horse cove partners high yield strategy · horse cove partners high yield strategy ... standard...

TRANSCRIPT

678-905-5723 www.horsecovepartners.com

Horse Cove Partners High Yield Strategy

Horse Cove Partners LLC Suite 120

1899 Powers Ferry RD SE Atlanta, GA 30339

Horse Cove Partners LLC Absolute Return Strategy

Profiting from the Art and Science of taking Risk.

2

We do not believe we are smarter than the market, nor can we time the market in any given week or month. As a result, we take an approach similar to an insurance company in our investment strategy that focuses on probability of success and the management of risk. All investments entail risk. Loss events do occur. As advisers, we understand that events will occur. “When” they will occur is the unknown. One of the keys to success is to take intelligent losses when those events occur and expect that the trading strategy will result in positive performance net of those losses over time. We believe our success comes from focusing on the risk of each trade. By maintaining a weekly investments horizon and relying on over 60 years of history of market movement we believe it is possible to realize positive returns through option transactions, while maintaining acceptable risk limits.

Horse Cove Partners Philosophy

3

Horse Cove Partners LLC Horse Cove Partners LLC utilizes a highly disciplined investment strategy, replicated weekly, to extract absolute returns from trading short volatility option spreads. Target returns for existing accounts are 24% per annum net of fees. The firm singularly focuses on the art and science of taking risk with options on behalf of its clients. The firm provides its services as advisors for separately managed accounts only. Headquartered in Atlanta, Georgia, Horse Cove Partners was formed in 2013 to build on the strength of option trading expertise developed since 2002. [The firm is affiliated with FISCO Alpha Management, LLC and FISCO Appreciation Management LLC by partial common ownership. ]

4

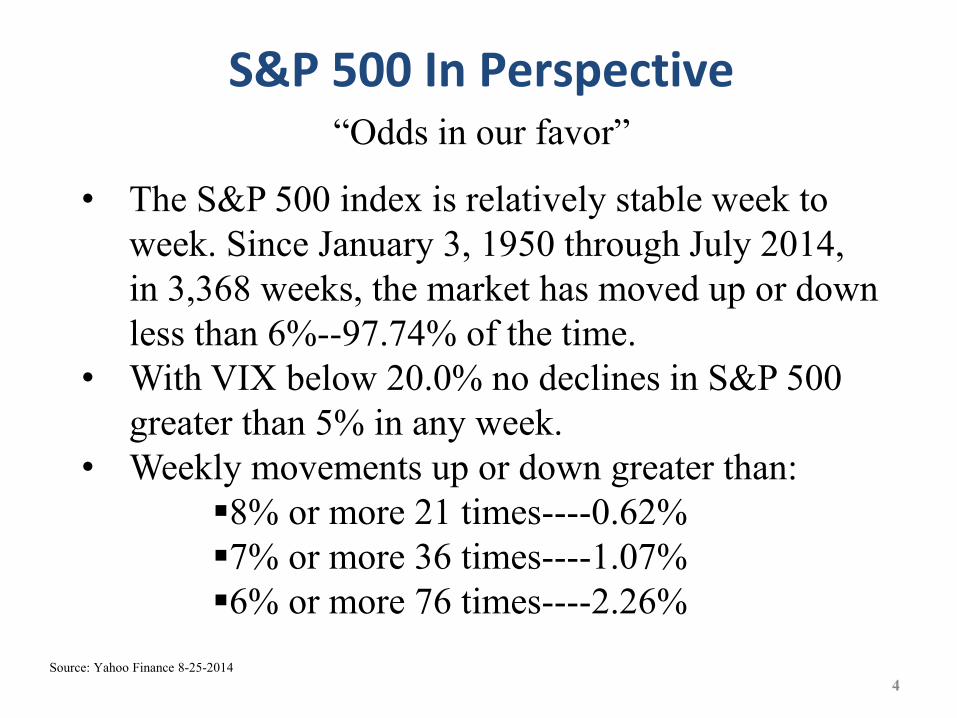

“Odds in our favor”

