high deductible health plan (hdhp) is it a good option for you?

TRANSCRIPT

High Deductible Health Plan (HDHP)

Is it a good option for you?

The legal definition of a High Deductible Health Plan (HDHP) from the IRS is:

A higher annual deductible than typical health plans, and a maximum limit on the sum of the annual deductible and out-of-pocket medical expenses that you must pay for covered expenses; Out-of-pocket expenses include copayments and other amounts, but do not include premiums.

What is a High Deductible Health Plan (HDHP)?

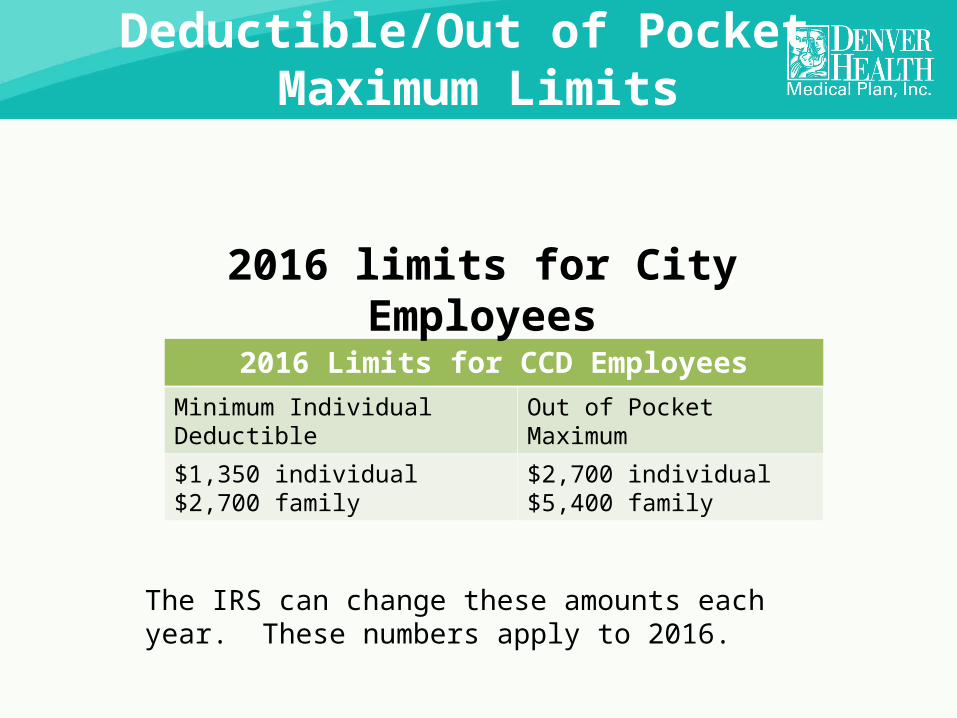

The IRS can change these amounts each year. These numbers apply to 2016.

2016 Limits for CCD EmployeesMinimum Individual Deductible Out of Pocket Maximum

$1,350 individual$2,700 family

$2,700 individual$5,400 family

2016 limits for City Employees

Deductible/Out of Pocket Maximum Limits

■ Preventive care is covered at $0 for members

■ Annual check ups

■ Prenatal visits

■ Well child care

■ Well woman exams

■ Immunizations

All of the above are covered at $0 with NO deductible or coinsurance.

IMPORTANT NOTE

Preventive Care

Urgent Care visitBilled Charges ………….………….…………$500Allowed Charges (after DHMP contract rate discount)……………….…$250 YOU pay……… $250

Urgent Care visitBilled Charges ………….………….…………$500Allowed Charges (after DHMP contract rate discount)……………….…$250 YOU pay……… $250

The $250 you pay is applied to both your deductible and your out-of-pocket max

Deductible

Example:

Once you meet the applicable deductible, DHMP will begin to share the cost of medical care expenses with you. This is called coinsurance.

Coinsurance is a percentage of allowed charges.

