how to deal with stress-testing today

TRANSCRIPT

Regulatory Stress-testing | EBA, CCAR … Implementing an optimized Stress testing process

May 2014

2

Overview Why a dedicated offer now ?

THE RIGHT TIME

THE RIGHT EXPERTISE

THE RIGHT ANSWER

The difficulties encountered during the AQR exercise led to a new way of thinking the stress tests. Time is come to rethink it

All the results from AQR have been challenged. Each bank’s maturity would be judged on the capacity to face these new challenges (Data challenger models, PIT Parameters …)

Banks shouldn’t focus only on stress test results. Internal processes are also under judgment to ensure high quality and the timely delivery of the assessment (quality assurance process)

Key learnings of recent AQR & CCAR exercises suggest that some significant moves are required to fulfill market & regulators expectations That is why, based on our recent dialogues with the Financial industry, we have come to the conclusion that new objectives came to light:

Stress-testing | Overview – timeline of recent exercises

Focus | 2014 EBA stress test

Stakes | Key challenges and success factors

Contacts

Appendix

Agenda

1

2

3

4

3

5

4

Stress-testing| Overview – timeline of recent exercises Some background 1.

Stress testing is a key component of financial institutions risk management framework, helping them determine capital levels , but also spot emerging risks and take preventive actions

The 2008-2009 financial crisis highlighted some shortcomings in practices (i.e. less severe scenarios based on historical data, limited involvement of the top management, etc.) that prompted the Basel Committee to issue in May 2009 recommendations on how to conduct stress-tests*

For Institutions, in the short-term the main challenges are threefold:

- Methodology: quickly adopt and implement new approaches / scenarios proposed by supervisors - Project implementation: identify work blocks, wisely plan and provide with adequate resources - Time (submission): submit in time, under tight deadlines and with the appropriate quality of outputs

Incr

eas

ing

inte

nsi

ty,

sco

pe

an

d f

req

ue

ncy

* “Principles for sound stress testing practices and supervision”, Basel Committee on Banking Supervision, May 2009

Between 2008 and 2013, many stress-tests have been held to cope with the sovereign crisis or before a bail out of financial sectors in troubled countries: Greece, Slovenia, Spain, Portugal, Cyprus, Ireland. Stress-testing has become a regular regulatory process and used as a tool to test resilience of financial sectors

In 2014, the CCAR in US demonstrated that new generation of stress-tests are much more intensive and broader. The EBA stress-test will follow suit before the enforcement of the SSM (ECB new central supervisor). For banks, it’s no longer enough to meet current regulatory requirements (e.g. for ICAAP purposes)

2010/2011 EBA Macro Stress Tests

Today

5

Stress-testing| Overview – timeline of recent exercises Mounting regulatory pressure on financial institutions around the world 1.

BIS principles for sound stress testing practices and supervision

US Supervisory Capital Assessment Program (SCAP)

UK liquidity and reverse stress-testing

2009

Collapse of Lehman-Brothers: financial crisis hits US

The crisis spreads to Europe

2008

2nd EBA stress tests

US CCAR + CPAR (≥$10bn)

2011 US CCAR + DFAST

Company stress-tests (≥$50bn and $10bn- $50bn)

UK FDSF

2013

US CCAR + DFAST Company stress-tests

(≥$50bn)

2012

Enforcement of Basel III framework

2015

AQR + EBA stress-tests

BoE stress tests

HKMA liquidity stress-tests

CHINA ST

US CCAR + DFAST Company stress-tests

2014

1st EBA stress tests

2010

Stress-testing progressively has become a cornerstone amid increasing regulatory expectations

• Core templates: Minimum Data required by the EBA - Advance Data Collection (ADC): collected prior to commencing the stress test - Calculation Support and Validation data (CSV): supplied to CAs as input to their quality assurance process; Also used to automatically populate transparency templates - Transparency (TR): Data on stress test outcomes to be disclosed on a bank‐by‐bank basis.

