hellenic petroleum company presentation hellenic petroleum company presentation dr e. tzellas...

TRANSCRIPT

Hellenic Petroleum Company Presentation

Hellenic Petroleum Company Presentation

Dr E. TzellasChairman and Managing Director

Dr E. TzellasChairman and Managing Director

4th Annual Capital Link Forum Conference

New York

October 30, 2000

4th Annual Capital Link Forum Conference

New York

October 30, 2000

Business Business EnvironmentEnvironment

-3-

Total Primary Energy Demand (PED)Total Primary Energy Demand (PED)Total Primary Energy Demand (PED)Total Primary Energy Demand (PED) Structure of Energy SupplyStructure of Energy SupplyStructure of Energy SupplyStructure of Energy Supply

CAGRCAGR2000-20102000-2010

Source: Source: IEAIEA Source: Source: IEAIEA

4.4%4.4%

4.4%4.4%2.7%2.7%

0.3%0.3%

CAGR (2000-2010) 3.8%

CAGR (2000-2010) 3.8%

00

1010

2020

3030

4040

5050

19901990 19951995 20002000 20052005 20102010

(mto

e)

(mto

e)

OtherOther CoalCoal GasGas OilOil

4%4% 4%4%6%6%

3%3%

7%7%

3%3%6%6%

0%0%

20%20%

40%40%

60%60%

80%80%

100%100%

19951995 20002000 20052005 20102010

CoalCoal OilOil GasGas OtherOther

35%35% 32%32% 39%39% 29%29%

60%60% 58%58% 59%59% 62%62%

Greek Energy MarketGreek Energy Market

Benefit from geographical positionBenefit from geographical position No major natural sources of energy except for ligniteNo major natural sources of energy except for lignite Oil and coal provide 58% and 33% respectively of PEDOil and coal provide 58% and 33% respectively of PED Development of natural gas infrastructure is progressing well and is strongly Development of natural gas infrastructure is progressing well and is strongly

supported by the Government and EUsupported by the Government and EU

-4-

Drivers of GrowthDrivers of Growth

00

55

1010

1515

2020

2525

19901990 19951995 20002000 20052005 20102010

IndustryIndustry Residential/CommercialResidential/Commercial TransportTransport OtherOther

(mto

e(m

toe

))

Oil Consumption by SectorOil Consumption by SectorOil Consumption by SectorOil Consumption by Sector Natural Gas InfrastructureNatural Gas InfrastructureNatural Gas InfrastructureNatural Gas Infrastructure

Key drivers: growth in transportation and residential consumption

Source: IEA

CAGR (2000-2010) 4.4%

CAGR (2000-2010) 4.4%

(EU Average: 1.3%)

(EU Average: 1.3%)

-5-

Regional Environment - Growth PotentialRegional Environment - Growth PotentialRegional Environment - Growth PotentialRegional Environment - Growth Potential

Economic recovery and the need for modernisation of the oil and gas Economic recovery and the need for modernisation of the oil and gas

sectors in the region is expected to provide significant opportunities to sectors in the region is expected to provide significant opportunities to

expand product sales into the neighbouring countriesexpand product sales into the neighbouring countries

Economic recovery and the need for modernisation of the oil and gas Economic recovery and the need for modernisation of the oil and gas

sectors in the region is expected to provide significant opportunities to sectors in the region is expected to provide significant opportunities to

expand product sales into the neighbouring countriesexpand product sales into the neighbouring countries

Business ActivitiesBusiness Activities

-7-

Refining - Current positionRefining - Current position

50% of the refining capacity in 50% of the refining capacity in

Greece and 57% of the marketGreece and 57% of the market

Competitive advantagesCompetitive advantages::– strategic position strategic position – complexitycomplexity– strong logistics infrastructurestrong logistics infrastructure– unified operationsunified operations

Significant investment on stream at Significant investment on stream at the end of 1999the end of 1999

Production in compliance to Auto Oil Production in compliance to Auto Oil

I specifications I specifications Aspropyrgos

Refinery

Aspropyrgos

Refinery

Thessaloniki

Refinery

Skopje

Refinery

Skopje

Refinery

Crude PipelineCrude Pipeline

Burgas

Alexandroupolis

pipeline

(proposed)

Burgas

Alexandroupolis

pipeline

(proposed)

-8-

Environmental 1166 77 2233

Logistics 1133 33 1166

Capacity and complexity increases 3344 116677 220011

Other 1188 1111 2299

Total 8811 118888 226699

Refining - Going forwardRefining - Going forward

High growth in domestic and export salesHigh growth in domestic and export sales

Substantial capex toSubstantial capex to::

