ihh investor presentation may 2014 - bursa malaysia · 10.9% stake in apollo hospitals ... growing...

TRANSCRIPT

IHH Investor Presentation

May 2014

General Overview

Quick Facts

2

World’s second-largest private healthcare provider by market cap

• IHH Healthcare Berhad (IHH) is a leading international provider of healthcare

services

• Listed concurrently on 25 Jul 2012 on Bursa Malaysia (“5225”) and Singapore

Exchange (“QOF”)

• Market capitalization of over RM30bil (US$10bil) as at 30th May 2014

• Strong track record and experienced management team

• Backed by two reputable major shareholders

� Khazanah – 45%

� Mitsui – 20%

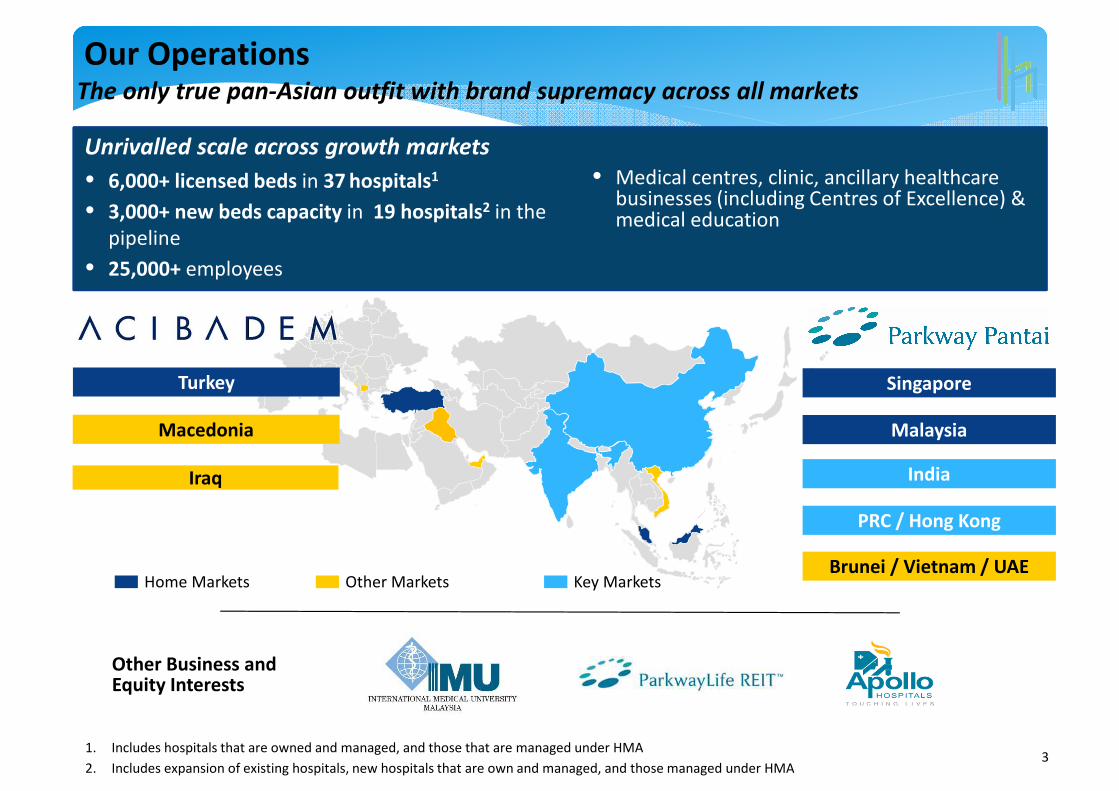

Our Operations

• 6,000+ licensed beds in 37 hospitals1

• 3,000+ new beds capacity in 19 hospitals2 in the

pipeline

• 25,000+ employees

• Medical centres, clinic, ancillary healthcare businesses (including Centres of Excellence) & medical education

