h1 2016 analyst & investor presentation - easyjet plc/media/files/e/easyjet/...h1 2016 analyst...

TRANSCRIPT

H1 2016 Analyst & investor

presentation

Tuesday 10 May 2016

Introduction

Carolyn McCall

Chief Executive Officer

3 3

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet’s resilient model continues to deliver

Robust performance despite the impact from external shocks

Continued focus on building strong network positions

Increased revenue and passenger growth at stable load factors

Strong cost performance secured flat PBT and PBT margin at constant currency

Capital structure review delivers proposed 50% payout ratio

Strong H1 performance despite shocks

3

Financial review

Andrew Findlay

Chief Financial Officer

5 5

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Financial performance

H1 2016 H1 2015 Change* Change*

£m £m % % @ CC

Total revenue 1,771 1,767 0.3% 2.9%

Fuel (462) (516) 10.5% 9.7%

Costs excluding fuel (1,333) (1,244) (7.2%) (7.9%)

(Loss) / profit before tax (24) 7

Profit before tax at constant currency 5 7

EBITDAR 111 130 (14.8%) 9.3%

EBITDAR margin 6.2% 7.3%

Earnings per share (pence) (5.1) 1.3

*Favourable / (adverse)

** Profit before tax at constant currency after balance sheet revaluations

5

**

6 6

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Revenue performance

H1 2016 H1 2015 Change*

Seats flown (m) 34.5 32.2 7.4%

Load factor (%) 89.7% 89.7% 0.0ppt

Passengers (m) 31.0 28.9 7.4%

Average sector length (km) 1,054 1,072 (1.7%)

Total revenue - reported (£m) 1,771 1,767 0.3%

Total revenue - constant currency (£m) 1,817 1,767 2.9%

Total revenue per seat - reported (£) 51.29 54.91 (6.6%)

Total revenue per seat - constant currency (£) 52.62 54.91 (4.2%)

6

* Favourable / (adverse)

7 7

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

1.48

0.72

1.04

0.48

0.47 1.33

Resilient revenue performance

Revenue per seat bridge

H1 2016

51.29

FX

Before FX

52.62

Other Easter Underlying softness

Sharm el-Sheikh Paris H1 2015

54.91

7

(2.7%)

(1.3%)

(1.9%)

(0.9%)

(0.9%)

8 8

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

A strong focus on costs

Total cost per seat bridge

0.48

0.72

0.39

0.77

0.130.28

0.54

2.47

0.38

51.98

P&L FX

Fuel Before movement in fuel and FX

54.93

Other cost savings

H1 2016 A320 mix Before management

action

56.42

54.70

Lean engineering

contract

Inflation* Balance sheet

revaluations

Disruption Regulated airports inflation

H1 2015

Management action

External factors

• Total cost per seat at constant currency: 4.3% decrease

• Cost per seat ex fuel at constant currency: 0.5% increase

* Operational price increases including unregulated airports, ground handling, navigation and crew costs

8

9 9

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Impact of fuel & currency

H1 2016 fuel impact favourable / (adverse) H1 2016 H1 2015

Fuel $ per metric tonne

Market rate 409 707

Effective price 786 925

US dollar rate

Market rate 1.48 1.55

Effective price 1.61 1.59

Actual cost of fuel £ per metric tonne 489 581

H1 2016 currency impact favourable / (adverse) EUR CHF USD Other Total

£m

Revenue (47) 2 1 (2) (46)

Fuel - - 4 - 4

Prior year balance sheet revaluations (3) 1 (2) - (4)

Costs excluding fuel and prior year balance sheet

revaluations18 (2) (2) (1) 13

Total (32) 1 1 (3) (33)

2 cents

92

Change

298

139

(7 cents)

9

10 10

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strong cash generation

10

2194121

314

45215

12392

80

23

Net working capital

31 March 2016

1,057*

Ordinary dividend

Before dividend

1,276

Depn & amort

Operating loss

1 October 2015

939*

Increased borrowings

Tax paid CAPEX Other FX Other operating

*Includes money market deposits but excludes restricted cash

• Net cash: £296m (FY15: £435m)

