hsbc greater china financials day

TRANSCRIPT

1 TWSE Code 5871

HSBC Greater China Financials Day

May 27, 2014

Disclaimer

This presentation contains forward-looking statements concerning the financial condition, results

of operations and businesses of Chailease Holding Company Limited (the "Company"). All

statements other than statements of historical fact are, or may be deemed to be, forward-looking

statements. Forward-looking statements are statements of future expectations that are based on

management’s current expectations and assumptions and involve known and unknown risks and

uncertainties that could cause actual results, performance or events to differ materially from those

expressed or implied in these statements. Forward-looking statements include, among other

things, statements concerning the potential exposure of the Company to market risks and

statements expressing management’s expectations, beliefs, estimates, forecasts, projections and

assumptions. These forward-looking statements are identified by their use of terms and phrases

such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘intend’’, ‘‘may’’, ‘‘plan’’,

‘‘objectives’’, ‘‘outlook’’, ‘‘probably’’, ‘‘project’’, ‘‘will’’, ‘‘seek’’, ‘‘target’’, ‘‘risks’’, ‘‘goals’’,

‘‘should’’ and similar terms and phrases. There are a number of factors that could affect the

future operations of the Company and could cause those results to differ materially from those

expressed in the forward-looking statements included in this document. All forward-looking

statements contained in this document are expressly qualified in their entirety by the cautionary

statements contained or referred to herein. Readers should not place undue reliance on forward-

looking statements. Each forward-looking statement speaks only as of the date of this

presentation. Neither the Company nor any of its subsidiaries undertake any obligation to publicly

update or revise any forward-looking statement as a result of new information, future events or

other information. In light of these risks, results could differ materially from those stated, implied

or inferred from the forward-looking statements contained in this presentation.

2

Agenda

Business Review

1Q2014 Performance Review

Segment Review

Q&A

Appendix

Company Overview

3

Leading Taiwan-based SME Finance Company with Focus on Greater China and Emerging Asia

Commenced operations in 2005 with national

leasing license

Focus on capital leasing and expanding into

factoring and trade financing

~8,000 clients (90% are local enterprises)

25 offices nationwide and 500 sales personnel

PRC

Taiwan

37 years of operating track record since 1977

Leading market position in leasing and

installment sales

Full SME financing platform

Diversified SME-focused customer base with

over 18,000 corporate clients

12 offices and over 900 sales personnel

Thailand

Commenced operations in 1989

Focus on automobile installment

sales, equipment leasing and

factoring

7 offices in key commercial hubs

Vietnam

Commenced operations in 2007

Focus on capital leasing

3 offices in Hanoi, HCMC and Cantho

Notes

Unless otherwise indicated, all figures are as of Dec. 31, 2012

1. Others include assets from our U.S. and Vietnam operations as well as those of the holding companies; the Company is engaged in commercial real estate financing in the U.S. (Los Angeles) and focuses mainly on asset

management and risk control since the subprime crisis

4

Agenda

Business Review

1Q2014 Performance Review

Segment Review

Q&A

Appendix

Company Overview

5

Customized SME Financing Solutions and

New and Innovative Products

■Chailease has presence

in 12 locations in Taiwan

– Covers all the major

commercial centers

■More than 900 sales

personnel as at June 30,

2013

■ 45% of total contract

value of new leasing and

installment sales

contracts among TLA

members in 2013 in

Taiwan

Hsinchu

Kaohsiung

Tainan

Changhwa

Ilan

Taichung

Taipei Taoyuan

New Taipei

Hsinchung

Chungli

Chiayi

1977

1980

1986

1989

1995

2011

2012

Leasing Installment sales

International factoring

Automobile installment sales

Domestic factoring

Direct financing

Automobile leasing

Car rental

ESCO financing

Insurance brokerage

2006

Extensive Distribution Network

Market Leader in the Taiwan Leasing Industry

2003

Aircraft financing

2013

6

Well Positioned to Capture the Significant Growth Potential in the PRC

Extensive Footprint across Major

Industrial & Commercial Hubs in PRC(2)

