how is gcc preparing for a 'aa' world

DESCRIPTION

How is GCC Preparing for a 'AA' WorldTRANSCRIPT

Kuwait Financial Centre “Markaz”

R E S E A R C H

How is GCC preparing for a “AA+” World? One more crisis to live with

The rating downgrade that rattled financial markets in August 2011 was of milder intensity compared to the 2008 tsunami financial crisis, whose impact

is still being felt. However, the downgrade enabled to perpetuate one thing i.e., maintain the policy response intact which is where the catch is. The world

will have a low interest rate environment at least for another one to two years

and may lay the foundation for yet another “Bubble-Burst” scenario.

The impact assessment of GCC is what this paper is all about. Successful articulation of polices will need to keep in mind several key and collateral risks

that have erupted as a result of series of crisis including the latest downgrade

crisis. In our opinion, the biggest challenge in a crisis ridden world will be to efficiently and effectively manage the surplus generated in good times. This will enable the GCC governments to progress with their investment program which brings us back to the question of managing risks.

GCC Impact

Areas

Assessment

Surplus The biggest challenge to GCC would be to deploy effectively

and efficiently its huge surplus generated through the oil boom of recent years. With limited absorptive capacity inside,

and a crisis ridden world outside, the deployment challenge will be onerous.

Oil Price The rating downgrade does not directly trigger an oil price

fall. It may happen indirectly through triggering a double dip recession which in turn pulls down the oil price. However,

having built sufficient reserves, the region can weather weak oil prices for a stretch of time before it hurts them.

Currency US dollar is clearly declining in value and credibility and so the

issue of the GCC currency pegs will come increasingly into focus. However, US dollar weakness was accounted for even

before the downgrade. Lack of alternatives also gives some

comfort

Investments GCC governments have undertaken large domestic investment programs based on their huge reserves. Being non-reliant on foreign investments is a huge plus.

September 2011

Research Highlights:

Analyzing the implications of the US credit downgrade on

the GCC region

Markaz Research is

available on Bloomberg

Type “MRKZ” <Go>

M.R. Raghu CFA, FRM

Head of Research

+965 2224 8280 [email protected]

Layla Al-Ammar

Assistant Manager

+965 2224 8000 ext. 1205 [email protected]

Madhu Soothanan

Senior Research Analyst

+965 2224 8000 ext. 4603 [email protected]

Kuwait Financial Centre

S.A.K. “Markaz”

P.O. Box 23444, Safat 13095, Kuwait

Tel: +965 2224 8000

Fax: +965 2242 5828 markaz.com

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

2

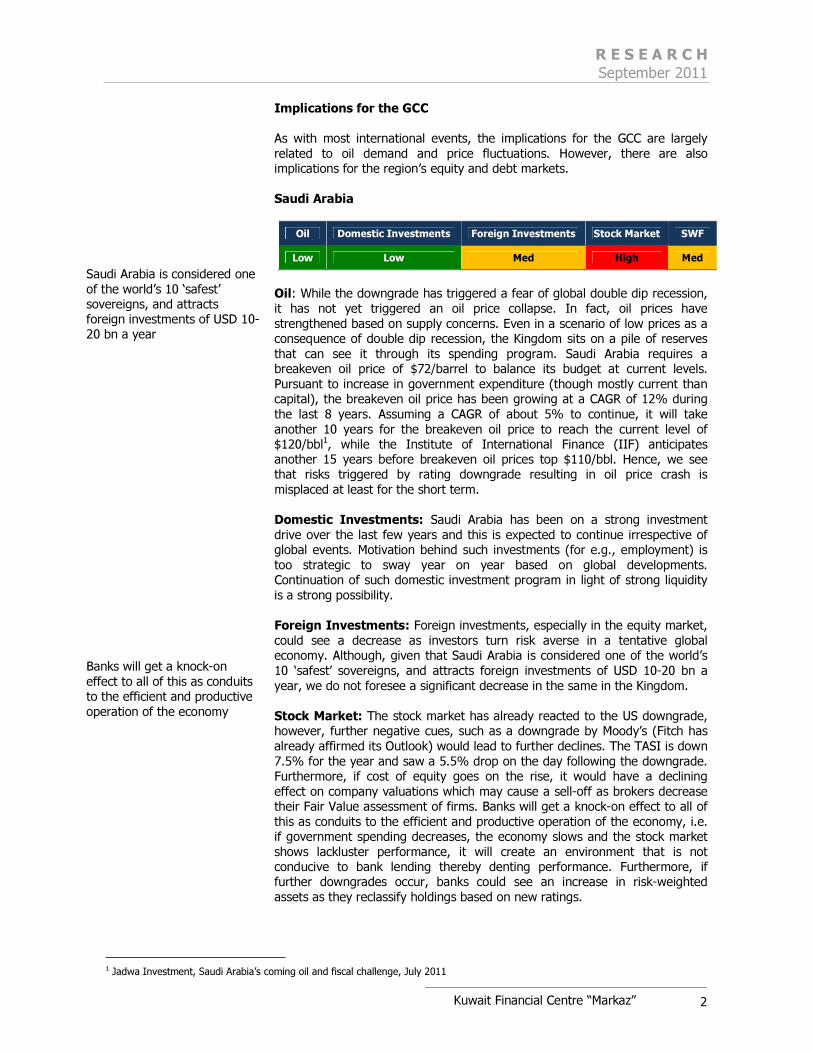

Implications for the GCC

As with most international events, the implications for the GCC are largely

related to oil demand and price fluctuations. However, there are also implications for the region’s equity and debt markets.

Saudi Arabia

Oil Domestic Investments Foreign Investments Stock Market SWF

Low Low Med High Med

Oil: While the downgrade has triggered a fear of global double dip recession,

it has not yet triggered an oil price collapse. In fact, oil prices have

strengthened based on supply concerns. Even in a scenario of low prices as a consequence of double dip recession, the Kingdom sits on a pile of reserves

that can see it through its spending program. Saudi Arabia requires a breakeven oil price of $72/barrel to balance its budget at current levels.

Pursuant to increase in government expenditure (though mostly current than capital), the breakeven oil price has been growing at a CAGR of 12% during

the last 8 years. Assuming a CAGR of about 5% to continue, it will take

another 10 years for the breakeven oil price to reach the current level of $120/bbl1, while the Institute of International Finance (IIF) anticipates another 15 years before breakeven oil prices top $110/bbl. Hence, we see that risks triggered by rating downgrade resulting in oil price crash is

misplaced at least for the short term.

Domestic Investments: Saudi Arabia has been on a strong investment

drive over the last few years and this is expected to continue irrespective of global events. Motivation behind such investments (for e.g., employment) is

too strategic to sway year on year based on global developments. Continuation of such domestic investment program in light of strong liquidity

is a strong possibility.

Foreign Investments: Foreign investments, especially in the equity market,

could see a decrease as investors turn risk averse in a tentative global economy. Although, given that Saudi Arabia is considered one of the world’s

10 ‘safest’ sovereigns, and attracts foreign investments of USD 10-20 bn a

year, we do not foresee a significant decrease in the same in the Kingdom.

Stock Market: The stock market has already reacted to the US downgrade, however, further negative cues, such as a downgrade by Moody’s (Fitch has

already affirmed its Outlook) would lead to further declines. The TASI is down

7.5% for the year and saw a 5.5% drop on the day following the downgrade. Furthermore, if cost of equity goes on the rise, it would have a declining

effect on company valuations which may cause a sell-off as brokers decrease their Fair Value assessment of firms. Banks will get a knock-on effect to all of

this as conduits to the efficient and productive operation of the economy, i.e. if government spending decreases, the economy slows and the stock market

shows lackluster performance, it will create an environment that is not conducive to bank lending thereby denting performance. Furthermore, if further downgrades occur, banks could see an increase in risk-weighted

assets as they reclassify holdings based on new ratings.