Key MarketsHome Markets Other Markets

Turkey

Macedonia

Singapore

Malaysia

India

PRC / Hong Kong

Brunei / Vietnam / UAE

Other Business andEquity Interests

3

The only true pan-Asian outfit with brand supremacy across all markets

Unrivalled scale across growth markets

1. Includes hospitals that are owned and managed, and those that are managed under HMA

2. Includes expansion of existing hospitals, new hospitals that are own and managed, and those managed under HMA

Iraq

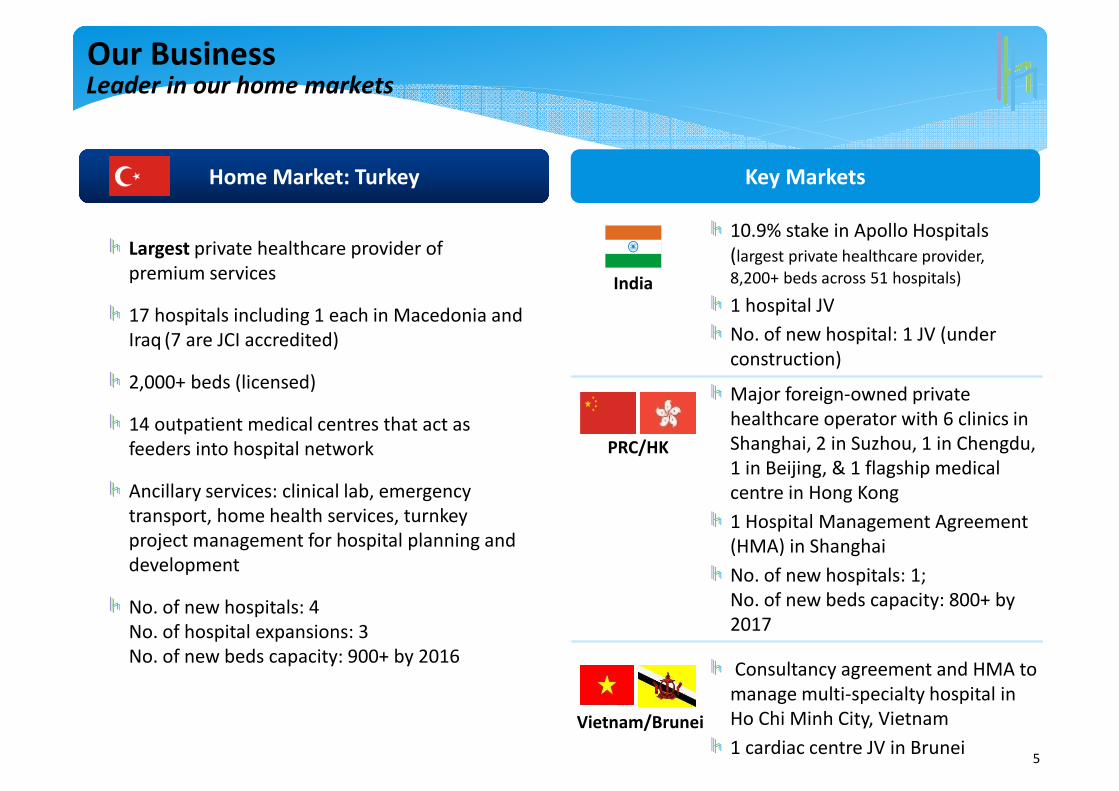

Home Market: MalaysiaHome Market: Singapore

Our BusinessLeader in our home markets

Largest private healthcare provider

Owns and operates 4 hospitals (all are JCI

accredited)

Hospital brands: Mount Elizabeth, Gleneagles

and Parkway East

44% market share

900+ beds (licensed)

Operates Parkway Shenton clinics, Medi-Rad

Associates clinics, Parkway Labs

Runs Parkway College comprising 3 schools

(Nursing, Allied Healthcare and Healthcare

Management)

2nd largest private healthcare provider

Owns and operates 12 hospitals (2 are JCI

accredited ; 9 accredited by MSQH)

Hospital brands: Pantai and Gleneagles

2 more hospitals under development

15% market share

2000+ beds (licensed)

Operates Pantai Premier Pathology, Pantai

Integrated Rehab and one ambulatory care

centre

Runs IMU (Malaysia’s leading private

healthcare university) and Pantai College

(trains nurses and allied health professionals)

No. of new hospitals: 2;

No. of hospital expansions: 3

No. of new beds capacity: 700+ by 20164

Key Markets

Our BusinessLeader in our home markets

10.9% stake in Apollo Hospitals

(largest private healthcare provider,

8,200+ beds across 51 hospitals)

1 hospital JV

No. of new hospital: 1 JV (under

construction)

Major foreign-owned private

healthcare operator with 6 clinics in

Shanghai, 2 in Suzhou, 1 in Chengdu,

1 in Beijing, & 1 flagship medical

centre in Hong Kong

1 Hospital Management Agreement

(HMA) in Shanghai

No. of new hospitals: 1;

No. of new beds capacity: 800+ by

2017

Consultancy agreement and HMA to

manage multi-specialty hospital in

Ho Chi Minh City, Vietnam

1 cardiac centre JV in Brunei

Largest private healthcare provider of

premium services

17 hospitals including 1 each in Macedonia and

Iraq (7 are JCI accredited)

2,000+ beds (licensed)

14 outpatient medical centres that act as

feeders into hospital network

Ancillary services: clinical lab, emergency

transport, home health services, turnkey

project management for hospital planning and

development

No. of new hospitals: 4

No. of hospital expansions: 3

No. of new beds capacity: 900+ by 2016

Home Market: Turkey

India

5

PRC/HK

Vietnam/Brunei

Our full service offeringAn integrated, comprehensive suite of services

Primary

Tertiary and

Secondary

Quaternary

Centres of Excellence and Clinical Programmes

Complementary ancillary services

Parkway Shenton

(c.60 clinics)

