iar : french bioeconomy cluster · innovation drivers for the various players (agrifood, biotech,...

TRANSCRIPT

………………………………………………………………………………….

IAR : FRENCH BIOECONOMY

CLUSTER

«What has been accomplished in

the bioeconomy in France?”

Jacky VANDEPUTTE, Biobased chemical

and biotechnology Project Manager

………………………………………………………………………………………….........

………………………………………………………………………………………….........

IAR – COVERING THE FULL VALUE CHAIN

370+ members: large companies,

SMEs, start-ups, universities, RTOs, VCs, innovation agencies,local authorities

CROP

ALGAE

WOOD

MUNICIPAL WASTE

FOOD AGRI WASTE

INSECTS

MICROORGANISM…

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Our main mission

Connect the different actors of the bioeconomy value chains in

order to develop long-term collaborations

BIOREFINERIES CONCEPT AND BIOECONOMY

Source: Biobased Industries Consortium

France

1,9 millions jobs

Food /agri : 195 000 jobs

Turn Over : 300 billions €/y

………………………………………………………………………………………….........

………………………………………………………………………………………….........

IAR’S STRATEGICAXIS

………………………………………………………………………………………….........

………………………………………………………………………………………….........

LES MEMBRES DE LA COMMISSION BIOMOLECULES:

En bleu les acteurs membres actifs du « bureau » de la commission (jusque 2014) depuis ouvert à tous –En Gras les acteurs les plus actifs dans les commissions et Groupe de travail déclinés (hors participation aux journées techniques).

AGRO - FOOD Chemistry Biotechnology Process

Equipment

Applications Recherche & Transfert&

Association

ARD

AVRIL

CHAMTOR

CRISTAL UNION

IMPROVE

INEOS

ENTERPRISES

OLEON SAS

PIVERT SAS

PROCETHOL 2G

ROQUETTE FRERES

SOUFFLET GROUPE

TEREOS

UNGDA

VANDEPUTTE

OLEO

CHEMICALS

VIVESCIA …

ACTIVATION

AIR LIQUIDE

FRANCE

ARKEMA

AXENS

CREE

DEHON INVENTEC

INVENTEC

PERFORMANCE

CHEMICALS

LEFRANT RUBCO

NOPCO

NOVACAP

OMEGA CAT

SYSTEM

PCAS

PENNAKEM

SOLVAY

SPEICHIM

PROCESSING

SPR – SOCIETE

PICARDIE

REGENRATION

STRATOZ

SURFACTGREEN

TOTAL

WEYLCHEM

YPSO-FACTO

…

ABOLIS

AELRED

AJINOMOTO

FOODS

ALDERYS

ARBIOM

BGENE

CELODEV

GLOBAL

BIOENERGIES

LEAF

METABOLIC

EXPLORER

PILI BIO

PROTEUS

ROOT LINES

TECHNOLOGY

SYNGULON

TWB

VITO NV

…

ALFA LAVAL

BARRIQUAND

TECHNOLOGIES

THERMIQUES

BOCCARD

CHIMEX

DELTA NEU SAS

FLOTTWEG

GEA PROCESS

ENGINEERING

KADANT LAMORT

PROCESSIUM

SAIREM

…

MATERIA NOVA

EURODIA

NOVASEP PROCESS

LEBAS INDUSTRIES

IPSB

Coatings Cosmetics AGROPARISTECH

CEA

CENTRALE

SUPELEC

CBG

CHAIRE ABI

CRITT POLYMERE

EBI

ESCOM

EXTRATIS

FRCA C.A

INP PAGORA

ICMUB

IFMAS SAS

IFPEN

INRA

INSTITUT CHARLES

VIOLLETTE

IRDL (UBS)

ITERG

LA PAILLASSE

LRGP

NEOMA

SATT AXLR

SFR CONDORCET

SUP BIOTECH ECOLE

TERRES INNOVIA

UIC

UNILASALLE

UNIV LILLE 1

UPJV

UTC

UTT

VALAGRO

PROPSA

AC&CS GROUPE CRM

BOSTIK

LIFCO INDUSTRIE

LINEA COLLES

INDUSTRIELLES

…

BIOLIE

ALTINAT /

GREENTECH

GIVAUDAN

L’Oréal

LVMH

SENSIENT

COSMETIC

TECHNOLOGIES

SEPPIC

…

Lubricants Detergence

CONDAT

MOLYDAL

NYCO

…

BIO ATTITUDE

SALVECO

…

WOOD PAPER Modelisation Plant protection

NORSKE SKOG

Emin leydier…

BIOPTIMIZE

PROSIM

SNC LAVALIN

SYNSIGHT

…

ELEPHANT VERT

ROULLIER

SDP

…Waste Management

AFYREN

INERIS NORD

VEOLIA

ENVIRONNEMENT

Autres

ALGAE

ALGAE NATURAL

FOOD

ALGAMA

ALGOSOURCE

FERMENTALG

NOCARBON

SPIRIS

SUNOLEO

COLAS

DENIS & FILS

MICHELIN

PCA

SAFRAN

WOODOO

HARMONICA

PHARMA

…

INSECTS

ENTOMOFARM

INNOVAFEED

NEXTALIM

PROEARTH

PROTIFLY

YNSECT

………………………………………………………………………………………….........

………………………………………………………………………………………….........

IAR’S REGIONS

Building on 2 strong agricultural regions• Over 5 million hectares dedicated to

agricultural production• 75% of the French sugar production• More than 2/3 of the French potato

production• 20+% of flax production• ...

To support the bio-baseddevelopment of more than 370 members everywhere in France (and beyond…)

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Innovation Drivers for the various players (agrifood, biotech, chemestry..)

