iasb projects a pocketbook guide - ey · leases (joint project ... iasb projects - a pocketbook...

TRANSCRIPT

IASB Projects A pocketbook guide As at 30 September 2014

IASB Projects - A pocketbook guide 1

In this edition...

Introduction ....................................................................................................................................................................... 2

Financial instruments − macro hedging ........................................................................................................................ 3

Leases (joint project) ..................................................................................................................................................... 5

Insurance contracts ....................................................................................................................................................... 7

Implementation projects ................................................................................................................................................... 9

2 IASB Projects - A pocketbook guide

Introduction

This will be the final edition of EY’s pocketbook guide, which was designed to summarise the key features of the active projects of the International Accounting Standards Board (IASB or the Board), along with potential implications of the proposed standards and our views on certain projects. We will continue to keep you informed about the active projects of the IASB in our publication IFRS Update of standards and interpretations (IFRS Update). This edition of the pocketbook guide focuses on certain of the IASB’s projects as at 30 September 2014, with emphasis on the macro hedging, leases and insurance contracts projects. Since the June 2014 edition of the pocketbook guide, the IASB has issued the new standard on financial instruments, IFRS 9 Financial Instruments (July 2014), which includes the requirements for classification, measurement, impairment and hedging. In addition, in August 2014, the IASB issued narrow scope amendments to IAS 27 Separate Financial Statements. In September 2014, the IASB issued narrow scope amendments to IFRS 10 Consolidated Financial Statements and IAS 28 Investments in Associates and Joint Ventures, and completed the 2012-2014 cycle of improvements to IFRS, setting out five amendments to four standards.

For details of IASB projects for which new or amended IFRSs have been issued prior to 31 August 2014, we refer you to our publication, IFRS Update and our IFRS Developments series, all of which are available on www.ey.com/ifrs. We trust that you will find this guide useful. Yours sincerely, Leo van der Tas Global Leader — IFRS Services Global Professional Practice October 2014

IASB Projects - A pocketbook guide 3

Major IFRS projects

Financial instruments − macro hedging Public consultation Q2–Q4 2014

Key developments to date Implications

Background ► The IASB decoupled the project on accounting for dynamic risk management

(i.e., macro hedging) from the IFRS 9 project so that it did not impact the effective date or timing of the completion of the IFRS 9 hedge accounting project.

► The IASB published a discussion paper (DP) in April 2014. The comment period ends on 17 October 2014.

Scope ► The project addresses specific accounting for risk management strategies relating

to open portfolios rather than individual contracts. The hedge accounting requirements in IAS 39 and IFRS 9 do not provide specific solutions to the issues associated with macro hedging.

Key features ► The DP is the first stage of the macro hedging project. The DP seeks public

comment on a possible approach to accounting for an entity’s dynamic risk management activities – the portfolio revaluation approach (PRA).

► Among other things, the DP seeks comment on: ► Whether the PRA would apply to all activities that are subject to dynamic risk

management or only to those in which the risks are actually mitigated ► How dynamically risk-managed exposures would be revalued ► The disclosures concerning an entity’s dynamic risk management activities

► The potential new accounting approach for macro hedging could differ substantially from what is colloquially referred to as macro hedging under IAS 39.

► The PRA is most relevant for banks and their management of interest rate risk, but may apply to other industries and risks in which dynamic risk management occurs.

► Under the PRA, preparers can consider internal derivatives for income statement presentation without the need to identify related external trading derivatives, and model deposits as an exposure on the basis of client behaviour. This mitigates two of the most often cited difficulties with the existing hedge accounting solutions for dynamic risk management. However, from the perspective of many banks, if the scope of application of the PRA is linked to the risk management activity rather than risk mitigation activity, the perceived benefits from these changes could be outweighed by the reported volatility in profit or loss from intentionally unhedged positions.

4 IASB Projects - A pocketbook guide

Financial instruments − macro hedging cont’d

Key developments to date Implications

Transition ► The IASB carried forward the existing IAS 39 macro fair value hedge accounting

requirements when issuing IFRS 9 (2013) and is expected to allow their application until a new approach to accounting for macro hedging is finalised and becomes effective.