12 hospitals

• Cancer Centre / Institute

• Cardiac Centre / Programme

• Haematology and Stem Cell

Transplant Centre

• Eye Centre

• Women’s and Children

Centre

• Neuroscience Centre

• Orthopaedic Centre

• Transplant Programme

4 hospitals 17 hospitals

(including 1 each in

Macedonia & Iraq)

Twin Towers

Medical Clinic

14 medical

centres

6

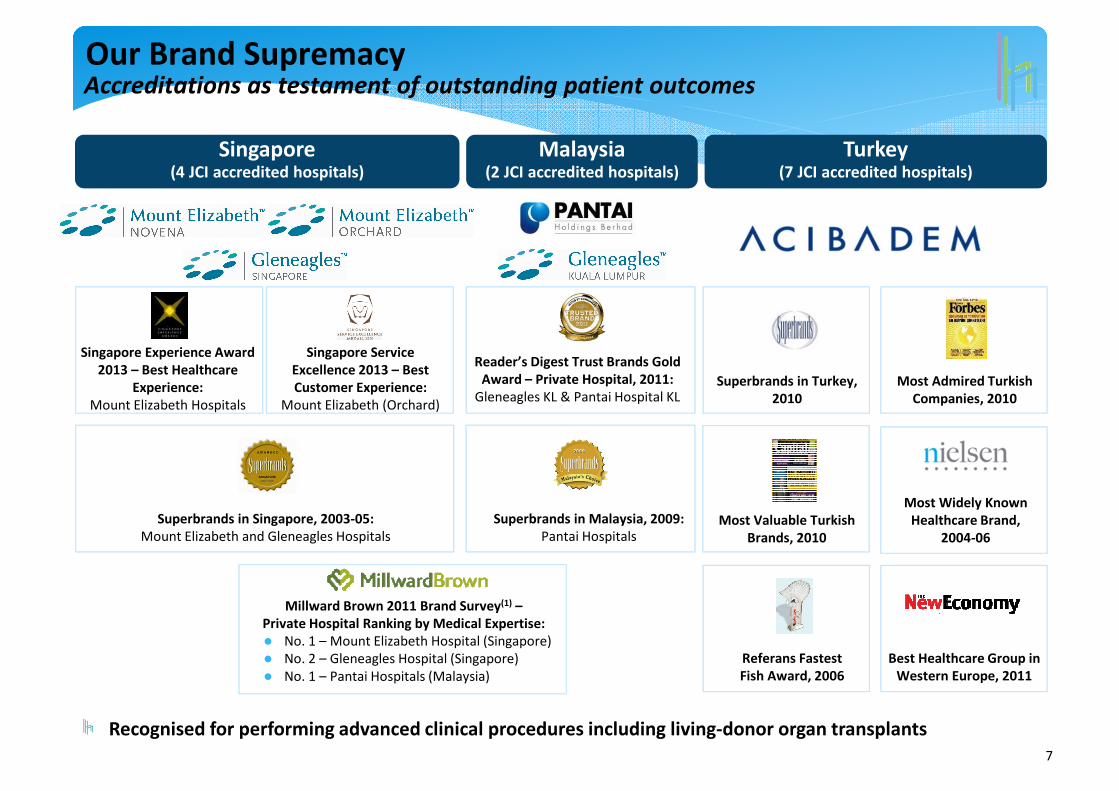

Singapore (4 JCI accredited hospitals)

Malaysia (2 JCI accredited hospitals)

Turkey (7 JCI accredited hospitals)

Our Brand Supremacy

Reader’s Digest Trust Brands Gold

Award – Private Hospital, 2011:

Gleneagles KL & Pantai Hospital KL

Millward Brown 2011 Brand Survey(1) –

Private Hospital Ranking by Medical Expertise:

� No. 1 – Mount Elizabeth Hospital (Singapore)

� No. 2 – Gleneagles Hospital (Singapore)

� No. 1 – Pantai Hospitals (Malaysia)

Superbrands in Singapore, 2003-05:

Mount Elizabeth and Gleneagles Hospitals

Superbrands in Malaysia, 2009:

Pantai Hospitals

Superbrands in Turkey,

2010

Most Admired Turkish

Companies, 2010

Most Valuable Turkish

Brands, 2010

Most Widely Known

Healthcare Brand,

2004-06

Best Healthcare Group in

Western Europe, 2011

Referans Fastest

Fish Award, 2006

Accreditations as testament of outstanding patient outcomes

Recognised for performing advanced clinical procedures including living-donor organ transplants

7

Singapore Experience Award

2013 – Best Healthcare

Experience:

Mount Elizabeth Hospitals

Singapore Service

Excellence 2013 – Best

Customer Experience:

Mount Elizabeth (Orchard)

9 Awards in 2012 Component of 6 Major Equity Indices

Our Brand SupremacyGrowing recognition for corporate strength & excellence

Best IPO

Best Malaysia Deal

Most Transparent Company 2012 - New Issue

Best Equity Deal/Best IPO (Asia)

