healthy ecosystems healthy economy -...

TRANSCRIPT

@KITTYVDHEIJDEN

HEALTHY ECOSYSTEMS

=

HEALTHY ECONOMY

KITTY VAN DER HEIJDEN, DIRECTOR EUROPE WRI

2014 GO TO THINK TANK (JAN 2015) TOP ENVIRONMENTAL THINK TANK

1. World Resources Institute

2. Stockholm Environment Institute (SEI)

3. Worldwatch Institute

4. Brookings Institution

5. Center for Climate and Energy Solutions

6. Chatham House

7. Ecologic Institute

8. Potsdam Institute for Climate Research

9. International Institute for Sustainable Devt

10.Center for Environmental Research

SIX GOALS, THREE CROSS-CUTS

Climate Energy Food Forests Water Cities &

Transport

Business

Governance

Finance

OUR GLOBAL NETWORK

Institutional

Project staff on the ground

and/or project office

Active partnership

Liaison office

Planned office

Population Growth

Climate Change

Economic growth

Erosion of Ecosystems [60 % loss]

$15 trillion

$30tr

$50tr

$100tr

1970

1990

2010

Real GDP

(2005 dollars)

2030

Source: U.S. Department of Agriculture, Economic Research Service

1990

1 Billion

2010

2 Billion

2030

5 Billion

Source: Reuters, OECD 2010

THE RISE OF THE GLOBAL MIDDLE CLASS

EXPONENTIAL ENVIRONMENTAL TRENDS

(WRI chart using World Bank data, 2012)

ARE WE RUNNING OUT? Price trends of major commodity bundles (real 2005 dollars)

Pri

ce

in

re

al 2

00

5 d

oll

ars

250

200

150

100

50

1960 1970 1980 1990 2000 2010

Food

Energy

Timber

Fertilizers

Metals and Minerals

NO ABSOLUTE DECOUPLING…

THE HIGH COST OF ENVIRONMENTAL DEGRADATION

0

2

4

6

8

10

Co

st

of

en

vir

on

me

nta

l d

eg

rad

ati

on

as

% o

f G

DP

eq

uiv

ale

nt

CHINA: 9.2% OF GDP

(World Bank reports, 2005-2012)

14

Source: NCE estimate, based on WHO mortality data

ECONOMIC VALUE OF PREMATURE DEATH FROM pm 2.5

AIR POLLUTION

UNECONOMIC GROWTH

Source: UNU-IHDP, 2012

MASSIVE OPPORTUNITIES FOR RESOURCE EFFICIENCY

Global Green / Circular / Low Carbon Economy

• Prevailing economic model not leading to equitable and sustainable development

• Market and institutional failures

• What policies/reforms to address these shortcomings?

• GDP growth

• Globalization

• Deregulation

• Privatization

Prevailing growth model

• Output

• Incomes

• Living standards for many

Benefits • Poverty

• Inequality

• Ecosystem degradation

• GHG emissions

Costs

Prevailing economic growth model has benefits and shortcomings

These shortcomings derive from a series of market and institutional failures

Failures • Externalities • Under-provision of public goods • Missing markets • Asymmetrical information • Insecure property rights • Competitive barriers

But economic policies can provide a partial fix

Failures • Externalities • Under-provision of public goods • Missing markets • Asymmetrical information • Insecure property rights • Competitive barriers

Fixes • Getting prices right • Sustained public investments • Payments for ecosystem services • Labeling and 3rd party certification • Tenure reform, benefit sharing • Fair trade agreements

