how resilient will international supply chains prove in 2010?

TRANSCRIPT

2

How resilient will international supply chains prove in 2010?An report, in association with RBS

921922.indd 2 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

3

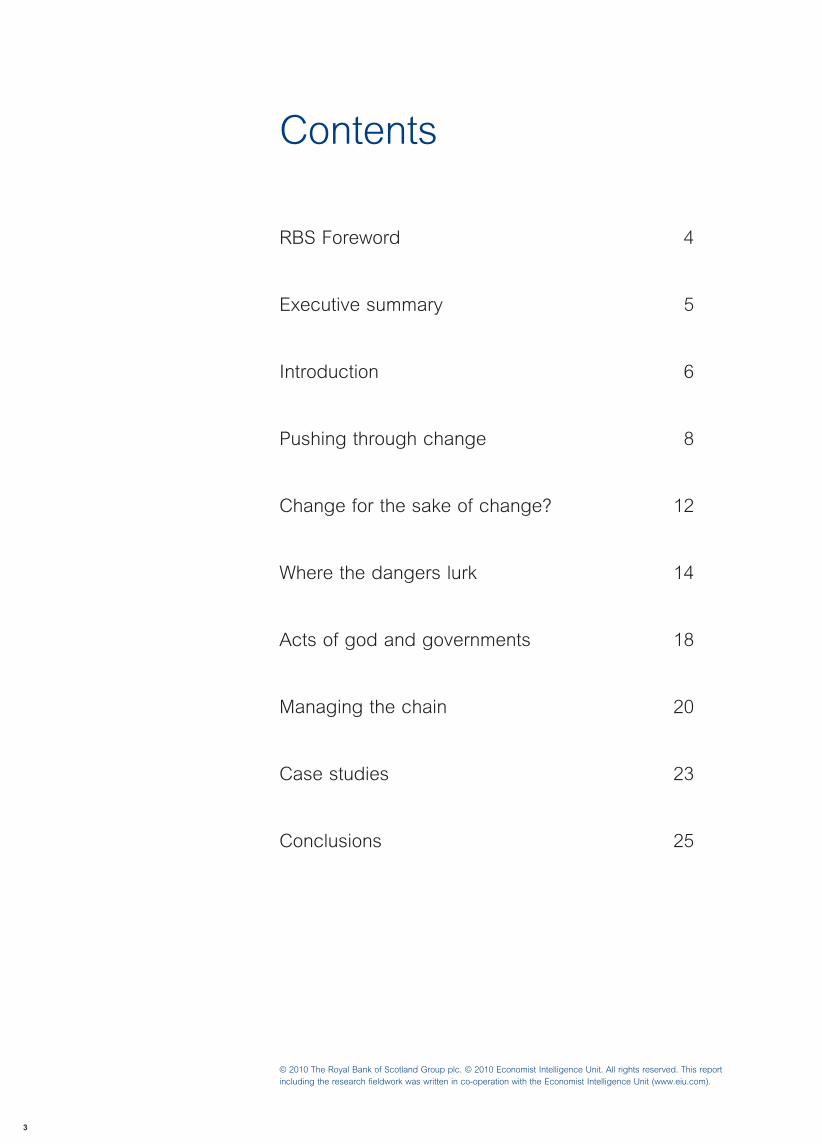

RBS Foreword 4

Executive summary 5

Introduction 6

Pushing through change 8

Change for the sake of change? 12

Where the dangers lurk 14

Acts of god and governments 18

Managing the chain 20

Case studies 23

Conclusions 25

Contents

© 2010 The Royal Bank of Scotland Group plc. © 2010 Economist Intelligence Unit. All rights reserved. This report including the research fieldwork was written in co-operation with the Economist Intelligence Unit (www.eiu.com).

921922.indd 3 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

4

RBS Foreword

That’s why we’ve commissioned the Economist Intelligence Unit to produce this independent report which provides insight into the general health of supply chains within a sample of 250 UK-based corporates.

The results show that over half the companies surveyed were confident that they would increase their revenues in 2010.

Interestingly, even for larger companies, the report shows that China is not the obvious choice it once was. If the financial markets are to be believed, the competitive advantage that China’s undervalued currency brings may not be available for much longer. Buyers will therefore extend their supply chains to other areas of the globe in search of cheaper or better sources. But of course, a supply chain is only as strong as its weakest link. As globalisation on both the supply and market side increases, the complexity of supply chains also increases, leading to a closer, more co-dependent relationship with suppliers. This, as we know, can often be a delicate balance. What is certain, however, is that supply chains are gradually playing a more prominent part in the fortunes of companies, and the effective management of these chains is becoming a critical determinant of competitiveness.

That’s where RBS can help. Although this report suggests progress is definitely being made in managing the risks inherent in extended supply chains, there is still much work to be done. We have years of experience when it comes to supporting our customers’ international operations. And our extensive international network in over 35 countries means we can really help your business make the most of the opportunities out there.

I’d like to take this opportunity to thank you for your interest in the Economist Intelligence Unit survey and report. I hope you find it of use.

John LyonsHead of Global Transaction Services UKThe Royal Bank of Scotland plc

Please note that the report contained in this paper is sponsored by The Royal Bank of Scotland Group plc (RBS), although the findings expressed do not necessarily reflect our views. No representation or warranty, express or implied, is or will be made and no responsibility or liability is or will be accepted by RBS or any of our officers or employees in relation to the accuracy or completeness of this report and any such liability is expressly disclaimed.

There’s no doubt that the economic challenges of the last year have changed the face of commerce in the UK. But as companies look to diversify and take advantage of the potential profits international markets can offer, they must also balance the risks and supply costs involved. This means that the importance of maintaining healthy and cost‑effective supply chains has never been greater.

921922.indd 4 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

5

Executive summary

A key strategy for increasing revenues and preserving margins is cutting costs with suppliers. Some 63% of respondents negotiated lower prices in the past year, and 41% hoped to do so in 2010. A fifth had switched the countries in which suppliers are located, a third had reduced the number of suppliers and half reported that their relationships with their remaining suppliers were, indeed, more cooperative than before the recession.

Modern supply chain management (SCM), however, extends well beyond price cutting. The term SCM recognises that when some 80% of a product’s content is bought in, as is now common practice, the producing company relies heavily on its selection of suppliers, and close cooperation with them. Survey respondents listed specialist expertise as the second most important consideration when choosing a supplier, after cost.

In spite of the fragile state of the global economy, the financial stability of suppliers is just the third most important consideration when selecting a supplier. Only 36% of respondents selected financial stability as a consideration when choosing an overseas supplier. However, after a supplier is selected, financial accounts are the top area for ongoing monitoring, chosen by 64% of respondents.

