hot topics and update on credits and incentives - baker tilly · · 2018-04-182012-05-01 · hot...

TRANSCRIPT

Hot topics and update on dit d i ticredits and incentives

May 1, 2012

© 2011 Baker Tilly Virchow Krause, LLPBaker Tilly refers to Baker Tilly Virchow Krause, LLP,

an independently owned and managed member of Baker Tilly International.

1

Presenters

Moderator Panelist PanelistPanelist

Gina Staudacher Kate CrowleyJon Skavlem Ellen ErnstPrincipal

Strategic Tax Baker Tilly

ManagerState and Local Tax

Baker Tilly

DirectorState and Local Tax

Baker Tilly

ManagerStrategic Tax

Baker Tilly

2

Agenda

> Federal credits and incentives– Green investments– Work Opportunity Tax Credit (WOTC)– New Markets Tax Credit– TechnologyTechnology

> State and local tax credits> Tax increment financing> C&I t t i d itf ll> C&I strategies and pitfalls > Wrap-up and questions

3

Federal credits and incentives

4

Corporate activities leading to federal incentives

> Energy or “green-”related investments

R d li t fit– Remodeling or retrofit– Energy production efforts

> Job creation and/or retention

Tax considerations, credits and incentive

opportunities

> Investing in technology and development

5

“Green” activities

> Related tax-advantaged programs where “green” activities might result in additional federal or state tax benefits– Increasing energy efficiency of existing buildingsIncreasing energy efficiency of existing buildings– Designing new facilities with increased efficiency– Incorporating systems which harness energy through waste

conversionP d ti f lt ti f l– Production of alternative fuels

– Solar, wind, geothermal, combined heat and power development

6

Energy-related programs

> Section 179D: Energy Efficient Building Deduction – Enhanced deduction for improvements made to facilities

> Section 45: Renewable Electricity Production Credits> Section 45: Renewable Electricity Production Credits– Credit for the sale of electricity produced from qualified energy sources

> Section 48: Energy Credit – 10% or 30% credit on cost of qualified equipment including fuel cell, q q p g ,

small wind energy, geothermal, solar– Equipment used to generate, produce, and distribute electricity from

qualified property> Section 1603: Energy Grant> Section 1603: Energy Grant

– 30% grant for qualified energy property– Construction must have begun prior to Dec. 31, 2011

7

179D - Overview

> Referred to as Energy Efficient Commercial Building Deduction or 179D deduction– Also applicable to residential rental structures more than three storiesAlso applicable to residential rental structures more than three stories

> Timeframe: improvements/retrofits placed in service after Dec. 31, 2005, and before Jan. 1, 2014

> Current-year deduction for energy-efficiency expenses> Applies to new construction AND existing buildings (remodel or

retrofit)> Three separate systems – maximum of $0.60 per square foot

each:each: – Lighting– HVAC/hot water– Building envelope

8

179D example

> Company retrofits 300,000-square-foot warehouse with new energy-efficient lighting

> Installed lighting qualifies for the full $0 60 per square foot> Installed lighting qualifies for the full $0.60 per square foot deduction, yielding potential $180,000 179D deduction before adjusted basis modification

> Cost of materials and installation of new lighting is $200,000> Client applies for and receives $50,000 in utility rebates> Adjusted cost basis of lighting is $150,000 ($200,000 cost less

$50,000 in rebates)> 179D potential deduction of $150 000> 179D potential deduction of $150,000

9

Background and qualifications

> Building must meet overall 50% energy-savings threshold as compared to a “reference” building

> Energy-savings measurement based on ASHRAE 90 1-2001> Energy-savings measurement based on ASHRAE 90.1-2001 standards

> Requires certification of savings> Can file in the current year, file an amended return, or submit a

Form 3115

10

Who can claim the deduction?

> Building owners – Deduction follows depreciation

> *Designers of government owned buildings> Designers of government-owned buildings– Deduction may be assigned to the “designer” for the taxable year in

which the property is placed in service– Attractive yet overlooked benefit to the building designer:

“f d”“found” money – The “designer” can be numerous parties, i.e., split among architect,

engineering firm, environmental consultant, general contractor, etc.

11

Highlight of additional energy incentives

Energy Credit/Investment Tax Credit § 48(a)> Credit equal to 30% or 10% of eligible project costs> What is “energy property”?

