heritage commercial insurance - ecclesiastical … heritage commercial... · heritage commercial...

TRANSCRIPT

policy document HERITAGE COMMERCIAL INSURANCE

Version 3

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 2

3 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

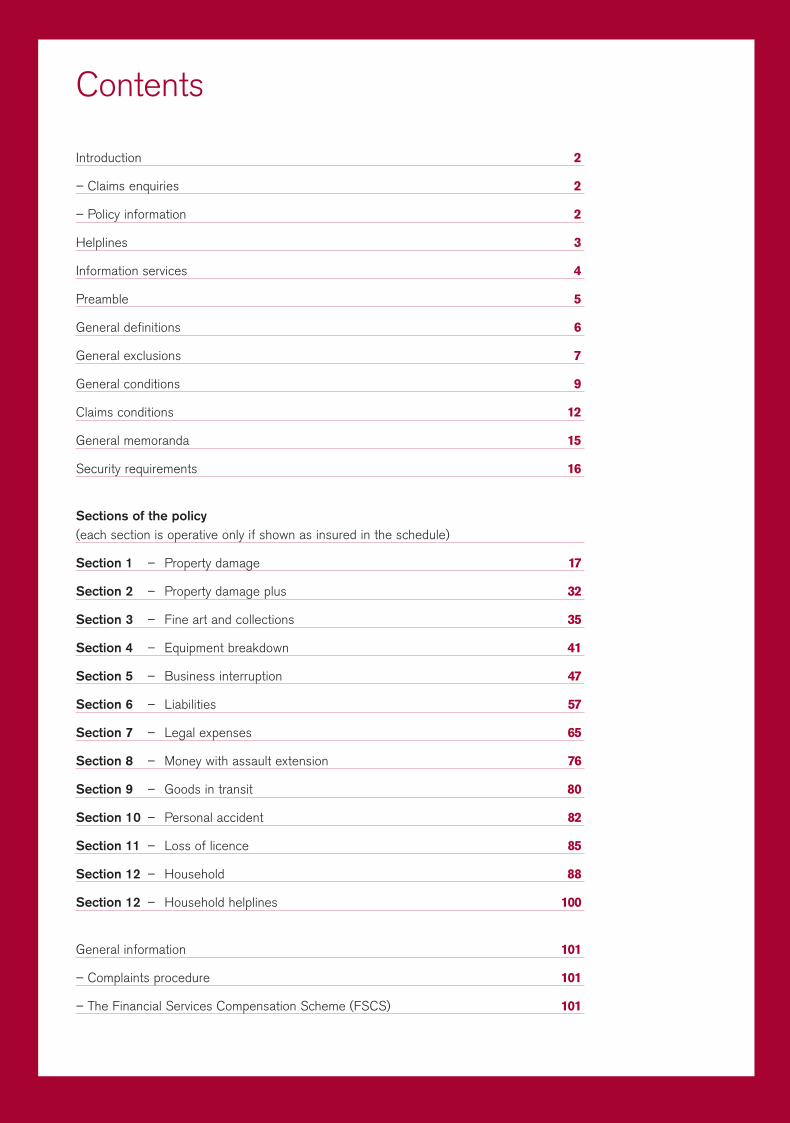

Contents

Introduction 2

– Claims enquiries 2

– Policy information 2

Helplines 3

Information services 4

Preamble 5

General definitions 6

General exclusions 7

General conditions 9

Claims conditions 12

General memoranda 15

Security requirements 16

Sections of the policy (each sectio n is operative only if shown as insured in the schedule)

Section 1 – Property damage 17

Section 2 – Property damage plus 32

Section 3 – Fine art and collections 35

Section 4 – Equipment breakdown 41

Section 5 – Business interruption 47

Section 6 – Liabilities 57

Section 7 – Legal expenses 65

Section 8 – Money with assault extension 76

Section 9 – Goods in transit 80

Section 10 – Personal accident 82

Section 11 – Loss of licence 85

Section 12 – Household 88

Section 12 – Household helplines 100

General information 101

– Complaints procedure 101

– The Financial Services Compensation Scheme (FSCS) 101

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 3

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 2

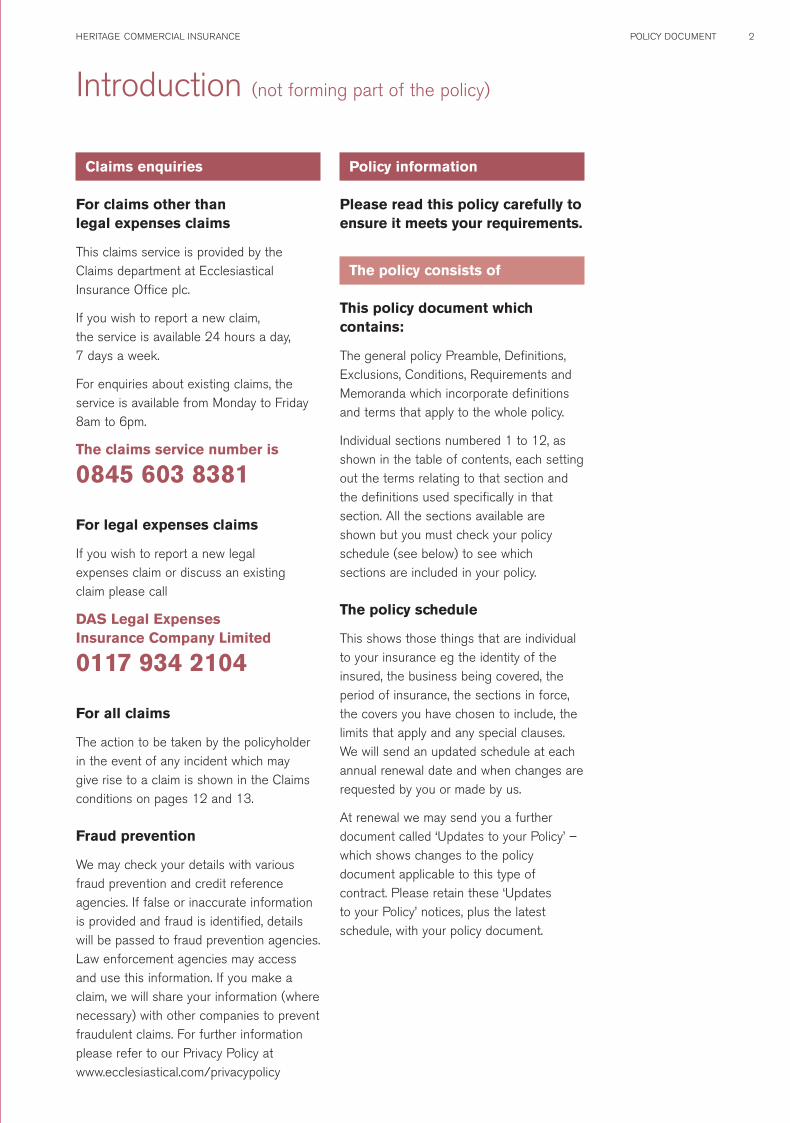

Claims enquiries

For claims other than legal expenses claims

This claims service is provided by theClaims department at EcclesiasticalInsurance Office plc.

If you wish to report a new claim, the service is available 24 hours a day, 7 days a week.

For enquiries about existing claims, theservice is available from Monday to Friday8am to 6pm.

The claims service number is

0845 603 8381

For legal expenses claims

If you wish to report a new legal expenses claim or discuss an existing claim please call

DAS Legal Expenses Insurance Company Limited

0117 934 2104

For all claims

The action to be taken by the policyholderin the event of any incident which may give rise to a claim is shown in the Claimsconditions on pages 12 and 13.

Fraud prevention

We may check your details with variousfraud prevention and credit referenceagencies. If false or inaccurate informationis provided and fraud is identified, detailswill be passed to fraud prevention agencies.Law enforcement agencies may accessand use this information. If you make aclaim, we will share your information (wherenecessary) with other companies to preventfraudulent claims. For further informationplease refer to our Privacy Policy atwww.ecclesiastical.com/privacypolicy

Policy information

Please read this policy carefully toensure it meets your requirements.

The policy consists of

This policy document whichcontains:

The general policy Preamble, Definitions,Exclusions, Conditions, Requirements andMemoranda which incorporate definitionsand terms that apply to the whole policy.

Individual sections numbered 1 to 12, asshown in the table of contents, each settingout the terms relating to that section andthe definitions used specifically in thatsection. All the sections available areshown but you must check your policyschedule (see below) to see which sections are included in your policy.