BIOBASED CHEMICAL MARKETS – DRIVERS (2005)

➢ “Finding new outlets for the Agri-co-products - Anticipating the modifcation of the CAP (European commonagricultural policy) and development of biorefineries - Availability of a low cost bio-based material” (C5,sugar beetpulp, lignin glycerol due to biodiesel) Ex : propanediol or epichlhorydrine -

➢ INNOVATION : Taking advantage of the biomass composition in niche market and Providing new technical performance Ex : 2,5 FDCA - Production of a PET equivalent with improved performance (thermal resistance), polyethylene 2,5-furanedicarboxylate (PEF) - Sebacic acid - Production of high-performance polyamides (PA 10, PA 11)

➢ Growing awerness of the environnemtal impacts by customers and a way to differenciate their product thanks to « natural and good image of non food use biomass» Ex: Ethylene - Precursor for the production of polyethylene sold at a premium price as a result of its better environmental performance.

➢ Replacing hazardous chemical intermediates - Ex: Isosorbide - Production of isosorbide diester (substitute for phthalates PVC production)

➢ Anticipating the Rarefaction of fossil fuel and Increasing in Oil prices and risk of shortage - Strain on petro-based supplies, due to the use of shale gas in North America

➢ Ex : Butadiene - Isoprene Use of shale gas in North America crackers which do not allow currently to produce these two intermediates - However resurgence of old petro-based technologies which compete with bio-based.

ISO PROCESS - ISO PRICE , ISO PROPERTIES - ISO PRODUCT - OR BETTER

PERFROMANCE AND LOWER ENVRONMENTAL IMPACT

………………………………………………………………………………………….........

………………………………………………………………………………………….........

BIOTFUEL (2G BIOFUELS)

2016 Compiègne

TERRALAB (SUSTAINABLE AND

INNOVATIVE CROPS PRODUCTION)

2015 Reims

PIVERT (PLANT BASED CHEMISTRY -

OILSEEDS) 2015 Compiègne

PROCETHOL 2G ( 2G

BIOFUELS) 2012 Bazancourt

BIODEMO (WHITE

BIOTECHNOLOGY)

2010 Bazancourt

IMPROVE (PROTEINS)

2014 Amiens

FRD (Plant fibers) 2012 Troyes

ARD (BIOTECH and

crops valorization)

2007 and 2015Bazancourt

CEBB EUROPEAN INSTITUTE

FOR BIOECONOMY AND

BIOTECHNOLOGY

(Training and research) 2015

Bazancourt

Bioeconomy

Park

2016 Bazancourt

OZONIA (OZONE

TECHNOLOGY) 2016 IPLB Beauvais

EXTRACTIS (BIOMASS

FRACTIONNATION) 1984 Amiens

CODEM (BIOBASED MATERIALS

FOR BUILDING) 2016 Amiens

BIOGAZ VALLEE

(BIOGAZ) 2016Troyes

BIOTFUEL (2G BIOFUELS)

2016 Dunkerque

Farms network AGRT (SUSTAINABLE AND

INNOVATIVE CROPS PRODUCTION) 2015 Estrées-Mons

SYNDIESE (2G

BIOFUELS)

2015 Bure Saudron

281 millions € investment> 500 direct jobsECOSYSTÈME D’INNOVATION IAR

IFMAS (BIOBASED

MATERIALS) 2015 Lille

9

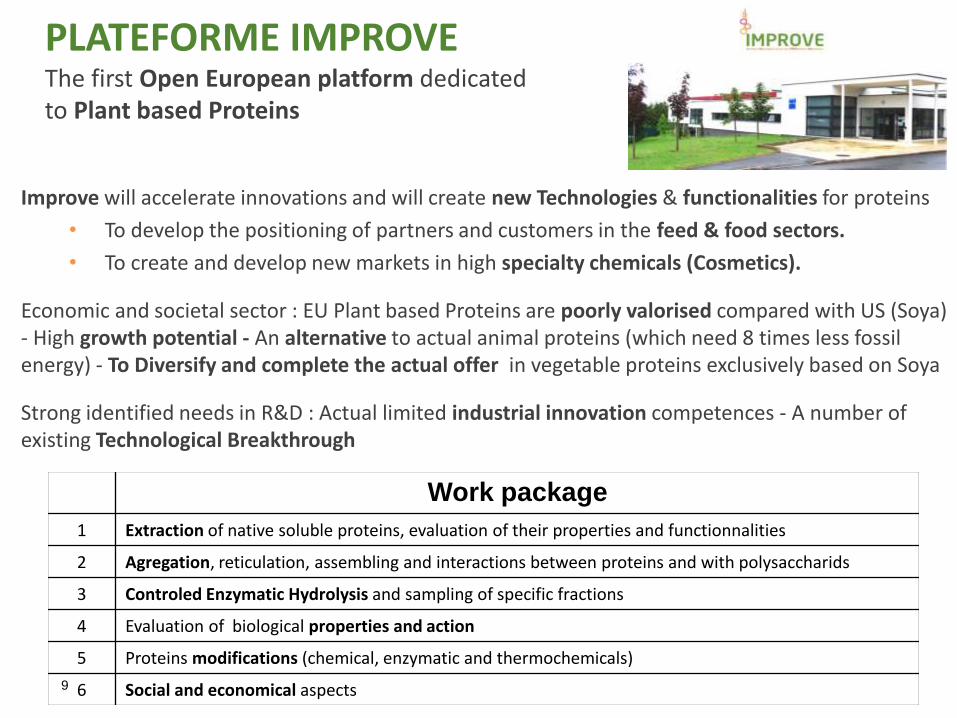

PLATEFORME IMPROVE The first Open European platform dedicated to Plant based Proteins

Improve will accelerate innovations and will create new Technologies & functionalities for proteins

• To develop the positioning of partners and customers in the feed & food sectors.

• To create and develop new markets in high specialty chemicals (Cosmetics).