– Tangible property (not including a building) that is an integral part of the facility

– Tax payer constructed OR acquired for original usep y q g– Examine the type of energy associated to determine benefit

> 1603 grant in lieu of Energy Credit – Lingering opportunity: project must have “commenced

construction” by Dec 31 2011construction” by Dec. 31, 2011> Place property in service before specified dates depending on

property type

12

Section 48 – Energy Credit

Credit of 30% of project costs for the following property: 1. Solar property – equipment utilizing solar to heat, cool, generate

electricity or provide solar process heatelectricity, or provide solar process heat2. Fuel cell property – must be a fuel cell power plant 3. Small wind – wind turbines used to generate electricityCredit of 10% of project costs for the following property:Credit of 10% of project costs for the following property: 1. Microturbines – gas turbine engine, combustor, regenerator, or

generator converting a fuel into electricity or thermal energy2. Geothermal – heat pump system using ground or ground water to heat

or cool a structure3. Combined heat and power (CHP) – systems that simultaneously

generate electrical/mechanical power AND steam/thermal power for heating or cooling g g

13

Job Creation Incentive:Th W k O t it T C dit (WOTC)The Work Opportunity Tax Credit (WOTC)

14

WOTC overview

> Employer tax credit based on a percentage of qualified wages paid to the new employee

> Goal: provide incentive for employers to hire individuals from> Goal: provide incentive for employers to hire individuals from certain population/socio-economic groups– Nine targeted employee groups generate the credit

> Actual benefit to employers: – Up to $2,400 per employee for most target groups– Variations based on particular groups

> Certification process: data must be gathered prior to hiring

15

WOTC program: targeted groups historically

1. Long-term TANF recipient2. Short-term TANF recipient3. Qualified veteran4. 18-39 year-old SNAP (food stamps) recipient5. 18-39 year-old Designated Community resident: lives in a

C ( C)Rural Renewal County (RRC)6. Vocational rehabilitation referral – disability related

7. Ex-felon – hired within one year after the date of the conviction or l f irelease from prison

8. Supplemental Security Income (SSI) recipient

Nonveteran groups and Empowerment Zones (EZ) expired on Dec. 31, 2011

16

What is new?

VOW to Hire Heroes Act of 2011: enhancement and extension of credit pertaining to veteran group:

Currently only active group– Currently only active group> New veteran hires must begin work on or after Nov. 22, 2011,

and before Jan. 1, 2013> Simplified certification p> Increased benefit for employers – dependent on wages paid:

– Disabled veterans hired within one year of discharge – credit capped at $4,800 Disabled veteran unemployed for 6 months credit capped at– Disabled veteran unemployed for 6 months – credit capped at $9,600

– Veterans unemployed for at least 6 months – credit capped is up to $6,000

17

Future of program

> Hiatus: Nonveteran groups may be reauthorized> Employers may and should still submit certification requests for

t t t tnonveteran groups to states> States will accept requests but not issue determinations until

WOTC is reauthorized

18

Three steps to apply

Employers apply for and receive a certification from their State Workforce Agency (SWA):1. Complete page 1 of IRS From 8850, Pre-Screening Notice and

Certification Request for the Work Opportunity Tax Credit.– Qualified veterans hired from Nov. 22, 2011 – May 22, 2012 -

8850 to be submitted on or before June 19, 20122. Complete ETA Form 9061, Individual Characteristics Form or ETA

Form 9062, Conditional Certification Form.3. Mail the signed/dated IRS and ETA forms to the respective SWA.

19

New Markets Tax Credit

20

New Markets Tax Credit program history

> Congress passed the Community Renewal Tax Relief Act of 2000– Created the New Markets Tax Credit (NMTC) program

Encourage investment in qualified Low Income Communities (LIC)– Encourage investment in qualified Low-Income Communities (LIC)– Initially designed to generate $15 billion in new private sector

investments in low-income communities through 2007– Program has been extended through 2011

> The Community Development Financial Institutions (CDFI) Fund, a branch of the Department of the Treasury, administers the program

> Annual allocations of tax credits are made to Community D l t E titi (CDE ) th h li ti hDevelopment Entities (CDEs) through an application process who then have 5 years to put the credits to work in qualified projects

21

NMTC program and project qualifications

> Investors make a cash or cash equivalent qualified equity investment (QEI) into a CDE