• Additional templates: not required by the EBA but can be required by NCAs - Advance Data Collection (ADC)

6

Key aspects

• The process is not a substitute to existing obligations regarding stress-testing (i.e. ICAAP pillar 2) • Risk coverage : Credit risk, Market risk, Sovereign risk, Securitization, Cost of funding, operational risk (standard approach);

CAs may include additional risks • Assumptions : a static balance sheet , prescribed approaches to market risk and securitization, and a series of caps and floors on net interest

income, risk weighted assets (RWAs) and net trading income • Horizon : over the period 2014-2016 with 31/12/2013 as a starting point • Regulatory (capital) hurdles :

- 8% Common Equity Tier 1 ratio for the baseline scenario - 5.5% Common Equity Tier 1 ratio for the adverse scenario

• Banks will have a maximum of 4 months to complete the process (results due in October 2014)

Scenarios

Disclosures

• Baseline scenario : - Based on the winter 2014 forecast (EU) extended through a

model-based approach to cover the year 2006 (2016 is outside the 2-year horizon of the winter forecast)

• The results will be disclosed on a bank by bank basis consistent at least with 2011 EU-wide stress test. Components: the capital position of banks, risk exposures and sovereign holdings

• Banks are expected to cover potential capital shortfalls within 6 to 9 months after the release of the results

Focus| 2014 EBA stress – test (1/2) The most complex and comprehensive test to date 2.

Data

Risk modeling

Credit risk • Perimeter: banking book excluding counterparty credit risk. • Calculation of Point-in-time PD and LGD • ECB EL benchmarks available for banks

with no point-in-time models • Application of macro-economic scenario to

PIT and regulatory parameters • Regulatory risk parameters to be used for

stressed RWA calculation

Market risk • Simplified approach (Var-banks & Non-Var

banks) : projection of NTI based on bank’s historical loss (2009-2013)

• Comprehensive approach (Var-banks) : translation of macro-economic scenarios to project gains & losses on FV positions using internal models

• CVA and IRC also stressed • RWA: SVar used in adverse scenario

Securitization risk • FV positions : market risk methodology • Impairment estimates for positions not

held for trading • RWA based on risk profile (3 risk buckets)

Sovereign risk • FV positions : market risk methodology • Banking book: credit risk methodology for impairment estimates based on rating migration

• Stress-scenario : - Macro-eco: global debt markets sell-off, a rise in funding

costs, a new recession, and deep dives in property and equity prices.

- Market shocks: set of common stressed market parameters

Key elements • New Segmentation for Clients & Exposures in

the Banking book • Trading Book notional amounts to be re-valued

using IFRS 13 hierarchy • Higher granularity for asset classifications and

the Real Estate portfolio • ‘Simplified version’ of 2013 EBA Forbearance &

Performing/NPLs definitions to be used

7

Project Implementation/Governance/

Resources

Scenarios

Results/ Documentation

Focus| 2014 EBA stress – test (2/2) Preliminary questions that the banks start to ask 2.

Data

Risk modeling

• What processes? How to ensure involvement of the top management in the end-to-end process?

• What is the optimal mix of competences?

• What coverage of risks? Which portfolios? Which entities?

• What scenarios to be used? At which level of severity? What is the planning horizon?

• What models? What parameters to be stressed? How to translate macro-scenarios into risk factors? What level of sophistication? How to value capital impact?

• How to leverage on existing documentation? What are the new requirements?

• How to align the task of documentation with actual performance of the test? How to dot it on time ?

• What data are necessary inputs for scenarios and stress-tests? How to respond to additional data requests from regulators?

• What level of industrialization achieved by implementing (or not) a stress library?

