ignoring esg is a breach of fiduciary duty, legally and ... · ignoring esg is a breach of...

TRANSCRIPT

Ignoring ESG is a breach of fiduciary duty, legally and

ethically Discussion by Carlos Joly

Chair, Natixis AM Climate Change Scientific Advisory Committee

At RI Seminar 11.11.2009, Amsterdam

Four years ago

The AMWG’s question to Freshfields Bruckhaus Deringer:

‘Is the integration of ESG issues into investment policy – including asset allocation, portfolio construction and stock-picking or bond-picking – voluntarily permitted, legally required or hampered by law and regulation; primarily as regards public and private pension funds, secondarily as regards insurance company reserves and mutual funds?’

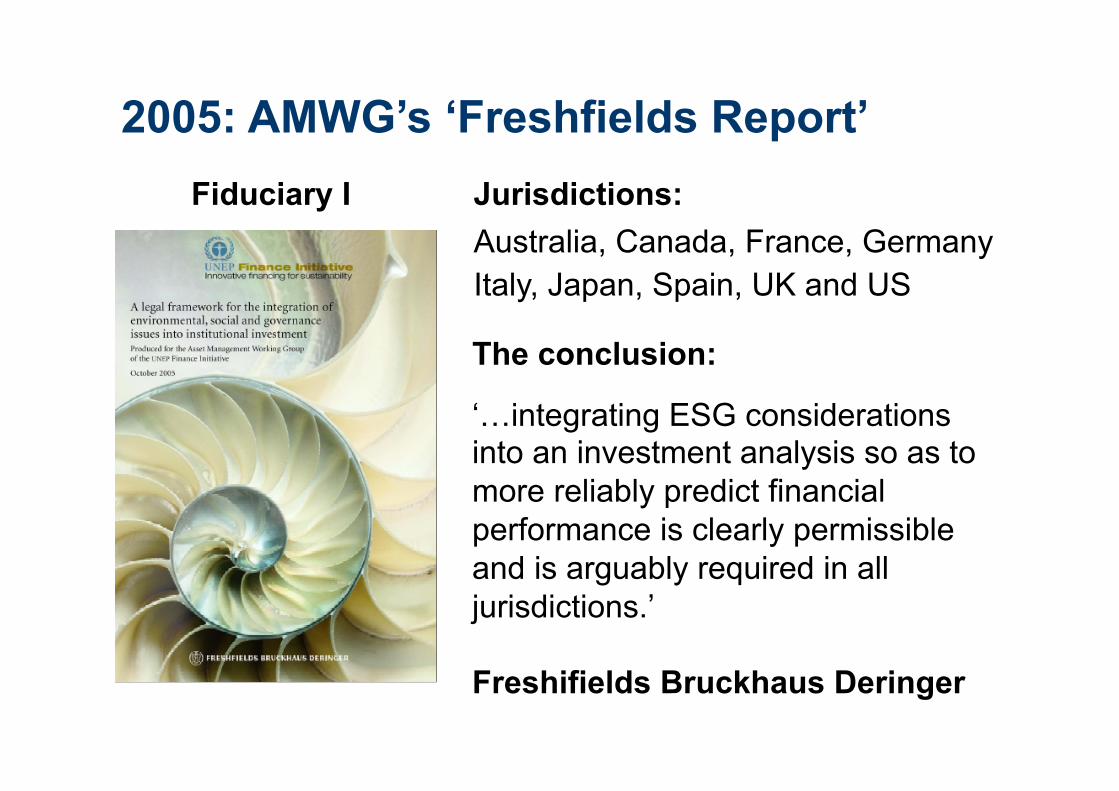

2005: AMWG’s ‘Freshfields Report’ Fiduciary I Jurisdictions: Australia, Canada, France, Germany

Italy, Japan, Spain, UK and US

The conclusion:

‘…integrating ESG considerations into an investment analysis so as to more reliably predict financial performance is clearly permissible and is arguably required in all jurisdictions.’