Insolvency of a supplier is a major threat to the supply chains of a significant minority of respondents. 29% of respondents have experienced an insolvency in the past year and a quarter see insolvency of a supplier as one of the biggest threats to the resilience of their supply chains over the next year.

Respondents are also looking to take advantage of opportunities created by the recession. The top three opportunities spotted were greater availability of talented workers in the labour market, lower interest rates (which makes financing of debt less expensive) and better prospects for mergers and acquisitions. A quarter will use the impetus of the recession to review and/or rationalise their supply chains.

The financial crisis has put the spotlight on companies’ supply chains as management struggles to realise the benefits of outsourcing and reduce risks. The results of this survey suggest that their efforts have paid off: well over half the companies were confident of increasing their revenues in 2010, retaining their customer base and preserving their margins. Other major findings include:

921922.indd 5 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

6

Introduction

At the same time, the number of foreign subsidiaries has massively increased over the past 20 years – tripling, according to estimates from McKinsey. Of the most talked about hotspots, China recovered from the financial crisis well enough in the last quarter of 2009 to notch up 10.7% annualised growth, and growth is forecast to continue at least 8% for the next few years. And India is not far behind, producing hundreds of thousands of trained engineers every year, and growing economically at a pace just slightly slower than China’s.

Companies that can take advantage of such fast-evolving supply opportunities wherever they may arise hold a valuable competitive weapon, but require a well-managed modern supply chain with the ability to cope with rapid change and volatility. This type of supply chain requires a standard of management several degrees higher than that usually encountered in the traditional purchasing role.

The supply chain model is now more of a network, with suppliers assuming the role of partners and frequently carrying some of the risk. The recent recession and the credit crisis have tested such supply chains and relationships as never before, and many suppliers have gone out of business – 29% of respondents to this survey reported such instances in the past year. Companies that have adopted lean production techniques, such as just-in-time inventory and reduced numbers of suppliers, have had to be especially vigilant.

‘Companies don’t compete: supply chains compete’ is an old adage that is becoming more compelling as the years go by. In the days when companies manufactured, refined or processed everything themselves, their fate was largely in their own hands. Now, approximately 80% of the material value of a complex product, whether an Airbus passenger jet or a Stannah stairlift, is likely to have been bought in, whether on the grounds of price for a simple plastic moulding or expertise for an electronic control system.

921922.indd 6 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

7

It is not surprising, therefore, that at this stage of the economic cycle, risk is still at the forefront of everyone’s minds. The moment of truth for a hard-pressed company can be the point at which sales start to increase again after a recession, but when the cash requirements finally exceed resources. That perhaps explains why in this survey all but a few of the larger companies (those with annual revenues in excess of $1bn) apparently attach high priority to the risks lurking in their supply chains, and are aware that they need to be constantly alert to possible problems. Extending the supply chain concept from supplier to customer is not uncommon (if not always effective) in the consumer industries (see the case study on PJ Cussons), but elsewhere it is still a rare concept. The arguments in its favour are universal but, in many companies, departmental boundaries may prove insuperable.

Overall, however, the results suggest that by managing their supply chains effectively, respondents have come through the financial crisis in pretty good shape. Of course, the survey does not cover the failures, only the survivors, but well over half the respondents to this survey of 282 UK companies, conducted in January 2010, were confident of preserving their margins over the next 12 months, increasing their revenues and retaining their existing customer base.

Still, many had reduced both the number of suppliers and their supply chain staff, but claimed they now monitor the remaining suppliers more closely. Collaboration and their systems have improved, and (perhaps as a result) their demand forecasting and continuity planning are more accurate.

The implication is that communication within the company is now generally smoother than in the past, especially between the supply chain managers and the sales and marketing teams. But some believe it is still not good enough, specifically in their liaison with the far end of the chain (i.e. their customers).

Effective liaison assumes greater importance given the increasing volatility in both the target markets and the suppliers’ markets. The chief supply chain officer (if one is appointed) acts as piggy-in-the-middle, who has the added responsibility, whatever the financial pressures, of keeping inventories at a safe minimum and unit costs at a level that satisfies the finance director, while leaving the supplier with enough incentive to provide a reliable service.

As a company’s national and international operations develop, the complexity in the supply chain increases exponentially, with different markets, different products and different manufacturing and distribution centres. Yet still, the survey shows that frequently the supply chain has no single head, or is decentralised. It is difficult to see how a process of optimisation could be achieved in such circumstances.

Many companies, it seems, have yet to wake up to the scale of possibilities that a well-managed supply chain can offer, not just in terms of operational efficiency, but as an indispensable weapon in the modern competitive world.

921922.indd 7 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

8

“Don’t waste a good crisis”, as White House chief of staff Rahm Emanuel told financial regulators last year. Far‑sighted managers can seize the opportunity to initiate a long‑desired radical change at a time when nervous colleagues and other stakeholders are more receptive to change. The supply chain, involving as it does practically every department in the company, as well as a long list of suppliers, sometimes needs a crisis before all parties will fall into line.

For example, Toyota, facing a $2bn loss in the 2009/10 financial year as a result of the recession, even before the devastating eight million car product recall programme, announced in December 2009 that, among other changes, it was merging three purchasing divisions into two and imposing a 30% cut in prices to suppliers for a range of components for its 2013 models.

Despite its recent problems Toyota is still considered a world leader in managing its supply chain, having demonstrated in the Toyota Production System how to work with suppliers to reduce costs on both sides and improve productivity. Its ‘obeya’ process brings all parties together to discuss ideas and projects, and break down functional silos.

The evidence from this survey is that on a smaller scale, many respondents are faced with similar problems to Toyota and appear to be following the car firm’s lead: 56% said they were taking steps to improve collaboration and 48% went further by introducing systems to connect and align interests more closely with supply partners.

Their primary objective, as always, was to find ways to cut costs by negotiating lower prices – 63% said they had done so in the past year and 41% hoped to in the coming year. Perhaps to focus their relationships, 33% had reduced the number of suppliers they used and, possibly for that reason, 35% had cut their own supply chain staff. Whatever the results of their efforts, 50% agreed that suppliers were more cooperative as a result of the recession.

Pushing through change

921922.indd 8 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

9

Source: Economist Intelligence Unit

Which of the following steps has your organisation taken in the past 12 months as a result of the current downturn?

