ias 32 39 chapter21 financialinstruments2007 gripping ifrs 2008 by icap

TRANSCRIPT

Gripping IFRS Financial instruments

Chapter 21

646

Chapter 21

Financial Instruments

Reference: IAS 32; IAS 39 and IFRS 7 Contents:

Page

1. Introduction

648

2. Definitions Example 1: financial assets Example 2: financial liabilities

648 648 649

3. Financial Risks 3.1 Overview 3.2 Market risk

3.2.1 Interest rate risk 3.2.2 Currency risk 3.2.3 Price risk

3.3 Credit risk 3.4 Liquidity risk

649 649 649 649 649 650 650 650

4. Derivatives 4.1 Options 4.2 Swaps

Example 3: swaps 4.3 Futures

650 650 650 650 651

5. Compound financial instruments Example 4: splitting of compound financial instruments Example 5: compulsorily convertible preference shares Example 6: redeemable debentures issued at a discount

651 652 653 654

6. Categories of financial liabilities 6.1 Overview 6.2 Financial liabilities measured at fair value through profit and loss

Example 7: fair value through profit and loss 6.3 Financial liabilities not measured at fair value through profit and loss

Example 8: other financial liabilities

656 656 656 657 657 657

7. Categories of financial assets 7.1 Overview 7.2 Fair value through profit or loss

Example 9: fair value through profit or loss financial assets 7.3 Held to maturity financial assets

Example 10: held to maturity 7.4 Loans and receivables

Example 11: loans and receivables 7.5 Available for sale financial assets

Example 12: available for sale

658 658 658 658 659 659 659 660 660 660

Gripping IFRS Financial instruments

Chapter 21

647

Contents continued:

Page

8. Reclassification of financial instruments 8.1 Overview 8.2 Fair value through profit or loss 8.3 Held to maturity 8.4 Available for sale 8.5 Instruments previously measured at amortised cost

661 661 661 661 661 661

9. Impairment of financial instruments

661

10. Offsetting of financial assets and liabilities

661

11. Disclosure Example 13: disclosure of financial instruments

662 663

12. Summary

666

Gripping IFRS Financial instruments

Chapter 21

648

1. Introduction Most students find the financial instruments section very difficult, but by simply learning and understanding the various definitions and rules, it will be made a lot easier. The IAS and IFRS standards covering the recognition, measurement and disclosure of financial instruments are very long, and therefore this chapter contains only the most important aspects.

2. Definitions The definitions that follow may be found in IAS 32 and 39. Financial instrument: is any contract that gives rise to a financial asset in one entity and a financial liability or equity instrument in another. The contract need not be in writing. An equity instrument: is any contract that results in a residual interest in the assets of an entity after deducting all of its liabilities A financial asset: is any asset that is: • cash; • an equity instrument of another entity; • a contractual right to receive cash or another financial asset from another entity; • a contractual right to exchange financial instruments with another entity under conditions

that are potentially favorable to the entity; or • a contract that will or may be settled in the entity’s own equity instruments and is: - a non-derivative for which the entity is or may be obliged to receive a variable number of

the entities own equity instruments; or - a derivative that will or may be settled other than by the exchange of a fixed amount of

cash or another financial asset for a fixed number of the entity’s own equity instruments. A financial liability: is a liability that is: • a contractual obligation to deliver cash or another financial asset to another entity; • a contractual obligation to exchange financial instruments with another entity under

conditions that are potentially unfavorable to the entity; • a contract that will or may be settled in the entity’s own equity instruments and is: - a non-derivative for which the entity is or may be obliged to deliver a variable number of

the entity’s own equity instruments; or - a derivative that will or may be settled other than by the exchange of a fixed amount of

cash or another financial asset for a fixed number of the entity’s own equity instruments. Compound instruments: are instruments that contain both a liability and equity component. A derivative: is a financial instrument or other contract with all three of the following characteristics: • its value changes in response to a change in a specified interest rate, financial instrument

price, foreign exchange price etc; • it requires no initial net investment or an initial net investment that is smaller than would

be required for other types of contracts that would be expected to have a similar response to changes in market factors; and

• is settled at a future date. Derivatives are commonly used to manage financial risks. Example 1: financial assets Discuss whether any of the following are financial assets: a. Inventory b. Debtors c. Cash d. Property, plant and equipment

Gripping IFRS Financial instruments

Chapter 21

649

Solution to example 1: financial assets a. No, there is no contractual agreement to receive cash or otherwise simply by holding stock. b. Yes, there is a contractual right to receive a payment of cash from the debtor. c. Yes, it is cash d. No, there is no contractual right to cash or another instrument by owning property, plant and

equipment. Example 2: financial liabilities Discuss whether any of the following are financial liabilities: a. Creditors b. Redeemable preference shares c. Warranty obligations d. Bank loans Solution to example 2: financial liabilities a. Yes, the entity is contractually obligated to settle the creditor with cash. b. Yes, the entity must, in the future, redeem the preference shares with cash. c. If the entity has to pay the warranty obligation in cash, it is a financial liability. If the entity

merely has to repair the goods, then, since there is no obligation to pay cash or any other financial instrument, it is not a financial liability.

d. Yes, there is a contractual obligation to repay the bank for the amount of cash received plus interest.

