idfc us equity fund deck 04

TRANSCRIPT

IDFC US Equity Fund of FundBenefit from Strong Structural Opportunities in a Resilient US Market

NFO Opens: 29th July 2021NFO Closes: 12th August 2021

?

3. Why IDFC US Equity Fund of Fund?

2. Why Invest in US Equities Now?

1. Why Invest in US Equities?

Participation only in Indian assets has historically limited the Indian investor’s portfolio

TraditionalDiversification

Strategies in the Home Country /

Domestic Market

Asset Class

Split between Equity,Fixed Income,

Commodities, etc

Within Asset Class

Split basis company size, sector,

creditworthiness, etc

Geographical

Split across different markets in the world

Suggested Additional

Diversification

Investing in global markets offers a powerful opportunity for improved diversification

3

Russell 1000 Growth index considered as investment in US markets and Nifty 50 as investment in India. Both the indices have been rebased to 10,000 on Dec 2011 to arrive at the above rolling returns.

Source: Russell website, investing.com, internal analysis

Data as on 30th June 2021

Past performance is not an indicator of future performance

Low Correlation between India and US equity markets

Rolling 1 year returns

Combining investments with low correlation improves portfolio efficiency and diversification

-40%

-20%

0%

20%

40%

60%

80%

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

Jun

-13

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

Sep

-18

Dec

-18

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Mar

-20

Jun

-20

Sep

-20

Dec

-20

Mar

-21

Jun

-21

US equity market India equity market

4

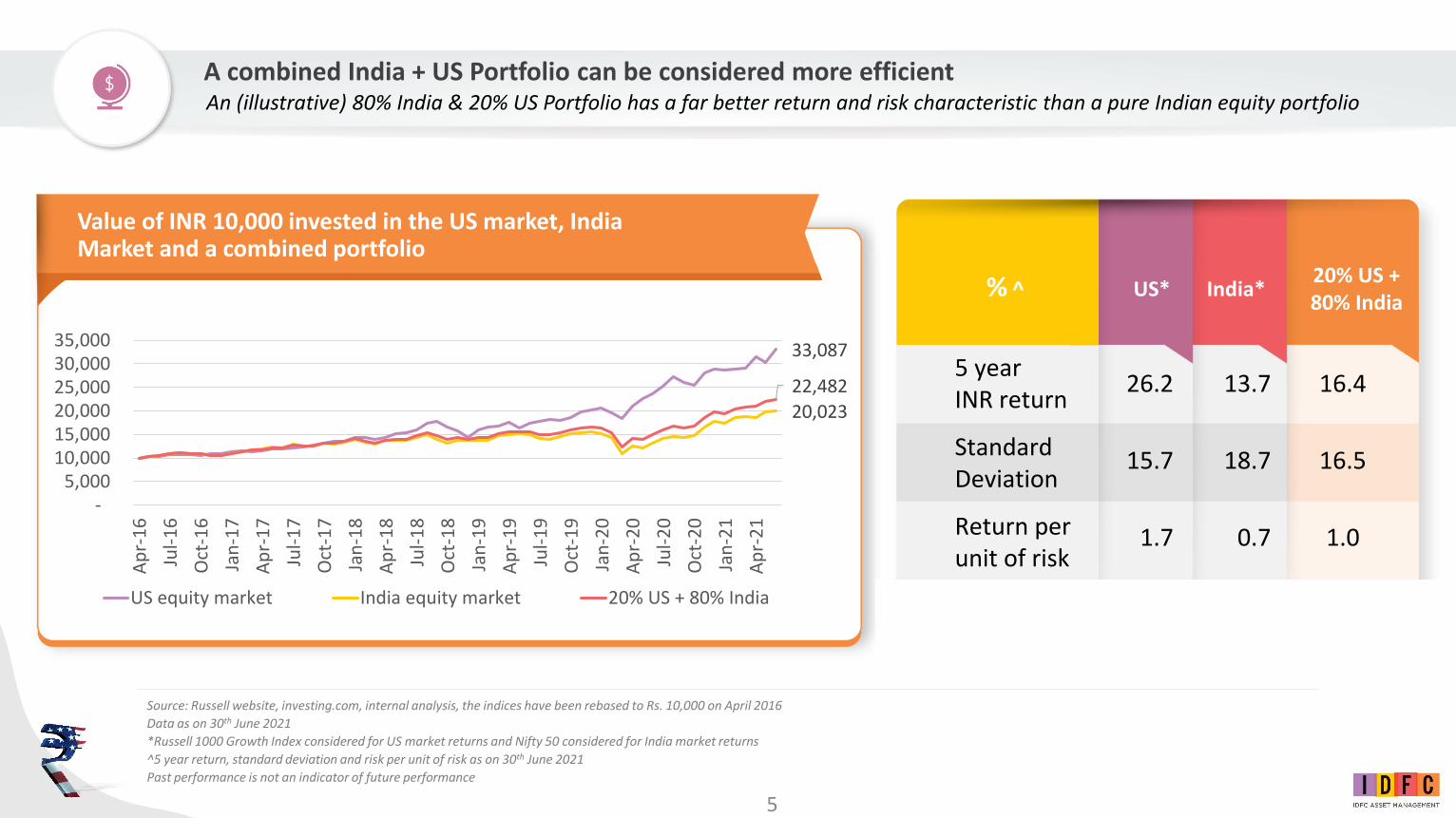

Source: Russell website, investing.com, internal analysis, the indices have been rebased to Rs. 10,000 on April 2016

Data as on 30th June 2021

*Russell 1000 Growth Index considered for US market returns and Nifty 50 considered for India market returns

^5 year return, standard deviation and risk per unit of risk as on 30th June 2021

Past performance is not an indicator of future performance

Value of INR 10,000 invested in the US market, India Market and a combined portfolio

% ^ US* India*20% US +80% India

5 year INR return

Standard Deviation

Return per unit of risk

26.2 13.7 16.4

15.7 18.7 16.5

1.7 0.7 1.0

A combined India + US Portfolio can be considered more efficient

33,087

20,023

22,482

- 5,000

10,000 15,000 20,000 25,000 30,000 35,000

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

Jul-

19

Oct

-19

Jan

-20

Ap

r-2

0

Jul-

20

Oct

-20

Jan

-21

Ap

r-2

1

US equity market India equity market 20% US + 80% India

An (illustrative) 80% India & 20% US Portfolio has a far better return and risk characteristic than a pure Indian equity portfolio

