illinois grh update - dyzz9obi78pm5.cloudfront.net · june 25, 2015 illinois grh update usda is an...

TRANSCRIPT

June 25, 2015

Illinois GRH Update

USDA is an equal opportunity provider and employer. If you wish to file a Civil Rights program complaint of discrimination, complete the USDA Program Discrimination Complaint Form (PDF), found online at http://www.ascr.usda.gov/complaint_filing_cust.html, or at any USDA office, or call (866) 632-9992 to request the form. You may also write a letter containing all of the information requested in the form. Send your completed complaint form or letter to us by mail at U.S. Department of Agriculture, Director, Office of Adjudication, 1400 Independence Avenue, S.W., Washington, D.C. 20250-9410, by fax (202) 690-7442 or email at [email protected].

United States Department of Agriculture Rural Development

TURN TIMES We are currently processing complete applica ons received June 25, 2015. Current turn mes can be found on our website!

HANDBOOK 3555 The handbook can be accessed on the RD Handbooks website.

NEED A FORM? Forms for the new 3555 regula on can be found on the Agency’s eForms website.

HOLIDAY HOURS Our offices will be closed Friday, July 3rd in observance of Independence Day.

QUESTIONS?

Toll Free 866‐481‐9575 Email Champaign‐[email protected]

REMINDERS Color photos are required for all appraisal reports submi ed to the agency to ensure photo

integrity and legibility. If a lender closes a loan with a loan amount or interest rate that is higher than what is listed

on the commitment, the Agency does not have an obliga on to issue a loan note guarantee. Lenders may con nue to close loans with lower interest rates and loan amounts than what is listed on the commitment without prior Agency approval.

Discount points are eligible to be financed for low income applicants only. In these cases, discount points financed will not exceed two percentage points of the loan amount and must represent a reduc on to the interest rate.

Seller concessions are limited to 6% of the sales price.

4506-T Due to a recent IRS data breach, the IRS is rejec ng some requests for tax return transcripts in order to deter fraud. Please refer to the following ListServ no fica on sent by the Na onal Office on June 18th for direc ons on how to handle such instances. Note: these guidelines do not apply to “rejected” requests from the IRS due to misspelled names or incorrect data.

Effec ve October 1, 2015, the start of Fiscal Year (FY) 2016, the Up‐Front Guarantee Fee and Annual Fee structure will be as follows:

The FY 2016 fee structure is applicable to all condi onal commitments on or a er October 1, 2015. Requests submi ed to Rural Development by September 30, 2015, for which a commitment has not been issued, will be subject to the FY 2016 fee structure. There are no excep ons to the FY 2016 fee structure. Therefore, star ng on October 1, 2015 all condi onal commitments will be subject to the FY 2016 fee structure, regardless of the date the request was received by Rural Development.

UP-FRONT GRH FEE 10/1/2015 Through 9/30/2016

Purchases & Refinances 2.750%

ANNUAL FEE 10/1/2015 Through 9/30/2016

Purchases & Refinances (no change)

0.50%

FY 2016 FEE STRUCTURE

RAD! On June 18th, the Na onal Office released two new reference documents: Resource Assistance Document (RAD) Quick Reference Guide These documents provide FAQs organized by subpart and sec ons of the regula on and handbook. Both documents are included and follow this

update.

1

Morgan, Nicki - RD, Champaign, IL

From: [email protected]: Thursday, June 18, 2015 9:18 AMTo: [email protected]: SFH Origination Update IRS 4506-T Requests

June 18, 2015

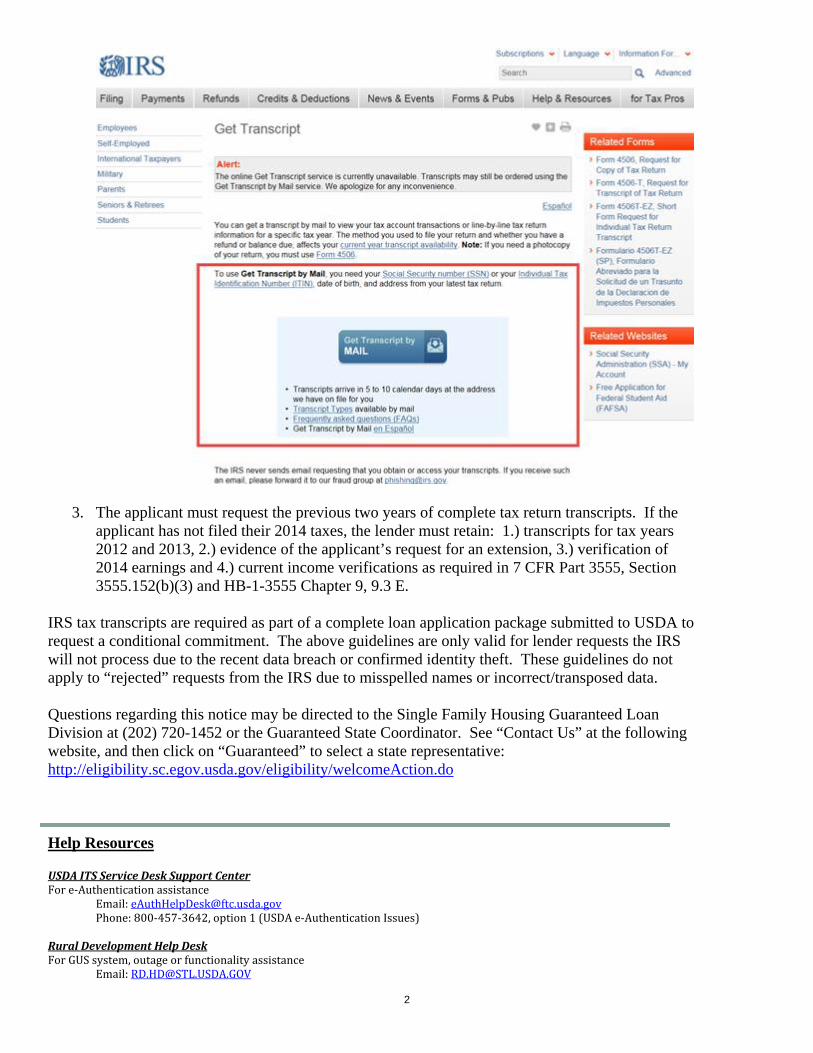

Update: IRS 4506-T Requests HB-1-3555 Chapter 9, 9.3 E requires lenders to obtain income tax return transcripts from the Internal Revenue Service (IRS) for all adult household members. The tax return transcripts assist lenders to validate the income documentation submitted by household members that is used to determine eligibility for the Single Family Housing Guaranteed Loan Program (SFHGLP). Due to a recent IRS data breach, the IRS is rejecting some lender requests for tax return transcripts in order to deter fraud. When an IRS Form 4506-T request from a lender returns the following message: “Due to limitations, the IRS is unable to process this request. The IRS will mail a notification to the borrower to explain this reason; please contact your borrower.” the following steps may apply:

1. The lender must retain the determination from the IRS that their request cannot be processed.

2. The applicant may request their tax return transcripts and deliver them to the lender. Information to request transcripts by mail is available online at: http://www.irs.gov/Individuals/Get-Transcript.

2

3. The applicant must request the previous two years of complete tax return transcripts. If the

applicant has not filed their 2014 taxes, the lender must retain: 1.) transcripts for tax years 2012 and 2013, 2.) evidence of the applicant’s request for an extension, 3.) verification of 2014 earnings and 4.) current income verifications as required in 7 CFR Part 3555, Section 3555.152(b)(3) and HB-1-3555 Chapter 9, 9.3 E.

IRS tax transcripts are required as part of a complete loan application package submitted to USDA to request a conditional commitment. The above guidelines are only valid for lender requests the IRS will not process due to the recent data breach or confirmed identity theft. These guidelines do not apply to “rejected” requests from the IRS due to misspelled names or incorrect/transposed data. Questions regarding this notice may be directed to the Single Family Housing Guaranteed Loan Division at (202) 720-1452 or the Guaranteed State Coordinator. See “Contact Us” at the following website, and then click on “Guaranteed” to select a state representative: http://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do Help Resources USDAITSServiceDeskSupportCenterFore‐Authenticationassistance

Email:[email protected]:800‐457‐3642,option1(USDAe‐AuthenticationIssues)

RuralDevelopmentHelpDeskForGUSsystem,outageorfunctionalityassistance

Email:[email protected]

3

Phone:800‐457‐3642,option2(USDAApplications);thenoption2(RuralDevelopment) To unsubscribe from this list, please do the following: Go to http://www.rdlist.sc.egov.usda.gov and enter your email address and click on the “SFH Origination News” checkbox and then click on the “Unsubscribe” button. To ensure delivery of our emails, please have your IT department or service provider add *usda.gov domains to your Safe Sender’s List and add to it your individual Safe Senders List. To Subscribe to this list or other available lists or unsubscribe an old email address and subscribe a new email address, go to http://www.rdlist.sc.egov.usda.gov and enter your email address and click on the appropriate e-mail list(s) to which you wish to subscribe and then click on the “Subscribe” button.

USDA is an equal opportunity provider and employer. If you wish to file a Civil Rights program complaint of discrimination, complete the USDA Program Discrimination Complaint Form, found online at http://www.ascr.usda.gov/complaint_filing_cust.html, or at any USDA office, or call (866) 632-9992 to request the form. You may also write a letter containing all of the information requested in the form. Send your completed complaint form or letter to us by mail at U.S. Department of Agriculture, Director, Office of Adjudication, 1400 Independence Avenue, S.W., Washington, D.C. 20250-9410, by fax (202) 690-7442 or email at [email protected].

1

Single Family Housing Guaranteed Loan Program

Resource Assistance Document

Spring 2015

2

THE RESOURCE ASSISTANCE DOCUMENT (RAD) IS AVAILABLE FROM THE SINGLE FAMILY HOUSING GUARANTEED LOAN PROGRAM (SFHGLP)

ONLY FOR EDUCATION AND TRAINING PURPOSES.

The RAD has been developed to achieve the following goals:

1. Help familiarize users with 7 CFR Part 3555 and HB‐1‐3555 by subpart and handbook chapter

2. Assist users to quickly locate information in the regulation and handbook

3. Address frequently asked questions by providing the regulation and handbook reference(s)

The RAD does not:

1. Replace 7 CFR Part 3555 or HB‐1‐3555

2. Negate the need to review information within the regulation and/or handbook

Effective search tip: Hold down “Control” and then select “F” to access a quick search data field. Enter a key word of the topic. This will allow a

more efficient search of the document.

Every SFHGLP loan must be originated, underwritten, closed and serviced under the guidance of 7 CFR Part 3555. This document will be updated

as necessary. Future changes to the regulation and/or handbook will take precedence over guidance provided in this document.

