howden africa holdings limited annual report 2009

TRANSCRIPT

www.howden.com

Howden Africa Holdings Limited

Annual Report 2009

Ho

wd

en Africa H

old

ings Lim

ited A

nnual Rep

ort 2009

Mission statementHowden Africa is a market-driven, customer-

orientated company. The main business activities of

the Group are the design, manufacture and marketing

of specialised air and gas handling solutions to a wide

range of industries. The Group’s principal products

and services are split into two main areas.

Major industries supplied include power generation,

petrochemical, mining, construction, refrigeration,

water treatment and general industry. Howden Africa

has a commitment to environmental awareness.

In pursuit of this policy all product designs and

manufacturing are scrutinised for environmental

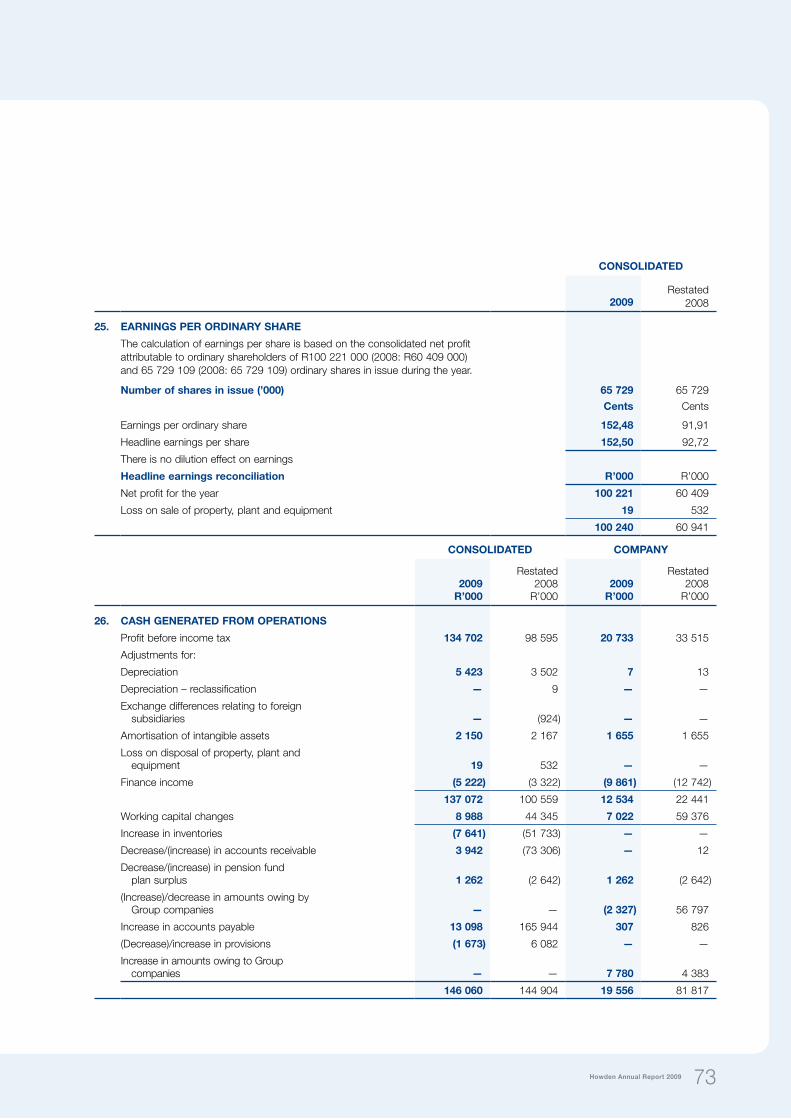

friendliness.

Design and drawing activities are computerised and

manufacturing is concentrated on the production

of key components. Manufacturing facilities are

located in Booysens (Johannesburg) and Struandale

(Port Elizabeth).

Contents

IFC Mission statement01 Other Group salient features02 Directorate04 Five-year Group financial summary05 Value added statement06 Group at a glance07 Group structure08 Chairman’s statement10 Review of operations18 Integrated sustainability report25 Corporate governance28 Directors’ responsibility28 Certificate by the Company Secretary29 Report of the Audit Committee30 Report of the independent auditors31 Financial reports87 Notice of the annual general meeting91 Form of proxy

Fans and Heat Exchangers pg 10

Environmental Control pg 14

BASTION GRAPHICS

01Howden Annual Report 2009

2009R’000

Restated2008

R’0002007*

R’000 2006*R’000

2005*R’000

Net asset value per share (cents) 258,90 111,39 133,96 39,81 264,75

Depreciation 5 423 3 511 3 312 2 540 2 625

Amortisation 2 150 2 167 1 881 1 834 1 720

Capital expenditure 14 963 18 879 11 311 5 120 5 878

Capital commitments

– Authorised and contracted 570 2 842 4 685 286 463

– Authorised not contracted — — — 4 787 —

Operating profit to revenue (%) 13,26 11,71 12,96 10,21 7,21

Number of employees 563 520 492 443 437

Closing share price (cents) 950 1 035 1 000 400 490

Total number of shares traded 7 734 551 4 767 207 5 582 799 9 146 620 11 209 071

Average price for the year (cents) 950 981 692 471 399

Total value of shares traded at average price (R) 73 478 235 46 759 690 38 632 969 43 080 580 44 724 193

Volume of shares traded to total weighted average number of shares (%) 11,77 7,25 8,49 13,92 17,05

*Impact of changes in accounting policies has not been taken into account.

Other Group salient featuresfor the years ended 31 December

0

20

40

60

80

100

120

140

160

180

Earnings per share(cents)

05 06 07 08 09

152,

48

91,9

1

93,8

5

25,1

738,8

8

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

Pro�t before tax(R’000)

05 06 07 08 09

134

702

98 5

95

87 1

96

55 9

23

42 9

11

0

200 000

400 000

600 000

800 000

1 000 000

Revenue(R’000)

05 06 07 08 09

976

332

813

625

686

387

510

942

497

495

Notes to the financials statements continuedfor the year ended 31 December 2010

02 Howden Annual Report 2009

Directorate

1. RJ Cleland (62)Non-executive director and Chairman (British)

Bob Cleland was appointed Chief Executive of Howden

Global in 1999. He was previously Group Operations

Director on the board of Triplex Lloyd plc and prior to

that was an Executive of British Steel Stainless, now

part of Outokumpu. He was appointed a non-executive

director of the Howden Africa Holdings Limited board

on 2 March 2000.

2. S Meyer (55)Group Financial Director

Shane Meyer joined the Group in 1977. In 1991, he was

promoted to Group Financial Director of Howden Group

South Africa Limited. He was appointed Financial Director

of Howden Africa Holdings Limited upon its incorporation.

3. M Malebye (38)Independent non-executive director

Morongwe Malebye provides consulting services in mining.

She is a qualified engineer. She has graduated with M.Sc

Industrial Engineering and B.Sc Mechanical Engineering

degrees, and in addition has completed an MBA. She has

worked at Eskom, Sasol, Spoornet, Armscor and Babcock

Africa. She serves on the board of African Oxygen Limited

(Afrox) and is a mentor for the Allan Gray Foundation.

4. AB Mashiatshidi (50)Independent non-executive director

Arthur Mashiatshidi is an independent businessman. His

primary activities consist of managing his portfolio of private

investments and he serves as a non-executive director and

chairman of the board of Kaya FM (Pty) Limited. Arthur

is a non-executive director of Total South Africa Limited;

a non-executive director of TCS (Tosaco Commercial

Services); financial director of a platinum exploration

company, Wesizwe Platinum Limited and also serves on

the Admissions Committee of the AltX of the JSE Limited.

5. T Bärwald (47)Chief Executive Officer (German)

Thomas Bärwald originally relocated from Germany to join

Howden Africa in 1990. He was promoted to Operations

Director of Howden Power, a division of James Howden

Holdings Limited in September 1997. In 1998 he relocated to

Australia and was appointed Executive Director of Howden

Australia in 1999 and Managing Director of Howden Australia

in 2002. He was appointed Managing Director of Howden Hua

(China) in 2007 to lead a change management assignment

for a period of 18 months ending December 2008. He was

appointed to the Howden Africa Holdings Limited board as

Chief Executive Officer on 1 January 2009.