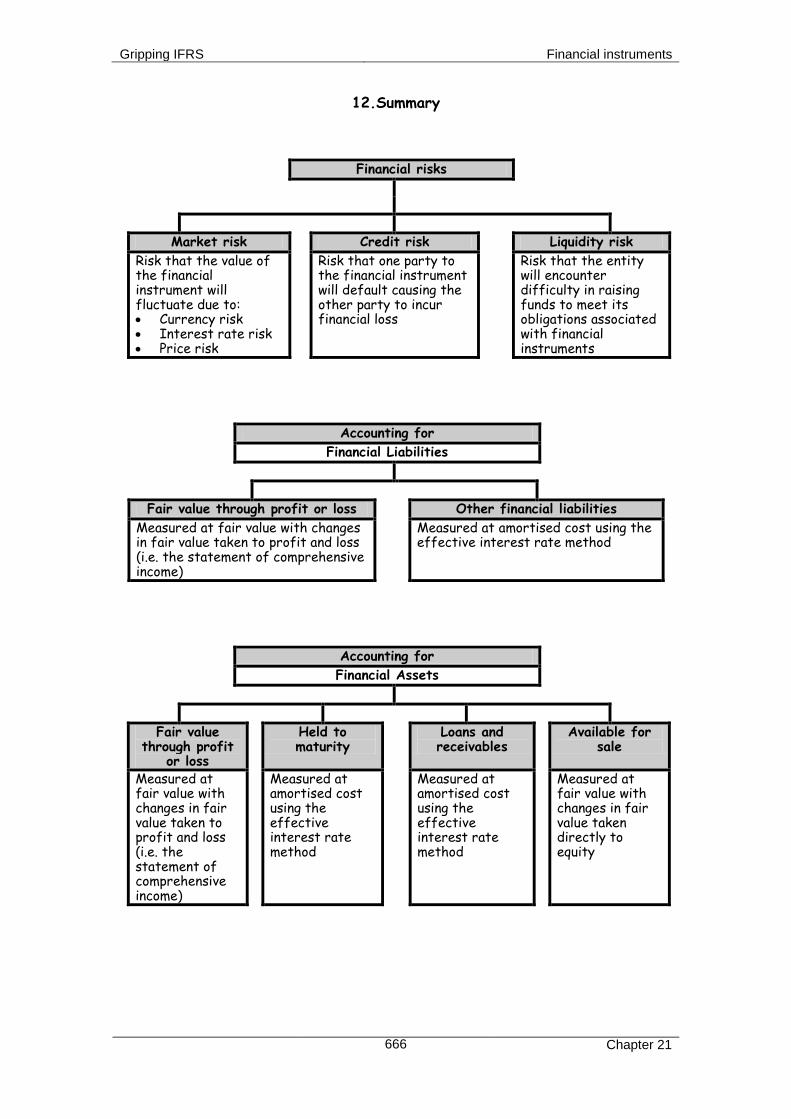

3. Financial risks

3.1 Overview There are three categories of financial risks and they are: • market risk (affected by price risk, interest rate risk and currency risk); • credit risk; and • liquidity risk. 3.2 Market risk (IFRS7; Appendix A) Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market prices. Market risk comprises of: • interest rate risk; • currency risk; and • other price risk. 3.2.1 Interest rate risk Interest rate risk is the risk that the value of the instrument will fluctuate with changes in the market interest rate. A typical example is a bond: a bond of C100 earning a fixed interest of 10% (i.e. C10) would decrease in value if the market interest rate changed to 20%, (theoretically, the value would halve to C50: C10/ 20%). If the bond earned a variable interest rate instead, the value of the bond would not be affected by interest rate fluctuations.

3.2.2 Currency risk Currency risk is the risk that the value of the instrument will fluctuate because of changes in the foreign exchange rates. A typical example would be where we have purchased an asset from a foreign supplier for $1 000 and at the date of order, the exchange rate is $1: C10, but where the local currency weakens to $1: C15. The amount owing to the foreign creditor has now grown in local currency to C15 000 (from C10 000).

Gripping IFRS Financial instruments

Chapter 21

650

3.2.3 Price risk Price risk is the risk that the value of the financial instrument will fluctuate as a result of changes in the market prices. For example: imagine that we committed ourselves to purchasing 1 000 shares on a certain date in the future, when the share price was C10 on date of commitment. By making such a commitment, we would be opening ourselves to the risk that the share price increases (e.g. if the share price increased to C15, we would have to pay C15 000 instead of only C10 000). 3.3 Credit Risk This is the risk that the one party to a financial instrument will fail to discharge an obligation and cause the other party to incur a financial loss. A typical example is a debtor, being a financial asset to the entity, who may become insolvent and not pay the debt due (i.e. where a debtor becomes a bad debt). 3.4 Liquidity Risk This is the risk that the entity will encounter difficulty in raising funds to meet commitments associated with the financial instrument. An example would be where we (the entity) found ourselves with insufficient cash to pay our suppliers (i.e. where we become a bad debt to one of our creditors).

4. Derivatives There are many types of derivatives of which we discuss a few: 4.1 Options An option gives the holder the opportunity to buy or sell a financial instrument on a future date at a specified price. The most common option that we see involves options to buy shares on a future date at a specific price (strike price). These are often granted to directors or employees of companies. Another example is an option to purchase currency on a future date at a specific exchange rate. Options may be used to limit risks (as the exercise price of an option is always specified) or they may be used for speculative purposes (i.e. to trade with). 4.2 Swaps A swap is when two entities agree to exchange their future cash flows relating to their financial instruments with one another. A common such agreement is an ‘interest rate swap’. For example, one entity (A) has a fixed-rate loan and another entity (B) has a variable-rate loan. The two entities may agree to exchange their interest rates if A would prefer a variable rate and B would prefer a fixed rate. Example 3: swaps Company A has a loan of C100 000 with a fixed interest rate of 10% per annum. Company B has a loan of C100 000 with a variable interest rate, which is currently 10% per annum. Company A and Company B agree to swap their interest rates. The variable rate changed to 12% in year 2. The variable rate changed to 8% in year 3. Required: Journalise the receipts/ payments of cash in Company A’s books for year 2 and year 3.

Gripping IFRS Financial instruments

Chapter 21

651

Solution to example 3: swaps Debit Credit Year 2 Interest expense (finance charges) 10 000 Bank 10 000 Interest on fixed rate loan paid to lender: 100 000 x 10% Interest expense (finance charges) 2 000 Bank 2 000 Difference between variable and fixed rate loan paid to Company B: 100 000 x (12% - 10%)

Year 3 Interest expense (finance charges) 10 000 Bank 10 000 Interest on fixed rate loan paid to lender: 100 000 x 10% Bank 2 000 Interest income 2 000 Difference between variable and fixed rate loan received from Company B: 100 000 x (12% - 10%)

4.3 Futures A future is an agreement by the entity to buy a specified type and quantity of a financial instrument on a specified future date at a specified price. For example, if A does not have the cash to purchase shares immediately but believes that they are a worthwhile investment, it may enter into a futures contract with another entity (B) whereby A commits to buying them on a future date. The difference between a future and an option is that a future commits the entity whereas an option does not.

