health insurance and managed care (b) committee - naic.org · lori k. wing-heier alaska larry...

TRANSCRIPT

© 2018 National Association of Insurance Commissioners 1

Date: 11/12/18 2018 Fall National Meeting San Francisco, California

HEALTH INSURANCE AND MANAGED CARE (B) COMMITTEE

Friday, November 16, 2018 8:00 – 10:00 a.m.

Hilton San Francisco Union Square—Continental 4—Ballroom Level

ROLL CALL

Dean L. Cameron, Chair Idaho John Elias New Hampshire Jessica Altman, Vice Chair Pennsylvania Mike Causey North Carolina Lori K. Wing-Heier Alaska Larry Deiter South Dakota Nancy G. Atkins Kentucky Todd E. Kiser Utah Al Redmer Jr. Maryland Osbert E. Potter Virgin Islands Jessica Looman Minnesota Mike Kreidler Washington Mike Chaney Mississippi Ted Nickel Wisconsin Matthew Rosendale Montana NAIC Support Staff: Jolie H. Matthews/Brian R. Webb/Jennifer R. Cook

AGENDA

1. Consider Adoption of its Oct. 24, Oct. 2 and Summer National Meeting Minutes —Director Dean L. Cameron (ID) 2. Consider Adoption of its Subgroup, Working Group and Task Force Reports

—Director Dean L. Cameron (ID) • Consumer Information (B) Subgroup—Angela Nelson (MO) • CO-OP Solvency and Receivership (B) Subgroup—Commissioner Doug Ommen (IA) • Health Care Reform Regulatory Alternatives (B) Working Group

—Commissioner Ted Nickel (WI) and J.P. Wieske (WI) • Health Actuarial (B) Task Force—Director Patrick M. McPharlin (MI) and Kevin Dyke (MI) • Regulatory Framework (B) Task Force—Commissioner Ted Nickel (WI) and J.P. Wieske (WI) • Senior Issues (B) Task Force—Director Lori K. Wing-Heier (AK)

3. Hear a Presentation from Centers for Medicare and Medicaid Services (CMS)—Randy Pate (CCIIO) 4. Hear a Presentation on Health Care Cost Drivers, Network Adequacy Issues and Surprise Billing--Dr. Jack

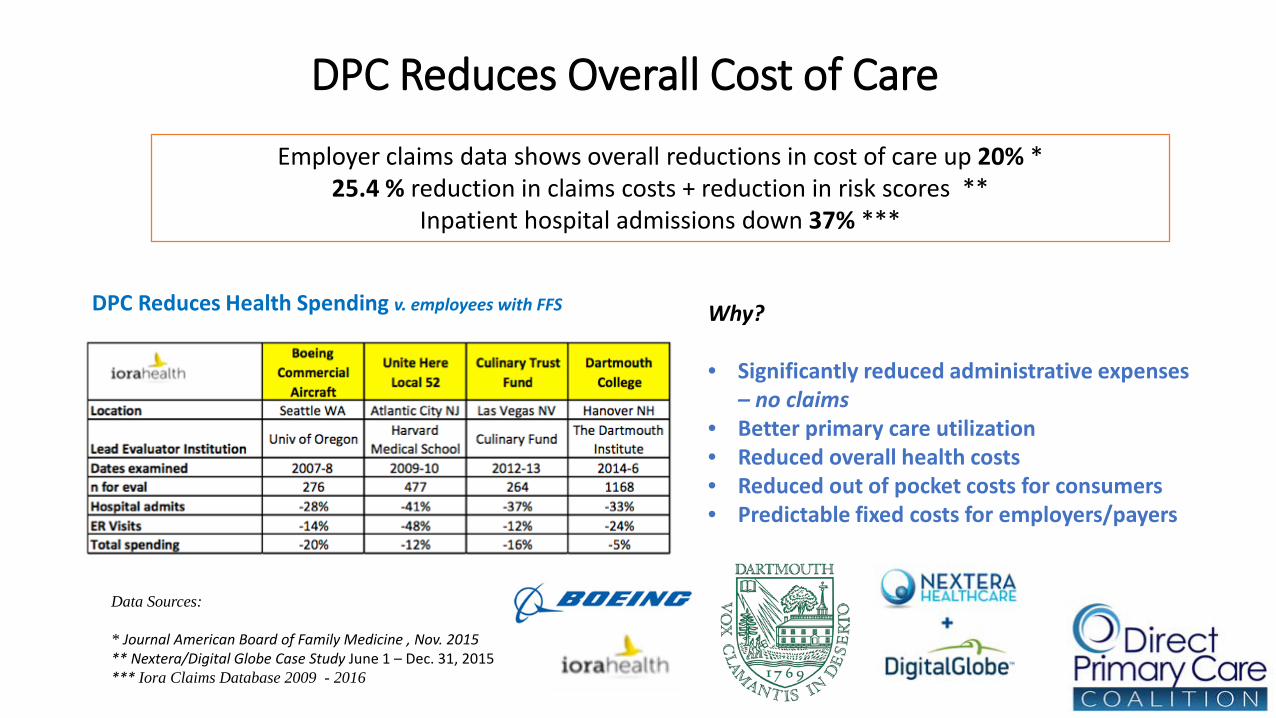

Resneck (American Medical Association—AMA) 5. Hear a Briefing on State Legislative and Administrative Actions to Address Prescription Drug Cost-Sharing —Carl Schmid (The AIDS Institute) 6. Hear a Panel Presentation on Direct Primary Care Arrangements—Dr. Julie Gunther and Dr. Clint Flanagan

(Direct Primary Care Coalition) 7. Hear a Panel Presentation on Health Care Sharing Ministries—JoAnn Volk (Georgetown University, Center

on Health Insurance Reforms—CHIR) and Brad Hahn (Solidarity HealthShare) 8. Recess W:\National Meetings\2018\Fall\Agenda\B CmtePart1.docx

© 2018 National Association of Insurance Commissioners 2

Page Intentionally Left Blank

© 2018 National Association of Insurance Commissioners 3

Agenda Item #1

Consider Adoption of its Oct. 24, Oct. 2 and Summer National Meeting Minutes —Director Dean L. Cameron (ID)

Attachment Two Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 11/5/18

Health Insurance and Managed Care (B) Committee Conference Call October 24, 2018

The Health Insurance and Managed Care (B) Committee met via conference call Oct. 24, 2018. The following Committee members participated: Dean L. Cameron, Chair (ID); Jessica Altman, Vice Chair (PA); Lori K. Wing-Heier represented by Jacob Lauten (AK); Nancy G. Atkins (KY); Al Redmer Jr. represented by Robert Morrow and Catherine Grason (MD); Jessica Looman represented by Fred Andersen, Kristi Bohn and Melinda Domzalski-Hansen (MN); Mike Chaney represented by Josh Ammerman (MS); Matthew Rosendale represented by Ashley Perez (MT); Mike Causey represented by Candy Holbrook and Ted Hamby (NC); John Elias represented by Alain Couture (NH); Larry Deiter represented by Melissa Klemann (SD); Todd E. Kiser represented by Jaakob Sundberg, Tanji Northrup and Tomasz Serbinowski (UT); Mike Kreidler represented by Jane Beyer and Molly Nollette (WA); and Ted Nickel represented by J.P. Wieske, Jennifer Stegall, Barbara Belling and Sue Ezalarab (WI). Also participating was: Kevin Dyke (MI). 1. Adopted the Health Actuarial (B) Task Force’s 2019 Proposed Charges Eric King (NAIC) explained that the Health Actuarial (B) Task Force’s 2019 proposed charges contain only minor changes from the Task Force’s 2018 charges. Mr. Dyke said that the charge to revise the Health Insurance Reserves Model Regulation (#10) to reflect appropriate long-term care insurance (LTCI) reserving standards, has been removed. He explained that the Task Force no longer wishes to pursue these revisions. Director Cameron said that the appropriate steps would be taken to close the Model Law Development Request. Ms. Northrup made a motion, seconded by Commissioner Atkins, to adopt the Health Actuarial (B) Task Force’s 2019 proposed charges (see Health Actuarial (B) Task Force, Attachment _____). The motion passed unanimously. 2. Adopted the Regulatory Framework (B) Task Force’s 2019 Proposed Charges Mr. Wieske said that the major change to the Regulatory Framework (B) Task Force’s 2019 proposed charges is the addition of the charge addressing pharmacy benefit managers (PBMs):

Consider developing a new NAIC model to establish a licensing or registration process for pharmacy benefit managers (PBMs). The Subgroup may consider including in the new NAIC model provisions on PBM prescription drug pricing and cost transparency.

