how fragile is britain’s recovery? · how fragile is britain’s recovery? ... taped in a...

TRANSCRIPT

97

71

47

22

06

08

5

>5

0

ww

w.m

on

eyw

eek.

com £3.45

How fragile is Britain’s recovery?How fragile is Britain’s recovery?

13 December 2013 Issue 670 Britain’s best-selling financial magazine

Matthew Lynn: Politicians should get out of the housing market P16

Opinion: Bitcoin may be as big as the internet P22

Profile: The billionaire backing Bob Diamond in Africa P32

HOW TO MAKE IT, HOW TO KEEP IT, HOW TO SPEND IT

13 December 2013 Issue 670 Britain’s best-selling financial magazine

Page 24Page 24

Politicians Opinion: may be as big as the internet

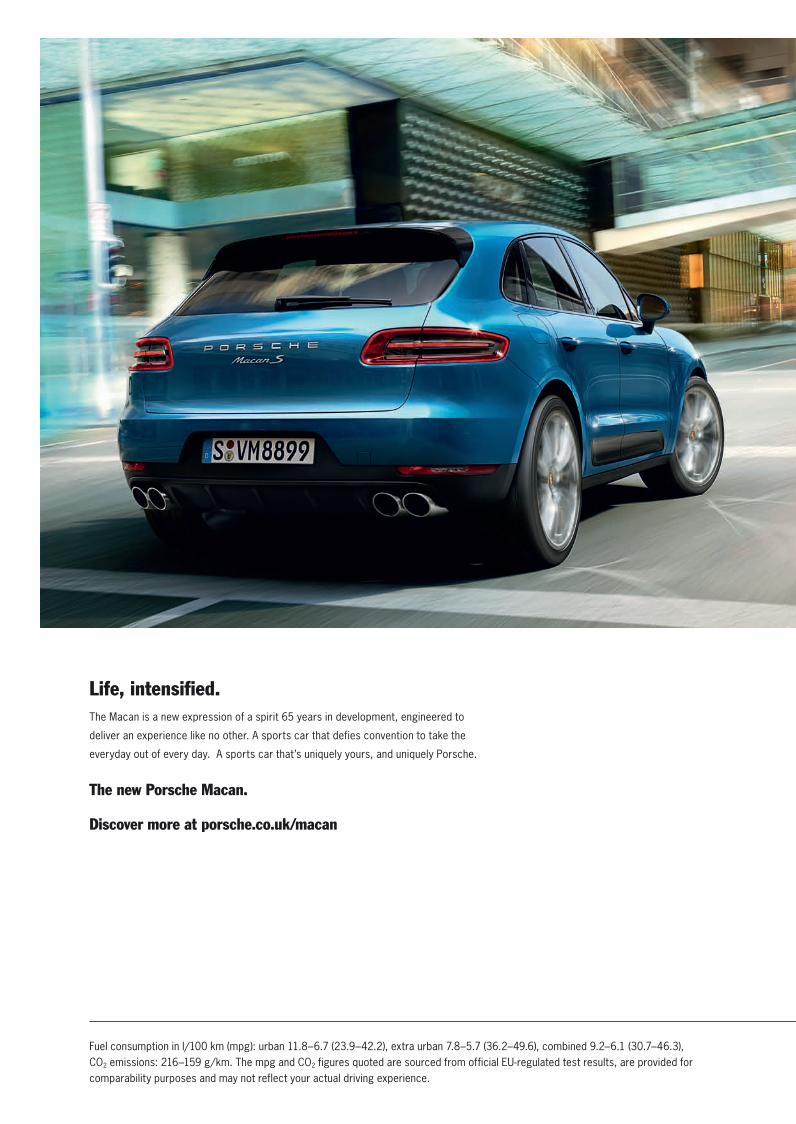

Fuel consumption in l/100 km (mpg): urban 11.8–6.7 (23.9–42.2), extra urban 7.8–5.7 (36.2–49.6), combined 9.2–6.1 (30.7–46.3), CO2 emissions: 216–159 g/km. The mpg and CO2 figures quoted are sourced from official EU-regulated test results, are provided for comparability purposes and may not reflect your actual driving experience.

Life, intensified.The Macan is a new expression of a spirit 65 years in development, engineered to

deliver an experience like no other. A sports car that defies convention to take the

everyday out of every day. A sports car that’s uniquely yours, and uniquely Porsche.

The new Porsche Macan.

Discover more at porsche.co.uk/macan

11132 Mac_NatAd3_DPS_297x420-left MoneyWk.pdf 1 28/11/2013 12:05

11132 Mac_NatAd3_DPS_297x420-left MoneyWk.pdf 2 28/11/2013 12:05

www.moneyweek.com 13 December 2013 MoneyWeek 5

Poor Hugh Hendry. The Eclectica hedge fund manager was one of the most vocal proponents of the bear case before the credit crunch, and gained lots of media exposure for his straight-talking put-downs of pompous talking

heads during the eurozone crisis. But now he’s been forced to throw in the towel by the Fed’s endless money-printing. As we note on page 8, it’s not that Hendry has turned bullish – he still thinks everything will end badly. But while the printing presses are running hard, he doesn’t see any benefit to fighting the world’s central banks as governments across the globe compete for growth by devaluing their currencies.

Hendry’s dilemma sums up the problem with bubble spotting. You might be certain that a market is being propped up artificially, and that the fundamentals are firmly against it. But how can you tell when the fundamentals will reassert themselves? You can’t. Sure, there are often psychological cues that suggest a bubble’s days are numbered. The mass scorn that greeted the brave souls who stepped into the market at its low is now aimed at the bears. At the bottom, all you hear are arguments that begin: “Yes, the market looks cheap, but...” At the top, the arguments begin: “Sure, the market looks expensive, but...”

So what do you do? Well, the good news is that, unlike most fund managers, no one pressurises you to be in any particular market

How to spot cheap marketsif you don’t think it is good value. So if you don’t see any opportunities, you can just be patient. Secondly, while the US stockmarket certainly looks expensive, there are still some cheap and hated markets out there that should offer good returns in the long run. A piece in The Wall Street Journal this week sums it up. On the one hand it argues that, while the cyclically adjusted price/earnings (Cape) ratio implies that US “stock returns in the near future will be lower than average... the ratio has gone much higher than its current level during past rallies”. Which sounds a lot like a “the market is expensive, but...” argument to me. On the other hand, in the same piece, various ‘experts’ warn sagely that the Cape isn’t reliable for overseas markets, even though they look cheap.

But the actual data suggest that’s nonsense. According to fund manager Mebane Faber, at the end of 2012 Greece, Ireland, Argentina, Russia and Italy were the cheapest markets in the world, on Cape.

By 4 December all but Russia (down 7.9%) had gained at least 14% – Ireland was up 40%. Meanwhile, the most expensive markets – Peru, Colombia, Indonesia, Mexico and Chile – had all fallen. Mexico was down by just 3%, but the others shed at least 16% (Colombia) and as much as 31% (Peru). As for the year to come, the cheap markets line-up remains the same. Many of you will know I favour Italy, but I’m increasingly tempted by Russia too. As for the most expensive market? It’s the US.

from the editor

13 December 2013 ISSUE 670Editor-in-chief:

Merryn Somerset Webb

Editor: John StepekMarkets editor: Andrew Van Sickle

Senior writers: Phil Oakley, Matthew Partridge

Contributors: Emily Hohler, Ruth Jackson, Jane Lewis, Simon Wilson, Piper Terrett

Digital managing editor: Ed BowsherWebsite editor: Ben Judge

Web production assistant: Chris CarterAdministrative assistants:

Nehal Patel, Sophie Crooks

Production editor: Stuart Watkins Chief sub-editor: Joanna GibbsArt director: Kevin Cook-Fielding Picture editor: Natasha Langan

Founder and editorial director: Jolyon Connell

Publisher: Bill Bonner

Managing director: Toby Bray Advertising sales director: Simon Cuff (020-7633 3720)

Head of marketing:Ryan McErlean (020-7633 3764)

Marketing manager: Vilte Burneikaite, Marketing executive: Hannah Jordan

Head of digital:Sarah Pott (020-7633 3682)

Editorial queries: Please note: Our staff are unable to respond to readers’ personal investment queries as

MoneyWeek is not authorised to provide individual investment advice.

Email: [email protected]: 020-7633 3651

Post: please use address below

Subscriptions & Customer Services

Telephone: 020-7633 3780 Mon-Fri, 9.00am – 5.30pm

(Wed, 9.00am – 2.00pm only)Website: contactus.moneyweek.com

Post: please use address below

Subscription costs: £89.95 a year (credit card/cheque), or £19.95 every 13 issues (direct debit).

MoneyWeek is published by:

MoneyWeek Ltd, 8th Floor, Friars Bridge Court, 41-45 Blackfriars Road,

London SE1 8NZ.

MoneyWeek and Money Morning are reg-istered trade marks owned by MoneyWeek

Limited.©MoneyWeek 2013

ISSN: 1472-2062• ABC, Jan - Jun 2013: 52,027

MoneyWeek magazine is an unregulated product. Information in the magazine is for general informa-tion only and is not intended to be relied upon by

individual readers in making (or not making) specific investment decisions. Appropriate independent

advice should be obtained before making any such decision. MoneyWeek Ltd and its staff do not

accept liability for any loss suffered by readers as a result of any investment decision.