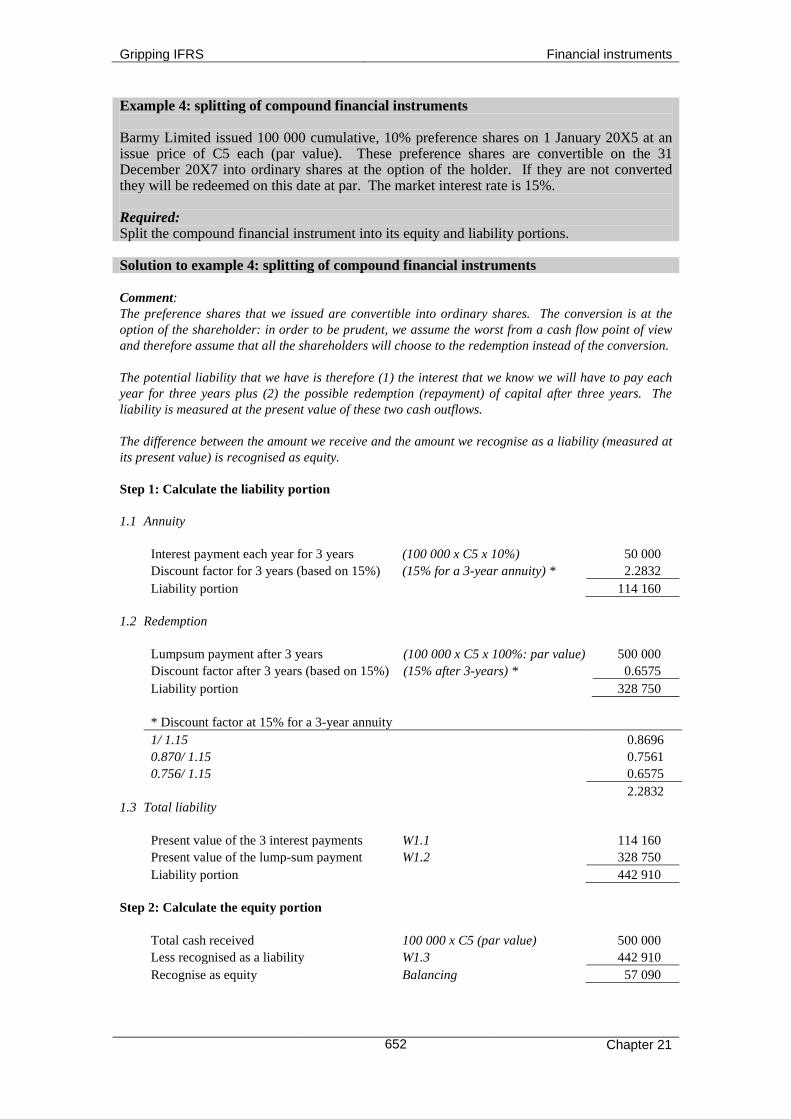

5. Compound financial instruments (IAS 32.15 - .16) Some financial instruments have both equity and liability portions. These are referred to as compound instruments. These instruments must be split into the two separate elements based on their substance rather than on their legal form. The difference between equity and liabilities is that: • liabilities involve a contractual obligation to deliver cash or exchange financial

instruments with another entity under conditions that are potentially unfavorable; whereas • equity involves no such obligation. The method used to split a compound financial instrument is: • first: find the value of the liability portion; and • then: balance back to the equity portion (the total value – the value of the liability). It must be remembered that the classification of an instrument in the statement of financial position will affect other financial statements too: if, for example, a financial instrument such as preference shares is treated as partly equity and partly liability, then the portion of the preference dividend that relates to the equity component will be recognised as a dividend in the statement of changes in equity, but the portion of the dividend that relates to the liability component will be recognised as interest (finance costs) in the statement of comprehensive income.

Gripping IFRS Financial instruments

Chapter 21

652

Example 4: splitting of compound financial instruments Barmy Limited issued 100 000 cumulative, 10% preference shares on 1 January 20X5 at an issue price of C5 each (par value). These preference shares are convertible on the 31 December 20X7 into ordinary shares at the option of the holder. If they are not converted they will be redeemed on this date at par. The market interest rate is 15%. Required: Split the compound financial instrument into its equity and liability portions. Solution to example 4: splitting of compound financial instruments Comment: The preference shares that we issued are convertible into ordinary shares. The conversion is at the option of the shareholder: in order to be prudent, we assume the worst from a cash flow point of view and therefore assume that all the shareholders will choose to the redemption instead of the conversion. The potential liability that we have is therefore (1) the interest that we know we will have to pay each year for three years plus (2) the possible redemption (repayment) of capital after three years. The liability is measured at the present value of these two cash outflows. The difference between the amount we receive and the amount we recognise as a liability (measured at its present value) is recognised as equity. Step 1: Calculate the liability portion 1.1 Annuity

Interest payment each year for 3 years (100 000 x C5 x 10%) 50 000 Discount factor for 3 years (based on 15%) (15% for a 3-year annuity) * 2.2832 Liability portion 114 160

1.2 Redemption

Lumpsum payment after 3 years (100 000 x C5 x 100%: par value) 500 000 Discount factor after 3 years (based on 15%) (15% after 3-years) * 0.6575 Liability portion 328 750

* Discount factor at 15% for a 3-year annuity 1/ 1.15 0.8696 0.870/ 1.15 0.7561 0.756/ 1.15 0.6575 2.2832

1.3 Total liability

Present value of the 3 interest payments W1.1 114 160 Present value of the lump-sum payment W1.2 328 750 Liability portion 442 910

Step 2: Calculate the equity portion

Total cash received 100 000 x C5 (par value) 500 000 Less recognised as a liability W1.3 442 910 Recognise as equity Balancing 57 090