8

3. Stakes | Key challenges and success factors (1/2) Key issues

Successful completion of a stress-

testing process

Data, systems & disclosures

Project implementation

Resources and capabilities

Methodology

Governance & communication

The limited period allowed for the exercises, require a very efficient project management to meet regulatory tight deadlines

Tasks need to be clearly defined, streamlined and rigorously monitored

Supervisors assess results as well as the way they are produced

Completeness, consistency (e.g. finance vs. risk data) and (more importantly) quality

Massive data from different sources

Compliance with stress test requirements (e.g. AQR results used as inputs)

Consistency with external definitions (e.g. EBA definitions of forbearance and NPLs) and accounting principles in force

Heavy documentation, flexibility to answer additional data requests from supervisors

Stress-testing is a very burdensome process.. Recent CCAR exercises suggest that banks will need more people dedicated to the process

The increased complexity and scope require a mix of quantitative, financial, IT and/or economic skills

Excellent capacity for the analysis of regulatory guidelines and identify which texts apply to the bank

Flexibility in incorporating new approaches in ST framework is key

Optimize internal modeling since supervisors increasingly rely on internal models and assess their quality

Translate macro-scenarios into risk factors Leverage on benchmark Detailed documentation of modeling

approaches used by the bank

More integrated approach across all areas and business lines of the bank (front office, finance, risk, etc.)

Board and senior management need to be involved in the development and operation of the stress-testing : close oversight and communication throughout the process

Failure to pass the tests, and the way to process the stress exercise, can lead to an unexpected impact on the firm’s reputation vis–à-vis the market or investors

9

3. Stakes | Key challenges and success factors (2/2) Why CH&Cie?

CH&Cie CREDENTIALS

We accompanied several tier 1 Investment banks in the development of their ICAAP / Stress-testing and risk appetite frameworks

Our experts performed several projects in response to the EBA stress test (design, implementation, impact calculation…) for leading actors of the industry

We are proud to leverage on our internal “Global research Analytics” quantitative department, and have realized extensive works on stress testing methodologies (Sensitivity test, Scenario analysis – historical & hypothetical - , Maximum Loss, Extreme Value Theory…)

Based on our extensive experience in the industry, we understand several banks individual set-ups, know the teams and specific constraints /obligations and modeling approaches

We can also provide with benchmark for our clients to access best practices (see appendix 5B & 5C)

Beyond the 2014 exercise requirements, our work will be designed in order to support periodic needs

A STATE of THE ART EXPERTISE

USED TO WORK UNDER HIGH PRESSURE

RESPECT of DEADLINES & FLEXIBILITY

A RESULTS-DRIVEN TEAM

HIGH QUALITY DELIVERY & COMPLIANCE WITH REGULATORY REQUIREMENTS

Key learnings of the AQR demonstrate the needs of a new approach combining strong and tailored skills

London

Paris

Hong Kong

10

4. Contacts

Our experts will remain at your disposal to discuss further the aforementioned topics

We will be very pleased to share with you the latest developments in implementing stress testing as well as best practices

Stéphane EYRAUD, CEO E-mail: [email protected] Phone number : + 44 78 34 55 03 98 + 33 (0)6 12 41 64 06

Benoit GENEST, Partner and Head of GRA E-mail: [email protected] Phone number : +33 (0)7 87 68 81 77

Ziad FARES, Manager E-mail: [email protected]

Phone number +33 (0)6 62 96 25 00

Matthieu SACHOT, Director E-mail: [email protected]

Phone number +852 9433 0753

Appendix A – Stress parameters – Methodologies

Appendix B – Benchmark on supervisory requirements

Appendix C – Benchmark on central bank models

Appendix D – Regulatory Stress testing - What is required from banks?