> Th CDE i t b t ti ll ll f th QEI t k> The CDE, in turn, uses substantially all of the QEI to make a qualified low-income community investment (QLICIs) into a qualified active low-income community business (QALICB)

> The QALICB must be located in a low-income community:> The QALICB must be located in a low income community:– Census tract where there is a poverty rate of at least 20%, or;– Census tract where median income does not exceed 80% of the

comparable median incomeD di th CDE’ NMTC ll ti t th– Depending upon the CDE’s NMTC allocation agreement, other factors may be considered as “higher distress” including brownfield designation, unemployment, locally established economic development zone, and others

22

NMTC program and project qualifications

> The QALICB must meet basic business tests to qualify for the QLICI investment including:

At least 40% of the business’s tangible property is located in the LIC– At least 40% of the business s tangible property is located in the LIC– The employees of the business must perform at least 40% of their

services in the community> Ineligible QALICB activities include:

– Residential rental property– Certain “sin” businesses excluded

23

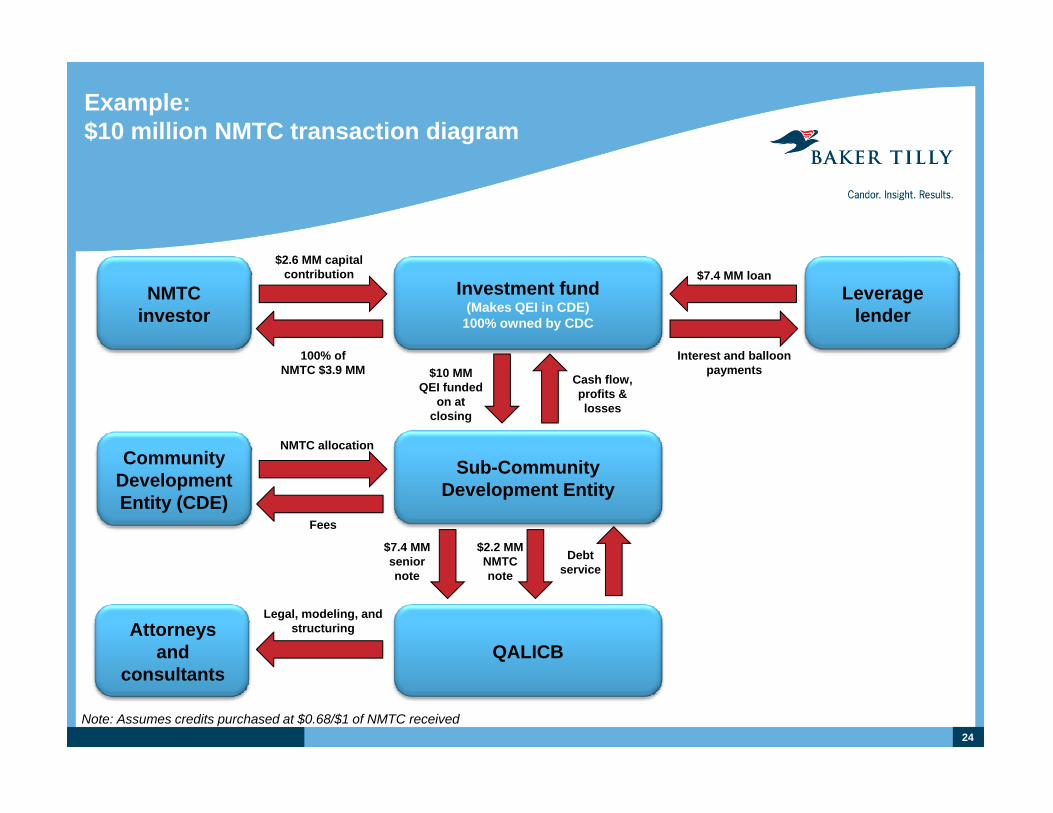

Example:$10 million NMTC transaction diagram

NMTC investor

Investment fund(Makes QEI in CDE)

100% owned by CDC

Leverage lender

$2.6 MM capital contribution

100% of

$7.4 MM loan

Interest and balloon

Community

100% of NMTC $3.9 MM

Interest and balloon payments

NMTC allocation

$10 MMQEI funded

on at closing

Cash flow, profits & losses

Community Development Entity (CDE)