Gripping IFRS Financial instruments

Chapter 21

653

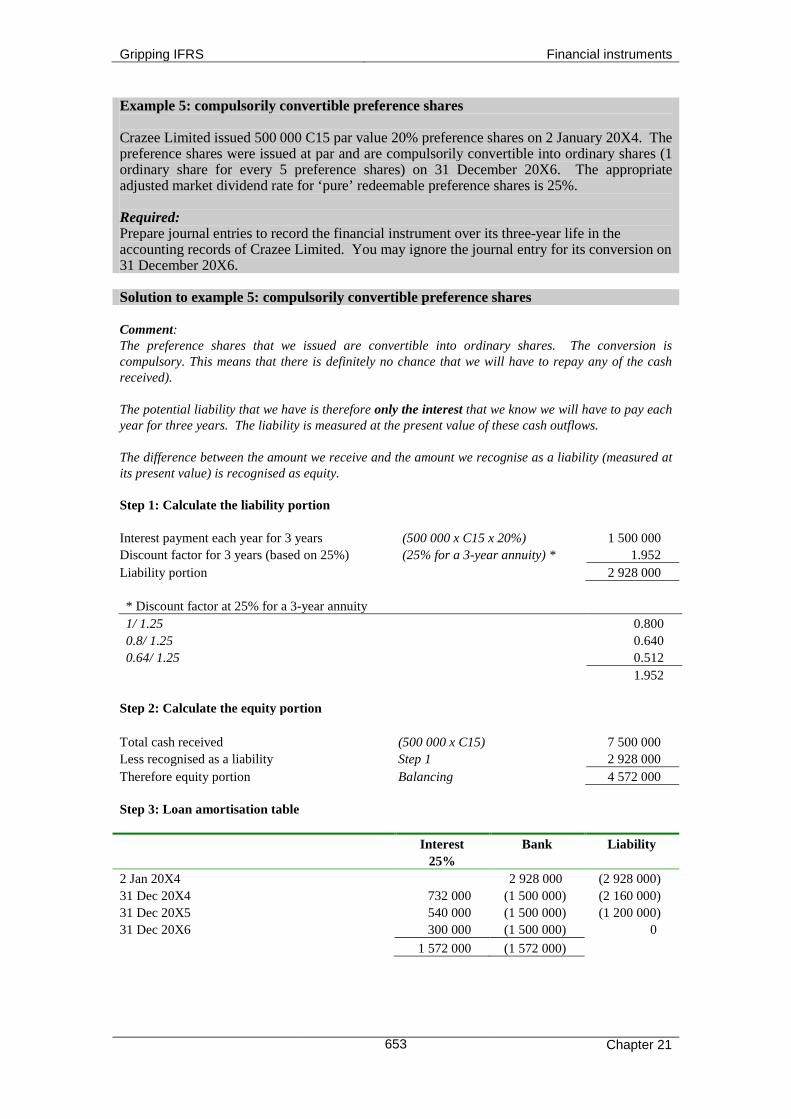

Example 5: compulsorily convertible preference shares Crazee Limited issued 500 000 C15 par value 20% preference shares on 2 January 20X4. The preference shares were issued at par and are compulsorily convertible into ordinary shares (1 ordinary share for every 5 preference shares) on 31 December 20X6. The appropriate adjusted market dividend rate for ‘pure’ redeemable preference shares is 25%. Required: Prepare journal entries to record the financial instrument over its three-year life in the accounting records of Crazee Limited. You may ignore the journal entry for its conversion on 31 December 20X6. Solution to example 5: compulsorily convertible preference shares Comment: The preference shares that we issued are convertible into ordinary shares. The conversion is compulsory. This means that there is definitely no chance that we will have to repay any of the cash received). The potential liability that we have is therefore only the interest that we know we will have to pay each year for three years. The liability is measured at the present value of these cash outflows. The difference between the amount we receive and the amount we recognise as a liability (measured at its present value) is recognised as equity. Step 1: Calculate the liability portion Interest payment each year for 3 years (500 000 x C15 x 20%) 1 500 000 Discount factor for 3 years (based on 25%) (25% for a 3-year annuity) * 1.952 Liability portion 2 928 000 * Discount factor at 25% for a 3-year annuity 1/ 1.25 0.800 0.8/ 1.25 0.640 0.64/ 1.25 0.512 1.952

Step 2: Calculate the equity portion Total cash received (500 000 x C15) 7 500 000 Less recognised as a liability Step 1 2 928 000 Therefore equity portion Balancing 4 572 000 Step 3: Loan amortisation table Interest Bank Liability 25% 2 Jan 20X4 2 928 000 (2 928 000) 31 Dec 20X4 732 000 (1 500 000) (2 160 000) 31 Dec 20X5 540 000 (1 500 000) (1 200 000) 31 Dec 20X6 300 000 (1 500 000) 0 1 572 000 (1 572 000)

Gripping IFRS Financial instruments

Chapter 21

654

Journals Debit Credit 2 January 20X4 Bank 7 500 000 Financial liability (preference shares) 2 928 000 Preference share equity 4 572 000 Issue of convertible preference shares 31 December 20X4 Finance costs 732 000 Financial liability (balancing) 768 000 Bank 1 500 000 Payment of preference dividend 31 December 20X5 Finance costs 540 000 Financial liability (balancing) 960 000 Bank 1 500 000 Payment of preference dividend 31 December 20X6 Finance costs 300 000 Financial liability (balancing) 1 200 000 Bank 1 500 000 Payment of preference dividend Example 6: redeemable debentures issued at a discount On 2 January 20X4, Redvers Limited issued 10 000 C500 par value debentures, at a discount of C100 on par value, details of which are as follows: • These debentures are compulsorily redeemable at a premium of 10% over par value, 4

years later. • The debentures bear interest at 15% per annum payable in arrears. • The internal rate of return on the debentures is 25.23262%. Required: Prepare journal entries to record the financial instrument over its three-year life in the accounting records of Redvers Limited. Solution to example 6: redeemable debentures issued at a discount Comment: The debentures that we issued are redeemable. There is no possibility of conversion and therefore there is definitely no equity component. The liability that we have is therefore (1) the interest that we know we will have to pay each year for four years plus (2) the definite redemption (repayment) of capital after four years. The liability is measured at the present value of these two cash outflows. The difference between the amount we receive and the amount we recognise as a liability (measured at its present value) is recognised as equity. This will work out to zero since the issue price will have been worked out based on our rate of return combined with the 15% interest cost and the 10% premium.

