hsl research - hdfcsec.com

TRANSCRIPT

Date: 15 April, 2020

HSL RESEARCH

The Daily Viewpoint

Page 2HSL Research

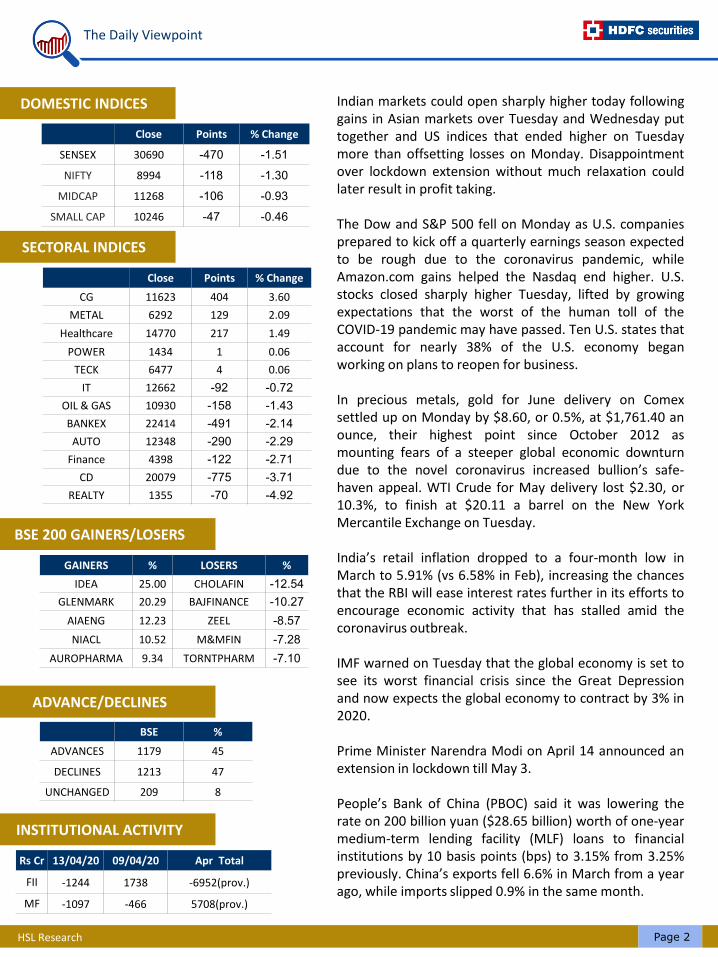

DOMESTIC INDICES

Close Points % Change

SENSEX 30690 -470 -1.51

NIFTY 8994 -118 -1.30

MIDCAP 11268 -106 -0.93

SMALL CAP 10246 -47 -0.46

SECTORAL INDICES

Close Points % Change

CG 11623 404 3.60

METAL 6292 129 2.09

Healthcare 14770 217 1.49

POWER 1434 1 0.06

TECK 6477 4 0.06

IT 12662 -92 -0.72

OIL & GAS 10930 -158 -1.43

BANKEX 22414 -491 -2.14

AUTO 12348 -290 -2.29

Finance 4398 -122 -2.71

CD 20079 -775 -3.71

REALTY 1355 -70 -4.92

BSE 200 GAINERS/LOSERS

GAINERS % LOSERS %

IDEA 25.00 CHOLAFIN -12.54

GLENMARK 20.29 BAJFINANCE -10.27

AIAENG 12.23 ZEEL -8.57

NIACL 10.52 M&MFIN -7.28

AUROPHARMA 9.34 TORNTPHARM -7.10

ADVANCE/DECLINES

BSE %

ADVANCES 1179 45

DECLINES 1213 47

UNCHANGED 209 8

INSTITUTIONAL ACTIVITY

Rs Cr 13/04/20 09/04/20 Apr Total

FII -1244 1738 -6952(prov.)

MF -1097 -466 5708(prov.)

Indian markets could open sharply higher today followinggains in Asian markets over Tuesday and Wednesday puttogether and US indices that ended higher on Tuesdaymore than offsetting losses on Monday. Disappointmentover lockdown extension without much relaxation couldlater result in profit taking.

