hillsdale county medical care facility - michigan307509... · the financial position of hillsdale...

TRANSCRIPT

Hillsdale County Medical Care Facility

Financial Report

with Additional Information

December 31, 2012

Hillsdale County Medical Care Facility

Contents

Report Letter 1-2

Management's Discussion and Analysis 3-7

Financial Statements

Balance Sheet 8

Statement of Revenue, Expenses, and Changes in Net Position 9

Statement of Cash Flows 10-11

Notes to Financial Statements 12-22

Additional Information 23

Schedule of Net Service Revenue 24

Schedule of Operating Expenses 25

Independent Auditor's Report

To the Board of DirectorsHillsdale County Medical Care Facility

Report on the Financial Statements

We have audited the accompanying financial statements of Hillsdale County Medical CareFacility (the "Facility"), a component unit of Hillsdale County, as of and for the years endedDecember 31, 2012 and 2011 and the related notes to the financial statements, whichcollectively comprise Hillsdale County Medical Care Facility's basic financial statements as listedin the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financialstatements in accordance with accounting principles generally accepted in the United States ofAmerica; this includes the design, implementation, and maintenance of internal control relevantto the preparation and fair presentation of financial statements that are free from materialmisstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. Weconducted our audits in accordance with auditing standards generally accepted in the UnitedStates of America. Those standards require that we plan and perform the audits to obtainreasonable assurance about whether the financial statements are free from materialmisstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor’sjudgment, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of theentity’s internal control. Accordingly, we express no such opinion. An audit also includesevaluating the appropriateness of accounting policies used and the reasonableness of significantaccounting estimates made by management, as well as evaluating the overall presentation of thefinancial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinion.

1

To the Board of DirectorsHillsdale County Medical Care Facility

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects,the financial position of Hillsdale County Medical Care Facility as of December 31, 2012 and2011 and the changes in its financial position and cash flows for the years then ended, inaccordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplemental Information

Accounting principles generally accepted in the United States of America require that themanagement's discussion and analysis on pages 3-7 be presented to supplement the basicfinancial statements. Such information, although not a part of the basic financial statements, isrequired by the Governmental Accounting Standards Board, which considers it to be an essentialpart of financial reporting for placing the basic financial statements in an appropriate operational,economic, or historical context. We have applied certain limited procedures to the requiredsupplemental information in accordance with auditing standards generally accepted in the UnitedStates of America, which consisted of inquiries of management about the methods of preparingthe information and comparing the information for consistency with management's responses toour inquiries, the basic financial statements, and other knowledge we obtained during our auditof the basic financial statements. We do not express an opinion or provide any assurance on theinformation because the limited procedures do not provide us with sufficient evidence toexpress an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise Hilldale County Medical Care Facility's basic financial statments. The otheradditional information, as identified in the table of contents, is presented for the purpose ofadditional analysis and is not a required part of the basic financial statements. Such information isthe responsibility of management and was derived from and relates directly to the underlyingaccounting and other records used to prepare the basic financial statements. The informationhas been subjected to the auditing procedures applied in the audit of the basic financialstatements and certain additional procedures, including comparing and reconciling suchinformation directly to the underlying accounting and other records used to prepare the basicfinancial statements or to the basic financial statements themselves, and other additionalprocedures in accordance with auditing standards generally accepted in the United States ofAmerica. In our opinion, the other additional information is fairly stated in all material respectsin relation to the basic financial statements as a whole.

May 15, 2013

2

Hillsdale County Medical Care Facility

Management's Discussion and Analysis

The management's discussion and analysis of Hillsdale County Medical Care Facility's (the"Facility") financial performance provides an overview of the Facility's financial activities for thefiscal years ended December 31, 2012 and 2011. Please read it in conjunction with the Facility'sfinancial statements, which begin immediately following the management's discussion andanalysis. Unless otherwise indicated, amounts are in thousands throughout the management'sdiscussion and analysis section.

Financial Highlights

The Facility's net position increased in the current year and decreased in the previous yearwith a $779, or 8 percent, increase in 2012 and ($806) or an 8 percent decrease in 2011.

The Facility reported operating income in 2012 of $262 and an operating loss in 2011 of($1,266).

Nonoperating revenue increased by $55 or 10 percent in 2012 compared to 2011.Nonoperating revenue decreased in 2011 by $198, or 27 percent, compared to 2010.

Using this Annual Report

The Facility's financial statements consist of three statements: a balance sheet, a statement ofrevenue, expenses, and changes in net position, and a statement of cash flows. These financialstatements and related notes provide information about the activities of the Facility, includingresources held by the Facility but restricted for specific purposes by contributors, grantors, orenabling legislation.

The Balance Sheet and Statement of Revenue, Expenses, and Changes in Net Position

Analysis of the Facility’s finances is presented on the following pages. One of the most importantquestions asked about the Facility's finances is, "Is the Facility, as a whole, better or worse off asa result of the year's activities?" The balance sheet and the statement of revenue, expenses, andchanges in net position report information about the Facility's resources and its activities in a waythat helps answer this question. All assets and liabilities are recorded using the accrual basis ofaccounting. All of the current year's revenue and expenses are taken into account regardless ofwhen cash is received or paid.

These two statements report the Facility's net position and changes in them. You can think ofthe Facility's net position, the difference between assets and liabilities, as one way to measurethe Facility's financial health, or financial position. Over time, increases or decreases in theFacility's net position are one indicator of whether its financial health is improving ordeteriorating. You will need to consider other nonfinancial factors, however, such as changes inthe Facility's resident base and measures of the quality of service it provides to the community,as well as local economic factors, to assess the overall health of the Facility.

3

Hillsdale County Medical Care Facility

Management's Discussion and Analysis (Continued)

The Statement of Cash Flows

The final required statement is the statement of cash flows. The statement reports cashreceipts, cash payments, and net changes in cash resulting from operating, investing, andfinancing activities. It provides answers to such questions as, "Where did cash come from?","What was cash used for?", and "What was the change in cash balance during the reportingperiod?"

The Facility's Net Position

The Facility's net position is the difference between its assets and liabilities reported in thebalance sheet following this section. The Facility's net position increased by $779 (8 percent) in2012, as you can see from Table 1.

Table 1: Assets, Liabilities, and Net Position (whole dollars)

2012 2011 2010

AssetsCash and cash equivalents $ 1,541,791 $ 1,560,480 $ 2,862,028Resident accounts receivable 1,431,359 1,795,372 1,398,532Other assets 263,487 319,025 282,766Estimated third-party payor settlements 473,862 - -Taxes receivable 757,827 706,684 620,352

Property and equipment 12,448,270 12,771,385 12,644,910

Total assets 16,916,596 17,152,946 17,808,588

LiabilitiesAccounts payable 348,719 315,531 205,922Construction accounts payable - - 403,045Funds held for residents 24,100 20,235 18,790Accrued compensation and related liabilities 497,098 405,995 392,174Accrued compensated absences 332,752 287,723 269,091Accrued professional and other liability claims 132,473 140,151 321,315Deferred taxes 757,827 706,685 620,352Estimated third-party payor settlements - 805,610 242,420Other 196,035 227,313 357,622Debt payable 2,590,000 2,985,000 3,430,000

Postemployment benefit obligation 1,824,000 1,824,000 1,307,000

Total liabilities 6,703,004 7,718,243 7,567,731

Net PositionNet investment in capital assets 9,858,270 9,786,385 9,614,388

Unrestricted 355,322 (351,682) 626,469

Total net position $ 10,213,592 $ 9,434,703 $ 10,240,857

4

Hillsdale County Medical Care Facility

Management's Discussion and Analysis (Continued)

Significant components of the changes in the Facility's total assets are due to the collection andreconciliation of past due accounts receivable of $364 and asset disposals totaling $349 of fullydepreciated old assets.

Table 2: Operating Results and Changes in Net Position (whole dollars)

2012 2011 2010

Operating RevenueNet service revenue $ 15,401,981 $ 13,374,566 $ 12,969,699Other operating revenue 48,382 46,107 53,664

Quality assurance supplement 2,036,803 1,879,798 1,953,666

Total operating revenue 17,487,166 15,300,471 14,977,029

Operating ExpensesSalaries 9,634,002 8,626,581 7,951,657

Other expenses 7,591,504 7,939,895 8,261,039

Total operating expenses 17,225,506 16,566,476 16,212,696

Operating Income (Loss) 261,660 (1,266,005) (1,235,667)

Nonoperating Income (Expenses)Interest income 4,603 51,790 17,966Loss on disposal of property (7,265) (429) (1,974)Contributions 2,419 2,699 1,467Tax revenue 699,578 595,518 787,755

Interest expense (102,008) (107,160) (64,570)

Total nonoperating income 597,327 542,418 740,644

Surplus (Deficit) of Revenue Over Expenses 858,987 (723,587) (495,023)

Transfer to County (80,098) (82,567) (86,958)

Increase (Decrease) in Net Position $ 778,889 $ (806,154) $ (581,981)

Increase (Decrease) in Net Position

The first component of the overall change in the Facility's net position is its income (loss);generally, this is the difference between net service revenue and the expenses incurred toperform those services. During the past two years, the Facility has reported income in 2012 of$262 and a loss in 2011 of ($1,266).

5

Hillsdale County Medical Care Facility

Management's Discussion and Analysis (Continued)

The primary components of these operating financial changes are as follows:

The most significant change in the increase (decrease) in net position is due to thediscontinuation of offering a postretirement insurance benefit for our retirees. As a result,the actuarially determined accrual for unfunded pension benefit was unchanged from 2011,resulting in a required contribution of $0 for 2012 and thus reducing our expense in 2012by an estimated $517 compared to the prior year.

GASB Statement No. 45 requires the Facility to accrue for future costs forpostemployment healthcare benefits. The accruals resulting from this requirement were$0 for 2012 and $517 for 2011 and account for most of the loss totals that we have had forthe past few years. We have reduced the annual expense accrual to $0 by eliminating theretirement benefits for all future employees. All current retirees are still on the retirementplan. Also, by revising our retirees insurance program and requiring all retired employeesover 65 to enroll in a Medicare Supplement plan, we have reduced our yearly insuranceretiree expense by $84 during the 2012 operating year.

Health insurance premiums decreased $438 for 2012 over 2011. In addition to changingthe retirees' insurance program, the employees' health and dental insurance plans werechanged as well. The Facility has changed from a Priority POS insurance plan with nodeductible to a Blue Cross/Blue Shield HRA with a higher deductible funded by the facilityand the dental plan was changed to a 100 percent facility funded plan. The cost savings forthe medical and dental insurance premium changes for 2012 was a total of $477.

