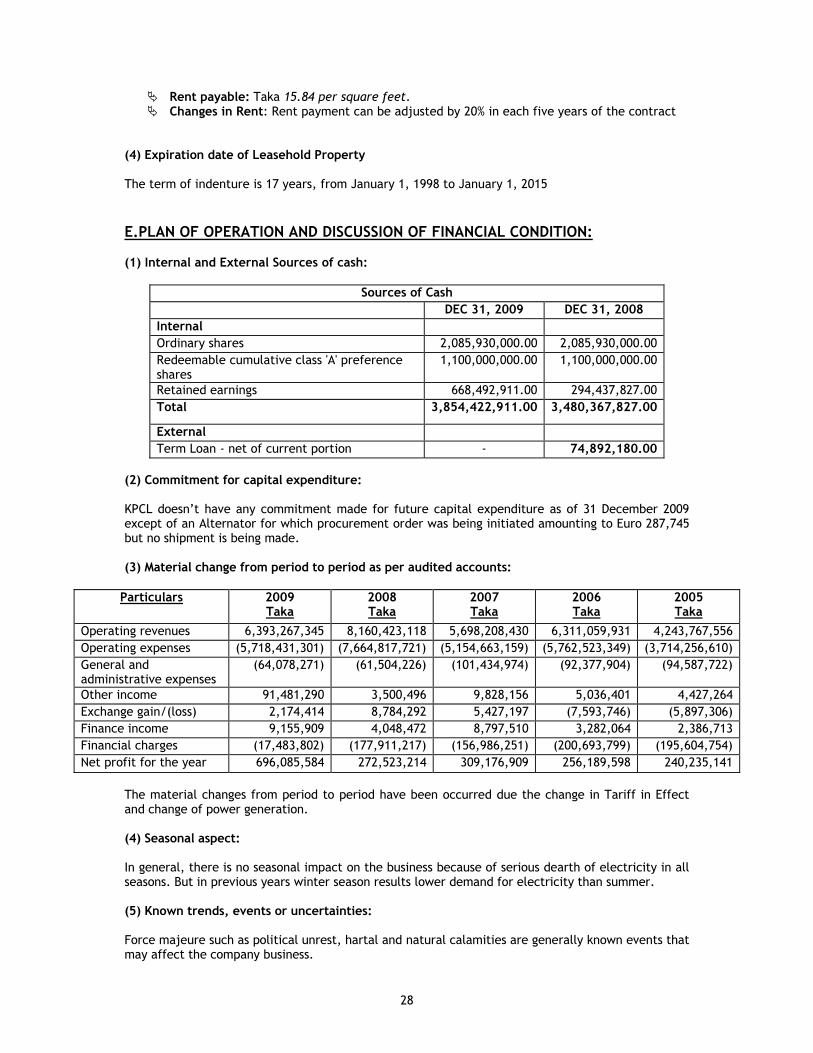

im- word file-final corrected version-21-3-2010 - dsebd.org dhaka electric supply company ltd. dse...

TRANSCRIPT

Information Document for

Direct Listing in DSE & CSE of

Khulna Power Company Ltd. Corporate Office: Summit Centre (5th Floor),

18 Karwan Bazar C/A, Dhaka-1215, Bangladesh Phone: [+8802] 9132437-8; 8125142; 8125433;

Fax: [+8802] 9125682; Website: www.khulnapower.com

Offloading of 5,21,48,250 Ordinary Shares of Tk 10.00 each

Listing Date: 15th March 2010 DSE & 18th March 2010 CSE

Indicative Price for Book Building Purpose Tk.162.00

Eligible institutional investors’ bidding on April 04, 05, 06, 2010

Manager to the Issue

Amin Court, 4th Floor (Suite # 404), 31 Bir Uttam Shahid Ashfaqueus Samad Road, Motijheel C/A, Dhaka-1000

Phone: +8802 9559602, +8802 9567726 Fax: +8802 9558330 Web-site: www.aaawebbd.com, e-mail: [email protected]

DATE OF THE INFORMATION DOCUMENT

18th March, 2010

Credit Rating Report by Credit Rating Information and Services Limited (CRISL)

Long Term Short Term

Entity Rating AA ST-1

Outlook Stable Date of Rating 16 September, 2009

“CONSENT OF THE EXCHANGES HAS BEEN OBTAINED TO THE ISSUE/OFFER OF THESE SECURITIES UNDER THE DHAKA STOCK EXCHANGE & CHITTAGONG STOCK EXCHANGE (DIRECT LISTING) REGULATIONS, 2006. IT MUST BE DISTINCTLY UNDERSTOOD THAT IN GIVING THIS CONSENT THE EXCHANGES DO NOT TAKE ANY RESPONSIBILITY FOR THE FINANCIAL SOUNDNESS OF THE COMPANY, ANY OF ITS PROJECTS OR THE ISSUE PRICE OF ITS SHARE OR FOR THE CORRECTNESS OF ANY OF THE STATEMENTS MADE FOR OPINION EXPRESSED WITH REGARD TO THEM. SUCH RESPONSIBILITY LIES WITH THE ISSUER, ITS DIRECTORS, CHIEF EXECUTIVE OFFICER/ CHIEF FINANCIAL OFFICER, ISSUE MANGER AND/OR AUDITOR. “THE MONEY (PROCEEDS) AGAINST SALE OF SHARES THROUGH THIS INFORMATION DOCUMENT WILL BELONG TO THE SPONSORS/SHAREHOLDERS CONCERNED. THE COMPANY WILL NOT GET THIS MONEY.”