5

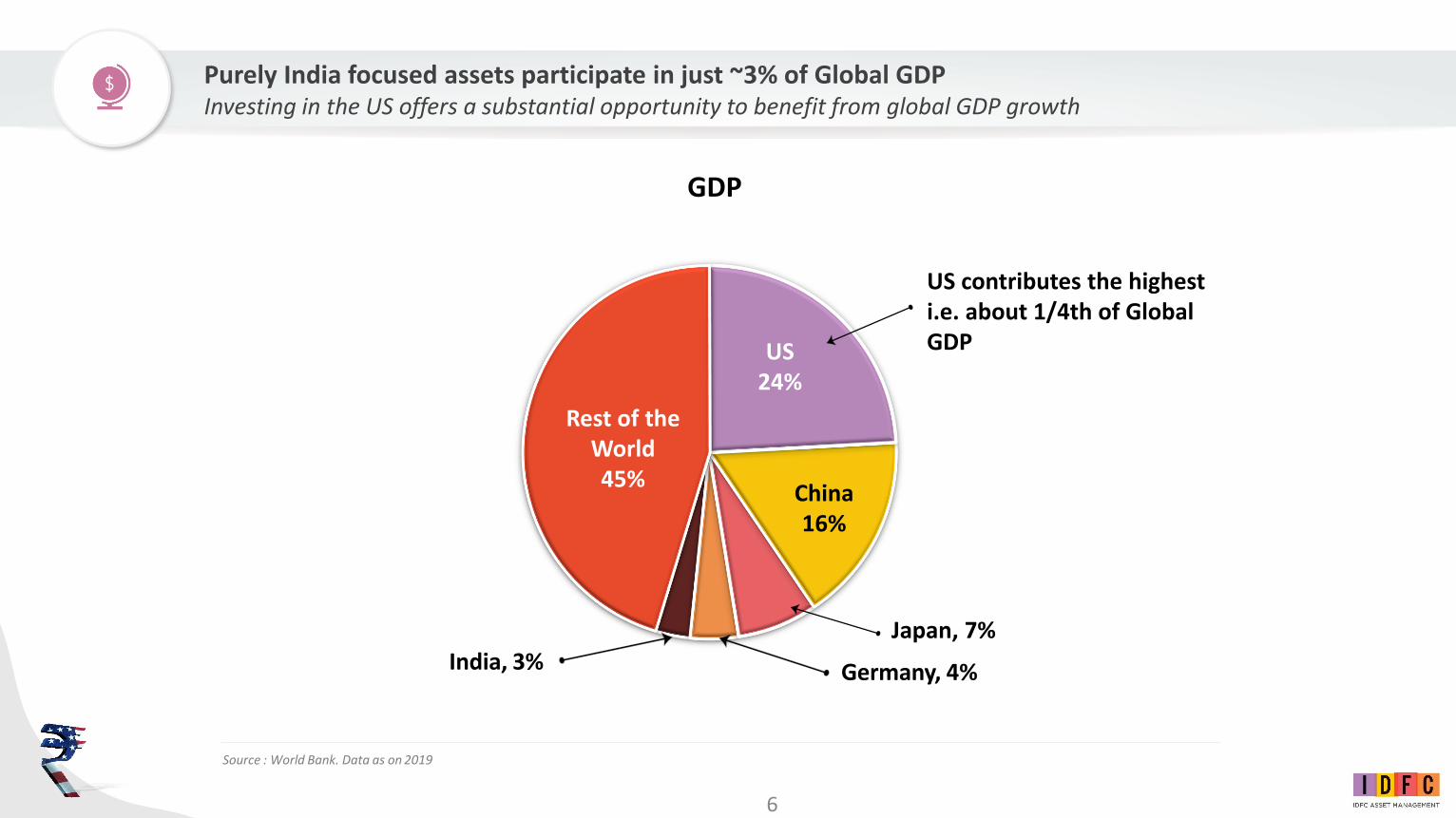

Source : World Bank. Data as on 2019

US24%

China16%

US contributes the highest i.e. about 1/4th of Global GDP

Japan, 7%

Germany, 4%India, 3%

Rest of the World45%

GDP

Purely India focused assets participate in just ~3% of Global GDPInvesting in the US offers a substantial opportunity to benefit from global GDP growth

6

*includes companies invested in by the underlying fund of IDFC US Equity FoF. Data as on 31st Mar’21; Source: Factset

Global Revenue split of US companies*

59%US Market

41% Non -

US Market

US Companies are a good mix of US and Global RevenuesOver 40% of Revenues in a portfolio of US Equities* can come from Non-US revenue pools

7

Source: Factset, MSCI, Standard & Poor’s, J.P. Morgan Asset Management.

Returns are total returns based on MSCI indices, except the U.S., which is the S&P 500. China return is based on the MSCI China index. 10-yr total (gross) return data is used to calculate annualized returns (Ann. Ret.) and annualized volatility and reflect the period 30/04/11 - 30/04/21. Past performance is not an indicator of future performance

