativeHousingSocieties

CAYASHWANT J.KASAR 53

ActivityofHousingSocietyØFormationofSocietyoncompletionofbuilding

ØAllotmentofSharetoit’smember

ØContribution frommembersformaintenanceofBuilding

WhetherExemptionisavailableonthiscontributionfromMember?

CAYASHWANT J.KASAR 54

Services ofhousingsocietiesorResidentWelfareAssociationThisserviceis'HomeOwners'Association' andfallsunderserviceclassificationtariff999598.

Servicebyanunincorporatedbodyoranon- profitentityregisteredunderanylawforthetimebeing inforce,toitsownmembersbywayofreimbursement ofchargesorshareofcontributionuptoanamountofRs 7,500permemberforsourcingofgoodsorservicesfromathirdpersonforthecommonuseofitsmembersinahousingsocietyoraresidentialcomplexareexempt.

ServicesprovidedbyhousingsocietyorRWAforprovisionofservicewhichisexemptfromGST

Servicebyanunincorporatedbodyoranon-profitentityregisteredunderanylawforthetimebeing inforce,toitsownmembersbywayofreimbursement ofchargesorshareofcontribution fortheprovisionofcarryingoutanyactivitywhichisexemptfromthelevyofGoodsandServiceTaxisexempt[Thisprovisionapplieswhenthehousing societyorRWAundertakesactivitywhichisexemptfromGSTlikemedicalcamp,socialactivitiesetc.]

CAYASHWANT J.KASAR 55

WhetheranyExemptionisallowedtoHousingSocietyEntryNo.77ofNotificationNo.12/2017- CentralTax (Rate)

Servicebyanunincorporatedbodyoranon-profitentityregisteredunderanylawforthetimebeing inforce,toitsownmembersbywayofreimbursement ofchargesorshareofcontribution–

(a)asatradeunion;

(b)for theprovisionofcarryingoutanyactivitywhichisexemptfromthelevyofGoodsandServiceTax;or

(c)up toanamountof 1[seventhousand fivehundred] rupeespermonthpermember forsourcingofgoodsorservicesfromathirdperson forthecommonuseofitsmembersinahousing societyoraresidentialcomplex.