6. J Brown (50)Non-executive director (British)

James Brown, after qualifying as a chartered accountant,

joined British Aerospace. In 1989 he joined Howden Group.

He has served as Finance Director in a number of operating

companies in the Howden Group in the UK. In 2003 he was

appointed as Group Financial Director of Howden Group

Limited. He was appointed non-executive director of the

Howden Africa Holdings Limited board on 1 March 2005.

A singular focus

1. RJ Cleland (62)

Non-executive director and Chairman (British)

2. S Meyer (55)

Group Financial Director

5. T Bärwald (47)

Chief Executive Officer (German)

3. M Malebye (38)

Independent non-executive director

4. AB Mashiatshidi (50)

Independent non-executive director

6. J Brown (50)

Non-executive director (British)

03Howden Annual Report 2009

Notes to the financials statements continuedfor the year ended 31 December 2010

04 Howden Annual Report 2009

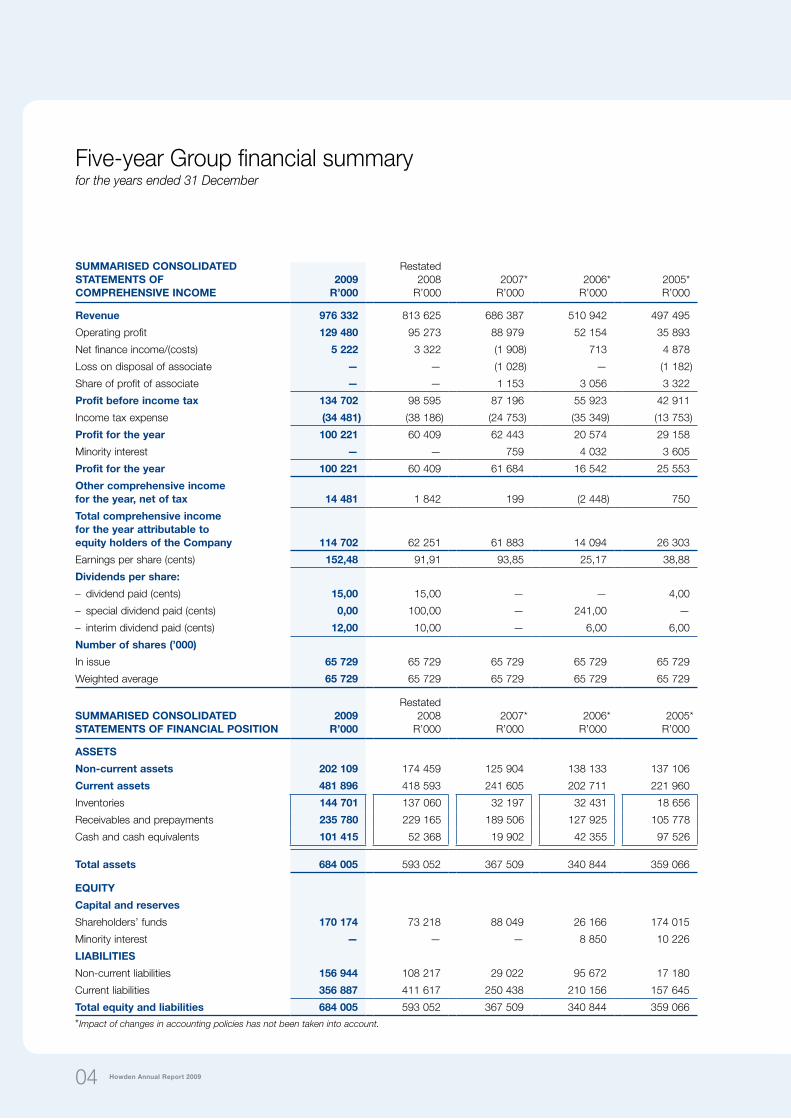

Five-year Group financial summaryfor the years ended 31 December

SUMMARISED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

2009R’000

Restated 2008R’000

2007*R’000

2006*R’000

2005*R’000

Revenue 976 332 813 625 686 387 510 942 497 495

Operating profit 129 480 95 273 88 979 52 154 35 893

Net finance income/(costs) 5 222 3 322 (1 908) 713 4 878

Loss on disposal of associate — — (1 028) — (1 182)

Share of profit of associate — — 1 153 3 056 3 322

Profit before income tax 134 702 98 595 87 196 55 923 42 911

Income tax expense (34 481) (38 186) (24 753) (35 349) (13 753)

Profit for the year 100 221 60 409 62 443 20 574 29 158

Minority interest — — 759 4 032 3 605

Profit for the year 100 221 60 409 61 684 16 542 25 553

Other comprehensive income for the year, net of tax 14 481 1 842 199 (2 448) 750

Total comprehensive income for the year attributable to equity holders of the Company 114 702 62 251 61 883 14 094 26 303

Earnings per share (cents) 152,48 91,91 93,85 25,17 38,88

Dividends per share:

– dividend paid (cents) 15,00 15,00 — — 4,00

– special dividend paid (cents) 0,00 100,00 — 241,00 —

– interim dividend paid (cents) 12,00 10,00 — 6,00 6,00

Number of shares (’000)

In issue 65 729 65 729 65 729 65 729 65 729

Weighted average 65 729 65 729 65 729 65 729 65 729

SUMMARISED CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

2009R’000

Restated2008

R’000 2007*R’000

2006*R’000

2005*R’000

ASSETS

Non-current assets 202 109 174 459 125 904 138 133 137 106

Current assets 481 896 418 593 241 605 202 711 221 960

Inventories 144 701 137 060 32 197 32 431 18 656

Receivables and prepayments 235 780 229 165 189 506 127 925 105 778

Cash and cash equivalents 101 415 52 368 19 902 42 355 97 526

Total assets 684 005 593 052 367 509 340 844 359 066

EQUITY

Capital and reserves

Shareholders’ funds 170 174 73 218 88 049 26 166 174 015

Minority interest — — — 8 850 10 226

LIABILITIES

Non-current liabilities 156 944 108 217 29 022 95 672 17 180

Current liabilities 356 887 411 617 250 438 210 156 157 645

Total equity and liabilities 684 005 593 052 367 509 340 844 359 066

*Impact of changes in accounting policies has not been taken into account.

05Howden Annual Report 2009

Value added statementfor the year ended 31 December 2009

2009

R’000

Restated 2008R’000

Revenue 976 332 813 625

Finance income 14 682 13 310

Less: Paid to suppliers for materials and services (598 774) (478 114)

Total value added 392 240 348 821

Distributed as follows:

To employees as salaries, wages and other benefits 208 278 181 701

To lenders finance costs 9 460 9 988

To depreciation and amortisation 7 573 5 678

To shareholders as dividends 17 746 82 160

To government as tax expense 34 481 38 186

Proceeds from borrowings — (31 143)

Total value added distributed 277 538 286 570

Portion of value added reinvested to sustain and expand the business 114 702 62 251

Total value added distributed and reinvested 392 240 348 821

Notes to the financials statements continuedfor the year ended 31 December 2010

06 Howden Annual Report 2009

Group at a glance

Percentage of market served by industry

n Transport

n Environment

n HVAC

n Mining

n Petrochemical

n Industrial

n Steel/cement

n Power

n Other

2009

1% 1%

Fans and Heat Exchangers

Products: Boiler fans, heat exchangers, site

services, HVAC fans, standard and industrial

fans and blowers, main surface fans, auxiliary

mine fans, centrifugal blowers and dust

extraction on coal mines.

Environmental Control

2008

11% 5%

5%

7%

22%

11%

3%

1%

2%

1%

6%

18%

47% 56%

Products: Gas cleaning plant, combustion

engineering, furnaces, incinerators, process

compressors, refrigeration equipment, water

chillers, positive displacement blowers,

waste water treatment and control and

instrumentation.