“If you have any queries about this document, you may consult issuer, issue managers.”

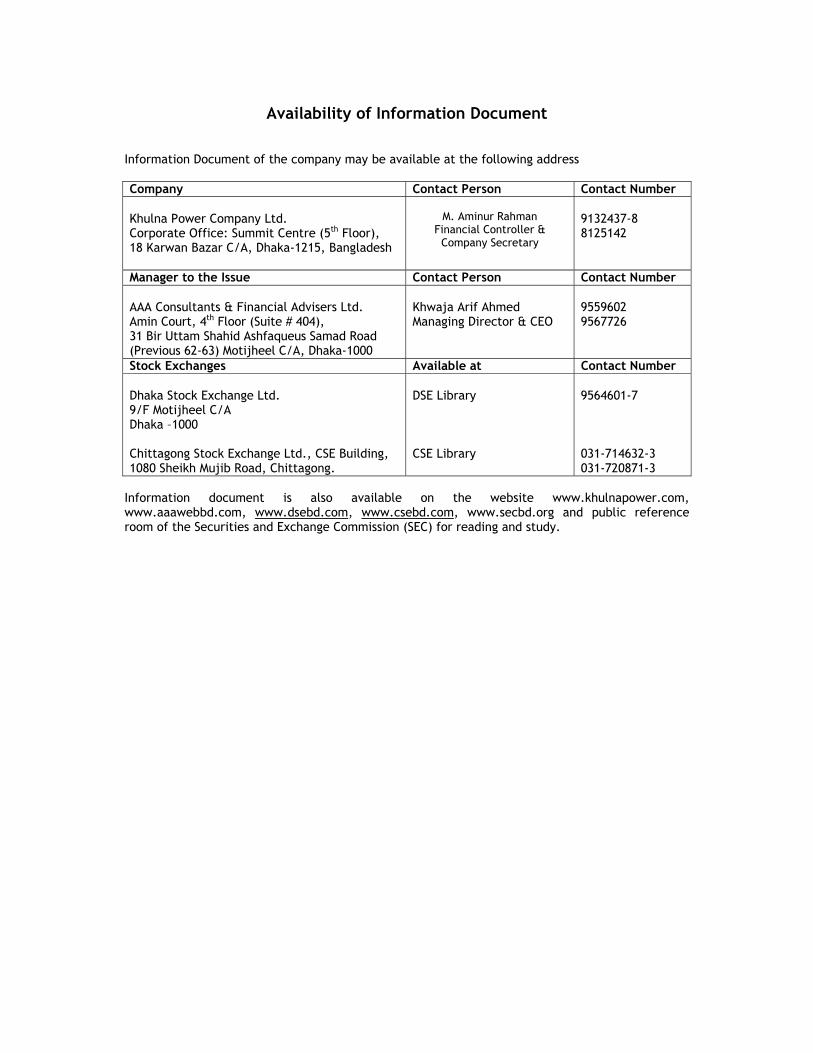

Availability of Information Document

Information Document of the company may be available at the following address Company Contact Person Contact Number Khulna Power Company Ltd. Corporate Office: Summit Centre (5th Floor), 18 Karwan Bazar C/A, Dhaka-1215, Bangladesh

M. Aminur Rahman

Financial Controller & Company Secretary

9132437-8 8125142

Manager to the Issue Contact Person Contact Number AAA Consultants & Financial Advisers Ltd. Amin Court, 4th Floor (Suite # 404), 31 Bir Uttam Shahid Ashfaqueus Samad Road (Previous 62-63) Motijheel C/A, Dhaka-1000

Khwaja Arif Ahmed Managing Director & CEO

9559602 9567726

Stock Exchanges Available at Contact Number Dhaka Stock Exchange Ltd. 9/F Motijheel C/A Dhaka –1000 Chittagong Stock Exchange Ltd., CSE Building, 1080 Sheikh Mujib Road, Chittagong.

DSE Library CSE Library

9564601-7 031-714632-3 031-720871-3

Information document is also available on the website www.khulnapower.com, www.aaawebbd.com, www.dsebd.com, www.csebd.com, www.secbd.org and public reference room of the Securities and Exchange Commission (SEC) for reading and study.