Nonoperating Revenue

The change in nonoperating revenue of $55 consists of the taxable values in Hillsdale Countyincreasing tax revenue by $104 and an interest income decrease of approximately ($47).

The Facility's Cash Flows

The Facility’s cash flows are consistent with the changes in operating income (loss) andnonoperating revenue and expenses. The change in cash of ($19) is accounted for by severalfactors during the year, such as a change in the financing activities due to the cottage addition($113) and an addition to our tax revenue of $104, along with various other smaller changes.

Capital Assets and Debt Administration

Capital Assets

At the end of 2012, the Facility had $12.4 million of net investment in capital assets, as detailed inNote 4 to the financial statements. During 2012, $229 of assets were capitalized. The Facilitydisposed of $349 of fully depreciated assets. In 2011, the Facility added new fixed assets costing$2.5 million, which was mainly for the cottage project.

6

Hillsdale County Medical Care Facility

Management's Discussion and Analysis (Continued)

Debt

At year end, the Facility had $2.6 million in bonds and debt service obligations owed to theCounty of Hillsdale and the Building Authority. The Facility’s formal debt issuances cannot beissued without approval of the Hillsdale County Board of Commissioners. The amount of debtissued is subject to limitations that apply to the County and its component units as a whole.

Other Economic Factors

Funding for the Facility has remained relatively stable for the past two years. Medicare/Medicaidrates have remained fairly consistent with prior year rates. The Facility is still included in theState’s quality assurance program. We continue to have a nursing shortage in the area, forcingus to remain very competitive with wages.

The Facility is currently a 170-bed facility and our occupancy remains consistent at 97 percent.We seem to be seeing a predicted national trend with residents being discharged morefrequently, causing our beds to turn over more often.

During the past year, we have made several improvements to our building to enhance ourresidents' lifestyle to accommodate the Eden facility principle. We have upgraded 20 of ourresident beds and have updated the older rooms in our building to provide a facelift for a morepleasant environment.

Contacting the Facility's Financial Management

This financial report is designed to provide our residents, suppliers, taxpayers, and creditorswith a general overview of the Facility's finances and to show the Facility's accountability for themoney it receives. If you have questions about this report or need additional financialinformation, contact the Facility’s business office at 140 West Mechanic Road, Hillsdale, MI49242.

7

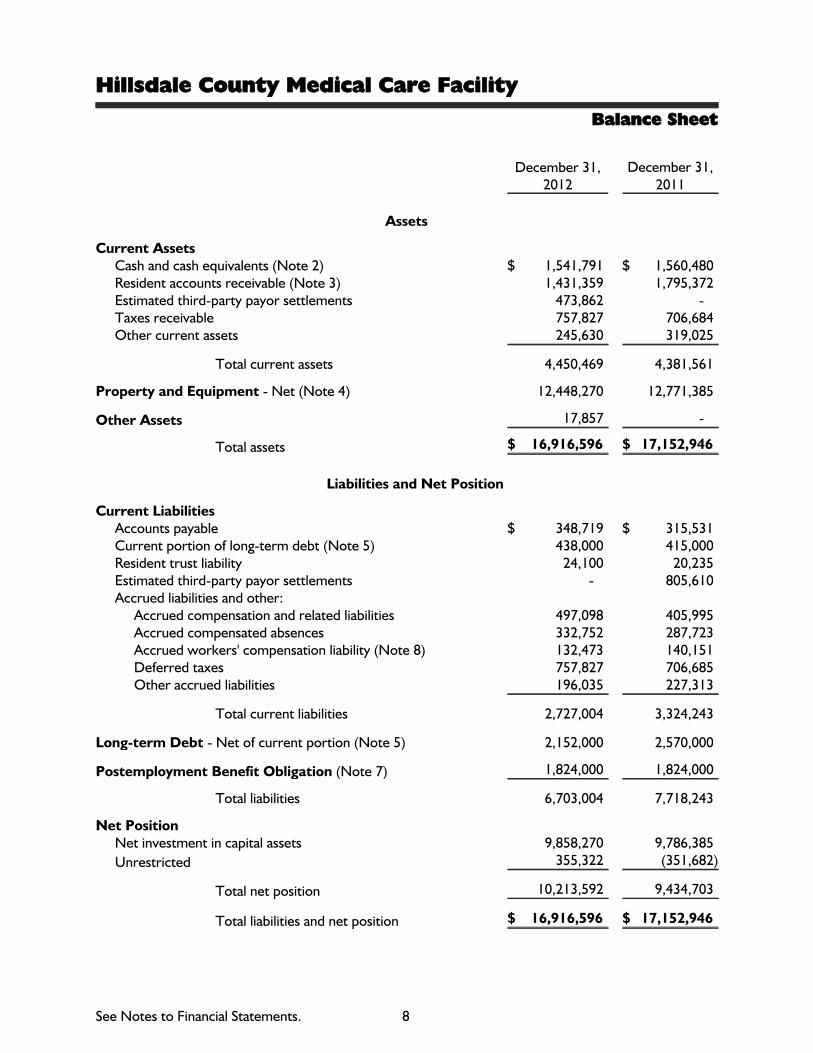

Hillsdale County Medical Care Facility

Balance Sheet

December 31,2012

December 31,2011

Assets

Current AssetsCash and cash equivalents (Note 2) $ 1,541,791 $ 1,560,480Resident accounts receivable (Note 3) 1,431,359 1,795,372Estimated third-party payor settlements 473,862 -Taxes receivable 757,827 706,684Other current assets 245,630 319,025

Total current assets 4,450,469 4,381,561

Property and Equipment - Net (Note 4) 12,448,270 12,771,385

Other Assets 17,857 -

Total assets $ 16,916,596 $ 17,152,946

Liabilities and Net Position

Current LiabilitiesAccounts payable $ 348,719 $ 315,531Current portion of long-term debt (Note 5) 438,000 415,000Resident trust liability 24,100 20,235Estimated third-party payor settlements - 805,610Accrued liabilities and other:

Accrued compensation and related liabilities 497,098 405,995Accrued compensated absences 332,752 287,723Accrued workers' compensation liability (Note 8) 132,473 140,151Deferred taxes 757,827 706,685Other accrued liabilities 196,035 227,313

Total current liabilities 2,727,004 3,324,243

Long-term Debt - Net of current portion (Note 5) 2,152,000 2,570,000

Postemployment Benefit Obligation (Note 7) 1,824,000 1,824,000

Total liabilities 6,703,004 7,718,243

Net PositionNet investment in capital assets 9,858,270 9,786,385

Unrestricted 355,322 (351,682)

Total net position 10,213,592 9,434,703

Total liabilities and net position $ 16,916,596 $ 17,152,946

See Notes to Financial Statements. 8

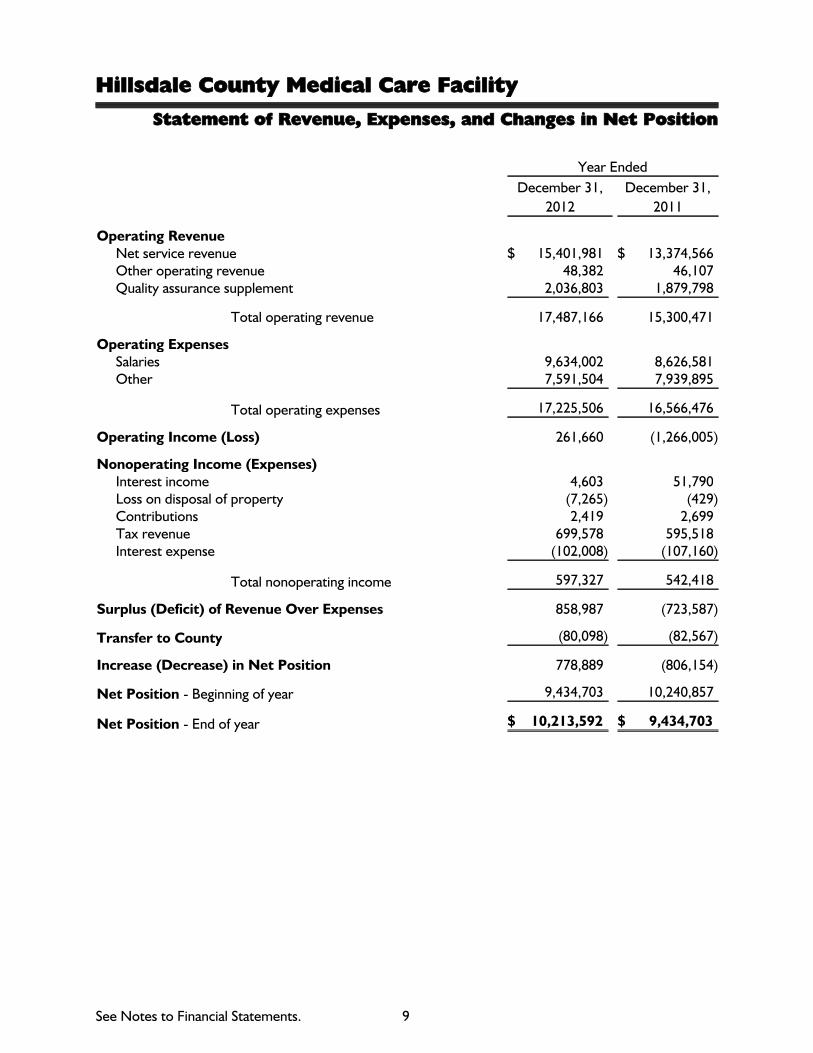

Hillsdale County Medical Care Facility

Statement of Revenue, Expenses, and Changes in Net Position

Year Ended

December 31,

2012

December 31,

2011

Operating RevenueNet service revenue $ 15,401,981 $ 13,374,566Other operating revenue 48,382 46,107Quality assurance supplement 2,036,803 1,879,798

Total operating revenue 17,487,166 15,300,471

Operating ExpensesSalaries 9,634,002 8,626,581Other 7,591,504 7,939,895

Total operating expenses 17,225,506 16,566,476

Operating Income (Loss) 261,660 (1,266,005)

Nonoperating Income (Expenses)Interest income 4,603 51,790Loss on disposal of property (7,265) (429)Contributions 2,419 2,699Tax revenue 699,578 595,518Interest expense (102,008) (107,160)

