header 58 pt - fidelity.com

TRANSCRIPT

November 6, 2018

Opportunities in a changing world using option strategies

Fidelity Investments

@PeterLusk

2

Options involve risks and are not suitable for all investors. Prior to buying or selling an option, an investor must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker or from The Options Clearing Corporation at www.theocc.com. Futures trading is not suitable for all investors and involves risk of loss. The information in this presentation is provided solely for general education and information purposes. No statement within this presentation should be construed as a recommendation to buy or sell a security or future or to provide investment advice. Any strategies discussed, including examples using actual securities or futures price data, are strictly for illustrative and educational purposes only. In order to simplify the computations, commissions, fees, margin interest and taxes have not been included in the examples used in this presentation. These costs will impact the outcome of all transactions and must be considered prior to entering into any transactions. Multiple leg strategies involve multiple commission charges. Investors should consult with their tax advisors to determine how the profit and loss on any particular option strategy will be taxed. Past performance does not guarantee future results. Supporting documentation for any claims, comparisons, statistics or other technical data in this presentation is available from Cboe upon request. Cboe, Cboe Exchange, Inc., Cboe Volatility Index, CFE and VIX are registered trademarks and Cboe Futures Exchange, Cboe Short-Term Volatility Index, Cboe 3-Month Volatility Index, Cboe Mid-Term Volatility Index, Execute Success, RVX, SPX, The Options Institute VXST, VXN, VXV and VXMT are service marks of Cboe Exchange, Inc (Cboe). S&P 500® is a registered trademark of Standard & Poor's Financial Services, LLC and has been licensed for use by Cboe and Cboe Futures Exchange, LLC (CFE). Cboe's and CFE’s financial products based on S&P indices are not sponsored, endorsed, sold or promoted by S&P and S&P makes no representation regarding the advisability of investing in such products. Russell 2000® is a registered trademark of Russell Investments, used under license. The NASDAQ-100 Index®, NASDAQ-100®, and NASDAQ® are trademark or service marks of The NASDAQ Stock Market, Inc. (with which its affiliates are the "Corporations"). These marks are licensed for use by Cboe in connection with the trading of products based on the NASDAQ-100 Index. The products have not been passed on by the Corporations as to their legality or suitability. The products are not issued, endorsed, sold or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE PRODUCT(S). Cboe is not affiliated with Interactive Brokers. This presentation should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe product or service described in this presentation.

Copyright © 2018 Cboe Exchange, Inc. All rights reserved.

Disclosure

3

What’s Trading?

A little bit of this

And a lot of that

4

Option Price Components Six Option Pricing Factors

Pricing Concepts

5

Delta: Impact of underlying price

Gamma: Change in delta

Theta: Impact of time Vega: Impact of volatility

Pricing Concepts

6

SPX – Expected Range Example

Converting the 1-year standard deviation:

Underlying Price × I.V. × √ Days to Exp √ Days per year

SPX Index Level 2,700 Days to Expiration 28 Implied Volatility 12%

2,700 × .12 × √ 28 √ 365

= 90

7

Implied Volatility

• How do some traders choose strike prices? • What is the fair value ATM straddle implying? Strike Calls Puts 40 $10.60 $0.30 45 $6.55 $1.40 50 $2.30 + $2.10 = $4.40 55 $1.25 $6.20 60 $0.40 $10.20 65 $0.10 $14.90