Mr. Wieske explained that there was an interest in looking at the issue of PBM licensure or registration separate from the Health Carrier Prescription Drug Benefit Management Model Act (#22), which is more consumer focused and addresses PBM issues through the regulation of the insurers. He said that consumers, the Pharmaceutical Research and Manufacturers of America (PhRMA) and the medical community have all expressed an interest in seeing the charge move forward. He said that the issue of licensure or registration was discussed in the context of Model #22, but the focus was on consumers and how to make them whole. Mr. Wieske said that Model #22 can stand on its own, but it makes sense to look at regulating PBMs as regulated entities separate from the insurance contract. Chris Petersen (Arbor Strategies) spoke on behalf of the Pharmaceutical Care Management Association (PCMA) in opposition to the proposed charge. He said that the PCMA opposes the charge for several reasons. He said, first, a new PBM model act does not meet the NAIC’s parameters on model laws. He said that with nearly half the states already adopting PBM licensure or registration laws, it would be impossible for two-thirds of the states to commit to promoting the adoption of a new model law in their states. He said that the second reason the PCMA opposes a new charge is because PBM licensure was thoroughly discussed and rejected as an option during the Model #22 revision process. He said that the third reason the PCMA opposes the charge is because it is vague and misleading in calling for the consideration of PBM licensure or registration in addition to pricing transparency. He said that PBMs do not set drug prices, but drug manufacturers set drug prices. Mr. Petersen said the PCMA suggests that the NAIC, through the Pharmacy Benefit Manager Regulatory Issues (B) Subgroup, develop a white paper or a guideline on PBM licensure or registration. Mr. Morrow said that prescription drug costs are a large part of the health care landscape. He said that many PBMs operate nationally and a national response is desirable. He said that PBMs play an important role in the pricing of prescription drugs

Attachment Two Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

and there is not transparency. He said that there is a level of complexity with PBMs that is hard to address through regulation of the insurers. He said that he supports the charge and looks forward to taking a look at the role of PBMs and deciding whether developing a new model is appropriate. Mr. Weiske said that there was a discussion during the revision of Model #22, but there continues to be deeper concerns about PBMs and how to keep a handle on it, outside of the consumer context, which is the focus of Model #22. He said that it makes sense to look at regulating PBMs separately outside of the insurance contract. Carl Schmid (The AIDS Institute) said that NAIC consumer representatives support moving forward with the charge. He said several proposals were discussed that did not make it into Model #22 but would fit under this proposed charge. Leanne Gassaway (America’s Health Insurance Plans—AHIP) said that AHIP did not believe a separate model was necessary. She said that the issue has been well discussed in the states, and she doubted states that already have laws in place would remove their existing laws to adopt the NAIC model. She said that studying the issue would be acceptable, but she did not anticipate discovering a situation that would support the development of a separate model at this point. Jeremy Crandall (Blue Cross Blue Shield Association—BCBSA) agreed with AHIP and Mr. Petersen and said that half of the states already regulate PBMs, and more information is needed regarding all drug pricing components, not just PBMs. He said that the BCBSA supports a white paper or guidelines, but not model law development. Mr. Morrow said that the time to develop a white paper has passed. He said the issue is well understood. He agreed that there are many components to the drug pricing structure—manufacturers, wholesalers, pharmacies, providers—but PBMs negotiate prices and touch every part of the pricing structure. Director Cameron reiterated that the charge, as drafted, says “consider” developing a model. Mr. Wieske said that there would be a process before work on a model could start. He explained that the idea of developing a model would have to be discussed. If there was agreement to create a model, then a model law development request would have to be adopted by the Regulatory Framework (B) Task Force, the Health Insurance and Managed Care (B) Committee and the Executive (EX) Committee. Given the process he just outlined, work on a new model could start, at the earliest, in February 2019. Mr. Wieske made a motion, seconded by Ms. Northrup, to adopt the Regulatory Framework (B) Task Force’s 2019 proposed charges (see Regulatory Framework (B) Task Force, Attachment _____). The motion passed unanimously. 3. Adopted the Senior Issues (B) Task Force’s 2019 Proposed Charges Director Cameron said that the Senior Issues (B) Task Force’s 2019 proposed charges had been distributed prior to the conference call. There were no major changes to report. Ms. Klemann made a motion, seconded by Commissioner Altman, to adopt the Senior Issues (B) Task Force’s 2019 proposed charges (see Senior Issues (B) Task Force, Attachment _____). The motion passed unanimously. 4. Adopted its 2019 Proposed Charges Director Cameron said that the Committee’s draft 2019 proposed charges were distributed prior to the conference call. He said that Jolie H. Matthews (NAIC) reviewed the 2019 proposed charges during the Committee’s last conference call and explained that the revisions were intended to better reflect the Committee’s current work. Sarah Lueck (Center for Budget and Policy Priorities—CBPP) said that the NAIC consumer representatives had submitted a letter requesting that the Committee consider adding the following charge for 2019:

Coordinate with the Market Regulation and Consumer Affairs (D) Committee, as necessary, to collect uniform data and monitor market conduct trends on plans that are not regulated under the Affordable Care Act, including short-term, limited-duration insurance, association health plans, and packaged indemnity health products.

Ms. Lueck said that the NAIC consumer representatives were deeply concerned about the potential for fraud and abuse, insolvency, unpaid claims, and consumer confusion associated with the non-federal Affordable Care Act (ACA) products named in the charge. She said that there is only limited data collected on these products through current NAIC reporting statements, tools and products. She said that these concerns about the need for additional data on these types of coverage are

Attachment Two Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 3

shared by the Market Analysis Procedures (D) Working Group, and they have agreed to issue a data call to monitor 2018 and 2019 experience in these product markets. She said that the results of the data call will likely inform whether these non-ACA products might be added to the Market Conduct Annual Statement (MCAS) for health, which is something the consumer groups support. She said that coordination between the Health Insurance and Managed Care (B) Committee and the Market Regulation and Consumer Affairs (D) Committee will be particularly important as the Working Group develops a data call and any updates to the MCAS. Ms. Northrup made a motion, seconded by Commissioner Altman, to adopt the Health Insurance and Managed Care (B) Committee’s 2019 proposed charges, including the additional charge suggested by the consumer representatives (Attachment ___). The motion passed unanimously.

Having no further business, the Health Insurance and Managed Care (B) Committee adjourned. W:\National Meetings\2018\Fall\Cmte\B\B Cmte 10-24-18 ConfCallMin.docx

Attachment Two Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 10/9/18

Health Insurance and Managed Care (B) Committee Conference Call October 2, 2018

The Health Insurance and Managed Care (B) Committee met via conference call Oct. 2, 2018. The following Committee members participated: Dean L. Cameron, Chair (ID); Jessica Altman, Vice Chair (PA); Lori K. Wing-Heier represented by Anna Latham (AK); Nancy G. Atkins (KY); Al Redmer Jr. represented by David Cooney (MD); Jessica Looman represented by Fred Andersen and Kristi Bohn (MN); Mike Chaney represented by Bob Williams (MS); Matthew Rosendale represented by Michael Kakuk (MT); John Elias represented by Jennifer Patterson (NH); Todd E. Kiser represented by Tanji Northrup (UT); Mike Kreidler (WA); and Ted Nickel represented by JP Wieske (WI). 1. Adopted the Limited Long-Term Care Insurance Model Act and the Limited Long-Term Care Insurance Model Regulation David Torian (NAIC) provided an overview and history of the proposed new Limited Long-Term Care Insurance Model Act and the proposed new Limited Long-Term care Insurance Model Regulation. He explained that in response to consumer advocate concerns, at the 2016 Summer National Meeting, the Senior Issues (B) Task Force appointed the Short-Term Health Policies Providing Long-Term Care Benefits (B) Subgroup to determine the appropriate means of addressing long-term care insurance (LTCI) policies of short duration with a duration of less than 12 months. He said the Short-Term Health Policies Providing Long-Term Care Benefits (B) Subgroup found that these LTCI policies are excluded from the Long-Term Care Insurance Model Act (#640) and the Long-Term Care Insurance Model Regulation (#641), but do not quite fit into the Accident and Sickness Insurance Minimum Standards Model Act (#170), which is where regulation of these policies currently is addressed. Mr. Torian said the Subgroup was concerned that the provisions of Model #170 do not provide the protections found in Model #640 and Model #641, such as provisions related to third-party premium notice, guaranteed renewability/non-cancellable, nonforfeiture benefits, elimination periods and inflation protection. He said that in response to the Short-Term Health Policies Providing Long-Term Care Benefits (B) Subgroup’s findings, at the 2016 Fall National Meeting, the Senior Issues (B) Task Force disbanded the Subgroup and appointed the Short Duration Long-Term Care Policies (B) Subgroup to create new NAIC models to address LTCI policies of short duration that are excluded from Model #640. Mr. Torian said the Short Duration Long-Term Care Policies (B) Subgroup met via conference call 14 times to develop the models. He said the Short Duration Long-Term Care Policies (B) Subgroup adopted the new models March 7. The Senior Issues (B) Task Force adopted them June 7. Commissioner Kreidler said he submitted a comment letter to the Committee expressing concerns about limited LTCI products and explaining why Washington plans to vote against the motion to adopt both models. He said Washington is concerned these products provide an illusory benefit to consumers and do not meet its current standards applicable to benefits, disclosure and consumer protection. Commissioner Kreidler also expressed concern about how these products would be marketed to consumers. Mr. Wieske expressed support for adopting the models. He said Wisconsin has seen the sale of limited LTCI products in its market, but Wisconsin does not have a clear regulatory structure for them. Mr. Wieske said that given this, he believes adopting these models would benefit consumers because they provide a regulatory scheme with the necessary consumer protections. Mr. Wieske made a motion, seconded by Ms. Northrup, to adopt the Limited Long-Term Care Insurance Model Act (see NAIC Proceedings – Summer 2018, Senior Issues (B) Task Force, Attachment One-A). The motion passed from those Committee members present and voting, with Alaska, Idaho, Kentucky, Maryland, Minnesota, Mississippi, Montana, New Hampshire, Utah and Wisconsin voting in favor of the motion and Washington voting against the motion. Ms. Northrup made a motion, seconded by Mr. Wieske, to adopt the Limited Long-Term Care Insurance Model Regulation (see NAIC Proceedings – Summer 2018, Senior Issues (B) Task Force, Attachment One-B). The motion passed from those Committee members present and voting, with Alaska, Idaho, Kentucky, Maryland, Minnesota, Mississippi, Montana, New Hampshire, Utah and Wisconsin voting in favor of the motion and Washington voting against the motion. 2. Adopted a Request for an Extension of Time to Develop Amendments to Model #10 Jolie Matthews (NAIC) said the Health Actuarial (B) Task Force is requesting an extension of time to develop amendments to the Health Insurance Reserves Model Regulation (#10). The Task Force is revising the model to reflect appropriate LTCI reserving standards.