Freshifields Bruckhaus Deringer

AMWG’s ‘Fiduciary II’ report Fiduciary II Purpose: Legal roadmap to operationalise

fiduciaries’ commitment to integrate ESG raison d'être of the PRI

Takes off from where the Freshfields Report left and brings ESG to the point of contract : 1. Sample legal language for

investment management contracts

2. Practical recommendations on implementation

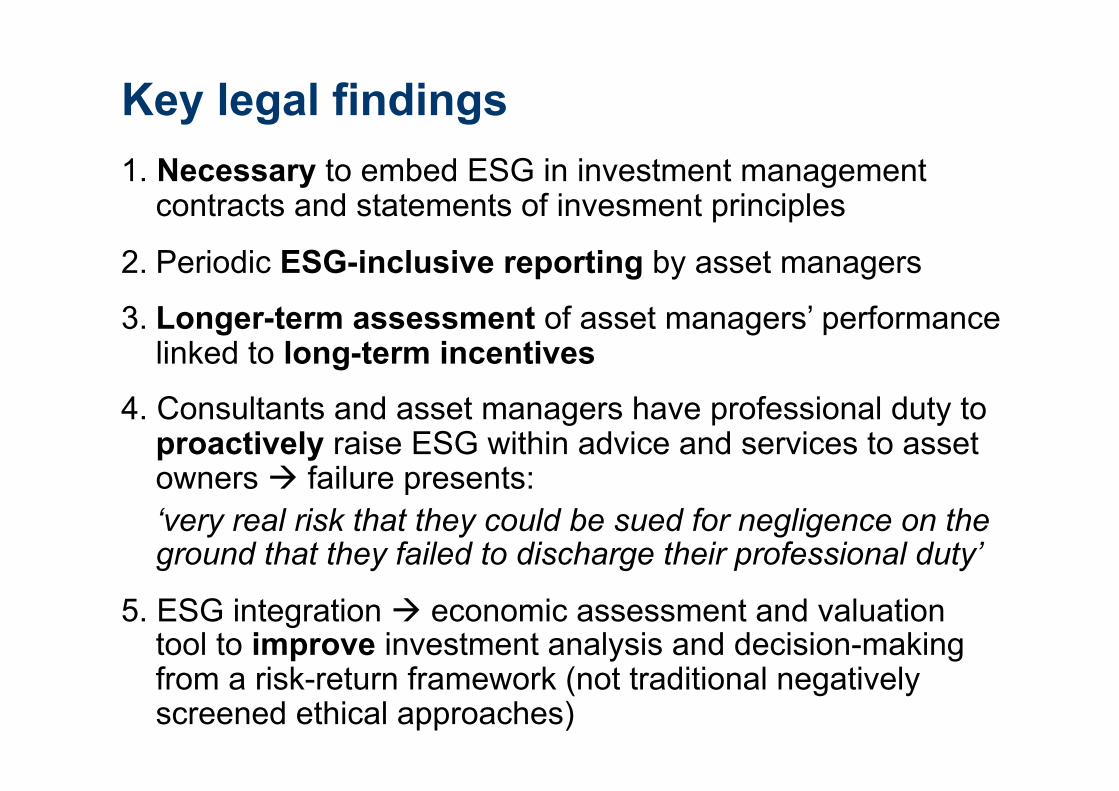

Key legal findings 1. Necessary to embed ESG in investment management

contracts and statements of invesment principles

2. Periodic ESG-inclusive reporting by asset managers

3. Longer-term assessment of asset managers’ performance linked to long-term incentives

4. Consultants and asset managers have professional duty to proactively raise ESG within advice and services to asset owners failure presents: ‘very real risk that they could be sued for negligence on the ground that they failed to discharge their professional duty’

5. ESG integration economic assessment and valuation tool to improve investment analysis and decision-making from a risk-return framework (not traditional negatively screened ethical approaches)

