homebuyers guide 2016

TRANSCRIPT

1

Buyers’ Guide The Home Buying Process

Pam Tucker, Realtor

BBA, GRI, MCNE, SRS, SRES

Relocation Specialist

Real Estate Consultant

936-355-6057

2

3

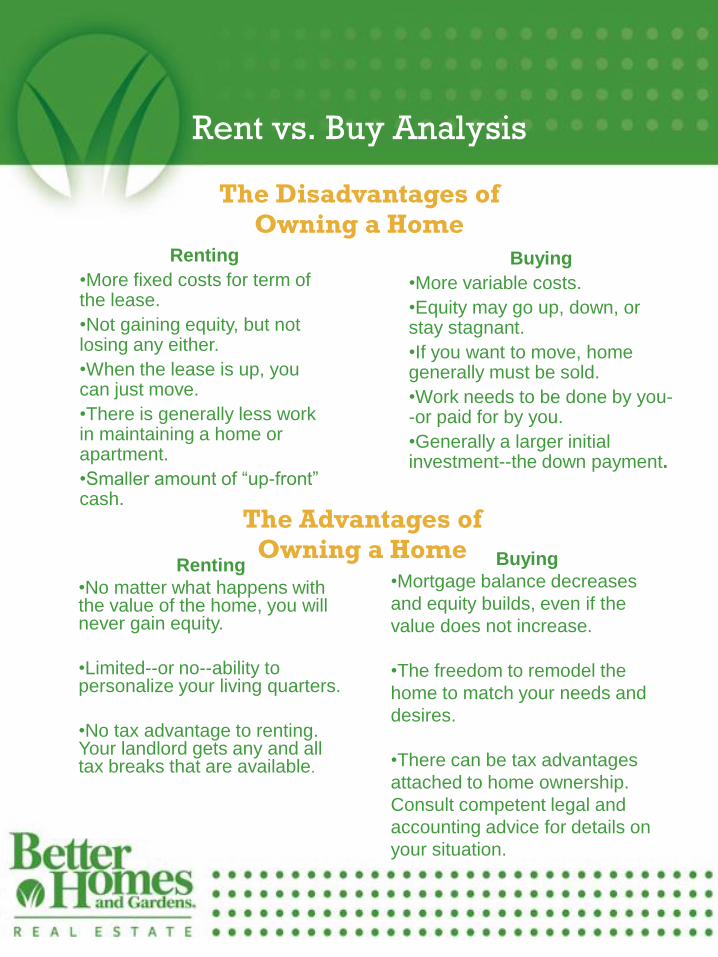

Rent vs. Buy Analysis

The Disadvantages of Owning a Home

Renting

•More fixed costs for term of the lease.

•Not gaining equity, but not losing any either.

•When the lease is up, you can just move.

•There is generally less work in maintaining a home or apartment.

•Smaller amount of “up-front” cash.

Buying

•More variable costs.

•Equity may go up, down, or stay stagnant.

•If you want to move, home generally must be sold.

•Work needs to be done by you--or paid for by you.

•Generally a larger initial investment--the down payment.

The Advantages of Owning a Home

Renting

•No matter what happens with the value of the home, you will never gain equity.

•Limited--or no--ability to personalize your living quarters.

•No tax advantage to renting. Your landlord gets any and all tax breaks that are available.

Buying

•Mortgage balance decreases

and equity builds, even if the

value does not increase.

•The freedom to remodel the

home to match your needs and

desires.

•There can be tax advantages

attached to home ownership.

Consult competent legal and

accounting advice for details on

your situation.