EXAMPLE: LOCATING REFERENCES

7 CFR Part 3555: 3555.208(b)(3)(i) HB‐1‐3555: 12.6 A 1

7 CFR Part 3555 Section 3555.208

3555.208(b)

3555.208(b)(3)

3555.208(b)(3)(i)

HB‐1‐3555 Chapter 12

Paragraph 12.6

12.6 A

12.6 A 1

3

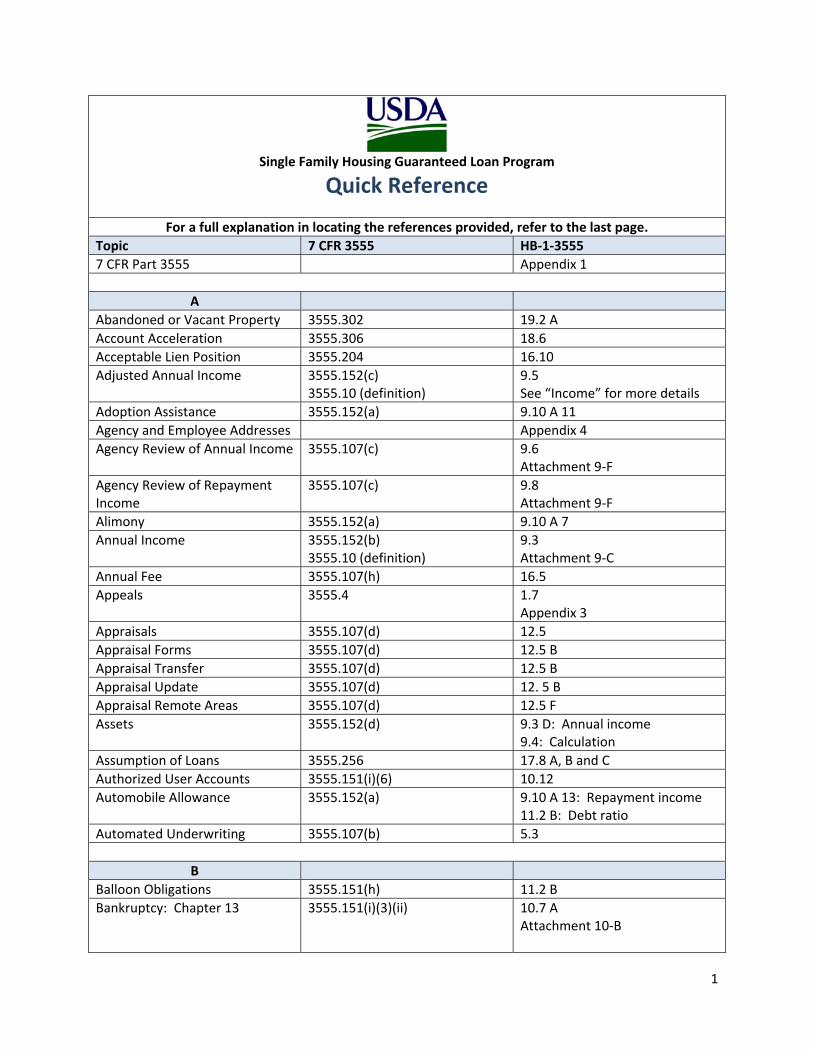

Subpart A: General 7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ’s

3555.1: Applicability 1.3: Getting additional help

3555.2: Purpose 1.4: SFHGLP Goals 1.5: SFHGLP Summary

What is a demonstration program? Pilot programs (i.e. rural refinance pilot).

3555.3: Civil Rights 1.6: Civil Rights

3555.4: Mediation and appeals 1.7: Review and Appeals Appendix 3

Who must be notified of a USDA loan denial? All “participants” as defined in 3555.10.

3555.5: Environmental requirements

12.10: Due Diligence12.10: Hazard Identification 16.11: Ownership Requirements 17.2: Required Servicing Actions

Is there an environmental regulation? 7 CFR Part 1940 Subpart G Are there additional considerations for new or proposed dwellings? Refer to 7 CFR Part 1924 Subpart A. What are the flood insurance requirements for an existing dwellings located in a SFHA? 3555.5(d)(5) and (6) and HB 16.11 C 2 Are new or proposed dwellings located in a SFHA eligible? Yes. 3555.5(d)(7) and HB 12.10 B Are flood elevation certificates required? Existing dwellings: No. New/proposed dwellings: Yes, prepared by a licensed engineer or surveyor. 3555.(d)(7) and HB 12.10 B Is flood insurance required for structures detached from the primary residence? No, per HFIAA of 2014. 3555.5(d)(7) and HB 12.10 B Are there maximum coverage/deductibles for insurance? Flood insurance: HB 12.10 B and HB 16.11 C 2. Flexibility is provided for State and Federal law therefore new FEMA deductibles are eligible. Non‐SFHA properties: HB 16.11 C 1.

3555.6: State and local law 1.8: State and local laws Do State issued publications require review by the National Office? Yes. HB 1.8

3555.7: Exception authority 1.9: Exception authority 3555.8: Conflict of interest 1.10: Conflict of interest

Form RD 3555‐21

Will a prohibited relationship result in loan denial/ineligible? No. 3555.8(d) and HB 1.10 B

3555.9: Enforcement 3555.10: Definitions and abbreviations

Appendix 10: Glossary

4

Subpart B: Lender Participation 7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ’s

3555.51: Lender eligibility 3.2: Lender approval criteria3.6: Lender responsibility 3.8: Monitoring Origination/Servicing of Loans Chapter 4: Lender Responsibilities 5.1: Introduction Attachment 4‐A and 4‐B

Are members of the Federal Reserve System now eligible to apply for approved lender status (i.e. FHLB, NCUA, etc.)? Yes. 3555.51(a)(8) and HB 3.2 B 4 What documentation is required to demonstrate an ability to originate and underwrite loans? 3555.51(a)(9), HB 3.2 B 1 and Attachment 3‐A

3555.52: Lender approval 3555.52: Lender approval 3.3: Application

3.4: Agency Review 3.9: Revoking lender eligibility 3.10: Voluntary Withdrawal 4.11: Withdrawal of Approval Attachment 3‐A and 3‐B Form RD 3555‐16

Is mandatory training required for new lenders prior to lender approval? Yes. Lender modules are available on USDA LINC. Why did I get a “Pre‐Approval” letter? All required documentation was not received for a full approval. 3555.52(a) and (b) and HB 3.4 A Can a lender voluntarily withdrawal their own approval? Yes. 3555.52(c)(2) and HB 3.10

3555.53: Contracting for loan origination

3.2: Participation as an Agent of an approved lender

3555.54: Sale of loans to approved lenders

3.5: Lender sale of guaranteed loans 4.6: Sell loans only to approved lenders 4.11: Withdrawal of Approval Form RD 3555‐11

5

Subpart C: Loan Requirements7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ’s

3555.101: Loan purposes 6.2: Eligible loan purposesAttachment 6‐A Chapter 12 Section 7: Combination Construction Permanent Loans

Do all repairs/rehabilitation work have to be completed prior to the lender’s request for the LNG? Yes, unless minor exterior/interior work remains that is eligible per 3555.202(c) and HB 6.2 B Can the cost of a washer/dryer/refrigerator be included in the loan amount if sufficient equity exists between the purchase price and appraised value? Yes. 3555.101(b)(1) and HB 6.2 C If appliances are purchased with loan funds should there be a rider or other agreement attached to the mortgage that these items will remain within the home in the event of a sale? No. Can discount points used to permanently buydown the interest rate be included in the loan amount for moderate income applicants? No. This is only allowed for low income applicants. 3555.101(b)(6)(vi), 3555.102(d) and HB 6.3 Can an escrow cushion be established for the annual fee? Yes, not to exceed two months. 3555.101(b)(6)(xi) Can the applicant finance all or a portion of a real estate commission, auction fee, or other purchase transaction fee? No. These are not customary fees. 3555.101(b) Is USDA responsible to review the loan to ensure the lender has not exceeded applicable CFPB thresholds for reasonable lender fees? No. This is a Federal law the approved lender must ensure is met. HB 6.2 C Is the SFHGLP up‐front and/or annual fee included in the applicable CFPB calculation for reasonable lender fees? No. HB 6.2 C “Reasonable Lender Fees” Where can I find complete information about the combination construction and permanent loans? Refer to 3555.105 and HB Chapter 12, Section 7. Is an interim construction loan used to construct or repair/rehabilitate a dwelling eligible for a guaranteed loan? Yes. The upfront guarantee fee for purchase transactions will apply. 3555.101(d)(1) and HB 6.2 D 1

6

Can the balance of a lot loan be included in the total loan amount for the construction of a new dwelling on this site? Yes. 3555.101(d)(2)(ii) and HB 6.2 D 2 Is an applicant with a current FHA/VA/Fannie/Freddie mortgage eligible to refinance into a new guaranteed loan? No. 3555.101(d)(3) Is a current guaranteed loan borrower subject to a new upfront guarantee fee and annual fee (even if their current loan does not have the annual fee requirement)? Yes. 3555.101(d)(3)(ix) and (ix) and HB 6.2 D 3 E and F Can a current borrower be removed from the loan? A streamlined or non‐streamlined refinance may remove existing borrowers, but at least one original borrower must remain. 3555.101(d)(3)(iv) HB Attachment 6‐A “Applicant Eligibility” Can GUS be used for streamlined and non‐streamlined refinances? Yes. HB Attachment 6‐A “Use of GUS”

Can late payment fees be included in the “loan balance” eligible for refinance? No. 3555.101(d)(3)(v) and HB 6.2 D 3 A and Attachment 6‐A “Loan Purpose and Limitations” Can a second lien be included in the refinance? No, these would require subordination. 3555.101(d)(3) and HB 6.2 D 3 A and Attachment 6‐A “Loan Purpose and Limitations” Is a new property inspection required for a refinance transaction? No. Inspection costs/repairs identified by the approved lender in order to maintain the collateral are not eligible to be part of the loan amount. 3555.101(d)(3)(vii) and HB 6.2 D 3 B and Attachment 6‐A “Inspections”

How do I know if the applicant has a direct loan? Typically the credit report will show the mortgage creditor as “USDA.” The applicant can contact their current loan servicer to verify the type of loan. Are Section 502 Leveraged Loans eligible for refinance? No. 3555.101(d)(3) and HB 6.2 D 4 A

3555.101: Loan purposes

(continued)

7

How do I obtain a payoff and recapture amount for a direct borrower that received subsidy? Submit by fax: 1.) a copy of a recent appraisal,2.) GFE or estimate of closing costs statement and 3.) a request on letterhead that includes the borrower’s name, account number, address and date the payoff should be valid through to the Customer Service Center (CSC) at (314) 457‐4433. Payoffs and subsidy recapture amounts will not be provided verbally. Current direct borrowers may contact the CSC with loan questions at 1‐800‐414‐1226.

3555.102: Loan restrictions 6.3: Prohibited Loan Purposes Where can I find more information regarding manufactured homes? 3555.208 and HB Chapter 13 Section 2 “Manufactured Homes” If a property has a barn or extra garage is it ineligible? Properties must be residential in character, design and use. Property that currently is an operational farm or business, agriculture enterprise, or has tillable land/equipment/signage that will remain post loan closing may be ineligible. Barns/storage sheds/additional garages typically do not render a property ineligible. 3555.201(b) and HB 12.4. Where can I find more information regarding refinancing? 3555.101(d), HB 6.2 D and Attachment 6‐A. Is there a maximum limit on seller concessions? Yes, six percent of the property sales price. 3555.102(h) and HB 6.3 Can a borrower receive excess seller concessions at loan closing as cash back? No. Seller concessions must be used for eligible loan purposes per 3555.101. Are lender credits secured through premium pricing included in the six percent limitation? No. HB 6.3

3555.103: Maximum loan amount 7.2: Maximum Loan Amount Can the upfront guarantee fee be included in the loan amount? Yes. 3555.103(a) and HB 7.2 Is there a CLTV maximum? No. USDA will only guarantee the maximum LTV as provided in 3555.103. If the appraised value is less than the property sales price, can an applicant bring in the difference at loan closing? Yes. HB 7.2

3555.101: Loan purposes

(continued)