Sub-Community Development Entity

Fees

Debt $2.2 MM NMTC

$7.4 MM senior

Attorneys and QALICB

Legal, modeling, and structuring

serviceNMTC note

seniornote

consultants

Note: Assumes credits purchased at $0.68/$1 of NMTC received24

Technology and manufacturing-related incentives

25

Incentivizing US production

> Efforts focused on developing technology continue to receive preferential tax treatment

Green efforts and job creation components– Green efforts and job creation components> Domestic Production Activities Deduction (DPAD):

additional deduction for US manufacturing> Research and Development incentives: credits and> Research and Development incentives: credits and

deduction for US development and technology efforts

26

Domestic Production Activities Deduction

> Enacted in 2005 to promote US manufacturing and production > Permanent deduction > Benefit equal to 9% of income derived from domestic production> Benefit equal to 9% of income derived from domestic production> Qualifying Activities:

– Manufacturing, growing, extracting, producing propertyo Includes softwareo c udes so t a e

– Construction activities in US– Engineering or architectural services for US projects

> Qualified Production Income capped at taxable income– If QPAI is less than TI – opportunity for additional benefit

> State conformity

27

Research and development (R&D): credits and deductions

Purpose: stimulate US investment in R&D, technology, engineering → preserve/encourage domestic employment

> Federal deduction: allowed for costs related to engineering and> Federal deduction: allowed for costs related to engineering and design of products, processes, or improvements to designs, products, or processes

> Federal credit: income tax credit based on product/process development

– Rule of thumb: 4% - 7% of R&D spend– Carry back 1 year and carry forward 20 years– Expenditures:– Expenditures:

o Employee wages; o Supplies; o Contractor expenditures.

28

Future of development incentives

> Research and development deduction – available for taxpayers; permanent benefit

> Research and development tax credit – currently expired;> Research and development tax credit – currently expired; available for tax years through 2011

– Refunds available → taxpayers may amend to include the credit for open tax yearsN t t fil d 2011 t t t t l t t l i thi i ti– Not yet filed 2011 tax return → not too late to claim this incentive

> Likelihood of future benefit– Permanent vs. continued temporary extension – Bipartisan support to:Bipartisan support to:

o Increase benefito Create more highly favored classes (advanced technology)o Exceptions for AMT

29

State R&D considerations

> Currently, more than 75% states provide some type of state R&D tax credit

– Continually increasing – Florida enacted credit for tax yearsContinually increasing Florida enacted credit for tax years 2012

> Most states adopt the federal definition of qualified research activities and compute expenses in a similar fashion

St t li bilit t il ti d t f d l t i– State applicability not necessarily tied to federal extension> Overall structure of state research credits varies significantly

from state to state> Keep in mind headquarters AND all regional manufacturing/ p q g g

technology centers– Activities must occur in the state to be eligible

30

State opportunities

Illinois> R&D credit available to C corporations, S corporations, and partnerships> C dit i l t 6 5% f th f t bl Illi i> Credit is equal to 6.5% of the excess of taxable year Illinois expenses

over a base > Credit recently extended through 2016IndianaIndiana> R&D credit available to C corporations, S corporations, and partnerships> Two computation methods available

– 15% of the excess of taxable year Indiana expenses over base period up to15% of the excess of taxable year Indiana expenses over base period up to $1 million (10% for incremental QREs in excess of $1 million)

– 10% of Indiana QREs that exceed 50% of QREs in prior 3 years (effective for QREs incurred after Dec. 31, 2009)

> Actual credit benefit → 7 5% of actual Indiana spend> Actual credit benefit → 7.5% of actual Indiana spend

31

State opportunities

Wisconsin> R&D credit is only available to C corporations> C dit i l t 5% f th f t Wi i> Credit is equal to 5% of the excess of current-year Wisconsin

QREs over base period QREs (alternative incremental method is also available)

> NEW: “Super” R&D credit – companies that have been p psignificantly ramping up R&D

– Effective tax year 2011– Taxpayers can claim super R&D credit equal to Wisconsin research

expenses that exceed 125% of average research expenses in priorexpenses that exceed 125% of average research expenses in prior 3 years

32

Refundable state R&D opportunities

Minnesota> R&D credit available to C corporations, S corporations, and

partnerships beginning tax year 2010partnerships beginning tax year 2010> Credit is equal to 10% of the first $2 million of Minnesota QREs that

exceed the base period QREs and 2.5% of incremental QREs over $2 million

Virginia – new in 2011> Refundable R&D credit available to C corporations, S corporations,

and partnerships > Credit is equal to 15% of first $167,000 in Virginia QREs that

exceed base amount (cap of $25,000)> Benefit → Limited to $25,000 refundable tax credit per year

33

State and local taxes, credits, and incentives

34

The “original” incentive

The first state taxThe first state tax incentive for economic

development is thought to have

occurred in 1791occurred in 1791. New Jersey offered a

tax abatement to Alexander Hamilton to

locate his manufacturing plant in

the state.