Total nonoperating income 597,327 542,418

Surplus (Deficit) of Revenue Over Expenses 858,987 (723,587)

Transfer to County (80,098) (82,567)

Increase (Decrease) in Net Position 778,889 (806,154)

Net Position - Beginning of year 9,434,703 10,240,857

Net Position - End of year $ 10,213,592 $ 9,434,703

See Notes to Financial Statements. 9

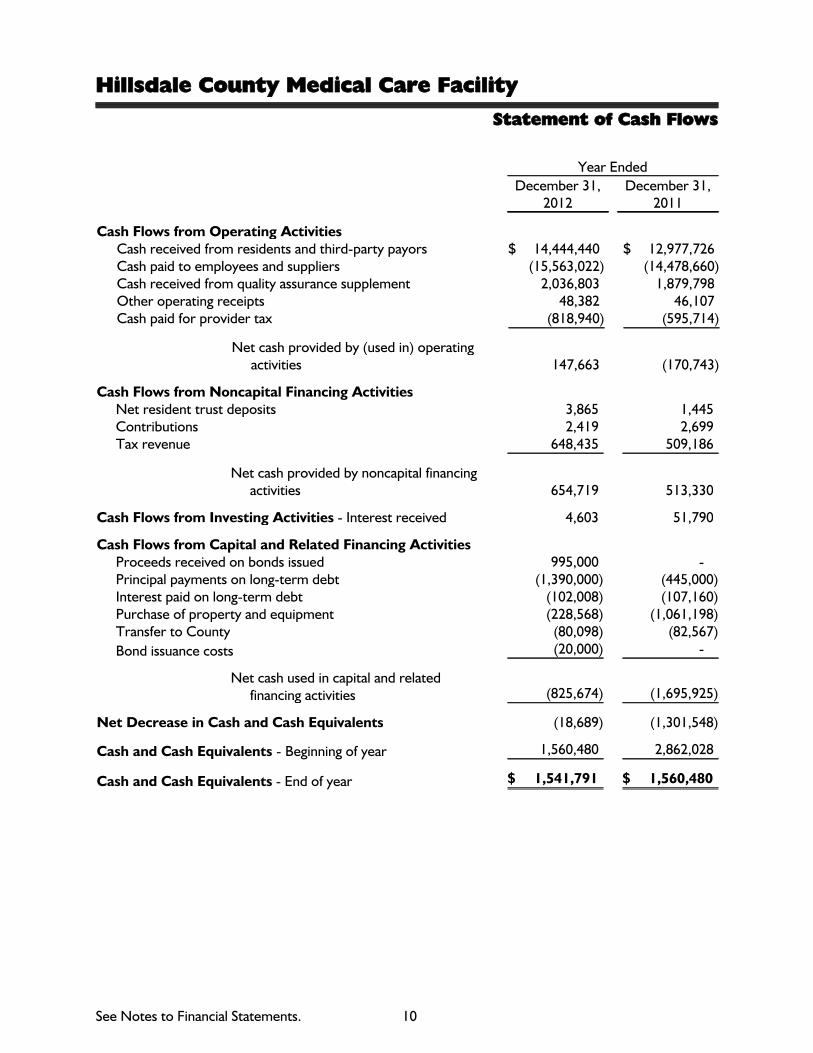

Hillsdale County Medical Care Facility

Statement of Cash Flows

Year Ended

December 31,2012

December 31,2011

Cash Flows from Operating ActivitiesCash received from residents and third-party payors $ 14,444,440 $ 12,977,726Cash paid to employees and suppliers (15,563,022) (14,478,660)Cash received from quality assurance supplement 2,036,803 1,879,798Other operating receipts 48,382 46,107Cash paid for provider tax (818,940) (595,714)

Net cash provided by (used in) operatingactivities 147,663 (170,743)

Cash Flows from Noncapital Financing ActivitiesNet resident trust deposits 3,865 1,445Contributions 2,419 2,699Tax revenue 648,435 509,186

Net cash provided by noncapital financingactivities 654,719 513,330

Cash Flows from Investing Activities - Interest received 4,603 51,790

Cash Flows from Capital and Related Financing ActivitiesProceeds received on bonds issued 995,000 -Principal payments on long-term debt (1,390,000) (445,000)Interest paid on long-term debt (102,008) (107,160)Purchase of property and equipment (228,568) (1,061,198)Transfer to County (80,098) (82,567)

Bond issuance costs (20,000) -

Net cash used in capital and relatedfinancing activities (825,674) (1,695,925)

Net Decrease in Cash and Cash Equivalents (18,689) (1,301,548)

Cash and Cash Equivalents - Beginning of year 1,560,480 2,862,028

Cash and Cash Equivalents - End of year $ 1,541,791 $ 1,560,480

See Notes to Financial Statements. 10

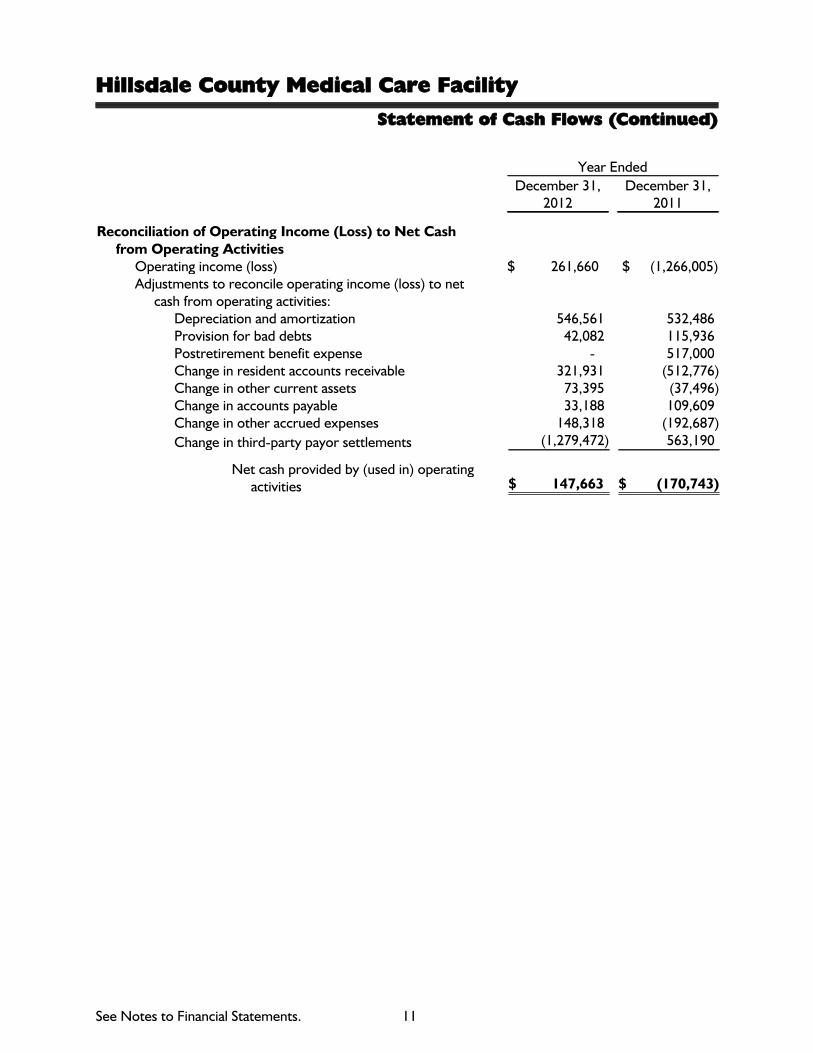

Hillsdale County Medical Care Facility

Statement of Cash Flows (Continued)

Year Ended

December 31,2012

December 31,2011

Reconciliation of Operating Income (Loss) to Net Cashfrom Operating Activities

Operating income (loss) $ 261,660 $ (1,266,005)Adjustments to reconcile operating income (loss) to net

cash from operating activities:Depreciation and amortization 546,561 532,486Provision for bad debts 42,082 115,936Postretirement benefit expense - 517,000Change in resident accounts receivable 321,931 (512,776)Change in other current assets 73,395 (37,496)Change in accounts payable 33,188 109,609Change in other accrued expenses 148,318 (192,687)

Change in third-party payor settlements (1,279,472) 563,190

Net cash provided by (used in) operatingactivities $ 147,663 $ (170,743)

See Notes to Financial Statements. 11

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 1 - Nature of Business and Significant Accounting Policies

Hillsdale County Medical Care Facility (the “Facility”) is a 170-bed, long-term carefacility owned and operated by Hillsdale County (the “County”). The Facility is acomponent unit of the County of Hillsdale. It is governed by the Hillsdale CountyDepartment of Human Services Board. This board consists of three members, two ofwhom are appointed by the County Board of Commissioners and one who is appointedby the Michigan governor. Further, the County Board of Commissioners approves theFacility’s revenue and expenses as a line item in the County's budget.

Basis for Presentation - The financial statements have been prepared in accordancewith accounting principles generally accepted in the United States of America asprescribed by the Governmental Accounting Standards Board (GASB) in StatementNo. 34, Basic Financial Statements - and Management’s Discussion and Analysis - for Stateand Local Governments, issued in June 1999. The Facility follows the “business-type”activities reporting requirements of GASB Statement No. 34, which provides acomprehensive look at the Facility’s financial activities.

Proprietary Fund Accounting - Because the Facility provides a service to citizens thatis financed by a user charge, the Facility utilizes the proprietary fund method ofaccounting whereby accounting revenue and expenses are recognized on the full accrualbasis.

Cash and Cash Equivalents - Cash and cash equivalents include certain investments inhighly liquid debt instruments with original maturities of three months or less.

Resident Accounts Receivable - Accounts receivable are recorded at stated amountsbased on a unit rate for services provided to individuals qualified to receive servicesfrom the Facility. An allowance for doubtful accounts is established based on a specificassessment of all receivables that remain unpaid following normal collection periods. Allamounts deemed to be uncollectible are charged against the allowance for doubtfulaccounts in the period that determination is made.

Property and Equipment - Property and equipment purchases are recorded at cost.Donated property and equipment are recorded at the estimated fair market value at thetime of donation. Depreciation is computed principally on the straight-line basis overthe estimated useful lives of the assets. Equipment under capital leases is amortized onthe straight-line method over the estimated useful life of the equipment. Suchamortization is included in depreciation and amortization in the financial statements.Interest cost incurred on borrowed funds during the period of construction of capitalassets is capitalized as a component of the cost of acquiring those assets. Costs ofmaintenance and repairs are charged to expense when incurred.

