housing wealth isn’t wealth

DESCRIPTION

Housing Wealth Isn’t Wealth. Willem H. Buiter, 2008 Presentation by Aleksey M. Martynyuk. Summary. Background Housing Wealth – Life-cycle Hypothesis Paper’s Summary Related Findings Conclusion. Life-Cycle Hypothesis. Households smooth out fluctuations in current income - PowerPoint PPT PresentationTRANSCRIPT

Housing Wealth Isn’t WealthWillem H. Buiter, 2008

Presentation by Aleksey M. Martynyuk

Summary

• Background• Housing Wealth –

Life-cycle Hypothesis• Paper’s Summary• Related Findings• Conclusion

Life-Cycle Hypothesis

• Households smooth out fluctuations in current income

• Changes in wealth are built into consumption plans; unanticipated changes lead to a revision of those plans

Wealth Effects

• Direct Wealth Effects

• Credit Constraint Channel

• Common Cause Channel

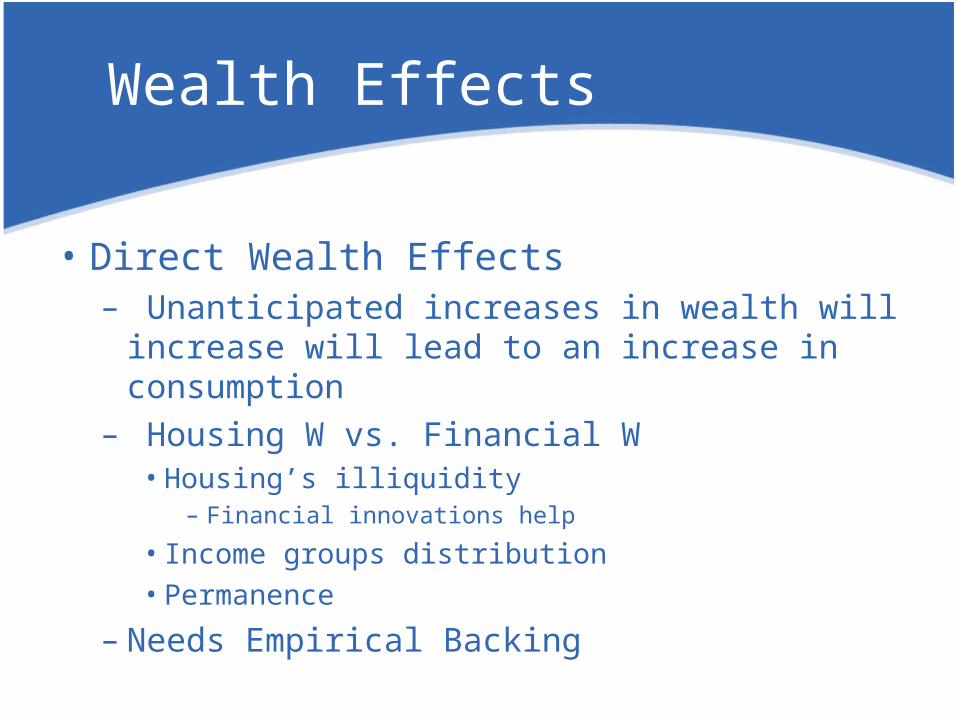

Wealth Effects

• Direct Wealth Effects– Unanticipated increases in wealth will increase

will lead to an increase in consumption– Housing W vs. Financial W• Housing’s illiquidity