Economic and societal sector : EU Plant based Proteins are poorly valorised compared with US (Soya) - High growth potential - An alternative to actual animal proteins (which need 8 times less fossil energy) - To Diversify and complete the actual offer in vegetable proteins exclusively based on Soya

Strong identified needs in R&D : Actual limited industrial innovation competences - A number of existing Technological Breakthrough

Work package

1 Extraction of native soluble proteins, evaluation of their properties and functionnalities

2 Agregation, reticulation, assembling and interactions between proteins and with polysaccharids

3 Controled Enzymatic Hydrolysis and sampling of specific fractions

4 Evaluation of biological properties and action

5 Proteins modifications (chemical, enzymatic and thermochemicals)

6 Social and economical aspects

© SAS PIVERT 2018

Mission

Développement de solutions

❖ Innovantes

❖ Performantes

❖ Industrielles

❖ Biosourcées

© SAS PIVERT 2018

Positionnement de la SAS PIVERT

▪ Un programme de recherche pluriannuel qui alimente le « pipe » d’innovation (Budget = 60+ M€)

▪Une plateforme de développement industriel pour la montée en échelle des procédés : équipements de pré-traitement de la biomasse, chimie, biotechnologie…

▪Des partenariats de développement pour l’industrialisation des technologies et l’accès au marché

© SAS PIVERT 2018

Offre commerciale

▪Des solutions innovantes

pour

– La nutrition et santé des

plantes

– Les additifs industriels

– L’alimentation animale

(additifs)

………………………………………………………………………………………….........

………………………………………………………………………………………….........

TEACHING APPLIED R & D INDUSTRY

BIOREFINERY RESEARCH AND INNOVATION

A center of excellence in biotech teaching, with leading engineering schools

An open Biotech platform, from lab-scale to demonstration scale

A Technology center welcoming new start-ups

BRI: Biorefinery Research Innovation

CRISTAL UNION,

CRISTANOL, VIVESCIA,

SICLAE, CHAMTOR,

IAR OPEN INNOVATION PLATFORMS

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Our services in favor of innovation

IAR CLUSTER

Boost your competitiveness through innovation Assistance in setting up projects

Inform for better decisionsBusiness intelligence platform for biobased products and processes

Develop your networks and markets

International support

Access to private fundingAccompanying the fundraiser

Accelerate the commercialization of your biobased

Internet data base to promote biobased products

(www.agrobiobase.com)

280 Collaborative R&DI Projects – global budget : 1,7 Milliards €

500 Millions

IAR DO brazil (2014)

10 collaborations

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Databases

TREMPLIN

Configurable and

customizable home interface

through an editorial style

www.iar-tremplin.com/membres

Demonstration tool for

testing content

………………………………………………………………………………………….........

………………………………………………………………………………………….........

• Easy search throughmarket approach

• 400+ products

www.agrobiobase.com

SHOWCASE OF BIO-BASED PRODUCTS

………………………………………………………………………………………….........

………………………………………………………………………………………….........

FRENCH BIOECONOMY STRATEGY

• January 18th 2017 , established by the Ministries of agriculture, environment, industry, and research and stakehodlers of the whole value chain the french bioeconomy strategy between 2018 – 2020

• Give a framework and tools for sustainable development of the bioeconomy taking intoconsideration the availability of biomass on the territory.

• With an action plan dedicated in 2018-2020 on Non food Uses. 5 Axis: Improving the knowledgeon bioeconomy - Promoting the bioeconomy and the bioproducts - Creating the necessaryconditions to facilitate the demands and offers -Producing, mobilizing and transformation of the biomass - Lift bareers and mobilising finance

………………………………………………………………………………………….........

………………………………………………………………………………………….........

FRENCH BIOEOCONOMYACTION PLAN (2018 –2020) - (5 AXIS)

Improving the knowledge on bioeconomy• Developping Scientific Congress on Bioeconomy • Promoting of the ONRB National Observatory on biomass with a CST, • Launching a prospective study - state of the art on blue economy (biomass coming from marine and freshwater

fish, algae), • Improving LCA Methodology for the bioeconomy value chains completed with social and economic LCA at territory

Level• Putting Bioeconomy on the national education• Creating Interdisciplinarity: Chaire on Bioeconomy on social and economics impacts• Evaluating the bioressource on overseas territory and especially endemic species with biotechnology potential• Assessing the new non food outlets on agriculture value and income and competitivness of the food sector

Promotion of the bioeconomy and the bioproducts• Communication campaign targetting consumer and Citizen. sensitizing on environmental and territories challenges• Label ‘biobased Product » based on CEN/TEC/41 biobased content with for each range of products with specific

rate and taking onto account the envronmental performance• Promoting the databases on biobased products – AGROBIOBASE• Website on bioeconomy with exemples projects on biotechnology marine and applications• A roadshow with a house with all products made from biomass• Awards of Bioeocnomy• The week of the Bioeconomy and open house day• Olympic Games village on biobased materials

………………………………………………………………………………………….........

………………………………………………………………………………………….........

FRENCH BIOEOCONOMYACTION PLAN (2018 –2020)

Create the necessary conditions to link the demands and offers• Campaign on each range of products for the players (specifications) targetting industrial association,

federation• Helping used of biobased product with norms and insurance (PTR, demo plant, Life laboratory,

European technology Verification » - Faisability• Business convention upstream and downstream• Good Practices dissemination through collaborative action• Large retail outlets Meeting • Specific valorization on whool and skin of ovine…leather cow…animal …fibers, hemps and Linseed,

overseas biomass

Produce, mobilize and transform the biomass• Biomass Sustanability - Equipement and datas on harverst - Intermediary plantation for energy supply

Sustainable Energy

Lift bareers and mobilising finance• National Governance on bioeconomy, adopt legislation and rules dedicated to bioeconomy, • Strategy with the different ministery, reform to facilitate the public purchase (hospital , school)

mobilizing financement of PAC, end of life alert, reduce legislation hurdles on methanisation, acessto bank garantee, promoting BBI, Including Bioeconomy in different call ANR and PIA3 (cartography), call PIA dedicated on advanced Biofuels, and for captive fleets, discussion withterritories implementation, create a europeean strategy, certification of biomass, bioinspired …

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Biobased chemical and industrial Biotechnologies

STRATEGIC AREA BIOMOLECULES

Matériaux

Formulation et Additifs

Chemical

Interdemidiates

Polymers

Addtives

Formulation

Process

Cosmetic

Crop

Protection

Materials

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Biobased Chemical and Industrial Biotechnology

MARKET DATAS

ADEME « Marché actuel des produits biosourcés et évolutions 2020 et 2030 » - déc 2014 -

Estimation des tonnages pour les différents secteurs.