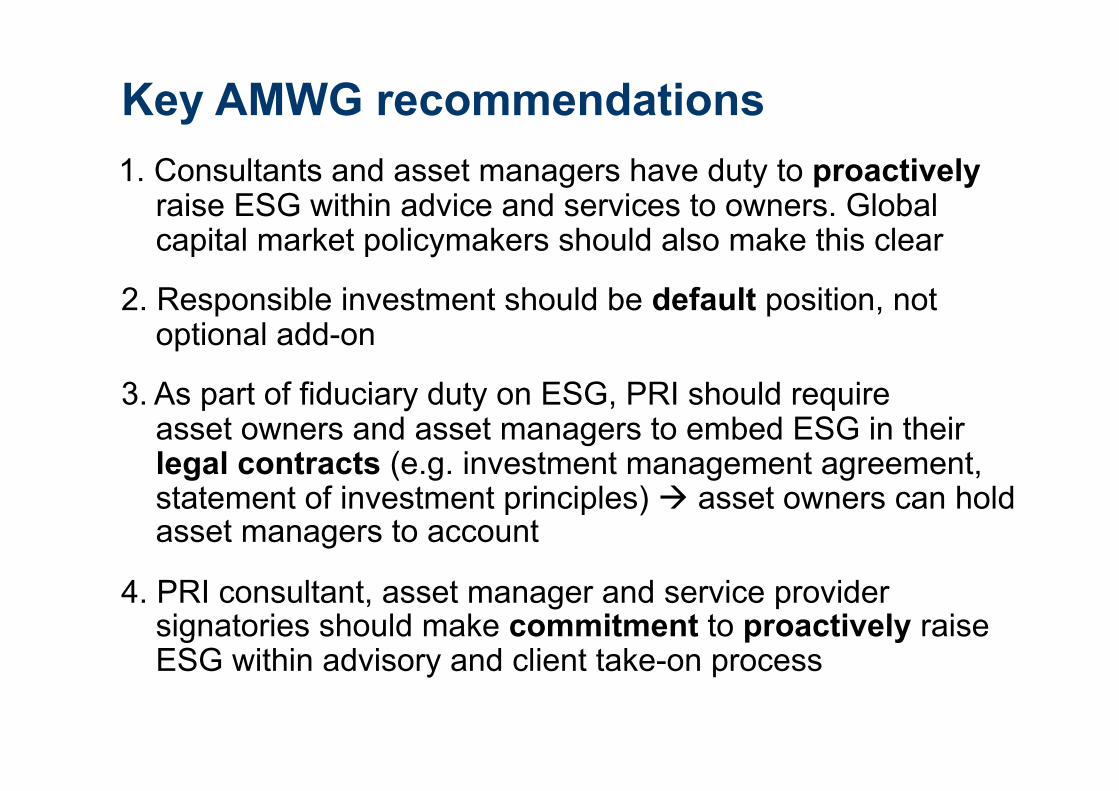

Key AMWG recommendations

1. Consultants and asset managers have duty to proactively raise ESG within advice and services to owners. Global capital market policymakers should also make this clear

2. Responsible investment should be default position, not optional add-on

3. As part of fiduciary duty on ESG, PRI should require asset owners and asset managers to embed ESG in their legal contracts (e.g. investment management agreement, statement of investment principles) asset owners can hold asset managers to account

4. PRI consultant, asset manager and service provider signatories should make commitment to proactively raise ESG within advisory and client take-on process

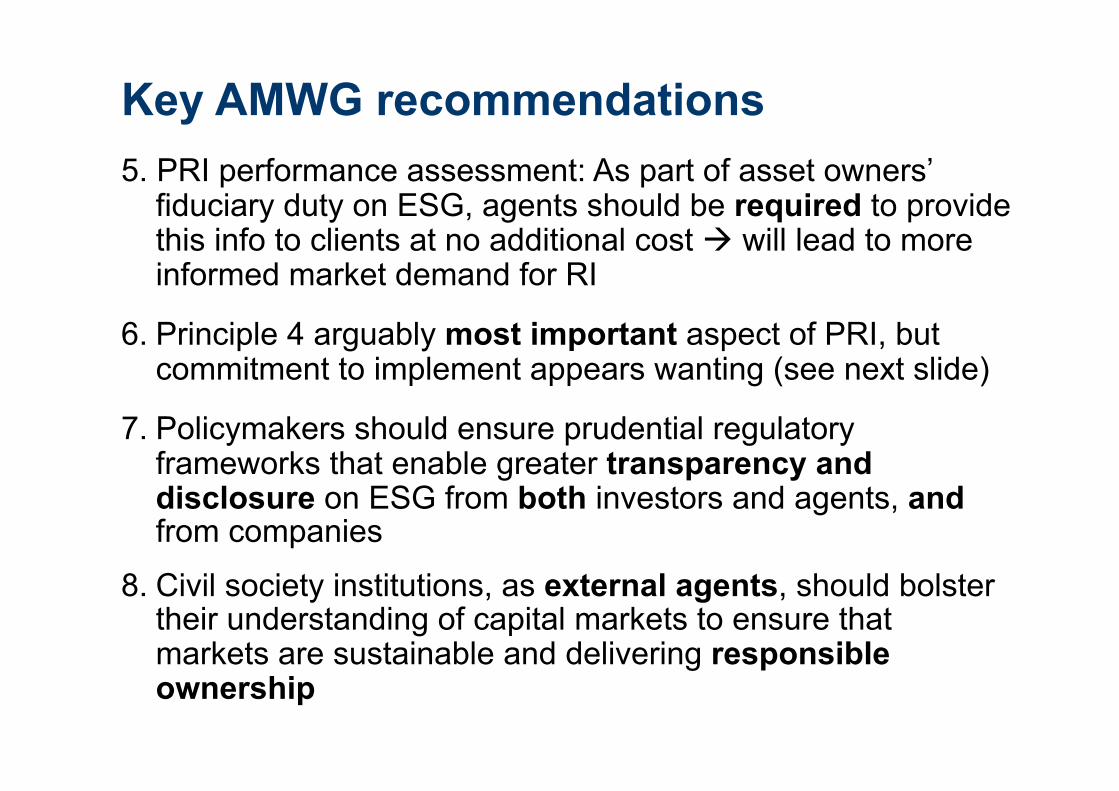

Key AMWG recommendations

5. PRI performance assessment: As part of asset owners’ fiduciary duty on ESG, agents should be required to provide this info to clients at no additional cost will lead to more informed market demand for RI

