h1 economic review 2015-quka consulting

TRANSCRIPT

QUKA CONSULTING ECONOMIC REVIEW

“IDEAS, INSIGHT & INNOVATION”

2015 MID-YEAR ANALYSIS: H1

VOLUME 1: 1

Quka Consulting: Ideas, Insight & Innovation © 2015

CONTENTS

Global Economy

Local Economy

Forecast

Quka Consulting: Ideas, Insight & Innovation © 2015

GLOBAL ECONOMY

US INTEREST RATE POLICY

GLOBAL COPPER

GLOBAL OIL

Quka Consulting: Ideas, Insight & Innovation © 2015

US INTEREST RATE HIKE: GLOBAL EFFECT

The last Fed hike was in 2004.Federal Reserve Chief Janet Yellen said in Mid July 2015 she expects to raise interest rates in 2015 after seven years of unprecedented easy money helped the economy shake the financial crisis and recession. Consensus currently estimates that this will happen in September

US Treasuries which are a safe haven for investors will become more attractive increasing US treasury demand. This will cause a stronger dollar

Most commodities are quoted in Dollars. They include, Gold, copper, Oil among many others. A rate hike will make the dollar stronger which will make these commodities more expensive on the global market which will dampen their demand.

Source: US Federal Reserve Bank

Quka Consulting: Ideas, Insight & Innovation © 2015

Brazil, Turkey and South Africa will likely have a tough time in the second half of 2015 because money will flow toward the U.S. This applies to other emerging markets; Zambia falls in this

bracket as well.

The hike in US Fed rate will make the dollar strong; hence the Kwacha will depreciate against the dollar.

Copper, which accounts for over 70% of Zambia’s forex earning will be hit by a stronger dollar which will make copper expensive and dampen global demand. This will hit Zambia’s trade

deficit hard at least in the short term.

The double whammy here also includes the effect of a weaker Kwacha in Zambia’s oil import bill, which directly affects Zambia’s inflation rate.

If September is indeed the month in which the US fed raises rates then Zambia and other emerging markets need to brace themselves for a tough time.

US INTEREST RATE HIKE: ZAMBIA EFFECT

Quka Consulting: Ideas, Insight & Innovation © 2015

LOWER COPPER PRICES DUE TO LOWER GLOBAL DEMAND & A STRONG DOLLAR

Copper has continued to decline on the global market due to lower global demand and a strong dollar which is poised to become even stronger with the impending rate hike

Concerns about the resilience of the Chinese economy have resurfaced in light of recent events in the Chinese stock market

Growth in China has began to slow down with manufacturing indexes posting substantial contractions