Biobased Market

▪ Cosmetic is the main application

sector (market share 50%)

▪ Biodegradable or Medium

Performance polymers are

targeted niche market

▪ Coating market is quite dynamic

▪ Speciality chemical niche

market : biolubricants, solvents,

surfactants

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Afterthe boomingPhase of biobasedchemicaland biotechnology

1) 2007-2014 : a booming industry

2) 2014 - today : the disillusionment ?

What are the feedbacks ?

3) Future : slope of enlightenment ?

How to choose the right target

molecule ?

Today ?

DESILLUSIONMENT PERIOD….

………………………………………………………………………………………….........

………………………………………………………………………………………….........

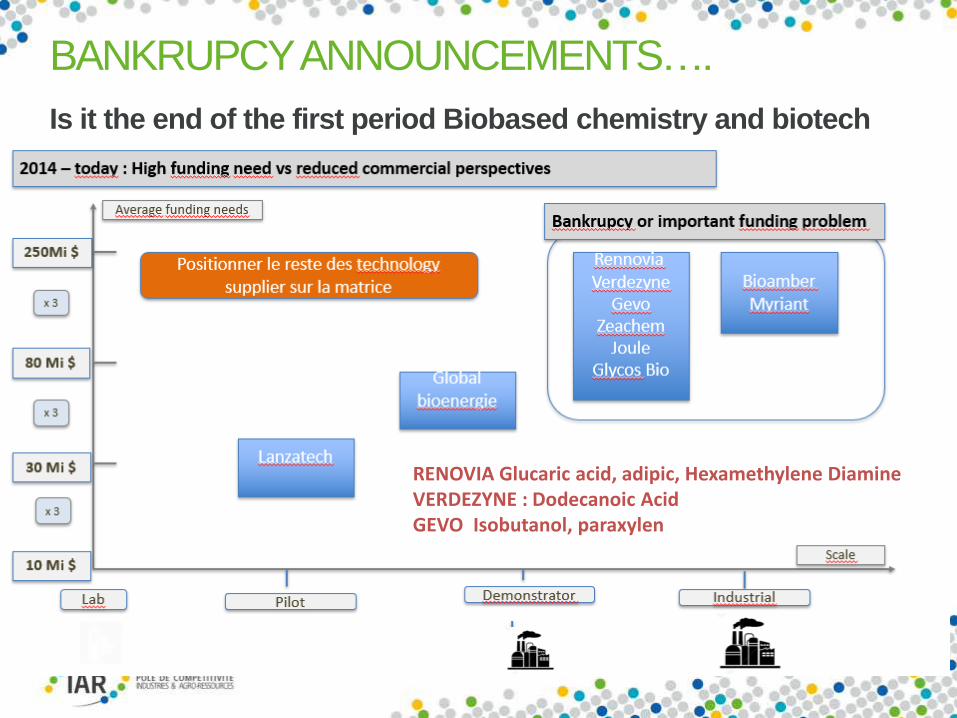

Is it the end of the first period Biobased chemistry and biotech

BANKRUPCYANNOUNCEMENTS….

RENOVIA Glucaric acid, adipic, Hexamethylene DiamineVERDEZYNE : Dodecanoic AcidGEVO Isobutanol, paraxylen

………………………………………………………………………………………….........

………………………………………………………………………………………….........

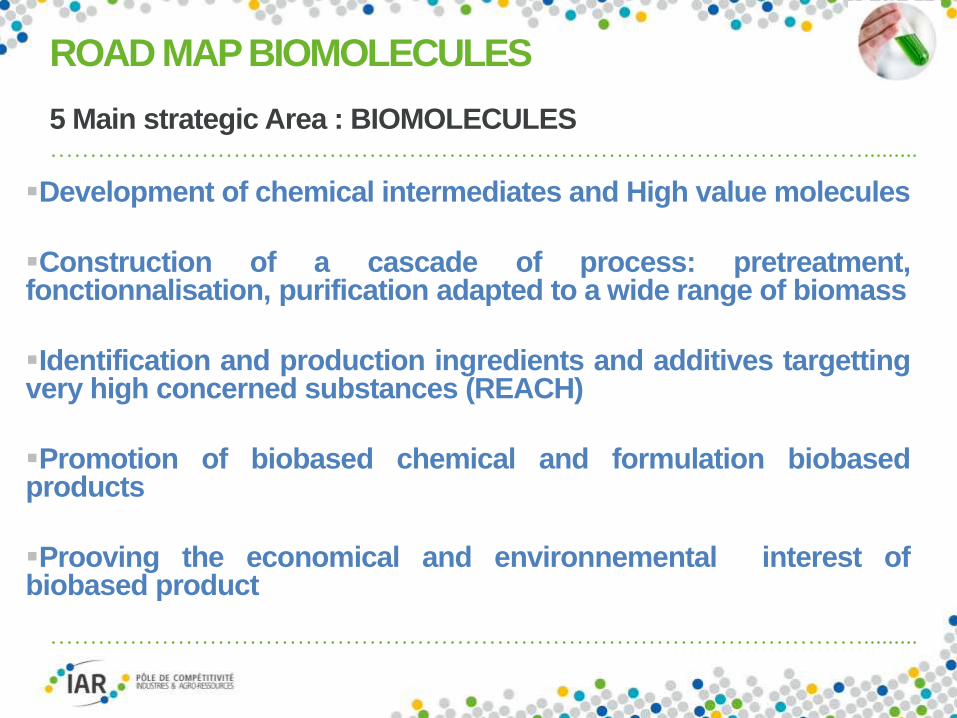

5 Main strategic Area : BIOMOLECULES

ROAD MAP BIOMOLECULES

▪Development of chemical intermediates and High value molecules

▪Construction of a cascade of process: pretreatment,fonctionnalisation, purification adapted to a wide range of biomass

▪Identification and production ingredients and additives targettingvery high concerned substances (REACH)

▪Promotion of biobased chemical and formulation biobasedproducts

▪Prooving the economical and environnemental interest ofbiobased product

………………………………………………………………………………………….........