4

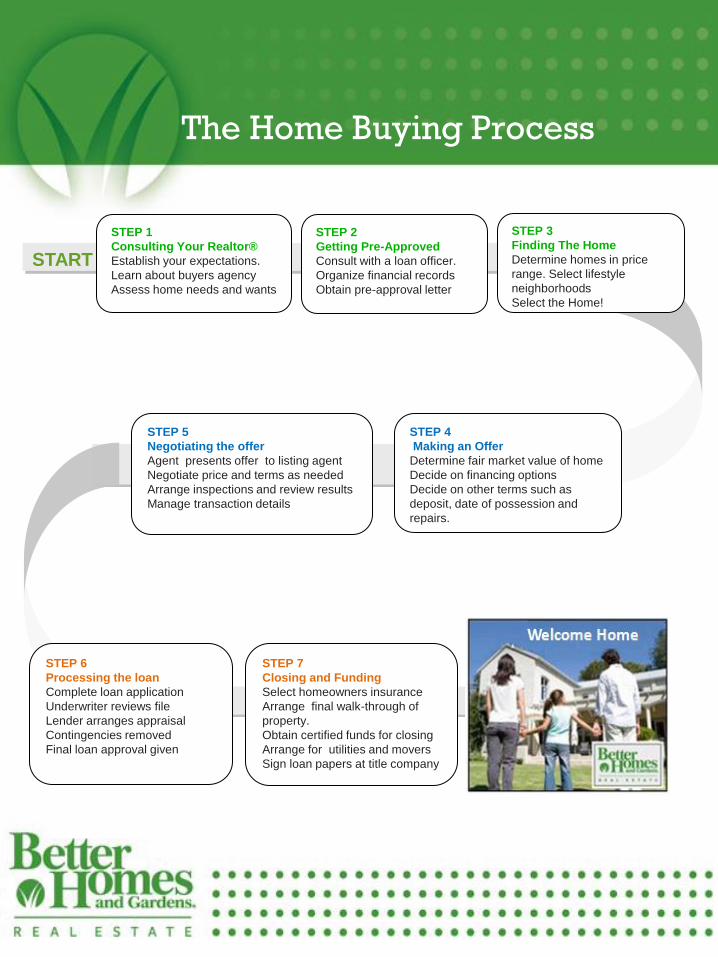

The Home Buying Process

START

STEP 1

Consulting Your Realtor®

Establish your expectations.

Learn about buyers agency

Assess home needs and wants

STEP 2

Getting Pre-Approved

Consult with a loan officer.

Organize financial records

Obtain pre-approval letter

STEP 3

Finding The Home

Determine homes in price

range. Select lifestyle

neighborhoods

Select the Home!

STEP 4

Making an Offer

Determine fair market value of home

Decide on financing options

Decide on other terms such as

deposit, date of possession and

repairs.

STEP 5

Negotiating the offer

Agent presents offer to listing agent

Negotiate price and terms as needed

Arrange inspections and review results

Manage transaction details

STEP 6

Processing the loan

Complete loan application

Underwriter reviews file

Lender arranges appraisal

Contingencies removed

Final loan approval given

STEP 7

Closing and Funding

Select homeowners insurance

Arrange final walk-through of

property.