► Entities may make an accounting policy choice to continue to apply the hedge accounting requirements of IAS 39 for all of their hedging relationships. Entities may later change that policy and apply the hedge accounting requirements in IFRS 9 before they eventually become mandatory. This choice is intended to be removed when the IASB completes its project on accounting for macro hedging.

How we see it

Although simple in concept, the PRA would represent a significant change from the existing accounting for dynamic risk management; the operational challenges in making that change should not be underestimated.

We encourage entities that have macro hedging strategies to analyse the DP in order to understand potential opportunities or risks in applying the suggested accounting to their risk management strategies, and to participate in the public consultation process.

Further information on this project can be found on www.ey.com/ifrs.

IASB Projects - A pocketbook guide 5

Leases (joint project) Redeliberations Q1–Q4 2014

Key developments to date Implications

Background ► The Boards are redeliberating their second leases exposure draft (ED), which was

issued in May 2013. The redeliberations are focusing on ways to simplify and reduce the cost of applying a revised lease accounting standard in a number of areas, including: definition and scope; lessee and lessor accounting models; measurement provisions; and disclosure requirements.

► The Boards plan to redeliberate several remaining issues, including: the definition of a lease; a recognition and measurement exemption for leases of small assets; lessee disclosures; and transition. A standard is not expected before the second half of 2015.

Scope ► Leases of all assets, with certain exceptions. However, because the May 2013 ED

focused on control, certain contracts that are currently accounted for as leases (e.g., capacity contracts) may no longer be considered leases.

Key features ► The IASB supports a single on-balance sheet model that would require lessees to

account for all leases (subject to certain exemptions) as Type A leases (i.e., financings). The FASB supports a dual on-balance sheet lessee model that would classify leases as either Type A or Type B using the classification principles in IAS 17 Leases for finance or operating leases.

► Lessees would recognise a liability to pay rentals with a corresponding asset for both types of leases. Type A leases generally would have an accelerated expense recognition pattern while Type B leases (FASB only) generally would have a straight-line expense recognition pattern.

► For today’s operating leases that would be Type A leases under the proposals, the lease expense recognition pattern for lessees would generally be accelerated.

► As a result of the changes, key balance-sheet metrics such as leverage and finance ratios, debt covenants and income statement metrics, such as EBITDA, could be impacted. Also the cash flow statement for IFRS lessees would be impacted as payments for the principal portion of most of today’s operating leases would be presented within financing activities.

► Lessor accounting, as discussed in the redeliberations, would result in significantly fewer changes from today’s lessor accounting compared with the May 2013 ED.

► The resolution of the definition of a lease is of added importance because it will determine which contracts (or portions of contracts) are subject to the proposed lease accounting standard. Such evaluation will also be important to determine which contracts (or portions of contracts) are subject to the new revenue recognition standard (for lessors).

6 IASB Projects - A pocketbook guide

Leases (joint project) cont’d

Key developments to date Implications

Key features cont’d ► The IASB supports a recognition and measurement exemption for leases of ’small

assets’ (e.g., office furniture), but the FASB does not. The IASB has not yet defined ‘small assets’.

► Reassessment of certain key considerations (e.g., lease term, variable rents based on an index or rate, discount rate) by the lessee would be required upon certain events. Lessors would not reassess the lease term or variable rents based on an index or rate.

► Lessor accounting would be similar to today’s lessor accounting, using IAS 17’s dual classification approach. The Boards have different views on the recognition of selling profit for certain Type A leases. The difference focuses on whether to evaluate the transfer of substantially all the risks and rewards from the lessor’s perspective (IASB preference) or the lessee’s perspective (FASB preference).

Transition and effective date ► The effective date has not been determined, but is not expected to be before

2018.The Boards have not yet redeliberated transition. However, in the May 2013 ED, the Boards proposed a modified retrospective approach for transition. Certain optional relief would be available. Full retrospective application would also be permitted.