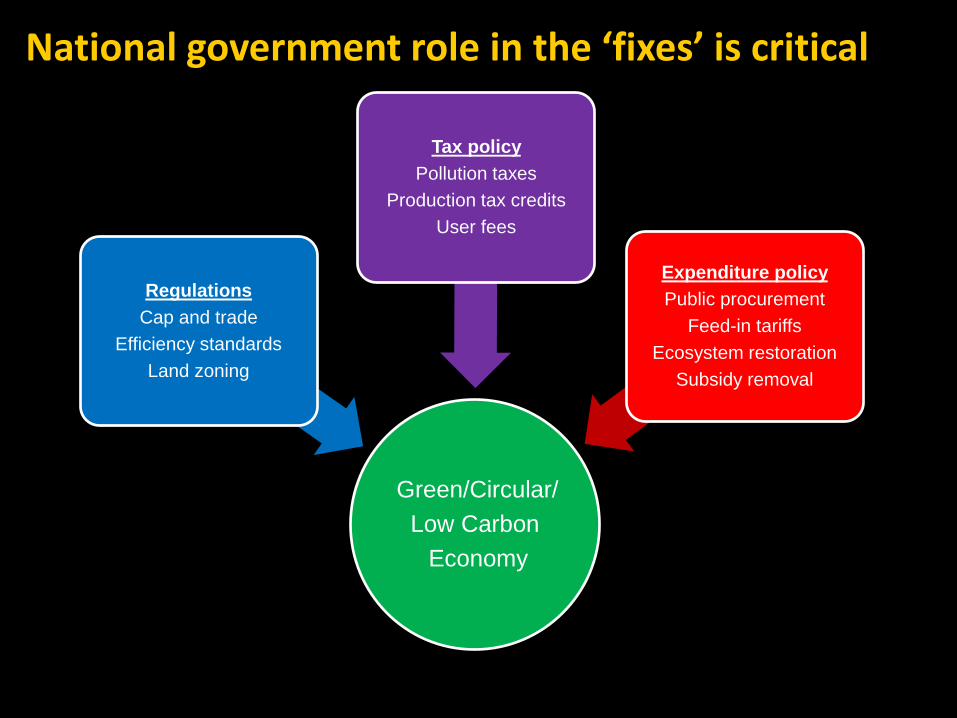

National government role in the ‘fixes’ is critical

Green/Circular/

Low Carbon

Economy

Regulations

Cap and trade

Efficiency standards

Land zoning

Tax policy

Pollution taxes

Production tax credits

User fees

Expenditure policy

Public procurement

Feed-in tariffs

Ecosystem restoration

Subsidy removal

1

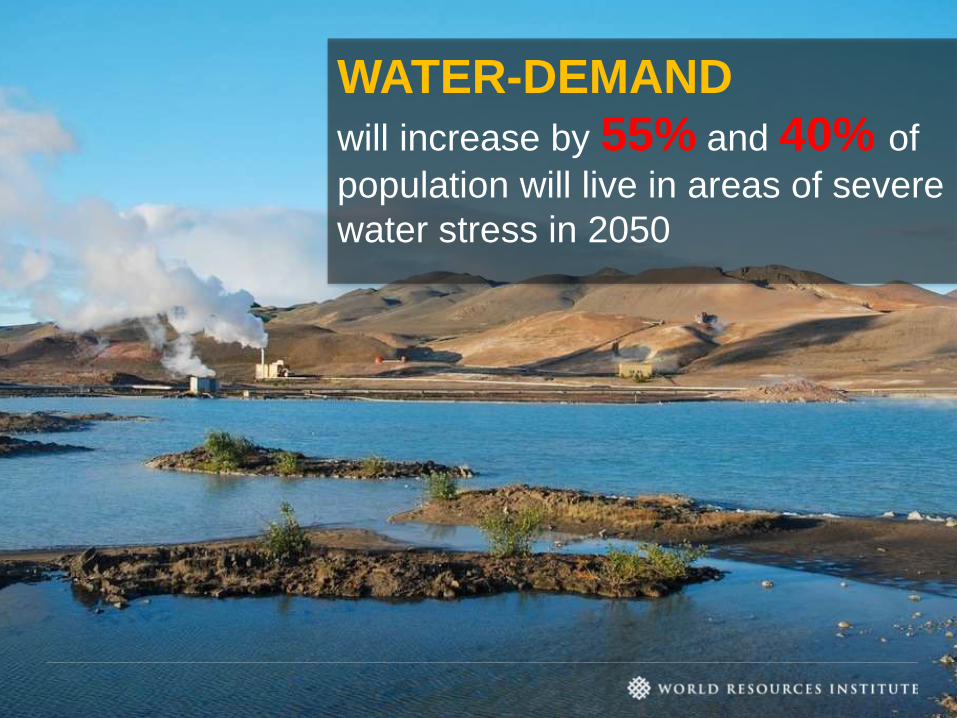

WATER-DEMAND

will increase by 55% and 40% of

population will live in areas of severe

water stress in 2050

WATER IS SCARCE TO START WITH

IN PRINCIPLE, THERE IS WATER FOR ALL

2.9 billion people live in highly to extremely highly water-stressed countries

Source: MIT, 2014

1.8 B

2020

2030

2040

Additional people in

(at least) moderate

water stress

2050

WATER SCARCITY ON THE RISE

Source: OECD Environmental Outlook Baseline; output from IMAGE

Environmental Outlook to 2050: Water

Global water demand: Baseline scenario, 2000 and 2050

irrigation domestic livestock manufacturing electricity

0

1 000

2 000

3 000

4 000

5 000

6 000

2000 2050 2000 2050 2000 2050 2000 2050

World OECD BRIICS RoW

Km

3

+400%

+130%

+140%

GLOBAL WATER RISK MAPPING

39% of irrigated cropland in this region is located in areas of water stress concern

Baseline Water Stress in areas with Irrigated Agriculture

39% of irrigated cropland in this region is located in areas of water stress concern