Best Deal (Malaysia)

Best IPO 2012

Malaysia Capital Markets Deal of the Year

Best Dual-Listed IPO of the Year (2012)

Best Equity Deal of the Year (2012)

FTSE Bursa Malaysia KLCITop 30 companies on Bursa’s Main Market

FTSE Straits Times IndexTop 30 companies on Singapore Exchange’s Mainboard

FTSE All-World Index (Large Cap)

FTSE All-Emerging Index

FTSE Global Style Index

MSCI Global Standard Indices (Large Cap)

8

Expand Further

in Asia and

CEEMENA

2

Strengthen

Leadership in

Home Markets

1

Our Roadmap ahead

Realise Synergies

to Enhance

ProfitabilityContinue to

Capture Growth in Medical

Travel

We aim to strengthen and expand our leading market positions, continuously improve the

quality of our healthcare services and deliver long-term value for our shareholders

3

4

9

Clear growth strategy

1Q FY2014 Financial Updates

Inpatient volumes and revenue intensity grew strongly against last year

11

Inpatient Admission Volumes1 (Number)

Average Revenue per Inpatient Admission1 (RM)

1. Based on Singapore, Malaysia and Acibadem Holdings hospitals only. International hospitals not included.

2. Specialist fees not included in Singapore and Malaysia but included in Acibadem Holdings’ average revenue per inpatient admission

3. Based on a uniform exchange rate throughout the periods shown (SGD: 2.6031; TL: 1.4928)

Q1 YoY Growth 6.4% Q1 YoY Growth 9.3% Q1 YoY Growth 5.9%

Q1 YoY Growth 7.6% Q1 YoY Growth 8.5% Q1 YoY Growth 8.2%

12

Project Progress – Malaysia

Type Hospital Description Target Completion

Expansion

Project

Pantai Hospital

Kuala Lumpur

Phase 1: 200 consultant suites,

8 COEs

Phase 2: 120 beds capacity

• Planning stage:

Phase 1: End 2014

Phase 2: Planning stage

Expansion

Project

Pantai Hospital

Klang80 beds capacity

• Planning stage

• Target Completion: Early 2016

Expansion

Project

Gleneagles Kuala

Lumpur100 beds capacity

• Under construction

• Target Completion: End 2014

Greenfield

Project

Pantai Hospital

Manjung100 beds capacity • Opened on 19 May 2014

Greenfield

Project

Gleneagles Kota

Kinabalu250 beds capacity

• Under construction

• Target Completion: Early 2015

Greenfield

ProjectGleneagles Medini Phase 1a: 150 bed capacity

• Under construction

• Target Completion of Phase 1a: Early 2015

13

Type Hospital Description Target Completion

Consultancy

Agreement, HMA

China

Shanghai International

Medical Centre

450 bed capacity• Construction completed

• Hospital opening in phases

Consultancy Agreement, HMA

Abu Dhabi, UAEDanat Al Emarat Hospital

126 bed capacity• Under construction

• Target Completion: End 2014

50-50% JV

Greenfield Project

India

Gleneagles Khubchandani,

Mumbai

450 bed capacity• Under Construction

• Target Completion: End 2014

60-40% JV

Greenfield Project

Hong Kong

Gleneagles Hong Kong

Hospital

500 bed capacity• Design & Tender Documentation stage.