– Financial innovations help

• Income groups distribution• Permanence

– Needs Empirical Backing

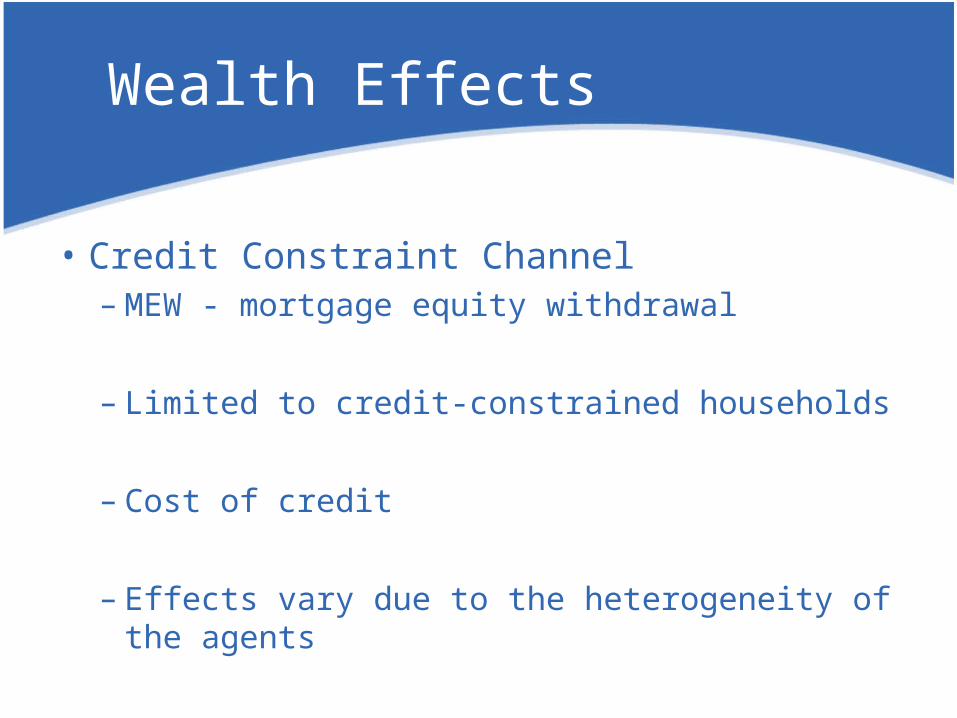

Wealth Effects

• Credit Constraint Channel– MEW - mortgage equity withdrawal

– Limited to credit-constrained households

– Cost of credit

– Effects vary due to the heterogeneity of the agents

Wealth Effects

• Common Cause Channel– Financial Liberalization– Increase in both secured (collateralized) and

unsecured debt– Consumption increase for all agent

– Real interest rates, productivity shocks, expectations

Buiter’s position

“In a representative agent model, a decline in house prices does create a negative wealth effect on aggregate consumption demand. On average, consumers are neither worse off nor better off.”

Buiter’s position

“The fundamental value of a house is the present discounted value of its current and future rentals, actual or imputed.”

Buiter’s position

• Consumer durable example

• Long housing vs. Short housing

• Landlords vs. Tenants

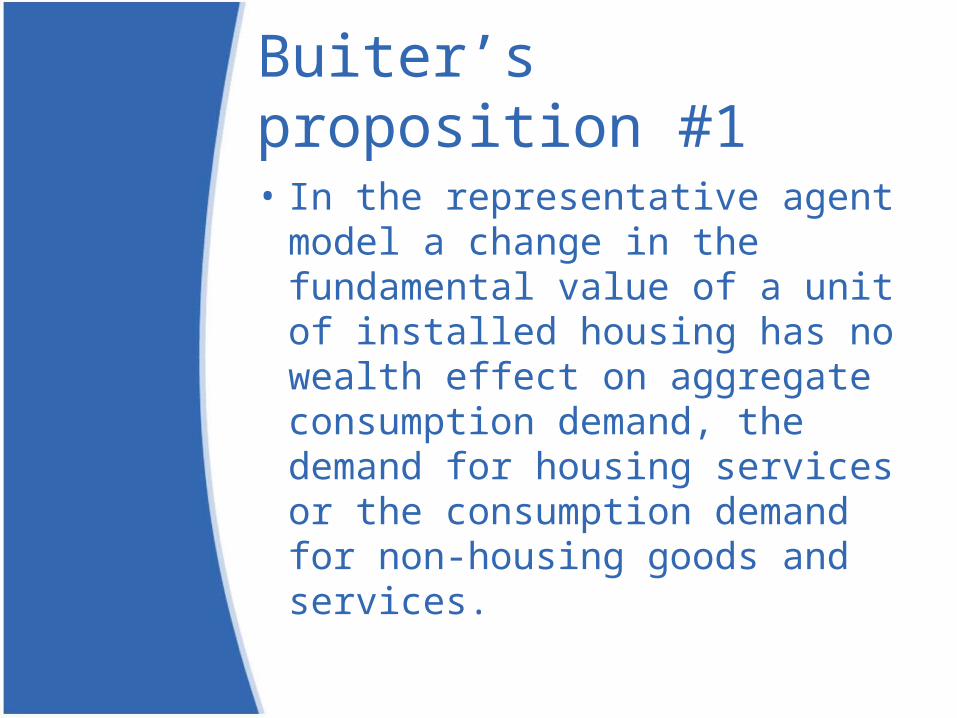

Buiter’s proposition #1

• In the representative agent model a change in the fundamental value of a unit of installed housing has no wealth effect on aggregate consumption demand, the demand for housing services or the consumption demand for non-housing goods and services.

