hft 2403 chapter 5 the income statement. major financial statements used by business income...

TRANSCRIPT

HFT 2403

Chapter 5

The Income Statement

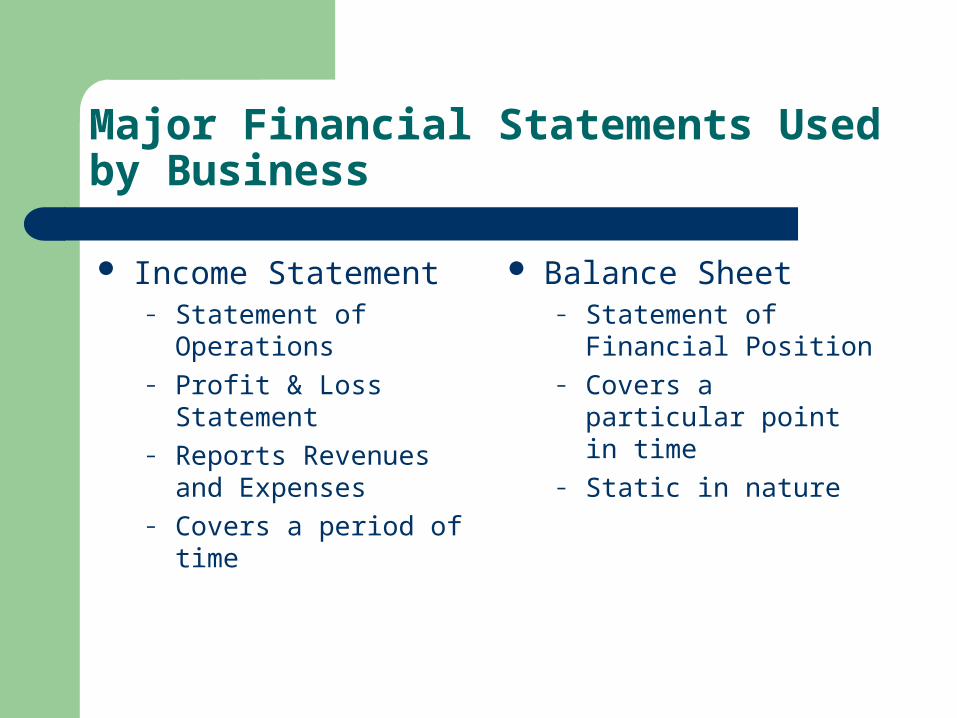

Major Financial Statements Used by Business

Income Statement– Statement of Operations– Profit & Loss Statement– Reports Revenues and