9 Markets Nelson Mandela took South Africa a long way – but it still has far to go.10 Strategy What are split caps and are they worth investing in?12 Shares in focus This builders’ merchant is still booming.18 Briefing The drive to free up more of our data for the common good.29 Personal finance How to make the

most of your savings.35 Travel A trip to Copenhagen is the perfect way to get in the Christmas spirit.38 Christmas gifts If you’re looking for a truly tasty treat, try one of these hampers.41 Blowing it Is rampant consumerism a sign of a civilisation in decline?46 Last word First the pope, now Barack Obama: who wants to live in North Korea?

In this issue

John Stepekemail: [email protected]

“How can you tell when the

fundamentals will reassert themselves?

You can’t”

Cove

r illu

stra

tion:

Ada

m St

ower

.

6 MoneyWeek 13 December 2013 www.moneyweek.com13 December 2013 www.moneyweek.com

news

Housing rebound has slowed but not stopped

US economic data have continued to improve. Payrolls grew by 203,000 in November and t he unemployment rate declined to a five-year low of 7%. The University of Michigan’s gauge of consumer sentiment climbed to a five-month high. An index tracking manufacturing activity is at a two-and-a-half-year high. Annualised GDP growth accelerated to 3.6% in the third quarter.

What the commentators said“Never mind” government budget cuts and October’s shutdown, said Economist.com’s Free Exchange blog. The economy is “plugging along at a surprisingly steady clip”. The housing recovery has lost a little momentum of late as mortgage rates have risen, while corporate America still seems to be “hunkering down and curbing capital spending”. But the employment recovery and the decline

©B

loom

berg

in inflation, boosting real incomes, are underpinning household spending.

Meanwhile, the outlook is encouraging, according to Capital Economics. September and October saw a surge in building permits, suggesting that higher mortgage rates have simply dampened, rather than choked off, the housing rebound. The fiscal drag from Washington is also set to ease over the next 12 months after this year’s cuts. That should outweigh any further increase in long-term interest rates.

That’s because the US Federal Reserve has made it clear that its benchmark interest rate is set to stay at near-zero for another two years, and liquidity-addicted markets have twigged that tapering quantitative easing – reducing the pace of money printing, as the Fed is likely to do soon – is not the same thing as tightening policy. So another sharp jump in long-term interest rates, as occurred when markets confused tapering with tightening earlier this year, is unlikely.Consequently, 2014 “could be the year that the recovery finally shifts into top gear”, concluded Capital Economics.

The recovery gathers pace

Clampdown on Wall Street Four years after it was first proposed, US regulators have approved the Volcker Rule. Named after the former chairman of the US Federal Reserve, this bans banks from making bets with their own money – proprietary (prop) trading – in

order to reduce the likelihood of Wall Street’s big players engaging in overly risky activity and requiring a bailout.

What the commentators saidWhat pointless “crowd-pleasing tokenism”, said Allister Heath in City AM. Property and small business lending “have sunk far more banks than trading ever has”. That certainly applied in the global crisis, when loan losses vastly outweighed trading losses. “Proprietary trading did not cause the recession or the bail-outs.”

Still, as the FT pointed out, implicit state guarantees for big banks and lax regulation of prop trading helped fuel the credit bubble. But turning the Volcker rule into a workable law has proved “fiendishly difficult”. A key issue is deciding what constitutes prop trading and what is market making, whereby a bank buys and sells assets for clients.

For instance, said The Daily Telegraph, the process of making a market, or establishing a price, for a client will often involve the firm holding a certain amount of the product on its own balance sheet. “How do you know whether a certain amount of overstocking might amount to no more than an optimistic view on trading volumes rather than an outright bet on... the product’s price?

Practical difficulties notwithstanding, said David Reilly in The Wall Street Journal, the Volcker rule will be worthwhile if it marks a first step towards stopping banks having their fingers in so many pies that they become

America

£800 The value of the cocaine the former X-factor judge Tulisa Contostavlos (pictured) is charged with supplying. She was arrested in June after being secretly taped in a newspaper sting allegedly boasting that she could get the drug for an undercover reporter.

£11m How much a failing Shropshire construction company claimed an £8,000 ruby was worth in order to inflate its accounts.

$500,000 How much loose change was left at security

checkpoints in American airports in the year to October.

$2.50 The typical wage in Mexico’s manufacturing sector – around a fifth lower than in China. Mexico’s share of North America’s auto jobs has jumped from 12% to 39% since 2000.

52 How many laws the US Congress has

passed in 2013, its least productive year since 1945.

£3.65 What a half litre of vodka will cost in Russia from 1 January. The price will then climb further, to £4.25, in August 2014. The government is trying to clamp down on alcohol addiction, which plays a part in 30% of deaths.

6,000 How many Western tourists have visited North Korea this year, up from 700 in 2004.

£80 What a hand from the Lenin statue destroyed by protesters in Kiev was on sale for on a Ukrainian website this week.

The bottom line ©

Rex

Fea

ture

s

www.moneyweek.com 13 December 2013 MoneyWeek 7

news

● The way we live nowBritain’s first “social supermarket” has opened its door in Yorkshire. It sells, at hefty discounts, major retailers’ surplus food and household products that would normally be thrown away: excess produce created by forecasting errors, seasonal promotions, or packaging faults. Only people on means-tested benefits can apply to become a member of the discount store. “We are aiming to fill a gap between food banks and mainstream retail,” said Sarah Dunwell of Company Shop, which runs the scheme. “Lots of families are not in an emergency situation but are on the cusp of food poverty.”

Renzi: can he help push through reform?

©G

etty

Imag

es

Italy crawls out of recessionItaly’s two-year recession is over. According to revised data, GDP was unchanged in the third quarter of 2013 compared to the previous three months. Companies have begun to spend again: industrial production expanded by 0.5% in October. A forward-looking survey of activity in the sector rose to a two-and-a-half-year high. However, the Italian economy is still 7.3% smaller than at its pre-crisis peak and has barely expanded in the past 20 years. Meanwhile, Matteo Renzi, the 38-year-old mayor of Florence, has been chosen as the new leader of the centre-left Democrats.

What the commentators saidThe recession may be over, said Alen Mattich in The Wall Street Journal, but “normal growth is still a long way off”. Exports have ticked up but the domestic economy remains subdued due to a “crippled banking sector”, which continues to withdraw credit from the economy. The International Monetary

Fund expects Italy to grow by 0.7% next year and then by 1% a year – the glacial pace common before the crisis.

Another key reason for that is the long list of urgently needed structural reforms to raise Italy’s long-term growth potential, and thus allay fears that Italy will eventually go bust. The reforms are wearingly familiar, said Hugo Dixon on Breakingviews: privatisations to cut debt; lowering employment taxes and dismantling red tape in the labour market to encourage hiring; exposing a series of cossetted professions to competition; making the business start-up process easier; and reforming the judicial system.

These changes are all the more urgent now because Italy is unique in Southern Europe in having seen no improvement in its competitive position in the past five years, noted Simon Nixon in

EuropeThe Wall Street Journal. The difficulty is confronting the vested interests, notably unions and employers, who have blocked previous reform attempts. The hope is that Prime Minister Letta, possibly galvanised by Renzi, will be able to push through changes now that the influence of his predecessor, Silvio Berlusconi, has waned. Given the evidence of recent years, however, we probably shouldn’t hold our breath.

©C

omm

unity

Sho

p

% change

FTSE 6,549.13* 0.94%**

Nikkei 15,515.06 0.70%

S&P 500 1,802.62 0.42%

Nasdaq 4,060.49 0.58%

CAC40 4,123.40 -0.12%

Dax 9,148.65 0.39%

$ per e 1.38 2.22%

e per £ 1.19 -1.65%

$ per £ 1.63 -0.61%

Gold ($ per oz) 1,256.36 2.86%

Brent crude oil ($) 108.90 -2.52%

*11 December **since 4 December

Winners % change

Price

Hargreaves Lansdown (HL) 5.77% 1,284p

Smiths Group (SMIN) 5.38% 1,411p

Persimmon (PSN) 4.46% 1,194p

Schroders (SDR) 4.37% 2,486p

TUI Travel (TT) 4.21% 384p

Weir Group (WEIR) 4.08% 2,142p

Sports Direct (SPD) 3.93% 766p

Experian (EXPN) 3.81% 1,118pRoyal Dutch Shell B (RDSB)

3.67% 2,177p

Royal Dutch Shell A (RDSA) 3.52% 2,086p

Losers % change Price

Next (NXT) -1.89% 5,440p

Tullow Oil (TLW) -1.94% 859p

Reckitt Benckiser (RB) -1.95% 4,722p

Imperial Tobacco (IMT) -2.22% 2,249p

Tesco (TSCO) -2.26% 332p

Marks & Spencer (MKS) -2.42% 464p

William Hill (WMH) -2.56% 377p

Aggreko (AGK) -3.00% 1,552pStandard Chartered (STAN)

-4.00% 1,285p

Vedanta Resources (VED) -4.67% 806p

Best and worst-performing shares

Weekly change to FTSE 100 stocks. Prices as of midday 11/12/13

Vital numbers

too big to fail. Why, for instance, are they allowed to run their own fund management arms, when implicit government backing gives them an advantage over stand-alone firms and encourages risk taking? And shouldn’t other companies, rather than banks, handle market making? We must get “banks back to being banks”.