The Dow and S&P 500 fell on Monday as U.S. companiesprepared to kick off a quarterly earnings season expectedto be rough due to the coronavirus pandemic, whileAmazon.com gains helped the Nasdaq end higher. U.S.stocks closed sharply higher Tuesday, lifted by growingexpectations that the worst of the human toll of theCOVID-19 pandemic may have passed. Ten U.S. states thataccount for nearly 38% of the U.S. economy beganworking on plans to reopen for business.

In precious metals, gold for June delivery on Comexsettled up on Monday by $8.60, or 0.5%, at $1,761.40 anounce, their highest point since October 2012 asmounting fears of a steeper global economic downturndue to the novel coronavirus increased bullion’s safe-haven appeal. WTI Crude for May delivery lost $2.30, or10.3%, to finish at $20.11 a barrel on the New YorkMercantile Exchange on Tuesday.

India’s retail inflation dropped to a four-month low inMarch to 5.91% (vs 6.58% in Feb), increasing the chancesthat the RBI will ease interest rates further in its efforts toencourage economic activity that has stalled amid thecoronavirus outbreak.

IMF warned on Tuesday that the global economy is set tosee its worst financial crisis since the Great Depressionand now expects the global economy to contract by 3% in2020.

Prime Minister Narendra Modi on April 14 announced anextension in lockdown till May 3.

People’s Bank of China (PBOC) said it was lowering therate on 200 billion yuan ($28.65 billion) worth of one-yearmedium-term lending facility (MLF) loans to financialinstitutions by 10 basis points (bps) to 3.15% from 3.25%previously. China’s exports fell 6.6% in March from a yearago, while imports slipped 0.9% in the same month.