1 Jadwa Investment, Saudi Arabia’s coming oil and fiscal challenge, July 2011

Saudi Arabia is considered one

of the world’s 10 ‘safest’ sovereigns, and attracts foreign investments of USD 10-20 bn a year

Banks will get a knock-on

effect to all of this as conduits to the efficient and productive

operation of the economy

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

3

SWF: Lower state revenues will also have implications for the Kingdom’s Sovereign Wealth Fund (SWF). The SWF and Monetary Authority’s reserves

and investments are mostly held in USD denominated investments and US

treasuries; this exposure insolated the SWF in the 2009 global financial crisis where its portfolio actually gained in value versus peers like ADIA and KIA.

The SWF might not be so lucky this time around as it will be hit both with the currency factor of a weakening dollar in addition to a hit in treasuries.

Kuwait

Oil Domestic Investments Stock Market SWF

Low Low High Med

Oil: Like Saudi Arabia, Kuwait has built considerable reserves during the oil boom. Measured in GDP terms, in fact, it has performed even better than

Saudi Arabia in terms of reserve building as budget expenditure grew more

moderately during the last few years when benchmarked with Saudi Arabia. At a breakeven oil price of $70/bbl the current oil price provides a cushion of

$50/bbl. Even in a scenario where oil price reaches the breakeven level, the State of Kuwait can begin to draw on its reserve pile for a long time before it

drains out.

Domestic Investments: Kuwait’s domestic investments have been lagging

for some time. The country’s Development Plan came in to sort out this problem; much of the USD 125 bn plan is built on government spending

coupled with increasing the attractiveness of Kuwait to Foreign Investors. While the cost of finance will rise pursuant to US debt downgrade, it may not

reach a point where the domestic investments could be scaled down. Foreign

investment in the country is weak by regional standards, at less than USD 150 mn a year2.

Stock Market: The stock market has already declined 15% for the year and

tumbled 2.5% on the day following the US downgrade. The Kuwait market

has become hypersensitive to global cues; consequently, sustained negative news (such as a worsening of the Euro-crisis, a further downgrade of the US or a downgrade of another G7 nation) would cause further declines to the market. According to the IMF, the State’s banks are well-capitalized; the

sector’s Capital Adequacy Ratio (CAR) increased to 19% in 2010 (17% in 2009) due to capital increases during the year while leverage ratios are

averaging about 13%. NPLs are down to about 9% in 2010 (11.5% in 2009)

though still high by regional standards. Bank’s loans are heavily concentrated on Real Estate (26%), Retail loans (33%) and non-bank financial institutions

(12%) which are essentially Investment Companies3. The Real Estate and Investment sectors make up the bulk of the market and remain distressed

post the financial crisis of 2008/2009. An increase in cost of equity and

weakening of the dollar could be detrimental to the sector’s balance sheet which would ultimately impact the bank’s loan portfolios.

SWF: The sovereign wealth fund, Kuwait Investment Authority (KIA),

receives the majority of the government’s revenues for investment purposes;

and the same is deployed on a globally spread portfolio across various asset classes. To the extent the SWF investments are exposed to US treasuries and

the US$ currency, it runs the risk of value erosion. However, we don’t foresee a significant decline in KIA’s earnings as investments tend to be

2 The World Bank 3 IMF Country Report, July 2011

The stock market has already

declined 17% for the year and

tumbled 2.5% on the day following the US downgrade

The Real Estate and Investment sectors make up

the bulk of the market and remain distressed post the financial crisis of 2008/2009

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

4

geographically spread4 rather than concentrated in one country or risk-bracket.

UAE

Oil Domestic Investments Stock Market SWF

Abu Dhabi Low Low Med Med

Given that much of Abu Dhabi’s economic growth and diversification strategy is dependent on government spending of oil revenues, a prolonged decline in

oil prices due to a slowing world economy could put a damper on progress. However, we believe that given the reserves built up in addition to the wealth

generated and deployed by the Abu Dhabi Investment Authority (whose

assets are reportedly upwards of USD 630 bn5), the emirate should be able to maintain its spending plans despite any nominal decline in the value of its

reserve assets.

The Abu Dhabi stock market has remained relatively well isolated from negative global market cues; it remains one of the best performer in the GCC

on a year to date basis (-5%), despite suffering a 2.5% drop following the US

downgrade. Abu Dhabi banks have also held up relatively well during the downturn, 2Q11 net earnings came in at USD 1.17bn, a 74% YoY increase,

while 1H11 net profits were at USD 2.12bn, a 38% YoY increase. We expect the banks to continue to be supported by strong government spending in

addition to healthy economic growth.

Domestic

Investments Foreign

Investments Stock Market

Bond Market

Dubai High High High Med

Dubai is in a slightly more precarious situation given the declines suffered as

a result of the global credit crisis, which it is still recovering from, in addition to the fact that it has more of a global linkage than Abu Dhabi.

Given that the Dubai economy is reliant mainly on Trade and Tourism for GDP growth, these may see a decline should world economic growth decline.

Should economic growth in Dubai be hindered, it could prove detrimental to domestic investment by the government and private sector. This may also

affect the confidence factor for foreign investors, who would increase their

risk premium on Dubai post the US debt downgrade. However, one should note the fact that Dubai has strong ties with foreign institutions which have

been reaffirmed post-crisis through successful bond raises and continuation of major infrastructure projects across the emirate.

A further downgrade in the US and/or another G7 nation could result in cost

increases for foreign and local firms. Additionally, declining global growth and

poor market conditions could increase risk aversion among foreign investors, leading to a pull out of Arab markets.

Banks could see an escalation of risky assets as ratings change leading to a

squeeze on capital adequacy ratios, which coupled with an increase in

provisions would dent bottom line performance going forward. Additionally, the stock market has been performing poorly for the year, down by about

4 based on news articles and anecdotal evidence 5 Sovereign Wealth Fund Institute

The Abu Dhabi stock market

has remained relatively well isolated from negative global

market cues

A further downgrade in the US

and/or another G7 nation could result in cost increases for

foreign and local firms

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

5

11%, and we expect it to continue to be hypersensitive to global and regional cues.

Qatar

Oil Domestic

Investments Foreign

Investments Stock Market

Bond Market SWF

Low Low Med Med Med Med

Qatar enjoys similar comfort as that of Saudi Arabia, Kuwait, and Abu Dhabi when viewed from oil and gas resources and reserves. Hence, we perceive

lower risk on that account. Qatar has also been one of the best performing markets in the GCC over the last two years, successfully skirting the global

financial crisis while maintaining its growth trajectory. Consequently, we see a

mid-level risk in terms of the stock market, which is down about 3% for the year.

Despite the fact that the economy is highly dependent on LNG production, we

expect the reserves and revenues built up by the State through the years to allow it to continue to implement large-scale development plans such as the

USD 125 bn National Development Strategy which was put in place this year.

Lower state revenues may have implications for Qatar’s Sovereign Wealth

Fund (SWF) whose reserves and investments most likely have a US bias (detailed information on holdings is unavailable) which may see a nominal

devaluation as the dollar weakens.

