ifrs 9 financial instruments - hvg...

TRANSCRIPT

IFRS 9 Financial instruments:Impairment

In July 2014, the International Accounting Standards Board (IASB) issued the final version of IFRS 9 Financial Instruments (IFRS 9, or the Standard), bringing together the classification and measurement, impairment and hedge accounting phases of the IASB’s project to replace IAS 39 Financial Instruments: Recognition and Measurement and all previous versions of IFRS 9. The expected impairment requirements must be adopted with the other IFRS 9 requirements from 1 January 2018, with early application permitted, subject to EU approval.

CredentialsWe have developed a comprehensivelandscape of services in the field offinancial asset impairment covering bothmethodological as well as quantitativeaspects.

Our client base is located across:

• CSE

• Austria

• Russia

• CIS countries

Our strengths include our absolute focuson yourneeds, deep subject matter expertiseand our quick and targeted response tochallenges relevant to hedge accounting.

The introduction of our services is justthe beginning of what we strive for – along-lasting relationship with continuedsupport and significant added value foryou – our client. al simplifications will be allowed) .

• Measurement of expected credit losses will involve calculation of a probability weighted outcome, correct settingof the time value of money and use of reasonable and supportable information.

• A general and simplified model will be available for several types of financial instruments.

• New extensive disclosures will be required to improve comparability of information provided by different entities.These disclosures will be very demanding on data necessary to comply with all requirements.

• New extensive back-testing will be mandated which will require a new flexible calculation environment.

What you need to know about IFRS 9 in relation to impairment

• The new impairment requirements in IFRS 9 are based on an expected credit loss model and replace the IAS 39incurred loss model.

• The expected credit loss model applies to debt instruments recorded at amortized cost or at fair value throughother comprehensive income, lease receivables and most loan commitments and financial guarantee contracts.

• Entities are required to recognize either 12-month or lifetime expected credit losses, depending on whetherthere has been a significant increase in credit risk since initial recognition.

• The measurement of expected credit losses should reflect a probability-weighted outcome, the time valueof money and reasonable and supportable information that is available without undue cost or effort.

Application challenges

A successful transition towards IFRS 9 requires an early start and an analysis of the implications of the new standard.The new impairment requirements give rise to a number of implementation challenges:

• New models will need to be developed to incorporate the forward looking concept that is the basis of the standard.More judgement will need to be exercised by management.

• Entities will need to accurately capture the occurrence of significant deterioration in credit risk ( severaloperation

EY | Assurance | Tax | Transactions | Advisory

Why EY Over the last five years the EY Financial Services Advisory practice has grown rapidly in response to market developments and the needs of our clients. In Central Europe, we now have over 20 partners leading a team of over 300 people, working closely with global EY hubs for financial services. All our people focus on the financial sector and therefore they have a deep understanding of the challenges you face.

We have arguably the deepest and largest dedicated advisory practice in the financial services market globally. We were rated the EMEA market leader in consulting by revenue and market share in the financial services sectors of banking, securities and insurance by Gartner in 2014.

Our clients rightly expect us to bring genuine insight and ideas on how to respond to the key issues impacting them. They need practical, grounded experience on how to implement and sustain change in an increasingly complex, interconnected environment. As a single, integrated practice, we are able to draw on an unrivalled depth and range of industry, technical and consulting expertise to support your needs.

That’s how EY makes a difference.