8 MoneyWeek 13 December 2013 www.moneyweek.com

“It is past time to recognise the deflation danger facing Europe,” says French economist Jean Pisani-Ferry. In November, the annual inflation rate in the eurozone had slid to 0.9%. In the autumn of 2012, it was over 2%. Greece, Ireland and Cyprus have already suffered outright deflation (falling prices). On current trends, Spanish and Italian prices will soon be falling. With demand so subdued, inflation is set to keep melting away, says Capital Economics.

The main danger with deflation is that it raises the real value of a fixed sum of debt. So the huge debt burdens already crushing the south will grow. And if the economy is already shrinking, debt as a proportion of GDP will soar. Italy’s public debt, for instance, has risen from 119% of GDP to 133% in just over two years, says Ambrose Evans-Pritchard in The Daily Telegraph. With the south in the grip of deflation, concerns that these countries will default could rapidly return, sending bond yields, or long-term interest rates, upwards and further undermining economies.

Meanwhile, the periphery can’t get its debt written off and can’t inflate its way out. Eurozone countries have no control over interest rates and no longer have

their own currency. With Europe far more export-dependent than other regions, the south desperately needs a weaker euro to fuel a recovery.

Unfortunately, the euro has climbed by 6% against the dollar this year. A strong currency negates any gains in competitiveness stemming from reduced labour costs. According

to France’s industry minister Arnaud Montebourg, every 10% rise in the euro costs France 150,000 jobs. Evans-Pritchard highlights a Deutsche Bank study noting that Germany can cope with a euro-dollar rate of up to $1.79, while the “pain threshold” for France and Italy is a respective $1.24 and $1.17. The rate is currently $1.37. And a high currency reduces inflation further.

With interest rates already at rock-bottom and banks still reluctant to lend, the only way the European Central Bank (ECB) can help the weaker states is by weakening the currency. The trouble is that, having promised to do “whatever it takes” to save the eurozone, the foreign-exchange markets appear to be testing the ECB’s resolve by keeping the euro buoyant. The current state of affairs makes it more likely that the ECB will be forced into quantitative easing – which bodes well for European stocks.

markets

Last bear standing throws in the towelHugh Hendry has been bearish for years. Rattled by the debt build-up before the global crash, the founder of Eclectica Asset Management cashed in on his scepticism as his contrarian strategy gave him a 30% return in 2008.

So this week’s news that the self-styled “last bear standing” has thrown in the towel raised eyebrows. But he hasn’t suddenly decided that everything is fine. “It will all end badly,” he says of the current market rebound, because the fundamentals remain lousy. But he is “tactically bullish” for now because it’s become increasingly clear that the world’s central bankers will keep this party going for as long as possible. That gives equities plenty of scope for further gains. “Stronger growth in one part of the world… will be countered by even looser policy elsewhere.” Overall, then, tighter policy will keep getting postponed.

This macro environment, along with the recent pattern displayed by US stocks, means that “markets look to us much as they did in 1928 or in 1998” – a major spurt away from the top. Japan could be especially promising, Hendry reckons, not because Abenomics will work, but because it won’t. That would imply panic-stricken “money printing without limit”. Hendry is betting on the Nikkei hitting 40,000 by April 2018.

The euro: dangerously buoyant

©B

loom

berg

Europe’s deflation danger

Dow Jones index adjusted for inflation20,000

500

1,000

2,000

3,0004,0005,000

10,000

15,000

1900 2010 30 40 50 60 70 80 200090 10 20Source: chartoftheday.com

Chart of the week: Dow is treading waterInvestors are only really growing their cash pile if their returns beat inflation. So it’s interesting to note that for all the talk of new all-time highs in US markets in recent months, the Dow Jones index is only just back to its 1999 record if inflation is taken into account. The 1999 peak in real terms was 16,261. So the index has been treading water for 14 years. This period of drift followed the biggest bull market on record, a surge from 2,000 to almost 16,000 over 18 years.

www.moneyweek.com 13 December 2013 MoneyWeek 9

South Africa’s transition to a multi-racial free-market democracy was “a near-miracle for which the whole world must thank” Nelson Mandela, says The Economist. He ditched the Communist economic dogma of the liberation movement the ANC before assuming power. The ANC’s embrace of largely market-friendly policies, buttressed by sound macroeconomic management, notably a clampdown on debt and inflation, ensured that South Africa today boasts sub-Saharan Africa’s “biggest and most sophisticated economy”.

Post-apartheid buoyancyThe economy bounced back from apartheid-era stagnation and since 1994 has tripled. Of the past 73 quarters, only three, during the global crisis, saw national income retreat. In recent years the global commodity boom has provided an additional tailwind. The government has been able to expand access to basic amenities and welfare services. Now 84% of South Africans have access to electricity, up from 58% in 1996.

Nonetheless, this has barely begun to address many of South Africa’s problems. Indeed, 47% of South Africans remain below the national poverty line of $43 a month; in 1994, this was 45.6%. Officially unemployment has risen to 25%; unofficially, it’s around 40%. And the outlook is clouding over. “At best”, says Jim Armitage in The Independent, today’s South Africa is “underperforming... at worst, it’s in a quagmire with little sign of improvement”. Compared to most

emerging markets, its growth rate has been pedestrian in recent years, rarely exceeding 4%-5% – not enough to make a dent in unemployment – and recently falling to 2%. The country’s low economic speed limit is due to several structural problems, notably a poor education system, which affects productivity and employment.

That in turn is undermined by an inflexible labour market, labour conflicts and huge pay rises. Power shortages and infrastructure bottlenecks are also obstacles. And all these issues are looking less likely to be tackled properly now that the ANC has become “a byword for weak leadership and cronyism”, says the FT.

A shot in the footUnder the current president, Jacob Zuma, the ANC has “conflated the interests of

party and state”, says The Economist, attempting to undermine the independence of the courts and the press and “dishing out contracts for public works as rewards for loyalty”. Unions have also used their close ties to the governing party to maintain their power bases and resist significant changes to the labour market.

South Africa has long been dominated by large firms and unions to the exclusion of the informal sector and the unemployed, says the University of Cape Town’s Haroon Bhorat on Nytimes.com. Now the insiders are becoming more powerful, leaving the outsiders – the unemployed and small business people without connections – ever more marginalised. All this hampers growth, in turn repelling potential investors and further reducing South Africa’s potential.

South Africa is shooting itself in the foot just as external headwinds are mounting. China’s growth model is shifting towards consumption and away from investment, which bodes ill for commodity producers such as South Africa. South Africa also has a huge current account deficit, worth 6.8% of GDP. Economies with external deficits need to import foreign capital to cover the gap, and this capital is less likely to come to emerging markets when America is looking likely to tighten monetary policy, as is now the case. If the political environment worsens, it may also be more reluctant to fuel the economy in good times. As such, South Africa’s economy and stockmarket may be in for a bumpy ride over the next few years.

South Africa’s long walk isn’t over yet

markets

Will India’s surge run out of steam?Indian stocks have been on a tear, rising by more than 15% since early September and hitting a new record this week. It’s a marked contrast from this summer, when its currency and equities tanked. One reason investors have returned is that the new central bank governor, Raghuram Rajan, has proved a safe pair of hands, attempting to squeeze out high inflation by raising interest rates twice.

The current-account deficit has fallen, thanks to higher import duties on gold, so India is now less dependent on foreign capital and its assets are thus less vulnerable to global sentiment. Meanwhile, the lacklustre growth of the past few years appears to be bottoming out. In the third quarter, year-on-year GDP growth accelerated to 4.8% from the previous quarter’s 4.4%. And investors were cheered by the victory of the opposition, led by the pro-business Narendra Modi, in three state polls.

Yet the market surge seems unlikely to be sustained, says Capital Economics. For starters, growth may have ticked up, but there is a “bumpy recovery” ahead. The improving global economy and recent slide in the rupee have boosted exports, but the key driver of growth is the domestic economy, and this still looks “shaky” due to the “poor investment environment”, with pervasive red tape hampering a series of major projects.

As the government’s efforts to rectify this have made little progress, it’s no wonder investors are looking forward to the opposition taking over the national government in May. But it will still probably need support from “fickle, regional parties” to govern. High inflation, moreover, continues to constrain household and corporate budgets. India’s long-term prospects may be compelling, but for now, as Capital Economics concludes, markets are getting ahead of themselves.

©B

loom

berg

Further progress faces headwinds

10 MoneyWeek 13 December 2013 www.moneyweek.com

A few years ago split capital investment trusts were mired in scandal as some investors lost lots of money in risky funds. However, for those looking for higher rates of income and prepared to take on higher risks, they can play a useful role in a portfolio.

What are they?Split capital trusts are investment trusts that issue more than one class of share. This means an investor can decide whether they’d rather have a high rate of income, or a focus on capital growth from the same trust. The trusts tend to have a fixed term (usually five to ten years) with a pre-determined wind-up date. The make-up of a split capital trust can be complicated as it can issue many different types of shares. The most common ones are zero dividend preference shares (zeros) then income and capital shares. The shares are ranked in order of payment priority at the wind-up date. Any borrowings the trust has are paid first, followed by zeros, then income and capital shares.