Furthermore, Qatar is currently implementing many regulatory reforms and

developments, such as encouraging firms to lower Foreign Ownership Limits (in order to be upgraded to MSCI Emerging Market status) in addition to

setting up an organized bond market. These measures, coupled with large-scale projects relating to the World Cup 2022 event, should keep foreign

investor interest sustained.

Oman and Bahrain

Domestic Investments Foreign Investments

Oman High -

Bahrain High High

Oman and Bahrain have both had a relatively difficult 1H11 with political

turmoil dampening the economy and market sentiment. Oman, down 15%, is the worst performing GCC for the year while Bahrain, down 12%, is only

marginally better.

Lower global growth and dampened oil demand would make it relatively more difficult for Oman to enact domestic investment programs. This difficulty is

compounded by the lingering political issues, mainly relating to unemployment, which the government must address. As for the banking sector, it will be affected by a slowing economy and lackluster market

conditions.

The impact in Bahrain is expected to be higher; the country does not have oil

revenues to fall back on (the economy depends on tourism and the financial sector) in order to boost public spending and consequently, any further strain

on the economy will lead to declining domestic investments. Moreover, the government currently runs a deficit of about -6% of GDP, placing further

strain on government spending. Furthermore, banks have already suffered

Qatar is currently implementing many regulatory

reforms and developments

Oman and Bahrain have both

had a relatively difficult 1H11

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

6

during the year, due to political strife, with some businesses moving offices to ‘safer’ locales like Qatar or Dubai. Consequently, the risk perception of the

country has risen, with 5 yr CDS spreads up 42% for the year, which would

make it difficult to attract foreign investors back.

GCC Equity Markets-Post AAA Downgrade

The short term effect has been felt already with the GCC stock markets

experiencing large declines following the announcement; Saudi’s Tadawul tumbled 5.5% on the 6th of August (Table 1). When other GCC markets

opened on Sunday, they experienced sharp declines; Qatar and Dubai were down 5% at the open while Kuwait quickly shed around 3%. However, the markets managed to regain some of the lost ground, but still closed in the

red. Qatar and Kuwait (weighted index) both closed down 2.51% while Dubai lost 3.7%. GCC stock markets have shed USD 31 bn in market cap since the

announcement of the US debt deal at the end of July. The stock markets could decline further as international markets fluctuate wildly on varying risk

assessments.

Table 1: Immediate Impact of Downgrade on Local Exchanges

Index losses Saudi Arabia

Kuwait Dubai Abu Dhabi

Qatar Oman Bahrain S&P GCC Index

1st Day Impact* (Rating Downgrade)

-5.50% -2.51% -3.70% -2.53% -2.51% -1.87% -0.33% -1.20%

27th July – 10th Aug (Debt Deal announcement)

-6.30% -3.55% -3.05% -1.44% -2.95% -7.66% -2.53% -5.32%

USD bn GCC Total

Market Cap Decline (27 July – 10th Aug)

-21 -4 -1 -1 -3 -1 0 -31

Note: Kuwait represents Kuwait Weighted Index Note*: 1st Day Impact represents 6th of August for Saudi Arabia and 7th of August for other GCC Markets. Source: Reuters Eikon, Markaz Research

CDS spreads, which give an indication to the level of risk perceived in a

market, saw increases across the board following the US debt deal and downgrade (Figure 1). All markets saw spreads jump between 7.5% and 22%

in the case of Oman. We would expect CDS spreads to remain volatile while equity markets fluctuate.

Figure 1: Impact on CDS Spreads (5 yr USD)

As global equity markets re-price risk, prices will undoubtedly be affected. Regional Brokers / financial institutions will have to come to terms on whether

The short term effect has been

felt already with the GCC stock

markets experiencing large declines following the

announcement

We would expect CDS spreads to remain volatile while equity markets fluctuate

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

7

they will accept US Treasuries as collateral for their short term funding requirement. While it may take time to come to a consensus on this, in the

short term, it will surely affect capital markets. The situation will become

more important if any other agency downgrades US, leading to a systemic problem of triggering margin calls.

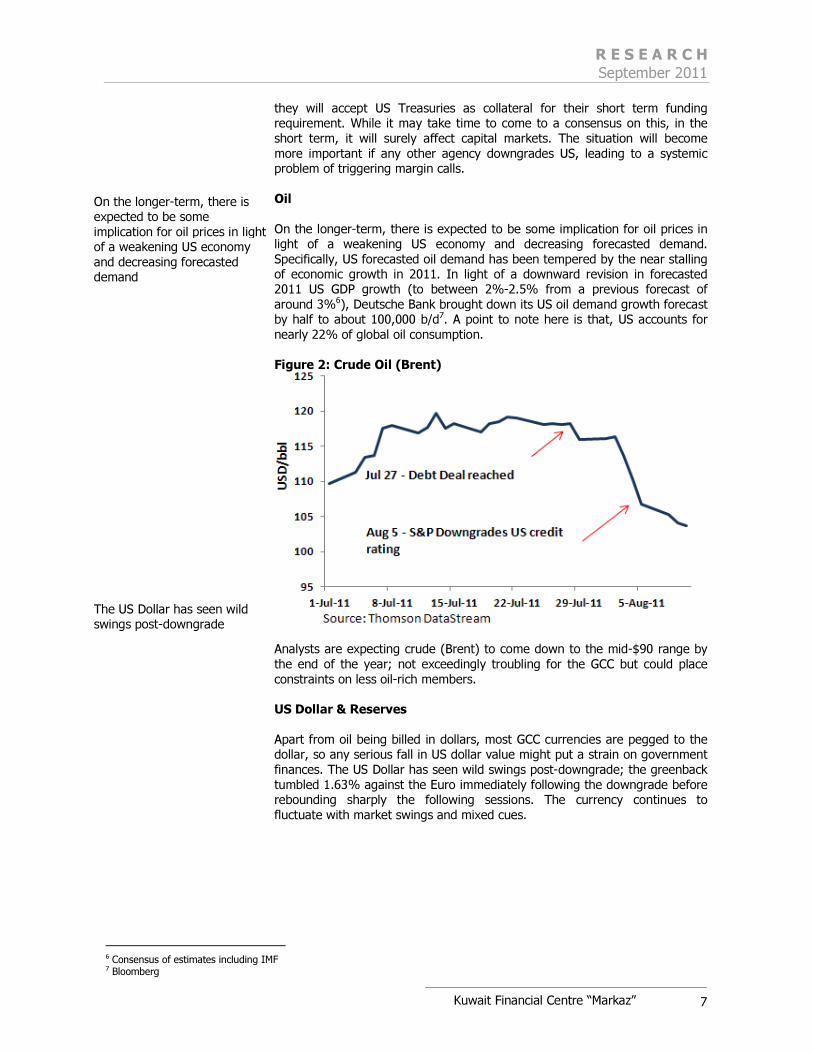

Oil

On the longer-term, there is expected to be some implication for oil prices in light of a weakening US economy and decreasing forecasted demand.

Specifically, US forecasted oil demand has been tempered by the near stalling of economic growth in 2011. In light of a downward revision in forecasted 2011 US GDP growth (to between 2%-2.5% from a previous forecast of

around 3%6), Deutsche Bank brought down its US oil demand growth forecast by half to about 100,000 b/d7. A point to note here is that, US accounts for

nearly 22% of global oil consumption.