Expenses– Covers a period of time

Balance Sheet– Statement of Financial

Position– Covers a particular point

in time– Static in nature

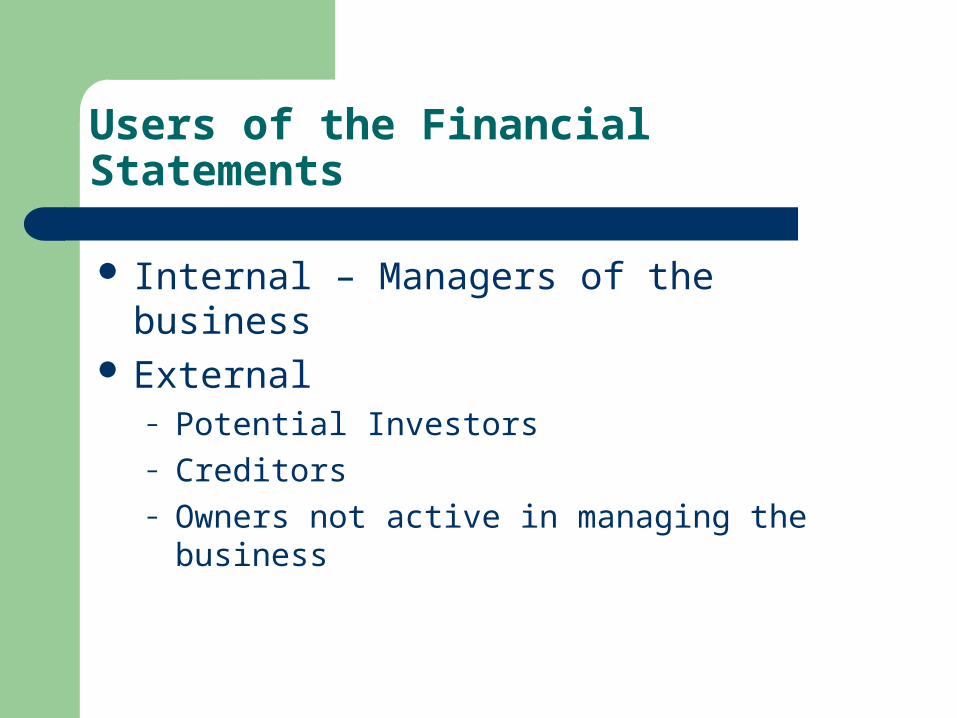

Users of the Financial Statements

Internal – Managers of the business External

– Potential Investors– Creditors– Owners not active in managing the business

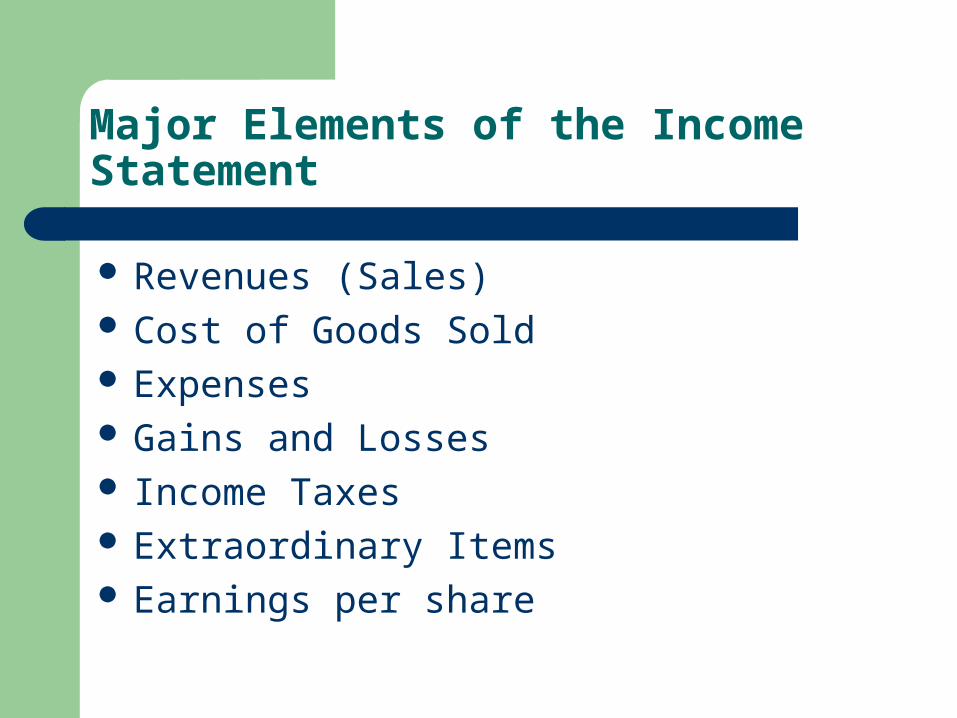

Major Elements of the Income Statement

Revenues (Sales) Cost of Goods Sold Expenses Gains and Losses Income Taxes Extraordinary Items Earnings per share

Revenues

Revenues for services are recorded when the event occurs– Legal title passes from the seller to the buyer– Selling price has been established– Seller’s obligation is complete– The service has been exchanged for another

asset (cash or accounts receivable)

Cost of Goods Sold

Goods that are purchased for resale are initially recorded as inventory

When they are sold, they are transferred to the Cost of Goods Sold expense account

