home credit and finance bank · home credit and finance bank consolidated financial statements ......

TRANSCRIPT

Home Credit and Finance Bank

Consolidated Financial Statementsfor the year ended 31 December 2006

Home Credit and Finance BankConsolidated Financial Statements

for the year ended 31 December 2006

3

4

5

6

7

Consolidated Statement of Cash Flows

Notes to the Consolidated Financial Statements

Contents

Independent Auditors' Report

Consolidated Income Statement

Consolidated Balance Sheet

- 2 -

ZAO KPMG, a company incorporated under the Laws of the Russian Federation, is a member firm of KPMG International, a Swiss cooperative.

Report on the Consolidated Financial Statements

ZAO KPMG 27 February 2006

Management’s Responsibility for the Financial Statements

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financialstatements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity’s preparation and fair presentation of the financial statements in orderto design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinionon the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accountingprinciples used and the reasonableness of accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

In our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financialposition of the Group as at 31 December 2006, and its consolidated financial performance and its consolidated cashflows for the year then ended in accordance with International Financial Reporting Standards.

Opinion

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. Weconducted our audit in accordance with International Standards on Auditing. Those standards require that we complywith relevant ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financialstatements are free of material misstatement.

+7 (495) 937 4477 +7 (495) 937 4400/99 www.kpmg.ru

ZAO KPMG 11 Gogolevsky Boulevard Moscow 119019 Russia

Telephone Fax Internet

Independent Auditors' Report

To the Council of OOO Home Credit and Finance Bank

We have audited the accompanying consolidated financial statements of OOO “Home Credit & Finance Bank” and itssubsidiaries (the “Group”), which comprise the consolidated balance sheet as at 31 December 2006, the consolidatedincome statement and consolidated statement of cash flows for the year then ended, and a summary of significantaccounting policies and other explanatory notes.

Management is responsible for the preparation and fair presentation of these consolidated financial statements inaccordance with International Financial Reporting Standards. This responsibility includes: designing, implementingand maintaining internal control relevant to the preparation and fair presentation of financial statements that are freefrom material misstatements, whether due to fraud or error; selecting and applying appropriate accounting policies; andmaking accounting estimates that are reasonable in the circumstances.

Auditors’ Responsibility

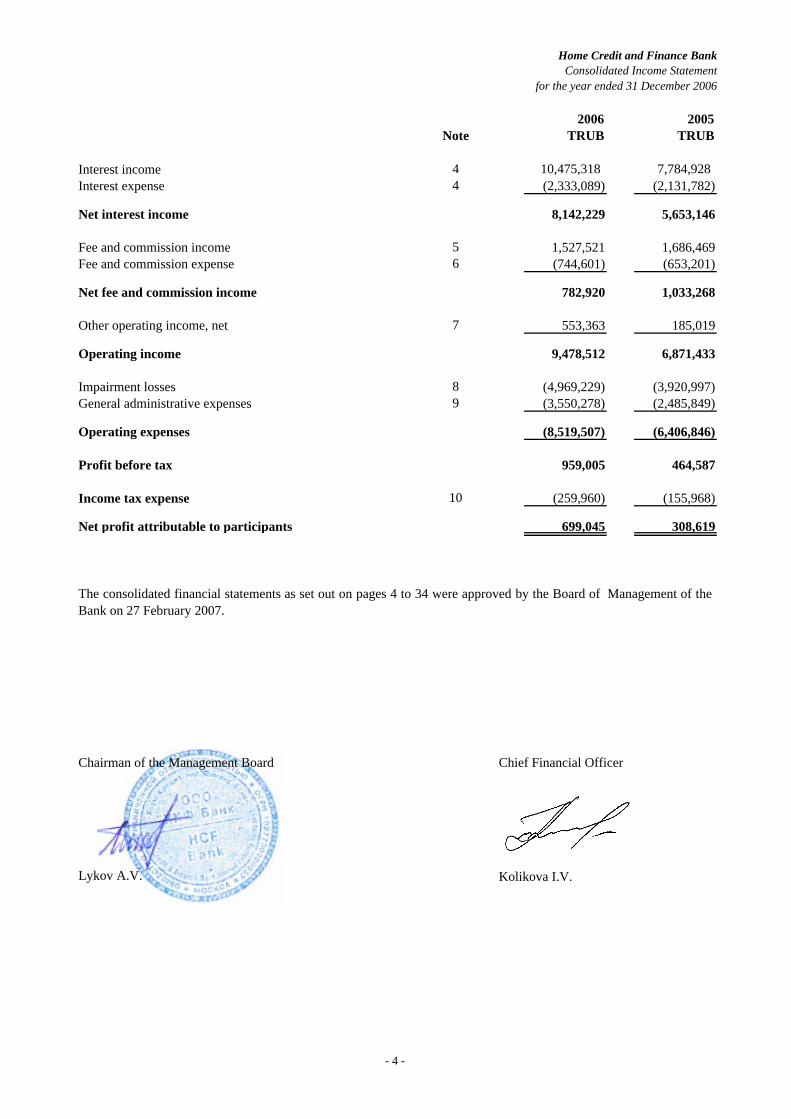

Home Credit and Finance BankConsolidated Income Statement

for the year ended 31 December 2006

Note

44

56

7

89

10

2006 2005TRUB TRUB

10,475,318 7,784,928(2,333,089) (2,131,782)

8,142,229 5,653,146

1,527,521 1,686,469 (744,601) (653,201)

782,920 1,033,268

553,363 185,019

9,478,512 6,871,433

(4,969,229) (3,920,997) (3,550,278) (2,485,849)

(8,519,507) (6,406,846)

959,005 464,587

The consolidated financial statements as set out on pages 4 to 34 were approved by the Board of Management of theBank on 27 February 2007.

(259,960) (155,968)

699,045 308,619

Income tax expense

Impairment lossesGeneral administrative expenses

Operating expenses

Profit before tax

Net profit attributable to participants

Fee and commission expense

Net fee and commission income

Other operating income, net

Operating income

Fee and commission income

Interest incomeInterest expense

Net interest income

Chairman of the Management Board Chief Financial Officer

Kolikova I.V.Lykov A.V.

- 4 -

Home Credit and Finance BankConsolidated Balance Sheet

for the year ended 31 December 2006

Note

1112131415

21

16

1718192021

22

23

TRUB TRUB2006 2005

5,699,391 9,466,2031,055,806 163,675

4,390,821 790,004

31,780,630 25,631,9161,041,509 1,888,075

1,855 6,553423,880 -

963,045 1,407,644

45,386,446 39,354,070

(24,318,770) (22,224,670)(6,803,288) (5,015,032)(3,170,607) (3,055,366)

(169,817) (38,695)

(325,938)

9,962,116 8,556,721

- (118,909)(539,881) (18,739)Current income tax payable

Other liabilities

Net assets attributable to participants

(421,967)

Property, equipment and intangible assetsInvestment in associateDeferred tax asset

Financial liabilities at fair value through profit or loss

Current income tax receivable

Cash and cash equivalents

Loans to customersFinancial assets at fair value through profit or loss

ASSETS

Placements with banks and other financial institutions

29,509 -Other assets

Total assets

LIABILITIES

Debt securities issuedDue to banks and other financial institutionsCurrent accounts and deposits from customers

Deferred tax liability

- 5 -

Home Credit and Finance BankConsolidated Statement of Cash Flowsfor the year ended 31 December 2006

Note

8

9

Increase/(decrease) in deposits from banks and other financial institutions

23

11

11

TRUB TRUB2006 2005

464,587

4,969,229 3,920,997

Net accrued general administrative expenses 160,106 (60,064)

(85,616)

182,788 108,079

223,291 (826,514)(134,906) (77,307)

(91,215)

1,602

24,005

3,472,701

(10,342,848)(868,482) 383,730

Net operating cash flow before changes in working capital

Increase in loans to customers (11,062,141)(Increase)/decrease in placements with banks and other financial institutions

5,408,924

698,728 (1,657,514)392,516 (1,271,251)

(484,012)

4,133

-

1,076,982

(3,789,603) (574,851)

(311,113) (38,502)

2,010,279

5,479,899

(5,000)

(1,896,712)

1,968

9,466,203

5,479,899

3,005,304

Cash flows from investing activities

Proceeds from the issue of charter capital and other capital contributions

5,699,391

706,350

(3,563,132)

(3,785,470)

706,350

Cash and cash equivalents at 31 December

(Decrease)/increase in other liabilities

Cash flows from operations

Income taxes paid

Cash flows from operating activities

Investing activitiesProceeds from sale of property and equipmentAcquisition of property, equipment and intangible assets

Financing activities

Cash flows from financing activities

Decrease/(increase) in financial assets at fair value through profit or lossDecrease/(increase) in other assets

Increase in debt securities issuedIncrease in current accounts and deposits from customers

Net accrued interest expense/(income) Net accrued fee income

(Gain)/loss on revaluation of financial assets at fair value through profit or loss

Loss on disposal of financial assets at fair value through profit or loss

Operating activitiesProfit before taxAdjustments for:

1,865

Depreciation and amortisation Net loss on disposal of property, equipment and intangible assets

(857,115)

959,005

Impairment losses Net unrealised foreign exchange gain

2,932(4,124)

(203,680) 75,650

20,685,05595,344

(14,300,409)

3,162,479(35,700)

120,498

Foreign exchange effect on cash and cash equivalents

(172,899) (1,858,210)

9,466,203

Net (decrease)/increase in cash and cash equivalents

Cash and cash equivalents at 1 January

(577,883)

Acquisition of investment in associate

6,385,249

- 6 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

Registered office

Participants Country of incorporation

The Netherlands-

The ultimate controlling entity is PPF Group N.V. registered in the Netherlands.