Figure 2: Crude Oil (Brent)

Analysts are expecting crude (Brent) to come down to the mid-$90 range by

the end of the year; not exceedingly troubling for the GCC but could place

constraints on less oil-rich members. US Dollar & Reserves

Apart from oil being billed in dollars, most GCC currencies are pegged to the dollar, so any serious fall in US dollar value might put a strain on government

finances. The US Dollar has seen wild swings post-downgrade; the greenback

tumbled 1.63% against the Euro immediately following the downgrade before rebounding sharply the following sessions. The currency continues to

fluctuate with market swings and mixed cues.

6 Consensus of estimates including IMF 7 Bloomberg

On the longer-term, there is expected to be some

implication for oil prices in light of a weakening US economy

and decreasing forecasted demand

The US Dollar has seen wild swings post-downgrade

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

8

Figure 3: USD Impact

Corporates will have to pay more for their imports billed in other currencies. GCC countries depend on imports for most food items; any increase in food

prices will stroke inflation fears affecting economic growth.

Table 2: GCC Economic Indicators

USD bn 2007 2008 2009f 2010f 2011f

Reserves ex. gold 421 513 503 546 601

Imports 403 510 428 472 484

% of GDP 33.2 34.0 35.6 34.1 NA

Inflation (ave. % change) 6.9 11.1 2.7 3.3 4.4

Source: IIF

Gulf countries and sovereign wealth funds are estimated to hold a large amount of US Treasuries and dollar denominated assets which will depreciate

impacting mark to market valuations. Private Banks and other financial

institutions also have exposure to US Treasury, a mark down in their value will affect profitability – despite it being a notional loss. Officials from the UAE and Oman have already indicated that they are in no

hurry to discontinue their dollar peg. In fact, following the conclusion of the

debt deal, but prior to the downgrade, the UAE central bank made a surprise announcement that it had no US Treasury Bills in its reserves or any other

financial instrument issued by the US government, citing “very low return”. The announcement came as a surprise given the currency peg to the Dollar.

Anecdotal evidence suggests that the Central Bank has turned to Japan for Dollar-denominated government debt.

Given declining credibility in the US government, further dollar weakening and a larger divorce between economic realities between the two, the GCC

governments may wish to revisit and speed up plans to create a unified GCC currency as pegging to dollar leaves policymakers with limited room to

implement independent monetary policy decisions.

Cost of borrowing could see an increase thereby affecting corporate balance

sheets. Should US Treasury yields reverse their current course and begin rising, cost of equity would see an increase thereby affecting not only

US forecasted oil demand has been tempered by the near

stalling of economic growth in 2011

The US Dollar has seen wild

swings post-downgrade

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

9

corporate balance sheets but also valuation of said companies which may have stock market implications.

Floating rate bonds which are linked to US LIBOR rate might see increase in yields. Short term funding and refinancing will take a hit if liquidity dries up in

the market. As S&P downgrades other institutions related to US government, counterparty credit risk will increase leading to liquidity problems.

Will the sovereign wealth funds step in this time to support US Treasuries remains a big question.

Any increase in food prices will

stroke inflation fears affecting economic growth

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

10

Appendix1: AAA Fiasco: A Primer

On the 5th of August 2011 the S&P ratings agency downgraded the U.S.'s AAA credit rating for the first time,

slamming the nation's political process and criticizing lawmakers for failing to cut spending enough to reduce record budget deficits. The historic move signals a blow to the world’s largest economy and throws doubt on

an already tentative global economic recovery. S&P downgraded the rating by one notch from AAA to AA+ with a “negative” long-term outlook, implying that the agency could lower the long-term rating to 'AA' within

the next two years if there is less reduction in spending than agreed to, a rise in US interest rates, or new

fiscal pressures resulting in higher general government debt. The downgrade has wide-ranging implications in terms of not only borrowing costs, but also casting doubt on the US status as a global reserve currency.

According to JPMorgan Chase & Co, the downgrade could raise the US’ borrowing cost by about $100 bn a year. There are also significant medium and long term implications for currencies, commodities and the already fragile global economic recovery.

S&P’s decision follows Moody's and Fitch which affirmed their AAA credit ratings following the signing of the

$2.1 trillion deficit-reduction plan which includes a decision to increase the debt-ceiling. Moody's and Fitch also said that downgrades were possible if lawmakers fail to enact debt reduction measures in addition to

the economy weakening further. Chinese credit rating agency Dagong has also downgraded US credit rating from A+ to A with a negative outlook.

Rising public debt burden and policy uncertainty were the primary reasons behind the downgrade. Under S&P’s base case fiscal scenario net general government debt is expected to rise from an estimated 74% of

GDP by the end of 2011 to 79% in 2015 and 85% by 2021. Meanwhile, Fitch projects U.S. government debt, including debt incurred by state and local governments, to reach 100% of GDP by 2012, and continue to rise

over the medium term.

What is behind the downgrade?

This is not the first time the US faced a downgrade threat; a similar crisis loomed in 1995. It is worth noting that at the time, the debt was at just $4.9 trillion8 (or 71% of GDP) versus over $14 trillion (or 91.5% of

GDP) currently. However, at that time, the US economy was on a steady growth trajectory, growing at about 4% a year versus current sluggish growth. Given the political deadlocks which formed the backdrop of the

US debt crisis (See Appendix 2 for a timeline of events), much of the S&P downgrade report spoke of the

inadequacy of the US government and fractious political leadership which has proven unable, or unwilling, to efficiently lead the country’s fiscal management versus an inability to repay debts. S&P advocated a mixed

solution of spending cuts and revenue growth. But as the recent negotiations made it clear, the Republicans have been unwilling to allow any tax increases.

The fact remains that a downgrade has been a long time coming and there are structural issues within the US economy and fiscal situation that the governing parties have been largely unwilling to deal with in a

meaningful way.

Debt

A statutory limitation on federal debt is a long standing feature of the US fiscal framework and applies to nearly all Treasury debt. The debt limit has been changed many times in the past — ten in the last decade

and twice in 2009 alone. The agreement passed on August 2nd provides for an initial increase of the debt limit of $400 bn and introduces procedures that would allow the limit to be raised further in two additional

steps, for a cumulative increase of between $2.1 trillion and $2.4 trillion by end-2011. The debt deal also calls for as much as $2.4 trillion of reductions in expenditure over the next decade. These cuts will be

implemented in two steps: the $917 bn agreed to initially, followed by an additional $1.5 trillion that the

newly formed Congressional Joint Select Committee on Deficit Reduction is supposed to recommend by November 2011. The act contains no measures to raise taxes or otherwise enhance revenues, though the

committee could recommend them.

8 AP, August 3rd 2011

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

11

Figure 4: USA Federal Debt as % of GDP, 1940 – 2010

0

20

40

60

80

100

120

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Pu

bli

c D

ebt

as %

of

GD

P

Source: White House Office of Management and Budget

Deficit Critics of the last-ditch deficit-reduction plan say it amounts to little more than “can kicking” as it does not solve the major spending issues related to Social Security, Medicare and Medicaid and existing tax benefits

to the wealthy and business segments. Analysts have also been critical of the fact that the plan is largely dependent on spending cuts which could further derail the already tentative economic recovery. In addition

to nearly $10 trillion of outstanding treasury debt, the US is estimated to have $66 trillion of future liabilities at “net present cost”. Payments due from Medicaid, Medicare & Social Security alone are over six times the

current obligations of Treasury debt9. Social entitlement programs currently account for 58% of US expenses

amounting to nearly $2 trillion in 2010.

The US has been running budget deficit for the last 9 years continuously and suffers long-run fiscal problems of rising health costs, an aging population, and a staunch unwillingness to raise taxes.

Figure 5: US Fiscal Budget

Source: White House Office of Management and Budget.