Source Company

PRC Strategy

1 Expand presence gradually from coastal regions to inland cities

2 Broaden industry exposure

3 Expand product offerings and enter niche financing businesses

4 Further strengthen risk and human resources management

Note : 2013 Loan portfolio % by region

Eastern China 25%, Southeast China 18%, Southern China 19%, Central and

Southeast China 11% and Northern China 28%

7

Strategic Alliances with major banks to

ensure sufficient funding to support growth

Offshore Funding

Dim Sum Bond

Continue to diversify sources of funding

and lower funding cost

• Bank Loans

• Commercial Papers

• Corp Bonds

• TWSE Listing

• Securitization

Taiwan PRC

Adequate and Diverse Funding to Support Business Growth

8

Effective Credit Risk Management System and Risk Pricing Mechanism

Credit Policy

■ Enforcement of the credit grading and scoring system

■ Performance review tied to asset quality

Effective Credit Review and Approval Process to Ensure Adequate Return Risk Exposure

1

Review Application Documents

• Whether the application has any element falling into the blacklist

• Whether all the required documents are in order

• Any need to request other documents

Credit Rating and Approval

• Proceed within the scope of authorisation

3 Confirmation and Approval

Initial Application 2

Discussion Between Business Department and Credit Department

Case Assignment

• The management of credit department assigns the application to a credit officer

• Discuss and clarify the structure of the application and identify issues

On-Site Visit

Analyse credit data

Decide the credit amount and financing terms

Appraisal

Prepare credit analysis reports

Credit rating and scoring, and applying the risk model

• On-site credit investigation to reduce the possibility of misjudgment

• Face-to-face credit investigation to verify the accuracy of information provided or to supplement information

Information Gathering and Analysis

Credit Approval Process

Credit Review and Decision Process

■ Standardized operating procedure of credit evaluation

■ Segregation of sales and credit appraisal functions

■ Streamlined credit approval process

9

■ Develop various credit risk

management models based on the

use of credit rating system

■ Integrate qualitative and

quantitative client information to

quantify a client’s creditworthiness

and provide an early earning

mechanism with regard to its

overall risk exposure

■ The IRB approach consists of:

Comprehensive Credit Risk Model Increases the Accuracy of Assessment

Internal Rating Based (“IRB”) Approach Model Structure Model Application

Credit Risk

Management Model

(Quantification)

Credit Rating System

(Expertise/

Quantification)

■ Built according to actual SME

samples

■ Financial and non-financial factors

included

■ Constructed using diversified statistical

methods

■ Suitable for SME risk assessment

■ Periodical review to ensure adequacy

of the model

■ Estimate and quantify the risk

(EAD*PD)

■ Provide the basis for underwriting and

financing terms structuring (e.g. adjust

financing terms or make credit

enhancement)

■ Calculate the expected loss and

provide allowance for impairment

losses

Expected

Loss

Exposure

At

Default

Probabi-

lity of

Default

Loss

Given

Default = x x

The Company Calculates

Probability of Default for Each

Rating Level Based on the

Risk Assessment Model

Input Output

Scoring

Materials

■ Default assessment

■ Default point

■ Probability of

default

1 Enhance risk management capability with a standardized and tested methodology

2 Enhance accuracy of risk assessment and credit exposure

3 Reduce potential loss

Effective Credit Risk Management System and Risk Pricing Mechanism (Cont’d)

10

Agenda

Business Review

1Q2014 Performance Review

Segment Review

Q&A

Appendix

Company Overview

11

Management Highlight

Consolidated portfolio growth in line with plan

Employee turnover improved and stabilized in

China

YOY YTD

Consolidated 20% 5%

Taiwan 31% 7%

China 10% 0.4%

Thailand 9% 6%

12

Total Portfolio Consolidated

Source: unaudited financial statements

Unit: NT$ million

13

Revenue Consolidated

Source: unaudited financial statements

14

Source: unaudited financial statements

58% 51%

19%

22% 11%

11%

10%

5%

11%

2%

Unit: NT$ million

Revenue Mix Consolidated

15

Source: unaudited financial statements Note: 2013 EPS has been retroactively adjusted.