Consolidated subsidiaries Country of incorporation

Associates Country of incorporation

Global Credit Payment Services (LLC) Russian Federation

Board of Management

100.00

100.00100.00

Eurasia Capital S.A.Eurasia Structured Finance No.1 S.A.

Ownership interest (%)2006 2005

100.00100.00

Financial Innovations (LLC) Russian FederationGlobal Credit Bureau (LLC)

Luxemburg

0.01

Luxemburg

Eurasia Capital S.A. and Eurasia Structured Finance No.1 S.A. are special purpose entities established tofacilitate the Group’s issues of debt securities (refer to Note 17).

see belowsee below

Dolezel IgorKolikova Irina Member

The principal activity of the Bank and its subsidiaries (together referred to as the “Group”) is the provision ofconsumer financing to private individual customers in the Russian Federation. The activities of the Group areregulated by the Central Bank of the Russian Federation (“the CBR”).

Principal activities

Deputy ChairmanDeputy ChairmanChvatal Ladislav Member Mosolov Dmitri

ChairmanDeputy Chairman First Deputy Chairman

Council

Smejc Jiri ChairmanStanek Stanislav Soukup Vaclav

Lykov Andrei

Member Stanek Stanislav

Liko-Technopolis (LLC) Russian Federation Russian FederationInfobos (LLC)

1. Description of the Group

317A ZelenogradMoscow 124482Russian Federation

Home Credit and Finance Bank (the “Bank”) was established in the Russian Federation as a Limited LiabilityCompany and was granted its general banking license in 1990.

2006

Chvatal LadislavHome Credit B.V.

Ownership interest (%)2005

99.990.01

99.99

100.00100.00 Russian Federation

50.0050.00

2005Ownership interest (%)

2006

100.00see belowsee below

- 7 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(a)

(b)

(c)

(d)

(i)

(ii)

(iii)

Associates are those enterprises in which the Group has significant influence, but not control, over the financialand operating policies. The consolidated financial statements include the Group’s share of the total recognisedgains and losses of associates on an equity accounted basis, from the date that significant influence effectivelycommences until the date that significant influence effectively ceases. When the Group’s share of lossesexceeds the Group’s interest in the associate, that interest is reduced to nil and recognition of further losses isdiscontinued except to the extent that the Group has incurred obligations in respect of the associate.

2. Basis of preparation

Statement of compliance

Basis of measurement

Basis of consolidation

The national currency of the Russian Federation is the Russian Rouble (“RUB”). Management have determinedthe Group’s functional currency to be the RUB as it reflects the economic substance of the underlying eventsand circumstances of the Group. The RUB is also the Group’s presentation currency for the purposes of thesefinancial statements. Financial information presented in RUB has been rounded to the nearest thousand.

The consolidated financial statements have been prepared in accordance with International Financial ReportingStandards (IFRS), including International Accounting Standards (IAS), promulgated by the InternationalAccounting Standards Board (IASB) and interpretations issued by the International Financial ReportingInterpretations Committee (IFRIC) of the IASB.

The consolidated financial statements for the year ended 31 December 2006 comprise the Bank and itssubsidiaries.

The consolidated financial statements are prepared on the historical cost or amortised historical cost basisexcept that financial instruments at fair value through profit or loss and available-for-sale assets are stated atfair value. Other financial assets and liabilities are stated at amortised cost. Non-financial assets and liabilitiesare stated at historical cost, restated for the effects of inflation as described in Note 3(b).

Subsidiaries

Presentation and functional currency

Associates

Subsidiaries are those enterprises controlled by the Group. Control exists when the Group has the power,directly or indirectly, to govern the financial and operating policies of an enterprise so as to obtain benefitsfrom its activities. The financial statements of subsidiaries are included in the consolidated financial statementsfrom the date that control effectively commences until the date that control effectively ceases.

Special purpose entities

The Group has established a number of special purpose entities (SPEs) for the purposes of raising finance. TheGroup does not have any direct or indirect shareholdings in these entities. These SPEs are controlled by theGroup through the predetermination of the activities of SPEs, having rights to obtain the majority of benefits ofthe SPEs, and retaining the majority of the residual risks related to the SPEs.

- 8 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(iv)

(e)

(a)

2. Basis of preparation (continued)

Use of estimates and judgments

Management has made a number of estimates and assumptions relating to the reporting of assets and liabilitiesand the disclosure of contingent assets and liabilities to prepare these consolidated financial statements. Actualresults could differ from those estimates. In particular, information about significant areas of estimation,uncertainty and critical judgments made by management in preparing these consolidated financial statements inrespect of impairment recognition for financial assets is described in Note 3(h) and Notes 13 and 28.

3. Significant accounting policies

Foreign currency transactions

Transactions in foreign currencies are translated to Roubles at the foreign exchange rate ruling at the date of thetransaction. Monetary assets and liabilities denominated in foreign currencies at the balance sheet date aretranslated to roubles at the foreign exchange rate ruling at that date. Foreign exchange differences arising ontranslation are recognised in the income statement. Non-monetary assets and liabilities denominated in foreigncurrencies, which are stated at historical cost, are translated to roubles at the foreign exchange rate ruling at thedate of the transaction.

Transactions eliminated on consolidation

As at 1 January 2006, the Group adopted the amendment to International Financial Reporting Standard IAS 39“Financial Instruments: Recognition and Measurement” – “The Fair Value Option” . Upon application of thisamendment, the Group may designate a financial instrument as at fair value through profit or loss only if certainconditions are met. Financial instruments which were designated as at fair value through profit or loss as at 31December 2005 complied with the requirements of the amendment and were retained within this category uponits application.

Application of the above amendments required the comparative figures for the year 2005 to be restated but didnot have an impact on the figures shown in the financial statements of the Group as of 31 December 2005.

Intra-group balances and transactions, and any unrealised gains arising from intra-group transactions, areeliminated in preparing the consolidated financial statements. Unrealised gains arising from transactions withassociates are eliminated to the extent of the Group’s interest in the enterprise. Unrealised gains arising fromtransactions with associates are eliminated against the investment in the associate. Unrealised losses areeliminated in the same way as unrealised gains, but only to the extent that there is no evidence of impairment.

The following significant accounting policies have been applied in the preparation of the consolidated financialstatements. The accounting policies have been consistently applied. Changes in accounting policy due tochanges in the IFRS are discussed in the following paragraphs.

As at 1 January 2006, the Group adopted the amendment to International Financial Reporting Standard IAS 39“Financial Instruments: Recognition and Measurement” and IFRS 4 “Insurance Contracts” – “FinancialGuarantee Contracts” . Upon application of this amendment, a financial guarantee issued is recognised initiallyat its fair value net of associated transaction costs, and is measured subsequently at the higher of the amountinitially recognised less cumulative amortisation or the amount of provision for losses under the guarantee.

- 9 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(b)

(c)

(d)

(i)

3. Significant accounting policies (continued)

- the assets or liabilities are managed and evaluated on a fair value basis; - the designation eliminates or significantly reduces an accounting mismatch which would otherwise arise; or

Financial assets and liabilities at fair value through profit or loss are not reclassified subsequent to initialrecognition.

Cash and cash equivalents

- acquired or incurred principally for the purpose of selling or repurchasing in the near term;

Classification

- are a derivative (except for a derivative that is a designated and effective hedging instrument); or

- the asset or liability contains an embedded derivative that significantly modifies the cash flows that wouldotherwise be required under the contract.

Financial instruments

The Group considers cash, nostro accounts and term placements with the CBR, banks and other financialinstitutions due within one month to be cash and cash equivalents. The minimum reserve deposit with the CBRis not considered to be a cash equivalent due to restrictions on its withdrawability.

- are part of a portfolio of identified financial instruments that are managed together and for which there isevidence of a recent actual pattern of short-term profit-taking;

The Group designates financial assets and liabilities at fair value through profit or loss where either:

Inflation accounting

Available-for-sale assets are financial assets are those financial assets that are designated as available for saleor are not classified as loans and receivables, held to maturity investments or financial instruments at fair valuethrough profit or loss.

Financial instruments at fair value through profit or loss are financial assets or liabilities that are:

All trading derivatives in a net receivable position (positive fair value), as well as options purchased, arereported as an asset. All trading derivatives in a net payable position (negative fair value), as well as optionswritten, are reported as a liability.