3%

07Howden Annual Report 2009

Group structure

Howden Africa Holdings Limited

Fans and Heat Exchangers Environmental Control

Howden Group South Africa

Limited

James Howden & Godfrey Overseas

Limited

Institutional & private investors

100% 100%

47,90% 7,49% 44,61%

100% 100%

Howden Holdings A/S

Charter International plc

Notes to the financials statements continuedfor the year ended 31 December 2010

08 Howden Annual Report 2009

Chairman’s statement

Structural changes to Group

activities

No significant changes to Group

structures have been made over the

last year.

Black economic empowerment

Continuous focus on improving our BEE

status covering management control,

employment equity, skills development,

procurement, enterprise development

and socio-economic development has

led to an improvement in our assessment

against the DTI’s generic scorecard.

It is pleasing to report that the Group

is now recognised as a value adding

level 5 contributor, giving our customers

100% procurement recognition on all

monies spent with Group companies.

Health and safety

The Group takes the health and safety of

employees extremely seriously. Monthly

performance reports are generated on

health and safety matters and these

I am pleased to report an excellent set of results

for the year ended 31 December 2009. Earnings

per share attributable to equity holders of the

Company increased to 152,48 cents per share

(2008: 91,91 cents per share), an increase of

65,9%.

General review

Although the economy experienced

negative growth over the first two

quarters of 2009 there appears to

be signs of a bottoming out from the

recession with moderate growth forecast

in 2010. Under these circumstances it

is pleasing to report that the Group has

been able to hold the order book at

levels close to those that were reported

at the beginning of 2009.

In 2009 revenue of R976,3 million is

reported compared to R813,6 million

in 2008, an increase of 20%, and

operating profit has increased by 35,9%

to R129,5 million (2008: R95,3 million).

Improved project margins in both

divisions, and strong increases in

revenue achieved in the Environmental

Control division, has contributed to profit

margins above those reported last year.

Of considerable importance to the

Group was the extent of our inclusion

in Eskom’s new build programme. This

has resulted in sustainability of business

given that work on Eskom’s return

to service programme has started to

decline. Another important issue for the

Group has been the execution of the

contract for the supply and erection of

a dedusting system at ArcelorMittal.

Progress to date on this project gives

encouragement that the Environmental

Control division has delivered a project

which could lead to further opportunities

elsewhere.

Order intake levels have moved largely in

line with revenue through the year. The

exception has been in the Environmental

Control division where a decline in the

order book has been reported. This

raises challenges for the division but

signs of increasing production volumes

in both the mining and manufacturing

sectors of the economy should lead to

an improvement in prospects through

2010.

The review of operations covers the

divisions more specifically.

09Howden Annual Report 2009

are taken into account in evaluating the

performance of senior managers. Lost

time accidents reported in 2009 totalled

three compared to the seven reported in

2008, and 1,8 million hours have been

worked with no lost time accidents since

February 2009.

In recognition of the excellent work

being done by the Company’s Booysen’s

site in developing an improved safety

performance and reducing the number

of lost time incidents, it was awarded the

Howden Global Environmental, Health

and Safety Award for Most Improved

Unit worldwide. It is also pleasing to

report that Howden Donkin achieved

OHSAS 18001 accreditation early in the

year, resulting in both manufacturing

sites carrying this certification.

Group companies will continue to

be tasked with the responsibility of

raising the profile of health and safety

throughout their respective business

units, further supporting the policy to

achieve a safety culture where managers

and employees believe a lost time

accident rate of zero is realistic.

Environment compliance

Good progress has been made through

the year in raising environmental

awareness in the Group, leading to both

manufacturing sites achieving certification

against the ISO 14001 international

environmental standard. The Group is

committed to the needs of customers

in an environmentally sound and

sustainable manner, through continuous

improvement in our environmental

performance in all activities. Howden

technology and know-how helps the

power generation, oil and gas, mining

and other industries it supplies to

operate in a less environmentally harmful

manner.

Board of directors

Mr Thomas Bärwald was appointed to

the Board as Chief Executive Officer from

1 January 2009. There were no other

changes in the directorate during the

period under review.

Dividends

In line with our previous intention to

commit to regular dividend payments, it

is pleasing to announce the declaration

of a dividend of 20 cents per share

payable to shareholders for the year

ended 31 December 2009.

Management and staff

In conclusion, I thank management and

staff for the contribution made through

the year in generating an excellent set of

results.

RJ CLELAND

Non-executive Chairman

12 May 2010

RJ Cleland

Non-executive Chairman

Notes to the financials statements continuedfor the year ended 31 December 2010

10 Howden Annual Report 2009

Review of operations

> The standard fan business produced a solid performance in a very

competitive market, achieving profit margins in line with expectations

> The business unit focused on the mining market and concentrated its

efforts on the coal and gold mining markets where conditions appeared

more favourable

> Negotiations for a five-year National Draught Plant Framework

Agreement with Eskom were successfully concluded during the year

Fans and Heat Exchangers

Contribution to Group revenue

62%

Notes to the financials statements continuedfor the year ended 31 December 2010

12 Howden Annual Report 2009

Review of operations continued

Fans and Heat Exchangers

aforesaid programme, and success in

converting select new build opportunities,

performance levels in this business should

at least be maintained.

Negotiations for a five-year National

Draught Plant Framework Agreement

with Eskom were successfully concluded

during the year. The agreement covers the

supply of general spares and maintenance

on air heaters and draught plant fans

installed at Eskom’s coal-fired power

stations, and replaces individual contracts

previously in place at the respective

stations. This will allow a more focused

effort on skills development and training

to support Eskom’s drive to improve

efficiencies and plant availability.

The return to service (RTS) and capacity

increase projects within Eskom provided

continuous support for the aftermarket

business within the power generation

industry. The RTS programme is nearing

completion but it is planned to replace

this business with increased aftermarket

activity and the new build programme

connected to Medupi and Kusile power

stations.

Strong order book levels have been

maintained through the year, and although

there is evidence of some margin slippage

due to product mix, existing prospects

support the view that another good year

of earnings should be forthcoming in

the Fans and Heat Exchangers division

in 2010.

Order intake for fans and heat

exchangers totalled R751 million,

which represents 76% of the

total order intake, compared to

R849 million the previous year.

The standard fan business produced a

solid performance in a very competitive

market, achieving profit margins in

line with expectations. It is pleasing to

report that the business also achieved

success in obtaining certification against

the OHSAS 18001 occupational health

and safety management standard, and

the international environmental standard

ISO 14001. Tender activity has remained

high through the year and certain capital

projects, previously postponed, have been

released for updated pricing and should

offer opportunity through 2010.

A sharp drop in commodity prices during

the second half of 2008 raised concerns

that the platinum mining and industrial

metals processing markets would be

difficult in 2009. The business unit focused

on this market therefore concentrated

its efforts on the coal and gold mining

markets where conditions appeared more

favourable. These efforts, coupled with

a drive to increase aftermarket business,

resulted in improved profitability being

reported in the period. Good progress

was also achieved in the production

of cooling tower fans connected to

Eskom’s new build programme. Assuming

no unforeseen postponements to the

Notes to the financials statements continuedfor the year ended 31 December 2010

14 Howden Annual Report 2009

Review of operations continued

> Good progress made in executing the order received from ArcelorMittal

for the supply and erection of a meltshop dedusting system, the first of

its kind to be installed in South Africa

> Orders connected to deep level mine cooling have recently been

converted and work continues in developing further prospects in this

market

> Environmental legislation will continue to lead to opportunities for the

dust extraction and gas treatment technologies in our possession

Environmental control

Contribution to Group revenue

38%

Notes to the financials statements continuedfor the year ended 31 December 2010

16 Howden Annual Report 2009

Review of operations continued

Environmental control

and available prospects. Certain staff

reductions were effected during the year

due to difficult trading conditions but

the business remains optimistic about

emerging opportunities. Orders connected

to deep level mine cooling have recently

been converted and work continues

in developing further prospects in this

market.

The division has increased its base

of earnings substantially over the last

two years. Although challenges exist in

building its order book and identifying

future opportunities, a number of

prospects are developing which could

materially alter the position for the better

over the coming year. The division has,

however, realistically budgeted for a tough

year taking into account the nature of

prospects being targeted and the length

of time needed to convert them.