Net Profit & EPS Consolidated

16

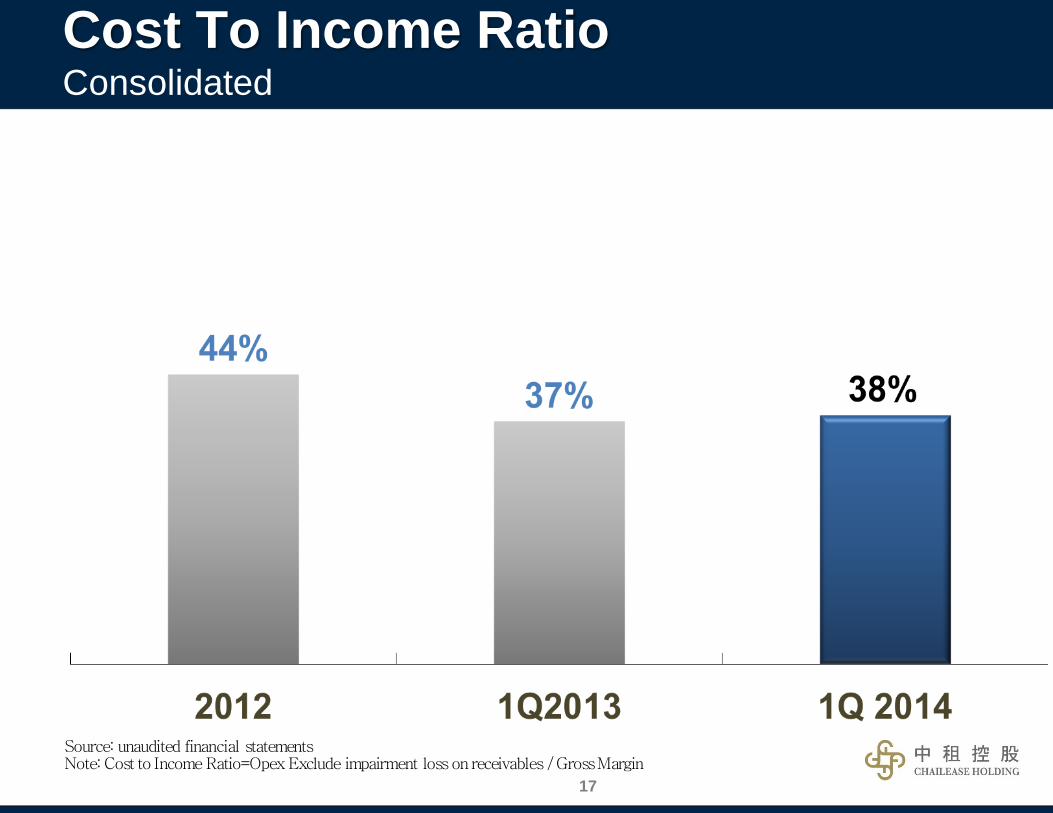

Note: Cost to Income Ratio=Opex Exclude impairment loss on receivables / Gross Margin Source: unaudited financial statements

Cost To Income Ratio Consolidated

17

ROA ROE

Source: unaudited financial statements

ROA & ROE Consolidated

18

Delinquency Allowance

Notes:

Definitions of delinquencies:

• Check payments: overdue by 7 days or more

• Equipment leasing with non-check payments: overdue by 30 days or more

• Automobile installment sales in Thailand: overdue by 90 days or more

Excludes US securitization asset

Source: unaudited financial statements

Asset Quality Consolidated

19

Agenda

Business Review

1Q2014 Performance Review

Segment Review

Q&A

Appendix

Company Overview

20

Unit: NT$ million

Source: unaudited financial statements

Total Loans & Receivables Taiwan

21

Unit: NT$ million

Source: unaudited financial statements

Revenue Taiwan

22

Unit: NT$ million

Source: unaudited financial statements

Net Profit Taiwan

23

Delinquency Allowance

Note: Definitions of delinquencies • Check payments: overdue by 7 days or more

• Equipment leasing with non-check payments: overdue by 30 days or more

Source: unaudited financial statements

Asset Quality Taiwan

24

Unit: NT$ million

Source: unaudited financial statements

Total Loans & Receivables China

25

Unit: NT$ million

Source: unaudited financial statements

Revenue China

26

Unit: NT$ million

Source: unaudited financial statements

Net Profit China

27

Delinquency Allowance

Definitions of delinquencies • Check payments: overdue by 7 days or more

• Equipment leasing with non-check payments: overdue by 30 days or more

Source: unaudited financial statements

Asset Quality China

28

Unit: NT$ million

Source: unaudited financial statements

Total Loans & Receivables Thailand

29

Unit: NT$ million

Source: unaudited financial statements

Revenue Thailand

30

Source: unaudited financial statements

Unit: NT$ million

YOY -3%

Net Profit Thailand

31

Asset Quality Thailand

Delinquency Allowance

Notes: Definitions of delinquencies: • Equipment leasing with non-check payments: overdue by 30 days or more • Automobile installment sales in Thailand: overdue by 90 days or more