39% of irrigated cropland in this region is located in areas of water stress concern

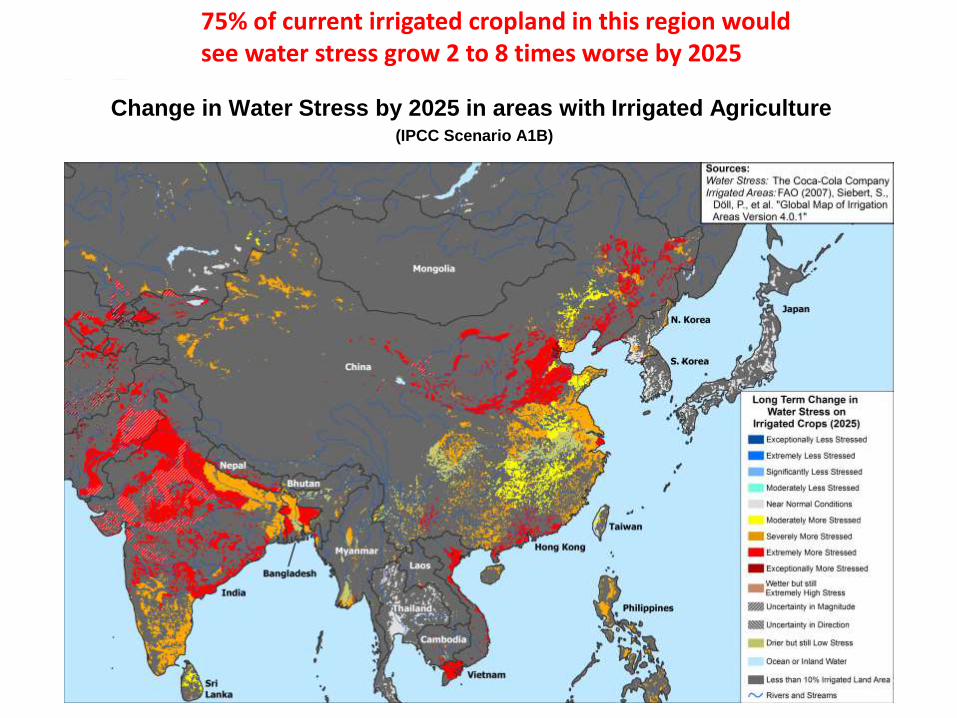

75% of current irrigated cropland in this region would see water stress grow 2 to 8 times worse by 2025 nt irrigated cropland in this region would see water stress grow 2 to 8 times worse by 2025 Change in Water Stress by 2025 in areas with Irrigated Agriculture

(IPCC Scenario A1B)

Energy Demand will grow by 1/3 by 2035 and electricity

demand will grow by 70% by 2035. Yet

90% of global power generation is water

intensive

19% of power plant design capacity in this region is located in areas of water stress concern

Baseline Water Stress and Power Plants

55% of current power plant design capacity in this region

would see water stress grow 2 to 8 times worse by 2025

Change in Water Stress by 2025 and Power Plants (IPCC Scenario A1B)

55% of POWER CAPACITY WILL SEE WATER STRESS

GROW 2 – 8 TIMES WORSE BY 2025

Source: Rio Times

Photo: flickr: queulat00

BRAZIL DRY SEASON

POWER PRICE UP 60%

THE IMPACT OF DROUGHT

Made it to nr # 20 this year in

(WRI, 2012)

COAL | PROPOSED NEW COAL POWER CAPACITY

COAL | PROPOSED NEW COAL POWER CAPACITY

(WRI, 2012)

INDIA

(WRI, 2012)

COAL | PROPOSED NEW COAL POWER CAPACITY

INDIA

CHINA

THREATS TO ENERGY

WHO SUFFERS FROM WATER SCARCITY?