– increase capacity and complexityincrease capacity and complexity

– increase margins and reduce costsincrease margins and reduce costs

– increase light product yieldsincrease light product yields

– produce on produce on Auto Oil II specificationsAuto Oil II specifications

Refining capex Drs bnRefining capex Drs bn Refining capex Drs bnRefining capex Drs bn 2000E - 2001E2000E - 2001E2000E - 2001E2000E - 2001E 2002E - 2004E2002E - 2004E2002E - 2004E2002E - 2004ETotalTotal

2000 - 20042000 - 2004TotalTotal

2000 - 20042000 - 2004

-9-

Marketing - Current PositionMarketing - Current Position

Leading market shareLeading market share

Presence in more than 1600 retail Presence in more than 1600 retail

stationsstations

Well perceived brand namesWell perceived brand names

High quality fuels and lubricantsHigh quality fuels and lubricants

Country-wide coverageCountry-wide coverage

Strong logistics infrastructureStrong logistics infrastructure

Strong position in LPG and industrial Strong position in LPG and industrial

salessales

-10-

Marketing - Going ForwardMarketing - Going Forward

Increase market share through acquisitions Increase market share through acquisitions

Upgrade the retail network Upgrade the retail network

Expand retail network outside GreeceExpand retail network outside Greece

Development of non - fuel retail salesDevelopment of non - fuel retail sales

Development of motorway service station networkDevelopment of motorway service station network

Marketing Capex, Drs bnMarketing Capex, Drs bnMarketing Capex, Drs bnMarketing Capex, Drs bn 2000E - 2001E2000E - 2001E2000E - 2001E2000E - 2001E 2002E - 2004E2002E - 2004E2002E - 2004E2002E - 2004ETotal Total

2000 - 20042000 - 2004Total Total

2000 - 20042000 - 2004

Acquisitions 2255 -- 2255

Organic Growth 11 44 55

Retail Stations Modernisation 66 1100 1166

Logistics – Other 1111 22 2200

Total 4433 2244 6677

-11-

Petrochemicals - Current PositionPetrochemicals - Current Position

Only volume producer in GreeceOnly volume producer in Greece

Leading market positionLeading market position

Integrated with refining operationsIntegrated with refining operations

Strong geographical location Strong geographical location

advantage over importsadvantage over imports

Restructuring programme well Restructuring programme well

underwayunderway

Start up of BOPP film plant (Start up of BOPP film plant (DIAXON)DIAXON)

Thessaloniki industial complexThessaloniki industial complexPVC production unit PVC production unit

-12-

Petrochemicals - Going ForwardPetrochemicals - Going Forward

Development of new, high growth and high margin Development of new, high growth and high margin

productsproducts

Further closure/downsizing of unprofitable unitsFurther closure/downsizing of unprofitable units

Profit improvement programme in petrochemical Profit improvement programme in petrochemical

operations after success in refiningoperations after success in refining

Petrochemicals capex, Drs bnPetrochemicals capex, Drs bnPetrochemicals capex, Drs bnPetrochemicals capex, Drs bn 2000E - 2001E2000E - 2001E2000E - 2001E2000E - 2001E 2002E - 2004E2002E - 2004E2002E - 2004E2002E - 2004ETotalTotal

2000 - 20042000 - 2004TotalTotal

2000 - 20042000 - 2004

Polypropylene Plant 3377 -- 3377

ΒΟΡΡ – film plant 99 55 1144

Upgrade of existing units 11 -- 11

Logistics – other 33 11 44

Total 5500 66 5566

-13-

Exploration and Production - Current PositionExploration and Production - Current Position

Exclusive rights over 54000 KmExclusive rights over 54000 Km2 2 in in

GreeceGreece

Participation in exploration in 4 areas in Participation in exploration in 4 areas in

Western Greece in consortia with Western Greece in consortia with

international companiesinternational companies

Right to receive royalties for any Right to receive royalties for any

production in Greeceproduction in Greece

Natural Gas field in EpanomiNatural Gas field in Epanomi

Participation (30%) with OMV in by-back Participation (30%) with OMV in by-back

service contract in Iranservice contract in Iran

Evaluation of E&P projects in Albania, Evaluation of E&P projects in Albania,

LibyaLibya

Strong commercial relationships with Strong commercial relationships with

producing countriesproducing countries

-14-

Participate in consortia for production sharing agreements internationally

Leverage of Greek acreage portfolio to attract JV partners

E&P in Greece 22 11 33

Epanomi gas field development 66 55 1111

E&P Internationally 3344 1155 4499

Acquisitions – Other 1133 11 1144

Total 5555 2222 7777

E&P capex, Drs bnE&P capex, Drs bnE&P capex, Drs bnE&P capex, Drs bn 2000E - 2001E2000E - 2001E2000E - 2001E2000E - 2001E 2002E - 2004E2002E - 2004E2002E - 2004E2002E - 2004ETotalTotal

