guide to law office bookkeeping - law society of … · guide to law office bookkeeping ... society...

TRANSCRIPT

GUIDE TO LAW OFFICE BOOKKEEPING

© 2005 The Law Society of Saskatachewan

GUIDE TO LAW OFFICE BOOKKEEPING

Edited by: John E. Allen, C.A. Auditor/Inspector

The Law Society of Saskatchewan 1100 - 2500 Victoria Avenue

Regina, SK S4P 3X2

(Patterned after The Law Society of Alberta Guide to Manual Law Office Bookkeeping

by Paul McLaughlin)

TABLE OF CONTENTS OVERVIEW Page 1 INTRODUCTION Page 3 1.1 Potential Users of Manual Bookkeeping Page 3 1.2 Downsides of Manual Bookkeeping Systems Page 3 1.3 What This System Does and Does Not Provide Page 4 1.4 General Comments about Law Office Accounting in Saskatchewan Page 5 1.5 Financial Classifications and Debits/Credits Page 6 ACCOUNTS/SUPPLIES Page 8 THE TRUST ACCOUNTING SYSTEM Page 10 3.1 Trust Records Page 10 3.2 Deposits to Pooled Trust Page 11 3.3 Pooled Trust Cheques Page 14 3.4 Separate Interest-Bearing Trust Accounts Page 16 3.5 Trust Transfer Journal Page 21 3.6 Trust Reconciliations Page 22 3.7 Appendix A Page 22 THE GENERAL LEDGER (“GL”) ACCOUNTING SYSTEM Page 23 4.1 GL Accounting Records Page 23 4.2 The GL Synoptic (Daily General Journal) Page 22 4.3 General Cheques Page 24 Routine Office Expenses (Page 25) Office Expenses Payment posted to Multiple Accounts (Page 25) Bank Charges and Overdraft Interest (Page 26) Business Loan (Page 26) Draws (Page 27) Client Disbursements (Page 27) Payroll (Page 27) GST (Page 29) 4.4 Rendering Accounts to Clients Page 29 4.5 General Account Deposits Page 31 Payment of Fees and Disbursements (Page 31) Capital Contribution (Page 32) Bank Loan Increase (Page 32) Recoveries (Page 33) 4.6 Office Credit Card Page 33 4.7 Disbursements Page 34 4.8 Monthly GL Reconciliation and Report Page 36 APPENDIX “A” - Trust Accounting Examples APPENDIX “B” - General Ledger Accounting Examples

1

OVERVIEW This guide is intended to assist lawyers using either manual or computerized bookkeeping systems although reference is made mainly to manual systems. The INTRODUCTION (Page 3), outlines who should consider using a manual system, what it provides and what it doesn’t provide, and offers some general comments about law office accounting in Saskatchewan. Part 2, SUPPLIES (Page 6), lists what you will have to buy to implement a manual system. Part 3, THE TRUST ACCOUNTING SYSTEM (Page 8), details the records needed for trust accounting. It will guide you through the steps needed to record basic trust transactions, including: ► Deposits to the trust account. ► Payments from the trust account. ► Payments to and transfers from separate interest-bearing trust accounts. ► Monthly trust reconciliation. Part 4, THE GENERAL ACCOUNTING SYSTEM (Page 22), details the records needed for general ledger (“GL”) accounting. It will guide you through the steps needed to record basic general account transactions, including: ► Payments from the general account for expenses, service charges, interest, loan payments, credit card payments, drawings, client disbursements, payroll, GST and PST.

► Rendering accounts to clients. ► Receiving payments from clients for fees, disbursements and interest. ► Receiving capital contributions and loan advances. ► Charges to credit cards. ► Disbursements incurred on behalf of a client. ► A monthly GL reconciliation and report.

2

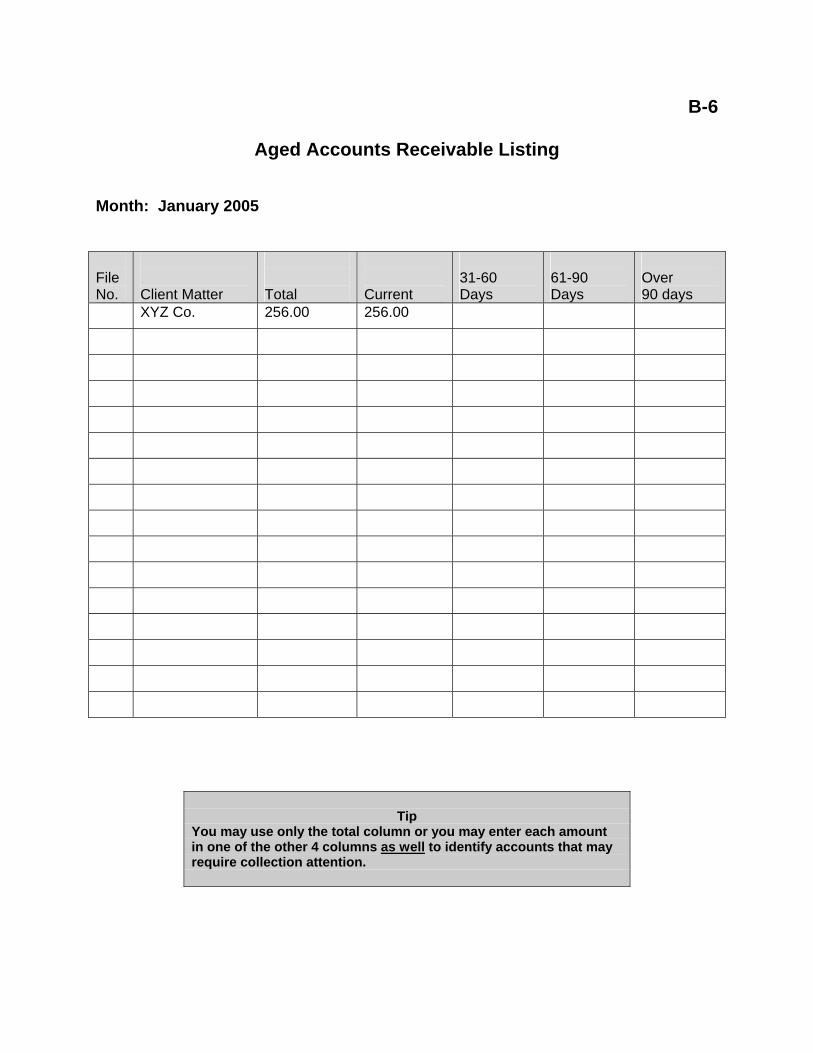

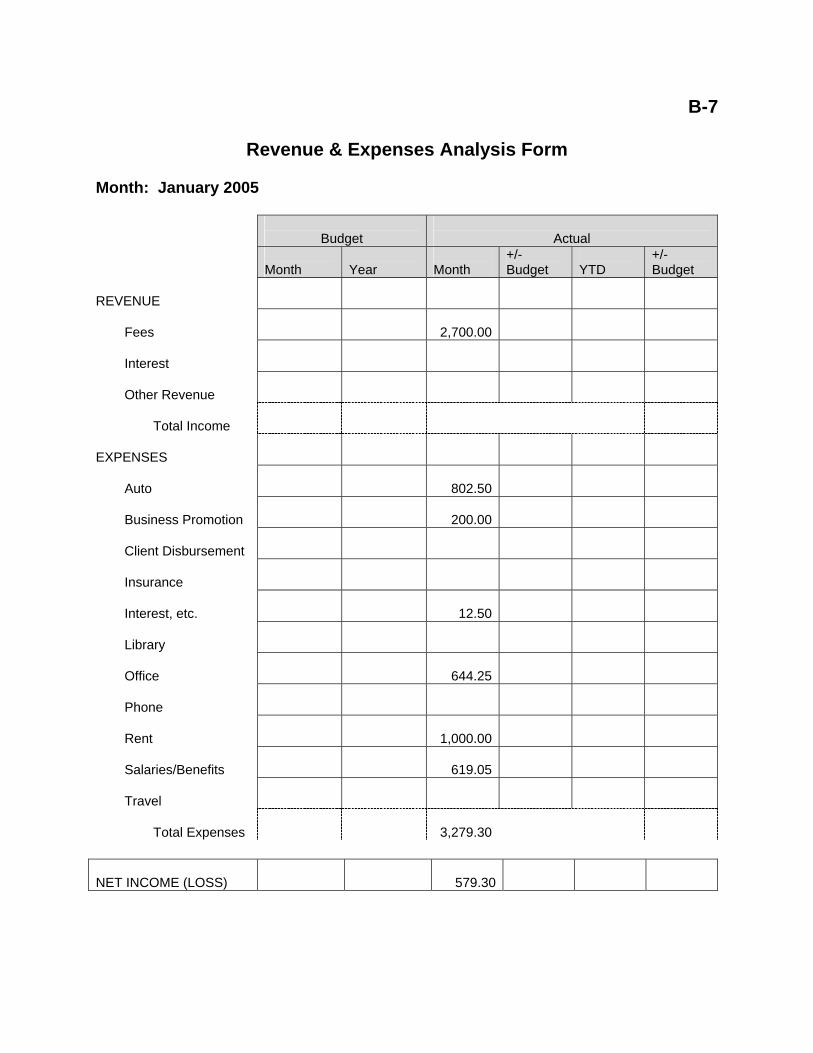

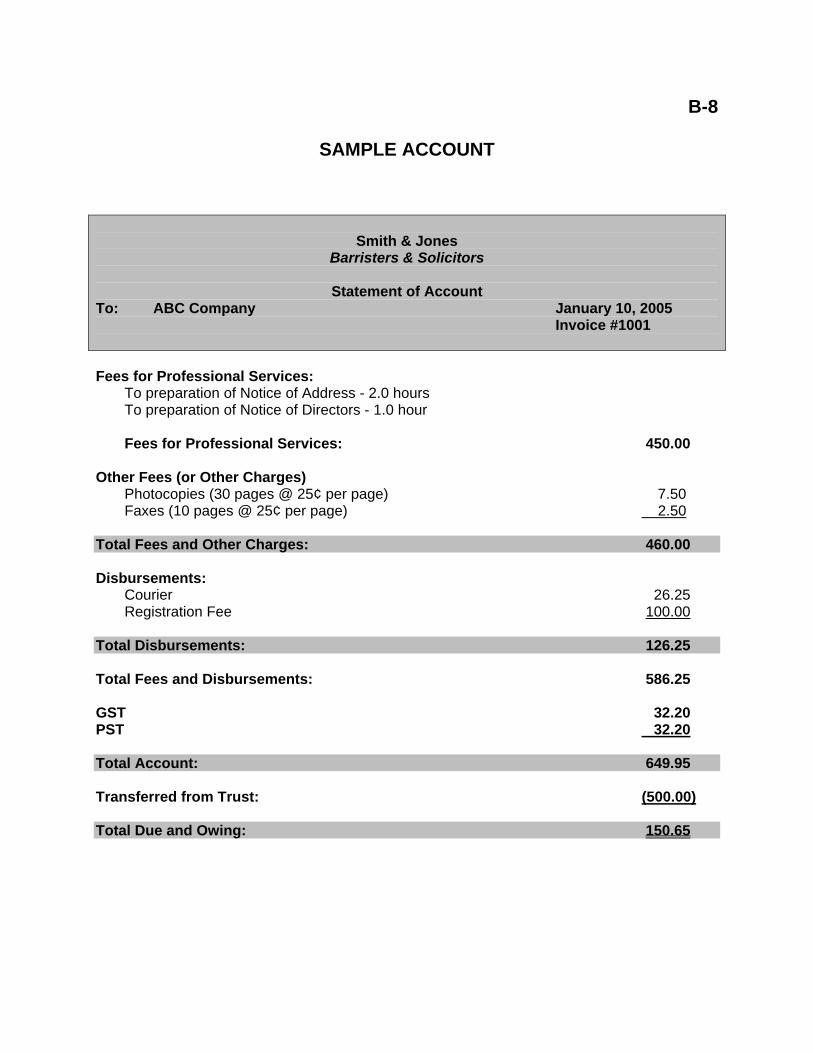

APPENDIX A ► Trust Journal - Example ► Trust Journal - Column Descriptions ► Trust Journal - Entry Descriptions ► Trust Reconciliation Checklist ► Trust Reconciliation (including outstanding cheque list and SIBA list) and Client Trust Listing - Example - Blank Forms APPENDIX B ► General Ledger Synoptic (General Daily Journal) ► General Ledger Synoptic - Column Description ► General Ledger Synoptic- Entry Descriptions ► General Ledger Reconciliation and Checklist ► General Account Reconciliation (including outstanding deposits and cheques) - Example - Blank Form ► Aged Accounts Receivable Listing - Example - Blank Form ► Revenue and Expense Analysis - Example - Blank Form ► Sample Account

3

Part 1 INTRODUCTION

1.1 Potential Users of Manual Bookkeeping Although computerized accounting and management information systems are used widely in today’s law offices, there is still a place for manual bookkeeping systems, particularly for: ► Lawyers just starting out. ► Lawyers with a minimal amount of bookkeeping (low volume). ► Lawyers who do not want to computerize. A manual bookkeeping system is inexpensive to set up and operate and gives the practitioner invaluable exposure to the basic requirements of law office accounting. It is necessary to understand basic accounting requirements/principles to evaluate accuracy and adequacy of computer system output. Whether a system is manual or computerized, the difference is in the process, not in the records themselves. Both require: ► Receipts. ► Deposit Slips. ► Cheques. ► Client Trust Ledger, etc. 1.2 Downsides of Manual Bookkeeping Systems When deciding whether to use manual bookkeeping, the practitioner should keep several things in mind: ► Keeping a manual system current requires a significant commitment of time, energy and attention to detail. ► Manual bookkeeping requires posting and other procedures that will often appear time-consuming and repetitious. ► Manual bookkeeping has few built-in audit controls to prevent errors. ► Manual bookkeeping systems do not easily produce management information.

4

1.3 What a Manual System Does and Does Not Provide A manual system provides: ► A complete trust accounting system, including the monthly trust reconciliation. ► A system for identifying and tracking disbursements. ► A system for identifying and tracking accounts receivable. ► A partial expenses accounting system. ► Rules for balancing the GL monthly. ► A limited amount of management information in the form of a few basic monthly reports. However, the manual system described is not a full law office accounting and management information system and it does not provide: ► Time keeping. ► A Profit and Loss Statement or a Balance Sheet (although it does produce most of the information needed for those records). ► Management information beyond some very basic reports. ► Cash flow analysis or projection.

TIP

This system is not the only way to do manual bookkeeping; any system that complies with the Law Society Rules may be used. For tax and business purposes, your system should comply with generally accepted accounting principles.

TIP It is up to you to familiarize yourself with the Rules of the Law Society respecting accounting and to exercise sound professional judgement when implementing your accounting system.

5

1.4 General Comments about Law Office Accounting in Saskatchewan ► The Law Society Rules apply to all aspects of trust accounting; they also apply to many aspects of General Ledger (“GL”) accounting. ► Specific Rules and processes apply to the receipt of cash and particularly large amounts of cash. These Rules currently prohibit a member from receiving more than $7,500.00 in cash relating to one transaction. Consideration is also being given to requiring members to follow certain procedures when receiving cash from and/or refunding cash to clients. Members are advised to check current Rules or contact the Law Society if this issue is encountered. ► Independent practitioners that share a trust account must maintain a common set of trust accounting books and records. ► When you open a new practice, you must file a Form TA-1 (Commencement Report). Each year thereafter, you will file a Form TA-3 (Practice Declaration), being your annual certification to the Law Society with respect to trust account activity, due 90 days after your fiscal year end. You will also have to engage an accountant to conduct a review of your records and complete and file a Form TA-5 or TA-5S (Accountant’s Report) also within 90 days of your fiscal year end. ► All accounting records and certain supporting information must be retained for at least 6 years (Rule 980(1)) with records referred to in Rule 962(a) and (b) and 963(c) required to be kept for at least 10 years. Canada Revenue Agency and other regulatory bodies may require different retention periods and the member/firm must ensure all requirements are met before records are destroyed. ► If you discover an inadvertent discrepancy in your trust account (e.g. the bank deducted cheque printing charges), you must make payment to trust to cover the deficiency immediately and advise the Law Society of any discrepancies greater than $100.00 along with a description of the circumstances and corrective action taken. ► Help is available. The Law Society’s Auditor is available to answer questions on the Law Society Rules relating to accounting and accounting procedures.

6

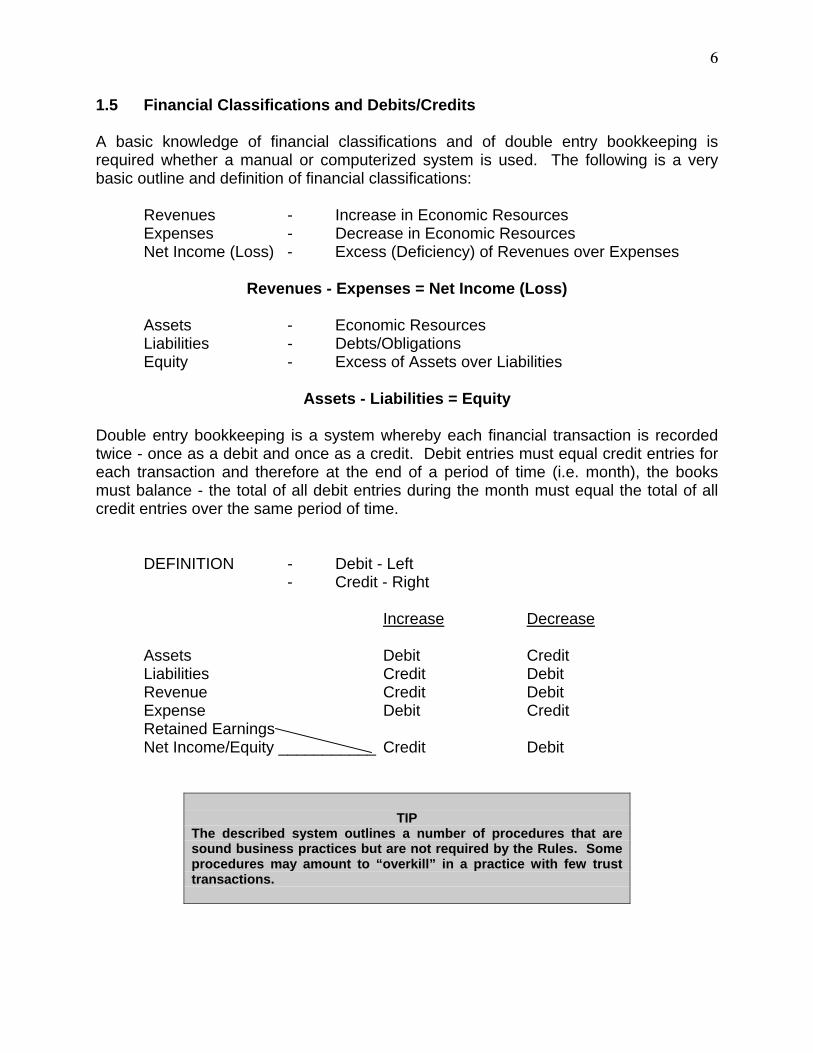

1.5 Financial Classifications and Debits/Credits A basic knowledge of financial classifications and of double entry bookkeeping is required whether a manual or computerized system is used. The following is a very basic outline and definition of financial classifications: Revenues - Increase in Economic Resources Expenses - Decrease in Economic Resources Net Income (Loss) - Excess (Deficiency) of Revenues over Expenses

Revenues - Expenses = Net Income (Loss)

Assets - Economic Resources Liabilities - Debts/Obligations Equity - Excess of Assets over Liabilities

Assets - Liabilities = Equity Double entry bookkeeping is a system whereby each financial transaction is recorded twice - once as a debit and once as a credit. Debit entries must equal credit entries for each transaction and therefore at the end of a period of time (i.e. month), the books must balance - the total of all debit entries during the month must equal the total of all credit entries over the same period of time. DEFINITION - Debit - Left - Credit - Right Increase Decrease Assets Debit Credit Liabilities Credit Debit Revenue Credit Debit Expense Debit Credit Retained Earnings Net Income/Equity ___________ Credit Debit

TIP

The described system outlines a number of procedures that are sound business practices but are not required by the Rules. Some procedures may amount to “overkill” in a practice with few trust transactions.

7

It should be noted when recording entries in the General Ledger Synoptic (Daily General Journal - Appendix B) that each column is labeled as either a “debit” column or a “credit” column. If a credit amount is to be entered in a debit column or vice versa, that amount is shown in brackets. See Appendix B, Line 10, for an example.

8

Part 2 ACCOUNTS/SUPPLIES

To implement the accounting system, you will need: ► A pooled trust account, that is, an interest-bearing account in a Saskatchewan branch of an “approved depository” (defined as “a chartered bank, trust corporation or credit union”), designated as a “trust account” in your name. This account will hereinafter be referred to as your trust bank or trust bank account.

TIP

You are required by Rule 911(2) to instruct your trust bank to remit the interest on your pooled trust account to the Law Foundation at least quarterly.

TIP You must make sure your bank agrees not to recover service charges or amounts from your trust account. Arrangements can be made with your bank to have these amounts charged directly to your general account. Alternatively, a nominal amount of up to $100.00 may be deposited into trust under your name, against which service charges and like bank fees may be charged.

► A general bank account maintained in connection with the firm’s law practice.

► Deposit books for each of your trust and general bank accounts (supplied by your bank).

► Prenumbered and preprinted trust cheques and general cheques preferably with stubs (supplied by your bank). Trust cheques must be printed with the words “trust” or “trust account” clearly printed on the face of the cheque. This is usually above the signature area on the cheque.

TIP

To avoid the embarrassment of issuing cheques on the wrong account, order your trust and general cheques in distinctly different colours.

9

► Two bound three-part receipt books, preferably prenumbered, one for trust and one for general (manual system). ► Three ledger books consisting of a ring-type book, ledger cards and index cards, to use as your client trust ledgers and your client accounts receivable ledgers (manual system).

TIP

The Rules allow you to open more than one trust account and more than one general account. Keeping track of more than one trust and/or general account will increase the volume and complexity of your bookkeeping and significantly increase the chances for error. You should therefore limit yourself to one trust and one general account unless you have a sound business reason for having more.

► An accounting journal book (daily journal) with approximately 8 columns for the date, particulars, receipt/cheque #, deposits, cheques and balance to use as your Trust Receipts and Disbursements Journal (manual system). ► An accounting journal book (general journal) with columns for the date and particulars, and 24 to 28 columns for numbers across two pages (this is referred to as a General Journal) (manual system). ► Several three-ring binders (manual system).

TIP

A journal is an accounting record, usually multi-columned, designed to record a variety of different transactions chronologically.

TIP A ledger is an account record, also usually multi-columned, designed to record chronologically all the transactions that relate to a specific account and to show the balance of that account. Ledgers are usually in loose-leaf form.

10

Part 3 THE TRUST ACCOUNTING SYSTEM

3.1 Trust Records Your trust records will consist of: ► Trust Receipts Book. ► Trust Deposit Book. ► Pooled Trust Account Cheque Book. ► Trust Receipts and Disbursements Journal (also known as the daily journal), in which you will keep a running record of all trust transactions and a running balance of your overall trust balance. ► Client Trust Ledger, where you will keep track of your trust transactions on a client-by-client basis.

TIP

When you receive trust money from one client for more than one matter at the same time, it will be easier to keep track of the flow of funds if you open separate client trust ledger accounts for each matter.

► Bank statements, including pooled trust account statements, passbooks for daily interest savings accounts and statements regarding term deposits. ► Monthly reconciliation forms, including the monthly trust listing. ► Any material in your files that substantiates your trust posting, such as mortgage advance transmittal letters, releases, directions to pay, statements of adjustment, statements of account, trust statements, etc.

11

TIP You must keep your records at your place of practice except during such period as your accountant may need them to complete Form TA-5 or TA-5S.

TIP All posting must be done in ink.

TIP Try to avoid abbreviations, the meaning of which is not obvious.

TIP The Rules require you to keep your books current at all times.

TIP The order in which procedures are described in this Guide is meant to help keep your records up to date. You should therefore carry out the procedures in order.

TIP One of the functions of bookkeeping is to establish an audit trail that ties together all the records that relate to a transaction. Therefore, the same information may be recorded several times in various journals and ledgers.

3.2 Trust Receipts/Deposits to Pooled Trust The following steps are required to process a receipt of trust monies and deposit those monies to your pooled trust account.

TIP

Rule 910(1) requires you to deposit trust money “forthwith” -- the same or the next banking day.

12

3.2.1 Issue a receipt. The receipt, preferably prenumbered, should contain full information about the transaction, including: ► Date of receipt.

► From whom the funds were received. ► Why the funds were paid to you (e.g. retainer, balance to close, mortgage advance). ► File number and/or client name. ► Amount. 3.2.2 Consider photocopying the deposit instrument. Record the date, the file number and the purpose for the deposit on the photocopy (optional procedure).

TIP

If you intend to disburse trust money to a third party immediately after receiving it from your client, you should require certified funds unless the source of the funds is another lawyer or a financial institution. It is less important to get certified funds where the money will remain in your trust account for some time before being disbursed, but it may be prudent if you do not know the client well.

3.2.3 Record the deposit in the cheque book. Record the deposit on your cheque book stubs and update the running balance (optional).

“Funds”, as defined in the Rules, includes credit card slips. If you deposit a credit card slip into trust, associated service charges, fees and discounts are your responsibility and must be paid from your general bank account. The client must receive credit for the full amount paid. You must deposit the credit card slip “expeditiously”, so you cannot hold a blank, signed credit card slip as security for your fees and disbursements. You should understand your bank’s clearing rules for credit card slips to ensure that you do not disburse funds that have not cleared. Also, caution is advised if trust amounts must be received via telephone (unsigned) as the credit card company may reverse this amount for up to a year after processing.

13

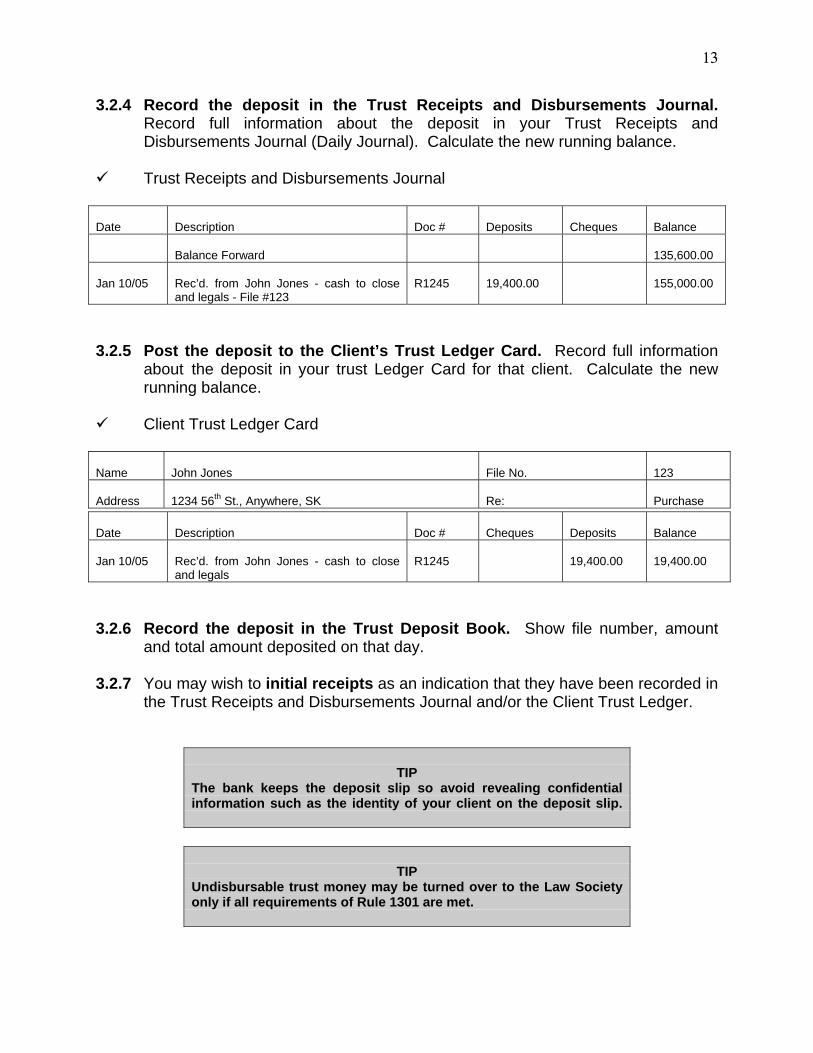

3.2.4 Record the deposit in the Trust Receipts and Disbursements Journal. Record full information about the deposit in your Trust Receipts and Disbursements Journal (Daily Journal). Calculate the new running balance.

Trust Receipts and Disbursements Journal Date

Description

Doc #

Deposits

Cheques

Balance

Balance Forward

135,600.00

Jan 10/05

Rec’d. from John Jones - cash to close and legals - File #123

R1245

19,400.00

155,000.00

3.2.5 Post the deposit to the Client’s Trust Ledger Card. Record full information about the deposit in your trust Ledger Card for that client. Calculate the new running balance.