Zeros don’t pay any income. The interest here is capital gain. When the shares are first issued, they are sold at a discount to a fixed redemption price which is received at the wind-up date. These shares can be useful for higher-rate taxpayers: by selling their shares before the wind-up date, they only have to pay tax on capital gains they make above their annual allowance of £10,900 at 28%, rather than income tax at 40%-45%.

A traditional income share gives you the right to most of the trust’s income, with a redemption price at the wind-up date. This is the safest income option. There are also annuity income shares that can pay a high and rising income. However, there is no capital protection here as capital is depleted and converted into income. These types of shares are best held in a tax-sheltered account, such as an Isa. Ordinary income shares try to provide a high income and a right to a share of the remaining trust assets. These are more risky than zeros, as you could lose your investment if the trust performs badly.

Capital shares have no pre-determined wind-up price, and are entitled to the assets left over at the wind-up date. There is always a risk there may not be any money left, but spectacular gains could

be made if assets rise a lot. These are very risky and only for adventurous investors.

Working out the risks and returnsLook at what the trust is investing in, because this will determine the returns. Is it investing in blue-chip shares or bonds? Or riskier stuff, like smaller firms or technology? One of the biggest risks with a split capital trust is gearing, which comes in two forms. Firstly, it comes from any money borrowed by the trust. This magnifies returns. It’s great if the

trust is performing well, but if it performs badly your investment could be wiped out. Gearing also comes from the trust’s structure. The best way to think about this is to consider who is in front of you when it comes to getting paid. The biggest risk comes from a capital share in a trust with debt, zeros and income shares all in front of it in the payment pecking order.

With zeros and income shares with fixed redemption prices, look at the gross redemption yield (see page 44) of the share. This gives you your total return from paying the current share price and holding it until the wind-up date with the target redemption payment.

Another thing to look for is the share’s hurdle rate. This tells you how much the trust’s assets will have to grow by in order to pay out the full redemption value at the wind-up date. A negative hurdle rate is a good sign as it means that the assets could fall in value by a certain amount and still pay the full redemption value. A similar measure is the wipe-out hurdle rate – how much the assets have to fall by to leave you with nothing.

Asset cover also looks at how many times the trust’s current assets cover the redemption value of the shares. So a cover of two means that there is 200p in assets for every 100p of redemption value – assets can fall by 50% before the redemption value is in danger.

Take a close look at the risk before buying in

Is it time to return to split capital trusts?

investment strategy

©Th

inks

tock

by Phil Oakley

For the safer zero dividend preference shares, Aberforth Geared Income Trust (LSE: AGIZ), with a gross redemption yield of 4.2%, might be worth a look. Aberforth is a value investor specialising in smaller companies. The shares wind up in June 2017 with a target redemption price of 159.7p, which is already covered 2.4 times by the trust’s gross assets. These assets can fall by nearly 20% a year before the redemption value is threatened.

For income shares, you could consider JP Morgan Income & Growth (LSE: JIGI). The trust invests a lot of its money in blue-chip dividend-paying shares with a wind-up date of November 2016. At 92.75p, it trades on a 11.5% discount to

its net asset value and a 4.7% dividend yield. The redemption value is just about covered by assets, but the shares have a gross redemption yield of 8.8%.

Capital shares are few and far between. M&G High Income (LSE: MGHC) is highly geared with zeros and income shares ahead in the pecking order. It winds up in March 2017 and doesn’t yet have enough money to pay anything to shareholders. It needs to grow 6.8% per year just to avoid wiping shareholders out and by 7.7% to get to the current share price. However, if you think the stockmarket will go on a spectacular bull run – and assets go up by more than 8% – the high gearing could see you make several times your money. Not for the nervous.

Three to consider

I WANT MORE THAN JUST AN ADVANCED PLATFORM, COMPETITIVE PRICING AND SERVICE.

I WANT IT ALL.

You can have it all with CMC Markets

As a global market leader, we offer the complete trading package including:

Award-winning* platform

100% automated execution

Customisable tools and award-winning** charting

Custom-built apps for iPhone, iPad and Android™

Competitive pricing

Cash rebates for high volume traders^

Visit cmcmarkets.co.uk

Experience the difference

*Awarded Best Online Trading Platform by the 2013 MoneyAM and Shares awards. **Awarded Best Online Charts by the 2013 MoneyAM awards. Apple, iPad, and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc. Android and Google Play are trademarks of Google Inc.

Spread betting & CFD trading can result in losses that can exceed your initial deposit.^Conditions apply, please see our website.

You can have it all with CMC Markets

As a global market leader, we offer the complete trading package including:

Visit cmcmarkets.co.uk

12 MoneyWeek 13 December 2013 www.moneyweek.com

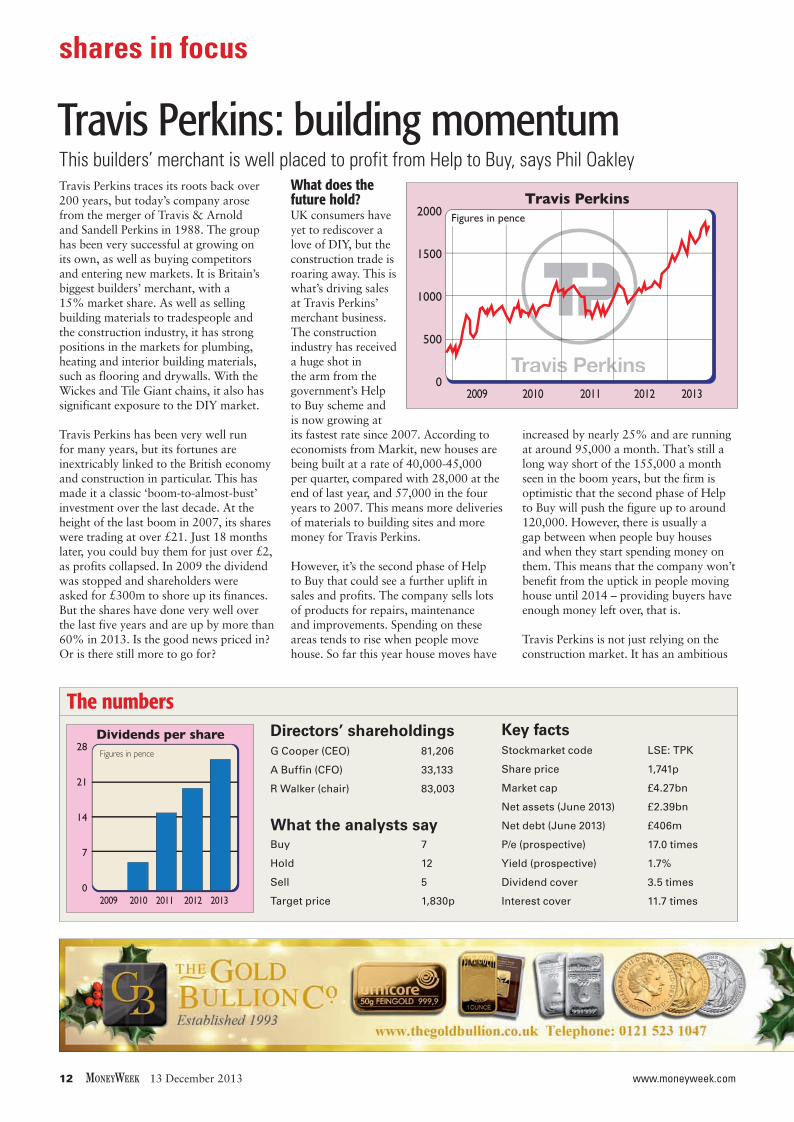

2000

1500

1000

500

02012

Figures in pence

20132010 20112009

Travis Perkins

Travis Perkins: building momentumTravis Perkins traces its roots back over 200 years, but today’s company arose from the merger of Travis & Arnold and Sandell Perkins in 1988. The group has been very successful at growing on its own, as well as buying competitors and entering new markets. It is Britain’s biggest builders’ merchant, with a 15% market share. As well as selling building materials to tradespeople and the construction industry, it has strong positions in the markets for plumbing, heating and interior building materials, such as flooring and drywalls. With the Wickes and Tile Giant chains, it also has significant exposure to the DIY market.

Travis Perkins has been very well run for many years, but its fortunes are inextricably linked to the British economy and construction in particular. This has made it a classic ‘boom-to-almost-bust’ investment over the last decade. At the height of the last boom in 2007, its shares were trading at over £21. Just 18 months later, you could buy them for just over £2, as profits collapsed. In 2009 the dividend was stopped and shareholders were asked for £300m to shore up its finances. But the shares have done very well over the last five years and are up by more than 60% in 2013. Is the good news priced in? Or is there still more to go for?

What does the future hold?UK consumers have yet to rediscover a love of DIY, but the construction trade is roaring away. This is what’s driving sales at Travis Perkins’ merchant business. The construction industry has received a huge shot in the arm from the government’s Help to Buy scheme and is now growing at its fastest rate since 2007. According to economists from Markit, new houses are being built at a rate of 40,000-45,000 per quarter, compared with 28,000 at the end of last year, and 57,000 in the four years to 2007. This means more deliveries of materials to building sites and more money for Travis Perkins.