………………………………………………………………………………………….........

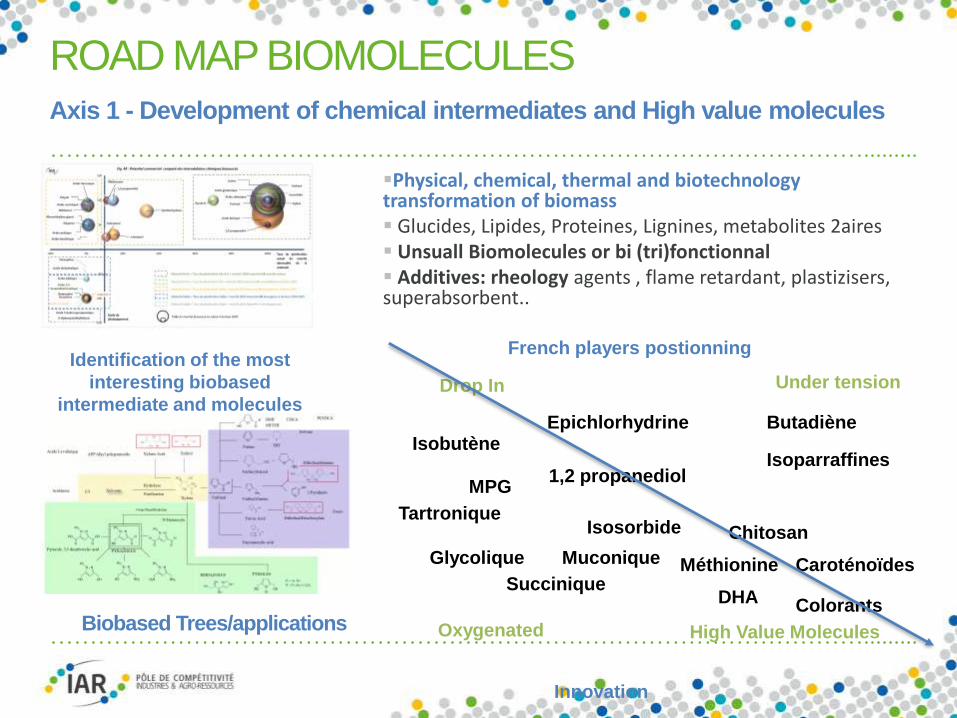

Axis 1 - Development of chemical intermediates and High value molecules

ROAD MAP BIOMOLECULES

Biobased Trees/applications

Identification of the most

interesting biobased

intermediate and molecules

Under tension

High Value Molecules

IsobutèneButadiène

Isoparraffines

Muconique

Chitosan

Drop In

Méthionine

▪Physical, chemical, thermal and biotechnologytransformation of biomass▪ Glucides, Lipides, Proteines, Lignines, metabolites 2aires▪ Unsuall Biomolecules or bi (tri)fonctionnal▪ Additives: rheology agents , flame retardant, plastizisers, superabsorbent..

French players postionning

Innovation

Isosorbide

Oxygenated

Caroténoïdes

ColorantsDHA

Epichlorhydrine

1,2 propanediol

Glycolique

Tartronique

MPG

Succinique

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Axis 2 - Construction of a cascade of process: pretreatment, fonctionnalisation, purification adapted to a wide range of biomass

ROAD MAP BIOMOLECULES

• Adaptating the process to biomass :

• Physical and chemical process (catalyse, reactions media, activations, molécules, variability and impurities)

• Biotechnology process : microorganisms and enzymes, hybride catalysis

• Down stream processing (DSP) : purification of a blend of molecules

• Identification of Scale-up bottlenecks (génie des procédés) « from the laboratory dream to the real industrialarea »

• KEY and Emerging Technologies (BIOKET), coupling technology, intensified process – future plante –green chemicals

Organosolv

Explosion à la vapeur - AFEX

Flash détente

Gazéification

Liquéfaction Hydrothermal

Pyrolyse

Torréfaction

Pretreatment Biomass

CEP (Champs Electriques Pulsés)

CO2 supercritique

DEHT (Décharges électriques de haute Tension)

Détente Instantannée Contrôlée

Eau Subcritique

Electrodyalyse

CPC (Chromatographie Partage Centrifuge)

Micro onde

Ultrasons et Sonochimie

Extrusion Reactive

Ionisation

Microreacteur

Photochimie

Plasma

Synthesis intensification Extraction - purification

Modelisation

………………………………………………………………………………………….........

………………………………………………………………………………………….........

ROAD MAP BIOMOLECULES

Axis 3 - Identification and production ingredients and additives targeting very high concerned substances (REACH)• Sheets VEGEREACH – substitution of very high concerned molecules

(phtalates, silicones, parabenes, isocyanates…)• Promotion of predictive tools on toxicity and ecotoxicity

Axis 4 - Promotion of biobased chemicals and formulation help of biobasedproducts• Agrobiobase• Workshop on Formulation of biobased products – cross fertilisation • Formulation tools, datas bases and Modelisation structure properties

▪Axis 5 - Prooving the economical and environnemental interest ofbiobased product

• IAR LCA and methodology coupled with MTD (best available technology)

Main strategic Area : BIOMOLECULES

………………………………………………………………………………………….........

………………………………………………………………………………………….........

The production capacities are mainly concentrated in North America for newmolecules and Asia for more mature molecules

A WORLD WIDE MARKET COMPETITION

• The highest TRL products have a very strong manufacturing presence in Asia

45 % Manufacturing Biobased chemical in China, 30

% USA, 15 % Europe, 10 % Brazil.

. Because of a lack of incentive policies, the share of

European production capacities is stagnating despite the

installation of many new pilot sites.

………………………………………………………………………………………….........

………………………………………………………………………………………….........