Coinsurance

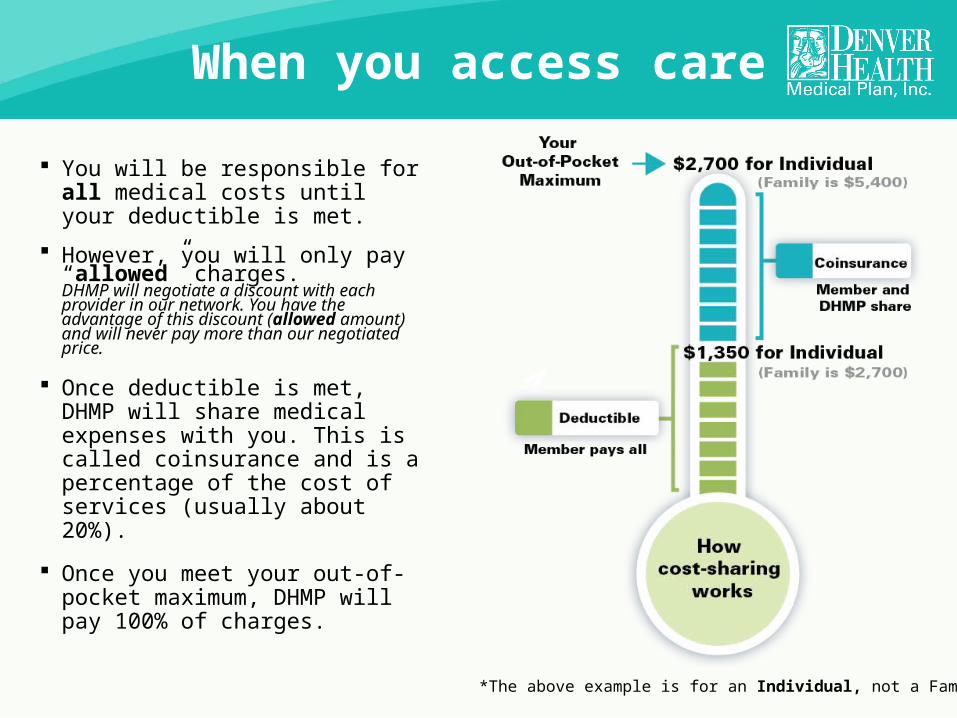

When you access care

You will be responsible for all medical costs until your deductible is met.

However, you will only pay “allowed” charges. DHMP will negotiate a discount with each provider in our network. You have the advantage of this discount (allowed amount) and will never pay more than our negotiated price.

Once deductible is met, DHMP will share medical expenses with you. This is called coinsurance and is a percentage of the cost of services (usually about 20%).

Once you meet your out-of-pocket maximum, DHMP will pay 100% of charges.

*The above example is for an Individual, not a Family.

HDHP Video

How will I pay for medical services on January 1st?

Answer: Your Health Savings Account (HSA)

Participation in a HDHP makes you eligible to have a HSA account. This is a tax-free account — both you and your employer can add funds to this account.

The Big Question

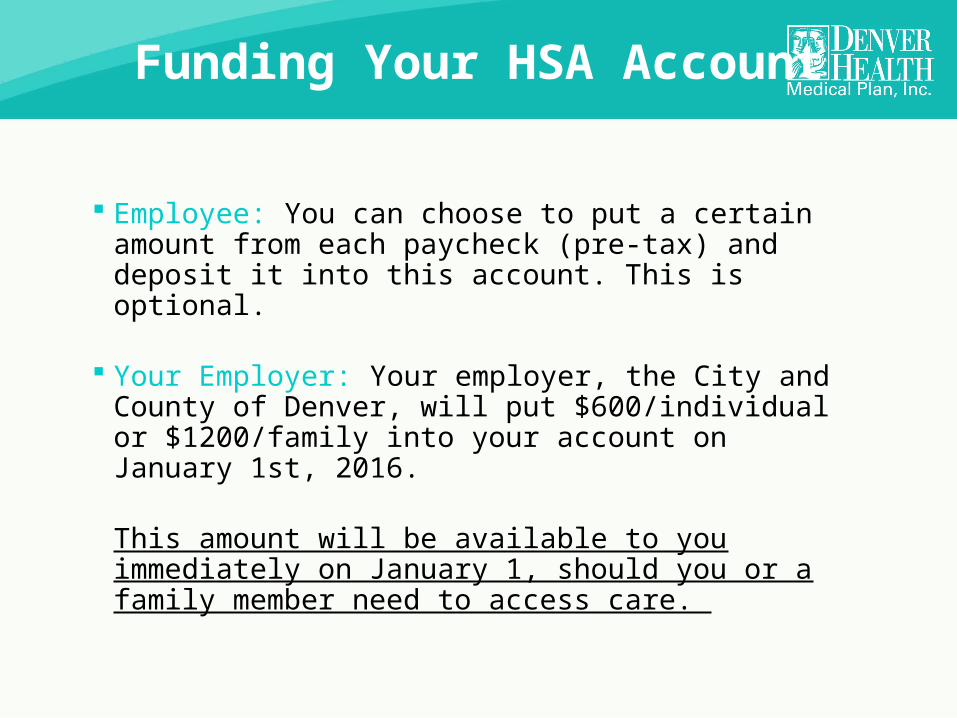

Employee: You can choose to put a certain amount from each paycheck (pre-tax) and deposit it into this account. This is optional.

Your Employer: Your employer, the City and County of Denver, will put $600/individual or $1200/family into your account on January 1st, 2016.

This amount will be available to you immediately on January 1, should you or a family member need to access care.