8

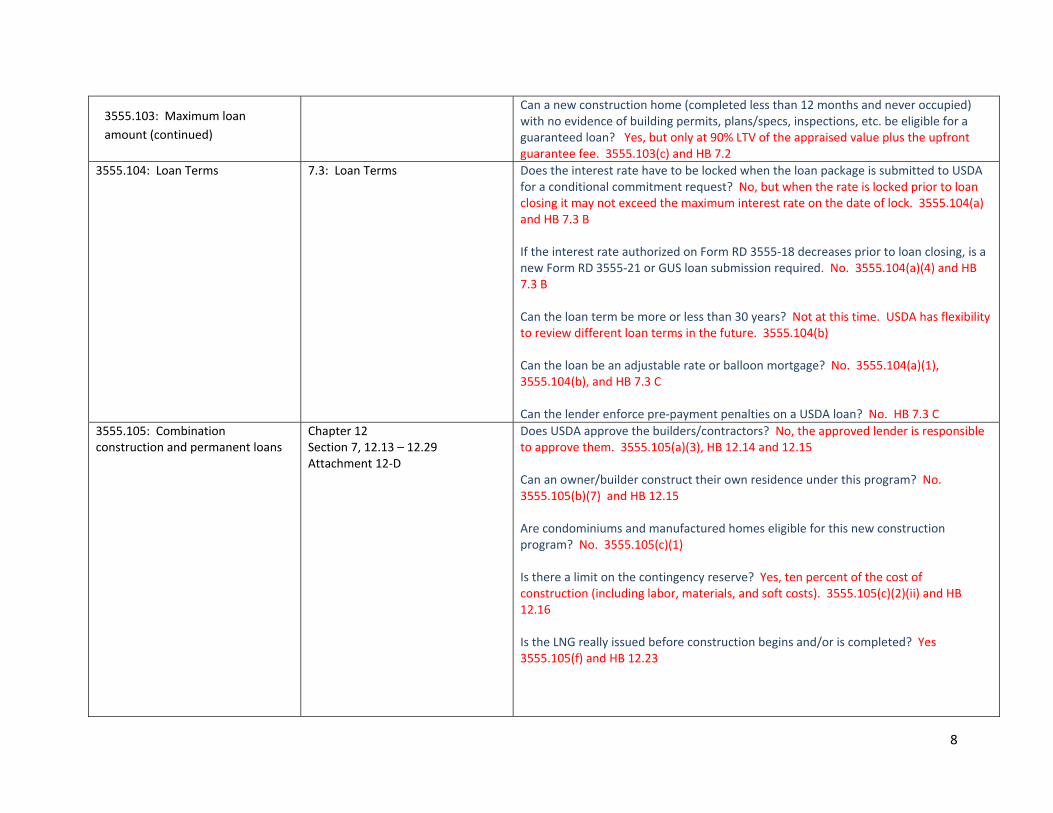

Can a new construction home (completed less than 12 months and never occupied) with no evidence of building permits, plans/specs, inspections, etc. be eligible for a guaranteed loan? Yes, but only at 90% LTV of the appraised value plus the upfront guarantee fee. 3555.103(c) and HB 7.2

3555.104: Loan Terms 7.3: Loan Terms

Does the interest rate have to be locked when the loan package is submitted to USDA for a conditional commitment request? No, but when the rate is locked prior to loan closing it may not exceed the maximum interest rate on the date of lock. 3555.104(a) and HB 7.3 B If the interest rate authorized on Form RD 3555‐18 decreases prior to loan closing, is a new Form RD 3555‐21 or GUS loan submission required. No. 3555.104(a)(4) and HB 7.3 B Can the loan term be more or less than 30 years? Not at this time. USDA has flexibility to review different loan terms in the future. 3555.104(b) Can the loan be an adjustable rate or balloon mortgage? No. 3555.104(a)(1), 3555.104(b), and HB 7.3 C Can the lender enforce pre‐payment penalties on a USDA loan? No. HB 7.3 C

3555.105: Combination construction and permanent loans

Chapter 12 Section 7, 12.13 – 12.29 Attachment 12‐D

Does USDA approve the builders/contractors? No, the approved lender is responsible to approve them. 3555.105(a)(3), HB 12.14 and 12.15 Can an owner/builder construct their own residence under this program? No. 3555.105(b)(7) and HB 12.15 Are condominiums and manufactured homes eligible for this new construction program? No. 3555.105(c)(1) Is there a limit on the contingency reserve? Yes, ten percent of the cost of construction (including labor, materials, and soft costs). 3555.105(c)(2)(ii) and HB 12.16 Is the LNG really issued before construction begins and/or is completed? Yes 3555.105(f) and HB 12.23

3555.103: Maximum loan

amount (continued)

9

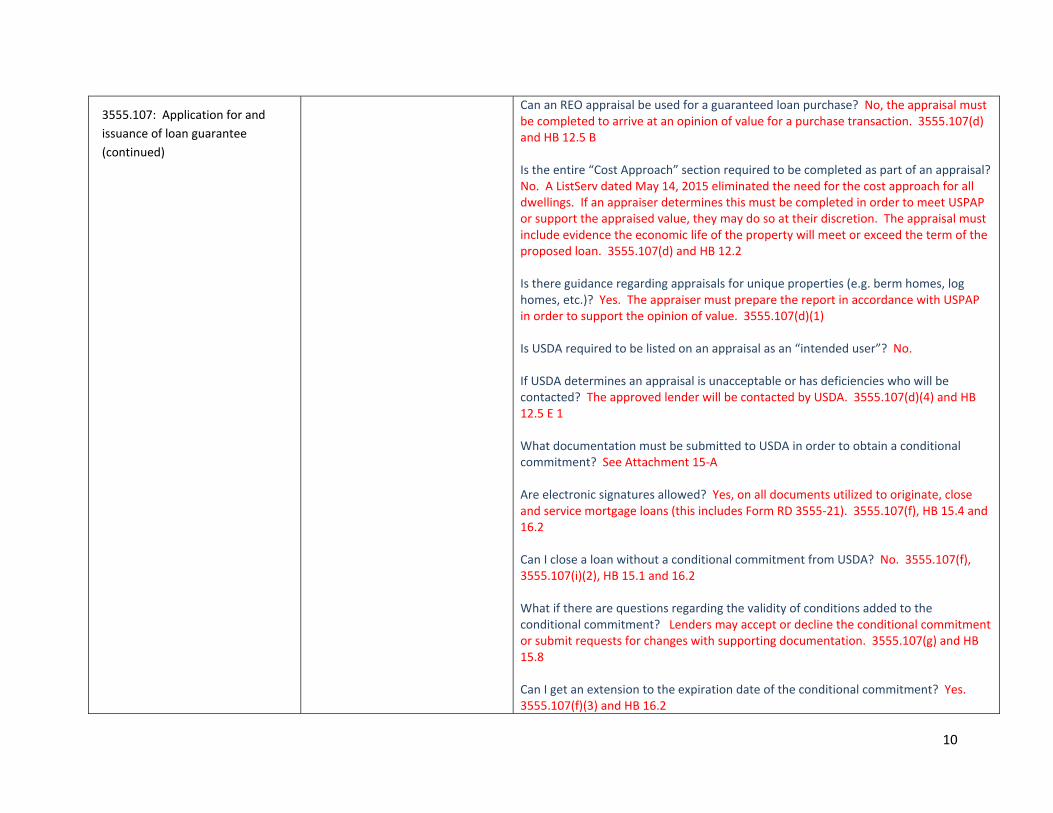

3555.107: Application for and issuance of loan guarantee

Chapter 14: Funding Priorities5.3: Utilizing GUS 12.5: Residential Appraisal Reports Chapter 15: Submitting the Application Package Chapter 16: Closing the Loan and Requesting the Guarantee

Can I close a loan if Form RD 3555‐18 says “Subject to receipt of congressionally appropriated funds”? Yes, but the approved lender remains liable for the loan until funds are received and a LNG can be issued. HB 14.4 B If I have a conditional commitment from USDA but the loan will not close, should I contact USDA? Yes. The obligated loan funds will be released to accommodate other loans. HB 14.5 If GUS renders an “Accept” underwriting recommendation my loan has been approved. No. A GUS recommendation is not an approval and should not be the exclusive reason a loan is approved. The approved lender is responsible to determine final loan approval. Data integrity issues may determine the recommendation is not supported. 3555.107(b), 3555.107(b)(6), HB 5.3, 5.3 C, 5.3 I, 5.3 J, and 5.3 N If a GUS “Accept” is rendered, is a verification of rent required? The lender must retain evidence of all data entered into GUS. If rent was entered on the “Income and Expenses” application page, evidence to support this amount must be retained in the permanent loan file. 3555.107(b)(1) and (2) and HB 5.3 M Where is guidance for rent verification methods? HB 10.13 Are GUS loans excluded from indemnification requirements? No. 3555.107(b)(3) Are color photographs required for appraisals? Yes. ListServ dated 4‐17‐2015. HB‐1‐3555 will be revised to clarify “color” photographs. Can USDA refuse to accept a specific appraisers report? Yes. 3555.107(d)(5) How long is my appraisal valid? 120 days (purchase, new construction or refinance). 3555.107(d)(7) If my appraisal is expired what options do I have? 1.) The lender may have a 30 day grace period with no approval required from USDA (150 days total). 3555.107(d) and HB 12.5 B. 2.) The lender may obtain an appraisal update to extend the validity of the current appraisal. 3555.107(d) and HB 12.5 B Can one lender transfer an appraisal to another lender? Yes. 3555.107(d) and HB 12.15 B

10

Can an REO appraisal be used for a guaranteed loan purchase? No, the appraisal must be completed to arrive at an opinion of value for a purchase transaction. 3555.107(d) and HB 12.5 B Is the entire “Cost Approach” section required to be completed as part of an appraisal? No. A ListServ dated May 14, 2015 eliminated the need for the cost approach for all dwellings. If an appraiser determines this must be completed in order to meet USPAP or support the appraised value, they may do so at their discretion. The appraisal must include evidence the economic life of the property will meet or exceed the term of the proposed loan. 3555.107(d) and HB 12.2 Is there guidance regarding appraisals for unique properties (e.g. berm homes, log homes, etc.)? Yes. The appraiser must prepare the report in accordance with USPAP in order to support the opinion of value. 3555.107(d)(1) Is USDA required to be listed on an appraisal as an “intended user”? No. If USDA determines an appraisal is unacceptable or has deficiencies who will be contacted? The approved lender will be contacted by USDA. 3555.107(d)(4) and HB 12.5 E 1 What documentation must be submitted to USDA in order to obtain a conditional commitment? See Attachment 15‐A Are electronic signatures allowed? Yes, on all documents utilized to originate, close and service mortgage loans (this includes Form RD 3555‐21). 3555.107(f), HB 15.4 and 16.2 Can I close a loan without a conditional commitment from USDA? No. 3555.107(f), 3555.107(i)(2), HB 15.1 and 16.2 What if there are questions regarding the validity of conditions added to the conditional commitment? Lenders may accept or decline the conditional commitment or submit requests for changes with supporting documentation. 3555.107(g) and HB 15.8 Can I get an extension to the expiration date of the conditional commitment? Yes. 3555.107(f)(3) and HB 16.2

3555.107: Application for and

issuance of loan guarantee

(continued)

11

If a conditional commitment has been issued and a natural disaster occurs in the area 1.) prior to loan closing or 2.) after loan closing but prior to signing the lender certification and submission of a loan closing package to USDA, is a new appraisal required? The lender is responsible to ensure the collateral, employment and all documentation utilized to support the conditional commitment has sustained no adverse changes. It will be up to the lender to ensure the collateral is secure before submitting the loan package to USDA. 3555.107(d) and 3555.107(i)(2) Is any part of the upfront guarantee fee refundable in the event the home is sold, loan refinanced or paid in full? No. 3555.107(g) and HB 16.4 Does the annual fee cease when a specified LTV is reached? No. The annual fee is for the life of the loan. 3555.107(h) and HB 16.5 If the borrower makes additional monthly or annual principal mortgage payments will this reduce the annual fee that is due? No, the annual fee is calculated on the average annual scheduled unpaid principal balance. 3555.107(h) Can a Power of Attorney (POA) be used at a loan closing? Yes when the POA complies with state law. 3555.107(i) and HB 16.2 What documents are required to request a LNG? 3555.107(i) and HB Attachment 16‐A I submitted my loan closing package to USDA within the required timeframe. At the time USDA processed the request for LNG the loan was in default. Can I still obtain a LNG? Yes. If the loan was current at the time the Lender Certification (Form RD 3555‐18) was signed and the loan was submitted to USDA. 3555.107(j)(3) and HB 16.3 What does USDA refer to as the “closing date”? The date of closing is defined as the settlement date as it appears on the HUD‐1 settlement statement (or comparable document). HB 16.7