Gripping IFRS Financial instruments

Chapter 21

655

Step 1: Calculate the liability portion 1.1 Annuity

Interest payment each year for 4 years (10 000 x C500 x 15%) 750 000 Discount factor for 4 years (for 25.23262%) (25.23262% for a 4-year annuity)* 2.3518567 Liability portion 1 763 890

1.2 Redemption

Lumpsum payment after 4 years (10 000 x C500 x 110%) 5 500 000 Discount factor after 3 years (for 25.23262%) (15% after 3-years) * 0.4065654 Liability portion 2 236 110

* Discount factor at 25.2326% for a 4-year annuity 1/ 1.252326 0.7985141 0.7985/ 1.252326 0.6376248 0.6376/ 1.252326 0.5091524 0.5092/ 1.252326 0.4065654 2.3518567

1.3 Total liability

Present value of the 4 interest payments W1.1 1 763 890 Present value of the lump-sum payment W1.2 2 236 110 Liability portion 4 000 000

Step 2: Calculate the equity portion (not required: there can be no equity since these are compulsorily redeemable: calculation provided for interest)

Total cash received 10 000 x C400 (issue value) 4 000 000 Less recognised as a liability W1.3 4 000 000 Recognise as equity Balancing 0

Step 3: Loan amortisation table Interest Bank Liability 25.23262% 2 Jan 20X4 4 000 000 4 000 000 31 Dec 20X4 1 009 305 (750 000) 4 259 305 31 Dec 20X5 1 074 734 (750 000) 4 584 039 31 Dec 20X6 1 156 673 (750 000) 4 990 712 31 Dec 20X7 1 259 287 (750 000) 5 500 000 (5 500 000) 4 500 000 (4 500 000) Journals Debit Credit 2 January 20X4 Bank 4 000 000 Financial liability debentures 4 000 000 Issue of convertible preference shares

Gripping IFRS Financial instruments

Chapter 21

656

Journals continued … Debit Credit 31 December 20X4 Finance costs 1 009 305 Financial liability (balancing) 259 305 Bank 750 000 Finance costs on debentures 31 December 20X5 Finance costs 1 074 734 Financial liability (balancing) 324 734 Bank 750 000 Finance costs on debentures 31 December 20X6 Finance costs 1 156 673 Financial liability (balancing) 406 673 Bank 750 000 Finance costs on debentures 31 December 20X7 Finance costs 1 259 287 Financial liability (balancing) 509 287 Bank 750 000 Finance costs on debentures Financial liability 5 500 000 Bank 5 500 000 Redemption of debentures

6. Categories of financial liabilities 6.1 Overview (IAS 39.9 and .43) There are two main categories of financial liabilities, classified based on how they are measured. Financial liabilities may be measured at: • Fair value through profit or loss; or • Not at fair value through profit or loss (‘other financial liabilities’). Measurement of financial liabilities that are classified as fair value through profit or loss does not include transaction costs. Financial liabilities that are not classified as fair value through profit and loss are initially recognised at the fair value of the consideration received, net of transaction costs. For example if debentures were issued for C100 000, with C1 000 transaction costs, the entity would have received a net amount of C99 000 and therefore the debentures would be recognised at C99 000 in the statement of financial position. 6.2 Financial liabilities that are measured at fair value through profit or loss (IAS

39.9) These financial liabilities are essentially liabilities that are: • held for trading (i.e. purchased with the intention to sell or repurchase in the short term;

derivatives other than hedging instruments or are part of a portfolio of financial instruments where there is a recent actual evidence of short-term profiteering or are derivatives); or

• designated by the entity as fair value through profit and loss. This designation is only allowed where it provides more relevant information:

Gripping IFRS Financial instruments

Chapter 21

657

• through eliminating measurement or recognition inconsistency, or • because the financial liability is evaluated by the entity’s key management personnel

(e.g. board of directors) on a fair value basis in accordance with its documented risk management or investment strategy.

The designation of fair value through profit and loss is not allowed if • the contract including the financial liability includes embedded derivatives that do not

significantly change the cash flows otherwise required by the contract, or where the separation of the embedded derivative is not allowed; and

• it involves an equity instrument that does not have an active market in which it has a quoted market price and whose fair value cannot be measured reliably.

Fair value through profit or loss financial liabilities are carried at fair value and any changes in fair value from one year to the next are recognised in profit or loss. Example 7: fair value through profit or loss Mousse Limited issued 100 000 debentures on the 1 January 20X5, proceeds totaled C200 000. On the 31 December 20X5 the debentures had a fair value of C300 000. Mousse Limited designated these debentures to be held at ‘fair value through profit or loss’. Required: Provide the necessary journal entries to show how Mousse Limited should account for the change in the fair value of the debentures. Solution to example 7: fair value through profit or loss 1 January 20X5 Debit Credit Bank 200 000 Debentures (liability) 200 000 Issue of debentures 31 December 20X5 Loss on financial liabilities held at fair value (expense) 100 000 Debentures (liability) 100 000 Re-measurement of debentures at year-end 6.3 Financial liabilities that are not measured at fair value through profit or loss A liability that is not held for trading, (and not otherwise designated as fair value through profit or loss on acquisition) is measured at amortised cost using the effective interest rate method. This ensures that all the finance costs incurred are recognised over the life of the financial liability. Example 8: other financial liabilities Tempo Limited issued 200 000 debentures on the 1 January 20X5 at par of C7. The debentures are redeemable on the 31 December 20X7 for C10. Required: Calculate the finance costs and the carrying amount of the debentures for each affected year.

Gripping IFRS Financial instruments

Chapter 21

658

Solution to example 8: other financial liabilities The effective interest rate is calculated using a financial calculator as 12.6248% PV = -7 FV=10 N = 3 COMP i

Date Finance Costs @ 12,6248% Carrying Amount 1 Jan 20X5 1 400 000 200 000 x C7 31 Dec 20X5 176 747 1 576 747 31 Dec 20X6 199 061 1 775 808 31 Dec 20X7 224 192 2 000 000 Redemption (2 000 000)

7. Categories of financial assets 7.1 Overview (IAS 39.9) There are four main categories of financial assets and they are: • Fair value through profit or loss; • Held to maturity; • Loans and receivables; and • Available for sale. 7.2 Fair value through profit or loss (IAS 39.9; .11A and .50) These financial assets are essentially assets that are: • held for trading, being:

• acquired with the intention to sell in the short term; • acquired as part of a selling portfolio; or • derivatives; or

• designated by the entity as fair value through profit and loss. This designation is only allowed where it provides more relevant information: • through eliminating measurement or recognition inconsistency, or • because the financial asset is evaluated by the entity’s key management personnel

(e.g. board of directors) on a fair value basis in accordance with its documented risk management or investment strategy.

The designation of fair value through profit and loss is not allowed if: • the contract including the financial asset includes embedded derivatives that do not

significantly change the cash flows otherwise required by the contract, or where the separation of the embedded derivative is not allowed; and

• it involves an equity instrument that does not have an active market in which it has a quoted market price and whose fair value cannot be measured reliably.