Outlook

The Group has reported material

improvements in results over the last three

years, with record earnings reported for

2009. Initiatives taken over the recent past

and the successful completion of certain

large-value contracts have contributed to

this improvement. This raises challenges in

maintaining a higher base of earnings given

market uncertainties being experienced

worldwide. Firming commodity prices,

and a moderate recovery in industrial

production, would give support to the

Group remaining cautiously optimistic

looking ahead.

The Environmental Control

division recorded orders of

R239 million, representing

24% of the total order intake,

compared to R407 million in

the previous year. The domestic

economy experienced negative

growth over the first two

quarters of 2009 and this raised

challenges for the Environmental

Control division which started the

year with a strong order book but

witnessed a decline through the

year.

The division made good progress in

executing the order received from

ArcelorMittal for the supply and erection

of a meltshop dedusting system, the first

of its kind to be installed in South Africa.

The gas cleaning market, however, proved

to be difficult through the year with many

industrial plants having scaled back

production, thereby postponing the need

for addressing issues of an environmental

nature. Environmental legislation will

continue to call for an increase in cleaning

standards and the Group remains

optimistic that the dust extraction and gas

treatment technologies in our possession

will play an active part in meeting future

requirements.

As the division is run as a project

management business, resources

fluctuate according to order book levels

Notes to the financials statements continuedfor the year ended 31 December 2010

18 Howden Annual Report 2009

Integrated sustainability report

to add to its range of environmental

control technologies in order to respond

positively to requests for solutions in this

regard.

Howden will continue to develop its

aftermarket business, including through

the increased installed base following

recent high levels of new equipment

sales.

Shareholder information

Howden is a publicly listed company.

Ordinary shares are listed on the

JSE Limited (share code: HWN) in South

Africa. Major shareholders are disclosed

in note 13 to the financial statements.

Economic performance and

governance

Howden’s role in the African and

South African markets

Howden is a subsidiary of Howden

Global, the world’s leading designer

and supplier of fans and heaters for use

in coal-fired electricity generation. The

Company is licensed to supply product

mainly for use in the Southern Africa and

African markets and has a presence on

all 13 of Eskom’s coal-fired generation

plants. The Group has a manufacturing

presence in both Gauteng and the

Eastern Cape, and sales offices in the

Western Cape and Mpumalanga. Another

indication of our economic contribution is

both the direct and indirect employment

created by the Group, as mentioned

above.

Financial performance in 2009

Notwithstanding trying economic

circumstances, the Group delivered a

satisfactory financial performance for the

year. Details of this performance for the

financial year may be found elsewhere in

the annual report.

Howden Africa’s approach to

sustainability is grounded in the belief

that our stakeholders gave us our licence

to operate, therefore the way we do

business as a responsible corporate

citizen must be in their best interests.

Accordingly, sustainability is an integral

part of our business at the economic,

social and environmental level and spans

our employees, suppliers, communities,

business partners, media and the

government at every level.

This integrated sustainability report, the

first to be published by the Group, covers

the 2009 financial year, the intention

being to compile the report on an annual

basis in future, with a commitment to

incremental improvements in disclosure

as data collation methods and systems

are developed.

Sustainability issues covered in this

report have been prepared in accordance

with guidelines of the Global Reporting

Initiative (GRI – G3) and cover the three

development spheres of economic, social

and environmental performance. Note

that corporate governance is addressed

elsewhere in the annual report.

No significant changes to the Group

structure have been effected during the

year. This report covers those operations

in which the Group has a significant

interest and which the Company

manages.

Corporate profile

Howden today

Howden Africa is a market-driven,

customer-orientated company. The main

business activities of the Group are the

design, manufacture, installation and

maintenance of specialised air and gas

handling solutions to a wide range of

industries. The Group’s principal products

and services are split into two main

areas:

• Fans and Heat Exchangers

• Environmental Control

Corporate headquarters are located in

Booysens, Johannesburg. Manufacturing

facilities are located in Booysens

(Johannesburg), and Struandale (Port

Elizabeth). At 31 December 2009, the

Company employed 1 155 people,

largely in South Africa, of whom

469 were full-time employees and

686 contractors, some of which

are paid by employment brokers

(FY08: 1 069 people, including

contractors). Significant capital

expenditure in recent years has largely

been aimed at increasing manufacturing

capacity at the Booysens site and

improving the health and safety

environment throughout the Group.

Quality management systems of the

Company’s operating divisions are in

compliance with ISO 9001, and

the two main manufacturing sites have

been successfully assessed against the

provisions of the ISO 14001 international

environmental standard and OHSAS

18001 occupational health and safety

management standard.

Strategy

A significant part of Howden’s business is

the supply of equipment to the electricity

supply industry and the mining industry

on the African continent. Eskom’s new

build programme, high commodity

prices, and the Company’s large base

of reference plant should continue to

create demand for Howden products and

services. The requirement for emission

control products due to increasingly

stringent government regulation will also

create demand and the Group continues

Review of operations continued

19Howden Annual Report 2009

code and it is the intention to continue

with positive developments beyond the

set requirements.

Ethical standards

More fully covered under corporate

governance in the annual report.

Political donations

It is Group policy not to make donations

or other contributions to political parties

or causes.

Significant legal issues and fines

No significant fines were paid by the

Company in any of its areas of operation.

Safety and occupational health

Safety management

The responsibility for safety performance

follows the general management

organisation chart. This means that local

management at each Howden business

has primary responsibility for:

• Compliance with local regulatory

requirements;

• Following Howden policies and

procedures;

• Implementing standards issued by the

Company;

• Assessing and managing operational

risks;

• Implementing management systems

and driving continuous improvement.

Certification of our safety management

systems has been a recent priority as

it provides a high level of assurance

that the systems being implemented

are of an appropriate standard. In this

regard it is pleasing to report that our

two main manufacturing sites have

been successfully assessed against the

provisions of OHSAS 18001.

Key features of the financial performance

in 2009 are:

Orders received R990 millionRevenue generated of R976 millionCapital expenditure of R15 million Operating profit for the year of R130 million Operating margin of 13,3%At the end of December, Howden’s market capitalisation was R624 million

Payments to government

R’000

Total income tax paid 67 168

Withholding tax (STC) 1 775

Indirect taxes and duties 3 317

VAT paid 55 138

VAT refunded (13 218)

Employee taxes and other contributions

30 854

Skills development levy paid 1 356

MERSETA refund (988)

Total 145 402

No significant assistance was received

from government.

Economic transformation and

empowerment

Howden is fully committed to economic

transformation and empowerment, being

certified as a level 5 contributor in terms

of the DTI Codes of Good Practice. The

Group is also recognised as a value-

adding supplier and this allows our

customers a procurement recognition of

100% on each Rand spent with Howden.

Key areas of interest here are:

Management and control

Howden has achieved a compliance

rating of 82% against this element of

the code. It is the intention to continue

making progress at this level and

additional board appointments will be

considered in due course associated

with increasing corporate governance

demands.

Employment equity

A rating of 37% against this element

indicates that more work needs to be

done in this area to meet the compliance

targets set by the code. Although steady

progress has been made in appointing

HDSAs into non-technical positions,

the skills crisis in the engineering sector

raises challenges in improving this rating

materially in the short term. This is

compounded by the fact that engineering

has not traditionally attracted skilled

females into the sector.

Skills development

Plans are in place to improve the

existing rating of 54% over the next two

years. The recent establishment of an

apprentice and learner programme has

resulted in full recognition being obtained

for this aspect of skills development

but this needs to be rolled out to all

areas of the organisation. A learning

and development manager has been

appointed to assist with progress in this

regard.

Preferential procurement

The Group continues to exert pressure

on its supplier base in terms of improving

their respective B-BBEE credentials. This

has resulted in positive outcomes with

the Group achieving a 97% rating on this

element of the code. Already 535 (54%)

of all vendors have provided certification

of their B-BBEE status and it is therefore

likely to increase in time.

Enterprise and socio-economic

development

Initiatives developed over recent years

have resulted in a 100% rating being

achieved against these elements of the

Notes to the financials statements continuedfor the year ended 31 December 2010

20 Howden Annual Report 2009

One of the key contributions that Howden Africa makes to sustainability is the stability of our work environment and the track record of being able to retain experienced scarce skills while developing a pipeline of potential skills in a sector which is riddled with a lack of technical and engineering skills.