Attachment Two Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

Ms. Northrup made a motion, seconded by Commissioner Atkins, to adopt the Health Actuarial (B) Task Force’s request for an extension of time to develop its amendments to Model #10. The motion passed unanimously. 3. Adopted a Request for an Extension of Time to Develop the New Limited LTCI Models Ms. Matthews said the Senior Issues (B) Task Force is requesting an extension of time to develop the proposed new limited LTCI models. She said that although the Committee adopted the models in the previous agenda item, technically, the Task Force did not meet the deadline under the NAIC’s model law development procedures to finish its work within one year following the Executive (EX) Committee’s approval of its Request for NAIC Model Law Development. As such, the Committee needs to approve an extension of model law development until the Fall National Meeting. Mr. Wieske made a motion, seconded by Commissioner Altman, to adopt the Senior Issues (B) Task Force’s request for an extension of time to develop the proposed limited LTCI models. The motion passed unanimously. 4. Reviewed and Exposed the Committee’s 2019 Proposed Charges Ms. Matthews said she distributed prior to the call the Committee’s draft 2019 proposed charges. She reviewed the proposed changes highlighting the proposed revision to the Health Care Reform Regulatory Alternatives (B) Working Group’s charges. Ms. Matthews explained the Working Group’s current charges were adopted soon after the enactment of the federal Affordable Care Act (ACA). She said that since then, there have been dramatic changes in how the ACA is being implemented such that the Working Group’s current charges no longer reflect its current work. Ms. Matthews said the Working Group’s draft 2019 proposed charges are intended to better reflect its current work. She urged state insurance regulators and interested parties to review the Committee’s draft 2019 proposed charges and submit any comments on them to her as soon as possible because the Committee plans to consider adoption of the charges during its Oct. 24 conference call.

Having no further business, the Health Insurance and Managed Care (B) Committee adjourned. W:\National Meetings\2018\Fall\Cmte\B\B Cmte 10-2-18 ConfCallMin.docx

Draft Pending Adoption

© 2018 National Association of Insurance Commissioners 1

Draft: 8/15/18

Health Insurance and Managed Care (B) Committee Boston, Massachusetts

August 5, 2018

The Health Insurance and Managed Care (B) Committee met in Boston, MA, Aug. 5, 2018. The following Committee members participated: Dean L. Cameron, Chair (ID); Jessica Altman, Vice Chair (PA); Lori K. Wing-Heier (AK); Nancy G. Atkins (KY); Al Redmer Jr. represented by Robert Morrow (MD); Jessica Looman (MN); Mike Chaney (MS); Matthew Rosendale represented by Michael Kakuk (MT); Mike Causey represented by Ted Hamby (NC); John Elias represented by Jennifer Patterson (NH); Larry Deiter (SD); Todd E. Kiser (UT); Osbert E. Potter represented by Dolace McLean (VI); Mike Kreidler (WA); and Ted Nickel and JP Wieske (WI). Also participating were: Kenneth Ryan James (AR); Dave Jones and Perry Kupferman (CA); Michael Conway and Peg Brown (CO); Craig Wright (FL); Gordon I. Ito (HI); Kevin Dyke (MI); Angela Nelson and Mary Mealer (MO); Bruce R. Ramge (NE); Paige Duhamel (NM); Maria T. Vullo and Troy Oechsner (NY); Cuc Nguyen (OK); Andrew Stolfi (OR); Michael Humphreys and Brian Hoffmeister (TN); and Jan Graeber (TX).

1. Adopted its June 28, April 19 and Spring National Meeting Minutes

The Committee met June 28, April 19 and March 25. During its June 28 meeting, the Committee: 1) adopted Valuation Manual revisions to VM-25, Health Insurance Reserves Minimum Reserve Requirements, and VM-30, Actuarial Opinion and Memorandum Requirements; and 2) discussed a referral from the Receivership and Insolvency (E) Task Force requesting the Committee review relevant health maintenance organization (HMO) models to determine if revisions need to be made for consistency with the revisions made to the Life and Health Insurance Guaranty Association Model Act (#520). The Committee decided to accept the referral and directed the Regulatory Framework (B) Task Force to conduct the review and report back to the Committee.

During its April 19 meeting, the Committee: 1) adopted its 2017 Fall National Meeting minutes (see NAIC Proceedings – Fall 2017, Health Insurance and Managed Care (B) Committee); 2) adopted a request from the Health Actuarial (B) Task Force to extend the time to develop revisions to the Health Insurance Reserves Model Regulation (#10) to reflect appropriate long-term care insurance (LTCI) reserving standards; 3) disbanded the Medical Loss Ratio Quality Improvement Activities (B) Subgroup; and 4) adopted the following subgroup, working group and task force reports: the Consumer Information (B)Subgroup; CO-OP Solvency and Receivership (B) Subgroup; the Health Care Reform Regulatory Alternatives (B) WorkingGroup, including its March 24 minutes; the Health Actuarial (B) Task Force; the Long-Term Care Insurance (B/E) TaskForce; the Regulatory Framework (B) Task Force; and the Senior Issues (B) Task Force.

Mr. Wieske made a motion, seconded by Commissioner Atkins, to adopt the Committee’s June 28 (Attachment One), April 19 (Attachment Two) and March 25 (see NAIC Proceedings – Spring 2018, Health Insurance and Managed Care (B) Committee) minutes. The motion passed unanimously.

2. Adopted its Subgroup, Working Group and Task Force Reports

Mr. Wieske made a motion, seconded by Ms. Patterson, to adopt the Committee’s subgroup, working group and task force reports: the Consumer Information (B) Subgroup, including its May 22 (Attachment Three) and April 6 (Attachment Four) minutes; the CO-OP Solvency and Receivership (B) Subgroup; the Health Care Reform Regulatory Alternatives (B) Working Group (Attachment Five); the Health Actuarial (B) Task Force; the Long-Term Care Insurance (B/E) Task Force; the Regulatory Framework (B) Task Force; and the Senior Issues (B) Task Force, not including the proposed new NAIC models: the Limited Long-Term Care Insurance Model Act and the Limited Long-Term Care Insurance Model Regulation. The motion passed unanimously.

3. Heard a Panel Presentation on Health Care Cost Drivers

Leanne Gassaway (America’s Health Insurance Plans—AHIP) and Kim Holland (Blue Cross and Blue Shield Association—BCBSA) discussed: 1) what each organization believes are the top five health care cost drivers; 2) what would be each organization’s approach, if any, to addressing those cost drivers; 3) what each organization is specifically doing, if anything, to address rising prescription drug costs; and 4) what each organization thinks state insurance regulators should do to address the issue. Ms. Gassaway said AHIP believes the following five factors are affecting premium rates: 1) taxes and fees; 2) value-based models; 3) which care providers participate in the plan network; 4) prescription drug prices;

Draft Pending Adoption

© 2018 National Association of Insurance Commissioners 2

and 5) who is covered under the plan. She also noted that market instability also affects premium rates. Ms. Gassaway said that with respect to prescription drug prices, lowering drug list prices is AHIP’s key policy solution for addressing increasing prescription drug prices. She also discussed the issues AHIP believes are affecting health care costs and savings. Those issues include: 1) medical management; 2) networks; 3) pharmacy benefit managers (PBMs); 4) coverage mandates; and 5) pharmacy issues.

Ms. Holland discussed the challenge of the high cost of health care services and coverage, noting that prices paid by private health insurance carriers are growing faster and are higher than in government programs. She also discussed what BCBSA believes are the sources of the growth and the potential growth of health care costs, such as prices for health care goods and services. Ms. Holland said increased health care goods and services prices result from a number of factors, including technological development, provider consolidation and demand and inflation. She said higher provider prices can be contributed to: 1) provider consolidation; 2) administrative costs; 3) capital acquisition and technology adoption; and 4) market demand. To address high prices and costs, Ms. Holland said BCBSA’s plans are: 1) promoting price and qualitytransparency; 2) pursuing innovative provider network designs; and 3) developing and/or promoting chronic care programsand incentives. She said the states can help address increasing health care costs by: 1) imposing a state individual mandate;2) avoiding enacting policies that create an unlevel playing field; 3) avoiding policies that discourage provider networkparticipation; and 4) resisting mandating benefits.

Ms. Patterson asked if all payer claims databases (APCDs) could be a tool for state insurance regulators in addressing rising health care costs. Ms. Gassaway said APCDs offer some promise in addressing the issue, but, to date, AHIP has not seen data obtained indicating that APCDs have helped to reduce costs. She said one challenge is the lack of data standardization among the states. Mr. Wieske asked why it appears that wearable devices, such as Fitbits and other types of activity trackers, have not been a factor in the health insurance industry in reducing costs unlike the property/casualty (P/C) insurance industry. Ms. Holland said health insurance is different because of more heightened privacy concerns with health information.

4. Heard a Briefing on Recent State Legislative and Administrative Actions to Address Prescription Drug Costs

Claire McAndrew (Families USA) and Eric Ellsworth (Consumer Checkbook) discussed state legislative and administrative actions to address prescription drug costs. Ms. McAndrew said state insurance regulators have an essential, unique voice in the effort to control prescription drug costs. She discussed some mechanisms state insurance regulators can use to address drug costs, such rate reviews that prioritize prescription drug cost transparency, reviewing pharmaceutical drug manufacturer pricing information and directly regulating PBMs. Ms. McAndrew discussed several state models that have been used to address prescription drug costs, including states using their rate review process and states reviewing pricing information from prescription drug manufacturers. She left the Committee with several key takeaways: 1) the costs of prescription drugs and costs of insurance premiums are intrinsically connected; 2) state insurance regulators have a unique role as trusted experts; and 3) to lower drug prices, solutions must address all parts of the pharmaceutical manufacturing and distribution chain.

5. Heard a Discussion of the Effects of Drug Couponing and Third-Party Payment Arrangements on the Cost ofPrescription Drugs

Jennifer Chen (Center for Health Policy & Outcomes, Memorial Sloan Kettering Cancer Center) discussed prescription drug copayment assistance programs and the potential effects of such programs on the price of prescription drugs. She explained how pharmaceutical drug manufacturers use copayment assistance programs by using coupons to provide consumers access to their prescription drugs. Ms. Chen said copayment coupons affect the health care system by: 1) diminishing price pressure; 2) keeping patients from acting as consumers; 3) undermining high-deductible/low-premium plan benefit designs and shiftingthe financial burden to the insurer; and 4) reducing negotiating leverage for insurers. She discussed how copay accumulatorsfactor into prescription drug costs and prices for consumers. Ms. Chen presented several policy recommendations forpolicymakers to consider for copayment assistance equity and limits on drug price inflation for all stakeholders involved,including pharmaceutical drug manufacturers and pharmacies.