However, it’s the second phase of Help to Buy that could see a further uplift in sales and profits. The company sells lots of products for repairs, maintenance and improvements. Spending on these areas tends to rise when people move house. So far this year house moves have

increased by nearly 25% and are running at around 95,000 a month. That’s still a long way short of the 155,000 a month seen in the boom years, but the firm is optimistic that the second phase of Help to Buy will push the figure up to around 120,000. However, there is usually a gap between when people buy houses and when they start spending money on them. This means that the company won’t benefit from the uptick in people moving house until 2014 – providing buyers have enough money left over, that is.

Travis Perkins is not just relying on the construction market. It has an ambitious

This builders’ merchant is well placed to profit from Help to Buy, says Phil Oakley

Figures in pence28

21

14

7

0

Dividends per share

2012 20132009 2010 2011

The numbers

What the analysts sayBuy 7

Hold 12

Sell 5

Target price 1,830p

Directors’ shareholdingsG Cooper (CEO) 81,206

A Buffin (CFO) 33,133

R Walker (chair) 83,003

Key factsStockmarket code LSE: TPK

Share price 1,741p

Market cap £4.27bn

Net assets (June 2013) £2.39bn

Net debt (June 2013) £406m

P/e (prospective) 17.0 times

Yield (prospective) 1.7%

Dividend cover 3.5 times

Interest cover 11.7 times

shares in focus

www.moneyweek.com 13 December 2013 MoneyWeek 13

strategy to grab a bigger share of existing builders’ merchant markets, move into related ones, and become more efficient. As well as growing its merchant depot sites by ten to 15 a year, and adding Toolstation outlets, I wouldn’t be surprised if the company goes out and buys some of the bigger local firms still out there. This would boost its formidable buying power and help profits grow.

There’s also a lot it can do with Wickes. Households are not splashing out on DIY at the moment, so the goal is to make Wickes a serious option for tradesmen by focusing on value for money. It is also likely to increase the number of Wickes stores across Britain. Other areas of expansion include bathroom and interior building supplies. By spending more on where it can get the best bang for its buck, the company reckons it can grow trading profits by more than 10% a year for the next three to five years, and boost its return on capital by 2%-3%. That would be good for shareholders. The company is also feeling confident enough to pay out a bigger slice of its profits each year, which should see a big increase in dividends.

It’s not all plain sailing. Travis Perkins’ lines of business makes it a riskier investment than many. It also has a lot of fixed costs, because it rents rather than owns most of its outlets, making profits very sensitive to changes in sales. Long-term shareholders will know of the pain this can bring, but with business picking

up there’s a good chance that profits in coming years could be higher than many analysts expect. The shares are not cheap on 17 times 2013 earnings, but this falls to 14.7 times next year’s forecast profits.

Travis Perkins looks like it is still building earnings momentum and that’s what could drive the share price higher still.

Verdict: buy

In April last year, I said Drax was a ‘sell’. It looked expensive on 18 times expected earnings, and I thought future profits would be hit by carbon emissions allowances costs, and as it made its power station comply with regulations. A plan to convert from coal to biomass looked to be stuck in the starting gates.

But events have proved me wrong. Although profits in 2013 are set to be lower than in 2012, Drax’s prospects may have been transformed by the government, which last week agreed to let it charge a minimum of £105 per megawatt hour (more than twice the current market price) for the electricity it generates from burning biomass (mainly wood pellets). This runs until 2021, and looks good enough to underpin its £700m investment in turning half of the power station to biomass. UBS reckons it makes Drax

a more attractive takeover target: a bidder could justify paying more than £10 a share, or even £12 if four of the six power units are converted. Barclays Capital reckons Drax could end up paying out up to £1.5bn to shareholders in a few years’ time.

Drax now trades on over 22 times next year’s earnings. But analysts expect profits to almost double over the next three years. With coal-generated electricity a lot more profitable than gas generated, the medium term looks rosy. It may be worth considering how long the price guarantee will last – a future government could change its mind, particularly as it will mean higher electricity bills. But no one seems worried at the moment.

Verdict: hold if you own

Company in the news: Drax (LSE: DRX)

Gamble of the week:Domino’s Pizza (LSE: DOM) 800

600

400

200

0

Domino’s PizzaFigures in pence

20132009 2010 2011 2012

When reviewing Domino’s in July, I thought it was a great business, but way too expensive on 26 times earnings, leaving no room for slip-ups. That proved to be the case. The shares are now down 25% after a tough few months. On the trading front, it seems that replicating the success of its UK business in Germany is not going to happen quickly, if at all. It will take longer than expected for losses to turn into profits. Back in Britain analysts are starting to fret that it won’t be able to open as many new stores as they had expected. When that gets factored into their spreadsheet models, it probably means the business is worth less too.

If that wasn’t bad enough, last week the chief executive said he was leaving. Coming so quickly after the finance director said he was retiring, this did not sit well with investors, who unsurprisingly wondered: ‘what have they seen that outsiders haven’t?’ Investors hate uncertainty, which is why the shares have been hammered.

Analysts are not yet taking a knife to their forecasts. They still expect earnings to grow by 20% in 2014. If Domino’s can deliver on that, the shares trade on a less punchy 17.4 times forward earnings and offer a prospective dividend yield of 3.8%.

The chairman, Stephen Hemsley, who ran Domino’s for a decade, is apparently ready to step in to steady the ship. Time will tell whether Domino’s can keep on growing strongly, but sometimes the market overreacts to news. Domino’s shares could bounce back if some confidence is restored. The shares are a risky, short-term punt.

Verdict: a speculative buy

shares in focus

14 MoneyWeek 13 December 2013 www.moneyweek.com

Murray Income Trust’s (LSE: MUT) objective is three-pronged: to generate a high income, a growing income, and capital growth. The best way to do this is to concentrate on companies with strong market positions and robust balance sheets that have the potential to grow their earnings (and hence their dividends) over the long term. Perhaps surprisingly, over the last 18 months earnings growth for the UK market in aggregate has, so far at least, failed to show signs of improvement. The returns we have seen as the market has moved ahead have been due to a rerating (where investors are willing to pay more for a given level of earnings). Of course, markets can’t perform well forever without earnings making progress, so it’s important to focus on companies that have the potential to deliver strong earnings growth over a long timeframe. I believe the three below fit the bill.

The first is Compass (LSE: CPG), a leading global contract-catering company benefiting from the long-term trend for companies to outsource more of their non-core functions. Around half of its £200bn market is outsourced, with healthcare and education particularly underpenetrated. The company also has scope to gently increase operating margins via cost savings in areas such as labour scheduling and food procurement. Compass is steadily increasing its exposure to emerging markets (by expanding operations in countries such as India and Brazil) while also offering various support services, a market that is growing at around twice the pace of catering. The combination of likely high single-digit earnings growth, a prospective dividend yield close to 3%, and an on-going share buy-back (given its strong cash flow characteristics) provides an attractive total return.

My second choice is Cobham (LSE: COB), a company that has endured a more difficult period over the past couple of years as US defence spending has been reined in. Indeed,

trading is likely to remain difficult in the short term as contract awards are delayed. However, the company has leading market positions in a number of areas such as air-to-air refuelling and antennae that provide the opportunity to expand into new geographical markets. Cobham is also making good progress with its efficiency measures. Through this more challenging period the company has been retuning its operations to focus on its civil aerospace business where growth remains robust. The company has a target to grow its dividend (from a current yield of 3.5%) by 10% a year. It also offers a strong balance sheet that gives it the option to acquire rivals, buy back shares, or perhaps announce a special dividend, and it trades on an attractive valuation of 12.5 times 2013 earnings.

The final company is Inmarsat (LSE: ISAT), the market leader in satellite communications. The company benefits from significant barriers to entry, including the requirement for spectrum rights, orbital slots and sizeable capital requirements. Within the next 18 months Inmarsat will be launching its next-generation service (known as Global Xpress), offering significantly enhanced data speeds and capacity. Further growth will come from the company’s focus on its core area of operations, with machine-to-machine and in-flight connectivity potentially significant markets. The shares offer a dividend yield of more than 4% and, while not cheap on 22 times December 2013 earnings, they offer the prospect of delivering long-term earnings and dividend growth from a unique competitive standpoint.

©Th

e Te

legr

aph

2013

personal view

Three strong dividend streams

A professional investor tells MoneyWeek where he’d put his money now. This week:Charles Luke, fund manager, Murray Income Trust

The stocks Charles Luke likes12mth high 12mth low Now

CPG 964.5p 711.5p 920.5pCOB 312.5p 209p 261.5pISAT 749p 579p 727p

16 MoneyWeek 13 December 2013 www.moneyweek.com

Politicians: salesmen with skin in the game

city view

Known for bending the truth? Check. Slick but not very sincere? Check. Everyone hates them? Check. The list of similarities between estate agents and politicians is

already surprisingly long. But now there is another. They are both a largely parasitic class living off a percentage of property sales and with a big stake in keep the market artificially frothy.

Government finances are becoming increasingly dependent on stamp duty. What used to be a relatively insignificant tax has become a major revenue source for the state, with higher rates and more and more transactions being pushed into the top brackets. That is hardly wise. Just like an estate agency, it makes the government dangerously dependent on the property market for its own finances – and gives it an incentive to meddle.