• Target Completion: End 2016

Project Progress – International

14

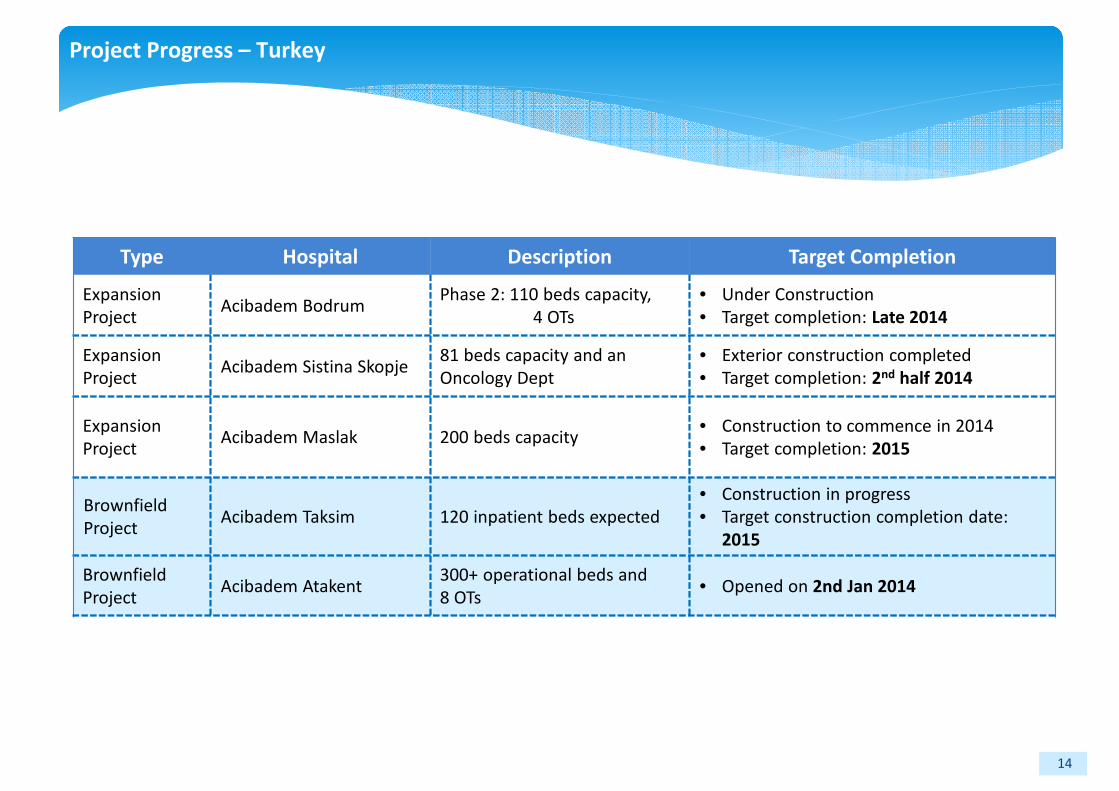

Type Hospital Description Target Completion

Expansion

ProjectAcibadem Bodrum

Phase 2: 110 beds capacity,

4 OTs

• Under Construction

• Target completion: Late 2014

Expansion

ProjectAcibadem Sistina Skopje

81 beds capacity and an

Oncology Dept

• Exterior construction completed

• Target completion: 2nd half 2014

Expansion

ProjectAcibadem Maslak 200 beds capacity

• Construction to commence in 2014

• Target completion: 2015

Brownfield

ProjectAcibadem Taksim 120 inpatient beds expected

• Construction in progress

• Target construction completion date:

2015

Brownfield

ProjectAcibadem Atakent

300+ operational beds and

8 OTs• Opened on 2nd Jan 2014

Project Progress – Turkey

15

Type Hospital Description Target Completion

Greenfield

ProjectAcibadem Altunizade

Located in Istanbul

Expected: 250+ bed capacity

• Construction to commence in 2014

• Target Completion: 2015

Greenfield

ProjectAcibadem Kartal Located in Istanbul

Expected: 120 bed capacity• Project under evaluation and

related discussions are ongoing

Greenfield

ProjectAcibadem Atasehir

Located in IstanbulExpected: 180 bed capacity

• Project under evaluation and related discussions are ongoing

Project Progress – Malaysia

Revenue & EBITDA grew +8% and 11% respectively vs Q1 last yearPATMI (Excl EI) +35% vs Q1 last year

∗ Robust performance driven by volume and revenue intensity

∗ Mount Elizabeth Novena Hospital, Acibadem Ankara Hospital and Acibadem Bodrum Hospital continues toramp up their operations since their opening in FY2012 compared to significant startup costs incurred in Q12013

∗ Acibadem Atakent Hospital was opened on 2 January 2014

∗ Operating leverage reaped from higher patient volumes as well as from the Group’s expanding operations

∗ PATMI (Excl EI) growth driven by:- Double-digit EBITDA growth

Offset by:- incremental depreciation and finance cost relating to new hospitals which had to be recognised in the

P&L after completion

∗ Benefits of diversification with strong Singapore Dollar offsetting weak Turkish Lira on translation ofsubsidiary group’s income statements* and balance sheets- Group Revenue and EBITDA growth eroded by the weak Turkish Lira- However, effect on PATMI minimal- Net foreign currency translation gains recognised in the Group’s other comprehensive income - boosted

by the strong Singapore Dollar when translating the balance sheets of the Group’s Singapore operations