Client Trust Ledger Card Name

John Jones

File No.

123

Address

1234 56th St., Anywhere, SK

Re:

Purchase

Date

Description

Doc #

Cheques

Deposits

Balance

Jan 10/05

Rec’d. from John Jones - cash to close and legals

R1245

19,400.00

19,400.00

3.2.6 Record the deposit in the Trust Deposit Book. Show file number, amount and total amount deposited on that day. 3.2.7 You may wish to initial receipts as an indication that they have been recorded in the Trust Receipts and Disbursements Journal and/or the Client Trust Ledger.

TIP

The bank keeps the deposit slip so avoid revealing confidential information such as the identity of your client on the deposit slip.

TIP Undisbursable trust money may be turned over to the Law Society only if all requirements of Rule 1301 are met.

14

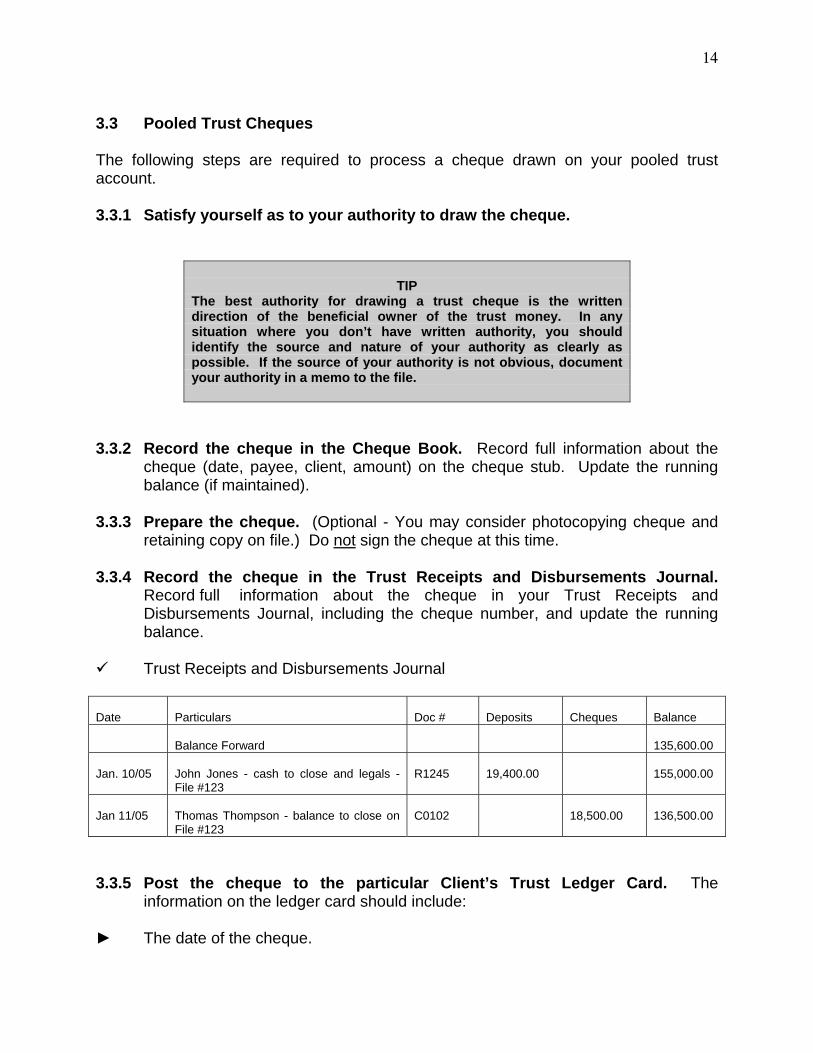

3.3 Pooled Trust Cheques The following steps are required to process a cheque drawn on your pooled trust account. 3.3.1 Satisfy yourself as to your authority to draw the cheque.

TIP

The best authority for drawing a trust cheque is the written direction of the beneficial owner of the trust money. In any situation where you don’t have written authority, you should identify the source and nature of your authority as clearly as possible. If the source of your authority is not obvious, document your authority in a memo to the file.

3.3.2 Record the cheque in the Cheque Book. Record full information about the cheque (date, payee, client, amount) on the cheque stub. Update the running balance (if maintained). 3.3.3 Prepare the cheque. (Optional - You may consider photocopying cheque and retaining copy on file.) Do not sign the cheque at this time. 3.3.4 Record the cheque in the Trust Receipts and Disbursements Journal. Record full information about the cheque in your Trust Receipts and Disbursements Journal, including the cheque number, and update the running balance.

Trust Receipts and Disbursements Journal Date

Particulars

Doc #

Deposits

Cheques

Balance

Balance Forward

135,600.00

Jan. 10/05

John Jones - cash to close and legals - File #123

R1245

19,400.00

155,000.00

Jan 11/05

Thomas Thompson - balance to close on File #123

C0102

18,500.00

136,500.00

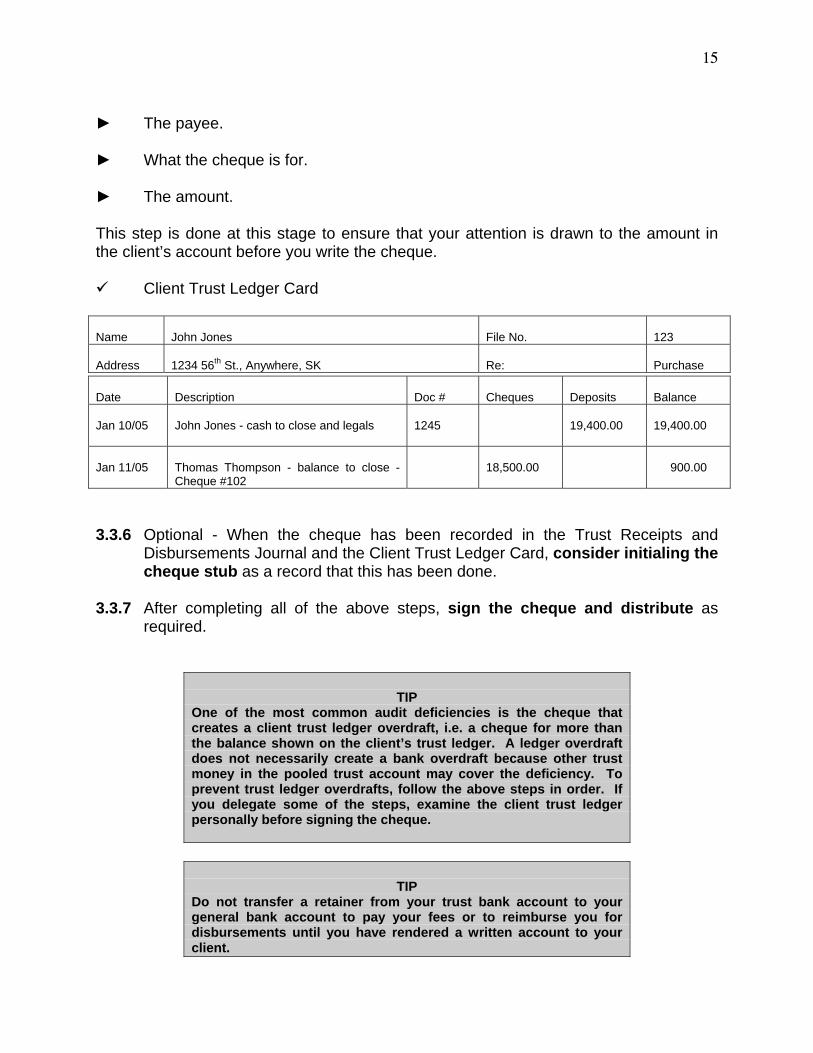

3.3.5 Post the cheque to the particular Client’s Trust Ledger Card. The information on the ledger card should include: ► The date of the cheque.

15

► The payee. ► What the cheque is for. ► The amount. This step is done at this stage to ensure that your attention is drawn to the amount in the client’s account before you write the cheque.

Client Trust Ledger Card Name

John Jones

File No.

123

Address

1234 56th St., Anywhere, SK

Re:

Purchase

Date

Description

Doc #

Cheques

Deposits

Balance

Jan 10/05

John Jones - cash to close and legals

1245

19,400.00

19,400.00

Jan 11/05

Thomas Thompson - balance to close - Cheque #102

18,500.00

900.00

3.3.6 Optional - When the cheque has been recorded in the Trust Receipts and Disbursements Journal and the Client Trust Ledger Card, consider initialing the cheque stub as a record that this has been done. 3.3.7 After completing all of the above steps, sign the cheque and distribute as required.

TIP

One of the most common audit deficiencies is the cheque that creates a client trust ledger overdraft, i.e. a cheque for more than the balance shown on the client’s trust ledger. A ledger overdraft does not necessarily create a bank overdraft because other trust money in the pooled trust account may cover the deficiency. To prevent trust ledger overdrafts, follow the above steps in order. If you delegate some of the steps, examine the client trust ledger personally before signing the cheque.

TIP Do not transfer a retainer from your trust bank account to your general bank account to pay your fees or to reimburse you for disbursements until you have rendered a written account to your client.

16

TIP Withdrawals from trust must be by cheque. Wire transfers require a cheque and a written request signed by a lawyer.

TIP Money which belongs to you must be withdrawn promptly from your trust account (within 1 week from date of invoice).

TIP The Rules prohibit trust cheques made payable to “Cash” or “Bearer” and post-dated cheques. The cheque must clearly indicate that it is a cheque drawn on a trust account be dated and completed as to the payee and the amount and be signed by the member from whose trust account the withdrawal is made or another authorized member. Record the file number on the face of the cheque.

Tip The basic rule is that any withdrawal or transfer of trust money requires the signature of a lawyer authorized by the firm to sign. From time to time, solo practitioners need to have trust cheques issued when they are not available to sign themselves. The simplest way to deal with this problem is to make arrangements for another member of the Law Society to have temporary signing authority on the trust account so the cheque can be signed in the lawyer’s absence. Trust cheques must never be signed only by a non-member.

3.4 Separate Interest-Bearing Trust Accounts The Rules permit you to deposit trust money for a specific client from the pooled trust account into a separate interest-bearing trust account where the interest will accrue to the benefit of that specific client. ► Trust money must not be deposited directly in a separate interest-bearing trust account. All trust money you receive must first be deposited to the pooled trust account, then paid, with client authority, from the pooled trust account to the separate interest-bearing trust account. ► Trust money belonging to a specific client may be deposited (paid from the pooled trust account) in a separate interest-bearing account with an approved

17

depository insured by the Canadian Deposit Insurance Corporation (“CDIC”), the Credit Union Insurance Fund or other investment if approved in writing by the client. A copy of this written approval must be retained by the member. ► A separate interest-bearing account may contain only trust money belonging to one client. ► Trust money may be transferred between the pooled trust and a separate interest-bearing account in the same branch by a letter or other document showing the amount and date of the transfer, the accounts involved and sufficient information to identify the client (e.g. a file number or description that does not disclose confidential client information). The letter or document must be signed the same as a cheque (i.e. by a member). A copy of this signed letter must be retained by the member. ► Interest earned on separate interest-bearing accounts is the property of the beneficial owner of the money and must be accounted for. It must be posted when you are informed it has been paid. If the account is closed in the middle of the month. the accrued interest will be posted at that time. On daily interest savings accounts and some term deposits, the interest is normally posted by the financial institution on a monthly basis; part of your monthly reconciliation procedure will be to determine the amount of the interest from the financial institution and post it to the client’s separate interest bearing trust account. On other term deposits, the interest is paid at the completion of the term and the interest should be posted when the investment comes due. Interest on a term deposit that is rolled into a new term deposit should be posted when it is rolled over, not when the deposit is eventually cashed in.

TIP

Placing a client’s money in a separate interest-bearing trust account may generate a considerable amount of bookkeeping, so make sure that the interest to be generated justifies the time and hassle involved.

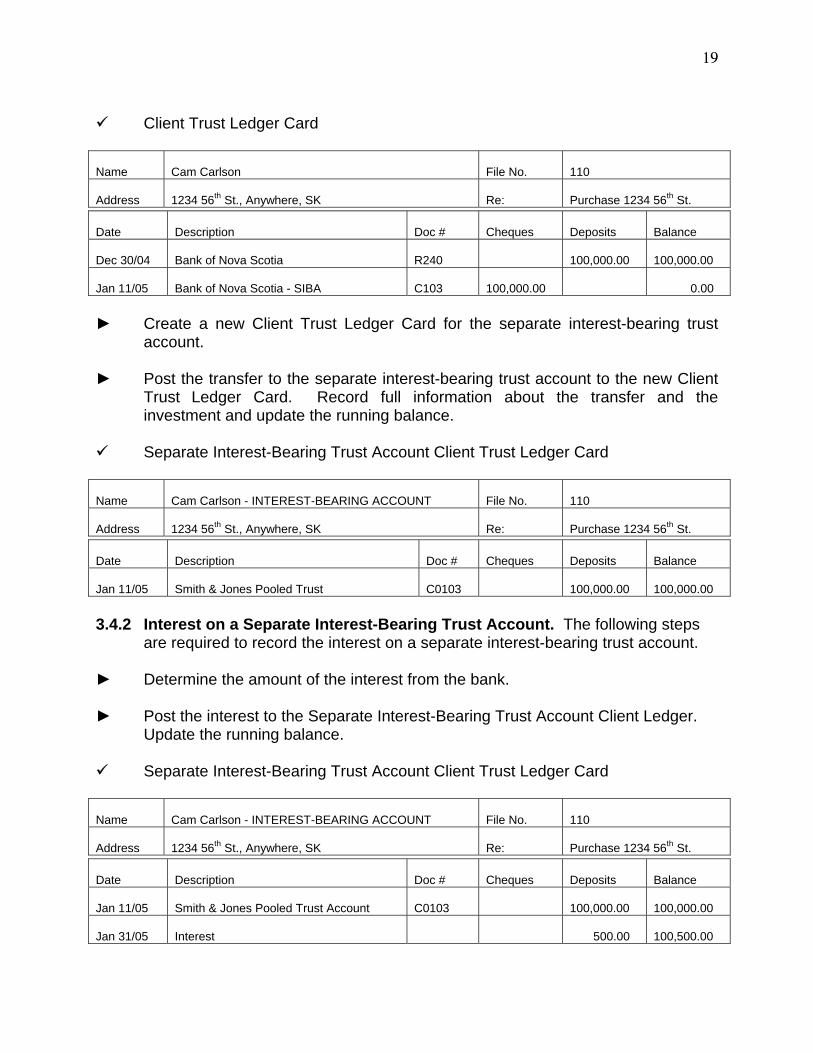

► A new client trust ledger card should be created for money transferred to a separate interest-bearing trust account. Removing the interest-bearing funds from the main pooled trust ledger card will prevent you from accidentally creating a negative balance for the client in the pooled trust account or writing an NSF cheque in the mistaken belief that there are sufficient funds in your pooled trust account to cover it. The new ledger card should be readily distinguishable as a ledger card for a separate interest-bearing account. The particulars of the separate interest-bearing account should be shown on the card.

18

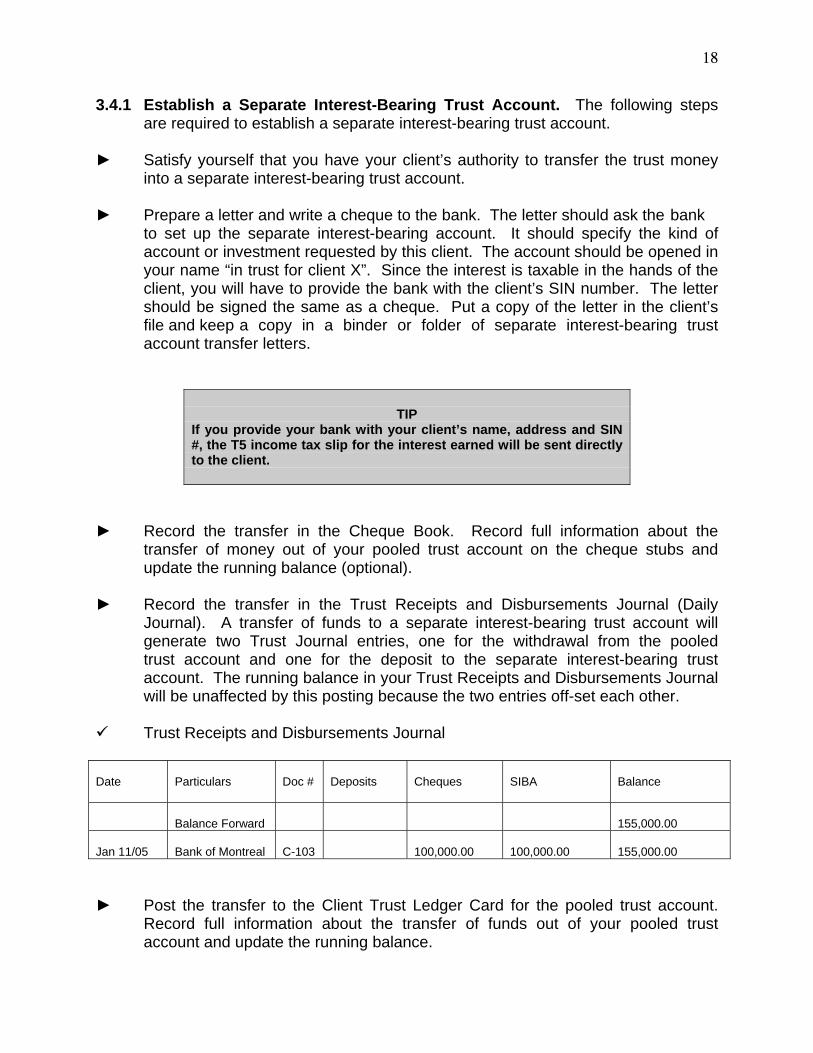

3.4.1 Establish a Separate Interest-Bearing Trust Account. The following steps are required to establish a separate interest-bearing trust account. ► Satisfy yourself that you have your client’s authority to transfer the trust money into a separate interest-bearing trust account. ► Prepare a letter and write a cheque to the bank. The letter should ask the bank to set up the separate interest-bearing account. It should specify the kind of account or investment requested by this client. The account should be opened in your name “in trust for client X”. Since the interest is taxable in the hands of the client, you will have to provide the bank with the client’s SIN number. The letter should be signed the same as a cheque. Put a copy of the letter in the client’s file and keep a copy in a binder or folder of separate interest-bearing trust account transfer letters.

TIP

If you provide your bank with your client’s name, address and SIN #, the T5 income tax slip for the interest earned will be sent directly to the client.

► Record the transfer in the Cheque Book. Record full information about the transfer of money out of your pooled trust account on the cheque stubs and update the running balance (optional). ► Record the transfer in the Trust Receipts and Disbursements Journal (Daily Journal). A transfer of funds to a separate interest-bearing trust account will generate two Trust Journal entries, one for the withdrawal from the pooled trust account and one for the deposit to the separate interest-bearing trust account. The running balance in your Trust Receipts and Disbursements Journal will be unaffected by this posting because the two entries off-set each other.

Trust Receipts and Disbursements Journal Date

Particulars

Doc #

Deposits

Cheques

SIBA

Balance

Balance Forward

155,000.00

Jan 11/05

Bank of Montreal

C-103

100,000.00

100,000.00

155,000.00

► Post the transfer to the Client Trust Ledger Card for the pooled trust account. Record full information about the transfer of funds out of your pooled trust account and update the running balance.

19

Client Trust Ledger Card

Name

Cam Carlson

File No.

110

Address

1234 56th St., Anywhere, SK

Re:

Purchase 1234 56th St.

Date

Description

Doc #

Cheques

Deposits

Balance

Dec 30/04

Bank of Nova Scotia

R240

100,000.00

100,000.00

Jan 11/05

Bank of Nova Scotia - SIBA

C103

100,000.00

0.00

► Create a new Client Trust Ledger Card for the separate interest-bearing trust account. ► Post the transfer to the separate interest-bearing trust account to the new Client Trust Ledger Card. Record full information about the transfer and the investment and update the running balance.

Separate Interest-Bearing Trust Account Client Trust Ledger Card Name

Cam Carlson - INTEREST-BEARING ACCOUNT

File No.

110

Address

1234 56th St., Anywhere, SK

Re:

Purchase 1234 56th St.

Date

Description

Doc #

Cheques

Deposits

Balance

Jan 11/05

Smith & Jones Pooled Trust

C0103

100,000.00

100,000.00

3.4.2 Interest on a Separate Interest-Bearing Trust Account. The following steps are required to record the interest on a separate interest-bearing trust account. ► Determine the amount of the interest from the bank. ► Post the interest to the Separate Interest-Bearing Trust Account Client Ledger. Update the running balance.

Separate Interest-Bearing Trust Account Client Trust Ledger Card Name

Cam Carlson - INTEREST-BEARING ACCOUNT

File No.

110

Address

1234 56th St., Anywhere, SK

Re:

Purchase 1234 56th St.

Date

Description

Doc #

Cheques

Deposits

Balance

Jan 11/05

Smith & Jones Pooled Trust Account

C0103

100,000.00

100,000.00

Jan 31/05

Interest

500.00

100,500.00

20

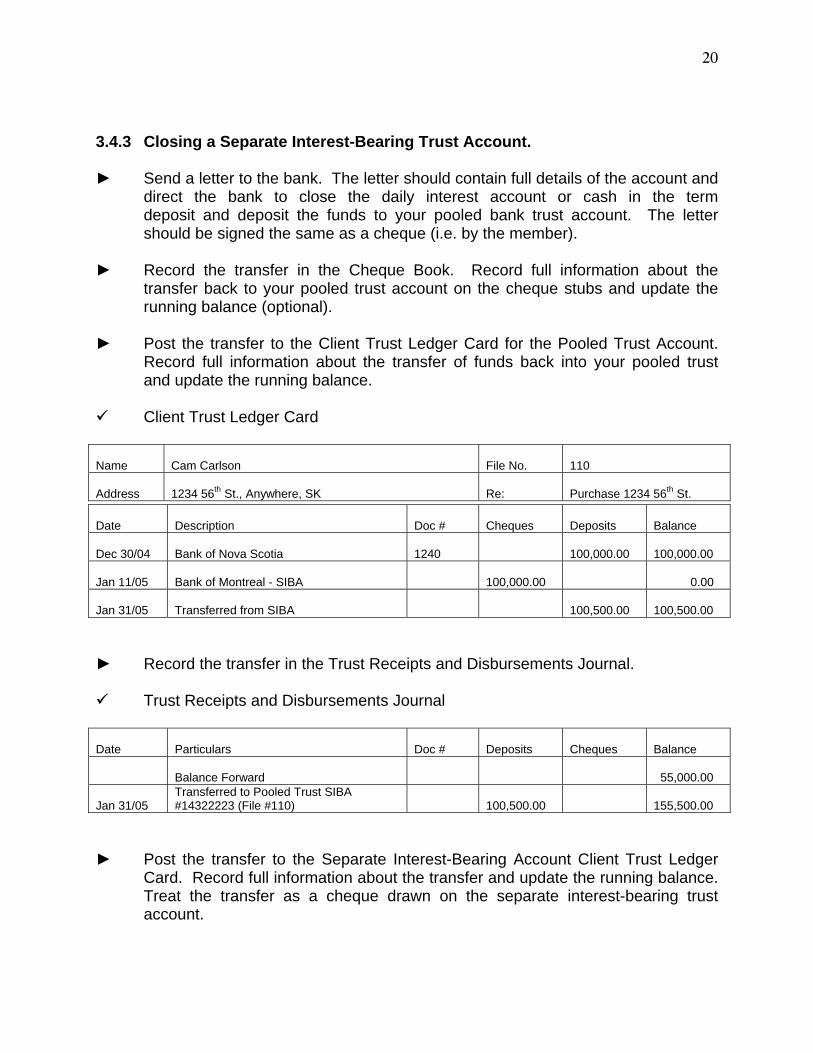

3.4.3 Closing a Separate Interest-Bearing Trust Account. ► Send a letter to the bank. The letter should contain full details of the account and direct the bank to close the daily interest account or cash in the term deposit and deposit the funds to your pooled bank trust account. The letter should be signed the same as a cheque (i.e. by the member). ► Record the transfer in the Cheque Book. Record full information about the transfer back to your pooled trust account on the cheque stubs and update the running balance (optional). ► Post the transfer to the Client Trust Ledger Card for the Pooled Trust Account. Record full information about the transfer of funds back into your pooled trust and update the running balance.

Client Trust Ledger Card Name

Cam Carlson

File No.

110

Address

1234 56th St., Anywhere, SK

Re:

Purchase 1234 56th St.

Date

Description

Doc #

Cheques

Deposits

Balance

Dec 30/04

Bank of Nova Scotia

1240

100,000.00

100,000.00

Jan 11/05

Bank of Montreal - SIBA

100,000.00

0.00

Jan 31/05

Transferred from SIBA

100,500.00

100,500.00

► Record the transfer in the Trust Receipts and Disbursements Journal.

Trust Receipts and Disbursements Journal Date

Particulars

Doc #

Deposits

Cheques

Balance

Balance Forward

55,000.00

Jan 31/05

Transferred to Pooled Trust SIBA #14322223 (File #110)

100,500.00

155,500.00

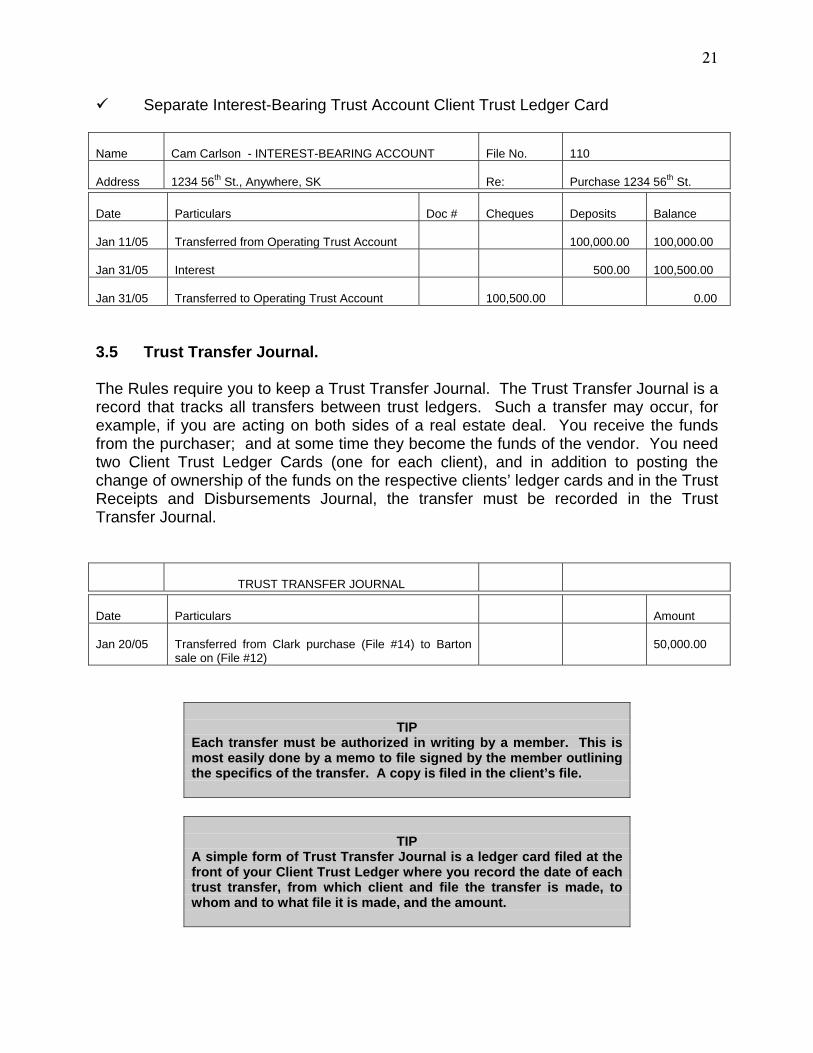

► Post the transfer to the Separate Interest-Bearing Account Client Trust Ledger Card. Record full information about the transfer and update the running balance. Treat the transfer as a cheque drawn on the separate interest-bearing trust account.

21

Separate Interest-Bearing Trust Account Client Trust Ledger Card Name

Cam Carlson - INTEREST-BEARING ACCOUNT

File No.

110

Address

1234 56th St., Anywhere, SK

Re:

Purchase 1234 56th St.

Date

Particulars

Doc #

Cheques

Deposits

Balance

Jan 11/05

Transferred from Operating Trust Account

100,000.00

100,000.00

Jan 31/05

Interest

500.00

100,500.00

Jan 31/05

Transferred to Operating Trust Account

100,500.00

0.00

3.5 Trust Transfer Journal. The Rules require you to keep a Trust Transfer Journal. The Trust Transfer Journal is a record that tracks all transfers between trust ledgers. Such a transfer may occur, for example, if you are acting on both sides of a real estate deal. You receive the funds from the purchaser; and at some time they become the funds of the vendor. You need two Client Trust Ledger Cards (one for each client), and in addition to posting the change of ownership of the funds on the respective clients’ ledger cards and in the Trust Receipts and Disbursements Journal, the transfer must be recorded in the Trust Transfer Journal.