6. Principle 4 arguably most important aspect of PRI, but commitment to implement appears wanting (see next slide)

7. Policymakers should ensure prudential regulatory frameworks that enable greater transparency and disclosure on ESG from both investors and agents, and from companies

8. Civil society institutions, as external agents, should bolster their understanding of capital markets to ensure that markets are sustainable and delivering responsible ownership

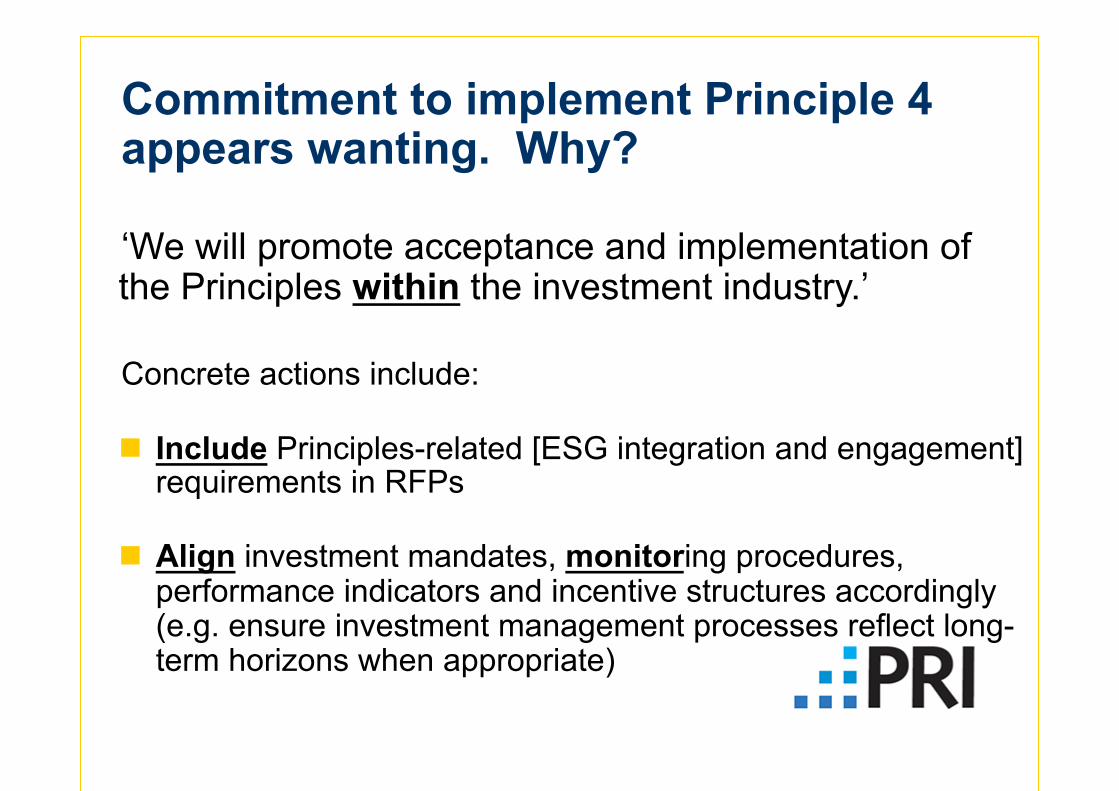

Commitment to implement Principle 4 appears wanting. Why?

‘We will promote acceptance and implementation of the Principles within the investment industry.’

