hungary - international university of japan territory at the second battle of mohacs in 1687,...

TRANSCRIPT

Country Profile 2003

HungaryThis Country Profile is a reference work, analysing thecountry�s history, politics, infrastructure and economy. It isrevised and updated annually. The Economist IntelligenceUnit�s Country Reports analyse current trends and provide atwo-year forecast.

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where itslatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

Copyright© 2003 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-6061

Symbols for tables�n/a� means not available; �-� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

Hungary 1

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

Contents

3 Basic data

4 Politics4 Political background5 Recent political developments8 Constitution, institutions and administration10 Political forces15 International relations and defence

18 Resources and infrastructure18 Population19 Education20 Health22 Natural resources and the environment23 Transport, communications and the Internet24 Energy provision

27 The economy27 Economic structure28 Economic policy35 Economic performance38 Regional trends

38 Economic sectors38 Agriculture40 Mining and semi-processing40 Manufacturing42 Construction43 Financial services45 Other services

45 The external sector45 Trade in goods47 Invisibles and the current account48 Capital flows and foreign debt49 Foreign reserves and the exchange rate

51 Appendices51 Membership of regional organisations53 Sources of information54 Reference tables55 Labour force55 Transport statistics55 Structure of energy sources (production plus imports)56 Central state budget56 Money supply57 Gross domestic product57 Gross domestic product by expenditure58 Gross value added by sector58 Prices58 Volume indices of sales of agricultural products

2 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

59 Livestock numbers59 Output of energy, minerals and mineral products59 Industrial production by sector60 Construction60 Budapest Stock Exchange60 Retail sales61 Imports61 Main trading partners62 Balance of payments63 External debt, World Bank estimates64 Foreign reserves64 Exchange rates

Hungary 3

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

Hungary

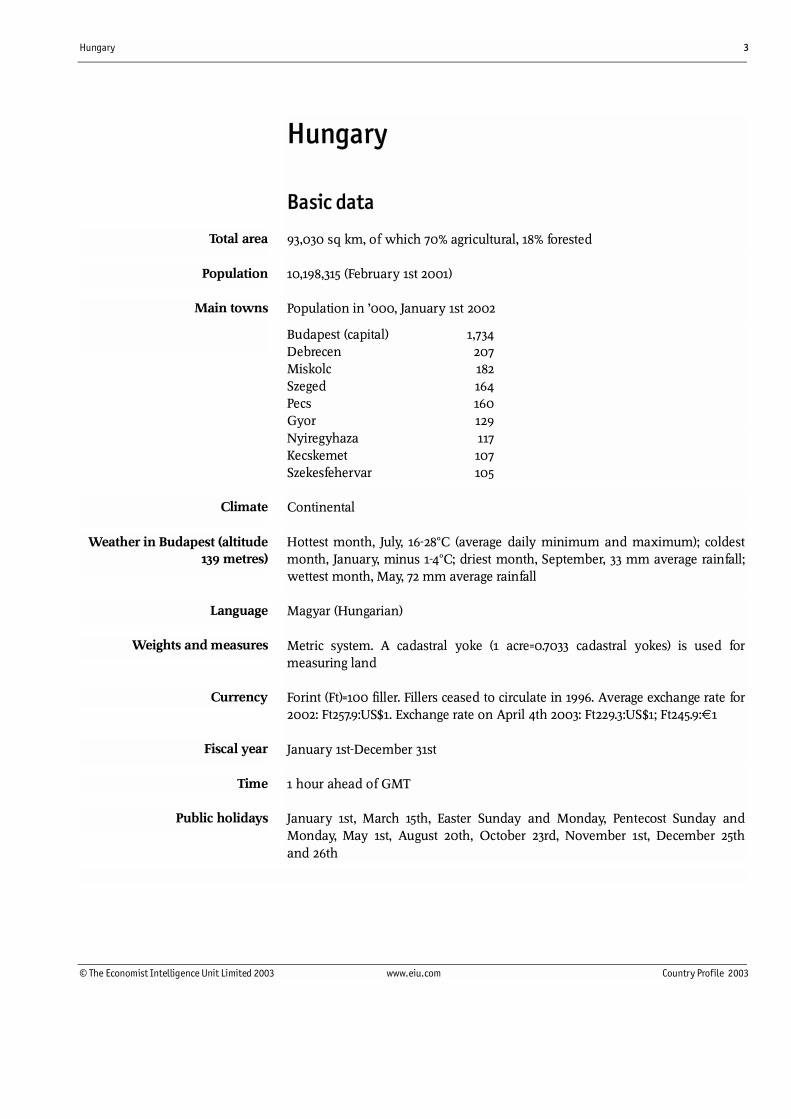

Basic data

93,030 sq km, of which 70% agricultural, 18% forested

10,198,315 (February 1st 2001)

Population in �000, January 1st 2002

Budapest (capital) 1,734Debrecen 207Miskolc 182Szeged 164Pecs 160Gyor 129Nyiregyhaza 117Kecskemet 107Szekesfehervar 105

Continental

Hottest month, July, 16-28°C (average daily minimum and maximum); coldestmonth, January, minus 1-4°C; driest month, September, 33 mm average rainfall;wettest month, May, 72 mm average rainfall

Magyar (Hungarian)

Metric system. A cadastral yoke (1 acre=0.7033 cadastral yokes) is used formeasuring land

Forint (Ft)=100 filler. Fillers ceased to circulate in 1996. Average exchange rate for2002: Ft257.9:US$1. Exchange rate on April 4th 2003: Ft229.3:US$1; Ft245.9:€1

January 1st-December 31st

1 hour ahead of GMT

January 1st, March 15th, Easter Sunday and Monday, Pentecost Sunday andMonday, May 1st, August 20th, October 23rd, November 1st, December 25thand 26th

Total area

Population

Weights and measures

Currency

Fiscal year

Time

Public holidays

Main towns

Climate

Language

Weather in Budapest (altitude139 metres)

4 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

Politics

The head of state is the president, currently Ferenc Madl, who was elected byparliament for a five-year term on June 6th 2000, although power rests mostlywith parliament. A centre-left coalition government, comprising the HungarianSocialist Party and the liberal Alliance of Free Democrats, took office in May2002, and is led by the prime minister, the Socialists� Peter Medgyessy. TheSocialists and Free Democrats also co-operated in government in 1994-98 andreplace a right-of-centre coalition, led by the Fidesz-Hungarian Civic Party(commonly referred to as �Fidesz�). Since the end of communist rule, reform-minded centre-right and centre-left coalitions have alternated in power.

Political background

Magyar tribes from the region between the Volga, Kama and Belaya rivers andthe Ural mountains, now in Russia, settled in the Carpathian Basin towards theend of the ninth century. The date of settlement is traditionally commemoratedas 896. The foundation of the Hungarian state is dated to 1000, when King(later Saint) Stephen also adopted Christianity. The medieval Hungariankingdom suffered a catastrophic defeat at the hands of the Ottomans in thebattle of Mohacs in 1526 and was partitioned between Austria, the Ottomansand a nominally independent Transylvania. The Austrians drove the Turks fromHungarian territory at the second battle of Mohacs in 1687, allowing Austria totake control of all of Hungary under the 1699 Treaty of Karlowitz.

National and social tensions under Austrian rule led to a nationalist/liberaluprising as part of the pan-European 1848 revolutions. Lajos Kossuthestablished an independent national government, but this was crushed in 1849with Russian help. However, the Compromise (Ausgleich) of 1867 reorganisedthe Habsburg empire as the Dual Monarchy of Austria and Hungary, allowingMagyar domination of Hungarian lands and German domination of Austrianlands, with Slav-inhabited areas divided between the two. The last quarter ofthe nineteenth century saw political stability, an economic boom and muchsocial and infrastructural modernisation, with the newly-unified Budapestacquiring many of its major public buildings.

The military defeat of the Austro-Hungarian monarchy in 1918 led to a dramaticreduction in the area and population of Hungary. The 1920 Trianon Treatyreduced Hungary�s territory from 288,000 sq km to 93,000 sq km, and thepopulation from 18.2m to 7.6m, leaving sizeable Hungarian minorities inneighbouring Czechoslovakia, Romania and the future Yugoslavia. Acommunist-dominated revolutionary government in March-August 1919 gaveway to a long period of conservative rule under the regency of Admiral MiklosHorthy. In the 1930s Hungary grew increasingly close to Germany, allying itselfwith the Nazi power in the hopes of regaining territory from Czechoslovakia,Romania and Yugoslavia. It allied itself with the German side in the secondworld war. Germany occupied Hungary from March 1944 until the Soviet RedArmy pushed out its troops in early 1945.

Early history

Austro-Hungary

Hungary 5

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

A free election in November 1945 resulted in a majority for the Smallholders�Party, but another�this time flawed�election in 1947 gave the largest vote shareto the Communist Party, which established one-party rule and nationalisedproperty. Stalinism dominated Hungary until 1953. A revolution began inBudapest on October 23rd 1956. The reform communist prime minister, ImreNagy, declared Hungary�s neutrality and withdrawal from the Warsaw Pact,prompting a Soviet Red Army invasion on November 4th. By mid-December allresistance had been crushed and Janos Kadar, the general secretary of therestyled Hungarian Socialist Workers� Party (MSZMP), began the task ofpolitical consolidation.