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Copper US cents/Lb

Copper US cents/Lb

Source: Bank of Zambia

Quka Consulting: Ideas, Insight & Innovation © 2015

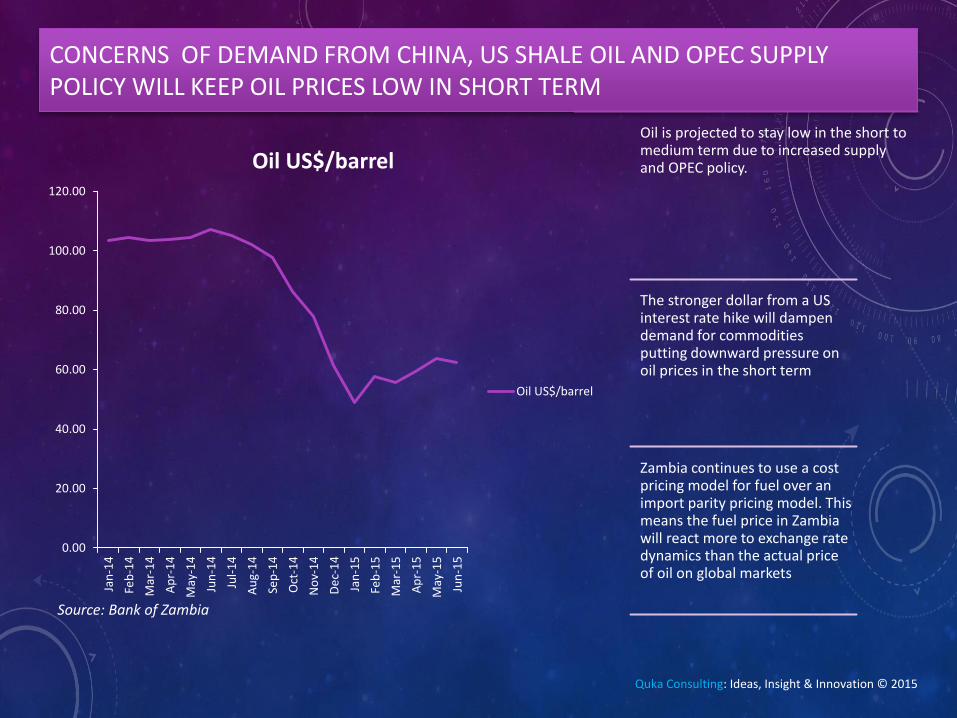

CONCERNS OF DEMAND FROM CHINA, US SHALE OIL AND OPEC SUPPLY POLICY WILL KEEP OIL PRICES LOW IN SHORT TERM

0.00

20.00

40.00

60.00

80.00

100.00

120.00

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Oil US$/barrel

Oil US$/barrel

Oil is projected to stay low in the short to medium term due to increased supply and OPEC policy.

The stronger dollar from a US interest rate hike will dampen demand for commodities putting downward pressure on oil prices in the short term

Zambia continues to use a cost pricing model for fuel over an import parity pricing model. This means the fuel price in Zambia will react more to exchange rate dynamics than the actual price of oil on global markets

Source: Bank of Zambia

Quka Consulting: Ideas, Insight & Innovation © 2015

LOCAL ECONOMY

Government budget deficit & Debt overshadows the

economy

Fragile Mining sector weakens Balance of trade

Kwacha depreciates against dollar

Quka Consulting: Ideas, Insight & Innovation © 2015

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

8.2

%

Inflation rate

The Consumer Price Index (CPI) measures changes over time in the general level of prices of goods and services that households acquire for the purpose of consumption

The Inflation rate has been dropping over the first half of the year with substantial drops in the first quarter due to lower food prices and fuel prices

The inflation rate rose in the second quarter. This increase is mainly attributed to increases in Non-food items particularly Liquid Fuels (Diesel, Kerosene and Petrol) and House rentals.

INFLATION ON COURSE TO BE AROUND GOVERNMENT’S YEAR END TARGET OF 7%

Source: Bank of Zambia

Quka Consulting: Ideas, Insight & Innovation © 2015

The Kwacha has depreciated against its major convertibles with a very noticeable depreciation against the US Dollar

Availability of the US Dollar in Zambia has been declining

The depreciation is largely due to lower foreign exchange earnings while the dollar strengthened against major convertibles

Bank of Zambia has reiterated its position to not use too much of its reserves to halt the kwacha fall.

Commercial banks have already expressed their concerns over the increase in statutory reserves indicating its negative impact on operations.

KWACHA DEPRECIATED IN H1 DUE TO LOWER FOREIGN EXCHANGE EARNINGS WHILE DOLLAR STRENGTHENS AGAINST MAJOR CONVERTIBLES

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

USD/Kwacha Rate

USD/Kwacha Rate

Source: Bank of Zambia Quka Consulting: Ideas, Insight & Innovation © 2015

Trade Deficit is a situation where a country is importing more than it is exporting in value terms.

Zambia faced a widening trade deficit in the first half of 2015 recording consecutive trade deficits from January to May.

While there has been an increase in Non Traditional Exports in the first half of 2015, the decrease in the total value of Metal exports kept total exports flat.