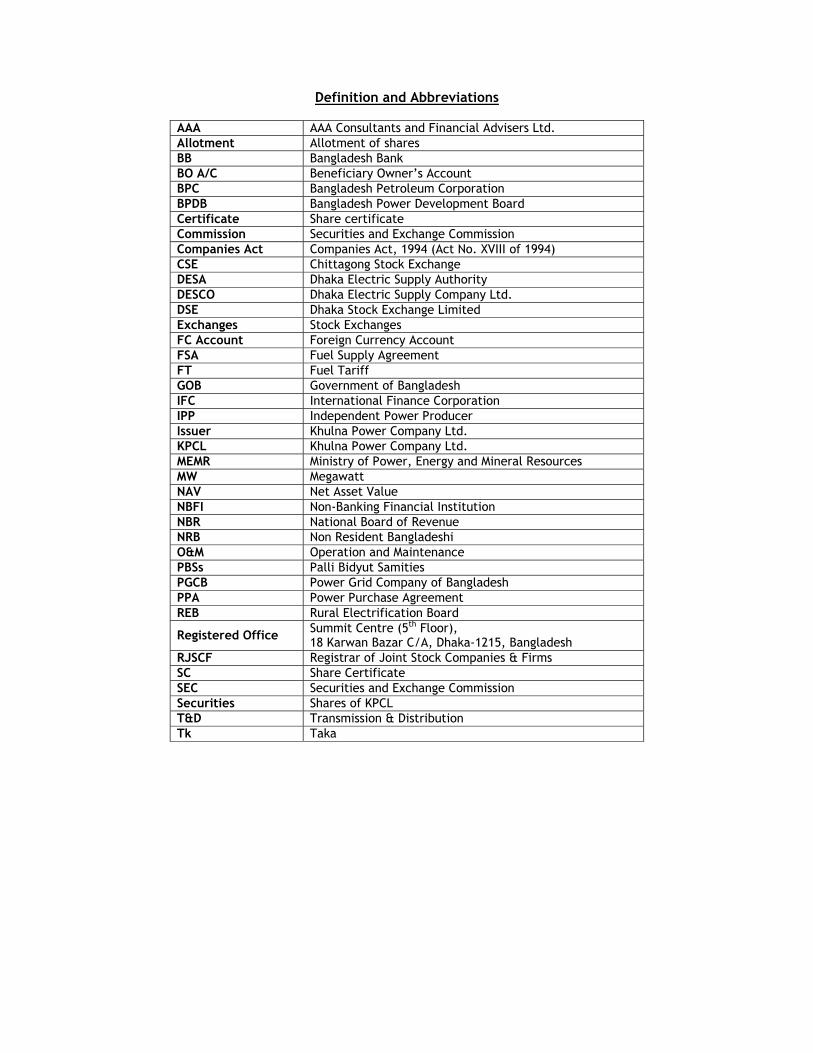

Definition and Abbreviations

AAA AAA Consultants and Financial Advisers Ltd. Allotment Allotment of shares BB Bangladesh Bank BO A/C Beneficiary Owner’s Account BPC Bangladesh Petroleum Corporation BPDB Bangladesh Power Development Board Certificate Share certificate Commission Securities and Exchange Commission Companies Act Companies Act, 1994 (Act No. XVIII of 1994) CSE Chittagong Stock Exchange DESA Dhaka Electric Supply Authority DESCO Dhaka Electric Supply Company Ltd. DSE Dhaka Stock Exchange Limited Exchanges Stock Exchanges FC Account Foreign Currency Account FSA Fuel Supply Agreement FT Fuel Tariff GOB Government of Bangladesh IFC International Finance Corporation IPP Independent Power Producer Issuer Khulna Power Company Ltd. KPCL Khulna Power Company Ltd. MEMR Ministry of Power, Energy and Mineral Resources MW Megawatt NAV Net Asset Value NBFI Non-Banking Financial Institution NBR National Board of Revenue NRB Non Resident Bangladeshi O&M Operation and Maintenance PBSs Palli Bidyut Samities PGCB Power Grid Company of Bangladesh PPA Power Purchase Agreement REB Rural Electrification Board

Registered Office Summit Centre (5th Floor), 18 Karwan Bazar C/A, Dhaka-1215, Bangladesh

RJSCF Registrar of Joint Stock Companies & Firms SC Share Certificate SEC Securities and Exchange Commission Securities Shares of KPCL T&D Transmission & Distribution Tk Taka