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are notquoted in an active market, other than those that the Group intends to sell immediately or in the near term, thosethat the Group upon initial recognition designates as at fair value through profit or loss, or those where its initialinvestment may not be substantially recovered, other than because of credit deterioration.

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixedmaturity that the Group has the positive intention and ability to hold to maturity, other than loans andreceivables and instruments designated as at fair value through profit or loss or as available for sale.

- are, upon initial recognition, designated by the Group as at fair value through the profit or loss.

The Russian Federation ceased to be hyperinflationary with effect from 1 January 2003 and accordingly noadjustments for hyperinflation have been made for periods subsequent to this date. The hyperinflation-adjustedcarrying amounts of the Group’s assets, liabilities and equity items as at 31 December 2002 became theircarrying amounts as at 1 January 2003 for the purpose of subsequent accounting.

- 10 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(ii)

(iii)

(iv)

(v)

3. Significant accounting policies (continued)

Fair value measurement principles

Where discounted cash flow techniques are used, estimated future cash flows are based on management’s bestestimates and the discount rate is a market related rate at the balance sheet date for an instrument with similarterms and conditions. Where pricing models are used, inputs are based on market related measures at thebalance sheet date.

The fair value of derivatives that are not exchange-traded is estimated at the amount that the Group wouldreceive or pay to terminate the contract at the balance sheet date taking into account current market conditionsand the current creditworthiness of the counterparties.

Gains and losses on available-for-sale financial assets are recognised directly in net assets attributable toparticipants (except for impairment losses and foreign exchange gains and losses) until the asset isderecognised, at which time the cumulative gain or loss previously recognised in equity is recognised in theincome statement.

Recognition

Measurement

For financial assets and liabilities carried at amortised cost, a gain or loss is recognised in the income statementwhen the financial asset or liability is derecognised or impaired, and through the amortisation process.

Gains and losses on financial instruments classified as at fair value through profit or loss are recognised in theincome statement.

Financial assets and liabilities are recognised in the balance sheet when the Group becomes a party to thecontractual provisions of the instrument. All regular way purchases of financial assets are accounted for at thesettlement date.

Gains and losses on subsequent measurement

Subsequent to initial recognition, financial assets, including derivatives that are assets, are measured at their fairvalues, without any deduction for transaction costs that may be incurred on sale or other disposal, except forloans and receivables and held to maturity investments which are measured at amortised cost less impairmentlosses and investments in equity instruments that do not have a quoted market price in an active market andwhose fair value cannot be reliably measured which are measured at cost less impairment losses.

A financial asset or liability is initially measured at its fair value plus, in the case of a financial asset or liabilitynot at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issueof the financial asset or liability.

All financial liabilities, other than those designated at fair value through profit or loss and financial liabilitiesthat arise when a transfer of a financial asset carried at fair value does not qualify for derecognition, aremeasured at amortised cost. Amortised cost is calculated using the effective interest method. Premiums anddiscounts, including initial transaction costs, are included in the carrying amount of the related instrument andamortised based on the effective interest rate of the instrument.

The fair value of financial instruments is based on their quoted market price at the balance sheet date withoutany deduction for transaction costs. If a quoted market price is not available, the fair value of the instrument isestimated using pricing models or discounted cash flow techniques.

- 11 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(vi)

(vii)

(viii)

(ix)

(e)

3. Significant accounting policies (continued)

Financial guarantees

A financial guarantee is a contract that require the Group to make specified payments to reimburse the holderfor a loss it incurs because a specified debtor fails to make payment when due in accordance with the terms of adebt instrument.

A financial guarantee liability is recognised initially at fair value net of associated transaction costs, and ismeasured subsequently at the higher of the amount initially recognised less cumulative amortisation or theamount of provision for losses under the guarantee. Provisions for losses under financial guarantee arerecognised when losses are considered probable and can be measured reliably.

Derecognition

Derivative financial instruments

Financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legallyenforceable right to set off the recognised amounts and there is an intention to settle on a net basis, or realise theasset and settle the liability simultaneously.

Securities sold under sale and repurchase agreements are accounted for as secured financing transactions, withthe securities retained in the balance sheet and the counterparty liability included in amounts due to other banksor to customers, as appropriate. The difference between the sale and repurchase price represents interestexpense and is recognised in the income statement over the terms of the agreement.

Financial guarantee liabilities are included within other liabilities.

Repurchase and reverse repurchase agreements

A financial asset is derecognised when the contractual rights to the cash flows from the financial asset expire orwhen the Group transfers substantially all of the risks and rewards of ownership of the financial asset. Anyrights or obligations created or retained in the transfer are recognised separately as assets or liabilities. Afinancial liability is derecognised when it is extinguished.

Offsetting

Securities purchased under agreements to resell are recorded as due from banks or customers as appropriate.The differences between the sale and repurchase prices are treated as interest and accrued over the life of theagreement using the effective interest method.

The Group uses derivative financial instruments to economically hedge its exposure to foreign exchange andinterest rate risk arising from financing activities. These instruments do not qualify for hedge accounting andthus any gain or loss on the derivative financial instruments is recognised in the income statement.

- 12 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(f)

(i)

(ii)

(iii)

(iv)

(g)

(i)

Operating leases, under the terms of which the Group does not assume substantially all the risks and rewards ofownership, are expensed on a straight line basis.

Leasehold improvements

Goodwill arising on an acquisition represents the excess of the cost of the acquisition over the fair value of thenet identifiable assets and liabilities acquired. Goodwill is stated at cost less impairment losses (refer to Note3(h) below).

5 years

Items of property and equipment are stated at cost less accumulated depreciation (refer below) and impairmentlosses (refer to Note 3(h) below). The cost for self-constructed assets includes the cost of materials, directlabour and an appropriate proportion of production overheads.

Owned assets

Expenditure incurred to replace a component of an item of property, plant and equipment that is accounted forseparately, including major inspection and overhaul expenditure, is capitalised. Other subsequent expenditure iscapitalised only when it increases the future economic benefits embodied in the item of property, plant andequipment. All other expenditure is recognised in the income statement as an expense as incurred.

Depreciation

Subsequent expenditure

Depreciation is charged to the income statement on a straight line basis over the estimated useful lives of theindividual assets. Property and equipment are depreciated from the date the asset is available for use. Theestimated useful lives are as follows:

Where an item of property, plant and equipment comprises major components having different useful lives,they are accounted for as separate items of property, plant and equipment.

5 years

5 yearsFurnitureVehicles

4 years

Goodwill

Leases in terms of which the Group assumes substantially all the risks and rewards of ownership are classifiedas finance leases. Equipment acquired by way of finance lease is stated at an amount equal to the lower of itsfair value and the present value of the minimum lease payments at inception of the lease, less accumulateddepreciation (refer below) and impairment losses (refer to Note 3(h) below).

Buildings 17-50 years

Computers and equipment

Leased assets

3. Significant accounting policies (continued)

Property and equipment

Intangible assets

- 13 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(ii)

(iii)

1-5 years1-5 years

(h)

(i)

Future cash flows are estimated on the basis of contractual cash flows of the assets and historical lossexperience for assets with similar credit risk characteristics. Historical loss experience is adjusted on the basisof current observable data to reflect the effects of current conditions that did not affect the period on which thehistorical loss experience is based and to remove the effects of conditions in the historical period that do notexist currently. The methodology and assumptions used for estimating future cash flows are reviewed regularlyby the Group to reduce any differences between loss estimates and actual loss experience.

As retail lending is relatively new to Russia, the Group and the industry have limited historical experience inthis type of lending on which to base the assessment of recoverable amount of its retail loan portfolio. TheGroup estimates impairment on its retail loan portfolio based on its past historical loss experience for thesetypes of loans, portfolio delinquency and collection rates and overall economic conditions. Changes incollection estimates could affect the loan impairment. Should actual repayments be less than managementestimates, the Group would be required to record additional loan impairment losses.

All impairment losses in respect of loans and receivables are recognised in the income statement and are onlyreversed if a subsequent increase in recoverable amount can be related objectively to an event occurring afterthe impairment loss was recognised.

Financial assets carried at amortised cost

Intangible assets, which are acquired by the Group, are stated at cost less accumulated amortisation andimpairment losses (refer to Note 3(h) below). Expenditure on internally generated goodwill and brands isrecognised in the income statement as an expense as incurred.

Amortisation is charged to the income statement on a straight-line basis over the estimated useful lives ofintangible assets. Goodwill is not amortised; other intangible assets are amortised from the date the asset isavailable for use. The estimated useful lives are as follows:

Financial assets carried at amortised cost consist principally of loans and other receivables (“loans andreceivables”). The Group reviews its loans and receivables, to assess impairment on a regular basis. A loan orreceivable is impaired and impairment losses are incurred if, and only if, there is objective evidence ofimpairment as a result of one or more events that occurred after the initial recognition of the loan or receivableand that event (or events) has had an impact on the estimated future cash flows of the loan that can be reliablyestimated.

