homogenization and other multi-scale problems in...

TRANSCRIPT

Homogenization and other multi-scale problemsin Bellman-Isaacs equations

Martino Bardi

Dipartimento di Matemetica Pura ed ApplicataUniversità di Padova

New Trends in Analysis and Control of Nonlinear PDEsRoma, June 13–15, 2011

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 1 / 29

Plan

1 Homogenization of non-coercive Hamilton–Jacobi equations(joint work with G. Terrone)

I Some previous results

I Examples of non-homogenization

I Homogenization on subspaces

I Convex-concave eikonal equations and differential games

2 Optimal control with stochastic volatility(joint work with A. Cesaroni and L. Manca)

I Motivation: financial models

I Singular perturbations of H-J-B equations

I Merton portfolio optimization with stochastic volatility

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 2 / 29

Plan

1 Homogenization of non-coercive Hamilton–Jacobi equations(joint work with G. Terrone)

I Some previous results

I Examples of non-homogenization

I Homogenization on subspaces

I Convex-concave eikonal equations and differential games

2 Optimal control with stochastic volatility(joint work with A. Cesaroni and L. Manca)

I Motivation: financial models

I Singular perturbations of H-J-B equations

I Merton portfolio optimization with stochastic volatility

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 2 / 29

1. Homogenization of Hamilton–Jacobi Equations

Problem: let ε → 0+ in

uεt + H

(x , x

ε , Duε)

= 0 in (0, T )× RN

uε(0, x) = h(x , x

ε

).

ZN− periodic case:

H(x , ξ + k , p) = H(x , ξ, p), h(x , ξ + k) = h(x , ξ) ∀k ∈ ZN .

Goal: find continuous effective Hamiltonian and initial data H, h s.t.

uε → u locally uniformly, and u solves

ut + H (x , Du) = 0 in (0, T )× RN

u(0, x) = h (x) .

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 3 / 29

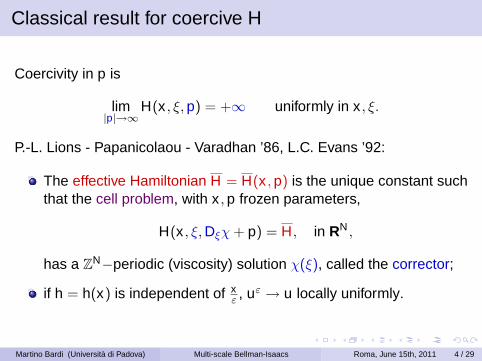

Classical result for coercive H

Coercivity in p is

lim|p|→∞

H(x , ξ, p) = +∞ uniformly in x , ξ.

P.-L. Lions - Papanicolaou - Varadhan ’86, L.C. Evans ’92:

The effective Hamiltonian H = H(x , p) is the unique constant suchthat the cell problem, with x , p frozen parameters,

H(x , ξ, Dξχ + p) = H, in RN ,

has a ZN−periodic (viscosity) solution χ(ξ), called the corrector;

if h = h(x) is independent of xε , uε → u locally uniformly.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 4 / 29

Classical result for coercive H

Coercivity in p is

lim|p|→∞

H(x , ξ, p) = +∞ uniformly in x , ξ.

P.-L. Lions - Papanicolaou - Varadhan ’86, L.C. Evans ’92:

The effective Hamiltonian H = H(x , p) is the unique constant suchthat the cell problem, with x , p frozen parameters,

H(x , ξ, Dξχ + p) = H, in RN ,

has a ZN−periodic (viscosity) solution χ(ξ), called the corrector;

if h = h(x) is independent of xε , uε → u locally uniformly.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 4 / 29

Classical result for coercive H

Coercivity in p is

lim|p|→∞

H(x , ξ, p) = +∞ uniformly in x , ξ.

P.-L. Lions - Papanicolaou - Varadhan ’86, L.C. Evans ’92:

The effective Hamiltonian H = H(x , p) is the unique constant suchthat the cell problem, with x , p frozen parameters,

H(x , ξ, Dξχ + p) = H, in RN ,

has a ZN−periodic (viscosity) solution χ(ξ), called the corrector;

if h = h(x) is independent of xε , uε → u locally uniformly.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 4 / 29

The effective initial data

If the initial data h = h(x , xε ) must find the initial condition h(x).

O. Alvarez - M. B. (ARMA ’03):Assume there exists the recession function of H

H ′(x , ξ, p) := limλ→+∞

H(x , ξ, λp)

λ.

Consider, for frozen x , wt + H ′(x , ξ, Dξw) = 0, w(0, ξ) = h(x , ξ).

If limt→+∞ w(t , ξ) = constant =: h(x),

then limt→0 limε→0 uε = h(x).

In the coercive case h (x) = minξh(x , ξ).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 5 / 29

The effective initial data

If the initial data h = h(x , xε ) must find the initial condition h(x).

O. Alvarez - M. B. (ARMA ’03):Assume there exists the recession function of H

H ′(x , ξ, p) := limλ→+∞

H(x , ξ, λp)

λ.

Consider, for frozen x , wt + H ′(x , ξ, Dξw) = 0, w(0, ξ) = h(x , ξ).

If limt→+∞ w(t , ξ) = constant =: h(x),

then limt→0 limε→0 uε = h(x).

In the coercive case h (x) = minξh(x , ξ).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 5 / 29

The effective initial data

If the initial data h = h(x , xε ) must find the initial condition h(x).

O. Alvarez - M. B. (ARMA ’03):Assume there exists the recession function of H

H ′(x , ξ, p) := limλ→+∞

H(x , ξ, λp)

λ.