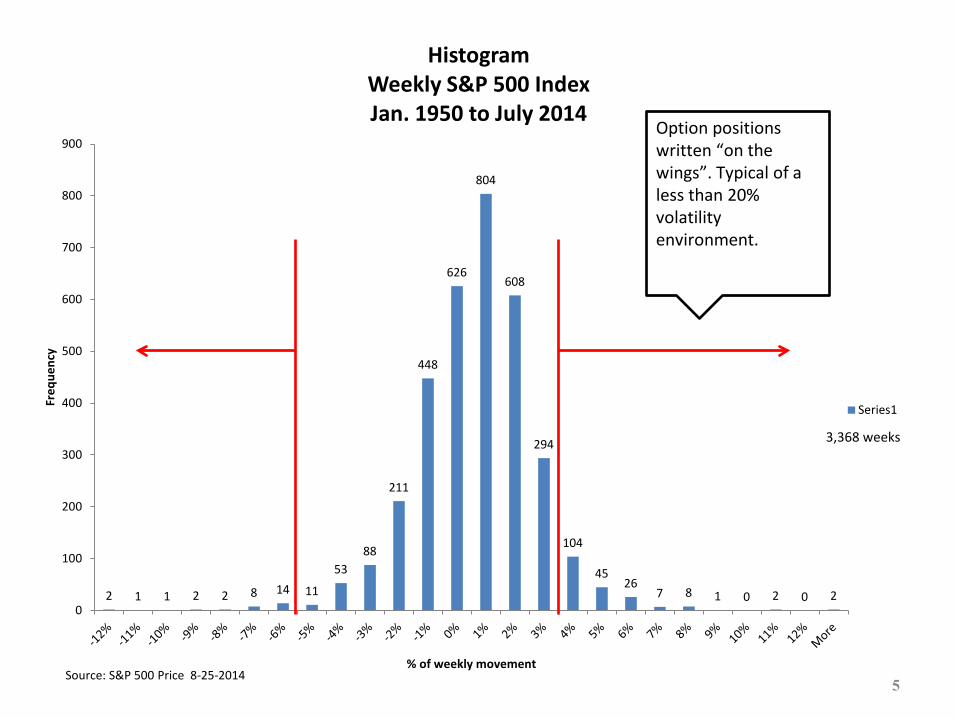

• The S&P 500 index is relatively stable week to week. Since January 3, 1950 through July 2014, in 3,368 weeks, the market has moved up or down less than 6%--97.74% of the time.

• With VIX below 20.0% no declines in S&P 500 greater than 5% in any week.

• Weekly movements up or down greater than: �8% or more 21 times----0.62% �7% or more 36 times----1.07% �6% or more 76 times----2.26%

S&P 500 In Perspective

Source: Yahoo Finance 8-25-2014

2 1 1 2 2 8 14 11

53 88

211

448

626

804

608

294

104

45 26

7 8 1 0 2 0 2 0

100

200

300

400

500

600

700

800

900

Freq

uenc

y

% of weekly movement

Histogram Weekly S&P 500 Index Jan. 1950 to July 2014

Series1

3,368 weeks

Option positions written “on the wings”. Typical of a less than 20% volatility environment.

Source: S&P 500 Price 8-25-2014 5

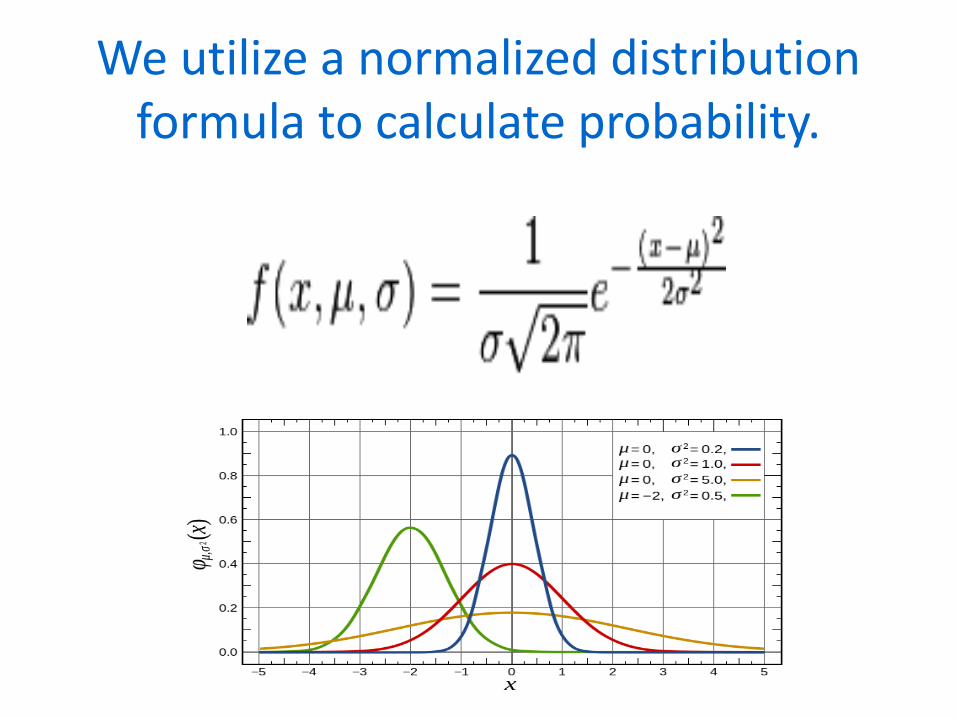

We utilize a normalized distribution formula to calculate probability.