Can the US get its rating back?

There are currently 18 countries which enjoy a AAA rating, following the downgrade of the US to AA+ status. The US was the oldest member of the club, followed by France. The US is certainly not the first, nor

will it be the last, to lose the coveted AAA status. However, it has been shown that once losing the rating, it can be very difficult to recover (Table). According to S&P, restoring the AAA rating can take a country

9 Kleiner Perkins Caulfield & Byers

World War II

2010 Public Debt = 62% of GDP

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

12

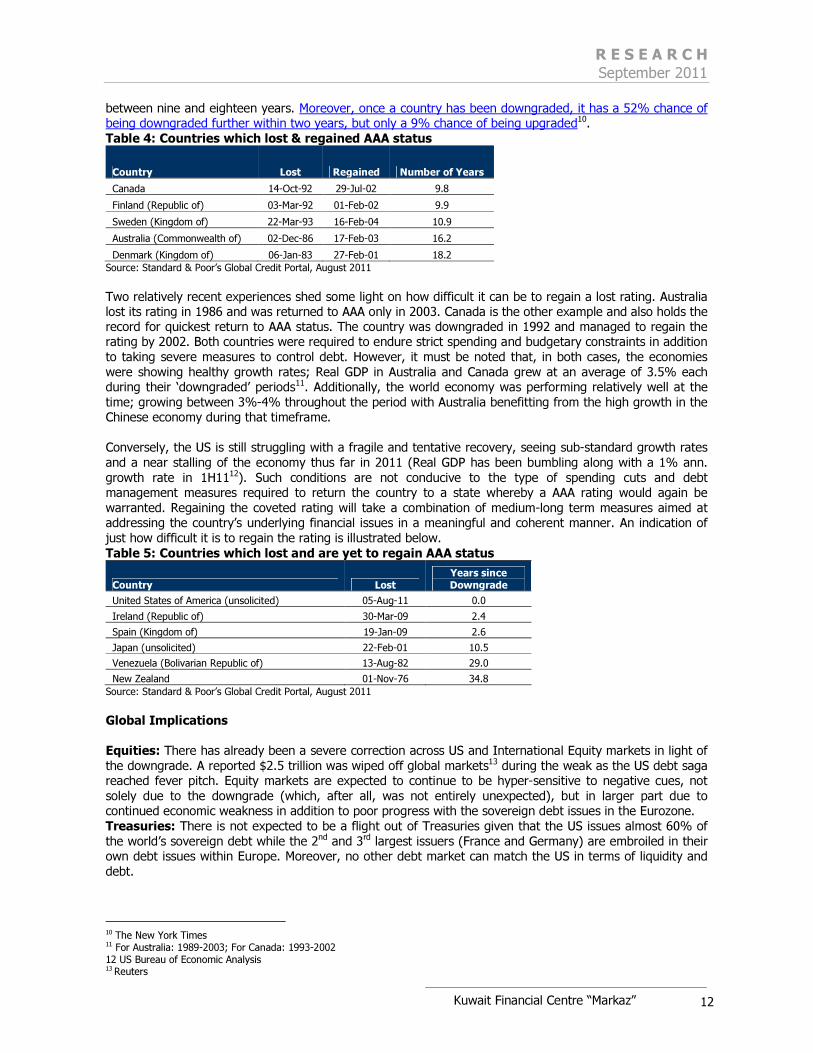

between nine and eighteen years. Moreover, once a country has been downgraded, it has a 52% chance of being downgraded further within two years, but only a 9% chance of being upgraded10.

Table 4: Countries which lost & regained AAA status

Country Lost Regained Number of Years

Canada 14-Oct-92 29-Jul-02 9.8

Finland (Republic of) 03-Mar-92 01-Feb-02 9.9

Sweden (Kingdom of) 22-Mar-93 16-Feb-04 10.9

Australia (Commonwealth of) 02-Dec-86 17-Feb-03 16.2

Denmark (Kingdom of) 06-Jan-83 27-Feb-01 18.2

Source: Standard & Poor’s Global Credit Portal, August 2011

Two relatively recent experiences shed some light on how difficult it can be to regain a lost rating. Australia lost its rating in 1986 and was returned to AAA only in 2003. Canada is the other example and also holds the record for quickest return to AAA status. The country was downgraded in 1992 and managed to regain the rating by 2002. Both countries were required to endure strict spending and budgetary constraints in addition

to taking severe measures to control debt. However, it must be noted that, in both cases, the economies

were showing healthy growth rates; Real GDP in Australia and Canada grew at an average of 3.5% each during their ‘downgraded’ periods11. Additionally, the world economy was performing relatively well at the

time; growing between 3%-4% throughout the period with Australia benefitting from the high growth in the Chinese economy during that timeframe.

Conversely, the US is still struggling with a fragile and tentative recovery, seeing sub-standard growth rates

and a near stalling of the economy thus far in 2011 (Real GDP has been bumbling along with a 1% ann.

growth rate in 1H1112). Such conditions are not conducive to the type of spending cuts and debt management measures required to return the country to a state whereby a AAA rating would again be

warranted. Regaining the coveted rating will take a combination of medium-long term measures aimed at addressing the country’s underlying financial issues in a meaningful and coherent manner. An indication of

just how difficult it is to regain the rating is illustrated below.

Table 5: Countries which lost and are yet to regain AAA status

Country Lost Years since Downgrade

United States of America (unsolicited) 05-Aug-11 0.0

Ireland (Republic of) 30-Mar-09 2.4

Spain (Kingdom of) 19-Jan-09 2.6

Japan (unsolicited) 22-Feb-01 10.5

Venezuela (Bolivarian Republic of) 13-Aug-82 29.0

New Zealand 01-Nov-76 34.8

Source: Standard & Poor’s Global Credit Portal, August 2011

Global Implications

Equities: There has already been a severe correction across US and International Equity markets in light of

the downgrade. A reported $2.5 trillion was wiped off global markets13 during the weak as the US debt saga reached fever pitch. Equity markets are expected to continue to be hyper-sensitive to negative cues, not

solely due to the downgrade (which, after all, was not entirely unexpected), but in larger part due to continued economic weakness in addition to poor progress with the sovereign debt issues in the Eurozone.

Treasuries: There is not expected to be a flight out of Treasuries given that the US issues almost 60% of

the world’s sovereign debt while the 2nd and 3rd largest issuers (France and Germany) are embroiled in their own debt issues within Europe. Moreover, no other debt market can match the US in terms of liquidity and

debt.

10 The New York Times 11 For Australia: 1989-2003; For Canada: 1993-2002 12 US Bureau of Economic Analysis 13 Reuters

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

13

US 10 year treasuries tumbled 8% prior to the downgrade before jumping 6.5% post-announcement. Yields have been pushed down to 10-month lows (down to 2%), reinforcing belief in the US’ creditworthiness.

Japan, the 2nd largest holder of treasuries, indicated that despite the downgrade, they remain attractive

investment targets. Treasury yields could come back up by 60-70bps over the “medium-term”14. According to Citi, given the distribution of US Treasuries, we are unlikely to see a flight from the asset either

willingly or through mechanical or ‘forced’ selling. Institutions, Funds, the Fed and non-US Central Banks and SWFs hold about 70% of the pie; these entities would either a) be willing and able to hold non-AAA rated

debt, or b) be unwilling to drop the paper for various political and economic reasons. The question mark

here, as Citi sees it, lies with the non-US Private Investors, who hold about 13% of the total. It is unclear whether they would move into other, more highly rated debt or into other US-denominated instruments.