The regime relaxed its political stance somewhat from the early 1960s onwards,with a final amnesty for the revolutionaries declared in March 1963. In 1968Hungary introduced the New Economic Mechanism, a reform packagedesigned to increase enterprise autonomy and the role of markets in economicdecision-making. The more liberal system resulted in a boom in agriculturaland consumer goods production, but income inequality increased and globalrecessions following the 1973 and 1979 oil price shocks undermined the reformefforts. Worsening terms of trade, combined with excessive imports of Westerntechnology and consumption goods, increased the country�s foreign debt toalmost US$11bn by the early 1980s. Signs of social difficulties appeared, such asthe start of population decline on the back of high death and low birth rates.

Recent political developments

When the 13th Congress of the MSZMP in 1985 failed to bring substantialchanges in policy, unrest among reformers within the party and state apparatusbegan to increase. Karoly Grosz replaced Mr Kadar as general secretary of theMSZMP in May 1988, and reformists (led by Imre Pozsgay and the architect ofthe 1968 economic reform, Rezso Nyers) gained control of the party in 1989. Theprime minister, Miklos Nemeth, also enacted political liberalisation. In adramatic break with the past, Imre Nagy, who had been secretly executedfollowing the 1956 revolution, was given a public funeral and reburial in June1989. The MSZP joined with opposition groups in national roundtablenegotiations about establishing democracy and, in October 1989, transformeditself into the Hungarian Socialist Party.

Post-communist Hungary has benefited from a high level of political stability.Despite often bitter conflict between government and opposition, democraticprocedures have become accepted and ensure a smooth and orderly transfer ofpower. The four democratic parliamentary elections since 1990 have eachbrought changes in direction�an alternation between centre-right and centre-left�with all three previous governments retaining a working majority andserving out their four-year term. The current Socialist-liberal coalition lookslikely to do the same. Party politics has also been relatively stable, with all fourparties represented in the current parliament present in the legislature since1990. Political stability has been reinforced by negotiations for EU membershipsince 1998 and accession to NATO in March 1999.

The communist takeover

Post-communist Hungary

End of the communist era

6 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

In the March-April 1990 parliamentary election the opposition HungarianDemocratic Forum emerged as the most popular party and formed a coalitiongovernment with two other conservative parties, the IndependentSmallholders� Party and the Christian Democratic People�s Party. The liberalparties, the Alliance of Free Democrats and the Federation of Young Democrats(Fidesz), joined the Socialists in opposition. Jozsef Antall, the president of theHungarian Democratic Forum, became the prime minister and made a post-election deal with the Free Democrats that increased his powers, as well aseliminating the two-thirds majority requirement on most legislation. Althoughthe government set some important institutional reforms in motion, in 1993-94it pursued an undisciplined spending programme that left the budget in severedeficit and had a negative effect on the current-account deficit.

The May 1994 election returned the Socialists to power. Despite having anabsolute majority, the Socialists formed a coalition government with the FreeDemocrats. The government introduced an austerity programme (the �BokrosPackage�) in March 1995 designed to curb the government deficit and theexternal account imbalances. Economic growth decelerated and real wages fellsharply as a result, but by 1997 the government�s policies began to yield results,with real GDP growth hitting a post-communist high. However, economicrecovery came too late for the Socialist-led government, which was punishedby voters for the effects of its earlier austerity measures. Fidesz�which by thistime had added the Hungarian Civic Party to its official name and had evolvedinto a right-of-centre party�emerged the clear winner in the 1998 parliamentaryelection and formed a new coalition government with two other right-wingopposition parties, the Hungarian Democratic Forum and the IndependentSmallholders� Party. Like both its predecessors, this government served out itsfour-year term, while continuing with economic reform.

The April 2002 parliamentary election resulted in another change ingovernment, but only after an emotional and often negative campaign�dominated by the Socialists and Fidesz�divided the country sharply betweenleft and right. The Socialists and the Free Democrats, which had formed anelection alliance, emerged after the second and final round of the election witha slim, ten-seat majority in Hungary�s 386-seat parliament. Two parties from theprevious, conservative government, Fidesz and the Hungarian DemocraticForum, went into opposition. No other party won more than 5% of the vote,the threshold for parliamentary representation.

Local elections in October 2002 and the tactics of the right ensured thatHungarian society remained highly politicised for most of 2002. As well asraising doubts about the validity of the April election results, albeit withoutever challenging them directly, Viktor Orban, the prime minister in the1998-2002 government and de facto leader of Fidesz, encouraged grassrootsorganisations�the so-called civic circles�to take to the streets and demonstrateagainst the Socialist-led government. Demonstrations reached a peak in themiddle of the year, which also saw the emergence of a controversy, centring onthe past of the new prime minister, Peter Medgyessy. The opposition pressrevealed that Mr Medgyessy was a counter-intelligence officer in the secret

Power alternates betweencentre-right and centre-left

Bruising election politicisesHungarian society in 2002

Hungary 7

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

service of the former communist regime. Subsequent investigations seemed toback up Mr Medgyessy�s account of his past�he never spied on any fellowHungarians�while also implicating politicians from previous governments,both centre-left and centre-right.

Despite Mr Orban�s tactics and the revelations concerning Mr Medgyessy�s past,support for the government grew steadily throughout most of the year,culminating in a landslide victory in the October local elections. This, alongwith the successful completion of EU accession negotiations in December,strengthened the hand of the government at the national level and sent theopposition into disarray, from which it has yet to recover. Despite its slimmajority, the Socialist-liberal government looks likely to serve out its term,which runs until mid-2006.

Important recent events

July 1997

Hungary is invited to begin accession negotiations with the EU and NATO. EUaccession negotiations begin in 1998.

May 1998

The Fidesz-Hungarian Civic Party (Fidesz) wins the general election and forms aright-wing coalition government under Viktor Orban.

March 1999

Hungary, the Czech Republic and Poland join NATO.

January 2001

Industrial trade with the EU becomes fully liberalised.

May 2001

Preparations begin for full convertibility of the forint, after the currency�s exchange-rate bands are widened.

October 2001

The forint becomes fully convertible.

April 2002

The Hungarian Socialist Party wins the general election and forms a centre-leftcoalition government under Peter Medgyessy.

December 2002

Hungary completes accession negotiations with the EU and receives a formalinvitation to join at the EU�s Copenhagen summit.

December 2002

The government permits the US to train members of the Iraqi opposition at theTaszar air base.

January 2003

Mr Medgyessy signs the �Gang of Eight� letter in support of US policy on Iraq,joining leaders from the UK, Spain, Italy, Portugal, Denmark, Poland and theCzech Republic.

8 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

March 2003

The government permits US-led coalition forces to use Hungarian airspace and airbases as part of the war in Iraq.

April 2003

Hungarians vote overwhelmingly in favour of EU membership in a referendum..

Constitution, institutions and administration

The constitution is a heavily amended version of the communist constitutionintroduced in 1949. A multiparty committee worked on a comprehensive newconstitution between 1994 and 1998, but divisions between parties and withinthe government prevented parliament from approving a new document. Thereis no state religion, but recognised religions receive state funding. Hungary is aparliamentary democracy with a single-chamber National Assembly.

The electoral system is complex, combining elements of majority andproportional voting. Of the 386 seats in the National Assembly, 176 are electedfrom individual electoral constituencies, where voters cast two votes in the firstround, one for the local MP by name, and one for the local party list. Anabsolute majority is required for election to an individual district in the firstround. The top three candidates, or all candidates achieving more than 15% inthe first round, advance to the second round of voting, where a pluralitysuffices for victory. Candidates are not required to reside in the district in whichthey run. The remaining 210 seats are distributed proportionally after the firstround according to the party-list vote�a maximum of 152 seats on the basis oflocal party lists, with a national list (for which citizens do not vote) operating asa top-up mechanism. In 1990 there was a 4% minimum threshold (of the party-list vote) for parties to enter parliament. The threshold was raised to 5% beforethe 1994 election.

The president, elected by parliament for a five-year term, has few formalpowers. The position is responsible for the nomination of certain posts, but islargely ceremonial. Mr Madl took office in August 2000. The constitutionpermits a maximum of two terms.

Until recently the judiciary was a three-tier system, involving local, county andhigh courts. A 1997 constitutional amendment added an additional tier, a courtof appeal, but the 1998-2002 government failed to provide funding for itsimplementation. In accordance with constitutional requirements, the presentgovernment established in June 2002 five regional courts of appeal, which willhear appeals to county court decisions that are currently being heard by theSupreme Court. The regional courts of appeal will begin operating in July 2003(2004 for the courts in Gyor and Debrecen) and are expected to help toalleviate the serious backlog of cases currently before the Supreme Court. Thereis also a Constitutional Court, which is modelled on the powerful Germanmodel and has been highly activist. It has the power to review and invalidateparliamentary acts.