7

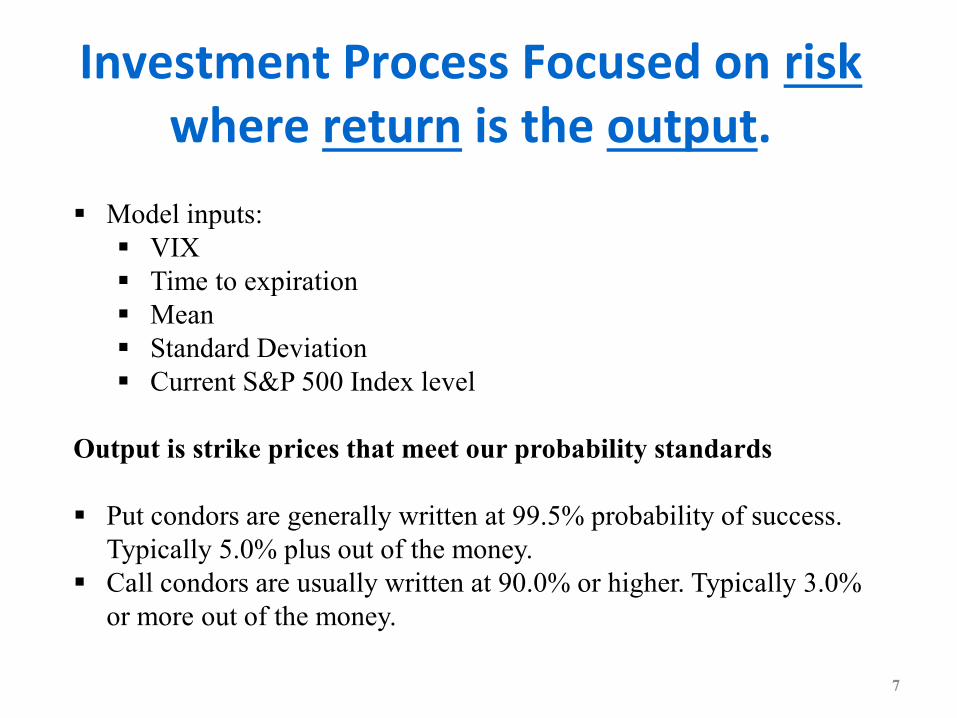

� Model inputs: � VIX � Time to expiration � Mean � Standard Deviation � Current S&P 500 Index level

Output is strike prices that meet our probability standards � Put condors are generally written at 99.5% probability of success.

Typically 5.0% plus out of the money. � Call condors are usually written at 90.0% or higher. Typically 3.0%

or more out of the money.

Investment Process Focused on risk where return is the output.

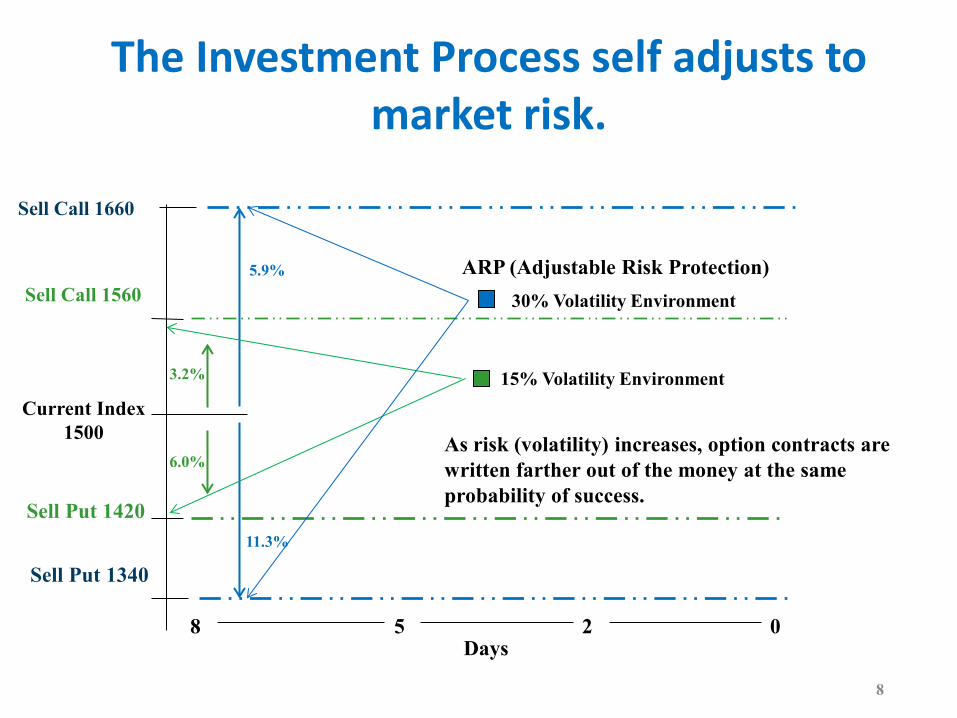

The Investment Process self adjusts to market risk.

8

Sell Call 1660

Sell Call 1560

Sell Put 1420

Sell Put 1340

8 5 2 0 Days

3.2%

6.0%

30% Volatility Environment

15% Volatility Environment Current Index

1500

5.9%

11.3%

ARP (Adjustable Risk Protection)

As risk (volatility) increases, option contracts are written farther out of the money at the same probability of success.