3. Significant accounting policies (continued)

SoftwareLicenses

Impairment

Intangible assets

Amortisation

- 14 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(ii)

(iii)

(i)

(j)

(k)

Non-financial assets

The Government of the Russian Federation is responsible for providing pensions and retirement benefits to theGroup's employees. A regular contribution linked to employees’ salaries is made by the Group to theGovernment to fund the national pension plans. Payments under these pension schemes are charged as expensesas they fall due.

Significant accounting policies (continued)

According to relevant Russian legislation, a participant in a limited liability company may unilaterally withdrawfrom the company. In such case the company is obliged to pay the withdrawing participant’s share of net assetsof the company. As a result, charter capital, other capital contributions and retained earnings attributable to theparticipants in the Bank have been presented as a liability in order to comply with the revised IAS 32 FinancialInstruments: Disclosure and Presentation (refer to Note 23).

A provision is recognised in the balance sheet when the Group has a legal or constructive obligation as a resultof a past event, and it is probable that an outflow of economic benefits will be required to settle the obligation.If the effect is material, provisions are determined by discounting the expected future cash flows at a pre-taxrate that reflects current market assessments of the time value of money and, where appropriate, the risksspecific to the liability.

Financial assets carried at cost

Pensions

All impairment losses in respect of these investments are recognised in the income statement and can not bereversed.

Financial assets carried at cost include unquoted equity instruments included in available-for-sale assets that arenot carried at fair value because their fair value can not be reliably measured. If there is objective evidence thatsuch investments are impaired, the impairment loss is calculated as the difference between the carrying amountof the investment and the present value of the estimated future cash flows discounted at the current market rateof return for a similar financial asset.

3.

Other non financial assets, other than deferred taxes, are assessed at each reporting date for any indications ofimpairment. The recoverable amount of non financial assets is the greater of their fair value less costs to selland value in use. In assessing value in use, the estimated future cash flows are discounted to their present valueusing a pre-tax discount rate that reflects current market assessments of the time value of money and the risksspecific to the asset. For an asset that does not generate cash inflows largely independent of those from otherassets, the recoverable amount is determined for the cash-generating unit to which the asset belongs. Animpairment loss is recognised when the carrying amount of an asset or its cash-generating unit exceeds itsrecoverable amount.

All impairment losses in respect of non financial assets are recognised in the income statement and reversedonly if there has been a change in the estimates used to determine the recoverable amount. Any impairment lossreversed is only reversed to the extent that the asset’s carrying amount does not exceed the carrying amount thatwould have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

Provisions

Net assets attributable to participants

- 15 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(l)

(m)

(n)

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will beavailable against which the temporary differences, unused tax losses and credits can be utilised. Deferred taxassets are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

Interest income and expense

Fee and commission income

Interest income and expense is recognised in the income statement as it accrues, taking into account theeffective yield of the asset or an applicable floating rate. Interest income and expense includes the amortisationof any discount or premium or other differences between the initial carrying amount of an interest bearinginstrument and its amount at maturity calculated on an effective interest rate basis.

Loan origination fees, loan servicing fees and other fees that are considered to be integral to the overallprofitability of the loan together with the related direct costs, are deferred and recognised as an adjustment tothe effective interest rate.

Fee and commission income is recognised when the corresponding service is provided.

Taxation

3. Significant accounting policies (continued)

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted orsubstantially enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

Deferred tax is provided using the balance sheet liability method, providing for temporary differences betweenthe carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxationpurposes. The following temporary differences are not provided for: goodwill not deductible for tax purposes,the initial recognition of assets or liabilities that affect neither accounting nor taxable profit and temporarydifferences related to investments in subsidiaries, branches and associates where the parent is able to control thetiming of the reversal of the temporary difference and it is probable that the temporary difference will notreverse in the foreseeable future. The amount of deferred tax provided is based on the expected manner ofrealisation or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantiallyenacted at the balance sheet date.

Income tax on the profit or loss for the year comprises current and deferred tax. Income tax is recognised in theincome statement except to the extent that it relates to items recognised directly to equity, in which case it isrecognised in equity.

- 16 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(o)

(p)

3. Significant accounting policies (continued)

IFRIC 9 “Reassessment of embedded derivatives” , which is effective for annual periods beginning on or after1 November 2006, clarifies that an embedded derivative shall be assessed for separation from the host contractand accounted for as a derivative when the Group first becomes a party to the contract. Subsequentreassessment is prohibited unless there is a significant change in the terms of the contract, i.e. in the terms ofeither the host contract or the embedded derivative or both.

IFRS 7 “Financial Instruments: Disclosures” , which is effective for annual periods beginning on or after1 January 2007, provides disclosure requirements regarding the significance of financial instruments to theGroup’s financial position and performance, and qualitative and quantitative information about the nature andextent of risks arising from financial instruments. The Standard supersedes IAS 30 “Disclosures in theFinancial Statements of Groups and Similar Financial Institutions” and the disclosure requirements in IAS 32“Financial Instruments: Presentation and Disclosure” . A large portion of existing disclosure requirements inInternational Financial Reporting Standard IAS 32 “Financial Instruments: Presentation and Disclosure” istransferred to the new Standard. The title of International Financial Reporting Standard IAS 32 is amended toIAS 32 “Financial Instruments: Presentation” .

IFRS 8 “Operating Segments” , which is effective for annual periods beginning on or after 1 January 2009,specifies how the Group should report information about its operating segments and sets out requirements forrelated disclosures about products and services, geographical areas and major customers. Operating segmentsare components of the Group about which separate financial information is available that is evaluated regularlyby the chief operating decision maker in deciding how to allocate resources and in assessing performance.Financial information is required to be reported on the same basis as is used internally for evaluating operatingsegment performance and deciding how to allocate resources to operating segments. IFRS 8 “OperatingSegments” will replace International Financial Reporting Standard IAS 14 “Segment Reporting”.

IFRIC 10 “Interim Financial Reporting and Impairment” , which is effective for annual periods beginning onor after 1 November 2006, clarifies that impairment loss recognised in a previous interim period in respect ofgoodwill, an investment in an equity instrument or a financial asset carried at cost should not be reversed.

New standards and interpretations not yet adopted

The Group operates in one business and geographical segment. Therefore separate segment reporting is notpresented.

Segment reporting

A number of new Standards, amendments to Standards and Interpretations are not yet effective as at31 December 2006, and have not been applied in preparing these consolidated financial statements. Of thesepronouncements, potentially the following will have an impact on the Group’s operations. The Group plans toadopt these pronouncements when they become effective. The Group has not yet analysed the likely impact ofthese new standards on its financial statements.

Amendment to IAS 1 “Presentation of Financial Statements – Capital Disclosures” , which is effective forannual periods beginning on or after 1 January 2007. The Standard will require increased disclosure in respectof the Group’s capital.

- 17 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

6. Fee and commission expense

Customer payments processing and account maintenance

Cash operations

744,601

8,952

185,019

Insurance agent commissions22,257

195,767

Other

140,8681,393

Fees from retailers 955,652393,402

452,883

TRUB

1,184

2006

Securities 128,280

Debt securities issued

Loans to corporations

7,784,928

1,155,795

7,003

2,201

2006TRUB

(122,439)

109,430

183,74417,294

1,306,448

2005

2,131,782

TRUB

653,201

4.2006

553,363

9,937,687353,528

TRUB

5. Fee and commission income

Interest expense

(4,834)

Product delivery fees 276,796Other

TRUBTRUB

557,55498,17988,868

(22,103)

7.

Net foreign exchange expense

Other operating income, net

95,339

248,630

2005TRUB

34,40459,862

(71,078)

Customer payments processing and account maintenance 367,453

544,383

(23,782)

Contractual penalties from customers

Loss on early redemption of debtNet gains/(losses) from operations with securities

1,686,469

36,206

20052006

1,527,521

52,567

2,333,089

Current accounts and deposits from customersDue to banks and other financial institutions 973,786

1,879,022

Loans to individuals

2005

7,576,887

TRUB

Placements with banks and other financial institutions

Interest income

Interest income and interest expense

55,823

10,475,318

Other

- 18 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

15

Note

Payroll related taxesOccupancy

9. General administrative expenses

-Current tax expense - overprovided in previous periods

188,666 120,046Depreciation and amortisation

1,442,868

10. Income tax expense

TRUB

3,549

959,005

Advertising and marketing

3,550,278

133,483

2,485,849

114,475

107,01171,22065,024

Overprovided in previous periods

(36,762)

3,5493,414Effect of income taxed at lower tax rates

229,786

55,71142,197

2005

2005TRUBTRUB

2006

20052006

3,874

(155,968)

2006

887,286

167,826151,069

-

TRUB

327,289

Impairment losses

(155,968)

320,226

TRUB

(259,960)

(89,782)

TRUB

(66,186)

108,079

311,379282,413

(230,161)

464,587

(44,531)64

(259,960)

Net non-deductible costs

(806,298)

Profit before tax

Current tax expense - current year

Deferred tax benefit/(expense)

Income tax using the applicable tax rate (24%) (111,501)

2005

(5,007)

TRUB

3,917,123

TRUB

4,974,236

3,920,9974,969,229

263,077

182,788

Employee compensationCommunications and information servicesTaxes other than income tax

2006

Other

Professional services

Travel expensesRepairs and maintenance

464,208

542,789

8.