TRUST TRANSFER JOURNAL

Date

Particulars

Amount

Jan 20/05

Transferred from Clark purchase (File #14) to Barton sale on (File #12)

50,000.00

TIP

Each transfer must be authorized in writing by a member. This is most easily done by a memo to file signed by the member outlining the specifics of the transfer. A copy is filed in the client’s file.

TIP A simple form of Trust Transfer Journal is a ledger card filed at the front of your Client Trust Ledger where you record the date of each trust transfer, from which client and file the transfer is made, to whom and to what file it is made, and the amount.

22

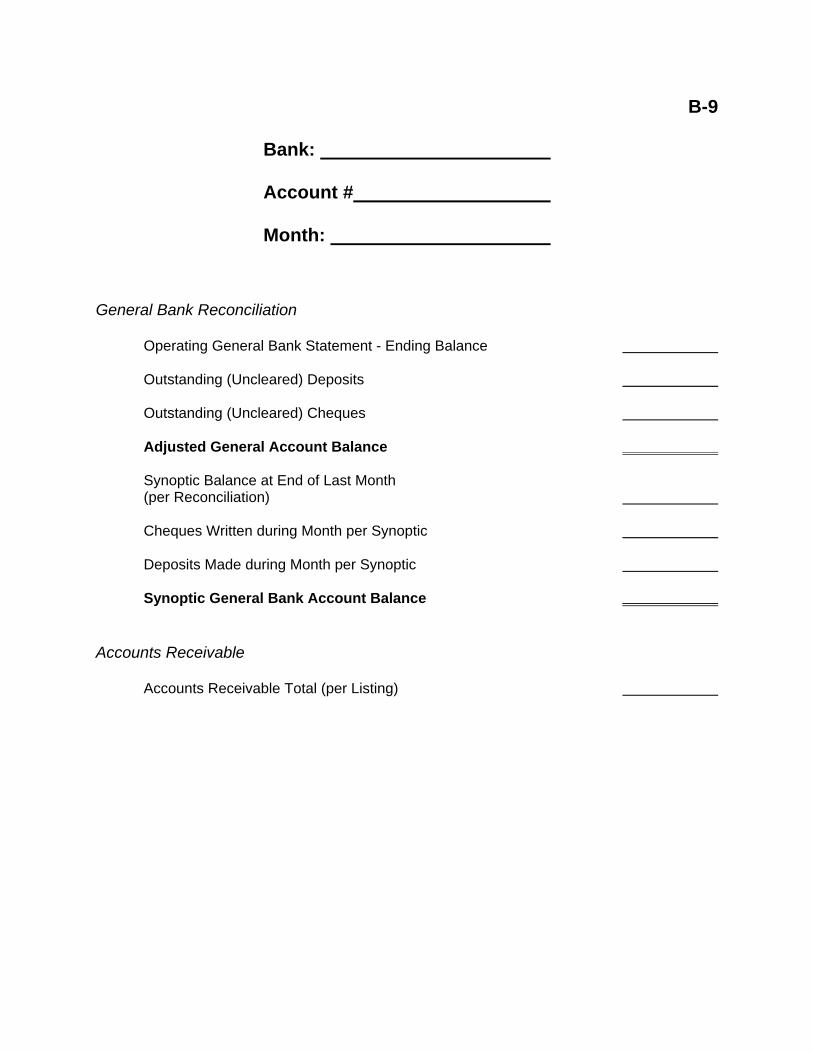

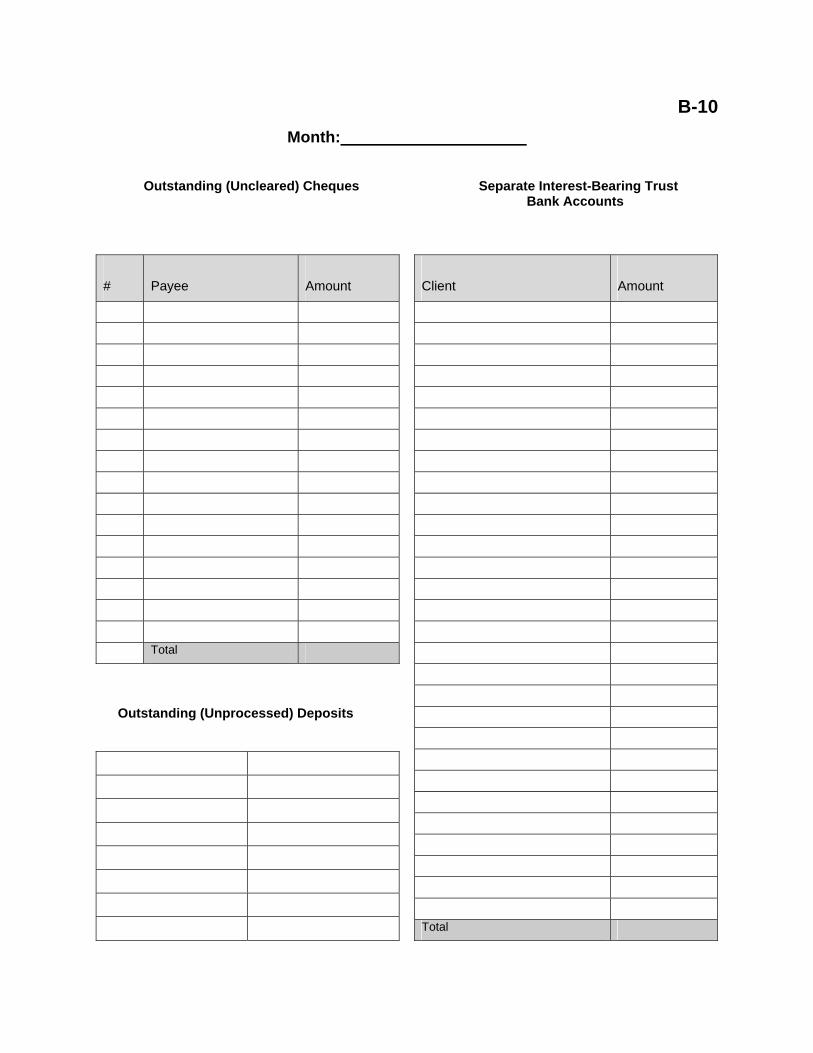

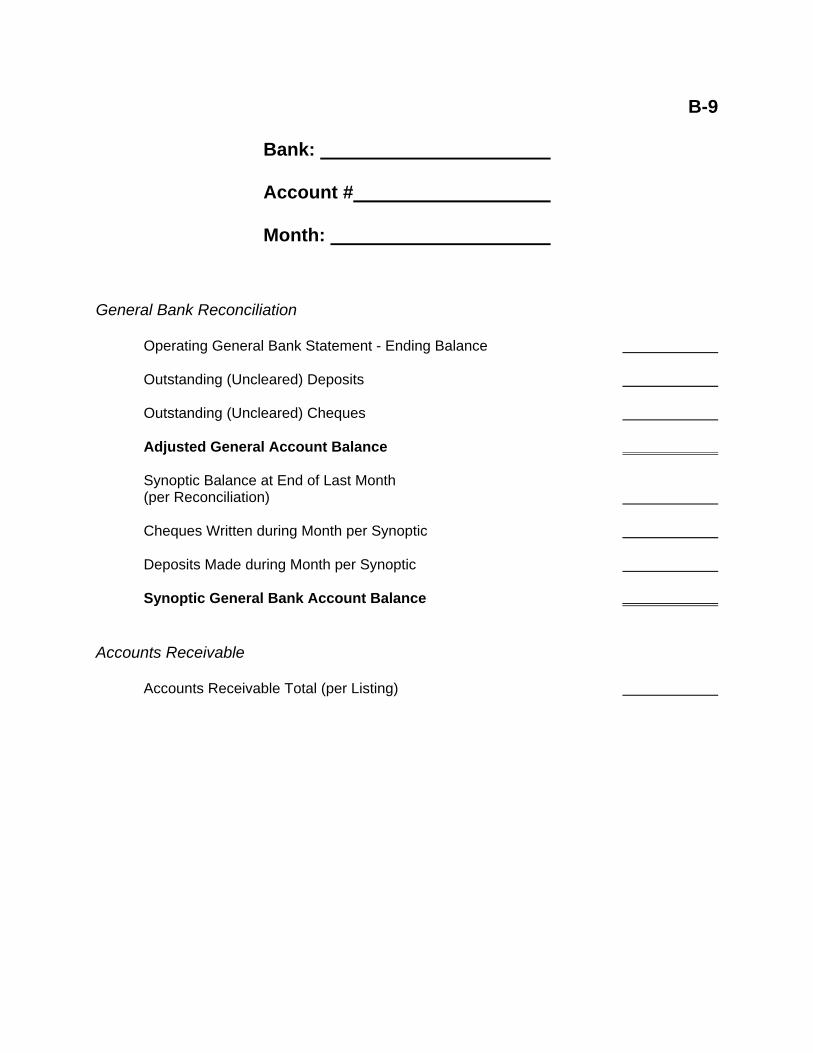

3.6 Trust Reconciliations Your trust accounts must be reconciled monthly. The trust reconciliation is a simple arithmetical operation that involves showing that three sources of information are consistent as at a certain date (each month end): ► Bank Statement(s) - The total of the balances on the bank statement for your pooled trust bank account and on the up-dated statements for any separate interest-bearing accounts, adjusted to take into account any unprocessed cheques and/or deposits. ► Trust Receipts and Disbursements Journal Balance - The running balance shown in your Trust Receipts and Disbursements Journal. ► Client Trust Listing Total - The total of the client trust ledger balances shown on your Trust listing, which is a listing of the balances shown on all your client trust ledger cards, including separate interest-bearing trust account client ledger cards. The Rules require you to reconcile your trust account within 20 days of the end of each month. The reconciliation should be dated and signed by the member. A Trust Reconciliation Checklist and Form may be found in Schedule “A”.

TIP

You have to do a trust reconciliation even if you have no transactions in the month and even if you have no funds in trust.

3.7 Appendix A provides a hypothetical example of a: ► Trust journal with column and transaction description. ► Trust reconciliation checklist. ► Trust bank reconciliation and supporting listings. ► Client trust listing. Blank forms have also been included for your use if you wish.

23

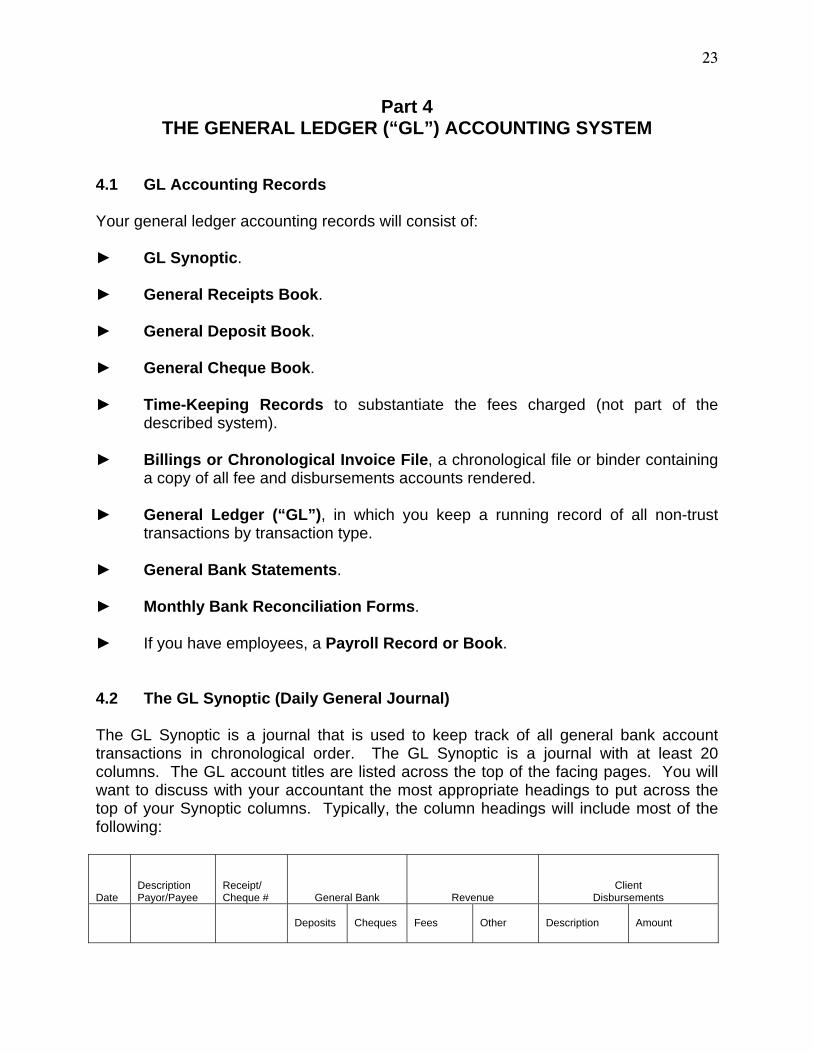

Part 4 THE GENERAL LEDGER (“GL”) ACCOUNTING SYSTEM

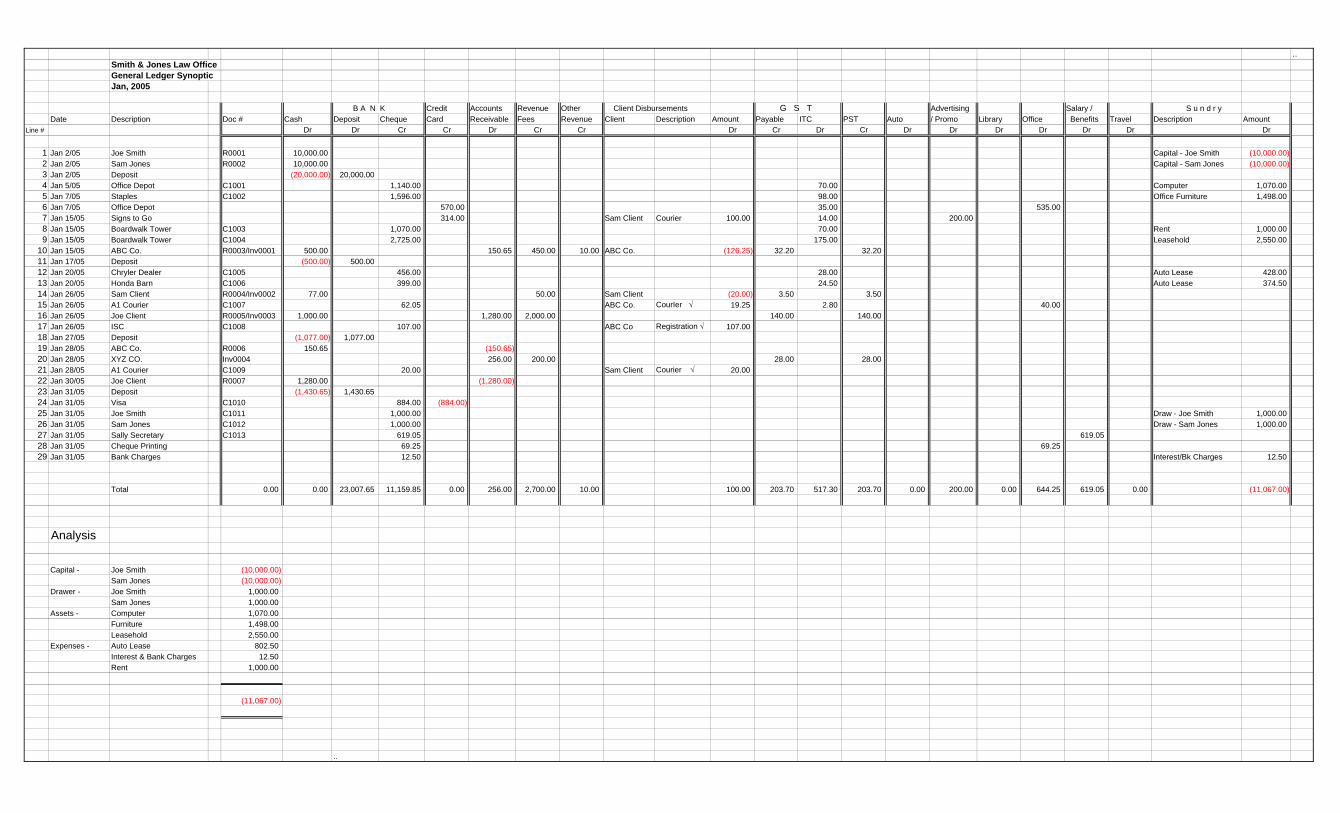

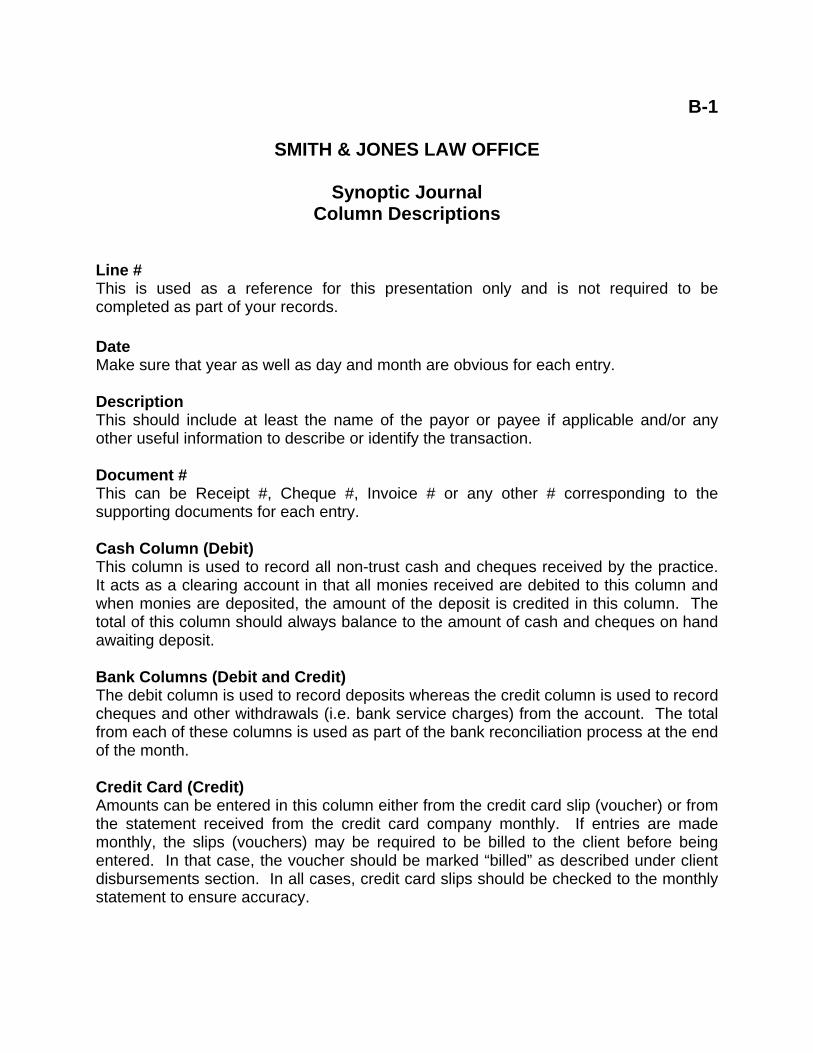

4.1 GL Accounting Records Your general ledger accounting records will consist of: ► GL Synoptic. ► General Receipts Book. ► General Deposit Book. ► General Cheque Book. ► Time-Keeping Records to substantiate the fees charged (not part of the described system). ► Billings or Chronological Invoice File, a chronological file or binder containing a copy of all fee and disbursements accounts rendered. ► General Ledger (“GL”), in which you keep a running record of all non-trust transactions by transaction type. ► General Bank Statements. ► Monthly Bank Reconciliation Forms. ► If you have employees, a Payroll Record or Book. 4.2 The GL Synoptic (Daily General Journal) The GL Synoptic is a journal that is used to keep track of all general bank account transactions in chronological order. The GL Synoptic is a journal with at least 20 columns. The GL account titles are listed across the top of the facing pages. You will want to discuss with your accountant the most appropriate headings to put across the top of your Synoptic columns. Typically, the column headings will include most of the following: Date

Description Payor/Payee

Receipt/ Cheque #

General Bank

Revenue

Client Disbursements

Deposits

Cheques

Fees

Other

Description

Amount

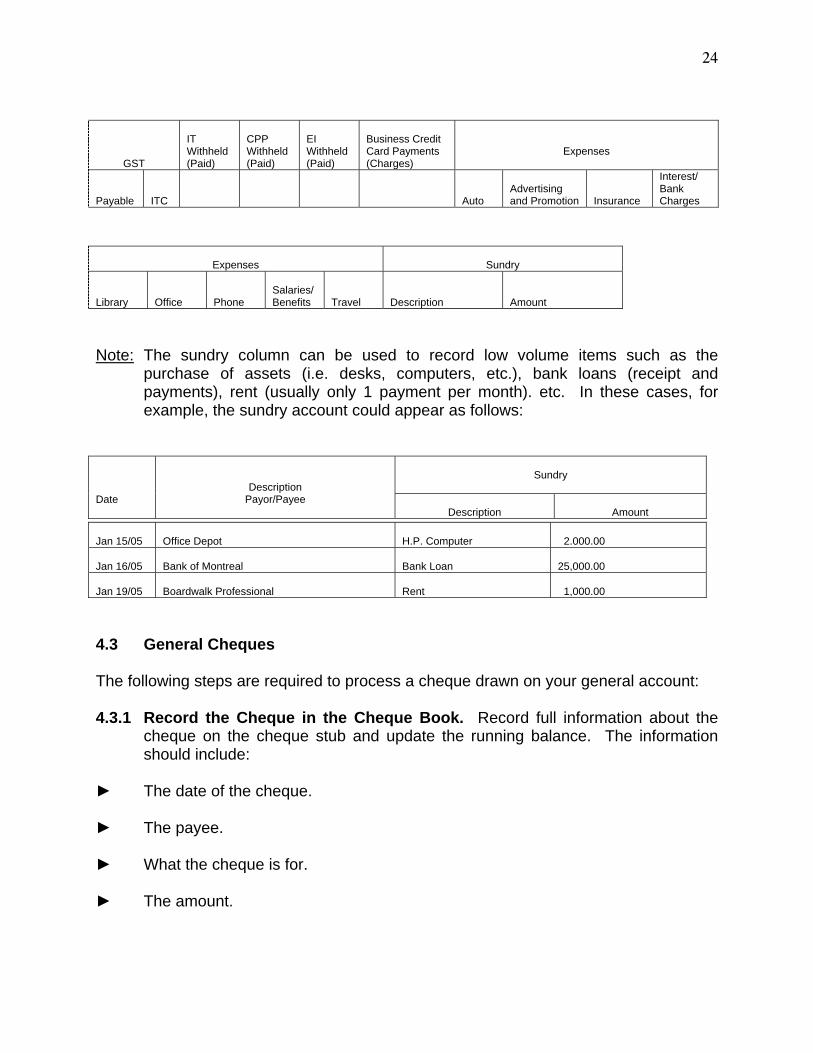

24

GST

IT Withheld (Paid)

CPP Withheld (Paid)

EI Withheld (Paid)

Business Credit Card Payments (Charges)

Expenses

Payable

ITC

Auto

Advertising and Promotion

Insurance

Interest/ Bank Charges

Expenses

Sundry Library

Office

Phone

Salaries/ Benefits

Travel

Description

Amount

Note: The sundry column can be used to record low volume items such as the purchase of assets (i.e. desks, computers, etc.), bank loans (receipt and payments), rent (usually only 1 payment per month). etc. In these cases, for example, the sundry account could appear as follows:

Sundry

Date

Description Payor/Payee

Description

Amount

Jan 15/05

Office Depot

H.P. Computer

2.000.00

Jan 16/05

Bank of Montreal

Bank Loan

25,000.00

Jan 19/05

Boardwalk Professional

Rent

1,000.00

4.3 General Cheques The following steps are required to process a cheque drawn on your general account: 4.3.1 Record the Cheque in the Cheque Book. Record full information about the cheque on the cheque stub and update the running balance. The information should include: ► The date of the cheque. ► The payee. ► What the cheque is for. ► The amount.

25

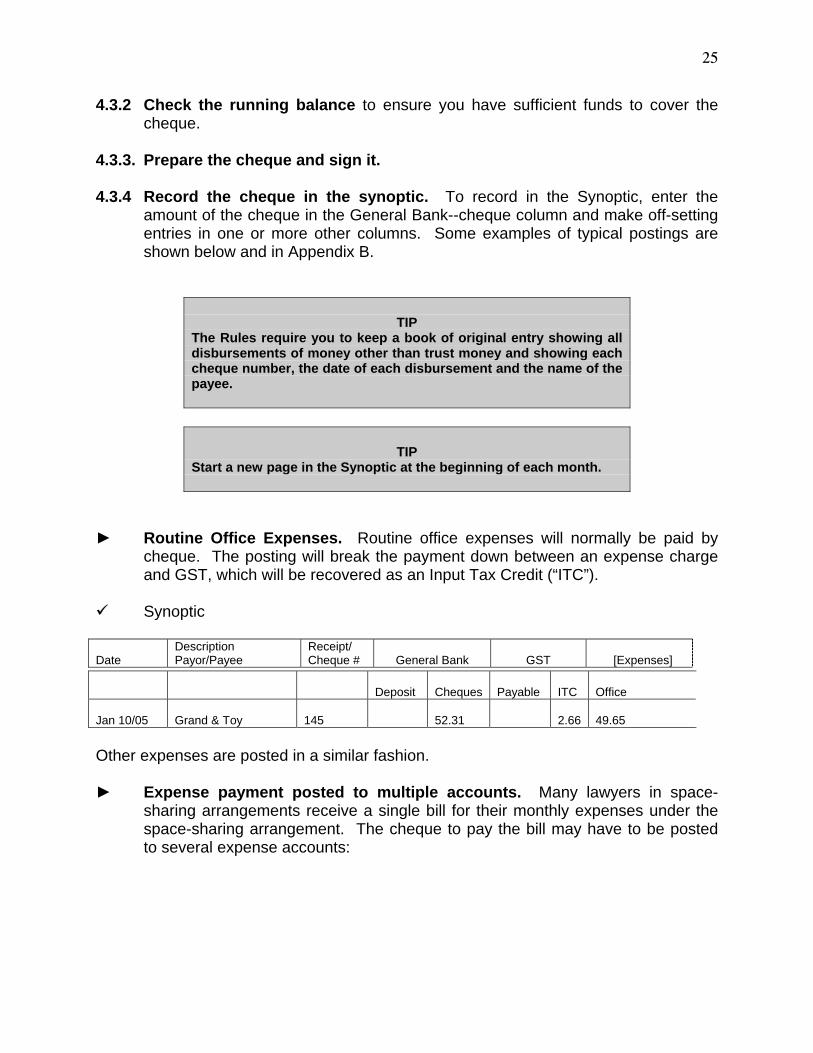

4.3.2 Check the running balance to ensure you have sufficient funds to cover the cheque. 4.3.3. Prepare the cheque and sign it. 4.3.4 Record the cheque in the synoptic. To record in the Synoptic, enter the amount of the cheque in the General Bank--cheque column and make off-setting entries in one or more other columns. Some examples of typical postings are shown below and in Appendix B.

TIP

The Rules require you to keep a book of original entry showing all disbursements of money other than trust money and showing each cheque number, the date of each disbursement and the name of the payee.

TIP Start a new page in the Synoptic at the beginning of each month.

► Routine Office Expenses. Routine office expenses will normally be paid by cheque. The posting will break the payment down between an expense charge and GST, which will be recovered as an Input Tax Credit (“ITC”).