Negotiated lower prices from suppliers

Reduced headcount in supply chain function

Reduced number of suppliers

Implemented a sustainability strategy

Diversified supply chain

Increased payment terms to suppliers

Invested in supply chain management technology

Reduced capacity levels

Moved production to lower-cost countries

Increased output volumes

None of the above

0 10 20 30 40 50 60 70 80 90 100%

63%

34%

33%

32%

29%

26%

25%

23%

19%

18%

5%

921922.indd 9 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

10

Source: Economist Intelligence Unit

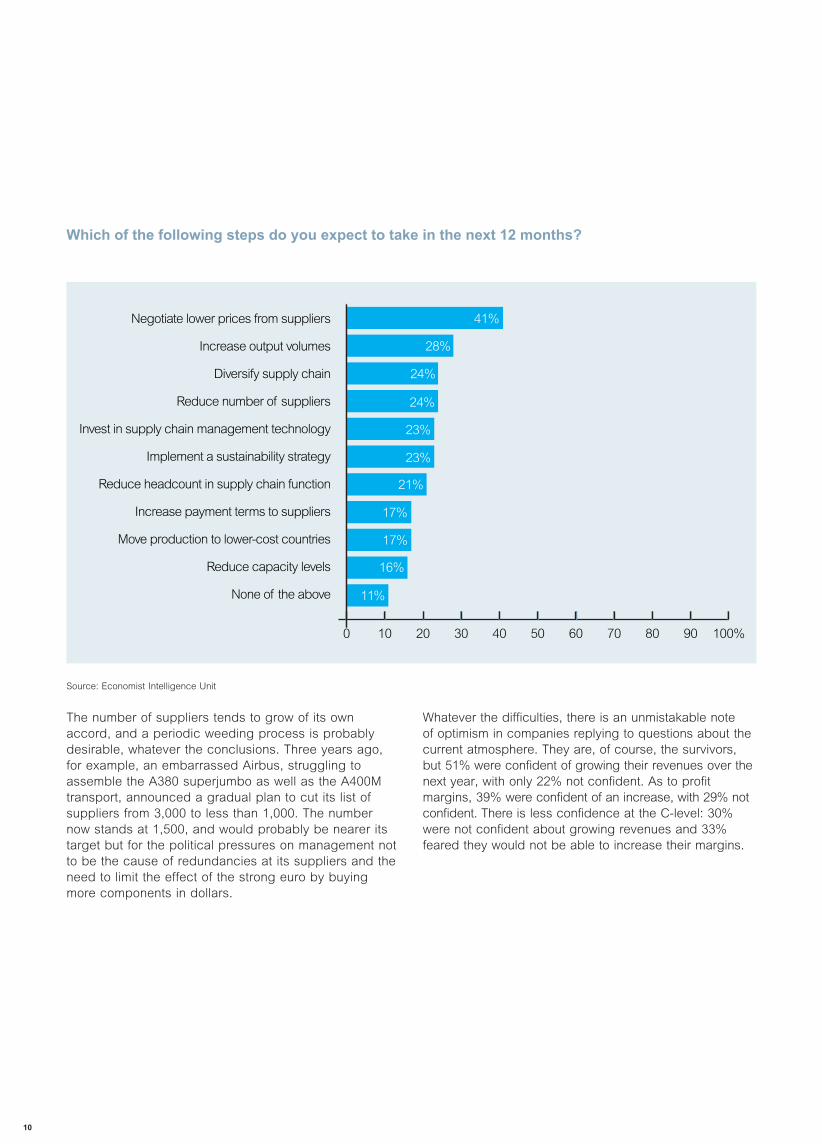

Which of the following steps do you expect to take in the next 12 months?

The number of suppliers tends to grow of its own accord, and a periodic weeding process is probably desirable, whatever the conclusions. Three years ago, for example, an embarrassed Airbus, struggling to assemble the A380 superjumbo as well as the A400M transport, announced a gradual plan to cut its list of suppliers from 3,000 to less than 1,000. The number now stands at 1,500, and would probably be nearer its target but for the political pressures on management not to be the cause of redundancies at its suppliers and the need to limit the effect of the strong euro by buying more components in dollars.

Whatever the difficulties, there is an unmistakable note of optimism in companies replying to questions about the current atmosphere. They are, of course, the survivors, but 51% were confident of growing their revenues over the next year, with only 22% not confident. As to profit margins, 39% were confident of an increase, with 29% not confident. There is less confidence at the C-level: 30% were not confident about growing revenues and 33% feared they would not be able to increase their margins.