The policy schedule

This shows those things that are individualto your insurance eg the identity of theinsured, the business being covered, theperiod of insurance, the sections in force,the covers you have chosen to include, thelimits that apply and any special clauses.We will send an updated schedule at eachannual renewal date and when changes arerequested by you or made by us.

At renewal we may send you a furtherdocument called ‘Updates to your Policy’ –which shows changes to the policydocument applicable to this type ofcontract. Please retain these ‘Updates to your Policy’ notices, plus the latestschedule, with your policy document.

Introduction (not forming part of the policy)

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 2

3 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

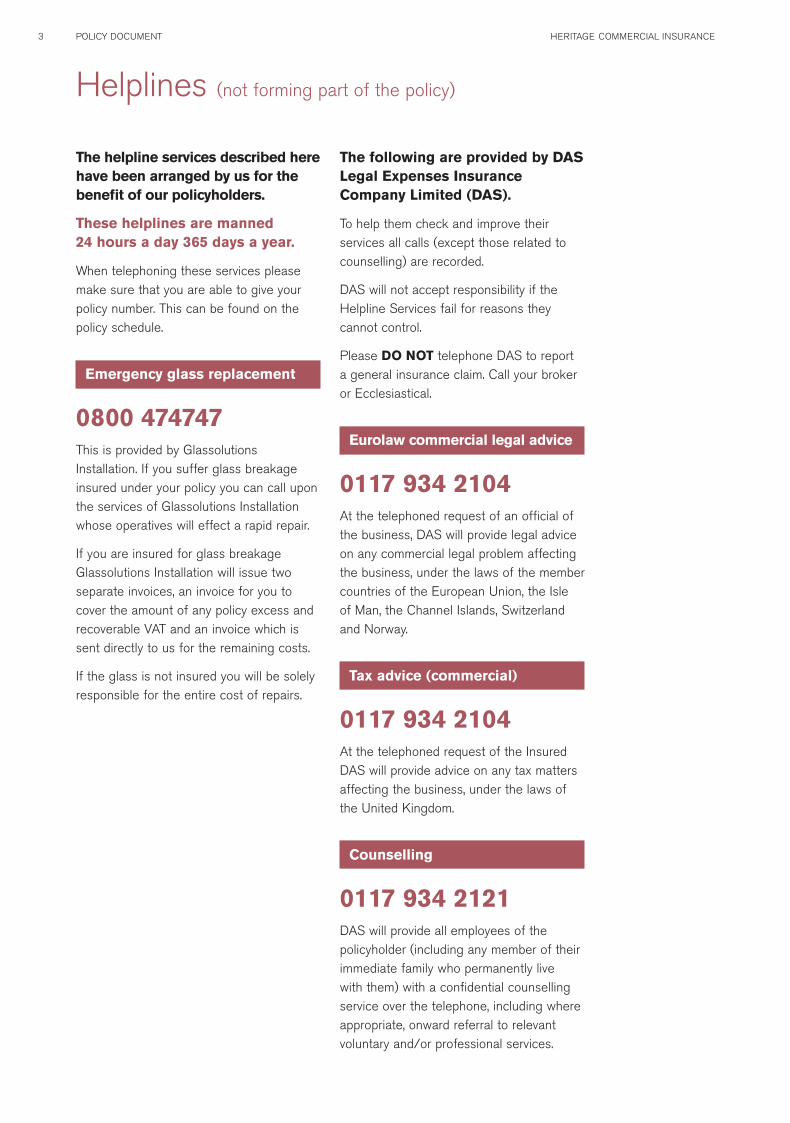

The helpline services described herehave been arranged by us for thebenefit of our policyholders.

These helplines are manned 24 hours a day 365 days a year.

When telephoning these services pleasemake sure that you are able to give yourpolicy number. This can be found on thepolicy schedule.

Emergency glass replacement

0800 474747 This is provided by GlassolutionsInstallation. If you suffer glass breakageinsured under your policy you can call uponthe services of Glassolutions Installationwhose operatives will effect a rapid repair.

If you are insured for glass breakageGlassolutions Installation will issue twoseparate invoices, an invoice for you tocover the amount of any policy excess andrecoverable VAT and an invoice which issent directly to us for the remaining costs.

If the glass is not insured you will be solelyresponsible for the entire cost of repairs.

The following are provided by DASLegal Expenses InsuranceCompany Limited (DAS).

To help them check and improve theirservices all calls (except those related tocounselling) are recorded.

DAS will not accept responsibility if theHelpline Services fail for reasons theycannot control.

Please DO NOT telephone DAS to report a general insurance claim. Call your brokeror Ecclesiastical.

Eurolaw commercial legal advice

0117 934 2104 At the telephoned request of an official ofthe business, DAS will provide legal adviceon any commercial legal problem affectingthe business, under the laws of the membercountries of the European Union, the Isle of Man, the Channel Islands, Switzerlandand Norway.

Tax advice (commercial)

0117 934 2104At the telephoned request of the InsuredDAS will provide advice on any tax mattersaffecting the business, under the laws ofthe United Kingdom.

Counselling

0117 934 2121 DAS will provide all employees of thepolicyholder (including any member of theirimmediate family who permanently live with them) with a confidential counsellingservice over the telephone, including whereappropriate, onward referral to relevantvoluntary and/or professional services.

Helplines (not forming part of the policy)

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 3

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 4

The following are provided by DASLegal Expenses InsuranceCompany Limited (DAS).

Employment manual

The DAS Employment manual offers comprehensive, up to date guidance on rapidly changing employment law.

To view the Employment Manual please visit the DAS website at

www.das.co.uk From the Home Page click on theEmployment manual icon. All the sectionsof this web-based document can be printedoff for your own use.

Email DAS at

[email protected] with your email address, quoting your policy number and DAS will contact you by email to inform you of future updates tothe information.

DAS businesslaw

At www.dasbusinesslaw.co.uk you will find an online reference full of the sorts of letters, articles and forms that will help you run your business successfully. DAS businesslaw users can also access interactive document builders, to help make composing commercial documents as easy as possible.

From new legislation and employment issues to property law and taxation, you will find the content provided by DAS businesslaw is updated regularly by legal experts to help you keep your business one step ahead.

To register your details, access the DAS businesslaw website at

www.dasbusinesslaw.co.uk When asked for your policy number, please insert your Ecclesiastical policy number prefixed with ‘EIG’ and the password is DAS472301

Information services (not forming part of the policy)

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 4

5 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

The Ecclesiastical Insurance Office plc (the Company) and the Insured named inthe schedule agree that

(1) the application or proposal form or any other information supplied shall beincorporated into the contract

(2) this policy document the schedule(including any replacement schedule)and any endorsement shall togetherform the policy and be considered asone document

(3) the Insured will pay the premium(4) the Company will subject to the terms

and conditions of this policy provideinsurance under the sections specifiedin the schedule during the period ofinsurance or any subsequent period for which the Insured shall pay and the Company shall accept the renewal premium

(5) this policy (other than the Legalexpenses section and the Family legalprotection part of the Householdsection) shall be governed by andconstrued in accordance with the lawof England and Wales unless theinsured’s habitual residence (in thecase of an individual) or centraladministration and/or place ofestablishment is located in Scotland in which case the law of Scotland shall apply

Heritage commercial insurance policy

Preamble

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 5

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 6

Each time any of the following words orphrases appear in this document inbold italic type (or in capital letters in theschedule) they will take the specificmeaning shown below unless morespecifically defined under each individualpolicy section

Where words or phrases are not highlightedin this manner the normal everyday meaningof the word or phrase will apply

Businessmeans the business of the Insured asstated in the schedule

Company/we/our/usmeans Ecclesiastical Insurance Office plc

Damagemeans physical loss destruction or damage

Denial of service attackmeans any actions or instructionsconstructed or generated with the ability todamage interfere with or otherwise affectthe availability of networks network servicesnetwork connectivity or information systems

This includes but is not limited to thegeneration of excess traffic into networkaddresses the exploitation of system ornetwork weaknesses and the generation of excess or non-genuine traffic betweenand amongst networks

Excessmeans the first amount of each and everyloss (after applying any adjustment forunderinsurance) up to the amount set out in the schedule to this policy relevant to that loss

Geographical limitsmeans England Scotland Wales NorthernIreland the Channel Islands and the Isle of Man