2000 - 20042000 - 2004TotalTotal

2000 - 20042000 - 2004

Exploration and Production - Going ForwardExploration and Production - Going Forward

-15-

Asprofos Asprofos Asprofos Asprofos

Largest engineering company in Largest engineering company in

SE EuropeSE Europe

Activities currently focus on Activities currently focus on

projects within the Groupprojects within the Group

Rapildy expanding engineering Rapildy expanding engineering

services to third parties and abroadservices to third parties and abroad

-16-

Natural Gas - Current PositionNatural Gas - Current Position

Main infrastructure already in Main infrastructure already in

place place

High demand growth rates High demand growth rates

Market liberalisation from 2007Market liberalisation from 2007

Substantial EU fundingSubstantial EU funding

35% stake in DEPA35% stake in DEPA

Option to acquire the remainder Option to acquire the remainder

from the Greek Statefrom the Greek State

-17-

Participation in DEPA 6644 -- 6644

Capex 1111 1144 2255

Total 7755 1144 8899

Natural Gas - Going ForwardNatural Gas - Going Forward

Strong expected demand growthStrong expected demand growth

Development of new business based on Development of new business based on Natural Gas feedNatural Gas feed

Introduction of strategic investors/operators Introduction of strategic investors/operators entryentry

Expansion of household consumption Expansion of household consumption

Natural Gas capex, Drs bnNatural Gas capex, Drs bnNatural Gas capex, Drs bnNatural Gas capex, Drs bn 2000E - 2001E2000E - 2001E2000E - 2001E2000E - 2001E 2002E - 2004E2002E - 2004E2002E - 2004E2002E - 2004ETotalTotal

2000 - 20042000 - 2004

TotalTotal

2000 - 20042000 - 2004

Financial HighlightsFinancial Highlights(IAS)(IAS)

-19-

Group Net Income and CapexGroup Net Income and CapexGroup Net Income and CapexGroup Net Income and Capex

