health insurance exchange (hix): hix the basics€¦ · health insurance exchange (hix): hix –...

TRANSCRIPT

Health Insurance Exchange (HIX):

HIX – the Basics

Sheila Cooper, Client Executive

Robin Chacon, Client Executive

August 19, 2012

Agenda

8/19/12 © 2012 CSG Government Solutions 2

Overview of HIX basics

Exchange governance

Managing challenging timeframes

The evolution of Medicaid as health insurance

Eligibility determination: demystifying Modified Adjusted Gross Income (MAGI)

Discussion of challenges faced by states

HIX Basics

8/19/12 © 2012 CSG Government Solutions 3

A Health Insurance Exchange:

Is a marketplace for consumers to purchase commercial health insurance coverage. Types of plans offered include individual policies and small group policies.

Establishes a single access point to health coverage programs including Medicaid, CHIP, and publicly-subsidized commercial insurance.

Supports both individual and small group insurance markets.

Provides premium tax credits for eligible individuals to purchase health coverage.

Offers a two-year tax credit that subsidizes premium costs for eligible small employers that have lower-wage workers.

HIX Basics

8/19/12 © 2012 CSG Government Solutions 4

Patient Protection and Affordable Care Act (ACA) rules governing the Exchange can be found primarily in three parts: Establishment of Exchanges and Qualified Health Plans;

Exchange Standards for Employers 45 CFR Subparts 155, 156, and 157

Medicaid Program Eligibility Changes under ACA found in 42 CFR Subparts 431,435, and 457

Standards Related to Reinsurance, Risk Corridors, and Risk Adjustment found in 45 CFR Part 135

HIX Basics

8/19/12 © 2012 CSG Government Solutions 5

ACA created the ability for state’s to establish a State-based Exchange entity or elect (default) to a Federally-facilitated Exchange (FFE).

The primary functions of the Exchange include: Eligibility and enrollment for Individuals into Insurance

Affordability Programs, Medicaid, CHIP

Eligibility and enrollment for Small Business Health Options Program (SHOP)

Plan Management

Financial Management

Consumer Assistance for the Exchange

State/Federal Exchange Models

8/19/12 © 2012 CSG Government Solutions 6

State-based Exchange Model – All core functions of the Exchange are operated by the state. Must have HHS approval by 1/1/13.

Consortium or Regional Exchange Model – More than one state partner together to establish an exchange that serves the population of participating states. Must have HHS approval by 1/1/13.

Federal Partnership Exchange Model –States may elect to participate in the Federally-facilitated Exchange (FFE) model but retain and operate certain functions of the Exchange. Primary example would be the state retaining the functions of plan management and consumer assistance and eligibility and enrollment managed by the FFE.

Federally-facilitated Exchange Model – All core functions of the Exchange are operated by the United States Department of Health and Human Services (HHS) on behalf of a state.

HIX Basics: Supreme Court Ruling

8/19/12 © 2012 CSG Government Solutions 7

The individual mandate was upheld without modification. Implication: timeframes are extremely short, open

enrollment begins 10/1/13

Medicaid expansion was made optional for states; states who chose not to participate in the expansion will not lose existing federal Medicaid funding Implication: states who chose not to expand Medicaid will

need additional state $$ (see next slide)

Upheld that it is within the regulative authority for the government to require guaranteed issue. Implication: risk adjustment will play a critical role

HIX Basics: Supreme Court Ruling

8/19/12 © 2012 CSG Government Solutions 8

States have the option to expand Medicaid and considerations include:

Initial federal funding under the ACA provides for three years of 100% Federal Medical Assistance Percentage (FMAP) for the expansion population. Beyond this initial three year period, there is a phased reduction in this FMAP rate until the state’s rate is equal for both the current population and the expansion population.

Individuals under 100% of FPL are ineligible for the tax credit and would not be covered by Medicaid if a state chose not to take part in the Medicaid expansion.

All Medicaid rules such as eligibility determination using modified adjusted gross income (MAGI), maintenance of effort requirements, etc. will apply regardless of whether or not a state chooses to expand Medicaid.