Consider, for frozen x , wt + H ′(x , ξ, Dξw) = 0, w(0, ξ) = h(x , ξ).

If limt→+∞ w(t , ξ) = constant =: h(x),

then limt→0 limε→0 uε = h(x).

In the coercive case h (x) = minξh(x , ξ).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 5 / 29

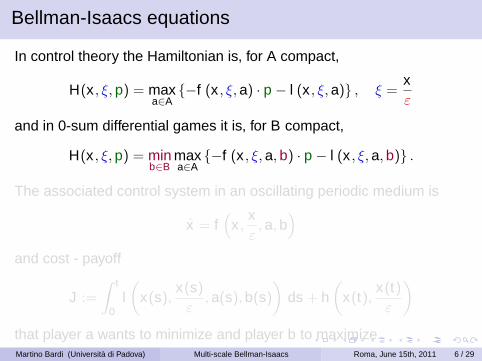

Bellman-Isaacs equations

In control theory the Hamiltonian is, for A compact,

H(x , ξ, p) = maxa∈A

{−f (x , ξ, a) · p − l (x , ξ, a)} , ξ =xε

and in 0-sum differential games it is, for B compact,

H(x , ξ, p) = minb∈B

maxa∈A

{−f (x , ξ, a, b) · p − l (x , ξ, a, b)} .

The associated control system in an oscillating periodic medium is

x = f(

x ,xε, a, b

)and cost - payoff

J :=

∫ t

0l(

x(s),x(s)

ε, a(s), b(s)

)ds + h

(x(t),

x(t)ε

)that player a wants to minimize and player b to maximize.Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 6 / 29

Bellman-Isaacs equations

In control theory the Hamiltonian is, for A compact,

H(x , ξ, p) = maxa∈A

{−f (x , ξ, a) · p − l (x , ξ, a)} , ξ =xε

and in 0-sum differential games it is, for B compact,

H(x , ξ, p) = minb∈B

maxa∈A

{−f (x , ξ, a, b) · p − l (x , ξ, a, b)} .

The associated control system in an oscillating periodic medium is

x = f(

x ,xε, a, b

)and cost - payoff

J :=

∫ t

0l(

x(s),x(s)

ε, a(s), b(s)

)ds + h

(x(t),

x(t)ε

)that player a wants to minimize and player b to maximize.Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 6 / 29

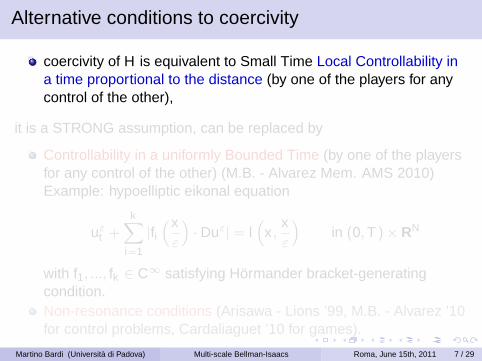

Alternative conditions to coercivity

coercivity of H is equivalent to Small Time Local Controllability ina time proportional to the distance (by one of the players for anycontrol of the other),

it is a STRONG assumption, can be replaced by

Controllability in a uniformly Bounded Time (by one of the playersfor any control of the other) (M.B. - Alvarez Mem. AMS 2010)Example: hypoelliptic eikonal equation

uεt +

k∑i=1

|fi(x

ε

)· Duε| = l

(x ,

xε

)in (0, T )× RN

with f1, ..., fk ∈ C∞ satisfying Hörmander bracket-generatingcondition.Non-resonance conditions (Arisawa - Lions ’99, M.B. - Alvarez ’10for control problems, Cardaliaguet ’10 for games).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 7 / 29

Alternative conditions to coercivity

coercivity of H is equivalent to Small Time Local Controllability ina time proportional to the distance (by one of the players for anycontrol of the other),

it is a STRONG assumption, can be replaced by

Controllability in a uniformly Bounded Time (by one of the playersfor any control of the other) (M.B. - Alvarez Mem. AMS 2010)Example: hypoelliptic eikonal equation

uεt +

k∑i=1

|fi(x

ε

)· Duε| = l

(x ,

xε

)in (0, T )× RN

with f1, ..., fk ∈ C∞ satisfying Hörmander bracket-generatingcondition.Non-resonance conditions (Arisawa - Lions ’99, M.B. - Alvarez ’10for control problems, Cardaliaguet ’10 for games).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 7 / 29

Alternative conditions to coercivity

coercivity of H is equivalent to Small Time Local Controllability ina time proportional to the distance (by one of the players for anycontrol of the other),

it is a STRONG assumption, can be replaced by

Controllability in a uniformly Bounded Time (by one of the playersfor any control of the other) (M.B. - Alvarez Mem. AMS 2010)Example: hypoelliptic eikonal equation

uεt +

k∑i=1

|fi(x

ε

)· Duε| = l

(x ,

xε

)in (0, T )× RN

with f1, ..., fk ∈ C∞ satisfying Hörmander bracket-generatingcondition.Non-resonance conditions (Arisawa - Lions ’99, M.B. - Alvarez ’10for control problems, Cardaliaguet ’10 for games).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 7 / 29

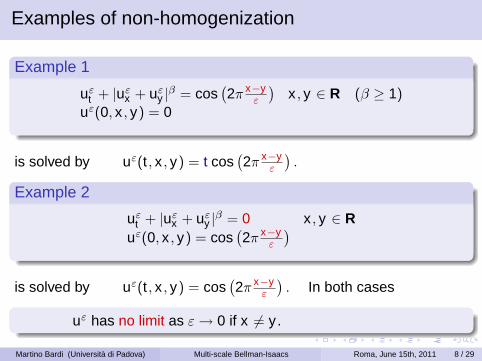

Examples of non-homogenization

Example 1

uεt + |uε

x + uεy |β = cos

(2π x−y

ε

)x , y ∈ R (β ≥ 1)

uε(0, x , y) = 0

is solved by uε(t , x , y) = t cos(2π x−y

ε

).