35

State and local taxes, credits, and incentives

State and local tax opportunities and incentives

> Property tax incentives including tax increment financing (TIF), tax opportunities and incentives g ( )abatements, reduced assessments

> Income tax credits (refundable vs. nonrefundable), deductions, and abatements

> Sales and use tax exemptions rebates> Sales and use tax exemptions, rebates, and credits

> Target zones e.g., enterprise, technology> Green and alternative energy incentives> Employment incentives and training> Employment incentives and training

grants> State research tax credits and grants> Low cost financing – IRBs, loans> Infrastructure improvements> Infrastructure improvements

36

Types of incentives

Statutory

> Must simply meet statutory or administrative requirements

> Normally do not require pre-approval from government

> Most commonly take form of tax deductions, exemptions, or credits

Negotiated

> Must be approved by state or local government, usually before decision is made

> Often subject to annual caps or Negotiated j pappropriations

> Multiple levels of government/agencies> Non-tax incentives e.g., grants often most

lucrative> Binding contract with state or local

governments

37

State and local C&I trends

> Major job creation– Grow New Jersey Assistance Program

Save Colorado Jobs program– Save Colorado Jobs program > Green and renewable energy

– Florida investment and renewable energy production credit– Utah alternative energy development and manufacturing creditgy p g– Incentives for agricultural waste and biomass processing, and energy

production e.g., New Mexico, Oregon, Wisconsin

38

State and local C&I trends

> Manufacturing – Wisconsin production activities and targeted industries tax credits

(dairy product manufacturing, meat processing, food processing)(dairy product manufacturing, meat processing, food processing)> Technology

– Alabama and Nebraska data center tax incentive programs – Louisiana digital interactive media and software

f hi /i t ditfranchise/income tax credit> Enterprise and development zones

– Pennsylvania expansion of Keystone Opportunity Program– California authorizes new enterprise zonesCalifornia authorizes new enterprise zones – Michigan Community Revitalization Program

39

State and local C&I trends

> Venture capital – InvestMaryland program is making $84 million of venture capital

available to life sciences and technology businessesavailable to life sciences and technology businesses> Small business

– Virginia grant program for investments in small businesses> Assistance benefitting veterans

– Alabama, New Mexico, Utah, and Wisconsin recently enacted targeted tax credits for hiring unemployed or disabled veterans

> Health and wellness– Maryland’s Health Enterprise Zone program provides income taxMaryland s Health Enterprise Zone program provides income tax

credits to certified heath care practitioners

40

State and local C&I trends

> Increased accountability and transparency– Recapture (“clawback”) clauses in C&I agreement

Compliance and information reporting– Compliance and information reporting– Budget caps and allotments e.g., Wisconsin Food Processing and

Warehousing Credit– Sunset provisions – Oregon BETC program– Repeal or “downsizing” of C&I programs perceived to be ineffective

e.g., Arizona repeal of its film production credits> Transferability of tax credits and incentives

– Liability for penalties and interest passed to purchaser of tax credits y p p pacquired from original claimant. (Kowalchik v. Brohl, Colo. Ct. App., No. 11CA2634, 3/15/12)

41

Top credits and incentives

atio

n”

C h t dJobs credits –

C&I awards with greatest impact

P t t

“job

s cr

ea Cash grants and forgivable loans

IRBs or private activity

refundable vs. nonrefundable

Property tax abatements

Tax incremental Green and renewable

hwor

d is

“ IRBs or private activity bonds

Tax incremental financing

Green and renewable energy incentives

Investment andE t i Z

Training funds – In-kind incentives i f t t

Wat

ch Enterprise Zone credits

ggrants and subsidies e.g., infrastructure

improvements

42

Tax Increment Financing

43

TIF basics

What is Tax Increment Financing?> TIF is an economic development tool that allows local

governments to capture an increase in property taxes (and ingovernments to capture an increase in property taxes (and in some states, other types of incremental taxes) and invest the funds in infrastructure and other public improvements (which may include business incentives)

> TIF Districts are created around geographic areas that are proven to have a need for economic development (determined by different factors in each state)

44

TIF basics (cont.)