Figure 6: US Treasury Ownership by Segment

What about China?

China, which is the largest holder of US Treasuries, has repeatedly pushed Washington towards increased

fiscal responsibility given the contagion it would have in the global monetary system. Following the

downgrade, China condemned the US for its “debt addiction” stating that given China’s position as “the largest creditor of the world's sole superpower, [it] has every right now to demand the United States

address its structural debt problems and ensure the safety of China's dollar assets.15” Table 7: Major Foreign Holders of Treasury Securities as at May-11

Country Value (USD bn)

China 1,160

Japan 912

UK 347

Oil Exporters# 230

Brazil 211

Others 1,654

Total 4,514 # - Oil exporters include Ecuador, Venezuela, Indonesia, Bahrain, Iran, Iraq, Kuwait, Oman, Qatar, Saudi Arabia, the United Arab

Emirates, Algeria, Gabon, Libya, and Nigeria

Source: Dept of Treasury

China urged the US to cut military and social welfare spending (which make up the bulk of “sticky” expenditures) and make serious changes to its fiscal management to avoid further downgrades which could

trigger widespread financial turmoil. The country went further by calling for “international supervision over

the issue of the U.S. dollar and a new, stable and secured global reserve currency” as “an option to avert a catastrophe caused by any single country.”

US Monetary Policy: the enacting of QE3 seems more likely than ever as the Fed has already announced

intentions to keep interest rates low for an extended period.

14 JPMorgan Chase 15 Xinhua news agency, August 5th 2011

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

14

Commodities: Gold’s status as a safe haven is likely to be reinforced by the rating downgrade; the precious metal is already at record highs (hovering around $1,858/oz), a gain of 31% YTD. Silver is already up about

39% for the year and is unlikely to see as much benefit from the uncertainty given that it has an industrial

component which will be negatively affected by weaker economic growth.

Currencies: The move will likely see a further weakening of the US Dollar, which is already down 7% against the Euro for the year. The other two “safe” currencies, i.e. Swiss Franc and Japanese Yen, are likely

to gain from the Greenback’s decline, at least in the short-term. The Yen is already up about 6% against the

Dollar for the year. Given the increased likelihood of QE3 coupled with a view (at least in some quarters) that this might be the first in a series of downgrades (especially given the Negative outlook by S&P and

Moody’s), the US Dollar is likely to weaken further in the medium term as Central Banks and sovereign institutions move out of USD and into other, ‘safer’ currencies. Questions are also being raised about America’s ability to continue to print the world’s reserve currency. With European Union not showing any

stability, US dollar will retain its status to be the world’s reserve currency at least in the medium term albeit with decreasing share of global reserves.

Appendix 2: International & Regional Viewpoints

Mohamed A. El-Erian, PIMCO – El-Erian expects that credit costs for American borrowers will be higher

over time and there will be an increase in risk premiums and volatility. He said “Animal spirits, already hobbled by the debt ceiling debacle, will again be dampened, constituting yet another headwind to the

generation of investment and employment”. El-Erian feels that the US Dollar’s status as the global reserve

currency is not in jeopardy following the downgrade. While criticism is sure to follow, at the moment, there is simply no alternative to the greenback. “… No other country is able and willing to replace the US at the

core of the global system…. Specifically, will it simply come to a new normality, with an AA+ at its core, or are further structural changes now inevitable?”

China - In its commentary, Chinese state-run Xinhua News Agency issued government statements which

severely criticized the US for living beyond its means and heralding the S&P downgrade as a sign that the

days of unlimited borrowing are gone. The agency urged citizens to become more self-disciplined and contribute towards rebuilding the economy “…. mounting debts and ridiculous political wrestling in

Washington have damaged America's image abroad. All Americans, both beltway politicians and those on Main Street, have to do some serious soul-searching to bring their country back from a potential financial

abyss.” The country went further by calling for international supervision over the US Dollar: “a new, stable

and secured global reserve currency may also be an option to avert a catastrophe caused by any single country.”

Citigroup Global Markets – According to Citigroup, the rating was not only expected, but was entirely

justified given the lack of fiscal leadership and inability to agree on appropriate debt and deficit reduction measures in the US. They also believe that downgrades could now spread across other developed nations

such as France and Germany. “We could be moving towards a world without AAA G7 sovereigns. The criteria applied by the rating agencies to the G7 sovereigns in the past have been, in our view, far too lenient.” Citigroup indicates that post-World War II, there has been a severe erosion in “tax administration capacity,

diminishing tax compliance in the private sector, and the evolution of political decision-making institutions, processes and practices that make it possible to mandate public spending without ensuring sustainable

funding for these expenditures.” The US downgrade brings an end to the time where a AAA rating for

advanced countries was not only ‘correct’, but a ‘right’. “Only a few small countries with a surviving culture of tax compliance and political institutions that effectively impose the government’s intertemporal budget

constraint may have AAA ratings in the not too distant future. For portfolio allocation, relative risk will be the driver now that 'risk free' is no longer an option.” Absolute Return Partners - In a letter to investors, the firm said that it feels the rating downgrade

doesn’t carry any meaning as the U.S. has only dollar denominated debt. “A nation that issues debt denominated solely in its own currency and which is in full control of its monetary policy, cannot default

unwillingly. Nations default because they run out of foreign currency to service their debt, but the U.S.

doesn’t need foreign currency to service its debt”. The letter also stated that this downgrade might have be a precursor to further downgrades in Europe as well. “With its downgrade of U.S. sovereign debt, Standard

and Poor’s has started a chain of events which can only make things worse in an already crisis hit eurozone.

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

15

For that reason, the decision to downgrade was not only badly timed but also ill considered; that it was probably justified is of little relevance at the moment.”

JPMorgan Chase & Co.’s - Terry Belton on a conference call hosted by the Securities Industry and Financial Markets Association forecasted that a rating cut could increase borrowing costs. “A U.S. credit-

rating cut would likely raise the nation’s borrowing costs by increasing Treasury yields by 60 to 70 basis points over the medium term”. He also predicted that “$100 billion a year is money being used for higher

interest rates and that’s money being taken away from other goods and services.”

Barclay’s Capital – The firm is of the view that the US debt downgrade will be a positive for dollar. "We

separate our discussion of the impact of a potential US downgrade into two – the immediate and the slightly longer-run consequences… The immediate effect would be one in which risk aversion increases and liquidity decreases, both of which support the USD.” Over the long term, Barclay’s Capital sees growth getting

curtailed because of tight monetary policies. “However, the fact that this is a US-driven risk, the USD will likely lag other safe-haven currencies (such as the JPY and CHF). Further out, we see fiscal tightening

weighing on growth and the USD weakening further, as monetary policy is kept looser for longer than the market is expecting."