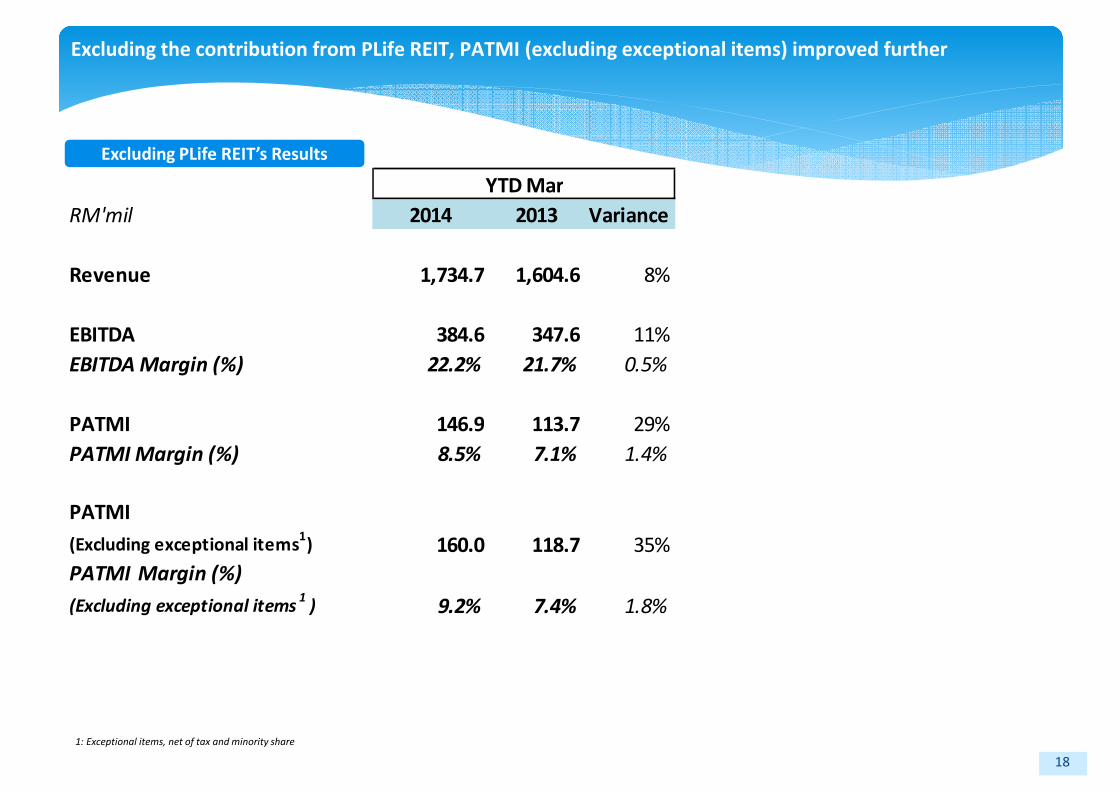

Key Group Highlights (Excluding PLife REIT’s results)

16

*: Key average exchange rates used to translate the YTD results of significant overseas subsidiaries into RM:

31 Mar 2014 31 Mar 2013

1 Singapore Dollar 2.5994 2.4961

1 Turkish Lira 1.4897 1.7220

IHH Group achieved double-digit EBITDA and PATMI (excluding exceptional items) growth over last year

17

1: Exceptional items, net of tax and minority share

RM'mil 2014 2013 Variance

Revenue 1,757.6 1,624.6 8%

EBITDA 436.5 394.2 11%

EBITDA Margin (%) 24.8% 24.3% 0.6%

PATMI 159.1 127.3 25%

PATMI Margin (%) 9.0% 7.8% 1.2%

PATMI

(Excluding exceptional items1) 172.1 132.2 30%

PATMI Margin (%)

(Excluding exceptional items1

) 9.8% 8.1% 1.7%

YTD Mar

Total Group Results

RM'mil 2014 2013 Variance

Revenue 1,734.7 1,604.6 8%

EBITDA 384.6 347.6 11%

EBITDA Margin (%) 22.2% 21.7% 0.5%

PATMI 146.9 113.7 29%

PATMI Margin (%) 8.5% 7.1% 1.4%

PATMI

(Excluding exceptional items1) 160.0 118.7 35%

PATMI Margin (%)

(Excluding exceptional items1

) 9.2% 7.4% 1.8%

YTD Mar

Excluding the contribution from PLife REIT, PATMI (excluding exceptional items) improved further

18

Excluding PLife REIT’s Results

1: Exceptional items, net of tax and minority share

IHH Group recorded 35% growth to its bottom-line (excluding exceptional items and PLife REIT)

19

RM'mil 2014 2013 Variance

Profit after tax and minority interests 159.1 127.3 25%

Add back/(Less): Exceptional Items

Professional and consultancy fees for acquisitions 0.2 0.2

Write off property, plant and equipment 0.1 0.0

Gain on disposal of property, plant and equipment (1.6) (0.2)

Exchange loss on net borrowings2

28.6 10.2

27.3 10.2

Add/(less): Tax effects on exceptional items (5.7) (2.0)

21.5 8.2

Add/(less): Minority interest share of exceptional items (8.5) (3.2)

13.1 5.0

Profit after tax and minority interests

(Excluding exceptional items1) 172.1 132.2 30%

Less: PATMI contribution from PLife REIT (12.2) (13.6)

Profit after tax and minority interests

(Excluding exceptional items1

and PLIfe REIT) 160.0 118.7 35%

YTD Mar

Note:

1. Exceptional items, net of tax and minority share

2. Relates to exchange differences arising from foreign currency denominated borrowings/payables net of foreign currency denominated cash/receivables, recognised by Acibadem Holdings