Synoptic Date

Description Payor/Payee

Receipt/ Cheque #

General Bank

GST

[Expenses]

Deposit

Cheques

Payable

ITC

Office

Jan 10/05

Grand & Toy

145

52.31

2.66

49.65

Other expenses are posted in a similar fashion. ► Expense payment posted to multiple accounts. Many lawyers in space- sharing arrangements receive a single bill for their monthly expenses under the space-sharing arrangement. The cheque to pay the bill may have to be posted to several expense accounts:

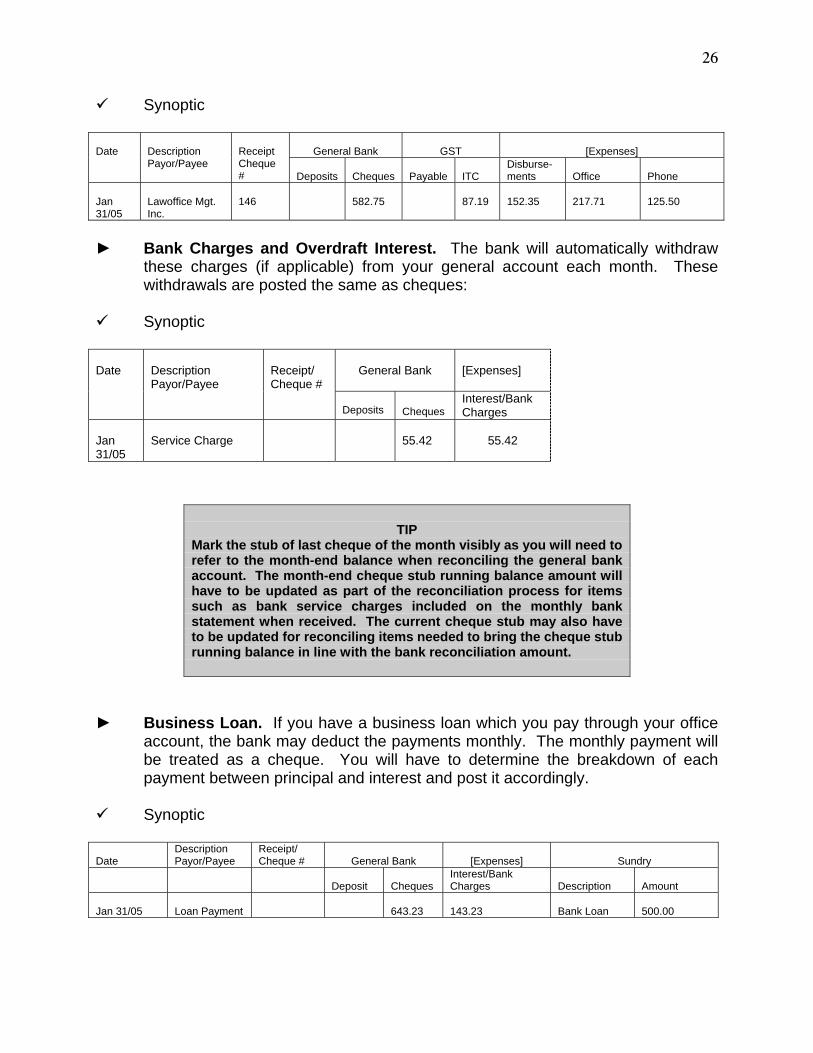

26

Synoptic

General Bank

GST

[Expenses]

Date

Description Payor/Payee

Receipt Cheque #

Deposits

Cheques

Payable

ITC

Disburse- ments

Office

Phone

Jan 31/05

Lawoffice Mgt. Inc.

146

582.75

87.19

152.35

217.71

125.50

► Bank Charges and Overdraft Interest. The bank will automatically withdraw these charges (if applicable) from your general account each month. These withdrawals are posted the same as cheques:

Synoptic

General Bank

[Expenses]

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits

Cheques

Interest/Bank Charges

Jan 31/05

Service Charge

55.42

55.42

TIP

Mark the stub of last cheque of the month visibly as you will need to refer to the month-end balance when reconciling the general bank account. The month-end cheque stub running balance amount will have to be updated as part of the reconciliation process for items such as bank service charges included on the monthly bank statement when received. The current cheque stub may also have to be updated for reconciling items needed to bring the cheque stub running balance in line with the bank reconciliation amount.

► Business Loan. If you have a business loan which you pay through your office account, the bank may deduct the payments monthly. The monthly payment will be treated as a cheque. You will have to determine the breakdown of each payment between principal and interest and post it accordingly.

Synoptic Date

Description Payor/Payee

Receipt/ Cheque #

General Bank

[Expenses]

Sundry

Deposit

Cheques

Interest/Bank Charges

Description

Amount

Jan 31/05

Loan Payment

643.23

143.23

Bank Loan

500.00

27

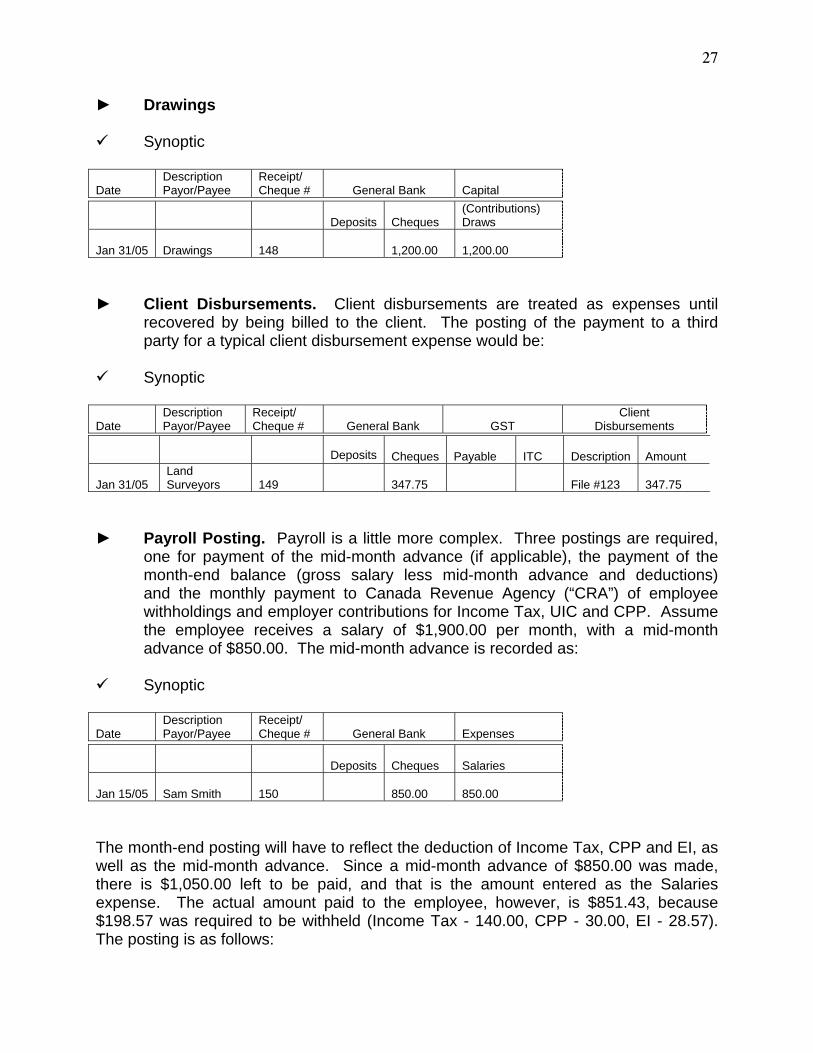

► Drawings

Synoptic Date

Description Payor/Payee

Receipt/ Cheque #

General Bank

Capital

Deposits

Cheques

(Contributions) Draws

Jan 31/05

Drawings

148

1,200.00

1,200.00

► Client Disbursements. Client disbursements are treated as expenses until recovered by being billed to the client. The posting of the payment to a third party for a typical client disbursement expense would be:

Synoptic Date

Description Payor/Payee

Receipt/ Cheque #

General Bank

GST

Client Disbursements

Deposits

Cheques

Payable

ITC

Description

Amount

Jan 31/05

Land Surveyors

149

347.75

File #123

347.75

► Payroll Posting. Payroll is a little more complex. Three postings are required, one for payment of the mid-month advance (if applicable), the payment of the month-end balance (gross salary less mid-month advance and deductions) and the monthly payment to Canada Revenue Agency (“CRA”) of employee withholdings and employer contributions for Income Tax, UIC and CPP. Assume the employee receives a salary of $1,900.00 per month, with a mid-month advance of $850.00. The mid-month advance is recorded as:

Synoptic Date

Description Payor/Payee

Receipt/ Cheque #

General Bank

Expenses

Deposits

Cheques

Salaries

Jan 15/05

Sam Smith

150

850.00

850.00

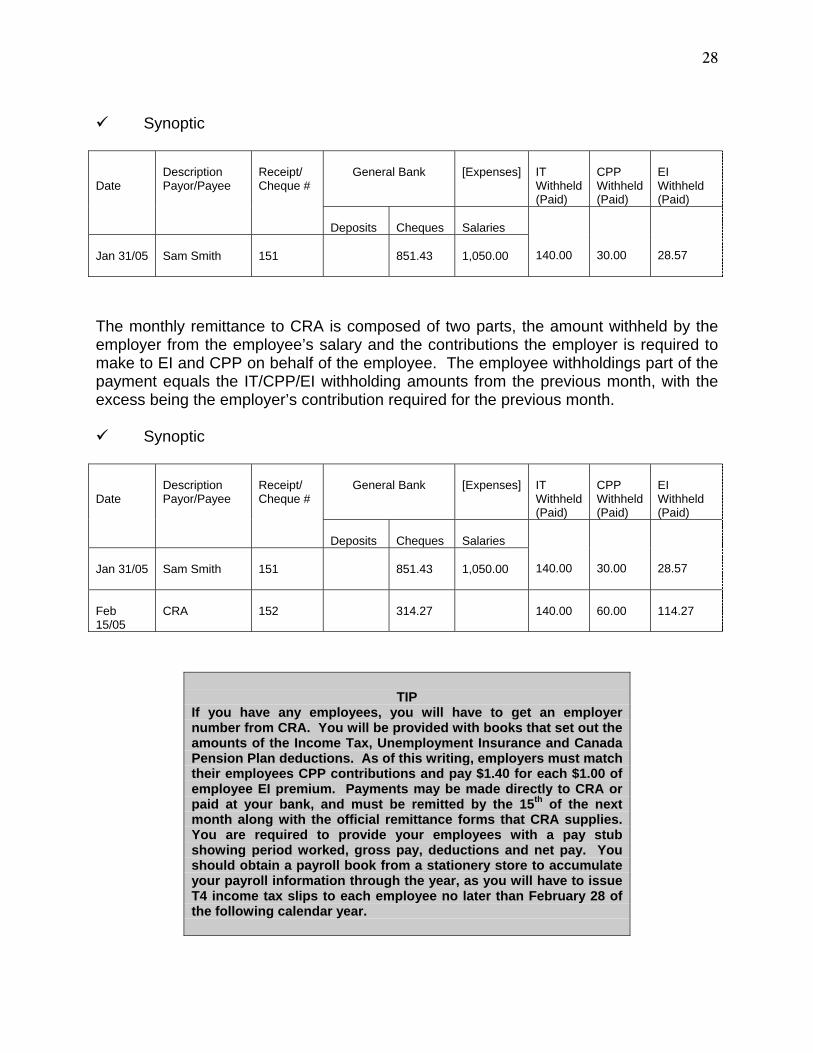

The month-end posting will have to reflect the deduction of Income Tax, CPP and EI, as well as the mid-month advance. Since a mid-month advance of $850.00 was made, there is $1,050.00 left to be paid, and that is the amount entered as the Salaries expense. The actual amount paid to the employee, however, is $851.43, because $198.57 was required to be withheld (Income Tax - 140.00, CPP - 30.00, EI - 28.57). The posting is as follows:

28

Synoptic

General Bank [Expenses]

IT Withheld (Paid)

CPP Withheld (Paid)

EI Withheld (Paid)

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits

Cheques

Salaries

Jan 31/05

Sam Smith

151

851.43

1,050.00

140.00

30.00

28.57

The monthly remittance to CRA is composed of two parts, the amount withheld by the employer from the employee’s salary and the contributions the employer is required to make to EI and CPP on behalf of the employee. The employee withholdings part of the payment equals the IT/CPP/EI withholding amounts from the previous month, with the excess being the employer’s contribution required for the previous month.

Synoptic

General Bank

[Expenses]

IT Withheld (Paid)

CPP Withheld (Paid)

EI Withheld (Paid)

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits

Cheques

Salaries

Jan 31/05

Sam Smith

151

851.43

1,050.00

140.00

30.00

28.57

Feb 15/05

CRA

152

314.27

140.00

60.00

114.27

TIP

If you have any employees, you will have to get an employer number from CRA. You will be provided with books that set out the amounts of the Income Tax, Unemployment Insurance and Canada Pension Plan deductions. As of this writing, employers must match their employees CPP contributions and pay $1.40 for each $1.00 of employee EI premium. Payments may be made directly to CRA or paid at your bank, and must be remitted by the 15th of the next month along with the official remittance forms that CRA supplies. You are required to provide your employees with a pay stub showing period worked, gross pay, deductions and net pay. You should obtain a payroll book from a stationery store to accumulate your payroll information through the year, as you will have to issue T4 income tax slips to each employee no later than February 28 of the following calendar year.

29

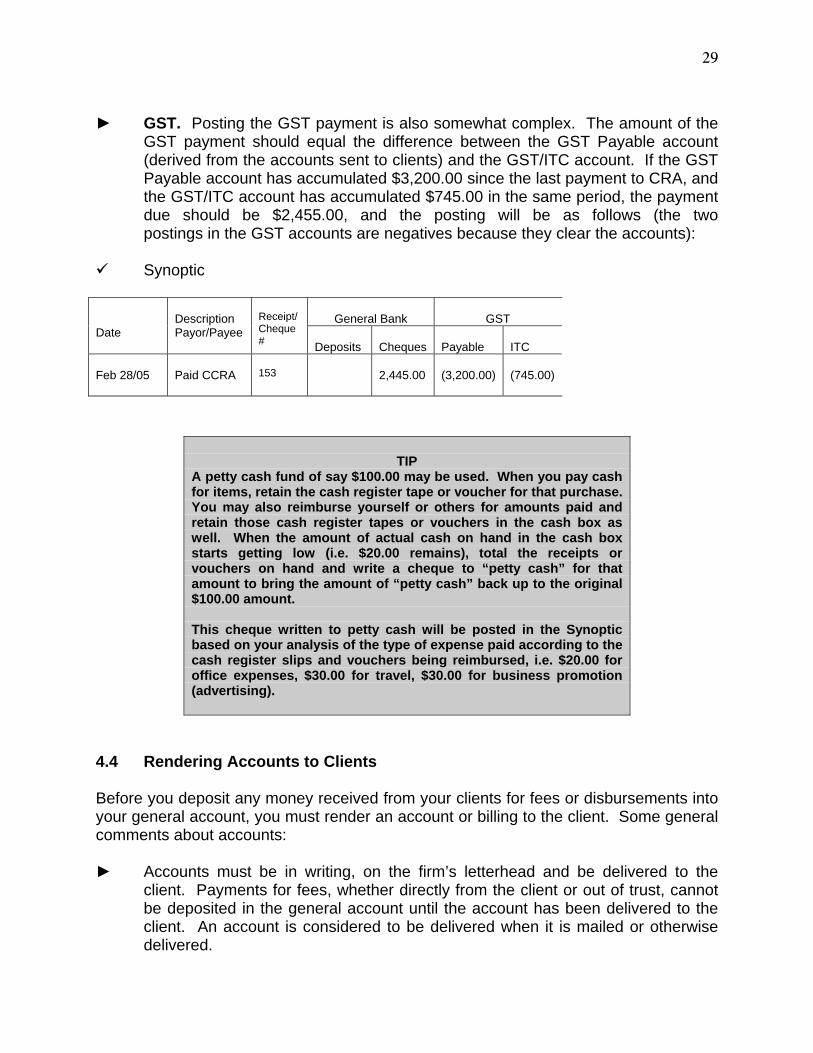

► GST. Posting the GST payment is also somewhat complex. The amount of the GST payment should equal the difference between the GST Payable account (derived from the accounts sent to clients) and the GST/ITC account. If the GST Payable account has accumulated $3,200.00 since the last payment to CRA, and the GST/ITC account has accumulated $745.00 in the same period, the payment due should be $2,455.00, and the posting will be as follows (the two postings in the GST accounts are negatives because they clear the accounts):

Synoptic

General Bank

GST

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits

Cheques

Payable

ITC

Feb 28/05

Paid CCRA

153

2,445.00

(3,200.00)

(745.00)

TIP

A petty cash fund of say $100.00 may be used. When you pay cash for items, retain the cash register tape or voucher for that purchase. You may also reimburse yourself or others for amounts paid and retain those cash register tapes or vouchers in the cash box as well. When the amount of actual cash on hand in the cash box starts getting low (i.e. $20.00 remains), total the receipts or vouchers on hand and write a cheque to “petty cash” for that amount to bring the amount of “petty cash” back up to the original $100.00 amount. This cheque written to petty cash will be posted in the Synoptic based on your analysis of the type of expense paid according to the cash register slips and vouchers being reimbursed, i.e. $20.00 for office expenses, $30.00 for travel, $30.00 for business promotion (advertising).

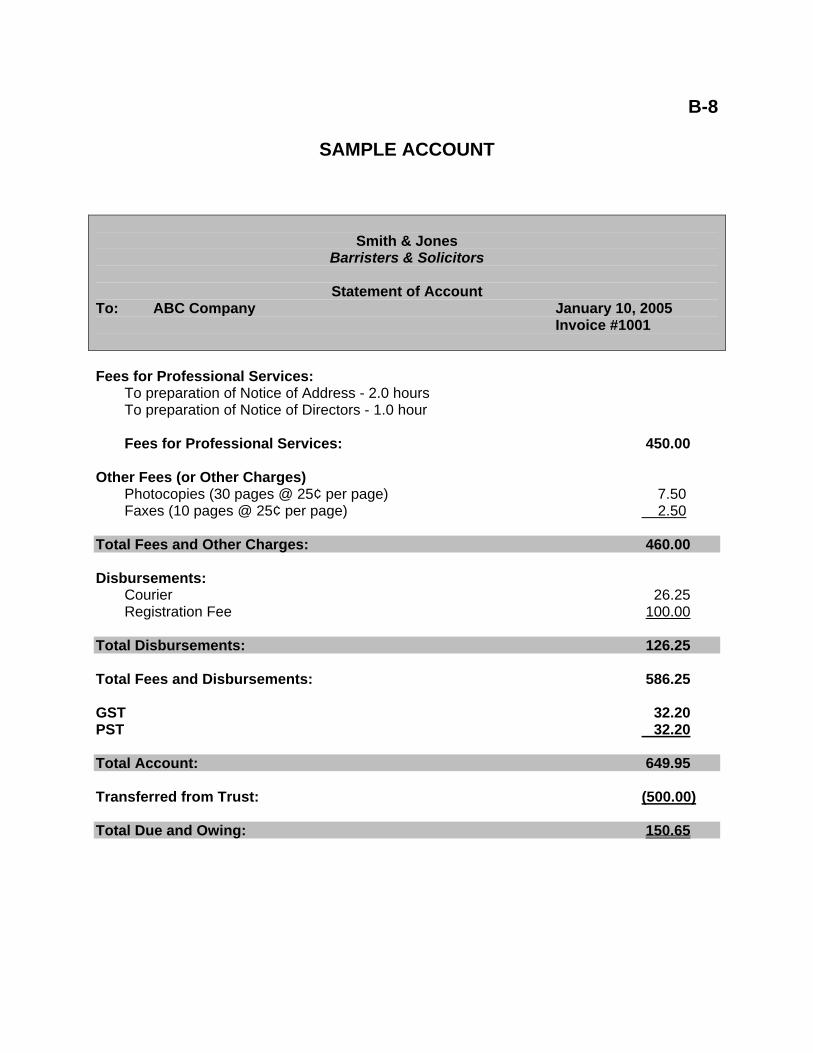

4.4 Rendering Accounts to Clients Before you deposit any money received from your clients for fees or disbursements into your general account, you must render an account or billing to the client. Some general comments about accounts: ► Accounts must be in writing, on the firm’s letterhead and be delivered to the client. Payments for fees, whether directly from the client or out of trust, cannot be deposited in the general account until the account has been delivered to the client. An account is considered to be delivered when it is mailed or otherwise delivered.

30

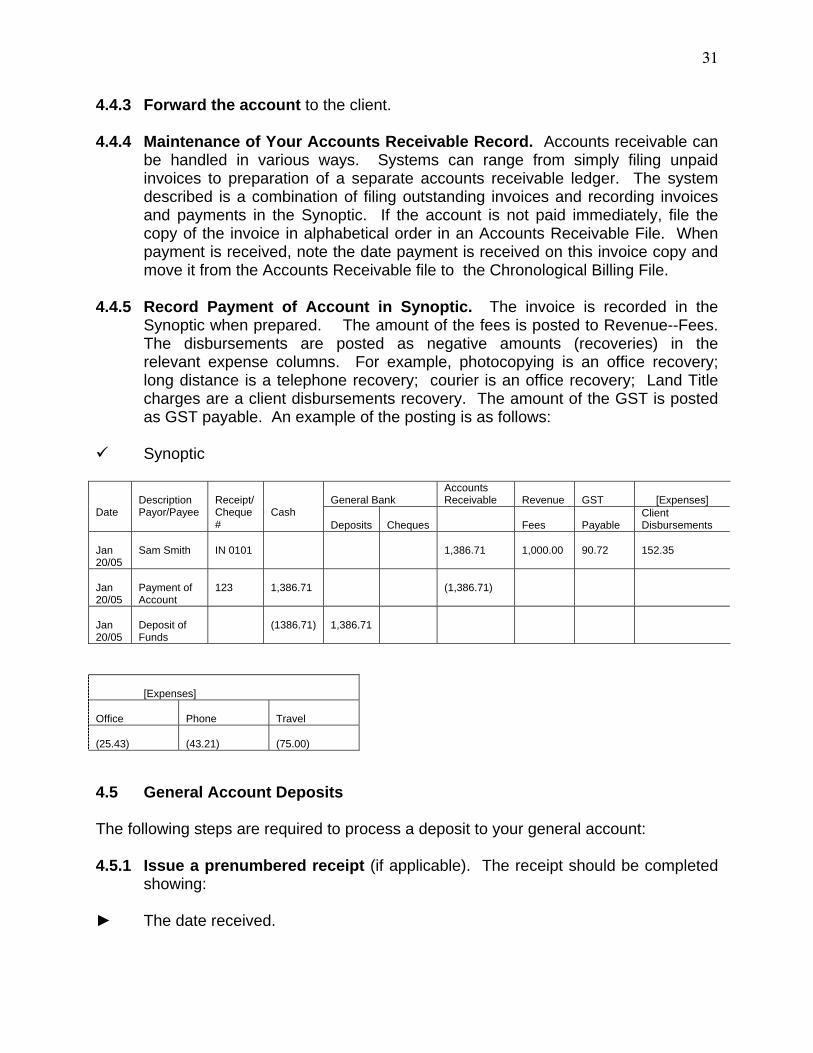

► One category of charges is fees for professional services. The services for which the fees are charged should be particularized to the degree necessary to inform the client fully about the services provided. ► A second category of charges is disbursements, that is, payments to third parties made by the member on the client’s behalf. Disbursements typically include such payments as Land Title charges, long distance charges, courier charges, registration fees and so on. ► Many lawyers charge only fees and disbursements, and absorb the cost of non- legal internal services such as photocopying, file opening, receiving and sending faxes and word processing as part of the overhead costs of the firm included in the professional fees. However, it is proper to add an “Other Charges” category to the fees portion of the account for such non-legal services, provided they are reasonable, are shown as such on the account, and were brought to the client’s attention in advance. ► GST and PST will also be shown on the account as applicable. ► The Rules require you to keep a chronological file of all accounts to clients showing the fees and other charges billed to the client, the date of the bill and the client to whom the account is rendered. The Rules also require you to keep a ledger or some other suitable system that shows your accounts receivable position with respect to each client. The system described below meets both of these requirements through the filing of unpaid and paid invoices. The procedure for rendering an account is a follows: 4.4.1 Check for unbilled disbursements in the disbursements column of the Synoptic and in the unbilled disbursements voucher file. 4.4.2 Prepare the account. Prepare the original for the client and make a file copy and a copy for the Chronological Billing File.

TIP

You need to be able to determine your client accounts receivable position quickly. A simple, practical solution to this problem is to file the chronological copy of each account that is not paid immediately in alphabetical order in an Unpaid Accounts folder or binder. Partial payments are noted on the copy. When the account is paid in full, the copy is then filed in chronological order in the chronological billing file.

31

4.4.3 Forward the account to the client. 4.4.4 Maintenance of Your Accounts Receivable Record. Accounts receivable can be handled in various ways. Systems can range from simply filing unpaid invoices to preparation of a separate accounts receivable ledger. The system described is a combination of filing outstanding invoices and recording invoices and payments in the Synoptic. If the account is not paid immediately, file the copy of the invoice in alphabetical order in an Accounts Receivable File. When payment is received, note the date payment is received on this invoice copy and move it from the Accounts Receivable file to the Chronological Billing File. 4.4.5 Record Payment of Account in Synoptic. The invoice is recorded in the Synoptic when prepared. The amount of the fees is posted to Revenue--Fees. The disbursements are posted as negative amounts (recoveries) in the relevant expense columns. For example, photocopying is an office recovery; long distance is a telephone recovery; courier is an office recovery; Land Title charges are a client disbursements recovery. The amount of the GST is posted as GST payable. An example of the posting is as follows:

Synoptic

General Bank

Accounts Receivable

Revenue

GST

[Expenses]

Date

Description Payor/Payee

Receipt/ Cheque #

Cash

Deposits Cheques

Fees

Payable

Client Disbursements

Jan 20/05

Sam Smith

IN 0101

1,386.71

1,000.00

90.72

152.35

Jan 20/05

Payment of Account

123

1,386.71

(1,386.71)

Jan 20/05

Deposit of Funds

(1386.71)

1,386.71

[Expenses] Office

Phone

Travel

(25.43)

(43.21)

(75.00)

4.5 General Account Deposits The following steps are required to process a deposit to your general account: 4.5.1 Issue a prenumbered receipt (if applicable). The receipt should be completed showing: ► The date received.

32

► From whom the funds were received. ► Why the funds were paid to you (e.g. fees, paid on account, capital contribution, expense recovery). ► Invoice number or date (if applicable). ► If amount has been paid from trust, the receipt and the invoice should be marked “paid from trust”. 4.5.2 Post the deposit to the General Cheque Book. Record deposit on the current cheque stub in your General Cheque Book and update the running balance. 4.5.3 Write the deposit up in the General Deposit Book. 4.5.4 If the deposit is in payment of a client account receivable, locate the particular invoice being paid, record the date monies are received on the invoice, and mark invoice as paid. Record the invoice in the Synoptic as shown in Item 4.4.5.

TIP

To pay an account out of trust money, write a trust cheque to yourself (i.e. Smith Law Office) and deposit it into your general account. The account must be prepared and sent to the client before or at the time funds are removed from trust.