WORLD ECONOMIC FORUM: WATER IS A GLOBAL RISK

Water crises

WATER ‘A GIFT OF NATURE’ ?

BUT THAT WILL (NEED TO) CHANGE

Environmental Outlook to 2050: Socioeconomic Developments

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

2010 2015 2020 2025 2030 2035 2040 2045 2050

Bill

ions o

f consta

nt 2010 U

SD

OECD BRIICS RoW US China India

Projections for real gross domestic product: Baseline, 2010-2050

Environmental Outlook to 2050: Climate Change

0

10

20

30

40

50

60

70

80

90

2010 2015 2020 2025 2030 2035 2040 2045 2050

GtC

O2e

OECD AI Russia & rest of AI Rest of BRIICS ROW

•Source: OECD Environmental Outlook Baseline; output from ENV-Linkages.

GHG emissions by region: Baseline, 2010-2050

•49

We need growth !

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

1996 1998 2000 2002 2004 2006 2008 2010 2012

Mill

ion

s To return to 2007 employment levels

Additional unemployed since 2007 (Right hand axis)

Employment growth (%) (Left hand axis)

Jobs

0

2

4

6

8

10

12

14

16

Per cent of GDP

Deficit improvement to achieve 60% debt to GDP by 2025

Debt Demographics

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Pensions

Long term care

Health

Percent of GDP

Changes in age related public spending to 2025

GLOBAL COMMISSION on the ECONOMY & CLIMATE

Co-Chair:

Felipe Calderón Dan Doctoroff Luisa Diogo Minouche Shafik Co-Chair: Lord

Nicholas Stern

Ingrid Bonde Sharan Burrow Helen Clark

Kris Gopalakrishnan Chad Holliday Sri Mulyani Indrawati Ricardo Lagos Trevor Manuel

Paul Polman Zhu Levin

Takehiko Nakao

Chen Yuan Angel Gurría Jens Stoltenberg Michel M. Liès Annise Parker

Caio Koch-Weser

Eduardo Paes

Maria

van der Hoeven

52

The exam question …

Can we have better growth and a better

climate at the same time?

Fighting Climate Change

Promoting Economic Growth

VS

53

GLOBAL NEW CLIMATE ECONOMY PARTNERSHIP

Global Commission

Chaired by former President of Mexico, Felipe

Calderón

Comprising 24 members, including former heads

of government and finance ministers, and

leaders in business, finance and economics,

from 20 countries

Economic Advisory Panel

14 world leading economists, chaired by

Professor Lord Nicholas Stern

Includes:

Two Nobel prize winners:

Daniel Kahneman and Michael Spence

7 Commissioning Countries

Colombia

Ethiopia

Indonesia

Norway

Sweden

South Korea

United Kingdom

8 Partner Research Institutes

Climate Policy Initiative (USA)

Ethiopian Development and Research Institute

Indian Centre for Research on Economic

Relations (ICRIER)

Global Green Growth Institute (South Korea)

London School of Economics (UK)

Stockholm Environment Institute (Sweden)

Tsinghua University (China)

World Resource Institute (USA)

54

A different growth pathway

CARBON

BUBBLE

TODAY

LIMITS TO

GROWTH

Growth

performance

Good

Bad

Bad Good

Climate performance

NEW CLIMATE

ECONOMY

55

Main findings of the Commission:

• Economic growth and climate mitigation can be achieved together. We do

not need to choose.

• A growing number of businesses, cities and countries are demonstrating

this. Recent technological and policy developments mean that even more

opportunities are available today.

• About US$ 90 trillion will be invested in infrastructure to 2030 – need to

choose if it is low-carbon and climate resilient. Low-carbon would not cost

much more, and fuel savings could fully offset additional investment costs.

• But if we lock-in the wrong path, we risk significant economic and social

impacts of climate change. Need to act urgently.