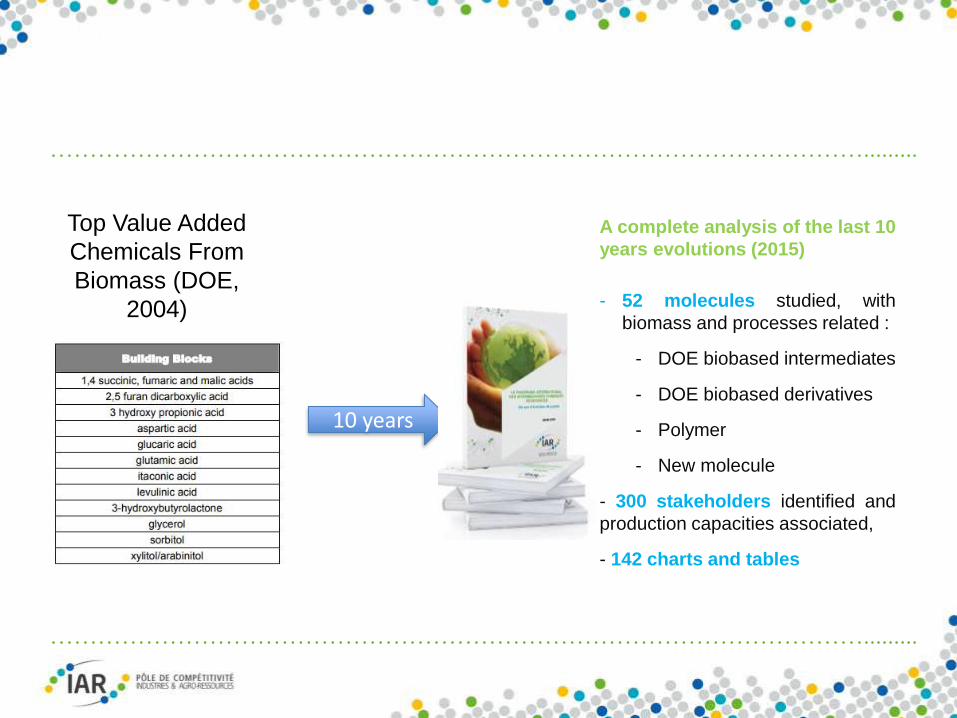

Top Value Added

Chemicals From

Biomass (DOE,

2004)

10 years

A complete analysis of the last 10

years evolutions (2015)

- 52 molecules studied, with

biomass and processes related :

- DOE biobased intermediates

- DOE biobased derivatives

- Polymer

- New molecule

- 300 stakeholders identified and

production capacities associated,

- 142 charts and tables

………………………………………………………………………………………….........

………………………………………………………………………………………….........

At the end of 2014 – the big picture

2007-2014 : A BOOMING INDUSTRY

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Pilot and demonstration unit building

2007-2014 : A BOOMING INDUSTRY

▪ On average between 2007 and 2014:

1,75 new molecule per year onpilot scale

0,25 new molecule per year ondemonstrator

9 pilot or demonstrator peryear (ethanol 2G including)

• Main interesting intermediate andderivates selected in the DOE study(2004) are produced to pilot scale

New molecule on demonstrationscale

New molecule on pilot scale

New pilot and demonstrationunits

………………………………………………………………………………………….........

………………………………………………………………………………………….........

IAR FRENCH PLAYERS – Scaling up - From pilot to Flagship

BIOBASED CHEMICAL INTERMEDIATES

BIOBUTYRIC

VALORIZATION BIOBUTYRIC ACID, coproduct 1,3 PDO

fermentation process

Process METABOLIC EXPLORER :

1,3 PDO, coproduct

BIOBUTYRIC market: fragrances, polymers, Foodsaromae: 50 000 MT - 75 M $

/ Y (1500 $/y) tonne

BioButadiene ISOSORBIDE Isobutene - Met

Catalytic Process

(Project BIOButterly)

Michelin

Applications : syntheticrubbers (60 % world production for tyre)

10,4 Mt/an

Shift naphta to gas => Tension on butadiene price

Sorbitol dehydratation

(Project BIOHUB)

ROQUETTE

Applications :plastiziserPC, PU, PE…BPA

alternative… Polycarbonate Isosorbide

Catalytic oxydation of Isobutene into

Methymetacrylate

(Project BIOMA +)

Global Bioenergie

Arkema

Applications : Coating , ciment…

shortage need increasecapacities in Europe

SOLVAY : Epichlorydine – sebasic PA 6,10

………………………………………………………………………………………….........

………………………………………………………………………………………….........

ROQUETTE - World largest production of isosorbide

EX : PERFORMANCE BIOBASED MATERIAL

High performance

………………………………………………………………………………………….........

………………………………………………………………………………………….........

FRENCH PLAYERS – Scaling up - From pilot to Flagship

BIOBASED CHEMICAL INTERMEDIATES (2)

Glycolic

Catalytic Process to convert glycerol to Glycolic acid

(Project GENESYS)

PIVERT

Application : polyglycolic or biocompatibles polymers as PLGA [i.e., poly(lactic-co-

glycolic acid)],

Polymer Market > 500 000 T ; solvents and ink

(fluidifiantes properties) ; • cosmetic

MethylTHF Succinic Carotenoids

FURFURAL AS A BUILDING BLOCK

(Projects)

Applications: MeTHFSolvents , produced from

agricultural by-products

FFA : China (70%) - 150000 MT/year, 65 units - Rép

Dominicain (11%) - 1170 $/t

Biosuccninc

(Projet Acosite)

ROQUETTE

Scaling up ARD (BIOAMBER)

Optimization of CAROTENOIDS production

(Project DEINOCHEM).

DEINOVE

Market Carotenoïds : Dying

and antioxydantes

1,8 billions $ (2019)

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Biobased Products coming from Projects IAR

INNOVATION BIOMOLECULES

BioSolvents

DEGREASING ECOFRIENDLY SOLVENT

(Projet DELTA 3).