As at the end of December 2009 Howden Africa’s total employment complement was 1 155, made up of 469 permanent employees (41%), full-time contractors 94 (8%), and 592 (51%) site-based contractors. Employment is spread out primarily in Gauteng, Mpumalanga (mainly site service workers and on average we employ 358 contractors through the year) and the Eastern Cape. TurnoverThe Company continues to regularly monitor and evaluate staff turnover. This is more so given the scarcity of skills in the engineering sector. The turnover figure for the Group in 2009 was 6,0% and of this figure 2,5% was retiring employees and redundant positions. A number of strategic human resource initiatives have been put in place among which is the appointment of a talent manager to put in place effective strategies that address attraction and retention of key staff as well as transfer of skills.

Safety performanceHowden’s target for safety is zero lost time injuries. Progress towards this is monitored by tracking the lost time injuries per 200 000 hours worked (LTIFR). In 2009, LTIFR was 0,18, around a third less than 2008. The number of days away from work per 200 000 hours worked was reduced by 30 percent from 57 in 2008 to 40 in 2009. A total number of 1,8 million hours has been worked without a lost time accident since the last reported incident. Correcting unsafe conditions before they result in serious injuries is an important part of the management system and the target is to increase the reporting of near misses and unsafe conditions by at least 10% in 2010.

More than 90% of the Group’s workforce participated indirectly in formal joint management-worker health and safety programmes. The workforce is represented on the committee by elected spokespersons.

Occupational health managementHowden provides access to quality healthcare through company-managed facilities, third-party service providers or medical aids to all employees, some contractors and many dependants. Howden’s two medical centres provide an effective range of medical support services to on-site employees with access to 24-hour casualty departments at nominated hospitals.

Exposure to noise levels over an extended period of time can lead to loss of hearing and the Company endeavours to limit noise levels through the installation of equipment that lowers the level of noise, and the provision of advanced hearing protection devices. This is an ongoing programme.

In 2005, an HIV/Aids programme was implemented with assistance from a specialist third-party organisation. Awareness training is offered on a continuous basis and more than 50% of staff members participated in the voluntary counselling and testing offered. The process has been recently extended into a wellness programme which includes employee assistance beyond conventional medical fields as well.

While HIV is not classified as an occupational illness, it is a key priority for Howden given the impact it has on the Company, our employees and their communities.

HIV and AIDS performanceA 2003 HIV/AIDS impact analysis using the Actuarial Society of South Africa model 2003 (ASSA2003) estimated that around 6,3% of Howden’s employees could be HIV positive. Actual experience to date gives indication of a prevalence rate lower than the actuarial estimation.

Howden Africa as an employerLabour practices and decent workA significant and stable employerHowden Africa prides itself in being a progressive and responsible employer who at all times is constantly seeking best practice methods or knowledge in attracting, developing and retaining our core asset which is human capital. At the heart of this is the strategic management of people and processes. This is achieved through various mechanisms but underpinning this is committed leadership.

Integrated sustainability report continued

21Howden Annual Report 2009

notice period required in respect of organisational change affecting 50 or more employees. A 60-day notice and consultation period regarding any proposed restructuring or organisational change is allowed in terms of section 189A of the Act.

Training and developmentHowden Africa has a demonstrable commitment to the ongoing training and development of its employees. In 2009 money spent on training programmes was in excess of R3 million. This was evident in the strong training drive for technical skills. Flagship programmes include Howden Academy. This is an academy that was established by Howden Global specifically for skills training for young engineers. This has been a resounding success and to date Howden Africa has sent on average 15 young engineers, predominantly HDSAs. This programme sees the engineers spending a three-week tenure with the best lecturers and practical exposure needed in this sector.

Another successful initiative is the

apprenticeship programme which talks

directly to sectoral skills in conjunction

with the Merseta. Our annual intake has

remained constant and 2009 included

a female student. There are now

35 apprentices and 10 learners on the

books of subsidiary companies.

Human resource developmentAt the core of people management strategies is human resource development or organisational development. A concerted effort has been made in the past year to strategically establish learning and development, the outcome of which includes a long-term learning and development strategy (three to five-year plan). It is the aim of Howden to develop and train employees to achieve strategic business objectives while at the same time promoting a culture of learning for career progression as well as to reward employees and teams for high performance. A high performance culture is evident in that all salaried employees are on the Company’s performance management system, regular feedback to staff is done throughout the year and those meeting and or exceeding objectives are recognised through incentives and or bonuses. Non-salaried staff are unionised and relationships including wages and terms and conditions of employment are achieved through collective negotiation. The Company seeks to reward employees for their personal contribution and hence production bonuses are given to deserving employees.

Talent management strategy has been initiated and at the heart of it is managing high performers, creating talent pools, and also managing poor performers for corrective action.

Employee benefitsHowden Africa as an employer offers benefits that are aligned to market practices. These would include leave, annual performance bonuses, long-term incentives, medical aid, and maternity/paternity leave, educational bursaries for children of employees, disability cover, life insurance, and pension fund. Any other

benefits would be in line with legislated or collective bargaining agreements.

Provision is made for employees post-retirement through pension and provident funds. Provident funds are funded on an accumulation basis through employer and employee contributions which were fixed when the funds were constituted in South Africa. A total of 266 employees belong to funds managed by the Metal Industries Benefit Fund Administrators and 270 to Company pension funds. Full details of retirement benefit obligations can be found in the notes to the accounts.

Annual wage negotiations were concluded in July 2007 to cover a three-year period. Average increases in 2009 were 9% in respect of all wage categories.

Howden Africa observes and uses the Labour Relations Act as an instrument of guidance should there be any operational changes that require minimum notice periods. The Act governs the minimum

Collective bargaining

Wages Salaried

72

0

20

40

60

80

0

66

13

4

16

■ NUMSA■ SOLIDARITY■ UASA

Notes to the financials statements continuedfor the year ended 31 December 2010

22 Howden Annual Report 2009

people. This is in line with its broader

transformation objective. While

substantial progress has been made

in making appointments from the

historically disadvantaged community

at managerial level this remains an

ongoing effort especially in the face of

scarcity of skills and the challenges in

attracting women to this industry. Senior

management representation improved in

the past year.

Employment equity statistics

These statistics are for the period ending

September 2009 resulting in variances to

numbers stated above.

Howden also identified the need to

qualify mature workers (unqualified but

operating as an artisan) and engaged

22 candidates in a 24 – 28 week

accelerated training programme aimed

at achieving artisan qualifications.

Howden Africa’s training programmes

have culminated in the training of

272 employees which is equivalent to

6 090 training hours approximating

an average of 22,4 training hours per

employee.

Other learning programmes are put in

place to enhance management skills from

junior to senior management, to improve

customer skills as well as interpersonal

skills which we believe also contribute

to the overall transformation agenda of

the organisation. Learning interventions

in the period past were 52 in total.

Howden Africa in partnership with the

Merseta also started an accelerated skills

programme for semi-skilled workshop

employees in a drive to assist them

to become certified. This was largely

successful and future efforts will be

ongoing.

While Howden Africa is not a

discriminatory employer it remains

committed to the upliftment and

recruitment of previously disadvantaged

Occupational levels Male Female Total

A C I W A C I W

Top management 1 1

Senior management 2 4 1 7

Professionally qualified and experienced specialists and mid-management 18 5 5 58 6 1 1 5 99

Skilled technical and academically qualified workers, junior management, supervisors, foremen and superintendents 22 36 5 65 4 3 7 142

Semi-skilled and discretionary decision-making 71 48 1 3 19 11 6 17 176

Unskilled and defined decision-making 8 1 1 10

TOTAL PERMANENT 121 90 11 131 31 12 10 29 435

Temporary employees 34 15 0 21 5 2 2 79

GRAND TOTAL 155 105 11 152 36 14 10 31 514

Integrated sustainability report continued

23Howden Annual Report 2009

members participated in the annual Business Trust corporate relay, run from Qunu in the Eastern Cape to Soweto.

Taking responsibility for our productHowden designs, manufactures, installs and maintains fans, preheaters and environmental control equipment. The majority of the Group’s products are bespoke to individual customer’s specifications.