Negotiate lower prices from suppliers

Increase output volumes

Diversify supply chain

Reduce number of suppliers

Invest in supply chain management technology

Implement a sustainability strategy

Reduce headcount in supply chain function

Increase payment terms to suppliers

Move production to lower-cost countries

Reduce capacity levels

None of the above

0 10 20 30 40 50 60 70 80 90 100%

41%

28%

24%

24%

23%

23%

21%

17%

17%

16%

11%

921922.indd 10 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

11

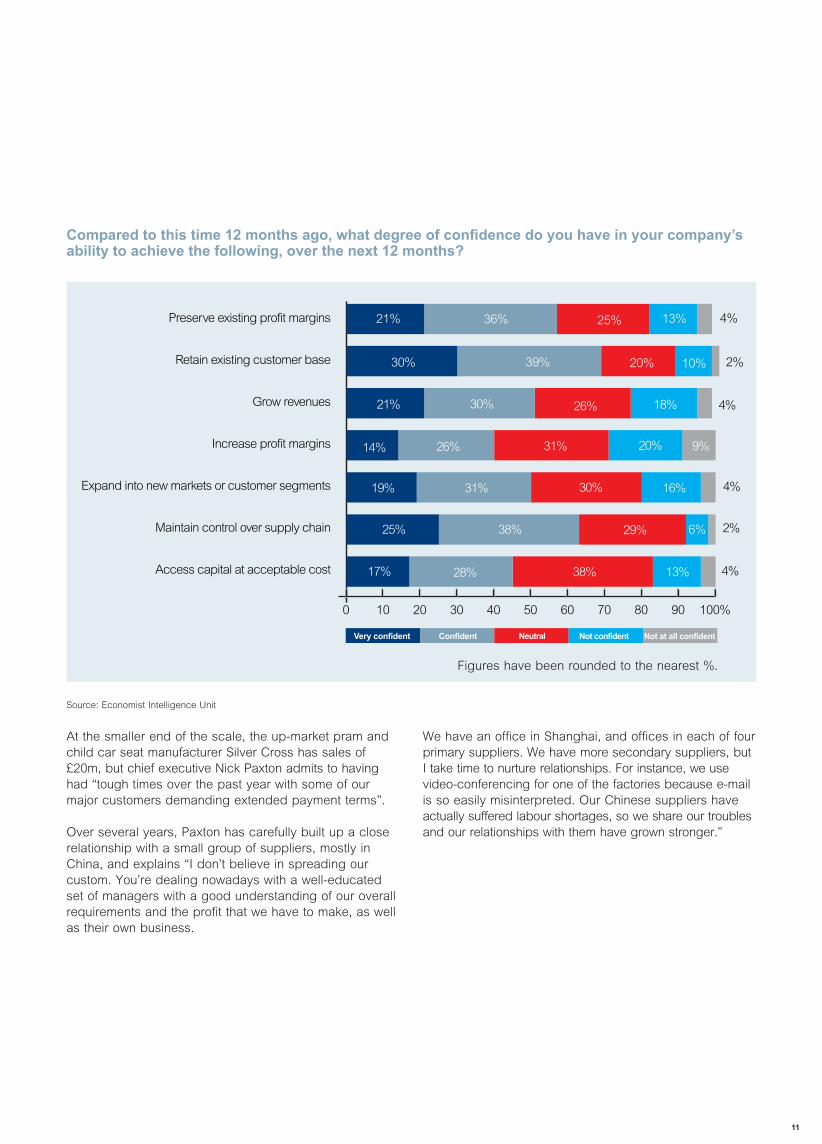

Compared to this time 12 months ago, what degree of confidence do you have in your company’s ability to achieve the following, over the next 12 months?

Source: Economist Intelligence Unit

Figures have been rounded to the nearest %.

At the smaller end of the scale, the up-market pram and child car seat manufacturer Silver Cross has sales of £20m, but chief executive Nick Paxton admits to having had “tough times over the past year with some of our major customers demanding extended payment terms”.

Over several years, Paxton has carefully built up a close relationship with a small group of suppliers, mostly in China, and explains “I don’t believe in spreading our custom. You’re dealing nowadays with a well-educated set of managers with a good understanding of our overall requirements and the profit that we have to make, as well as their own business.

We have an office in Shanghai, and offices in each of four primary suppliers. We have more secondary suppliers, but I take time to nurture relationships. For instance, we use video-conferencing for one of the factories because e-mail is so easily misinterpreted. Our Chinese suppliers have actually suffered labour shortages, so we share our troubles and our relationships with them have grown stronger.”

Preserve existing profit margins

Retain existing customer base

Grow revenues

Increase profit margins

Expand into new markets or customer segments

Maintain control over supply chain

Access capital at acceptable cost

16%

6%

21% 36% 25% 13%

30% 39% 20%

4%

10% 2%

21% 30% 26% 18% 4%

14% 26% 31% 20% 9%

19% 31% 30% 4%

25% 38% 29% 2%

17% 28% 38% 13% 4%

Very confident Confident Neutral Not confident Not at all confident

0 10 20 30 40 50 60 70 80 90 100%

921922.indd 11 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

12

Change for the sake of change?

Even among larger companies, China is not quite the obvious choice that it once was. Some 47% of larger companies, with over £1bn in revenues, source some of their supplies there, compared to only 19% of firms with less than £500m. But if the financial markets are to believed, the competitive advantage that China has because of its undervalued currency may not be available for much longer. Output continues to rise in China, but so do wages, therefore cheaper cost of labour is not a guarantee either.

Perhaps in consequence, while 47% of the largest firms currently source from China, just 42% say they are enthusiastic about sourcing opportunities there over the next three years, with slightly more (43%) now favouring India. Oddly, smaller firms have moved in the opposite direction, with just 19% currently sourcing from China but, 27% say they expect to source from there next year and for it to offer the greatest sourcing opportunities over the next three years. Equally surprising, while 41% of companies currently source some of their purchases in North America, just 28% expect to over the next year, and just 14% say it will offer the best opportunities over the next three years.

What Paxton and bosses in a similar position disapprove of is switching suppliers, even countries, for a relatively small cost advantage. Among all survey respondents, 19% reported moving their production to lower cost countries. Significantly, the proportion was 12% in companies with below £500m turnover but 26% in those above £1bn. The critics say that however big the saving, it is likely to be temporary. Meanwhile, the quality and reliability of the supplies over a period will be untested, and the advantages of close cooperation in design, marketing and finance will have to be built anew.

921922.indd 12 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

13

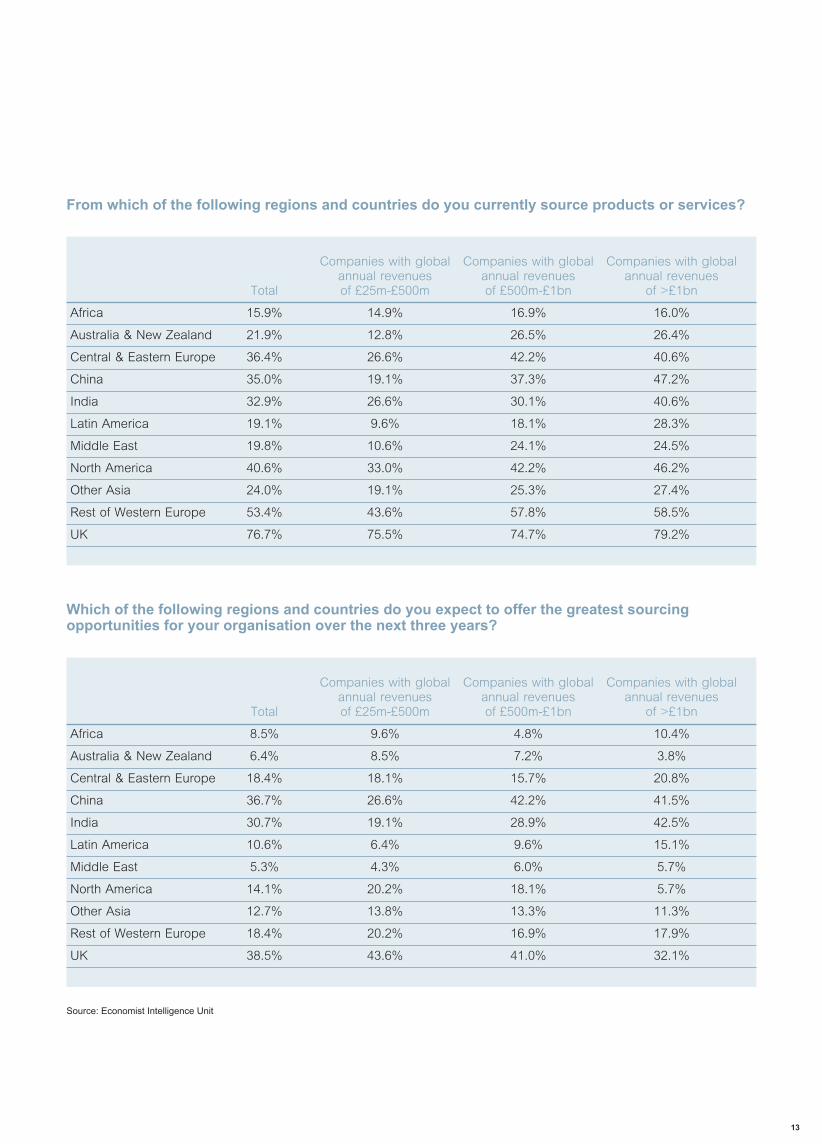

From which of the following regions and countries do you currently source products or services?

