hsbc latam smid cap conference

DESCRIPTION

HSBC LatAm SMid Cap ConferenceTRANSCRIPT

July 2014

Corporate Presentation

Executive Summary

He

avy C

on

str

uctio

n

•

• Market leader, extensive track record, with more than 60 years of experience

• Focus on: large and complex infrastructure projects

• Products: engineering solutions and rental of formwork and shoring

• Services: planning, design, technical supervision, equipment and related services

• Main clients:

Re

al E

sta

te

•

• Market leader; acquired in 2008

• Focus on: residential and commercial constructions

• Products: engineering solutions and rental of formwork, shoring and suspended access

• Services: planning, design, technical supervision, equipment and related services

• Clients: real estate companies, such as:

Re

nta

l

• Market leader; started in 2008

• Focus on: civil construction, industry, retail e others

• Products: rental and sale of motorized access equipment, such as aerial work platforms and telescopic handlers

• Cross-selling with all other Mills’ business units

• Elected "Best Company for Access of the Year" by the International Awards for Powered Access (IAPA Awards) for the year of 2011

Mills - Business Units

2

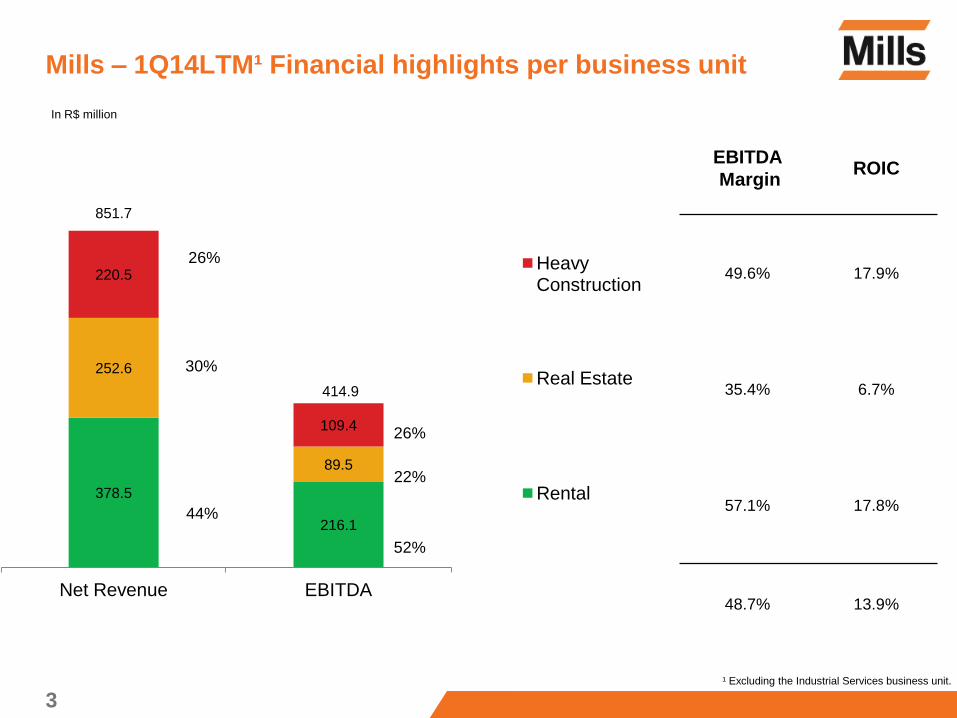

378.5

216.1

252.6

89.5

220.5

109.4

851.7

414.9

Net Revenue EBITDA

Heavy Construction

Real Estate

Rental

3

Mills – 1Q14LTM¹ Financial highlights per business unit

EBITDA

Margin ROIC

49.6% 17.9%

35.4% 6.7%

57.1% 17.8%

48.7% 13.9%

26%

22%

52%

26%

30%

44%

¹ Excluding the Industrial Services business unit.

In R$ million

4

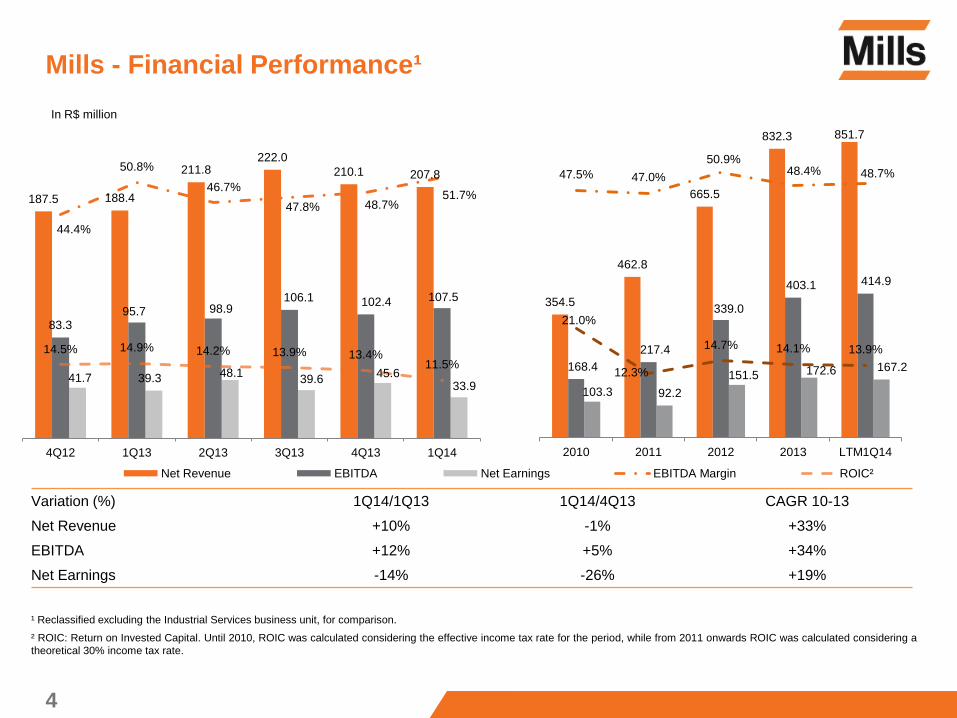

Mills - Financial Performance¹

¹ Reclassified excluding the Industrial Services business unit, for comparison.

² ROIC: Return on Invested Capital. Until 2010, ROIC was calculated considering the effective income tax rate for the period, while from 2011 onwards ROIC was calculated considering a

theoretical 30% income tax rate.

Variation (%) 1Q14/1Q13 1Q14/4Q13 CAGR 10-13

Net Revenue +10% -1% +33%

EBITDA +12% +5% +34%

Net Earnings -14% -26% +19%

In R$ million

187.5 188.4

211.8 222.0

210.1 207.8

83.3 95.7 98.9

106.1 102.4 107.5

41.7 39.3 48.1 39.6

45.6 33.9

44.4%

50.8%

46.7%

47.8% 48.7% 51.7%

14.5% 14.9% 14.2% 13.9% 13.4% 11.5%

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Net Revenue EBITDA Net Earnings EBITDA Margin ROIC²

354.5

462.8

665.5

832.3 851.7

168.4

217.4

339.0

403.1 414.9

103.3 92.2

151.5 172.6 167.2

47.5% 47.0%

50.9% 48.4% 48.7%

21.0%

12.3%

14.7% 14.1% 13.9%

2010 2011 2012 2013 LTM1Q14

Estamos presentes em 16 estados no Brasil com 56 unidades

Mills – Geographic Presence

5

Branches location As of March 31, 2014

Minas Gerais

Rio Grande do Sul

Santa Catarina

São Paulo

Mato Grosso do Sul

Rio de Janeiro

(Headquarter)