11

5. Appendix

Stress parameters - Methodologies Illustrative examples on PD

Different kinds of models can be used to translate a shift in PD or LGD parameters from macro economics data In terms of benchmarking, 5 types of methods are usually implemented (or derivative models)

Method Description Illustration

1

2

3

4

5

Diffusion Models

Regression models

Interpolation models

EVT (Extreme Value Theory)

Bayesian networks

• The model is based on a differential equation of the variable to be explained following the explanatory variables in order to translate the dynamics of evolution of this variable

• ARCH , GARCH models are part of this family

2

2

( )( ( ), ( ), ( ))

PDf X t Y t Z t

t

PD differential equation

Explanatory variable

functions (GDP …)

• The objective is to determine a causal relation between the PD

and explanatory variables

• In other terms, the goal is to put into equation the PD based on a combination of selected explanatory variables, which will lead to the projection of the PD

( ) (0,893. ( ( 1))

0,062. ( 2)

0,02. ( ) 0,54)

PD t InvLogit Logit PD t

Inflation t

Chômage t

• It’s an iterative method for projecting the PD based on the maximum of likelihood

• It’s done through an intermediary stage of assessment of the expectation and then of the maximization of the expectation

• The method is based on extreme values of the variables

• Answers to the question: How will evolve the PD if a extreme though plausible phenomenon occurs?

Change in initial

trend– Extreme event / Outliers

• Probabilistic model based on Bayes theory and conditional probabilities

• Thus it is used to infer the relation between the PD and the evolution of risk parameters

GDP

Unemploy-ment

Interpolation

Oil

PD

12

5A

Bank of Greece

Regulator

13

Theme Benchmark

Definition of default

In models based on loan performance, the key dependent variables are the NPL ratio, the LLP ratio and the historical default frequencies

Model used

Vector autoregressive model using a Logit transformation

Sample used

[2000Q1 - 2007Q4] : First, given our data length and the asymptotic properties of the VAR analysis, a re-estimation of the model is necessary once a new/revised data set comes available

Finally, only one economic indicator is modeled, yet the shock may be directly generated through a range of indicators that influence the level of the NPLs and interact with economic growth

Acknowledging the problems of inference associated with a VAR on a short data series

We find a significant effect of the changes in the euro exchange rates and the Euribor interest rates on the non-performing loan ratio while the effect of GDP growth, albeit small, is found to be significant too

Explanatory variables

Sample used

Explanatory variables

its Financial System Report (Bank of Japan 2007), the BoJ estimates a VAR model comprising five macroeconomic variables (GDP, inflation rate, bank loans outstanding, effective exchange rate, and the overnight call rate)

Explanatory variables

The model analyzes the relationship between a logit transformation of Canadian sectoral default rates and two macroeconomic variables (GDP and interest rate). particular, in stressful periods, when the default rate reaches its historical peak; without nonlinearities, even the extreme shocks would have had a very limited impact on default rates.