Source: Economist Intelligence Unit

Which of the following regions and countries do you expect to offer the greatest sourcing opportunities for your organisation over the next three years?

Companies with global Companies with global Companies with global annual revenues annual revenues annual revenues Total of £25m-£500m of £500m-£1bn of >£1bn

Africa 15.9% 14.9% 16.9% 16.0%

Australia & New Zealand 21.9% 12.8% 26.5% 26.4%

Central & Eastern Europe 36.4% 26.6% 42.2% 40.6%

China 35.0% 19.1% 37.3% 47.2%

India 32.9% 26.6% 30.1% 40.6%

Latin America 19.1% 9.6% 18.1% 28.3%

Middle East 19.8% 10.6% 24.1% 24.5%

North America 40.6% 33.0% 42.2% 46.2%

Other Asia 24.0% 19.1% 25.3% 27.4%

Rest of Western Europe 53.4% 43.6% 57.8% 58.5%

UK 76.7% 75.5% 74.7% 79.2%

Companies with global Companies with global Companies with global annual revenues annual revenues annual revenues Total of £25m-£500m of £500m-£1bn of >£1bn

Africa 8.5% 9.6% 4.8% 10.4%

Australia & New Zealand 6.4% 8.5% 7.2% 3.8%

Central & Eastern Europe 18.4% 18.1% 15.7% 20.8%

China 36.7% 26.6% 42.2% 41.5%

India 30.7% 19.1% 28.9% 42.5%

Latin America 10.6% 6.4% 9.6% 15.1%

Middle East 5.3% 4.3% 6.0% 5.7%

North America 14.1% 20.2% 18.1% 5.7%

Other Asia 12.7% 13.8% 13.3% 11.3%

Rest of Western Europe 18.4% 20.2% 16.9% 17.9%

UK 38.5% 43.6% 41.0% 32.1%

921922.indd 13 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

14

If nothing else, the data shows just how volatile supply chains have, or are expected to, become. Labour costs, exchange rates and local productivity all play their part, but meanwhile commodity prices have fluctuated in the past two years and show no sign of stabilising. Oil, as always, is the key commodity, and its price has swung from a high of $147 in July 2008 down to $31 in early 2009 and now stands at around $85. With renewed economic growth, common sense says the price can only go up, affecting a vast array of material and transport costs.

At Contico, for example, a £10m supplier and manufacturer of cleaning equipment and materials, operations director Phil Macey complains that in three months last year, the cost of resin for plastic mouldings increased by 78%. Meanwhile, the range of exotic metals and rare earths now required in modern technologies and markets adds a further dimension to the expertise demanded of the supply chain manager, who must pay particular attention to their market costs and guarantees of availability.

As the supply chain extends across the globe in search of cheaper or better supplies, volatility and the range of demands placed on it have risen, as have the volume and severity of the underlying risks involved. The company’s future depends on the risks being at least managed if not avoided. But 28% of respondents admitted to under-estimating the risks inherent in the supply chain, and the figure grew to 34% amongst the largest companies (with more than £1bn in annual revenue). Not far behind, the lack of a risk culture was cited by 18%. The range of events afflicting companies in the past year extended from straightforward insolvency through falling quality (16%) to sabotage (3%). By far the most frequent was severe weather at 40%. However, a fifth of companies (21%) were lucky enough not to have faced any such events.

The consequential damage to a company’s business by events of these kind is well-illustrated by the case of Land Rover’s sole supplier of Discovery chassis, which went bankrupt in 2002. The supplier’s receivers, accounting firm KPMG, demanded £60m just to maintain supplies. To find a new supplier would require a fresh investment of at least £12m and a six-month wait, and meanwhile, all production on the Discovery line would have to cease. The case went to court and Land Rover (then owned by Ford) settled for £15m.

Where the dangers lurk

921922.indd 14 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

15

Which of the following events affecting the supply chain has your organisation experienced over the past year?

Source: Economist Intelligence Unit

Severe weather event

Insolvency

IT failure

Increased tariffs

Falling quality standards after honeymoon period

Labour dispute

Transport shut-down

Theft

Product tampering

Sabotage

Other reasons

None of the above

0 10 20 30 40 50 60 70 80 90 100%

29%

22%

19%

16%

16%

13%

12%

5%

3%

1%

40%

20%

921922.indd 15 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

16

Land Rover was lucky. It was alleged at the time that the supplier had been making a loss on every chassis made at the price that Land Rover had negotiated. No doubt Land Rover had initially been satisfied with the deal, oblivious to the risk it was running with the source of a critical component. Putting a supplier in that position, as any supply chain director will advise, is seldom the best policy. But having taken on the risk of relying on a single supplier, the company compounded its problems by not keeping a close check on the supplier’s financial health and stepping in before the receivers were called. It evidently failed to foresee the further risk posed by KPMG’s attempt to exploit the strength of its position.

In another case, Mr Squiggles, the toy electronic hamster made by Cepia, a large toy company in the US, caught the world market’s imagination in the run up to Christmas 2009 and 600,000 were expected to be sold in the UK alone. Then tests in a California laboratory surfaced, appearing to show too-high levels of the toxic chemical antimony in the hamster’s fur. Sales were halted and frantic phone calls around the world were made.

Cepia had all the right safety certificates in place and quickly proved the results were a mistake, but not quickly enough to prevent a dip in sales. With modern telecommunications, rumours can cause real damage anywhere in the world in an instant and, at that time of year, it could have been a disaster for Cepia.

The inference from these two examples is that a supply chain disaster, actual or potential, can come from any quarter, so when 52% of respondents judged their companies’ audit of supplier risk to be effective and 53% thought their assessment and identification of risks were effective, the verdicts have to be treated with some scepticism.

The great majority of the sample say they have stepped up their due diligence research on potential suppliers (60%) and on-going monitoring of existing ones (58%). Possibly as a result, those who fear insolvency among their suppliers (29%) are outnumbered by those who say they do not (34%) – but 35% would not commit themselves.