The Company manufactures product essentially made of steel and derivatives thereof. Steel is bought in as a raw material and thereafter processed to form end products for sale to customers. The life cycle of most of our products exceeds 30 years, during which time they receive continuous care in order to maintain designed efficiencies. At the end of the life cycle the product would typically be available for recycling.

The Company has not been exposed to any incidents of non-compliance with regulations or voluntary codes concerning safety and health impacts of its product, nor have there been any incidents or complaints of non-compliance with regulations and voluntary codes in respect of product labelling or service information.

Environmental performanceManagement approachIn selecting performance indicators for environmental impact, Howden has taken into account government guidelines and the worldwide concerns over climate change. As a result, the Group has selected as performance indicators the reduction of direct and indirect energy usage, water consumption and improved recycling practices. Focusing on these performance indicators is also expected to drive efficiency gains and cost savings.

Human rightsHowden Africa endeavours to respect and uphold human rights as enshrined in the human rights charter and as contained in the Constitution of South Africa. In this respect we endorse the International Labour Organisation’s principles relating to the prohibition of forced, compulsory or child labour. In 2009 no contraventions in this regard were reported, nor any incidents of discrimination.

In relation to salaries Howden Africa’s remuneration philosophy is based on ability and competence and is market related regardless of race or gender.

Working with the communityCorporate social responsibilityHowden’s formal corporate social investment (CSI) programme is closely aligned with our business objectives. The aim of the programme is to contribute to an improved and equitable social environment by providing support and opportunities in the communities where we operate.

We concentrate on projects that have been identified as sustainable, address a social need and ultimately offer a means to help communities help themselves through empowerment or developing lasting skills that can lead to a better quality of life. We also look for projects that give our own people the opportunity to participate on a personal level.

Our current flagship project is based in Port Elizabeth. Working with Howden subsidiary Donkin Fans, we are sponsoring the Viva English project at Mount Pleasant School which aims to improve pupils’ skills in this language as

the gateway to opportunity in the 21st century. The Company also equipped the Kwazamokuhle High School near Hendrina in Mpumalanga with a laboratory to the value of R100 000.

Howden has a long-standing relationship with a number of established organisations, including Cotlands, St Mary’s Orphanage, and Girls & Boys Town, all based in Johannesburg. We also provide ongoing financial assistance, focused on academic improvement, to a designated beneficiary at United Cerebral Palsy. We also support community sports teams near customer sites by donating kits for team members. During the year, some R50 000 was allocated to ad hoc requests from different non-government organisations.

Howden maintains its membership of the Business Trust, a partnership between private sector and government aimed at creating jobs and building capacity. In support of this initiative, Howden staff

Notes to the financials statements continuedfor the year ended 31 December 2010

24 Howden Annual Report 2009

Gas emissions

Group operations are of a nature not

leading to large scale gaseous emissions.

It is the intention, however, to monitor

these in order to provide more specific

details in future reports.

During the year, welding fume extractors

were installed in the workshops in

Booysens and Port Elizabeth. The

extractors draw welding fumes away

from the face of the operator during the

welding process, thereby enhancing

health protection. This is the largest

installation of its type in South Africa

completed by the nominated supplier.

Materials usage

Steel is the raw material used at most

of our manufacturing sites and all scrap

steel is collected in an organised manner

for collection by scrap merchants. Scrap

steel equals less than 5% of total steel

worked on in any one year.

Waste areas have been established for

the collection of waste products prior to

removal and disposal in accordance with

relevant health, safety and environmental

legislation.

The responsibility for environmental

performance follows the general

management organisation chart. This

means that local management at

each Howden business has primary

responsibility for:

• Compliance with local regulatory

requirements;

• Following Howden policies and

procedures;

• Implementing standards issued by the

Company;

• Assessing and managing operational

risks;

• Implementing management systems

and driving continuous improvement.

Certification of our environmental

management systems has been a

recent priority as it provides a high level

of assurance that the systems being

implemented are of an appropriate

standard. In this regard it is pleasing to

report that our two main manufacturing

sites have been successfully assessed

against the provisions of ISO 14001.

The Company sees opportunity to

contribute to local environmental

programmes through application of its

diverse range of technology solutions,

particularly in areas of air pollution

control.

Environmental targets

To address and minimise the impact

of the Company’s operations on the

environment, taking into account

regulatory requirements, the board is

committed to developing a number

of five-year targets relating to energy

consumption and recycling and this will

be communicated in future reports.

Significant environmental incidents

There have been no reports of significant

spillages.

Environmental expenditure and

financial provision

No environmental fines were received.

Energy management

Howden’s energy consumption is

primarily in the form of electricity, mainly

required for the Group’s manufacturing

operations. To a lesser extent, gas

and diesel are also consumed. Energy

consumption costs account for less than

2% of the operating cost base.

Water management

Howden’s operations make limited use

of metered water, with all drawn water

returned to the city recycle system.

Emissions

Dust released from Howden’s

manufacturing operations is limited. No

dust-related complaints from community

members have been received.

Biodiversity

Howden does not operate on any land

in, or adjacent to, protected areas of high

biodiversity outside protected areas.

Integrated sustainability report continued

25Howden Annual Report 2009

Corporate governance

of the articles of association, subject to

retirement by rotation and re-elected by

shareholders. The number of directors

to retire must be at least one-third of

the board. The appointments of new

directors are subject to confirmation by

shareholders at the next annual general

meeting following their appointment.

Attendance at meetings

There were four meetings held during the

year.

DirectorDate

appointed Attendance

RJ Cleland (Chairman)

2 March 2000 4/4

AB Mashiatshidi31 July

2003 4/4

S Meyer3 May 1996 4/4

T Bärwald1 January

2009 4/4

M Malebye7 November

2007 4/4

J Brown1 March

2005 4/4

Audit Committee

The Audit Committee consists of two

independent, non-executive directors,

and one non-executive director with the

Company Secretary as secretary.

The Audit Committee’s main task is to

ensure the maintenance of, and where

necessary, the review of the effectiveness

of internal financial controls, along with

the maintenance of adequate accounting

records and disclosures. It also oversees

the financial reporting process and is

concerned with the review of important

accounting issues, pending material

litigation, specific disclosures in the

financial statements and a review of audit

recommendations in compliance with the

Overview

The board and management of Howden

Africa Holdings Limited are committed

to the principles of openness, integrity

and accountability as advocated in the

King Report on Corporate Governance

for South Africa – 2002 (King II Report).

The board has endorsed the Code

of Corporate Practices and Conduct

contained in the King II Report and

believes that in all material respects the

Company complied with the principles

contained in such code through the year

under review. The Company complies

with all requirements concerning

corporate governance in the Listings

Requirements of the JSE Limited, South

Africa. The board is currently formulating

a roadmap for the implementation of the

King Report on Corporate Governance

for South Africa – 2009 (King III Report).

The primary objective of any system of

corporate governance is to ensure that

directors, officers and managers, to

whom the running of large corporations

has been entrusted by the shareholders,

carry out their responsibilities faithfully

and effectively, placing the interests

of the corporation ahead of their own.

This process is facilitated through the

establishment of appropriate reporting

and control structures within the

organisation.

Directorate and executive

management

The board of Howden Africa Holdings

Limited is balanced between executive

and non-executive directors. The roles

of Chairman and Chief Executive Officer

vest in different persons. There are

presently four non-executive directors

of which two are independent, and two

executive directors, none of whom have

contracts exceeding two years. New

appointments to the board are submitted

to the board as a whole for approval

prior to appointment. The board meets

at least quarterly and retains full and

executive control over the Group. The

board monitors management ensuring

that material matters are subject to board

approval. The executive management

attend board meetings by invitation.

All directors have unlimited access to

the advice and services of the Company

Secretary, who is responsible to the

board for ensuring that the board

procedures are followed.

All directors are entitled to seek

independent professional advice at the

Group’s expense, concerning the affairs

of the Group, after obtaining the approval

of the Chairman.

The board is ultimately responsible for

ensuring that the business is a going

concern, and to this end effectively

controls the Group and its management

and is involved in all decisions that

are material for this purpose. The

board functions in terms of a Board

Charter which requires that there is

an appropriate balance of power and

authority on the board.