6. Discussed State PBM Legislative Activities

Holly Weatherford (NAIC) provided an overview of recent state legislative activities concerning PBM regulation. She said the NAIC Legal Division prepared a chart highlighting state activity related to PBM regulation based on the major provisions in the proposed National Conference of Insurance Legislators’ (NCOIL) Pharmacy Benefits Manager Licensure and Regulation Model Act. She detailed the different types of PBM laws reflected in the chart. The Committee deferred additional discussion and any potential action related to the issue until a later date.

Draft Pending Adoption

© 2018 National Association of Insurance Commissioners 3

7. Heard an Update on an Issues Paper

Sarah Lueck (Center on Budget and Policy Priorities—CBPP) discussed the issue paper “Non-ACA-Compliant Plans and the Risk of Market Segmentation: Considerations for State Insurance Regulators.” She said the paper provides additional background research and information on the risks posed by alternative coverage options—such as short-term, limited-duration plans (STLDPs), association health plans (AHPs) and transitional plans—that do not comply with all or most of the federal Affordable Care Act’s (ACA) consumer protections. Ms. Lueck said the paper discusses how these plans have or will contribute to market segmentation and adverse selection against the ACA-compliant plans and result in additional individual market instability and volatility. She also discussed recent federal regulatory activities related to these alternative coverage options specifically focusing on STLDPs and the potential adverse impact of these plans on consumers due to their coverage gaps and consumer confusion. Additionally, Ms. Lueck discussed different state approaches to regulating STLDPs, including limiting the duration of such plans. Superintendent Vullo expressed support for Ms. Lueck’s comments concerning the potential for STLDPs to destabilize the individual market and harm consumers. She noted that New York has banned the sale of such plans.

8. Heard an Update from the HHS on STLDPs

William Brady (U.S. Department of Health and Human Services—HHS) updated the Committee on how HHS pursuant to the Trump administration’s Executive Order (EO) 12866 is striving to provide more affordable options and choices for consumers to obtain health insurance coverage in light of the increasing premium rates and declining insurer participation in the health insurance exchanges. Mr. Brady discussed the recently issued final federal regulations on AHPs and STLDPs in furtherance of the goals of the EO. He noted the regulations included important disclosure provisions to help to ensure consumers understand what they are purchasing prior to purchase. Mr. Brady also noted the flexibility provided to the states in the final regulations and encouraged and urged the states to take advantage of this flexibility. Mr. Wieske expressed appreciation for that flexibility. Commissioner Stolfi explained that Oregon limits the duration of STLDPs to three months. He noted that even with such a limitation on STLDPs, in Oregon, recent federal legislative and regulatory actions concerning STLDPs and AHPs and the zeroing out of the ACA’s individual mandate penalty have contributed to premium rate increases for ACA-compliant plans. Director Cameron asked about STLDP renewability. Mr. Brady said the states have different options with respect to STLDP renewability and whether to require guaranteed renewability of such plans.

9. Heard a Panel Discussion on STLDPs

The Committee heard a panel discussion on STLDPs from representatives of Health Insurance Innovations (HII), GoHealth, Simple Health Plans and IHC Carrier Solutions. Gavin Southwell (HII) discussed how STLDPs and short-term medical (STM) products benefited certain consumers, particularly given the increased premiums for ACA-compliant plans. Jan Dubauskas (IHC Carrier Solutions) discussed the evolution of STM products and new types of STM products coming to the market that provide a preexisting condition benefit to address concerns that STM products do not cover preexisting conditions. Brad Burd (GoHealth) and Cameron Girouard (Simple Health Plans) discussed how technology and enhanced websites can play a key role in ensuring consumer understanding as part of the shopping and purchasing experience. The presenters also stressed the importance of disclosures to help to ensure consumers understand what they are purchasing prior to the actual purchase because a STLDP or STM products may not be appropriate for all consumers.

Commissioner Altman noted the difference of opinion among the Committee members concerning STLDPs and STM products. She noted, however, that each Committee member agrees that disclosure and an accurate presentation of these products is essential. Commissioner Altman expressed concern about potential marketing issues related to such plans where some insurance producers or insurer websites might try to market STM products as comparable to ACA-compliant plans. She noted that in the past two years, Pennsylvania has revoked the licenses of eight agents and brokers because of deceptive marketing of these products. Commissioner Altman asked if any of the panelists have best practices for their companies to ensure these products are being marketed and sold appropriately. Mr. Southwell said HII has invested a significant amount of money to ensure adequate consumer disclosure. He said it is bad business to sell policies to consumers that do not meet their needs. Mr. Burd discussed how standardization could help to ensure consumers receive the appropriate information as part of their purchasing experience.

Director Ramge noted that consumers in Nebraska’s health insurance market could benefit from having access to STM products. He expressed concern, however, with some of the marketing practices, such as telemarketing with spoofed telephone numbers, related to the sale of such products. Mr. Southwell said HII has addressed these issues with its distribution channels. Mr. Oechsner said the ACA has worked well in New York although the same cannot be said for other states. He said STM products are substandard products being sold with the premise that “junk” insurance is better than having

Draft Pending Adoption

© 2018 National Association of Insurance Commissioners 4

no insurance and questioned whether disclosures alone will be enough to help consumers know what they are buying prior to purchase. Commissioner Jones also expressed concern with these products. He said he reviewed each of the panelists’ company websites and did not find any specific information on any of the websites about the products they sell. Mr. Southwell said HII does not sell these products on its website. Consumers are directed to an agent, and the agent provides the relevant information to the consumer. Ms. Dubauskas said it is difficult for a company doing business in more than one state to provide specific product disclosure information because each state has different requirements. 10. Heard a Briefing on the DOJ’s Determination Regarding Texas v. United States and its Potential Effects on the Market

and Enforcement Anthony Shelley (Miller & Chevalier) provided an overview of Texas v. United States. He said the case rises from a suit by 20 states and individual plaintiffs alleging the ACA is unconstitutional. The plaintiffs allege the ACA is unconstitutional because: 1) the individual mandate survived an earlier constitutional challenge because it was a tax the U.S. Congress has authority to enact; 2) the repeal of the tax penalty associated with the individual mandate means that it is not a tax anymore; and 3) because a key pillar of the ACA is now unconstitutional, the remainder of the law cannot be severed and must be declared unconstitutional as well. Fearing the Trump administration would not defend the ACA, other states and the District of Columbia successfully intervened in the case. Mr. Shelley characterized the litigation as being a “civil war” among the “red” states and the “blue” states. He discussed the likely path of the case to the U.S. Supreme Court possibly in 2019. Mr. Shelley discussed the U.S. Department of Justice’s (DOJ) position regarding the case, including its position that parts of the ACA will be determined as unconstitutional. He noted, however, that the DOJ does not agree with the plaintiff states that all of the ACA is invalid. Mr. Shelley discussed the ramifications of the DOJ’s position on the states because the DOJ’s position that parts of the ACA are unconstitutional means the federal government can and should refrain from enforcing those parts of the ACA. He said the case is a serious and potential mortal challenge to the ACA in the individual market. Mr. Shelley discussed several issues that could affect the case’s result. Those issues included: 1) the plaintiff states’ standing; 2) the Congress’ intent regarding the ACA’s severability when it zeroed out the individual mandate tax penalty without addressing the rest of the law; and 3) the impact of prior U.S. Supreme Court rulings on the constitutionality of the ACA. 11. Deferred Discussion of Various Market Approaches and State Actions Related to Market Stabilization Director Cameron said the Committee would defer until the Fall National Meeting discussion of various market approaches and state actions related to market stabilization. Having no further business, the Health Insurance and Managed Care (B) Committee adjourned. W:\National Meetings\2018\Summer\Cmte\B\08-Bmin.docx

© 2018 National Association of Insurance Commissioners 4

Agenda Item #2

Consider Adoption of its Subgroup, Working Group and Task Force Reports —Director Dean L. Cameron (ID)

• Consumer Information (B) Subgroup—Angela Nelson (MO) • CO-OP Solvency and Receivership (B) Subgroup—Commissioner Doug Ommen (IA) • Health Care Reform Regulatory Alternatives (B) Working Group

—Commissioner Ted Nickel (WI) and J.P. Wieske (WI) • Health Actuarial (B) Task Force—Director Patrick M. McPharlin (MI) and Kevin

Dyke (MI) • Regulatory Framework (B) Task Force—Commissioner Ted Nickel (WI) and J.P.

Wieske (WI) • Senior Issues (B) Task Force—Director Lori K. Wing-Heier (AK)

© 2018 National Association of Insurance Commissioners 1

Conference Calls

CONSUMER INFORMATION (B) SUBGROUP September 7, 14, and 21, 2018 October 1, 5, 19, and 30, 2018

Summary Report

The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Sept. 7, Sept. 14, Sept. 21, Oct. 1, Oct. 5, Oct. 19, and Oct. 30, 2018. During these calls, the Subgroup: 1. Developed and adopted a Health Coverage Shopping Tool. The tool is intended as a document that state regulators can

customize as appropriate and then provide to consumers in their states. The tool helps consumers compare multiple health policies and encourages them to consider coverage and out-of-pocket costs in addition to premiums.

2. Revised and adopted Frequently Asked Questions about Health Care Reform (FAQ). The FAQ is intended to be used by

state regulators to educate them about health care reform and assist them in responding to questions from consumers and others. It is not intended to be a consumer-facing document. Revisions to the FAQ included updates to reflect policy changes since the last revision and additional drafting notes to indicate where states may choose to add state-specific information.

