iasb update agenda paper 5 - aossg · the views expressed in this presentation are those of the...

TRANSCRIPT

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

November 2013

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IASB update

IFRS technical update

• The new IASB work plan

• Recently issued IFRSs

• Major standards and projects – Financial Instruments

– IASB-FASB MoU projects

– Other projects

• Implementation – Interpretations

– Narrow scope amendments

– Post-implementation Reviews

• Research

November 2013 Project update and the future work plan

2

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

The new IASB work plan

November 2013 Project update and the future work plan

IASB agenda consultation

• The new work plan has been shaped by the Agenda Consultation

• Public review of the IASB’s technical programme every three

years

• Helps the IASB establish a broad strategic direction for its work

plan: – Establish a balance between:

– improvements (new IFRSs); and

– maintenance (implementation)

– Determine whether to return to projects that have been deferred

– Identify areas where improvements are needed

4

November 2013 Project update and the future work plan

Technical Programme

• Major projects – Research programme

– Standards-level programme

• Conceptual Framework

• Implementation and Maintenance – Interpretations

– Narrow-scope improvements

– Post-implementation Reviews

5

November 2013 Project update and the future work plan

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Major Standards-level projects

November 2013 Project update and the future work plan

IASB Work plan – as at 5 November 2013 7

November 2013 Project update and the future work plan

Next major project milestonex

2013 Q4 2014 Q1 2014 Q2 2014 Q3

IFRS 9: Financial Instruments (replacement of IAS 39)

Classification and Measurement

(Limited amendments) IFRS

Impairment IFRS

Hedge Accounting IFRS

Accounting for Macro Hedging DP

Insurance Contracts Redeliberations

Leases Redeliberations

Rate-regulated Activities

Interim IFRS IFRS

Rate Regulation DP

Revenue Recognition IFRS

Major IFRSs

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Revenue Recognition

© 2012 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Revenue recognition

• Objective – to develop a single, principle-based revenue standard

for IFRSs and US GAAP

• Expected publication of IFRS Q1 2014

• Effective date 1 January 2017 with early application permitted

9

November 2013 Project update and the future work plan

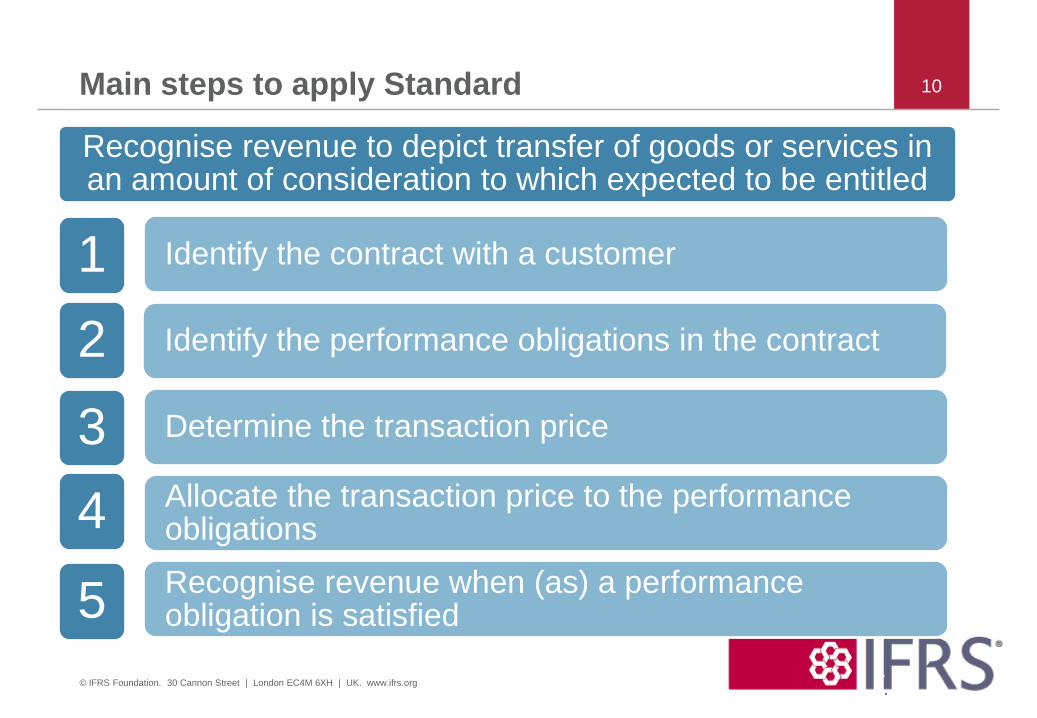

Main steps to apply Standard

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

10

Recognise revenue to depict transfer of goods or services in an amount of consideration to which expected to be entitled