Any financial asset may be deemed by the entity, when acquired, to be held for trading, but may not be later reclassified. Fair value through profit or loss financial assets are carried at fair value and any changes in fair value from one year to the next are recognised as income or expenses. Example 9: fair value through profit or loss financial assets Grime Limited purchased 25 000 debentures at a total cost of C 25 000 on the 1 November 20X5. At the year end (31 December 20X5) the fair value of the debentures was C55 000. Grime Limited purchased these debentures with the intention to sell in the short term. Required: Show the necessary journal entries to record the change in fair value.

Gripping IFRS Financial instruments

Chapter 21

659

Solution to example 9: fair value through profit or loss financial assets 1 November 20X5 Debit Credit Debentures (asset) Given 25 000 Bank 25 000 Purchase of debentures 31 December 20X5 Debentures (asset) 55 000 – 25 000 30 000 Profit on financial liabilities held at fair value 30 000 Re-measurement of debentures at year-end 7.3 Held to maturity financial assets (IAS 39.9) These assets include: • non-derivatives; • fixed rate instruments; • fixed maturity instruments; and • assets that the entity has both the ability and intention to hold until maturity. If, however, one of these assets has been sold by the entity in the past 2 years that type of asset is now tainted and may not be classified as held to maturity. Held to maturity financial assets are held at amortised cost using the effective interest rate. Example 10: held to maturity Eternity Ltd purchased 10% debentures for C 200 000 on 1 January 20X5, (redeemable on the 31 December 20X6). They intended to hold them to maturity, (and had the ability to do so). They had never held such debentures before. The fair value on 31 December 20X5 was C400 000. Required: Prepare the necessary journal entries to show how Eternity Ltd should account for the debentures for the year ended 31 December 20X5. Solution to example 10: held to maturity Debit Credit 1 January 20X5 Debentures (asset) Given 200 000 Bank 200 000 Purchase of debentures 31 December 20X5 Debentures (asset) 200 000 x 10% 20 000 Interest income 20 000 Interest earned on debentures Notice that no entry is made for the increase in fair value. 7.4 Loans and receivables (IAS 39.9) These assets are: • Non-derivatives • Involving fixed/ determinable payments • That are not quoted in an active market. These assets include, for example, debtors, loans granted to a third party, and bank deposits.

Gripping IFRS Financial instruments

Chapter 21

660

Loans and receivables are carried at amortised cost using the effective interest rate method. Example 11: loans and receivables Obliged Limited lent C50 000 to Grateful Limited on 30 June 20X5. Interest as per the agreement was charged at 20%. No repayments were made on the loan. Required: Show the necessary journals to account for the loan for the year ended 31 December 20X5. Solution to example 11: loans and receivables Debit Credit 30 June 20X5 Loan to Grateful Limited (asset) Given 50 000 Bank 50 000 Loan granted to Grateful Ltd 31 December 20X5 Loan to Grateful Limited (asset) 50 000 x 20% x 6 / 12 months 5 000 Interest income 5 000 Interest charged for the year ended 31 December 20X5 7.5 Available for sale financial assets (IAS 39.9) Available for sale financial assets are all those non derivative financial assets that are designated as Available for Sale or are classified into any of the three other categories. Available for sale financial assets are recorded at fair value, with the resultant changes in fair value recognised in other comprehensive income (i.e. equity). Example 12: available for sale Dilly Limited purchased 500 000 shares in Sane Limited on the 31 March 20X5. They were purchased for C1 000 000. On the 31 December the fair value of these shares was C2 000 000. These shares were classified as available for sale. Required: Prepare the necessary journal entries to show how Dilly Limited should account for these shares. Solution to example 12: available for sale 31 March 20X5 Debit Credit Shares in Sane Limited (asset) Given 1 000 000 Bank 1 000 000 Purchase of shares in Sane Limited 31 December 20X5 Shares in Sane Limited (asset) 2 000 000 – 1 000 000 1 000 000 Equity: gain on revaluation of shares 1 000 000 Shares in Sane Limited revalued to fair value

Gripping IFRS Financial instruments

Chapter 21

661

8. Reclassification of financial instruments 8.1 Overview There are a variety of situations where financial instruments may need to be re-classified. The most important issues are stated below. 8.2 Fair value through profit or loss (IAS 39.50) An entity is not allowed to reclassify a financial instrument into or out of the ‘fair value through profit or loss’ category whilst it is held or issued. 8.3 Held to maturity (IAS 39.51) If, as a result of a change in intention or ability, it is no longer appropriate to classify an instrument as ‘held to maturity’, it shall be reclassified as ‘available for sale’ and re-measured at fair value. The difference between carrying amount and fair value must be recognised in other comprehensive income. 8.4 Available for sale (IAS 39.54) If, as a result of a change in intention or ability (or the fair value is no longer able to be reliably measured), it becomes appropriate to measure at cost or amortised cost rather that at fair value, then the previous fair value carrying amount becomes the de facto cost or amortised cost from that date onwards. Any gain or loss recognised in other comprehensive income whilst it was measured as available for sale must be recognised in profit or loss: • over the remaining life of the financial asset if it has a fixed maturity; • when the financial asset is sold or otherwise disposed of. 8.5 Instruments previously measured at amortised cost (IAS 39.53) If a reliable measure becomes available for a financial instrument which was previously not available, and the financial instrument would have been measured at fair value had fair value been available, such financial instrument shall be re-measured at fair value. The difference between its fair value and its carrying amount must be taken directly to equity. [IAS 39.53]

9. Impairment of financial instruments (IAS 39.58 – 70) The entity must assess whether its financial assets are impaired at the end of the reporting period. A financial asset (or group of financial assets) is only impaired at the end of a reporting period if there is objective evidence that suggests: • that one or more events occurred after the initial recognition; • where the event causes loss; and where • this ‘loss event’ has an impact on estimated future cash flows of the financial asset or

group of financial assets; and • the amount of the loss can be reliably estimated.

10. Offsetting of financial assets and liabilities (IAS 32.42 - .50) Financial assets and liabilities may not be offset against one another unless: • the entity has a legal right to set off the two amounts; and • the entity intends to settle the two instruments simultaneously or on a net basis.

Gripping IFRS Financial instruments

Chapter 21

662

11. Disclosure

The following narrative disclosure is required (required by IFRS 7): • For credit risk:

- Amount of maximum credit risk - Collateral held as security - Other credit enhancements - Credit quality of financial assets (not past due) - Carrying amount of financial assets past due/ impaired/ re-negotiated.

• For liquidity risk: - Maturity analysis for financial liabilities - Description of how liquidity risk is managed.