Segments

GROUP -1% 8%

GROUP (Excl REIT) -1% 8%

PLife REIT 0% 14%

Others -100% -

IMU Health 3% 1%

Acibadem Holdings (New) - -

Acibadem Holdings -9% -2%

PPL-International (New) - -

PPL-International 1% 21%

PPL-Malaysia (New) - -

PPL-Malaysia 0% 11%

PPL-Singapore 3% 14%

Q1'14

vs Q4'13

YTD'14

vs YTD'13

639.7 657.8

307.0 308.2

- -77.6 78.3- -

684.3 625.5

-14.7

48.850.3

0.0-

22.822.9

40.241.0

1,780.1 1,757.6

Q4 2013 Q1 2014

575.3657.8

277.8

308.2-

-

64.7

78.3

-

-

637.1

625.5

-

14.7

49.7

50.3

-

-

20.0

22.9

37.4

41.0

1,624.6

1,757.6

YTD 2013 YTD 2014

Robust year-on-year revenue growth from existing operations

20

Revenue (RM ‘mil) Variances

“Others” segment comprises of IHH Group corporate offices as well as other

investment holding entities

“New Hospitals” as referred to in these slides refers to:

Malaysia

- Pantai Hospital Manjung

- Gleneagles Hospital; Medini

- Gleneagles Hospital Kota Kinabalu

- International

- GHK Hospital

IHTYL (Turkey)

- Acibadem Halkali/Atakent Hospital

- Acibadem Altunizade Hospital

PLife REIT (Intersegment)

-1%

8%

Segments

GROUP -3% 11%

GROUP (Excl REIT) -5% 11%

PLife REIT 17% 11%

Others -41% -23%

IMU Health 42% -1%

Acibadem Holdings (New) NM NM

Acibadem Holdings -5% -1%

PPL-International (New) -107% NM

PPL-International 5% 31%

PPL-Malaysia (New) -53% NM

PPL-Malaysia -11% 15%

PPL-Singapore 1% 31%

YTD'14

vs YTD'13

Q1'14

vs Q4'13

Healthy EBITDA growth and margin improvement vs last year driven by higher revenues and operating

leverage; Partially offset by pre-operating costs of new operations

21

EBITDA (RM ‘mil) Variances

Margins

Margins

w/o New

Hospitals & PLife

REIT

w/o PLife

REIT

142.1 143.4

106.8 94.6

(1.8) (2.8)

23.324.5

132.1124.9

(3.3) (9.9)

14.921.2

(7.4)(10.4)

44.351.9

450.6 436.5

Q4 2013 Q1 2014

109.6

143.4

82.1

94.618.7

24.5

125.6

124.9

(1.0)(9.9)

21.4

21.2

(8.5)(10.4)

46.7

51.9

394.2

436.5

YTD 2013 YTD 2014

23.1% 22.2% 21.7% 22.2%

23.4% 23.1% 21.7% 23.1%

-3%

11%

Excluding the New Hospitals and PLife REIT, IHH Group’s

EBITDA margins increased 1.4% to 23.1% in YTD 2014,

contributed by operating leverage achieved by the

Group’s major operations:

EBITDA Margin

PPL-Singapore

PPL-Malaysia

PPL-International

Acibadem Holdings

IMU Health

YTD 2013 YTD 2014

19.1% 21.8% 2.7%

29.5% 30.7% 1.1%

28.9% 31.4% 2.5%

19.7% 20.0% 0.3%

43.0% 42.1% -0.9%

YTD'14

vs YTD'13

Balance Sheet

As at

31 Mar 2014

As at

31 Dec 2013

RM'mil RM'mil

Total Assets 27,701 27,261

- Tangible Assets 16,195 15,752

- Intangible Assets

Goodwill 8,919 8,881

Other intangibles 2,587 2,628

Total Liabilities (7,530) (7,338)

Total Equity 20,171 19,923

Non-controlling Interests (1,799) (1,848)

Total Shareholders' Equity (excluding non-controlling interests) 18,372 18,075

Net Tangible Assets (excluding non-controlling interests) 6,866 6,566

Total Debt (4,562) (4,461)

Total Cash 2,269 2,145

Net Debt (2,293) (2,316)

Net Debt / NTA 0.33 0.35

Net Debt / Equity 0.11 0.12

Maintained strong balance sheet

Healthy net gearing ratio of 0.11 times

22

Strong operating cash flows to support annual dividends and capital expenditure for expansion

23

Cashflows @ 31 March 2014 (RM’mil)

Cash Reconciliation to Cashflow Statement: RM'mil

Cash per Balance Sheet 2,269

Less:

Cash collateral received (5)

Fixed deposits pledged (4)