Identify the contract with a customer

Identify the performance obligations in the contract

Determine the transaction price

Allocate the transaction price to the performance obligations

Recognise revenue when (as) a performance obligation is satisfied

1

2

3

4

5

Extensive due process 11

2010 2014 2011

December 2008

Discussion Paper

Preliminary Views on

Revenue Recognition

in Contracts with

Customers

211 comment letters

June 2010

Exposure Draft

Revenue from

Contracts with

Customers

974 comment letters

Roundtables

Q1 2014

Final Standard (IFRS)

IFRS X Revenue from

Contracts with Customers

Effective date: 1 Jan 2017

November 2011

Revised Exposure

Draft

Re-exposure of

Revenue from

Contracts with

Customers

358 comment letters

Roundtables

2008

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Collectibility (ie, customer credit risk)

• Constraint on estimates of variable consideration

• Implementation Guidance: Licenses

Topics discussed in October 2013

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

12

• Public discussion to support initial application of the new Revenue

Standard

• Will not issue authoritative guidance

• Limited life group

Revenue Transition Resource Group 13

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Leases

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14

Leases

• The FASB and IASB have developed a common model

• Lessee accounting: – All leases of more than 12 months are on-balance sheet

– Most equipment leases: recognise amortisation and interest

expense separately

– Most property leases: recognise a single lease expense on a

straight-line basis

• Lessor accounting: – Most equipment leases: recognise lease receivable and residual

asset

– Most property leases: continue to recognise the property being

leases

15

November 2013 Project update and the future work plan

Investors and analysts – General support for proposals

Leases create assets and liabilities

Current disclosures insufficient

Proposals an improvement to financial reporting

Industry-specific analysts agree with income statement proposals

– Some concerns

Any change affects trend information

Some prefer ‘whole asset’/ongoing commitments approach to

measurement

Some prefer single model—treat all leases as financing

Feedback (as of 30 September) 16

Preparers – Most agree leases create assets and liabilities

– Concerns about complexity

Dual model

Materiality / short-term / small ticket leases

– Very few indicate behavioural changes

– Some don’t support the proposals

Costs outweigh benefits

Others (regulators; standard setters; audit firms) – Support recognition of assets and liabilities on the balance sheet

– Prefer single model—treat all leases as financing

– Some audit firms—cost/benefit concerns

Feedback (as of 30 September) 17

Next Steps 18

Issued Exposure Draft May 2013

Comment period ends

September 13, 2013

Joint Redeliberations

Q413

New Standard Issued

TBD

New Standard Effective

TBD

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Other projects

November 2013 Project update and the future work plan

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Rate-regulated Activities

© 2012 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

20

The new Rate-regulated Activities project

IASB started renewed Rate-regulated Activities

project in September 2012

2 distinct paths

Short-term interim solution (Exposure Draft (ED) Regulatory Deferral Accounts published in November 2013 – deadline for comment 4 September 2013)

Longer-term comprehensive project (starting with a research phase to develop a Discussion

Paper (DP))

21

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Interim solution: ED Regulatory Deferral Accounts 22

Interim solution:

• permit first-time adopters of IFRS to continue to recognise regulatory balances in accordance with their existing local GAAP (recognition and measurement)

• require the impact of recognising regulatory balances to be isolated in order to allow direct comparison with rate-regulated entities that do not recognise regulatory balances (presentation and disclosure)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Will be issued in Q1 2014

Rate-regulated Activities DP

More research is needed on the nature of different types of rate regulation

• Request for Information-Rate Regulation (issued in March 2013)

• IASB Consultative Group established (first meeting July 2013)

Responses will feed into the DP:

• what information about the effects of rate regulation are most useful to users

• does rate regulation create assets/liabilities (links to restarted Conceptual Framework project)

23

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Authority of rate regulator is established by statute

• Rates must balance interests of customers and the supplier

• Rate regulation supports monopoly supplier – explicit licence

– other barriers to competition

• Supplier has obligations to maintain supply – “essential” goods/services

– price inelasticity

– low demand risk

Common features (1)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

24

• Rate regulation establishes prices (rates) – limits negotiation with customers

– prices require approval of rate regulator

• Rate-regulatory mechanism provides strong assurance about

certainty of future cash flows that relate to past events – objective mechanism

– ‘automatic’ adjustment

Common features (2)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

25

Rate-regulated activities project timeline

July 2009

IASB published Exposure Draft of

Rate-regulated Activities proposals

September 2010

IASB suspended project

March 2013

IASB published Request for Information -

Rate Regulation (research project)