Obtain certified funds for closing

Arrange for utilities and movers

Sign loan papers at title company

5

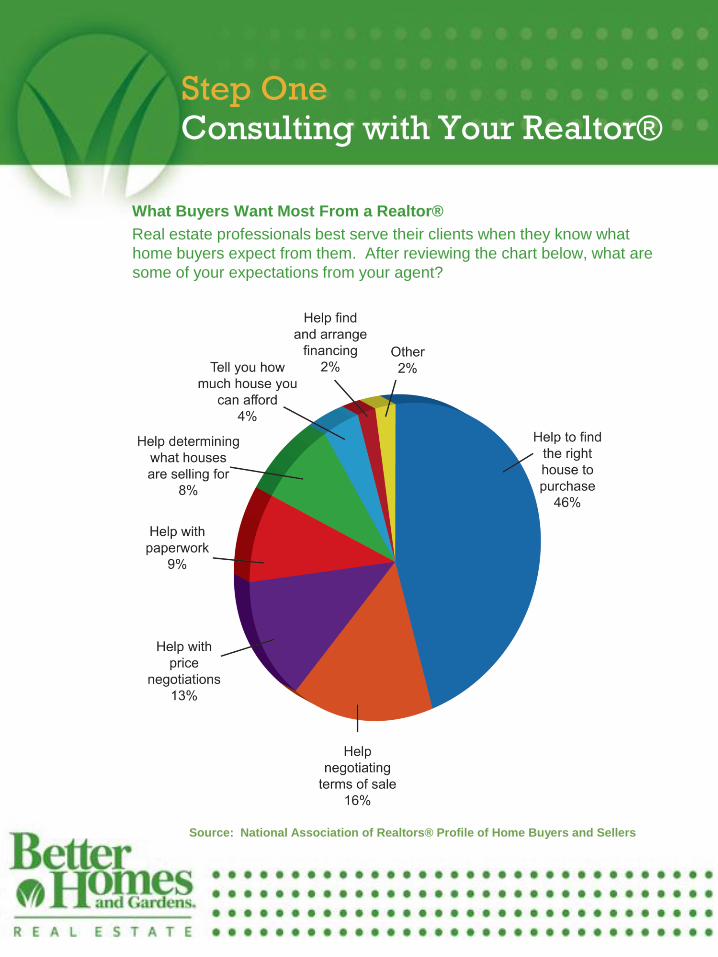

Step One Consulting with Your Realtor®

What Buyers Want Most From a Realtor®

Real estate professionals best serve their clients when they know what

home buyers expect from them. After reviewing the chart below, what are

some of your expectations from your agent?