There is a clear division of responsibilities

between the members of the Board of

Directors.

New appointments are recommended

to the board by the Remuneration

Committee. All directors are, in terms

Notes to the financials statements continuedfor the year ended 31 December 2010

26 Howden Annual Report 2009

loss of unauthorised acquisition, use or

disposition, and that transactions are

properly authorised and recorded.

The system includes a documented

organisational structure and division of

responsibility, established policies and

procedures, including a code of ethics

to foster a strong ethical climate, which

is communicated throughout the Group,

and careful selection, training and

development of people.

Internal audit monitors the operation of

the internal control system and report

findings and recommendations to

management, audit committee and the

board of directors. Corrective actions

are taken to address control deficiencies

and other opportunities for improving

the system as they are identified. The

Group’s assessment of the effective

controls over the financial reporting and

safeguarding of assets was considered

to meet all the necessary criteria for the

year ended 31 December 2009. The

internal audit examines and evaluates

the adequacy and effectiveness of the

organisation’s system of internal control

and quality performance in carrying out

assigned responsibilities.

Ethical standards

Howden Africa Holdings Limited has

adopted a code of conduct policy. This

incorporates the Group’s operating,

financial and behavioural policies in a

set of integrated values, including the

ethical standards required of employees

of the Group in their interaction with

Code of Corporate Practice and Conduct

as well as the Group’s code of ethics.

The committee monitors any non-audit

services undertaken by the independent

auditors in terms of a formal policy which

has been adopted in this regard.

Both the internal and external auditors

have unrestricted access to this

committee. The committee meets at

least twice a year and these meetings

are attended by external auditors and

appropriate members of executive

management including those involved in

risk management, control and finance.

The committee reviews the effectiveness

of internal control in the Company with

reference to the findings of both the

internal and external auditors.

Audit Committee meetings’

attendance

There were three meetings held during

the year.

DirectorDate

appointed Attendance

AB Mashiatshidi (Chairman)

31 July 2003 3/3

M Malebye7 November

2007 3/3

J Brown26 February

2009 3/3

Remuneration Committee

The Remuneration Committee consists of

the chairperson, who is an independent

non-executive director, and a non-

executive director. It is authorised by the

board to review remuneration packages

of all directors and senior managers.

The committee has formal terms of

reference approved by the board. The

remuneration philosophy of the Group is

to ensure that employees are rewarded

for their contribution according to the

Group’s industry, market and country

benchmarks.

The committee is responsible for the

assessment and approval of broad

remuneration strategy for the Group.

The financial statements accompanying

this report make full disclosure of the

total of executive and non-executive

directors’ earnings and other benefits in

accordance with the requirements of the

Companies Act, 1973, the King Report II

and the JSE requirements.

Remuneration Committee meetings’

attendance

There were two meetings held during

the year.

DirectorDate

appointed Attendance

M Malebye (Chairperson)

11 June 2009 2/2

RJ Cleland 2 March 2000 2/2

Corporate governance

Internal control systems

To meet its responsibility with respect to

providing reliable financial information,

the Group maintains financial and

operational systems of internal control.

These controls are designed to provide

reasonable assurance that transactions

are concluded in accordance with

management’s authority, that the assets

are adequately protected against material

Corporate governance continued

27Howden Annual Report 2009

one another and with all stakeholders.

Detailed policies and procedures are

in place across the Group covering the

regulation and reporting of transactions

in securities of Group companies by

directors and officers. The code is

distributed to all employees of the

company, and its subsidiaries. The

directors regularly review this code

to ensure it reflects best practice in

corporate governance and whistle

blowing procedures are in place to

encourage the reporting of unethical

behaviour. The directors are of the

opinion that ethical standards are being

met and supported by the code.

The environment, health and safety

The Group strives to conform to

environmental, health and safety laws

in its operations and also seeks to

add value to the quality of life of its

employees through preventive health

programmes. Although the Group’s

major activities do not pose a major

threat to the environment, the Group’s

risk management activities continue to

focus on compliance with key features of

existing environmental, health and safety

legislation and international standards.

Business continuity plan

The Group has a business continuity

plan in place to enable Howden Africa

to manage risks and prevent incidents

and disasters. It also gives guidance in

reporting to such incidents. The plan is

divided into two sections; Proactive Risk

Management and Post Incident Plan.

This plan is managed by the Business

Continuity Management Committee and

the Crisis Management Committee.

The Business Continuity Management

Committee is responsible for proactive

risk management, disaster prevention

and minor incidents. The Crisis

Management Committee is there to

assist in major incidents or disasters.

Human resources

Employment equity, skills development

and empowerment

The Company is committed to

empowering all its employees, particularly

those from previously disadvantaged

backgrounds. The Employment Equity

Act and Skills Development Act provide

a useful framework for formalising our

approach. Recruitment and development

strategies are aligned to this objective

and advancement is achieved by training,

rewarding and managing our talent

effectively. Programmes such as our

mentorship and engineers in training

initiatives ensure that we grow internal

talent pipelines as well as contribute

to the broader national agenda on

skills development. We are proud of

our apprenticeship programme which

continues to add qualified artisans into

our workforce as well as into the broader

labour market.

Notes to the financials statements continuedfor the year ended 31 December 2010

28 Howden Annual Report 2009

Directors’ responsibility

The financial statements are prepared in accordance with

International Financial Reporting Standards (IFRS) and

incorporate responsible disclosures in line with the accounting

philosophy of the Group. The financial statements are based

on appropriate accounting policies consistently applied

and supported by reasonable and prudent judgements and

estimates. The directors believe that the Group will be a going

concern in the year ahead. For this reason they continue to

adopt the going-concern basis in preparing the Group annual

financial statements.

These financial statements, which appear on pages 32 to 86,

have been approved by the board of directors and are signed

on its behalf by:

J BROWN S MEYER

Non-executive director Group Financial Director

12 May 2010

The directors are responsible for the integrity of the financial

statements and related information included in this annual

report.

For the board to discharge its responsibilities management

has developed and continues to maintain a system of internal

financial control. The board has ultimate responsibility for this

system of internal control and reviews the effectiveness of its

operations, primarily through the Group Audit Committee and

other risk-monitoring committees and functions.

The internal financial controls include risk-based systems of

accounting and administrative controls designed to provide

reasonable, but not absolute, assurance that assets are

safeguarded and that transactions are executed and recorded

in accordance with generally accepted business practices and

the Group’s written policies and procedures. These controls

are implemented by trained, skilled staff with clearly defined

lines of accountability and appropriate segregation of duties.

The controls are monitored by management and include

comprehensive budgeting and reporting systems operating

within strict deadlines and an appropriate control framework.

The external auditors are responsible for reporting on the

financial statements.

In my opinion as Company Secretary, I hereby confirm that, in terms of section 268 (d) of the Companies Act, 1973, as amended, that

for the year ended 31 December 2009, the Company had lodged, with the Registrar of Companies, all such returns as required of a

public company in terms of this Act and that all such returns are true, correct and up to date.

MM LUTHULI

Company Secretary

12 May 2010

Certificate by the Company Secretary

29Howden Annual Report 2009

Report of the Audit Committee

Members of the Audit Committee

The membership of the Audit Committee consists of two

independent non-executive directors, AB Mashiatshidi

(chairman) and M Malebye; and a non-executive director

J Brown.

The members of the Audit Committee have at all times acted

in an independent manner.

Frequency of meetings

The Audit Committee met three times in the financial year under

review. Provision is made for additional meetings to be held,

when and if necessary.

Persons “in attendance” and “by invitation”

The external auditors, in their capacity as auditors to the

Company, attended and reported to all meetings of the Audit

Committee. Executive directors and relevant senior managers

attended meetings on a “by invitation” basis.

Independence of audit

During the year under review the Audit Committee reviewed

a report by the external auditor and, after conducting its own

review, confirmed the independence of the auditor.

Expertise and experience of financial director

As required by the JSE Listings Requirements 3.84(h), the Audit

Committee has satisfied itself that the Financial Director has

appropriate expertise and experience.