Reform of the legal system has generally been based on west European norms,with a view to preparing the judiciary for EU entry. In its progress reports the

The president and judiciary

Hungary 9

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

European Commission has noted that although the judiciary functionssatisfactorily and the training of judges in EU law has progressed�nearly three-quarters of all judges have received training�there are still many problemareas, related primarily to a lack of budgetary resources. The previous, Fidesz-led government was particularly prone to cutting spending proposals needed tobring the judiciary up to Western levels. Low pay remains a problem, and thewhole system is handicapped by the lack of adequate investment in buildingsand information systems. Staff numbers are still insufficient to keep up withincreasing caseloads.

The current government has taken steps to address the pay issue, and byestablishing the regional courts of appeal it has removed a major hurdle toincreased efficiency. It is also in the process of finalising legislation that wouldincrease the judiciary�s financial independence. According to the Commission�slast progress report, �the constitutional and legislative guarantees of judicialindependence are well-established in Hungary and the system of judicial self-administration functions efficiently�.

Despite extensive formal decentralisation to the local level, the central govern-ment retains strong powers. Local governments are small and fragmented,numbering over 3,000, and remain heavily dependent on the centre for funds.The 19 county governments (and the Budapest city government) are directlyelected but lack policymaking and fund-raising powers. The seven new regionalbodies set up to participate in EU structural fund programmes are purelyadministrative, lack independent funds and consist of government appointeesand local delegates. Under the 1993 minority rights law, there are national and,where relevant, local governments for ethnic minorities.

The national government centres on a powerful position of prime minister. Theprime minister can be replaced only by a so-called positive vote of noconfidence, which requires the naming of an alternative candidate at the time ofthe vote. Individual ministers in the government are not subject to parliamen-tary votes of confidence, but only to the prime minister�s authority. Ministriescan be powerful through the use of orders and decrees to implement policy. Thetraditionally conservative Ministry of Finance is regarded as first among equalsamong the ministries (although its status was downgraded momentarily duringthe Fidesz administration, in favour of the Ministry of Economy and Transport).

The use of close personal networks in policymaking and administration iscommon and probably inevitable in a country with such a small elite.Government is still seen to some extent as an opportunity for patronage. Thevarious ombudsmen and the State Audit Office have achieved a goodreputation for independence.

Policymaking in the current cabinet

A greater emphasis on consensus

An important aspect of the cabinet under Peter Medgyessy, the current primeminister, is that its power is less centralised than under the previous government.Under the previous, conservative administration, there was often debate on issues ofpolicy within the government, but these nearly always came to an immediate end

Central and local government

10 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

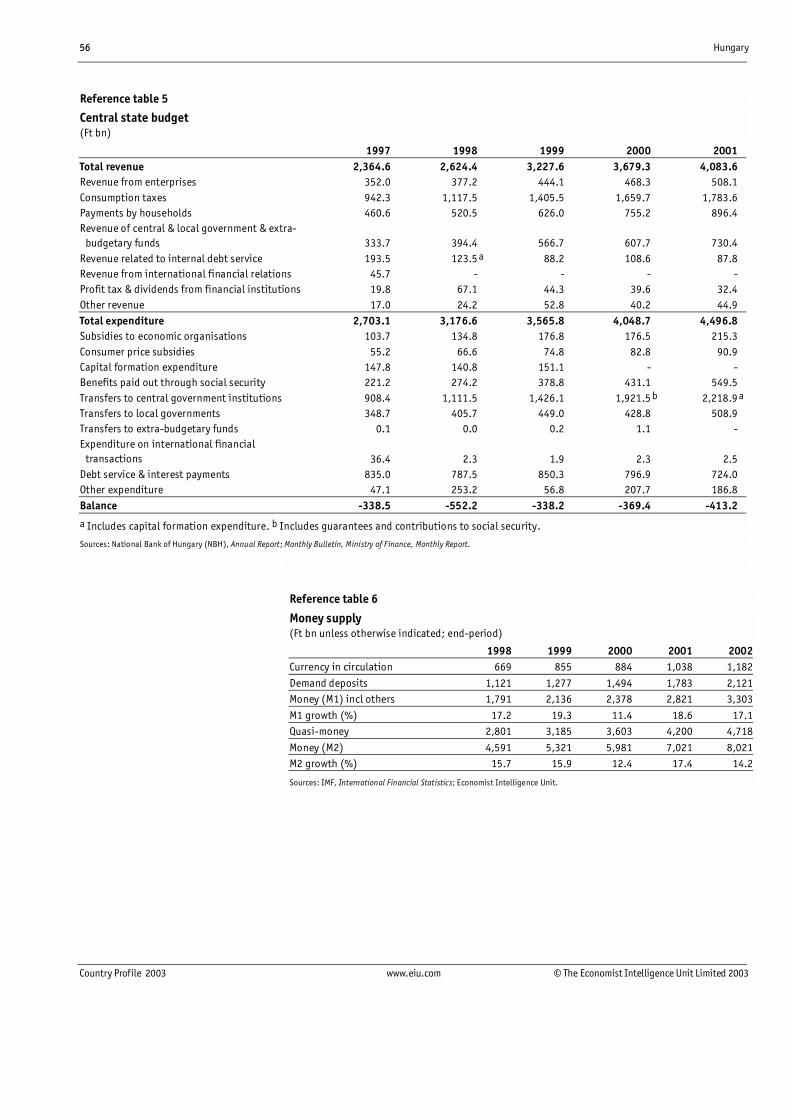

once the then prime minister, Viktor Orban, took a public stand on an issue. Bycontrast, Mr Medgyessy does not wield the strong �final arbiter� role of hispredecessor, preferring a more participatory, consensus-based management style.The epicentre of the government�s economic policy is the Ministry of Finance, andthe seemingly omnipresent finance minister, Csaba Laszlo, takes a hands-on role.The influence of Mr Laszlo, ostensibly a fiscal moderate, has been demonstrated inbudget plans that see the fiscal deficit being slashed to just 3% of GDP by 2006. Thisdid not keep him, however, from supporting the government�s expansionary first�100 days� programme, which shows he is not above putting state funds to workfor political ends. Although favouring anti-inflationary policies, Mr Laszlo placesgreater stress on growth and a reduction in state price intervention. He has alsosucceeded in gaining the acquiescence of the National Bank of Hungary (NBH, thecentral bank) for a 2007-08 target date for joining European economic and monetaryunion (EMU), rather than the bank�s preferred date of 2006. He is likely to haveplayed a behind-the-scenes role in the NBH�s recent decision to abandon inflation-targeting temporarily.If Mr Laszlo and his finance ministry is instrumental in setting the financialframework for government policy, much of the implementation is left in the handsof Istvan Csillag, who heads the Ministry of Economy and Transport. This isparticularly true of areas of public-private importance�in particular, the regulatoryenvironment, investment incentives, promotion of small and medium-sizedenterprises (SMEs), and infrastructure development. Mr Csillag was delegated by theliberal Alliance of Free Democrats. Like his predecessors at the head of the economyministry, Gyorgy Matolcsy and Attila Chikan, Mr Csillag comes from a moreacademically oriented background as a research economist.The policy role of the Prime Minister�s Office (PMO), unofficially known as theChancellery, should not be underestimated. The PMO has an immense institutionalrole and is responsible for inter-ministerial co-ordination on all aspects of thegovernment�s programme, and has primary responsibility in the areas of governmentthat do not fall under the aegis of other ministries. One of its main duties will be toco-ordinate all matters relating to the use of EU funds, giving it and the responsibleofficials wide-ranging power over the purse strings. In addition, the PMO overseesthe state privatisation agency, APV. It was led, until recently, by Elemer Kiss�likeMr Csillag, not a member of any party�who resigned in February when it wasrevealed that his law firm had illegally won a tender from Malev, the national airline,which is administered by the APV. He has been replaced by Peter Kiss (no relation).Although Mr Medgyessy is prime minister, he is not a member of the HungarianSocialist Party. The highest-ranking party official in the government is thereforeLaszlo Kovacs, the foreign minister and also party president. He and his Ministry ofForeign Affairs thus play an important role in the current cabinet, with Mr Kovacsserving as the Socialists� voice in government. In the event that Mr Medgyessy wereunable to continue in office for any reason, Mr Kovacs would probably becomeprime minister.

Political forces

Hungarian public life is strongly polarised around a historically and culturallyrooted split between the left and the right. In the Hungarian context, the liberalFree Democrats are in effect on the left, because of their internationalist,

Political polarisation

Hungary 11

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

universalist and progressive outlook. Government-opposition conflict is oftenbitter, but opposition parties have sometimes been willing to co-operate overmore technical issues of bipartisan concern. Under normal circumstances, theneed for a two-thirds majority to amend some laws can give the oppositionsome leverage.