The Daily Viewpoint

Page 3HSL Research

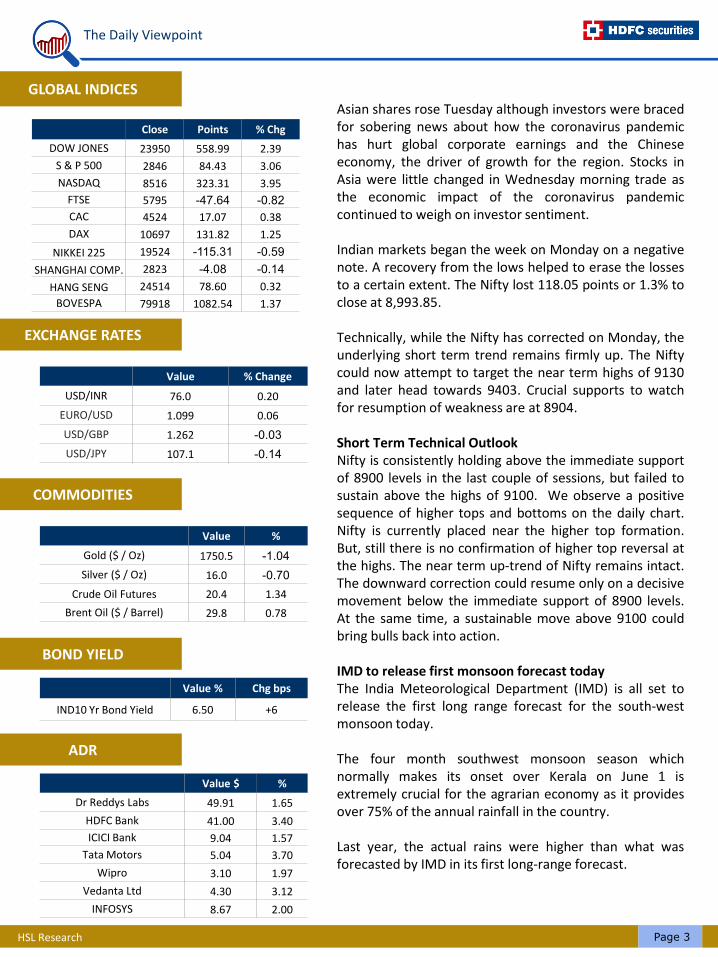

GLOBAL INDICES

EXCHANGE RATES

Value % Change

USD/INR 76.0 0.20

EURO/USD 1.099 0.06

USD/GBP 1.262 -0.03

USD/JPY 107.1 -0.14

COMMODITIES

Value %

Gold ($ / Oz) 1750.5 -1.04

Silver ($ / Oz) 16.0 -0.70

Crude Oil Futures 20.4 1.34

Brent Oil ($ / Barrel) 29.8 0.78

BOND YIELD

Value % Chg bps

IND10 Yr Bond Yield 6.50 +6

ADR

Value $ %

Dr Reddys Labs 49.91 1.65

HDFC Bank 41.00 3.40

ICICI Bank 9.04 1.57

Tata Motors 5.04 3.70

Wipro 3.10 1.97

Vedanta Ltd 4.30 3.12

INFOSYS 8.67 2.00

Close Points % Chg

DOW JONES 23950 558.99 2.39

S & P 500 2846 84.43 3.06

NASDAQ 8516 323.31 3.95

FTSE 5795 -47.64 -0.82

CAC 4524 17.07 0.38

DAX 10697 131.82 1.25

NIKKEI 225 19524 -115.31 -0.59

SHANGHAI COMP. 2823 -4.08 -0.14

HANG SENG 24514 78.60 0.32

BOVESPA 79918 1082.54 1.37

Asian shares rose Tuesday although investors were bracedfor sobering news about how the coronavirus pandemichas hurt global corporate earnings and the Chineseeconomy, the driver of growth for the region. Stocks inAsia were little changed in Wednesday morning trade asthe economic impact of the coronavirus pandemiccontinued to weigh on investor sentiment.

Indian markets began the week on Monday on a negativenote. A recovery from the lows helped to erase the lossesto a certain extent. The Nifty lost 118.05 points or 1.3% toclose at 8,993.85.

Technically, while the Nifty has corrected on Monday, theunderlying short term trend remains firmly up. The Niftycould now attempt to target the near term highs of 9130and later head towards 9403. Crucial supports to watchfor resumption of weakness are at 8904.

Short Term Technical OutlookNifty is consistently holding above the immediate supportof 8900 levels in the last couple of sessions, but failed tosustain above the highs of 9100. We observe a positivesequence of higher tops and bottoms on the daily chart.Nifty is currently placed near the higher top formation.But, still there is no confirmation of higher top reversal atthe highs. The near term up-trend of Nifty remains intact.The downward correction could resume only on a decisivemovement below the immediate support of 8900 levels.At the same time, a sustainable move above 9100 couldbring bulls back into action.

IMD to release first monsoon forecast todayThe India Meteorological Department (IMD) is all set torelease the first long range forecast for the south-westmonsoon today.

The four month southwest monsoon season whichnormally makes its onset over Kerala on June 1 isextremely crucial for the agrarian economy as it providesover 75% of the annual rainfall in the country.

Last year, the actual rains were higher than what wasforecasted by IMD in its first long-range forecast.

The Daily Viewpoint

Page 4HSL Research

Retail inflation eases to 4-month low in Mar on lower food pricesA sharp fall in vegetable prices has led India’s retail inflation to ease from 6.58% in February to a four-monthlow of 5.91% in March.

Food inflation declined from 10.81% in February to 8.76% in March because of falling onion prices. This wasreflected in vegetable inflation softening from 31.61% to 18.63% in the two-month period.

The number gives a false sense of improvement in inflation, given that the real impact of the lockdown will befelt in April as prices of food items have increased quite sharply.

In March, rural inflation at 6.09% stood higher than urban inflation at 5.66% while fuel inflation marginallyrose to 6.59% from 6.36% in February.

FTSE Russell proposes to raise India's weight in its global indicesGlobal index providers have taken note of the government’s decision to virtually increase foreign ownershipin listed companies. After MSCI, FTSE Russell has proposed to increase India’s weight on its global indices,which are tracked by funds with billions of dollars in corpus.

On Tuesday, the UK-based entity issued a new methodology to compute the weight of the country andindividual stocks in its indices.

The move could increase India’s weight on the widely-tracked emerging market (EM) indices by as much as156 basis points (bps). This could result in $2 billion of passive inflows into the Indian markets.

Wipro Q3FY20 earnings previewWhen IT major Wipro releases its March quarter earnings today, market will focus on the company’s updateon revenue growth outlook for Q1FY21, timeline for the appointment of a new CEO, work from home (WFH)measures and its impact on business and margin trajectory in view of the Covid-19 crisis.