1. Substituted for"fivethousand"byNotificationNo.2/2018-CentralTax(Rate),dated25-1-2018,w.e.f. 25-1-2018.

CAYASHWANT J.KASAR 56

CAYASHWANT J.KASAR 57

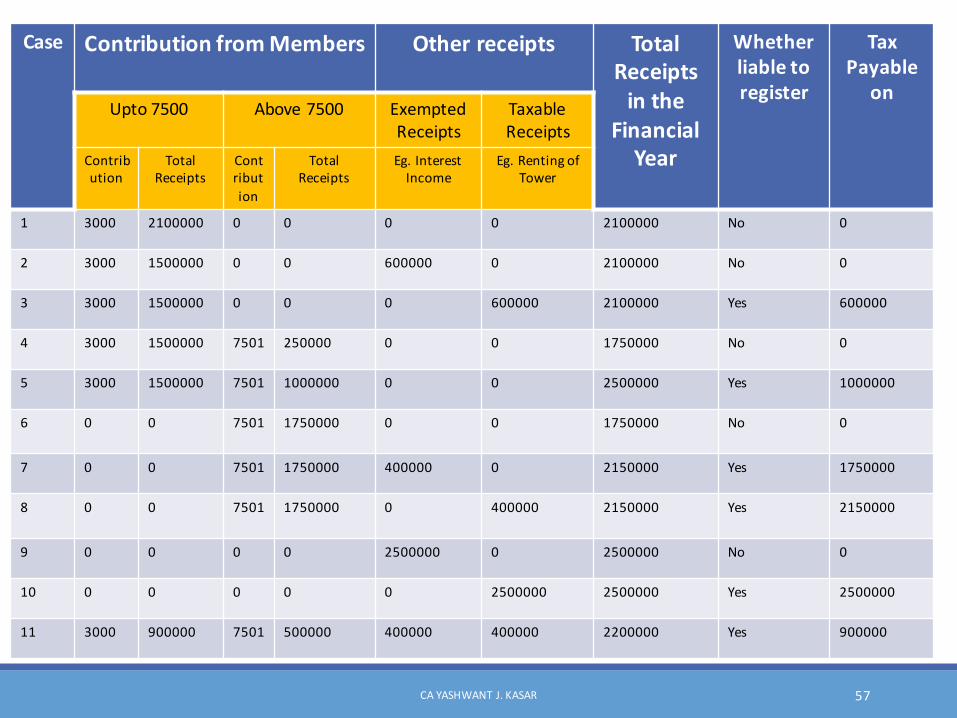

Case ContributionfromMembers Other receipts TotalReceiptsinthe

FinancialYear

Whetherliabletoregister

TaxPayable

onUpto 7500 Above7500 Exempted

ReceiptsTaxableReceipts

Contribution

TotalReceipts

Contribution

TotalReceipts

Eg.InterestIncome

Eg.RentingofTower

1 3000 2100000 0 0 0 0 2100000 No 0

2 3000 1500000 0 0 600000 0 2100000 No 0

3 3000 1500000 0 0 0 600000 2100000 Yes 600000

4 3000 1500000 7501 250000 0 0 1750000 No 0

5 3000 1500000 7501 1000000 0 0 2500000 Yes 1000000

6 0 0 7501 1750000 0 0 1750000 No 0

7 0 0 7501 1750000 400000 0 2150000 Yes 1750000

8 0 0 7501 1750000 0 400000 2150000 Yes 2150000