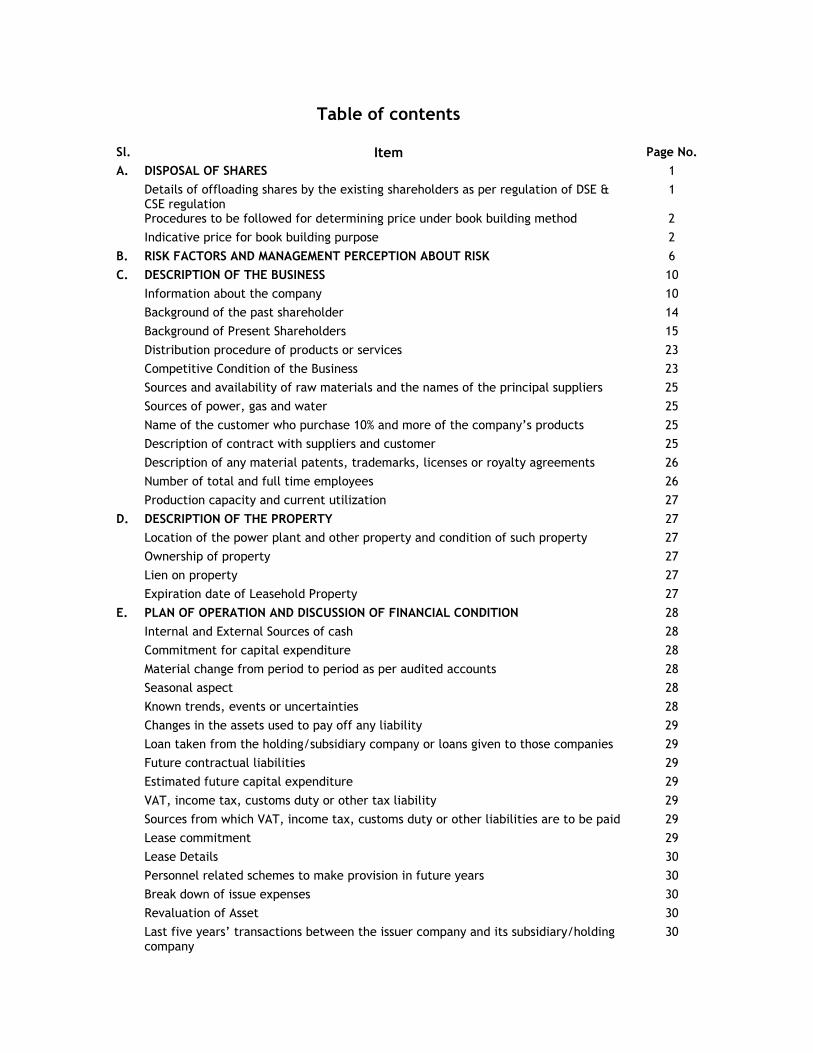

Table of contents

Sl. Item Page No. A. DISPOSAL OF SHARES 1 Details of offloading shares by the existing shareholders as per regulation of DSE &

CSE regulation 1

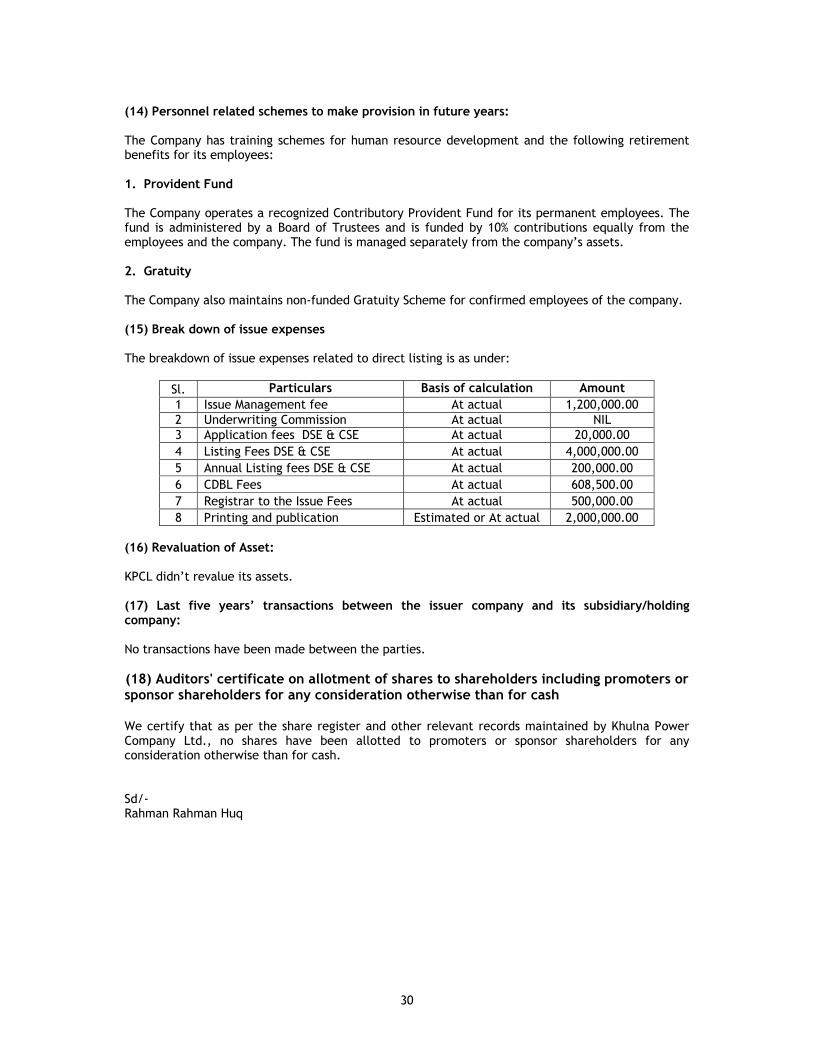

Procedures to be followed for determining price under book building method 2 Indicative price for book building purpose 2 B. RISK FACTORS AND MANAGEMENT PERCEPTION ABOUT RISK 6 C. DESCRIPTION OF THE BUSINESS 10 Information about the company 10 Background of the past shareholder 14 Background of Present Shareholders 15 Distribution procedure of products or services 23 Competitive Condition of the Business 23 Sources and availability of raw materials and the names of the principal suppliers 25 Sources of power, gas and water 25 Name of the customer who purchase 10% and more of the company’s products 25 Description of contract with suppliers and customer 25 Description of any material patents, trademarks, licenses or royalty agreements 26 Number of total and full time employees 26 Production capacity and current utilization 27 D. DESCRIPTION OF THE PROPERTY 27 Location of the power plant and other property and condition of such property 27 Ownership of property 27 Lien on property 27 Expiration date of Leasehold Property 27 E. PLAN OF OPERATION AND DISCUSSION OF FINANCIAL CONDITION 28 Internal and External Sources of cash 28 Commitment for capital expenditure 28 Material change from period to period as per audited accounts 28 Seasonal aspect 28 Known trends, events or uncertainties 28 Changes in the assets used to pay off any liability 29 Loan taken from the holding/subsidiary company or loans given to those companies 29 Future contractual liabilities 29 Estimated future capital expenditure 29 VAT, income tax, customs duty or other tax liability 29 Sources from which VAT, income tax, customs duty or other liabilities are to be paid 29 Lease commitment 29 Lease Details 30 Personnel related schemes to make provision in future years 30 Break down of issue expenses 30 Revaluation of Asset 30 Last five years’ transactions between the issuer company and its subsidiary/holding

company 30

Auditors certificate on allotment of shares to shareholders including promoters and sponsor shareholders for any consideration otherwise than for cash