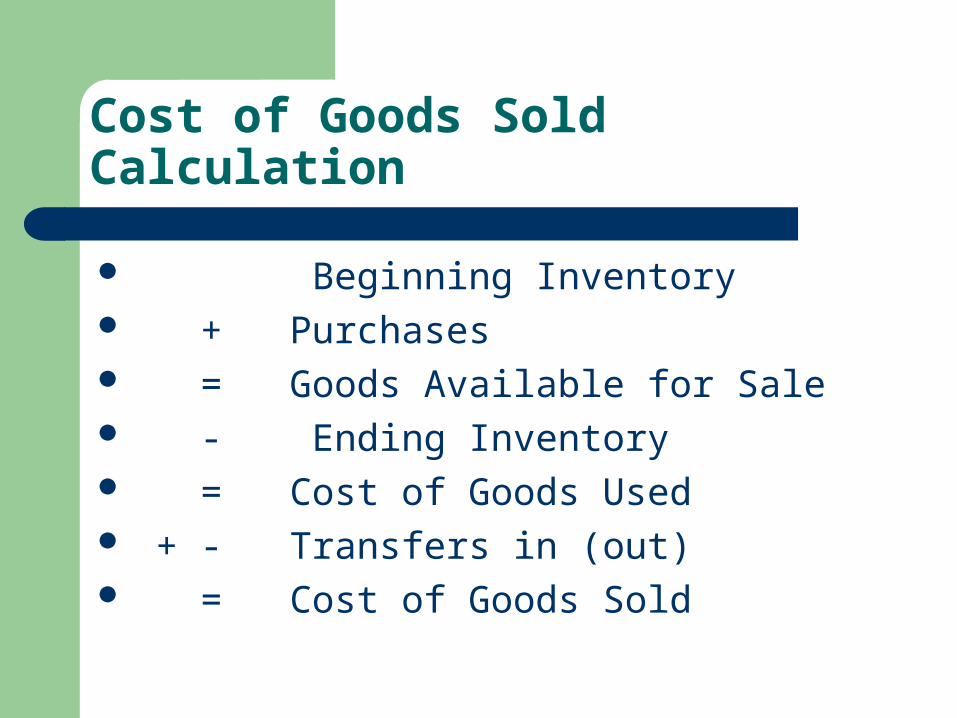

Cost of Goods Sold Calculation

Beginning Inventory + Purchases = Goods Available for Sale - Ending Inventory = Cost of Goods Used + - Transfers in (out) = Cost of Goods Sold

Expenses

Day to Day Operational Expenses Payroll Expenses Specific Departmental Expenses Repair & Maintenance Expense Sales Expenses Administrative Expenses Other Undistributed Expenses

Gains & Losses

Gains – Increases in assets, reductions in liabilities or a combination of both resulting from incidental transactions

ie: Sale of used equipment Losses – Decreases in assets, increases in

liabilities or a combination of both resulting from incidental transactions

ie: Storm Damage Deductibles

Income Taxes

Based on the relevant revenues and expenses

Usually a variance in taxes booked and taxes paid – due to various accruals

Recorded as deferred income taxes (liability)