HIX Basics: the Exchange Entity

8/19/12 © 2012 CSG Government Solutions 9

An Exchange entity must be one of the following:

An incorporated non-profit entity with demonstrated experience on a state or regional basis in the individual and small group health insurance markets and in benefits coverage. Can not be a health insurance issuer.

The state Medicaid agency

Other state agency

An Exchange that is a non-profit or an independent state agency must have a governing board and follow prescribed board member composition and principles.

A state may elect to have an FFE or, if a state does not have a “blueprint” conditionally approved by HHS by 1/1/13, the state will be defaulted to the FFE.

Eligibility and Enrollment

8/19/12 © 2012 CSG Government Solutions 10

Eligibility determination functions include: Accept and process applications

Conduct verifications of applicant information

Determine eligibility for enrollment in a QHP

Determine or assess Medicaid & CHIP eligibility

The Exchange must follow federal rules for verification of application data: Use of Modified Adjusted Gross Income (MAGI) income

methodology

Use of federal Data Hub envisioned for citizenship, residency, and income data elements

On-line, real-time verification is envisioned

Enrollment of individual into QHP, Medicaid, CHIP, as applicable.

Enrollment into Minimum Essential Coverage (MEC) is required. Consumer choice on Medal level of plan

Eligibility Complexity: Premium Tax Credit

8/19/12 © 2012 CSG Government Solutions 11

Household income must be between 100% and 400% of the Federal Poverty Level.

Covered individuals must be enrolled in a Qualified Health Plan (QHP).

Covered individuals must be legally present in the U.S., not incarcerated, and not eligible for other qualifying coverage (e.g. Medicare, other employer-sponsored coverage).

The credit amount is generally equal to the difference between the premium for the “benchmark plan” and the taxpayer’s expected contribution and capped at the premium amount (so that no one receives a credit that is larger than the amount they actually pay for their plan.

The credit may be advanced, with advance payments made directly to the insurance plan on the individual’s behalf and reconciled at the end of the year.

Eligibility Complexity

8/19/12 © 2012 CSG Government Solutions 12

Depending on whether a state chooses state-based or FFE, the interface between the Insurance Affordability Programs and Medicaid is complex.

Single stream-lined application: difference in the amount of information needed for MAGI versus Non-MAGI Medicaid.

Business process flows for Insurance Affordability Programs and Medicaid – ensuring individuals have a “seamless” experience.

Medicaid assessment versus full determination: Medicaid assessment data could be standardized across states and the FFE.

Eligibility Complexity: FFE

8/19/12 © 2012 CSG Government Solutions 13

SHOP

8/19/12 © 2012 CSG Government Solutions 14

The Exchange requires states to establish Small Business Health Option Program (SHOP) Exchanges to help small employers find and purchase health insurance for their employees, to assist qualified employers, and to facilitate the enrollment of qualified employees into qualified health plans (QHP’s).

The design of the SHOP exchange encompasses many features and policy considerations that make it distinct from the individual exchange including:

The SHOP Exchange must bill employers

The SHOP Exchange must collect premium payments

The SHOP Exchange must make payments to QHP’s for all enrollees

States face challenges developing successful SHOP exchanges: the value proposition for the SHOP exchange is less obvious.

Plan Management

8/19/12 © 2012 CSG Government Solutions 15

The State Insurance Agency (in most states) will work with the issuer to certify and manage the Qualified Health Plan (QHP).

Plan management functions include: Oversee plan selection and shopping approach

Certify, recertify, and decertify QHPs

Collection and analysis of plan rate and benefit package information

Issuer monitoring and oversight

Ongoing issuer account management

Issuer outreach and training

Possibly advantageous for state’s with large Medicaid managed care programs to align the QHP offering with the Medicaid MCO offering in order to provide continuity to individuals who move in and out of coverage groups.