Versatile / Multifunctions:

Solvent - Dégreassing - Tar -

- Depolluating

BioLubrificants Biobased Resines Biobased Coating

« LUBA 18 »

(Projet AGROLUB)

Range of lubricants extremepression for the metal work

Range of resinesunsaturated polyester

ENVIROGUARD®

(Project Acosite)

Estetic® BioAir

(Project Sorago)

Coil coating

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Afyren scaling up - 70 000 liters

AFYNERIE

Afyren has realized proof of concept in validating its technology

for a volume 70 000 litres at Cristal Union à Clermont-Ferrand,

from some tonnes of sugar coproducts to hundred Kg of biobased

carboxylic acid for nutrition, chemestry and cosmetic: acide

acetic, propionic, butyric, isobutyric, valeric, isovaleric

caproïc.

fermentation de 3 m3,

………………………………………………………………………………………….........

………………………………………………………………………………………….........

1,3 PDO / Acid Butyric Metabolic Explorer Plant

NEXT PLANT –LONG WAY FROMLABTO REAL INDUSTRY

V.0 2007 V.1 2010 V.2 2014 V.3 2017 V.4 2020

Lab strain(pure

glycerol)

Metabolicengineering

(clostr acet) ana continuous

Industrialstrain (crude

glycerine)

Coproduction AB – Effluent treatments

Continuousimprovment

Development of process separation and purification (Processium)Design

Plant Phase 1 :

5 KT PDO + 1 KT AB

for 2020 on Carling – 25 M€

COPRODUCTION BUTYRIC ACIDDecrease 40 % DCO

Acces to specific market

WASTE WATER TREATMENT

- Biogas- Ammonium Sulfate as fertilizer

20 % OPEX

Cost competitive

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Highly functional and chiral platform molecule Levoglucosenone

THE NEXT BIOBASED BUILDING BLOCKS

In partnership with:

2014 – today : some companies have high exposure to oil price

Shale gas

Low exposure – most of time biomass is competitive

High exposure to oil price –biomass can be competitive

Drop in

New functionnalities

No exposure – biomass isvery competitive

Exposure to oil price

Very High exposure to oil price –biomass theoretically no competitive

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Strategy after 12 years development / low price oil

DEVELOPPING TOGETHER THE BIOECONOMY

➢ Targetting Chemical Intermediates, preferently very High concerrned molecules replacement, oxygenated and high value biomolecules which cannot be effectively accessed from petrochemical feedstocks, with a wide range of valuable chemicals, which can be obtained by minimal steps

➢ Developping the Second Generation of biomolecules derivatives based on mature chemicalintermediates (going back to the laboratory)

➢ Finding new properties of materials made with biobased chemicals (modelisation - relation structure/ properties from chemical intermediates to material performance)

➢ Keep on opening the chemical intermediates outlets, formulation additives, and working on positionning the Biobased derivatives properties (solvent or surfactants cartography) /vs oilproduct

➢ Future Process : think about hybrid catalysis, but also the process and scaling up…

➢ Still Catalytic Process to update from biomass (ex: cellulose derivatives for cosmetic applications)

………………………………………………………………………………………….........

………………………………………………………………………………………….........

PROJECTS SUMMARY 2017Projects with IAR Label / financed project

• 35 Projects with IAR Label• 33 Projects Funded (Budget 106 M€)

within 2 BBI Success rate : 80 % (ANR compris)

PROJECTS LABELLISED et FINANCED (since 2005)

• Nbre projects labellised et financed : 270

• Budget: 1,7 Milliards €

• Public founding : 572 Millions €

• Publications : 714

• Patents : 186

• Products et process : 106

Répartition par Projets Financés 2017 (en nombre)

REGION12%

FUI3%

ANR ET ANRT25%

GRAINE21%

PROJETS STRUCTURANTS

21%

EUROPE18%

REGION FUI ANR ET ANRT GRAINE PROJETS STRUCTURANTS EUROPE

BIOMOLECULES43%

BIORAFFINERIE3%

INGREDIENTS24%

METHANISATION6%

RESSOURCES BIOLOGIQUES

15%

MATERIAUX BIOSOURCES

9%

BIOMOLECULES BIORAFFINERIE

INGREDIENTS METHANISATION

RESSOURCES BIOLOGIQUES MATERIAUX BIOSOURCES

………………………………………………………………………………………….........

………………………………………………………………………………………….........

INNOVATION AXIS –PROJECTFINANCED IN 2017 (EXAMPLES)

• Exploration strategy and valorization of the biomass biomolecules: Algaes (Projets I-chem algae, SPIRAL G et ZYMALGO), Forest (Projet Extraforest)

• New biobased chemical (Projet OPTISOCHEM, isobutene 2G ou EBONITE) - high value market (SINAPUV, antiUV cosmetic ou Crytose cages)

• Development of high performance biobased materials and recycling (Project BITUME 2 .0 bitume based on plant oil recycling

• Fish protein with insectes (PROTEIN)

………………………………………………………………………………………….........

………………………………………………………………………………………….........

BBI

PROJET SPIRALG

Production of phytocyanin from the Spirula Arthospira sp. Revisiting the sourcing, the extraction and the co-valorization of the whole algae in the frame of an industrial biorefinery concept and a business model strategy

• Demonstration plant -10 MT of phycocyanin per year / 100 MT world market

• Blue chemical colorants authorized are toxic, look for natural solutions, 4 China competitors with bigger production capacity, any producer in Europe, already approved by FDA and EC and sold for food and cosmetics and pharmaceuticals

Coordinator : Greensea (34 -extraction and separation treatment and drying of phycocyanin)

•Partners : MICROLIFE (spirulina) - ALGAIA (valorization of the coproducts) - MIAL (LCC,valorization of the coproducts) - UCD (LCA)

Budget : 5,6 M€ – Finance: 4,05 M€ - Period : 4 years

………………………………………………………………………………………….........

………………………………………………………………………………………….........