Source: National Association of Realtors® Profile of Home Buyers and Sellers

6

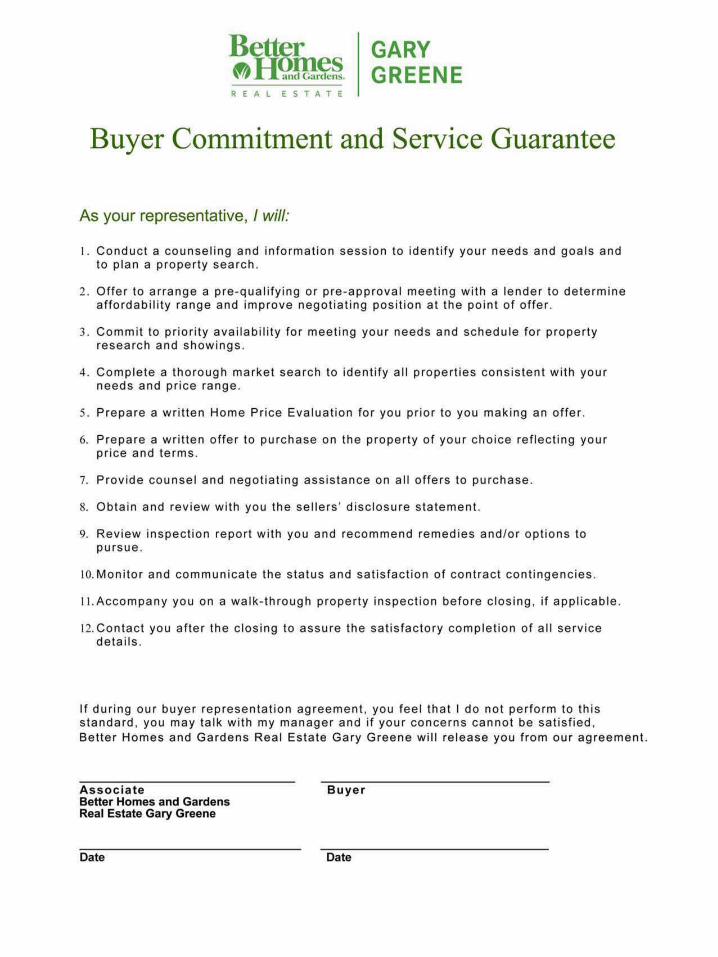

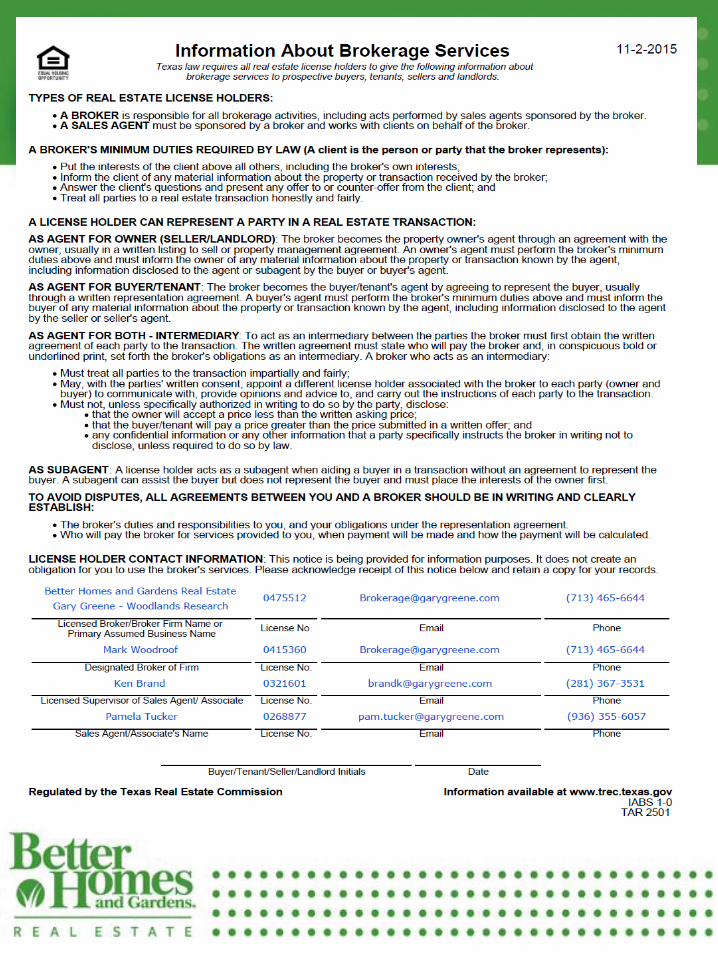

Why Choose Buyer Representation One of the most important services I can perform for you is to represent you in the purchase of your home! My fiduciary duties to you are fully disclosed in a buyer’s representation agreement which I will include under separate cover for you to review. A summary is below.

As your buyers agent, I will be able to:

1. Offer advice and counsel.

2. Show you all the homes listed in the MLS and new construction

3. Show you the market trends and comps surrounding the home you wish to purchase

4.. Most important of all – NEGOTIATE IN YOUR BEHALF

Whether you're a first time buyer or an experienced buyer, it is good to know that your real estate agent has your best interests in mind as you select a home.

I’ve also included for your review, “Information about Brokerage Services” required by law and approved by the Texas Real Estate Commission. The form explains broker representation. As a buyer, please review thoroughly and endorse as verification that you are familiar with the types of representation and understand the parties duties and obligations to each other.

Step One Consulting with Your Realtor®

7

Step One: Consulting with Your Realtor®

Have you looked at any

homes yet?

What did you like about

them?

What didn’t you like?

What would make your new

home a special find?

If you could take one thing

with you from your present

home, what would it be?

8

Step One Consulting with Your Realtor®

Finding the Right Home Finding the right home can be a time consuming process. Answering a few questions ahead of time can help narrow your choice of properties and make the home finding experience a more enjoyable journey.

Housing Information:

Current Address:______________________________________________

Current Commute time(s):_______________________________________

Approximate Value: ___________________Estimated Equity: __________

Down Payment Available: __________Is house currently on market? _____

What is the driving force behind your move? Why are you moving? (Job, family, more space, schools, lifestyle)

_____________________________________________________________

How soon would you like to be in your new home?_____________________

How long do you plan on living in the new home? _____________________

Family Information:

Children/Ages:_________________________________________________

Favorite Activities:______________________________________________

How large is your family likely to grow? _____________________________

Are there any special needs? ____________________________________

9

Step One Consulting with Your Realtor®

Requirements For Your Community: How you live will help determine where you live!

Desired Area(s): ____________________________________________

Will you want to live near work, near schools, near family, near shopping, entertainment, etc. __________________________________________________________

Considering family activities, will community need to be near or have any of the following:

Pool: _________ Golf Course: _________ Waterfront: __________

View: __________Other: _______________________

Requirements For Your Home Purchase:

Price Range: ______________Square feet: _________________________

Age of home: ______________Stories: ____________________________

Bedrooms: ____________(Master up/Down)______ Features: __________

Bathrooms: ___________ Features Required: _______________________

Kitchen Requirements: _____ Garage: _____________________________

What are your top three “Must Have” Features from this page:

1. __________________2. _________________3 ___________________

What would be nice – but do not HAVE to have now: (hardwood floors,

granite, study, pool etc)________________________________________

10

Step Two: Getting Pre-Approval

Have you worked out the details of how you will pay for your new home?