Solvency, quality, financial resources and the customer base can indeed be checked, while commodity prices, exchange rates and protectionism can in some degree be forecast and the effects mitigated, but there will always be risks which are more difficult to manage.

921922.indd 16 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

17

Do you agree or disagree with the following statements?

Source: Economist Intelligence Unit

I am fearful that partners in my company’ssupply chain may become insolvent

in the next year

My company has stepped up the levelof due diligence performed on potential

supply chain partners as a resultof the recession

My company has increased the level ofongoing monitoring of my company’s supply

chain partners as a result of the recession

My company has introduced systemsto more closely connect and align interests

with supply partners

6% 34% 28% 7%23% 2%

2%

Strongly agree Agree Neutral Disagree Strongly disagree

9% 26% 10%50% 2%

6% 26% 12% 2%51% 2%

7% 38% 10% 1%42% 2%

Don’t know

0 10 20 30 40 50 60 70 80 90 100%

Figures have been rounded to the nearest %.

921922.indd 17 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

18

Earthquakes, tsunamis, forest fires and floods are another matter, and are likely to need more careful assessment in the future as globalisation and the possible effects of climate change increase. Local politics, too, must be taken into account by the supply chain management, as Nestlé’s recent experience in Zimbabwe shows.

Nestlé’s local management had come under pressure in October 2009 to break its existing supply contracts with local farmers, and purchase its milk instead from farms that had been requisitioned and were now controlled by President Mugabe and his Zanu-PF party. Human rights groups in neighbouring South Africa heard about it and appealed for a boycott of all Nestlé products there if it gave in. Then in December Nestlé found itself threatened with nationalisation and physical violence if it would not accept milk from Mugabe’s farms. It immediately halted all production at its Harare factory, and only restarted once it had received (from the Minister of Industry and Commerce) a written guarantee of the security of its management and staff and non-interference in its operating processes.

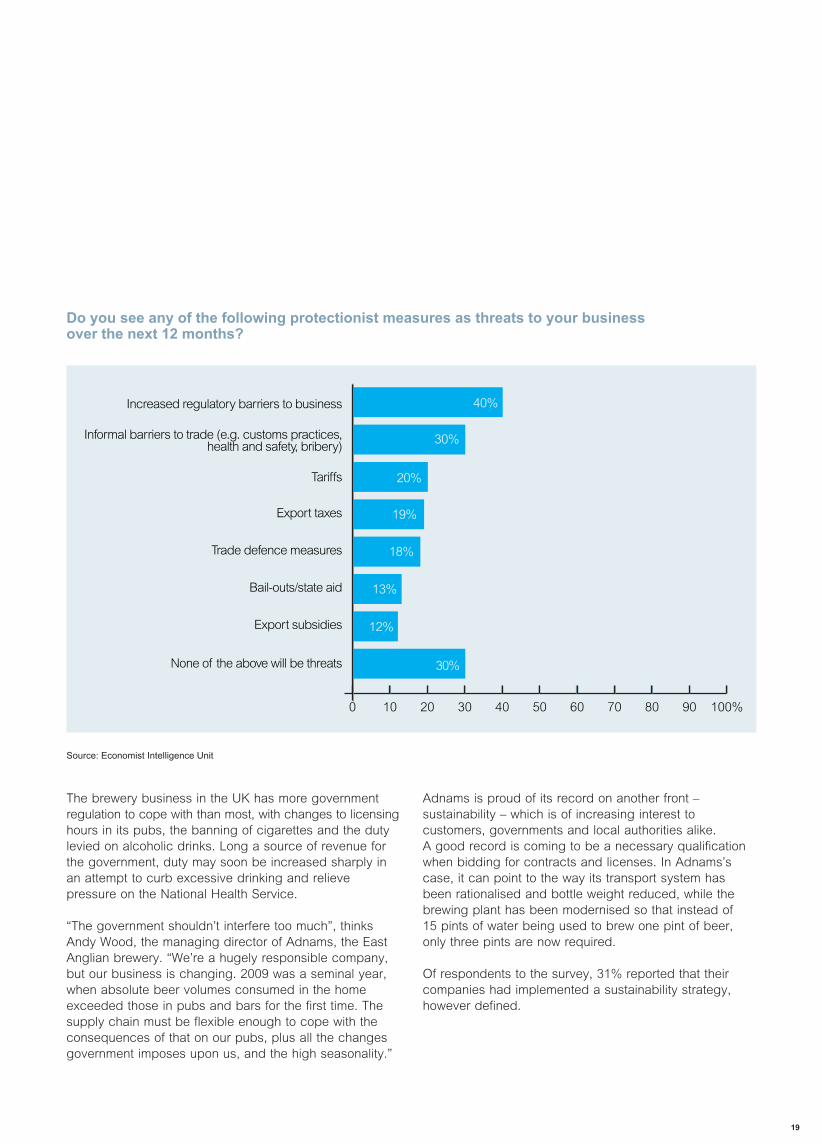

No doubt the Nestlé management will be keeping a very close eye on progress in Zimbabwe. But even in the best-governed countries, the way regulations affect a particular business may not be apparent until it is too late to have them changed. 39% of survey respondents expected regulations, benign or otherwise, to increase over the next year, while 29% foresaw informal barriers increasing, including problems with customs, health and safety regulations and bribery. On the other hand, a further 29% had no fear of government regulations.

Even well-intentioned government activity in the UK has sorely tested companies’ supply chains. The climate change levy, for example, has borne particularly heavily on the UK’s aluminium extrusion industry, according to Tim Eagles, joint managing director of Stannah (see case study), the dominant manufacturer of domestic stairlifts. He says “We have every concern for the environment, but the levy is applied only in the UK, so we’ve had to buy our extrusions from suppliers in southern Europe.”

Acts of god and governments

921922.indd 18 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

19

Source: Economist Intelligence Unit

Do you see any of the following protectionist measures as threats to your business over the next 12 months?

The brewery business in the UK has more government regulation to cope with than most, with changes to licensing hours in its pubs, the banning of cigarettes and the duty levied on alcoholic drinks. Long a source of revenue for the government, duty may soon be increased sharply in an attempt to curb excessive drinking and relieve pressure on the National Health Service.

“The government shouldn’t interfere too much”, thinks Andy Wood, the managing director of Adnams, the East Anglian brewery. “We’re a hugely responsible company, but our business is changing. 2009 was a seminal year, when absolute beer volumes consumed in the home exceeded those in pubs and bars for the first time. The supply chain must be flexible enough to cope with the consequences of that on our pubs, plus all the changes government imposes upon us, and the high seasonality.”