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 9/14/18

Consumer Information (B) Subgroup Conference Call

September 7, 2018 The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Sept. 7, 2018. The following Subgroup members participated: Angela Nelson, Chair, Amy Hoyt, Mary Mealer, Jessica Schrimpf and Molly White (MO); Elaine Mellon (ID); Jenifer Groth and Karl Knable (IN); Kristi Bohn and Maybeth Moses (MN); Katie Dzurec (PA); Gretchen Brodkorb (SD); Heidi Clausen and Jaakob Sundberg (UT); Melanie Anderson and Jane Beyer (WA); and Sue Ezalarab and Julie Walsh (WI). Also participating were: Jacob Lauten (AK); Christopher Citko and Stesha Hodges (CA); Robin Taylor (DE); Matthew Guy (FL); Debra Peirce (GA); Angela Boston and Jennifer Lindberg (IA); Frank Opelka (LA); Michael Kakuk, Jeannie Keller and Ashley Perez (MT); Jennifer Patterson (NH); Chanell McDevitt (NJ) Jana Jarrett (OH); Doug Danzeiser (TX); Jackie Myers (VA); and Mark Hooker and Ellen Potter (WV).

1. Discussed Coverage Comparison Tool Ms. Nelson reminded the Subgroup that it last met on May 22. During that call, the Subgroup discussed two items: the Frequently Asked Questions About Health Care Reform (FAQ) document and the next Subgroup Project. The FAQ document is in the process of being updated and once the content has been updated, the Subgroup agreed to turn it into a training tool for insurance department staff, possibly a power point presentation, that might be useful for new employees. Ms. Nelson said a draft FAQ document would be distributed to the Subgroup for review and comment. Ms. Nelson said that, during its last call, the Subgroup agreed that a checklist-type document to help consumers compare plans would be a useful project to work on next. She said the Subgroup talked about a document that has questions and spaces for consumers to fill in the answers. Ms. Nelson said that regulators and interested parties were asked to submit suggested questions to include in a checklist for consumers. The comments that were received were circulated to the Subgroup as well as links to existing checklist-type resources for consumers to use to compare plans. Ms. Nelson pointed out that most comparison tools on the internet focus on comparing marketplace plans. Ms. Nelson said that with Association Health Plans (AHP) and short-term limited duration (STLD) plans on the horizon, Missouri is looking for a way to help their consumers make informed choices. JoAnn Volk (Georgetown University, Center on Health Insurance Reforms—CHIR) cautioned against using terms of art like “major medical” or “short-term limited duration plans” in a consumer-facing document and reminded the Subgroup that NAIC Consumer Representative Brenda Cude (University of Georgia) stands ready to perform a readability review on any consumer-facing document the Subgroup develops. Ms. Nelson said Washington has a checklist that is simple and informative. Ms. Dzurec asked whether Washington has received any feedback from consumers. She also said that healthcare.gov is a very good resource for information and perhaps the tool should have a question that refers to healthcare.gov. Ms. Volk said she was concerned about referencing healthcare.gov because there are other places authorized to sell qualified health plans. Ms. Nelson said she envisioned a more universal tool that could be useful for consumers looking beyond the marketplace for health insurance. She said that if consumer is looking at a marketplace plan, they will get a summary of benefits and coverage (SBC). Other kinds of plans will not have an SBC, so it is important to have something that will help consumers figure this out. Eric Ellsworth (Consumers’ Checkbook) said that the tool that the Subgroup develops should include a preamble explaining why consumers should ask these questions and care—that there are things beyond the premium that need to be considered. He said, for example, exclusions are going to leave consumers with the worst potential consequences. Ms. Dzurek suggested that perhaps different checklists could be developed for different audiences—the individual working three jobs but has no insurance versus the self-employed individual who may be able to get coverage under an AHP. Ms. Nelson said she liked the idea of keeping different audiences in mind, but she wants to have something available by Open Enrollment. She said she thought that questions could be crafted so that consumers will understand what they are looking at. Ms. Beyer said Washington issued a rule on STLD plans that includes an embedded template to focus on questions consumers might ask. Mr. Ellsworth said that the right checklist could take the place of an explanatory preamble. Peggy Camerino (Torchmark Corporation) cautioned against assuming features for different kinds of plans. For example, not all STLD plans have preexisting condition exclusions.

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

Ms. Nelson said that she and Ms. Mealer would put together a draft comparison tool based on the Subgroup’s conversation and distribute it to the Subgroup for discussion during its next call scheduled for Sept. 14. Having no further business, the Consumer Information (B) Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\9-7-18 confcall Reviewed.docx

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 10/2/18

Consumer Information (B) Subgroup Conference Call

September 14, 2018 The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Sept. 14, 2018. The following Subgroup members participated: Angela Nelson, Chair, Amy Hoyt, Mary Mealer and Jessica Schrimpf (MO); Yada Horace (AL); Donna Daniel and Kathy McGill (ID); Karl Knable (IN); Mary Kwei (MD); Kristi Bohn, Candace Gergen and Alley Zoellner (MN); Martin Swanson (NE); Dave Buono and Elizabeth Hart (PA); Gretchen Brodkorb and Candy Holbrook (SD); Nancy Askerlund and Jaakob Sundberg (UT); Jane Beyer (WA); and Sue Ezalarab, Barbara Belling, Jennifer Stegall and Julie Walsh (WI). Also participating were: Jacob Lauten (AK); Stesha Hodges (CA); Robin Taylor (DE); Matthew Guy (FL); Debra Peirce (GA); Angela Burke Boston and Jennifer Lindberg (IA); Renee Campbell (MI); Michael Kakuk, Pam Koenig, Jeannie Keller and Ashley Perez (MT); Eireann Aspell (NH); Jana Jarrett (OH); Brian Fordham (OR); Chris Orr (TX); Jackie Meyers (VA); and Greg Elam, Joylynn Fix, Dena Wildman and Ellen Potter (WV). 1. Discussed Coverage Comparison Tool Ms. Nelson reviewed the purpose of the document under discussion—to give the states a template for a document that helps consumers shop for health plans. Ms. Nelson asked regulators and interested parties for comments and suggestions on the draft document. JoAnn Volk (Georgetown University, Center on Health Insurance Reforms—CHIR) said the draft looks good. She added that part of educating consumers is getting them to think about the possibility of unexpected illness or injury, so something to address that could be added. Noah Isserman (Blue Cross and Blue Shield Association—BCBSA) suggested that terms like “cost-sharing” and “deductible” could use explanatory bullets—he stated that they will not mean much to consumers without them. He said order is important, noting that deductible should be covered first because consumers must pay their deductible before they get coverage. Ms. Nelson explained that, in drafting, she tried to avoid jargon. Definitions can be added if the group wants, but she really does not want to make the document too long. She said Mr. Isserman’s idea about the order of items was a great point. Mr. Isserman said the federal Centers for Medicare & Medicaid Services (CMS) designed Healthcare.gov’s shopping experience as it was launched. He said people do not understand terms like “copay” or “coinsurance.” Brenda Cude (University of Georgia) stated that there are a lot of existing materials that could be connected to this document that have been consumer-tested. Ms. Nelson and Ms. Cude discussed the format of the document and whether it would be posted online. Ms. Nelson pointed out that it would not necessarily be an NAIC document, but it would be more so something the states can take and use. Marty Mitchell (America’s Health Insurance Plans—AHIP) suggested that the document be divided into three steps: 1) answer questions on health and providers; 2) provide information about plan coverage; and 3) compare premiums and costs. Candy Gallaher (AHIP) asked about the question on the coordination of benefits, and Ms. Nelson explained that the tool is not aimed only at comprehensive health coverage, but it is intended to point out differences between other types of coverage. Chris Petersen (Arbor Strategies) suggested that the question ask about other types of coverage the consumer may have. Ms. Volk and others stated that these were included, so the question should be deleted. Mr. Mitchell said the coordination of benefits is a big issue for a small group of consumers. Ms. Nelson said the question would be deleted, but if anyone has a better way to address the issue, it could be brought back. Dennis McHugh (American Dental Association—ADA) asked whether the document would address the coverage of dental benefits at all. Ms. Nelson stated that with limited space, dental would not be addressed right now, unless subgroup members thought differently.

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

Ms. Nelson said she and Ms. Mealer would revise the draft comparison tool based on the Subgroup’s conversation and distribute it to the Subgroup for discussion. She suggested a follow-up conference call on Sept. 21, to which the group agreed. Having no further business, the Consumer Information (B) Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\Minutes 9.14.18 reviewed.docx