• Adjusted net debt: £474m (FY15: £363m)

Cash flow bridge

Cash generated from operations

(excl dividends): £461m

11 11

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strong balance sheet

£m H1 2016 H1 2015

Goodwill and other intangible assets 501 476

Property, plant and equipment 3,089 2,720

Derivative financial instruments (338) (281)

Other assets (excluding cash and money market deposits) 367 355

Unearned revenue (1,080) (1,091)

Other liabilities (excluding debt) (883) (856)

Capital employed 1,656 1,323

Cash and money market deposits 1,057 976

Debt (761) (560)

Net cash 296 416

Net assets 1,952 1,739

11

12 12

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Gross capital expenditure

c.£800mc.£850m

c.£900m

c.£650m

c.£550m

£0m

£500m

£1,000m

FY 2020 FY 2019 FY 2018 FY 2017 FY 2016 FY 2015

£536m

FY 2014

£449m

FY 2013

£421m

FY 2012

£392m

FY 2011

£556m

12

- Assumes base case fleet plan

13 13

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Capital Structure Review

• The scope of the review entailed:

A strong balance sheet is a core part of easyJet’s strategy and is fully aligned with shareholder interests

Liquidity buffer

Gearing

Residual Values

Dividend Policy

13

14 14

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Capital Structure Review – Key Changes

14

50% PAT dividend ratio

Current Position Updated Position

Liquidity buffer Cash position of £4 million per aircraft Liquidity buffer including cash and revolving credit facility

Cover peak unearned revenue

Minimum position of £2.6 million per 100 seats

Funding Mortgage funding secured on aircraft Unsecured funding via EMTN programme

Mortgage funding secured on aircraft

Revolving credit facility to support liquidity

Gearing Target gearing between 15% and 30% No specific gearing target

Intend to maintain current credit rating (subject to events

outside easyJet’s control)

Residual Value Downside flexibility through leasing arrangements

Move from 70/30 owned vs leased split to 80/20 to

reduce ownership costs

Rolling sale and leaseback programme on A319 fleet

No material change to 80/20 fleet mix outcome

Downside flexibility maintained

Hedging Semi-active fuel and foreign exchange hedging

Simple forward contracts

No change

Dividend 40% payout ratio of post-tax income Increase in payout ratio to 50% of post-tax