Adnams is proud of its record on another front – sustainability – which is of increasing interest to customers, governments and local authorities alike. A good record is coming to be a necessary qualification when bidding for contracts and licenses. In Adnams’s case, it can point to the way its transport system has been rationalised and bottle weight reduced, while the brewing plant has been modernised so that instead of 15 pints of water being used to brew one pint of beer, only three pints are now required.

Of respondents to the survey, 31% reported that their companies had implemented a sustainability strategy, however defined.

Increased regulatory barriers to business

Informal barriers to trade (e.g. customs practices, health and safety, bribery)

Tariffs

Export taxes

Trade defence measures

Bail-outs/state aid

Export subsidies

None of the above will be threats

0 10 20 30 40 50 60 70 80 90 100%

30%

20%

19%

18%

13%

40%

30%

12%

921922.indd 19 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

20

Managing the chain

Ideally, he or she has to have a strategic view of the company’s future and the ability to create the necessary supply chain capacity to match, yet be a diplomat rather than a driver, able to see which are the weak links and where to find solutions. The supply chain manager’s real role, says consultant and author John Gattorna, is in supplying customers with what they want – “it’s more of a philosophy than a function”. In practice, he says, supply chains are often still seen as cost centres, little more than purchasing and logistics departments.

Respondents to the survey reported in 43% of cases that the supply chain head reported to the CEO or other director, while in a further 44% there was no single head but the structure was ‘fairly centralised’. In the remainder it was decentralised. It may be significant that in the ‘C-level’ view, 51% of companies had supply chain heads reporting to the CEO or other director. The implication is that there is a certain amount of confusion in the reporting structure, which is likely to reduce performance. In the decentralised cases, circumstances or the nature of the business may obviate the need for a single coherent supply chain.

There is a gradual trend towards greater centralisation, however in supply chains as in so much else, everything depends on the nature and structure of the business and also the geographic spread. For practical reasons the supply chain may be split into two or more – as reported by 28% of respondents. But there is wide variation, even within a single business, according to the nature of the product: fashionable items, or ones given heavy promotional support require one structure; short-life products with many optional features (such as mobile phones) demand another; slow-moving or price-sensitive lines demand a third. As globalisation on both the supply and the market side increases, the complexity of the supply chain or chains also increases, and, in the opinion of some, places a limit on its optimum size.

A supply chain is only as strong as its weakest link, and in a company of any size, there are many links, extending from the supplier, to the procurement team, to the design and production teams, to finance, IT, marketing, sales, customers and after‑sales service. In fact, it is more of a network than a chain, with each function responsible for a few links, and a single chief supply chain officer a rarity.

921922.indd 20 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

21

Source: Economist Intelligence Unit

How would you describe the way in which your company’s supply chain is managed?

With complexity comes obfuscation. Like other consultants, Gattorna reports finding companies struggling under masses of data, but making only slow progress in creating an accurate and timely picture of the whole supply chain so that it can be managed effectively. Measures of success, apart from reducing costs, are difficult to find, so Gattorna favours using the cash-flow return on investment, which everyone can understand, as the principal metric to guide management.

With some 2,000 products and 120 suppliers, Macey at Contico says that it is the quality of his staff that makes sure the supply chain works. “We’re not just selling in the UK – we sell in Japan and the Middle East, and have just set up Contico Europe in Amsterdam. Here in Cornwall we’re incredibly lucky with staff. They have tremendous knowledge of our products and exactly what the targets are.

“We spend a lot of time with stats, covering the whole chain from supplier to customer, and half of what we sell we manufacture ourselves. We measure everything to the nth degree – our shipping performance, our credit notes and quality in every aspect. The aim is not just to prove how we’re doing, but to help in tendering, and ensuring that salesmen know what to quote.”

Supply chain executives in larger companies are usually organised into their functional specialities but, as the survey shows, communication then suffers: 31% of respondents believed that poor communications across the chain was one of the main obstacles to improving performance. Also cited were poor liaison with customers (6%) and inadequate cooperation between sales and production (13%). Some 25% of companies had invested in supply chain technology, or automated control or information systems (17%). Adnams for one is abandoning its old economic resource planning (ERP) system and moving towards a more user-friendly web-based system. However, supply chain managers say that although ERP and other systems can help, solutions are to be found in human more than electronic interaction.

In certain cases, Gattorna favours creating small multi-disciplinary teams to focus on a group of customers rather than a specific function. That way, he claims, communication is much improved, and changes, for example in product specification, can be accomplished in a matter of days rather than weeks. “Adidas, the German sports equipment supplier, did this at the time of the last football World Cup, because it knew that if Italy beat France, say, sales of Italian shirts would go up 300% overnight.”

Companies with global Companies with global Companies with global annual revenues annual revenues annual revenues Total of £25m-£500m of £500m-£1bn of >£1bn

Single supply chain head reporting to the CEO or director 42.7% 44.1% 41.0% 42.7%

No single supply chain head but fairly centralised 43.7% 39.8% 49.4% 42.7%

Decentralised 13.6% 16.1% 9.6% 14.6%

921922.indd 21 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

22

Improving collaboration with suppliers is a widespread ambition for all the obvious reasons – to cope with the growing volatility of the market, to ensure quality and reliability standards are maintained and to improve productivity so that costs can be reduced with minimum pain. But suppliers are frequently referred to as partners because the fortunes of both parties are in practice intertwined. The relationship may actually involve some considerable capital investment on the part of the supplier. Risk-sharing is rare however, at least on the scale that, for example, Boeing has chosen for firms assembling some 70% of its new 787 Dreamliner, which has already become a case study in the problems of managing a global supply chain.

As the bought-in content of many products has grown, suppliers’ contributions in terms of marketing as well as technical innovation are all the greater. Ideally, products will be designed jointly – but the company needs to have confidence in the relationship where precious patents, drawings and tooling are at stake, as demonstrated by the Land Rover case, where these vital assets came to be controlled by the receivers. With a sound relationship, too, the supplier is likely to be sympathetic to a request from the company to defer payment; and if the shoe is on the other foot, the company will have more confidence in supporting the supplier.

In fact, half of companies questioned found that cooperation was better since the recession, while 56% said they were improving it further, to increase the resilience of their supply chains. Some 48% claimed to have introduced systems to more closely connect and align interests with supply partners. Improvements have been made to forecasts (31%) and continuity planning (33%), perhaps giving suppliers more confidence in their customer. However, a further question revealed that while 43% of respondents had confidence in their companies’ demand forecasts, 19% did not. There is clearly still some way to go.

Progress is also needed, according to larger firms, in the hiring and training of supply chain staff. Ted Kondis, consulting vice president of the supply chain specialist Ariba, says that the pressure on costs over the past two years has left companies short of skilled supply chain staff to cope with renewed growth. So the question in the minds of top executives should be “Do I have the right talent?”