Extraordinary Items

Must meet two criteria– Must be of a high degree of abnormality and be

clearly unrelated to the ordinary and typical activities of the business

– Infrequent occurrence – must not be reasonably expected to occur again

Earnings per Share

Total net earnings of the business for each common share outstanding

EPS = Net Income Common Shares Outstanding

Only used for business organized as corporations or LLC

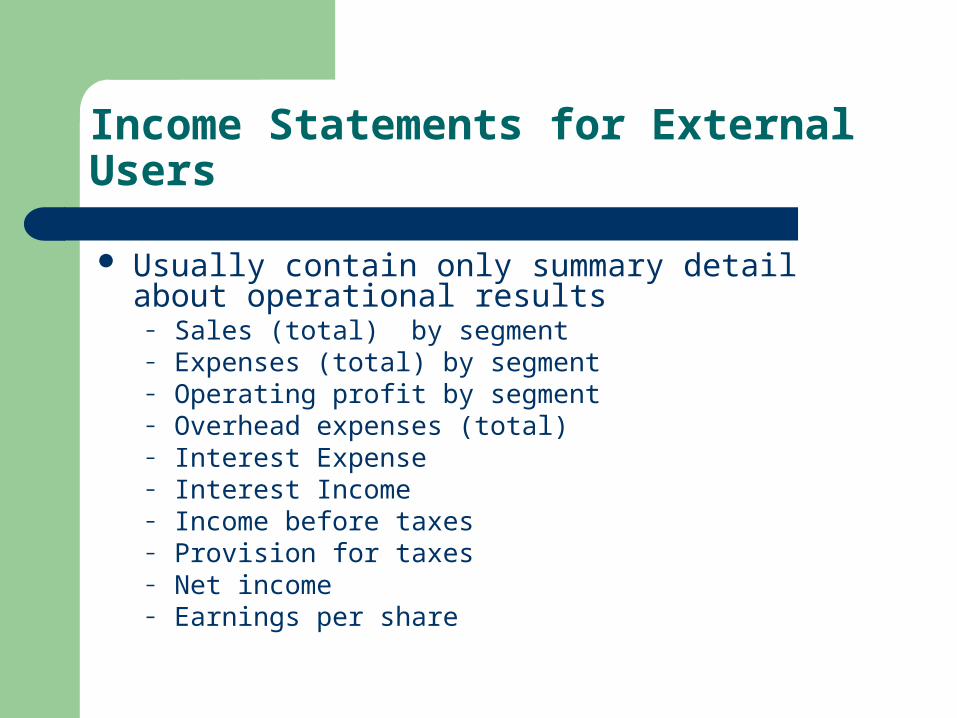

Income Statements for External Users

Usually contain only summary detail about operational results

– Sales (total) by segment– Expenses (total) by segment– Operating profit by segment– Overhead expenses (total)– Interest Expense– Interest Income– Income before taxes– Provision for taxes– Net income– Earnings per share

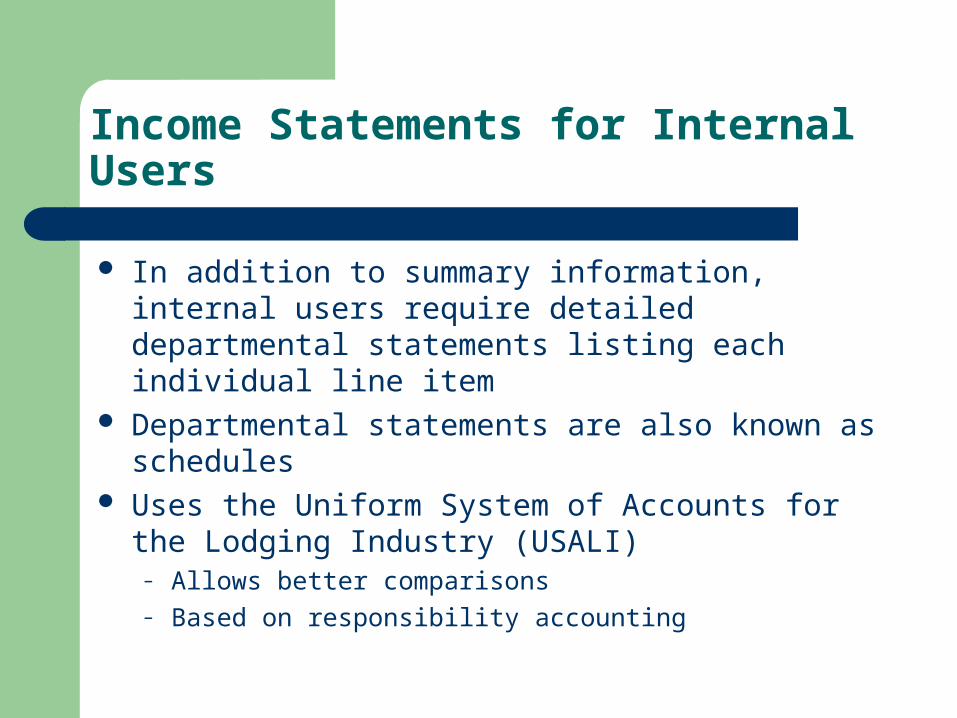

Income Statements for Internal Users

In addition to summary information, internal users require detailed departmental statements listing each individual line item

Departmental statements are also known as schedules

Uses the Uniform System of Accounts for the Lodging Industry (USALI)