income

Board to keep Balance sheet under review

Business Review

Carolyn McCall

Chief Executive Officer

16 16

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

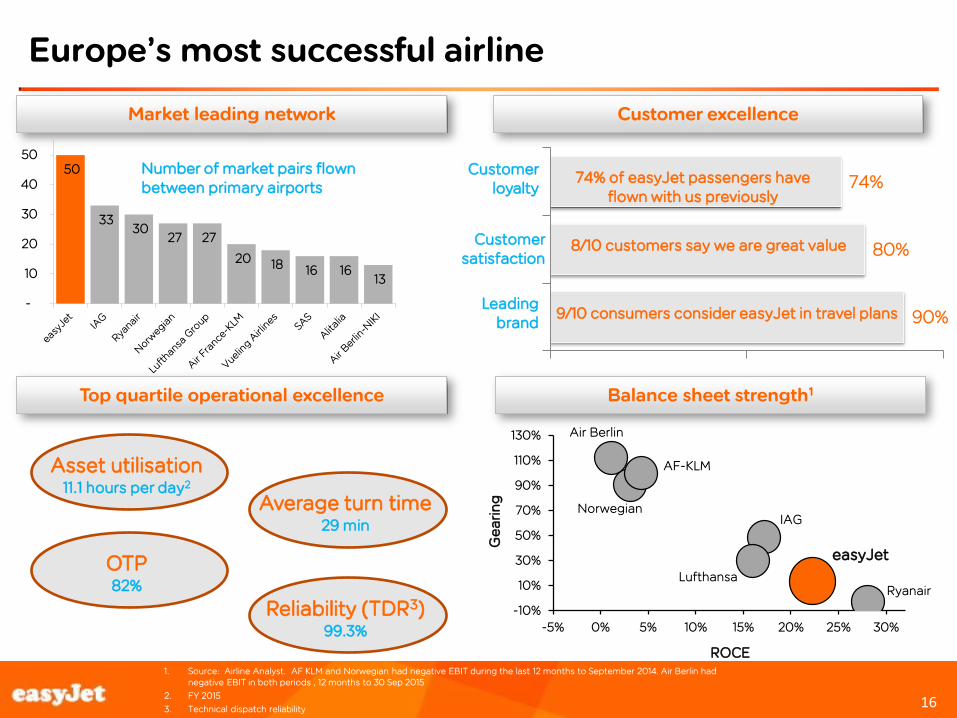

Europe’s most successful airline

1. Source: Airline Analyst. AF KLM and Norwegian had negative EBIT during the last 12 months to September 2014. Air Berlin had negative EBIT in both periods , 12 months to 30 Sep 2015

2. FY 2015

3. Technical dispatch reliability

16

50

33 30

27 27

20 18 16 16 13

-

10

20

30

40

50Number of market pairs flown between primary airports

-10%

10%

30%

50%

70%

90%

110%

130%

-5% 0% 5% 10% 15% 20% 25% 30%

Ge

ari

ng

ROCE

Market leading network

Balance sheet strength1 Top quartile operational excellence

Ryanair

IAG

AF-KLM

Air Berlin

Norwegian

Lufthansa

easyJet

Customer excellence

90%

80%

74%

9/10 consumers consider easyJet in travel plans

8/10 customers say we are great value

74% of easyJet passengers have flown with us previously

Leading brand

Customer satisfaction

Customer loyalty

Asset utilisation 11.1 hours per day2

OTP 82%

Reliability (TDR3) 99.3%

Average turn time 29 min

17 17

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet - Delivering growth and returns to shareholders

17

Growth

Margin

Returns

• Passenger growth of 7%-8% CAGR

• Top quartile ROCE

• 50% PAT pay-out ratio

• Stable margin

• Strong cost underpin

18 18

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Resilient H1 trading Growth

Flow Trading

UK- Beach

Paris touching

Sharm el Sheikh

touching

UK – Ski

City – City

Trading by traffic flow

18

19 19

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet Air France

Ryanair KLM

Vueling British

Thomson Monarch

Alitalia other

7.4% easyJet capacity growth over winter

United Kingdom +9.4%

France +6.5 %

Italy 11.7%*

Spain +4.5%

Switzerland +8.1%

Germany +7 %

Source : OAG, scheduled data and Internal easyJet projection April 2016. Country capacity growth is based on network touching seats. * Excludes Rome capacity

Investment in the network in H1

9% 7%

4%

7%

9% 12%

5%

12%

8% 5%

7% 5%

Market growth easyJet growth in the market Netherlands +27%

7%

27%

Portugal +21.3%

12%

21%

Growth

19

Market share on easyJet routes

20 20

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Depth in high GDP markets

1) Catchment areas defined as population living within 50km of airports within the market and ranked according to GDP for that area; 2) Rank of short haul capacity for the 12 months to September 2015; 3) Manchester catchment includes Liverpool airport; 4) Dusseldorf catchment includes Cologne, Dortmund, Friedrichshafen, Nuremburg and Paderborn; 5) Zurich catchment includes Basel

20

easyJet network

- Number 1 or 2 position in the primary airport in 12 of Europe’s top 25 catchment areas by GDP1

Growth

21 21

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

1) Based on theoretical max runway capacity at airport, Peak = first wave departures (before 8.30am) on weekdays in IATA Summer season . For leisure destinations may also include weekend peak demand periods