The Hungarian Socialist Party, the name the ruling MSZMP adopted in October1989 after agreeing to democratic politics, has steadily transformed itself into atraditional social-democratic party. Under the leadership of the former MSZMP�sreformist wing, the party received only 11% of the proportional vote in 1990 andwent into opposition. After the election the former foreign minister, Gyula Horn,became party chairman and united the party�s various factions: liberaleconomists who sought radical reform of the state-centred economy, socialdemocrats, trade unionists and middle- and lower-level officials from theprevious regime. Mr Horn led the Socialists to victory in the 1994 election.Austerity measures implemented by the Socialist-led government provokedpopular dissatisfaction with the party, dooming it to defeat in the 1998 election.Mr Horn retired and was replaced by his protégé, Laszlo Kovacs (the foreignminister in both the previous and the current Socialist-led governments).Unable to expand the Socialists� appeal among voters, Mr Kovacs remained asparty leader but stepped aside in June 2001 to allow Peter Medgyessy to benominated as the party�s compromise candidate for the post of prime minister.Mr Medgyessy, who was a finance minister for part of the 1994-98administration and is not even a member of the party, led the Socialists tovictory partly by moving their policies ever closer to the centre. The party hasrecently considered changing its name to the Hungarian Social Democratic Party,another signal of the continued marginalisation of the party�s traditional tradeunionist wing in favour of those espousing a more liberal view of the economy.

The Fidesz-Hungarian Civic Party (commonly known as Fidesz), the seniorgovernment party in 1998-2002, is the main right-wing force in Hungary. It wasformed in 1988 by students in the law faculty at Budapest�s Eotvos University.During the conservative government of 1990-94, Fidesz espoused a liberalideology and often co-operated with the Free Democrats in opposition. Underthe leadership of Viktor Orban, the party began to transform itself into aconservative party, which resulted in the departure of its more liberal leaders in1993. Remaining in opposition after the 1994 election, Mr Orban made attemptsto broaden the party�s appeal. Having already dropped its upper age limit of 35in 1993, Fidesz added Hungarian Civic Party to its name in 1995. The same year,in effort to change its image as a �youth� movement, the party officiallydropped �Federation of Young Democrats� from its name, adopting instead itsHungarian acronym �Fidesz�.

Mr Orban became prime minister after Fidesz�s victory in the May 1998election, but his abrasive style of governing corresponded with a fall in theparty�s popularity. Nevertheless, Mr Orban and Fidesz pursued an increasinglypopulist and confrontational style of politics that energised right-wing votersbut also limited the party�s ability to reach out beyond its core supporters. Sincegoing into opposition after a close defeat in April 2002, those who are

Hungarian Socialist Party

Fidesz-Hungarian Civic Party

12 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

sympathetic to the party�s message have shown little compunction abouttaking to the streets in protest against the current government�s policies.Mr Orban relinquished the party leadership in 1999, but he remains Fidesz�s defacto leader and is tipped to return as party president in May 2003. Like theSocialists, Fidesz has considered a name change, as it continues its quest toconsolidate the right under its auspices.

The Alliance of Free Democrats is the country�s main liberal party. It has itsroots in the dissident democratic opposition of the 1980s, which was prominentin the political transformation of 1988-89. In the 1990 election the FreeDemocrats finished a strong second to the Hungarian Democratic Forum. In1994 the Free Democrats again finished second, but entered what turned out tobe a difficult coalition with the Socialists, who did not need the liberals�support to stay in government. By the 1998 election the party�s support haddropped substantially and has subsequently failed to recover. Some voters,especially those with ties to the dissident movement under the previousregime, have never forgiven the Free Democrats for entering into governmentwith a party descended from the communists. However, in current politicalcircumstances, the Socialists remain the party�s natural partner, and the twohave once again formed a ruling coalition, although this time more of apartnership of equals than the 1994-98 coalition. The Free Democrats draw theirmain support from wealthier, well-educated urban voters, which explains theirhold on the Budapest mayoralty, with Gabor Demszky in the post since 1990.Mr Demszky�s attempt to combine his Budapest post with the party leadershipin 2001 was unhappy and short-lived; the party leadership has now reverted toformer interior minister Gabor Kuncze.

Once the leading force in government, but now a minor partner of Fidesz onthe right, the Hungarian Democratic Forum was formed in 1987 by a group ofpopulist-oriented intellectuals and cultural figures. As prime minister and partyleader, Jozsef Antall consolidated control over the party and moved it awayfrom its more populist roots and towards a more conservative and ChristianDemocratic profile. This change angered many radicals within the DemocraticForum, which had difficulty regaining unity after the expulsion of one of itsfounders, the ultra-nationalist Istvan Csurka, and the subsequent death ofMr Antall. After a heavy defeat in the 1994 election, many moderates left toform their own party.

The Hungarian Democratic Forum�s political viability is totally beholden to itsalliance with Fidesz. Without Fidesz co-operation the party would not havesecured a presence in the 1998-2002 parliament�it failed to gain representationbased on the proportional party-list vote in the 1998 election. For the 2002election the Democratic Forum abandoned all hope of achieving parliamentaryrepresentation alone and in effect merged with Fidesz for electoral purposes, asthe two parties stood on the first joint regional lists in Hungary�s post-communist electoral history. After the election, a merger of the two parties wasmooted, but the Democratic Forum�s chairwoman, Ibolya David, continues toreject Fidesz�s attempts at consolidation, instead positioning her party as a trueconservative alternative to the more populist Fidesz.

Alliance of Free Democrats

Hungarian Democratic Forum

Hungary 13

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

Parliamentary election results1998 2002

% vote forparty list

Districtswon

Seats inparliament % of seats

% vote forparty list

Districtswon

Seats inparliament % of seats

Alliance of Free Democrats 7.6 2 24 6.2 5.6 3 20 5.2Fidesz-Hungarian Civic Party (Fidesz)a 29.4 90 148 38.3 41.1 95 188 48.7

Hungarian Democratic Foruma 2.8 17 17 4.4 - - - -Hungarian Justice and Life Party 5.5 0 14 3.6 4.4 0 0 0.0

Hungarian Socialist Party 32.9 54 134 34.7 42.1 78 178 46.1Independent Smallholders� Party 13.2 12 48 12.4 0.8 0 0 0.0

Other parties 8.6 0 0 0.0 6.0 0 0 0.0Independent candidates - 1 1 0.3 - 0 0 0.0Total 100.0 176 386 100.0 100.0 176 386 100.0Memorandum itemTotal votes cast 4,547,682 - - - 5,616,750 - - -

a Fidesz and Democratic Forum ran 78 joint candidates in 1998 and all joint lists and candidates in 2002. Fidesz now holds 164 seats, theDemocratic Forum 24.

Source: National Election Office

Main political figures

Peter Medgyessy

A minister in the last years of communist rule and the last finance minister of thegovernment led by the Hungarian Socialist Party in 1994-98. In the latter role, hepresided over the pension reform and the improvements in growth, inflation andexternal accounts that followed the implementation of his predecessor�s �BokrosPackage�. He held senior posts in the private financial sector and worked as aconsultant after 1998, before returning to the political stage after being chosen as theHungarian Socialist Party�s prime ministerial candidate in 2001. He is not a memberof parliament or the party. His liberal economic record and business links helped hisemergence as a compromise candidate for the party�s nomination, especially as itappeared increasingly likely that the Socialists would need a repeat partnership withthe liberal Alliance of Free Democrats in order to govern again. Investigations in 2002into Mr Medgyessy�s past as a counter-intelligence officer during the communist erafailed to turn up any further damaging information�for instance, evidence that hespied on his fellow citizens contrary to his claims that he did not�but the revelationswere serious enough that the Free Democrats, with their roots in the 1980s dissidentmovement, almost left government.

Viktor Orban

Prime minister in the last conservative government (1998-2002) and leading figure ofthe Fidesz-Hungarian Civic Party (Fidesz), although he gave up the party leadershipat the end of 1999. From the fiery speech at the reburial of Imre Nagy in 1989demanding the withdrawal of Soviet troops with which he first made his mark,Mr Orban has often courted controversy with outspoken rhetoric. Under hisunchallenged leadership since 1993, Fidesz has shed its liberal political identity andmoved steadily to the right. He was an energetic prime minister, but his imperiousstyle alienated many. After his party�s narrow defeat in the April 2002 election,Mr Orban receded from party and parliamentary politics. As part of his continuingefforts to consolidate the right, he actively encouraged supporters to organise intosmall local groups, called �civic circles�, to be mobilised for street protests. Mr Orban

14 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

remains the unofficial leader of the civic circle movement, dubbed �Hajra,Magyarorszag!� (�Go Hungary!�)�a popular football chant and Mr Orban�s own sign-off at public speaking appearances since the campaign season. It is also a deliberateecho of Italy�s �Forza Italia!�, a similar political movement led by Silvio Berlusconi,the Italian prime minister. Since mid-2002 Mr Orban has adopted a more Eurosceptictone, and more recently an anti-US stance as part of his open criticism of thegovernment�s support for the US�s war effort in Iraq. His rhetoric, however, tends tobe much more radical than the actions of his party in parliament.

Laszlo Kovacs

The most senior Socialist in the government is the foreign minister and party�spresident. A high-ranking member of the communist party before the transition,Mr Kovacs has remained a key figure throughout the transition period, also servingas foreign minister in the 1994-98 Socialist-led administration. Mr Kovacs is widelyexpected to become prime minister if Mr Medgyessy cannot continue for anyreason�for example, if earlier reports of health problems prove substantial enoughthat he must later leave office. Mr Kovacs, a seasoned diplomat and skilled partypolitician, is said to lack a strong leadership hand, managing through delegation andconsensus rather than hands-on decision-making. Although these characteristicsreportedly cost him his party�s nomination as prime minister, Mr Medgyessy�s styleis similar�if events eventually put Mr Kovacs in the prime minister�s post,substantive continuity could be expected.