Hackingmeans unauthorised access to anycomputer or other equipment or componentor system or item which processes storestransmits retrieves or receives data whetheryour property or not

Insured/you/yourmeans the Insured shown in the schedule

Premisesmeans that part of the premises at theaddresses shown in the schedule owned or occupied by you in connection with the business

Terrorism means an act including but not limited tothe use of force or violence and/or thethreat thereof of any person or group(s) ofpersons whether acting alone or on behalfof or in connection with any organisation(s)or government(s) committed for politicalreligious ideological ethnic or similarpurposes or reasons including the intentionto influence any government and/or to put the public or any section of the public in fear

Unoccupiedmeans unoccupied or untenanted or not in use

Virus or similar mechanismmeans program code programminginstruction or any set of instructionsintentionally constructed with the ability to damage interfere with or otherwiseadversely affect computer programs data files or operations whether involvingself-replication or not

This includes but is not limited to Trojan horses worms and logic bombs

General definitions

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 6

7 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

This policy does not cover

Excess

any excess shown in the schedule

Other insurances

property more specifically insured underanother policy

Radioactive contamination

(a) damage to any property whatsoever or any loss or expense whatsoeverresulting or arising therefrom or anyconsequential loss

(b) any legal liability of whatsoever naturedirectly or indirectly caused by orcontributed to by or arising from (i) ionising radiations or contamination

by radioactivity from any nuclear fuel or from any nuclear waste fromthe combustion of nuclear fuel

(ii) the radioactive toxic explosive or other hazardous properties of anyexplosive nuclear assembly or nuclear component thereof

Exclusion 3 does not apply to the Personal accident section

Exclusions 3(b)(i) and (ii) do not apply toCover 1 of the Liabilities section except in respect of liability of any principal andliability assumed by agreement

War risks

any contingency liability or damageoccasioned by or happening through warinvasion act of foreign enemy hostilities(whether war be declared or not) civil warrebellion revolution insurrection or militaryor usurped power

Exclusion 4 does not apply to Cover 1 of the Liabilities section

4

3

2

1

Sonic bangs

damage directly occasioned by pressurewaves caused by aircraft and other aerial devices travelling at sonic or supersonic speeds

Date recognition

any consequential or other loss costs andexpenses and any legal liability accidentalbodily injury or damage to property directlyor indirectly caused by or contributed to by or consisting of or in any way relating toor connected with the failure or possiblefailure of any computer(a) correctly to recognise any date as

its true calendar date (b) to capture save or retain and/or

correctly to manipulate interpret orprocess any data or information orcommand or instruction as a result of treating any date otherwise than as its true calendar date

(c) to capture save retain or correctlyprocess any data as a result of theoperation of any command which has been programmed into anycomputer being a command whichcauses the loss of data or the inabilityto capture save retain or correctly to process such data on or after any date

but this shall not exclude subsequentdamage or consequential loss not otherwise excluded which itself results from a defined peril

6

5

General exclusions

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 7

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 8

Definitions specific to exclusion 6

Computer means computer or other equipment media or system (or any part of them) forprocessing storing or retrieving data toinclude without limitation any microchipintegrated circuit or similar device or anycomputer software

Defined peril means any of the insured events specifiedin any section(s) of this policy insuringproperty (other than section 4 Equipmentbreakdown) excepting (a) accidental loss destruction or damage

and (b) causes excluded from these

insured events

Exclusion 6 does not apply to the assaultextension of the Money section and thePersonal accident section

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 8

9 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Misrepresentation and misdescription

This policy shall be voidable in the event ofa material misrepresentation misdescriptionor non-disclosure

Precedents to liability

The due observance and fulfilment of theterms of this policy in so far as they relateto anything to be done or complied with by you shall be conditions precedent to any liability of the Company to make anypayment under this policy

Reasonable care

You shall take all reasonable precautions to prevent damage accident illness anddisease and shall exercise reasonable care in ensuring that all statutory and otherobligations and regulations are dulyobserved and complied with and shallmaintain the premises and works machineryand plant in sound condition

If any defect is discovered by complaint orotherwise you shall take immediate steps to remedy the same and in the meantimeshall cause such temporary precautions tobe taken as the circumstances may require

Unoccupied buildings

When a building or part of a buildinginsured by this policy becomes unoccupiedor when an unoccupied building or part of a building is again occupied it is a conditionof this policy that immediate notice is given to us

Upon any alteration as described above we shall be entitled to cancel the policy or impose special terms or charge anadditional premium but in any event fromthe time of alteration until we advise you of our decision the insurance by theProperty damage Fine art and collectionsand Household sections in respect of any unoccupied building is restricted to

4

3

2

1 Insured event 1 (Fire lightning andexplosion) and Insured event 2 (Aircraft)

For the Household section of this policy orfor personally owned items insured underthe fine art and collections section we donot regard periods of up to 90 daystemporary absence as constitutingunoccupancy

Alteration of risk

If after the commencement of theinsurance there is any alteration of the risk (a) whereby the risk of damage accident

or liability increases(b) whereby the premises are undergoing

major structural alterations or majorrepair (that does not include whereworkmen are allowed on the premisesto carry out minor repairs alterationsand general maintenance not involvingexternal scaffolding)

(c) whereby your interest ceases exceptby will or operation of law

(d) whereby an administrator or aliquidator or receiver is appointed orwhere you enter into a voluntaryarrangement

(e) by any other material change in use of the premises

it is a condition of this policy thatimmediate notice is given to us

Upon any alteration as described above weshall be entitled to cancel the policy fromthe date of such alteration or impose specialterms or charge an additional premium

Warranties

Every warranty to which the property or risk insured or any item thereof is or maybe made subject shall from the time thewarranty attaches apply and continue to bein force during the whole currency of thispolicy and non-compliance with any suchwarranty in so far as it increases the risk of damage shall be a bar to any claim inrespect of such damage

6

5

General conditions

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 9

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 10

Multiple insurances

(a) All sections except Equipment breakdown Liabilities Legal expenses Money with assault extension Personal accident and Loss of licence sections

If at the time any claim arises under this policy there are any otherinsurances in force covering the same damage or liability we shall not be liable for more than ourrateable proportion and if such other insurance is subject to any condition of underinsurance this policy if notalready subject to any condition of underinsurance shall be subject to that condition of underinsurance

(b) Loss of licence section

If at the time of the cancellation of the licence insured by this policy there is any other insurance in forcecovering your interest we shall not beliable to pay or contribute more thanour rateable proportion

(c) Equipment breakdown Liabilities Legal expenses and Money sections apart from the assault extension

If at the time of any claim arisingunder this policy you are or would butfor the existence of this policy beentitled to indemnity under any otherpolicy or policies we shall not be liableexcept in respect of any additionalamount beyond the amount whichwould have been payable under suchother policy or policies had thisinsurance not been effected

7 (d) Personal accident and

assault extension of the Money section

Irrespective of the number of policiesissued by us which provide cover to an insured person we shall not paypersonal accident benefits under morethan one policy for any one occurrence

The policy which provides the greatestbenefit shall apply

Fraudulent claims

If any claim upon this policy is in anyrespect fraudulent or if fraudulent means ordevices are used by you or anyone actingon your behalf to obtain benefit under thispolicy or if any damage is occasioned byyour wilful act or with your connivance allbenefit under this policy shall be forfeited

Arbitration

If any difference shall arise as to the amountsthat should be paid under this policy (liabilitybeing otherwise admitted) such differenceshall be resolved by arbitration in accordancewith the statutory provisions in force at the time by (a) an arbitrator agreed to in writing by the

parties or if the parties cannot agree (b) an arbitrator appointed by the

Chartered Institute of Arbitratorsfollowing a request from either partyafter a seven day written notice by one party to the other requiring an agreement

You must not take legal action against us over the dispute before the arbitrator has reached a decision

9

8

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 10

11 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Cancellation

Paragraph (i) is applicable to RetailCustomers only (the schedule will indicate ifyou are a Retail Customer)

(i) Your right to cancel in the cooling-off period

If after insuring with us and receiving the full written policy documentationincluding the schedule you subsequentlychange your mind you have 14 days to write to the sender confirming thatyou do not wish to continue

No charge will be made and anypremium you have already paid will be refunded

After this cooling-off period your rightto cancel the policy is as described inparagraph (ii) below

Paragraphs (ii) and (iii) are applicableto all customers

(ii) Your right to cancel the policy

You may cancel the policy providedthat you give us notice in writing

As long as you have not made a claimyou will receive a refund of the part of your premium which covers thecancelled period provided this exceeds £10