2) Based on summer 2016 schedule

Airport Current morning peak utilisation? 1

easyJet touching aircraft2

London Gatwick 69

Geneva 20

Bristol 14

Luton 21

Basel 14

Manchester 12

Schiphol 13

Milan Malpensa 22

Edinburgh 11

Belfast 9

A network that is difficult to replicate

>90% utilised 80-90% utilised

Growth

Strong positions at key airports Increasing frequencies

<80% utilised

21

0

1

2

3

4

5

6

1-2 2-3 3-4 4-5 5-6 6-7

We

ekl

y F

req

ue

nc

y A

dd

itio

n Y

oY

Number of Daily Flights

Average Topups Per Week

Average

For flights previously with at least a daily frequency, easyJet added YoY on average 1.2 frequencies per week.

22 22

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Investing in our network

Deepening the network New bases

22

Growth

Venice Marco Polo London Luton

Amsterdam Schiphol

23 23

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Leading in digital

23

Growth

24 24

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Leading in data

FLIGHT CLUB

24

Growth

25m marketable customers

74% returning customers

41.5 average age

25 25

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Grow revenue

25

Growth

26 26

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

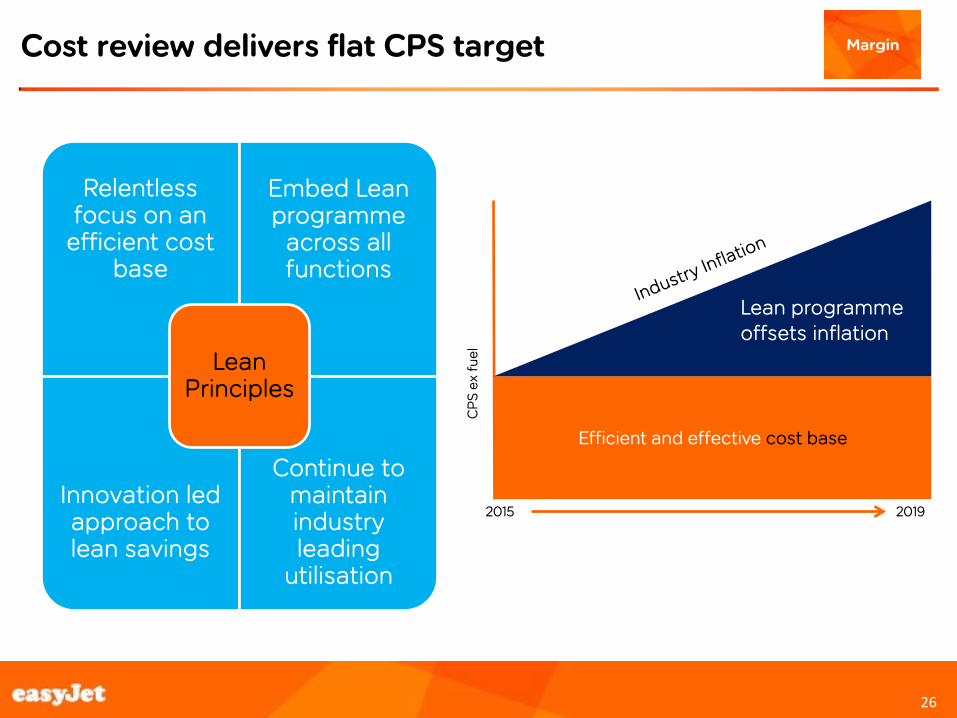

Cost review delivers flat CPS target

26

Margin

Efficient and effective cost base

Lean programme offsets inflation

CP

S e

x fu

el

Relentless focus on an

efficient cost base

Embed Lean programme

across all functions

Innovation led approach to lean savings

Continue to maintain industry leading

utilisation

Lean Principles

2015 2019

27 27

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Strong pipeline of cost saving initiatives