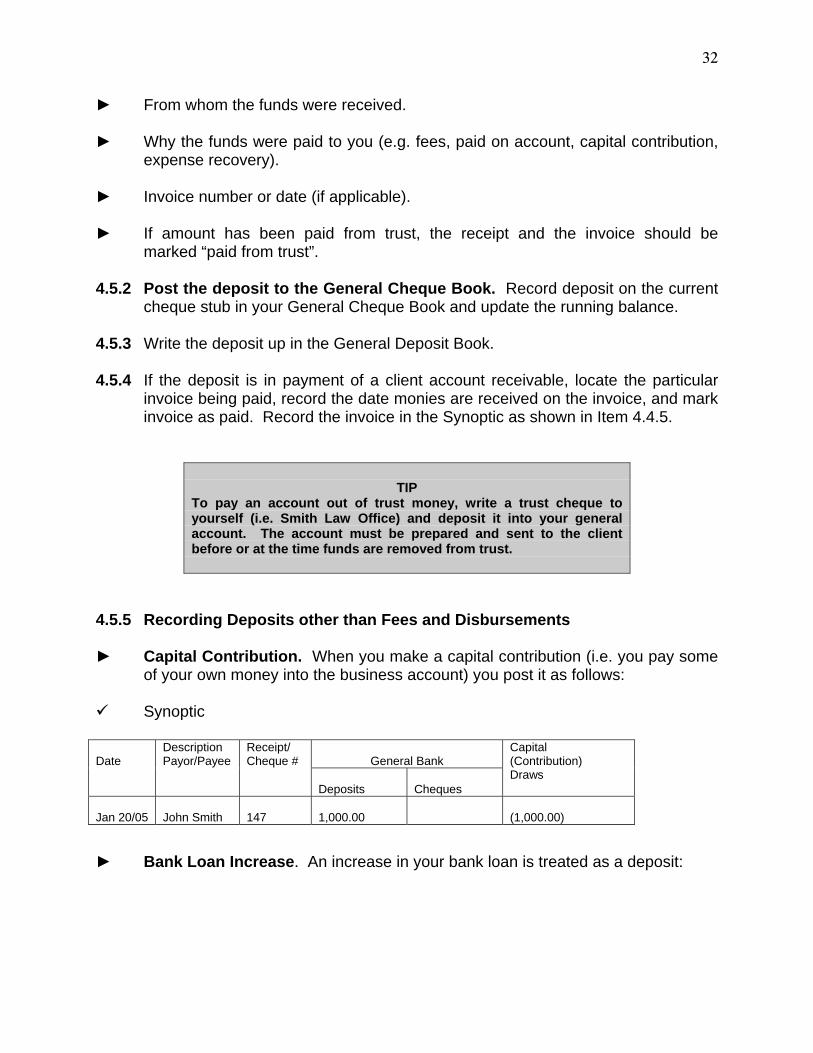

4.5.5 Recording Deposits other than Fees and Disbursements ► Capital Contribution. When you make a capital contribution (i.e. you pay some of your own money into the business account) you post it as follows:

Synoptic

General Bank

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits

Cheques

Capital (Contribution) Draws

Jan 20/05

John Smith

147

1,000.00

(1,000.00)

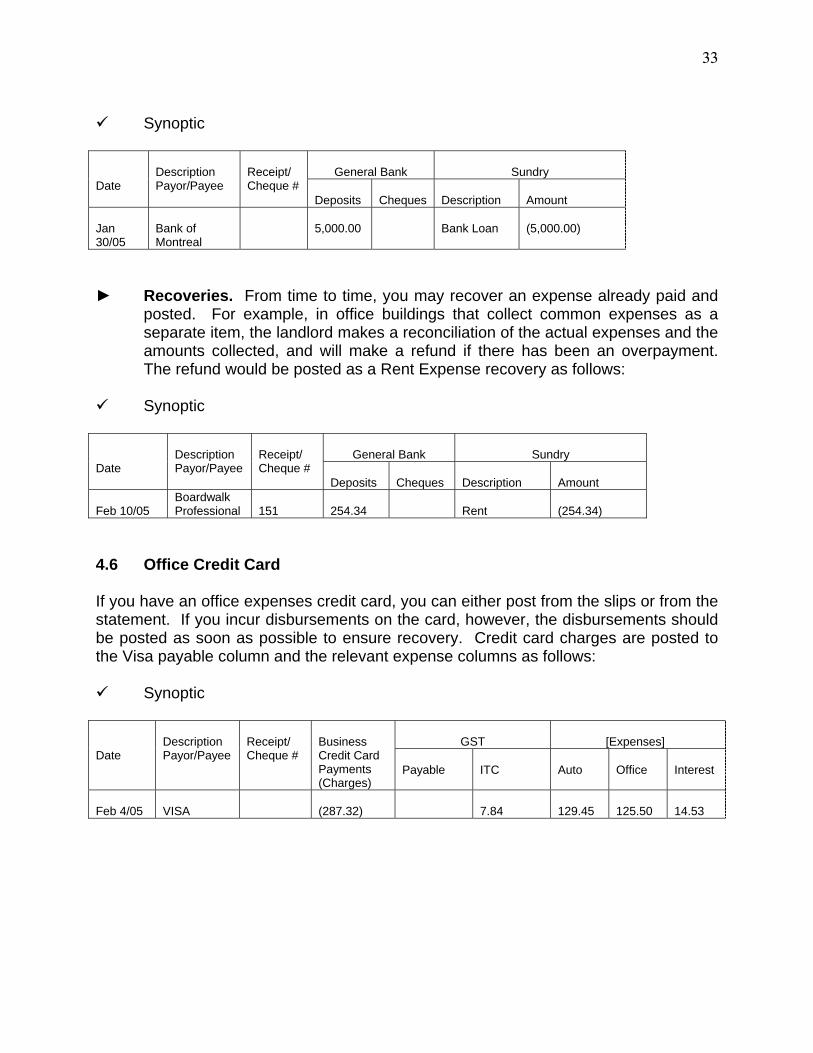

► Bank Loan Increase. An increase in your bank loan is treated as a deposit:

33

Synoptic

General Bank

Sundry Date

Description Payor/Payee

Receipt/ Cheque #

Deposits Cheques

Description

Amount

Jan 30/05

Bank of Montreal

5,000.00

Bank Loan

(5,000.00)

► Recoveries. From time to time, you may recover an expense already paid and posted. For example, in office buildings that collect common expenses as a separate item, the landlord makes a reconciliation of the actual expenses and the amounts collected, and will make a refund if there has been an overpayment. The refund would be posted as a Rent Expense recovery as follows:

Synoptic

General Bank

Sundry

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits Cheques

Description

Amount

Feb 10/05

Boardwalk Professional

151

254.34

Rent

(254.34)

4.6 Office Credit Card If you have an office expenses credit card, you can either post from the slips or from the statement. If you incur disbursements on the card, however, the disbursements should be posted as soon as possible to ensure recovery. Credit card charges are posted to the Visa payable column and the relevant expense columns as follows:

Synoptic

GST

[Expenses]

Date

Description Payor/Payee

Receipt/ Cheque #

Business Credit Card Payments (Charges)

Payable

ITC

Auto

Office

Interest

Feb 4/05

VISA

(287.32)

7.84

129.45

125.50

14.53

34

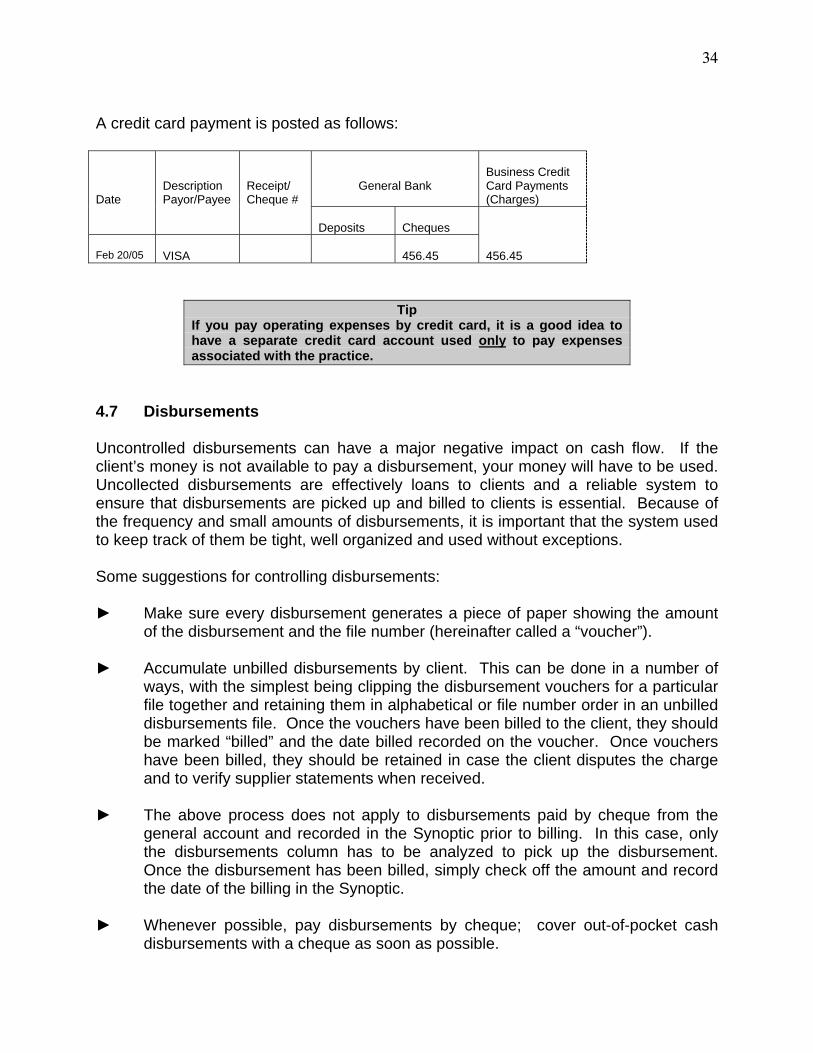

A credit card payment is posted as follows:

General Bank

Business Credit Card Payments (Charges)

Date

Description Payor/Payee

Receipt/ Cheque #

Deposits

Cheques

Feb 20/05

VISA

456.45

456.45

Tip If you pay operating expenses by credit card, it is a good idea to have a separate credit card account used only to pay expenses associated with the practice.

4.7 Disbursements Uncontrolled disbursements can have a major negative impact on cash flow. If the client’s money is not available to pay a disbursement, your money will have to be used. Uncollected disbursements are effectively loans to clients and a reliable system to ensure that disbursements are picked up and billed to clients is essential. Because of the frequency and small amounts of disbursements, it is important that the system used to keep track of them be tight, well organized and used without exceptions. Some suggestions for controlling disbursements: ► Make sure every disbursement generates a piece of paper showing the amount of the disbursement and the file number (hereinafter called a “voucher”). ► Accumulate unbilled disbursements by client. This can be done in a number of ways, with the simplest being clipping the disbursement vouchers for a particular file together and retaining them in alphabetical or file number order in an unbilled disbursements file. Once the vouchers have been billed to the client, they should be marked “billed” and the date billed recorded on the voucher. Once vouchers have been billed, they should be retained in case the client disputes the charge and to verify supplier statements when received. ► The above process does not apply to disbursements paid by cheque from the general account and recorded in the Synoptic prior to billing. In this case, only the disbursements column has to be analyzed to pick up the disbursement. Once the disbursement has been billed, simply check off the amount and record the date of the billing in the Synoptic. ► Whenever possible, pay disbursements by cheque; cover out-of-pocket cash disbursements with a cheque as soon as possible.

35

► Unbilled disbursements system should be updated daily. If your disbursement recording system is not kept current, you will find yourself wasting an extraordinary amount of time hunting down relatively trivial amounts of disbursements. ► Use extended time and charges or called-back time and charges for long distance charges (don’t forget the tax) to create a voucher. ► Do not estimate disbursements; disbursements are actual amounts paid out on a client’s behalf and it is dishonest to represent an amount as such if you are not sure of the actual amount. ► Pay significant disbursements from trust money provided for that purpose. ► An alternative to the system described above is posting to an Unbilled Client Disbursements Ledger. The Unbilled Client Disbursement Ledger is a ledger that keeps track of unbilled disbursements on a client-by-client basis. Disbursements are charged to this ledger as soon as they are incurred; when they are billed, they are removed from the ledger. The following steps are required, on a daily basis, to post disbursements to the unbilled client disbursements ledger: 4.7.1 Assemble disbursement vouchers. 4.7.2 Record the date, the particulars and the amount of the disbursements on the appropriate Unbilled Client Disbursements Ledger Cards. There is no Synoptic posting for unbilled disbursements until you actually pay them; they are then recorded as expenses. When you are reimbursed for disbursements by your client, the reimbursement is recorded as an expense recovery. 4.7.3 Mark the vouchers to show that they have been posted. 4.7.4 File the vouchers as part of your accounting information; do not file them in the client file, as they will be needed to verify the statements you will receive from the courier, the Land Titles Office, the phone company, etc. If you ever need to substantiate an account, you can trace them back through the date on the Client Unbilled Disbursement Ledger Card.

TIP

There are numerous processes to ensure disbursements get billed and you may adapt this or other systems to “what works best for you”. Volume is a significant factor in determining the best system to use.

36

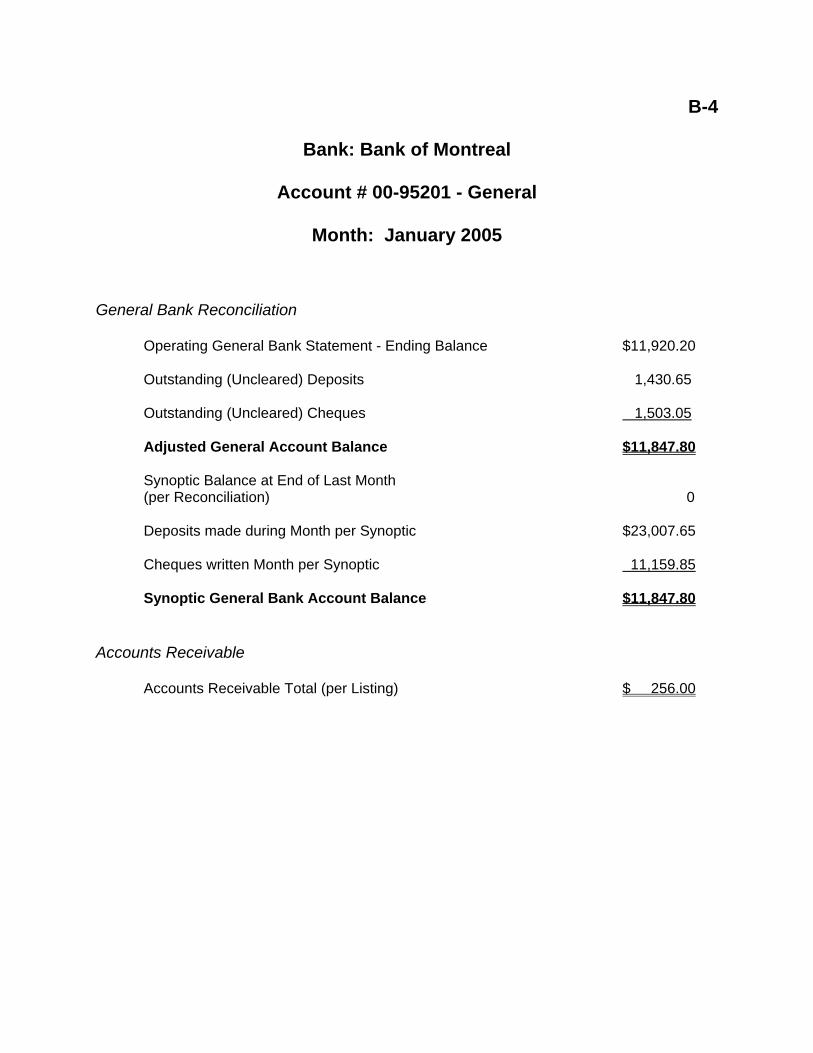

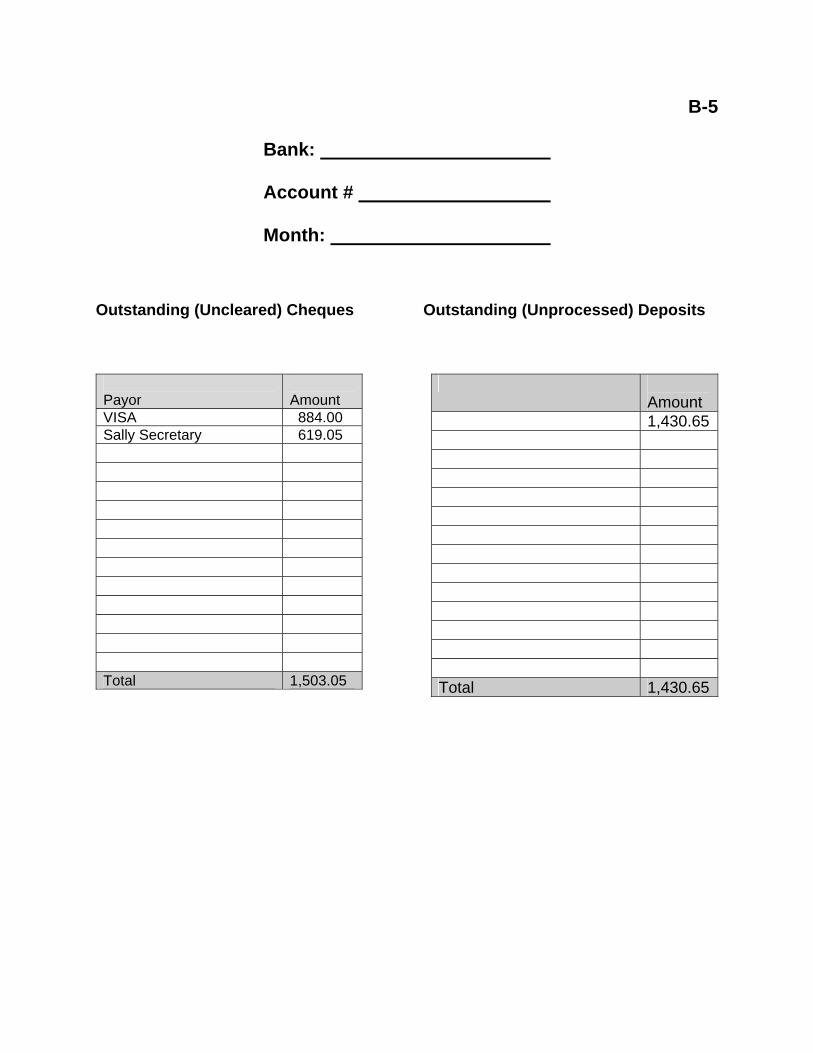

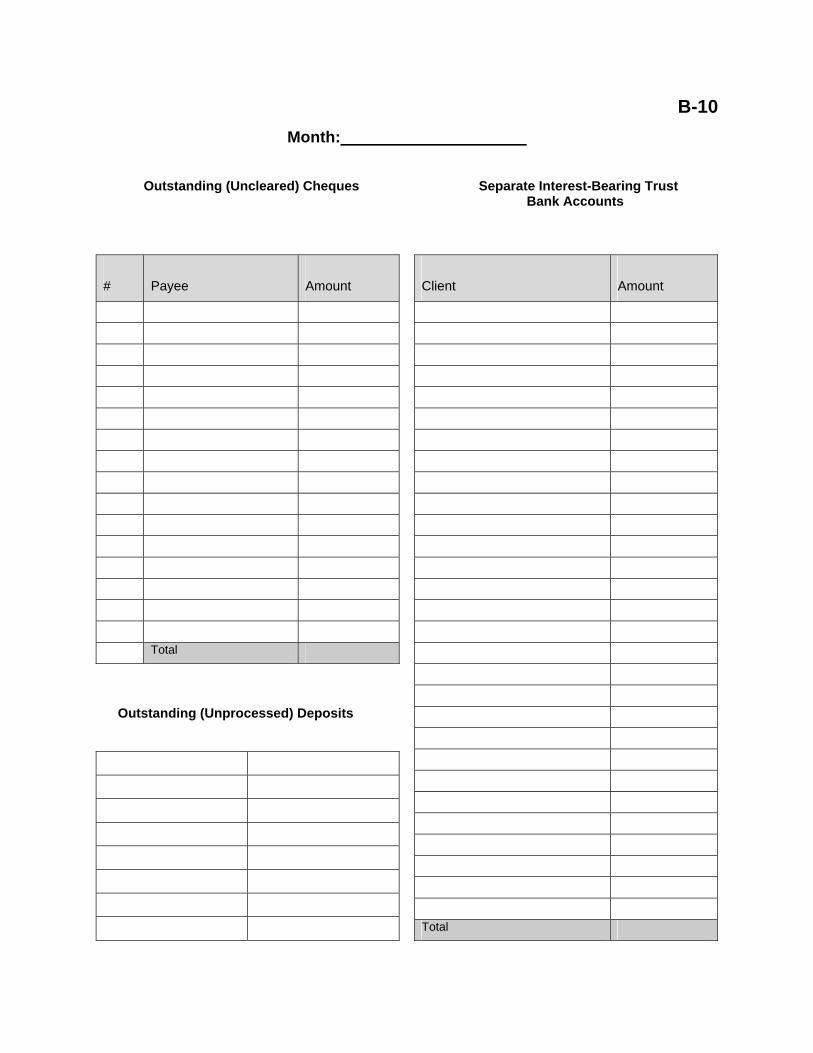

4.8 Monthly GL Reconciliation and Report Your general bank account should be reconciled monthly when the statement is received from the bank. The reconciliation requires you to reconcile your General Bank Statement with the General Bank columns of the Synoptic. Use the forms in Schedules “B” and “C” if you wish.