11

Meeting with a Loan Officer

Starting the financing process early will help us make sure we are looking at

homes in the right price range. It will also give you any “heads up” in case

there are some credit issues or anything else in the way of you getting a loan

on the house you want. You can talk with more than one lender. Getting a

pre-approval letter is not an obligation for a loan. A pre-approval will tell you

how much home you can afford, give you the power to negotiate and even

make an offer, and show sellers that you're a qualified buyer.

Step Two: Getting Pre-Approval

The pre-approval process involves:

1. Calculating your income vs. debt ratios

2. Running a credit check.

Pre-approval is different than pre-qualify.

Pre-qualification is an initial step in the loan

process, where your finances are

presented and the loan officer can give you

a guesstimate of the amount of your

purchase power – but there is no analysis

of your credit report or an in-depth study of

your ability to purchase a house.

Organize your personal information

Check with your lender for a complete list, but listed below are a few

items you might want to start gathering for the process:

____ Names, addresses and social security numbers for all borrowers

involved

____ Copies of bank statements, account numbers, names and

addresses of institutions

____ Copies of last 2 months of pay checks

____ Copies of last two years of tax returns

____ Loan numbers, names and addresses of all credit card accounts

____ Contact information for your current mortgage or landlord

____ Information regarding retirement funds, stocks and bonds etc

____ Gather documents such as financial statements and tax forms.

12

Step Three: Finding The Home

Online Tools: I’ll perform an initial search to find homes matching your

criteria and set up an e-mail alert so we’ll be the first to know

when a new listing enters that matches your criteria.

Feel free to use the Lifestyle/Community search on

www.BHGRealestate.com to find the right community – and

let me know which homes you would like to see!

Use our Look tool to find statistics on neighborhoods,

schools, and other demographic information important in

your search for a home. I can send you additional info as

well.

Search for a home:

Allow me to give you a tour of the area(s) you are interested

in. You’ll get a feel for different neighborhoods.

It’s also good to visit your preferred neighborhoods at

different times of the day and on different days of the week

to observe patterns of noise and traffic.

As your buyers agent, I can also show you any “For Sale By

Owner” homes or builder homes that you may see. You will

want someone to represent you in any transaction that

involves the purchase of your home.

13

Step Four: Making the Offer -

Before making the offer – my research on

home values in the area will assist in

determining how much to offer.

Competitive Market Analysis

Recently sold homes

Current competition

Homes that did not sell

Written Offers

Leverage your negotiating power

14

Step Four: Making the Offer

What Makes for a Winning Offer?

1. Offer a Competitive Price Making an offer to purchase involves more than picking a price. We will review comparable properties in the neighborhood that have sold recently and examine the sellers disclosure in detail. Market conditions will dictate the selling price. 2. Make a strong deposit part of your offer You'll want to submit an earnest money deposit when writing an offer, payable to a reputable escrow company, to be delivered by your agent no more than three business days after the acceptance of the offer. Even when delivering an offer below asking price, offer a large deposit if possible, and it will pay dividends in the end. A higher deposit will most likely strengthen your negotiating power.

3. Submit offer with pre-approval letter When an offer is submitted with a pre-approval letter, sellers will know it is serious. Many prefer to negotiate with a pre-approved buyer because they know you are able to obtain the financing needed to close the transaction. Buyers with a pre-approval letter usually have an advantage in cases where there are multiple offers.

4. Understand and adjust to the seller’s interest Asking the right questions prior to writing an offer can often make the difference between an accepted offer and a stalled negotiation. Some contract terms may be of great significance to the seller, whereas only a slight inconvenience for you. Remember that price is not the only negotiating factor in a contract. Other items include: Repairs, home improvements, closing costs and date of possession. 5. Provide an appropriate time for the seller's response Time is of the essence once you decide to take the plunge, especially regarding a newer listing in which the risk is high that other buyers will potentially submit offers. Typically, the seller is given until 5PM on the third day from receipt of the offer to respond, unless you write in a different date and time. If the offer is strong, speed up the response time.