Go back a couple of decades and stamp duty was just a small, irritating charge that got added on when you bought a property. In 1993, there was a single rate of stamp duty of 1%, and it only kicked in when a transaction was worth more than £60,000 – more than the average house price at the time. Most ordinary people didn’t pay it, and when they did it was not a huge sum. It was similar to the solicitor’s bills, and less than buying the furniture or redecorating. Most people paid it without noticing.

But since then, it has kept on rising. After a series of reforms, we now have seven different rates of stamp duty, ranging from 0% for properties worth less than £125,000, to 3% for properties between £250,000 and £500,000, all the way up to 7% for those worth over £2m (and a punitive 15% if you buy through a corporation). The very top end could be dismissed as a tax on the super-rich: £2m houses are not exactly mass-market products, even in London. But £250,000 is hardly a fortune to spend on a family home these days, and for that middle section of the market, stamp duty is

now a major expense. According to the Taxpayers’ Alliance, a lobby group, two in every five homes bought in 2012-13 will be clobbered with the 3% rate, creating a bill of at least £7,500. By 2017 it predicts that 80% of homes will be hit by some form of stamp duty. In London, where prices are highest, many first-time buyers now have to pay the 3% rate, creating a huge bill that already cash-strapped young people struggle to pay.

A combination of rising stamp duty rates and house prices means that the revenue it brings in for the government keeps going up. Accountants Grant Thornton predict receipts will go up from £4.9bn a year now to £13.7bn in a decade. That is roughly the same as the tax raised from tobacco duty, and five times that raised through the bank levy. The Office for Budget Responsibility expects revenue raised from the tax to rise by 73% by 2018, bringing in an extra £6bn a year.

A big slice of government revenues are now a geared play on the housing market. Just like an estate agency, the higher house prices go, and the more turnover in the market, the more money it makes.

That is fine for private-sector companies. But it is hardly wise for the government.

There are two problems here. The minor one is that housing-market revenues are inevitably volatile. All markets go through boom and bust cycles, and the British property market is hardly an exception – indeed, it is usually an extreme example. When prices are rising strongly, as they are now, revenues shoot up. But if the market collapses, the cash raised from the tax will collapse as well. A well-designed tax should aim to bring in a stable, predictable stream of revenue – and stamp duty is far from that.

The major problem is that the government is hardly a disinterested player in the housing market. It controls both supply and demand. Planning laws dictate the supply of new homes, and in the medium term that sets prices for the whole market. As for demand, the government, via the Bank of England, controls interest rates; it influences the availability of mortgage through schemes such as Help to Buy; and it also controls immigration – the major short-term determinant of the number of homes that are needed. Pretty much everything that happens to the property market is influenced by the government.

But it now also has a financial stake in a buoyant market. Whether conscious of it or not, it has a big incentive to manipulate the market. If it wants prices to keep rising, it can achieve that by restricting supply and boosting demand. And the frothier the market gets, the more money flows into its coffers. It may not do it deliberately, but it is hard to believe it will not be influenced by that.

And yet, higher property prices are not necessarily good for the country. Young people find it too hard to get a foot on the ladder. And too much capital gets tied up in one sector that could be better used elsewhere. It might well be better for everyone if prices fell to more reasonable levels. But, through stamp duty, the government has turned itself into a giant estate agent, with a vested interest in rising prices. It shouldn’t be surprised if everyone ends up hating it as much as they do estate agents.

Our government has turned into a massive estate agent

©G

etty

Imag

es

18 MoneyWeek 13 December 2013 www.moneyweek.com

What is open data?“Open data is data that can be freely used, reused and redistributed by anyone – subject only, at most, to the requirement to attribute and sharealike,” according to the Open Definition, a set of principles created by key players in the open data movement. For data to be open, there are three main elements. “Availability and Access” means that it must be freely available in a convenient and modifiable form. “Reuse and Redistribution” states that it must be provided under terms that allow reuse and mixing with other datasets. “Universal Participation” prohibits discriminatory terms, such as restrictions on the use of the data for commercial purposes.

What sort of data is this?Mostly data collected and held by the government or other state authorities that could potentially be of use to individuals, organisations and businesses. This encompasses everything from crime rates to train timetables; details of government spending to copies of contracts; infection rates in hospitals to water quality analysis to power consumption patterns.

Why should data be open?“Data is the raw material of the 21st century – a resource that gets more plentiful every day,” say Tim Berners-Lee and Nigel Shadbolt, the founders of the Open Data Institute (ODI). So the principle is not just that open data is good in itself, or that it strengthens democratic accountability and transparency – though these are noble aims. The wider belief is that open data can allow businesses and social entrepreneurs to spot opportunities. “When the data has been released, applications have quickly followed,” as Berners-Lee and Shadbolt put it.

What are these applications?One of the most obvious uses is in the plethora of popular websites and smartphone apps that allow travellers to see when their bus is coming, find a parking space, or evade roadworks. Another well-known site is Fixmystreet.com, which allows citizens to log problems with their councils. And one of the ODI’s great success stories has been backing a start-up agency, Mastodon C, which analysed NHS prescribing data (along with Open Health Care UK and Ben Goldacre, the campaigning doctor) and identified £200m of NHS savings after looking at prescribing patterns for statins. For an overview of some of the ways in which open data is currently being used in Britain,

see the article “What did open data ever do for us?” on the homepage of the government’s open data site, Data.gov.uk.

Is open data new?In a sense, no. There are many past examples of “open data” leading to advances in knowledge. Berners-Lee and Shadbolt give the example of Florence Nightingale, who revolutionised nursing in the mid-19th century after using open data to show that most soldiers in the Crimean War died of disease rather from their wounds. John Snow, a London obstetrician, combined data on cholera deaths with the location of water wells and made the connection between contaminated water and outbreaks of the disease. This led to the building of the capital’s sewage system and hugely

improved public health. And in the 1940s the sociologist Robert King Merton

identified the importance of open scientific data, claiming each researcher must contribute their discoveries to the “common pot” in order to allow knowledge to move forward.

So why is open data now a big idea?The idea of “open data” might be rooted in scientific practice developed over centuries, but information technologies, including the internet, have opened radical possibilities for how open data can be analysed, processed and exploited. In recent years many governments have begun to make more information available as open data, a development that open data advocates are trying to capitalise on. The ODI has recently announced the creation of 13 affiliates, or “nodes” in countries from the US to Dubai, aimed at supporting companies, universities and non-governmental organisations in projects that make use of open data.

What’s Britain doing? The UK was one of the earliest countries to set up an official government site for open data and is recognised as one of the global leaders in the field. At the Open Government Partnership,

an international conference held in London this autumn, Britain committed to creating an open database of beneficial ownership of companies, which is expected to help tackle tax evasion and money laundering. This could produce some interesting results. An existing analysis of open data on company directors found that about 350 hold more than 100 directorships each, with a few holding up to 1,000 – a very high number for anyone hoping to fulfil the duties of a director.

Berners-Lee: opening up data for entrepreneurs©

Rex

Fea

ture

s

A quiet revolution in how we access government data is helping us do everything from catch buses to save money for the NHS. Simon Wilson investigates

Governments open their books

Is open data going global?There are a range of initiatives promoting the use of open data worldwide, such as Africa Open Data and OpenData Latinoamérica. Many projects are prompted by concerns about corruption, health, or environmental issues. In Brazil Infoamazonia.org has created a cross-border map of environmental degradation in the Amazon by analysing data from the National Institute for Space Research. In Kenya, the Data Dredger project, funded by USAID, the US development agency, tracks – among other things – the exodus of Kenya-trained doctors to other countries and how counterfeit drugs are hindering the fight against malaria. In Afghanistan and Mexico similar projects are mapping attacks on journalists.

investment briefing

SCOTTISH MORTGAGE INVESTMENT TRUST

Your call may be recorded for training or monitoring purposes. Baillie Gifford Savings Management Limited (BGSM) is the manager of the Baillie Gifford Investment Trust Share Plan and the Investment Trust ISA and is wholly owned by Baillie Gifford & Co, which is the manager and secretary of the Scottish Mortgage Investment Trust PLC. Your personal data is held and used by BGSM in accordance with data protection legislation. We may use your information to send you information about Baillie Gifford products, funds or special offers and to contact you for business research purposes. We will only disclose your information to other companies within the Baillie Gifford group and to agents appointed by us for these purposes. You can withdraw your consent to receiving further marketing communications from us and to being contacted for business research purposes at any time. You also have the right to review and amend your data at any time.

We’re 100% committed to making sure our fund managers never have a restricted outlook. That way, the long-term view is a clear one. So what’s the secret to their liberated attitude?

Well, our flagship fund, the Scottish Mortgage Investment Trust, is a global stock-picking fund that is completely free of asset allocation constraints, that ignores index weightings and that selects stocks purely on their merit. We feel that this freedom allows us to focus on the long term.

The Scottish Mortgage Investment Trust is managed by Baillie Gifford and is available through our Share Plan and ISA.

Please remember that changing stock market conditions and currency exchange rates will affect the value of your investment in the fund and any income from it. You may not get back the amount invested.