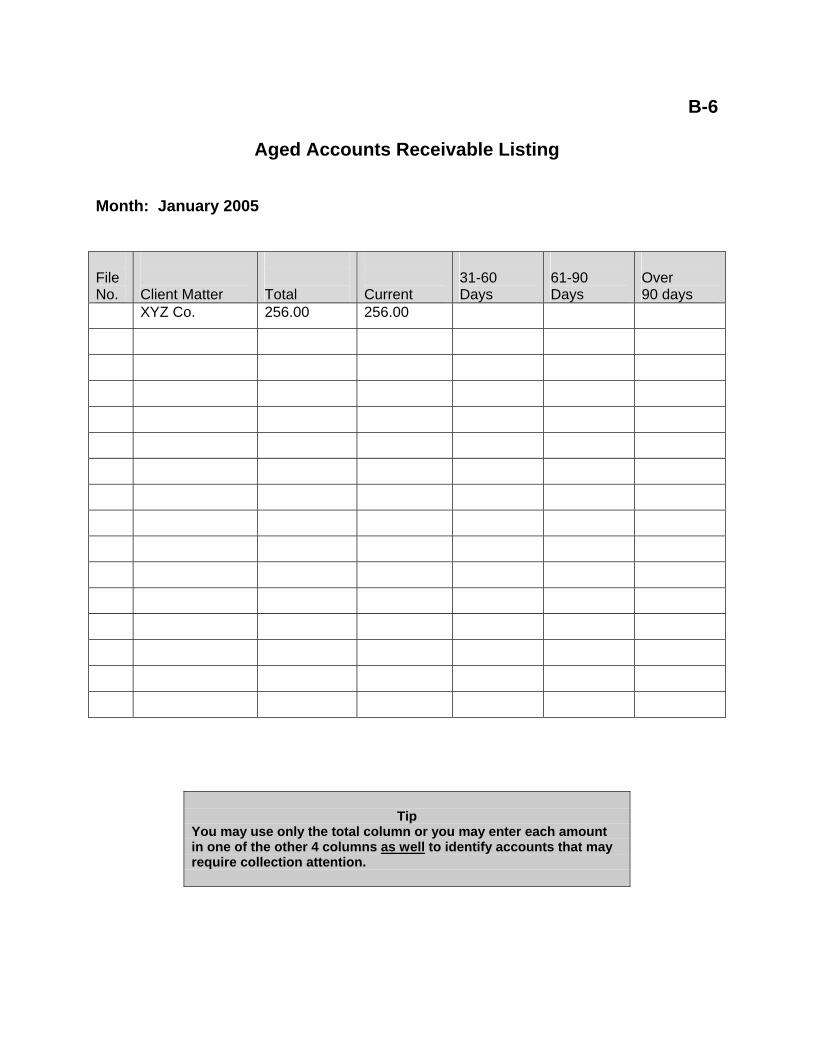

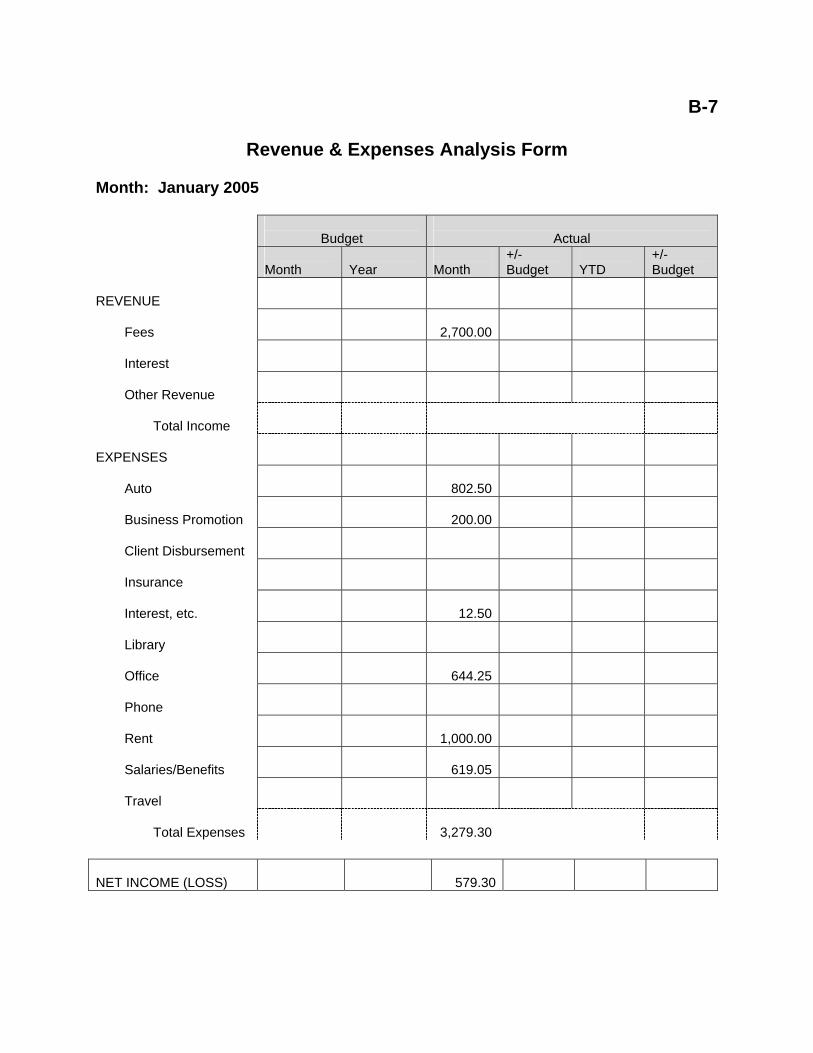

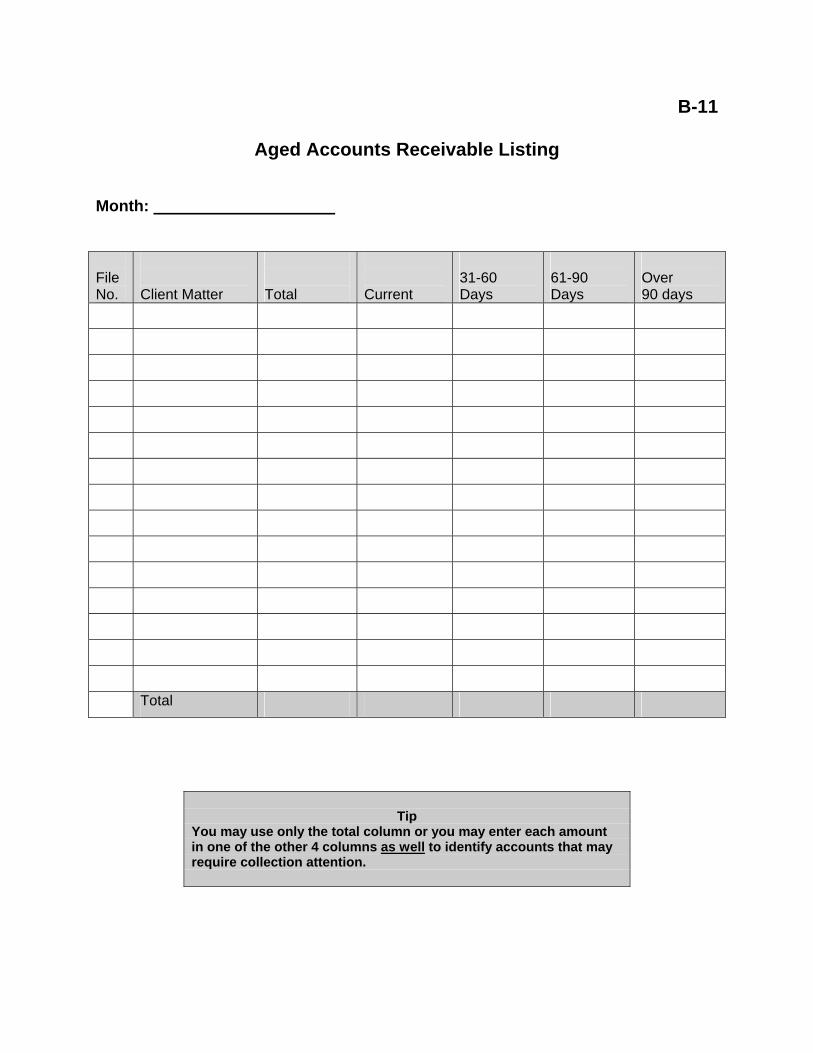

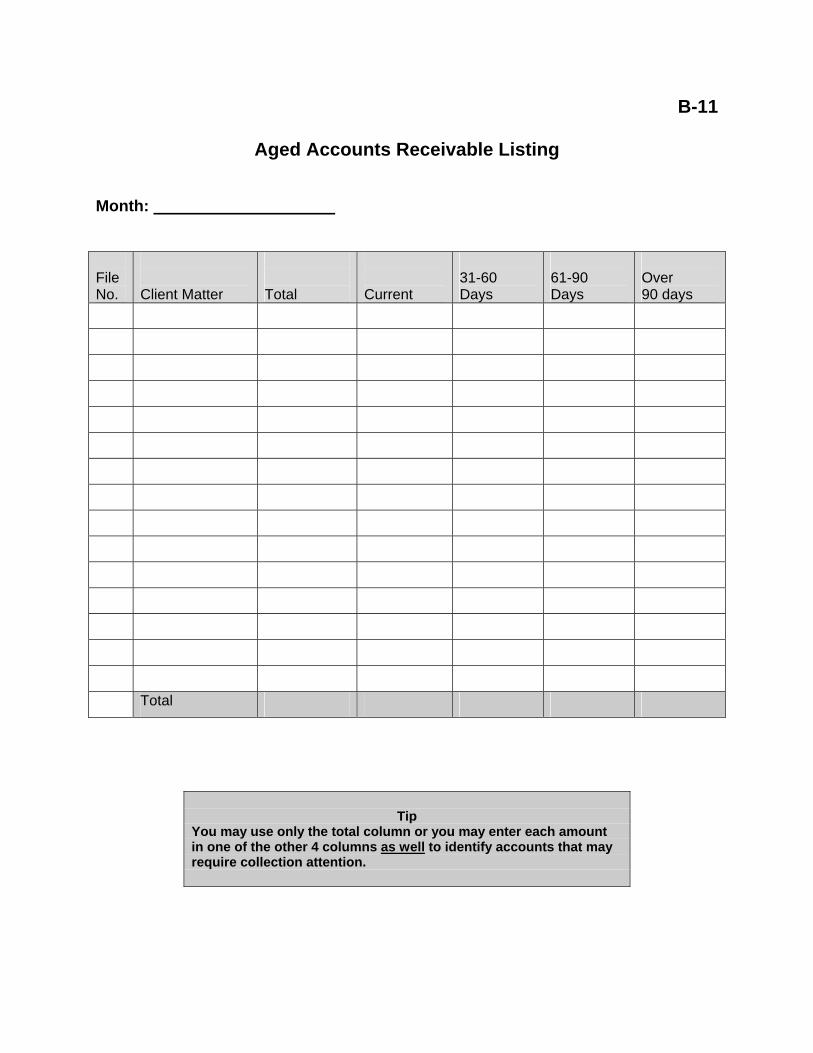

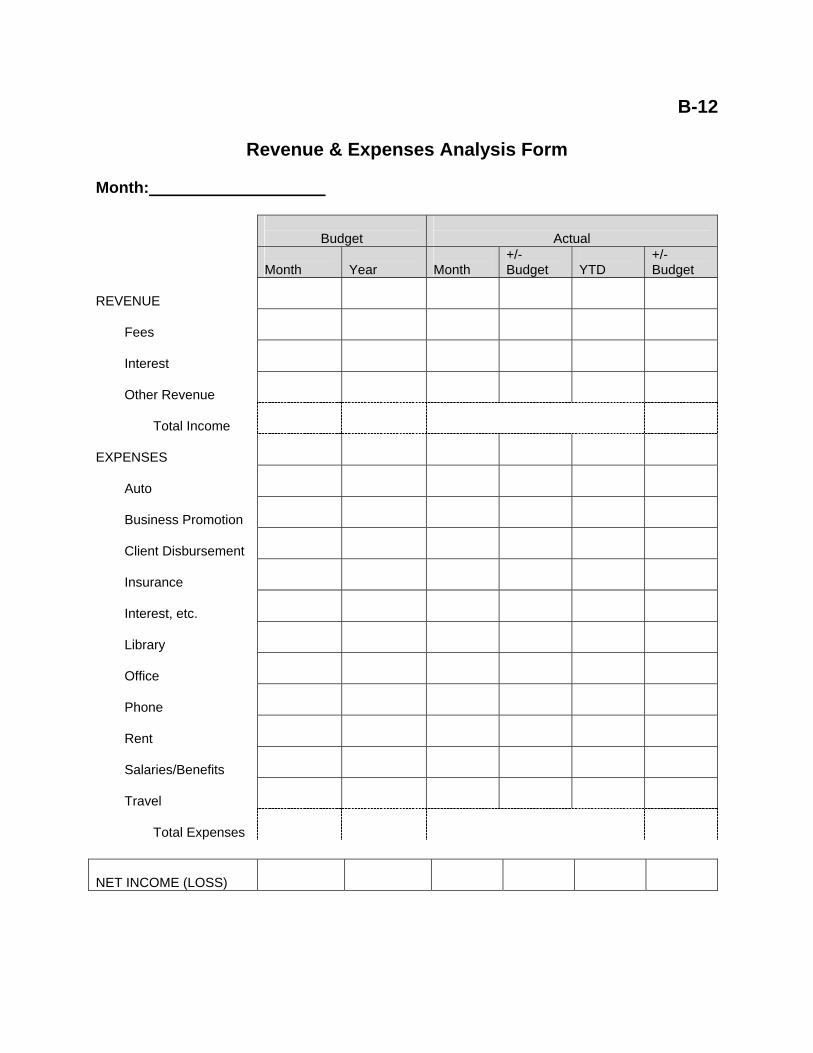

Because you are using a double entry bookkeeping system for the GL, your Synoptic must always be in balance (cross add). After reconciling the bank, the Synoptic must be “balanced”. If the Synoptic does not balance, you will have to go back over the entries and make sure each entry cross-adds. The GL Synoptic can also be used as the basis for a limited amount of analysis of your practice’s financial performance. Almost all the information needed for a Monthly Cash Flow Analysis and the Revenue and Expenses Analysis (Schedule “D”) can be taken off the Synoptic, the only exception being accounts receivable, which you must get from the unpaid invoices in the Accounts Receivable Binder, unbilled disbursements information, which you may have to get from the unbilled client vouchers or the Unbilled Client Disbursements Ledger. This form gives you a snap-shot of your practice from a financial perspective. In addition, the latter allows you to assess the performance of your practice against your budget (if available). These forms will give you some of the management information you will need to make decisions in relation to the future of your practice. 4.9 Appendix B provides a hypothetical example of a completed: ► General Ledger Synoptic - General Daily Journal with Column and Transaction Descriptions. ► A General Ledger Reconciliation Checklist. ► General Bank Reconciliation and supporting listings. ► Aged Accounts Receivable Listing. ► Revenue and Expense Analysis Forms. ► Invoice. Blank forms have also been included for your use if you wish.

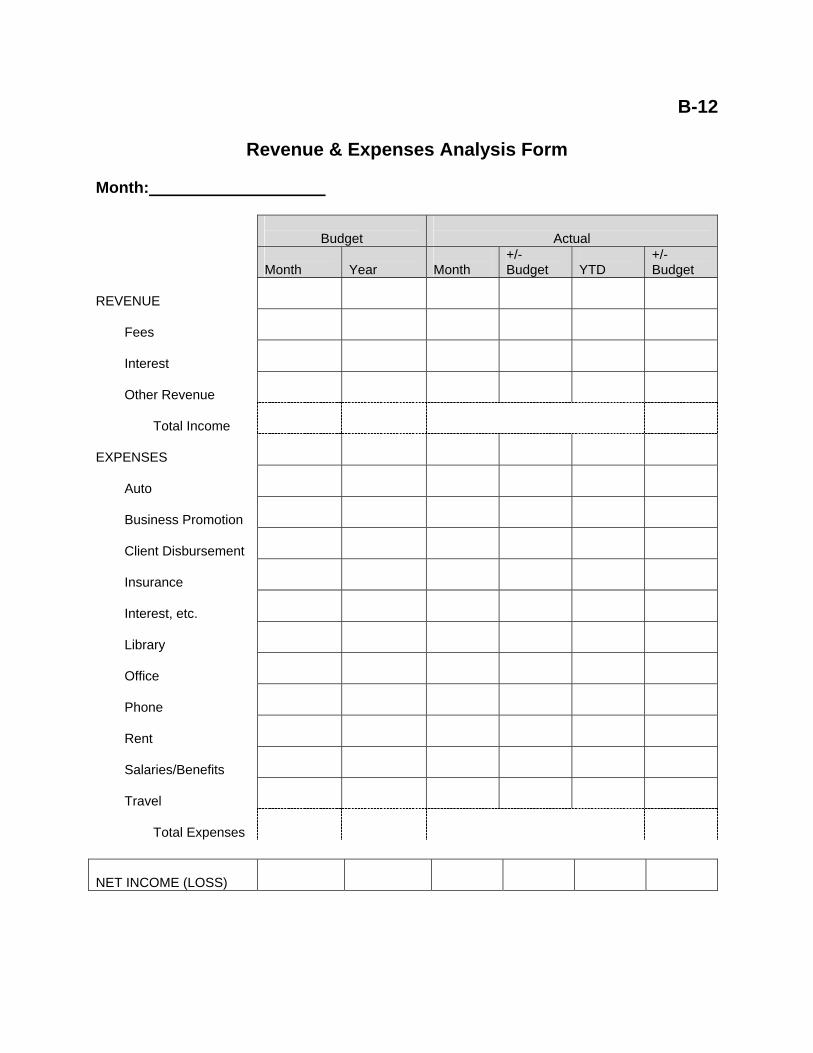

Appendix A

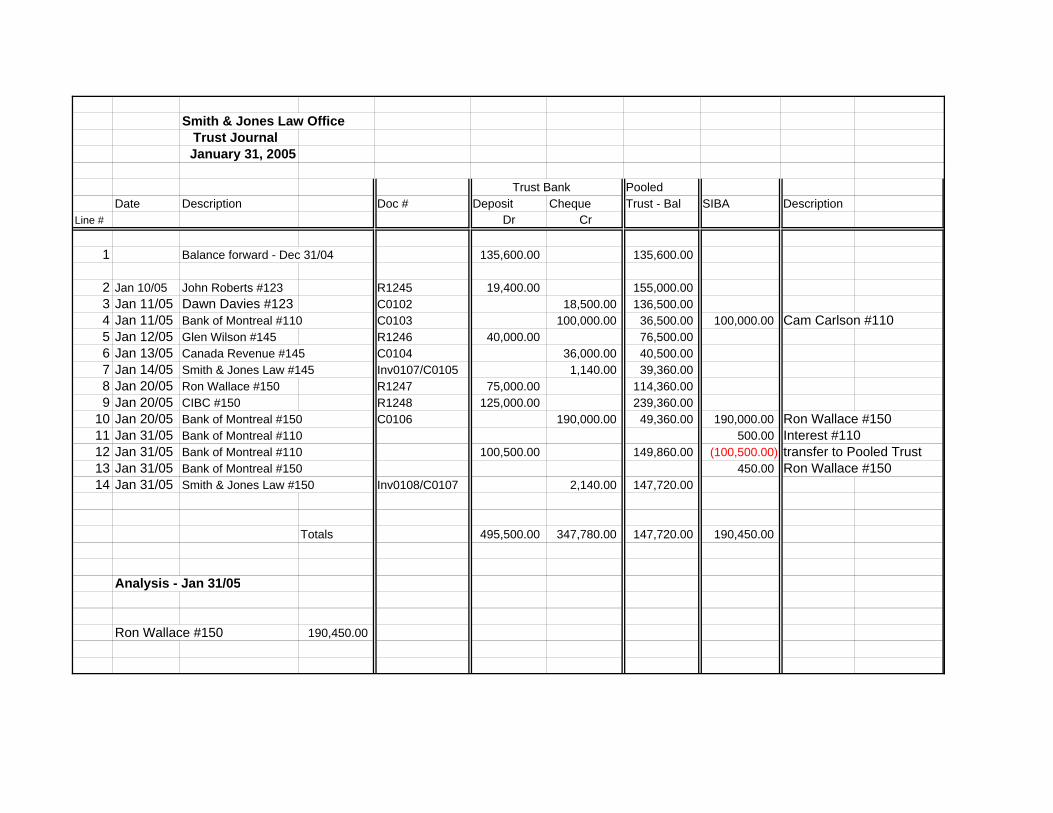

Smith & Jones Law Office Trust Journal

January 31, 2005

Trust Bank PooledDate Description Doc # Deposit Cheque Trust - Bal SIBA Description

Line # Dr Cr

1 Balance forward - Dec 31/04 135,600.00 135,600.00

2 Jan 10/05 John Roberts #123 R1245 19,400.00 155,000.003 Jan 11/05 Dawn Davies #123 C0102 18,500.00 136,500.004 Jan 11/05 Bank of Montreal #110 C0103 100,000.00 36,500.00 100,000.00 Cam Carlson #1105 Jan 12/05 Glen Wilson #145 R1246 40,000.00 76,500.006 Jan 13/05 Canada Revenue #145 C0104 36,000.00 40,500.007 Jan 14/05 Smith & Jones Law #145 Inv0107/C0105 1,140.00 39,360.008 Jan 20/05 Ron Wallace #150 R1247 75,000.00 114,360.009 Jan 20/05 CIBC #150 R1248 125,000.00 239,360.00

10 Jan 20/05 Bank of Montreal #150 C0106 190,000.00 49,360.00 190,000.00 Ron Wallace #15011 Jan 31/05 Bank of Montreal #110 500.00 Interest #11012 Jan 31/05 Bank of Montreal #110 100,500.00 149,860.00 (100,500.00) transfer to Pooled Trust13 Jan 31/05 Bank of Montreal #150 450.00 Ron Wallace #15014 Jan 31/05 Smith & Jones Law #150 Inv0108/C0107 2,140.00 147,720.00

Totals 495,500.00 347,780.00 147,720.00 190,450.00

Analysis - Jan 31/05

Ron Wallace #150 190,450.00

A-1

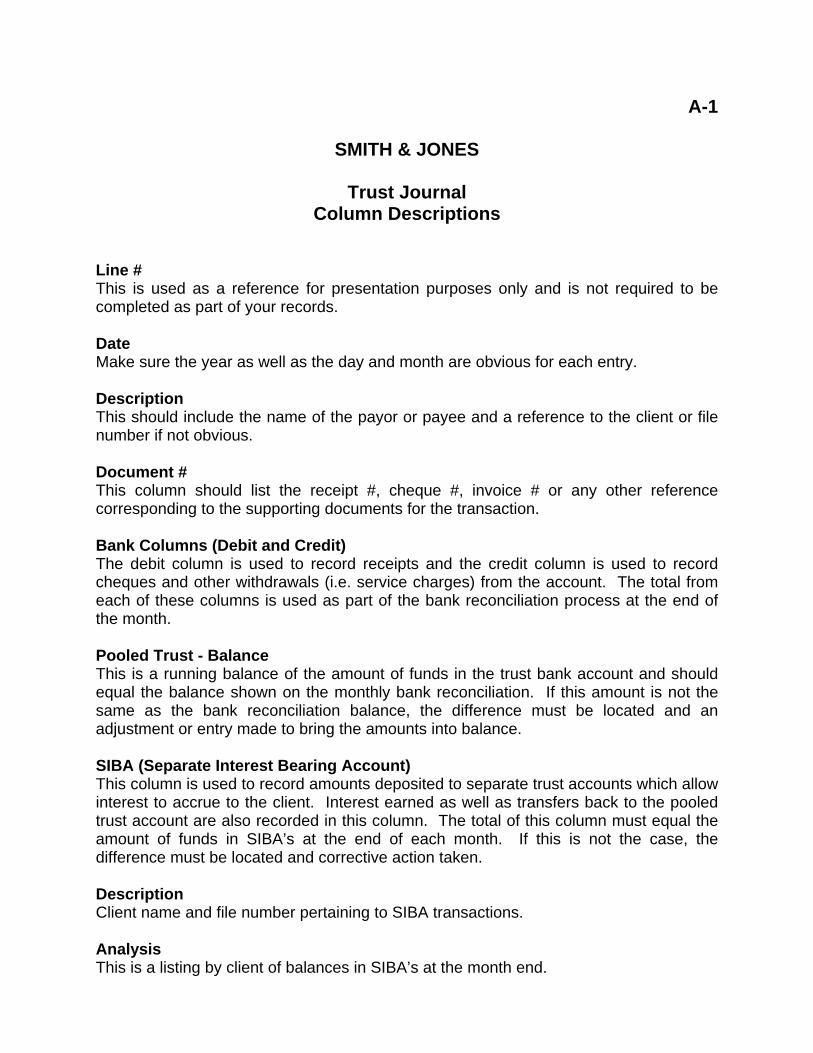

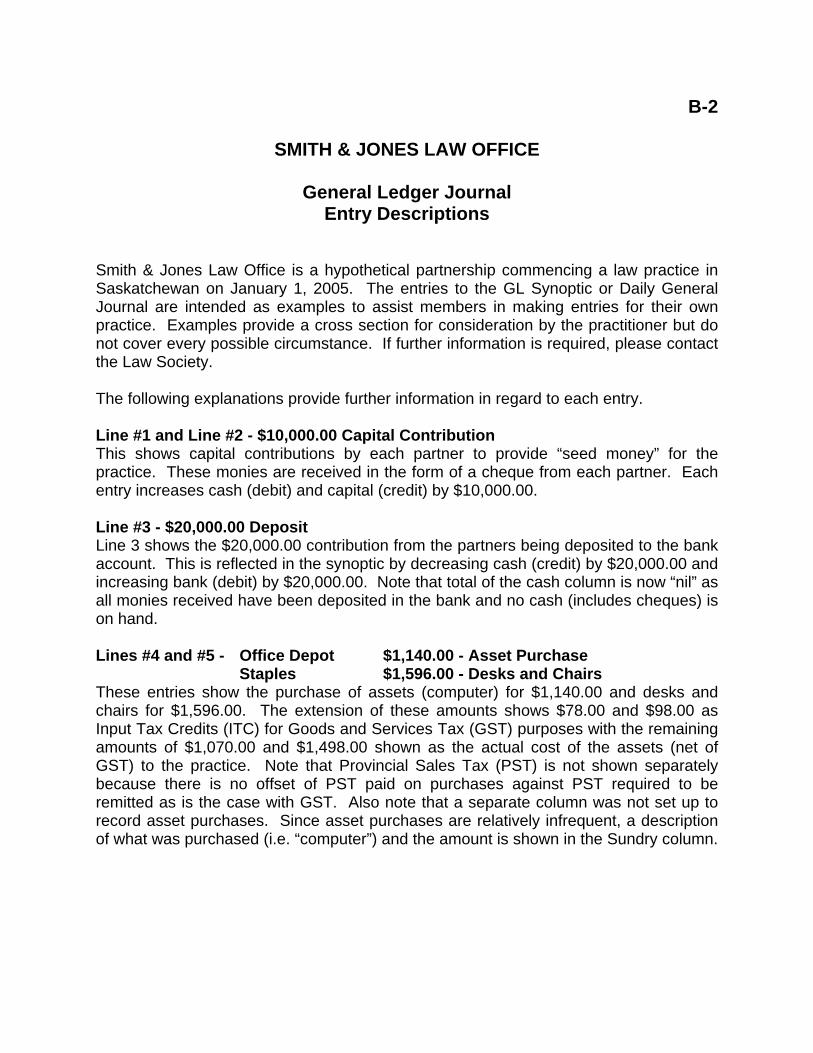

SMITH & JONES

Trust Journal Column Descriptions

Line # This is used as a reference for presentation purposes only and is not required to be completed as part of your records. Date Make sure the year as well as the day and month are obvious for each entry. Description This should include the name of the payor or payee and a reference to the client or file number if not obvious. Document # This column should list the receipt #, cheque #, invoice # or any other reference corresponding to the supporting documents for the transaction. Bank Columns (Debit and Credit) The debit column is used to record receipts and the credit column is used to record cheques and other withdrawals (i.e. service charges) from the account. The total from each of these columns is used as part of the bank reconciliation process at the end of the month. Pooled Trust - Balance This is a running balance of the amount of funds in the trust bank account and should equal the balance shown on the monthly bank reconciliation. If this amount is not the same as the bank reconciliation balance, the difference must be located and an adjustment or entry made to bring the amounts into balance. SIBA (Separate Interest Bearing Account) This column is used to record amounts deposited to separate trust accounts which allow interest to accrue to the client. Interest earned as well as transfers back to the pooled trust account are also recorded in this column. The total of this column must equal the amount of funds in SIBA’s at the end of each month. If this is not the case, the difference must be located and corrective action taken. Description Client name and file number pertaining to SIBA transactions. Analysis This is a listing by client of balances in SIBA’s at the month end.

A-2

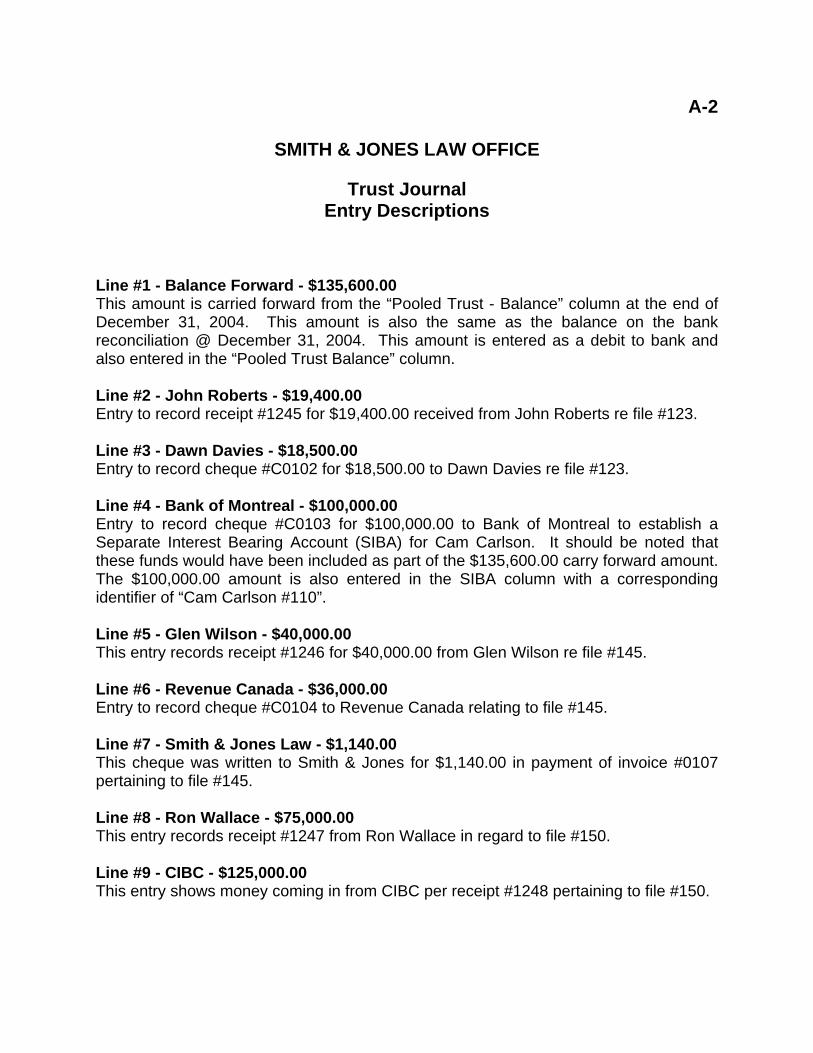

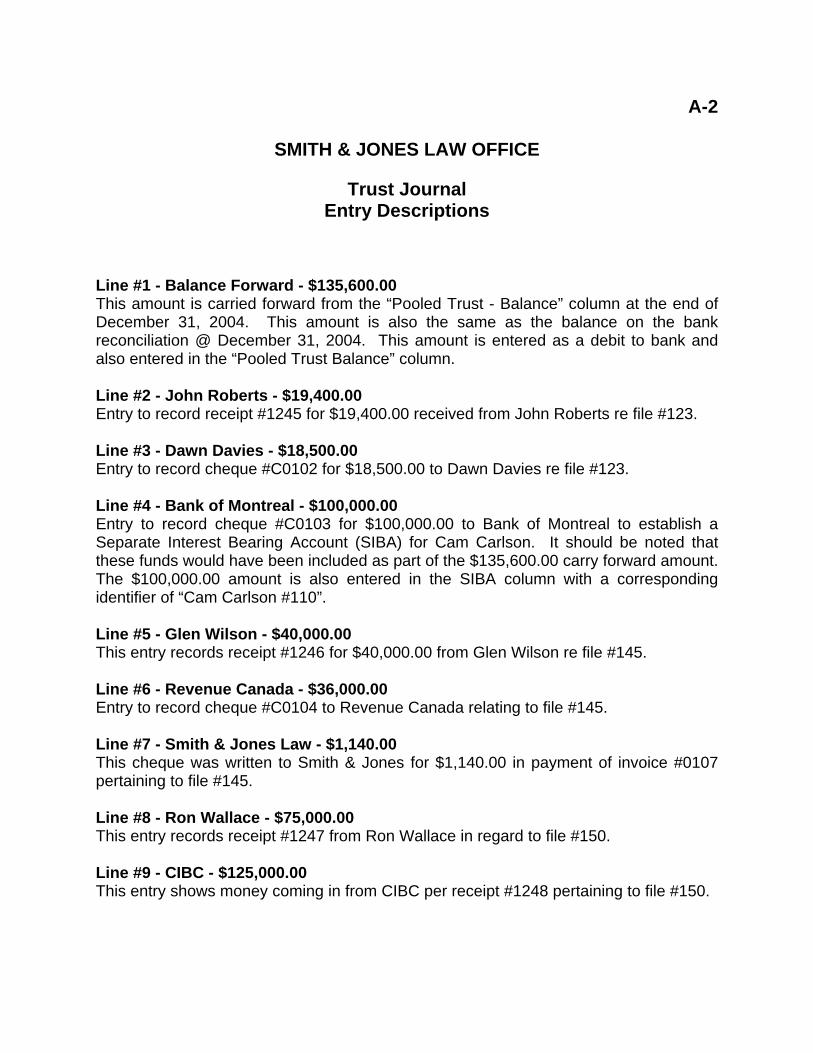

SMITH & JONES LAW OFFICE

Trust Journal Entry Descriptions

Line #1 - Balance Forward - $135,600.00 This amount is carried forward from the “Pooled Trust - Balance” column at the end of December 31, 2004. This amount is also the same as the balance on the bank reconciliation @ December 31, 2004. This amount is entered as a debit to bank and also entered in the “Pooled Trust Balance” column. Line #2 - John Roberts - $19,400.00 Entry to record receipt #1245 for $19,400.00 received from John Roberts re file #123. Line #3 - Dawn Davies - $18,500.00 Entry to record cheque #C0102 for $18,500.00 to Dawn Davies re file #123. Line #4 - Bank of Montreal - $100,000.00 Entry to record cheque #C0103 for $100,000.00 to Bank of Montreal to establish a Separate Interest Bearing Account (SIBA) for Cam Carlson. It should be noted that these funds would have been included as part of the $135,600.00 carry forward amount. The $100,000.00 amount is also entered in the SIBA column with a corresponding identifier of “Cam Carlson #110”. Line #5 - Glen Wilson - $40,000.00 This entry records receipt #1246 for $40,000.00 from Glen Wilson re file #145. Line #6 - Revenue Canada - $36,000.00 Entry to record cheque #C0104 to Revenue Canada relating to file #145. Line #7 - Smith & Jones Law - $1,140.00 This cheque was written to Smith & Jones for $1,140.00 in payment of invoice #0107 pertaining to file #145. Line #8 - Ron Wallace - $75,000.00 This entry records receipt #1247 from Ron Wallace in regard to file #150. Line #9 - CIBC - $125,000.00 This entry shows money coming in from CIBC per receipt #1248 pertaining to file #150.