Example 2

uεt + |uε

x + uεy |β = 0 x , y ∈ R

uε(0, x , y) = cos(2π x−y

ε

)is solved by uε(t , x , y) = cos

(2π x−y

ε

). In both cases

uε has no limit as ε → 0 if x 6= y .

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 8 / 29

Example 3

uεt + |uε

x | − |uεy | = cos

(2π x−y

ε

)x , y ∈ R

uε(0, x , y) = 0

is solved by uε(t , x , y) = t cos(2π x−y

ε

).

Example 4

uεt + |uε

x | − |uεy | = 0 x , y ∈ R

uε(0, x , y) =(2π x−y

ε

)is solved by uε(t , x , y) = cos

(2π x−y

ε

).

Again

uε has no limit as ε → 0 if x 6= y .

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 9 / 29

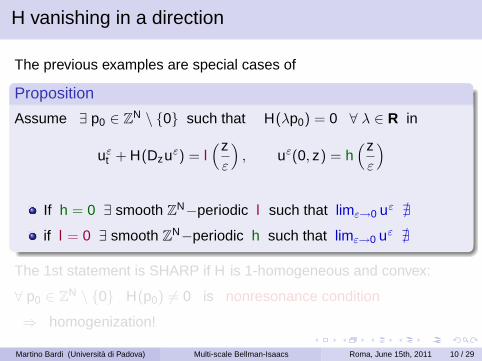

H vanishing in a direction

The previous examples are special cases of

Proposition

Assume ∃ p0 ∈ ZN \ {0} such that H(λp0) = 0 ∀ λ ∈ R in

uεt + H(Dzuε) = l

(zε

), uε(0, z) = h

(zε

)

If h = 0 ∃ smooth ZN−periodic l such that limε→0 uε @

if l = 0 ∃ smooth ZN−periodic h such that limε→0 uε @

The 1st statement is SHARP if H is 1-homogeneous and convex:

∀ p0 ∈ ZN \ {0} H(p0) 6= 0 is nonresonance condition

⇒ homogenization!

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 10 / 29

H vanishing in a direction

The previous examples are special cases of

Proposition

Assume ∃ p0 ∈ ZN \ {0} such that H(λp0) = 0 ∀ λ ∈ R in

uεt + H(Dzuε) = l

(zε

), uε(0, z) = h

(zε

)

If h = 0 ∃ smooth ZN−periodic l such that limε→0 uε @

if l = 0 ∃ smooth ZN−periodic h such that limε→0 uε @

The 1st statement is SHARP if H is 1-homogeneous and convex:

∀ p0 ∈ ZN \ {0} H(p0) 6= 0 is nonresonance condition

⇒ homogenization!

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 10 / 29

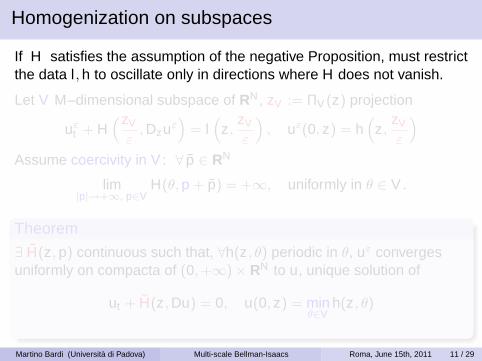

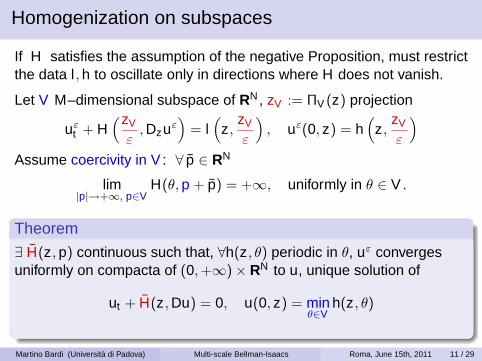

Homogenization on subspaces

If H satisfies the assumption of the negative Proposition, must restrictthe data l , h to oscillate only in directions where H does not vanish.

Let V M–dimensional subspace of RN , zV := ΠV (z) projection

uεt + H

(zV

ε, Dzuε

)= l(

z,zV

ε

), uε(0, z) = h

(z,

zV

ε

)Assume coercivity in V : ∀ p ∈ RN

lim|p|→+∞, p∈V

H(θ, p + p) = +∞, uniformly in θ ∈ V .

Theorem

∃ H(z, p) continuous such that, ∀h(z, θ) periodic in θ, uε convergesuniformly on compacta of (0,+∞)× RN to u, unique solution of

ut + H(z, Du) = 0, u(0, z) = minθ∈V

h(z, θ)

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 11 / 29

Homogenization on subspaces

If H satisfies the assumption of the negative Proposition, must restrictthe data l , h to oscillate only in directions where H does not vanish.

Let V M–dimensional subspace of RN , zV := ΠV (z) projection

uεt + H

(zV

ε, Dzuε

)= l(

z,zV

ε

), uε(0, z) = h

(z,

zV

ε

)Assume coercivity in V : ∀ p ∈ RN

lim|p|→+∞, p∈V

H(θ, p + p) = +∞, uniformly in θ ∈ V .