27

Margin

Focus area Savings*

Airports & ground handling (eg: LGW) £ £ £

Supplier relationship management £ £

Maintenance efficiency £ £ £

Fleet up-gauging £ £ £

Lean bases & smart scheduling £ £

Invest in people £

Detailed focus on overheads £ £

IT investment £ £

Use of data to drive efficiency £

Lean Target - Flat CPS ex-fuel between 2015-2019

• *Size of savings – More £ signs means larger saving • Lean target assumes pre abnormal levels of disruption •

Porto Barcelona

Maintenance

Ground handling

28 28

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Up-gauging our fleet

28

Margin

Up-gauging delivering CPS savings

156 seats 186 seats

Current generation

A319

New generation A320neo

13% -14%

New A320 cabin, 186 seats

- CPS savings based on fuel price quoted in original plan

29 29

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Operational excellence

29

Increased customer satisfaction

Greater operational efficiency

Delivering cost savings (single ground handling fleet)

Margin

30 30

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Outlook in 2016

Capacity (seats flown) • H2 c.+6.5% (before disruption)

• FY c.+7% (before disruption)

Revenue per seat at constant currency • Q3 revenue per seat: down c. 7%

• H2 revenue per seat: down low to mid single digits

Cost per seat at constant currency • FY cost per seat excluding fuel: down c. 1% (assuming normal levels of disruption)

FX • H2: c.£20 million adverse movement from foreign exchange rates

• FY: c.£55 million adverse movement from foreign exchange rates

Fuel • H2: unit fuel costs £85 million to £90 million favourable

• FY: unit fuel costs £170 million to £180 million favourable

• Expected total fuel cost £1,120 million

Rates at 9 May 2016 £/USD: 1.4390; £/EUR: 1.2635 Unit fuel guidance based on Jet fuel trading range of $350 / metric tonne to $450 / metric tonne

30

31 31

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyJet is a structural winner

• Europe's best network that is difficult to replicate

• Best customer proposition

• Constant innovation to drive demand and loyalty

• Cost plan to deliver flat CPS ex-fuel

• 50% profit after tax pay-out ratio

31

Q & A

appendix

34 34

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Fuel and foreign exchange hedging

Sensitivities – FY16

• $10 per tonne change in fuel price will impact the full year pre-tax result by +/- $1.5 million

• One cent movement in the £/$ will impact the full year pre-tax result by +/- £1.3 million

• One cent movement in the £/€ will impact the full year pre-tax result by +/- £0.6 million

Fuel

requirement US dollar

requirement Euro surplus CHF surplus

Six months ending 30 September 2016

87% at $793/ metric tonne

76% at $1.61/£ 79% at €1.25/£ 73% at CHF1.46/£

Full year ending 30 September 2016

87% at $814/ metric tonne

80% at $1.62/£ 86% at €1.23/£ 81% at CHF1.46/£

Full year ending 30 September 2017

76% at $626 / metric tonne

70% at $1.53/£ 71% at €1.32/£ 68% at CHF1.42/£

As at 6 May 2016 34

35 35

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

H2 forward bookings

% seats sold *

H2 (April 2016 to September 2016) as at 6 May 2016

H2 bookings in line with prior year

35

Apr May Jun Jul Aug Sep H2

Summer '15 Summer '16

36 36

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

easyjet

Ryanair Vueling

BA

AF-KLM

Other

Competitive capacity environment in H2

Source: Market capacity data from OAG scheduled data, as at 6 May 016 easyJet markets based on internal easyJet definition. easyJet growth based on H2 2016 schedule vs H2 2015 flown capacity

Short-haul market easyJet city to city pairs

7.6% split by carrier

36

5.6%

6.3% 6.3% 6.4%

5.4%

6.5%

8.2%

7.6%

Capacity change total SHMarket

easyJet capacity change Competitors on easyJetmarkets

Capacity Change easyJetmarkets

Summer 15 Summer 16

37 37

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Overall c. 6.6% capacity growth over summer

United Kingdom +6%

France +10 %

Italy 0%

Spain +6% Switzerland +5%

Germany +2 %

Source : OAG, scheduled data and Internal easyJet projection April 2016. Country capacity growth is based on network touching seats.