Stephan S. Roach, Non-Executive Chairman of Morgan Stanley Asia - In a commentary on change

in Chinese policies indicated that China has lost confidence in America’s government and will not risk its

economic stability on Washington’s promises. “In recent years, Chinese Premier Wen Jiabao and President Hu Jintao have repeatedly expressed concerns about US fiscal policy and the safe-haven status of

Treasuries….” He also pointed out that the Chinese are revisiting their strategy of export-led growth and massive accumulation of dollar-denominated assets. “Those days are over. China recognizes that it no

longer makes sense to stay with its current growth strategy – one that relies heavily on a combination of

exports and a massive buffer of dollar-denominated foreign-exchange reserves… Long the most powerful driver of Chinese growth, there is now considerable downside to an export-led impetus”

David A. Rosenberg, Gluskin Sheff - In a recent report, indicated that the downgrade will lead to

tightening of budgets which is a positive for bond markets. He expects equity prices to come under pressure because of sluggish demand growth. “The big news is that the screws have been tightened on the fiscal

stimulus front. So on net, the downgrade is a deflationary event and as such is not negative but positive for

the bond market. History shows that every time a AAA country gets downgraded, the budgetary belt is tightened and yields decline every time.” Rosenberg also feels that there will not be a huge impact because

of rating downgrade given that US is still the reserve currency and S&P’s emphasis was more on political factors. “The U.S. can print its own money and certainly has the wherewithal to pay its debts so the

downgrade is more symbolic than real…. But default risks are no different today than they were last Friday

morning, and the Treasury had already said repeatedly that bondholders would be made whole even if there was to be a government shutdown.”

Regional

Ibrahim Dabdoub, CEO of National Bank of Kuwait – Mr. Dabdoub feels that the US rating downgrade

was not a surprise and does not expect it to affect the economy. “….dollar remains the first reserve currency worldwide. Thus, the recent cut will unlikely have great influence on the US economy, on condition that the

US government takes the right measures to slash spending.” Ibrahim Dabdoub doesn’t foresee any major negative impact on GCC economies, because of large surpluses and government spending programs.

“….government spending remains the main driver for the GCC economies, expecting expenditure to accelerate in H2-11, after falling shy of expectations in the first half.”

Said A. Al Shaik, Group Chief Economist of NCB – In a recent report indicated that the near term implications will be minimal but expects negative impact on US Dollar over the long term. “The longer-term

effects are driven primarily by whether international markets will eventually also downgrade the US. Consequently, the biggest impact should be through the effect on the US dollar as a reserve currency”. Al

Shaik feels that the downgrade will impact Saudi Arabia in three ways – Crude Oil demand & price changes,

US Dollar movement and through official holdings of US treasuries. “Holders of US treasuries like Saudi Arabia should not be concerned that they may not receive interest payments on US bonds. However, the

value of those payments will essentially decline, given the fact that with more dollars in circulation due to the printing presses….”

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

16

Jadwa Investment in its report titled “Debt, downgrade and Saudi Arabia” expects US to continue its position as a safe haven despite the downgrade. “The breadth, depth and liquidity of the US financial

markets also support its safe haven status. No other financial market is of a comparable size or has the

same variety of financial instruments as the US”. They are also of the view that Saudi economy will not face any major negative consequences and that currency peg will continue. “We do not think ongoing events will

have too great an impact on the Saudi economy, as the growth momentum is coming from high government spending that can be afforded comfortably…. We do not think the downgrade will have an impact on the

exchange rate peg between the riyal and the dollar.”

Alshall Consulting in its Weekly Economic report indicated that US will continue its dominant position in

the world. “The USA will remain for one to two decades as the largest global economy, trustworthy, and the first destination for creditors and investors”. They are also of the view that there will be gradual transition of economic power and search for substitutes for US Dollar as reserve currency will take place. ”What is

happening is a more significant indicator for the beginning of an era in history during which the economic weight will shift from the West to the East and will gradually introduce alternatives and partners to the dollar

as a global reserve currency.”

Appendix 3: The US Downgrade: A Timeline16

The S&P downgrade is the culmination of a saga which began in late 2010 concerning the US’ rampant debt

and runaway deficit growth. The government has been running a rapidly widening deficit for the last decade with high debt accumulation.

Dec. 1, 2010 - A bipartisan deficit-reduction panel issues a report advocating a 10 yr plan which includes $3 trillion in spending cuts and $1 trillion in revenue increases.

January 2011 - Six Republican and Democratic senators, known as the "Gang of Six," begin talks on a

long-term deficit-reduction deal.

Feb. 19 - The House passes a current fiscal year budget that would cut $61 bn in spending. The

Democratic-controlled Senate defeats it one month later.

April 9 – The US government approaches a shutdown before Obama and congressional leaders cut an 11th

hour deal and agree on a fiscal budget that cuts $38 bn in spending. Billed as the largest spending cut in U.S. history, it actually causes the government to spend $3.2 bn more in the short term.

April 13 - After Obama's initial proposal is deemed inadequate, the president lays out a new deficit-

reduction plan that would save $4 trn over 12 yrs.

April 15 - The House passes a budget which cuts spending by $6 trillion over 10 yrs, in part by scaling back

medical care for the elderly and the poor.

May 9 - House Speaker John Boehner (Republican), says any increase in debt ceiling must be matched by

an equal amount of spending cuts. The Treasury estimates it needs at least $2 trn to cover borrowing through the 2012 elections.

May 11 - House Republicans release a spending outline for the coming fiscal year that has deep cuts in

education, labor and health programs which are highly prized by Democrats.

May 16 - The United States reaches its $14.3 trillion debt limit. The Treasury Department begins tapping other sources of money to cover the debt.

June 9 - Treasury Secretary, Timothy Geithner argues that tax increases need to be part of any debt deal,

but Republicans remain unmoved.

16 Reuters, July 25th 2011

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

17

June 23 - Republicans declare an impasse in talks with the White House, saying Democrats are insisting on roughly $400 bn in new revenue by closing tax breaks for the wealthy and certain business sectors.

June 29 - The International Monetary Fund says the United States must lift its debt limit soon to avoid a "severe shock" to global markets and a still-fragile economic recovery. Obama calls for new steps to spur job

growth and tax hikes on the rich, irking Republicans who remain focused on deficit cuts.

July 3 - Obama and Boehner discuss "grand bargain" that would save $4 trn over 10 yrs through a tax code

overhaul and trims to benefit programs.

July 8 - A dismal jobs report focuses new attention on the sputtering economy. Obama says uncertainty

about the debt ceiling talks is hurting economic expansion.

July 9 - Boehner says grand bargain is out of reach because Republicans will not accept the tax increases Democrats are demanding. He calls for a more modest $2 trillion package that would rely mostly on

spending cuts.

July 13 - Moody's puts the US on review for possible downgrade. Obama meets lawmakers for nearly two hours but a deal remains elusive.

July 14 – S&P Ratings says there is a 50% chance it could cut the U.S. credit rating if talks remain

stalemated. Obama suspends talks and gives party leaders 24-36 hours to deliver a deadlock-breaking "plan of action."

July 18 - Republicans push for a measure that would cut and cap government spending and require an amendment to the U.S. Constitution requiring a balanced budget. Obama says he will veto it should

Congress send it to his desk.

July 19 - The "Gang of Six" resurfaces with a deficit reduction plan that proposes $3.75 trillion in savings

over 10 years and contains $1.2 trillion in new revenues. Obama pushes Congress to take serious consideration of it.

July 21 - Obama and Boehner discuss a possible $3 trillion deficit-cutting deal that upsets Democrats for

not including enough tax rises to offset spending cuts. Obama repeats some revenues will need to be part of

any accord.

July 22 - Boehner breaks off talks with Obama over impasse on revenue increases, raising concerns about whether a deal can come together by the August 2nd deadline.

July 24 - Republicans and Democrats retreat to their corners and focus on separate plans to avert default. Democrats meet with Obama to discuss a proposal to cut $2.5 trillion in spending without revenue. Boehner

urges Republicans to stay united to secure the most budget cuts possible.

July 31 – Leaders of both political parties reach a last minute deal which aims to raise the debt ceiling by

$2.1 trillion with a plan to cut the fiscal deficit by up to $2.4 trillion over a 10 year period. The plan also includes the formation of a bipartisan committee to seek out $1.2 trillion in spending cuts by the end of the

year.