November 2013

IASB published Exposure Draft of

Regulatory Deferral Accounts

(interim ED)

Q1 2014

IASB expects to publish

Discussion Paper for Rate-regulated

Activities (research project)

Q1 2014

IASB expects to finalise interim

IFRS on Regulatory

Deferral Accounts

26

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Implementation

November 2013 Project update and the future work plan

IASB Work plan – as at 5 November 2013 28

November 2013 Project update and the future work plan

Next major project milestone

Narrow-scope amendments 2013 Q4 2014 Q1 2014 Q2 2013 Q4

Acquisition of an Interest in a Joint Operation

(proposed amendments to IFRS 11) Target IFRS

Actuarial Assumptions: Discount Rate

(proposed amendments to IAS 19) TBD

Annual Improvements 2010-2012 Target IFRS

Annual Improvements 2011-2013 Target IFRS

Annual Improvements 2012-2014 Target ED

Bearer Plants

(proposed amendments to IAS 41) Redeliberations

Clarification of Acceptable Methods of Depreciation

and Amortisation

(proposed amendments to IAS 16 and IAS 38)

Target IFRS

Defined Benefit Plans: Employee Contributions

(proposed amendments to IAS 19) Target IFRS

Implementation

IASB Work plan – as at 5 November 2013 29

November 2013 Project update and the future work plan

Next major project milestone

Narrow-scope amendments 2013 Q4 2014 Q1 2014 Q2 2014 Q3

Amendments to IAS1 (Disclosure Initiative) Target ED

Disclosure Requirements about Assessment of

Going Concern

(proposed amendments to IAS 1)

Target ED

Elimination of gains arising from ‘downstream’

transactions

(Proposed amendments to IAS28)

Target ED

Equity Method: Share of Other Net Asset

Changes

(proposed amendments to IAS 28)

Target IFRS

Fair Value Measurement: Unit of Account Target ED

Put Options Written on Non-controlling Interests

(proposed amendments to IAS 32) Target ED

Recognition of Deferred Tax Assets for

Unrealised Losses

(proposed amendments to IAS 12)

Target ED

Sale or Contribution of Assets between an

Investor and its Associate or Joint Venture

(proposed amendments to IFRS 10 and IAS 28) Target IFRS

Separate Financial Statements (Equity Method)

(proposed amendments to IAS 27) Target ED

Implementation (cont.)

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Bearer Plants

© 2012 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

30

Overview

Biological assets

Plants Animals

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

31

IAS 41 Fair value through

profit or loss

Current

requirements for

agricultural activity

Overview

Biological assets

Plants

Bearer plants Produce

growing on bearer plants

Other plants

Animals

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

32

IAS 16 Cost

or revaluation

model

IAS 41 Fair

value through

profit or loss

Proposed

requirements for

agricultural

activity

33 Scope of the amendments

• A bearer plant is plant that meets all of the following:

• used in production or supply of agricultural produce

• expected to bear produce for more than one period

• not intended to be sold as a living plant or harvested as

agricultural produce

• except incidental scrap sales

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Scope of the amendments

The following are not bearer plants:

• Plants to be harvested as agricultural produce

trees grown for lumber

• Plants both to produce agricultural produce and to

be harvested as agricultural produce or sold (other

than as scrap)

trees used for lumber and fruit

• Plants cultivated for sale only

plants in a garden centre

• Annual crops

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

34

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Post-implementation Reviews

November 2013 Project update and the future work plan

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS 3 Business Combinations

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

37 PiR of IFRS 3 Business Combinations

• The PiR of IFRS 3 Business Combinations is the IASB’s second review.

• The IASB discussed the PiR of IFRS 3 at its July 2013 meeting. At that meeting, the

IASB tentatively agreed that the scope of the PiR of IFRS 3 will include:

– the whole Business Combinations project (ie the first and second phases of the

project), which resulted in the issuance of IFRS 3 (2004) and IFRS 3 (2008); and

– any consequential amendments resulting from the Business Combinations project

(ie amendments to IAS 12 Income Taxes, IAS 27 Consolidated and Separate

Financial Statements, IAS 36 Impairment of Assets and IAS 38 Intangible Assets)

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

38 What we have heard so far • The following tables summarise the main areas of concern raised so far:

Conceptual matters

• Non-amortisation of goodwill: impairment test or amortisation?