• For market risk - Sensitivity analysis for each market risk - Methods and assumptions used in the analysis - Any changes in the above assumptions, together with reasons for the changes.

• For each class of financial assets and liabilities: - The criteria for recognition; - Basis for measurement - Methods and assumptions made to determine fair value - Fair value of the financial instrument (or the reasons why it cannot be determined,

information about the related market and the range of possible fair values). The following figures must be separately disclosed: • finance costs from financial liabilities must be presented as a separate line item. • the total change in fair value of the instruments reported in the statement of

comprehensive income • the changes in fair value that were taken directly to equity. The following is a suggested layout that you may find useful. Name of Company Statement of changes in equity For the year ended 31 December 20X5 (extracts)

Ordinary share

capital C

Share premium

C

Available for sale financial

assets C

Retained earnings

C

Total

C Balance: 1 January 20X5 xxx xxx xxx xxx xxx Ordinary shares issued xxx xxx xxx Total comprehensive income xxx xxx xxx Balance: 31 December 20X5 xxx xxx xxx xxx xxx Name of Company Statement of financial position (extracts) As at 31 December 20X5 Note 20X5

C 20X4

C EQUITY AND LIABILITIES or ASSETS Loan Financial instruments Preference shares

39

xxx xxx xxx

xxx xxx xxx

Gripping IFRS Financial instruments

Chapter 21

663

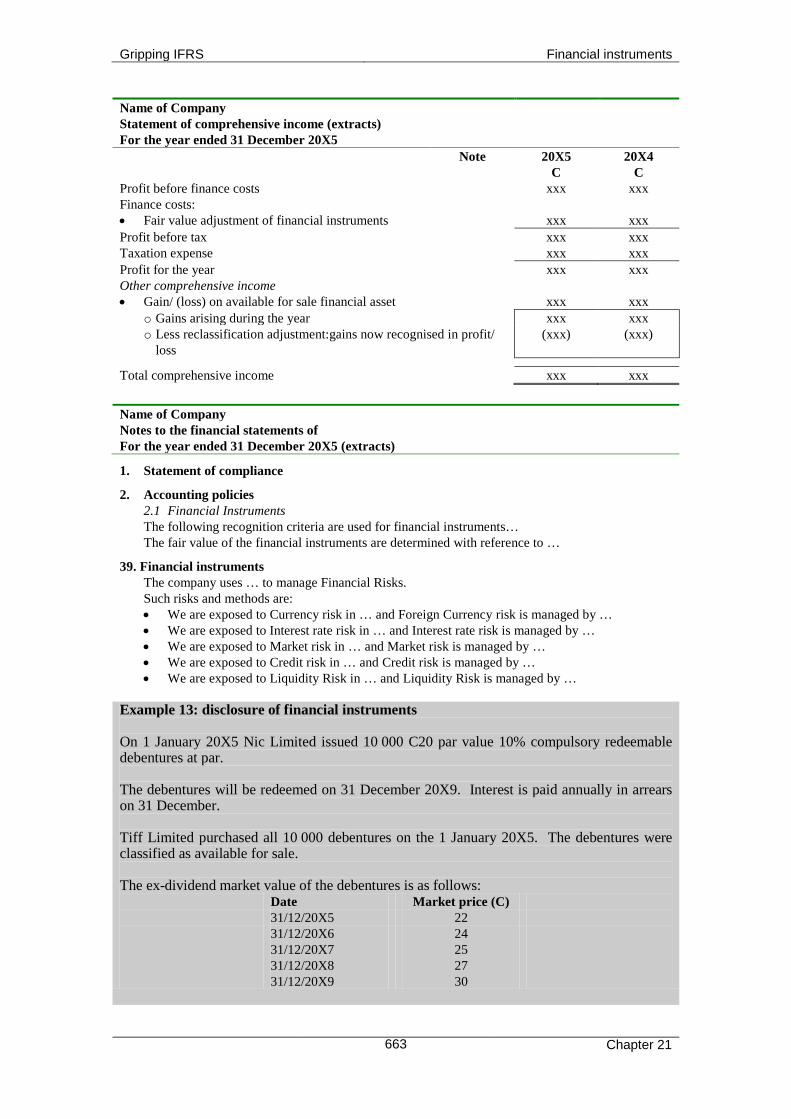

Name of Company Statement of comprehensive income (extracts) For the year ended 31 December 20X5 Note 20X5

C 20X4

C Profit before finance costs xxx xxx Finance costs: • Fair value adjustment of financial instruments

xxx

xxx

Profit before tax xxx xxx Taxation expense xxx xxx Profit for the year xxx xxx Other comprehensive income • Gain/ (loss) on available for sale financial asset xxx xxx

o Gains arising during the year xxx xxx o Less reclassification adjustment:gains now recognised in profit/

loss (xxx) (xxx)

Total comprehensive income xxx xxx

Name of Company Notes to the financial statements of For the year ended 31 December 20X5 (extracts) 1. Statement of compliance 2. Accounting policies

2.1 Financial Instruments The following recognition criteria are used for financial instruments… The fair value of the financial instruments are determined with reference to …

39. Financial instruments

The company uses … to manage Financial Risks. Such risks and methods are: • We are exposed to Currency risk in … and Foreign Currency risk is managed by … • We are exposed to Interest rate risk in … and Interest rate risk is managed by … • We are exposed to Market risk in … and Market risk is managed by … • We are exposed to Credit risk in … and Credit risk is managed by … • We are exposed to Liquidity Risk in … and Liquidity Risk is managed by …