ASEAN 32.4%

U.S. 2.1%

India 26.0%

U.S. 32.4%

India 23.9%

Japan 9.9%

U.S. 12.0%

China 54.3%

U.S. -4.4%

U.S. 31.5%

China 29.7%

Europe 11.0%

U.S. 14.2%

India 22.4%

India 20.9%

ASEAN -6.1%

China 23.1%

Japan 27.3%

U.S. 13.7%

U.S. 1.4%

APAC ex-JP 7.1%

India 38.8%

India -7.3%

Europe 24.6%

APAC ex-JP 22.8%

U.S.10.2%

China7.5%

China 20.6%

APAC ex-JP 18.4%

Europe -10.50%

ASEAN 22.8%

Europe 26.0%

China 8.3%

Europe-2.3%

ASEAN 6.2%

APAC ex-JP 37.3%

ASEAN -8.4%

China 23.7%

U.S. 18.4%

India 8.8%

Japan 7.3%

APAC ex-JP 16.8%

Japan 15.6%

Japan -14.2%

APAC ex-JP 22.6%

China 4.0%

ASEAN 6.4%

India -6.1%

Japan 2.7%

ASEAN 30.1%

Japan -12.6%

Japan 20.1%

India 15.9%

APAC ex-JP 3.6%

APAC ex-JP 6.4%

Europe 16.6%

U.S. 15.1%

APAC ex-JP -15.40%

Europe 19.9%

APAC ex-JP 3.7%

APAC ex-JP 3.1%

China -7.6%

China 1.1%

Europe 26.2%

APAC ex-JP -13.7%

APAC ex-JP 19.5%

Japan 14.9%

Japan 0.7%

Europe 5.4%

ASEAN 16.5%

China 4.8%

China -18.2%

U.S. 16.0%

India -3.8%

Japan -3.7%

APAC ex-JP -9.1%

Europe 0.2%

Japan 24.4%

Europe -14.3%

ASEAN 8.8%

Europe 5.9%

ASEAN -1.4%

India 4.5%

US 13.6%

Europe 4.5%

India -37.2%

Japan 8.4%

ASEAN -4.5%

Europe -5.7%

ASEAN -18.4%

India -1.4%

U.S. 21.8%

China -18.7%

India 7.6%

ASEAN -6.2%

China -1.8%

ASEAN 1.6%

Japan 13.4%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 YTD’21Annual Return

Risk (Volatility)

2010

US has been the most consistent equity market with low volatility over the last decadeIn addition to the highest return, it has also displayed the lowest risk (volatility)

In a Global rally, US has rewarded well; e.g. 2010, 2012, 2017

In a negative/low return environment Globally, US has shown resilience and performed better than other geographies; e.g. 2011, 2013, 2016

8

Source: Bloomberg, J.P. Morgan Asset Management. As of 31 December 2020. Past performance is not an indicator of future performance

US Equity Performance has been driven by higher Earnings growth Vs Rest-of-the-worldEarnings growth has averaged 6% in the US Vs -4% in the rest of the world

12.5%

9.9%

5.4%6.0%

3.6%

-3.6%-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

US Large Cap Growth Index(Russell 1000 Growth Index)

US Large Cap Index(S&P 500 Index)

World Index(MSCI ACWI ex-USA Index)

15 Year Annualized Performance and Earnings Growth

Return Earnings growth

9

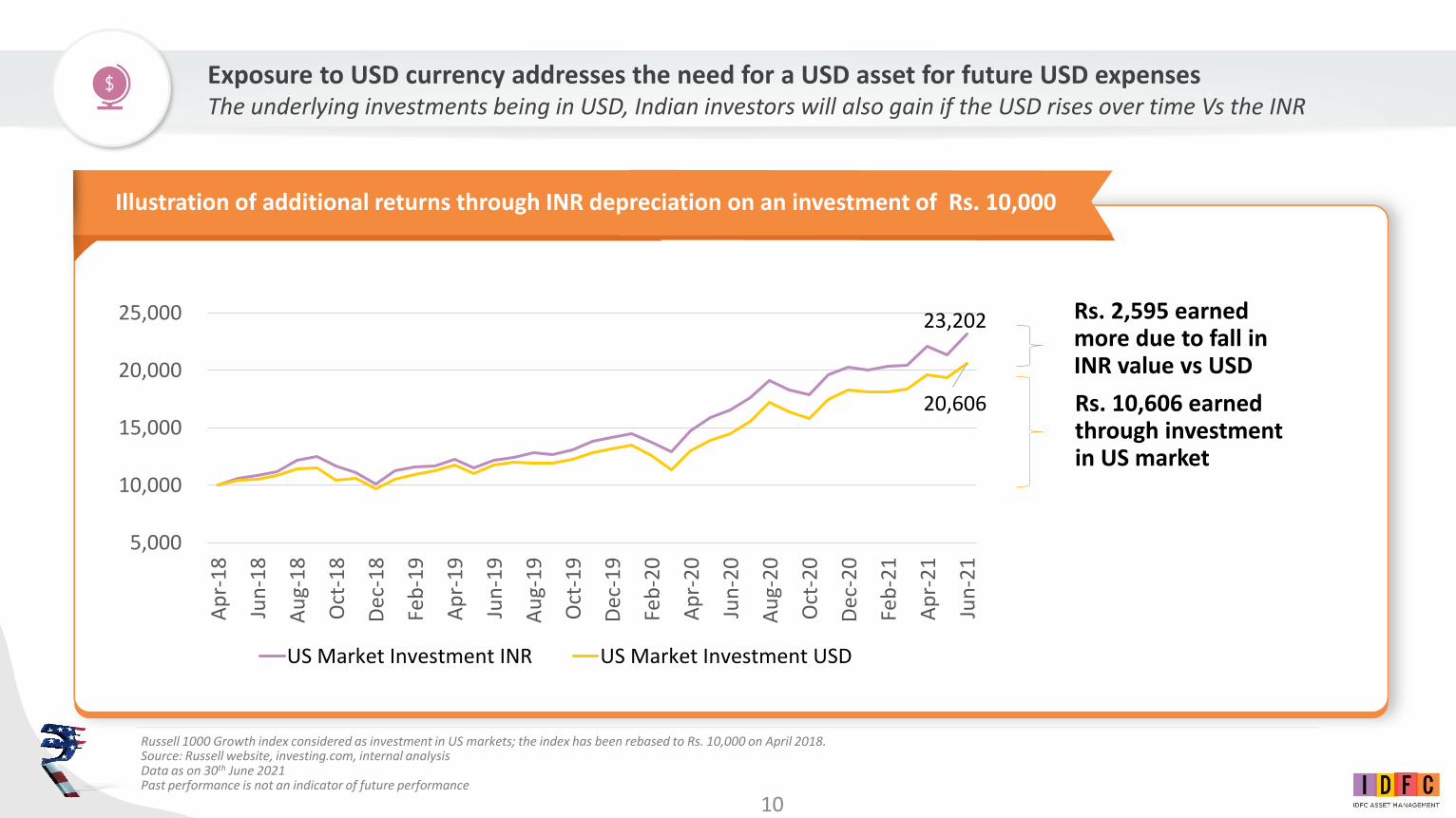

Russell 1000 Growth index considered as investment in US markets; the index has been rebased to Rs. 10,000 on April 2018.Source: Russell website, investing.com, internal analysisData as on 30th June 2021Past performance is not an indicator of future performance