Explanatory variables

Bank of Japan

Bank of Canada

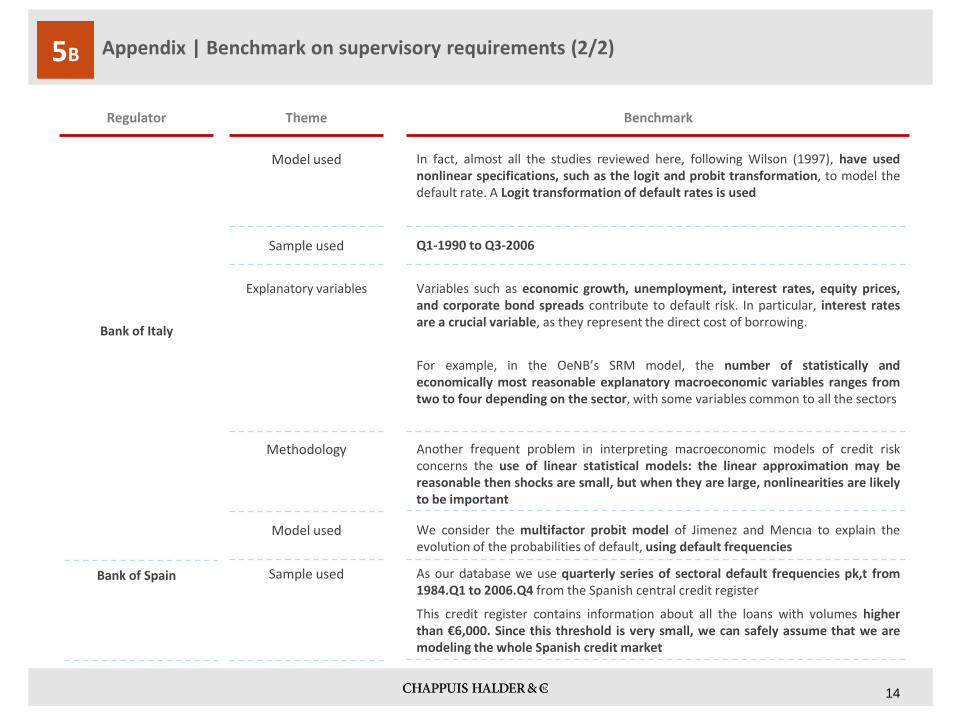

5B Appendix | Benchmark on supervisory requirements (1/2)

Bank of Italy

Regulator

14

Theme Benchmark

Model used

In fact, almost all the studies reviewed here, following Wilson (1997), have used nonlinear specifications, such as the logit and probit transformation, to model the default rate. A Logit transformation of default rates is used

Sample used

Q1-1990 to Q3-2006

Variables such as economic growth, unemployment, interest rates, equity prices, and corporate bond spreads contribute to default risk. In particular, interest rates are a crucial variable, as they represent the direct cost of borrowing.

Explanatory variables

We consider the multifactor probit model of Jimenez and Mencıa to explain the evolution of the probabilities of default, using default frequencies

Model used

Bank of Spain

For example, in the OeNB’s SRM model, the number of statistically and economically most reasonable explanatory macroeconomic variables ranges from two to four depending on the sector, with some variables common to all the sectors

Methodology

Another frequent problem in interpreting macroeconomic models of credit risk concerns the use of linear statistical models: the linear approximation may be reasonable then shocks are small, but when they are large, nonlinearities are likely to be important

As our database we use quarterly series of sectoral default frequencies pk,t from 1984.Q1 to 2006.Q4 from the Spanish central credit register

Sample used

This credit register contains information about all the loans with volumes higher than €6,000. Since this threshold is very small, we can safely assume that we are modeling the whole Spanish credit market