9 0 0 0 0 2500000 0 2500000 No 0

10 0 0 0 0 0 2500000 2500000 Yes 2500000

11 3000 900000 7501 500000 400000 400000 2200000 Yes 900000

CAYASHWANT J.KASAR 58

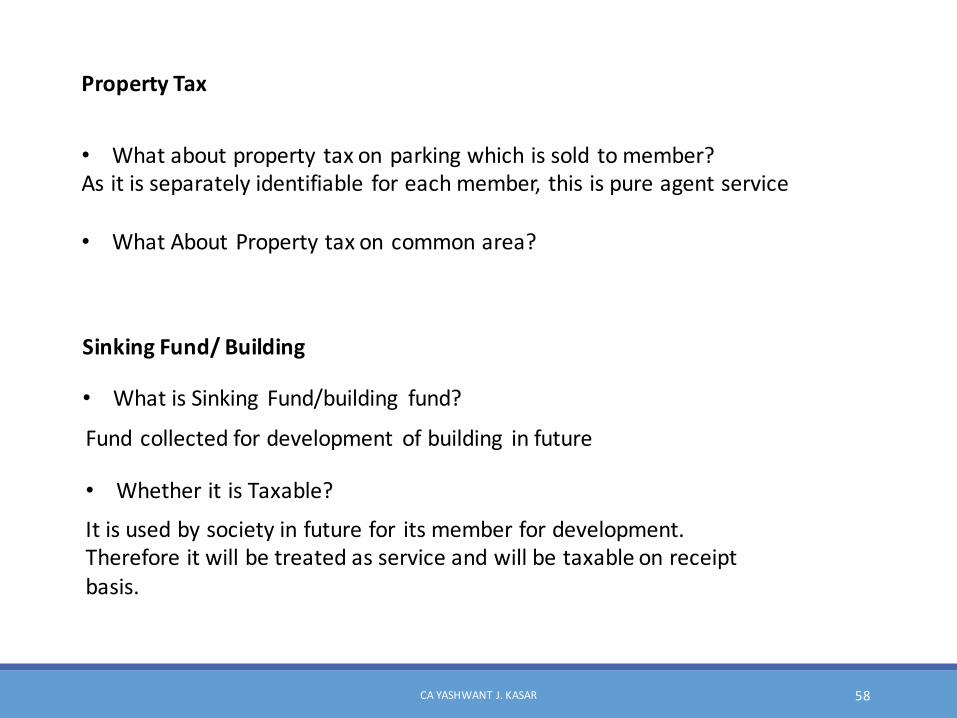

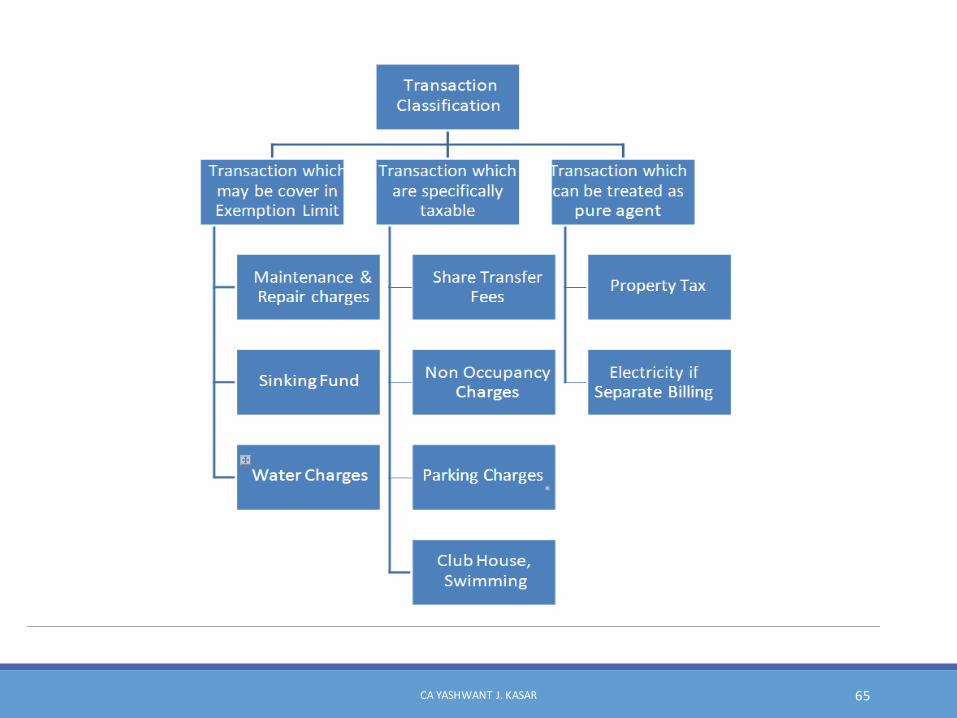

PropertyTax

• Whataboutproperty taxonparkingwhichissold tomember?Asitisseparatelyidentifiable foreachmember, thisispureagentservice

• WhatAboutPropertytaxoncommonarea?

SinkingFund/Building

• WhatisSinking Fund/building fund?

Fundcollectedfordevelopment ofbuilding infuture

• WhetheritisTaxable?

Itisusedbysocietyinfuturefor itsmemberfordevelopment.Thereforeitwillbetreatedasserviceandwillbetaxableonreceiptbasis.

CAYASHWANT J.KASAR 59

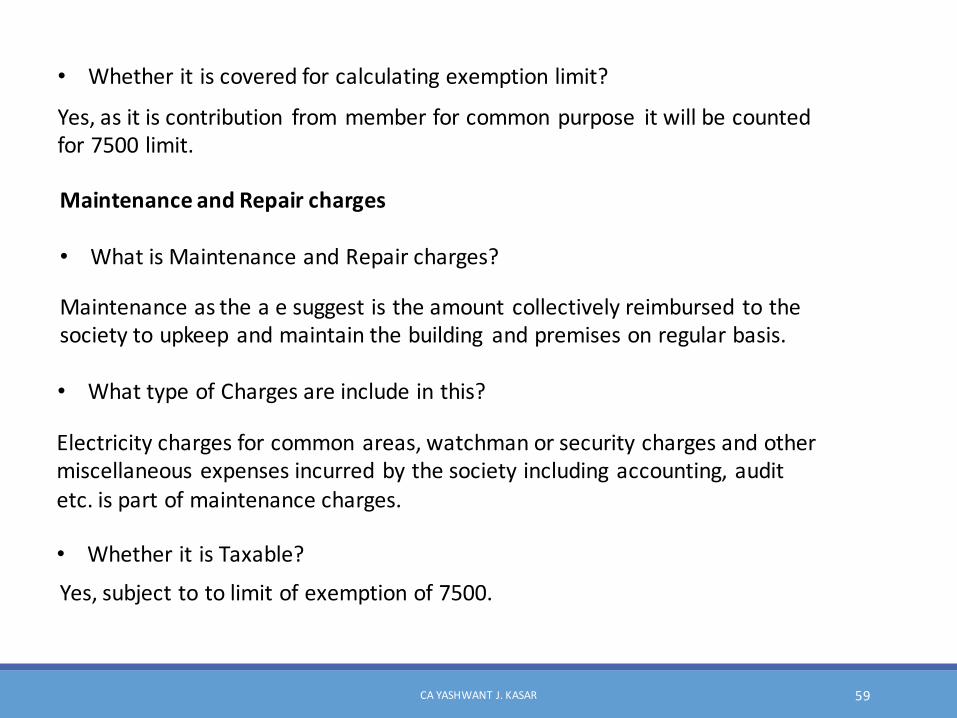

• Whetheritiscoveredforcalculatingexemptionlimit?