Source: unaudited financial statements 32

Agenda

Business Review

1Q2014 Performance Review

Segment Review

Q&A

Appendix

Company Overview

33

Agenda

Management Highlight

1Q2014 Performance Review

Segment Review

Q&A

Appendix

Company Overview

35

36

Source: unaudited financial statements

NTD'000 2014.03.31 2013.03.31 YOY(%) 2013.12.31 QOQ(%)

Cash and cash equivalents 7,454,389 10,649,208 (30) 7,586,221 (2)

Total fund and investments 11,444,613 6,906,167 66 9,046,339 27

Notes and trade receivables 18,790 20,045 (6) 13,538 39

Loan and receivables 169,046,406 140,995,072 20 161,724,215 5

Other receivables 5,016,375 6,047,756 (17) 5,000,217 0

Property, plant and equipment 7,170,797 6,297,413 14 7,186,367 (0)

Other assets 5,030,410 4,942,072 2 5,219,053 (4)

Total assets 205,181,780 175,857,733 17 195,775,950 5

Interest bearing loans and borrowings 132,984,864 113,091,517 18 123,923,289 7

Corporate bond payable 14,074,125 12,233,796 15 14,098,319 (0)

Bank overdraft 167,753 157,145 7 84,084 100

Other liabilities 25,845,584 23,217,578 11 27,229,065 (5)

Total liabilities 173,072,325 148,700,036 16 165,334,757 5

Common stock 9,958,304 9,053,004 10 9,958,304 0

Total equity attributable to equity holders 30,155,725 25,206,106 20 28,624,443 5

Minority interests 1,953,730 1,951,591 0 1,816,750 8

Total equity 32,109,455 27,157,697 18 30,441,193 5

Consolidated Balance Sheet Summary

Source: unaudited financial statements

NTD’000 1Q2014 1Q2013 YOY(%) 4Q13 QOQ(%) Interest revenue - capital leases 1,802,786 1,787,983 1 1,775,463 2

Rent revenue - operating leases 451,367 664,879 (32) 467,651 (3)

Interest revenue - installment sales 1,553,473 1,470,666 6 1,415,964 10

Sales revenue 1,861,528 1,238,285 50 2,817,830 (34)

Other reveune 2,777,769 1,327,017 109 3,014,606 (8)

Fee Income/Service Fee 918,562 697,642 32 968,081 (5)

Other Interest Income 855,539 500,820 71 909,156 (6)

Others 1,003,668 128,556 681 1,137,368 (12)

Total revenue 8,446,924 6,488,830 30 9,491,512 (11)

Interest expense (1,015,436) (1,002,369) 1 (996,662) 2

Cost of operating leases (347,904) (498,227) (30) (403,013) (14)

Depreciation of PPE-OL (298,747) (366,334) (18) (314,752) (5)

Impairment loss of PPE-OL (49,157) (131,893) (63) (88,261) (44)

Other cost (2,353,157) (1,263,934) 86 (3,187,876) (26)

COGS (1,645,761) (1,102,242) 49 (2,528,905) (35)

Other cost (707,396) (161,692) 337 (658,971) 7

Total cost (3,716,497) (2,764,530) 34 (4,587,550) (19)

Gross profit 4,730,426 3,724,300 27 4,903,962 (4)

Operating expense (2,572,925) (1,882,861) 37 (2,877,583) (11)

Employee compensation and benefits (1,033,743) (863,855) 20 (1,006,773) 3

Impairment loss (778,172) (505,811) 54 (1,039,369) (25)

Other expense (761,010) (513,195) 48 (831,440) (8)

Other operating gain and loss 35,467 36,724 (3) 45,696 (22)

Operating profit 2,192,968 1,878,163 17 2,072,075 6

Non-operating gains/loss 15,816 156,355 (90) 220,474 (93)

Profit before income tax 2,208,785 2,034,518 9 2,292,549 (4)

Income tax expense (570,981) (569,643) 0 (606,751) (6)

Profit after income tax 1,637,803 1,464,875 12 1,685,798 (3)

Attributable to equity holders 1,561,821 1,386,267 13 1,605,816 (3)

Attributable to minority interests 75,983 78,608 (3) 79,982 (5)

EPS 1.57 1.53 3 1.61 (2)

Consolidated Income Statement Summary

37