12

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

Gifts of long-lived assets such as land, buildings, or equipment are reported asunrestricted support and are excluded from deficiency of revenue over expenses, unlessexplicit donor stipulations specify how the donated assets must be used. Gifts of long-lived assets with explicit restrictions that specify how the assets are to be used and giftsof cash or other assets that must be used to acquire long-lived assets are reported asrestricted support. Absent explicit donor stipulations about how long those long-livedassets must be maintained, expirations of donor restrictions are reported when thedonated or acquired long-lived assets are placed in service.

Resident Trust Liability - The State Department of Treasury requires facilities toadminister and account for monies of residents. The resident trust liability on thebalance sheet represents resident trust fund deposits at December 31, 2012 and 2011.

Compensated Absences - Compensated absences are charged to operations whenearned. Unused benefits are recorded as a current liability in the financial statements.

Net Position - Net position of the Facility is classified in two components. Netposition of net investment of capital assets consists of capital assets net of accumulateddepreciation and reduced by the current balances of any outstanding borrowings usedto finance the purchase or construction of those assets. Unrestricted net position is theremaining net position that does not meet the definition of net investment of capitalassets or restricted net position.

Service Revenue - The Facility's principal activity is operating a long-term healthcarefacility for the elderly. Revenue is derived from participation in the Medicaid andMedicare programs, as well as from private-pay residents. Amounts earned under theMedicaid and Medicare programs are subject to review and audit by the third-partypayors and make up a significant portion of revenue earned during each year as follows:

2012 2011Percent of revenue:

Medicaid %79 %78Medicare %12 %15

The payment methodology related to these programs is based on cost and clinicalassessments that are subject to review and final approval by Medicaid and Medicare.Any adjustment that is a result of this final review and approval will be recorded in theperiod in which the adjustment is made. In the opinion of management, adequateprovision has been made for any adjustments that may result from such third-partyreview.

13

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

Services rendered to Medicare program beneficiaries are paid at prospectivelydetermined rates based upon clinical assessments completed by the Facility that aresubject to review and final approval by Medicare. Medicaid reimburses the Facility forroutine service costs, on a per diem basis, prospectively determined.

Laws and regulations governing the Medicare and Medicaid programs are complex andsubject to interpretation. Management believes it is in compliance with all applicablelaws and regulations and is not aware of any pending or threatened investigationsinvolving allegations of potential wrongdoings. While no such regulatory inquiries havebeen made, compliance with such laws and regulations can be subject to futuregovernment review and interpretation, as well as significant regulatory action includingfines, penalties, and exclusion from the Medicare and Medicaid programs.

The Medicare program has initiated a recovery audit contractor (RAC) initiative,whereby claims subsequent to October 1, 2007 will be reviewed by contractors forvalidity, accuracy, and proper documentation. A demonstration project completed inseveral other states resulted in the identification of potential significant overpayments.The RAC program began for Michigan in 2009. The Facility is unable to determine if itwill be audited and if so, the extent of liability for overpayments, if any. If selected foraudit, the potential exists for significant overpayment of claims liability for the Facility ata future date.

Quality Assurance Supplement - The Facility's Medicaid revenue has been partiallyfunded by a program called the quality assurance assessment program (QAAP). TheFacility receives additional payments based on the number of Medicaid days of careprovided and the cost of providing the care, subject to limits.

The Facility was assessed a provider tax. The State billed for the tax on a monthly basis.The provider tax is based on the number of non-Medicare days of service from the prioryear assessed data at a rate determined by the State. The rate is subject to change eachyear.

Certified Public Expenditures - In 2012, the State of Michigan received approval toallow county-owned facilities to receive reimbursement through the certified publicexpenditures program. The purpose of the program is to assure funding forunreimbursed costs incurred for services to Medicaid beneficiaries. The State approvalis retroactive to January 1, 2009. As of December 31, 2012, the Facility has estimatedapproximately $207,000 in reimbursements will be received under this program.

14

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

Property Taxes - Taxes are levied on December 1 and payable by February 15. Thecities and townships within the County bill and collect the property taxes for theCounty. Property taxes billed during the month of December will be used to financethe following year’s operations. As such, these taxes are recorded as deferred revenueat December 31. The Facility has had voter approval to levy up to $0.60 per $1,000 ofassessed valuation for the purpose of general operations of the Facility.

Maintenance of Effort - Maintenance of effort (MOE) is a County obligation to theState of Michigan. Every month, the County receives a bill from the State of Michiganfor each Medicaid resident day approved by the State during that month. MOE is beingpaid by the Facility and is recorded in operating expenses. MOE expense totaled$671,126 and $561,052 for the years ended December 31, 2012 and 2011, respectively.

Operating Revenue and Expenses - The Facility's statement of revenue, expenses,and changes in net position distinguishes between operating and nonoperating revenueand expenses. Operating revenue results from exchange transactions associated withproviding healthcare services - the Facility's principal activity. Nonoperating activity,including taxes, interest income, expenses, and donations, is reported as nonoperating.Operating expenses are all expenses incurred to provide healthcare services, other thanfinancing costs.

Use of Estimates - The preparation of financial statements in conformity withaccounting principles generally accepted in the United States of America requiresmanagement to make estimates and assumptions that affect the reported amounts ofassets and liabilities and disclosure of contingent assets and liabilities at the date of thefinancial statements and the reported amounts of revenue and expenses during thereporting period. Actual results could differ from those estimates.

New Accounting Pronouncements -The Facility has adopted GASB No. 62,Codification of Pre-November 30, 1989 FASB and AICPA Pronouncements, whichincorporates into GASB literature certain accounting and reporting guidance which isincluded in standards issued by the FASB, accounting principles board opinions, or theAICPA (via accounting research bulletins), which were issued before November 30,1989 and do not conflict with or contradict GASB pronouncements.

The Facility also adopted GASB No. 63, Financial Reporting of Deferred Outflows ofResources, Deferred Inflows of Resources, and Net Position, which changed some of theexisting terminology of the government-wide and proprietary fund balance sheets.

15

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 1 - Nature of Business and Significant Accounting Policies(Continued)

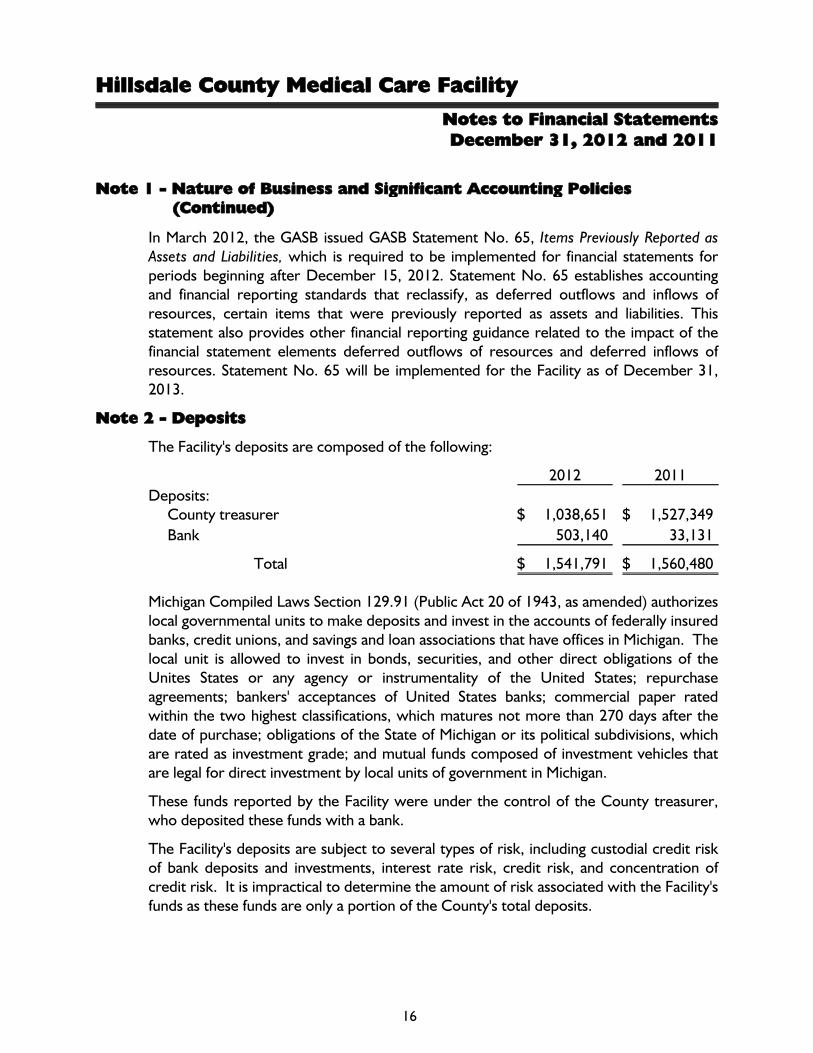

In March 2012, the GASB issued GASB Statement No. 65, Items Previously Reported asAssets and Liabilities, which is required to be implemented for financial statements forperiods beginning after December 15, 2012. Statement No. 65 establishes accountingand financial reporting standards that reclassify, as deferred outflows and inflows ofresources, certain items that were previously reported as assets and liabilities. Thisstatement also provides other financial reporting guidance related to the impact of thefinancial statement elements deferred outflows of resources and deferred inflows ofresources. Statement No. 65 will be implemented for the Facility as of December 31,2013.

Note 2 - Deposits

The Facility's deposits are composed of the following:

2012 2011

Deposits:County treasurer $ 1,038,651 $ 1,527,349

Bank 503,140 33,131

Total $ 1,541,791 $ 1,560,480

Michigan Compiled Laws Section 129.91 (Public Act 20 of 1943, as amended) authorizeslocal governmental units to make deposits and invest in the accounts of federally insuredbanks, credit unions, and savings and loan associations that have offices in Michigan. Thelocal unit is allowed to invest in bonds, securities, and other direct obligations of theUnites States or any agency or instrumentality of the United States; repurchaseagreements; bankers' acceptances of United States banks; commercial paper ratedwithin the two highest classifications, which matures not more than 270 days after thedate of purchase; obligations of the State of Michigan or its political subdivisions, whichare rated as investment grade; and mutual funds composed of investment vehicles thatare legal for direct investment by local units of government in Michigan.