Yes,asitiscontribution frommemberforcommonpurpose itwillbecountedfor7500limit.

MaintenanceandRepaircharges

• WhatisMaintenanceandRepaircharges?

Maintenanceastheaesuggestistheamountcollectivelyreimbursed tothesocietytoupkeepandmaintainthebuilding andpremisesonregularbasis.

• WhattypeofChargesareincludeinthis?

Electricitychargesforcommonareas,watchmanorsecuritychargesandothermiscellaneousexpensesincurredbythesocietyincludingaccounting,auditetc.ispartofmaintenancecharges.

• WhetheritisTaxable?

Yes,subjecttotolimitofexemptionof7500.

CAYASHWANT J.KASAR 60

ShareTransferFees

• WhatisShareandTransferFees?

Sharetransferfeesaretheamountchargedbythe societyfortransferofsharesbymember

• WhetheritisTaxable?

Yes,itistaxable.

• Whetheritiscoveredforcalculatingexemptionlimit?

No,itisnotcoverinexemptionasitisnotcontribution forsourcingofservicefromthirdperson.

CAYASHWANT J.KASAR 61

NonOccupancyCharges

• WhatisNonoccupancyCharges?

Nonoccupancychargesarechargesleviedbyahousing societyonlywhenaflatorunitisletoutbyitsmembers

• WhetheritisTaxable?

Yes,itistaxable

• Whetheritiscoveredforcalculatingexemptionlimit?

No,itisnotcoverinexemptionasitisnotcontribution forsourcingofservicefromthirdperson

CAYASHWANT J.KASAR 62

ParkingCharges

• WhatisParkingCharges?

Chargestoregulatetheparkingplacebetweenthemembersandproviding ofspacebyuseofvacantlandbelonging tothesocietyforaconsideration.

• WhetheritisTaxable?

YesitispurelyserviceandthusitistaxableinNature.

• Whetheritiscoveredforcalculatingexemptionlimit?

Noasthereisno3rd person isinvolved inthisservice.

CAYASHWANT J.KASAR 63

WaterCharges

• WhatisWaterCharges?thesocietyisnotselling thewatertoitsmembers.Itisjustproviding thepipeline todeliverwaterintheenterprises.

• WhatisroleofSocietyinthis?BillingbyMunicipal corporation inthenameofsocietyandthenonsomebasissocietycollectchargesfrommember.

• WhetheritisTaxable?Yes,asitisagaincontribution frommember forcommonuseofitsmember.Thisistaxablesubjecttolimitofexemptionof7500.

• WhataboutcommonWaterusedlikeSwimmingPool?Itisalsotaxablesubjecttolimitofexemptionof7500.

• Whatifdifferentmeterisprovided foreachmember?Itwillfallunderpureagentservice,sonottaxable.

CAYASHWANT J.KASAR 64

Chargesforuseofclubhouse,swimmingPool,etc

• WhatisWaterCharges?Thesearespecificservicesbythesocietytothememberopting forsuchfacilities.

• WhetheritisTaxable?Yes,subjecttoexemptionlimitofRs.7500.

OtherTransaction

• RentalforMobile towerRentingServiceLiabletotaxat

• Hording chargesAdvertisementChargesLiabletoTax

• UseofterraceforfunctionofnonmemberormemberRentingServiceLiabletotax

• InterestondefaultchargesNotcoveredinexemptionasitisnotinterestonadvances.Thereforeliabletotax

CAYASHWANT J.KASAR 65

CAYashwantJ.KasarB.Com,FCA,DISA,CISA,PMP,FAIA

Cell:+919822488777Email:[email protected]

ThankYou!

CAYASHWANT J.KASAR 66