Theorem

∃ H(z, p) continuous such that, ∀h(z, θ) periodic in θ, uε convergesuniformly on compacta of (0,+∞)× RN to u, unique solution of

ut + H(z, Du) = 0, u(0, z) = minθ∈V

h(z, θ)

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 11 / 29

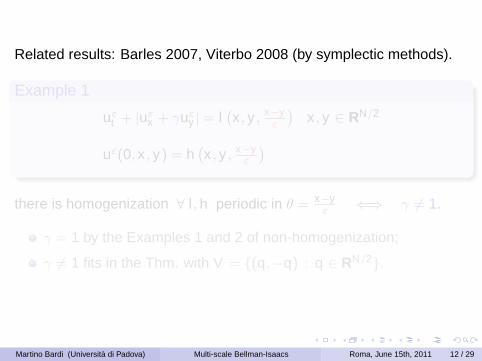

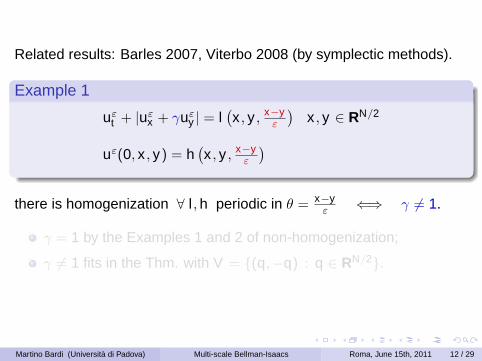

Related results: Barles 2007, Viterbo 2008 (by symplectic methods).

Example 1

uεt + |uε

x + γuεy | = l

(x , y , x−y

ε

)x , y ∈ RN/2

uε(0, x , y) = h(x , y , x−y

ε

)there is homogenization ∀ l , h periodic in θ = x−y

ε ⇐⇒ γ 6= 1.

γ = 1 by the Examples 1 and 2 of non-homogenization;

γ 6= 1 fits in the Thm. with V = {(q,−q) : q ∈ RN/2}.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 12 / 29

Related results: Barles 2007, Viterbo 2008 (by symplectic methods).

Example 1

uεt + |uε

x + γuεy | = l

(x , y , x−y

ε

)x , y ∈ RN/2

uε(0, x , y) = h(x , y , x−y

ε

)there is homogenization ∀ l , h periodic in θ = x−y

ε ⇐⇒ γ 6= 1.

γ = 1 by the Examples 1 and 2 of non-homogenization;

γ 6= 1 fits in the Thm. with V = {(q,−q) : q ∈ RN/2}.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 12 / 29

Related results: Barles 2007, Viterbo 2008 (by symplectic methods).

Example 1

uεt + |uε

x + γuεy | = l

(x , y , x−y

ε

)x , y ∈ RN/2

uε(0, x , y) = h(x , y , x−y

ε

)there is homogenization ∀ l , h periodic in θ = x−y

ε ⇐⇒ γ 6= 1.

γ = 1 by the Examples 1 and 2 of non-homogenization;

γ 6= 1 fits in the Thm. with V = {(q,−q) : q ∈ RN/2}.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 12 / 29

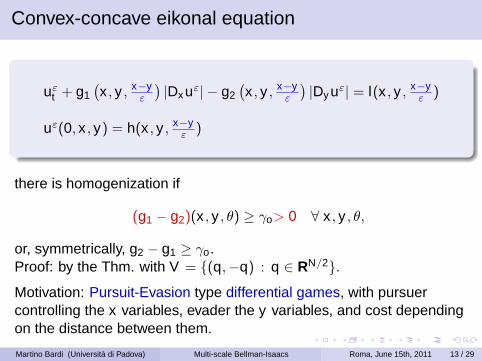

Convex-concave eikonal equation

uεt + g1

(x , y , x−y

ε

)|Dxuε| − g2

(x , y , x−y

ε

)|Dyuε| = l(x , y , x−y

ε )

uε(0, x , y) = h(x , y , x−yε )

there is homogenization if

(g1 − g2)(x , y , θ) ≥ γo> 0 ∀ x , y , θ,

or, symmetrically, g2 − g1 ≥ γo.Proof: by the Thm. with V = {(q,−q) : q ∈ RN/2}.

Motivation: Pursuit-Evasion type differential games, with pursuercontrolling the x variables, evader the y variables, and cost dependingon the distance between them.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 13 / 29

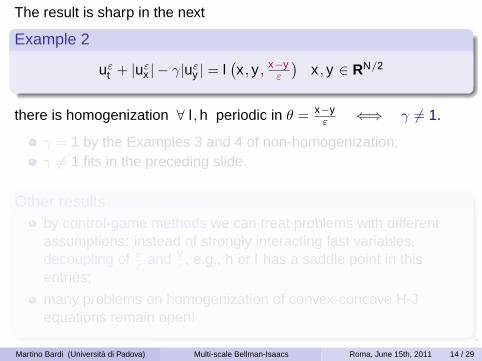

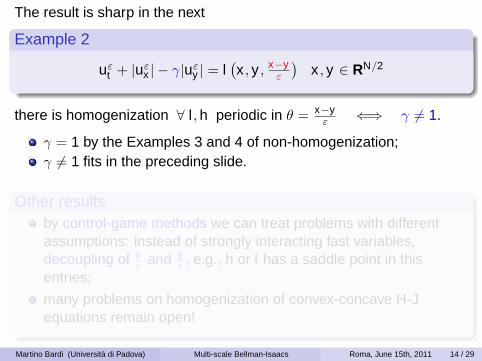

The result is sharp in the next

Example 2

uεt + |uε

x | − γ|uεy | = l

(x , y , x−y

ε

)x , y ∈ RN/2

there is homogenization ∀ l , h periodic in θ = x−yε ⇐⇒ γ 6= 1.