If you have made a claim then the full annual premium is due

(iii)Our right to cancel

In circumstances other than alteration of the risk (see condition 5)we may cancel the policy or anysection of it by sending seven days’notice by recorded delivery to you atyour last known address and shallrefund to you the proportionatepremium for the unexpired period ofcover

10 Adjustment of premium

If any part of the premium has beencalculated on estimates you shall withinthirty days from the expiry of each period ofinsurance furnish to us such information aswe may require and the premium for suchperiod shall be adjusted and the differencepaid by or allowed to you subject to anyminimum premium

Long term agreement

Where shown in the schedule that adiscount of premium is allowed inconsideration of you having made anagreement to offer annually certaininsurances under this policy on the terms inforce at the expiry of each period ofinsurance and to pay the premium annuallyin advance it is understood that(a) we shall be under no obligation to

accept an offer made in accordancewith the above-mentioned agreement

(b) the sum insured may be reduced at any time to correspond with anyreduction in value or variation in the business

This agreement shall apply to any policy or policies which may be issued by usin substitution for this policy and the same discount shall be allowed from the corresponding premium for any substitutedpolicy or policies issued by us

12

11

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 11

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 12

Your duties

On the happening of any incident whichmay give rise to a claim you shall

General all sections other than Legal expensesand Loss of licence sections and theFamily legal protection cover underthe Household section

(a) take all practicable steps to recoverproperty lost and otherwise minimisethe claim

(b) inform the Police immediately if the damage is caused by thievesmalicious persons or vandals or by riot civil commotion strikes or labour disturbances

(c) notify us as soon as possible (d) at our request and at our expense do

or allow to be done everythingreasonably required by us for thepurpose of making any recoveries fromother parties (whom we would beentitled to pursue upon settlement ofyour claim) whether such action isnecessary before or after we pay yourclaim under the policy

1

Property damage Property damage plus Equipment breakdown Money and Goods in transit sections excluding the Money assault extension

(a) within 30 days or such further time as we may in writing allow deliver to us a written claim providing at yourown expense all details proofs andinformation regarding the cause andamount of the damage as we mayreasonably require together withdetails of any other insurances on any property insured by this policy and (if demanded) a statutorydeclaration of the truth of the claimand of any related matters No claim under these sections shall be payable unless the terms of thiscondition have been complied with

(b) if we elect or become bound toreinstate or replace any propertyproduce at your own expense and give to us all such plans documentsand information as we may reasonably require

However we shall not be bound to reinstate exactly or completely but only ascircumstances permit and in reasonablysufficient manner and shall not in any casebe bound to expend in respect of any one ofthe items insured more than the sum insured

2

Claims conditions

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 12

13 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Business interruption section

within 30 days after the expiry of theindemnity period or within such further timeas we may in writing allow at your ownexpense deliver to us a statement settingout particulars of the claim together withdetails of all other insurances covering any part of the damage or resultingbusiness interruption

You shall at your own expense also provideus with such books of account and otherbusiness books vouchers invoices balancesheets and other documents proofsinformation explanations and other evidenceas may reasonably be required by us for thepurpose of investigating or verifying suchclaim together with (if demanded) a statutorydeclaration of the truth of the claim and ofany related matters

No claim under this section shall bepayable unless the terms of this conditionhave been complied with and in the eventof non-compliance any payment on account of the claim already made by us shall be repaid to us

3 Liabilities section and thePersonal liability part of theHousehold section

(a) not make nor allow to be made on your behalf any admission offerpromise payment or indemnity without our written consent

(b) forward to us every letter claim writsummons and process immediatelyupon receipt without acknowledgementand advise us in writing as soon as you have any knowledge of anyimpending prosecution inquest or fatal injury inquiry in connection with that event

Legal expenses section and the Family legalprotection part of theHousehold section

as described in those sections of the policy

Personal accident section and assault extension of the Money section

(a) at your own expense provide allcertificates information and evidenceas required by and in the formprescribed by us

(b) arrange for the insured person toundergo medical examination by theCompany’s medical practitioner as often as required at our expense

Loss of licence section

as described in the Loss of Licence section of the policy

7

6

5

4

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 13

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 14

Our rights

All sections except Personal accident the assault extension of the Money section theLegal expenses section and theFamily legal protection cover underthe Household section

(a) We may start take over defend andconduct any legal action in your nameor prosecute in your name for ourbenefit any claim for indemnity ordamages and shall have full discretionin the conduct and settlement of any such action

(b) We may enter any building wheredamage has occurred to deal withyour claim and to take temporarily forsafe-keeping any property insured bythis policyWe have the right to the salvage of theinsured property but you may not abandon property to us

This policy shall be proof that you havegiven us authority to exercise our rightsunder this condition

Liabilities section

We may at any time pay to you the limit of indemnity (a) in the case of Employers’ Liability or

Prosecution Defence Cost claims afterdeduction of any sum or sums alreadypaid or incurred

(b) in the case of Public and ProductsLiability claims after deduction of anysum or sums already paid or incurredas damages

or any less amount for which at ourdiscretion any claim or claims can be settledand we will then relinquish control of anysuch claim and be under no further liabilityexcept that in respect of any Public andProducts Liability claim (other than anyclaim originating from within the legaljurisdiction of the United States of America

2

1

or Canada) we will also pay any legal costsincurred prior to the date of such payment

Legal expenses section andthe Family legal protectioncover under the Householdsection

As described in those sections of the policy

Personal accident section and assault extension of the Money section

We shall in the event of death of any insuredperson be entitled to have a post mortem atour expense

4

3

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 14

15 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Designation

For the purpose of determining wherenecessary the heading under which anyproperty is insured we agree to accept the designation under which such propertyhas been entered in your books

Contracts – (Rights of Third Parties)

A person or company who is not a party tothis policy has no right under the Contracts(Rights of Third Parties) Act 1999 toenforce any term of this policy but this doesnot affect any right or remedy of a third partywhich exists or is available apart from that Act

2

1

General memoranda

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 15

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 16

Protection condition

It is a condition precedent to liability inrespect of damage at or to the premisescaused by theft or attempted theft that alllocks bolts and other protective devices(except intruder alarms) fitted to thepremises be brought into use wheneverthe premises are closed for business andare not attended by you or an authorisedemployee for the purpose of the business

Intruder alarm conditionapplicable only if shown as operative in the schedule

In respect of damage due to or arisingfrom theft or attempted theft at thepremises it is a condition precedent toliability under this policy that an intruderalarm system is installed at the premisesand that(a) the intruder alarm system shall be

installed in accordance with thespecification agreed in writing by usand no alteration or variation of thesystem or any structural alteration to the premises which would affect the system shall be made without our written consent

(b) the intruder alarm system shall bemaintained in full and efficient workingorder at all times and be serviced undera maintenance contract approved by usand immediate notice of any apparentdefect in the intruder alarm systemor its signalling shall be given to themaintenance contractor

(c) the intruder alarm system shall betested and set whenever the alarmedportion of the premises is closed forbusiness and is not attended by youor any person authorised by you to be responsible for the security of thepremises provided that any detectiondevices and their circuits connected for continuous protection shall be fullyoperative at all times

2

1 (d) all keys including duplicate keys and

notes of combination locks/electronicpass codes letters and numbersrelative to the intruder alarm systemshall be removed from the buildings ofthe premises whenever they areclosed for business and are leftunattended provided that at such timesif part of the premises is occupiedresidentially by you or an authorisedemployee the said keys shall beremoved from the business portion ofthe premises to the part occupiedresidentially

(e) immediate advice shall be given to us of any notice from the Police or asecurity organisation that intruderalarm system signals may be or will be disregarded

(f) you shall appoint at least twokeyholders and lodge written details(which must be kept up to-date) with the alarm company and policeauthorities

(g) in the event of notification of anyactivation of the intruder alarmsystem or interruption of the means of communication during any periodthat the intruder alarm system is seta keyholder shall attend the premisesas soon as is reasonably possible

Definitions specific to condition 2

Intruder alarm systemmeans the component parts including the means of communication used totransmit signals

Keyholder(s)means you or any person or keyholdingcompany authorised by you who isavailable at all times to accept notificationof faults or alarm signals relating to the intruderalarm system and attend and allow accessto the premises