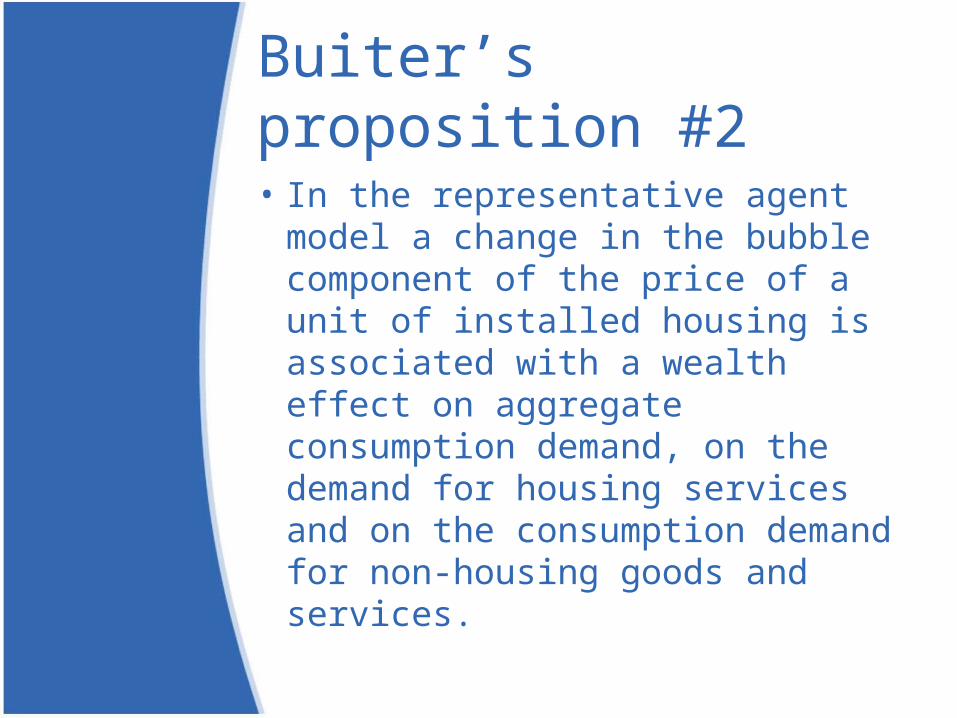

Buiter’s proposition #2

• In the representative agent model a change in the bubble component of the price of a unit of installed housing is associated with a wealth effect on aggregate consumption demand, on the demand for housing services and on the consumption demand for non-housing goods and services.