Espirito Santo

Bahia

Distrito Federal

Goias

Sergipe

Paraiba

Rio Grande Ceará

Piaui

Maranhão

Tocantins

Pará

Rondônia

Acre

Roraima Amapá

Amazonas

Mato Grosso

Parana

Alagoas

States with Mills’ Presence

Rental

Heavy Construction

Real Estate

Pernambuco

do Norte

We are present in 17 states of Brazil with 51 branches

Castelão stadium – Fortaleza, CE

Rental

7

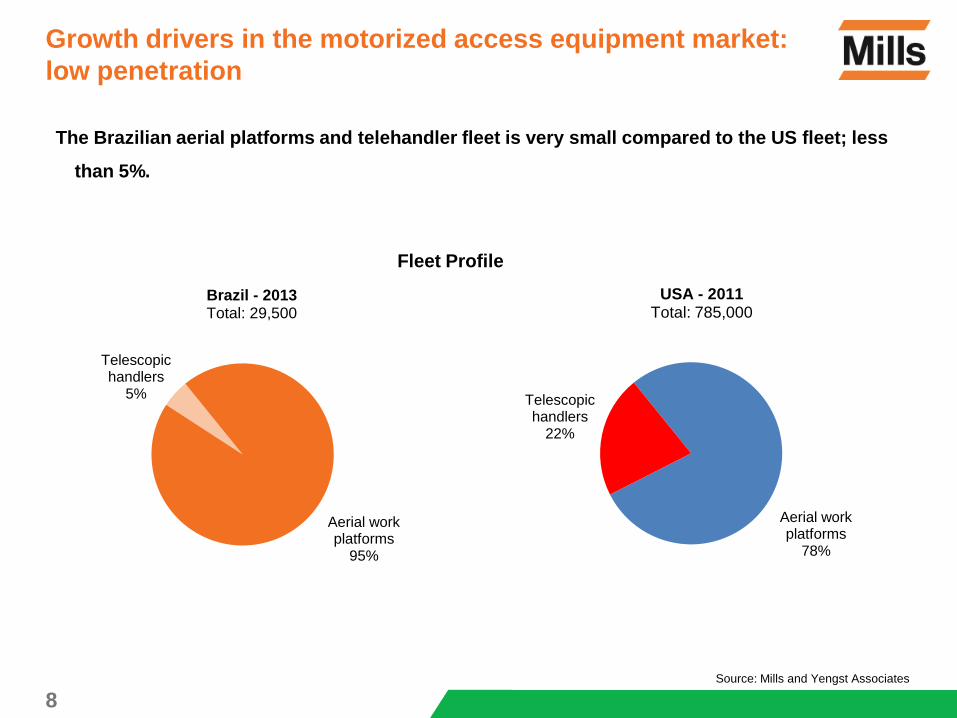

Growth drivers in the motorized access equipment market:

safety and productivity

Source: Mills

Market penetration

through

substitution of less

secure and

efficient access

methods

Recent safety standards (NR-18 and NR-35) oblige the use of aerial platforms to lift people,

increasing safety and productivity in the work site

Aerial work platforms

95%

Telescopic handlers

5%

Brazil - 2013 Total: 29,500

Growth drivers in the motorized access equipment market:

low penetration

8 Source: Mills and Yengst Associates

Aerial work platforms

78%

Telescopic handlers

22%

USA - 2011

Total: 785,000

Fleet Profile

The Brazilian aerial platforms and telehandler fleet is very small compared to the US fleet; less

than 5%.

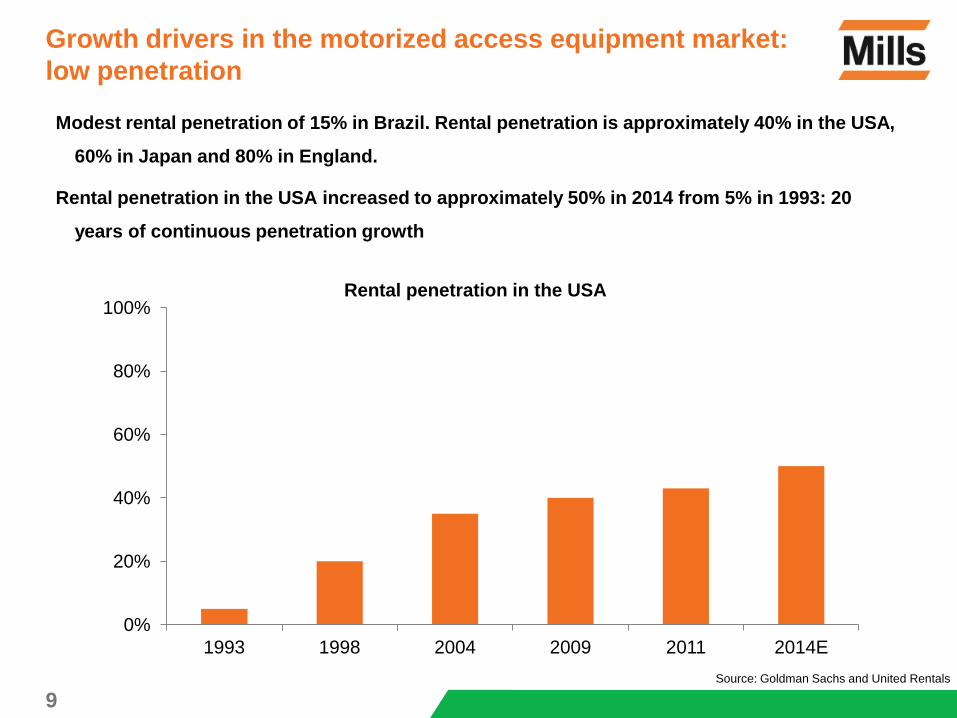

Modest rental penetration of 15% in Brazil. Rental penetration is approximately 40% in the USA,

60% in Japan and 80% in England.

Rental penetration in the USA increased to approximately 50% in 2014 from 5% in 1993: 20

years of continuous penetration growth

Growth drivers in the motorized access equipment market:

low penetration

9 Source: Goldman Sachs and United Rentals

20%

35% 40%

43%

50%

0%

20%

40%

60%

80%

100%

1993 1998 2004 2009 2011 2014E

Rental penetration in the USA

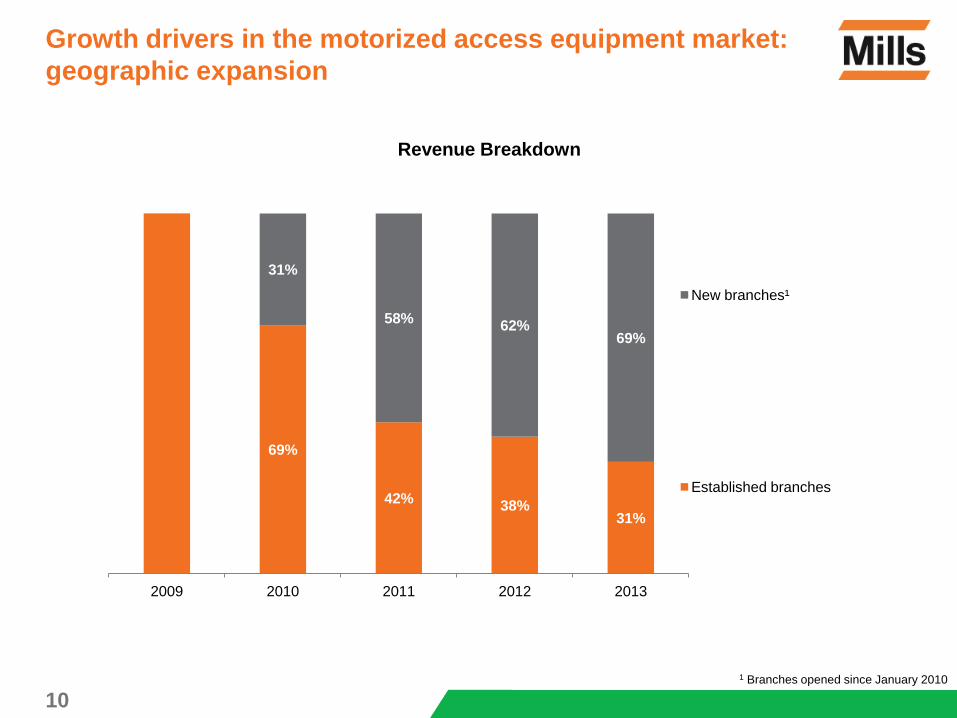

Revenue Breakdown

69%

42% 38%

31%

31%

58% 62%

69%

2009 2010 2011 2012 2013

New branches¹

Established branches

Growth drivers in the motorized access equipment market:

geographic expansion

10

1 Branches opened since January 2010

11

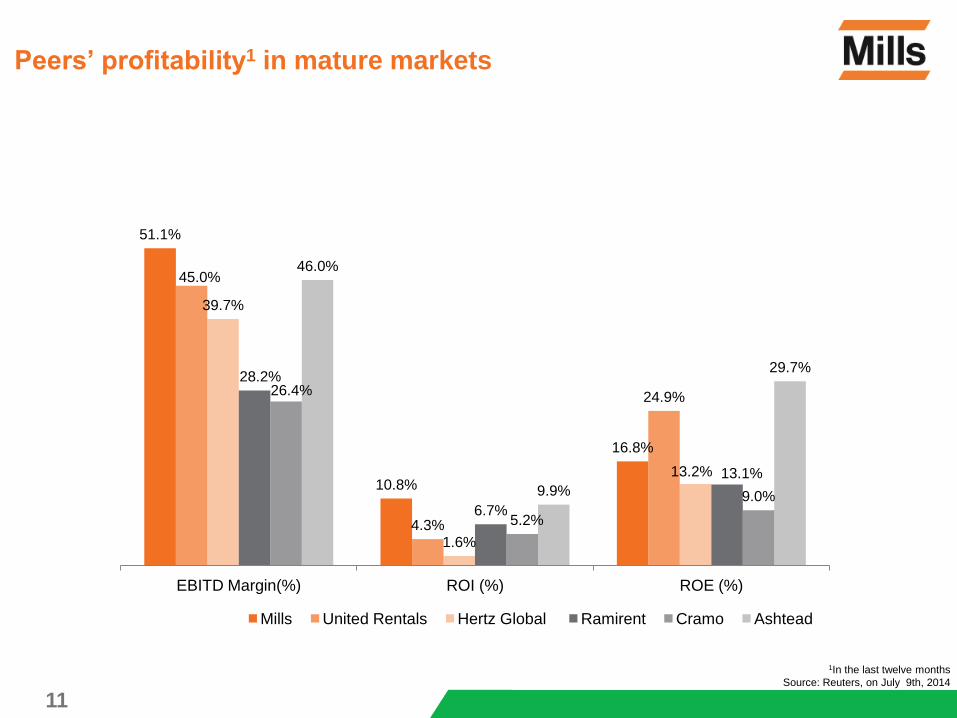

Peers’ profitability1 in mature markets

51.1%

10.8%

16.8%

45.0%

4.3%

24.9%

39.7%

1.6%

13.2%

28.2%

6.7%

13.1%

26.4%

5.2%

9.0%

46.0%

9.9%

29.7%

EBITD Margin(%) ROI (%) ROE (%)

Mills United Rentals Hertz Global Ramirent Cramo Ashtead

1In the last twelve months

Source: Reuters, on July 9th, 2014

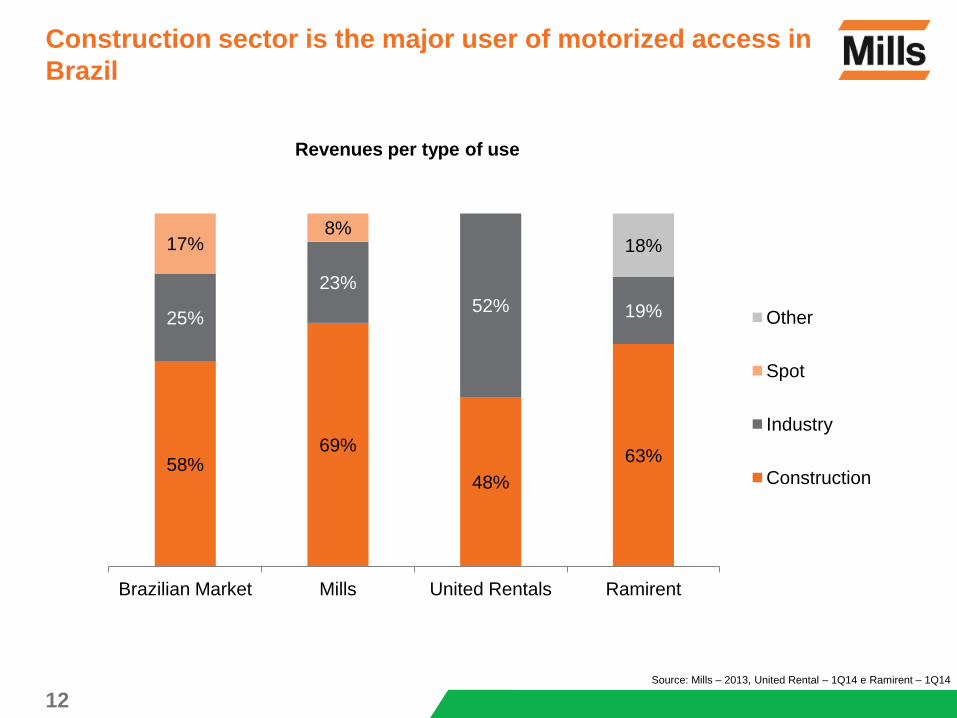

Revenues per type of use

58% 69%

48%

63%

25%

23%

52% 19%

17% 8%

18%

Brazilian Market Mills United Rentals Ramirent

Other

Spot

Industry

Construction

Construction sector is the major user of motorized access in

Brazil

12 Source: Mills – 2013, United Rental – 1Q14 e Ramirent – 1Q14

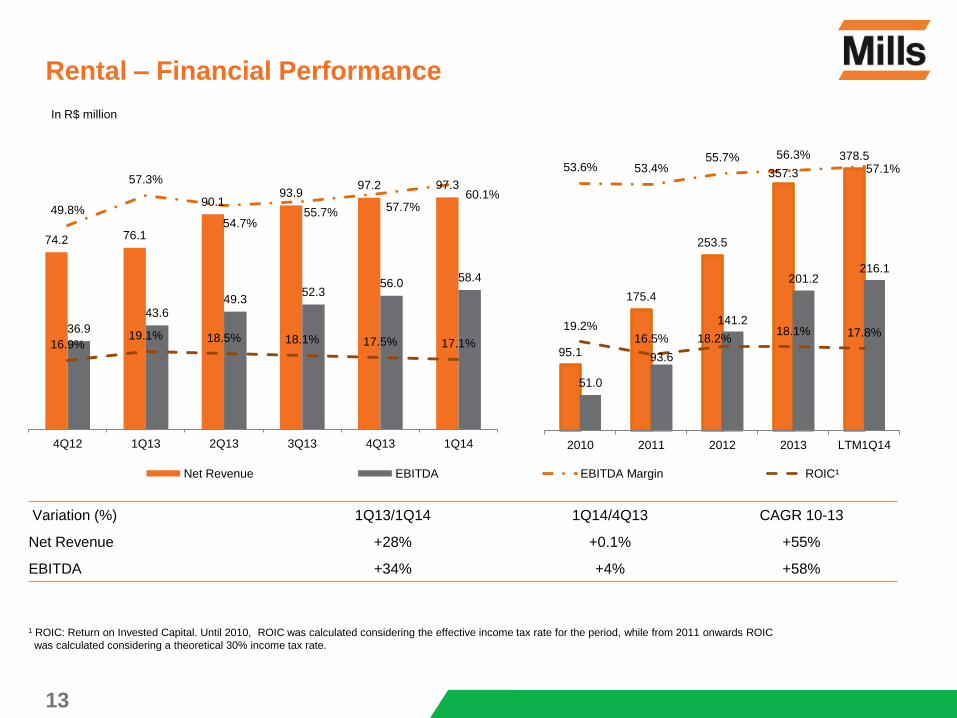

Variation (%) 1Q13/1Q14 1Q14/4Q13 CAGR 10-13

Net Revenue +28% +0.1% +55%

EBITDA +34% +4% +58%

Rental – Financial Performance

13

1 ROIC: Return on Invested Capital. Until 2010, ROIC was calculated considering the effective income tax rate for the period, while from 2011 onwards ROIC

was calculated considering a theoretical 30% income tax rate.