– Allows better comparisons– Based on responsibility accounting

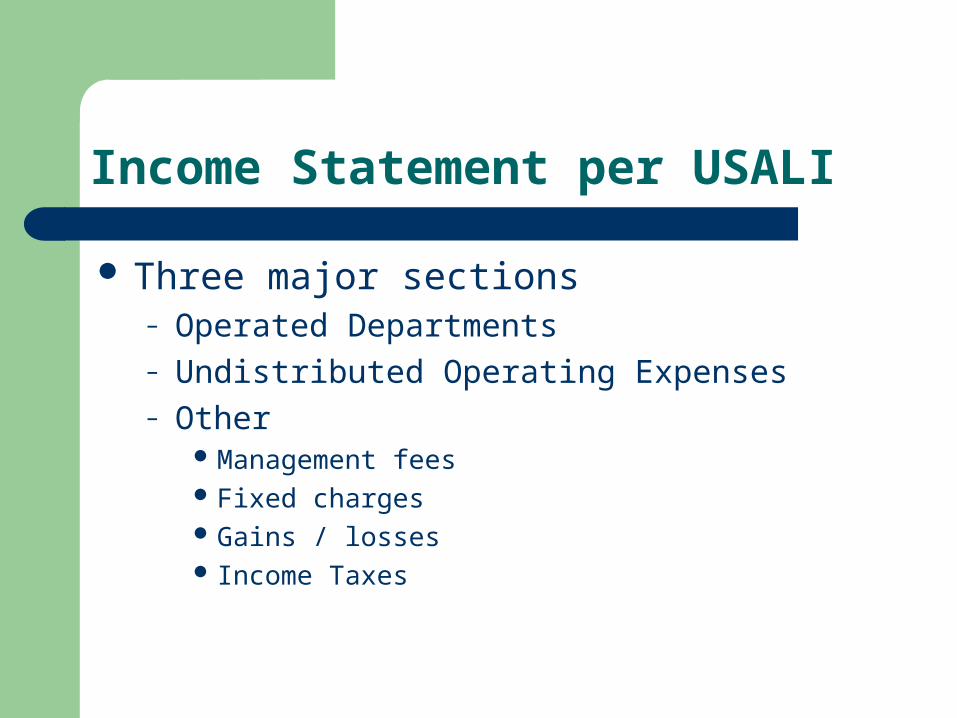

Income Statement per USALI

Three major sections– Operated Departments– Undistributed Operating Expenses– Other

Management fees Fixed charges Gains / losses Income Taxes

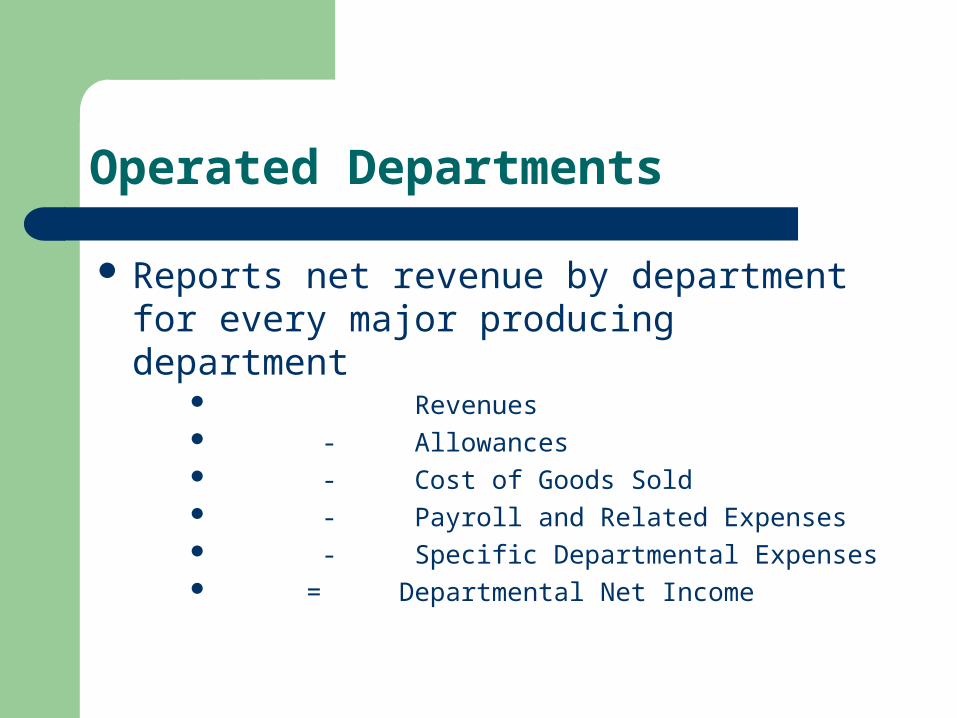

Operated Departments

Reports net revenue by department for every major producing department

Revenues - Allowances - Cost of Goods Sold - Payroll and Related Expenses - Specific Departmental Expenses = Departmental Net Income