9

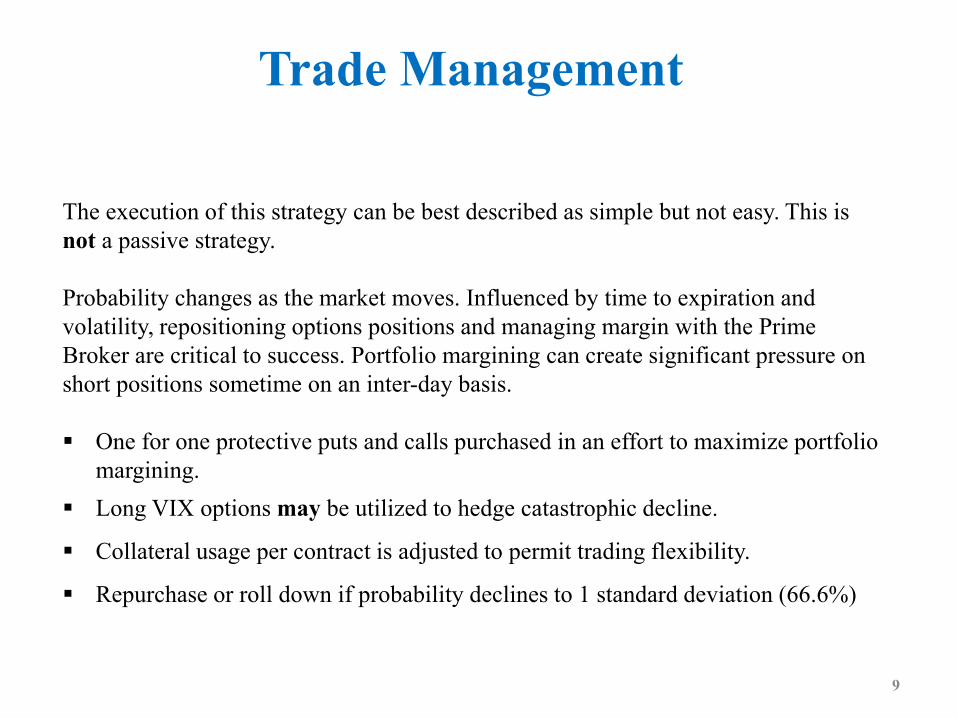

The execution of this strategy can be best described as simple but not easy. This is not a passive strategy. Probability changes as the market moves. Influenced by time to expiration and volatility, repositioning options positions and managing margin with the Prime Broker are critical to success. Portfolio margining can create significant pressure on short positions sometime on an inter-day basis. � One for one protective puts and calls purchased in an effort to maximize portfolio

margining. � Long VIX options may be utilized to hedge catastrophic decline.

� Collateral usage per contract is adjusted to permit trading flexibility.

� Repurchase or roll down if probability declines to 1 standard deviation (66.6%)

Trade Management

10

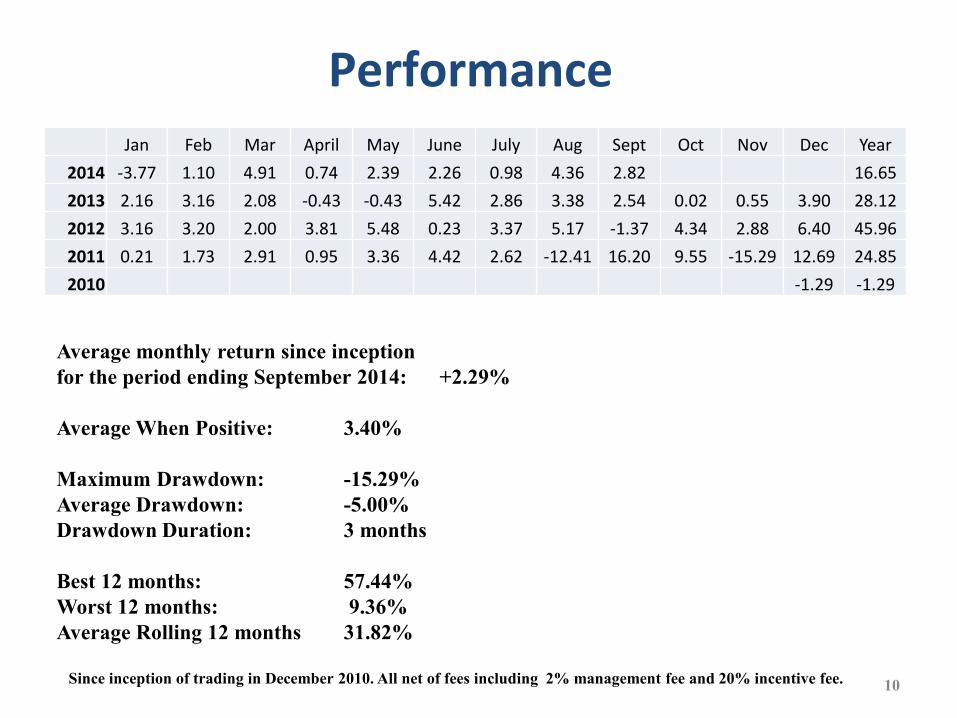

Performance

Since inception of trading in December 2010. All net of fees including 2% management fee and 20% incentive fee.

Jan Feb Mar April May June July Aug Sept Oct Nov Dec Year 2014 -3.77 1.10 4.91 0.74 2.39 2.26 0.98 4.36 2.82 16.65 2013 2.16 3.16 2.08 -0.43 -0.43 5.42 2.86 3.38 2.54 0.02 0.55 3.90 28.12 2012 3.16 3.20 2.00 3.81 5.48 0.23 3.37 5.17 -1.37 4.34 2.88 6.40 45.96 2011 0.21 1.73 2.91 0.95 3.36 4.42 2.62 -12.41 16.20 9.55 -15.29 12.69 24.85 2010 -1.29 -1.29

Average monthly return since inception for the period ending September 2014: +2.29% Average When Positive: 3.40% Maximum Drawdown: -15.29% Average Drawdown: -5.00% Drawdown Duration: 3 months Best 12 months: 57.44% Worst 12 months: 9.36% Average Rolling 12 months 31.82%