How we see it

The Boards’ decisions in redeliberations suggest there will be differences in lease accounting between IFRS and US GAAP (for lessee accounting, in particular). The Boards are continuing to redeliberate the leases project jointly. However, there is no timetable for if, how and when the Boards plan to revisit earlier decisions that gave rise to the differences.

Further information on this project can be found on www.ey.com/ifrs.

IASB Projects - A pocketbook guide 7

Insurance contracts Redeliberations Q1–Q4 2014

Key developments to date Implications

Background ► The IASB exposed its revised proposed comprehensive method of accounting for

insurance contracts in June 2013. In addition, the FASB published its proposals in June 2013.

Scope ► The standard would apply to all types of insurance contracts (i.e., life, non-life,

direct insurance and re-insurance), regardless of the type of entity that issued them, as well as certain guarantee and financial instrument contracts with discretionary participation features. A few scope exceptions would apply.

Key features ► The proposed approach for the measurement of the insurance contract liability is

based on the following building blocks: ► Expected present value of future cash flows ► A risk adjustment to the expected present value of cash flows ► A contractual service margin (CSM) that would eliminate any gain at inception

of the contract; the CSM would be adjusted subsequently for changes in estimates of future cash flows and the risk adjustment to the extent these changes relate to future coverage or other future services

► A discount rate that would be updated at the end of each reporting period (i.e., the liability discount rate would not be ‘locked-in’ at inception of the contract)

► Rather than prescribing a rate for discounting insurance contracts, the proposed approach would be based on the principle that the rate should reflect the characteristics of the liability.

► The IASB’s proposals are far-reaching and may have a significant impact on insurers and some non-insurers (e.g., estimating all future cash flows arising from the fulfilment of an insurance contract on a probability-weighted basis, and reporting revenue under the building block approach). This would have a related impact on key processes and internal controls.

► The IASB’s proposals differ from the FASB’s proposals in some important areas (e.g., margins, acquisition costs, and when to use the premium allocation approach). As a result of the differences, the Boards are not expecting to reach a converged solution on this project. Consequently, no joint redeliberations are currently planned.

8 IASB Projects - A pocketbook guide

Insurance contracts cont’d

Key developments to date Implications

Key features cont’d ► The objective of the insurance standard would be to provide principles on the

accounting for individual contracts, but contracts could be aggregated as long as this objective is met.

► An accounting policy choice would be permitted at a portfolio level to recognise the effect of changes in discount rates in either OCI or profit or loss.

► For contracts with participating features that contain a contractual right to share in the return of underlying items, the ED proposed that measurement and presentation of the insurance liability should be consistent with those items. The IASB has held a number of educational discussions on this topic and will revisit the treatment of participating contracts.

► Revenue would be reported in the income statement through earned premiums representing the insurer’s performance under the contracts in the period for all types of insurance contracts.

► A simplified approach based on a premium allocation could be applied to the liability for remaining coverage if contracts meet certain eligibility criteria (e.g., contracts with a coverage period of one year or less).

Transition and effective date ► The IASB has not yet concluded on the effective date, but it is expected to be

approximately three years from the issuance of the standard. The ED proposed a retrospective transition, with certain practical reliefs.

How we see it

We support the general direction of the revised ED, but believe that additional changes are necessary to improve the proposals. We are concerned that the IASB may not have struck the right balance in some areas, in terms of enhancing the usefulness of financial reporting versus the costs of applying the proposals.

Resolving the accounting for participating contracts will be key to finalising the project.

The Board’s tentative decision to make the use of OCI optional is a compromise necessary to complete the insurance contracts project. Having an option allows entities to reflect the differences that exist in how they run their businesses to fulfil their obligations under their insurance contracts. Despite the IASB showing its willingness to provide flexibility by making OCI optional, volatility will continue to exist in the proposed model unless further modifications are made.

Further information on this project can be found on www.ey.com/ifrs.

IASB Projects - A pocketbook guide 9

Implementation projects The IASB has a number of items on its work plan that address implementation issues. These include narrow scope amendments and interpretations. Below is a listing of the current implementation projects based on the IASB’s work plan as at 26 September 2014.