Security requirements

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 16

17 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

The schedule will show if this section applies and the cover in force

Definitions

Each time any of the following words or phrases appear in this section in bold italic type (or in capital letters in the schedule) they will take the specific meaning shown below

Where words or phrases are not highlightedin this manner the normal everyday meaningof the word or phrase will apply

Buildingsmeans the buildings of the premisesincluding landlord’s fixtures and fittingsoutbuildings walls gates and fences pipingducting cables wires and associated controlgear and accessories on the premises andextending to the public mains but only tothe extent of your responsibility fixedaerials and satellite dishes wind turbinessolar panels yards car parks roads andpavements storage tanks swimming poolsand associated apparatus

Unless stated otherwise buildings are brickstone or concrete built and roofed withslates tiles concrete metal asphalt orsheets or slabs composed of incombustiblemineral ingredients and exclude land piersjetties bridges culverts and excavations

Contents means business equipment plant machineryfurniture fixtures and fittings and all othercontents all belonging to you or for whichyou are legally responsible and contained in the buildings and elsewhere as stated inthis policy and the schedule including (1) the cost of materials labour

and computer time in reproducing (a) documents manuscripts and

business books (b) patterns models moulds plans

and designs

(c) computer systems records for an amount not exceeding 5% of the sum insured by the item on contents

but not any cost in connection with producing information to be recorded or for the value to you of the information contained therein

(2) the personal belongings of thefollowing persons whilst contained inthe premises in so far as they are nototherwise insured (a) directors trustees partners

employees and authorisedvolunteers for an amount notexceeding £1,000 per person

(b) visitors for an amount notexceeding £500 per person

Personal money is also insured up to £100 per person For this purpose ‘personal belongings’means personal articles worn used orcarried about the person excluding bankers’cards, credit cards and debit cards and any belongings otherwise insured

Contents excludes (i) stock(ii) landlord’s fixtures and fittings (iii) cash or money instruments of

any description whether negotiable or non-negotiable

(iv) vehicles licensed for road use(including accessories thereon)caravans trailers railway locomotivesrolling stock watercraft or aircraft

(v) any living creatures trees shrubs plants or other vegetation

(vi) explosives (vii) any other property more

specifically insured

Insured event(s) means any insurable event (from 1 Firelightning and explosion to 18 Glass and sanitary fixtures) set out as included in the schedule to this policy

Property damage 1

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 17

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 18

Items insured means the items insured as set out in theProperty damage section of the schedule tothis policy

Stock means stock and materials in trade and workin progress your property or held by you intrust or on commission for which you areresponsible in the buildings and elsewhereas stated in this policy and the schedule

Tenant’s improvements means improvements and decorations atthe premises which are your property orfor which you are responsible

Cover

We will indemnify you (by payment up tothe value of the items insured at the time of the damage or at our option by repairreinstatement or replacement) in respect of damage to the items insured by anyinsured event happening during the periodof insurance

Provided that our liability in any one periodof insurance shall not exceed the suminsured for each item nor in all the totalsum insured

Insurable events

Fire lightning and explosion

Fire

(whether resulting from explosion or otherwise) not occasioned by orhappening through (a) the property’s own spontaneous

fermentation or heating or itsundergoing any process involving the application of heat

(b) earthquake subterranean fire riot civil commotion

Lightning

1

Explosion

excluding(a) damage in respect of and originating

in any vessel machinery or apparatus orits contents belonging to you or underyour control which is required to beexamined to comply with any StatutoryRegulations unless such vesselmachinery or apparatus shall be thesubject of a policy or other contractproviding the required inspection service

(b) damage by fire resulting from explosion(c) damage consisting of the bursting

of a boiler economiser or other vesselmachine or apparatus in which internalpressure is due to steam only andbelonging to you or under your control

Aircraft

Aircraft and other aerial devices or articlesdropped from them

Riot

Riot civil commotion strikers locked-outworkers or persons taking part in labourdisturbances excluding (a) damage occasioned by or happening

through confiscation or destruction orrequisition by order of the governmentor any public authority

(b) damage resulting from cessation of work(c) damage occurring in Northern Ireland

Malicious persons

Malicious persons not acting on behalf of or in connection with any political organisation excluding (a) damage occasioned by or happening

through confiscation or destruction orrequisition by order of the governmentor any public authority

(b) damage resulting from cessation of work (c) damage occurring in Northern Ireland (d) damage by theft or attempted theft or

by risks described in insurable event 1fire lightning and explosion

4

3

2

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 18

19 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Earthquake

Subterranean fire

Storm

excluding(a) damage by

(i) the escape of water from thenormal confines of any natural or artificial water course or lakereservoir canal or dam

(ii) inundation from the sea whether resulting from storm or otherwise

(b) damage attributable solely to changein the water table level

(c) damage by frost subsidence or landslip

(d) damage to fences gates andmoveable property in the open

Flood

Flood caused by (a) the escape of water from the normal

confines of any natural or artificialwater course (other than water tanksapparatus or pipes) or lake reservoircanal or dam

(b) inundation from the sea

but excluding(i) damage attributable solely to change

in the water table level (ii) damage by frost subsidence

or landslip (iii) damage to fences gates and

moveable property in the open

Escape of water

Escape of water from any tank apparatus or pipe including damage to any watertank apparatus or pipe itself caused byfreezing of water excluding damage bywater discharged or leaking from aninstallation of automatic sprinklers

5

9

8

7

6

Impact

Impact with the property insured by anyroad vehicle or animal

Falling trees

Falling trees branches telegraph poles lampposts or pylons

Falling aerials

Breakage or collapse of television and radioreceiving aerials aerial fittings and mastssatellite dishes wind turbines solar panelsand security equipment

Escape of oil

Escape of oil from any fixed oil-firedheating installation

Sprinkler leakage

Accidental escape of water from anyautomatic sprinkler installation in thepremises not caused by explosionearthquake subterranean fire or heatcaused by fire

Accidental damage

Any other accidental damage excluding (a) damage which is specifically

included or excluded elsewhere under this section

(b) damage to the property insuredcaused by or consisting of inherent vice latent defect gradual deteriorationwear and tear its own faulty ordefective design or materials faulty ordefective workmanship but this shallnot exclude subsequent damagewhich itself results from a cause nototherwise excluded

10

15

14

13

12

11

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 19

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 20

(c) damage caused by or consisting ofcorrosion rust wet or dry rot shrinkageevaporation loss of weight dampnessdryness marring scratching vermininsects change in temperature colourflavour texture or finish

(d) damage consisting of (i) joint leakage failure of welds or

cracking fracturing collapse oroverheating of boilers economiserssuperheaters pressure vessels or any range of steam and feedpiping in connection therewith

(ii) mechanical or electrical breakdownor derangement in respect of theparticular machine apparatus orequipment in which such breakdownor derangement originates

(e) damage caused by or consisting of (i) acts of fraud or dishonesty (ii) disappearance unexplained or

inventory shortage misfiling ormisplacing of information

(f) damage caused by or consisting oferasure loss distortion or corruption of information on computer systems or other records programs or software

(g) damage(i) to a building or structure caused

by its own collapse or cracking (ii) in respect of moveable property

in the open fences and gates bywind rain hail sleet snow or dust

(iii) to property resulting from its undergoing any process of cleaningdyeing restoration productionpacking treatment testingcommissioning servicing or repair

(iv) to wind turbines

Subsidence

Subsidence heave or landslip of the site on which the premises stand excluding damage(a) attributable solely to change in the

water table level (b) to boundary walls gates fences piping

ducting cables wires and associatedcontrol gear and accessories yards carparks roads and pavements storagetanks and swimming pools unless alsoresulting in damage to a buildinginsured under this policy

(c) caused by or consisting of (i) the normal settlement or

bedding-down of new structures (ii) the settlement or movement

of made-up ground (iii) coastal or river erosion

(d) caused by defective design or workmanship or the use of defective materials

(e) caused by fire subterranean fireexplosion earthquake or the escape of water from any tank apparatus or pipe

(f) which originated prior to the inception of cover

(g) resulting from (i) demolition construction structural

alteration or repair of any property (ii) groundworks or excavation at the same premises

Special condition applicable to insurable event 16

You shall notify us immediately if youbecome aware of any demolitiongroundworks excavation or constructionbeing carried out on any adjoining site

We shall then have the right to vary theseterms or cancel this cover

16

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 20

21 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Theft or attempted theft

Theft or attempted theft (a) involving entry to or exit from the

buildings of the premises by forcibleand violent means (in respect ofemployee or authorised volunteers’personal belongings theft does not have to involve forcible and violent means)