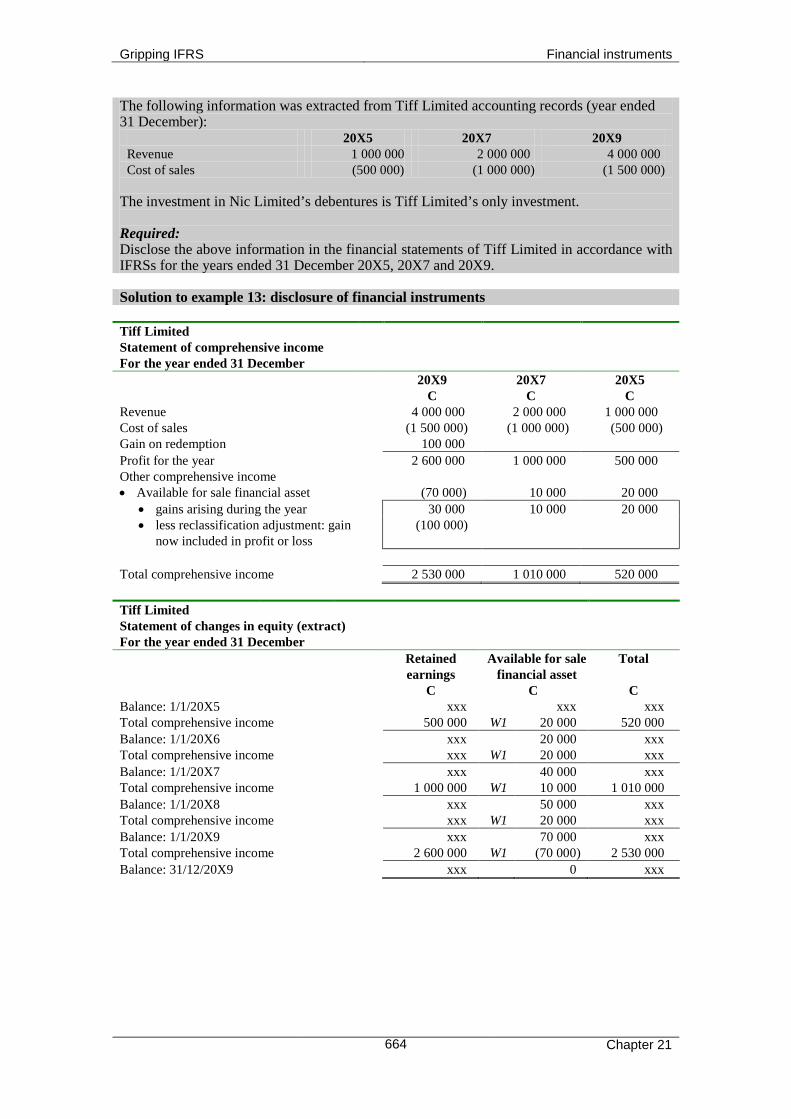

Example 13: disclosure of financial instruments On 1 January 20X5 Nic Limited issued 10 000 C20 par value 10% compulsory redeemable debentures at par. The debentures will be redeemed on 31 December 20X9. Interest is paid annually in arrears on 31 December. Tiff Limited purchased all 10 000 debentures on the 1 January 20X5. The debentures were classified as available for sale. The ex-dividend market value of the debentures is as follows:

Date Market price (C) 31/12/20X5 22 31/12/20X6 24 31/12/20X7 25 31/12/20X8 27 31/12/20X9 30

Gripping IFRS Financial instruments

Chapter 21

664

The following information was extracted from Tiff Limited accounting records (year ended 31 December):

20X5 20X7 20X9 Revenue 1 000 000 2 000 000 4 000 000 Cost of sales (500 000) (1 000 000) (1 500 000)

The investment in Nic Limited’s debentures is Tiff Limited’s only investment. Required: Disclose the above information in the financial statements of Tiff Limited in accordance with IFRSs for the years ended 31 December 20X5, 20X7 and 20X9. Solution to example 13: disclosure of financial instruments Tiff Limited Statement of comprehensive income For the year ended 31 December 20X9 20X7 20X5 C C C Revenue 4 000 000 2 000 000 1 000 000 Cost of sales (1 500 000) (1 000 000) (500 000) Gain on redemption 100 000 Profit for the year 2 600 000 1 000 000 500 000 Other comprehensive income • Available for sale financial asset (70 000) 10 000 20 000 • gains arising during the year 30 000 10 000 20 000 • less reclassification adjustment: gain

now included in profit or loss (100 000)

Total comprehensive income 2 530 000 1 010 000 520 000 Tiff Limited Statement of changes in equity (extract) For the year ended 31 December Retained

earnings Available for sale

financial asset Total

C C C Balance: 1/1/20X5 xxx xxx xxx Total comprehensive income 500 000 W1 20 000 520 000 Balance: 1/1/20X6 xxx 20 000 xxx Total comprehensive income xxx W1 20 000 xxx Balance: 1/1/20X7 xxx 40 000 xxx Total comprehensive income 1 000 000 W1 10 000 1 010 000 Balance: 1/1/20X8 xxx 50 000 xxx Total comprehensive income xxx W1 20 000 xxx Balance: 1/1/20X9 xxx 70 000 xxx Total comprehensive income 2 600 000 W1 (70 000) 2 530 000 Balance: 31/12/20X9 xxx 0 xxx

Gripping IFRS Financial instruments

Chapter 21

665

Tiff Limited Statement of financial position (extract) As at 31 December 20X9 20X7 20X5 ASSETS C C C Non-current assets Financial assets 0 250 000 220 000 W1. Calculation of gains recognised in other comprehensive income C Financial asset initially measured: 1/1/20X5 10 000 x 20 200 000 Fair value adjustment Balancing 20 000 Fair value on 31/12/20X5 10 000 x 22 220 000 Fair value adjustment Balancing 20 000 Fair value on 31/12/20X6 10 000 x 24 240 000 Fair value adjustment Balancing 10 000 Fair value on 31/12/20X7 10 000 x 25 250 000 Fair value adjustment Balancing 20 000 Fair value on 31/12/20X8 10 000 x 27 270 000 Fair value adjustment Balancing 30 000 Fair value on 31/12/20X9 10 000 x 30 300 000 Total fair value adjustments 20 000 + 20 000 + 10 000 + 20 000

+ 30 000 100 000

Gripping IFRS Financial instruments

Chapter 21

666

12.Summary

Financial risks

Market risk Credit risk Liquidity risk Risk that the value of

the financial instrument will fluctuate due to: • Currency risk • Interest rate risk • Price risk

Risk that one party to the financial instrument will default causing the other party to incur financial loss

Risk that the entity will encounter difficulty in raising funds to meet its obligations associated with financial instruments

Accounting for Financial Liabilities

Fair value through profit or loss Other financial liabilities Measured at fair value with changes

in fair value taken to profit and loss (i.e. the statement of comprehensive income)

Measured at amortised cost using the effective interest rate method

Accounting for Financial Assets

Fair value through profit

or loss

Held to maturity

Loans and receivables

Available for sale

Measured at fair value with changes in fair value taken to profit and loss (i.e. the statement of comprehensive income)

Measured at amortised cost using the effective interest rate method

Measured at amortised cost using the effective interest rate method

Measured at fair value with changes in fair value taken directly to equity