These funds reported by the Facility were under the control of the County treasurer,who deposited these funds with a bank.

The Facility's deposits are subject to several types of risk, including custodial credit riskof bank deposits and investments, interest rate risk, credit risk, and concentration ofcredit risk. It is impractical to determine the amount of risk associated with the Facility'sfunds as these funds are only a portion of the County's total deposits.

16

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 2 - Deposits (Continued)

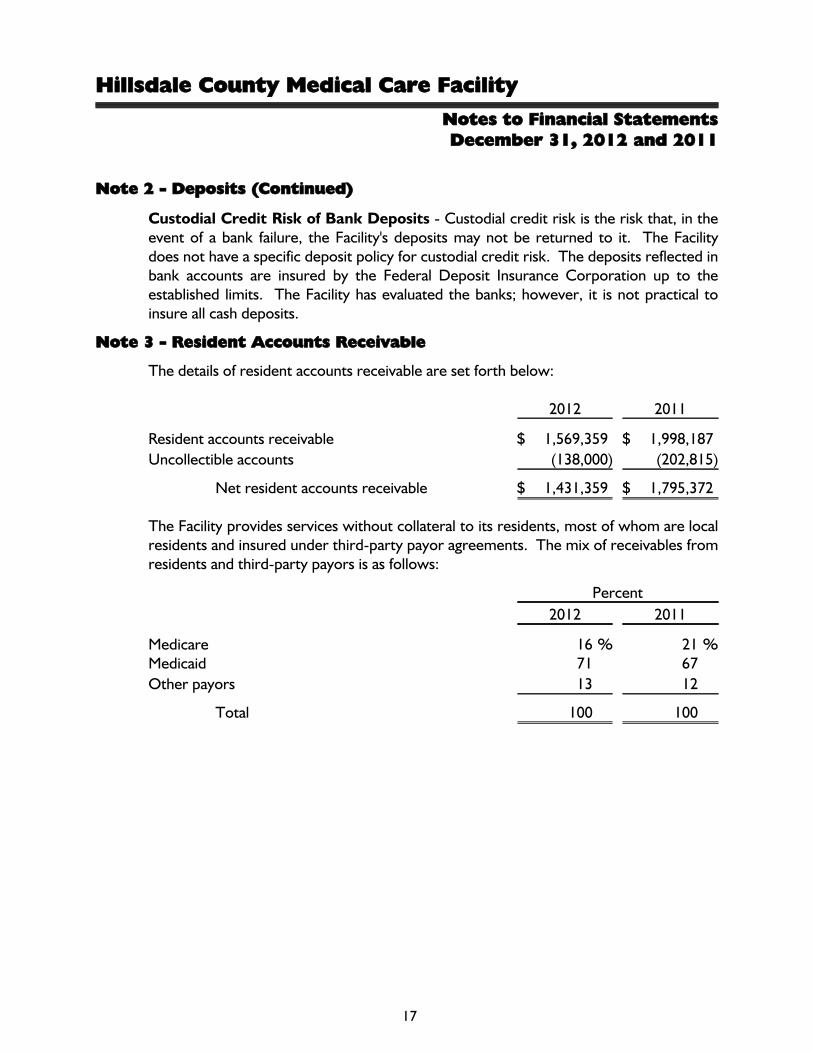

Custodial Credit Risk of Bank Deposits - Custodial credit risk is the risk that, in theevent of a bank failure, the Facility's deposits may not be returned to it. The Facilitydoes not have a specific deposit policy for custodial credit risk. The deposits reflected inbank accounts are insured by the Federal Deposit Insurance Corporation up to theestablished limits. The Facility has evaluated the banks; however, it is not practical toinsure all cash deposits.

Note 3 - Resident Accounts Receivable

The details of resident accounts receivable are set forth below:

2012 2011

Resident accounts receivable $ 1,569,359 $ 1,998,187

Uncollectible accounts (138,000) (202,815)

Net resident accounts receivable $ 1,431,359 $ 1,795,372

The Facility provides services without collateral to its residents, most of whom are localresidents and insured under third-party payor agreements. The mix of receivables fromresidents and third-party payors is as follows:

Percent

2012 2011

Medicare %16 %21Medicaid 71 67

Other payors 13 12

Total 100 100

17

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

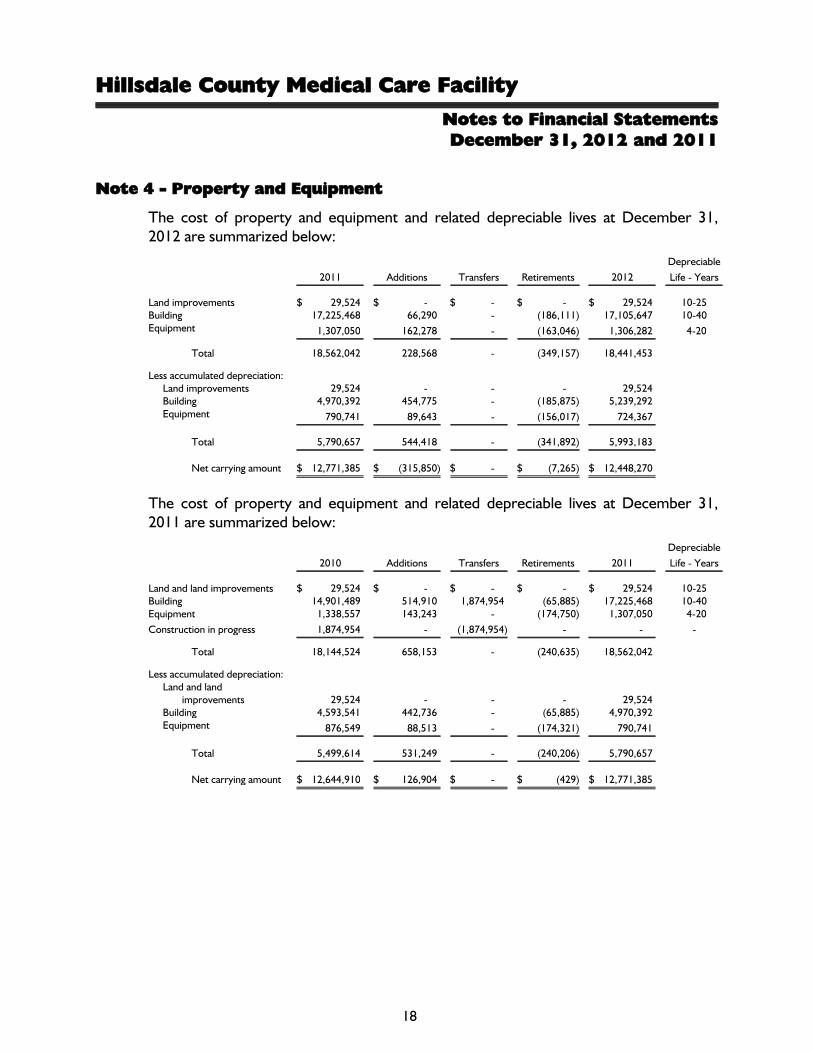

Note 4 - Property and Equipment

The cost of property and equipment and related depreciable lives at December 31,2012 are summarized below:

2011 Additions Transfers Retirements 2012

Depreciable

Life - Years

Land improvements $ 29,524 $ - $ - $ - $ 29,524 10-25Building 17,225,468 66,290 - (186,111) 17,105,647 10-40Equipment 1,307,050 162,278 - (163,046) 1,306,282 4-20

Total 18,562,042 228,568 - (349,157) 18,441,453

Less accumulated depreciation:Land improvements 29,524 - - - 29,524Building 4,970,392 454,775 - (185,875) 5,239,292Equipment 790,741 89,643 - (156,017) 724,367

Total 5,790,657 544,418 - (341,892) 5,993,183

Net carrying amount $ 12,771,385 $ (315,850) $ - $ (7,265) $ 12,448,270

The cost of property and equipment and related depreciable lives at December 31,2011 are summarized below:

2010 Additions Transfers Retirements 2011

Depreciable

Life - Years

Land and land improvements $ 29,524 $ - $ - $ - $ 29,524 10-25Building 14,901,489 514,910 1,874,954 (65,885) 17,225,468 10-40Equipment 1,338,557 143,243 - (174,750) 1,307,050 4-20

Construction in progress 1,874,954 - (1,874,954) - - -

Total 18,144,524 658,153 - (240,635) 18,562,042

Less accumulated depreciation:Land and land

improvements 29,524 - - - 29,524Building 4,593,541 442,736 - (65,885) 4,970,392Equipment 876,549 88,513 - (174,321) 790,741

Total 5,499,614 531,249 - (240,206) 5,790,657

Net carrying amount $ 12,644,910 $ 126,904 $ - $ (429) $ 12,771,385

18

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

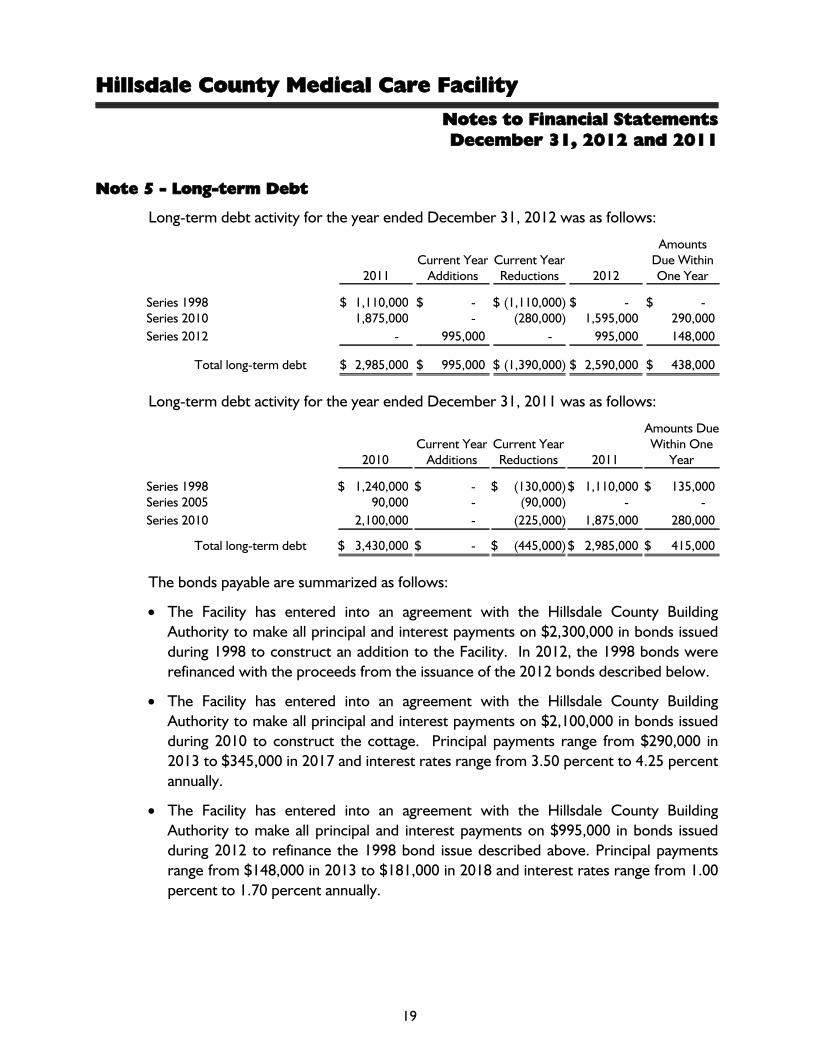

Note 5 - Long-term Debt

Long-term debt activity for the year ended December 31, 2012 was as follows:

2011Current Year

AdditionsCurrent YearReductions 2012

AmountsDue WithinOne Year

Series 1998 $ 1,110,000 $ - $ (1,110,000) $ - $ -Series 2010 1,875,000 - (280,000) 1,595,000 290,000

Series 2012 - 995,000 - 995,000 148,000

Total long-term debt $ 2,985,000 $ 995,000 $ (1,390,000) $ 2,590,000 $ 438,000

Long-term debt activity for the year ended December 31, 2011 was as follows:

2010Current Year

AdditionsCurrent YearReductions 2011

Amounts DueWithin One

Year

Series 1998 $ 1,240,000 $ - $ (130,000) $ 1,110,000 $ 135,000Series 2005 90,000 - (90,000) - -

Series 2010 2,100,000 - (225,000) 1,875,000 280,000

Total long-term debt $ 3,430,000 $ - $ (445,000) $ 2,985,000 $ 415,000

The bonds payable are summarized as follows:

The Facility has entered into an agreement with the Hillsdale County BuildingAuthority to make all principal and interest payments on $2,300,000 in bonds issuedduring 1998 to construct an addition to the Facility. In 2012, the 1998 bonds wererefinanced with the proceeds from the issuance of the 2012 bonds described below.

The Facility has entered into an agreement with the Hillsdale County BuildingAuthority to make all principal and interest payments on $2,100,000 in bonds issuedduring 2010 to construct the cottage. Principal payments range from $290,000 in2013 to $345,000 in 2017 and interest rates range from 3.50 percent to 4.25 percentannually.

The Facility has entered into an agreement with the Hillsdale County BuildingAuthority to make all principal and interest payments on $995,000 in bonds issuedduring 2012 to refinance the 1998 bond issue described above. Principal paymentsrange from $148,000 in 2013 to $181,000 in 2018 and interest rates range from 1.00percent to 1.70 percent annually.

19

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 5 - Long-term Debt (Continued)

The following is a schedule by year of bond principal and interest as of December 31,2012:

Years EndingDecember 31 Principal Interest

2013 $ 438,000 $ 79,7712014 463,000 66,4832015 486,000 51,7162016 503,000 35,8542017 519,000 19,132

2018 181,000 1,539

Total $ 2,590,000 $ 254,495

Note 6 - Pension Plan

As disclosed in Note 1, the Facility is a component unit of Hillsdale County. HillsdaleCounty, including the Facility, participates in the Hillsdale County Employees RetirementPlan, a defined contribution pension plan that covers all employees of the County. Theplan provides retirement and death benefits to plan members and their beneficiaries.This information can be requested by writing to the County of Hillsdale Courthouse,29 N. Howell, Hillsdale, Michigan 49242.

The obligation to contribute to and maintain the plan for these employees wasestablished by negotiations with the County's competitive bargaining units and requires acontribution from the employee of 2 percent. The Facility's contribution requirement is4 percent of employees' gross wages.

Facility contributions for the plan years ended December 31, 2012, 2011, and 2010were $358,191, $320,304, and $280,933, respectively.

Note 7 - Postretirement Benefits

Plan Description - The Facility participates in a defined benefit postretirement plansponsored by Hillsdale County that provides postretirement medical benefits toretirees. Prior to 2012, substantially all employees may become eligible for the benefitsif they reach normal retirement age while working at the Facility. In 2012, the Facilityfroze the plan to new beneficiaries and froze the accumulation proceeds. Thepostretirement obligation is expected to be paid from the Facility's General Fund.

Funding Policy - The Facility has no obligation to make contributions in advance ofwhen the premiums are due for payment (in other words, this may be financed on apay-as-you-go basis).

20

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

Note 7 - Postretirement Benefits (Continued)

Funding Progress - For the years ended December 31, 2012 and 2011, the Facility hasestimated the cost of providing retiree healthcare benefits through actuarial valuations asof December 31, 2012. The valuation computes an annual required contribution, whichrepresents a level of funding that, if paid on an ongoing basis, is projected to covernormal cost each year and amortize any unfunded actuarial liabilities over a period notto exceed 30 years. This valuation's computed contribution and actual funding aresummarized as follows for the years ended December 31, 2012, 2011, and 2010:

Facility Plan 2012 2011 2010

Other postemployment benefits(OPEB) cost $ 122,284 $ 711,756 $ 838,427

Amount contributed $ 105,819 $ 194,763 $ 168,613Net postretirement benefit obligation $ 1,824,000 $ 1,824,000 $ 1,307,000Percent contributed %86.53 %27.36 %20.11

Actuarial Methods and Assumptions - Actuarial valuations of an ongoing plan involveestimates of the value of reported amounts and assumptions about the probability ofoccurrence of events far into the future. Examples include assumptions about futureemployment, mortality, and the healthcare cost trends. Amounts determined regardingthe funded status of the plan and the annual required contributions of the employer aresubject to continual revision as actual results are compared with past expectations andnew estimates are made about the future.

Projections of benefits for financial reporting purposes are based on the substantive plan(the plan as understood by the employer and the plan members) and include the typesof benefits provided at the time of each valuation and the historical pattern of sharing ofbenefit costs between the employer and plan members to that point. The actuarialmethods and assumptions used include techniques that are designed to reduce theeffects of short-term volatility in actuarial accrued liabilities and the actuarial value ofassets, consistent with the long-term perspective of the calculations.

In the December 31, 2012 actuarial valuation (only required every other year), the entryage actuarial cost method was used. The actuarial assumptions included a 4 percentinvestment rate of return and a healthcare cost trend rate of 3 percent initially, reducedby decrements to an ultimate rate of 0 percent over three years. The unfunded actuarialaccrued liability (UAAL) is being amortized as a level percentage of projected payroll ona closed basis. The remaining amortization period at December 31, 2012 was 27 years.The table below is a summary of the UAAL:

Actuarial accrued liability (AAL) $ 2,662,056Unfunded actuarial accrued liability (UAAL) 2,662,056

21

Hillsdale County Medical Care Facility

Notes to Financial StatementsDecember 31, 2012 and 2011

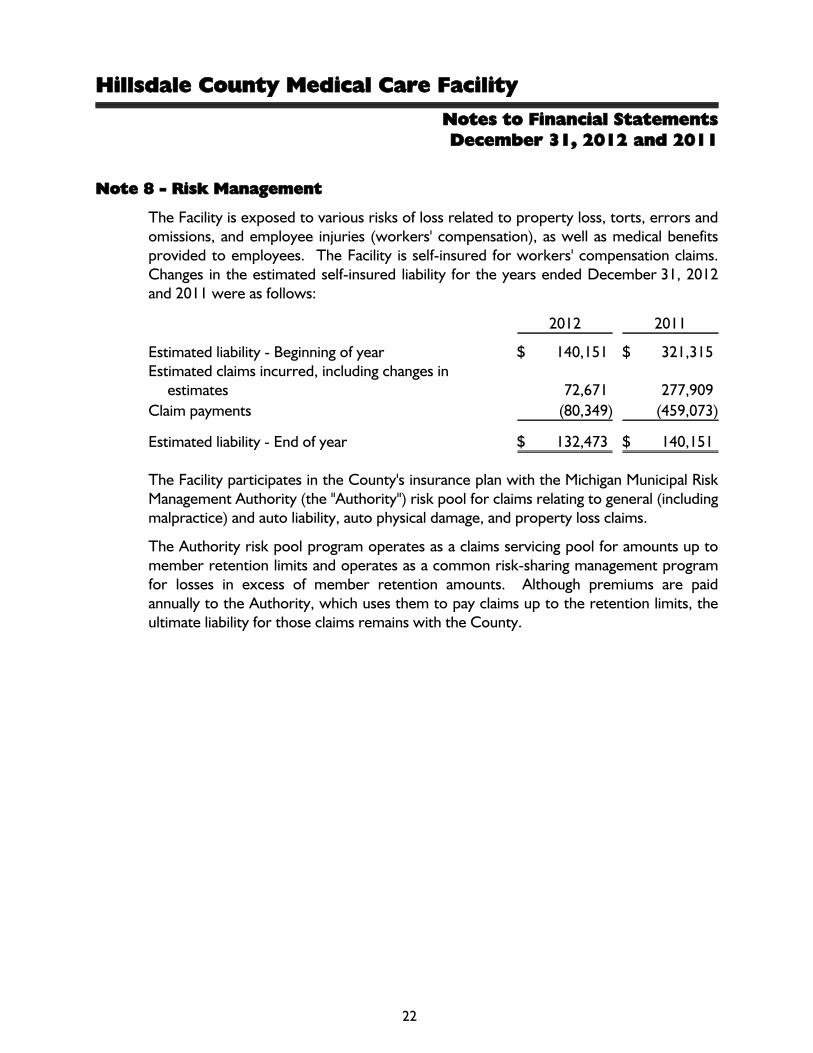

Note 8 - Risk Management

The Facility is exposed to various risks of loss related to property loss, torts, errors andomissions, and employee injuries (workers' compensation), as well as medical benefitsprovided to employees. The Facility is self-insured for workers' compensation claims.Changes in the estimated self-insured liability for the years ended December 31, 2012and 2011 were as follows:

2012 2011

Estimated liability - Beginning of year $ 140,151 $ 321,315Estimated claims incurred, including changes in

estimates 72,671 277,909

Claim payments (80,349) (459,073)

Estimated liability - End of year $ 132,473 $ 140,151

The Facility participates in the County's insurance plan with the Michigan Municipal RiskManagement Authority (the "Authority") risk pool for claims relating to general (includingmalpractice) and auto liability, auto physical damage, and property loss claims.