Csaba Laszlo

The voice of the government�s economic policy is the finance minister, a fiscalmoderate who favours responsible budget policies. Mr Laszlo�s background is mainlywith the Ministry of Finance, with a brief foray into the private sector before takingthe reins at the ministry himself. He started his career in the pre-transition financeministry in 1986, and by 1989 had reached a position of some responsibility as adepartment head. His successful upward career path at the ministry moved onthrough successive right- and left-wing governments, and he became deputy statesecretary for budget affairs during the tenure of the previous Socialist prime minister,Gyula Horn, and then administrative state secretary during the Orbanadministration. Mr Laszlo left the ministry in 1999, reportedly over disagreements onbudget policy. He went on to become deputy chief executive officer (CEO) andmember of the board at the local subsidiary of the Dutch bank ABN AMRO, andlater at K&H Bank after its merger with ABN AMRO. Although Mr Medgyessy ishimself a former finance minister, he gives Mr Laszlo a wide berth to form policywithin the framework of the government�s programme.

Zsigmond Jarai

Appointed governor of the National Bank of Hungary (NBH, the central bank) for asix-year term in March 2001, after serving almost three years as finance minister inthe Orban administration. His tenure as finance minister followed a career insenior private- and public-sector finance posts. His previous relations with theFidesz-led government probably explains his tolerance of pre-election fiscalloosening and his often contentious relations with the current government. Beforethe Socialists returned to power, Mr Jarai saw the adoption of a new central bankact that enhanced its independence and enshrines price stability as its overridinggoal. Mr Jarai was also responsible for the surprising widening of the forint�s

Hungary 15

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

exchange-rate band in May 2001, which helped to halve inflation within a year.However, the NBH�s strong forint policy elicited strong criticism from groupsworried about the competitiveness of Hungarian exports, mostly employers�organisations with strong ties to the current government. This only added to thestrong political backdrop to monetary policy, with the current government eventhreatening to curb the NBH�s independence before the European Commissionintervened in mid-2002. Mr Jarai has received praise for the NBH�s successfuldefence of the exchange-rate regime, which thwarted speculative interest in theforint in early 2003, but he has also received criticism for the damage done in theprocess to the NBH�s inflation-fighting credentials.

Ferenc Madl

Mr Madl began his first five-year presidential term in August 2000. After a career asan academic lawyer, he ran previously as the right�s candidate for the post in 1995.He was nominated again in 2000 as a compromise candidate intended to bridge arift between Fidesz and a junior coalition partner, the Independent Smallholders�Party. Mr Madl seems to have been accepted by the opposition as a non-partisanhead of state.

International relations and defence

The presence of large Hungarian minorities in neighbouring countries has beena source of problems for Hungary since the 1920 Treaty of Trianon, whichreallocated more than two-thirds of the country�s pre-first world war territory(mostly to Romania, Czechoslovakia and Yugoslavia). During the 1980s thedifficulties faced by Hungarian minorities, particularly in Romania, were animportant mobilising element for the opposition parties. Since the collapse ofcommunist rule, Hungarian governments have sought to balance the need tobuild constructive relations with neighbours with the wish to extend greatersupport to the Hungarian minorities. There are perhaps 2.7m-3.3m Hungariansin Hungary�s neighbouring states, including upwards of 1.6m in Romania andaround 500,000 in Slovakia. Generally, the Hungarian left has prioritised state-to-state relations, whereas the right has given greater weight to the claims ofthe minorities.

Relations with Romania and Slovakia, in particular, improved steadily underthe 1994-98 Socialist-led regime�basic treaties were signed guaranteeing existingborders as well as minority rights�but were again put under severe strain bythe so-called Status Law, passed by the Hungarian parliament in June 2001. Thelegislation offered Hungarians living in Hungary�s neighbouring states theopportunity to apply for a Hungarian identity card that would entitle them toeducation, healthcare, travel and cultural discounts, and short-term workopportunities in Hungary. Romania and Slovakia, however, regarded the StatusLaw as discriminatory and extra-territorial and feared that quasi-citizenshipamong Hungarian minorities could lead to territorial claims in the future. Abilateral memorandum in late 2001 that involved significant Hungarianconcessions, most notably the extension of the short-term employmentopportunity to all Romanian citizens, was attacked by the Socialists forthreatening the Hungarian labour market.

Minorities and neighbours

16 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

Despite the Socialists� return to power and the continuing important role playedby ethnic Hungarian parties in Slovakia and Romania, these two countries havenot backed down from their demands that the Status Law be amended further.They have been joined in their criticism by EU and NATO officials. The EU, inparticular, remains concerned about one member passing laws that affect thestatus of another member�s citizens�both Slovakia and Hungary are set to jointhe EU in May 2004. Further amendments of the Status Law are inevitable,however, in essence turning it into a mutually agreed framework for work andstudy exchanges.

Hungary was developing links with international bodies well before the 1991dissolution of the Warsaw Pact (established in 1955) and the Council for MutualEconomic Assistance (CMEA, or Comecon; 1949). It joined the UN in 1955, andthe IMF and the World Bank in 1982. Entry into the General Agreement onTariffs and Trade (GATT) in 1973 allowed it to become a founding member ofthe World Trade Organisation (WTO). Hungary signed a trade and co-operationagreement with the European Community in 1988 and was a founding memberof the European Bank for Reconstruction and Development (EBRD) in 1991. In1991 Hungary, Poland and Czechoslovakia formed the Central European Free-Trade Agreement (CEFTA). Hungary was invited to join the OECD in 1996, andjoined the International Energy Agency (IEA) in 1997.

Hungary is set to join the EU on May 1st 2004. Hungary first applied to join theEU in March 1994, and accession talks began in 1998. Throughout negotiationsHungary often proved itself more willing to make compromises in order toreach agreement earlier than other candidates. Negotiations only truly gainedmomentum, however, in the course of 2001, once the EU adopted enlargementin 2004 as an objective and named Hungary as one of ten states scheduled tojoin at that date. Hungarians� commitment to EU membership was confirmedin a referendum on April 12th 2003, four days before Mr Medgyessy signed thefinal accession treaty at the EU�s Athens summit.

Admission talks with NATO began in September 1997, and Hungary formallyjoined the alliance, along with Poland and the Czech Republic, on March 12th1999. Close co-operation between NATO and Hungarian armed forces has beenfostered by Hungary�s participation in the NATO-led Stabilisation Force (SFOR)and the earlier Implementation Force (IFOR) in Bosnia and Hercegovina (BiH).Hungary also served as a forward base for both operations.

Alone of the three most recent NATO members, however, Hungary has beencriticised for its lack of material commitment to the alliance. Hungary�sperformance as a NATO ally became the focus of attention in November 2002,when an article in a US journal, Foreign Affairs, quoted allegations that Hungarywas the �most disappointing new member of NATO� and �would have alreadybeen expelled [from the alliance] if an expulsion were possible�. The author ofthe article argued that Hungary�s example was a signal for caution in acceptingnew members to the alliance. In subsequent statements the defence minister,Ferenc Juhasz, confirmed that Lord Robertson, the NATO secretary-general, hadvehemently demanded that Hungary fulfil its pledges to modernise its forces.

Growing internationalintegration

Hungary set to join the EU

Defence

Hungary 17

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

Military forces, 2001Active forcesArmya 12,870Border guards 12,000Air force 7,700UN & peacekeeping 830Total incl others 33,400 Conscripts 22,900ReservesArmy 74,900Air force 15,400

a Includes 270 personnel in Army Maritime Wing.

Source: International Institute for Strategic Studies, The Military Balance, 2002-2003.

The government has sought to repair Hungary�s relations with NATO and theUS, which had suffered strains under the previous administration in particular.As a result, Hungary has renewed its commitments to strengthen its defencecapabilities. In early 2003 the government allowed the US to train members ofthe Iraqi opposition at the Taszar air base, and permitted coalition forces to useHungary�s airspace and air bases for the war in Iraq. Mr Juhasz has already saidthat Hungary would probably be willing to host a missile base if a NATOmissile defence system were to be built in Europe. In early 2003 the militaryand government jointly unveiled plans to eliminate conscription (which hasbeen cut to six months) by December 2004, but the pay increases needed toeffect this have proved difficult to fund in the past.

Security risk

Armed conflict

Hungary faces few external security risks, especially since becoming a member ofNATO. Austria borders Hungary, and three of Hungary�s neighbours have beeninvited to join NATO. The security situation in two other neighbours, Croatia andSerbia and Montenegro (formerly Yugoslavia), has improved markedly, and Ukrainehas long tried to establish closer ties with European security organisations. Securityalong the borders with Croatia, Serbia and Ukraine was an issue in EU accessionnegotiations, with Hungary having taken several steps to bolster surveillance.Sizeable minorities of ethnic Hungarians in Slovakia, Romania and Serbia have beena source of contention between Hungary and its neighbours in the past, butHungarian authorities long ago gave up claims to Hungary�s former lands. The riskof armed conflict is thus low.