In R$ million

74.2 76.1

90.1 93.9

97.2 97.3

36.9

43.6 49.3

52.3 56.0

58.4

49.8%

57.3%

54.7% 55.7% 57.7%

60.1%

16.9% 19.1% 18.5% 18.1% 17.5% 17.1%

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Net Revenue EBITDA EBITDA Margin ROIC¹

95.1

175.4

253.5

357.3

378.5

51.0

93.6

141.2

201.2 216.1

53.6% 53.4% 55.7% 56.3%

57.1%

19.2% 16.5% 18.2%

18.1% 17.8%

2010 2011 2012 2013 LTM1Q14

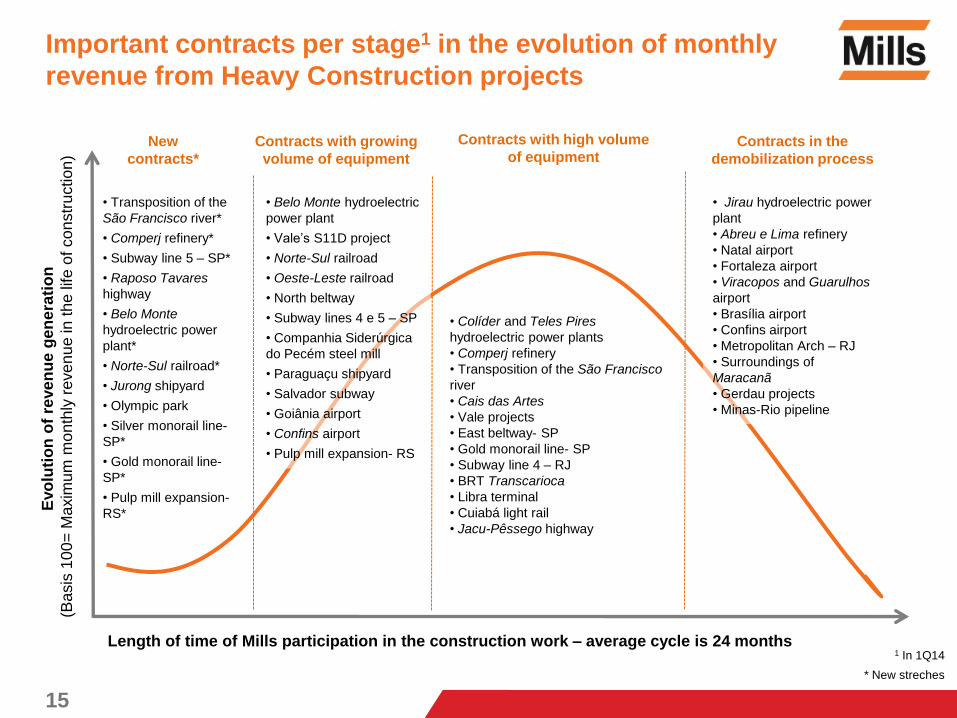

Heavy Construction

Cinta costeira - Panamá

• Transposition of the

São Francisco river*

• Comperj refinery*

• Subway line 5 – SP*

• Raposo Tavares

highway

• Belo Monte

hydroelectric power

plant*

• Norte-Sul railroad*

• Jurong shipyard

• Olympic park

• Silver monorail line-

SP*

• Gold monorail line-

SP*

• Pulp mill expansion-

RS*

Evo

luti

on

of

reve

nu

e g

en

era

tio

n

(B

asis

10

0=

Ma

xim

um

mo

nth

ly r

eve

nu

e in t

he

life

of co

nstr

uctio

n)

Length of time of Mills participation in the construction work – average cycle is 24 months

• Belo Monte hydroelectric

power plant

• Vale’s S11D project

• Norte-Sul railroad

• Oeste-Leste railroad

• North beltway

• Subway lines 4 e 5 – SP

• Companhia Siderúrgica

do Pecém steel mill

• Paraguaçu shipyard

• Salvador subway

• Goiânia airport

• Confins airport

• Pulp mill expansion- RS

• Colíder and Teles Pires

hydroelectric power plants

• Comperj refinery

• Transposition of the São Francisco

river

• Cais das Artes

• Vale projects

• East beltway- SP

• Gold monorail line- SP

• Subway line 4 – RJ

• BRT Transcarioca

• Libra terminal

• Cuiabá light rail

• Jacu-Pêssego highway

• Jirau hydroelectric power

plant

• Abreu e Lima refinery

• Natal airport

• Fortaleza airport

• Viracopos and Guarulhos

airport

• Brasília airport

• Confins airport

• Metropolitan Arch – RJ

• Surroundings of

Maracanã

• Gerdau projects

• Minas-Rio pipeline

New

contracts*

Contracts with growing

volume of equipment

Contracts with high volume

of equipment Contracts in the

demobilization process

* New streches

Important contracts per stage1 in the evolution of monthly

revenue from Heavy Construction projects

15

1 In 1Q14

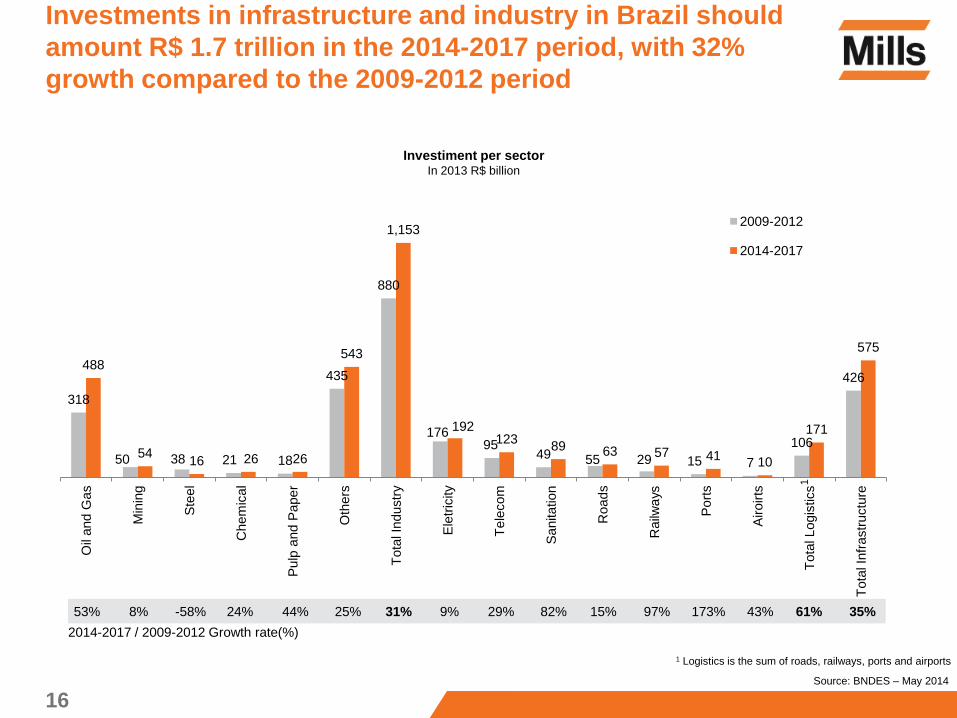

Investments in infrastructure and industry in Brazil should

amount R$ 1.7 trillion in the 2014-2017 period, with 32%

growth compared to the 2009-2012 period

16

318

50 38 21 18

435

880

176 95

49 55 29 15 7

106

426 488

54 16 26 26

543

1,153

192 123

89 63 57 41 10

171

575

Oil

and G

as

Min

ing

Ste

el

Chem

ical

Pulp

and P

aper

Oth

ers

Tota

l In

dustr

y

Ele

tric

ity

Tele

com

Sanitation

Roads

Railw

ays

Port

s

Airoirts

Tota

l Logis

tics

Tota

l In

frastr

uctu

re

2009-2012

2014-2017

Investiment per sector In 2013 R$ billion

2014-2017 / 2009-2012 Growth rate(%)