Rs. 10,606 earned through investment in US market

Rs. 2,595 earned more due to fall in INR value vs USD

23,202

20,606

5,000

10,000

15,000

20,000

25,000

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

Dec

-18

Feb

-19

Ap

r-1

9

Jun

-19

Au

g-1

9

Oct

-19

Dec

-19

Feb

-20

Ap

r-2

0

Jun

-20

Au

g-2

0

Oct

-20

Dec

-20

Feb

-21

Ap

r-2

1

Jun

-21

US Market Investment INR US Market Investment USD

Illustration of additional returns through INR depreciation on an investment of Rs. 10,000

Exposure to USD currency addresses the need for a USD asset for future USD expensesThe underlying investments being in USD, Indian investors will also gain if the USD rises over time Vs the INR

10

In Summary, 5 key reasons why US Equities are a powerful complementary addition for the Indian investor’s portfolio

1. Effective

Diversification

2. Access a

large Global

Revenue Pool

3. Consistent

Performance

4. Earnings

Driven5. Creation of

a USD asset

Low correlation with Indian Equities helps US Equities provide

attractive diversification

benefits

Not just the largest

economy, US

Equities offer

participation in a

significant global

revenue pool

Among major blocks,

the US has provided

attractive returns with

low risk – a great

combination of

reward with resilience

Higher US Equity market performance may be attributed to its superior earnings

growth

Add currency exposure to your portfolio to meet future expenses

and/or for potential gains from currency

movement

Past performance is not an indicator of future performance

11

?

3. Why IDFC US Equity Fund of Fund?

2. Why Invest in US Equities Now?

1. Why Invest in US Equities?

Aren’t US market valuations already

too high?

Isn’t the pandemic going to hurt US

growth?

Aren’t we too late to enter now?

Is the end of this bull market nearing?

What can drive US earnings

growth?

US Markets : Some of the dilemmas

13

Source: Factset, Standard & Poor’s, J.P. Morgan Asset Management, Guide to the Markets – U.S. Data as on 30th June 2021; P/E – Price to Earnings Ratio*based on last 12 months’ earnings^For about 25 years

Top 10 stocks

Next ~490 stocks

S&P 500

12 month Forward P/E

Average P/E ^

Premium (% of Average)

30.0x 19.6x 53%

18.9x 15.6x 21%

21.5x 16.3x 32%

Market Cap Weight in S&P 500

28.6%

71.4%

Earnings contribution*

30.5%

69.5%

US market: Is it expensive?Valuation Premium of non-Top 10 stocks more reasonable, which contribute significantly to overall Earnings

14

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. A bear market represents a 20% or more decline from the previous market high; a bull market represents a 20% increase from a market trough. Charts and labels refer to price return. Past performance is not a reliable indicator of current and future results. Data as of 31/03/21. Provided for information only to illustrate general market trends not to be construed as research or investment advice. Investments involve risks and are not similar or comparable to deposits. Not all investment ideas referenced are suitable for all investors. Provided for information only, not to be construed as investment advice.

• If the bull market ended today, it would be the shortest and the weakest bull market since the 1960s

• Low policy rates and stimulus/spending helping

S&P 500 bull market gains

Is the bull market over? Past Bull market phases have lasted longer

15

Source: FactSet, J.P. Morgan Asset Management, IDFC internal Analysis, investing.com; Data are as of 30th June 2021. Provided for information only to illustrate general market trends not to be construed as research or investment advice. Investments involve risks and are not similar or comparable to deposits. Not all investment ideas referenced are suitable for all investors.

Average cumulative S&P 500 total returns (Jan 1988 – Jun 2021)

Invest for the long-term – Timing doesn't matterInvesting when the market has touched a new high can provide reasonable returns too