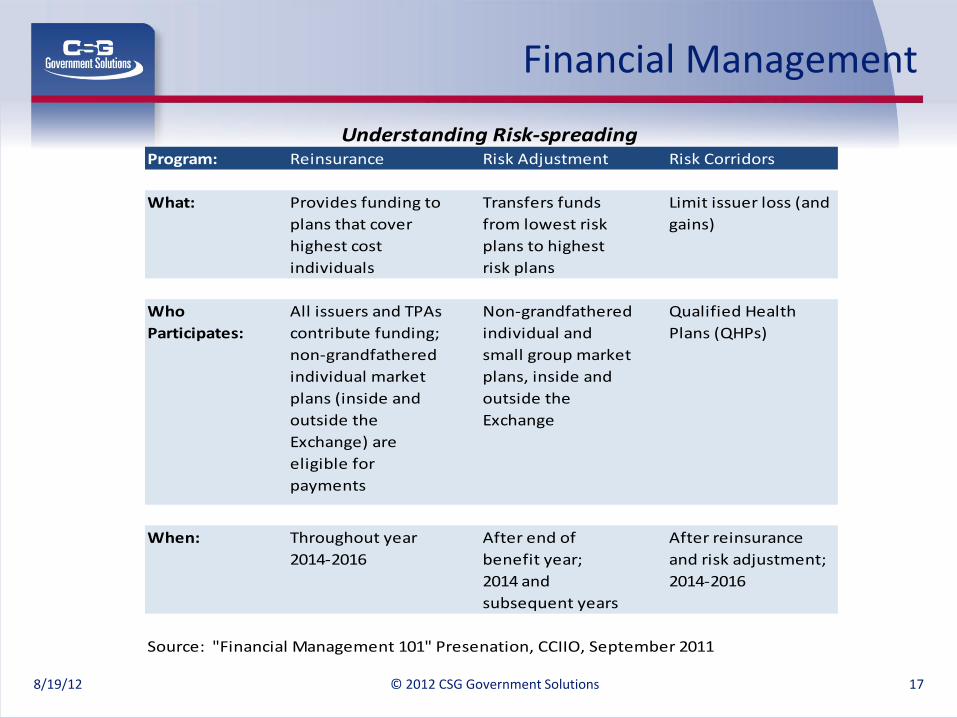

Financial Management

8/19/12 © 2012 CSG Government Solutions 16

Financial management functions include: Reporting of advance premium tax credits (APTCs) and

cost-sharing reductions (CSRs)

Premium processing and reporting

Financial sustainability revenue model to support exchange operations costs for state-based exchanges

Reinsurance, risk adjustment and risk corridor programs designed to spread the risk across markets to minimize the impacts of adverse selection and to stabilize premiums. (see next slide)

Program integrity and audit functions to ensure adequate financial controls and to detect fraud, waste and abuse.

Financial Management

8/19/12 © 2012 CSG Government Solutions 17

Program: Reinsurance Risk Adjustment Risk Corridors

What: Provides funding to

plans that cover

highest cost

individuals

Transfers funds

from lowest risk

plans to highest

risk plans

Limit issuer loss (and

gains)

Who

Participates:

All issuers and TPAs

contribute funding;

non-grandfathered

individual market

plans (inside and

outside the

Exchange) are

eligible for

payments

Non-grandfathered

individual and

small group market

plans, inside and

outside the

Exchange

Qualified Health

Plans (QHPs)

When: Throughout year

2014-2016

After end of

benefit year;

2014 and

subsequent years

After reinsurance

and risk adjustment;

2014-2016

Source: "Financial Management 101" Presenation, CCIIO, September 2011

Understanding Risk-spreading

Consumer Assistance

8/19/12 © 2012 CSG Government Solutions 18

Education and outreach

Website management

Call center management

Written correspondence with consumers to support eligibility and enrollment

Consumer appeals

Navigator management. Navigators are public or private entities or individuals that are qualified to assist consumers in “navigating” the eligibility and enrollment process. Qualifications will be determined by the Exchange and may

include licensure, certification or other standards established by the Exchange.

Governance

8/19/12 © 2012 CSG Government Solutions 19

State-based Exchange Model – select a governance and administration option that meets the state’s vision for:

Control/Authority: Executive Board, Advisory Board

Flexibility: The ability to adapt to changing policy and regulations

Accountability: Level of transparency

Interagency Coordination: Level of coordination required and/or supported by model

Federally-facilitated Exchange Model – the Final Rule is silent on the requirements for governance of states participating in the federal exchange, so states have greater flexibility.