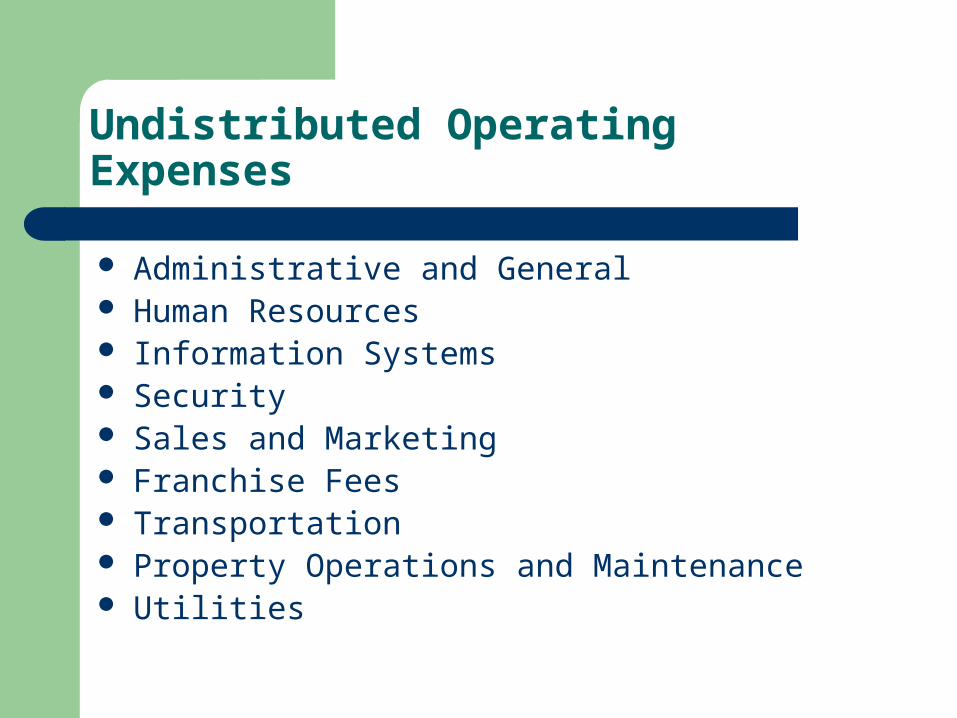

Undistributed Operating Expenses

Administrative and General Human Resources Information Systems Security Sales and Marketing Franchise Fees Transportation Property Operations and Maintenance Utilities