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 10/17/18

Consumer Information (B) Subgroup Conference Call

September 21, 2018 The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Sept. 21, 2018. The following Subgroup members participated: Angela Nelson, Chair, Amy Hoyt, Mary Mealer, Jessica Schrimpf and Molly White (MO); Elaine Mellon (ID); Jenifer Groth and Karl Knable (IN); Kristi Bohn and Maybeth Moses (MN); Katie Dzurec (PA); Gretchen Brodkorb (SD); Heidi Clausen and Jaakob Sundberg (UT); Melanie Anderson and Jane Beyer (WA); and Sue Ezalarab and Julie Walsh (WI). Also participating were: Jacob Lauten (AK); Christopher Citko and Stesha Hodges (CA); Robin Taylor (DE); Matthew Guy (FL); Debra Peirce (GA); Angela Boston and Jennifer Lindberg (IA); Frank Opelka (LA); Michael Kakuk, Jeannie Keller and Ashley Perez (MT); Jennifer Patterson (NH); Chanell McDevitt (NJ) Jana Jarrett (OH); Doug Danzeiser (TX); Jackie Myers (VA); and Mark Hooker and Ellen Potter (WV). 1. Discussed FAQ Ms. Nelson reminded the Subgroup that revisions to the Frequently Asked Questions About Health Care Reform (FAQ) document were posted on the Subgroup’s web page. She explained that the Subgroup is looking for input on the best way to convert the FAQ into a training tool for insurance departments to use to train employees—most likely individuals in the insurance departments’ consumer services divisions. Ms. Nelson pointed out that the section in the FAQ on the individual mandate was removed, with the idea the states with a state-based individual mandate could add a section describing it. Ms. Nelson also asked the states to consider how much information should be added to address alternative coverage options such as short-term limited duration plans or association health plans, given the variation among the states. 2. Discussed Revised Health Insurance Shopping Tool Ms. Nelson said a revised draft Health Insurance Shopping Tool was posted on the Subgroup’s web page for discussion on the call. NAIC consumer representative had submitted comments, which were also posted. The Subgroup reviewed the comments. Brenda Cude (University of Georgia) suggested that the Subgroup choose “coverage,” “policy” or “insurance” and use that term consistently. The Subgroup agreed to use the term “insurance” throughout. The Subgroup discussed a comment submitted by JoAnn Volk (Georgetown University, Center on Health Insurance Reforms—CHIR) suggesting, in addition to the sentence along the top of the document, “This tool has questions to help you compare health insurance policies and find coverage that best meets your needs,” the following concept should be added: “To answer these questions, you will need to gather plan documents, including the Summary of Benefits and Coverage if one is available for your plan. You may also need to call the insurer or talk to a Navigator or broker to get some of these answers.” Ms. Nelson agreed that this concept made sense to incorporate. The Subgroup discussed comments submitted by Eric Ellsworth (Consumers’ Checkbook) and Silvia Yee (Disability Rights Education and Defense Fund—DREDF) regarding the introductory language. Mr. Ellsworth suggested that consumers should be thinking about other things in addition to premium, such as prescriptions, doctors and other services. Ms. Yee suggested consumers needed to think about the other aspects of cost beyond premium, such as copays and deductibles. Ms. Cude suggested saying something like, “Don’t focus only on the premium; there more to consider than just cost.” Ms. Nelson agreed with these comments, noting that an initial mention of all the aspects of choosing health insurance grounds people. She said she would incorporate these concepts in the next draft. The Subgroup discussed moving the section titled “Information That is Important to Me” to the top of the document. Ms. Nelson agreed that it made sense to have consumers focus on assessing their own needs first, what the plans cover second and the cost last. The Subgroup discussed the direction to, “List the conditions you or your family have. Does this policy cover them?” and agreed that the wording is confusing. Ms. Nelson said she is trying to make sure that consumers think about themselves and anyone else covered under the plan. She agreed to revise it to get at that issue more clearly.

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

The Subgroup discussed pre-existing conditions and waiting periods and whether consumers are going to understand what those are. Ms. Nelson said the challenge is to keep this document short and focus in on the issues that will be most useful to consumers comparing different types of coverage—some that will cover pre-existing conditions and some that does not cover and others that may cover some conditions after a waiting period. Ms. Nelson said relocating the information will help and agreed to consider how else to highlight these issues in the next draft. The Subgroup agreed to simplify the question, “If I continue to pay my premiums on time, can this policy be cancelled or not renewed if I develop a health condition?” The Subgroup discussed the relevance of the question, “Will my doctor or hospital bill the insurance company, or do I have to pay up front and get reimbursed?” Ms. Nelson said her intention was to highlight whether the insurance was indemnity or network. The Subgroup agreed to keep the question, realizing that the states could always eliminate it if it is not an issue in their state. The Subgroup discussed the questions about prescription drugs and agreed there should be a line for specialty drugs. The Subgroup discussed the concepts of coinsurance and copayments and agreed to revise the questions in the section titled, “What Does This Plan Cover?” to better address these concepts. The Subgroup discussed whether there should be a reference to the Summary of Benefits and Coverage (SBC), which contains a lot of this information. Ms. Nelson said this tool is specifically designed to facilitate comparing different types of insurance, including those without an SBC. Consequently, she said she prefers to not reference the SBC and avoid any confusion by consumers who may look for an SBC for an insurance policy that does not have one. Ms. Mealer suggested that the states that would like to, could include a link to healthcare.gov. Ms. Nelson said she and Ms. Mealer would revise the draft Health Insurance Shopping Tool based on the Subgroup’s conversation and distribute it to the Subgroup for discussion during its Oct 1 conference call. Having no further business, the Consumer Information (B) Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\9-21-18 confcall final.docx

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 10/10/18

Consumer Information (B) Subgroup Conference Call October 1, 2018

The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Oct. 1, 2018. The following Subgroup members participated: Angela Nelson, Chair, and Amy Hoyt (MO); William Rodgers and Anthony Williams (AL); Elaine Mellon (ID); Cindy Hermes (KS); Mary Kwei (MD); Alley Zoellner (MN); Cuc Nguyen (OK); Katie Dzurec and Elizabeth Hart (PA); Candy Holbrook (SD); Tanji Northrup (UT); and Rebecca Rebholz, Barbara Belling, Jennifer Stegall and Julie Walsh (WI). Also participating were: Chantel Allbritton (AR); Stesha Hodges (CA); Matthew Guy (FL); Debra Peirce (GA); Bob Williams (MS); Michael Kakuk and Ashley Perez (MT); Yolanda Tennyson (VA); and Joylynn Fix, Dena Wildman and Ellen Potter (WV); Denise Burke (WY).

1. Discussed the Coverage Comparison Tool Ms. Nelson thanked the group for meeting on short notice and said that open enrollment for health insurance would begin in one month. She reviewed the goals for the document under discussion: 1) make it broad-based rather than focused on any one type of product; 2) allow consumers to understand a broader range of choices, including short-term plans and association health plans (AHPs); and 3) make it basic and prompt consumers to ask the appropriate questions. Ms. Nelson expressed a goal of getting the document to state insurance regulators within a couple of weeks. She began discussing the document, starting with the Opening Section and Part 1. JoAnn Volk (Georgetown University, Center on Health Insurance Reforms—CHIR) asked whether family history, which an insurer might consider a preexisting condition, is intended to be included in the question on preexisting conditions. She also asked whether the document would include links to a glossary. Ms. Nelson responded that states can add links or other resources if they would like, but they have not been added yet due to space constraints. Ms. Mellon suggested removing the reference to preexisting conditions in the health services question and providing more space to list doctors. Continuing to Part 2, Ms. Nelson explained she wanted to reference the Summary of Benefits and Coverage (SBC), but users can also ask someone they are working with if they do not know the answers to some of the questions about the comparison plans. Debra Judy (Colorado Consumer Health Initiative—CCHI) said that coverage limitations could take forms other than visit limits. She cited as an example health care sharing ministries that have a 10-month waiting period for maternity coverage. Ms. Nelson suggested changing the question of coverage of preexisting conditions, but Ms. Judy preferred that other restrictions be mentioned closer to the specific benefit categories. Ms. Miller suggested that the prescription drug tiers be defined, perhaps in parentheses. Eric Ellsworth (Consumer Checkbook) suggested using “generic” and “brand” rather than “Tier 1” and “Tier 2.” This does not line up with the SBC, but the SBC still has the best information. He said that consumers do not understand tiering. Ms. Mellon asked whether the tool should ask users to list specific drugs and their costs. Others thought this would be difficult. Ms. Nelson questioned whether the two mental health categories should be combined to save space, but Ms. Mellon and others said they should stay as is. Ms. Nguyen asked whether the document addresses maximum out-of-pocket amounts, and Ms. Nelson pointed out where it does. Ms. Nelson asked whether the Subgroup would be amenable to adopting the document via email once the changes suggested during the conference call were made. The Subgroup members generally agreed. Ms. Nelson stated that the Subgroup could make available both Microsoft Excel and portable document format (PDF) versions of the document, and states could customize it as they choose.

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

Ms. Nelson brought up the other document the Subgroup has committed to working on—Frequently Asked Questions (FAQ) About Health Care Reform. She asked whether the Subgroup would be ready to have another call in the near future to discuss it and asked about timing. Ms. Dzurec stated that the document is critical and that NAIC staff need it to get ready for open enrollment. She encouraged the Subgroup to move quickly in updating it. Ms. Nelson and others discussed possible times for a subsequent call devoted to the FAQ document and decided to schedule one for Oct. 5. Having no further business, the Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\Minutes 10.1.18 reviewed.docx

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 10/22/18

Consumer Information (B) Subgroup Conference Call October 5, 2018

The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Oct. 5, 2018. The following Subgroup members participated: Angela Nelson, Chair, Carrie Couch and Amy Hoyt (MO); Kathy McGill and Elaine Mellon (ID); Greta Hockwalt and Karl Knable (IN); Cindy Hermes (KS); Holly Doherty (ME); Joy Hatchette (MD); Kristi Bohn, Melinda Domzalski-Hansen, Candace Gergen and Alley Zoellner (MN); Martin Swanson (NE); Kathy Shortt (NC); Katie Dzurec (PA); Candy Holbrook (SD); Heidi Clausen and Jaakob Sundberg (UT); and Diane Dambach, Sue Ezalarab, Barbara Belling and Jennifer Stegall (WI). Also participating were: Robin Taylor (DE); Matthew Guy (FL); Mike Chrysler (IL); Pam Koenig (MT); Chanell McDevitt (NJ); Jana Jarrett (OH); Sarah Mathews and Patrick Merkel (TN); Yolanda Tennyson (VA); and Theresa Miller, Timothy Sigman and Ellen Potter (WV). 1. Adopted the Health Insurance Shopping Tool Ms. Nelson asked for an update on e-votes for adoption of the Health Insurance Shopping Tool. Joe Touschner (NAIC) reported that there were five votes submitted via email in favor of adoption. Ms. Nelson suggested that Subgroup members could provide their votes on the call if they had not already sent them by email. The roll was called and, combined with the e-votes, the total was 11 in favor of adoption and none opposed. The document was adopted (Attachment Health Coverage Shopping Tool.pdf). Ms. Nelson said that both Excel and PDF versions of the tool should be distributed to the states. She suggested the states could customize the tool as they find appropriate, especially because it uses many terms that consumer may not know, so the states can add links to definitions and other resources. 2. Discussed the FAQ Ms. Nelson reminded the group that the Frequently Asked Questions about Health Care Reform (FAQ) document was distributed Tuesday and she said she hoped participants had had a chance to review it. Ms. Nelson said she would like to focus on two areas. The first is what the document should say about short-term plans. Some participants expressed support for a general overall statement on short-term plans and the applicability of federal Affordable Care Act (ACA) protections, perhaps in Question 4. JoAnn Volk (Georgetown University, Center on Health Insurance Reforms—CHIR) asked whether there would be one separate section on ACA-compliant plans. Ms. Nelson said there should be a central touchstone so everyone has the same grounding. Ms. Dzurec said that many people will use the document, including market conduct, consumer services and legal staff. Mr. Swanson and Ms. Volk mentioned other types of plans that do not observe ACA protections, such as health care sharing ministries, association health plans and indemnity plans. The group discussed state authority over health care sharing ministries. Ms. Nelson said there could be a note at the beginning that says the states can tailor the answers based on their needs, as well as notes in answers saying the states may want to change the answer. Ms. Volk warned that users searching the document might jump to a particular question and lose context provided earlier. Ms. Dzurec mentioned that the federal Center for Consumer Information and Insurance Oversight (CCIIO) website has a checklist, with citations to regulations and a column for applicability. Ms. Nelson summarized the current suggestion as a new question on plans that do not have to be compliant, with a drafting note for the states to modify.