Funding Your HSA Account

FSA vs HSA

Worst Case Scenario

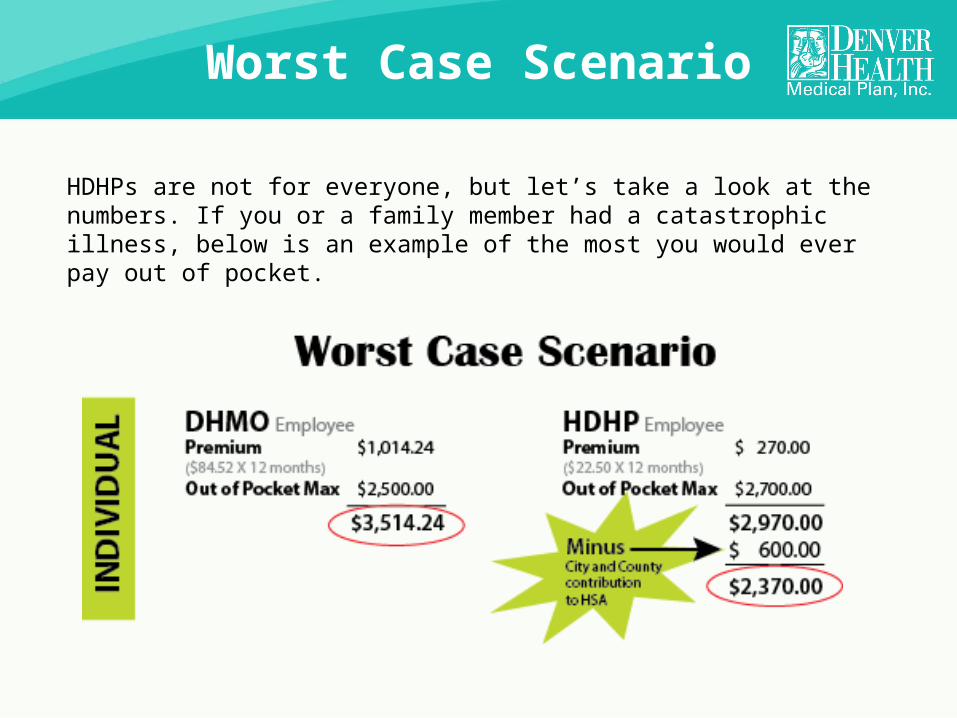

HDHPs are not for everyone, but let’s take a look at the numbers. If you or a family member had a catastrophic illness, below is an example of the most you would ever pay out of pocket.

Worst Case Scenario

What are your costs?

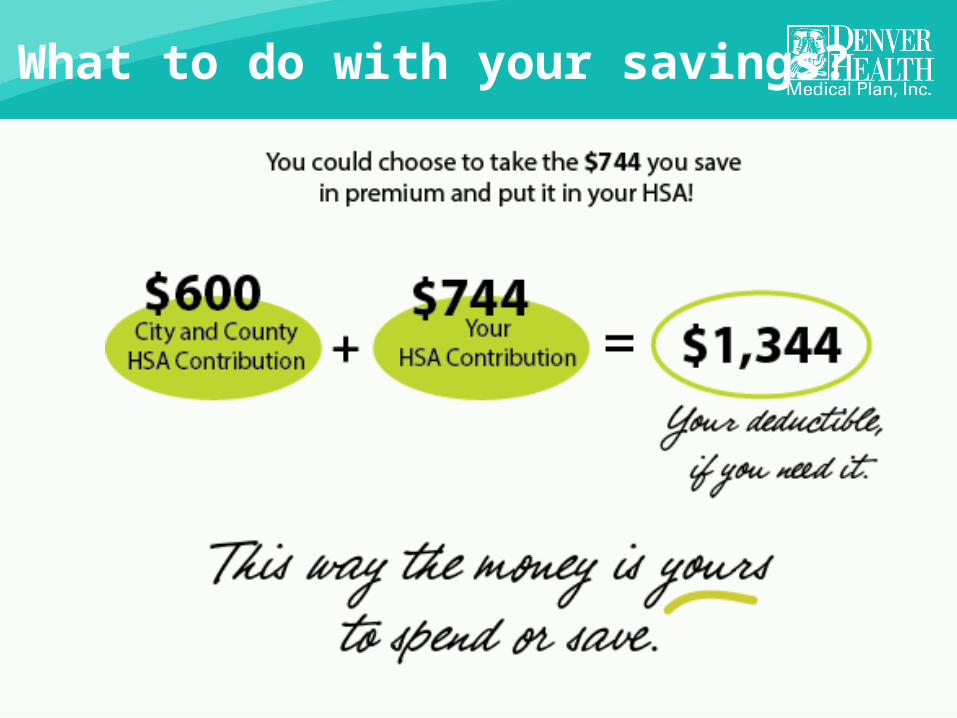

What to do with your savings?

HDHP plan Save money on

monthly premiums Have a tax-free HSA to

help you with unexpected health care expenses

Which is the plan for you?

DHMO plan Pay larger monthly premiumsLess out of pocket, butNo HSA

Questions?