14.3%

46.5%

79.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 year 3 years 5 years

16

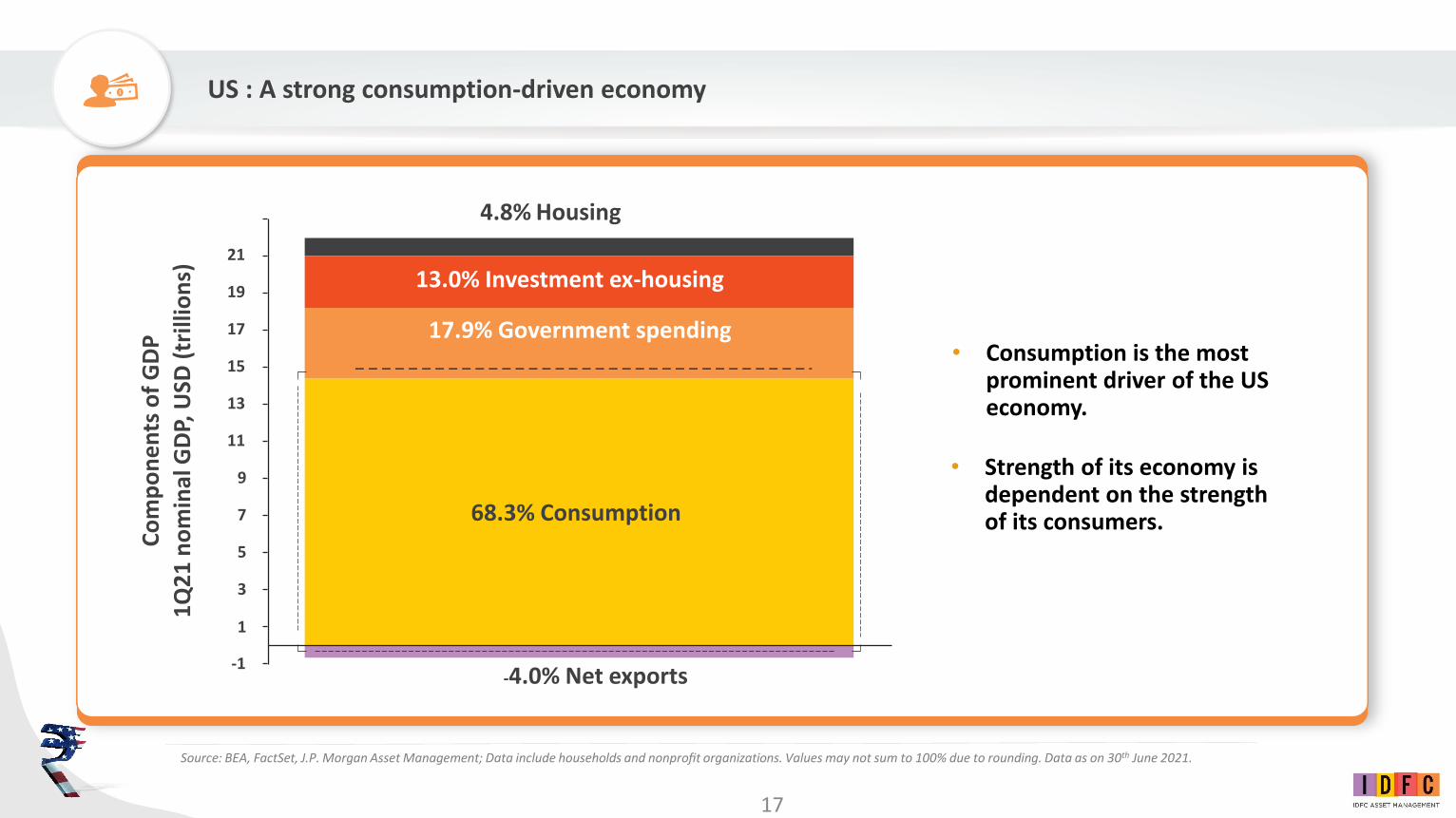

Source: BEA, FactSet, J.P. Morgan Asset Management; Data include households and nonprofit organizations. Values may not sum to 100% due to rounding. Data as on 30th June 2021.

21

19

17

15

13

11

9

7

5

3

1

-1-4.0% Net exports

13.0% Investment ex-housing

17.9% Government spending

68.3% Consumption

Co

mp

on

en

ts o

f G

DP

1Q

21

no

min

al G

DP,

USD

(tr

illio

ns)

4.8% Housing

• Consumption is the most prominent driver of the US economy.

• Strength of its economy is dependent on the strength of its consumers.

US : A strong consumption-driven economy

17

Source: (Left) Johns Hopkins University, World Bank – World Development Indicators, J.P. Morgan Asset Management. North America includes U.S. and Canada; Europe includes France, Germany, Italy, Spain, UK; Asia includes Australia, China, Hong Kong, India, Japan, Singapore and South Korea; Latin America includes Brazil, Chile, Peru and Mexico. Population numbers are based on World Bank data as of 31/12/19.; (Right) Source: Centers for Disease Control and Prevention, Johns Hopkins CSSE, Our World in Data, J.P. Morgan Asset Management. *Share of the total population that has received at least one vaccine dose. **Est. Infected represents the number of people who may have been infected by COVID-19 by using the CDC’s estimate that 1 in 4.6 COVID-19 infections were reported. ***Est. Infected & vaccinated assumes those infected equally likely to be vaccinated as those not infected. On March 6th, 2021, JP Morgan moved up their threshold for herd immunity from 60-80% to 70-90% based on the comments by Dr. Anthony Fauci that the prevalence of more contagious variants have pushed up the target herd immunity threshold for the U.S. Guide to the Markets –U.S. Data are as of May 31, 2021.

Daily increase in cases (region)(7-day moving average, per million people)

Progress to herd immunityPercentage of population, end of month

Aggressive Vaccination rollout and sharply falling Covid cases in the US have led to expectations of quicker normalization

18

Source: BEA. **1Q21 figures for debt service ratio and household net worth are J.P. Morgan Asset Management estimates. Data are as of 31st March, 2021. Provided for information only to illustrate general market trends not to be construed as research or investment advice. Investments involve risks and are not similar or comparable to deposits. Not all investment ideas referenced are suitable for all investors. SA – Seasonally Adjusted

Household Debt at a historic low Household Net Worth at a historic high+Household debt service ratioDebt payments as % of disposable personal income, SA

Household net worthNot seasonally adjusted, USD (billions)

Low household debt + Historically high net worth = Expected to unleash pent-up consumption demand

1Q80:10.6%

4Q07:13.2%

1Q21**:9.4%

3Q07:70,912

1Q21**:134,669

19

Source of Real GDP and forecast growth from 2Q21 onwards: JP Morgan Investment Banking

Source of Earnings per share: JP Morgan Asset Management; estimates as of 31st March 2021. Opinions, estimates, forecasts, projections and statements of financial market trends that are based on current market conditions constitute the judgement of JP Morgan Asset Management and are subject to change without notice.

Pent-up demand expected to drive GDP growth in the second half of 2021, with GDP growth expected to range between 6-7% for CY21, the highest in almost 40 years

Real GDP actual and forecast Earnings per share for S&P 500

Expectations of strong recovery in economic activity and earnings

20

i

Source: J.P. Morgan Asset Management. As of 31st March 2021. Opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgment and are subject to change without notice. There can be no guarantee they will be met. Image Source: Shutterstock. Provided for information only to illustrate general market trends not to be construed as research or investment advice. Investments involve risks and are not similar or comparable to deposits. Not all investment ideas referenced are suitable for all investors.

The US remains at the centre-stage of new-age innovations

• Innovations across sectors expected to advance the economy further

• Many of these innovative themes may not be directly available in India

Energy ENERGYSolar & Wind Energy

INDUSTRIALS / AUTOSElectric Vehicles

MEDIAConnected TV &

Streaming

CONSUMERHome Automation

HEALTHCAREMedical TechnologyUse of data / AI

FINANCIALSPayments

US

21

^Past performance is not an indicator of future performance

1. Expected broader market pick up

Lower Valuations for the Broader

market vs top 10 stocks, thereby

offering the potential to benefit from growth in the

Broader market

2. For the long-term investor

Irrespective of market timing, investing for the long-term offers significant potential^

In Summary, 5 key reasons why US equities continue to be well-poised to deliver growth

3. Highest GDP

growth in ~40

years expected

Being essentially a

consumption-driven

economy, US to

benefit from

consumers unleashing

their pent-up demand

and savings, supported

by low debt levels and

high net worth

4. Reopening of the US economy

US to benefit from lowering Covid-19 cases and reaching

herd immunity

5. Innovative themes

Participate in the

growth of innovative

themes that may not

be available in India

and are expected to

advance the US

economy further

22

?