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 2

Ms. Nelson introduced the next topic as the FAQ’s treatment of the individual mandate. Mr. Swanson suggested a simple statement that the mandate is in effect but there is no penalty, as well as notify consumers they may be eligible for a rebate if only one insurer is available to them in the marketplace. Ms. Volk suggested adding language on why a consumer should buy coverage even if there is no mandate. Ms. Nelson said she is unsure whether this answer would be too long and whether it is really about the individual mandate or special enrollment periods (SEPs) and the importance of coverage. Ms. Volk mentioned that the Center on Budget and Policy Priorities has a great chart on SEPs. Ms. Nelson suggested that the document move forward with an answer like the one suggested by Mr. Swanson. Mr. Touschner asked whether other mandate-related questions on exceptions and exemptions should be retained. Ms. Nelson said one question should be retained, others could be eliminated, maybe with a link to other websites with information on exceptions and exemptions. The Subgroup discussed whether the next version of the document should show redline changes from the previously approved version or from the latest revision. Ms. Nelson concluded it should show changes from the latest revision. Ms. Volk suggested that the document not refer to “most” health plans offering certain protections because it is unclear whether that will be the case. The Subgroup decided to meet again Oct. 19 via conference call. Having no further business, the Consumer Information (B) Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\Minutes 10.5.18 reviewed.docx

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 10/30/18

Consumer Information (B) Subgroup Conference Call October 19, 2018

The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Oct. 19, 2018. The following Subgroup members participated: Angela Nelson, Chair, Jessica Schrimpf and Amy Hoyt (MO); Elaine Mellon (ID); Karl Knable (IN); Joy Hatchette (MD); Judith Watters (ME); Cuc Nguyen and Mike Rhodes (OK); Elizabeth Hart, Katie Dzurec (PA); Gretchen Brodkorb, Candy Holbrook and Melissa Klemann (SD); Nancy Askerlund (UT); and Susan Ezalarab, Barbara Belling and Jennifer Stegall (WI). Also participating were: Robin Taylor (DE); Howard Liebers (DC); Pamela White (FL); Pam Koenig (MT); Glenn Shippey (NV); Sarah Mathews (TN); Yolanda Tennyson (VA); and Joylynn Fix, Tom Whitener, Dena Wildman and Ellen Potter (WV). 1. Discussed the Health Insurance Shopping Tool Ms. Nelson reminded the Subgroup that the Health Insurance Shopping Tool was distributed the week of Oct. 8. She mentioned that it was sent in both Excel and PDF versions to give the states the ability to make modifications and add information such as links or definitions. 2. Discussed the FAQ JoAnn Volk (Georgetown University, Center on Health Insurance Reforms—CHIR) stated that changes to the Frequently Asked Questions about Health Care Reform (FAQ) had gone a long way to making it more clear, but there are still some tweaks she would recommend. She questioned whether greater precision is needed in this document or possibly another. The Subgroup discussed whether the document is intended to be consumer-facing. Ms. Nelson said that the original intent is that it is not. Ms. Watters stated that Maine completely modified the document before it was used in the state. Brenda Cude (University of Georgia) stated that the language is not consumer-friendly and suggested a stronger warning that the language should not be used as-is in consumer materials. The Subgroup discussed a variety of wording changes, focusing on questions 4, 12, 24, 25, 57, 108, 125 and 127. Ms. Volk and Jessica Waltman (National Association of Health Underwriters) made several suggestions for edits and promised to send changes in writing. Ms. Watters and Ms. Mellon offered further suggestions. The Subgroup decided to next meet Oct. 30 via conference call. Having no further business, the Consumer Information (B) Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\Minutes 10.19.18 reviewed.docx

Attachment Three Health Insurance and Managed Care (B) Committee

11/16/18

© 2018 National Association of Insurance Commissioners 1

Draft: 11/7/18

Consumer Information (B) Subgroup Conference Call October 30, 2018

The Consumer Information (B) Subgroup of the Health Insurance and Managed Care (B) Committee met via conference call Oct. 30, 2018. The following Subgroup members participated: Angela Nelson, Chair, Mary Mealer and Amy Hoyt (MO); Elaine Mellon (ID); Karl Knable (IN); Joy Hatchette and Mary Kwei (MD); Alley Zoellner (MN); Mike Rhoads (OK); Gretchen Brodkorb, Candy Holbrook and Melissa Klemann (SD); Heidi Clausen and Jaakob Sundberg (UT); and Christina Keeley, Diane Dambach, Eric Cormany, Mary Kay Rodriguez, Sue Ezalarab, Rebecca Rebholz and Barbara Belling (WI). Also participating were: Dayle Axman (CO); Matthew Guy and Vicki Twogood (FL); Debra Peirce (GA); Angela Burke Boston (IA); Bob Williams (MS); Jana Jarrett (OH); Rachel Jrade-Rice (TN); Jackie Myers (VA); and Timothy Sigman and Ellen Potter (WV). 1. Discussed the FAQ Ms. Nelson thanked the Subgroup for the good discussion during its previous Oct. 19 conference call. She mentioned that revisions had been made to the Frequently Asked Questions about Health Care Reform (FAQ), and a new version had been distributed earlier in the day. Ms. Nelson asked if the Subgroup had any concerns with the revisions or comments in the document. Joseph Touschner (NAIC) said it would be beneficial to have direction on how to address comments that did not include a specific suggestion, such as those that marked a passage as unclear. Ms. Nelson led the Subgroup in addressing each of the comments in the document. The Subgroup discussed and agreed on final wording for each passage that had a comment (Attachment FAQ 10.30.18). Ms. Nelson asked for an e-vote once the agreed-upon changes are incorporated into the document. In order to have the document ready for the start of Open Enrollment on Nov. 1, the group agreed to establish Oct. 31 as the deadline for electronic voting. Having no further business, the Consumer Information (B) Subgroup adjourned. W:\National Meetings\2018\Fall\Cmte\B\CnsmrInfoSG\Cnsmr.Info.10.30.Min.docx

© 2018 National Association of Insurance Commissioners 1

Conference Call

CO-OP SOLVENCY AND RECEIVERSHIP (B) SUBGROUP

September 19, 2018

Summary Report The CO-OP Solvency and Receivership (B) Subgroup met via conference call on September 19, 2018. During these meetings, the Subgroup met in regulator-to-regulator session pursuant to paragraph 3 (specific companies, entities or individuals, including, but not limited to, collaborative financial and market conduct examinations and analysis) of the NAIC Policy Statement on Open Meetings to receive updates from impacted states on Consumer Operated and Oriented Plan (CO-OP) receiverships and lawsuits. Pursuant to the Subgroup’s charge, the Subgroup continues to provide a forum via quarterly conference calls for state insurance regulators to discuss and share information on the status of CO-OPs created under the federal Affordable Care Act (ACA).

© 2018 National Association of Insurance Commissioners 5

Agenda Item #4 Hear a Presentation on Health Care Cost Drivers, Network Adequacy Issues and Surprise Billing—Dr. Jack Resneck (American Medical Association—AMA)

© 2018 National Association of Insurance Commissioners 6

Agenda Item #5 Hear a Briefing on State Legislative and Administrative Actions to Address Prescription Drug Cost-Sharing—Carl Schmid (The AIDS Institute)