For more information call us on 0800 917 2112 or visit www.scottishmortgageit.com

Baillie Gifford – long-term investment partners

Freedom to roam.

WE LIVE IN A PERIOD OF EXPONENTIAL CHANGE PROVIDING FANTASTIC OPPORTUNITIES FOR STOCK PICKERS LIKE US.

MWK/SM/1213

20 MoneyWeek 13 December 2013 www.moneyweek.com

Money talkPlans to increase MPs’ pay by a massive 11% stem from their “craven unwillingness” in the past to face voters and argue for more money, says Philip Johnston. Instead, they conspired in developing a system of non-salary payments, such as second-home allowances to make up their perceived shortfall, which “appalled” the public when they came to light. Pay peaked around 2002 in real terms and has since fallen off, “a decline that coincided, unsurprisingly, with some of the more exotic expenses claims”. Today, the purchasing power of an MP’s salary of £66,300 is where it was 15 years ago. In 1937 Neville Chamberlain’s salary was worth £500,000 (David Cameron earns £142,500). But MPs’ allowances enable them to employ family members and nearly one in four does, costing £4m. They also have generous pensions. Neither the government nor the opposition should accept such largesse in times of austerity. There is never a good time to increase MPs’ pay, but this surely ranks as “one of the worst”.

“Regular cocaine users don’t look like this.”

Nigella Lawson (pictured) denying she abused

cocaine, quoted in The Daily Telegraph

“We’ve cut back dramatically… we never go out to dinner unless we go to somebody’s house. We never go to restaurants... We invite people here. I

cook. Well, if I’m giving a dinner party I get in help.”

Princess Michael of Kent on her experience of austerity, quoted in

The Times

“Advertising may be described as the science

of arresting human intelligence long enough

to get money from it.”Canadian writer Stephen

Leacock, quoted on Telegraph.co.uk

“In the old days, you could speak to someone in

charge over a sandwich. Now it has to be over

lunch at the Ivy. And you don’t have to keep sending

me flowers.“Comedian Jennifer

Saunders accuses the BBC of wasting money, quoted

in The Sunday Times

“We have the best government that money

can buy.”Mark Twain, quoted in a

PFP Wealth Management newsletter

Do MPs deserve an 11% pay rise?

Philip Johnston

The Daily Telegraph

best of the financial columnists

©R

ex F

eatu

res

Is it fair for the chancellor to offer £1m a year to the Duke of Roxburghe for letting the wind blow? asks Simon Jenkins. Or to promise a reported £1bn to Charles Connell, the Scottish shipbuilding company, over the next 25 years? British energy policy is “chaotic”. News that subsidies for onshore turbines will be cut in favour of offshore ones may be welcome aesthetically, but they are even more expensive and inefficient. The energy required to mine wind turbines’ rare materials and to build and erect them “makes a mockery of their ‘greenness’”. From Offa’s Dyke to the Cambrian Mountains and the open vistas of Scotland, turbines have destroyed (or are set to) some of Britain’s most beautiful landscapes. For what? Turbines rarely produce anywhere near their declared capacity; what they really generate is money – up to £30,000 a year each in subsidy, irrespective of how windy the site. Politicians have showered a tiny elite with public money. Our desecrated landscape is “their memorial”.

Britain’s energy policy is in chaos

Simon Jenkins

The Guardian

We have come to expect the bonus bonanzas, government cash and six-figure salaries of the City, but this also describes today’s charity sector, says Dominic Nutt. Viewers of this week’s Panorama, which “lifts the lid” on how some big charities make money, may be “surprised to learn how far they will go to hit the bottom line”. Between 2007 and 2009 I was head of news at Save the Children. It’s a charity that does excellent work. But it’s part of a problem at the heart of some non-governmental organisations (NGOs) that could “fatally” undermine the sector. NGOs need money, but some have begun to “contradict their founding principles” to boost income. When I was at Save the Children, a press release condemning British Gas for raising prices and forcing poor families to choose between heating or feeding their children was spiked because British Gas was a donor. This is just one example. “Companies want only one thing – good PR”, and that’s why they are “stuffing the mouths of some NGOs with gold”.

Charities – the PR wing of business

Dominic Nutt

The Independent

“Never mind Big Brother, the all-seeing state,” says Douglas Murray, the real menace is the Little Brothers, who “suck up” your personal data and “sell it to the highest bidder”. As you surf the web, thousands of third-party cookies track your browsing habits. Some companies are “scooping up your tweets or Facebook posts”, analysing them and selling on the results. This is “perfectly legal” and lucrative. One major ‘data broker’, Acxiom Corporation, is thought to hold information on 500 million consumers and has annual sales of over $1bn. Targeted advertisements are hardly a “sustained attack” on our freedom. And it’s an exchange. We let people “spy” on us and in return get a free service (Facebook, Google). But this is becoming “one-sided”. Most of us never read the terms and conditions we agree to. Maybe we should. A British firm recently included a clause staking a claim on “your immortal soul”: the “techie joke… harvested 7,000 souls in one day”.

The real menance is Little Brother

Douglas Murray

The Spectator

22 MoneyWeek 13 December 2013 www.moneyweek.com

The potential is vast for Bitcoin start-ups

opinion

Bitcoin is all over the news again. China has banned banks from transacting in the digital currency, just as Bank of America Merrill Lynch has argued that it has a ‘fair value’ of $1,300. But none of these stories grasp the really interesting part – how the underlying Bitcoin platform itself can be used to manage the ownership of real-world assets.

At heart, Bitcoin is simply a huge public ledger, recording who gave what to whom and when: a long list of transactions (27 million at last count), replicated across a network of thousands of computers. To work out how much Bitcoin money you have, you just look down the list of your transactions and add them up. To give someone Bitcoin money, you send a ‘transfer please’ message to the network, which copies the request around the computers and checks all is in order. It is put in a block of transactions, which are added to the ledger (the ‘block chain’). You can read more on the inner workings of the currency and how it’s mined at Moneyweek.com/Bitcoin. But I want to focus on its wider potential.

Coloured coins and ownership rightsWhat’s key is that Bitcoin transactions are not limited to A-to-B transfers. They can contain far more information, such as multiple payers and payees, and rules on the signatures needed for a payee to collect. There are even time locks that dictate how long a transaction is valid. This allows quite sophisticated systems to be built, such as escrow agents for payment dispute resolution, time-limited deposits, and the equivalent of post-dated cheques. This is all part of the Bitcoin system and requires no central authority – so you don’t need a bank or trust lawyer acting as an expensive middle man.

In a way the Bitcoin currency is just the first ‘app’ (software application) to run on the Bitcoin platform. And just as with the launch of the iPhone, the built-in apps will soon be eclipsed by the innovation the system unleashes. For example, the concept of ‘coloured coins’ would enable the Bitcoin system to manage the ownership of real-world assets – anything from shares to cars. A particular Bitcoin would be ‘coloured’ to signify ownership of an asset. Because the block chain is public, anyone can track the ownership

of that Bitcoin (and so the asset itself) through every transaction it has ever been involved in, and see who now owns it. The Bitcoin is purely a token – it’s like writing an IOU for a car on a dollar bill, then storing it in a public ledger.

Each colouring scheme defines its own rules, such as who is allowed to issue the coins, how they are redeemed, and the transactions permitted. One use would be for smart devices to hook up to the Bitcoin network. Let’s say you own a device that streams films from the internet (a smart TV, maybe). To do so, it has to connect to a central server (such as iTunes) to implement digital rights management (DRM) and check that you’ve bought the film, before allowing it to be played. This means the film’s producers can only sell via these services. It also means that if the service shuts down, you could lose access to your film library. In 2008 Microsoft announced it would shut down its MSN Music service (with its ironically named PlaysForSure DRM) and that its US customers would no longer be able to use it to transfer their music to their devices.

Coloured coins would avoid the need for such services. The Bitcoin system itself would hold the entitlements. Your device

could prove to any server storing the film that it was entitled to play it. And because Bitcoin allows for conditions to be attached to each transaction, films could be rented, sold, re-sold, loaned (one area where physical DVDs still beat online films, for example), or even bequeathed, all at the discretion of the owner.

The filmmaker would control the terms on which it offered its films, which, through competition, would result in a balance being struck between the producers and consumers. Just as the internet has cut out layers from the distribution network for books and films, Bitcoin could take it further, allowing producers to sell direct to consumers, without virtual middle-men, such as iTunes or Amazon, being involved.

An investment revolution And it’s not just the world of music and film. So much of today’s finance industry is based on trusted central services for trading, for asset registers and for clearing. But the Bitcoin network provides a public asset register and decentralised trading. A company could issue its own shares in the form of coloured coins. The ownership and trading of these would be done via the Bitcoin system. No need for share registrars. What would existing organisations do? Offer ancillary services (eg, for collecting dividend payments on behalf of a shareholder)? Will nominee services disappear? Will new ‘low-cost’ venues – cutting out a large part of the costly IT infrastructure currently needed – emerge for trading small business shares? Much will depend on the pace of regulatory change in the area – but the potential is vast.

So the best way to invest in Bitcoin is not to buy the currency, or a high-powered mining set-up, but companies that can offer services and products that run on top of the Bitcoin network. Unless you’re a venture capitalist, that means you’ll have to be patient for now – but in the longer run, be prepared for Bitcoin to be as big a gamechanger as the internet.