States will need the authority to enter into an agreement with HHS.

Even Federal Exchange participation will require state interaction. If a Federal Partnership model is selected, the State will need to select a model for overseeing the state-based functions.

Financial Sustainability

8/19/12 © 2012 CSG Government Solutions 20

Affordable Care Act 1311(d)(5)(A) requires Exchanges to be self-sustaining.

State-based Exchanges must provide a long-term operational budget and management plan, monitoring of finances, and tracking of costs and revenues.

State-based Exchanges must define methods for generating revenue (e.g., user fees).

States electing/defaulting to the FFE must pay fees for use of the federal Exchange; CMS has not yet published those fees.

Eligibility System Modernization

8/19/12 © 2012 CSG Government Solutions 21

In June 2011, HHS expanded the definition of MMIS to include Eligibility Determination systems (42 CFR §433 Subpart C). Provides states 90% Federal Financial Participation (FFP) to fund

Eligibility System technology projects.

Funding is available for expenses incurred through December 2015.

In order to access funding, new technology must support the Seven Standards and Conditions defined by CMS (published in April 2011).

Cost Allocation is critical

In a letter from HHS Secy. Sebelius in August 2011, cost allocation to other public assistance programs can be waived (OMB Circular A-87).

Cost allocation is required between the Exchange, Medicaid and CHIP to the extent that the Eligibility Determination system supports these programs.

CMS and CCIIO are coordinating closely through the Establishment Review and grant management process.

CMS has developed an expedited review checklist to support a streamlined approval process for eligibility system funding requests

High-Level Timeline

8/19/2012 © 2012 CSG Government Solutions 22

High Level Exchange Timeline

/

HHS approves

State Exchanges

January 1, 2013

Blueprint

Application

must be

submitted by

11/16/12 if

state chooses

state-based

Exchange

Exchanges

must be

ready to

determine

eligibility

for QHP

enrollment

10/1/13

Exchange

operational

January 1,

2014

State Decision and Funding Timeline

8/19/12 © 2012 CSG Government Solutions 23

8/19/12 © 2012 CSG Government Solutions 24

Essential Health Benefits are the minimum benefit package standard to be applied both inside and outside the Exchanges. Services include:

Ambulatory patient services

Emergency services

Hospitalizations

Maternity and newborn care

Mental health and substance use disorder services, including behavioral health

Prescription drugs

Rehabilitative and habilitative services and devices

Laboratory services

Preventive and wellness services and chronic disease management

Pediatric services, including oral and vision care

States may choose from a pre-set list of federally chosen options that include: States largest HMO; State employee health plan; Federal employee health plan; and the three largest small group health plans.

Decision must be made by September 30, 2012 or the federal government will choose the largest small group health plan.

Essential Health Benefits

8/19/12 © 2012 CSG Government Solutions 25

Medicaid Benchmark Newly eligible Medicaid recipients will receive the Medicaid

Benchmark package .

Each state may define their own Medicaid Benchmark package, and it must be at least equivalent to the essential health benefit package. ACA rules offer several “benchmark plan” options that states may choose from: largest commercial HMO, state employee plan, Federal Employees Health Benefit Plan Equivalent Coverage (FEHBP), and standard Medicaid (with HHS approval).

Basic Health Program Option States have the option to offer a Basic Health Program

(BHP) to individuals between Medicaid federal poverty level and up to 200%.

BHP’s will resemble Medicaid Managed Care Organizations (MCOs).

Health Insurance Benefits

8/19/12 © 2012 CSG Government Solutions 26

Federal hub and the FFE are not yet well defined

Limited number of Exchange solution vendors

Medicaid expansion decision

Extremely short timeframes

State Challenges

8/19/12 © 2012 CSG Government Solutions 27

Sharing of challenges faced by states

Questions and answers

Conclusion

Contact Information

Thank you!

www.CSGdelivers.com

© 2012 CSG Government Solutions 28 8/19/2012

Sheila Cooper

Client Executive

(512) 970-2336

Robin Chacon

Client Executive

(207) 592-1400