ADEME - GRAINE

PROJET ZYMALGO

Algae Biorefinerie : microalgae valorization by biocatalytic green process

• Thesis LIBio BIOLIE on the structural diversity of microalgae walls• Aquaous Enzym Extraction of High Value Molecules (with if necessary microwaves,

ultrasons to increase yield). Energy cost Reduction (no need to dry biomass), low environnemental impact

• High through put Screening of enzym cocktails (hydrolysis^parietal compounds) adapted of microalgaes and extracts required

• Production of innovative extracts (thanks to enzyms) for cosmetic market

Coordinator : BIOLIE (technologie d’extraction enzymatique brevetée)

Parteners : University of Lorraine (Laboratoire d’ingénierie des biomolécules)

Budget : 600 562 € – fund: 327 955 € - Duration : 3 year

………………………………………………………………………………………….........

………………………………………………………………………………………….........

AAP « Innovation et investissements pour l’amont forestier » du MAAP

PROJET EXTRAFOR_EST

Wood Extractibles from Est Forest– Socio-economical assessment of a value chain to valorize the chemical deversity of wood

extractibles…. not well known ...

– Species: sapin, épicéa, chêne, Douglas... Terpen and phenolic family (lignanes, flavonoïdes, stilbènes, tanins…) … anti-oxydative, antimicrobial properties…applications pharmaceutic, cosmetic, nutraceutic...

– Variability assessment of the extractibles in trees and industrials coproducts (mobilisable)

– Animation – Promotion - dissemination

Coordinator : UMR 1092 INRA-AgroParisTech - Laboratoire d'Etude des Ressources FOrêt-Bois

(Nancy)

Partners : LERFOB et le LERMAB, l’IGN (Institut Géographique National), le LEF (Laboratoire

d’économie forestière ; INRA Grand-Est) et le LOSI (Laboratoire d’optimisation des systèmes industriels de l’UTT).

Budget : 1 M€ – Finance: € - Duration : 3 year

………………………………………………………………………………………….........

………………………………………………………………………………………….........

ADEME - AAP Chimie du végétal et matériaux biosourcés

PROJET SYLCHEM

Démontrer la viabilité technico-économique d’un procédé de traitement de la biomasse végétale

• Demo Plant 5 000 T / year of biomass at Golbey

•To convert wood and paper into chemical : succinique, lactique, propylène glycol, polyols….

•Additionnal to the Project BBI SYLFEED, production of proteins for aquaculture with lignocellulose (10,9 M€ Arbiom)

Coordinator : ARBIOM (scale-up du procédé de valorisation de la biomasse végétale et développement des produits biosourcés)

Partenaires : NORSKE SKOG ( biomass supply and Demo to Golbey) - Prayon (recycling phosphoric acid)

Soprema (conversion lignine en polyols)

Budget Global : 22 M€ – Aide Demandée : 4 M€ - Durée : 3 ans

………………………………………………………………………………………….........

………………………………………………………………………………………….........

ANR

PROJET SINAPUV

(Bio)synthesis and study of physico-chemical/biological properties of sinapoylmalate analogues: non-toxic and biobased anti-UV compounds for cosmetics industry•Anti-UV compounds represent a huge market in the cosmetics industries for their capacity to protect humans from sun damages. Market size sun protection = 100 000 T.

•Unfortunately, current anti-UV compounds used in cosmetics (e.g., octinoxate) are made fromfossil oil, very high concerned biomolecules and allergens .

•Development of similar to malate sinapoyl. With anti UV-B properties, but not enoughquantitity for plant extraction way - Synthesis of sinapics acids and sinapoyl malates by biotechnology and DSP step

Coordinator : Chaire ABI (51)

Parteners : UMR INRA AGROPARITECH MICALIS (biologie synthèse) – INSERM U1194 (Perturbateur endocrinien)– Abolis BIotech (91) – Givaudan Active Beauty (95)

Budget Global : 2 197 724 € – Financement : 738 946 € - Durée : 4 ans

Octinoxate

Anti UV

………………………………………………………………………………………….........

………………………………………………………………………………………….........

ADEME - GRAINE

PROJET BITUME2.0

Development and characterisation of a biobased binder to replace bituminunen oil source, using biomass coproducts-

• For the formulation of road and roof materials with recycling Raw Materials (Food and oilplant refineries coproducts)

• Scientific challenge : imitate the properties of bituminen : liquide> 100 C, viscoelasticity -20 C et 60 °C,…

• Using process hydrothermal liquefaction to transform biomass in hydrophobic compounds. • And Chemical process to increase molecular weight and viscosity of oil plant derivatives.

Porteur : COLAS (78- leader mondial de la construction routière)

Partenaires : Ifsttar (44-acteur majeur de la recherche sur les liants pour le génie civil), CEISAM (Univ Nantes chimie et caractérisation des matériaux), ITERG (modifications chimiques des coproduits huileux) - CEA Liten (développement Liquéfaction Hydrothermal)...

Budget : 890 773 € – Aide Demandée : 399 905 € - Durée : 3 ans

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Examples Biobased Product and Process Bioinspired

BIOBASEDAND BIOINSPIRED INNOVATION

When the sea light us !

Biomimetism approach to

hydrolyse biomass Efficiently

Efficient Bionic agitator

for mixing fluids !

Anti-reflective coating

made from sucrose

Worm protein

Cybernose !

………………………………………………………………………………………….........

………………………………………………………………………………………….........

Anf if we did not need electricity to make light ?

GLOWEE, THAT ISTHE SEAWHICH LIGHT US ?

•90 % sea microorganisms, algaes, Jellyfish, squid, fish….Bioluminescence, chemical reactionregulated by a gene, which allow Light …

•Gene put in a Bacteria and plastic shell with it nutritionnal liquid…end of life

•Market : Soft Light, with no connections, for Shop windows, urban landscape, eventcommunications…

•Regulation : Prohibition illumination of non residential building !

………………………………………………………………………………….

IAR cluster

Thank you for your attention !

Jacky VANDEPUTTE

R&D Project

BIOBASED CHEMICAL

Tel : 03 23 23 97 51