(b) following actual or threatened assaultor violence

but excluding damage to the buildings asa result of theft or attempted theft

Glass and sanitary fixtures

Accidental breakage of any part of theexterior and interior glass sanitary fixturesor signs including the reasonable cost of (a) repairs to framework following

breakage of the insured glass (b) necessary boarding-up pending

replacement of the insured glass (c) in the case of multiple glazing

the additional cost of re-creating vacuums or the purchase andinstallation of new sealed units

(d) replacing any lettering painting oralarm foil on such glass

but excluding (i) damage to glass sanitary fixtures or

signs already damaged at thecommencement of the insurance

(ii) disfiguration or damage to glass notextending through the entire thicknessof the glass

(iii) breakage of glass while not fixed (iv) breakage occasioned by or traceable

to alterations to the premises or in the glass whereby the risk of breakageis increased

(v) damage to bulbs or tubes unless the signs in which they are containedare damaged at the same time

(vi) damage which is specificallymentioned elsewhere under this section

18

17 Extensions

The insurance by this section is extended to include the following

Non-invalidation

The cover by this section shall not beinvalidated by any act or omission or anyalteration whereby the risk of damage isincreased unknown to you or beyond yourcontrol provided that you immediately onbecoming aware of this give notice to usand pay an additional premium if required

Reinstatement of sum insured not applicable to any Limits in the extensions to this section

In consideration of your agreement to pay such additional premium as may berequired we will automatically reinstate the sum insured in full after damagehas occurred

Provided that(a) we have not given you notice within

30 days of you reporting the damageto us that we will not reinstate the sum insured

(b) in respect of damage by theft orattempted theft reinstatement will only apply subject to you completingany improvements to the securityprecautions at the premises that we may require and in any eventreinstatement following theft orattempted theft will apply only onceduring each period of insurance

2

1

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 21

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 22

Fees

If the buildings are insured architects’surveyors’ consulting engineers’ and legalfees necessarily and reasonably incurred inthe reinstatement of the property insuredconsequent upon its damage by aninsured event but not for preparing anyclaim it being understood that the amountpayable for such damage and fees shallnot exceed in the aggregate the suminsured by each item

Removal of debris

Costs and expenses necessarily incurred by you with our consent in (a) removing debris (b) dismantling and/or demolishing (c) shoring up or propping of the portion or portions of the propertyinsured by the said items destroyed ordamaged by any insured event it beingunderstood that the amount payable for such damage and costs incurred under (a) (b) and (c) shall not exceed in theaggregate the sum insured by each item

We will also pay the costs and expensesnecessarily incurred by you with ourconsent in removing fallen trees within the grounds of the premises

Provided that(1) the trees have fallen as a result of an

insured event(2) the buildings of the premises are

damaged by the same insured eventoccurring at the same time and a claim for this damage has beenadmitted by us

We will not pay for any costs or expenses(i) incurred in removing debris except

from the site of such propertydestroyed or damaged and the areaimmediately adjacent to such site

(ii) arising from pollution or contaminationof property not insured by this policy

4

3 European Union and PublicAuthorities includingundamaged portions

If the buildings are insured such additionalcost of reinstatement of the destroyed ordamaged property as may be incurredsolely by reason of the necessity to complywith the stipulations of (1) European Union legislation or (2) building or other regulations under or

framed in pursuance of any Act of Parliament or bye-laws of any public authority (hereinafter referred to as ‘the Stipulations’)

excluding(a) the cost incurred in complying with

the Stipulations (i) in respect of damage occurring prior

to the granting of this extension (ii) in respect of damage not insured

by this policy (iii) under which notice has been served

upon you prior to the happening ofthe damage

(iv) for which there is an existingrequirement which has to be implemented within a given period

(b) the additional cost that would havebeen required to make good theproperty lost destroyed or damaged to a condition equal to its conditionwhen new had the necessity to complywith the Stipulations not arisen

(c) the amount of any charge or assessment arising out of capitalappreciation which may be payable in respect of the property or by theowner of the property by reason of compliance with the Stipulations

5

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 22

23 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Special conditions applicable to extension 5

1 The work of reinstatement must becommenced and carried out withoutunreasonable delay and in any casemust be completed within twelvemonths after the damage or withinsuch further time as we may allow(during the said twelve months) andmay be carried out upon another site(if the Stipulations so necessitate)subject to our liability under thisextension not being thereby increased

2 If our liability under the policy apartfrom this extension shall be reduced by the application of any of the termsand conditions of the policy then ourliability under this extension (in respectof any such item) shall be reduced inlike proportion

3 The total amount recoverable underany item of the policy under thisextension shall not exceed (a) 15% of its sum insured (b) where the sum insured by the

item applies to property at morethan one premises 15% of the total amount for which we wouldhave been liable had the propertyinsured by the item at thepremises where damage hasoccurred been wholly destroyed

4 The total amount recoverable underany item of the policy shall not exceedits sum insured

5 All the terms of this policy except in so far as they may be expressly varied shall apply as if they had beenincorporated herein

Planning (Listed Buildings and Conservation Areas) Act 1990

The cost of meeting local authority conditionsmade under the Planning (Listed Buildingsand Conservation Areas) Act 1990 andamending legislation (or equivalent legislationin Scotland and Northern Ireland) followingdamage by any of the insured eventsshould these costs exceed the coverprovided within the buildings sum insured

The maximum we will pay under thisextension is 20% of the sum insured for buildings

Archaeological costs

The on-site costs of archaeological rescuework (including the recording of standingand collapsed fabric and damaged floorsurfaces but not the excavation of belowground deposits) necessarily and reasonablyincurred with our consent as a result ofdamage to the buildings

Excluding (i) The costs of any archaeological

research work which may be enabledor facilitated as a result of damagebut which is not a necessary part ofthe process of repair or rebuilding

(ii) The costs of analysis of datasubsequent to archaeological rescuework (except in so far as such costsare a necessary and integral part of the process of repair or rebuilding)

(iii) The costs of conservation or scientific analysis of materials orobjects retrieved in the course of an archaeological exercise

7

6

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 23

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 24

Definitions specific to extension 7

Archaeological rescue work means any archaeological exercise concernedwith the recording of information which wouldotherwise be lost or in danger of being lost

Archaeological research work means any other archaeological exercise

Limit £250,000 any one claim

Capital additions

Under the buildings and contentsitems (a) alterations and additions to the

property insured but not in respectof any appreciation in value

(b) newly acquired property so far as itis not otherwise insured anywherein the geographical limits

Provided that (1) at any one situation this cover shall

not exceed 10% of the total suminsured on such property or £500,000in respect of both buildings andcontents whichever is the less

(2) you undertake to give details of such extension of cover as soon aspracticable and to effect specificinsurance thereon and pay suchadditional premium as may be required from inception of the cover

Bequeathed property

Damage by an insured event to materialproperty anywhere in the geographicallimits bequeathed to you

Cover is operative from the commencementdate of your interest in the material property

Within three months of legal title of suchproperty passing to the Insured you musteither notify us about the property andarrange for it to be specifically insured bythis policy (or any other policy with us) orarrange for it to be insured elsewhere

9

8

If you arrange to insure such property withus any additional premium payable shall be calculated from the date the legal title of the property passed to you

Limit £50,000 any one bequest (single articlelimit £5,000) other than buildings for which the limit shall not exceed 10% of the buildings sum insured or £250,000whichever is the less

Excluding (i) motor vehicles licensed for road use

or their accessories trailers caravanswatercraft or aircraft

(ii) property insured under any other policy(iii) cash or money instruments of

any description whether negotiable or non-negotiable

Spontaneous heating

Damage to coal coke or wood blocks by its own spontaneous fermentationheating or combustion

Emergency services damage

Damage at any part of the premisesincluding its grounds caused by theemergency services in circumstanceswhere such damage would not otherwiseform part of a valid claim under this section

This includes damage which occurs whenthe emergency services are responding topotential danger to property or injury topersons but damage caused by Policeraids is specifically excluded

Limit £5,000 any one claim

Heating oil gas and metered water

We will pay for loss of heating oil gas ormetered water following damage to theheating system or water system by aninsured event

Limit £5,000 in any one period of insurance

12

11

10

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 24

25 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Sale of building

If the buildings are insured the interest of the purchaser in the insurance by thissection for the period from the written offerand acceptance or exchange of contractsuntil completion of the sale is noted