The Authority risk pool program operates as a claims servicing pool for amounts up tomember retention limits and operates as a common risk-sharing management programfor losses in excess of member retention amounts. Although premiums are paidannually to the Authority, which uses them to pay claims up to the retention limits, theultimate liability for those claims remains with the County.

22

Additional Information

23

Hillsdale County Medical Care Facility

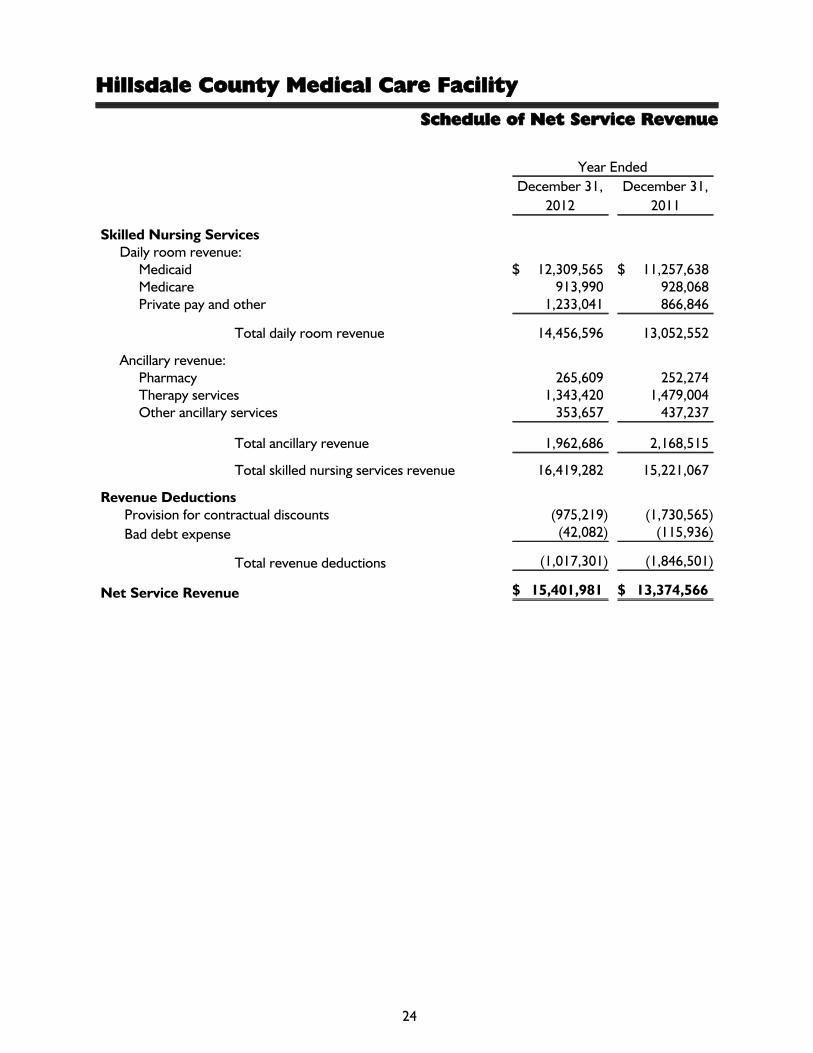

Schedule of Net Service Revenue

Year Ended

December 31,

2012

December 31,

2011

Skilled Nursing ServicesDaily room revenue:

Medicaid $ 12,309,565 $ 11,257,638Medicare 913,990 928,068Private pay and other 1,233,041 866,846

Total daily room revenue 14,456,596 13,052,552

Ancillary revenue:Pharmacy 265,609 252,274Therapy services 1,343,420 1,479,004Other ancillary services 353,657 437,237

Total ancillary revenue 1,962,686 2,168,515

Total skilled nursing services revenue 16,419,282 15,221,067

Revenue DeductionsProvision for contractual discounts (975,219) (1,730,565)

Bad debt expense (42,082) (115,936)

Total revenue deductions (1,017,301) (1,846,501)

Net Service Revenue $ 15,401,981 $ 13,374,566

24

Hillsdale County Medical Care Facility

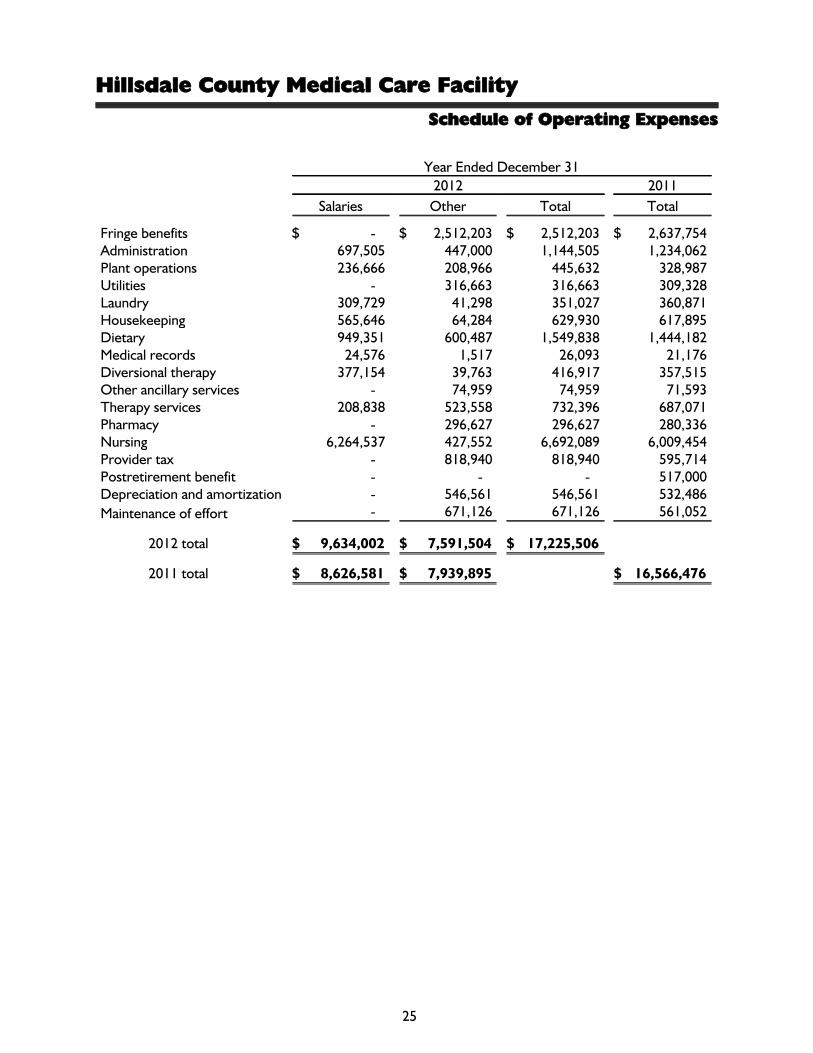

Schedule of Operating Expenses

Year Ended December 31

2012 2011

Salaries Other Total Total

Fringe benefits $ - $ 2,512,203 $ 2,512,203 $ 2,637,754Administration 697,505 447,000 1,144,505 1,234,062Plant operations 236,666 208,966 445,632 328,987Utilities - 316,663 316,663 309,328Laundry 309,729 41,298 351,027 360,871Housekeeping 565,646 64,284 629,930 617,895Dietary 949,351 600,487 1,549,838 1,444,182Medical records 24,576 1,517 26,093 21,176Diversional therapy 377,154 39,763 416,917 357,515Other ancillary services - 74,959 74,959 71,593Therapy services 208,838 523,558 732,396 687,071Pharmacy - 296,627 296,627 280,336Nursing 6,264,537 427,552 6,692,089 6,009,454Provider tax - 818,940 818,940 595,714Postretirement benefit - - - 517,000Depreciation and amortization - 546,561 546,561 532,486

Maintenance of effort - 671,126 671,126 561,052

2012 total $ 9,634,002 $ 7,591,504 $ 17,225,506

2011 total $ 8,626,581 $ 7,939,895 $ 16,566,476

25

1

May 15, 2013

To the Board Members of the

Department of Human Services

Hillsdale County Medical Care Facility

We have audited the financial statements of Hillsdale County Medical Care Facility (the

“Facility”) as of and for the year ended December 31, 2012 and have issued our report thereon

dated May 15, 2013. Professional standards require that we provide you with the following

information related to our audit which is divided into the following sections:

Section 1 - Internal Control Related Matters Identified in an Audit

Section II - Required Communications with Those Charged with Governance

Section III - Other Recommendations and Related Information

Section I includes any deficiencies we observed in the Facility’s accounting principles or internal

control that we believe are significant. Current auditing standards require us to formally

communicate annually matters we note about the Facility’s accounting policies and internal

control.

Section II includes information that current auditing standards require independent auditors to

communicate to those individuals charged with governance. We will report this information

annually to the board of directors of Hillsdale County Medical Care Facility.

Section III presents recommendations related to internal control, procedures, and other matters

noted during our current year audit. These comments are offered in the interest of helping the

Facility in its efforts toward continuous improvement, not just in the areas of internal control and

accounting procedures, but also in operational or administrative efficiency and effectiveness.

This report is intended solely for the use of the board of directors and management of Hillsdale

County Medical Care Facility and is not intended to be and should not be used by anyone other

than these specified parties.

We would like to take this opportunity to thank the Facility’s staff for the cooperation and

courtesy extended to us during our audit. We welcome any questions you may have regarding

the following communications and we would be willing to discuss any of these or other

questions that you might have at your convenience.

Very truly yours,

Plante & Moran, PLLC

J. Eric Conway, CPA, FHFMA

Partner

To the Board Members of the May 15, 2013

Department of Human Services

Hillsdale County Medical Care Facility

2

Section I - Communications Required Under AU 265

In planning and performing our audit of the financial statements of Hillsdale County Medical Care

Facility as of and for the year ended December 31, 2012, in accordance with auditing standards

generally accepted in the United States of America, we considered the Facility's internal control

over financial reporting (internal control) as a basis for designing audit procedures that are

appropriate in the circumstances for the purpose of expressing our opinion on the financial

statements, but not for the purpose of expressing an opinion on the effectiveness of the Facility's

internal control. Accordingly, we do not express an opinion on the effectiveness of the Facility's

internal control.