Appendix | Benchmark on supervisory requirements (2/2) 5B

Bank

15

Model

Bank of Canada

Explanatory variables Data

Logit transformation of default rates

- GDP Growth rate

- Unemployment rate

- Medium-term loans rate

Q1-1988 -> Q4-2005

Bank of England

Logit transformation of default rates

- GDP Growth rate

- Short term interest rate

- Equity return

No info

Bank of Italy

Logit transformation of default rates

- GDP Growth rate

- Interest rate

- Equity index

- Competitiveness index

Q1-1990 -> Q3-2006

Bank of Japan

Probit transformation of the probability of rating transition

- GDP Growth rate

- Interest rate

Q1-1985 -> Q4-2005

Bank of Spain

Probit transformation of the default rate

- Quarterely change in real GDP Growth

- Variation of 3-month real IR

- Term spread

Q4-1984 -> Q4-2006

Bank of Netherlands

Logit Transformation of default rates

- Real GDP growth

- Term spread

Q1-1990 -> Q4-2004

Appendix | Benchmark on central bank models (1/2) 5C

Bank

16

Model

Deutsche Bundesbank

Explanatory variables Data

Logit Transformation of Loan Loss Provisions

- Lagged dependent variable

- Credit Growth

- Real GDP Growth

- Variation short-term IR

Q1-1993 -> Q4-2006

ECB

EDF or euro-area corporates - Euro-area real GDP

- CPI inflation

- Real equity prices

- Real euro/US$ exchange rate

- Short term interest rate

Q1-1992 -> Q4-2005

Banque de France

Logit transformation of the probability of a rating transition

- GDP

- Short-term interest rate

- Long-term interest rate

No info

Oesterreichische National Bank

First difference of the Logit transforamtion of default rates

- Real GDP

- Unemployment rate

- Real short-term IR

- Real five-year IRrate

Q1-1969 -> Q4-2007

Swiss National Bank

Logit Transformation of Loan Loss Provisions

- GDP growth

- Unemployment rate

- Level of three month IR

Q1-1987 -> Q4-2004

Appendix | Benchmark on central bank models (2/2) 5C

17

ECB, EBA, NCA EC (economic scenario),

ESRB

Supervisor (s) / regulatory bodies

** China stress-tests details are set to be released in July 2014. At this point no relevant information on the process, methodology or scope are available

Eurozone

Regulatory Stress testing - What is required from banks? Stress tests approaches are aligned across regions

BoE / PRA / FPC

UK*

Federal Reserve

US

HKMA

HK**

EBA FINAL draft ITS (forbearance and NPLs exposures ), 20/02/2014

For IFRS banks: IAS 39, IAS 37, IFRS 13

Scope

Stress testing the UK banking system: guidance for participating firms, April 2014

CRD IV, IAS19

Dodd-Frank Act Stress-tests

TBD

At least 50% of each national banking sector,

At the highest level of consolidation

128 banks

Data requirements

8 major UK banks & building societies

At the highest level of UK consolidation

TBD

Historical/AQR Data – Core (ADC, TR, CSV) & Additional (CSV) Templates2,3

Risks covered (major)

FDSF (Firm Data Submission Framework) – Historical, Year-End Data & P/L Projections

FRY Reports – A/Q/M Data; P/L Projections

TBD

Credit and market risks, securitization, sovereign and funding risks

Scenarios

Credit and market risks,

securitization, operational risk and conduct costs, Pension risk, funding risks

“all potential sources of losses from all on/off balance sheet positions… potential to impact capital”

Liquidity risk (personal loan portfolios)

Regulatory Baseline Stress Scenario

Common EBA Baseline (except dynamic balance sheet)

Variant Stress scenario Bespoke Firm Stress

Baseline, Adverse, Severely Adverse;

Firms’ Scenarios

Personal loan consultation : 3% rise in interest rates

“different degrees of capital outflow”

Relevant regulations / accounting standards

CCAR : Large BHCs & FBO ( ≥ $50 bn in total consolidated assets)

DFAST : BHCs & FBO ( ≥ $10 bn)

Source : EBA, HKMA, Fed, BoE, Moody’s

* UK ST will complement those of the EBA with a more severe and UK-specific stress scenario (e.g. house prices down 35%, unemployment rising to 12% and interest rate to 4%) and four additional firms in the scope

5D

18

Bottom-Up & Top-Down; Firms’ Own Models

Modeling approach

Eurozone

Regulatory Stress testing - What is required from banks? (2) Stress tests approaches are aligned across regions

Bottom-Up /Granular; Firms’ Own Models

UK

Bottom-Up; Firms’ Own Models; Dynamic Projections

US

TBD

HK

Planning horizon 12 quarters (2014-2016)

Frequency

12 quarters (2014-2016) 9 quarters (30 sept.14-

Dec.15) TBD

Annual (2009-2011 EBA); 2014 (ECB)

Hurdles’ Requirements

Annual Annual (regulator-led) Semi-annual (bank-led)

Annual

8% CET1 for the baseline scenario

5.5% CET1 for the adverse scenario

Disclosure

7% CET1 for the baseline scenario (3% Tier 1 leverage ratio)

4.5% CET1 for the variant Stress scenario

CET1 ≥ 5% and above the required regulatory minimum levels in effect

TBD

Results in Oct. 14 (with

AQR results)

Results towards end of Q4

2014

Annual submission: 31/03

(disclosure in June) Semi-Annual submission:

31/03 and 05/07(March and September for disclosure)

TBD

Source : EBA, HKMA, Fed, BoE, Moody’s

5D