3555.108: Full faith and credit 4.9: Indemnification

3555.107: Application for and

issuance of loan guarantee

(continued)

12

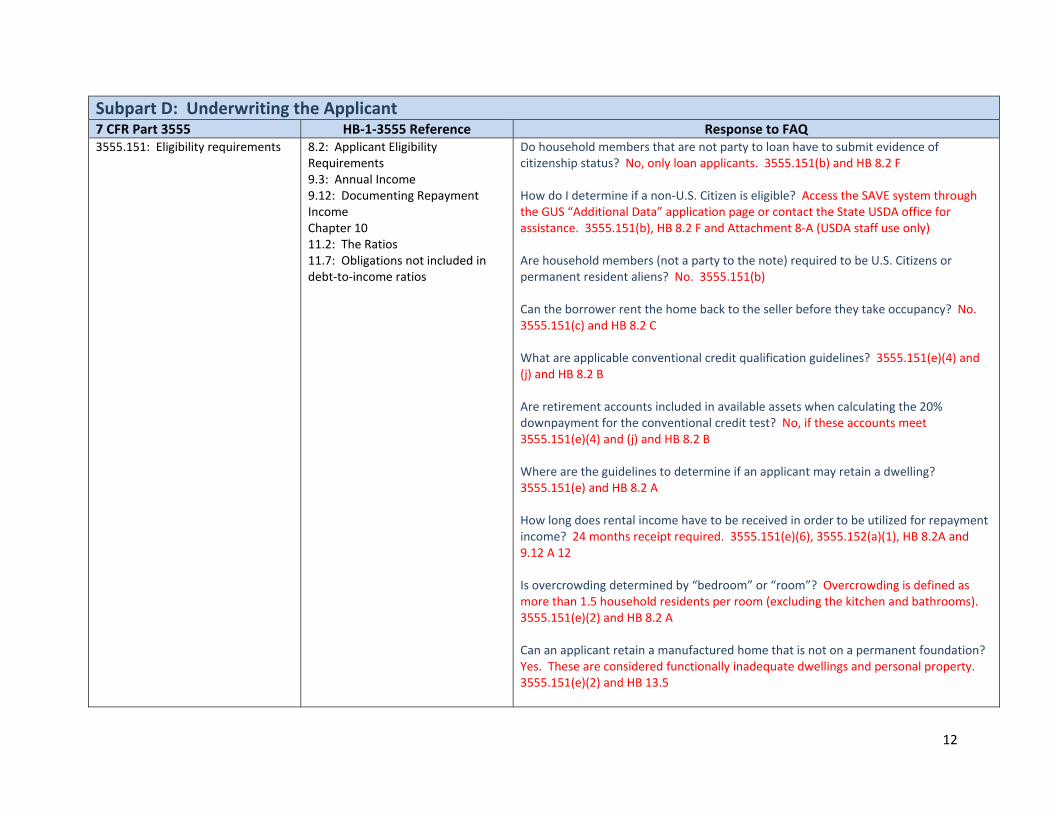

Subpart D: Underwriting the Applicant7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ 3555.151: Eligibility requirements 8.2: Applicant Eligibility

Requirements 9.3: Annual Income 9.12: Documenting Repayment Income Chapter 10 11.2: The Ratios 11.7: Obligations not included in debt‐to‐income ratios

Do household members that are not party to loan have to submit evidence of citizenship status? No, only loan applicants. 3555.151(b) and HB 8.2 F How do I determine if a non‐U.S. Citizen is eligible? Access the SAVE system through the GUS “Additional Data” application page or contact the State USDA office for assistance. 3555.151(b), HB 8.2 F and Attachment 8‐A (USDA staff use only) Are household members (not a party to the note) required to be U.S. Citizens or permanent resident aliens? No. 3555.151(b) Can the borrower rent the home back to the seller before they take occupancy? No. 3555.151(c) and HB 8.2 C What are applicable conventional credit qualification guidelines? 3555.151(e)(4) and (j) and HB 8.2 B Are retirement accounts included in available assets when calculating the 20% downpayment for the conventional credit test? No, if these accounts meet 3555.151(e)(4) and (j) and HB 8.2 B Where are the guidelines to determine if an applicant may retain a dwelling? 3555.151(e) and HB 8.2 A How long does rental income have to be received in order to be utilized for repayment income? 24 months receipt required. 3555.151(e)(6), 3555.152(a)(1), HB 8.2A and 9.12 A 12 Is overcrowding determined by “bedroom” or “room”? Overcrowding is defined as more than 1.5 household residents per room (excluding the kitchen and bathrooms). 3555.151(e)(2) and HB 8.2 A Can an applicant retain a manufactured home that is not on a permanent foundation? Yes. These are considered functionally inadequate dwellings and personal property. 3555.151(e)(2) and HB 13.5

13

Has USDA switched to a single ratio for loan qualification? No, USDA has the ability to consider a single ratio but at this time the PITI and TD are both required. 3555.151(h)(1) and HB 11.2 Are 401k loans included in the total debt ratio? No. 3555.151(h)(1)(iii) and HB 11.2 B “401k loans/personal asset loans” What debts must be considered for non‐purchasing spouses in community property states? Refer to the state lending law. 3555.151(h)(1)(iv) and HB 11.2 B “Debts of a non‐purchasing Spouse (NPS)” Can gift funds be used to pay off debts of the applicant(s)? Yes. Gift funds are considered the applicant’s own funds. Verify the gift funds as required. 3555.151(h)(1)(i) and HB 9.3 E 1 “Verification of Gifts” Can the payment reflected for a student loan on the credit report be used? Yes, if the payment is verified as fixed (fixed term, fixed interest rate, no future changes) with the loan servicer. Non‐fixed payment arrangements must include one percent of the outstanding balance reflected on the credit report (no additional documentation required). 3555.151(h)(1)(i) and HB 11.2 B “Student loans” Do divorce decrees allow the exclusion of debts assigned to the ex‐spouse? No. Divorce decrees do not remove a borrower from a liability. Refer to 3555.151(h)(1)(i) and HB 11.2 B “Previous mortgage” and “Co‐signed non‐mortgage debt/obligations” for additional guidance. Can an approved lenders underwriter include an installment debt with ten months or less repayment remaining? Yes, the approved lender underwriter can include any short term debts they feel have a significant impact on repayment ability. 3555.151(h)(1)(i) and HB 11.2B “Short term obligations” Are daycare/daily childcare expenses included in the debt ratio? No. 3555.151(h)(1)(iii) and HB 11.7 Do GUS “Accept” loan files require debt ratio waivers for files that exceed 29% and/or 41%? No. 3555.151(h)(2) and (3), HB 11.3 A, 5.3 I and the GUS Underwriting Findings Report

3555.151: Eligibility requirements

(continued)

14

What are the maximum debt ratios for a manually underwritten loan file? Maximum PITI is 32%, maximum TD is 44%. Additional eligibility requirements apply. 3555.151(h)(2) and HB 11.3 A What are the eligible compensating factors to support a debt ratio waiver request for a manually underwritten loan file? 3555.151(h)(2)(i), (ii), (iii) and (iv), HB 11.3 A and 11.3 B for manually underwritten refinance transactions How is the monthly MCC credit applied? Deduct the monthly credit from the PITI. 3555.151(h)(5), HB 11.4 and 9.11 A Where is information on funded buydown accounts? 3555.151(h)(7), HB 11.5 and 9.11 B Do GUS “Accept” loan files require a credit wavier to be submitted to USDA? No. 3555.151(i)(2), HB 10.7 A, 5.3 C, 5.3 I, and 5.3 K What tradelines are acceptable to validate the credit score? Examples of traditional tradelines that may be considered to validate the credit score for underwriting include but not are limited to: Loans (secured/unsecured), revolving credit, installment credit, collections, charge‐offs, and authorized user accounts (if they meet HB 10.12). Deferred loans, public records and payments for court ordered debts (child support, alimony, garnishments, etc.) are not eligible. 3555.152(i)(3) and HB 10.5 If an applicant does not have the required number of traditional tradelines (three) in order to validate the credit score, can nontraditional tradelines be verified to supplement? Yes. Include the valid traditional tradelines with eligible nontraditional tradelines to meet credit requirements. 3555.151(i)(6) and HB 10.6 Is a nontraditional tradeline eligible if it has been open for 12 months but the required payments are not every month (e.g. insurance due on an annual, semi‐annual or quarterly basis)? Yes. 3555.151(i)(6) and HB 10.6 If only one applicant has a validated credit score per HB 10.5, does the other applicant(s) require full nontraditional history credit histories to be verified? No. 3555.151(i)(3) and HB 10.5

3555.151: Eligibility requirements

(continued)

15

Can a credit supplement obtained outside of GUS to verify an undisclosed debt/removal of an authorized user account/ etc. be used to retain a GUS “Accept” underwriting recommendation? No. The credit report uploaded into GUS must be the accurate representation of the applicant(s) credit. 3555.151(i)(2) and HB 5.3 C,G,I and M If an applicant has a bankruptcy/foreclosure/short sale discharged less than 36 months, is a GUS “Accept” eligible to be retained? Yes. Ensure the credit report accurately reflects the credit instance and the “Declarations” on the URLA (1003) are properly completed. 3555.151(i)(2) and HB 10.1 Can medical collections and charge off accounts be ignored from the credit review? No. A credit analysis must always occur prior to a capacity analysis. 3555.151(i) and HB 10.9

3555.152: Calculation of income and assets

RD Instruction 1980‐D included language regarding spouses that were separated for less than 3 months (for reasons other than military or work assignment) must have the separated /soon to be ex‐spouse’s income included in annual income. Does this apply under 7 CFR Part 3555? No. The applicant must certify to the household member number under the regulation on Form RD 3555‐21. 3555.152(b), 3555.10 definition of “Household” and HB 9.1 Can student loans be used for repayment income/assets to close? No. 3555.152(a)(4)(i) Can foster child/adult payments be used for repayment income? No. 3555.152(a)(4)(v). Do not include these payments in annual income. 3555.152(b)(5)(ii) Can adoption assistance be used for repayment? Yes, if there is a history of receipt and 3 year likelihood of continuance. 3555.152(a) Do not include payments in excess of $480 per adopted child in annual income. 3555.152(b)(5)(viii) and HB 9.3 A A household member (not party to the note) receives Social Security payments/disability/etc. but the payment is received by an applicant. Can this be used for repayment income? Yes, if received by a minor and they are a household member. 3555.152(a)(2) and HB 9.10

3555.151: Eligibility requirements

(continued)

16

Is there guidance for applicants that are starting new jobs but employment has not yet commenced (e.g. teachers, etc.)? Yes. 3555.152(a) and HB 9.10 and 9.10 A

Would all income earned by a full time college student (age 18 and up‐not head of household or spouse) be included in annual income? No, only the first $480. 3555.152(b)(4)(iv) and HB 9.3 A Is an unborn child counted as a household member? No. 3555.152(c)(1) and HB 9.3 E 1 Is private school tuition paid for a household member attending K‐12 an eligible childcare expense? No, but expenses that meet 3555.152(c)(2) for children birth to Pre‐K age are eligible when paid by a household member. Are child support payments eligible as a childcare deduction? No. 3555.152(c)(2) What is a net family asset? See definition in 3555.10. Are only the assets of applicants considered for the annual income calculation? No, all adult household member assets must be reviewed. 3555.152(d) For calculation methods see HB 9.4 D If an applicant is currently on maternity leave at the time of loan application/loan closing, how is their income considered? Unless otherwise stated by the applicant, assume they will resume employment at the end of leave, required income verifications will confirm applicant intentions. 3555.152 and HB 9.3. Where is information regarding unreimbursed business expenses? 3555.152, HB 9.3 E 1 and HB 9.10 A 19