3. Why IDFC US Equity Fund of Fund?

2. Why Invest in US Equities Now?

1. Why Invest in US Equities?

Bringing the opportunity of investing in a Growth focused portfolio of US stocks

IntroducingIDFC US Equity Fund of Fund

• The underlying fund(/s) will be based on the existing US market view and outlook of the fund manager

• Currently, the fund will invest in an underlying fund with a Growth-style investing

Structure of the Investment

Investors IDFC US Equity Fund of Fund

Underlying Fund

Note: It will not be a dedicated feeder fund structure and the Indian fund is open to invest in funds that meet the investment objective and strategy

An overview of the IDFC US Equity Fund of FundAn open-ended fund of fund scheme investing in units/shares of overseas Mutual Fund Scheme (/s) / Exchange Traded Fund (/s) investing in US Equity securities

Equity sharesof US

companies

25

Underlying Fund: The J.P. Morgan US Growth FundA carefully chosen fund with a well-tested investment process and well-proven track record

60-90 stock portfolio – Large-cap focused with some mid-cap exposure ~ USD 1.8Bn of assets as on Jun’21

Fund Inception Date: 20th Oct’00Share Class inception date: 3rd Oct’13*

Global exposure: 40% of the revenue of the underlying stocks contributed by countries outside of US

Bottom-up investment approach to identify companies with :• A large addressable market undergoing meaningful change• Sustainable competitive advantage and strong execution• Good price momentum

An experienced lead portfolio manager supported by a team of sector research analysts

*Underlying fund is JPMorgan Funds – US Growth Fund; Class: JPM US Growth I (acc) USD

J.P. Morgan US Growth

Fund

26

• Run proprietary quantitative screens on Russell 1000 Growth Index (approx. 800 names)➢ earnings revisions➢ price momentum➢ valuation

• Narrow investable universe to 150-200 companies

• Company meetings

• Industry conferences

• Bottom-up, fundamental

• Giri Devulapally, lead portfolio manager, uses the fundamental analysis coupled with his insights to create a portfolio of 60-90 stocks

• Position sizes determined by conviction level➢ quality of business➢ risk/reward➢ diversification impact on portfolio

• Portfolio guidelines:➢ Sectors at + / - 10% relative to the

benchmark➢ Stocks at + / - 5% relative to the

benchmark

• Determine if a prolonged growth opportunity exists

• Assess competitive dynamics

• Evaluate the attractiveness of the business model

• Track record of management’s ability to execute

• Potential for margin expansion

• Balance sheet strength

Source: J.P. Morgan Asset Management

Idea Generation Fundamental Analysis Portfolio Construction

The Underlying Fund deploys a fundamentals driven, bottom-up process to build a portfolio of high conviction companies

27

Source: J.P. Morgan Asset Management. ESG = Environment, Social, and Governance.

• Decades of insight

• Globally consistent

• Systematic approach

Global Equity Research Team

A robust framework to evaluate each company under coverage on ESG dimensions

Supported by:Investment Stewardship ProfessionalsOver 20 years experience with corporate engagement and governance oversight

Environment

• Climate Change

• Natural Resources

• Pollution and Waste

• Environmental Opportunities

12 questions

Social

• Human Capital

• Product Liability

• Stakeholder Opposition

• Social Opportunities

12 questions

Governance

• Corporate Governance

• Corporate Behaviour

16 questions

ESG principles embedded in the research process of the Underlying Fund

28

Source: J.P. Morgan Asset Management. The securities highlighted above have been selected based on their significance and are shown for illustrative purposes only. It should not be interpreted as a recommendation to buy or sell. It should not be assumed that other securities in the portfolio have performed in a similar manner. The Strategy is an actively managed portfolio, holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager without notice.

Merchants spending more on digital advertising to build mindshare in the online world

• Emerging and innovative: Snap, Twitter, Pinterest

• Sizeable absolute positions in Alphabet and Facebook

Increased conviction in traditional financials while owning secular winners in payments

• Steady, high-quality franchises that have robust tailwinds: Charles Schwab, Morgan Stanley, Blackstone

• Payments: PayPal, Square

Companies that are well-positioned to benefit from technological innovation

• Industrials capitalizing on company-specific drivers:

Deere, Freeport-McMoran, Rockwell Automation

• Consumer-facing platforms:

Zillow, Carvana, Wayfair

Stocks that have outperformed substantially over the course of many years where fundamentals seem to be well-understood.

The Underlying Fund provides access to unique business models and companies

Digital Advertising Financials Technology - EnabledWhere the fundis less exposed

29

Source: J.P. Morgan Asset Management, Morningstar. Data as on 31st May 2021; 12-month forward EPS growth has been provided above.

Diversified Portfolio - with lower exposure to Top 10 index constituents

28%

46%

% weight in top ten index holdings

25%

20%

EPS Growth

Higher Earnings growth characteristics

Fund Benchmark

The Underlying Fund is actively managed with a broad-based, growth-oriented portfolioThe portfolio has a lower concentration among top index constituents and higher portfolio earnings growth

Fund Benchmark

30

Portfolio performance of the Underlying Fund (USD)

Source: J.P. Morgan Asset Management. Fund performance is shown based on the NAV of the share class I in USD with income (gross of shareholder tax) reinvested including actual ongoing chargesexcluding any entry and exit fees. Figures greater than 1 year are annualised. The benchmark figures are net of 30% withholding tax. The Fund changed its name from JPM US Strategic Growth Fund to JPMUS Growth Fund on 11th April 2011. Past performance may or may not be sustained in the future.