Cash per Cashflow Statement 2,260

Cash Debt

2,136

313

223

40

5

2,260

Cash @ 1/1/2014 Net cash from

Operating

Activities

Net cash used in

Investing

Activities

Net cash from

Financing

Activities

Effect of FX Cash @

31/03/2014

@ 31 Mar 2014 RM'mil

Parkway Pantai 830

Acibadem Holdings 303

IMU Health 165

Others 885

2,183

PLife REIT 85

2,269

@ 31 Mar 2014 RM'mil

Parkway Pantai 1,062

Acibadem Holdings 2,061

IMU Health -

Others 2

3,125

PLife REIT 1,437

4,562

RM' mil

Gleneagles Hong Kong Hospital 1,505.4

Gleneagles Penang (Expansion) 11.1

Pantai Hospital Kuala Lumpur (Expansion) 156.2

Gleneagles Medini 431.7

Gleneagles Kuala Lumpur (Expansion) 29.2

Pantai Hospital Klang 49.2

Gleneagles Kota Kinabalu 69.8

Pantai Hospital Manjung 19.3

Budgeted expenditure for approved projects 160.2

926.7

Acibadem Bodrum 29.9

Acibadem Maslak (Expansion) 135.4

Acibadem Taksim 75.4

Acibadem Altunizade 265.0

Acibadem Atasehir 234.8

Acibadem Kartal 175.6

Budgeted expenditure for approved projects 38.7

954.8

Total Unincurred Expansion Capital Expenditure 3,386.9

Projected

Disbursements

Q2 2014 till 2016

Expansion Capital Expenditure – Construction & Medical Equipment

24

*

Parkway will fund 60% of this balance through its bank

facility and the 40% partner for the HK Hospital Project

will fund balance of 40%

Funded from Malaysia’s operating cashflows and new bank

facilities if required

Acibadem will fund these from operating cashflows

and Acibadem’s bank facilities

Based on the following exchange rates:

1 SGD : 2.6031

1 INR : 0.0547

1TL : 1.4928

1 HKD : 0.4252

Outlook & Prospects

∗ Emerging markets will continue to enjoy higher growth in demandfor quality private healthcare driven by:- Demographics of home markets

- Faster growing upper/middle class

- Increased medical travellers from non-traditional markets to medical hubs

∗ Opening of new facilities will increase capacity to supportincreasing demand and hence drive revenue growth- Mount Elizabeth Novena Hospital will progressively open additional wards

- Pantai Hospital Manjung commenced operation on 19 May 2014.

- Acibadem Atakent Hospital opened in January 2014

∗ Inflationary impact on staff costs, rentals and other operatingexpenses and start-up costs of newly commissioned hospitals willbe mitigated through

- Increased mix of higher revenue intensity cases and price adjustments

- Operating leverage from growth in revenues and

- Especially from improved margins of the 3 new hospitals opened in 2012

25

Outlook & Prospects: Overall IHH Group (cont’d)

26

∗ Expect emerging markets to operate in an environment of volatileexchange rates :- IHH’s geographically diversified operating subsidiaries spreads currency risks arising

from translation differences in the Group’s balance sheet and income statement

- The Group minimises most of its currency risks by borrowing in the functional

currency of the borrowing entity or by borrowing in the same currency as its foreign

operations (ie. hedge of net investments).

- This is with the exception of Acibadem Holdings where it borrows in US-dollar and

hedges its cashflow instead

- through medical tourism receipts in hard currency and

- substantial USD cash buffer

∗ Continued strong balance sheet and operating cashflows willenable IHH to support its expansion plans.

ConclusionAttractive and unique healthcare asset

27

• Regional healthcare operator with presence in high growth markets of Asia and in the

CEEMENA

• Leading market position in three home markets (Malaysia, Singapore and Turkey) with

expanded presence in key markets (including China and India)

• Attractive industry dynamics (rising affluence, ageing population, structural deficit in

private hospitals)

• Proven management track record

• Clear growth strategy

• Diversified earnings base

• Strong balance sheet

Appendix

28

Core Businesses and Equity Interests

Wholly-owned holding company for Parkway and Pantai

healthcare businesses in Singapore and Malaysia

Has investments and operations in the PRC, India,

Hong Kong, Vietnam and Brunei

Indirect 60% owned leading integrated private healthcare

operator in Turkey

Wholly-owned private healthcare university in Malaysia,

with over 7,000 students trained since 1992

IHH owns 35.8% equity interest in Plife REIT

One of Asia’s largest healthcare real estate

investment trusts

Listed on the Singapore Stock Exchange

IHH owns 10.9% equity interest

One of India’s most prestigious and largest healthcare

providers

Listed on Bombay Stock Exchange and the National Stock

Exchange of India

AppendixAn integrated, comprehensive suite of services

Primary

Tertiary and

Secondary

Quaternary

29

Our Integrated services span:

Primary Care – Treatment of basic illnesses, checkups, vaccination and dental services

Secondary Care – Specialist consultation, local surgeries, emergency care,

diagnostics/imaging services and acute treatment on an inpatient/outpatient basis

Tertiary Care – Specialist consultative care, advanced treatment, complex surgery and

inpatient care with specialised equipment and facilities

Quarternary Care – High-intensity complex surgeries and organ transplants

Complementary Ancillary Services – Laboratory and pathology services, physiotherapy and

rehabilitation, emergency help and transportation, home health services, hospital project

management, design and refurbishment

Medical Education – Medical education and training for doctors-to-be, and ongoing training

for medical personnel

www.ihh-healthcare.com

-End of Presentation-