γ = 1 by the Examples 3 and 4 of non-homogenization;γ 6= 1 fits in the preceding slide.

Other resultsby control-game methods we can treat problems with differentassumptions: instead of strongly interacting fast variables,decoupling of x

ε and yε , e.g., h or l has a saddle point in this

entries;

many problems on homogenization of convex-concave H-Jequations remain open!

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 14 / 29

The result is sharp in the next

Example 2

uεt + |uε

x | − γ|uεy | = l

(x , y , x−y

ε

)x , y ∈ RN/2

there is homogenization ∀ l , h periodic in θ = x−yε ⇐⇒ γ 6= 1.

γ = 1 by the Examples 3 and 4 of non-homogenization;γ 6= 1 fits in the preceding slide.

Other resultsby control-game methods we can treat problems with differentassumptions: instead of strongly interacting fast variables,decoupling of x

ε and yε , e.g., h or l has a saddle point in this

entries;

many problems on homogenization of convex-concave H-Jequations remain open!

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 14 / 29

The result is sharp in the next

Example 2

uεt + |uε

x | − γ|uεy | = l

(x , y , x−y

ε

)x , y ∈ RN/2

there is homogenization ∀ l , h periodic in θ = x−yε ⇐⇒ γ 6= 1.

γ = 1 by the Examples 3 and 4 of non-homogenization;γ 6= 1 fits in the preceding slide.

Other resultsby control-game methods we can treat problems with differentassumptions: instead of strongly interacting fast variables,decoupling of x

ε and yε , e.g., h or l has a saddle point in this

entries;

many problems on homogenization of convex-concave H-Jequations remain open!

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 14 / 29

2. Optimal control with stochastic volatility

In Financial Mathematics the evolution of a stock S is described by

d log Ss = γ ds + σ dWs

and the classical Black-Scholes formula for the option pricing problemis derived assuming the parameters are constants.

However the volatility σ is not really a constant, it rather looks like anergodic mean-reverting stochastic process, so it is often modeled asσ(ys) with ys an Ornstein-Uhlenbeck diffusion process.It is argued in the book

Fouque, Papanicolaou, Sircar: Derivatives in financial markets withstochastic volatility, 2000,

that the process ys also evolves on a faster time scale than the stockprices. Next picture shows the typical bursty behavior.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 15 / 29

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 16 / 29

The model with fast stochastic volatility σ proposed in [FPS] is

d log Ss = γ ds + σ(ys) dWs

dys = 1ε (m − ys) + ν√

εdWs

For the option pricing problem the limit is given by the Black-Scholesformula of the model with (constant) mean historical volatility

d log Ss = γ ds + σ dWs, σ2 =

∫R

σ2(y)e−(y−m)2/2ν2

√2πν2

dy ,

the mean being w.r.t. the (Gaussian) invariant measure of theOrnstein-Uhlenbeck process driving ys.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 17 / 29

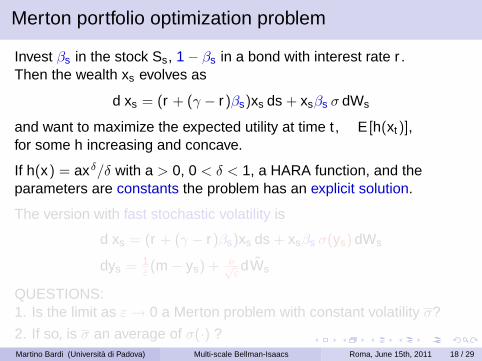

Merton portfolio optimization problem

Invest βs in the stock Ss, 1− βs in a bond with interest rate r .Then the wealth xs evolves as

d xs = (r + (γ − r)βs)xs ds + xsβs σ dWs

and want to maximize the expected utility at time t , E [h(xt)],for some h increasing and concave.

If h(x) = axδ/δ with a > 0, 0 < δ < 1, a HARA function, and theparameters are constants the problem has an explicit solution.

The version with fast stochastic volatility is

d xs = (r + (γ − r)βs)xs ds + xsβs σ(ys) dWs

dys = 1ε (m − ys) + ν√

εdWs

QUESTIONS:1. Is the limit as ε → 0 a Merton problem with constant volatility σ?

2. If so, is σ an average of σ(·) ?Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 18 / 29

Merton portfolio optimization problem

Invest βs in the stock Ss, 1− βs in a bond with interest rate r .Then the wealth xs evolves as

d xs = (r + (γ − r)βs)xs ds + xsβs σ dWs

and want to maximize the expected utility at time t , E [h(xt)],for some h increasing and concave.

If h(x) = axδ/δ with a > 0, 0 < δ < 1, a HARA function, and theparameters are constants the problem has an explicit solution.

The version with fast stochastic volatility is

d xs = (r + (γ − r)βs)xs ds + xsβs σ(ys) dWs

dys = 1ε (m − ys) + ν√

εdWs

QUESTIONS:1. Is the limit as ε → 0 a Merton problem with constant volatility σ?