3555.152: Calculation of income

and assets (continued)

17

Subpart E: Underwriting the Property7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ 3555.201: Site requirements 12.4: Site Requirements

Does a thirty percent site value guideline still apply? No. 3555.201(b)(1) Is there a reliable way to determine if a property is income producing? Properties that are currently an operational farm, business, agriculture enterprise, includes tillable land or equipment/signage that will remain post loan closing, it is likely income producing. Barns/storage sheds/additional garages may not render a property ineligible. 3555.201(b) and HB 12.4. Guidelines for non‐public water systems: 3555.201(b)(4) and HB 12.6 A 1: Privately owned, 12.6 A 2: Shared, 12.6 A 3: Community owned and 12.6 A 4: Required inspections and documentation Guidelines for non‐public waste systems: 3555.201(b)(4) and HB 12.6 B 1: Privately owned, 12.6 B 2: Community owned and 12.6 B 3: Required inspections and documentation

3555.202: Dwelling requirements 12.9: Existing and New Dwellings

What version of International Energy Conservation Code (IECC) is required to be met for new construction dwellings? The thermal standard must meet or exceed the version of IECC that is in effect at the time of construction. 3555.202(a) and HB 12.9 B Are escrow accounts limited to ten percent total for exterior and interior work or ten percent each (total of twenty percent)? A total of ten percent of incomplete work is allowed for exterior and interior development. 3555.202(c)(2) and HB 12.9 C and D What is the amount the exterior and/or interior escrow account must be funded? A minimum of 100 percent to assure the completion of remaining work. Lenders may require a higher amount if they choose. 3555.202(c)(3) and HB 12.9 C and D Where is guidance to establish an exterior and/or interior escrow account? 3555.202(c) and HB 12.9 C and 12.9 D Can borrowers complete exterior or interior development themselves? Yes, if all requirements of 3555.202(c)(4) are met. HB 12.9 E Are funds remaining in an escrow eligible to be returned to the original owner, assuming they were not financed into the loan amount? No. HB 12.9 C, D and E

18

Is there guidance for property conditions such as oil tanks, landfills, industrial sites, soil contamination, etc.? Yes. Refer to HUD Handbook minimum property standards and RD Instruction 1940‐G. 3555.202(b), 3555.107(d)(3) and HB 12.9

3555.203: Ownership requirements 13.4: Loans on Leasehold Estates Are there guidelines for leaseholds located on American Indian Restricted land? Yes. 3555.203(b)(3), HB 13.4 B and 16.11 B 2

3555.204: Security requirements Are junior liens allowed? Yes, but they must not adversely affect repayment or security of property. Lender must maintain first lien position. 3555.204(b) and HB 16.10

3555.205: Condominiums Chapter 12 Section 512.11: Condominiums and Planned Unit Developments

Is a condominium rider required? Yes. HB 12.11 A Are there ineligible condominiums? Yes. HB 12.11 A 1 Are site condominiums eligible? Yes if the criteria listed in HB 12.11 A 2 is met. Are HOA fees included in the PITI or TD ratio? Include in the PITI ratio: 3555.151(h)(1)(i). The PITI is part of the TD ratio: HB 11.2 B

3555.206: Community land trusts Chapter 13 Section 113.3: Loans for units in a community land trust

Are restrictions on resale prices of property allowed? Yes, when the terms of HB 13.3 C. May community land trust enforce a right of first refusal? Yes, when the terms of HB 13.3 D are met.

3555.207: Planned Unit Developments (PUD’s)

Chapter 13 Section 112.11: Condominiums and Planned Unit Developments

3555.208: Manufactured homes Chapter 13 Section 213.5 – 13‐11

Can an applicant retain a manufactured home that is not on a permanent foundation? Yes. These are considered functionally inadequate dwellings and personal property. 3555.151(e)(2) and HB 13.5 Are single wide manufactured homes eligible? Yes. New units must have a floor area of no less than 400 square feet. 3555.208(c)(1), HB 13.5 and 13.6 What is the difference between manufactured and modular homes? Manufactured homes must meet 3555.208. Modular homes must meet the requirements of existing and new dwellings 3555.202. See definition in HB 13.5 Can manufactured homes be taxed as personal property? No. They must be taxed as real estate. 3555.208(f)(2, HB 13.6 and 13.11 D

3555.202: Dwelling requirements

(continued)

19

Do dealer‐contractors have to be approved in each state? No. The applicant may purchase their unit from any manufactured home dealer. The applicant is responsible to select a contractor/builder that will meet the requirements in 3555.208(c), (d), (e), HB 13.8, 13.10 and 13.11

3555.209: Rural Energy Plus Loans 12.12 Rural Energy Plus Loans What are the expanded qualifying ratios for loans originated under these guidelines? At this time HB 12.12 does not allow for increased ratios. 3555.309

Subpart F: Servicing Performing Loans 7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ’s

3555.251: Servicing responsibly 4.6: Sell Loans Only to Approved Lenders 17.1: Introduction

Can a third party service the loan for an approved lender? Yes but the approved lender remains responsible for actions of this agent. 3555.251(b) and HB 17.1 B If an approved lender sells SFHGLP loans must USDA be notified? Yes. 3555.54, HB 4.6 and 17.1 A and C

3555.252: Required servicing actions

17.2: Required Servicing Actions17.3: Reporting Requirements 17.5: Insurance Proceeds Appendix 8: EDI Documentation

Does USDA have guidance regarding the Servicemembers Civil Relief Act (SSRCA)? Yes. 3555.252 and HB 17.2 K Can insurance payments for claims filed by the homeowners be released to them? Yes, if the criteria in HB 17.2 E is met. At this time released funds may not exceed $10,000. Are there monthly and quarterly reporting requirements for guaranteed loans? Yes. 3555.252(d), HB 17.3 A, B, C, D and E and Appendix 8

3555.253: Late payment charges 17.2: Required Servicing Actions What is the maximum late fee a lender may charge to a borrower for late payments? The maximum amount may not exceed the percentage of the payment due as prescribed by HUD, Fannie Mae or Freddie Mac. 3555.253(a) and HB 17.2 B

3555.254: Final payments 17.2: Required Servicing Actions

3555.255: Borrower actions requiring lender approval

17.7: Partial Release of Security17.9: Mineral Leases

Can the borrower sell part of the land associated with a loan post loan closing? Yes if the criteria of HB 17.7 is met. 3555.255(b) How must funds be distributed from a partial release sale? Please refer to 3555.255(b)(6) and HB 17.7 A 2 Does USDA allow approval of mineral leases? Yes if the criteria in 3555.255(a) and HB 17.9 are met.

3555.256: Transfer and assumptions

17.8: Transfer and Assumption Is USDA approval required for a transfer and assumption? Yes. 3555.256(b) and HB 17.8 B

3555.208: Manufactured homes

(continued)

20

3555.257: Unauthorized assistance 17.10: Unauthorized Assistance1.11: Unauthorized Assistance

Subpart G: Servicing Non‐Performing Loans 7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ’s

3555.301: General servicing techniques

18.1: Introduction18.3: Minimum Requirements 18.4: Documentation Requirements and Penalties

Are property inspections required while the property is delinquent? Yes. 3555.301(f) and HB 18.3 D Can a delinquent loan be expedited to foreclosure if it is abandoned? Yes. If the loan is delinquent, expedite foreclosure by referring the loan for acceleration within 15 days of the date of the inspection report confirming the vacancy. 3555.301(g) and HB 18.3 D What are the minimum requirements that must be met prior to proceeding with liquidation? 3555.306 and HB 18.3 E and 18.6 What collection records must the lender retain? 3555.301 and 18.4 A May penalties be assessed if a lender does not complete required collection actions? Yes. 3555.301, 3555.355(a)(1) and HB 18.4 B and C Can loss claims be denied or accrued interest reduced if servicing requirements are not met? Yes. 3555.301, 3555.355(a) and HB 18.4 C

3555.302: Protective advances 17.4: Protective Advances Are protective advances for emergency expenses allowed to protect the property? Yes. 3555.302(b) and HB 17.4 Are protective advances allowed for repairs? Yes. 3555.302(b) and HB 17.4 A Are protective advances allowed for taxes and insurance? Yes. 3555.302(a) and HB 17.4 B Can the lender approve protective advances for property repairs without USDA concurrence? Protective Advances that exceed $2,000 require USDA approval. 3555.302(b) and HB 17.4 A

21

3555.303: Traditional servicing options

18.5: Loss Mitigation Options Loss Mitigation Guide

All responses for this section contain additional information in HB 18.5 and the Loss Mitigation Guide

Is there a “waterfall” of servicing options that must be considered by the lender? Yes. 3555.303(b), HB 18.5 Does USDA offer Special forbearance agreements? Yes. 3555.303(b)(2), HB 18.5 What costs may be capitalized into a loan modification? 3555.303(b)(3)(ii), HB 18.5 What is an acceptable new loan term for a loan reamortization? Up to 30 years may be acceptable. 3555.303(b)(3)(iii), HB 18.5 Are there checklists available to assist lenders to determine borrower eligibility for servicing options? Yes. Loss Mitigation Guide

3555.304: Special servicing options 18.5: Loss Mitigation OptionsLoss Mitigation Guide

All responses for this section contain additional information in HB 18.5 and the Loss Mitigation Guide

Can special loan servicing options be utilized first? No. 3555.304(a) What are the target ratios when special loan servicing is utilized? The borrower’s total debt ratio must not exceed 55%. When a Mortgage Recovery Advance is utilized, the deferment is limited to an amount which achieves a total PITI ratio of 31% of gross monthly income. 3555.304(b)(1), 3555.304(d)(3) Can lender imposed late charges or fees be capitalized in special loan servicing options? No. 3555.304(b)(4) Are extended loan term modifications a servicing option? Yes. A repayment term of up to 40 years may be eligible. 3555.304(c) Can an extended term loan modification be used in conjunction with a mortgage recovery advance? Yes. Loss mitigation options may be layered as appropriate in order to assist a borrower to remain successfully in the home. 3555.304(c)(4) Is there a maximum amount allowed for a mortgage recovery advance? Yes, 30% of the unpaid principal balance as of the date of default. 3555.304(d)(2)

22

3555.305: Voluntary liquidation 18.5: Loss Mitigation OptionsLoss Mitigation Guide

When can a pre‐foreclosure sale/foreclosure be considered? Lenders must exhaust all traditional and special loan servicing options. 3555.305 If the borrower has abandoned the property refer to 3555.306

3555.306: Liquidation 18.6: Acceleration18.7: The Foreclosure Process 18.8: Managing the Foreclosure Process 18.13: Debt Settlement Reporting 19.2: Property Management Methods and Activities 19.3: Environmental Hazards 19.4: Property Dispositions Attachments 18‐A and 18‐B and 19‐A

Do state lending laws affect foreclosure timeframes required by USDA? Yes. Attachment 18‐A Is there guidance for lenders regarding a bid at the foreclosure sale? Yes. 3555.306(b)(3) and HB 18.7 B When can a mortgage account be reinstated? Unless required otherwise by State statute, the lender may reinstate an accelerated account if they meet 3555.306(c) and HB 18.7 C When a borrower has filed bankruptcy protection, when can a foreclosure be initiated? Within 90 calendar days once it is possible do so. 3555.306(b)(1), HB 18.8 A and Attachment 18‐A Are there guidelines for acceptable liquidation costs and fees? Yes. HB 18.8 B and Attachment 18‐B Where is information regarding maintaining a REO property? 3555.306(e) and HB 19.2 Are broker price opinions (BPO’s) acceptable for liquidation values? No, only appraisals. 3555.306(f) and HB 19.4 Is accrued interest allowed as an expense? Interest expenses accrued beyond 90 days of the foreclosure sale date or expiration of any redemption period is the not covered by the guarantee. 3555.306(f)(3) and HB 20.2 B Does USDA offer a “cash for keys” option? Yes. 3555.306(f) and HB 19.4 What is the correct REO date on the property disposition plan (PDP)? The date the lender acquired the title to the property. HB 19.1, 19.4 A and Attachment 19‐A Where do lenders report debt settlements? Lenders must report to the IRS and all national credit reporting repositories. 3555.306(g) and HB 18.13