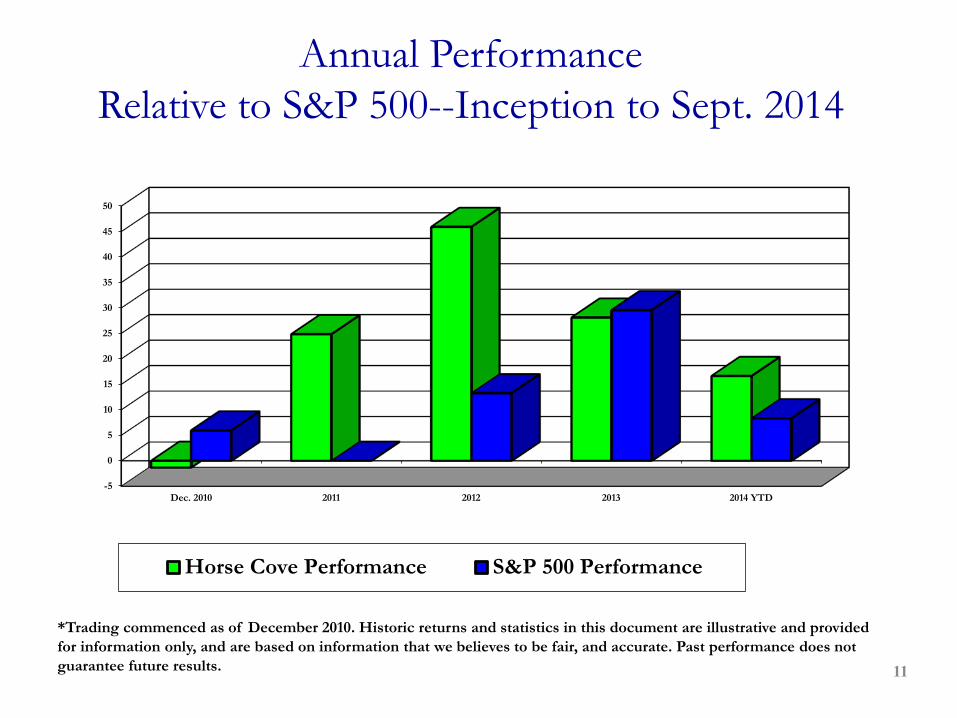

Annual Performance Relative to S&P 500--Inception to Sept. 2014

-5

0

5

10

15

20

25

30

35

40

45

50

Dec. 2010 2011 2012 2013 2014 YTD

Horse Cove Performance S&P 500 Performance

*Trading commenced as of December 2010. Historic returns and statistics in this document are illustrative and provided

for information only, and are based on information that we believes to be fair, and accurate. Past performance does not

guarantee future results. 11

12

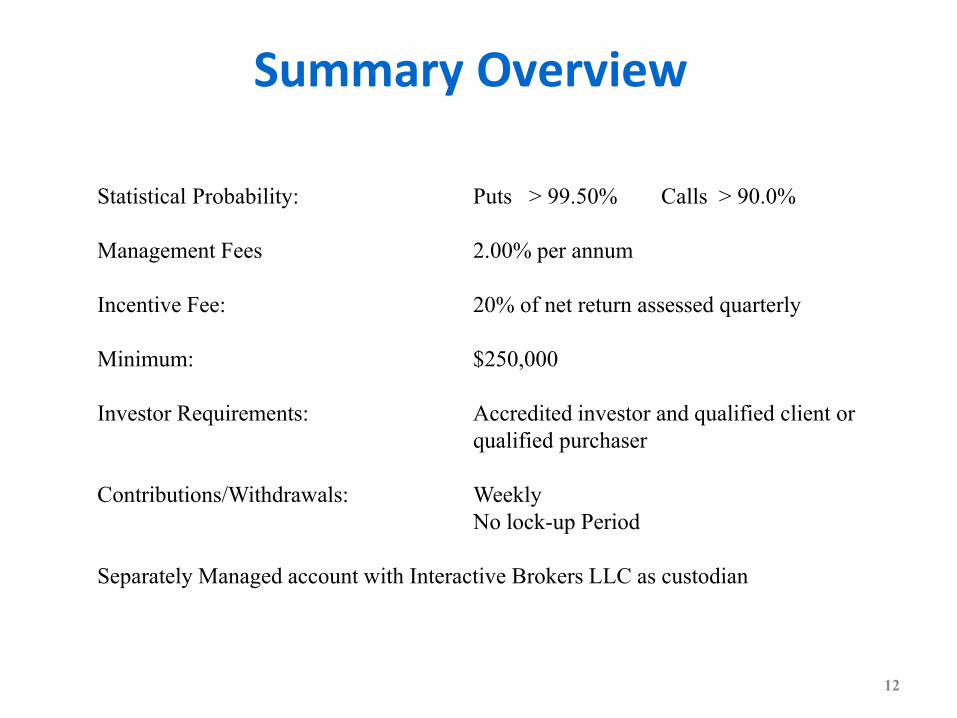

Statistical Probability: Puts > 99.50% Calls > 90.0% Management Fees 2.00% per annum Incentive Fee: 20% of net return assessed quarterly Minimum: $250,000 Investor Requirements: Accredited investor and qualified client or qualified purchaser Contributions/Withdrawals: Weekly No lock-up Period Separately Managed account with Interactive Brokers LLC as custodian

Summary Overview

13

� Samuel T. DeKinder

Managing Director and Portfolio Manager Samuel T. DeKinder has over 40 years of investment experience. He is the Founder of Horse Cove Partners. Following his

retirement from Invesco Ltd in 2006., Mr. DeKinder was a partner and Vice President of Marketing for FISCO Appreciation Management LLC. Mr. DeKinder served as a member on the Board of Directors of Invesco, MIM PLC (the predecessor to Invesco Ltd.), in addition to a variety of executive capacities during his nearly 20 years with Invesco. He currently serves as a member of the Board of Directors of Kennedy Capital Management. Previously, Mr. DeKinder was a Co-Founding Principal of DeMarche Associates, one of the nation’s most prominent investment consulting firms. He graduated from the University of Oklahoma with degrees in Economics and Statistics. � Kevin Ellis