15

Step Five: Negotiating the Offer

I’ll be your advocate during all negotiations

Assist you in strategizing and counter offers

for the best price and terms

Deliver your message clearly and

professionally to the seller and their agent

Keep the seller and their agent moving in a

timely manner

Keep the transaction at arm’s length while

maintaining a professional attitude and

demeanor

16

Step Five: Negotiating the Offer

Negotiating the repairs

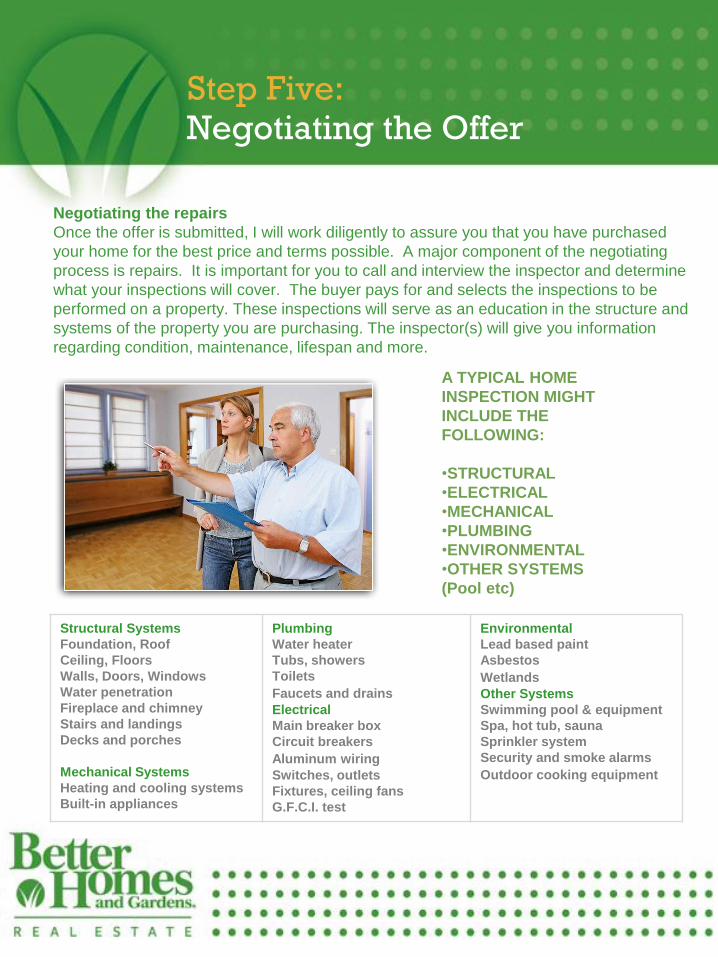

Once the offer is submitted, I will work diligently to assure you that you have purchased

your home for the best price and terms possible. A major component of the negotiating

process is repairs. It is important for you to call and interview the inspector and determine

what your inspections will cover. The buyer pays for and selects the inspections to be

performed on a property. These inspections will serve as an education in the structure and

systems of the property you are purchasing. The inspector(s) will give you information

regarding condition, maintenance, lifespan and more.

A TYPICAL HOME

INSPECTION MIGHT

INCLUDE THE

FOLLOWING:

•STRUCTURAL

•ELECTRICAL

•MECHANICAL

•PLUMBING

•ENVIRONMENTAL

•OTHER SYSTEMS

(Pool etc)

Structural Systems

Foundation, Roof

Ceiling, Floors

Walls, Doors, Windows

Water penetration

Fireplace and chimney

Stairs and landings

Decks and porches

Mechanical Systems

Heating and cooling systems

Built-in appliances

Plumbing

Water heater

Tubs, showers

Toilets

Faucets and drains Electrical

Main breaker box

Circuit breakers

Aluminum wiring Switches, outlets

Fixtures, ceiling fans

G.F.C.I. test

Environmental

Lead based paint

Asbestos

Wetlands Other Systems

Swimming pool & equipment

Spa, hot tub, sauna

Sprinkler system

Security and smoke alarms

Outdoor cooking equipment

17

Step Six: Processing the Loan

It’s important for you to

Submit documentation in a timely manner

Provide lender with additional documents

as required

Stay in touch with the mortgage officer

It’s important for me to

Communicate with the appraiser

Stay in touch with the mortgage officer

18

Step Six: Processing the Loan

Final Loan Approval

Now that you have the seller’s final approval, we need the lender’s final approval.

Final approval means unconditional. All conditions on the loan have been removed.

If there were any conditions on the loan, those conditions have been met. Your

lender will need a copy of the sales contract, and information on access to the

property for the appraisal.