23

3555.307: Assistance in natural disasters

18.10: Property Protection18.11: Special Relief Measures 18.12: Property Damage and Insurance Claims

Are special relief measures available for dwellings located in natural disasters? Yes. 3555.307(c) and HB 18.11 Do insurance claims have to be applied to principal loan balance? Yes, if the property will not be repaired or rebuilt. 3555.307(d) and HB 18.12

Subpart H: Collecting on the Guarantee7 CFR Part 3555 HB‐1‐3555 Reference Response to FAQ’s

3555.351: Loan guarantee limits 20.1: Overview20.2: Loss Claim Coverage

Is there an explanation of how the 90 percent loan note guarantee is calculated? 3555.351(b) and HB 20.2 A

3555.352: Loss covered by guarantee

20.2: Loss Claim Coverage Is there an explanation of the loss covered by the loan note guarantee including accrued interest? Accrued interest up to 90 days from the settlement date through the date the loss claim is paid is an eligible loss. 3555.352(a) and (b) and HB 20.2 B What is considered a reasonable cost that is covered under the loan note guarantee? 3555.352(c), (d) and (e) and HB 20.2 B, and C

3555.353: Net recovery value 20.2: Loss Claim Coverage 20.4: Calculating Net Recovery Value

Is there a timeframe loss claims for unsold REO properties must be filed by the lender to USDA? Claims must be filed within 30 days of obtaining liquidation value. 3555.353(b) and HB 20.2 C 2 Is there assistance to calculate actual net recovery value? 3555.353(a) and HB 20.4 A Is there assistance to calculate anticipated net recovery value? 3555.353(b) and HB 20.4 B

3555.354: Loss claim procedures 20.3: Filing a Loss ClaimAttachment 20‐A

Once the property is sold how many days before the claim must be submitted to USDA? 45 days. 3555.354 and HB 20.3 A Is there guidance for filing a loss claim for unsold REO properties? 3555.354(b) and HB 20.3 B Where is guidance to obtain a liquidation appraisal value for an unsold REO property? 3555.354(b)(2), HB 20.3 C and Attachment 20‐A

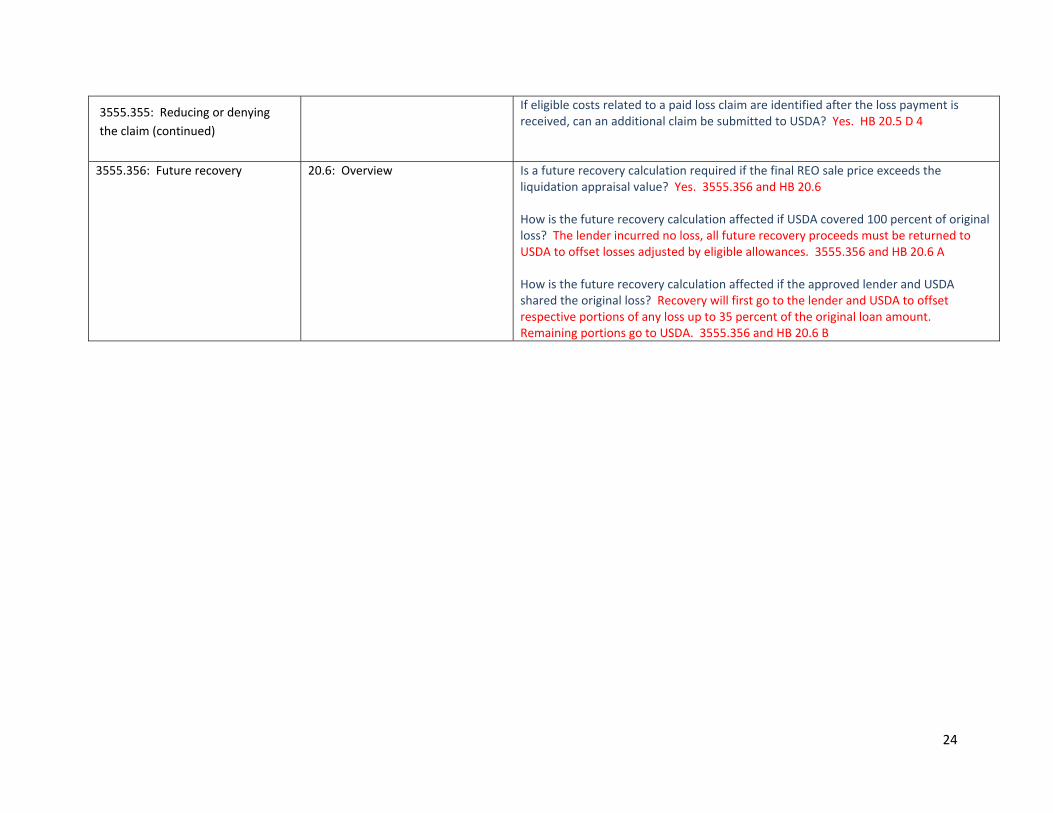

3555.355: Reducing or denying the claim

20.5: Agency Review Appendix 9

What factors may lead to the reduction or denial of a loss claim? 3555.355(a) and HB 20.5 Can the lender dispute the amount that is paid by USDA on a loss claim? Yes. 3555.355(b), HB 20.5 D 3 and Appendix 3

24

If eligible costs related to a paid loss claim are identified after the loss payment is received, can an additional claim be submitted to USDA? Yes. HB 20.5 D 4

3555.356: Future recovery 20.6: Overview Is a future recovery calculation required if the final REO sale price exceeds the liquidation appraisal value? Yes. 3555.356 and HB 20.6 How is the future recovery calculation affected if USDA covered 100 percent of original loss? The lender incurred no loss, all future recovery proceeds must be returned to USDA to offset losses adjusted by eligible allowances. 3555.356 and HB 20.6 A How is the future recovery calculation affected if the approved lender and USDA shared the original loss? Recovery will first go to the lender and USDA to offset respective portions of any loss up to 35 percent of the original loan amount. Remaining portions go to USDA. 3555.356 and HB 20.6 B

3555.355: Reducing or denying

the claim (continued)

25

RESOURCES USDA Income and Property Eligibility: Determine property and income eligibility http://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do Guaranteed Loan Coordinator Contacts: Find the contact for your state: https://eligibility.sc.egov.usda.gov/eligibility/welcomeActiondo?pageAction‐GetRHContact&NavKey‐contact@12 Regulations and Guidance: Only official publications and forms authorized by the National Office may be required and utilized for the nationwide delivery of the SFHGLP. There are no USDA forms published or required specific to the submission of credit waivers, debt ratio waiver requests, compensating factor identification, property inspections or payment shock. Regulations and Guidance Home Page: http://www.rurdev.usda.gov/RegulationsAndGuidance.html 7 CFR Part 3555: https://rurdev.usda.gov/rd_instructions.html HB‐1‐3555: https://www.rurdev.usda.gov/Handbooks.html#hb355501 Forms: http://forms.sc.egov.usda.gov/eForms/searchAction.do?pageAction=BrowseForms&_MenuAction=Yes USDA LINC: Access GUS, submit SFHGLP monthly and quarterly status reports, submit/monitor loss mitigation plans and loss claims, and submit payment of annual fees. https://usdalinc.sc.egov.usda.gov USDA LINC: Training and Resource Library: Access online training, support documents and resources for loan origination and servicing. https://usdalinc.sc.egov.usda.gov/USDALincTrainingResourceLib.do ListServ: Sign up to receive program updates by email for origination, servicing and/or GUS. http://www.rdlist.sc.egov.usda.gov/listserv/mainservlet USDA ITS Service Desk Support Center: For e‐Authentication assistance: Email: [email protected], or call 1‐800‐457‐3642, option 1 (USDA e‐Authentication Issues) Rural Development Help Desk: For GUS system outage or functionality assistance: Email: [email protected], or call 1‐800‐457‐3642, option 2 (USDA Applications) and then option 2 (Rural Development)

1

Single Family Housing Guaranteed Loan Program

Quick Reference

For a full explanation in locating the references provided, refer to the last page.

Topic 7 CFR 3555 HB‐1‐3555

7 CFR Part 3555 Appendix 1

A

Abandoned or Vacant Property 3555.302 19.2 A

Account Acceleration 3555.306 18.6

Acceptable Lien Position 3555.204 16.10

Adjusted Annual Income 3555.152(c) 3555.10 (definition)

9.5 See “Income” for more details

Adoption Assistance 3555.152(a) 9.10 A 11

Agency and Employee Addresses Appendix 4

Agency Review of Annual Income 3555.107(c) 9.6 Attachment 9‐F

Agency Review of Repayment Income

3555.107(c) 9.8 Attachment 9‐F

Alimony 3555.152(a) 9.10 A 7

Annual Income 3555.152(b) 3555.10 (definition)

9.3 Attachment 9‐C

Annual Fee 3555.107(h) 16.5

Appeals 3555.4 1.7 Appendix 3

Appraisals 3555.107(d) 12.5

Appraisal Forms 3555.107(d) 12.5 B

Appraisal Transfer 3555.107(d) 12.5 B

Appraisal Update 3555.107(d) 12. 5 B

Appraisal Remote Areas 3555.107(d) 12.5 F

Assets 3555.152(d) 9.3 D: Annual income 9.4: Calculation

Assumption of Loans 3555.256 17.8 A, B and C

Authorized User Accounts 3555.151(i)(6) 10.12

Automobile Allowance 3555.152(a) 9.10 A 13: Repayment income 11.2 B: Debt ratio

Automated Underwriting 3555.107(b) 5.3

B

Balloon Obligations 3555.151(h) 11.2 B

Bankruptcy: Chapter 13 3555.151(i)(3)(ii) 10.7 A Attachment 10‐B

2

Bankruptcy: Chapter 7 3555.151(i)(3)(ii) 10.7 A Attachment 10‐B

Bankruptcy: Chapter 7 discharged with foreclosure pending

3555.151(i)(3)(ii) Attachment 10‐B

Bankruptcy: Servicing 3555.306(d) 18.8 A

Bonus/Overtime Income 3555.152(a) and (b) 9.10 A 1: Repayment income 9.3 E: Verification

Business Debts 3555.151(h) 11.2 B

C

CAIVRS 3555.151(i)(5) 10.2: Credit eligibility 15.2: Loan application Appendix 7

Cash on Hand 3555.152(d)(1)(ii) and 3555.152(d)(2)(ii)

9.4 A

Certificate of Deposit (COD) 3555.152(d)(1) 9.4 A

Charge Off Accounts 3555.151(i) 10.9

Childcare Expenses 3555.152(c)(2) 9.5 B Adjusted income 11.2 B Debt ratios

Child Support 3555.152(a) 9.10 A 7 Annual income 11.2 B Debt ratios

Cisterns 3555.201(b)(4) 12.6 A 1

Citizenship and Immigration Status

3555.151(b) 8.2 F

Civil Rights 3555.3 1.6

Closing Costs 3555.101(b)(6)(vii) 6.2 C: Eligible costs 6.3: Prohibited costs

Closing Date 3555.10 (“Settlement Date definition)