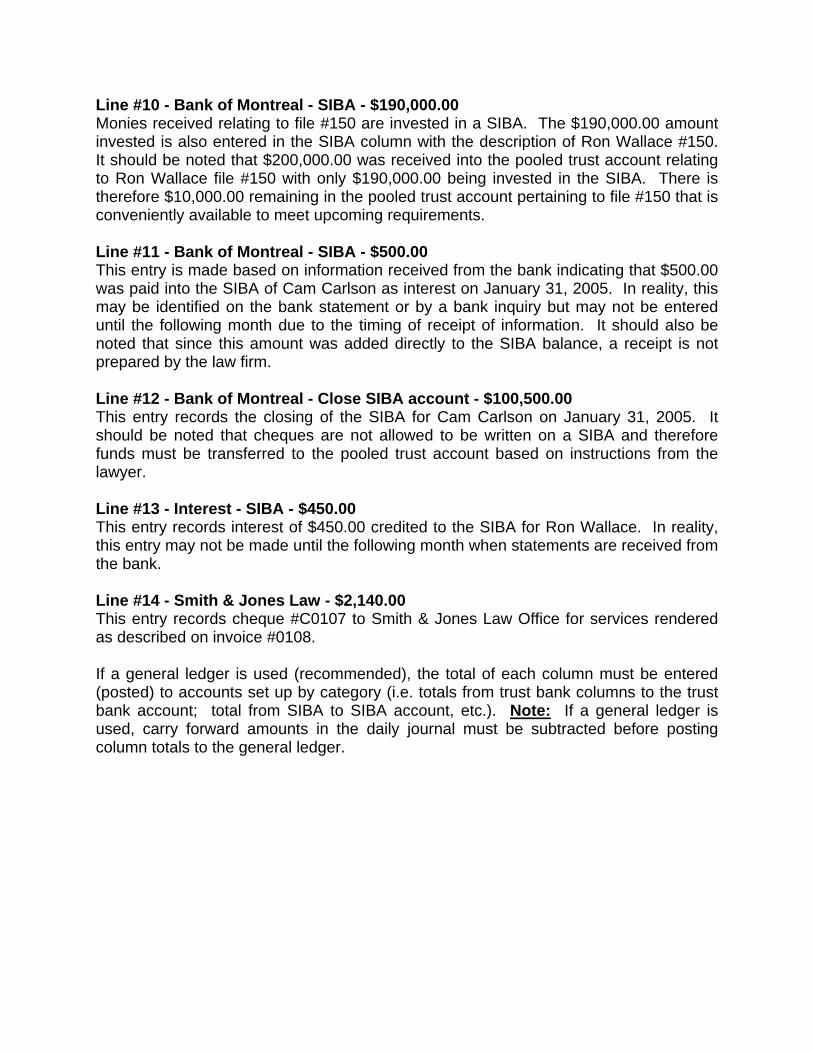

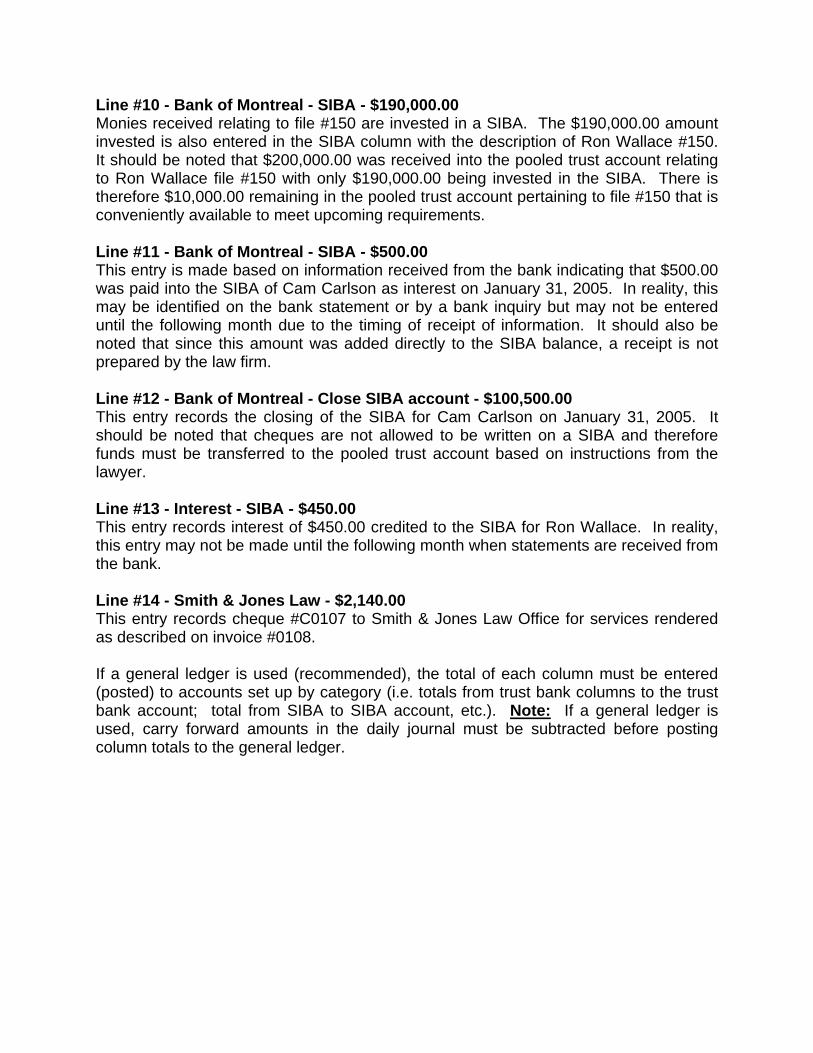

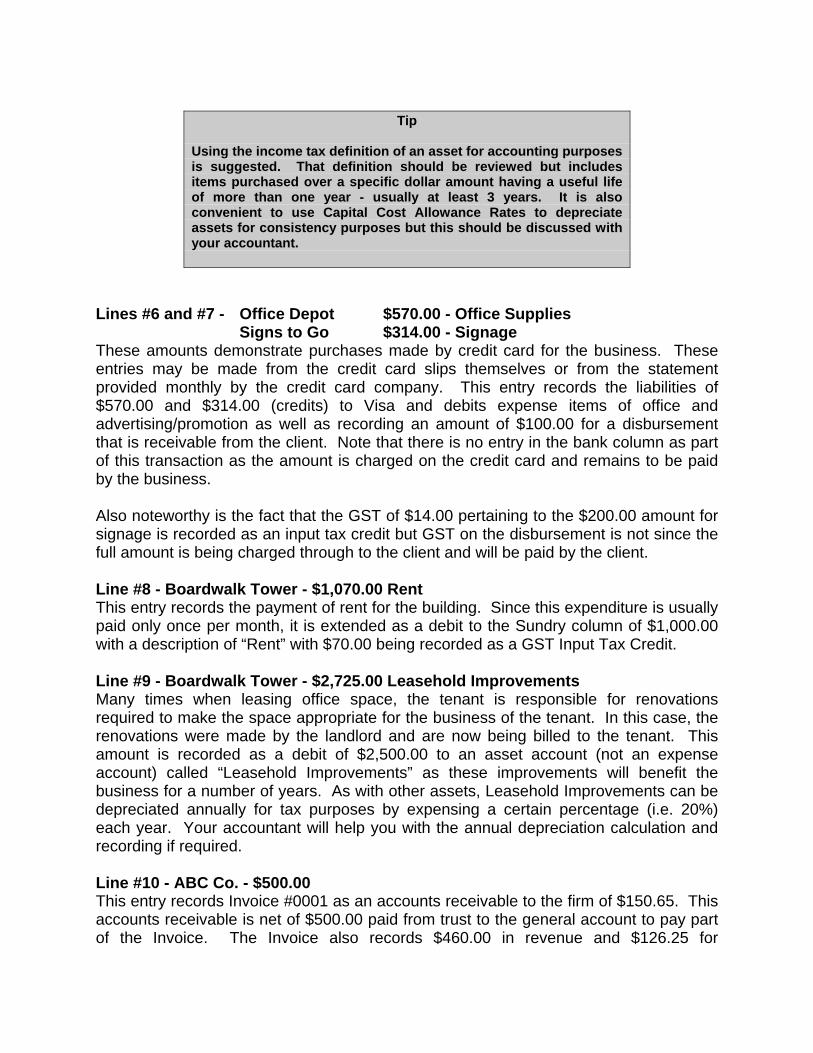

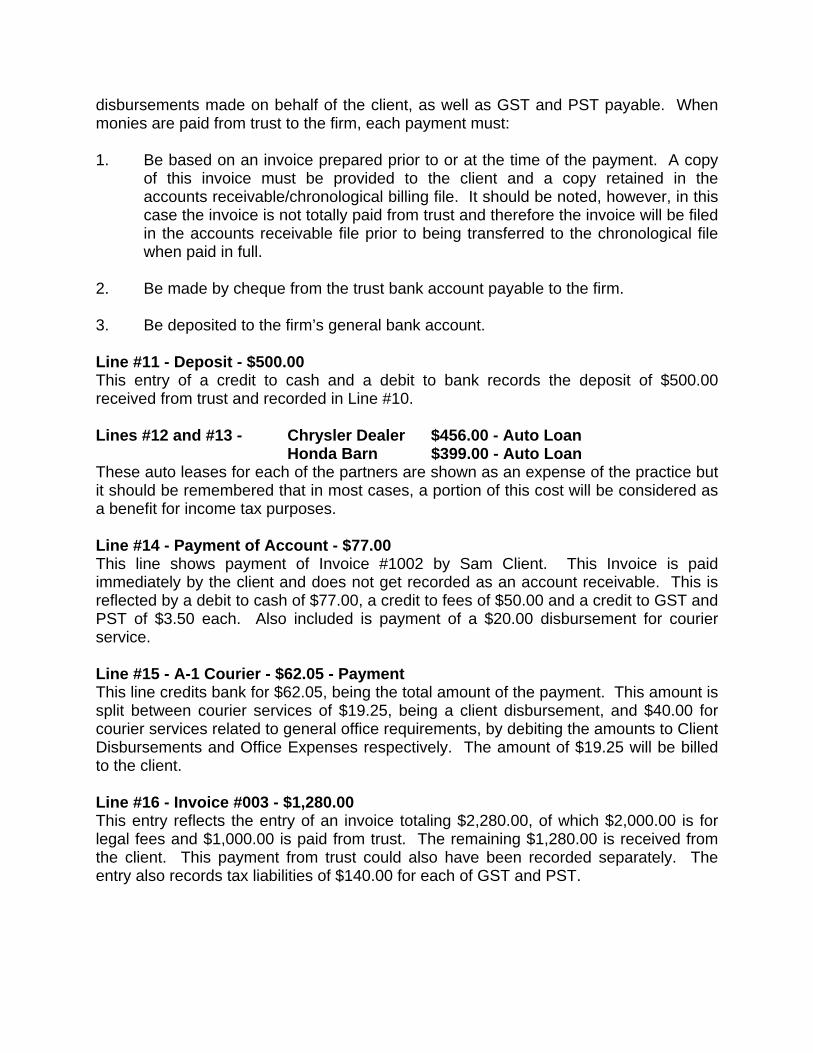

Line #10 - Bank of Montreal - SIBA - $190,000.00 Monies received relating to file #150 are invested in a SIBA. The $190,000.00 amount invested is also entered in the SIBA column with the description of Ron Wallace #150. It should be noted that $200,000.00 was received into the pooled trust account relating to Ron Wallace file #150 with only $190,000.00 being invested in the SIBA. There is therefore $10,000.00 remaining in the pooled trust account pertaining to file #150 that is conveniently available to meet upcoming requirements. Line #11 - Bank of Montreal - SIBA - $500.00 This entry is made based on information received from the bank indicating that $500.00 was paid into the SIBA of Cam Carlson as interest on January 31, 2005. In reality, this may be identified on the bank statement or by a bank inquiry but may not be entered until the following month due to the timing of receipt of information. It should also be noted that since this amount was added directly to the SIBA balance, a receipt is not prepared by the law firm. Line #12 - Bank of Montreal - Close SIBA account - $100,500.00 This entry records the closing of the SIBA for Cam Carlson on January 31, 2005. It should be noted that cheques are not allowed to be written on a SIBA and therefore funds must be transferred to the pooled trust account based on instructions from the lawyer. Line #13 - Interest - SIBA - $450.00 This entry records interest of $450.00 credited to the SIBA for Ron Wallace. In reality, this entry may not be made until the following month when statements are received from the bank. Line #14 - Smith & Jones Law - $2,140.00 This entry records cheque #C0107 to Smith & Jones Law Office for services rendered as described on invoice #0108. If a general ledger is used (recommended), the total of each column must be entered (posted) to accounts set up by category (i.e. totals from trust bank columns to the trust bank account; total from SIBA to SIBA account, etc.). Note: If a general ledger is used, carry forward amounts in the daily journal must be subtracted before posting column totals to the general ledger.

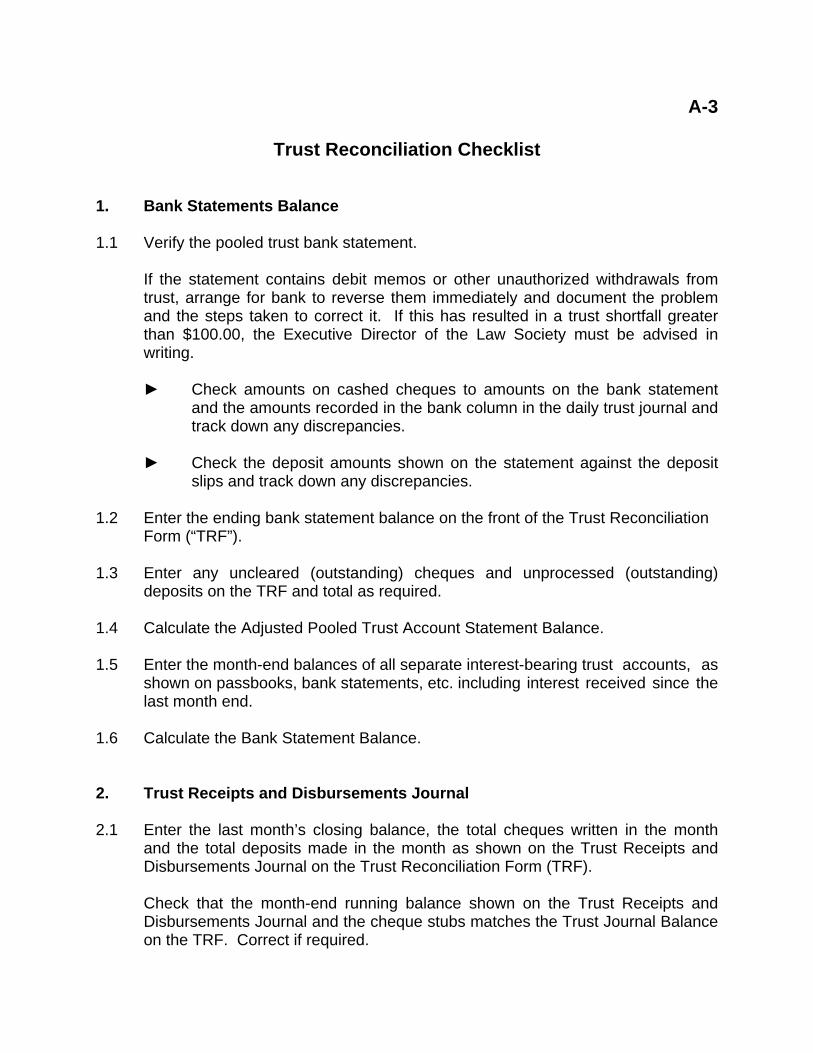

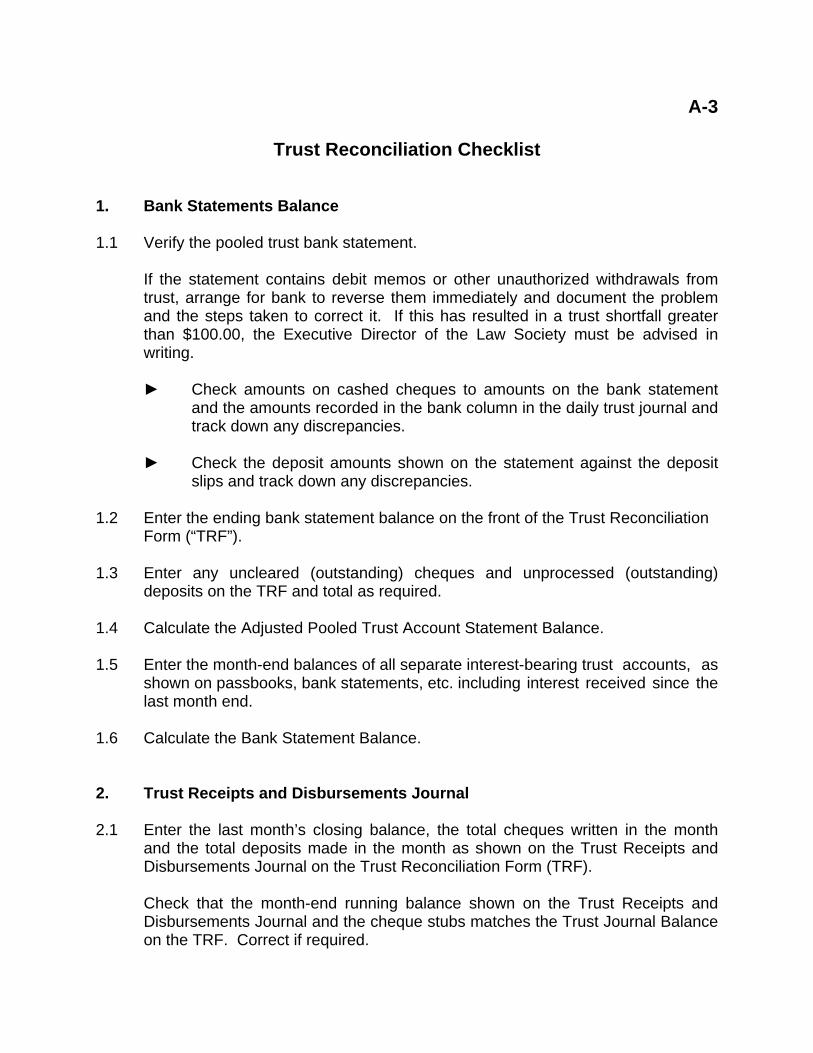

A-3

Trust Reconciliation Checklist 1. Bank Statements Balance 1.1 Verify the pooled trust bank statement. If the statement contains debit memos or other unauthorized withdrawals from trust, arrange for bank to reverse them immediately and document the problem and the steps taken to correct it. If this has resulted in a trust shortfall greater than $100.00, the Executive Director of the Law Society must be advised in writing.

► Check amounts on cashed cheques to amounts on the bank statement and the amounts recorded in the bank column in the daily trust journal and track down any discrepancies.

► Check the deposit amounts shown on the statement against the deposit slips and track down any discrepancies.

1.2 Enter the ending bank statement balance on the front of the Trust Reconciliation Form (“TRF”). 1.3 Enter any uncleared (outstanding) cheques and unprocessed (outstanding) deposits on the TRF and total as required. 1.4 Calculate the Adjusted Pooled Trust Account Statement Balance. 1.5 Enter the month-end balances of all separate interest-bearing trust accounts, as

shown on passbooks, bank statements, etc. including interest received since the last month end.

1.6 Calculate the Bank Statement Balance. 2. Trust Receipts and Disbursements Journal 2.1 Enter the last month’s closing balance, the total cheques written in the month and the total deposits made in the month as shown on the Trust Receipts and Disbursements Journal on the Trust Reconciliation Form (TRF). Check that the month-end running balance shown on the Trust Receipts and Disbursements Journal and the cheque stubs matches the Trust Journal Balance on the TRF. Correct if required.

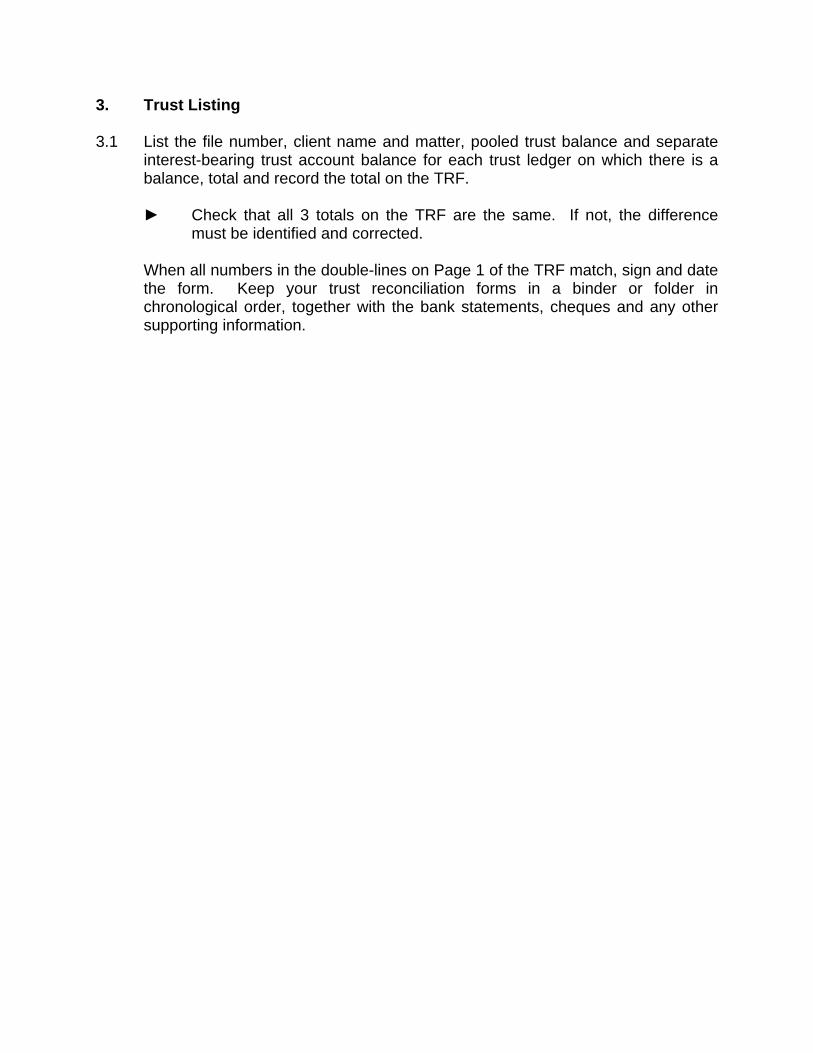

3. Trust Listing 3.1 List the file number, client name and matter, pooled trust balance and separate interest-bearing trust account balance for each trust ledger on which there is a balance, total and record the total on the TRF.

► Check that all 3 totals on the TRF are the same. If not, the difference must be identified and corrected.

When all numbers in the double-lines on Page 1 of the TRF match, sign and date the form. Keep your trust reconciliation forms in a binder or folder in chronological order, together with the bank statements, cheques and any other supporting information.

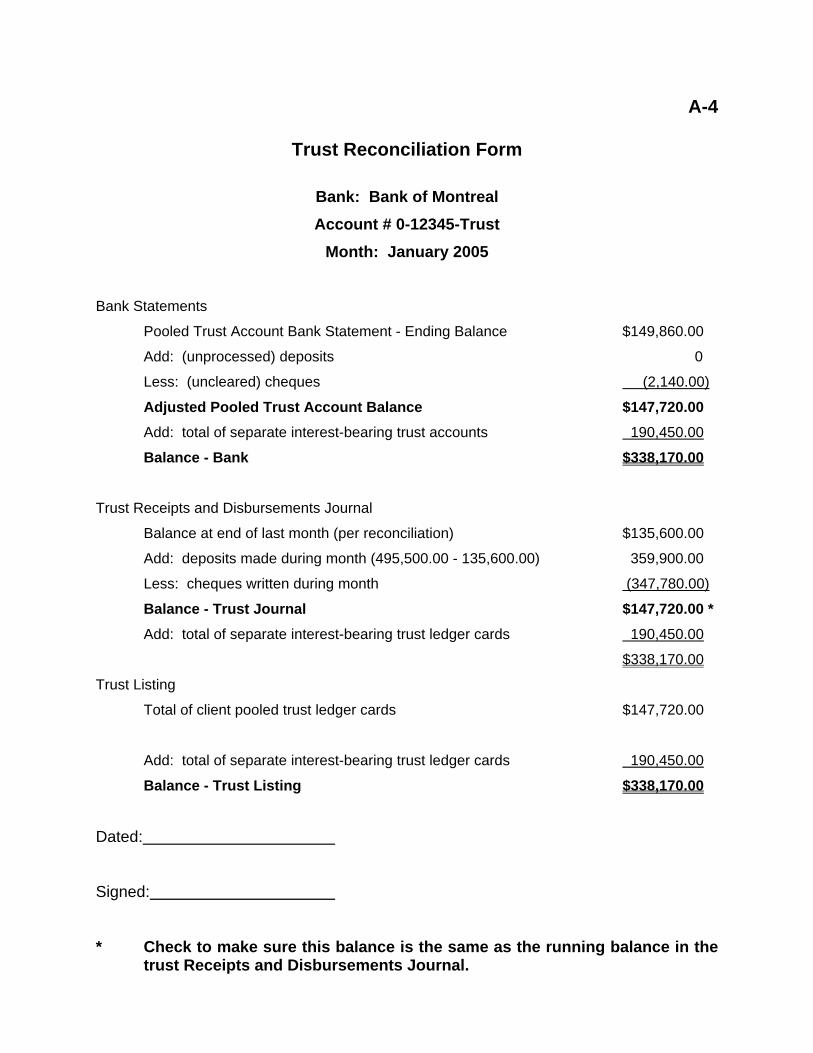

A-4

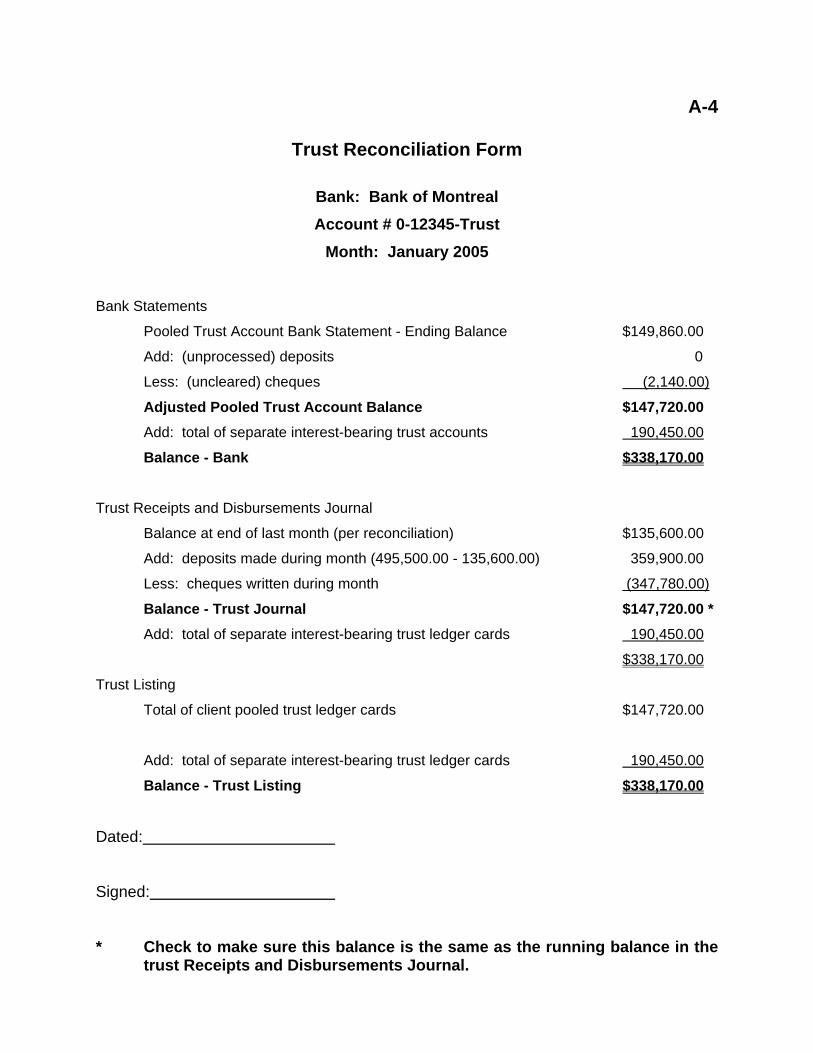

Trust Reconciliation Form

Bank: Bank of Montreal Account # 0-12345-Trust

Month: January 2005 Bank Statements

Pooled Trust Account Bank Statement - Ending Balance $149,860.00

Add: (unprocessed) deposits 0

Less: (uncleared) cheques (2,140.00)

Adjusted Pooled Trust Account Balance $147,720.00 Add: total of separate interest-bearing trust accounts 190,450.00

Balance - Bank $338,170.00

Trust Receipts and Disbursements Journal

Balance at end of last month (per reconciliation) $135,600.00

Add: deposits made during month (495,500.00 - 135,600.00) 359,900.00

Less: cheques written during month (347,780.00)

Balance - Trust Journal $147,720.00 * Add: total of separate interest-bearing trust ledger cards 190,450.00

$338,170.00

Trust Listing

Total of client pooled trust ledger cards $147,720.00

Add: total of separate interest-bearing trust ledger cards 190,450.00

Balance - Trust Listing $338,170.00

Dated:

Signed:

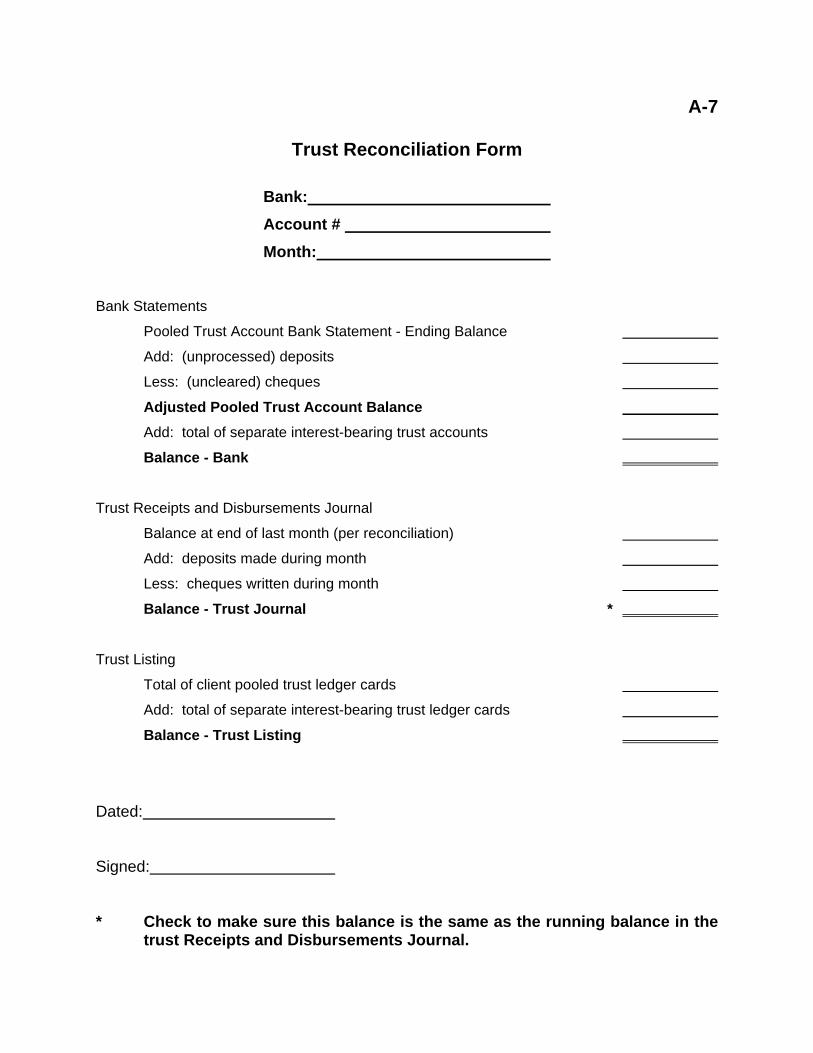

* Check to make sure this balance is the same as the running balance in the trust Receipts and Disbursements Journal.