Terrorism

By lending its airspace and military bases to the US-led �war on terror� and morerecently to the US-led war in Iraq, Hungary has probably increased the risks ofbecoming a terrorist target itself. However, the likelihood of a terrorist attackremains low.

Civil unrest

With the exception of the 1956 events, Hungary�s post-war history has been free ofcivil strife. The risk of violent civil or labour unrest is low, especially given Hungary�shomogenous society and lack of truly divisive issues. A majority of the population

18 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

looks forward to joining the EU, and an overwhelming majority maintains a pro-Western outlook.

Violent crime

Violent crime is not much of a problem in Hungary, although petty crime is aconcern and has been growing in frequency since the fall of communism. Touristsareas are especially the targets of petty criminals, pickpockets and scam artists. Theftof, and from, vehicles is also common. Although decreasing in number, incidents stilloccur infrequently in certain bars and restaurants in Budapest where tourists arecharged exorbitant prices.

Drug smuggling and organised crime

If Hungary faces any substantial security risks, they emanate from the activities oforganised crime in the country, particularly that of the Russian mafia. Since the fallof communism in the region, organised crime has risen significantly, especially thatof Russian, Italian, ethnic Albanian, Nigerian, and Chinese criminal gangs andColombian drug-trafficking groups. Hungary shares a border with seven countriesand its well-developed transportation network makes it a logical transit zone forsmuggling. Recent evidence shows that it also is a transit point on one of thepathways for smuggling heroin to western Europe from Afghanistan and other partsof Central Asia. Authorities have tightened border controls, altering smugglingmethods, but having little discernible impact on the extent of traffic.

Resources and infrastructure

Population

According to data from the February 2001 census, the population is 10,198,315, afigure that is higher than was previously thought after years of decline. Thecapital city, Budapest, is home to 17% of the population, with the next eightlargest cities accounting for just over 12% of the population. The vast majorityof Hungarians live in what are classified as urban areas. The age structure ofthe population is typical for Europe, with 17% of the population below the ageof 15 and 20% aged 60 or above in 2000. In ethnic terms, the population isrelatively homogeneous, relative to many other countries in the region. The2001 census confirmed that previous population surveys had beenundercounting ethnic minorities, which now account for almost 8% of thepopulation. The largest minority by far are the Roma (189,984), although theEuropean Roma Rights Centre claims that there are more than half a millionRoma in Hungary, or 5% of the population. Hungarian minorities inneighbouring countries are much larger, at least 3m, and thus have a higherpolitical profile than domestic minorities, who are mostly assimilated. Politicalmobilisation by Hungary�s Roma, however, has become increasingly visible.

The population has been falling steadily since 1981, when the death rate beganto exceed the birth rate. This trend accelerated at the beginning of the transition,but lately has begun to stabilise. As late as 1991, the birth rate stood at 12.3 per1,000 population, but this declined steadily over the next eight years, and sincethen has recorded only modest gains. It stood at a preliminary 9.5 per 1,000 in2002. The death rate peaked at 14.5 per 1,000 in 1993, before falling gradually, to

Population is small,homogeneous and ageing

Hungary 19

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

a preliminary 13.1 per 1,000 in 2002 The ageing population has placed anincreasing strain on the traditionally generous system of pensions and earlyretirement, and will continue to do so for the foreseeable future, despite theimplementation in 1998 of a public-private three-pillar pension system.

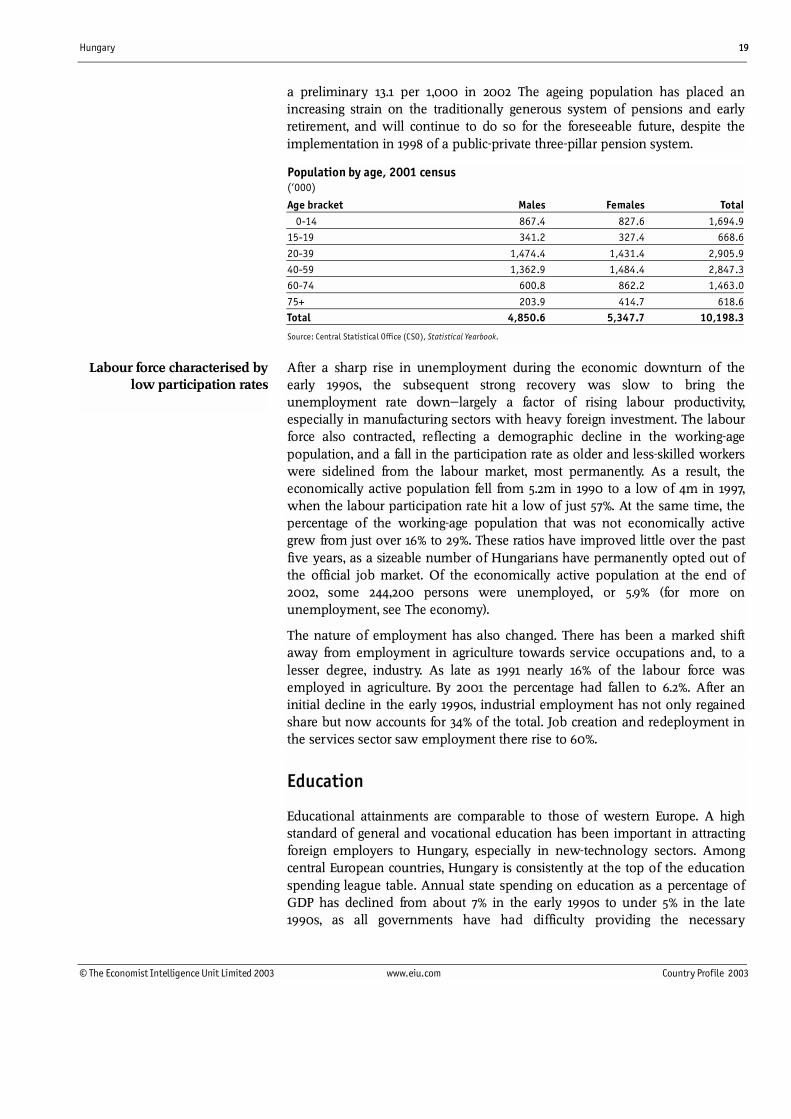

Population by age, 2001 census(�000)

Age bracket Males Females Total 0-14 867.4 827.6 1,694.915-19 341.2 327.4 668.6

20-39 1,474.4 1,431.4 2,905.940-59 1,362.9 1,484.4 2,847.360-74 600.8 862.2 1,463.0

75+ 203.9 414.7 618.6Total 4,850.6 5,347.7 10,198.3

Source: Central Statistical Office (CSO), Statistical Yearbook.

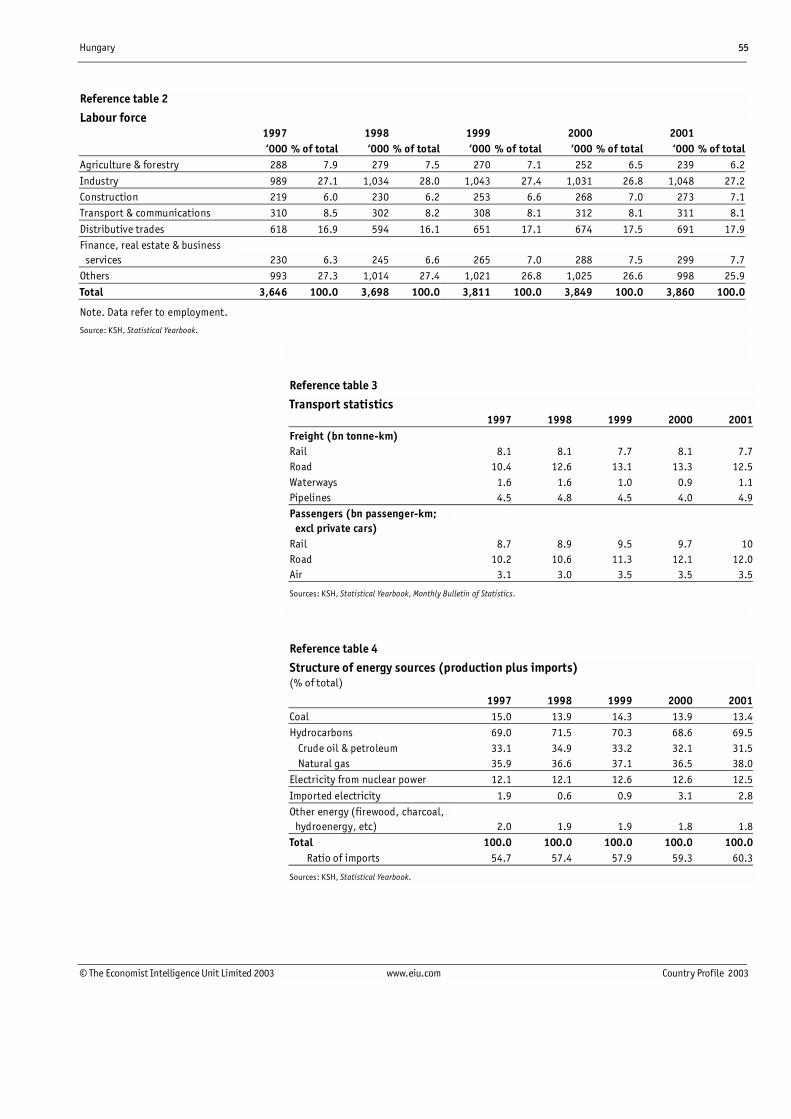

After a sharp rise in unemployment during the economic downturn of theearly 1990s, the subsequent strong recovery was slow to bring theunemployment rate down�largely a factor of rising labour productivity,especially in manufacturing sectors with heavy foreign investment. The labourforce also contracted, reflecting a demographic decline in the working-agepopulation, and a fall in the participation rate as older and less-skilled workerswere sidelined from the labour market, most permanently. As a result, theeconomically active population fell from 5.2m in 1990 to a low of 4m in 1997,when the labour participation rate hit a low of just 57%. At the same time, thepercentage of the working-age population that was not economically activegrew from just over 16% to 29%. These ratios have improved little over the pastfive years, as a sizeable number of Hungarians have permanently opted out ofthe official job market. Of the economically active population at the end of2002, some 244,200 persons were unemployed, or 5.9% (for more onunemployment, see The economy).