53% 8% -58% 24% 44% 25% 31% 9% 29% 82% 15% 97% 173% 43% 61% 35%

Source: BNDES – May 2014

1

1 Logistics is the sum of roads, railways, ports and airports

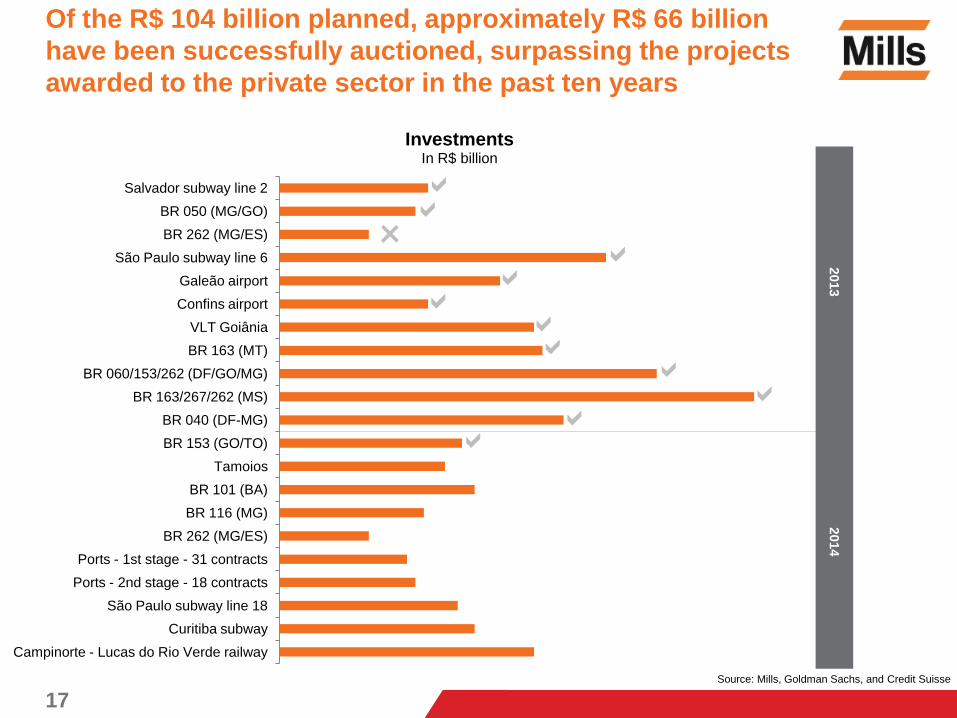

Of the R$ 104 billion planned, approximately R$ 66 billion

have been successfully auctioned, surpassing the projects

awarded to the private sector in the past ten years

17

Campinorte - Lucas do Rio Verde railway

Curitiba subway

São Paulo subway line 18

Ports - 2nd stage - 18 contracts

Ports - 1st stage - 31 contracts

BR 262 (MG/ES)

BR 116 (MG)

BR 101 (BA)

Tamoios

BR 153 (GO/TO)

BR 040 (DF-MG)

BR 163/267/262 (MS)

BR 060/153/262 (DF/GO/MG)

BR 163 (MT)

VLT Goiânia

Confins airport

Galeão airport

São Paulo subway line 6

BR 262 (MG/ES)

BR 050 (MG/GO)

Salvador subway line 2

Investments In R$ billion

2013

×

2014

Source: Mills, Goldman Sachs, and Credit Suisse

Source: Valor newspaper, June 24,2014, using data from BNDES, ministries and public agencies. Do not

include railways that are part of the Programa de Investimentos em Logística (Logistic Investment Program).

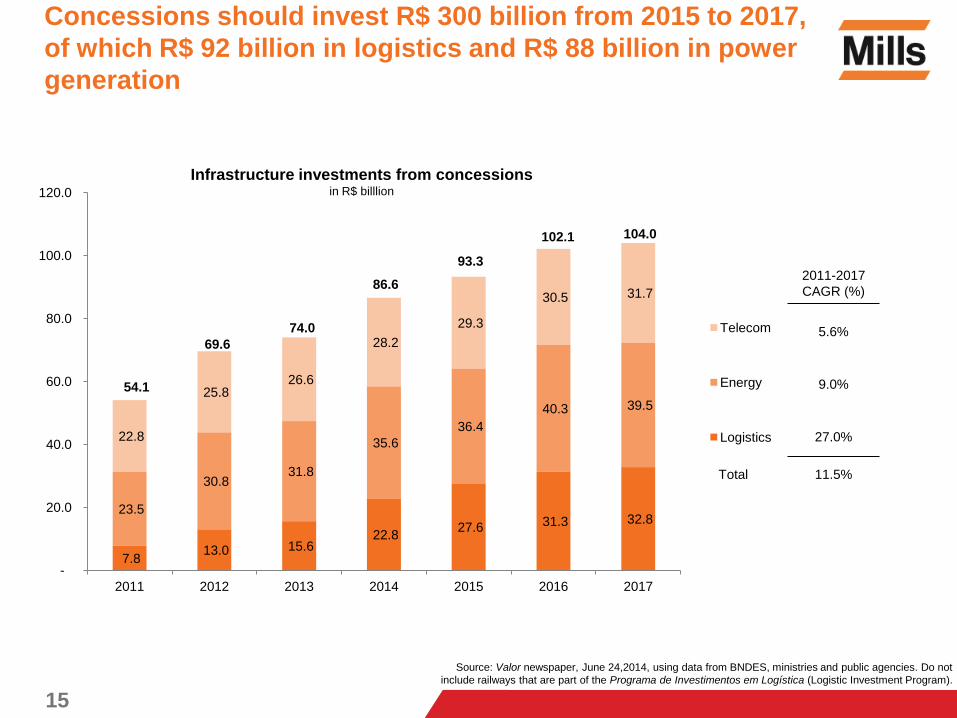

Concessions should invest R$ 300 billion from 2015 to 2017,

of which R$ 92 billion in logistics and R$ 88 billion in power

generation

15

2011-2017

CAGR (%)

Total

27.0%

9.0%

5.6%

11.5%

7.8 13.0 15.6

22.8 27.6 31.3 32.8

23.5

30.8 31.8

35.6

36.4

40.3 39.5

22.8

25.8 26.6

28.2

29.3

30.5 31.7

54.1

69.6

74.0

86.6

93.3

102.1 104.0

-

20.0

40.0

60.0

80.0

100.0

120.0

2011 2012 2013 2014 2015 2016 2017

Telecom

Energy

Logistics

Infrastructure investments from concessions in R$ billlion

In R$ million

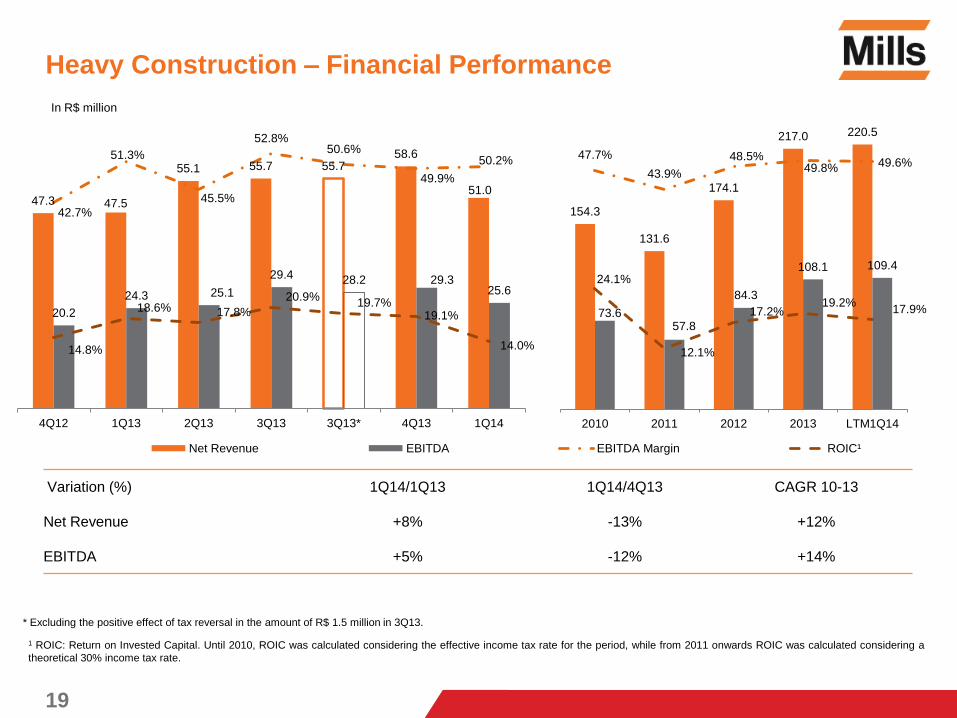

Variation (%) 1Q14/1Q13 1Q14/4Q13 CAGR 10-13

Net Revenue +8% -13% +12%

EBITDA +5% -12% +14%

Heavy Construction – Financial Performance

19

* Excluding the positive effect of tax reversal in the amount of R$ 1.5 million in 3Q13.