August 2 – Moody’s affirms US credit rating, but places the country on “Negative” outlook, indicating a

possible downgrade over 12-18 months. Fitch announces that it will provide its rating by end of August.

August 5 – S&P Ratings downgrades US long-term credit rating from AAA to AA+ with a “Negative” outlook, implying the chance for further downgrade within 2 years. The move causes the S&P 500 to finish

with its largest weekly decline since November 2008 (7.2%); other US and world indices see heavy declines.

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

18

Appendix 4a: S&P Global Ratings

AAA AA+ AA AA-

Australia (UR) Belgium (UR) Abu Dhabi China

Austria New Zealand Bermuda Japan (UR)

Canada United States of America (UR) Kuwait Saudi Arabia

Denmark

Qatar Taiwan (UR)

Finland

Slovenia

France (UR)

Spain

Germany (UR)

Guernsey

Hong Kong

Isle of Man

Liechtenstein

Luxembourg

Netherlands (UR)

Norway

Singapore (UR)

Sweden

Swiss Confederation (UR)

United Kingdom (UR)

A+ A A-

Chile Andorra Aruba

Italy (UR) Czech Republic Botswana

Slovak Republic Emirate of Ras Al Khaimah Malaysia

Estonia Poland

Israel

Korea

Malta

Oman

Trinidad and Tobago

Note: (UR) indicates Unsolicited Rating Source: Standard & Poor’s

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

19

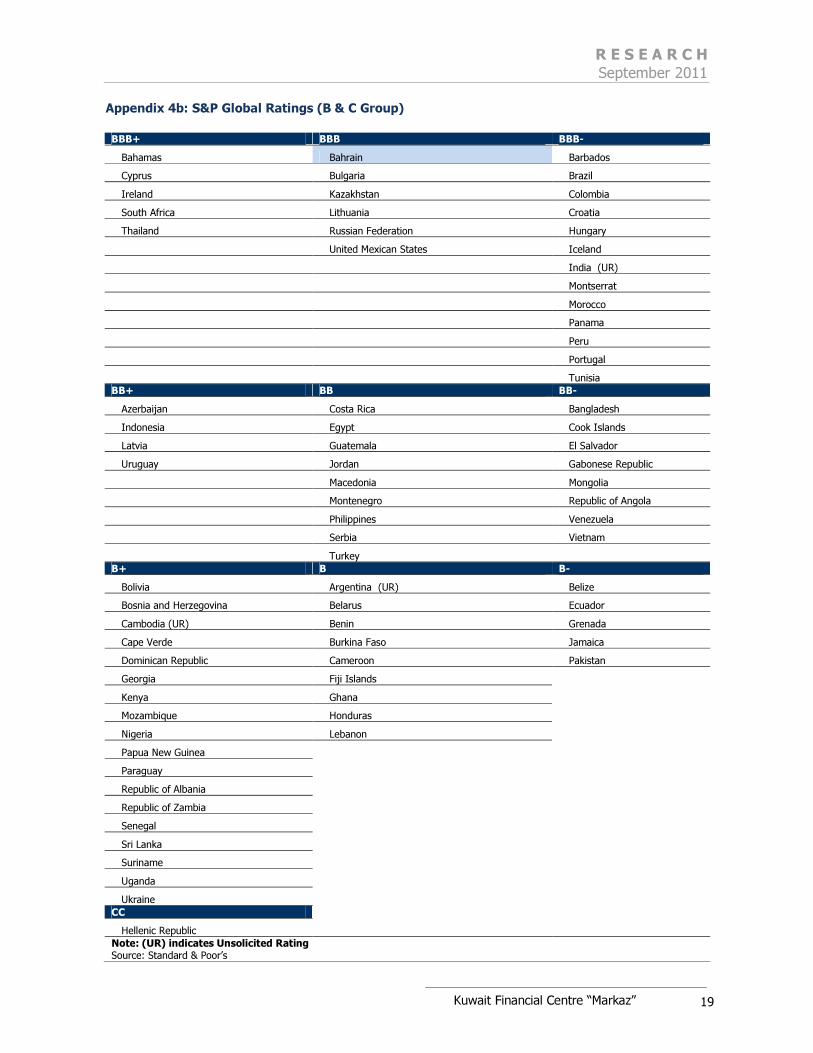

Appendix 4b: S&P Global Ratings (B & C Group)

BBB+ BBB BBB-

Bahamas Bahrain Barbados

Cyprus Bulgaria Brazil

Ireland Kazakhstan Colombia

South Africa Lithuania Croatia

Thailand Russian Federation Hungary

United Mexican States Iceland

India (UR)

Montserrat

Morocco

Panama

Peru

Portugal

Tunisia

BB+ BB BB-

Azerbaijan Costa Rica Bangladesh

Indonesia Egypt Cook Islands

Latvia Guatemala El Salvador

Uruguay Jordan Gabonese Republic

Macedonia Mongolia

Montenegro Republic of Angola

Philippines Venezuela

Serbia Vietnam

Turkey

B+ B B-

Bolivia Argentina (UR) Belize

Bosnia and Herzegovina Belarus Ecuador

Cambodia (UR) Benin Grenada

Cape Verde Burkina Faso Jamaica

Dominican Republic Cameroon Pakistan

Georgia Fiji Islands

Kenya Ghana

Mozambique Honduras

Nigeria Lebanon

Papua New Guinea

Paraguay

Republic of Albania

Republic of Zambia

Senegal

Sri Lanka

Suriname

Uganda

Ukraine

CC

Hellenic Republic Note: (UR) indicates Unsolicited Rating

Source: Standard & Poor’s

R E S E A R C H September 2011

Kuwait Financial Centre “Markaz”

20

R E S E A R C H September 2011

R E S E A R C H September 2011

R E S E A R C H September 2011

Disclaimer

This report has been prepared and issued by Kuwait Financial Centre S.A.K (Markaz), which is regulated by

the Central Bank of Kuwait. The report is owned by Markaz and is privileged and proprietary and is subject

to copyrights. Sale of any copies of this report is strictly prohibited. This report cannot be quoted without the

prior written consent of Markaz. Any user after obtaining Markaz permission to use this report must clearly

mention the source as “Markaz “.This Report is intended to be circulated for general information only and

should not to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financial

instruments or to participate in any particular trading strategy in any jurisdiction. The information and

statistical data herein have been obtained from sources we believe to be reliable but in no way are

warranted by us as to its accuracy or completeness. Markaz has no obligation to update, modify or amend

this report.

This report does not have regard to the specific investment objectives, financial situation and the particular

needs of any specific person who may receive this report. Investors are urged to seek financial advice

regarding the appropriateness of investing in any securities or investment strategies discussed or

recommended in this report and to understand that statements regarding future prospects may not be

realized. Investors should note that income from such securities, if any, may fluctuate and that each

security’s price or value may rise or fall. Investors should be able and willing to accept a total or partial loss

of their investment. Accordingly, investors may receive back less than originally invested. Past performance

is historical and is not necessarily indicative of future performance.

Kuwait Financial Centre S.A.K (Markaz) does and seeks to do business, including investment banking deals,

with companies covered in its research reports. As a result, investors should be aware that the firm may

have a conflict of interest that could affect the objectivity of this report. For further information, please contact ‘Markaz’ at P.O. Box 23444, Safat 13095, Kuwait. Tel: 00965 1804800 Fax: 00965

22450647. Email: [email protected]