Ken Tindell is an entrepreneur with experience in various industries, including automotive, embedded internet, and web TV. He currently runs a software development company.

The best way to invest in Bitcoin

©B

loom

berg

The digital currency will be as big a gamechanger as the internet, says Ken Tindell

www.moneyweek.com 13 December 2013 MoneyWeek 23

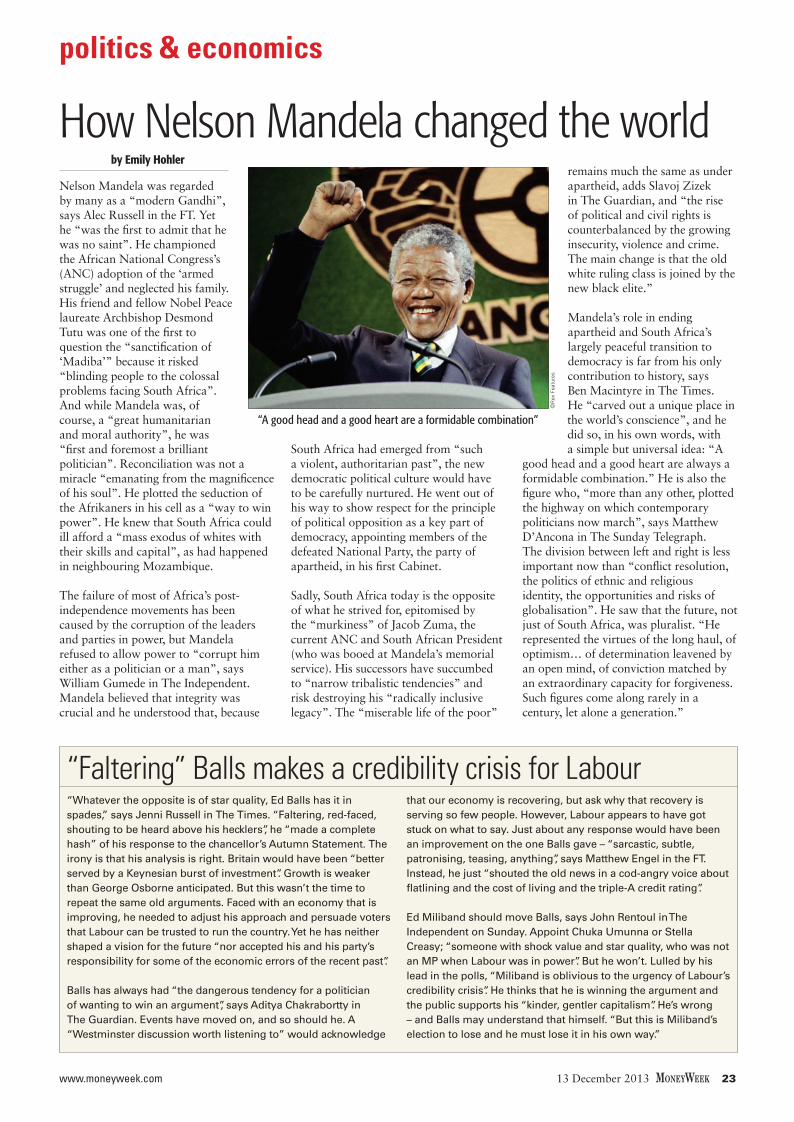

Nelson Mandela was regarded by many as a “modern Gandhi”, says Alec Russell in the FT. Yet he “was the first to admit that he was no saint”. He championed the African National Congress’s (ANC) adoption of the ‘armed struggle’ and neglected his family. His friend and fellow Nobel Peace laureate Archbishop Desmond Tutu was one of the first to question the “sanctification of ‘Madiba’” because it risked “blinding people to the colossal problems facing South Africa”. And while Mandela was, of course, a “great humanitarian and moral authority”, he was “first and foremost a brilliant politician”. Reconciliation was not a miracle “emanating from the magnificence of his soul”. He plotted the seduction of the Afrikaners in his cell as a “way to win power”. He knew that South Africa could ill afford a “mass exodus of whites with their skills and capital”, as had happened in neighbouring Mozambique. The failure of most of Africa’s post-independence movements has been caused by the corruption of the leaders and parties in power, but Mandela refused to allow power to “corrupt him either as a politician or a man”, says William Gumede in The Independent. Mandela believed that integrity was crucial and he understood that, because

South Africa had emerged from “such a violent, authoritarian past”, the new democratic political culture would have to be carefully nurtured. He went out of his way to show respect for the principle of political opposition as a key part of democracy, appointing members of the defeated National Party, the party of apartheid, in his first Cabinet.

Sadly, South Africa today is the opposite of what he strived for, epitomised by the “murkiness” of Jacob Zuma, the current ANC and South African President (who was booed at Mandela’s memorial service). His successors have succumbed to “narrow tribalistic tendencies” and risk destroying his “radically inclusive legacy”. The “miserable life of the poor”

remains much the same as under apartheid, adds Slavoj Zizek in The Guardian, and “the rise of political and civil rights is counterbalanced by the growing insecurity, violence and crime. The main change is that the old white ruling class is joined by the new black elite.” Mandela’s role in ending apartheid and South Africa’s largely peaceful transition to democracy is far from his only contribution to history, says Ben Macintyre in The Times. He “carved out a unique place in the world’s conscience”, and he did so, in his own words, with a simple but universal idea: “A

good head and a good heart are always a formidable combination.” He is also the figure who, “more than any other, plotted the highway on which contemporary politicians now march”, says Matthew D’Ancona in The Sunday Telegraph. The division between left and right is less important now than “conflict resolution, the politics of ethnic and religious identity, the opportunities and risks of globalisation”. He saw that the future, not just of South Africa, was pluralist. “He represented the virtues of the long haul, of optimism… of determination leavened by an open mind, of conviction matched by an extraordinary capacity for forgiveness. Such figures come along rarely in a century, let alone a generation.”

How Nelson Mandela changed the world

“Whatever the opposite is of star quality, Ed Balls has it in spades,” says Jenni Russell in The Times. “Faltering, red-faced, shouting to be heard above his hecklers”, he “made a complete hash” of his response to the chancellor’s Autumn Statement. The irony is that his analysis is right. Britain would have been “better served by a Keynesian burst of investment”. Growth is weaker than George Osborne anticipated. But this wasn’t the time to repeat the same old arguments. Faced with an economy that is improving, he needed to adjust his approach and persuade voters that Labour can be trusted to run the country. Yet he has neither shaped a vision for the future “nor accepted his and his party’s responsibility for some of the economic errors of the recent past”. Balls has always had “the dangerous tendency for a politician of wanting to win an argument”, says Aditya Chakrabortty in The Guardian. Events have moved on, and so should he. A “Westminster discussion worth listening to” would acknowledge

that our economy is recovering, but ask why that recovery is serving so few people. However, Labour appears to have got stuck on what to say. Just about any response would have been an improvement on the one Balls gave – “sarcastic, subtle, patronising, teasing, anything”, says Matthew Engel in the FT. Instead, he just “shouted the old news in a cod-angry voice about flatlining and the cost of living and the triple-A credit rating”. Ed Miliband should move Balls, says John Rentoul in The Independent on Sunday. Appoint Chuka Umunna or Stella Creasy; “someone with shock value and star quality, who was not an MP when Labour was in power”. But he won’t. Lulled by his lead in the polls, “Miliband is oblivious to the urgency of Labour’s credibility crisis”. He thinks that he is winning the argument and the public supports his “kinder, gentler capitalism”. He’s wrong – and Balls may understand that himself. “But this is Miliband’s election to lose and he must lose it in his own way.”

by Emily Hohler

“Faltering” Balls makes a credibility crisis for Labour

©R

ex F

eatu

res

politics & economics

“A good head and a good heart are a formidable combination”

24 MoneyWeek 13 December 2013 www.moneyweek.com

Last week was a good one for Chancellor George Osborne. He used

his Autumn Statement as an extended opportunity to rub the opposition’s face in Britain’s economic recovery. There were no big headline-grabbing changes, just a general sense that things were going as he’d planned (and after all, why splash out on any big giveaways when there are still 18 months to go until the election?). His shadow, Ed Balls, was left red in the face and with his position looking increasingly untenable (see page 23).

The reality, of course, is a little different. Yes, the British economy has rallied sharply in the past year – if you drop almost anything from a great enough height, it’ll bounce. Even the Office for Budget Responsibility (OBR) – the independent body charged with trying to give voters the unvarnished truth about a chancellor’s budget shenanigans – points this out. “The improvements are cyclical rather than structural.” The recovery is not “indicating stronger underlying growth potential”.

You can see this in the GDP figures if you look closely. As Richard Jeffrey of Cazenove Capital Management points out, most of the 0.8% growth seen in

the third quarter came from inventory rebuilding (companies replenishing stocks, which cannot sustain growth in the long run) and household spending. Business investment contributed very little, and exports actually fell. And it doesn’t help that GDP may be overstated in any case. The Office for National Statistics has started using a very forgiving ‘GDP deflator’ to measure real (after inflation) GDP. They don’t tell anyone precisely how this is calculated, but while it used to correspond closely to the retail prices index (RPI) measure,