After the appraisal, and verification of clear title from the title company, final

approval will be given:

#1. There are no liens on the house

#2. The house appraised at a value equal to or greater than the agreed upon sales

amount

Your lender should also be providing you with an expectation of payment and

closing costs. Your house payment has four components:

Principal and Interest $ __________________

Taxes $ __________________

Homeowners Insurance $ __________________

(PMI) Private Mortgage Insurance $ __________________

(if down payment less than 20%)

TOTAL ESTIMATED MONTHLY PAYMENT:$ __________________

19

Step Seven: Closing

Just before settlement, we will make one last inspection of the property to

ensure that the home is in the condition we expect.

Your loan officer should provide you with an estimate of closing costs broken down as

provided in the sample below. You will need this information because you will have to

bring certified funds for down payment and closing costs the day of closing. You

should verify the estimate is correct before arranging for funds. They will send you a

more detailed list.

Purchase Price of home $ _____________

Down Payment $ _____________

Amount Financed $ _____________

Estimated Closing Costs $ _____________

(Title fees, Settlement fees Recording fees, loan

origination fees etc)

Prior to closing:

___Arrange for Homeowners Insurance

___Arrange for a Home Warranty (optional)

___Arrange for change of utilities (recommend

start date same day as closing)

___Arrange for movers

___Arrange for change of address

At closing you will:

Sign documents

The loan will be funded

Title will be recorded

And you will get KEYS TO YOUR NEW

HOUSE!

20

Checklist for Moving

CHECKLIST FOR MOVING

1. Contact and arrange for a reputable moving company.

2. Check with your accountant or relocation company to see if any moving expenses will be deductible.

3. Arrange to have school records transferred.

4. Arrange to transfer any medical or dental records if needed

5. Arrange for homeowners insurance.

6. Obtain change-of-address cards from the post office. Send after final loan approval and walk through

7. Arrange for change of utilities

8. Separate important financial and personal records. Do not include them with your personal belongings in the move.

9. Pack an extra supply of medications (if moving out of town)

AFTER MOVE:

1. Arrange for transfer of vehicle licenses and driver’s licenses.

2. Read the “Make It Your Own Series” on www.BHGRealestate.com and have fun decorating, landscaping and making it your own!

.

21

Moving Tips

Moving with Young Children Are you excited and happy about moving? Or are you dreading the sorting, packing and other chores?

If you look at moving as an exciting adventure full of fun, new possibilities, then you’re halfway to getting your children on board for the ride. Your children will absorb your enthusiasm like little sponges.

– There will be some worries, of course, but you can defeat those with a little preparation and understanding.

– Most children don’t like the changes associated with moving. The younger the child, the less able they are to "see into the future" as you do. They tend to focus on losing the security they’re used to, and they worry about missing friends and family.

– You can make childish anger and doubt grow into a sense of wonder and adventure. You can do that by acknowledging and empathizing with the loss they feel and showing them how to balance their feelings with what they have to gain.

1. Communicate with your child patiently and frequently. Let your children know, step by step, what is happening and what is likely to happen next. Tell them what the move means to the family ……

2. List all the advantages there are for the child in the move. For example, will the family be closer to Grandma, the ocean, or another favorite person, place, or activity? Will they be able to see old friends and family frequently? Or at least at holiday time?

3. Show the child as much as you can about the new home. When you show your child their room, bath, and play area, make a game of it by asking where certain favorite toys or furniture should go. Have fun by showing your child the new house plans, or draw them yourself and let your child cut out furniture and toys to place in the rooms.

4. Introduce your child to the new community online. Draw a map, and show how close Mommy and Daddy work, where schools are, where Aunt Bea lives, and other points of interest to help them orient themselves in their new surroundings.

5. Be ready for those "What about me?" questions. If your child is in scouts, little league, or other organizations, contact those associations for referrals in your new neighborhood or city. Knowing they won't have to give up favorite hobbies or sports goes a long way toward helping children adjust.

6. Let your child participate. Make a fun activity out of researching services you’ll need online, like finding a new veterinarian for your dog. Older children can find blogs online about their new school.

7. Keep your child occupied by letting them plan and pack a box or two of their special things. Consider their input on new decor and the layout of their new rooms. Encourage them to take the time to exchange good-byes and contact information with friends..