Contacts

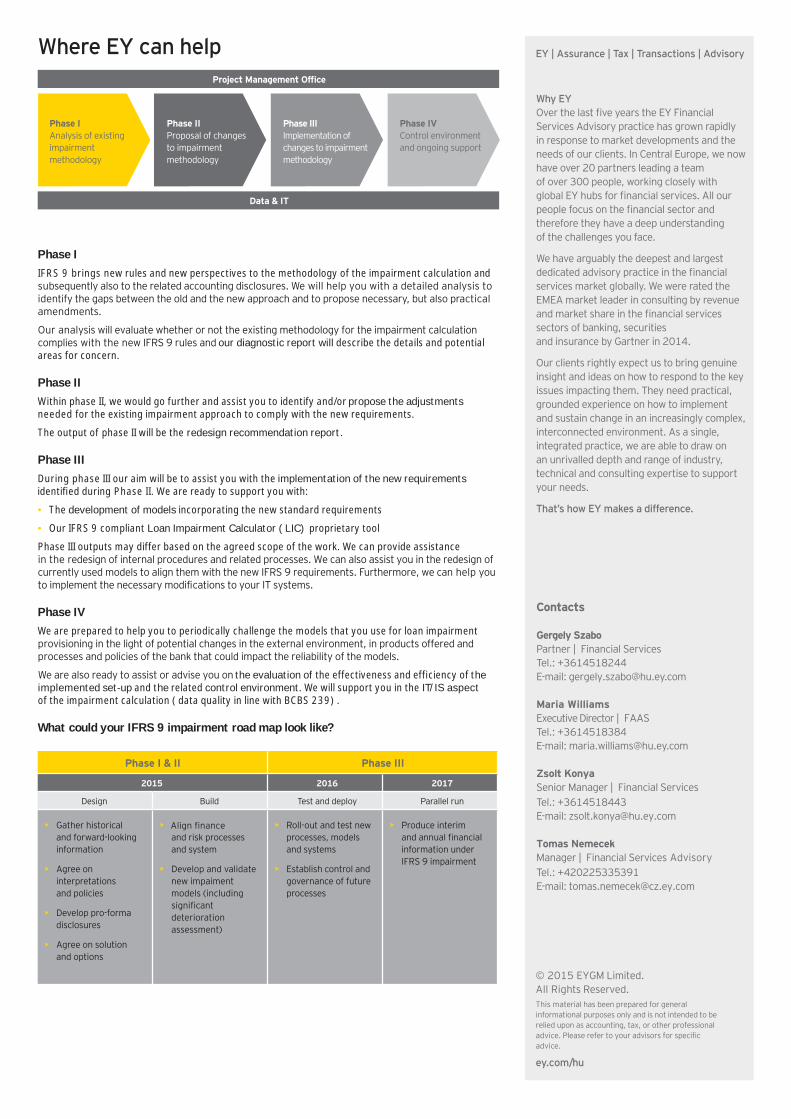

Phase IAnalysis of existing impairment methodology

Phase IVControl environment and ongoing support

Phase IIProposal of changes to impairment methodology

Phase IIIImplementation of changes to impairment methodology

Data & IT

Phase I & II Phase III

2015 2016 2017

Design Build Test and deploy Parallel run

• Gather historical and forward-looking information

• Agree on interpretations and policies

• Develop pro-forma disclosures

• Agree on solution and options

• and risk processes and system

• Develop and validate new impaiment models (including

deterioration assessment)

• Roll-out and test new processes, models and systems

• Establish control and governance of future processes

• Produce interim

information under IFRS 9 impairment

Where EY can help

© 2015 EYGM Limited.All Rights Reserved.This material has been prepared for generalinformational purposes only and is not intended to berelied upon as accounting, tax, or other professionaladvice. Please refer to your advisors for specificadvice.

ey.com/hu

Gergely SzaboPartner | Financial ServicesTel.: +3614518244E-mail: [email protected]

Maria WilliamsExecutive Director | FAASTel.: +3614518384E-mail: [email protected]

Zsolt KonyaSenior Manager | Financial ServicesTel.: +3614518443E-mail: [email protected]

Tomas NemecekManager | Financial Services AdvisoryTel.: +420225335391E-mail: [email protected]

Align finance

Phase IIFRS 9 brings new rules and new perspectives to the methodology of the impairment calculation andsubsequently also to the related accounting disclosures. We will help you with a detailed analysis toidentify the gaps between the old and the new approach and to propose necessary, but also practicalamendments.

Our analysis will evaluate whether or not the existing methodology for the impairment calculationcomplies with the new IFRS 9 rules and our diagnostic report will describe the details and potentialareas for concern.

Phase IIWithin phase II, we would go further and assist you to identify and/or propose the adjustmentsneeded for the existing impairment approach to comply with the new requirements.

The output of phase II will be the redesign recommendation report.

Phase IIIDuring phase III our aim will be to assist you with the implementation of the new requirements identified during Phase II. We are ready to support you with:

• The development of models incorporating the new standard requirements

• Our IFRS 9 compliant Loan Impairment Calculator ( LIC) proprietary tool

Phase III outputs may differ based on the agreed scope of the work. We can provide assistancein the redesign of internal procedures and related processes. We can also assist you in the redesign ofcurrently used models to align them with the new IFRS 9 requirements. Furthermore, we can help youto implement the necessary modifications to your IT systems.

Phase IVWe are prepared to help you to periodically challenge the models that you use for loan impairmentprovisioning in the light of potential changes in the external environment, in products offered andprocesses and policies of the bank that could impact the reliability of the models.

We are also ready to assist or advise you on the evaluation of the effectiveness and efficiency of theimplemented set-up and the related control environment. We will support you in the IT/IS aspectof the impairment calculation ( data quality in line with BCBS 239) .

What could your IFRS 9 impairment road map look like?