XYZ stock trading $50

8

Spread Opportunities - Examples

9

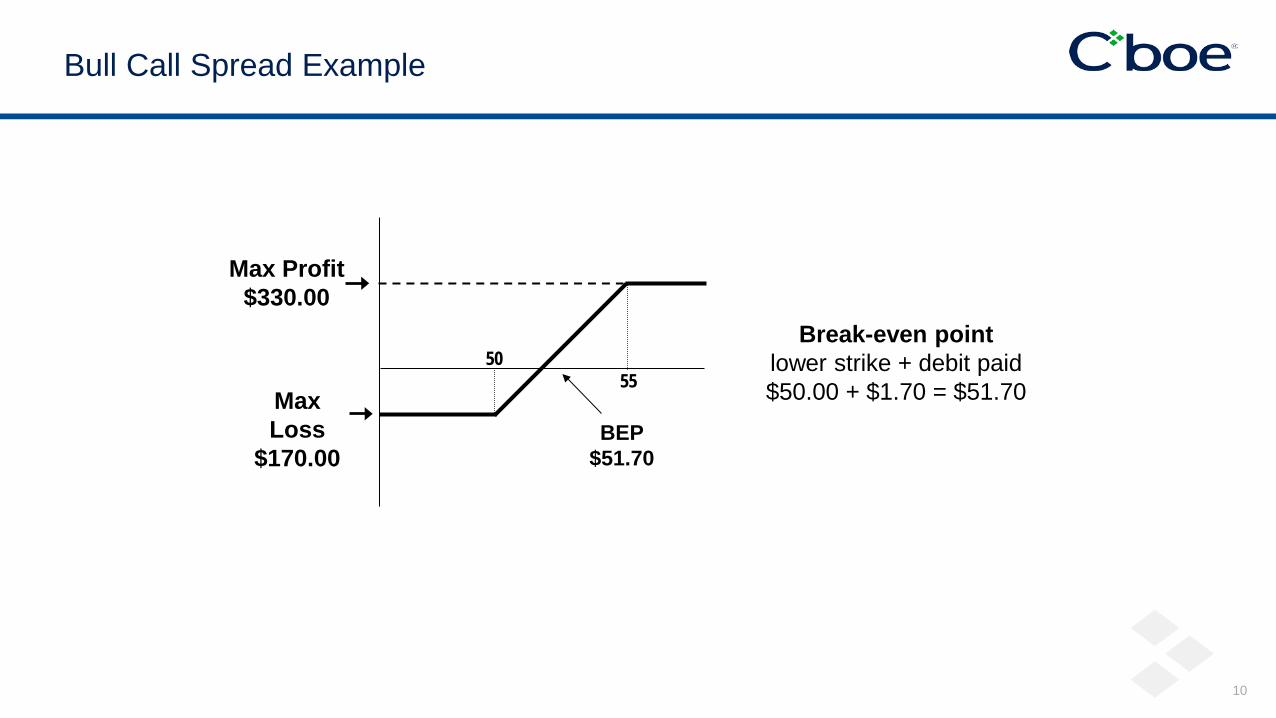

Bull Call Spread Example

Stock XYZ at $50.00

Spread: • buy 1 XYZ 50.00 call – $2.90 • sell 1 XYZ 55.00 call + $1.20

Position: • long 1 XYZ 50.00 call and short 1 XYZ 55.00 call • long XYZ 50.00-55.00 call spread • net debit = $1.70 or $170.00 total

10

Bull Call Spread Example

50 55

Max Loss

$170.00

Max Profit $330.00

BEP $51.70

Break-even point lower strike + debit paid $50.00 + $1.70 = $51.70

11

Bear Put Spread Example

Stock XYZ at $55.00

Spread: • buy 1 XYZ 55.00 put – $2.90 • sell 1 XYZ 50.00 put + $1.20

Position: • long 1 XYZ 55.00 put and short 1 XYZ 50.00 put • long XYZ 55.00-50.00 put spread • net debit = $1.70 or $170.00 total

12

Bear Put Spread Example

50

55 Max

Loss $170.00

Max Profit $330.00

BEP $53.30 Break-even point

higher strike - debit paid $55.00 - $1.70 = $53.30

13

Bear Call Spread Example

Stock XYZ at $50.00

Spread: • sell 1 XYZ 50.00 call + $2.90 • buy 1 XYZ 55.00 call - $1.20

Position: • short 1 XYZ 50.00 call and long 1 XYZ 55.00 call • short XYZ 50.00-55.00 call spread • net credit = $1.70 or $170.00 total

14

Bear Call Spread Example

50

55

Max Loss

$330.00

Max Profit $170.00

BEP $51.70 Break-even point:

Lower strike + net credit 50 + $1.70 = 51.70

15

• When establishing any position have a 3-part forecast

• Underlying

• Time

• Volatility

• Recognize what the ATM straddle is implying

• Spreads, spread off risk to a certain degree

Summary

16

Cboe Global Markets 400 South LaSalle Street Chicago, IL 60605 www.cboe.com

16