The nature of employment has also changed. There has been a marked shiftaway from employment in agriculture towards service occupations and, to alesser degree, industry. As late as 1991 nearly 16% of the labour force wasemployed in agriculture. By 2001 the percentage had fallen to 6.2%. After aninitial decline in the early 1990s, industrial employment has not only regainedshare but now accounts for 34% of the total. Job creation and redeployment inthe services sector saw employment there rise to 60%.

Education

Educational attainments are comparable to those of western Europe. A highstandard of general and vocational education has been important in attractingforeign employers to Hungary, especially in new-technology sectors. Amongcentral European countries, Hungary is consistently at the top of the educationspending league table. Annual state spending on education as a percentage ofGDP has declined from about 7% in the early 1990s to under 5% in the late1990s, as all governments have had difficulty providing the necessary

Labour force characterised bylow participation rates

20 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

resources. The 1998-2002 government, led by the Fidesz-Hungarian Civic Party,encouraged an expansion in higher education in particular�the number ofuniversity graduates each year grew by nearly 30% during this period�butwithout any major rise in education spending, which remained just above 5%of GDP in 1999-2001.

Schooling is compulsory for children between the ages of six and 16. Underthe communist regime, education in a general elementary school was usuallyfollowed by four types of outcomes: exit from school; apprentice school forskilled workers� training; vocational secondary school; and gymnasium orgeneral secondary school. The gymnasium was the primary feeder ofstudents to the universities, although other institutions of higher educationaccepted students from vocational secondary schools. This system haspersisted since 1989, and completion rates for general elementary schoolremain quite high. Apprentice schools have declined as a destination amongsecondary students. In 1990/91 almost half of those completing elementaryschool continued to apprentice schools; currently only about one-quarter doso. The percentage continuing to vocational secondary schools increased from28% in 1990/1991 to over 40% in 2001/2002, and the percentage continuing togymnasium rose from 21% to around 35%. Gymnasium schooling in gradesfive to eight has also re-emerged.

University and college education expanded rapidly in the 1990s. In 1990/91only 8.5% of the population aged 18-22 was attending university or college,applicants� success rate being 36%. By 2000/01 enrolment had almost trebled,with more than 20% of the university-age population in full-time study andacceptance rates reaching almost 60%. Expansion in the late 1990s was helpedby the Fidesz-led government�s elimination of the tuition fees for first-degreeprogrammes introduced by its predecessor. However, Fidesz has been accusedof opening the doors to university education wider to compensate for a lack ofreal employment opportunities for young Hungarians. University educationlasts for five years, and college-level programmes can range from three to four.The 89 universities, colleges and other institutions of higher education retaintheir traditional subject specialisms.

Health

Despite a high share of healthcare spending in GDP, Hungarians have the lowestlife expectancy among OECD member countries. The health of the Hungarianpopulation has been poor by international standards for several decades, andthe death rate from cardiovascular diseases is one of the highest in the world,according to the World Health Organisation (WHO). In 2001 life expectancy atbirth was 68 years for men and 76 years for women. The figure for men hasnow surpassed its 1964 peak, after hitting a low of 64.5 in 1993. The suicide rateis one of the highest in the world, at just less than 30 per 100,000 inhabitants,although the rate is gradually declining. Infant mortality has continued todecline, from 47.6 per 1,000 live births in 1960 to 8.1 per 1,000 in 2001.

Higher education expandsrapidly

Hungary 21

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

Hungary�s healthcare system is underfunded and in urgent need ofrestructuring. Rising costs in the sector, especially for pharmaceuticals, continueto put severe pressure on government budgets. In recent years the NationalHealth Insurance Fund (OEP) has covered roughly three-quarters of thecountry�s drug expenses. Hungarians grew accustomed to cheap medicationduring the communist era, and cutting government subsidies has not beenpolitically viable. Average annual drug consumption is the second highest inEurope after France; the Economist Intelligence Unit estimates that the drugs billaccounts for nearly 30% of state healthcare spending, compared with the usualrate of 10-15% seen in similar countries. As Hungary tackles healthcarefinancing, especially in preparation for EU membership, improvements inhealth will only be slight, and gains in life expectancy will lag behind those inthe EU and the US.

The main issues facing Hungary, however, have little to do with physicalcapacity or numbers of personnel, but are directly related to the need to re-orient the sector from institutional care towards care at the primary level. Somereorientation has begun, but the process is slow, with inertia coming fromlobbies in the industry as well as from the general population. The number ofhospital beds per 1,000 population dropped from 11 at the beginning of the1990s to just over eight in 1998, remaining broadly at this level in 2001. This isslightly lower than the ratio in Germany, on a par with that in France anddouble that in the UK and the US. Earnings in the healthcare sector relative tothe total economy ranked among the lowest in the OECD in 1996, and thecontinued erosion of pay against private-sector counterparts makes competentstaff hard to retain. The hospital sector has been hit by numerous cash crisesand threatened strikes in recent years.

Healthcare

Funding

Basic health services are available through the National Health Insurance Fund(OEP), part of the social security system. The OEP acts as purchaser of services ofdoctors, hospitals, and other providers. It has substantial autonomy, but was broughtunder closer supervision of the Ministry of Finance by the government led by theFidesz-Hungarian Civic Party in 1998 after a ballooning of the deficit. The OEPreceives a combination of employer and employee contributions, with peopleoutside the labour force covered by state contributions.Local governments are largely responsible for service provision, providing mostprimary healthcare and operating a majority of hospitals. Local district doctorsprovide basic healthcare services and make referrals to specialists. All services,including hospital care, are in theory free to the patient. Primary care is reimbursedby flat fees per patient, which are adjusted according to the age profile of the patientsand the qualifications of the doctors treating them. Outpatient treatment is paid onthe basis of a points system, and hospital care is reimbursed according to diagnosticgroup. However, tipping of doctors in the state system is common, particularly foradvanced services such as surgery. In addition, doctors receive private patients intheir free time, both in separate private practices and occasionally at their officialpractice. This informal system supplements the low salaries received by medicalprofessionals and encourages a de facto fee-for-service system. Medicines are heavily

Poorly structured healthcaresystem

22 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

subsidised, although price caps on prescribed drugs since 1999 have helped to reducethe resultant OEP deficit.

Systemic reform delayed

Responsibility for healthcare planning is divided between the OEP, the Ministry ofHealth and the finance ministry, with the Ministry of Economy and Transport andthe Prime Minister�s Office also involved. Turf wars between bureaucracies, thestrong lobbying efforts of doctors, and political conflict within the government andwith the opposition caused large-scale reform to stall under the Fidesz-ledgovernment. One step taken by Fidesz was to pass a law giving 7,000 generalpractitioners (GPs), paediatricians and dentists the right to practise free of charge.Currently these practitioners are contractors with the OEP and have been selectedthrough tenders offered by local councils. The legislation also set up a loan guaranteeprogramme for doctors to allow them to purchase offices and equipment from localcouncils. However, more drastic reform is needed, something that the newgovernment, led by the Hungarian Socialist Party, is keenly aware of. Fiscalconstraints, however, have limited all but the most modest proposals.

Natural resources and the environmentHungary has a land area of 93,030 sq km and a population in February 2001 of10,198,315, which gives the country a population density of 109.6 per sq km,similar to that of France and Poland. The country is a low-lying plain dividedroughly into three equal parts by two rivers running north-south, the morewesterly Danube and the Tisza towards the east. The land is generally fertile,with about 70% suitable for agriculture. Hungary lacks extensive domesticenergy resources and raw materials, except for bauxite.

There are three primary geographic regions. Transdanubia, the area lying westof the Danube, is a hilly region extending to the foothills of the Austrian Alps.It is primarily an agricultural area with crops, livestock and viticulture. TheGreat Plain (Nagy Alfold), lying east of the Danube and including the Tiszariver basin, contains about half of the country and includes regions of fertilesoil, sandy areas and wetlands. Drainage projects in the late 19th centurycurbed the traditional floods and opened the land for cultivation, although theflood problem has returned to the region in recent years. The northern hills runfrom north of Budapest to the north-east along the Slovak border. Thecountry�s limited mineral deposits (and the Tokay wine region) are largelylocated in this area, which was the location for most of the heavy industries ofthe communist era.