Reconciliation of effective tax rate

Loans to customersOther assets

- 19 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

Minimum reserve deposit with the CBR

Analysis of movements in accumulated impairment losses

38,780 -1,821,494

Mortgage loans

12.

11.

Cash

Placements with banks and other financial institutions

28,723(4,970,732)

Term deposits with banks and other financial institutions

163,6751,055,806

TRUB

4,341,1461,000,862

Consumer loans

TRUB

96,282

10,516

2006

25,631,916

2,823,70178,562

TRUB

TRUB2006

TRUB23,125,85611,736,509

31,780,630

2005

2006

5,699,391

Placements with banks and other financial institutions

8,199,993

2005

1,255,694Nostro accounts with the CBR

Cash and cash equivalents

13.

Accumulated impairment losses

Balance at 1 JanuaryImpairment losses recognised in the income statement 4,974,236

(2,685,060)(1,130,169)

Balance at 31 December

Amount related to loans written-off

67,393962,418

357,383

TRUB

9,466,203

(368,895)(918,261)

3,811,7254,970,732

Amount related to loans sold

The Group considers loans which are contractually overdue for more than 90 days to be non-performing. As of31 December 2006 total non-performing loans amounted to TRUB 5,203,158 (2005: TRUB 4,099,759). TheGroup created provisions for non-performing loans of 69.4% (2005: 73.4%). Performing loans are provided forat a rate 4.3% (2005: 3.2%).

3,917,123

2006

1,181,7583,811,725

TRUB

Loans to corporations

due within one month

Loans to customers

93,388

The minimum reserve deposit is a mandatory non-interest bearing deposit calculated in accordance withregulations issued by the CBR and whose withdrawability is restricted.

Cash loans

26,279,057

2005

due after one month

2005TRUB

262,321(3,811,725)

Credit card loans

- 20 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

25

-

403,403108,835

(39)

Furn

iture

223,729

Tot

al

3,399,949

4,853

Balance at 31 December(8,503)

Debt securities - trading

88,449

Lan

d &

bu

ildin

gs

Veh

icle

s

Balance at 31 December

Net book value

Disposals -6,331

Note

Balance at 1 January

Balance at 1 January 380,10824,6431,478Accumulated depreciation

185,9543,213,995

133,949

45,500(35)(4,754)

6306647,55725,611

184,476

TRUBTRUBTRUB

97,813

122,45619,996

233,003

-1,294

2,22123,295

387,630

512,199(5,191)

TRUB

Lea

seho

ld

impr

ovem

ents

Com

pute

rs

and

equi

pmen

t

TRUB

23,951Positive fair value of derivative instruments

4,390,821275,1963,393,618 506,4912,498124,569

15. Property, equipment and intangible assets

Depreciation charge

at 1 January

Net book value at 31 December

870,339-

3,792

10,312

21,557

133,790

362,826

Disposals

The Group has estimated the impairment on loans to customers in accordance with the accounting policydescribed in Note 3(h). Changes in collection estimates could affect the impairment losses recognised. Forexample, to the extent that estimated future cash flows of loans differs by plus/minus one per cent., the loanimpairment as of 31 December 2006 would be approximately TRUB 317,806 higher/lower (31 December 2005:TRUB 256,319).

Cost 595,829279,701941Additions

2,851

TRUB

(13,734)(1)5,216,981

166,135 3,789,603

TRUB

1,441,112130,619

TRUB2006

TRUB

1,664,346

2005

1,017,558

14. Financial assets at fair value through profit or loss

Loan and receivables overdue over one year where further collection procedures are economically unfeasibleare written off. The amount of loans written off during the year totalled TRUB 1,130,169 (2005:TRUB 368,895). In addition, during the year 2006 the Group sold non-performing loans with a carryingamount of TRUB 2,948,632 (2005: TRUB 1,050,739).

As at 31 December 2006 consumer loans with the total carrying amount of TRUR 4,527,318 (31 December2005: TRUB 2,999,973) were collateralised in relation to the notes issued by the Eurasia Structured FinanceNo.1 S.A. as a part of consumer loan securitisation transaction (refer to Note 17). Eurasia Structured FinanceNo.1 S.A. can not sell or repledge these consumer loans to other parties save for the obligation of the Bank torepurchase ineligible consumer loans.

1,888,0751,041,509

(7,735)826,160

(1)

119,373

296,753

Inta

ngib

le

asse

ts

(2,945)363,848

11,246 651,108182,787

790,004

13. Loans to customers (continued)

- 21 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

VariableUnsecured RUB bond issue 2 of TRUB 3,000,000 3,020,084

10,025

Unsecured RUB bond issue 3 of TRUB 3,000,000 Variable 3,002,039

May 2010

Class A1 consumer loans receivables backed notes of TEUR 100,000

Maturity

February 2008Loan participation notes issue 1 of TUSD 150,000

Loan participation notes issue 2 of TUSD 275,000 June 2008

Prepaid expenses

16. Other assets

Accrued income

20052006

17.

September 2010

May 2012

May 2012 455,365

438,436

Floating

Class B consumer loans receivables backed notes of TEUR 13,000

Class A2 consumer loans receivables backed notes of TEUR 13,500

7,516,817

October 2011 3,043,881

4,062,347

Fixed

Variable

Floating

May 2012

Settlements with suppliers

TRUB

TRUB

1,185,544

Materials, supplies and inventories

736,554

Taxes other than income tax30,030

TRUB

Other

Interest rate

55,42343,253

1,407,644963,045

16,979(7,173)

4,421,488

Floating

Fixed

86,747 67,983

20052006

Included in settlements with suppliers above are amounts paid under construction agreements ofTRUB 421,853 (31 December 2005: of TRUB 976,583).

Debt securities issued

Accumulated impairment losses

3,275,992

237,798

426,555

-

2,981,400

22,224,67024,318,770

Unsecured RUB bond issue 4 of TRUB 3,000,000

7,861,353

10,000

104,281

TRUB

33,214(2,171)

3,366,872

2,433,013

- 22 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

Debt securities issued (continued)

Term depositsOther balances

The USD denominated loan participation notes 2 were issued by the Group in June 2005 through EurasiaCapital S.A. (refer to Note 1). The proceeds from the issue were used to grant an unsecured loan to the Bank.

6,803,288

37,839

Included in unsecured loans above is exposure to three counterparties exceeding 10% of net assets attributableto participants totalling TRUB 5,415,098 (31 December 2005: exposure to one counterparty totallingTRUB 2,048,071).

5,015,032

5,438,025

399,000Subordinated loans 928,424Unsecured loans

Due to banks and other financial institutions

TRUB

The RUB denominated bonds 3 were issued by the Group in September 2005 with a fixed coupon rate valid forthe subsequent eighteen months. Coupon rates for the remaining period will be set by the Group on a quarterlybasis starting March 2007. Bondholders are entitled to require early redemption of the bond issue at par inMarch 2007.

18.2006

17.

1,738,489

The USD denominated loan participation notes 1 were issued by the Group in February 2005 through EurasiaCapital S.A. (refer to Note 1). The proceeds from the issue were deposited with a fiduciary bank which used theamount to grant an unsecured loan to the Bank.

Eurasia Capital S.A. and Eurasia Structured Finance No.1 S.A. are SPEs established by the Group with theprimary objective of raising finance through the issuance of debt securities and securitising part of Group’sconsumer loan portfolio. These SPEs are controlled by the Group through the predetermination of the activitiesof SPEs, having rights to obtain the majority of benefits of the SPEs, and retaining the majority of the residualrisks related to the SPEs.

The RUB denominated bonds 4 were issued by the Group in October 2006 with a fixed coupon rate valid forthe subsequent twenty four months. Coupon rates for the remaining period will be set by the Group on aquarterly basis starting October 2008. Bondholders are entitled to require early redemption of the bond issue atpar in October 2008.

The RUB denominated bonds 2 were issued by the Group in May 2005 with a fixed coupon rate valid for thesubsequent twelve months. Coupon rates for the remaining period are set by the Group each twelve monthsstarting in May 2006. A portion of the RUB bonds 2 were repurchased at par in May 2006. Some ofrepurchased bonds were subsequently sold by the Group on the open market.

2,773,967

The EUR denominated consumer loan receivables backed notes were issued by the Group in December 2005through Eurasia Structured Finance No.1 S.A. (refer to Note 1). Coupon rates are set on a monthly basis basedon the EURIBOR rate. The notes can be redeemed in full at the option of Eurasia Structured Finance No.1 S.A.at par in May 2010.