The balance of trade was unfavorable due to increased imports and reduced exports

The trade deficit was driven by increased imports of consumer and capital goods

ZAMBIA RECORDED A TRADE DEFICIT IN H1

-1500 -1000 -500 0

Jan-15

Feb-15

Mar-15

Apr-15

May-15

ZMW Millions

TradeBalance

Source: CSO

Quka Consulting: Ideas, Insight & Innovation © 2015

2,750.00

2,800.00

2,850.00

2,900.00

2,950.00

3,000.00

3,050.00

3,100.00

ZMW

Mill

ion

Metal Exports

MINING SECTOR PERFORMANCE REMAINS WEAK DUE TO LOWER COPPER PRICES AND AFTER EFFECTS OF TAX ISSUES

240 250 260 270 280 290 300

2014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

Mining Index

Mining Index

Source: CSO

Quka Consulting: Ideas, Insight & Innovation © 2015

INDUSTRIAL INDEX

• Industrial index dropped in H1

• Manufacturing index increased but growth in the sector will be undermined by Load shedding

0.00 50.00 100.00 150.00 200.00 250.00 300.00 350.00

2014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

Manufacturing Index

Mining Index

Industrial Index

Source: CSO

Quka Consulting: Ideas, Insight & Innovation © 2015

DOMESTIC BORROWING CONSTRAINED, EXTERNAL BORROWING LIMIT INCREASED

Treasury yields have been rising for the most part of the half year with noticeable declines after the new bond issuance

Domestic Financing conditions are constrained and new external financing could push government debt toward 40 per cent of GDP.

Rising debt burden could see interest costs rise sharply. Fitch estimates interest costs take up 17% of government revenue in 2015 up from 8% in 2012.

Greater reliance on non-concessionary external financing may increase refinancing risk. The “sinking fund” proposed by Government may mitigate this risk.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

91 days

182 days

273 days

364 days

Source: Bank of Zambia

Quka Consulting: Ideas, Insight & Innovation © 2015

MINING & AGRICULTURE REMAINED STEADY WHILE CREDIT TO OTHER SECTORS DROPPED

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

Real estate

Community, social and perconal services

Financial services

Transport, storage and communications

Wholesale and retail trade

Construction

Electricity, gas, water and energy

Manufacturing

Mining and quarying

Agriculture, forestry,Fishing and hunting

Source: Bank of Zambia

Credit to Wholesale sector increased

Credit to Real estate sector increased

Credit to most sectors dropped in the first quarter but picked up in the second quarter

Quka Consulting: Ideas, Insight & Innovation © 2015

0

2

4

6

8

10

12

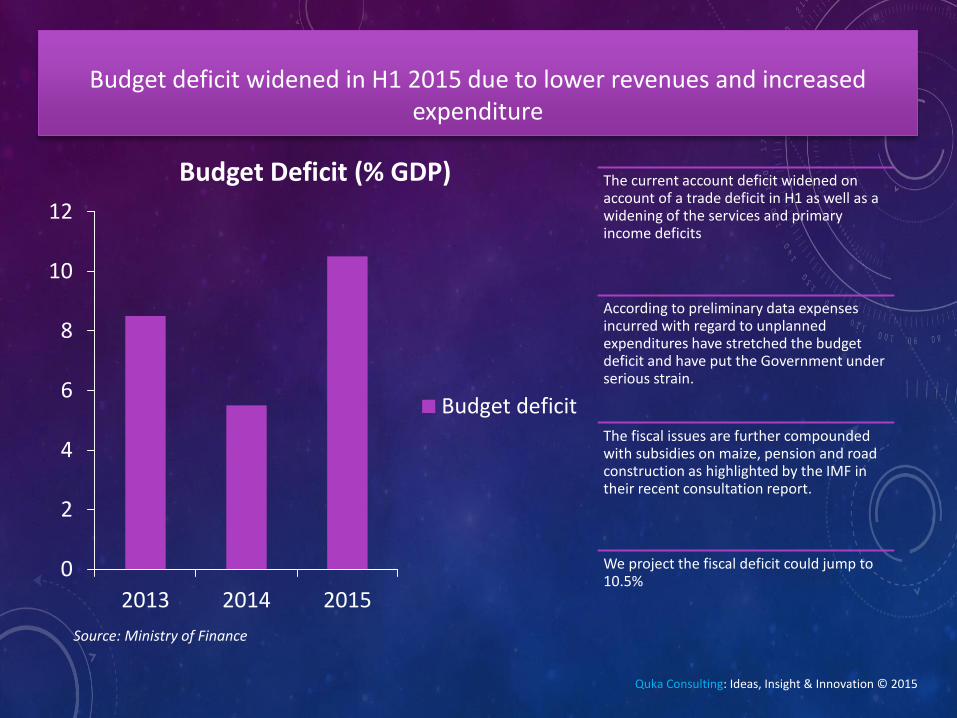

2013 2014 2015

Budget Deficit (% GDP)

Budget deficit

The current account deficit widened on account of a trade deficit in H1 as well as a widening of the services and primary income deficits

According to preliminary data expenses incurred with regard to unplanned expenditures have stretched the budget deficit and have put the Government under serious strain.