Managing Director Mr. Ellis brings more than 30 years of financial, administrative and operations experience to the Firm. Additionally, he is COO

and a Principal of FISCO Funds Management LLC; FISCO Alpha Management LLC; FISCO Appreciation Management LLC; and MVS Management LLC. He also serves as the Chief Operating and Compliance Officer for CARF Management LLC, a registered investment adviser to a mutual fund (River Rock IV Fund). Previously, Mr. Ellis served as a Founding Principal, Managing Director and COO at Labyrinth Group, LLC, an investment management firm utilizing structured securities. Prior to that, he was Manager of Corporate Development at Arthur Anderson, LLP, where he focused on finance, mergers and acquisitions. Earlier in his career, he served as Vice President of Business Planning at SUPERVALU, Inc. Mr. Ellis is a graduate of Minnesota State University-Mankato BA Finance and earned a Juris Doctorate from William Mitchell College of Law and was admitted to the bar in Minnesota in 1983.

Experienced Management Team

14

� John Monahan

Director of Development Mr. Monahan is a business development and client relations expert in the investment management industry. He began his

career as the youngest Regional VP – Group Pension Division for Union Mutual. In 1985 John co-founded and steered the build-out of PRIMCO Capital Management from the ground up, propelling assets under management from zero to $10B in 5 years. PRIMCO was acquired by INVESCO in 1991. He joined INVESCO as a Global Partner in 1991 and launched and led institutional market development spanning the US (Puerto Rico) Canada, the Middle East, South America, Bermuda, and the Caribbean. Since 2006 John has co-founded 3 firms, all subsidiaries of Peachtree Commonwealth. John completed executive education at The Wharton School of the University of Pennsylvania and earned a BA in American Studies from St. Michaels College. He possesses conversational fluency in French and basic fluency in Spanish.. � Pedro Gonzalez-Cerrud, PhD, CFA, CPA, CFP, CVA

Director of Research Dr. Gonzalez-Cerrud brings over two decades of institutional industry experience to the Firm. He is currently an adjunct

professor at the Graduate School of Business (MBA)at the University of Puerto Rico and serves as a consultant with ConsulTrust Global, an economic consultant to High Net Worth Individuals, Credit Unions and Insurance Companies. Dr. Gonzalez-Cerrud was a Managing Director and Business Development Executive at Invesco Institutional for Puerto Rico, Latin America and the Caribbean for more than a 15 years. Prior to joining Invesco Institutional, he was an institutional consultant at Salmon Smith Barney and the Financial Planning Group. Dr. Gonzalez-Cerrud earned a B.A. in economics from the Universidad de Panama, an MBA-Finance and Accounting from the University of Puerto Rico and also earned a PhD –Finance, with minors in Accounting and Econometrics from Lehigh University in Pennsylvania.

Experienced Management Team

15

� Mike Crissey

Vic President, Sales and Client Services Mike Crissey has over 30 years experience in Institutional Sales, Marketing, Client Servicing, Consultant Relations and Institutional Investment Consulting. From 2000 to 2013 Mr. Crissey, held sales, marketing and client servicing positions with Pathways Financial Partners, Fisco Investment Management, Principal Global Investors and Sirach Capital Management. Prior to Sirach Capital Management, Mr. Crissey was a Senior Vice President of DeMarche Associates, one of the nation’s leading investment consulting firms. At DeMarche he managed the operations of the firm and later created and ran a consulting service to 50 of the largest investment firms in the US. 1982 to 1999. Mr. Crissey is a native of Missouri and a graduate of the Penn Valley Community College receiving a degree in Computer Science with an emphasis in Systems Design. Mr. Crissey and his wife Judy reside in Tucson, Arizona.