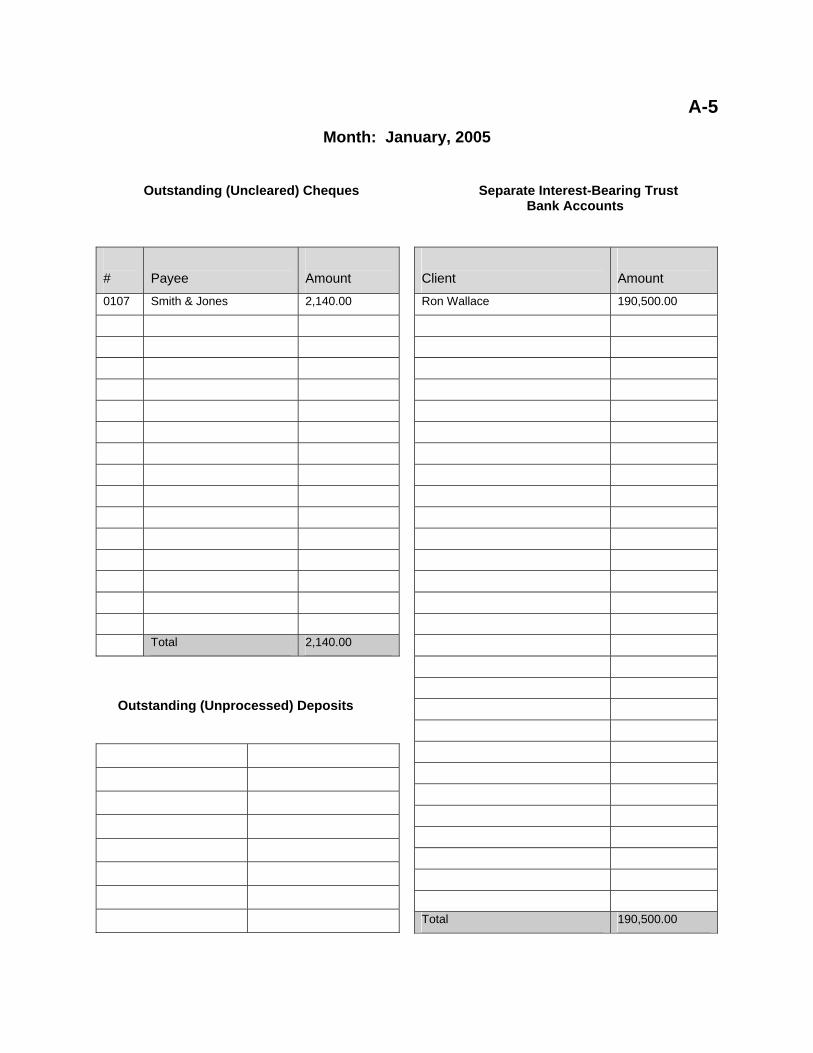

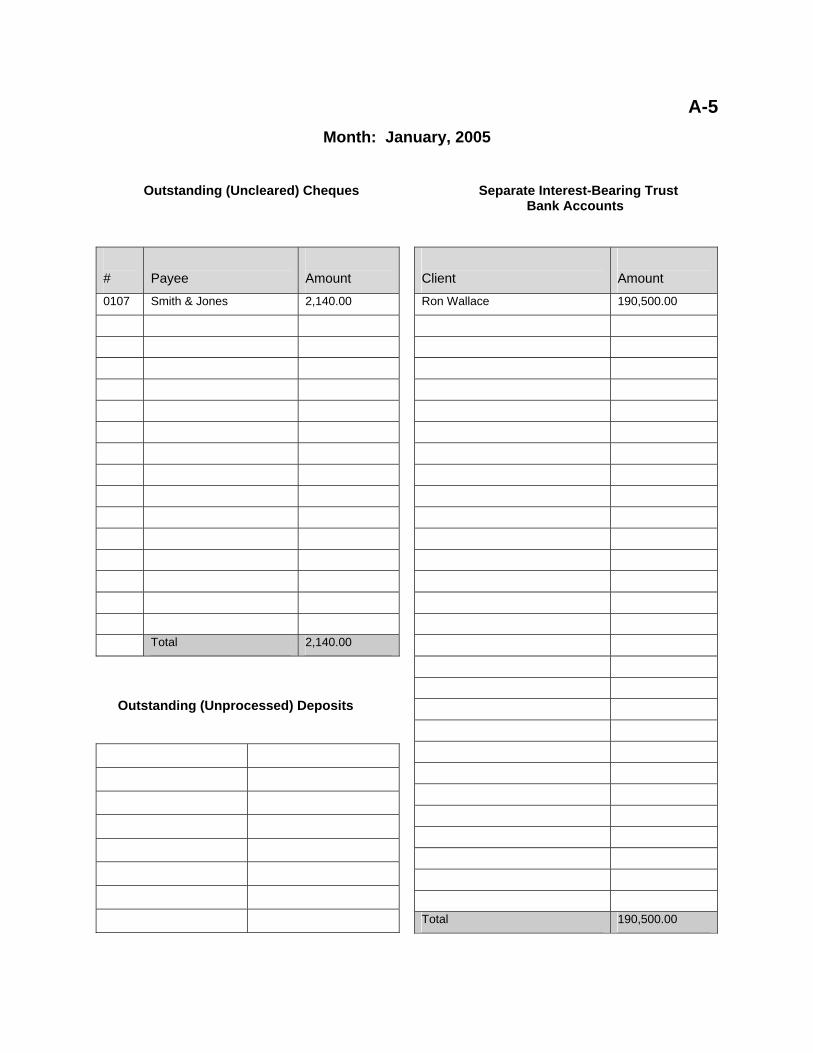

A-5 Month: January, 2005

Outstanding (Uncleared) Cheques Separate Interest-Bearing Trust Bank Accounts

#

Payee

Amount

0107 Smith & Jones 2,140.00

Total 2,140.00

Outstanding (Unprocessed) Deposits

Client

Amount

Ron Wallace 190,500.00

Total 190,500.00

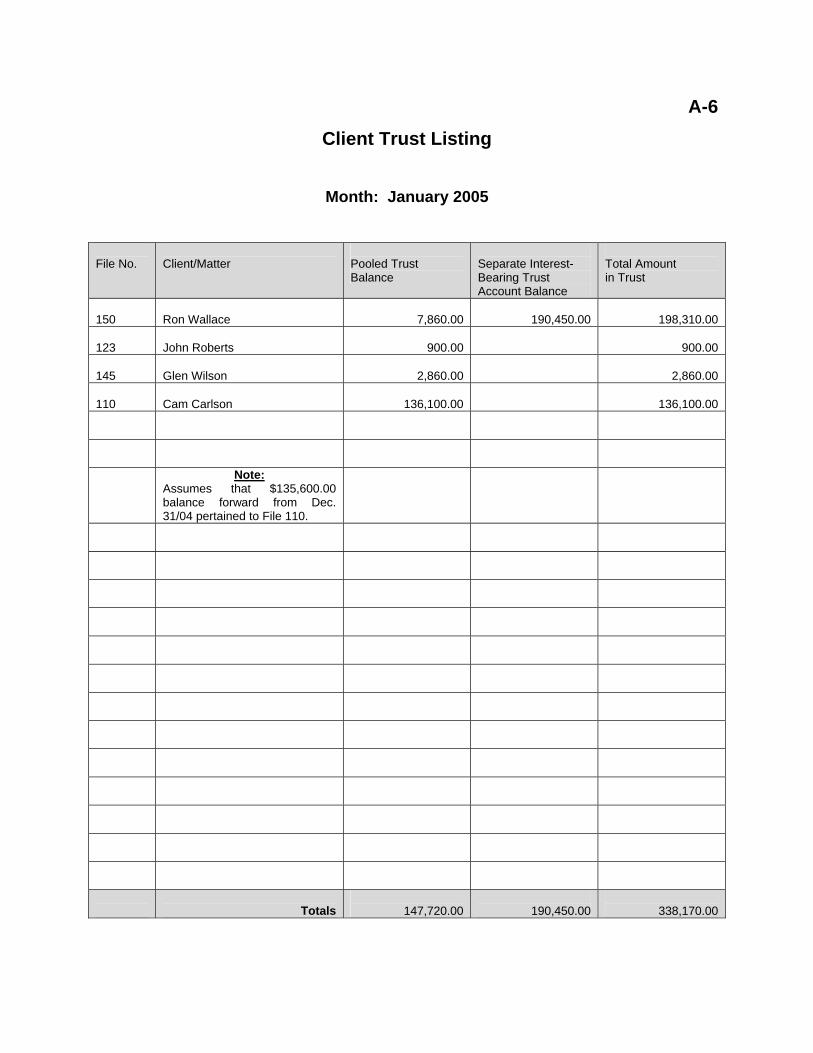

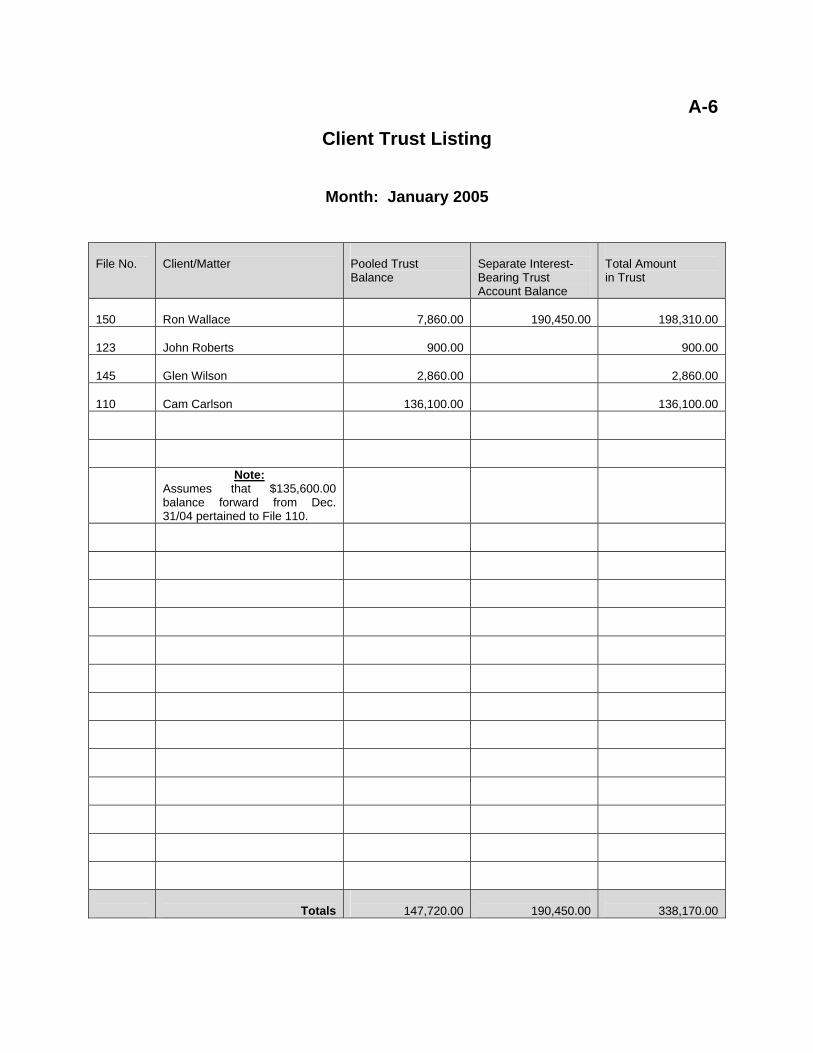

A-6 Client Trust Listing

Month: January 2005 File No.

Client/Matter

Pooled Trust Balance

Separate Interest- Bearing Trust Account Balance

Total Amount in Trust

150

Ron Wallace

7,860.00

190,450.00

198,310.00

123

John Roberts

900.00

900.00

145

Glen Wilson

2,860.00

2,860.00

110

Cam Carlson

136,100.00

136,100.00

Note: Assumes that $135,600.00 balance forward from Dec. 31/04 pertained to File 110.

Totals

147,720.00

190,450.00

338,170.00

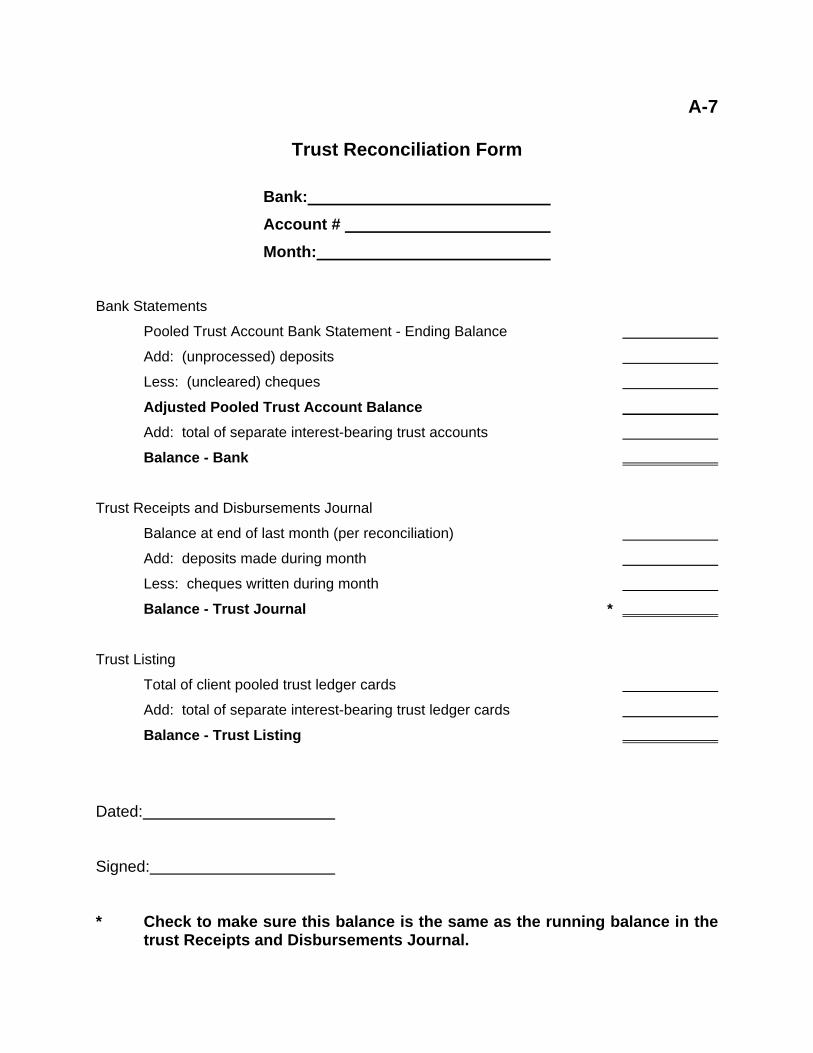

A-7

Trust Reconciliation Form

Bank: Account # Month:

Bank Statements

Pooled Trust Account Bank Statement - Ending Balance

Add: (unprocessed) deposits

Less: (uncleared) cheques

Adjusted Pooled Trust Account Balance

Add: total of separate interest-bearing trust accounts

Balance - Bank

Trust Receipts and Disbursements Journal

Balance at end of last month (per reconciliation)

Add: deposits made during month

Less: cheques written during month

Balance - Trust Journal * Trust Listing

Total of client pooled trust ledger cards

Add: total of separate interest-bearing trust ledger cards

Balance - Trust Listing

Dated:

Signed:

* Check to make sure this balance is the same as the running balance in the trust Receipts and Disbursements Journal.

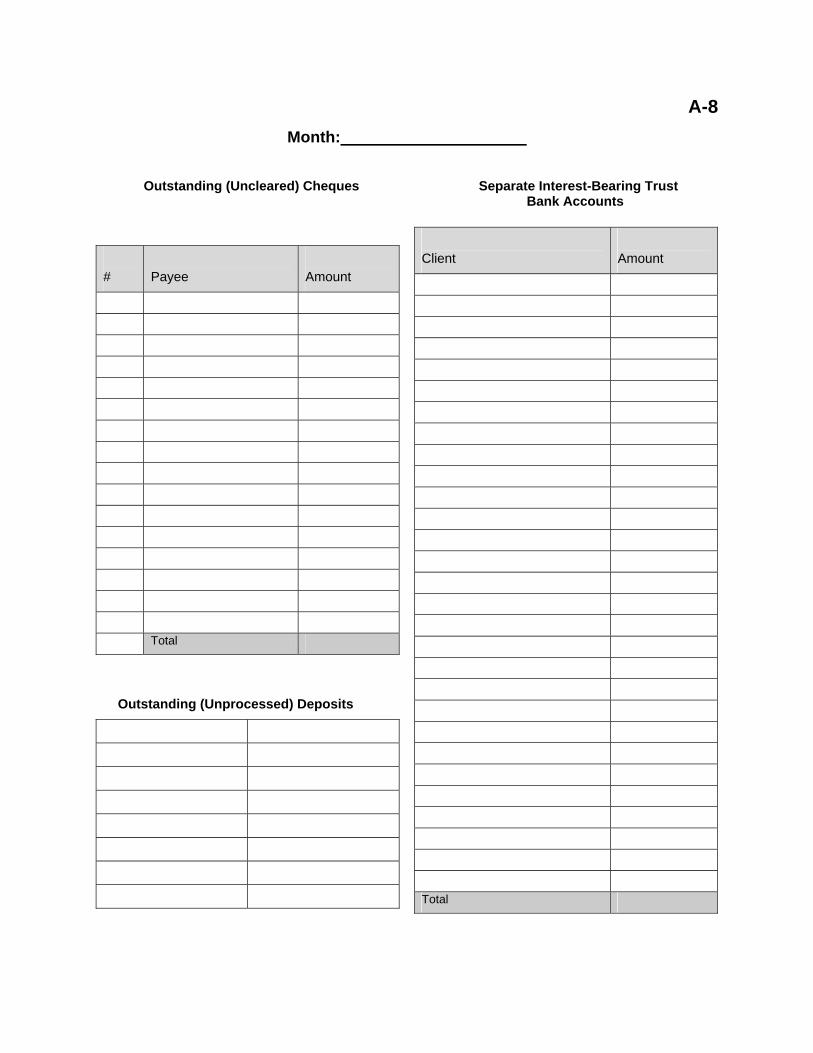

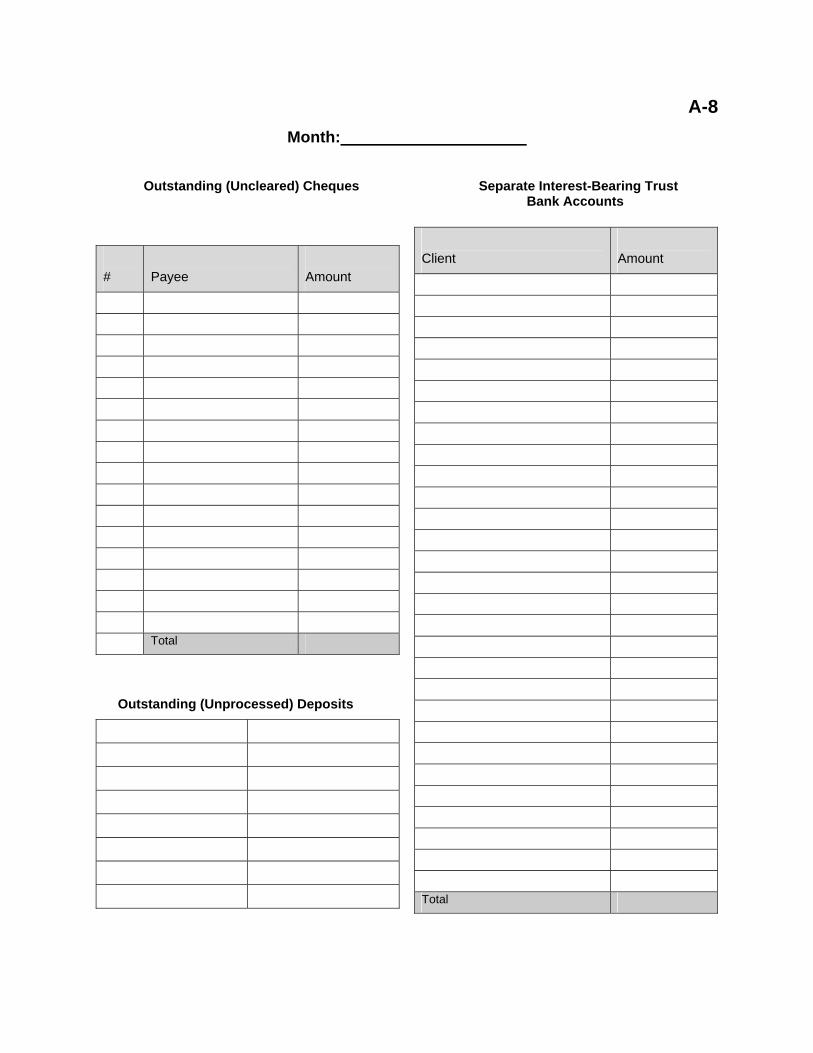

A-8 Month:

Outstanding (Uncleared) Cheques Separate Interest-Bearing Trust Bank Accounts

#

Payee

Amount

Total

Outstanding (Unprocessed) Deposits

Client

Amount

Total

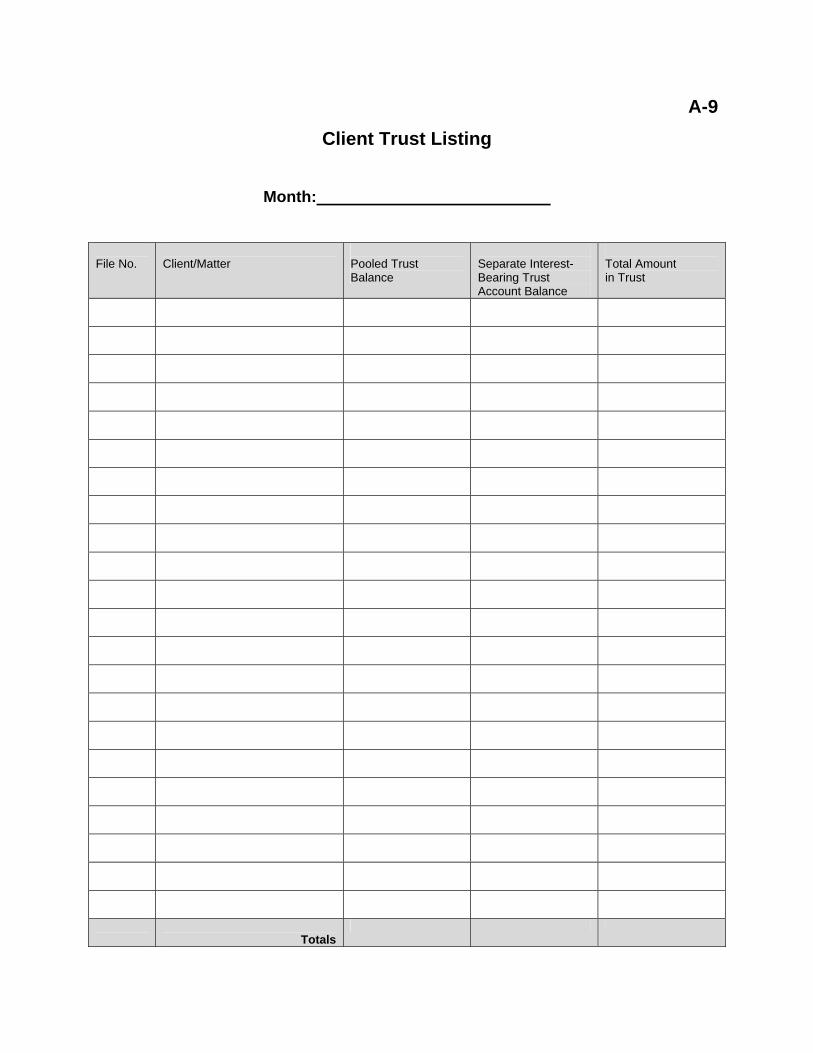

A-9 Client Trust Listing

Month: File No.

Client/Matter

Pooled Trust Balance

Separate Interest- Bearing Trust Account Balance

Total Amount in Trust

Totals

A-2

SMITH & JONES LAW OFFICE

Trust Journal Entry Descriptions

Line #1 - Balance Forward - $135,600.00 This amount is carried forward from the “Pooled Trust - Balance” column at the end of December 31, 2004. This amount is also the same as the balance on the bank reconciliation @ December 31, 2004. This amount is entered as a debit to bank and also entered in the “Pooled Trust Balance” column. Line #2 - John Roberts - $19,400.00 Entry to record receipt #1245 for $19,400.00 received from John Roberts re file #123. Line #3 - Dawn Davies - $18,500.00 Entry to record cheque #C0102 for $18,500.00 to Dawn Davies re file #123. Line #4 - Bank of Montreal - $100,000.00 Entry to record cheque #C0103 for $100,000.00 to Bank of Montreal to establish a Separate Interest Bearing Account (SIBA) for Cam Carlson. It should be noted that these funds would have been included as part of the $135,600.00 carry forward amount. The $100,000.00 amount is also entered in the SIBA column with a corresponding identifier of “Cam Carlson #110”. Line #5 - Glen Wilson - $40,000.00 This entry records receipt #1246 for $40,000.00 from Glen Wilson re file #145. Line #6 - Revenue Canada - $36,000.00 Entry to record cheque #C0104 to Revenue Canada relating to file #145. Line #7 - Smith & Jones Law - $1,140.00 This cheque was written to Smith & Jones for $1,140.00 in payment of invoice #0107 pertaining to file #145. Line #8 - Ron Wallace - $75,000.00 This entry records receipt #1247 from Ron Wallace in regard to file #150. Line #9 - CIBC - $125,000.00 This entry shows money coming in from CIBC per receipt #1248 pertaining to file #150.

Line #10 - Bank of Montreal - SIBA - $190,000.00 Monies received relating to file #150 are invested in a SIBA. The $190,000.00 amount invested is also entered in the SIBA column with the description of Ron Wallace #150. It should be noted that $200,000.00 was received into the pooled trust account relating to Ron Wallace file #150 with only $190,000.00 being invested in the SIBA. There is therefore $10,000.00 remaining in the pooled trust account pertaining to file #150 that is conveniently available to meet upcoming requirements. Line #11 - Bank of Montreal - SIBA - $500.00 This entry is made based on information received from the bank indicating that $500.00 was paid into the SIBA of Cam Carlson as interest on January 31, 2005. In reality, this may be identified on the bank statement or by a bank inquiry but may not be entered until the following month due to the timing of receipt of information. It should also be noted that since this amount was added directly to the SIBA balance, a receipt is not prepared by the law firm. Line #12 - Bank of Montreal - Close SIBA account - $100,500.00 This entry records the closing of the SIBA for Cam Carlson on January 31, 2005. It should be noted that cheques are not allowed to be written on a SIBA and therefore funds must be transferred to the pooled trust account based on instructions from the lawyer. Line #13 - Interest - SIBA - $450.00 This entry records interest of $450.00 credited to the SIBA for Ron Wallace. In reality, this entry may not be made until the following month when statements are received from the bank. Line #14 - Smith & Jones Law - $2,140.00 This entry records cheque #C0107 to Smith & Jones Law Office for services rendered as described on invoice #0108. If a general ledger is used (recommended), the total of each column must be entered (posted) to accounts set up by category (i.e. totals from trust bank columns to the trust bank account; total from SIBA to SIBA account, etc.). Note: If a general ledger is used, carry forward amounts in the daily journal must be subtracted before posting column totals to the general ledger.

A-3

Trust Reconciliation Checklist 1. Bank Statements Balance 1.1 Verify the pooled trust bank statement. If the statement contains debit memos or other unauthorized withdrawals from trust, arrange for bank to reverse them immediately and document the problem and the steps taken to correct it. If this has resulted in a trust shortfall greater than $100.00, the Executive Director of the Law Society must be advised in writing.

► Check amounts on cashed cheques to amounts on the bank statement and the amounts recorded in the bank column in the daily trust journal and track down any discrepancies.

► Check the deposit amounts shown on the statement against the deposit slips and track down any discrepancies.