1 ROIC: Return on Invested Capital. Until 2010, ROIC was calculated considering the effective income tax rate for the period, while from 2011 onwards ROIC was calculated considering a

theoretical 30% income tax rate.

47.3 47.5

55.1 55.7 55.7 58.6

51.0

20.2

24.3 25.1

29.4 28.2 29.3 25.6

42.7%

51.3%

45.5%

52.8% 50.6%

49.9%

50.2%

14.8%

18.6% 17.8%

20.9% 19.7%

19.1%

14.0%

4Q12 1Q13 2Q13 3Q13 3Q13* 4Q13 1Q14

Net Revenue EBITDA EBITDA Margin ROIC¹

154.3

131.6

174.1

217.0 220.5

73.6 57.8

84.3

108.1 109.4

47.7%

43.9%

48.5% 49.8% 49.6%

24.1%

12.1%

17.2% 19.2%

17.9%

2010 2011 2012 2013 LTM1Q14

Real Estate

Mast climbing platform

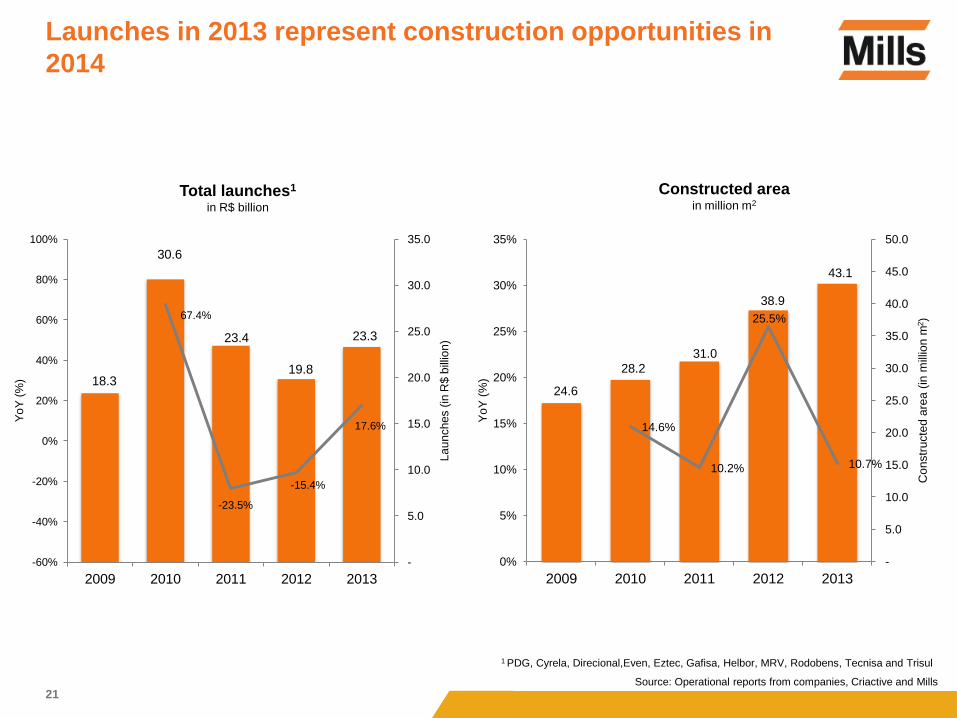

21

18.3

30.6

23.4

19.8

23.3

67.4%

-23.5%

-15.4%

17.6%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2009 2010 2011 2012 2013

Yo

Y (

%)

La

un

ches (

in R

$ b

illio

n)

1 PDG, Cyrela, Direcional,Even, Eztec, Gafisa, Helbor, MRV, Rodobens, Tecnisa and Trisul

Source: Operational reports from companies, Criactive and Mills

Total launches1

in R$ billion

24.6

28.2

31.0

38.9

43.1

14.6%

10.2%

25.5%

10.7%

0%

5%

10%

15%

20%

25%

30%

35%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2009 2010 2011 2012 2013

Yo

Y (

%)

Co

nstr

ucte

d a

rea

(in

mill

ion

m2)