Provided that(a) the building is not insured elsewhere

for the benefit of the purchaser(b) the purchaser complies with and is

bound by the terms of the policy

Temporary removal

(a) Contents are covered for the insuredevents while temporarily removed forcleaning renovation repair or othersimilar purpose to any other premisesand in transit between such locationsin the geographical limits

(b) Contents are covered for the insuredevents anywhere in the geographicallimits whilst such contents are in yourcustody or the custody of your trusteeemployee or duly authorised volunteeror at the home of any such person but excluding contents removed forthe purposes stated in (a) above

Limit £2,500 any one claim

(c) (i) Deeds and other documentsmanuscripts plans writings of every description and books (ii) Computer systems recordswhilst temporarily removed to apremises in the geographical limitswhich is not in your occupancy andwhilst in transit to and from suchlocation for an amount not exceeding10% of the relevant contents suminsured excluding items removed forthe purposes stated in (a) and (b)

Extensions (a) (b) and (c) exclude propertyif and so far as it is otherwise insured

For the purpose of this extension insurableevent 17 Theft or attempted theft appliesto any premises

14

13 Damage to the buildings by theft only applicable if insurable event 17 Theft or attempted theft is operative

The insurance extends to include yourresponsibility for (a) repairs to the buildings of the

premises following theft of externallead copper or other metal up to £15,000 in any one period of insurance

(b) damage to furnishings and interiordecorations directly caused as a resultof the entry of rainwater following thetheft of external metal up to £5,000 inany one period of insurance

(c) damage to the buildings of thepremises caused by theft or attempted theft (other than the theft of external metal) for an amount notexceeding £100,000 in any one periodof insurance

This extension does not apply during externalrepairs and/or restoration of the premises

Theft of keys only applicable if insurable event 17 Theft or attempted theft is operative

If contents are insured the reasonablecosts necessarily incurred in gaining accessto the premises and/or replacing locks atthe premises including locks of safes orstrongrooms in the premises if the keys are stolen

Limit £2,500 any one period of insurance

Property in the open

If the contents are insured damage to thefollowing property by the insured events(a) floodlighting external lighting and

security equipment fixed to thebuildings or in the grounds of thepremises

17

16

15

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 25

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 26

(b) groundsmen’s equipment while in theopen grounds of the premisesprovided that any mechanically orelectrically driven equipment isimmobilised when not in use

Limit£5,000 any one period of insurance

(c) fixed or unfixed equipment monumentsmemorials statues garden decorationsand ornaments in the grounds of the premises (other than provided by (a) and (b) above)

Limit £15,000 any one claim

(d) signage positioned outside but in theimmediate vicinity of the premises

Limit £5,000 any one claim

For the purpose of this extension (i) insurable event 17 (theft or attempted

theft) includes theft or attempted theftnot involving forcible and violent entry

(ii) the exclusion under insurable events 7 (storm) and 8 (flood) relating tomoveable property in the open doesnot apply

Hired-in property

Damage by an insured event to contentshired-in for the purposes of the businessfor which you are responsible

Limit 10% of the contents sum insured any one period of insurance

Freezer contents

If contents are insured damage to thecontents of chill or deep freeze food units as a result of failure of the unit failure of the electricity or gas supply orcontamination from refrigerant or refrigerantfumes

In addition we will pay if incurred thenecessary and reasonable cost of hiringtemporary alternative freezing space

18

19

Excluding(a) damage caused by your failure to pay

for the electricity or gas supply (b) damage to freezer contents where the

freezer or compressor is more than 15years old unless the refrigeration unitis the subject of a currentmanufacturers guarantee or an annualmaintenance contract

Limit £2,500 for the contents of any unit and£10,000 in total any one period ofinsurance

Trace and access

The costs and expenses necessarily andreasonably incurred by you with ourconsent in locating the source of a leakageof oil or water at the premises and insubsequent repair and making good

Limit £50,000 any one claim

Underground pipes and cables

Accidental damage to underground pipesand cables where the buildings areinsured by this section or where you areliable for repairs as tenant

Clearing of drains

The reasonable costs incurred by you forclearing or repairing drains gutters sewersand the like for which you are responsibleincurred as a direct result of damagecaused by an insured event

Limit £50,000 any one claim

20

21

22

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 26

27 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Extinguisher and alarm re-setting expenses

The reasonable costs incurred by you inrefilling fire extinguishing appliancesreplacing sprinkler heads and resetting fire or intruder alarm systems solely inconsequence of their activation following an insured event

Discharge of oil

Costs and expenses necessarily incurred by you with our consent to decontaminatethe grounds of the premises followingaccidental discharge of oil from any oil fired heating appliance or storage tank

Limit£5,000 any one claim

Minor building worksendorsement

This endorsement is only in force if youhave notified us and is shown as operativein the schedule

Definitions specific to this endorsement

Contract(s) means any contract or contracts with you as an employer for the repair alterationor extension of the buildings

Contractor(s) shall have the meaning attached to them in the contract

Specified perils means fire lightning explosion storm tempestflood escape of water from any water tanksapparatus or pipes aircraft and other aerialdevices or articles dropped from them riotcivil commotion or earthquake

24

23 Cover

This section extends to cover your insuranceobligations (other than for damage byterrorism) under Clause 5.4b of the 2005JCT Minor Works Building contract inrespect of repairs alterations and/orextensions to existing building structures (or any similar contract with our agreement)

Our liability under this endorsement for any one contract or series of contractsrelating to any one project at the premisesshall not exceed £100,000

For the purposes of this endorsement andfor the period of the contract the insurancefor (a) the existing structures and (b) any contents for which you are

responsible and the works and unfixed materials and goods intendedfor incorporation in the works

is considered to be in the joint names ofyou and the contractor but only in respectof damage by any specified perils youare obliged to insure against under theterms of the contract and provided thatour liability in any one period of insurance shall not exceed the sum insured for each item nor in all the total sum insured

Off-site storage

Cover extends to include materials orgoods designated to be included in thecontract works whilst temporarily held instore away from the contract site but notwhile they are being worked upon

Limit £7,500 any one storage site

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 27

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 28

Maintenance and defects liability period

We will indemnify you for damage to thepermanent works or any part thereofoccurring during any maintenance ordefects liability period not exceeding 12months duration specified in the conditionsof contract but only in respect of damagefor which you are liable (a) arising from a cause occurring prior

to the commencement of themaintenance period

(b) occasioned by you in course ofoperations carried out by you for the purpose of complying with yourobligations under the maintenanceconditions of the contract

Our maximum liability shall not exceed 10% of the contract sum insured

Exclusions applicable to this endorsement

We shall not be liable for (a) the first £250 of each and every

claim under this endorsement (b) builder’s plant tools and equipment (c) damage by any event which you are

not obliged to insure against under the terms of the contract

(d) damage to any property which alreadyexisted at the time of thecommencement of the contract

(e) penalties under the contract for delayor non-completion or consequentialloss of any nature except as specificallyprovided for under this endorsement

Memoranda

Reinstatement basis of settlement in the event of a claim

Applicable unless stated otherwise in theschedule

Subject to the following special conditionsthe basis upon which the amount payable in respect of (a) contents but excluding bed linen

personal belongings and stock(b) buildingsis to be calculated shall be the reinstatementof the property lost destroyed or damaged

For this purpose ‘reinstatement’ means (a) the rebuilding or replacement of

property lost or destroyed whichprovided our liability is not increasedmay be carried out (i) in any manner suitable to your requirements

(ii) upon another site (b) the repair or restoration of

property damaged in the case of (a) or (b) to a conditionequivalent to or substantially the same asbut not better or more extensive than itscondition when new

1

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 28

29 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Special conditions applicable to memorandum 1

1 If at the time of reinstatement the sumrepresenting 85% of the cost whichwould have been incurred inreinstating the whole of the propertycovered by any item subject to thismemorandum exceeds its sum insuredat the commencement of any damageour liability shall not exceed thatproportion of the amount of thedamage which the said sum insuredadjusted for index linking shall bear tothe sum representing the total cost ofreinstating the whole of such property at that time

2 Our liability for the repair or restorationof property damaged in part only shallnot exceed the amount which wouldhave been payable had such propertybeen wholly destroyed

3 No payment beyond the amount whichwould have been payable in the absenceof this memorandum shall be made (a) unless reinstatement commences

and proceeds without unreasonabledelay

(b) until the cost of reinstatement shallhave been actually incurred

(c) if the property insured at the timeof its damage shall be insured byany other insurance effected byyou or on your behalf which is notupon the same basis ofreinstatement