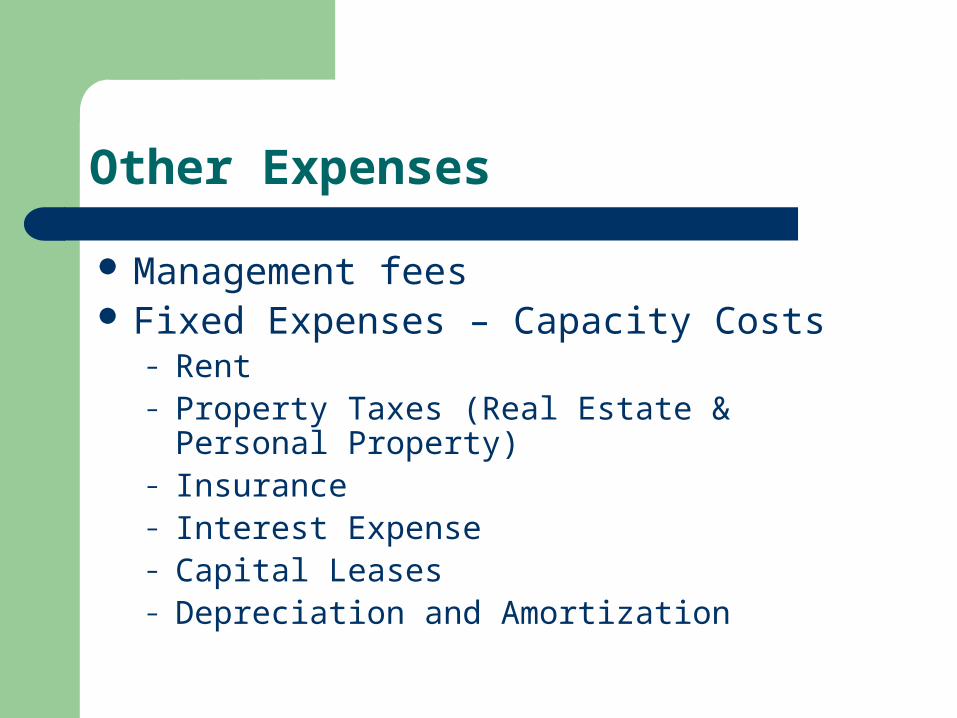

Other Expenses

Management fees Fixed Expenses – Capacity Costs

– Rent– Property Taxes (Real Estate & Personal Property)– Insurance– Interest Expense– Capital Leases– Depreciation and Amortization

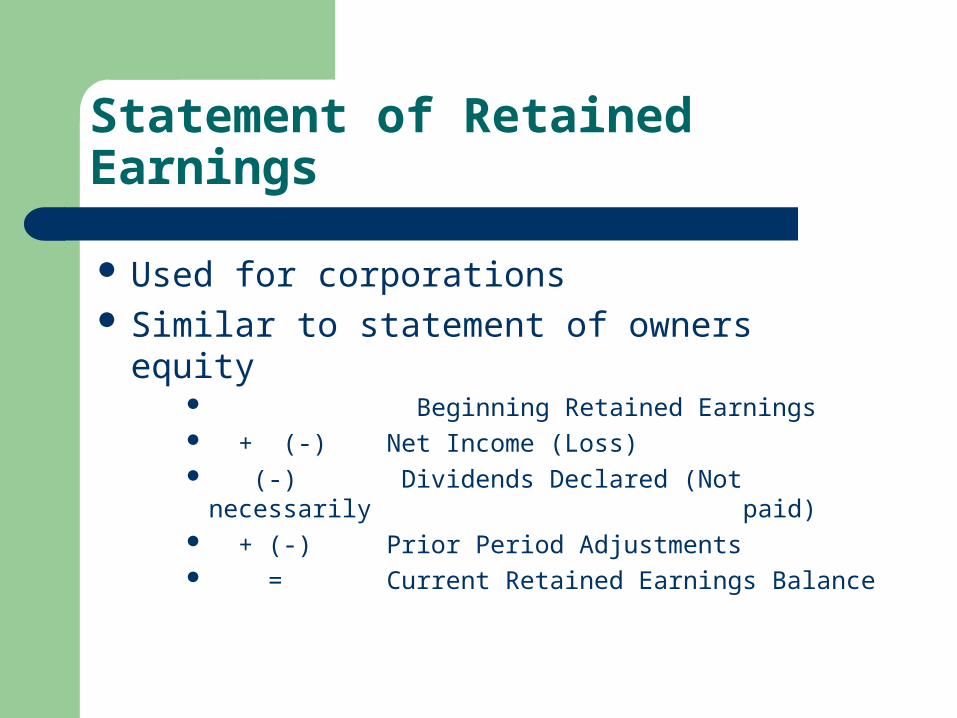

Statement of Retained Earnings

Used for corporations Similar to statement of owners equity

Beginning Retained Earnings + (-) Net Income (Loss) (-) Dividends Declared (Not necessarily