The fiscal issues are further compounded with subsidies on maize, pension and road construction as highlighted by the IMF in their recent consultation report.

We project the fiscal deficit could jump to 10.5%

Budget deficit widened in H1 2015 due to lower revenues and increased

expenditure

Source: Ministry of Finance

Quka Consulting: Ideas, Insight & Innovation © 2015

Government issues $1.25bn Eurobond at 9.3% on international markets

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015

Debt/GDP ratio % Zambia has issued a $1.25 billion Eurobond meant for infrastructure development

The Eurobond, with a coupon rate of 8.97 percent, has an eleven year average life repayments in 2025, 2026 and 2027

The funds will be used in infrastructure related projects in the area of road, energy, education, health, water and transport sectors

Despite a challenging capital markets environment arising from global economic uncertainties, Zambia’s bond issue was met with high demand from international investors

Zambia’s first Eurobond worth US$750 million was issued in 2012, while the second one worth US$1 billion was issued in 2014.

Source: Ministry of Finance

Quka Consulting: Ideas, Insight & Innovation © 2015

LUSAKA STOCK EXCHANGE: TRADES AND VOLUMES DOWN

The Market capitalization closed at K64.72 billion, up by 3.88% compared to the close of the 2nd quarter of last

Volume of shares traded in the 2nd quarter of 2015 decreased by 52.62% compared to the same period in 2014. Volumes traded in all 3 months of the 2nd quarter were less than those of the 2nd quarter of 2014.

The LASI dropped steadily over April, May and June in the 2nd Quarter of 2015, opposite to its movement in the same period in 2014.

The market turnover decreased by 8.05% compared to the same period in 2014

The number of trades on the bond market increased by 100% in the 2nd quarter of 2015 compared to the same period in 2014.

59

60

61

62

63

64

65

2014 2015

Bill

ion

s

Market Capitalisation Second Quarter

Source: Lusaka Stock Exchange

Quka Consulting: Ideas, Insight & Innovation © 2015

FORECASTS Economy is expected to grow at 5.5% in 2015

Year end Inflation expected around 7% macro economic target

Budget deficit expected to be 10% of GDP

Quka Consulting: Ideas, Insight & Innovation

GDP & OUTPUT GAP

ESTIMATION

Quka Consulting: Ideas, Insight & Innovation © 2015

$0

$5,000,000,000

$10,000,000,000

$15,000,000,000

$20,000,000,000

$25,000,000,000

$30,000,000,000

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

GDP (current US$)

GDP (current US$)

GROSS DOMESTIC PRODUCT HAS BEEN GROWING AT A FAST RATE SINCE 2004 DUE TO MINING, AGRICULTURE, WHOLESALE & RETAIL TRADE INCLUDING OTHER SECTORS

Quka Consulting: Ideas, Insight & Innovation © 2015

PHILLIPS CURVE INFLATION/OUTPUT GAP 2005-2015

The output gap, defined as the difference between the actual and potential output, relates to the state of the economy in its business cycle

y = 2,922,967.30x-0.54 R² = 0.43

0

2

4

6

8

10

12

14

16

18

0 10 20 30

Pri

ce L

eve

l

Quantity: Aggregate Demand

Billions

Inflation Output Gap

Inflation Output Gap

Power (Inflation Output Gap)

Quka Consulting: Ideas, Insight & Innovation © 2015

GDP RESIDUALS

-6

-4

-2

0

2

4

6

8

0 5E+09 1E+10 1.5E+10 2E+10 2.5E+10 3E+10

Re

sid

ual

s

Gross Domestic Product

Series1

Linear(Series1)

Quka Consulting: Ideas, Insight & Innovation © 2015

GDP Residuals measure the output gap as shown above. The output gap is the difference between actual GDP and potential GDP.