Narrow scope amendments Status/next steps

Annual Improvements ► The annual improvements process deals with non-urgent, but necessary, amendments

to IFRS. ► Annual Improvements to IFRSs 2012–2014 Cycle includes five amendments to four

standards: IFRS 5 Non-current Assets Held for Sale and Discontinued Operations; IFRS 7 Financial Instruments: Disclosures; IAS 19 Employee Benefits; and IAS 34 Interim Financial Reporting. The amendments are effective for annual periods beginning on or after 1 January 2016.

► The IFRS Interpretations Committee is discussing issues for the 2014-2016 annual improvements cycle. As of the date of publication, an issue related to short-term exemptions in IFRS 1 First-time Adoption of International Financial Reporting Standards is expected to be included in this cycle.

► Amendments on the 2012-2014 annual improvements cycle issued Q3 2014

► ED on 2014-2016 annual improvements cycle expected Q2 2015

10 IASB Projects - A pocketbook guide

Narrow scope amendments Status/next steps

Clarification of Classification and Measurement of Share-based Payment Transactions (Proposed amendments to IFRS 2) ► The objective of this project is to clarify, in IFRS 2 Share-based Payment, the

accounting for: ► A share-based payment (SBP) transaction in which the entity settles the

arrangement net by withholding a specified portion of equity instruments to meet its minimum statutory tax withholding

► A SBP arrangement that changes from cash-settled to equity-settled when the replacement SBP has a higher fair value than the original award

► The effects of vesting conditions on a cash-settled SBP

► ED expected Q4 2014

Classification of Liabilities (Proposed amendments to IAS 1) ► The objective of this project is to clarify, in IAS 1 Presentation of Financial Statements,

the distinction between current and non-current liabilities, within the context of loans that are rolled over or loans made when the holder has a right to defer settlement of the loan for at least 12 months after the reporting period.

► ED expected Q4 2014

IASB Projects - A pocketbook guide 11

Narrow scope amendments Status/next steps

Disclosure Initiative ► The IASB is undertaking a broad-based initiative, comprising a number of short and

longer-term projects, to explore how disclosures in IFRS financial reporting can be improved.

► As a part of the short-term project, the IASB has proposed narrow-scope amendments to IAS 1 that are intended to clarify, rather than significantly change, the existing requirements. The ED proposes to: ► Clarify the materiality requirements of IAS 1 that specific line items in the financial

statements can be disaggregated, and that entities have flexibility as to the order in which they present the notes

► Add requirements for how an entity should present subtotals in the financial statements

► Remove potentially unhelpful guidance in IAS 1 for identifying a significant accounting policy

► The IASB is also undertaking a short-term project in response to the Agenda Consultation in 2011. Users requested the Board to consider improving the disclosure requirements regarding ‘net debt’ by introducing a requirement to reconcile the opening and closing liabilities that form part of an entity’s financing activities.

► The Board is also undertaking a research project to identify and develop a set of principles for disclosure that could form the basis of a standard-level project. The focus is on reviewing the general requirements in IAS 1, IAS 7 Statement of Cash Flows and IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors and considering how they might be replaced by a single standard, in essence creating a disclosure framework.

► ED on IAS 1 issued Q1 2014; redeliberations commenced Q3 2014; amendments expected Q4 2014

► ED on net debt disclosures expected Q4 2014 ► DP on principles of disclosure expected