18,222,5

66,3

91,9

35,347,8

0

10

20

30

40

50

60

70

80

90

100

Net Income before taxes Capex

Drs Billion

1997 1998 1999

+ 94%+ 94%

+ 88%+ 88%

-20-

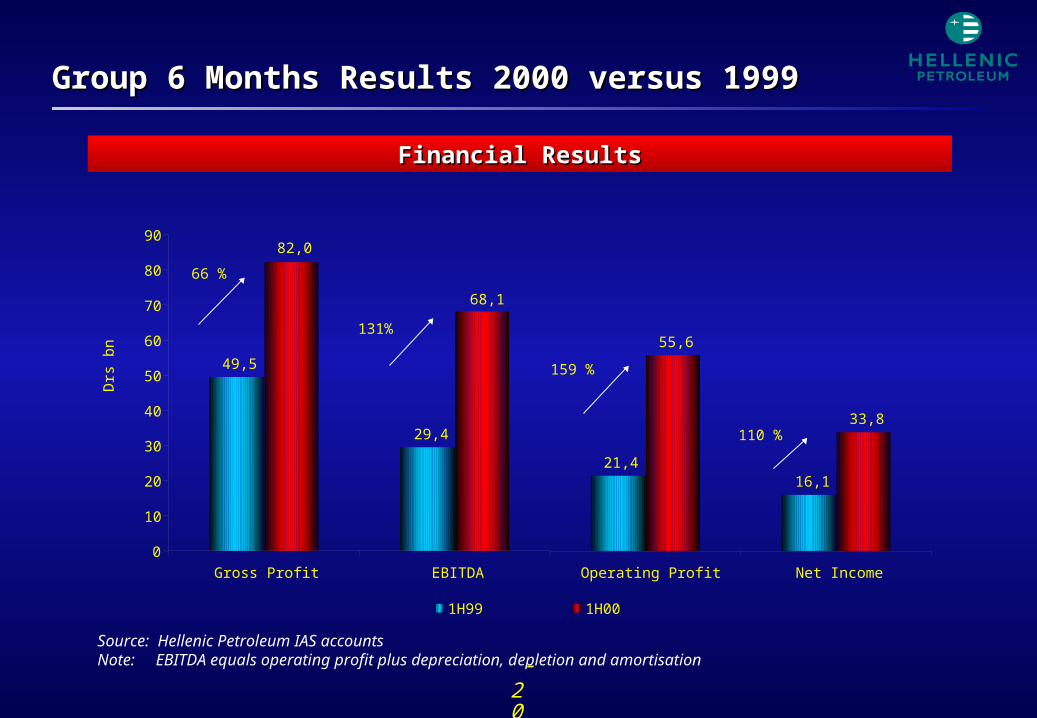

Group 6 Months Results 2000 versus 1999Group 6 Months Results 2000 versus 1999

Financial ResultsFinancial Results

Source: Hellenic Petroleum IAS accountsNote: EBITDA equals operating profit plus depreciation, depletion and amortisation

49,5

29,4

21,416,1

55,6

33,8

68,1

82,0

0

10

20

30

40

50

60

70

80

90

Gross Profit EBITDA Operating Profit Net Income

Drs

bn

1H99 1H00

66 %

131%

159 %

110 %

Strategy OverviewStrategy Overview

-22-

Corporate Competitive AdvantageCorporate Competitive Advantage

StrengthsStrengths Leading market position in GreeceLeading market position in Greece Premium refining marginsPremium refining margins Vertically integrated downstream operationsVertically integrated downstream operations Competitive advantage from logistics, geography and limited import Competitive advantage from logistics, geography and limited import

infrastructureinfrastructure Exposure to gas growth through increase in DEPA stakeExposure to gas growth through increase in DEPA stake Strong financial position to fund expansionStrong financial position to fund expansion

OpportunitiesOpportunities Growing domestic demand for light productsGrowing domestic demand for light products Option to increase stake in DEPAOption to increase stake in DEPA Regional R&M expansion in South Eastern EuropeRegional R&M expansion in South Eastern Europe Increased participation in E&P projectsIncreased participation in E&P projects

-23-

Vision - Strategic Target Vision - Strategic Target

Transform into a fully integrated Transform into a fully integrated energy group energy group

Significantly increase revenues Significantly increase revenues and profitability over the next and profitability over the next five yearsfive years

-24-

Corporate StrategyCorporate Strategy

Performance improvementPerformance improvement

— Reorganise operational structure in order to cut costs and improve Reorganise operational structure in order to cut costs and improve productivityproductivity

— Maximise refining efficiency and profitability Maximise refining efficiency and profitability

— Increase retail market share and improve retail margins Increase retail market share and improve retail margins

Operational/Geographical expansionOperational/Geographical expansion

— Increase production of lighter products Increase production of lighter products

— Increase exposure to natural gas Increase exposure to natural gas

— Continue restructuring petrochemicals (move to high value Continue restructuring petrochemicals (move to high value products)products)

— Expand downstream activities in the Balkans Expand downstream activities in the Balkans

— Develop upstream business Develop upstream business

-25-

19981998 2000E2000E 2002E2002E TotalTotalDrs BnDrs Bn -1999 -1999 -2001E -2001E -2004Ε -2004Ε 2000-20042000-2004

RefiningRefining 86,186,1 81,081,0 187,9187,9 268,9268,9

MarketingMarketing 25,425,4 43,143,1 23,523,5 66,666,6

ChemicalsChemicals 36,636,6 49,749,7 5,45,4 55,155,1

E&PE&P 0,30,3 53,653,6 21,221,2 74,874,8

IT-OthersIT-Others -- 4.44.4 2.12.1 6.56.5

AsprofosAsprofos 3,83,8 0,20,2 0,50,5 0,70,7

ParticipationsParticipations 29,029,0 88,588,5 15,015,0 103,5103,5

TotalTotal 180,2180,2 320,5320,5 255,6255,6 576,1576,1

Capex distribution 2000-2004Capex distribution 2000-2004

1,2%1,2%46,7%46,7%

13,0%13,0%

11,6%11,6%MarketingMarketing

17,9%17,9%ParticipationParticipationss

IT-othersIT-others

9,6%9,6%ChemicalsChemicals

Ε&PΕ&P

RefiningRefining

Major investments:Major investments:

– Thessaloniki Refinery upgradeThessaloniki Refinery upgrade– BOPP Film/Polypropylene new plantsBOPP Film/Polypropylene new plants– Retail upgradeRetail upgrade– E&P projectsE&P projects

– DEPA stakeDEPA stake

Capital Expenditure ProgrammeCapital Expenditure Programme