30

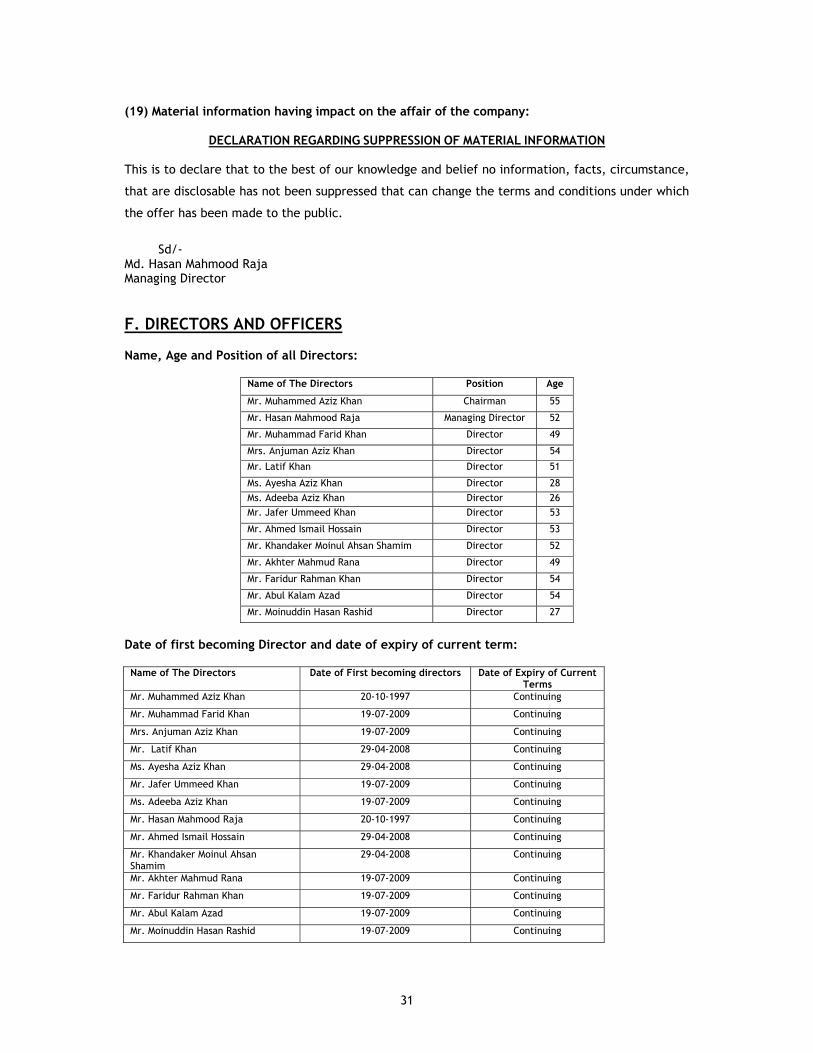

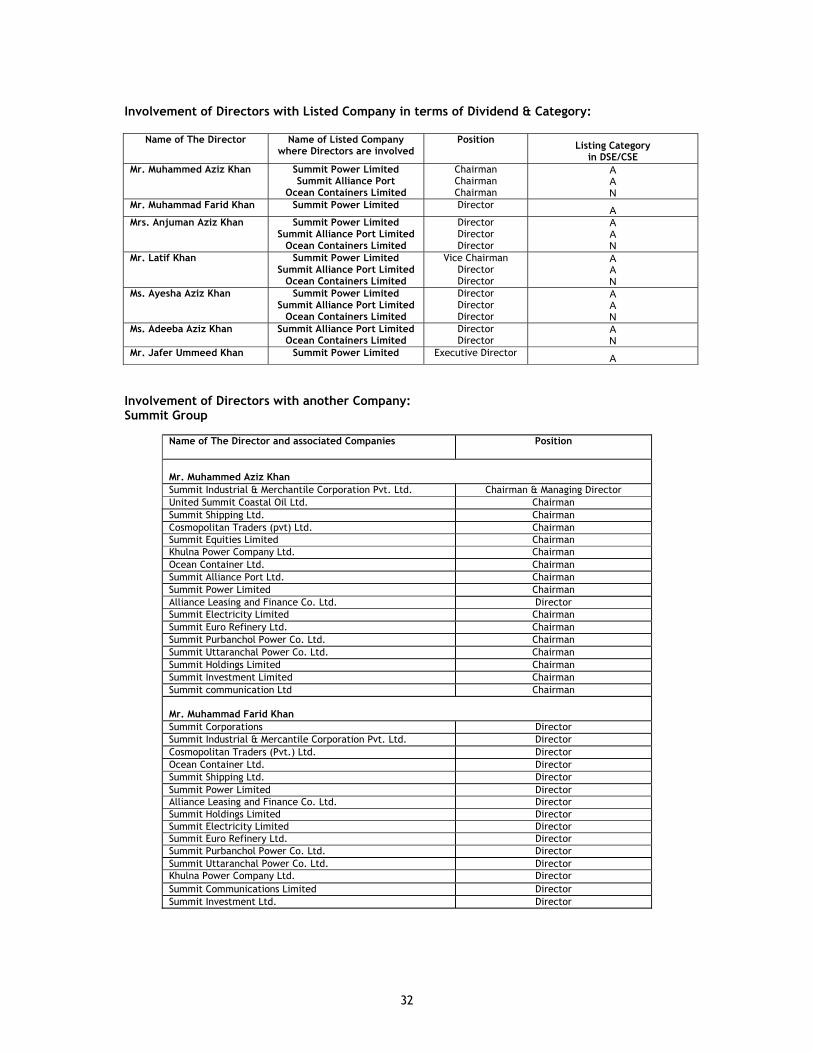

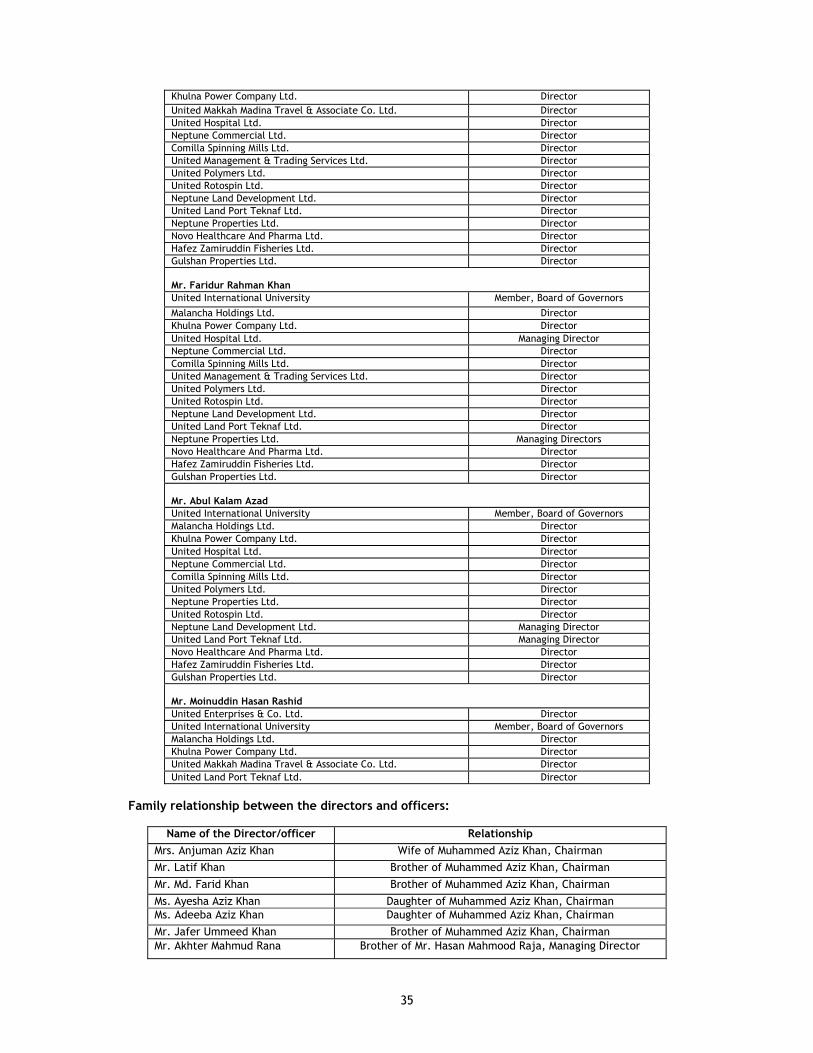

Material information having impact on the affair of the company 31 F. DIRECTORS AND OFFICERS 31 Name, Age and Position of all Directors 31 Date of first becoming Director and date of expiry of current term 31 Involvement of Directors with Listed Company in terms of Dividend & Category 32 Involvement of Directors with another Company 32 Family relationship between the directors and officers 35 Short biography of the directors and officers 36 Ownership List of shareholders who owns 5% or more than 5% share of the Company 38 Name and qualifications of the Senior Officers 38 G. INVOLVEMENT OF THE DIRECTORS AND OFFICERS IN CERTAIN LEGAL PROCEEDINGS 39 H. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS WITH RELATED PARTIES 39 I. EXECUTIVE COMPENSATION 40 J. OPTION GRANTED TO OFFICER, DIRECTORS AND EMPLOYEES 40 K. TRANSACTION WITH PROMOTERS BENEFIT FROM THE COMPANY 40 L. TANGIBLE ASSETS PER SHARE 41 M. OWNERSHIP OF COMPANY’S SECURITIES 42 Ownership List of shareholders who owns 5% or more than 5% share of the Company 42 The shareholding position of ordinary shares 42 N. DESCRIPTION OF SECURITIES OUTSTANDING OR BEING OFFERED 43 Dividend, voting and pre-emption rights of the shares outstanding or being offered 43 Conversion and liquidation rights of any preferred stock outstanding or being offered 43 Limitations on the Payment of dividends to common or preferred stockholders 43