5

45

TIF basics (cont.)

Examples of eligible uses for TIF funds (varies by state)

> Infrastructure> Financing costs> Property assembly, site preparation, and building demolition> Professional services> Ad i i t ti d i ti l t> Administrative and organizational costs> Relocation costs> Environmental clean-up> Public facilities> Public facilities> Affordable housing> Building renovation and rehabilitation> Business incentives

2

> Business incentives

46

TIF incentives

TIF business incentives> May be available when investment activities result in increased

property taxes (or other taxes as allowed in certain states)property taxes (or other taxes as allowed in certain states)> May be available if the project is located in an existing TIF

District or in an area that can qualify for the creation of a new District (qualifications vary by state)

> Discretionary incentive that can vary significantly depending on municipal objectives and financial health; typically range from 5%-20% of total project costs

> May be structured as a direct business incentive or as> May be structured as a direct business incentive or as reimbursement for public improvements/infrastructure.

> May be structured as a grant or a loan and can be paid upfront or over time

5

47

TIF incentives

Incentive examples

Capital investment Project costs TIF incentive

Corporate headquarters $50 million $14.6 million

M f t i f ilit $44 illi $3 6 illiManufacturing facility $44 million $3.6 million

Residential development $24 million $3.1 million

Commercial development $30 million $4.4 million

5

48

TIF incentives (cont.)

Upfront financial incentiveThe municipality incurs debt or draws on existing funds and

provides the business incentives upfront.> Traditional approach> Riskier for the municipality> Often req ires a corporate or personal g arantee from the> Often requires a corporate or personal guarantee from the

recipient (minimum assessment or tax payment)> More common to fund public improvements rather than

incentives

6

49

TIF incentives (cont.)

PayGo financial incentiveThe municipality pledges a certain amount of the annual

incremental taxes to the business. > Shifts the risk to the business> Creates incentive for business to perform> B siness often borro s against the pledged ann al increment> Business often borrows against the pledged annual increment> Becoming the prominent approach to funding incentives

6

50

TIF incentives (cont.)

Nonfinancial incentivesThe municipality may provide other types of incentives

including: > Land> Site improvements> Off site infrastr ct re impro ements> Off-site infrastructure improvements> Other incentives unique to the project needs (master lease,

relocation costs, etc.)

6

51

TIF incentives (cont.)

Development agreementsWhen a business is receiving TIF incentives, a development

agreement is executed that outlines the responsibilities of the business and the municipality related to the incentive. Key components of a development agreement may include:

> Business’s obligations> Business s obligations> Incentive to business> Municipality’s obligations> Timeline for project and paymentse e o p oject a d pay e ts> Clawbacks and protections> Equity kickers and cash flow participation

6

52

TIF incentives (cont.)

Business ObligationsThe development agreement will outline the business’s

obligations regarding the project. Examples of obligations include:

> Corporate or personal guarantee on a minimum assessment level or tax paymentor tax payment

> Prevailing wage requirements> Additional building or site design standards> Housing affordability and adaptability requirementsg y p y q> Green or sustainability requirements> Requirements to use minority, disadvantaged, or local contractors> Additional reporting and inspection requirements

6

53

C&I strategies and pitfalls

54

Public sector: Reason for credits and incentives

> Why do state and local governments offer credits and incentives?– Attract investment from other jurisdictions

Reward job creation and retention– Reward job creation and retention– Stimulate venture capital investments– Encourage development of economically disadvantaged or blighted

areas– Target specific industries or types of activity e.g., biotechnology,

tourism, corporate headquarters, historic preservation– Enhance quality of life or wellness of residents

55

Developing a C&I strategy

> Compile solid data and information about project e.g., amount of investment, number of jobs

> Develop a compelling story!> Develop a compelling story!> Research state-local tax impacts for potential sites or retain outside

expertise> Learn about available incentives. > Piggyback on federal C&I programs e.g., NMTC in Maine and

Nebraska> Identify points of contact with state, regional, and local officials:

Who will be the “quarterback”?Who will be the quarterback ?> Plan meeting with state and local officials at one or more sites > Possible tour of available sites – lease, buy, or build?