The company is expected to report flat revenue and profit growth in Q4FY20. Wipro is expected to report 0.5per cent revenue growth on a sequential basis and 3.6 per cent on a year-on-year basis.

EBIT margin and profit after tax (PAT) are likely to expand marginally by 20 basis points and 1.3 per cent on aQoQ basis.

Hindalco closes US$ 2.8 billion acquisition of US based Aleris CorpNearly two years after signing a deal to take over Ohio-based aluminium rolled products maker Aleris Corp,Hindalco Industries finally completed the acquisition through its subsidiary Novelis Inc. The enterprise valueof the deal at $2.8 billion is slightly higher than the initial estimate of $2.58 billion, but the deal closure willnow help Hindalco leapfrog into being one of the world’s largest aluminium makers.

The Aleris deal, crucially, enables the further diversification of metals downstream portfolio into otherpremium market segments, most notably aerospace.

The Daily Viewpoint

Page 5HSL Research

As of now, the closing purchase price of $2.8 billion consists of $775 million for the equity value, as well asapproximately $2 billion for the assumption or extinguishment of Aleris’ current outstanding debt and a $50million earn-out payment. Company said that it will have potential synergy benefits of $150 million on arecurring basis.

Legacy Aleris debt levels have increased since the initial acquisition announcement due to rise in workingcapital to support the ramp up of operations, while the earn-out is related to stronger than expectedperformance by Aleris’ U.S. business.

Galaxy Surfactants updates on incident at its plantThe small intermediate feed tank blast which has taken place at Tarapur M-3 Plant has led to two fatalitiesand three injuries.

Galaxy had taken the requisite approvals to operate during the lockdown and company has been adhering toall the Central and State guidelines for operating the plant.

Biocon, Mylan launch cancer drug in AustraliaBiocon, jointly with Mylan, has launched Fulphila, a biosimilar to Neulasta (pegfilgrastim) in Australia forcancer patients.

Fulphila was the first biosimilar pegfilgrastim to be approved in the US and was launched in July 2018.

Fulphila is approved by the Therapeutic Goods Administration for the treatment of cancer patients followingchemotherapy, to decrease the duration of severe neutropenia and reduce the incidence of infections, asmanifested by febrile neutropenia.

Important news/developments to influence markets India’s Retail inflation continued to ease in March on lower food and fuel prices and a fall in demand for

non-essential items amid a nationwide lockdown to combat the coronavirus pandemic. The ConsumerPrice Index-based inflation stood at 5.91 percent in March compared with 6.58 percent in February.

Japan Mar Money Supply M2 y/y: 3.3% v 2.9%e; M3 y/y: 2.7% v 2.5%e.