Other material rights of common or preferred stockholders 44 O. DEBT SECURITIES 44 Terms and conditions of debt securities that the company may have issued or to be

issued 44

Principal amount, maturity date, interest rate and other features of all debt securities

44

All other material provisions giving or limiting the rights of the holders of debt 44 Trustees designated by the indenture for outstanding debt or for debt being offered 44 Preference Share 44 Corporate Directory 45 CREDIT RATING REPORT 46 AUDIT REPORT & FINANCIAL STATEMENT 61 Financial Projection 87 Auditors' report under section 135(1) and Para 24(1) of Part II of Schedule III of the

Companies Act 1994 89

Ratio Analyses 91 Additional Disclosure by the Management 93

1

A. DISPOSAL OF SHARES:

1. Details of offloading shares by the Existing Shareholders as per Regulation 5 of Dhaka & Chittagong Stock Exchange (Direct Listing) Regulations, 2006 as amended The existing shareholders of the company shall offload 5,21,48,250 ordinary shares of Tk.10.00 per share worth Tk. 52,14,82,500 (Fifty Two crore Fourteen lac Eighty Two thousand and Five hundred) with a minimum market lot of 100 (Hundred) shares following the Regulation 5 of Stock Exchange (Direct Listing) Regulations,2006 as amended, the Depository Act,1999 and regulations issued there under:

i. As resolved in the Board of Directors of KPCL and also as per resolution taken in the EGM of KPCL, 25% or the minimum required by the regulation of the proposed offer (i.e. 5,21,48,250 shares) to be sold to the general public/institutions at Market Price.

ii. The information Document, as vetted by DSE/CSE, shall be published in at least two widely circulated national dailies (One in English and one in Bengali) minimum 7 (Seven) days before commencement of trade upon listing by DSE/CSE along with an electronic copy for posting in the web page of DSE/CSE.

iii. The company shall simultaneously submit the vetted Information Document with all exhibits to SEC, to the Stock Exchange(s) where it tends to list its securities.

iv. The existing shareholders of the company shall sell their shares through brokers of the exchanges upon listing.

v. No existing shareholders of the company shall sell more then 50% of his existing shareholdings until the company holds the annual general meeting after completion of one full accounting year of the company upon listing with the exchanges.

vi. The conditions stated clauses 4 and 5 are subject to the provision that the existing shareholders shall offer for sell at least 25% (twenty five percent) of the shareholdings in the Company within 30 (thirty )trading days from the date of commencing the normal trading, i.e., after the price of the listed share is discovered and fixed following the book building method as prescribed by SEC through Securities and Exchange Commission (Public Issue) Rules, 2006, to the extent those are applicable or relevant in these respect.

vii. A. Allocation/Distribution: 10% (ten percent) of the said 25% shareholdings shall be allocated/distributed to the eligible institutional bidder following the procedures prescribed for determining price under the book building method, balance quantity shall be available for general investors through normal trading system of the stock exchanges. B. Lock-in: There shall be lock-in of 15 (fifteen) trading days from the first trading day on the security issued to the eligible institutional investors through book building method.

C. Others: (i) The existing shareholders (i.e. sponsors/directors) shall be restricted from buying the company’s share until completed disposal of the targeted 25% shareholdings. (ii) The selling broker of the existing shareholders shall disclose through the stock exchanges the local number of shares sold everybody along with the cumulative quantity sold and the quantity of unsold shares until completion of sale of the said targeted 25% shareholdings. (iii) Normal trade for general investors begin two days after transfer of the shares allocated to the eligible institutional bidders is completed.

viii. SEC decision shall be final on certain matter. Notwithstanding anything contained in these Regulations, in the event of any confusion or difference of opinion on any matter whatsoever, the decision of the SEC shall be final and binding on all concerned.

The following declaration shall be made by the company in the Information Document, namely:- “Declaration about Listing of Shares with the stock exchanges: Applications have been made to the Dhaka and Chittagong Stock Exchanges for permission of the shares of the Company for dealing in the said Stock Exchanges and for the quotation of the stock exchanges. After fulfillment of all requirements by the Company, the Exchanges shall list the Company’s shares within three weeks from the date of Publication of the Information Document, as mentioned in regulation 4, under intimation to the Commission, provided there is no contrary opinion of the Commission in this respect. In case of failure to fulfill the requirements by the Company, the Exchanges shall reject the application for listing showing reasons thereof, under intimation to the Securities and Exchange Commission within 60 (sixty) days from the date of application.”

2

2. Procedures to be followed for determining price under book building method

i) The indicative price which has been determined by the issuer in association with issue manager and eligible institutional investors shall be the basis for formal price building with an upward and downward band of 20% (twenty percent) of indicative price within which eligible institutional investors shall bid for the allocated amount of security;

ii) Eligible institutional investors bidding shall commence after getting consent from the commission for this purpose;

iii) If institutional quota is not cleared at 20% (twenty percent) below indicative price, the issue will be considered cancelled unless the floor price is further lowered within the face value of security;

Provided that, the issuer’s chance to lower the price shall not be more than once;

iv) No institutional investors shall be allowed to quote for more than 10 %( ten percent) of the total security offered for sale through book building method, subject to maximum of 5 (five) bids;

v) Institutional bidding period will be 3 to 5 (three to five) working days which may be changed with the approval of the commission;

vi) The bidding will be handled through the uniform and integrated automated system of the stock exchanges;

vii) The volume and value of bid at different prices will be displayed on the monitor of the said system without identifying the bidder;

viii) The institutional bidders will be allotted security on pro-rata basis at the weighted average price of the bids (within the cut off price) that would be clear the total number of securities being issued to them;

ix) Institutional bidders shall deposit their bid with 20% (twenty percent) of the amount of bid in advance to the designated bank account and the rest amount to settle the dues against security to be issued to them shall be deposited within 2 (two) working days prior to the date of opening normal trade for general investors;

x) In case of failure to deposit remaining amount that is required to be paid by institutional bidders for settlement of the security to be issued in their favor, 50% (fifty percent) of bid money deposited by them shall be forfeited by the commission. The securities earmarked for the bidder who defaulted in making payment shall be added to the investor quota.