2. If so, is σ an average of σ(·) ?Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 18 / 29

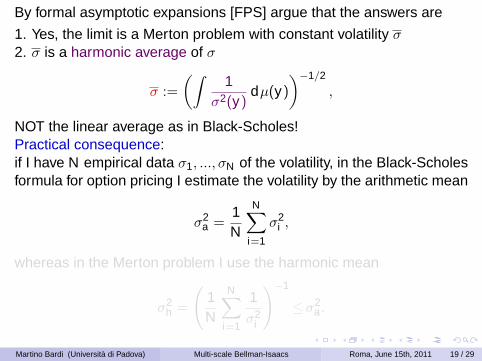

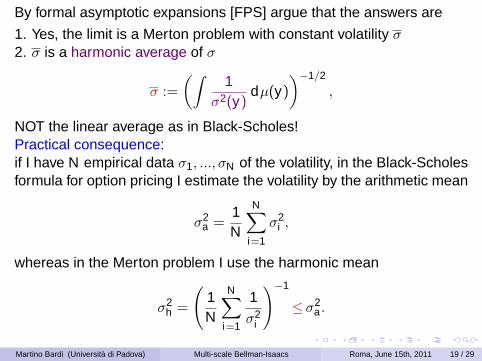

By formal asymptotic expansions [FPS] argue that the answers are

1. Yes, the limit is a Merton problem with constant volatility σ2. σ is a harmonic average of σ

σ :=

(∫1

σ2(y)dµ(y)

)−1/2

,

NOT the linear average as in Black-Scholes!Practical consequence:if I have N empirical data σ1, ..., σN of the volatility, in the Black-Scholesformula for option pricing I estimate the volatility by the arithmetic mean

σ2a =

1N

N∑i=1

σ2i ,

whereas in the Merton problem I use the harmonic mean

σ2h =

(1N

N∑i=1

1σ2

i

)−1

≤σ2a.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 19 / 29

By formal asymptotic expansions [FPS] argue that the answers are

1. Yes, the limit is a Merton problem with constant volatility σ2. σ is a harmonic average of σ

σ :=

(∫1

σ2(y)dµ(y)

)−1/2

,

NOT the linear average as in Black-Scholes!Practical consequence:if I have N empirical data σ1, ..., σN of the volatility, in the Black-Scholesformula for option pricing I estimate the volatility by the arithmetic mean

σ2a =

1N

N∑i=1

σ2i ,

whereas in the Merton problem I use the harmonic mean

σ2h =

(1N

N∑i=1

1σ2

i

)−1

≤σ2a.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 19 / 29

By formal asymptotic expansions [FPS] argue that the answers are

1. Yes, the limit is a Merton problem with constant volatility σ2. σ is a harmonic average of σ

σ :=

(∫1

σ2(y)dµ(y)

)−1/2

,

NOT the linear average as in Black-Scholes!Practical consequence:if I have N empirical data σ1, ..., σN of the volatility, in the Black-Scholesformula for option pricing I estimate the volatility by the arithmetic mean

σ2a =

1N

N∑i=1

σ2i ,

whereas in the Merton problem I use the harmonic mean

σ2h =

(1N

N∑i=1

1σ2

i

)−1

≤σ2a.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 19 / 29

Conclusion: the correct average seems to depend on the problem!

QUESTIONS:

Why?

Can the formula for the Merton problem be rigorously justified andwhat is the convergence as ε → 0?

Is there a unified "formula" for the two problems and for othersimilar problems?

Note: the Black-Scholes model has no control, the associated PDE isa heat-type linear equation;

Merton is a stochastic control problem whose Hamilton-Jacobi-Bellmanequation is fully nonlinear and degenerate parabolic.

I’ll present a result on two-scale Hamilton-Jacobi-Bellman equationsthat will answer these (and other) questions.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 20 / 29

The H-J approach to Singular Perturbations

Control system

dxs = f (xs, ys, αs) ds + σ(xs, ys, αs) dWs, xs ∈ Rn, αs ∈ A,

dys = 1ε g(xs, ys) ds + 1√

εν(xs, ys) dWs, ys ∈ Rm,

x0 = x , y0 = y

Cost functional Jε(t , x , y , α) :=∫ t

0 l(xs, ys, αs) ds + h(xt , yt)

Value function

uε(t , x , y) := infα∈A(t)

E [Jε(t , x , y , α)]

A(t) admisible controls on [0, t ].

GOAL: let ε → 0 and find a simplified model.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 21 / 29

The H-J approach to Singular Perturbations

Control system

dxs = f (xs, ys, αs) ds + σ(xs, ys, αs) dWs, xs ∈ Rn, αs ∈ A,

dys = 1ε g(xs, ys) ds + 1√

εν(xs, ys) dWs, ys ∈ Rm,

x0 = x , y0 = y

Cost functional Jε(t , x , y , α) :=∫ t

0 l(xs, ys, αs) ds + h(xt , yt)

Value function

uε(t , x , y) := infα∈A(t)

E [Jε(t , x , y , α)]

A(t) admisible controls on [0, t ].

GOAL: let ε → 0 and find a simplified model.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 21 / 29

Assumptions on data:

h continuous, supy h(x , y) ≤ K (1 + |x |2)

f , σ, g, τ, l Lipschitz in (x , y) (unif. in α) with linear growth

Then uε solves the HJB equation

∂uε

∂t+H

(x , y , Dxuε, D2

xxuε,1√ε

D2xyuε

)− 1

εLuε = 0 in R+×Rn ×Rm,

H (x , y , p, M, Z ) := maxa∈A

{−tr(σσT M)− f · p − l − tr(σνZ T )

}L := tr(ννT D2

yy ) + g · Dy .

Theorem (Da Lio - Ley). The value function uε is the unique viscositysolution with growth uε(t , x , y) ≤ C(1 + |x |2 + |y |2) of the Cauchyproblem with initial condition

uε(0, x , y) = h(x , y).

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 22 / 29

Next assume on the linear operator L

Ellipticity: ∃Λ(y) > 0 s.t. ∀ x ν(x , y)νT (x , y) ≥ Λ(y)I

Lyapunov: ∃w ∈ C(Rm), k > 0, R0 > 0 s.t.−Lw ≥ k for |y | > R0, ∀x ,

w(y) → +∞ as |y | → +∞.