56

Developing a C&I strategy

> Request preliminary C&I proposal> Prepare application and gather requested financial and operational

datadata> Second round information requests> Anticipate “trouble spots” e.g., recent job reductions, environmental

issues> Finalize C&I package through contracts and final applications> Review by outside or corporate legal counsel> Ongoing compliance e.g., annual certification of jobs

dd d/ t i d l d dd d t itadded/retained, valued added to site

57

Avoiding pitfalls during the C&I process

Before negotiations – Activities/issues that may compromise C&I efforts> Signing a lease> Signing a lease> Pulling building permits> Putting property in service> Hiring employees or placing help-wanted ads> Hiring employees or placing help-wanted ads> Purchasing land> Negotiating contracts with local builders and merchants> Press announcementsPress announcements> Financial disclosure requirements?

– Business entity– Owner’s personal financial data

58

Avoiding pitfalls during the C&I process

During negotiations> Proper completion of forms and supplying accurate information> C di ti f ti A t lki ith th i ht l ?> Coordination of meetings – Are you talking with the right people?> Meet time deadlines for submitting applications and requested

documents> Appearance before political bodies might be required e g TIF> Appearance before political bodies might be required e.g., TIF> Understanding financial impact on your business> State and local fiscal and economic impacts – have a proper

analysis “at the ready”> What job quality and employee welfare questions could be directed

at you?> Strategy for addressing past issues or perceived problems

59

Avoiding pitfalls during the C&I process

After negotiations> Timing – target date for moving forward with project> A l C&I t l l ( i b l l d i ?)> Analyze C&I agreement closely (review by legal advisor?)> Compliance requirements and reporting

– What reports/forms have to be filed and by what date?– Attestation or certification required by CPA or outside agency?Attestation or certification required by CPA or outside agency?

> Consequences of not meeting thresholds– Mitigation provisions in agreement?– Notification requirements? – Clawbacks?

> Transferability of tax credits and/or incentives

60

Be aware of “clawbacks”

> “Clawbacks” – repayment or recapture provisions of C&I contracts

– Performance based (automatic)Performance based (automatic)– Results based (optional)– Prorata– Statutory penalties

> Analyze in context of ROI– Can the clawback provision be negotiated?– Mitigation/hardship provisions?

61

C & I example

Approach> Baker Tilly conducted a multistate tax and

cost analysis of sites in seven states; two states were selected as the most suitable

> A preliminary review was performed of the dit d i ti il bl i b th

PROJECTBaker Tilly represented a large manufacturer credits and incentives available in both

> Baker Tilly made initial contact with state economic development officials and confirmed available credits & incentives

> Coordinated visits to various sites for

a large manufacturer opening a new plant that involved 110 new jobs and over $30 million of new investment in > Coordinated visits to various sites for

purchase and for lease> Prepared DCF analysis of various

incentives and credits offered> Assisted client with the buy vs. lease

of new investment in plant, equipment and working capital

Assisted client with the buy vs. lease decision; including analysis of local property tax burden

> Reviewed final package of credits and incentives as well as contract with state economic development agency

62

C & I example (cont.)

Results> Company obtained a C&I

commitment with a net profit

PROJECTBaker Tilly represented a large manufacturer commitment with a net profit

value of between $3.5 million. Included: cash award of $800,000, training grants, partial property tax abatement,

l / t f d d d

a large manufacturer opening a new plant that involved 110 new jobs and over $30 million of new investment in sales/use tax refunds, expanded

R&D credit, investment credits, jobs credits, and in-kind assistance e.g., state assistance with screening qualified job

of new investment in plant, equipment and working capital

g q japplicants.

63

Questions?

6464

Contact information

Moderator Panelist PanelistPanelist

Gina Staudacher Jon Skavlem Kate Crowley Ellen Ernst312 729 8182

[email protected] 777 5333

y608 240 6718

[email protected] 729 8148

65

Disclosure

The content in this presentation is a resource for Baker Tilly Virchow Krause, LLP clients and prospective clients. Nothing contained in this presentation shall be construed as legal advice, opinion, or as an offer to buy or sell any property or services. In conformity with U S Treasury Department Circular 230 tax advice contained in thisIn conformity with U.S. Treasury Department Circular 230, tax advice contained in this communication and any attachments is not intended to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code, nor may any such tax advice be used to promote, market or recommend to any person any transaction or matter that is the subject of this communication and any attachments. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.

6666