Q1-Q2 2015

12 IASB Projects - A pocketbook guide

Narrow scope amendments Status/next steps

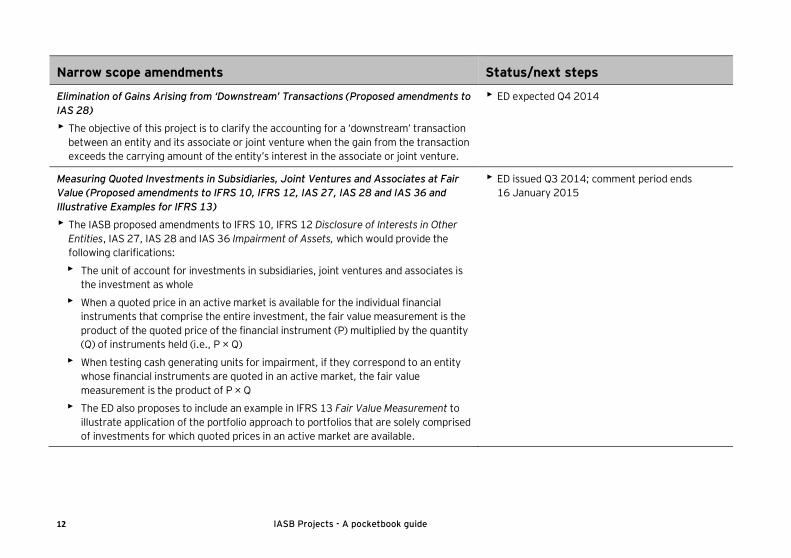

Elimination of Gains Arising from ‘Downstream’ Transactions (Proposed amendments to IAS 28) ► The objective of this project is to clarify the accounting for a ‘downstream’ transaction

between an entity and its associate or joint venture when the gain from the transaction exceeds the carrying amount of the entity’s interest in the associate or joint venture.

► ED expected Q4 2014

Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value (Proposed amendments to IFRS 10, IFRS 12, IAS 27, IAS 28 and IAS 36 and Illustrative Examples for IFRS 13) ► The IASB proposed amendments to IFRS 10, IFRS 12 Disclosure of Interests in Other

Entities, IAS 27, IAS 28 and IAS 36 Impairment of Assets, which would provide the following clarifications: ► The unit of account for investments in subsidiaries, joint ventures and associates is

the investment as whole ► When a quoted price in an active market is available for the individual financial

instruments that comprise the entire investment, the fair value measurement is the product of the quoted price of the financial instrument (P) multiplied by the quantity (Q) of instruments held (i.e., P × Q)

► When testing cash generating units for impairment, if they correspond to an entity whose financial instruments are quoted in an active market, the fair value measurement is the product of P × Q

► The ED also proposes to include an example in IFRS 13 Fair Value Measurement to illustrate application of the portfolio approach to portfolios that are solely comprised of investments for which quoted prices in an active market are available.

► ED issued Q3 2014; comment period ends 16 January 2015

IASB Projects - A pocketbook guide 13

Narrow scope amendments Status/next steps

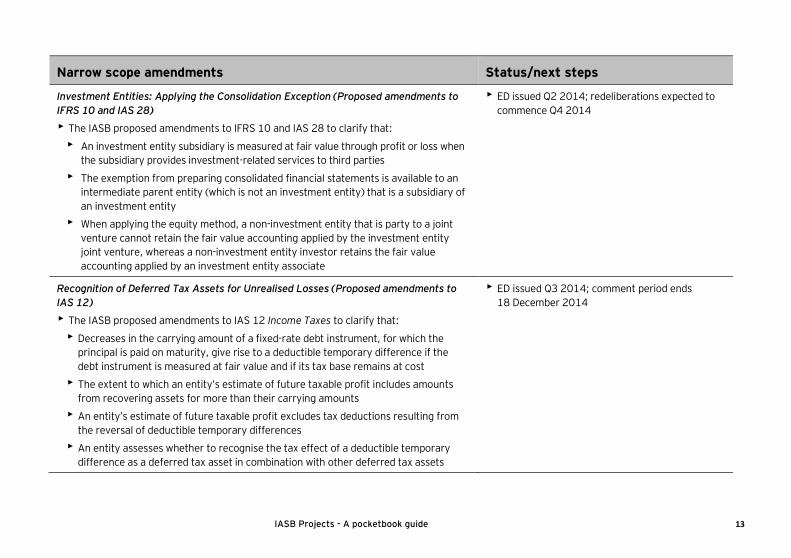

Investment Entities: Applying the Consolidation Exception (Proposed amendments to IFRS 10 and IAS 28) ► The IASB proposed amendments to IFRS 10 and IAS 28 to clarify that:

► An investment entity subsidiary is measured at fair value through profit or loss when the subsidiary provides investment-related services to third parties

► The exemption from preparing consolidated financial statements is available to an intermediate parent entity (which is not an investment entity) that is a subsidiary of an investment entity