Investment in the network

6% 8%

5%

10%

6%

0%

6% 10%

5%

0%

2% 5%

Market growth easyJet growth in the market

Netherlands +21%

7%

21%

Portugal +15%

14% 15%

37

38 38

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Profit before tax

Profit before tax per seat bridge

0.16

0.48

0.21

0.72

0.39

Underlying softness

Lean engineering

contract

A320 Mix

0.38

Disruption

0.28

Cost inflation*

0.77

Balance sheet

revaluations

0.13

Fuel

2.47

Regulated airports inflation

0.54

Other revenue

0.47

0.69

H1 2016 P&L Fx

0.85

H1 2016 @ CC

Other cost savings

1.04

Paris and Sharm

el-Sheikh

2.20

Easter H1 2015

* Operational price increases including unregulated airports, ground handling, navigation and crew costs

Revenue

Costs

39 39

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Loss after tax

39

£m H1 2016 H1 2015 Change

(Loss) / profit before tax (24) 7 (31)

Tax credit / (charge) 4 (2) (6)

(Loss) / profit after tax (20) 5 (25)

Effective tax 18.1% 20.4% 2.3ppt

40 40

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Revenue per seat

£ per seat H1 2016 H1 2015 Change

Seat revenue 50.39 54.05 (6.8%)

Non-seat revenue 0.90 0.86 4.6%

Total revenue 51.29 54.91 (6.6%)

40

41 41

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

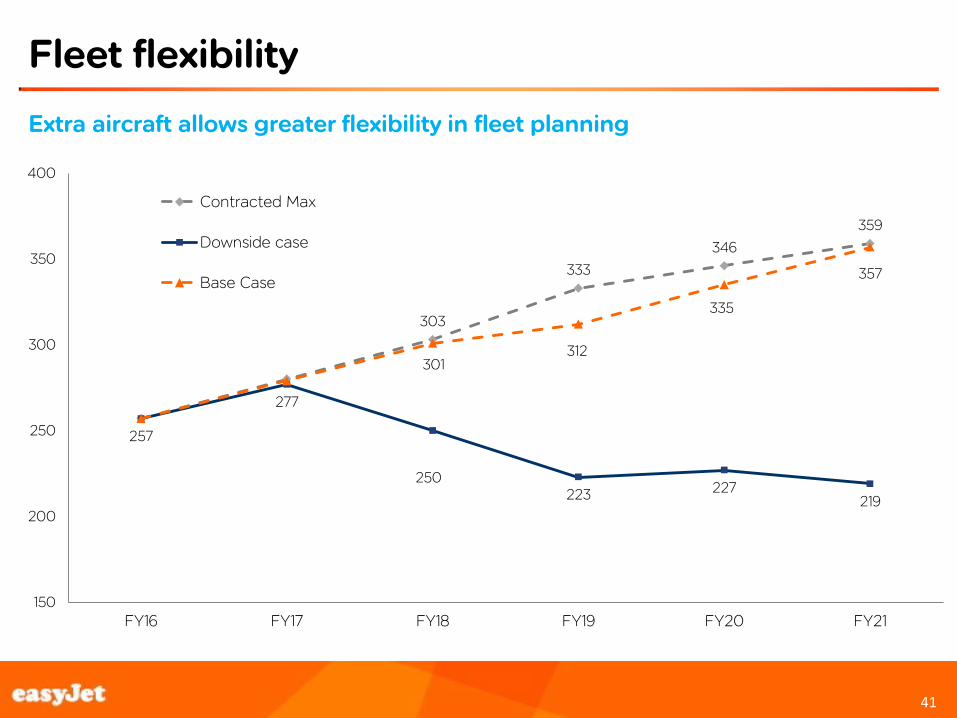

Fleet flexibility

Extra aircraft allows greater flexibility in fleet planning

303

333

346

359

257

277

250 223 227

219

301 312

335

357

150

200

250

300

350

400

FY16 FY17 FY18 FY19 FY20 FY21

Contracted Max

Downside case

Base Case

41

42 42

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Cost per seat excluding fuel - key drivers