8. Try to stick to normal routines as much as possible. Let your children know that, although they will soon live in a new house, the rules of the household will still be the same. Bedtime is still at 9 p.m., and homework must still be completed before TV time is allowed.

9. On moving day, have a bag packed of personal belongings for each member of the family, being careful to include medications, clothes, and personal items. Let your children choose what amusements and favorite "loveys" they wish to take along, and reassure them they will see their other favorite toys when they arrive in their new home. Your preparedness will go a long way in reassuring your children that their needs are being considered, even while big changes are happening around.

22

My Professional Experience

My Philosophy

You can get anything you want in life if

you’ll just help enough other people get

where they want to go.

My Credentials

Bachelor’s of Business Administration (BBA)

Cartus/Affinity Relocation Certified Specialist

Graduate Real Estate Institute (GRI)

Master Certified Negotiation Expert (MCNE)

Seller Representative Specialist (SRS)

Senior Real Estate Specialist (SRES)

My Background

Originally licensed in 1979, I’ve lived in the area for over 25

years. After obtaining a BBA in Business Administration, and

retiring from state service, I’ve returned to the market,

specializing in residential services.

Replace

h

Your

Photo

23

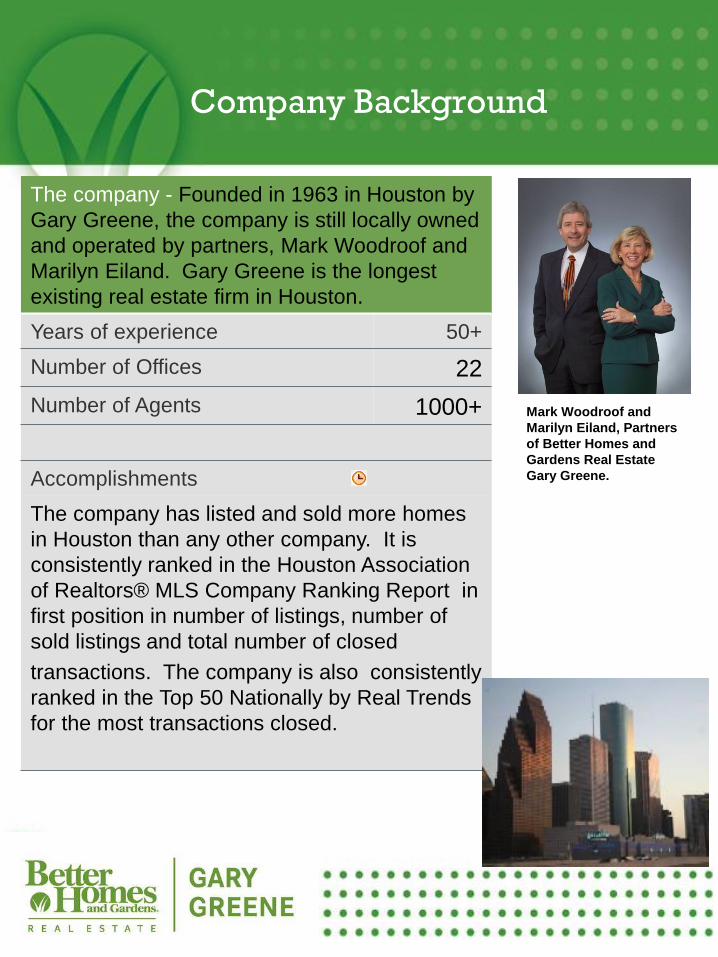

Company Background

The company - Founded in 1963 in Houston by

Gary Greene, the company is still locally owned

and operated by partners, Mark Woodroof and

Marilyn Eiland. Gary Greene is the longest

existing real estate firm in Houston.

Years of experience 50+

Number of Offices 22

Number of Agents 1000+

Accomplishments

The company has listed and sold more homes

in Houston than any other company. It is

consistently ranked in the Houston Association

of Realtors® MLS Company Ranking Report in

first position in number of listings, number of

sold listings and total number of closed

transactions. The company is also consistently

ranked in the Top 50 Nationally by Real Trends

for the most transactions closed.

Mark Woodroof and

Marilyn Eiland, Partners

of Better Homes and

Gardens Real Estate

Gary Greene.

24

25

Building Relationships for Life

Call on me at any time

Tell your friends and colleagues

about the service you received

26