Concrete actions include:

Include Principles-related [ESG integration and engagement] requirements in RFPs

Align investment mandates, monitoring procedures, performance indicators and incentive structures accordingly (e.g. ensure investment management processes reflect long- term horizons when appropriate)

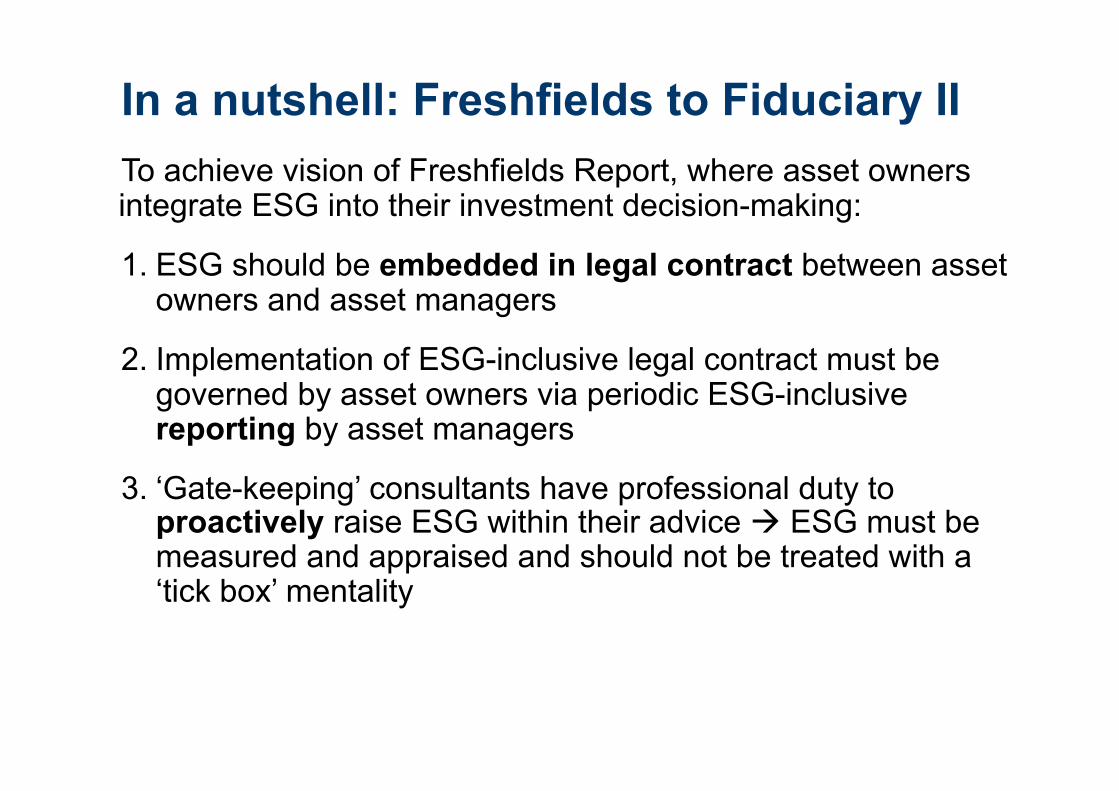

In a nutshell: Freshfields to Fiduciary II To achieve vision of Freshfields Report, where asset owners integrate ESG into their investment decision-making:

1. ESG should be embedded in legal contract between asset owners and asset managers

2. Implementation of ESG-inclusive legal contract must be governed by asset owners via periodic ESG-inclusive reporting by asset managers

3. ‘Gate-keeping’ consultants have professional duty to proactively raise ESG within their advice ESG must be measured and appraised and should not be treated with a ‘tick box’ mentality

Do we need Fiduciary III?

• Carlos Joly´s view: Fiduciary I and II reports do not go far enough: “Materiality” is not a strong enough justification, not a solid enough basis for justifying ESG as a necessary part of Fiduciary Duty

Fiduciary Duty and Materiality

• Is materiality necessary for ESG? – What does “materiality” really mean? It is a confused notion.

Timescale: short term or long term price expectation? Or is it past price performance?

– In practice, serves to justify lemming behavior and index relative portfolio strategies. This prevents forward-looking RI.

– Climate change not now generally in the price of equities, so is it “material” today? Can an investor opt not to consider CC?

– Can never know for sure beforehand what proves to be material, therefore “profit maximization” criterion is in any event aspirational.

– Market misprices opportunity and risk. Contradiction between index relative TE constraints and forward-looking RI.

Fiduciary Duty and Materiality

• Is materiality sufficient? – Many cases in which non financial interests of principals come

ahead of financial interests: eg tobacco exclusions, weapons exclusions, human rights violations. Test is implied consent, “overlapping consensus of values”. Therefore, ethics trumps “profit maximization”. See ethical guidelines of NGPF, FRR, Natixis Impact– Climate Change fund.

Non financial values must trump “materiality” since the former are a given

and the later is uncertain • ESG integration is a necessary aspect of and

fiduciary duty and a tool for aligning investments with the values of principals, provided no overriding reason to expect significant sacrifice to returns in medium to long term relative to goals established in the mandate.

• (Note: this is Joly´s formulation, not necessarily that of UN PRI or UNEP FI, but I believe it is implied by what we mean by RI)