Constructed area

in million m2

Launches in 2013 represent construction opportunities in

2014

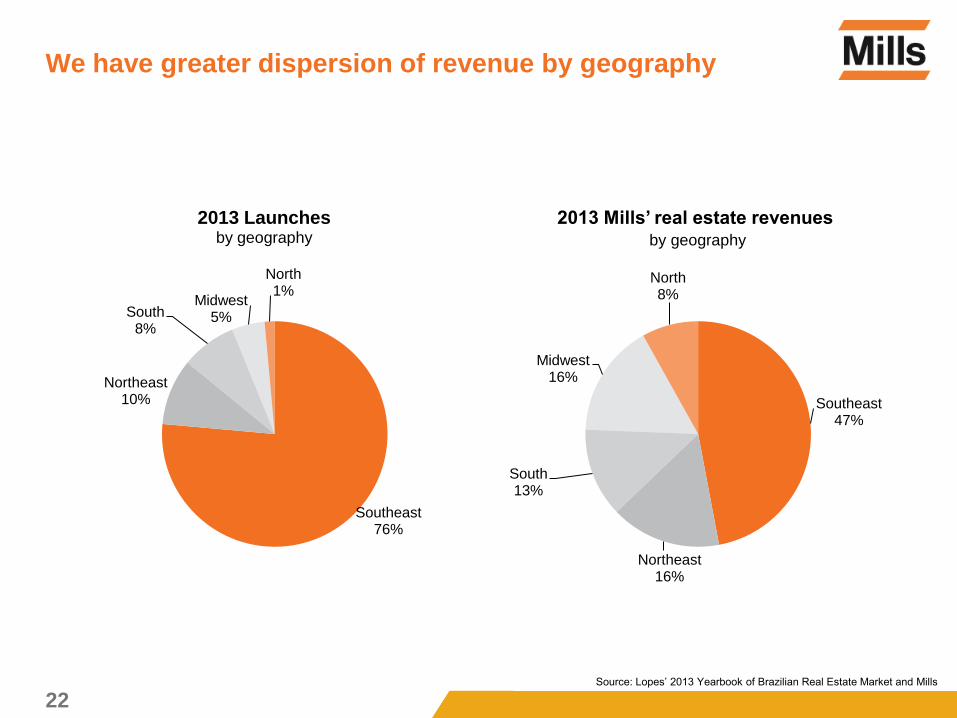

22

Southeast 76%

Northeast 10%

South 8%

Midwest 5%

North 1%

2013 Launches by geography

Southeast 47%

Northeast 16%

South 13%

Midwest 16%

North 8%

2013 Mills’ real estate revenues by geography

Source: Lopes’ 2013 Yearbook of Brazilian Real Estate Market and Mills

We have greater dispersion of revenue by geography

23

Growth drivers of the residential market

High housing deficit

Growing housing financing

Higher purchasing power

Lack of labor and higher labor cost

Industrialization of the construction process

Geographic expansion

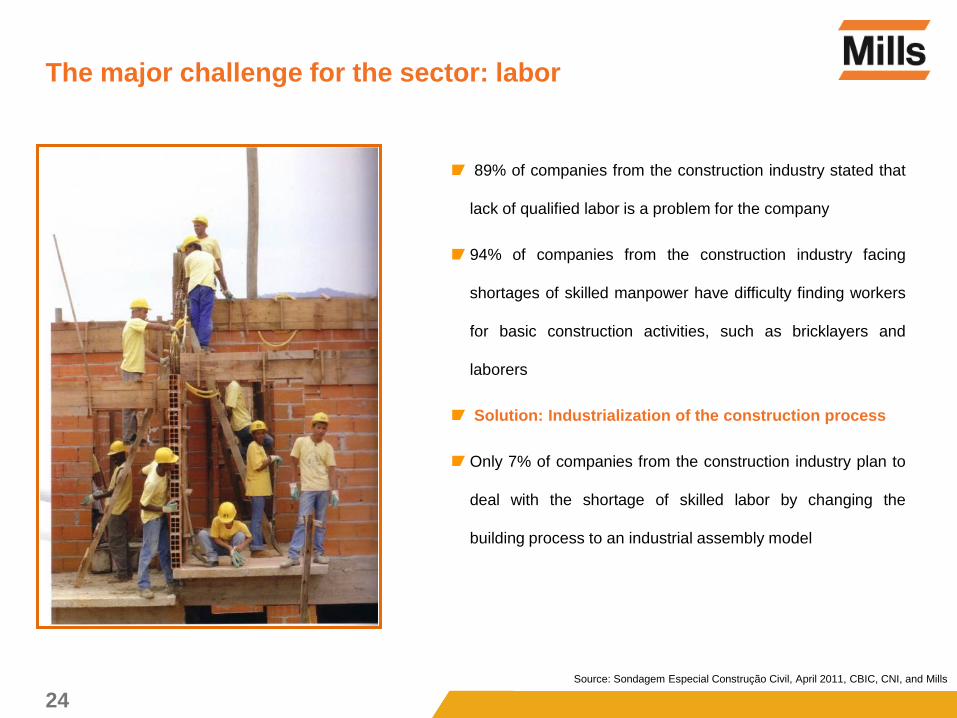

The major challenge for the sector: labor

24 Source: Sondagem Especial Construção Civil, April 2011, CBIC, CNI, and Mills

89% of companies from the construction industry stated that

lack of qualified labor is a problem for the company

94% of companies from the construction industry facing

shortages of skilled manpower have difficulty finding workers

for basic construction activities, such as bricklayers and

laborers

Solution: Industrialization of the construction process

Only 7% of companies from the construction industry plan to

deal with the shortage of skilled labor by changing the

building process to an industrial assembly model

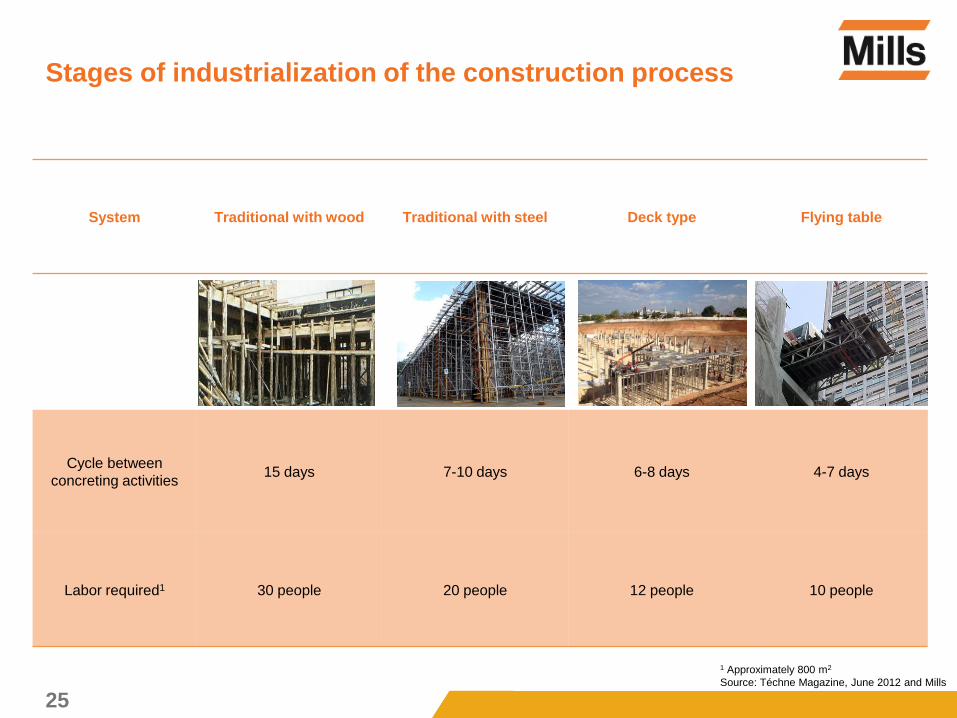

Stages of industrialization of the construction process

25

1 Approximately 800 m2

Source: Téchne Magazine, June 2012 and Mills

System Traditional with wood Traditional with steel Deck type Flying table

Cycle between

concreting activities 15 days 7-10 days 6-8 days 4-7 days

Labor required1 30 people 20 people 12 people 10 people

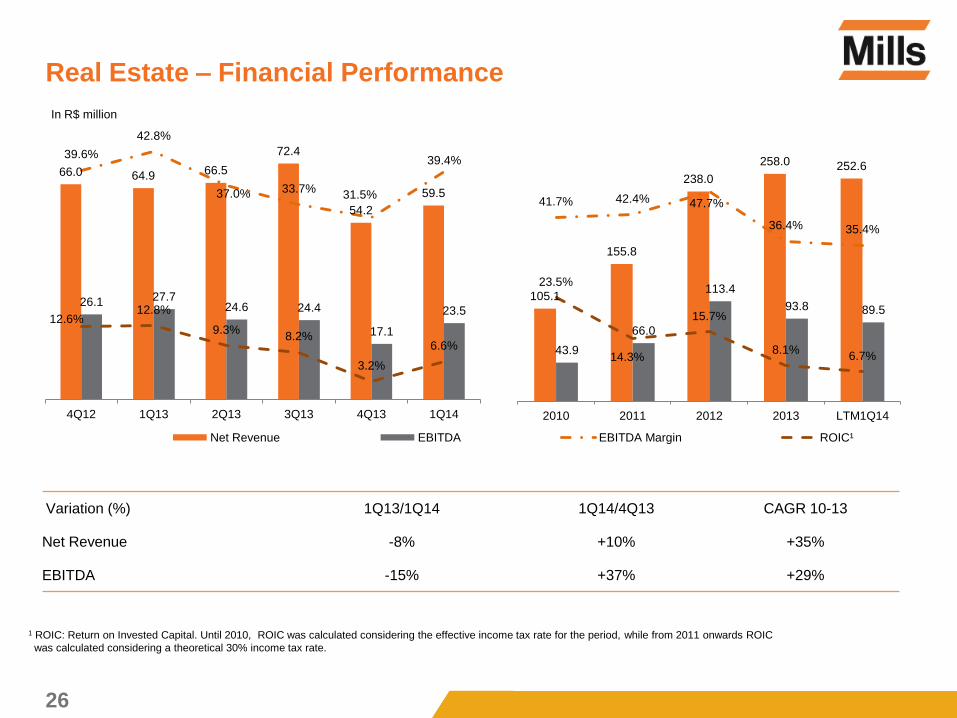

Variation (%) 1Q13/1Q14 1Q14/4Q13 CAGR 10-13

Net Revenue -8% +10% +35%

EBITDA -15% +37% +29%

Real Estate – Financial Performance

26

1 ROIC: Return on Invested Capital. Until 2010, ROIC was calculated considering the effective income tax rate for the period, while from 2011 onwards ROIC

was calculated considering a theoretical 30% income tax rate.