Introduction

The Audit Committee has pleasure in submitting this report, as

required by sections 269A and 270A of the Companies Act, which

was promulgated in the course of the year, as part of the measures

contained in the Corporate Laws Amendment Act 2006.

Functions of the Audit Committee

The functions of the Audit Committee include:

• Review of the year-end financial statements, culminating with

a recommendation to the board;

• Review of the external audit report, after audit of the year-end

financial statements;

• Review of the internal audit and risk management reports,

with, when relevant, recommendations being made to the

board.

In the course of its review the committee:

• takes appropriate steps to ensure that financial statements are

prepared in accordance with International Financial Reporting

Standards (IFRS);

• considers and, when appropriate, makes recommendations

on internal financial controls;

• verifies the independence of the external auditor and of any

nominee for appointment as external auditor;

• authorises the audit fees in respect of the year-end audits;

• specifies guidelines and authorises contract conditions for the

award of non-audit services to the external auditors;

• evaluates the effectiveness of risk management, controls and

the governance processes;

• deals with concerns or complaints relating to the following:

– accounting policies;

– internal audit;

– the audit or content of annual financial statements; and

– internal financial controls.

Notes to the financials statements continuedfor the year ended 31 December 2010

30 Howden Annual Report 2009

Report of the independent auditors

including the assessment of the risks of material misstatement of

the financial statements, whether due to fraud or error. In making

those risk assessments, the auditor considers internal control

relevant to the entity’s preparation and fair presentation of the

financial statements in order to design audit procedures that

are appropriate in the circumstances, but not for the purpose of

expressing an opinion on the effectiveness of the entity’s internal

control. An audit also includes evaluating the appropriateness of

accounting policies used and the reasonableness of accounting

estimates made by management, as well as evaluating the

overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient

and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all

material respects, the consolidated and separate financial

position of Howden Africa Holding Limited as of 31 December

2009, and its consolidated and separate financial performance

and its consolidated and separate cash flows for the year then

ended in accordance with International Financial Reporting

Standards, and in the manner required by the Companies Act of

South Africa.

PRICEWATERHOUSECOOPERS INC

Director: G Hauptfleisch

Registered Auditor

Johannesburg

12 May 2010

We have audited the Group annual financial statements and

annual financial statements of Howden Africa Holdings Limited,

which comprise the consolidated and separate statements of

financial position as at 31 December 2009, and the consolidated

and separate statements of comprehensive income, changes in

equity and cash flows for the year then ended, and a summary

of significant accounting policies and other explanatory notes,

and the directors’ report, as set out on pages 32 to 86.

Directors’ responsibility for the financial statements

The Company’s directors are responsible for the preparation

and fair presentation of these financial statements in accordance

with International Financial Reporting Standards, and in the

manner required by the Companies Act of South Africa. This

responsibility includes: designing, implementing and maintaining

internal control relevant to the preparation and fair presentation

of financial statements that are free from material misstatement,

whether due to fraud or error; selecting and applying appropriate

accounting policies; and making accounting estimates that are

reasonable in the circumstances.

Auditors’ responsibility

Our responsibility is to express an opinion on these financial

statements based on our audit. We conducted our audit in

accordance with International Standards on Auditing. Those

standards require that we comply with ethical requirements

and plan and perform the audit to obtain reasonable assurance

whether the financial statements are free from material

misstatement.

An audit involves performing procedures to obtain audit evidence

about the amounts and disclosures in the financial statements.

The procedures selected depend on the auditor’s judgement,

31Howden Annual Report 2009

32 Directors’ report

34 Statements of financial position

35 Statements of comprehensive income

36 Statements of changes in equity

37 Statements of cash flows

38 Notes to the financial statements

82 Restatement of prior years

85 Interest in subsidiary companies

Contents

32 Howden Annual Report 2009

Directors’ report

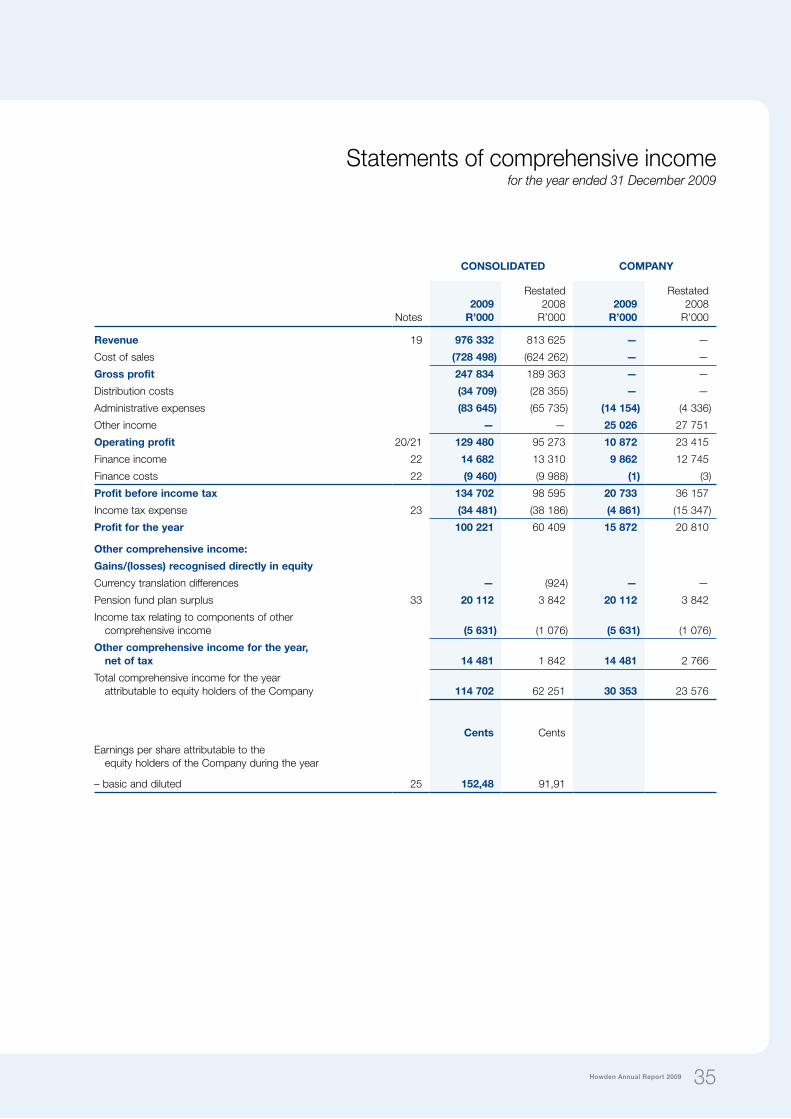

The directors have pleasure in submitting the annual report of the Group for the year ended 31 December 2009.

Restated2008

R’000Group results2009

R’000

Revenue 976 332 813 625Orders received 990 451 1 256 240 Profit before taxation 134 702 98 595 Assets 684 005 593 052 Liabilities 513 831 519 834 Depreciation 5 423 3 511 Capital expenditure 14 963 18 879

The detailed segmental report is shown in note 5 of the financial statements on pages 55 and 56.

Despite tough trading conditions brought on by recessionary conditions through the year, order intake remained at levels sufficient to report a closing order book of R712,0 million (2008: R718,9 million). Although the Company witnessed fewer large-value orders than reported last year, there was still a good spread of new equipment orders received to keep order books at satisfactory levels. Order intake in the aftermarket was particularly satisfying with an increase of 20% recorded over levels reported in 2008.

Higher revenue volumes in both business divisions, together with improved margins associated with progress on larger-value contracts, resulted in improved operating profit margins being reported against last year. FINANCIAL RESULTSIn 2009 revenue of R976,3 million is reported compared to R813,6 million in 2008, progress on contracts in the Environmental Control division, and increased activity in field service work contributing to the improvement. Reductions in revenue connected to Eskom’s return to service programme were effectively neutralised by increases in workload in other areas of the business.

Profit before tax of R134,7 million (2008: R98,6 million) is reported, higher revenue volumes and margins being reported in both operating divisions. Net financial income of R5,2 million compares to R3,3 million reported last year, a favourable outcome reflecting strong operating cash flow generation by Group companies.