There are a few moderately high ranges of mountains, but only 2% of thecountry reaches heights of 300 metres or more. The highest peak is Kekes at1,014 metres. Lake Balaton in Transdanubia is the largest lake in central Europe,measuring 78 km in length and between 3 km and 14 km in width. The hillssurrounding the lake are an important site of viticulture. Budapest and much ofthe remainder of the country have numerous thermal spas. The climate issubject to dramatic changes. Average daytime temperatures in Budapest rangefrom minus 1-4°C in January to 16-28°C in July. There is a slight variation in the

Three main regions

Hungary 23

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

climate across the country, with the south slightly warmer and the north andeast slightly cooler.

Transport, communications and the InternetDecades of underinvestment during the socialist period left rail, road andtelephone systems dilapidated. The trend has been reversed since 1989 assignificant inflows of international capital have been directed towardsinfrastructure. Public finance constraints, however, have led to the scaling-downor cancellation of some long-awaited projects.

Since the early 1990s upgrading of the motorway network has been one ofHungary�s main infrastructure priorities, although only one motorway so far�that connecting Budapest to Vienna�has been extended to one of Hungary�sborders. In 2000 the government approved a seven-year roadbuildingprogramme, involving the construction of 702km of roads, that was laterextended to 15 years and expanded to include other infrastructure projects. Thecurrent government has vowed to continue its predecessor�s programme, withpreference still being given to routes that form part of European transportcorridors. With support from the European Bank for Reconstruction andDevelopment (EBRD) and the EU�s instrument for structural policies for pre-accession (Ispa), the M3 motorway (running north-east from Budapest) is due toreach the border by 2004. The motorways running south-west and south-eastfrom Budapest are also under development, as are several bridges over theDanube and Tisza, and non-motorway inter-city roads and ring-roads.

Road transport has replaced railways as the primary form of freight haulage,reflecting both the improvements in main road provision and past lack ofinvestment in the state-owned railway, MAV. Waterway shipping began torecover in 1996 after the lifting of sanctions against Serbia and Montenegro(formerly Yugoslavia), but growth slowed in 1997-98 and another reversal wasinflicted by damage to bridges over the Danube at Novi Sad in Vojvodina duringNATO�s air strikes against Serbia in 1999. Although most of the debris had beencleared by mid-2000, temporary pontoon bridges continued to disrupt rivertraffic. Air cargo plays a minor role in the freight system, although smallvolumes of higher value-added products are imported and exported this way.

Although the dominant form of long-distance passenger traffic is still bus travel,the private car plays an important role in Hungarian life. Car ownershipincreased from 188 per 1,000 of the population in 1990 to 246 per 1,000 in2002. Air passenger traffic has grown rapidly in the past five years, but it stillmakes only a small contribution to total long-distance passenger traffic.Capacity at Budapest Ferihegy, the international airport, rose to 5.5m passengersper year after a recent expansion.

Nearly US$6bn in telecommunications investment, US$3bn of this from foreigninvestors, has transformed the moribund telecoms system inherited from thecommunist era into one of the best in the region. At the start of the 1990sHungary had one of Europe�s least-developed telecoms systems, with an

Freight haulage

Passenger transport

Motorway construction

Telecommunications progresshas slowed

24 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003

installed base of less than 1m main lines, a penetration rate of only nine linesper 100 inhabitants, and a call completion rate of less than 40%. Thegovernment soon transformed the fixed-line monopoly, Matav, into a joint-stock company, which oversaw the overhaul of the system. Full automationwas achieved in 1996 and digitalisation has reached over 90%. The number offixed lines has quadrupled over the past ten years. Matav, now controlled byDeutsche Telekom (Germany), still dominates the Hungarian fixed-linetelephone system, but a new telecoms law has opened the local, domestic andinternational markets in fixed-line phone services to competition. However,alternative telecoms providers were already on the scene, because voice overInternet protocol (VOIP) services were deemed not to violate monopolyconcessions. There is free competition in non-public fixed-line services, such asintra-company or data networks. Number portability, important to the easyswitching of customer accounts, is not envisaged until 2004.

The well-developed cellular telephone market has pushed Matav to improve.The number of mobile telephone service subscribers continued to grow rapidlyin 2002, with the market penetration rate increasing to above 55%, well beyondthat of the fixed-line market. The current market leader is Westel 900, a unit ofMatav, which now owns the mobile telephone operator outright, after taking anoption to purchase the 49% stake previously held by Matav�s parent company,Deutsche Telekom. The second largest operator is Pannon GSM, in which theDutch company KPN holds a 45% share. The latest entrant to the market,Vodafone, which started providing services on 1800 MHz in 1999, is the localunit of the UK mobile company of the same name, in a joint venture withAntenna Hungaria and RWE Telliance of Germany. All three service providersoffer wireless application protocol (WAP) services, although less than 10% ofsubscribers currently have WAP phones. General packet radio services (GPRS)facilities were introduced in 2001.

Matav�s hold over the country�s main telecoms networks has been difficult tobreak, and this is partly responsible for a loss of momentum in recent yearsthat has left Hungary with some of the region�s highest call and Internet accesscharges. Official figures showing 21 people per 100 population using theInternet probably overstate the numbers with access to the web�the numberof regular Internet users is probably about 1m. Besides the high cost of access,one of the main obstacles to the growth of Internet use is the relatively lownumbers of personal computers for home use.

Energy provision

Hungary is poorly endowed with natural resources, and has to import morethan half of its energy needs. Indigenous oil reserves, estimated at 58m tonnes,enabled domestic primary production of 1.8m tonnes in 2001, about one-fifthof refining input. Oil production declined steadily through the 1990s, afteraveraging around 2m tonnes/year before 1989. No new major oil discoveriesare expected. Estimated gas reserves are around 113bn cu metres, with domesticproduction now meeting around one-fifth of consumption, down from almosttwo-thirds of consumption in 1980. This reflects rising domestic consumption

Internet usage hindered bycosts and computer access

Mobile telephone penetrationsurpasses fixed-line market

Domestic resources are limited

Hungary 25

© The Economist Intelligence Unit Limited 2003 www.eiu.com Country Profile 2003

of gas, especially as a substitute for the less environmentally friendly coal, anda steady decline in domestic gas production from the 6.2bn cu metres recordedin 1989. There are natural gas deposits near Szeged, Miskolc and in easternHungary, and smaller crude oil deposits near Szeged, Zala county (westernHungary) and in other areas. Although there are small uranium deposits, themain mining company based near Pecs has closed after unsuccessful attemptsto sell the enterprise, leaving the Paks nuclear power plant (in central Hungary)dependent on imports.

Although energy consumption is forecast to rise as the economy expands, itsgrowth has so far been held down by sharp improvements in industrial energyefficiency. Electricity consumption growth is estimated to have been around 2%per annum in 1997-2001, even as overall economic growth was running atabout 4%. Under communism, energy use per unit of GDP was around2.5 times the OECD average. The 1989 level of industrial production wasregained during 1999 with around 25% less fuel use. Savings were achievedmainly through the closure of inefficient enterprises, motivated by a rise inindustrial fuel prices as subsidies were withdrawn.

As elsewhere in Europe, oil and natural gas had replaced coal as the primarysource of energy by the end of the 1970s. Gas already accounts for about 40%of Hungary�s electricity production, and most households and businesses relyon gas for heat. Hungary�s dependence on natural gas from the former SovietUnion was broken in 1996, when a pipeline between Gyor and Baumgartenlinked it to Austria�s gas grid for the first time. Oil supply has also started todiversify, with the opening of a pipeline to the Adriatic.

Gas sector

The National Oil and Gas Trust (MOL)

MOL, the Hungarian oil and gas company, was privatised in 1994, and the sixregional gas distribution companies (GDCs) in 1995. A subsequent share offering in1997 reduced the state stake in MOL from 59% to 25% plus one golden share, withforeign investors holding more than 30%. However, this did not mean an end topolitical influence on the company�s activities. MOL is the sole domestic producer,dominates imports (which account for 85% of Hungary�s gas needs), owns a networkof high-pressure gas transport and collection pipelines, is Hungary�s largest companyin terms of sales and is the sole distributor to the regional gas suppliers.The company�s distribution network must be open to competition if Hungary is toconform to the EU gas directive (which took effect in 2000), but progress towards thisand a liberalised price regime has been slow. Gas liberalisation raises the politicallysensitive problem that prices to industry and households will rise, owing to thewithdrawal of subsidy, before greater competition and efficiency leads to a fall. Thedate for full market liberalisation has been delayed several times, but liberalisationcould begin as early as mid-2003. Fearing the impact on inflation, and on poorerhouseholds� welfare, of a sharp rise in residential gas prices, governments past andpresent have usually restricted these to below inflation. The persistent lossesinflicted by these price controls have prompted attempts by MOL to sell itswholesale gas business. It has also prepared for eventual liberalisation of the sector,

26 Hungary

Country Profile 2003 www.eiu.com © The Economist Intelligence Unit Limited 2003