16.7

Closing Documentation 3555.107(f) 16.2, 16.3 Attachment 16‐A

CLTV 3555.103 7.2

Collection and Charge Off Accounts: Credit Analysis

3555.151(i) 10.9

Collection and Charge Off Accounts: Capacity Analysis

3555.151(h) and (i) 10.9: Capacity Analysis 11.2 B: Debt Ratio

Collection Efforts: Servicing 3555.252: Required servicing 3555.301: Delinquent accounts

17.2: Required servicing 18.2‐18.4: Delinquent accounts

Combination Construction Permanent Loans

3555.105 12.13 – 12.29

Commission Income 3555.152(a) and (b) 9.10 A 2: Repayment Income 9.3 E: Verification

Community Land Trusts 3555.206 13.3

Compensating Factors (Debt Ratio Waivers)

3555.151(h)(2) 11.3 A

3

Complete Loan Application 3555.107 15.3 Attachment 15‐A

Compliance Reviews 3555.51(b)(19) 3.8

Condominium 3555.205 12.11 A

Co‐Signed Debts: Non‐Mortgage 3555.151(h) 11.2 B

Co‐Signed Debts: Mortgage 3555.151(h) 11.2 B

Co‐Signors 3555.152(a) 9.9

Conditional Commitment 3555.107(f) 15.6

Conditional Commitment: Lender Response

3555.107(f) 15.8

Conventional Credit 3555.151(e)(4) 8.2 B

Credit Inquiries 3555.151(h) and 3555.151(i) 10.3 B

Credit Report 3555.151(i) 10.3

Credit Report Versions 3555.151(i) 10.4

Credit Report: NPS 3555.151(i)(7) 10.15

Credit Scores 3555.151(i) 10.7 Attachment 10‐A

Credit Score Validation 3555.151(i)(3) 10.5

Credit: Derogatory 3555.151(i)(3) 10.7 A

Custodial Property 3555.306(f) 19.1 ‐19.4

D

Debt Ratio Waivers 3555.151(h)(2) and (3) 11.3 A

Deed‐in‐Lieu of Foreclosure 3555.305(c) 18.5 Loss Mitigation Guide

Deed of Trust 3555.107(i) 16.3

Default Counseling 3555.301 18.2 Loss Mitigation Guide

Deferred Obligations (does not apply to student loans)

3555.151(h) 11.2 B

Deductions to Annual Household Income

3555.152(c)(1): Dependents 3555.152(c)(2): Childcare expenses 3555.152(c)(3): Disability care 3555.152(c)(4): Elderly family 3555.152(c)(5): Medical expenses

9.5 A 9.5 B 9.5 D 9.5 C 9.5 E

Delinquency Reporting 3555.51(b)(8) and 3555.301 18.9 Appendix 8

Dependents: Unborn Child 3555.10 “Household” definition 9.3 E 1

Dependents: Shared Custody 3555.10 “Household” definition 9.3 E 1

Depository Accounts 3555.152(d)(1)(ii) 9.4 A

Discount Points 3555.101(b)(6)(iv) and 3555.102(d)

6.3

Disputed Credit Accounts 3555.151(h) 10.11

Dividends 3555.152(a) 9.10 A 8

4

Duplicate Loan Note Guarantee 3555.107 16.8

E

Early Delinquent Loans 3555.301 18.5 Loss Mitigation Guide

Earned Income Tax Credit 3555.152(b)(5)(vii) 9.3 A

Earnest Money 3555.152(d)(1) 9.4 A

EDI Documentation: Monthly & Quarterly Reporting and Delinquency Reporting

3555.301 17.3 Appendix 8

EDI Access Appendix 8

Electronic Signatures 3555.51(b) and 3555.107(i)(2) 15.4

Electronic Verification of Employment

3555.152(a) 9.3 E 3

Eligible Areas 3555.201(a) 12.3

Eligible Loan Purposes 3555.101(a) 6.1 and 6.2 A, B, D and E

Eligible Loan Costs 3555.101(b) 6.2 C

Employer Differential Payments/Housing Allowances

3555.152(a) 9.10 A 9

Energy Saving Measures 3555.101(b)(2) 6.2 C

Environmental Requirements 3555.5 12.10

Escrow Accounts: Exterior 3555.202(c) 12.9 C

Escrow Accounts: Interior 3555.202(c) 12.9 D

Escrow Accounts: No Contractor 3555.202(c) 12.9 E

Escrowed Work Completion 3555.202(c) 12.9

Existing Dwelling Requirements: Minimum Property Standards Termite Thermal

3555.202(b) 12.9 A

Expiration of Credit Documents 3555.107(i) 120 days, must be valid at loan closing GUS: 5.3 A Income documents: 9.3 E Credit documents: 9.3 E 4 Credit report: 10.3 B Appraisal: 12.5 B Water/Septic/Termite: 12.6 A 1 Age of documents: 12.22

Extended term loan modification 3555.304(c) 18.5 Loss Mitigation Guide

F

Family Owned Business Employment

3555.152(a) 9.10 B

Federal Debts 3555.151(i)(5) 10.2 and 10.8: Credit 15.2: Verification

Fee Simple 3555.203(a) 16.11 B 1

5

FEMA Flood Elevation Certificate: New/Proposed Dwelling Only

3555.5(d)(7) 12.10 B

Flood Insurance Existing dwellings: 3555.151(d)(5) New/proposed dwellings: 3555.151(d)(7)

12.10 B

Flood Insurance Deductibles 3555.5(d)(5 and (7) 12.6 B

Foreclosure: Adverse Credit 3555.151(i)(3)(i) 10.7 A Attachment 10‐B

Foreclosure: Liquidation 3555.306(b) 18.7 and 18.8

Foreclosure: Acceptable Timeframes

3555.305(b)(1) 18.8 A Attachment 18‐A

Foreclosure: Acceptable Liquidation Costs and Fees

3555.305(b)(2) 18.8 B Attachment 18‐B

Forms 3555.107 Appendix 2

Foster Children/Adult Payments 3555.152(a)(4) 9.12

Funding Priorities 3555.107(a) 14.3

Future Recovery 3555.356 20.6

G

Gaps in Employment 3555.152(a)(1) 9.10

Garnishments 3555.151(h) 11.2 B

Gift Funds 3555.152(b)(5)(v) 9.3 E 1

Government Assistance Programs

3555.152(a) 9.10 A 11

Gross Up Non‐Taxable Income 3555.152(a) 9.10 A 4

Guaranteed Fee (Up‐Front) 3555.107(g) 16.4

Guaranteed Underwriting System (GUS)

3555.107(b) 5.3 Functionality: 5.3 A Gaining Access: 5.3 B UW Guidance for lenders: 5.3 C LOS/POS: 5.3 D Cash Reserves: 5.3 E Data Tolerances: 5.3 F UW Findings Report: 5.3 G Request Commitment: 5.3 H UW Recommendations: 5.3 I Lender Reliance: 5.3 J Lender File Docs: 5.3 K Resubmission Policy: 5.3 L Lender Representation: 5.3 M Termination: 5.3 N Attachment 15‐A

6

H

Hazard Insurance (non‐flood zones)

3555.107(e) and (i)(3) 16.11 C 1

Homeowner Association (HOA) fees

3555.151(h)(1)(i) 11.2 B

Homeownership Vouchers (Section 8)

3555.152(a) 9.11 C

Homeownership Counseling 3555.101(b)(6)(v) 6.2 C

Housing Counseling Clearing House (HCC): Distressed Homeowners

3555.301 18.2 Glossary

HUD‐1 3555.107(i) 16.3

I

Income: Annual Income 3555.152(b) 9.3 Attachment 9‐C

Income: Adjusted Annual Income

3555.152(c) 9.5

Income: Repayment Income 3555.152(a) 9.10

Income Documentation Worksheet

3555.152 Attachment 9‐A Attachment 9‐B (Case Study)

Income Documentation Forms (optional for use)

3555.152 9.13 Attachment 9‐G

Income Limits 3555.151(a) Appendix 5

Incomplete Loan Applications 3555.107 15.6 C Attachment 15‐A

Incomplete Loan Closing Package 3555.107 16.6 A Attachment 16‐A

Indemnification 3555.107(d) 4.11

Informal Forbearance Plan 3555.303(b)(1) 18.5 Loss Mitigation Guide

In‐ground Pools 3555.201 12.9 A

Insurance 3555.251 Hazard: 16.11 C 1 Flood: 16.11 C 2

Insurance Proceeds: Servicing 3555.252(c)(2) 17.5

Interest Rate 3555.104(a) Purchase: 3555.104(a) Refinance: 3555.101(d)(3)(i)

7.3 6.2 D 3 a & Attachment 6‐A Combination Construction to Permanent: 12.13 Rural Refinance Pilot: Unnumbered Letter (UL) dated 1‐21‐2015

7

Interest and Dividends 3555.152(a) 9.10 A 8

IRS 4506‐T 3555.152(b)(3) 9.3 E

J

Judgments 3555.151(i)(5) Federal: Attachment 10‐B Non‐Federal: 10.10 Attachment 10‐B

K

L

Late Fees 3555.253 17.2 B

Leasehold 3555.203(b) 13.4: Requirements 16.11 B 2: Closing requirements

Legal Capacity 3555.151(f) 8.2 D

Lender Approval 3555.52 3.2 – 3.4 Attachment 3‐A

Lender Certification 3555.107(f) 16.6 Form RD 3555‐18

Lender Eligibility 3555.51 3.2

Lender Charges and Fees 3555.101(b)(6)(vii) 6.2 C

Lender Responsibilities 3555.51(b) Chapter 4

Liquidation: Voluntary 3555.305 18.5 Loss Mitigation Guide

Liquidation: Involuntary 3555.306 18.7

Liquidation Value Appraisal 3555.353 Loss Mitigation Guide

Loan Application Package 3555.107 15.2 ‐15.3 Attachment 15‐A

Loan Closing Date 3555.107(f) 16.7

Loan Closing Checklist: Lender 3555.107(i) Attachment 16‐A

Loan Note Guarantee 3555.107(g) 16.6 Form RD 3555‐17

Loan Modification 3555.303(b)(3) 18.5 Loss Mitigation Guide

Loan Purposes 3555.101(a) 6.2 A, B and D

Loan Term 3555.104 7.3

Long Term Liabilities 3555.151(h) 11.2 B

Loss Claims 3555.354 20.2 ‐20.5

M

Manufactured Homes 3555.208 13.5‐13.11 Attachment 13‐A Attachment 13‐B

8

Maximum Loan Amount 3555.103 7.2 Refinances: Attachment 6‐A Rural Refinance Pilot: UL 1‐21‐2015

Medical Expense Deductions 3555.152(c)(5) 9.5 E

Mineral Leases 3555.255(a) 17.9

Military Income 3555.152(a) 9.3 E 1: Verification 9.10 A 5: Repayment income

Modest Housing 3555.10 (definition) 3555.101

12.8

Modular Homes 3555.202 13.12

Monitoring: Lender 3555.51(b)(19) 3.8

Mortgage Credit Certificate 3555.152(h)(5) 9.10 A 16: Repayment income 9.11 A: Enhancing repayment 11.4: Ratios

Mortgage Fraud: Lender Prevention

3555.51(b)(20) 4.10

Mortgage Recovery Advance 3555.304(d) 18.5 Loss Mitigation Guide

N

Natural Disasters: Origination 3555.107(d), 3555.107(i)(2) 16.2 Form RD 3555‐18 “Lender Certification”

Natural Disasters: Servicing 3555.307 18.10 ‐18.13

Net Recovery: Actual (Sold Property)

3555.353(a) 20.4 A

Net Recovery: Anticipated (Unsold REO Property)