As on 31st May 2021 One Year Three Years Five Years Since inception

JPM US Growth Fund 46.5% 27.2% 26.6% 19.9%

Russell 1000 Growth Index (Benchmark)

39.6% 22.6% 21.6% 17.9%

Excess Return 6.9% 4.6% 5.0% 2.0%

Annualised Return

31

Calendar year performance

Portfolio performance of the Underlying Fund (USD)

As on 31st May 2021 CY’21 YTD CY’20 CY’19 CY’18 CY’17 CY’16 CY’15 CY’14

JPM US Growth Fund 5.6% 55.7% 38.7% 0.6% 37.6% -2.5% 7.4% 12.7%

Russell 1000 Growth Index (Benchmark)

6.2% 38.1% 35.9% -1.9% 29.7% 6.6% 5.2% 12.5%

Excess Return -0.6% 17.7% 2.8% 2.4% 7.9% -9.1% 2.2% 0.2%

Source: J.P. Morgan Asset Management. Fund performance is shown based on the NAV of the share class I in USD with income (gross of shareholder tax) reinvested including actual ongoing chargesexcluding any entry and exit fees. Figures greater than 1 year are annualised. The benchmark figures are net of 30% withholding tax. The Fund changed its name from JPM US Strategic Growth Fund to JPMUS Growth Fund on 11th April 2011. Past performance may or may not be sustained in the future.

32

As on 31st May 2021 One Year Three Years Five Years Since inception

JPM US Growth Fund 40.5% 30.3% 28.5% 22.5%

Russell 1000 Growth Index (Benchmark)

33.9% 25.6% 23.5% 20.5%

Excess Return 6.6% 4.7% 5.0% 2.1%

Annualised Return

Portfolio performance of the Underlying Fund (INR)

Source: J.P. Morgan Asset Management and IDFC internal analysis. INR performance has been derived from the USD returns. Fund performance is shown based on the NAV of the share class I in USD withincome (gross of shareholder tax) reinvested including actual ongoing charges excluding any entry and exit fees. Figures greater than 1 year are annualised. The benchmark figures are net of 30%withholding tax. The Fund changed its name from JPM US Strategic Growth Fund to JPM US Growth Fund on 11th April 2011. Past performance may or may not be sustained in the future.

33

Calendar year performance

As on 31st May 2021 CY’21 YTD CY’20 CY’19 CY’18 CY’17 CY’16 CY’15 CY’14

JPM US Growth Fund 4.8% 59.4% 42.3% 9.6% 29.3% 0.0% 12.8% 14.9%

Russell 1000 Growth Index (Benchmark)

5.5% 41.3% 39.4% 6.9% 21.8% 9.4% 10.5% 14.8%

Excess Return -0.6% 18.1% 2.9% 2.7% 7.4% -9.3% 2.3% 0.2%

Portfolio performance of the Underlying Fund (INR)

Source: J.P. Morgan Asset Management and IDFC internal analysis. INR performance has been derived from the USD returns. Fund performance is shown based on the NAV of the share class I in USD withincome (gross of shareholder tax) reinvested including actual ongoing charges excluding any entry and exit fees. Figures greater than 1 year are annualised. The benchmark figures are net of 30%withholding tax. The Fund changed its name from JPM US Strategic Growth Fund to JPM US Growth Fund on 11th April 2011. Past performance may or may not be sustained in the future.

34

Sector positions

Source: Wilshire. The portfolio is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager without notice. As of September 2020, Russell Global Sectors (RGS) classification scheme has been decommissioned and has been replaced by the new Industry Classification Benchmark (ICB) classification. Data as on 31st May 2021.

Sector breakdown Vs the benchmark of the Underlying FundPortfolio repositioned towards cyclicals, beneficiaries of reopening of the economy

Portfolio Weight Benchmark Weight

Financials 9.2 2.0

Industrials 15.9 12.5

Basic Materials 1.8 0.3

Consumer Staples 4.2 3.5

Utilities - 0.1

Energy 0.1 0.3

Real Estate 1.3 2.0

Telecommunications 0.2 0.9

Consumer Discretionary 18.5 19.3

Health Care 9.5 13.3

Technology 39.3 45.8

7.2

3.4

1.5

0.7

(0.1)

(0.2)

(0.7)

(0.7)

(0.8)

(3.8)

(6.5)

Portfolio Over/ (Under) Weight

35

Top 10 Holdings Fund weight

(%)

Alphabet2 6.2

Apple 5.7

Microsoft 4.7

Facebook 4.6

Deere 3.4

PayPal Holdings 3.3

Amazon.com 3.2

Snap 2.6

Charles Schwab 2.3

Morgan Stanley 2.1

Source: Factset, Wilshire (excludes cash), J.P. Morgan Asset Management. 1. Relative to the Russell 1000 Growth Index. 2. Based on combining the positions of both Alphabet share classes (GOOGL and GOOG) which are listed in the Russell 1000 Growth Index. 3. excludes negatives *Indicates stock not held in the portfolio as of 31st May 2021. The portfolio is actively managed. Holdings, sector weights, allocations and leverage, as applicable, are subject to change at the discretion of the investment manager without notice.

Key Portfolio Statistics

Fund Benchmark

Weighted Average Market Cap

USD 499.9b

USD 763.0b

Price / Earnings,12-mth fwd3

23.6x 26.0x

EPS Growth, 12-mth fwd

24.8% 19.5%

Return on Equity, last 12-mth

22.9% 28.4%

Number of holdings

81 458

Portfolio Details of the Underlying FundAn active overweight in select ‘non-traditional’ stocks and an underweight in the recent winners

Top

5o

verw

eig

hts

1To

p 5

un

der

wei

ghts

1

Fund weight (%)

Relative position (%)

Deere 3.4 3.4

Snap 2.6 2.6

Charles Schwab 2.3 2.3

Morgan Stanley 2.1 2.1

Blackstone Group 2.0 2.0

Microsoft 4.7 -4.9

Apple 5.7 -4.5

Amazon.com 3.2 -3.8

Visa* 0.0 -2.0

UnitedHealth Group* 0.0 -1.7

36

As of 31st March 2021. Years of experience: Industry/Firm. *Back-up PM. There can be no assurance that professionals currently employed by JPMAM will continue to be employed by JPMAM or that past performance or success of such professionals serve as an indicator of the professionals’ future performance or success.