► When applying the equity method, a non-investment entity that is party to a joint venture cannot retain the fair value accounting applied by the investment entity joint venture, whereas a non-investment entity investor retains the fair value accounting applied by an investment entity associate

► ED issued Q2 2014; redeliberations expected to commence Q4 2014

Recognition of Deferred Tax Assets for Unrealised Losses (Proposed amendments to IAS 12) ► The IASB proposed amendments to IAS 12 Income Taxes to clarify that:

► Decreases in the carrying amount of a fixed-rate debt instrument, for which the principal is paid on maturity, give rise to a deductible temporary difference if the debt instrument is measured at fair value and if its tax base remains at cost

► The extent to which an entity’s estimate of future taxable profit includes amounts from recovering assets for more than their carrying amounts

► An entity’s estimate of future taxable profit excludes tax deductions resulting from the reversal of deductible temporary differences

► An entity assesses whether to recognise the tax effect of a deductible temporary difference as a deferred tax asset in combination with other deferred tax assets

► ED issued Q3 2014; comment period ends 18 December 2014

14 IASB Projects - A pocketbook guide

Narrow scope amendments Status/next steps

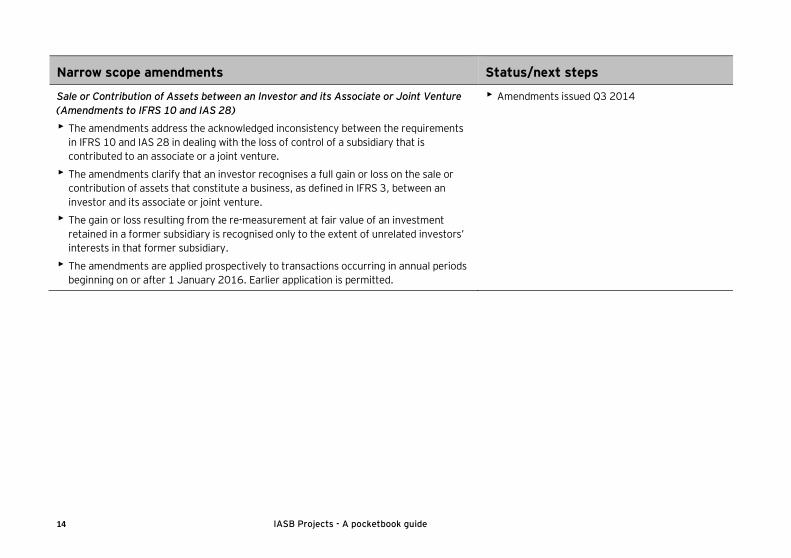

Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendments to IFRS 10 and IAS 28) ► The amendments address the acknowledged inconsistency between the requirements

in IFRS 10 and IAS 28 in dealing with the loss of control of a subsidiary that is contributed to an associate or a joint venture.

► The amendments clarify that an investor recognises a full gain or loss on the sale or contribution of assets that constitute a business, as defined in IFRS 3, between an investor and its associate or joint venture.

► The gain or loss resulting from the re-measurement at fair value of an investment retained in a former subsidiary is recognised only to the extent of unrelated investors’ interests in that former subsidiary.

► The amendments are applied prospectively to transactions occurring in annual periods beginning on or after 1 January 2016. Earlier application is permitted.

► Amendments issued Q3 2014

EY | Assurance | Tax | Transactions | Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. About EY’s International Financial Reporting Standards Group A global set of accounting standards provides the global economy with one measure to assess and compare the performance of companies. For companies applying or transitioning to International Financial Reporting Standards (IFRS), authoritative and timely guidance is essential as the standards continue to change. The impact stretches beyond accounting and reporting, to key business decisions you make. We have developed extensive global resources — people and knowledge — to support our clients applying IFRS and to help our client teams. Because we understand that you need a tailored service as much as consistent methodologies, we work to give you the benefit of our deep subject matter knowledge, our broad sector experience and the latest insights from our work worldwide.

© 2014 EYGM Limited. All Rights Reserved.

EYG no.AU2669

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com