TRUB2005

170,000332,576

- 23 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

Negative fair value of derivative instruments 25

(405,413)

Cash and cash equivalents, placements with banks and other financial institutions

Property, equipment and intangible assets

3,038,623

TRUB

421,967

Other taxes payable

166,068

Tax loss carry-forwards

15

254,519 12,354

15

43,975

(519)(340,720)

294,167498

296,120

325,938

35,07719,00312,270

39,589

22. Other liabilities2005

Loans to customers 726,291

(26,419)(70,141)

140,459-

Net deferred tax assets/(liabilities)

Note

169,817

169,817

51,181Accrued employee compensationSettlements with suppliers

- (26,419)3,094

TRUB

(24,989)(34,751)

2006TRUB

(118,909)

(34,751)

19. Current accounts and deposits from customers

TRUB

Deferred tax asset and liability

The Group’s applicable tax rate for deferred tax is 24% (2005: 24%). Temporary differences between thecarrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxationpurposes give rise to a net deferred tax asset as of 31 December 2006. These temporary differences, which haveno expiry dates (except for losses carried forward, that expire within 10 years from the year of origination), arelisted below at their tax effected accumulated values:

(24,989)

TRUB2006

Other items

(39,070)

Other

Current accounts and demand depositsTerm deposits

--

2006TRUB

Fair value of derivative financial instrumentsDebt securities issued

Assets

20052006

Financial liabilities at fair value through profit or loss

2005TRUB

38,695

15,532(63,011)

16,743

3,055,366

TRUB

38,695

TRUB

145,188385,571

(260,225)

(8,536) 95,927

21.

254,519

(63,011)

2005200620052006

(124,927)(504) (48,496)

20.

-

8,215

TRUB

-

Liabilities

3,170,607

2005TRUB TRUB

12,354

423,880

(48,511)

35,439

(35,976)

Net

3,162,392

- 24 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(a)

(b)

TRUB

Charter capitalTRUB TRUB

Retained earnings

Other capital

24. Financial instruments

-

4,630,585

-

Balance at 31 December 2006 4,405,707

Net profit attributable to participants

706,350

TotalTRUB

2,768,203

5,479,899

308,619

8,556,721

23. Net assets attributable to participants

Contributions by owners -

Balance at 31 December 2005

Net profit attributable to participants 308,619-

1,479,899

Management of the risk arising from financial instruments is fundamental to the Group’s business and is anessential element of the Group’s operations. The major risks faced by the Group are those related to creditexposures, liquidity and movements in interest rates and foreign exchange rates. These risks are managed in thefollowing manner:

699,045

9,962,116925,824

699,045

Credit risk is the risk of financial loss occurring as a result of default by a borrower or counterparty on theirobligation to the Group. The majority of the Group’s exposure to credit risk arises in connection with theprovision of consumer financing to private individual customers, which is the Group’s principal business. Asthe Group’s loan portfolio consists of large amount of loans with relatively low outstanding amounts, the loanportfolio does not comprise any significant individual items.

Interest rate risk

The Group has developed policies and procedures for the management of credit exposures, including creditscoring of customers, guidelines to limit portfolio concentration and the establishment of a credit departmentwhich actively monitors the Group’s credit risk.

Interest rate risk is measured by the extent to which changes in market interest rates impact on margins and netinterest income. To the extent the term structure of interest bearing assets differs from that of liabilities, netinterest income will increase or decrease as a result of movements in interest rates.

Interest rate risk is managed by increasing or decreasing positions within limits specified by the Group’smanagement. These limits restrict the potential effect of movements in interest rates on current earnings and onthe value of interest sensitive assets and liabilities. As part of its management of this position, the Group usesinterest rate derivatives (refer to Note 25).

Credit risk

A financial instrument is any contract that gives rise to the right to receive cash or another financial asset fromanother party or the obligation to deliver cash or another financial asset to another party.

Balance at 1 January 2005

4,405,707

-

Contributions by owners 4,000,000

3,924,235

706,350 -

226,779

(81,840)

-

405,707 2,444,336

- 25 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

24.

-- - - - -- - - 58Other currencies 0.0% 58 -

1,407

-

-

- -

-

-

- 497-

-3,988 3,096 - -

4.9%

5,835,182

6.9%7,084 6,667634

-

-

--

- -

More than 5 years Total2 to 5 years

More than 5 years

Less than 3 monthsTotal

Debt securities issued (EUR)

Debt securities issued (RUB)

Current accounts and deposits from customers

Placements with banks and other financial institutions

Loans to individuals (USD)Financial assets at fair value through profit or loss (RUB)Financial assets at fair value through profit or loss (USD)

Interest bearing financial liabilities

-

RUB

Loans and term deposits (other currencies )

- 1,830,559

Loans and term deposits (RUB) Loans and term deposits (USD)

12,562 -

-

13.8%46.4%

-

-

14,200 14,523

-

-

-

USD

Loans to customers Loans to corporations (RUB)

Current accounts and demand deposits (USD) Term deposits (RUB)

Loans to individuals (RUB)

438,599

Financial instruments (continued)

Less than 3 months

3 to 12 months 1 to 2 years

Effective interest

rate

TRUB

2 to 5 years

Effective interest rates and repricing analysis

In respect of interest-bearing financial assets and liabilities, the following table indicates their effective interest rates at the balance sheet date and the periods in which they reprice.

2005

3 to 12 months 1 to 2 years

Effective interest

rate

458,472 -3,090,206

2006

Due to banks and other financial institutions

Interest bearing financial assets

2.4%

11.5%

39,624 -

- 38,6307,518,0733,953,724

968,048

-

5,396,583

-

8.3% 1,198,613 631,946

5.2% 2,571,781 58,545

-

-

28,723- -

12,562-

2,630,326-

-

31,713,127150

5,102,211 15,139,119

7.7% - 428,454 421,269

32 602 -

-- - -

- - -

115 382 - -

Debt securities issued (USD)

Term deposits (EUR)

6.9%5.0%3.8%

7.6%8.7%

8.9%8.8%

Term deposits (USD)

- - 928,424- -

2,406,913 2,981,814 - -11,120,692 - - 11,579,164

6.7% 4,260,673 - -

6.0%

- - 4,260,673

8,478,933

- -

38,780

167,835 1,017,558

4.4% 2,069,597 357 -

-

2,854,682 53,480 - -

-

- 2,908,162

- - 2,069,954

-

- 258,05839.8% 4,550,734 17,871,610 220,717 2,730,797 - 25,373,85813.2%

- - -

155,266 102,792

7.0% 408,675 227,376 -

- - -

2,183 - 638,234

1,026,112 - 1,026,1129.0% - -

6,0550.1% 1,447 -

-- -- -

-

- -4.7% 360

-2,151 - - -

103

- -2.1% 486,8792,048,071 -

- -8.9% 741,593

- 12,282,841

1,738,489

9.5% - 3,020,084 2,981,4009.5%

--

- --

- -- -

6,001,48412,282,841

3,940,3456.3% 3,940,345 - -

486,8794,528,153

1,44712,722

2,5111,510

- 26 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

24.