Giri DevulapallyManaging DirectorPortfolio ManagerExperience: 29/18

Joe WilsonManaging Director

Co-PM*/Technology Analyst

Technology Experience: 16/7

Larry LeeManaging Director

Financials / Business Services Analyst

IT Services & Financial SvcsExperience: 28/15

Robert MaloneyVice President

Industrials, Energy & Materials Analyst

IndustrialsExperience: 21/8

Holly FleissExecutive Director

Health Care AnalystHealth Care

Experience: 16/9

Sarah DodsonExecutive DirectorConsumer Analyst

ConsumerExperience: 12/3

Also leverages the insights of the J.P. Morgan Equity organization, which includesover 40 research analysts in the U.S. and over 200 globally

The Underlying Fund has a tight-knit portfolio team focused on Large Cap Growth100+ years of combined experience

37

Investment in the FoF akin to any other Indian Mutual Fund

Investment Objective The Fund seeks to generate long term capital appreciation by investing in units/shares of overseas Mutual Fund Scheme (/s) / Exchange Traded Fund (/s) investing in US Equity securities.*

*However, there can be no assurance that the investment objective of the Scheme will be realized. ̂ Total Return Net of 30% withholding tax

Investment in the FoF

Exit Load1% of applicable NAV - if the units are

redeemed/switched out within 1 year from the date of allotment

Nil – if the units are redeemed / switched-out after 1 year from the date of allotment

Fund Manager Mr. Viraj KulkarniMr. Harshal Joshi

Benchmark Russell 1000 Growth Index^

NFO opens on 29th Jul’21NFO closed on 12th Aug’21

Minimum Application amount during New Fund Offer period:Rs.5,000/- and in multiples of Re. 1/- thereafter

38

In Summary, 5 key reasons to choose the IDFC US Equity Fund of Fund

#The IDFC US Equity Fund of Fund is open to invest in funds that meet the investment objective and strategy.

An actively managed

underlying Fund with

a well-tested,

fundamental,

bottom-up stock

selection process

1. Investment Approach 2. Portfolio

The Underlying Fund is Growth-oriented,

positioned to benefit from reopening of the economy while

majorly being invested in long term

secular trends

3. Reducedconcentration

Broad exposure to US equity markets without a sector/ market-cap bias, with currently a

lower exposure to top 10 index constituents

4. Expertise

Seasoned, proven fund management

team of the Underlying Fund

with deep US expertise#

5. Ease of Investment

Hassle-freeinvestment process

into US market; subscribe and

redeem like a regular Indian mutual fund

39

The IDFC US Equity Fund of Fund can invest only in similar mutual fund/s or exchange traded fund/s with similar investment strategy, similar investment objective, similar asset allocation, similar benchmark.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated asendorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared onthe basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only andmay have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information providedabove may not contain all the material aspects relevant for making an investment decision and the stocks may or may not continue to form part of the scheme’s portfolio in future. The decision of the InvestmentManager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipatedtrends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFCMutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special orconsequential including lost revenue or lost profits that may arise from or in connection with the use of the information.

This product is suitable for investors who are seeking*:To create wealth over long termDiversification of returns through investing in a fund mainly investing in units/shares of overseas Mutual Fund Scheme (/s) / Exchange Traded Fund (/s) which invests in US Equity securities

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Important Disclosure

40

The identity of the issuer of the Promotion Material and the investment product which is the subject of the Promotion Material and the content of the Promotion Material has been verified by the issuer thereof;The Promotion Material is not issued by J.P. Morgan Asset Management (Singapore) Limited (JPMAMSL), any of its Affiliates or a JPMorgan Fund and the Promotion Material does not relate to a direct investmentin any JPMorgan Fund; neither JPMAMSL, any of its Affiliates or a JPMorgan Fund has reviewed the contents of the Promotion Material and accordingly takes no responsibility for the accuracy of the contents ofthe Promotion Material or any liability for any statement or misstatement in the Promotion Material; and an investor would be investing into an investment product which is established, offered and sold by theCompany or its Affiliates and would not be investing in any JPMorgan Fund, and accordingly there is no contractual relationship between the Investor and JPMAMSL, any of its Affiliates or a JPMorgan Fund.Investors will bear the recurring expenses of the Scheme in addition to the expenses of the underlying schemes in which investments are made by the Scheme. IDFC US Equity Fund of Fund is not a dedicatedFeeder fund and investment in underlying fund will be undertaken subject to fulfilment of documentation and regulatory requirements applicable for investing in the underlying fund. The FoF performance issubject to the movements of the underlying fund. IDFC AMC does not have an active role in managing the underlying fund.

Thank You

IDFC Asset Management CompanyOne World Centre, 6th Floor, 841 Jupiter Mills Compound,

Elphinstone Road (West), Mumbai 400013,Maharashtra, India

www.idfcamc.comwww.idfcmf.com

www.idfc.com

Minimum Subscription / Redemption amountsDuring New Fund Offer: Rs.5,000/- and in multiples of Re. 1/- thereafterDuring Ongoing Offer:Subscription: Fresh Purchase (including switch-in) - Rs.5,000/- and in multiples of Re. 1/- thereafterAdditional Purchase (including switch-in) - Rs.1,000/- and any amount thereafterRedemption: Rs.1,000/- or the account balance of the investor, whichever is less.SIP: Rs.1,000/- and in multiples of Rs.1 thereafterSTP (being Target Scheme): Rs.1,000/- and any amount thereafter (for Fixed amount option) / Rs.500/- and any amount thereafter (for capital appreciation option)SWP: Rs. 200 and any amount thereafter

InstrumentsIndicative Allocation (as % of total assets) Risk Profile

Units/Shares of overseas Mutual Fund Scheme (/s) / Exchange Traded Fund (/s) investing in US Equity securities

95% - 100% Very High

Debt Securities, Money Market Instruments, and/or units of Debt and Liquid schemes

0% - 5% Low to Medium

Annexure: Other details of IDFC US Equity Fund of Fund

*plus applicable surcharge and Health & Education cess

Resident Investor Mutual Fund

Dividend*

Tax on Dividend As per respective slab rate or corporate tax rate applicable to the investor

Nil

Capital Gains*

Long Term (holding period more than 36 months) 20% with indexation Nil

Short Term (holding period up to 36 months) applicable to the investor

As per respective slab rate or corporate tax rate Nil

Taxation