• Recognition of intangibles separately from goodwill. Different recognition

criteria for intangibles: IFRS 3 vs. IAS 38 Intangible Assets.

• Different accounting treatments between IFRS 3 and other IFRSs: acquisition-

related costs, contingent consideration.

• Step acquisitions: recognition of gains/losses when remeasuring previously

held interests.

• Remeasurement of contingent consideration and recognition of gains/losses in

profit or loss.

• Measurement inconsistencies between initial recognition and subsequent

measurement for certain assets/liabilities; for example, decommissioning

liabilities.

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

39 What we have heard so far—continued

Matters for which further guidance or clarification may be needed

• Definition of a business

• Measurement of certain assets and liabilities at fair value has proved to be challenging (eg

intangibles, contingent consideration, previously held interests).

• Measurement of the settlement of pre-existing customer relationships.

• Distinguishing contingent consideration from remuneration.

• Measurement option for non-controlling interests (NCIs): should the option be per business

combination or should it be an accounting policy choice for all business combinations of an

entity?

• Accounting for impairment testing of goodwill when NCIs are recognised. In particular,

clarification of the requirements relating to:

(a) calculating the ‘gross up’ of the carrying amount of goodwill when partial goodwill is

recognised because NCI is measured on a proportionate share basis;

(b) allocation of impairment losses between the parent and NCI; and

(c) reallocation of goodwill between NCI and controlling interests after a change in a parent’s

ownership interest in a subsidiary that does not result in a loss of control.

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

40 What we have heard so far—continued

Matters on which further guidance or clarification may be needed

• Mandatory purchases of NCIs in business combinations and put options written on NCIs.

• Accounting treatment of acquisition-related costs and step acquisitions in separate financial

statements.

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

41 What have we heard so far—continued

Matters raised by users

• Information needed to be able to estimate the enterprise value of the acquiree. What are the

debts, pension liabilities, finance lease obligations assumed etc?

• Some users have stated that the measurement of assets and liabilities at fair value (eg

tangible/intangible assets, inventory) impairs the ability to assess the underlying performance

in the quarters subsequent to an acquisition. More information needed about inputs and

assumptions used in the valuations (sometimes ‘significant step-ups’ are observed).

• Require disclosure of the carrying amounts of the assets acquired and liabilities assumed

(former paragraph 67 of IFRS 3 (2004) removed in 2008).

• Information about the nature of the intangible assets acquired (intangibles with finite lives,

indefinite lives, intangibles that are sustained through expenditure that goes to profit or loss).

• Different views on the usefulness of goodwill amortisation vs impairment test.

• Comparative information should be required for proforma disclosures.

• It is difficult to track subsequent performance. Information about subsequent performance

would be useful for assessing whether an acquisition was successful.

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

42 Next steps

• We will bring the result of the consultations and activities undertaken during Phase I to

the November 2013 IASB meeting.

• At that meeting we will propose to the IASB the main areas that the Request for

Information (RfI) should focus on. Phase I of the PiR will conclude with the publication

of the RfI, which will set the scope for Phase II of the PiR.

• We aim to publish the RfI early next year with a comment period of 120 days.

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Research

November 2013 Project update and the future work plan

The standard-setting process 44

Research Discussion

Paper

Post-

implementation

Review

Exposure

Draft Final IFRS

Research

programme

Standards

programme

Review

programme

Proposal

Research programme

• A broad research and development programme

• Emphasis on defining the problem – Identify whether there is a financial reporting matter that justifies an

effort by the IASB

– Evidence based

• Discussion Papers – IASB staff papers

• Research Papers – Commissioned from others in the IFRS network

• Leads to project proposals, or recommendations not to develop an

IFRS

45

November 2013 Project update and the future work plan

Standards-level Programme

• Major projects feed from the research programme

• Narrower scope improvements feed from the interpretations

committee and the other implementation outreach

• More focused and disciplined development of standards

46

November 2013 Project update and the future work plan

Priority research projects

• Rate-regulated activities

• Business combinations under common control

• Discount rates

• Equity method

47

November 2013 Project update and the future work plan

Priority research projects

• Emissions trading schemes

• Extractive activities | Intangible assets | Research and

Development activities

• Financial Instruments with the Characteristics of Equity

• Foreign Currency Translation

• Liabilities – amendments to IAS 37

• Hyperinflation, and high inflation

48

November 2013 Project update and the future work plan

Thank you 49

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org