State Actions to Increase Patient Affordability of

Prescription Drugs

Carl SchmidThe AIDS Institute

Washington DC

National Association of Insurance CommissionersNovember 16, 2018

1

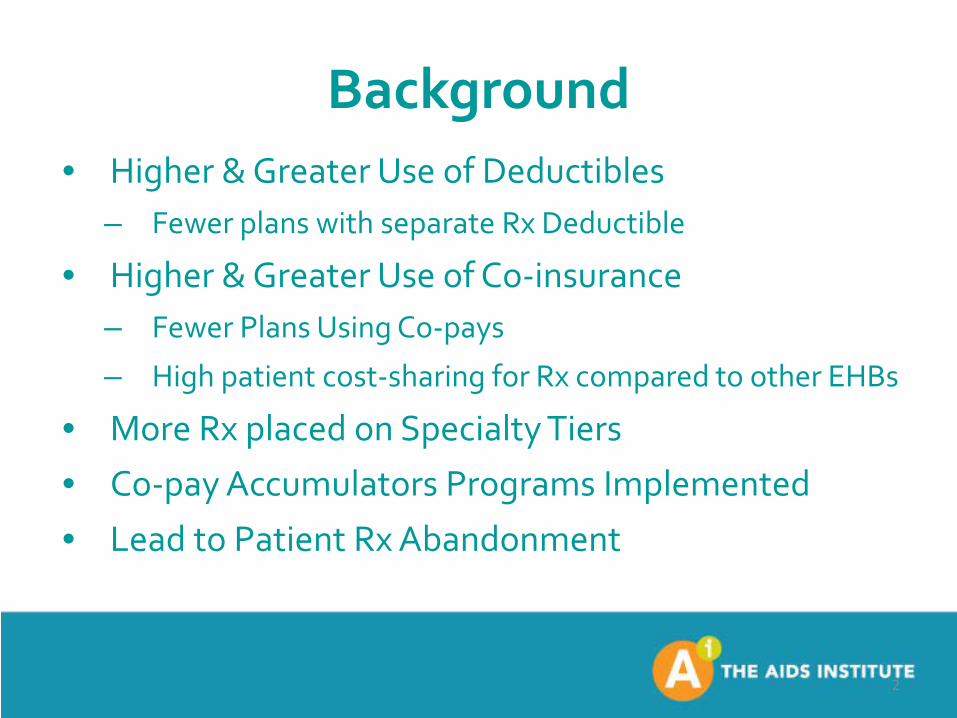

Background• Higher & Greater Use of Deductibles

– Fewer plans with separate Rx Deductible

• Higher & Greater Use of Co-insurance– Fewer Plans Using Co-pays

– High patient cost-sharing for Rx compared to other EHBs

• More Rx placed on Specialty Tiers• Co-pay Accumulators Programs Implemented

• Lead to Patient Rx Abandonment

2

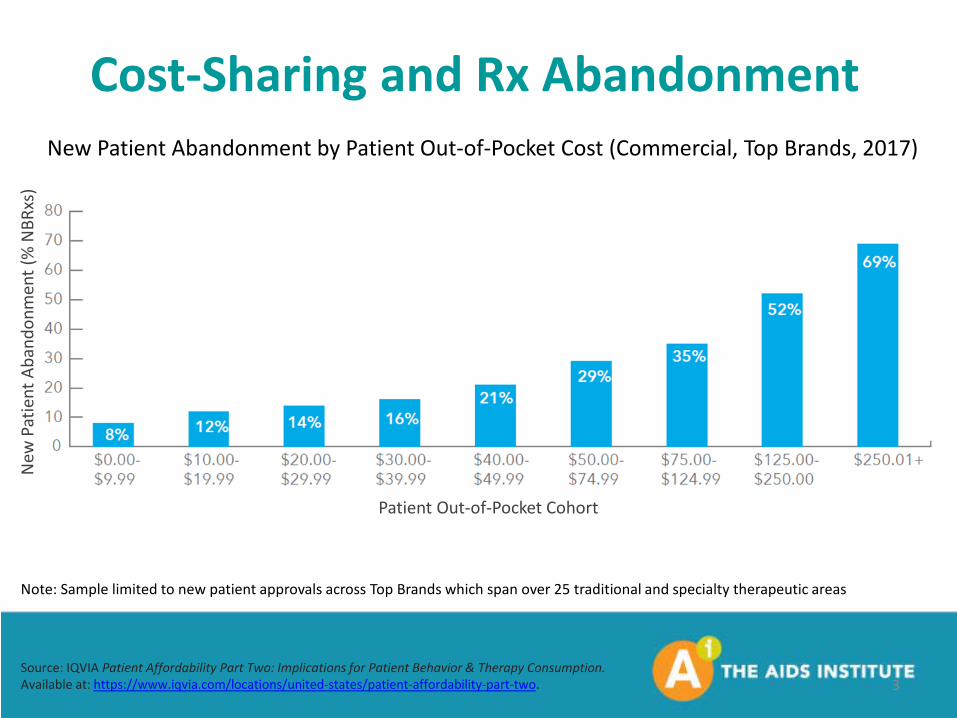

Cost-Sharing and Rx Abandonment

3Source: IQVIA Patient Affordability Part Two: Implications for Patient Behavior & Therapy Consumption. Available at: https://www.iqvia.com/locations/united-states/patient-affordability-part-two.

New Patient Abandonment by Patient Out-of-Pocket Cost (Commercial, Top Brands, 2017)

Patient Out-of-Pocket Cohort

New

Pat

ient

Aba

ndon

men

t (%

NBR

xs)

Note: Sample limited to new patient approvals across Top Brands which span over 25 traditional and specialty therapeutic areas

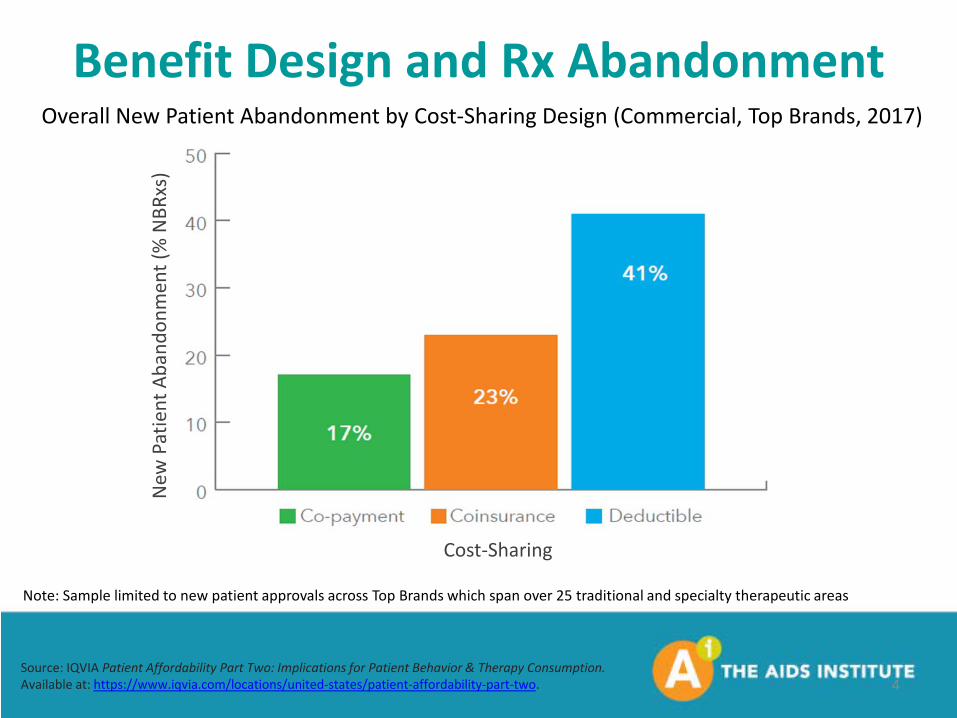

Benefit Design and Rx Abandonment

4Source: IQVIA Patient Affordability Part Two: Implications for Patient Behavior & Therapy Consumption. Available at: https://www.iqvia.com/locations/united-states/patient-affordability-part-two.

New

Pat

ient

Aba

ndon

men

t (%

NBR

xs)

Cost-Sharing

Note: Sample limited to new patient approvals across Top Brands which span over 25 traditional and specialty therapeutic areas

Overall New Patient Abandonment by Cost-Sharing Design (Commercial, Top Brands, 2017)

Copay Cards and Rx Abandonment

5Source: IQVIA Patient Affordability Part Two: Implications for Patient Behavior & Therapy Consumption. Available at: https://www.iqvia.com/locations/united-states/patient-affordability-part-two.

New

Pat

ient

Aba

ndon

men

t (%

NBR

xs)

Note: Sample limited to new patient approvals across Top Brands which span over 25 traditional and specialty therapeutic areas

New Patient Abandonment by Year and Patient Coupon Use (Commercial, Top Brands)

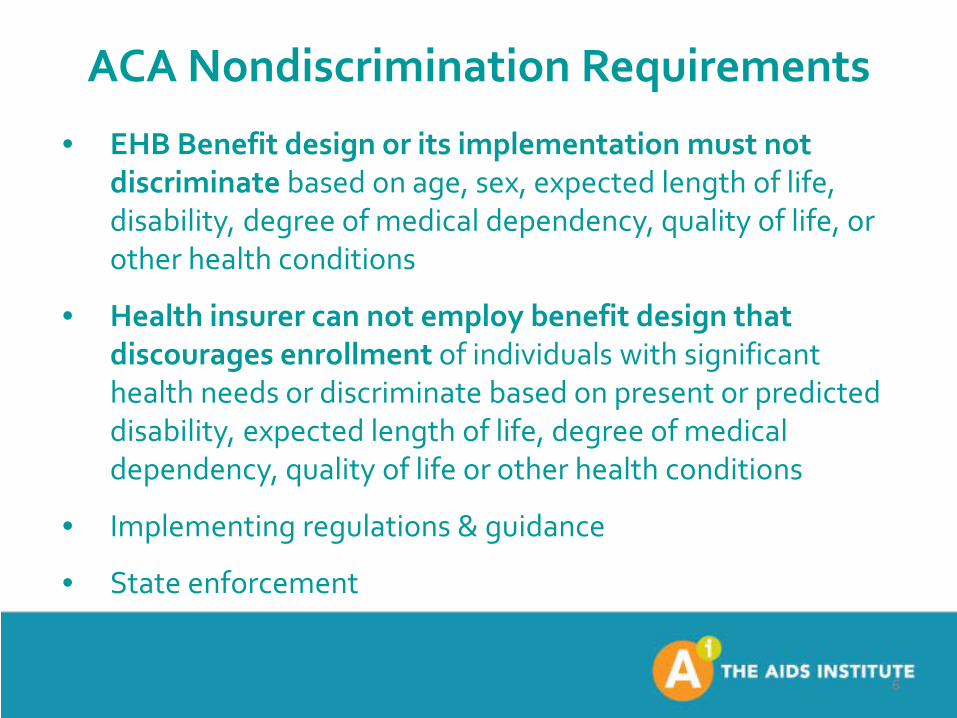

ACA Nondiscrimination Requirements

• EHB Benefit design or its implementation must not discriminate based on age, sex, expected length of life, disability, degree of medical dependency, quality of life, or other health conditions

• Health insurer can not employ benefit design that discourages enrollment of individuals with significant health needs or discriminate based on present or predicted disability, expected length of life, degree of medical dependency, quality of life or other health conditions

• Implementing regulations & guidance

• State enforcement

6

What Are States Doing?

• Enforcement Actions

• Prohibiting Specialty Tiers

• Capping co-pays

• Limit out-of-pocket maximum

• Required/Standardized Benefit Design

7

Florida HIV Rx Co-pay Limits• The AIDS Institute filed federal Discrimination Complaint against 4

insurers for placing all HIV Rx on highest tier & requiring Prior Authorization