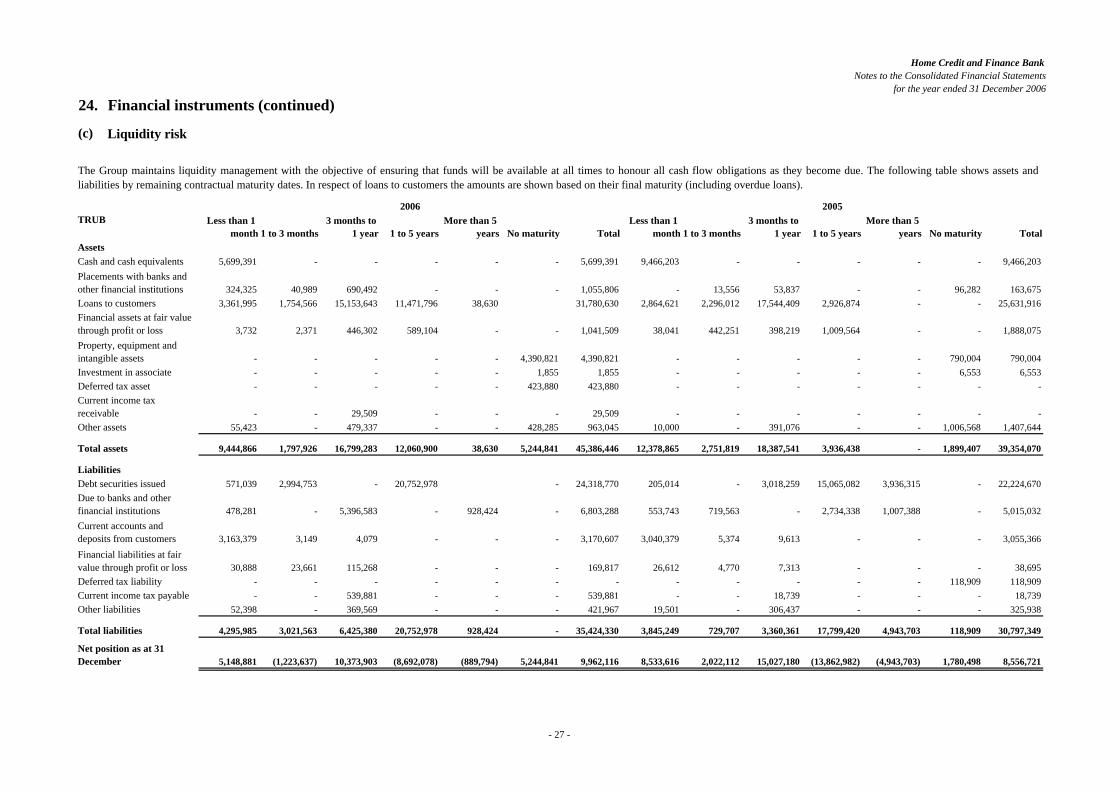

(c) Liquidity risk

- -- - - -- 423,880 423,880 -- - - -

4,943,703 118,909 30,797,3493,845,249 729,707 3,360,361 17,799,420

325,938

12,378,865 2,751,819 18,387,541 3,936,438 - 1,899,407 39,354,070

19,501 - 306,437 -

- 118,909- -

- -

118,909- - 18,739 - - - 18,739- -

- - 3,055,366

26,612 4,770 7,313 - - - 38,695

3,040,379 5,374 9,613 -

3,936,315 - 22,224,670

553,743 719,563 - 2,734,338 1,007,388 - 5,015,032

205,014 - 3,018,259 15,065,082

- - -10,000 - 391,076 - - 1,006,568 1,407,644

- - - -

- 790,004 790,004- - - - - 6,553 6,553- - - -

- - 25,631,916

38,041 442,251 398,219 1,009,564 - - 1,888,075

2,864,621 2,296,012 17,544,409 2,926,874

- - 9,466,203

- 13,556 53,837 - - 96,282 163,675

9,466,203 - - -

- 35,424,330

- - 539,881- - 421,967

928,4244,295,985 3,021,563 6,425,380 20,752,978

52,398 - 369,569 -- - 539,881 -

- - 169,817- - - - - - -

30,888 23,661 115,268 -

928,424 - 6,803,288

3,163,379 3,149 4,079 - - - 3,170,607

478,281 - 5,396,583 -

38,630 5,244,841 45,386,446

571,039 2,994,753 - 20,752,978 - 24,318,770

9,444,866 1,797,926 16,799,283 12,060,900

- - 29,50955,423 - 479,337 - - 428,285 963,045

- - 29,509 -

- 4,390,821 4,390,821- - - - - 1,855 1,855- - - -

38,630 31,780,630

3,732 2,371 446,302 589,104 - - 1,041,509

3,361,995 1,754,566 15,153,643 11,471,7961,055,806

5,699,391 -

324,325 40,989 690,492 -

-

Total liabilities

Net position as at 31 December

Financial instruments (continued)

2006

- - - 5,699,391

1 to 3 months3 months to

1 year

Financial liabilities at fair value through profit or lossDeferred tax liabilityCurrent income tax payableOther liabilities

LiabilitiesDebt securities issuedDue to banks and other financial institutionsCurrent accounts and deposits from customers

Investment in associate

Current income tax receivableOther assets

Total assets

Deferred tax asset

Loans to customers

Assets

Financial assets at fair value through profit or lossProperty, equipment and intangible assets

2005

Cash and cash equivalents

TRUB

Placements with banks and other financial institutions

1 to 5 yearsMore than 5

years No maturity Total

- -

Less than 1 month

More than 5 years No maturity

Less than 1 month 1 to 3 months

3 months to 1 year 1 to 5 years

(889,794) 5,244,841 9,962,116 8,533,6165,148,881 (1,223,637) 10,373,903 (8,692,078)

The Group maintains liquidity management with the objective of ensuring that funds will be available at all times to honour all cash flow obligations as they become due. The following table shows assets andliabilities by remaining contractual maturity dates. In respect of loans to customers the amounts are shown based on their final maturity (including overdue loans).

(4,943,703) 1,780,498 8,556,721

Total

(13,862,982)2,022,112 15,027,180

- 27 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

24.

(d)

- - -- 423,880 - -Deferred tax asset - - 423,880

110,540 -

9,125,332 45,418

109,189 -

10,362,026 4,266,736 (14,615,595)

8,556,721

(16,685,014) - -

9,962,116 (106,207) (507,822)347,816 156,491 9,376,703 81,107

(13,166)

35,424,330 16,814,999 4,269,346

- 13,271,707 3,413,307

30,797,34912,729,682 4,311,213 18,382,978 457 9,713,004 -

421,967 46 216,703 325,938155,161 45,952 220,455 399539,881 - - 18,73918,739 -3,550 536,331 -

- 38,695- - - - - - 8,369 118,909

- 3,055,366

- - 169,817 - 169,817 - - 38,695

- 5,015,03227,309 1,038 3,142,260 - 3,170,607 3,959 103,929 2,947,478

- 22,224,670968,048 - 5,835,182 58 6,803,288 4,528,153 - 486,879

45,418 39,354,070

11,579,164 4,260,673 8,478,933 - 24,318,770 12,282,841 3,940,345 6,001,484

41,863 1,407,644

2,715,472 200,968 42,375,276 94,730 45,386,446 3,437,085 348,217 35,523,350

- -35,281 7,776 839,621 80,367 963,045 18,570 1,492 1,345,719

- 6,553

- - 29,509 - 29,509 - - -

- 790,004- - 1,855 - 1,855 - - 6,553

- 1,888,075- - 4,390,821 - 4,390,821 - - 790,004

- 25,631,916

- - 1,041,509 - 1,041,509 1,026,113 - 861,962

- 163,67538,780 - 31,741,850 - 31,780,630 - - 25,631,916

3,555 9,466,203

224,712 - 831,094 - 1,055,806 1,094 - 162,581

2006 2005

2,416,699 193,192 3,075,137 14,363 5,699,391 2,391,308 346,725 6,724,615

USDUSD EUR RUBOther

currencies Total TotalOther

currenciesRUBEUR

Net position as of 31 December

Debt securities issuedDue to banks and other financial institutionsCurrent accounts and deposits from customersFinancial liabilities at fair value through profit or lossDeferred tax liabilityCurrent income tax payableOther liabilities

Effect of foreign currency derivatives

Total liabilities

Other assets

Total assets

Liabilities

Current income tax receivable

Loans to customersFinancial assets at fair value through profit or lossProperty, equipment and intangible assetsInvestment in associate

TRUB

AssetsCash and cash equivalentsPlacements with banks and other financial institutions

Financial instruments (continued)

Foreign currency risk

The Group has assets and liabilities denominated in several foreign currencies. Foreign currency risk arises when the actual or forecast assets in a foreign currency are either greater or less than theliabilities in that currency.

Foreign exchange rate risk mainly arises due to the funding of the Group operations with liabilities denominated in foreign currencies. Derivative financial instruments are used by the Group to hedgethe mismatches in the foreign currency structure of assets and liabilities.

- 28 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(e)

17

Carrying amount

2005TRUB

(22,224,670)

1,373

3 months to 1 year

Maturity Sell/Buy

1 to 3 months RUB/USD

less than 1 month RUB/USD

3 months to 1 year

less than 1 month

Foreign currency forward contracts

less than 1 month RUB/USD

13,691,505

Interest rate swap contractsFixed/Floating

(RUB)

1 to 3 monthsFixed/Floating

(RUB)

less than 1 month EUR/USD

At 31 December 2006 the following derivative contracts were outstanding:

Fair value

Notional amount (in thousands of

purchased currency) (TRUB)

Foreign currency futures contracts

Foreign currency swap contracts

9,000

Contract type

3 months to 1 year RUB/USD 249,700

26,000

44,000

328less than 1 month CZK/USD 500 (1)

(11,303)1 to 3 months RUB/USD 30,000 (13,069)

(83,050)

(7,985)1 to 3 months RUB/USD 33,000 (9,639)

(15,465)

less than 1 month RUB/EUR 123,222 (9,828)

RUB/USD

(29)

6,661,063 1,990

1,000 45

Fixed/Floating (RUB) 11,771,088 1,095

(145,866)

2006TRUB

(24,265,952)

Carrying amount

2006TRUB

(24,318,770)

24. Financial instruments (continued)

Derivative financial instruments25.

The Group's estimates of fair values of its other financial assets and liabilities are not materially different fromtheir carrying values.

Fair value has been determined either by reference to the market value at the balance sheet date or bydiscounting the relevant cash flows using current interest rates for similar instruments.