Experienced Management Team

16

RISK MANAGEMENT

17

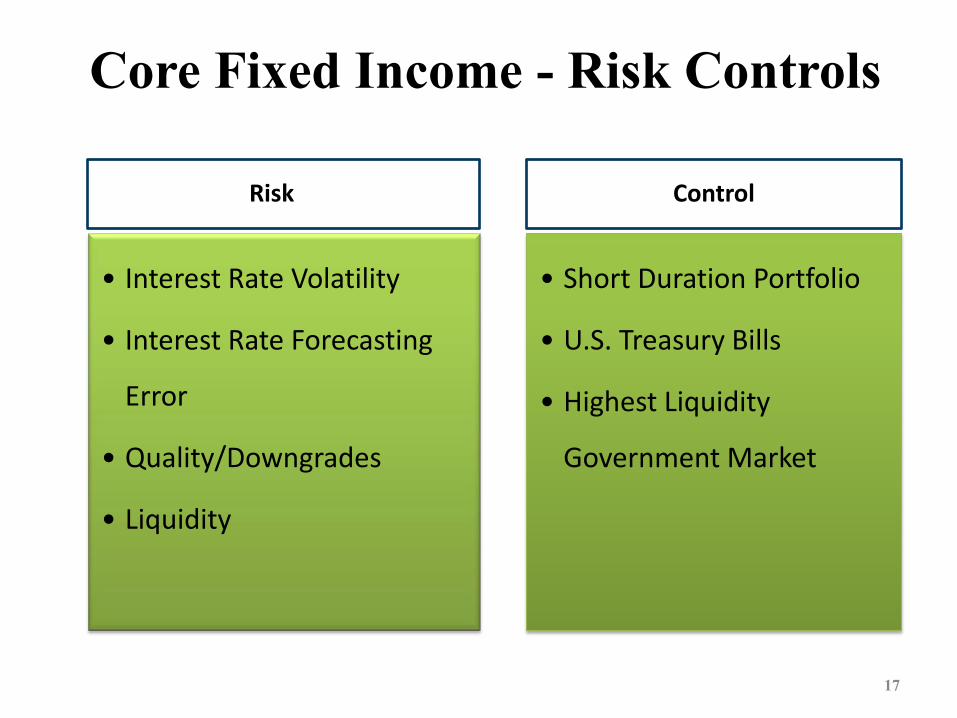

Core Fixed Income - Risk Controls

Risk

ͻ Interest Rate Volatility

ͻ Interest Rate Forecasting

Error

ͻ Quality/Downgrades

ͻ Liquidity

Control

ͻ Short Duration Portfolio

ͻ U.S. Treasury Bills

ͻ Highest Liquidity

Government Market

18

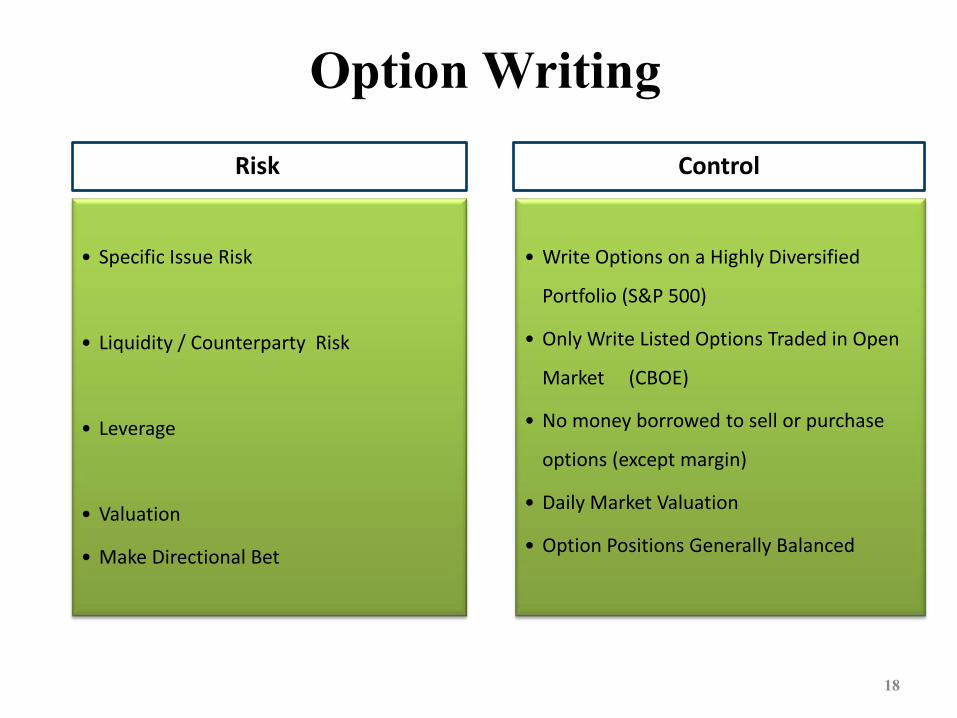

Option Writing Risk

ͻ Specific Issue Risk

ͻ Liquidity / Counterparty Risk

ͻ Leverage

ͻ Valuation

ͻ Make Directional Bet

Control

ͻ Write Options on a Highly Diversified

Portfolio (S&P 500)

ͻ Only Write Listed Options Traded in Open

Market (CBOE)

ͻ No money borrowed to sell or purchase

options (except margin)

ͻ Daily Market Valuation

ͻ Option Positions Generally Balanced

19

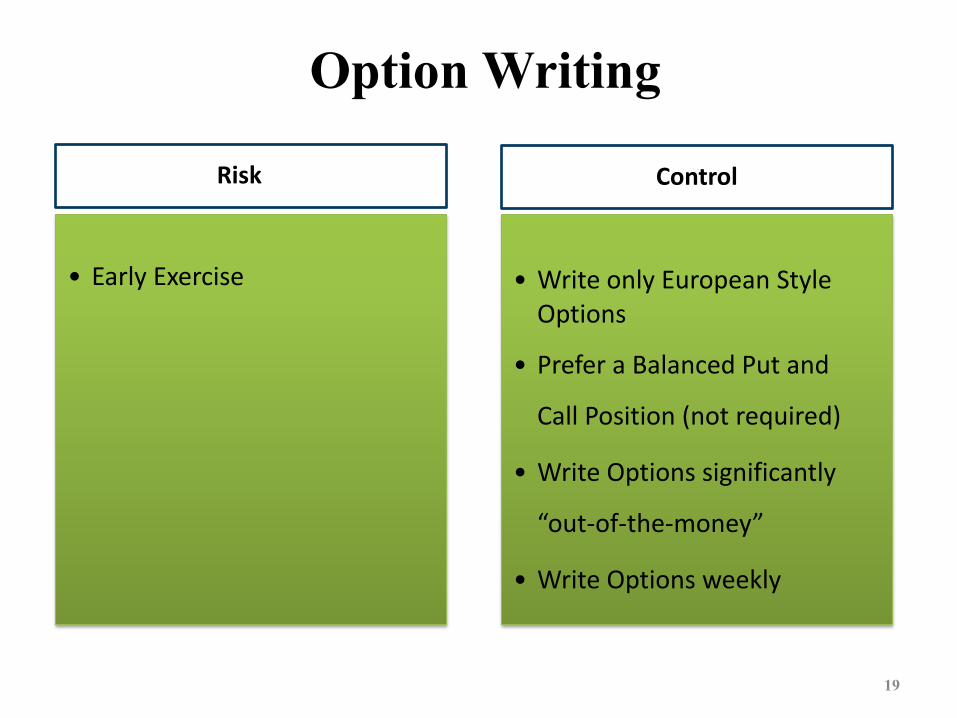

Option Writing

Risk

ͻ Early Exercise

Control

ͻ Write only European Style

Options

ͻ Prefer a Balanced Put and

Call Position (not required)