Then,

the fast subsystem rescaled by τ = s/ε and with x ∈ Rn frozen

(FS) dyτ = g(x , yτ ) dτ + ν(x , yτ ) dWτ ,

is uniquely ergodic, i.e., has a unique invariant measure µx .

Liouville property:any bounded subsolution of −Lv = 0 is constant.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 23 / 29

Next assume on the linear operator L

Ellipticity: ∃Λ(y) > 0 s.t. ∀ x ν(x , y)νT (x , y) ≥ Λ(y)I

Lyapunov: ∃w ∈ C(Rm), k > 0, R0 > 0 s.t.−Lw ≥ k for |y | > R0, ∀x ,

w(y) → +∞ as |y | → +∞.

Then,

the fast subsystem rescaled by τ = s/ε and with x ∈ Rn frozen

(FS) dyτ = g(x , yτ ) dτ + ν(x , yτ ) dWτ ,

is uniquely ergodic, i.e., has a unique invariant measure µx .

Liouville property:any bounded subsolution of −Lv = 0 is constant.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 23 / 29

Next assume on the linear operator L

Ellipticity: ∃Λ(y) > 0 s.t. ∀ x ν(x , y)νT (x , y) ≥ Λ(y)I

Lyapunov: ∃w ∈ C(Rm), k > 0, R0 > 0 s.t.−Lw ≥ k for |y | > R0, ∀x ,

w(y) → +∞ as |y | → +∞.

Then,

the fast subsystem rescaled by τ = s/ε and with x ∈ Rn frozen

(FS) dyτ = g(x , yτ ) dτ + ν(x , yτ ) dWτ ,

is uniquely ergodic, i.e., has a unique invariant measure µx .

Liouville property:any bounded subsolution of −Lv = 0 is constant.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 23 / 29

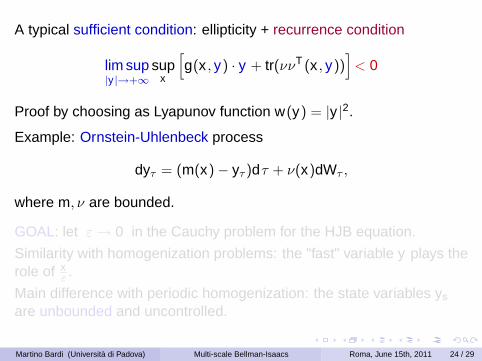

A typical sufficient condition: ellipticity + recurrence condition

lim sup|y |→+∞

supx

[g(x , y) · y + tr(ννT (x , y))

]< 0

Proof by choosing as Lyapunov function w(y) = |y |2.

Example: Ornstein-Uhlenbeck process

dyτ = (m(x)− yτ )dτ + ν(x)dWτ ,

where m, ν are bounded.

GOAL: let ε → 0 in the Cauchy problem for the HJB equation.

Similarity with homogenization problems: the "fast" variable y plays therole of x

ε .

Main difference with periodic homogenization: the state variables ys

are unbounded and uncontrolled.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 24 / 29

A typical sufficient condition: ellipticity + recurrence condition

lim sup|y |→+∞

supx

[g(x , y) · y + tr(ννT (x , y))

]< 0

Proof by choosing as Lyapunov function w(y) = |y |2.

Example: Ornstein-Uhlenbeck process

dyτ = (m(x)− yτ )dτ + ν(x)dWτ ,

where m, ν are bounded.

GOAL: let ε → 0 in the Cauchy problem for the HJB equation.

Similarity with homogenization problems: the "fast" variable y plays therole of x

ε .

Main difference with periodic homogenization: the state variables ys

are unbounded and uncontrolled.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 24 / 29

Convergence Theorem

Under the previous assumptions, the (weak) limit u(t , x) as ε → 0 ofthe value function uε(t , x , y) solves

(CP)

∂u∂t +

∫H(x , y , Dxu, D2

xxu, 0)

dµx(y) = 0 in R+ × Rn

u(0, x) =∫

h(x , y) dµx(y)

If, moreover, either g, ν do not depend on x or

g(x , ·), ν(x , ·) ∈ C1 and g(·, y), ν(·, y) ∈ C1b

Dxg, Dyg, Dxν, Dyν are Hölder in y uniformly w.r.t. x ,

then u is the unique viscosity solution (with quadratic growth) of (CP)

and uε(t , x , y) → u(t , x) locally uniformly on (0,+∞)× Rn.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 25 / 29

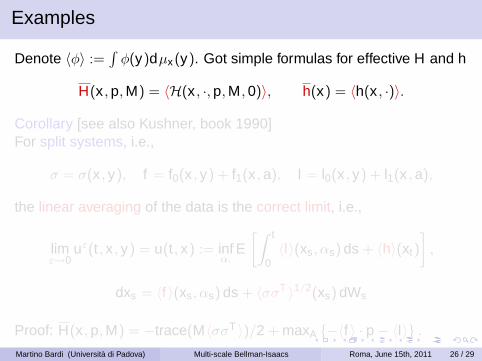

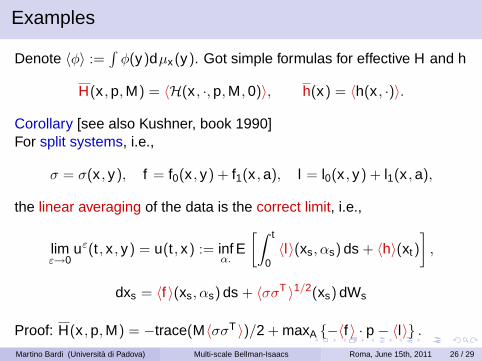

Examples

Denote 〈φ〉 :=∫

φ(y)dµx(y). Got simple formulas for effective H and h

H(x , p, M) = 〈H(x , ·, p, M, 0)〉, h(x) = 〈h(x , ·)〉.