paid) + (-) Prior Period Adjustments = Current Retained Earnings Balance

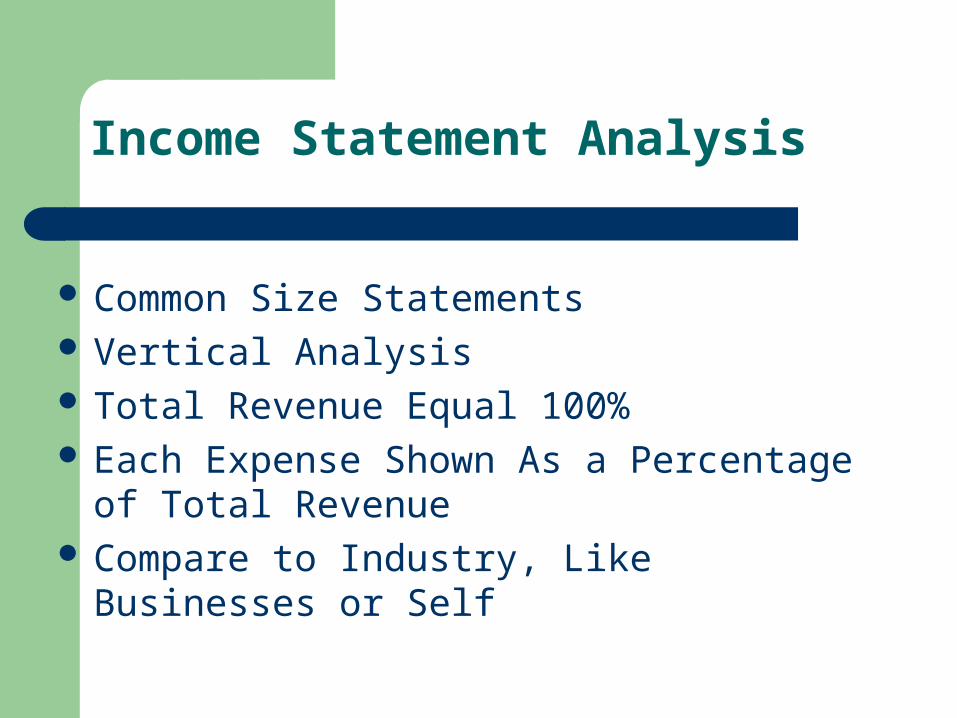

Income Statement Analysis

Common Size Statements Vertical Analysis Total Revenue Equal 100% Each Expense Shown As a Percentage of Total

Revenue Compare to Industry, Like Businesses or Self

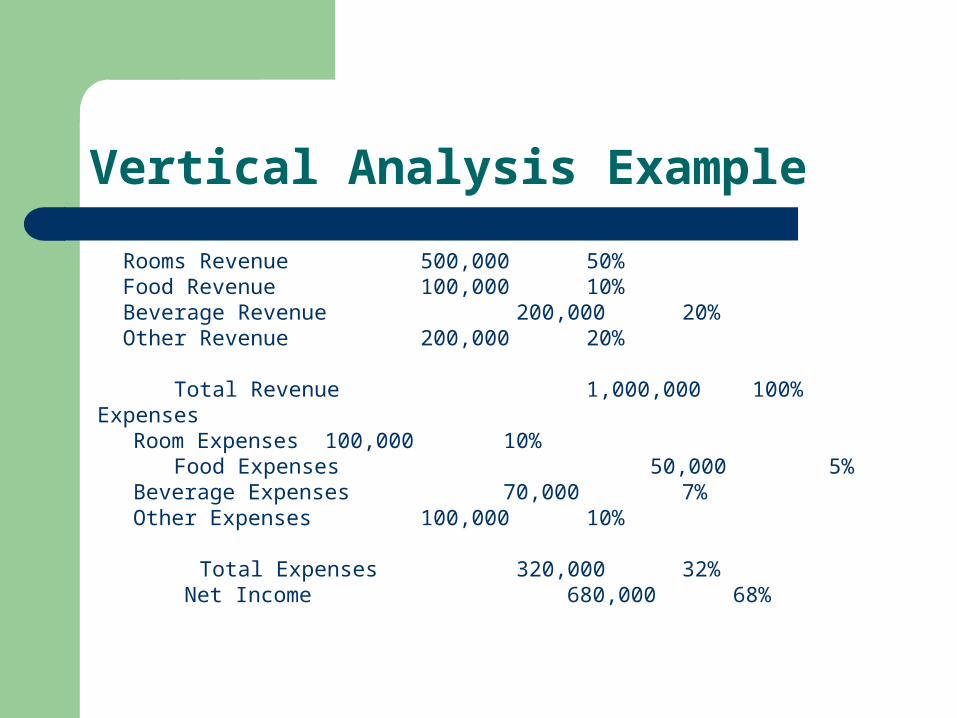

Vertical Analysis Example

Rooms Revenue 500,000 50% Food Revenue 100,000 10% Beverage Revenue 200,000 20% Other Revenue 200,000 20% Total Revenue 1,000,000 100%Expenses

Room Expenses 100,000 10% Food Expenses 50,000 5%

Beverage Expenses 70,000 7%Other Expenses 100,000 10%

Total Expenses 320,000 32% Net Income 680,000 68%

Homework Assignment

Problem 1 Problem 2 Problem 5 Problem 9 Problem 10 Problem 11