• There are multiple economic benefits of action, e.g. reduced health costs

from air pollution, less congestion & road deaths, enhanced energy, water

and food security. In many cases these will outweigh the costs of action.

56

Key drivers of growth and climate performance

RESOURCE

EFFICIENCY

INNOVATION

INFRASTRUCTURE

INVESTMENT

HIGH QUALITY, RESILIENT, INCLUSIVE = BETTER GROWTH

ENERGY LAND

USE CITIES

WIDER

ECONOMY

57

A different model of urban development is possible:

Atlanta and Barcelona have similar populations and wealth

levels but very different carbon productivities

Atlanta’s built-up area Barcelona’s built-up area

Population: 5.26 million

Total area: 16,605 km2

Urban area: 7692 km2

Transport carbon emissions: 6.9 tonnes CO2 p.c.

Population: 5 million

Total area: 3263 km2

Urban area: 648 km2

Transport carbon emissions: 1.2 tonnes CO2 p.c.

ATLANTA BARCELONA

Source: LSE research, drawing on data from Atlanta Regional Commission

(2014), Autoritat del Transport Metropolita (Area de Barcelona) (2013), GenCat

(2013), UCSB (2014), D’Onofrio (2014), based on latest data.

Per capita emissions of CO2 equivalent (2011)

Source: Cai et al. 2013, Hoornweg et al. 2011, Olivier et al. 2012

59

0

50

100

150

200

250

300

350

400

450

500

550

600

2005 2010 2015 2020

Source: Citi Research 2012; Bloomberg NEF (Turner 2013); AIE, World Energy Outlook 2013, WEO 2012

Cost of wind energy

USD/MWh

2000 2005 2010 2015 2020

150

100

90

160

140

130

120

110

50

70

60

80

10

0

Coal

Natural

gas

Cost of solar energy (solar panels)

USD/MWh

Actual Predicted Actual Predicted

2012 2012 Note: The graph shows a world average. In some markets

the cost of solar energy is competitive with other sources of

energy.

The cost of renewable energy is falling rapidly

Coal

Natural

gas

60

Wind turbines have evolved to have 100 times more power

generation capabilities than 30 years ago

Sources: Cityfix.com, NY Times, LSE and NCE Cities – Paper 03 Accessibility in Cities: Transport and Urban Form, p 10-11

61

A full accounting of the impact of a low carbon transition shows that

declining risks and operating costs could offset increased investment

needs

Financial Impact of a Coal to Renewable Energy Transition (2015-2035)

62

63

Investment in infrastructure: estimate for a low-carbon scenario

Source: OECD (2006, 2012), IEA ETP (2012), modelling by Climate Policy Initiative (CPI) for New Climate Economy (forthcoming), and New Climate Economy analysis.

$88

INCLUDES

REDUCTIONS IN

OPERATING

EXPENDITURES

65

Next steps The Global Commission recommends 10 transformative

actions

Source: NCE. For details please see the NCE Global Action Plan (2014)

1 Integrate climate risk into strategic decisions

Secure a strong international climate agreement

End perverse subsidies

Price carbon to send a clear market signal

Scale-up low-carbon innovation

Reduce the cost of capital for low-carbon investment

Move toward connected and compact cities

End deforestation

Restore degraded lands

Phase out unabated coal fast

2

3

4

5

6

7

8

9

10

Smart economic policies can provide a partial fix

Failures • Environmental externalities • Under-provision of public goods • Missing markets • Asymmetrical information • Insecure property rights • Competitive barriers

Fixes • Getting prices right • Sustained public investments • Payments for ecosystem services • Labeling and 3rd party certification • Tenure reform, benefit sharing • Fair trade agreements

National government role in the ‘fixes’ is critical

Green/Circular/

Low Carbon

Economy

Regulations

Cap and trade

Efficiency standards

Land zoning

Tax policy

Pollution taxes

Production tax credits

User fees

Expenditure policy

Public procurement

Feed-in tariffs

Ecosystem restoration

Subsidy removal

Ultimately … advancing a green/circular/low carbon economy is a political economy question

• Who has power?

• Who has control over resources?

• Who is involved in decisions?

• Where are vested interests?

• Are decisions transparent?

• Is there accountability?

• Is there adequate information?

Thank you !

@KittyvdHeijden