42

* Excludes foreign exchange gains and losses on balance sheet revaluations

Cost

per seat

excluding fuel

Variance at

constant

currency

Variance at

constant

currency

Weighting of

variance

£ £ % %

• Efficiency gained from upgauging our fleet

from an average of 164 to 166 seats per

aircraft

• Decrease in average sector length

• Improved crew scheduling

• Offset by pay increases

• Reduction in number of leased aircraft in the

fleet

• Savings from new maintenance contract

• Offset by Inflationary increases

Overhead 5.46 (0.14) (2.8%) (0.4%) • Higher disruption costs

• Rate increases and investment in ground

handling at Gatwick

• Offset by volume savings and savings from

new contracts

Navigation 3.91 0.01 0.4% - • Decrease in average sector length

• Depreciation on new aircraft purchased

• Offset against decreasing lease costs

38.68 (0.18) (0.5%) (0.5%)

Net Exchange (gains)/losses (0.07)

Total CPS excluding fuel 38.61

Airports and Ground handling 14.88

Ownership ex revaluations* 3.96 -

(0.19) (0.5%)

0.3%

0.6%

- -

7.25

3.22

1.6%

Drivers

(1.3%)

Crew 0.12

Maintenance 0.02 0.1%

43 43

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Increasing proportion of A320’s

43

H1 2016 H1 2015 Change

A319 (operating lease) 45 50 (5)

A319 (owned / finance lease) 99 99 0

A319 Total 144 149 (5)