The Daily Viewpoint

Page 6HSL Research

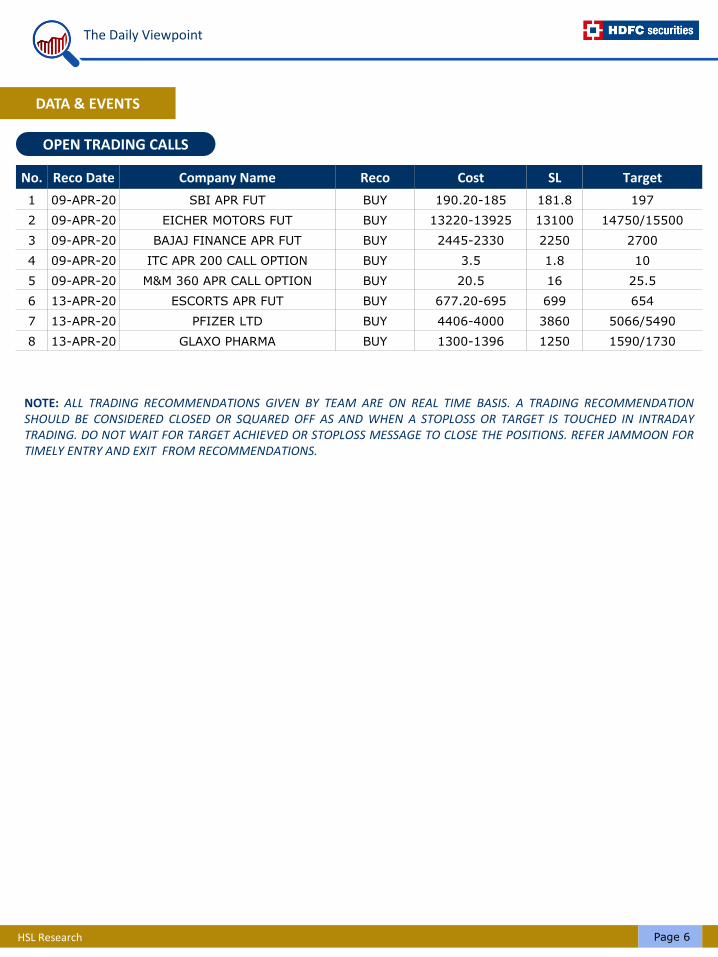

DATA & EVENTS

OPEN TRADING CALLS

NOTE: ALL TRADING RECOMMENDATIONS GIVEN BY TEAM ARE ON REAL TIME BASIS. A TRADING RECOMMENDATIONSHOULD BE CONSIDERED CLOSED OR SQUARED OFF AS AND WHEN A STOPLOSS OR TARGET IS TOUCHED IN INTRADAYTRADING. DO NOT WAIT FOR TARGET ACHIEVED OR STOPLOSS MESSAGE TO CLOSE THE POSITIONS. REFER JAMMOON FORTIMELY ENTRY AND EXIT FROM RECOMMENDATIONS.

No. Reco Date Company Name Reco Cost SL Target

1 09-APR-20 SBI APR FUT BUY 190.20-185 181.8 197

2 09-APR-20 EICHER MOTORS FUT BUY 13220-13925 13100 14750/15500

3 09-APR-20 BAJAJ FINANCE APR FUT BUY 2445-2330 2250 2700

4 09-APR-20 ITC APR 200 CALL OPTION BUY 3.5 1.8 10

5 09-APR-20 M&M 360 APR CALL OPTION BUY 20.5 16 25.5

6 13-APR-20 ESCORTS APR FUT BUY 677.20-695 699 654

7 13-APR-20 PFIZER LTD BUY 4406-4000 3860 5066/5490

8 13-APR-20 GLAXO PHARMA BUY 1300-1396 1250 1590/1730

The Daily Viewpoint

Page 7HSL Research

Disclaimer:This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The informationand opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believedto be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, ismade as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. Thisdocument is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are notintended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell anysecurities or other financial instruments.This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person orentity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication,reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration orlicensing requirement within such jurisdiction.If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and broughtto the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior writtenapproval of HSL.Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have anadverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values ofwhich are influenced by foreign currencies effectively assume currency risk.It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, orperform broking, or other services for, any company mentioned in this mail and/or its attachments.HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buyor sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earnbrokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act asan advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to anyrecommendation and other related information and opinions.HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustaineddue to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices ofshares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc.HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities andfinancial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may dealin other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have beenmandated by the subject company for any other assignment in the past twelve months.HSL or its associates might have received any compensation from the companies mentioned in the report during the period precedingtwelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance,investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normalcourse of business.HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party inconnection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict ofinterest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking,investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach differentconclusion from the information presented in this report.Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer,director or employee of the subject company. We have not received any compensation/benefits from the subject company or thirdparty in connection with the Research Report.

HDFC securities Limited, SEBI Registration No.: INZ000186937 (NSE, BSE, MSEI, MCX) |NSE Trading Member Code: 11094 | BSEClearing Number: 393 | MSEI Trading Member Code: 30000 | MCX Member Code: 56015 | AMFI Reg No. ARN -13549, PFRDA Reg. No- POP 04102015, IRDA Corporate Agent Licence No.-HDF2806925/HDF C000222657 , Research Analyst Reg. No. INH000002475, CIN-U67120MH2000PLC152193. Registered Address: I Think Techno Campus, Building, B, Alpha, Office Floor 8, Near Kanjurmarg Station,Kanjurmarg (East), Mumbai -400 042. Tel -022 30753400. Compliance Officer: Ms. Binkle R Oza. Ph: 022-3045 3600 Email:[email protected].

Mutual Funds Investments are subject to market risk. Please read the offer and scheme related documents carefully before investing.