Corollary [see also Kushner, book 1990]For split systems, i.e.,

σ = σ(x , y), f = f0(x , y) + f1(x , a), l = l0(x , y) + l1(x , a),

the linear averaging of the data is the correct limit, i.e.,

limε→0

uε(t , x , y) = u(t , x) := infα.

E[∫ t

0〈l〉(xs, αs) ds + 〈h〉(xt)

],

dxs = 〈f 〉(xs, αs) ds + 〈σσT 〉1/2(xs) dWs

Proof: H(x , p, M) = −trace(M〈σσT 〉)/2 + maxA {−〈f 〉 · p − 〈l〉} .

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 26 / 29

Examples

Denote 〈φ〉 :=∫

φ(y)dµx(y). Got simple formulas for effective H and h

H(x , p, M) = 〈H(x , ·, p, M, 0)〉, h(x) = 〈h(x , ·)〉.

Corollary [see also Kushner, book 1990]For split systems, i.e.,

σ = σ(x , y), f = f0(x , y) + f1(x , a), l = l0(x , y) + l1(x , a),

the linear averaging of the data is the correct limit, i.e.,

limε→0

uε(t , x , y) = u(t , x) := infα.

E[∫ t

0〈l〉(xs, αs) ds + 〈h〉(xt)

],

dxs = 〈f 〉(xs, αs) ds + 〈σσT 〉1/2(xs) dWs

Proof: H(x , p, M) = −trace(M〈σσT 〉)/2 + maxA {−〈f 〉 · p − 〈l〉} .

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 26 / 29

Example: we recover the Black-Scholes formula with stochasticvolatility.

In general, for system or cost NOT split,

H(x , p, M) = 〈maxA{...}〉 > max

A〈{...}〉

and the limit control problem is not obvious.We try to write H as a Bellman Hamiltonian in some other way in orderto find an explicit effective control problem approximating the singularlyperturbed one as ε → 0. We did it for

Merton problem with stochastic volatility (see next slides),

Ramsey model of optimal economic growth with (fast) randomparameters,

Vidale - Wolfe advertising model with random parameters,

advertising game in a duopoly with Lanchester dynamics andrandom parameters.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 27 / 29

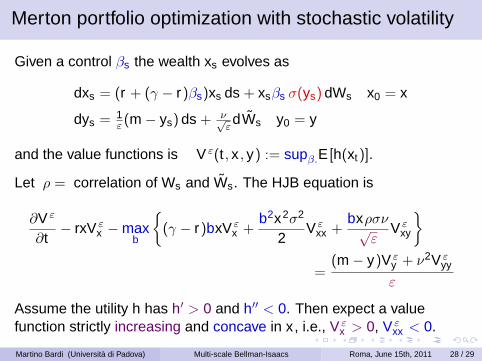

Merton portfolio optimization with stochastic volatility

Given a control βs the wealth xs evolves as

dxs = (r + (γ − r)βs)xs ds + xsβs σ(ys) dWs x0 = x

dys = 1ε (m − ys) ds + ν√

εdWs y0 = y

and the value functions is V ε(t , x , y) := supβ.E [h(xt)].

Let ρ = correlation of Ws and Ws. The HJB equation is

∂V ε

∂t− rxV ε

x −maxb

{(γ − r)bxV ε

x +b2x2σ2

2V ε

xx +bxρσν√

εV ε

xy

}=

(m − y)V εy + ν2V ε

yy

ε

Assume the utility h has h′ > 0 and h′′ < 0. Then expect a valuefunction strictly increasing and concave in x , i.e., V ε

x > 0, V εxx < 0.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 28 / 29

The HJB equation becomes

∂V ε

∂t− rxV ε

x +[(γ − r)V ε

x + xρσν√ε

V εxy ]2

σ2(y)2V εxx

=(m − y)V ε

y + ν2V εyy

ε

By the Theorem, V ε(t , x , y) → V (t , x) as ε → 0 and V solves

∂V∂t

− rxVx +(γ − r)2V 2

x

2Vxx

∫1

σ2(y)dµ(y) = 0 in R+ × R+

This is the HJB equation of a Merton problem with the harmonicaverage of σ as constant volatility

σ :=

(∫1

σ2(y)dµ(y)

)−1/2

.

Therefore this is the limit control problem.

The limit of the optimal control βε,∗s as ε → 0 can also be studied.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 29 / 29

The HJB equation becomes

∂V ε

∂t− rxV ε

x +[(γ − r)V ε

x + xρσν√ε

V εxy ]2

σ2(y)2V εxx

=(m − y)V ε

y + ν2V εyy

ε

By the Theorem, V ε(t , x , y) → V (t , x) as ε → 0 and V solves

∂V∂t

− rxVx +(γ − r)2V 2

x

2Vxx

∫1

σ2(y)dµ(y) = 0 in R+ × R+

This is the HJB equation of a Merton problem with the harmonicaverage of σ as constant volatility

σ :=

(∫1

σ2(y)dµ(y)

)−1/2

.

Therefore this is the limit control problem.

The limit of the optimal control βε,∗s as ε → 0 can also be studied.

Martino Bardi (Università di Padova) Multi-scale Bellman-Isaacs Roma, June 15th, 2011 29 / 29