A320 (operating lease) 18 18 0

A320 (owned / finance lease) 85 63 22

A320 Total 103 81 22

Total fleet 247 230 17

Percentage unencumbered 52% 44% 8ppt

Percentage operating lease 26% 30% -4ppt

Percentage of A320s in fleet 42% 35% 7ppt

Average seats per aircraft 166 164 1.0%

44 44

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

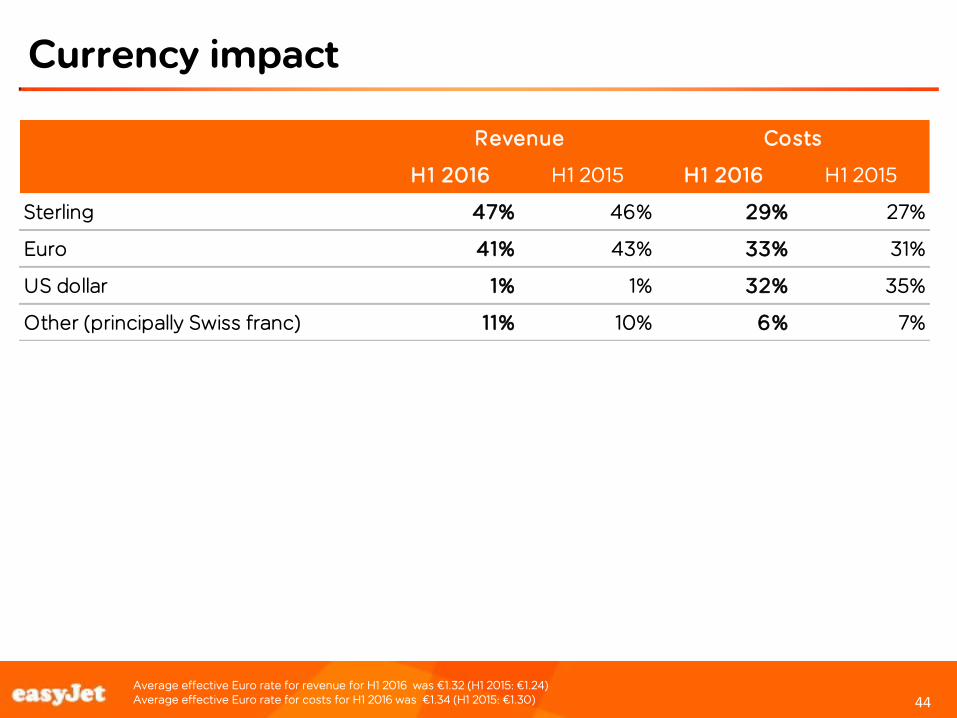

Currency impact

Average effective Euro rate for revenue for H1 2016 was €1.32 (H1 2015: €1.24) Average effective Euro rate for costs for H1 2016 was €1.34 (H1 2015: €1.30)

44

H1 2016 H1 2015 H1 2016 H1 2015

Sterling 47% 46% 29% 27%

Euro 41% 43% 33% 31%

US dollar 1% 1% 32% 35%

Other (principally Swiss franc) 11% 10% 6% 7%

Revenue Costs

45 45

Footer box on intersect of lines line h=8.03 9 and v=8.75 with font 10pt Arial not bold

Disclaimer

Certain statements in this presentation constitute or may constitute forward-looking statements. Any statement in this presentation that is not a statement of historical fact including, without limitation, those regarding the Company’s future expectations, operations, financial performance, financial condition and business is or may be a forward-looking statement. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those projected or implied in any forward-looking statement. These risks and uncertainties include, among other factors, changing economic, financial, business or other market conditions. These and other factors could adversely affect the outcome and financial effects of the plans and events described in this presentation. As a result, you are cautioned not to place any reliance on such forward-looking statements. The forward-looking statements reflect knowledge and information available at the date of this presentation and the Company undertakes no obligation to update its view of such risks and uncertainties or to update the forward-looking statements contained herein. Nothing in this presentation should be construed as a profit forecast or profit estimate and no statement in this presentation should be interpreted to mean that the future earnings per share of the Company for current or future financial years will necessarily match or exceed the historical or published earnings per share of the Company.

This communication is directed only at (i) persons having professional experience in matters relating to investments who fall within the definition of “investment professionals” in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001; or (ii) high net worth bodies corporate, unincorporated associations and partnerships and trustees of high value trusts as described in Article 49(2) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001. Persons within the United Kingdom who receive this communication (other than those falling within (i) and (ii) above) should not rely on or act upon the contents of this communication. Nothing in this presentation is intended to constitute an invitation or inducement to engage in investment activity for the purposes of the prohibition on financial promotion contained in the Financial Services and Markets Act 2000.

This presentation has been furnished to you solely for information and may not be reproduced, redistributed or passed on to any other person, nor may it be published in whole or in part, for any other purpose.

This presentation does not constitute or form part of, and should not be construed as, an offer for sale or subscription of, or solicitation of any offer to buy or subscribe for, any securities of easyJet plc (“easyJet”) in any jurisdiction nor should it or any part of it form the basis of, or be relied on in connection with, any contract or commitment whatsoever. This presentation does not constitute a recommendation regarding the securities of easyJet. Without limitation to the foregoing, these materials do not constitute an offer of securities for sale in the United States. Securities may not be offered or sold into the United States absent registration under the US Securities Act of 1933 or an exemption there from.

easyJet has not verified any of the information set out in this presentation. Without prejudice to the foregoing, neither easyJet nor its associates nor any officer, director, employee or representative of any of them accepts any liability whatsoever for any loss however arising, directly or indirectly, from any reliance on this presentation or its contents.

This presentation is not being issued, and is not for distribution in, the United States (with certain limited exceptions in accordance with the US Securities Act of 1933) or in any jurisdiction where such distribution is unlawful and is not for distribution to publications with a general circulation in the United States.

By attending or reading this presentation you agree to be bound by the foregoing limitations.

45