Our consideration of internal control was for the limited purpose described in the preceding

paragraph and was not designed to identify all deficiencies in internal control that might be

significant deficiencies or material weaknesses and therefore, material weaknesses or significant

deficiencies may exist that were not identified.

However, as discussed below, we identified a certain deficiency in internal control we consider

to be a material weakness and another deficiency we consider to be a significant deficiency.

A deficiency in internal control exists when the design or operation of a control does not allow

management or employees, in the normal course of performing their assigned functions, to

prevent or detect and correct misstatements on a timely basis.

A material weakness is a deficiency, or a combination of deficiencies, in internal control such that

there is a reasonable possibility that a material misstatement of the entity’s financial statements

will not be prevented or detected and corrected on a timely basis.

We consider the following deficiency in the Facility’s internal control to be a material weakness:

We noted Medicare charges billed by the Facility are not reconciled to gross revenue and

contractual allowance amounts recorded within the general ledger. While the net financial

statement impact is immaterial, the lack of reconciliation could result in material

misstatement of net service revenue. We recommend management implement a process to

reconcile amounts billed for services (as presented in billing summaries or similar reports) to

journal entries posted to the general ledger.

A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is

less severe than a material weakness, yet important enough to merit attention by those charged

with governance. We consider the following deficiency in the Facility’s internal control to be a

significant deficiency:

During the audit, two invoices were identified that were improperly excluded from the

accounts payable listing and the accounts payable accrual at December 31, 2012. The

implementation of a formal review process for invoices received after period end to

determine which period the services and goods were provided will prevent invoices from

being recorded in the incorrect fiscal year. We recommend management implement a

review process for monitoring invoices received after year end.

To the Board Members of the May 15, 2013

Department of Human Services

Hillsdale County Medical Care Facility

3

Section II - Communications Required Under AU 260

Our Responsibility Under U.S. Generally Accepted Auditing Standards

As stated in our engagement letter dated January 4, 2013, our responsibility, as described by

professional standards, is to express an opinion about whether the financial statements prepared

by management with your oversight are fairly presented, in all material respects, in conformity

with U.S. generally accepted accounting principles. Our audit of the financial statements does

not relieve you or management of your responsibilities. Our responsibility is to plan and

perform the audit to obtain reasonable, but not absolute, assurance that the financial statements

are free of material misstatement.

As part of our audit, we considered the internal control of Hillsdale County Medical Care

Facility. Such considerations were solely for the purpose of determining our audit procedures

and not to provide any assurance concerning such internal control.

We are responsible for communicating significant matters related to the audit that are, in our

professional judgment, relevant to your responsibilities in overseeing the financial reporting

process. However, we are not required to design procedures specifically to identify such

matters.

Planned Scope and Timing of the Audit

We performed the audit according to the planned scope and timing previously communicated to

you in our meeting about planning matters on January 4, 2013.

Significant Audit Findings

Qualitative Aspects of Accounting Practices

Management is responsible for the selection and use of appropriate accounting policies. In

accordance with the terms of our engagement letter, we will advise management about the

appropriateness of accounting policies and their application. The significant accounting policies

used by Hillsdale County Medical Care Facility are described in Note 1 to the financial

statements.

No new accounting policies were adopted and the application of existing policies was not

changed during 2012.

We noted no transactions entered into by the Facility during the year for which there is a lack of

authoritative guidance or consensus.

There are no significant transactions that have been recognized in the financial statements in a

different period than when the transaction occurred.

To the Board Members of the May 15, 2013

Department of Human Services

Hillsdale County Medical Care Facility

4

Accounting estimates are an integral part of the financial statements prepared by management

and are based on management’s knowledge and experience about past and current events and

assumptions about future events. Certain accounting estimates are particularly sensitive because

of their significance to the financial statements and because of the possibility that future events

affecting them may differ significantly from those expected. The most sensitive estimates

affecting the financial statements were the allowance for doubtful accounts, the estimate of

quality assurance supplement revenue, the estimate for certified public expenditures (CPE), and

the calculation of other postretirement benefit (OPEB) liability.

Management’s estimate of the allowance for doubtful accounts is based on historical collectibility

factors and review of individual balances outstanding as of December 31, 2012.

Management’s estimate of the quality assurance supplement revenue (approximately $2 million

for the year ended December 31, 2012) is based on the number of Medicaid days of service and

the respective rates for the year ended December 31, 2012.

Management’s estimate of the CPE receivable is based on the Medicaid census days from the

filed 2011 and 2010 Medicaid cost reports, and from the variable and plant cost rates on the

approved 2012, 2010, and 2009 Medicaid rate letters.

Management’s estimate of the OPEB liability (approximately $1.8 million as of December 31,

2012) is based on several factors, including retirement age for active employees, marital status,

life expectancy, turnover rates, healthcare cost trend rates, and healthcare premium rates.

We evaluated the inputs used to determine these estimates and determined that they are

reasonable in relation to the financial statements as a whole.

The disclosures in the financial statements are neutral, consistent, and clear.

Difficulties Encountered in Performing the Audit

We encountered no significant difficulties in dealing with management in performing and

completing our audit.

Disagreements with Management

For the purpose of this letter, professional standards define a disagreement with management as

a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction,

that could be significant to the financial statements or the auditor’s report. We are pleased to

report that no such disagreements arose during the course of our audit.

Corrected and Uncorrected Misstatements

Professional standards require us to accumulate all known and likely misstatements identified

during the audit, other than those that are trivial, and communicate them to the appropriate

level of management.

To the Board Members of the May 15, 2013

Department of Human Services

Hillsdale County Medical Care Facility

5

The attached schedule summarizes uncorrected misstatements of the financial statements which

were requested to be recorded. Management has determined their effects are immaterial, both

individually and in the aggregate, to the financial statements taken as a whole. In addition, none

of the misstatements detected as a result of audit procedures and corrected by management

were material, either individually or in the aggregate, to the financial statements taken as a

whole.

Significant Findings or Issues

We generally discuss a variety of matters, including the application of accounting principles and

auditing standards, business conditions affecting the Facility, and business plans and strategies

that may affect the risks of material misstatement with management each year prior to retention

as the Facility’s auditors. However, these discussions occurred in the normal course of our

professional relationship and our responses were not a condition of our retention.

Management Representations

We have requested certain representations from management that are included in the

management representation letter dated May 15, 2013.

Management Consultations with Other Independent Accountants

In some cases, management may decide to consult with other accountants about auditing and

accounting matters, similar to obtaining a “second opinion” on certain situations. If a consultation

involves application of an accounting principle to the Facility’s financial statements or a

determination of the type of auditor’s opinion that may be expressed on those statements, our

professional standards require the consulting accountant to check with us to determine that the

consultant has all the relevant facts. To our knowledge, there were no such consultations with

other accountants.

To the Board Members of the May 15, 2013

Department of Human Services

Hillsdale County Medical Care Facility

6

Section III - Other Recommendations and Related Information

During our audit, we noted areas where we believe there are opportunities for the Facility to

further strengthen internal control or to increase operating efficiencies. Our observations on

those areas are presented for your consideration below:

Provider Tax - We noted the Facility had approximately 51,000 Medicaid days in 2012, which

reaching would result in a lower provider tax rate on a per non-Medicare day basis. Maintaining

Medicaid census days over this threshold on a consistent basis could result in significant expense

reductions and increased cash flow. We recommend management explore strategies for

maintaining Medicaid census above this threshold consistently in future years. While adding

another 10 beds might help, it is uncertain how long the benefit of a reduced provider tax would

be available.

Postemployment Health Benefits - At this time, one of the other county-owned medical care

facilities is appealing a recent Medicaid audit adjustment to disallow contributions to a trust fund

for postemployment benefits. It is unclear whether these costs will ultimately be reimbursable.

However, Medicaid auditors will tend to disallow the costs if there is a question of whether they

are allowable. Therefore, it may be in the best interest of Hillsdale County Medical Care Facility

to restate the plan or terminate it entirely and replace it with some other benefit that would be

expected to the allowable under the Patient Protection and Affordable Care Act.

Healthcare Reform - Recent changes in healthcare legislation could have a dramatic effect on

employers with respect to the healthcare coverage options offered to employees.

Consideration of these changes and the anticipated effects on the Facility should be made well

ahead of the January 1, 2014 effective date. Additionally, beginning on January 1, 2018, there

will be limits imposed on costs to provide health benefits to employees. It will be important to

monitor costs prior to implementation of these limits to avoid any "excise tax" or

nonreimbursable expense.

FIDS Rate - Currently, the FIDS add-on paid to the Facility’s Medicaid rate is insignificant when

compared to the Facility’s normal Medicaid rate. This could result in significant cash flow issues

as reimbursements paid to the County related to renovation project costs are not fully covered

by the FIDS add-on. We recommend reviewing existing reimbursement agreements with the

County to consider changes to more closely align with additional Medicaid funds received under

the FIDS program.

Information Technology - During our audit procedures, we performed a review of the

information technology (IT) system and noted the following recommendations:

Currently, no formal documentation is kept to track user access additions or deletions from

the system. Also, user access reviews are not performed regularly. We recommend forms be

used to track access changes and user access reviews be performed at least annually.

Firewall logs are not reviewed regularly. We recommend the firewall logs be reviewed on a

regular basis.

To the Board Members of the May 15, 2013

Department of Human Services

Hillsdale County Medical Care Facility

7

Attachment

Client: Hillsdale County Medical Care Facility

Y/E: 12/31/2012

Ref. # Description of Misstatement Current Assets

Long-term

Assets

Current

Liabilities

Long-term

Liabilities Equity Revenue Expenses

Net Income

Impact

KNOWN MISSTATEMENTS:

A1 None

ESTIMATE ADJUSTMENTS:

B2 Allowance adjustment (19,000)$ 19,000$ (19,000)$

IMPLIED ADJUSTMENTS:

C1 None

- -$ -$ -$ -$ -$ - -

Total (19,000)$ -$ -$ -$ -$ -$ 19,000$ (19,000)$

PASSED DISCLOSURES:

D1 None

The pretax effect of misstatements and classification errors identified would be to increase (decrease) the reported

amounts in the financial statement categories identified below:

SUMMARY OF UNRECORDED POSSIBLE ADJUSTMENTS