ͻ Write Options significantly

“out-of-the-money”

ͻ Write Options weekly

20

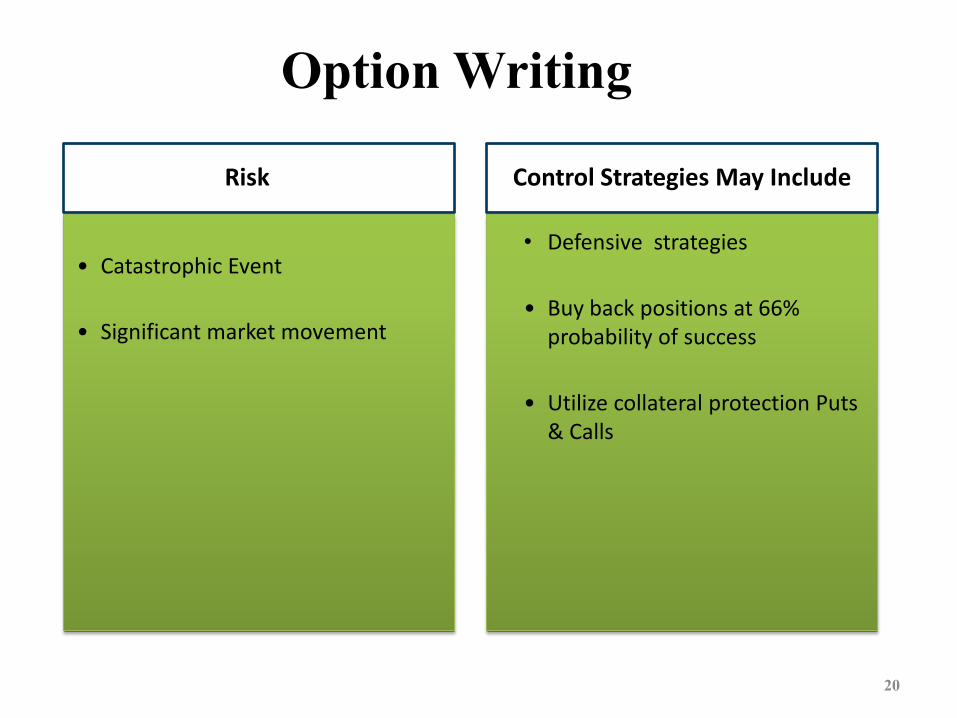

Risk

ͻ Catastrophic Event ͻ Significant market movement

S Control Strategies May Include

• Defensive strategies

ͻ Buy back positions at 66% probability of success

ͻ Utilize collateral protection Puts

& Calls

Option Writing

21

DISCLOSURE September 2014

Prior performance shows results achieved during past market periods and is not indicative of future results, which will depend, among other things, on future market conditions. No representation is being made that the strategy will or is likely to achieve returns similar to those shown. Results are shown net of fees and expenses but do not reflect withdrawals or income taxes that might be payable, the effects of which could significantly reduce cumulative returns. The strategy was not available until December, 2010. For the period commencing December 2010 and ending February 2013, the results reflect the monthly deduction of a 2% per annum management and 20% performance incentive, and brokerage fees and commissions which would have been incurred by the strategy . Commencing in March 2013, results are composite results net of 2% per annum management fee assessed daily and 20% incentive fee crystalized quarter all as calculated by the firms broker. There can be no assurance that the results shown will be replicated in the future. Options are speculative and highly leveraged. Although the strategy usually writes options that, when written, Manager believes will have a 90% or more probability of success based on volatility and term, specific market movements of the index underlying the option cannot be accurately predicted. As the writer of put and call options, the strategy is subject to the significant risk of loss if the index moves to levels below or above the strike price of the option. Economic leverage is possible if options move beyond the option strike price. The Manager may employ risk management strategies which are intended to reduce risk but cannot eliminate it. Costs of such strategies may reduce potential returns. Risk management strategies may include writing options on other indices, writing outside the strategy’s general parameters (including probabilities outside the stated target), and writing for longer or shorter durations. This document is for illustrative purposes only and should not be regarded as an offer or solicitation for advisory services offered by the Investment Manager or its affiliates, officers, directors, agents or employees. This material is not authorized for re-distribution unless it is accompanied by strategy disclosures. The strategy represents a speculative investment and may involve a high degree of risk. An investor may lose all or part of their investment. There can be no assurance that the strategy will achieve its investment objectives. Fees and expenses may offset trading profits. There are restrictions on redeeming interests in the fund, and there is no secondary market for the interests. Prospective investors should carefully review the offering memorandum and fund disclosures, and should consult with their financial advisors before making an investment.