The problem applies especially in firms that still see the supply chain as a fancy name for purchasing and logistics, and as some consultants observe, their staff often have an engineering background with a tendency to rely too heavily on their spreadsheets and delivery schedules, and not enough on relationships with the people concerned.

At PZ Cussons (see case study) the complexities of its manufacturing and marketing operations in 12 countries require ‘the right people’ with a rather broader view, and the need is recognised as one of its four strategic pillars, alongside its selection of markets, its brands and its ‘world-class supply chain’. Supply chain director John Pantelereis explains that the company believes in ‘growing its own timber’. It recruits 60 or 70 graduates every year, and develops the talent it needs to build human relationships with suppliers as well as to manage the purchasing of valuable raw materials and plan the distribution of the products. “For the supply chain, you need to hire the best people and give them as much responsibility as possible,” he says, implying that his company has got them – and does.

921922.indd 22 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

23

Case studiesStannah’s steady climb

With the UK’s housing stock having a preponderance of old houses built on two levels connected by a winding staircase, it is perhaps not surprising that the world leader in the stairlift market is a British firm that claims to have made 400,000 lifts since 1975. A family-owned company dating from the 1860s, its volumes have grown every year for the past decade, so that current turnover now tops £105m.

The skill consists as much in fitting the stairlifts into a confined space as in the mechanics, and also in controlling the second-hand market since its customers tend to have shorter lives than the lifts. Tim Eagles, joint managing director, is directly responsible for the supply chain and although his principal aim is to find better, cheaper supplies, competition in the market is growing and the efficiency of the whole supply chain is an important weapon.

Customers naturally want exactly the right product installed on the agreed installation day, and for that, all components have to be in place and to work as designed. But market dynamics may depend on suppliers themselves innovating to produce new components and facilities as required.

“In the past, practically everything was made in-house,” Eagles says, “but nowadays, perhaps 80% is sourced outside. Plastic mouldings and castings need higher volumes than we need ourselves to keep the price down. In our product, the carriage and chair is standard, but the rail it runs on is bespoke, so that has to be manufactured here and fitted by our staff.

“We have a reasonable level of spend in South-East Asia, but I don’t deal direct, and I turn over my stock up to 30 times a year. There’s always the risk of quality deteriorating, and other things being equal, I’d buy locally because of better responsiveness. But I have a very good relationship with our overseas suppliers. I also have very close cooperation with our sales force. We project sales forward for 18 months and have an umbrella agreement against which I can call off as needed.

“Are we getting the best performance? I don’t think you can tell. The supply chain delivers what’s needed, and we’re constantly making improvements. Ten years ago, our stockturn was around four a year. Now the average is 20. We’re very cautious with cash. If something goes wrong, I know I can count on my suppliers to cancel the Christmas party to put it right.”

“In the past, practically everything was made in‑house”

921922.indd 23 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

24

PZ Cussons’s four pillars of success

Not many companies take their supply chains quite as seriously as the £838m personal care group PZ Cussons. Founded 125 years ago, it was known until 2002 as Paterson Zochonis, and its best-known brand is Imperial Leather soap. With a new name, new brands and Imperial Leather relaunched, it has grown steadily in Europe, Africa and Asia, working to a four-point strategy: selected markets, leading brands, a world-class supply chain and the right people.

Its last annual report enlarged on the third point “We operate world-class supply chain networks that enable us to deliver our brands quickly and efficiently to our local customers... We take pride in our flexible distribution capability which is tailored specifically for the local market.”

The report refers, of course, to the selling end of the chain rather than the buying end, but that does not mean the latter is neglected. John Pantelireis, the corporate supply chain director, explains “We start our supply chain planning process with sales forecasts and any major marketing promotions that are planned, and work back through distribution to stock levels and purchasing needs.”

The company makes most of what it sells in a number of factories in Nigeria, Ghana and Kenya. But it also has factories in Asia and Europe, making for a very complex supply structure. Some materials are bought centrally, mainly the key commodities like phosphate, sulphates and tallow, and others locally, but under the eye of the management network. Charles Worthington, the hair care brand bought in 2004, maintains its own supply chain. The emphasis is on local flexibility, but carefully controlled by central management. “There’s always a target set for each country and product category,” says Pantelireis.

“There’s huge volatility in our markets now, and timing is vital. You need good people, and we don’t like to speculate or gamble. We only buy forward if we feel the need, because it absorbs working capital and we sometimes get it wrong. But as well as price fluctuations, we have to be ready for a huge new demand – for example the hand sanitisation programme to counter swine flu, which doubled and tripled the sales of handwash brands.

“We’re not yet at the forefront of the climate change controversy, but sustainability is a growing concern. We take an active interest in helping to develop Nigeria’s economy, where we’ve operated for 100 years. I’ve seen many small companies get into difficulties there, so we help where we can, and we’ve got two joint ventures, with Haier, the Chinese white goods company, and Glanbia, an Irish company making milk products. We’ve also opened four retail outlets for electrical goods to help stimulate the local economy.”

“We take pride in our flexible distribution capability, which is tailored specifically for the local market.”

921922.indd 24 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

25

Conclusions

Against a gloomy economic background, the optimism this survey reveals in the ability of respondents to increase revenues and profit margins at their companies over the next year belies conventional wisdom. What is certain is that their supply chains are gradually playing a more prominent part in the fortunes of companies as globalisation gathers pace.

The implication of the overall trend is that management of supply chains is going to become an ever-more critical determinant of companies’ competitiveness. Companies with the best suppliers benefit not just from price, but from quality, reliability, innovation and so forth – all to their customers’ satisfaction. But to maximise the advantages, a higher standard of management is called for, able to cooperate closely with suppliers’ management anywhere in the world. That ambition is declared by the majority of the sample, yet nearly half have reduced their supply chain head count in the past 12 months.

Able managers are not the only requirement. A structure is required to provide an overall supply picture with appropriate information to help management decision-making. Yet most responding companies have no single supply chain head or are decentralised. At a time when the volatility of world markets is increasing, and with it the risks inherent in an extended supply chain, this report indicates that while progress in managing those risks is being made, much work still lies ahead.

‘Able managers are not the only requirement.’

921922.indd 25 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010

The Royal Bank of Scotland plcRegistered Office: 36 St Andrew Square, Edinburgh EH2 2YB.Registered in Scotland No. 90312

RBS02288 21 April 2010

To find out more on how we can help fufil your international ambitions, speak to your Relationship Director or visit www.rbs.co.uk/international

921922.indd 26 10/05/2010 09:56

Generated at: Mon May 10 09:56:56 2010