4 All the terms and conditions of thepolicy shall apply (a) in respect of any claim payable

under this memorandum except in so far as they are varied hereby

(b) where claims are payable as if this memorandum had not beenincorporated

Day One basis – non-adjustable

This applies if a Day One figure is shownagainst an item in the schedule

1 You have agreed the declared valueincorporated in each item to which thisextension applies and the premium hasbeen calculated accordingly

‘declared value’ means your assessmentof the cost of reinstatement of theproperty insured (as defined in theReinstatement basis of settlementmemorandum) at the level of costsapplying at the inception of the period of insurance (ignoring inflationary factors which may operatesubsequently) together with in so far asthe insurance by the item provides dueallowance for (a) the additional cost of reinstatement

to comply with the stipulationsdefined in Extension 5 (EuropeanUnion and Public Authorities)

(b) professional fees (c) debris removal costs

2 At the inception of each period ofinsurance you shall notify us of thedeclared value of the property insuredby each of the said item(s)

In the absence of such declaration thelast amount declared by you (adjustedto reflect index linking) shall be takenas the declared value for the ensuingperiod of insurance

3 In respect of each item to which thisextension applies the following wordingsreplace Special conditions 1 and 4 of the Reinstatement memorandum (1) Each item insured under this

memorandum is declared to beseparately subject to the followingcondition of underinsurance namely

2

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 29

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 30

If at the time of damage the declaredvalue of the property covered by suchitem is less than the cost ofreinstatement (as defined in paragraph1 of the Day One memorandum) at theinception of the period of insurancethen our liability shall be limited to thatproportion thereof which the declaredvalue bears to such cost ofreinstatement

4 Where by reason of any of the aboveSpecial conditions no payment is to be made beyond the amount whichwould have been payable under thepolicy if this memorandum had not beenincorporated the rights and liabilities of the Company and the Insured inrespect of the damage shall be subjectto the terms of the policy including any condition of underinsurance as if this memorandum had not beenincorporated except that the sumsinsured shall be increased in proportionwith the additional amount charged in respect of this memorandum

Index-linking

The sum insured and where applicable thedeclared value of each item insured underthis section will be adjusted in accordancewith suitable indices selected by us

The annual renewal premium will beamended accordingly

Underinsurance

Unless otherwise shown in the schedule orelsewhere in this policy the sum insured byeach item insured is subject to thefollowing

If the property insured by any item of thissection shall at the commencement of anydamage to such property be collectively ofgreater value than such sum insured asadjusted for index-linking you will beconsidered as being your own insurer forthe difference and shall bear a rateableproportion of the loss accordingly

4

3

Other interests

The interest in the insurance by this sectionof the various mortgagees lessors andfreeholders of the property is noted

Antique items and Antiquities

Unless an article is specifically insured in a separate sum the indemnity provided under this section is limited to the cost ofrestoration so far as that may be practicableor the cost of modern replicas and not anyvalue attaching to the property by reason of its antiquity

Exclusions

We shall not be liable in respect of (1) damage caused by pollution or

contamination but this shall not exclude damage to the propertyinsured not otherwise excluded caused by (a) pollution or contamination

which itself results from any of the insured events other than 15 Accidental damage

(b) any of the insured eventsother than 15 Accidental damage which itself results from pollution orcontamination

(2) consequential loss of any kind (3) property insured under section 3

Fine art and collections

6

5

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 30

31 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

(4) damage cost or expense ofwhatsoever nature directly or indirectlycaused by resulting from or inconnection with terrorism regardless of any other contributory cause This insurance also excludes damagecost or expense of whatsoever nature directly or indirectly caused by resulting from or in connection with any action taken in controllingpreventing suppressing or in any way relating to terrorismIf we allege that by reason of thisexclusion any damage cost or expenseis not covered by this policy the burdenof proving the contrary shall be uponyou

(5) damage to any computer or otherequipment or component or system oritem which processes stores transmitsretrieves or receives data or any partthereof whether tangible or intangible(including but without limitation anyinformation or programs or software)and whether your property or notwhere such damage is caused by virus or similar mechanism orhacking or denial of service attack

(6) damage to any electrical plant orapparatus caused by self-ignition butthis exclusion shall apply only to thatpart of the electrical plant or apparatusin which self-ignition occurs

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 31

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 32

The schedule will show if this section applies and the cover in force

Cover A – Extended cover

Definition

Each time the following appears in thissection in bold italic type (or in capitalletters in the schedule) it will take thespecific meaning shown below

Where it is not highlighted in this mannerthe normal everyday meaning will apply

Item(s) insuredmeans the items insured shown in the Property damage plus section of the schedule

Cover

We will indemnify you (by payment up tothe value of the item insured at the time of the loss or at our option by repairreinstatement or replacement) in respect of damage to the item insured by anycause not specifically excluded happeningwithin the location stated in the schedule and during the period of insurance

Provided that our liability in any one periodof insurance shall not exceed the suminsured for each item nor in all the totalsum insured

Memoranda

Reinstatement basis of settlement in the event of a claim

Applicable unless stated otherwise in the schedule

The basis upon which the amount payablein respect of the property insured by thissection is to be calculated shall be (a) where the property is lost or destroyed

its replacement by similar property in acondition equal to but not better or moreextensive than its condition when new

(b) where property is damaged the repairof the damage and restoration of thedamaged portion of the property to acondition substantially the same as butnot better or more extensive than itscondition when new

Index-linking

The sum insured by each item insuredunder this section will be adjusted inaccordance with suitable indices selectedby us and the annual renewal premium will be amended accordingly

Reinstatement of sum insured

In consideration of your agreement to pay such additional premium as may be requiredwe will automatically reinstate the sum insured in full after damage has occurred provided that we have not given you notice within 30days of you reporting the damage to usthat we will not reinstate the sum insured

3

2

1

Property damage plus 2

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 32

33 POLICY DOCUMENT HERITAGE COMMERCIAL INSURANCE

Exclusions

We shall not be liable for (1) damage occasioned by or happening

through gradual deteriorationdepreciation mechanical or electricalbreakdown failure or breakage wearand tear atmospheric and climaticconditions (other than storm or flood)pollution or contamination rust dustmoth vermin or any process ofcleaning dyeing restoration or repair towhich the property is subjected delayconfiscation detention or destructionby order of the government or anypublic authority

(2) breakage of electrical valves bulbs ortubes unless the equipment in whichthey are contained is damaged at the same time

(3) consequential loss of any kind(4) damage to a trailer or caravan whilst

attached to or being towed by a motor vehicle

(5) damage due to theft attempted theftmalicious persons or vandals whilst theproperty is contained in an unattendedvehicle unless (i) the motor vehicle is locked at all

points of access(ii) there are visible signs of forcible or

violent entry to the vehicle(iii) the property unless permanently

fixed in position is out of sight in alocked compartment or locked bootwithin the vehicle

(6) property insured under section 3 Fineart and collections

Cover B – Deterioration of stock

We will indemnify you by payment up to thevalue of the items insured at the time ofloss in respect of damage to the contentsof the chill or deep freeze unit(s) describedin the schedule as a result of failure of theunit failure of the electricity or gas supplyor contamination from refrigerant orrefrigerant fumes happening during theperiod of insurance and if incurred thenecessary and reasonable cost of hiringtemporary alternative freezing space

Provided that our liability in any one periodof insurance shall not exceed the limit ofliability shown in the schedule

Memorandum

Reinstatement of sum insured

In consideration of your agreement to paysuch additional premiums as may berequired we will automatically reinstate thesum insured in full after damage hasoccurred provided that we have not givenyou notice within 30 days of you reportingthe damage to us that we will not reinstatethe sum insured

ME083 Q8_EI Heritage Policy doc 23/12/2013 09:52 Page 33

HERITAGE COMMERCIAL INSURANCE POLICY DOCUMENT 34

Exclusions

We shall not be liable for(1) damage caused by the deliberate act

of any electricity or gas supply authorityin withholding or restricting supply

(2) damage arising from the breakdown or malfunction of any unit which is over 15 years old unless therefrigeration unit is the subject of acurrent manufacturers guarantee or an annual maintenance contract

(3) damage caused by your wilful act or neglect

(4) damage insured under section 1Property damage extension 19 –Freezer contents

Cover A & B – Special condition

Underinsurance