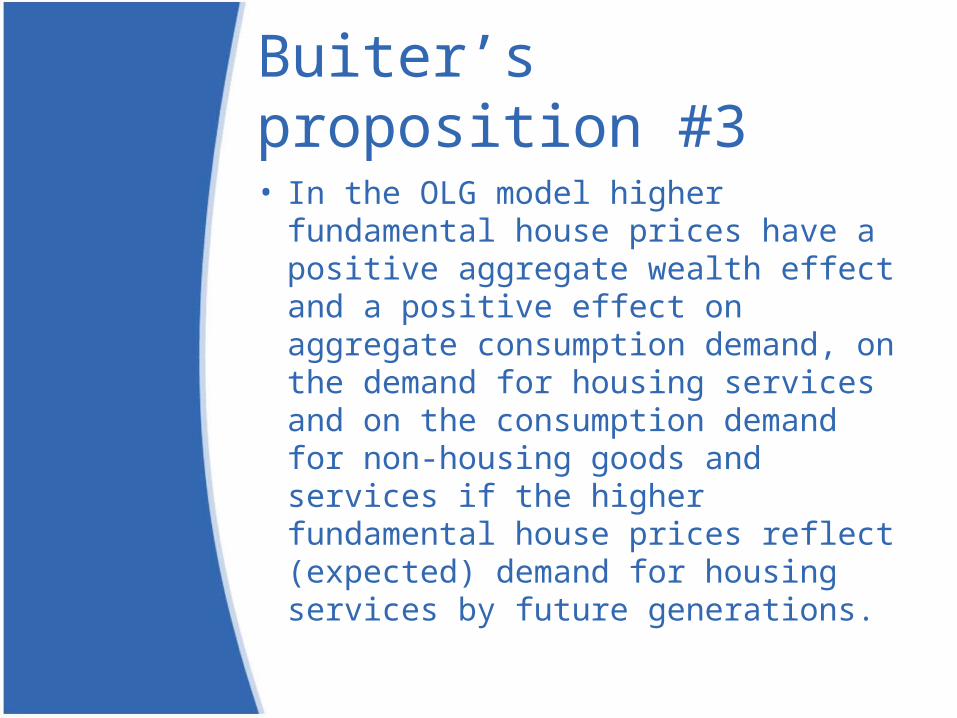

Buiter’s proposition #3

• In the OLG model higher fundamental house prices have a positive aggregate wealth effect and a positive effect on aggregate consumption demand, on the demand for housing services and on the consumption demand for non-housing goods and services if the higher fundamental house prices reflect (expected) demand for housing services by future generations.

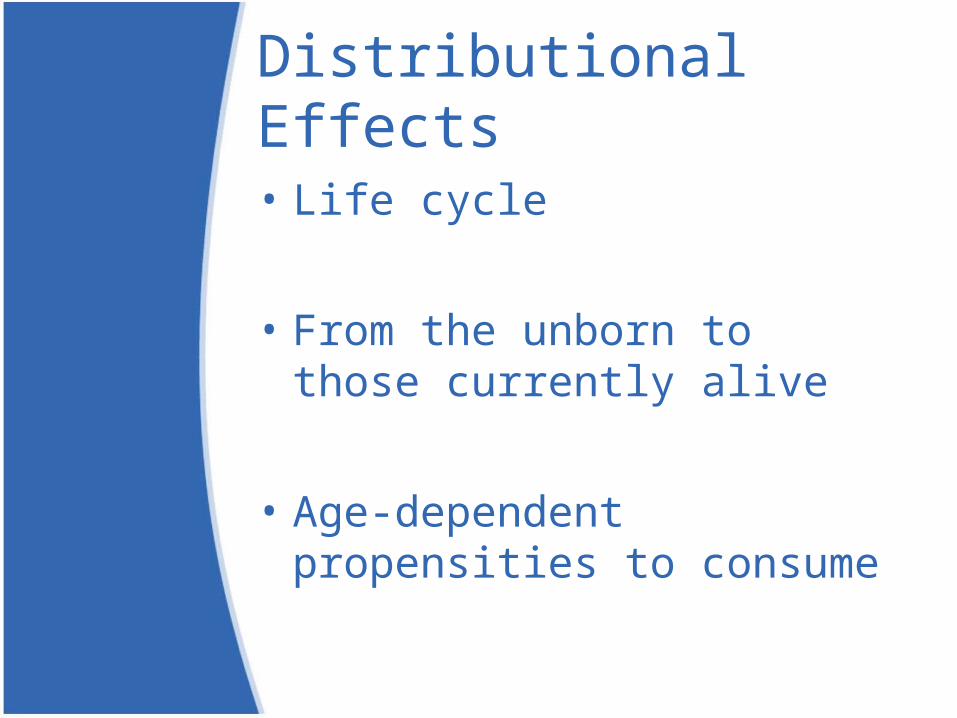

Distributional Effects

• Life cycle

• From the unborn to those currently alive

• Age-dependent propensities to consume

Age-dependent propensities to consume

• Older generation might have a higher propensity to consume

• Younger generation might be liquidity-constrained

Conclusion

• No change in consumption on aggregate

• Redistribution of wealth between long-housing and short housing

• Pure wealth effect if bubble is present

• Two indirect channels:– Difference in MPC– Credit effects