3555.353(b) 20.4 B

New Credit Charges 3555.151(h) 11.2 B

New Construction Dwellings 3555.202(a) 12.9 B

New Construction Dwellings: No evidence of plans/inspections/warranty

3555.103(c) 12.9 B

Newly Employed 3555.152 9.10 and 9.10 A

Non‐Purchasing Spouse (NPS) 3555.151(1)(h)(iv) 10.15: Credit history 11.2 B: Debt ratio inclusion 15.3: Credit report in loan application package 16.2: Closing the loan

O

Occupying the Property 3555.151(c) 8.2 C

Origination Checklist: Lender 3555.107 Attachment 15‐A

Outbuildings 3555.201(b) 12.4

Ownership Requirements 3555.203 16.11 B

Owning/Retaining a Dwelling 3555.151(e) 8.2 A

9

Overtime 3555.152(a)(2) 9.10 A 1

Owning a Dwelling 3555.151(e) 8.2 A

P

Partial Release of Security 3555.255(b) 17.7

Part‐Time Jobs 3555.152(a)(2) 9.10 A 3

Payment Shock 3555.151(h)(2) 10.14

Penalties: Servicing Non‐Compliance

3555.355 18.4 C, 20.5 Appendix 9

Personal Asset Loans/401(k) Loans

3555.151(h)(1)(iii) 11.2 B

Planned Unit Developments (PUD’s)

3555.207 12.11 B

Pre‐Foreclosure Sale 3555.305(b) 18.5 Loss Mitigation Guide

Previous Mortgage Loan 3555.151(h) 11.2 B

Previous USDA Mortgage Loan 3555.151(i)(3)(iv) 11.2 B

Projected Income 3555.152(a) 9.10 A 15

Promissory Note 3555.107(i) 16.3 Attachment 16‐A

Property Disposition Plan (PDP) 3555.306(f) 19.4 Attachment 19‐A

Protective Advances 3555.302 17.4

Purchase Agreement 3555.107(i) 15.3 Attachment 15‐A

Q

Qualified Alien 3555.151(b) 5.2 A, 8.2 F

R

Repayment Term 3555.104(b) and (c) 7.3 A

Ratios 3555.151(h) 11.2

Ratio Flexibility 3555.151(h)(2) – (7) 11.3 ‐11.6

Real Estate Owned (REO) Management

3555.306(e) and (f) 19.1 – 19.4

Record Retention: Lenders 3555.51(b)(21) 2.2

Record Retention: USDA RD Instruction 2033‐A 2.3 Attachment 2‐A

Recent/Undisclosed Debts 3555.151(h) Attachment 10‐B

Rent Verification 3555.151(i) 10.13

Retirement Income/ Accounts 3555.152(a) and (d)(2)(v) 9.4 B: Asset consideration 9.10 A 6: Repayment income

Rental Income 3555.152(a) 8.2 A: Eligibility to retain 9.3 E 1: Verification 9.10 A 12: Repayment income

Revolving Credit 3555.151(h) 11.2 B

10

Refinances 3555.101(d) 6.2 D Attachment 6‐A

Remote Area Appraisals 3555.107(d) 12.5 F

Request a Loan Note Guarantee 3555.107(g) – (j) 16.1 – 16.11 Attachment 16‐A

Reserves 3555.151(h)(2)(iii) 9.3 E 1 GUS: 5.3 E

Repairs 3555.101(a)(3) 6.2 B

Reporting: Performing Loans 3555.51 17.3

Reporting: Non‐Performing Loans

3555.51 18.9

Reporting: Debt Settlement 3555.51 18.13

Revoking Lender Eligibility 3555.52(c)(1) 3.9

Road Maintenance Agreement 3555.201(b)(3) 12.7 B

Rural Area Determination 3555.201(a) 12.3 Attachment 12‐A

Rural Energy Plus Loans 3555.209 12.12

S

Sale of Guaranteed Loans 3555.54 3.5, 4.6, 4.11 B

Sale Proceeds 9.4 A

SAM 3555.151(g) 8.2 E: Applicant eligibility 15.2: Loan application

SAVE 3555.151(b) 8.2 F

Schedule of Standard Attorney Fees

3555.306(b)(2) 18.8 B Attachment 18‐B

Section 8 Homeownership Vouchers

3555.151(h)(6) 9.10 A 18: Repayment income 9.11 C: Enhancing repayment 11.6: Ratios

Self‐Employed Applicants Annual Income: 3555.152(b) Repayment Income: 3555.152(a)

9.3 E 1, 9.10 C Attachment 9‐E

Seller Concessions 3555.101(b)(6)(xii), 3555.102(h) 6.3

Septic/Wastewater 3555.201(b)(4) 12.6 B

Servicing: Performing Loans 3555.251, 3555.252 17.1 ‐ 17.5

Servicing: Non‐Performing Loans 3555.301 – 3555.306 18.1 – 18.9

Shared Well 3555.201(b)(4) 12.6 A 2

Short Sale 3555.151(i) 10.7 A Attachment 10‐B

Site 3555.201(b) 12.4

Social Security Income 3555.152(a) 9.10 A 6

Special Forbearance Plan 3555.303(b)(2) 18.5 Loss Mitigation Guide

Special Loan Servicing 3555.304 18.5 Loss Mitigation Guide

Stable and Dependable Income 3555.152(a) 9.10

State Supplements 3555.6 Appendix 10

11

Street Access 3555.201(b)(3) 12.7 A

Student Loans 3555.151(h)(1)(i) 11.2 B

Suspension and Debarment 3555.151(g) 8.2 E

T

Termite: Existing 3555.202(b) 12.9 A

Termite: New 3555.202(a) 12.9 B

Temporarily Absent Family Members

3555.152(b)(4) 9.3 C

Temporary Interest Rate Buydowns

3555.152(h)(7) 9.11 B: Enhancing repayment 11.5: Ratios

Thermal Requirements: Existing 3555.202(b) 12.9 A

Thermal Requirements: New 3555.202(a) 12.9 B

Tip Income 3555.152(a) 9.10 A 17

Title Policy 3555.107(i), 3555.203, 3555.204 16.11

Termination of GUS Lender 3555.107(3) 5.3 N

Transfer and Assumption: Transfer without Assumption

3555.256(a) 17.8 D

Transfer and Assumption: Transfer with Assumption

3555.256(b) 17.8 B

Transfer and Assumption: Transfer without Approval

3555.256(c) 17.8 A

Transfer and Assumption: Transfer without due‐on‐sale clause

3555.256(d) 17.8 C

Trust Income 3555.152(a) 9.10 A 14

U

Unauthorized Assistance 3555.257 1.11: Program requirement 17.10: Servicing

Unborn Child 3555.10 “Household” definition 9.3 E 1

Unemployment Income 3555.152(a)(2) 9.3 E 1: Verification 9.10 A 3: Repayment income

Underwriting Analysis 3555.107(c) Attachment 15‐A

Up‐Front Guarantee Fee 3555.107(g) 16.4

Uniform Residential Loan Application (URLA)

3555.107(i) 15.3 Attachment 15‐A

Underwriting Analysis FNMA 1008/FHLMC 1077)

3555.107(c) 11.3 A: Ratio waiver 15.2, 15.3: Loan application Attachment 15‐A

Underwriting Responsibility 3555.51(b)(3) 4.8, 15.2

Unreimbursed Expenses 3555.152 9.3 E 1: Annual income 9.10 A 19: Repayment income

12

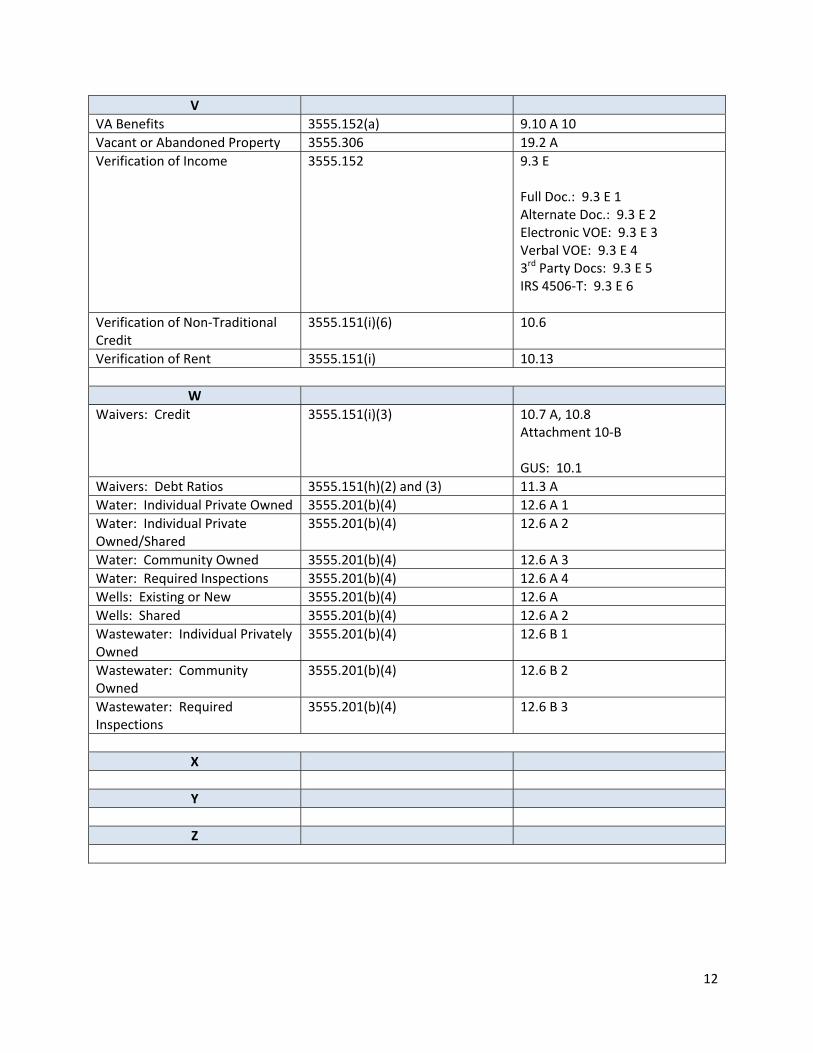

V

VA Benefits 3555.152(a) 9.10 A 10

Vacant or Abandoned Property 3555.306 19.2 A

Verification of Income 3555.152 9.3 E Full Doc.: 9.3 E 1 Alternate Doc.: 9.3 E 2 Electronic VOE: 9.3 E 3 Verbal VOE: 9.3 E 4 3rd Party Docs: 9.3 E 5 IRS 4506‐T: 9.3 E 6

Verification of Non‐Traditional Credit

3555.151(i)(6) 10.6

Verification of Rent 3555.151(i) 10.13

W

Waivers: Credit 3555.151(i)(3) 10.7 A, 10.8 Attachment 10‐B GUS: 10.1

Waivers: Debt Ratios 3555.151(h)(2) and (3) 11.3 A

Water: Individual Private Owned 3555.201(b)(4) 12.6 A 1

Water: Individual Private Owned/Shared

3555.201(b)(4) 12.6 A 2

Water: Community Owned 3555.201(b)(4) 12.6 A 3

Water: Required Inspections 3555.201(b)(4) 12.6 A 4

Wells: Existing or New 3555.201(b)(4) 12.6 A

Wells: Shared 3555.201(b)(4) 12.6 A 2

Wastewater: Individual Privately Owned

3555.201(b)(4) 12.6 B 1

Wastewater: Community Owned

3555.201(b)(4) 12.6 B 2

Wastewater: Required Inspections

3555.201(b)(4) 12.6 B 3

X

Y

Z

13

Locating 7 CFR Part 3555 and HB‐1‐3555 References

Example: 3555.208(b)(3)(i)

Example HB: 12.6 A 1

7 CFR Part 3555 Section 3555.208

3555.208(b)

3555.208(b)(3)(i)

3555.208(b)(3)

HB‐1‐3555 Chapter 12

Paragraph 12.6

12.6 A

12.6 A 1