In R$ million

66.0 64.9 66.5

72.4

54.2

59.5

26.1 27.7 24.6 24.4

17.1

23.5

39.6%

42.8%

37.0% 33.7% 31.5%

39.4%

12.6% 12.8%

9.3% 8.2%

3.2%

6.6%

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Net Revenue EBITDA EBITDA Margin ROIC¹

105.1

155.8

238.0

258.0 252.6

43.9

66.0

113.4

93.8 89.5

41.7% 42.4% 47.7%

36.4% 35.4%

23.5%

14.3%

15.7%

8.1% 6.7%

2010 2011 2012 2013 LTM1Q14

Growth Plan

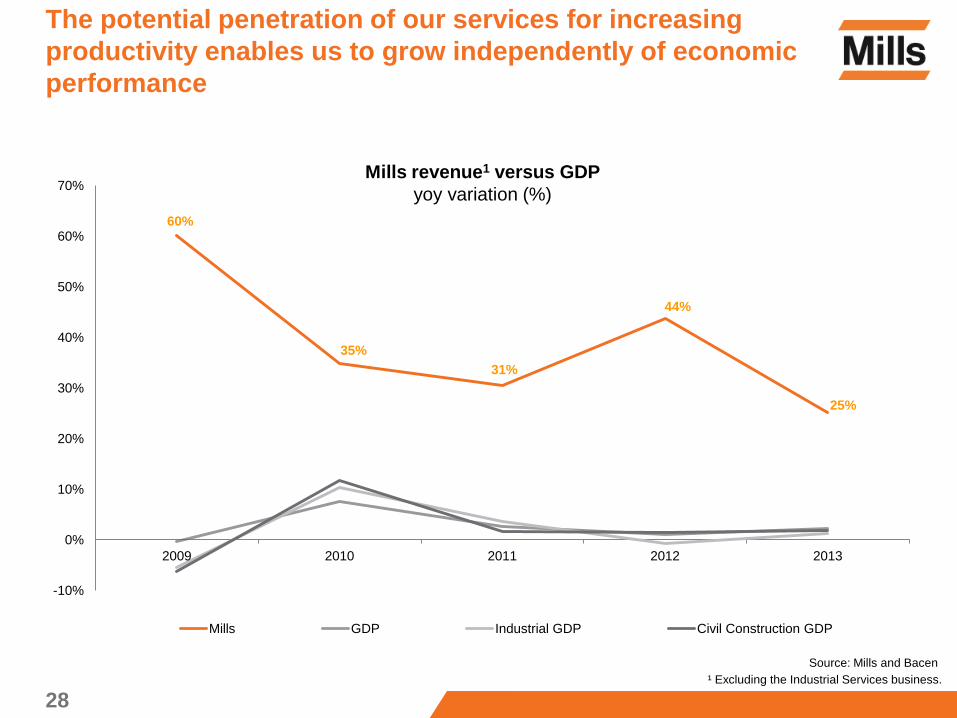

The potential penetration of our services for increasing

productivity enables us to grow independently of economic

performance

60%

35%

31%

44%

25%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

2009 2010 2011 2012 2013

Mills GDP Industrial GDP Civil Construction GDP

Source: Mills and Bacen

Mills revenue1 versus GDP

yoy variation (%)

28 ¹ Excluding the Industrial Services business.

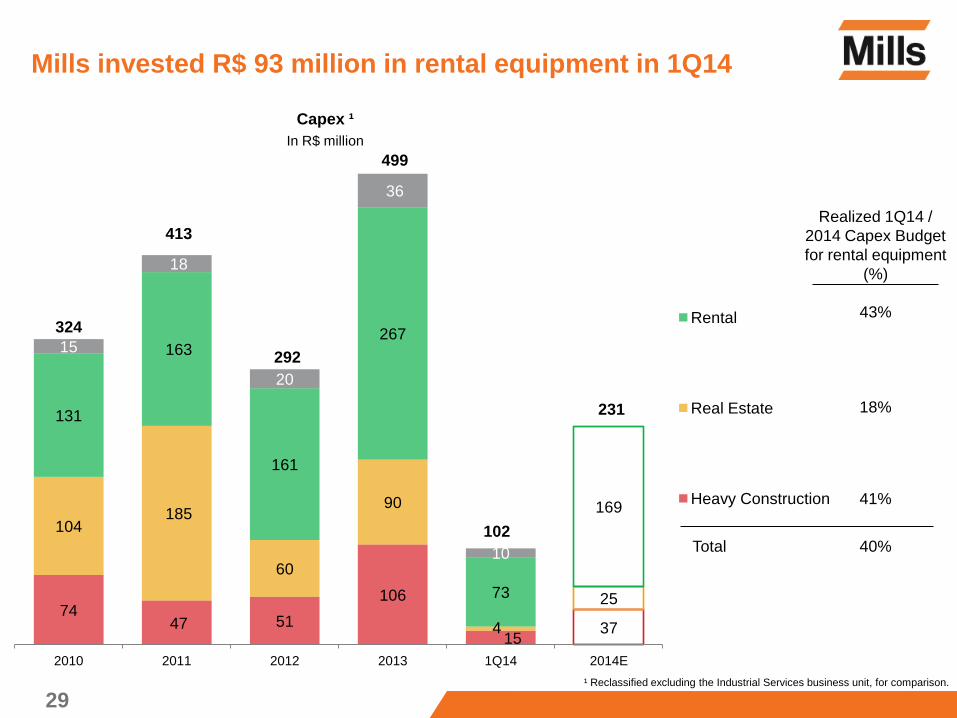

74 47 51

106

15 37

104 185

60

90

4

25

131

163

161

267

73

169

15

18

20

36

10

324

413

292

499

102

231

2010 2011 2012 2013 1Q14 2014E

Rental

Real Estate

Heavy Construction

In R$ million

Capex ¹

Realized 1Q14 /

2014 Capex Budget

for rental equipment

(%)

41%

18%

43%

Mills invested R$ 93 million in rental equipment in 1Q14

29 ¹ Reclassified excluding the Industrial Services business unit, for comparison.

Total 40%

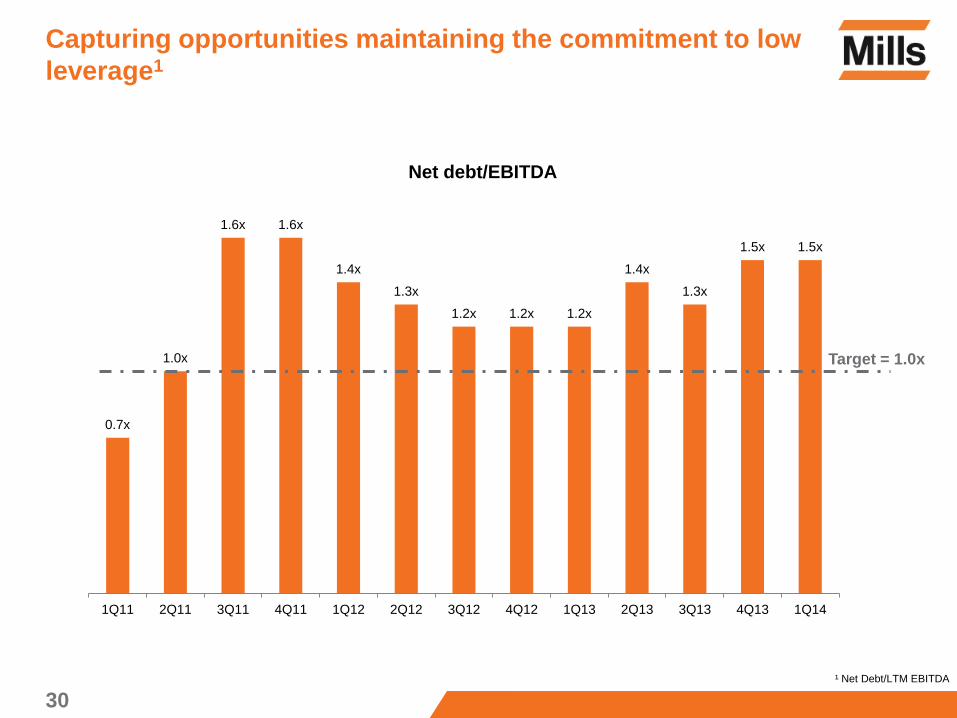

Capturing opportunities maintaining the commitment to low

leverage1

30

Net debt/EBITDA

¹ Net Debt/LTM EBITDA

0.7x

1.0x

1.6x 1.6x

1.4x

1.3x

1.2x 1.2x 1.2x

1.4x

1.3x

1.5x 1.5x

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Target = 1.0x