TRUB

Fair value of financial instruments

The fair values of the following financial instruments differ from their carrying amounts shown in the balancesheet:

2005Fair value

(22,345,747)Debt securities issued

Fair value

Note

- 29 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

At 31 December 2005 the following derivative contracts were outstanding:

25. Derivative financial instruments (continued)

4,546 1 to 3 months RUB/USD 109,000 41,748

Foreign currency forward contracts

Contract type Maturity Sell/Buy

Notional amount (in thousands of

purchased currency) Fair value

less than 1 month RUB/USD 24,000

1 to 3 months USD/RUB 115,200 (545)

(21,214) 3 months to 1 year RUB/USD 247,800 173,541

Foreign currency futures contracts

less than 1 month RUB/EUR 123,338

310 3 months to 1 year RUB/USD 44,000 (1,120)

1 to 3 months RUB/USD 13,000

(979)

Interest rate swap contracts less than 1 monthFixed/Floating

(RUB) 2,960,000 (1,556)

Foreign currency swap contracts less than 1 month EUR/USD 27,303

1 to 3 monthsFixed/Floating

(RUB) 4,516,050 (3,935)

185,034

3 months to 1 yearFixed/Floating

(RUB) 4,356,193 (5,762)

The Group has outstanding commitments to extend credit. These commitments take the form of approved creditlimits related to customer's credit card accounts, approved overdraft facilities and approved consumer loans.

2006 2005

Commitments

Credit related commitments

TRUB TRUB

Credit card commitments 9,040,338 3,294,194Undrawn overdraft facilities 1,222,827 54,280

11,614,278 4,635,280

Consumer loan commitments 1,351,113 1,286,806

The total outstanding contractual commitments to extend credit indicated above represent future cashrequirements, though some of these commitments may expire or terminate without being funded.

26.

- 30 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

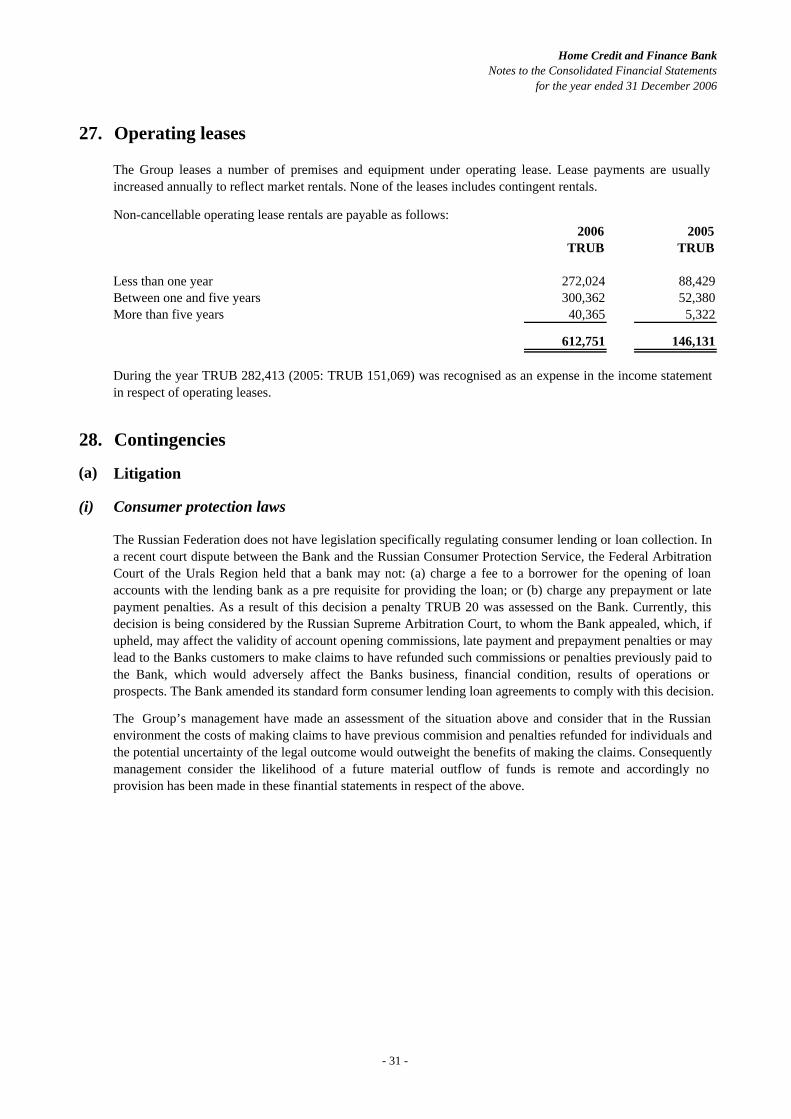

Non-cancellable operating lease rentals are payable as follows:

(a)

(i)

The Group leases a number of premises and equipment under operating lease. Lease payments are usuallyincreased annually to reflect market rentals. None of the leases includes contingent rentals.

2006 2005TRUB TRUB

Less than one year 272,024 88,429

612,751 146,131

Litigation

27. Operating leases

During the year TRUB 282,413 (2005: TRUB 151,069) was recognised as an expense in the income statementin respect of operating leases.

300,362 52,380More than five yearsBetween one and five years

40,365 5,322

28. Contingencies

The Group’s management have made an assessment of the situation above and consider that in the Russianenvironment the costs of making claims to have previous commision and penalties refunded for individuals andthe potential uncertainty of the legal outcome would outweight the benefits of making the claims. Consequentlymanagement consider the likelihood of a future material outflow of funds is remote and accordingly noprovision has been made in these finantial statements in respect of the above.

The Russian Federation does not have legislation specifically regulating consumer lending or loan collection. Ina recent court dispute between the Bank and the Russian Consumer Protection Service, the Federal ArbitrationCourt of the Urals Region held that a bank may not: (a) charge a fee to a borrower for the opening of loanaccounts with the lending bank as a pre requisite for providing the loan; or (b) charge any prepayment or latepayment penalties. As a result of this decision a penalty TRUB 20 was assessed on the Bank. Currently, thisdecision is being considered by the Russian Supreme Arbitration Court, to whom the Bank appealed, which, ifupheld, may affect the validity of account opening commissions, late payment and prepayment penalties or maylead to the Banks customers to make claims to have refunded such commissions or penalties previously paid tothe Bank, which would adversely affect the Banks business, financial condition, results of operations orprospects. The Bank amended its standard form consumer lending loan agreements to comply with this decision.

Consumer protection laws

- 31 -

Home Credit and Finance BankNotes to the Consolidated Financial Statements

for the year ended 31 December 2006

(ii)

(b)

29.

(a)

28. Contingencies (continued)

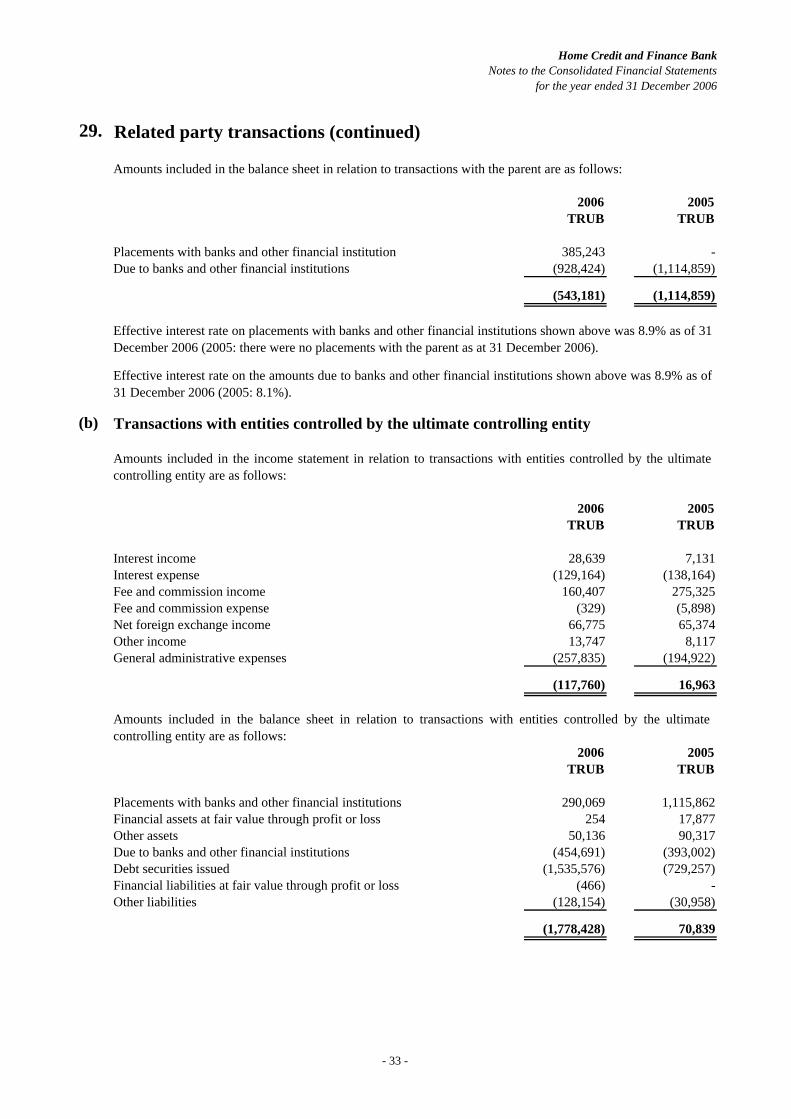

Amounts included in the income statement in relation to transactions with the parent are as follows:

2006 2005TRUB TRUB

-

Taxation contingencies