Zambia has been growing below potential output since 2014. This means the economy is in a state of contraction. In business cycle terms this can be explained as a dip.

QUADRATIC OUTPUT GAP

-25

-20

-15

-10

-5

0

5

10

15

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Quadratic Output Gap

Quka Consulting: Ideas, Insight & Innovation © 2015

The quadratic output gap above shows that monetary policy has been effective in controlling inflation by preventing the economy from heating up too much.

GDP GROWTH OF 2.73% IN H1

The Zambian economy is estimated to have grown by 2.73% in the first half of 2015

This is driven by growth in Construction, Real estate, Transport, Wholesale and retail trade, Agriculture, Financial services among others.

The mining sector is rebounding from a recession and we hope to see some growth in the third quarter.

Zesco load shedding is expected to put contractionary pressures on year end GDP

Potential GDP growth for H1 is estimate at 3.09% which means the Zambian economic growth is below its potential

This indicates the effectiveness of monetary policy by the Bank of Zambia in containing inflation

Quka Consulting: Ideas, Insight & Innovation © 2015

FORECASTS

We forecast Zambia will grow at a rate of 5.5% in 2015 on the backdrop of growth in Financial services, Agriculture, real estate, construction, transport including wholesale and retail trade

We estimate Zesco load shedding could take as much as 0.3% of GDP growth this year pulling growth from 5.8% to 5.5%

Inflation should close around the Government year end target of 7%.However depreciation of the kwacha which has the propensity to import inflation coupled with higher fuel costs will create upward inflationary pressures. It is unlikely that such pressure will preempt an interest rate hike ahead pf the central banks monetary policy committee meeting in august

We forecast Zambia will post a net trade deficit this year owning to its unfavorable balance of trade. Pressures on the depreciating Kwacha are poised to continue in the short to medium term

We anticipate further depreciation of the Kwacha with $1=K8 our upper limit estimate and $1=K7.5 our lower limit estimate for 2015.

The budget deficit is estimated to be 10% of GDP for 2015

We anticipate a stronger second half of the year than the first backed by seasonal aggregate demand in household consumption

Quka Consulting: Ideas, Insight & Innovation © 2015

ESTIMATION DISCLAIMER

While we respect the completeness of the data used in our Phillips curve regressed estimation of GDP we recognize it is

not devoid of inaccuracy

We can include monetary policy (interest rates) as well as the real exchange rate in our model but this will come at a

price of a lower adjusted mean square

A stronger model will include monetary policy and the real economy by using the unemployment rate and capacity utilization for a dynamic

stochastic equilibrium model

Quka Consulting: Ideas, Insight & Innovation © 2015

Quka Consulting: Ideas, Insight & Innovation

Who are we? Quka Consulting is a consultancy which leverages on three core pillars of Ideas, Insight and Innovation to solve our client’s problems. Our team is well prepared to work with our clients in creating solutions that address the many challenges that arise in a dynamic economy. What we do? Quka Consulting provides professional services ranging but not limited to the following: Market Intelligence Corporate Advisory Business Solutions How can we help you? Quka Consulting is based on three core pillars namely: Ideas – We work with our clients to execute solutions based on original thought & creative thought leadership Insight – We provide research & cutting edge analysis around our client’s needs and the dynamic market environment Innovation – We tailor bespoke solutions for our clients problems Contact Us Twitter: @QukaConsulting Facebook: Quka Consulting Website: www.qukaconsulting.com Email: [email protected] Phone: +260973833383

Contact Us

Quka Consulting is a Registered Partnership with the Patents and Company registration agency in

Lusaka, Zambia (2015). It is the sole custodian of the business name “Quka Consulting” and no one can

use this name in any official capacity without the written authority or consent of “Quka Consulting” and its

“partners”.

Jacqueline Musiitwa – Lead Advisor & Partner

Kampamba Shula – Economist & Partner

P.O. Box 50722, Ridgeway

Lusaka, Zambia

Tel: +260973833383

www.qukaconsulting.com

Quka Consulting: Ideas, Insight & Innovation