3. Indicative Price for Book Building Purpose

Based on Indicative Price Offers received from seven Institutional Investors from amongst four

groups of institutional investors referred in rule 8.B.(16)(4)(c) of the Securities And Exchange

Commission (Public Issue) Rules, 2006; the Indicative Price for Book Building Purpose is fixed, in

consultation with the issue Manager and price offer from the eligible institutional investors through

proper disclosure, presentation, document, etc. at Tk 162.00 only as follows:-

SI No Offered by Category Indicative Price

1 Standard Bank Ltd Financial Institution 165

2 Continental Insurance Ltd Insurance company 167

3 Swadesh Investment Management Ltd Merchant Banker 160

4 Bangladesh Finance & Investment Company Ltd

Non Banking Financial Institution 155

5 SAR Securities Ltd. Stock-Dealer (DSE) 160

6 B & B Enterprise Ltd Stock-Dealer (DSE) 165

7 Royal Capital Limited Stock-Dealer (CSE) 165

Average 162

3

The Indicative Price for Book Building Purpose is justified on the basis of the following qualitative and quantitative factors:-

A. Earnings Based Value per share (EBVPS) based on financial statement for the year ended

31 December 2009

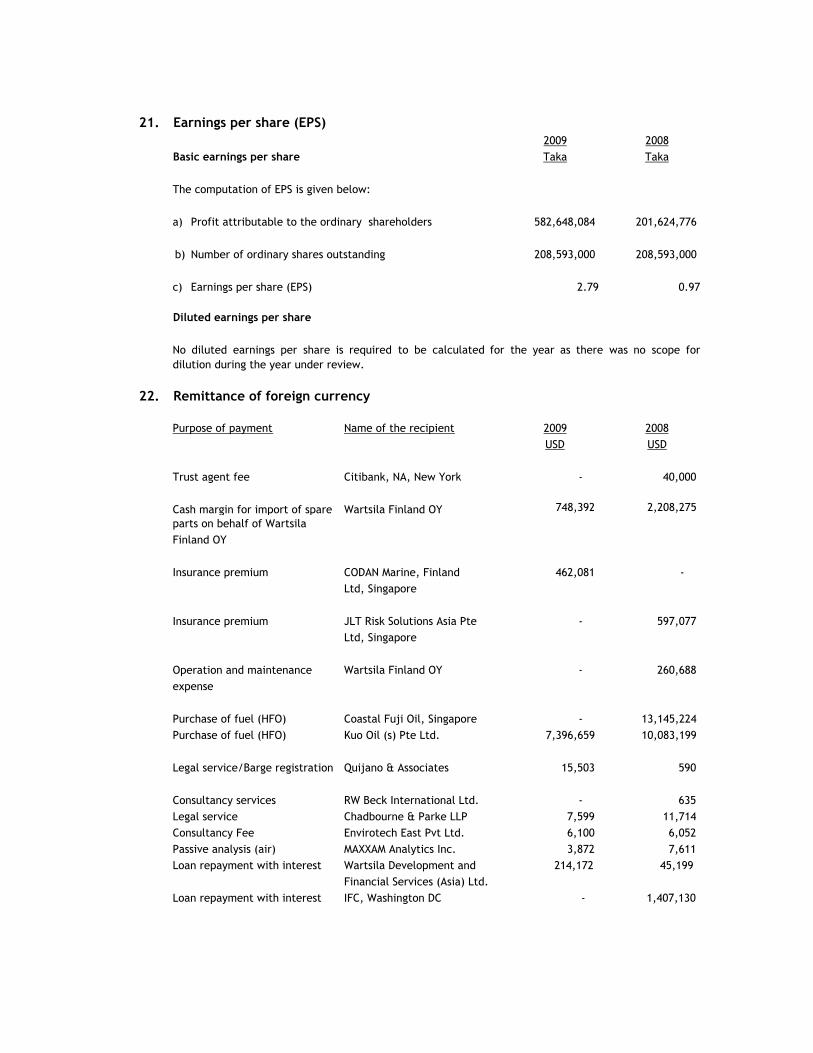

A.1 Earnings per share (EPS) 2.79

A.2 Average Market P/E of the sector 30

A.3 Earnings Based Value Per Share (A.1x A.2) 83.7

B. Earnings Based Value per share (EBVPS) based on projected financial statement for the year ended 31 December 2010 to 2014

B.1 Earnings per share (EPS) 6.62

B.2 Average Market P/E of the sector 30

B.3 Earnings Based Value Per Share (B.1x B.2) 198.6

C. Net Asset Value Per Share(NAVPS) based on financial statements for the year ended 31 December 2009

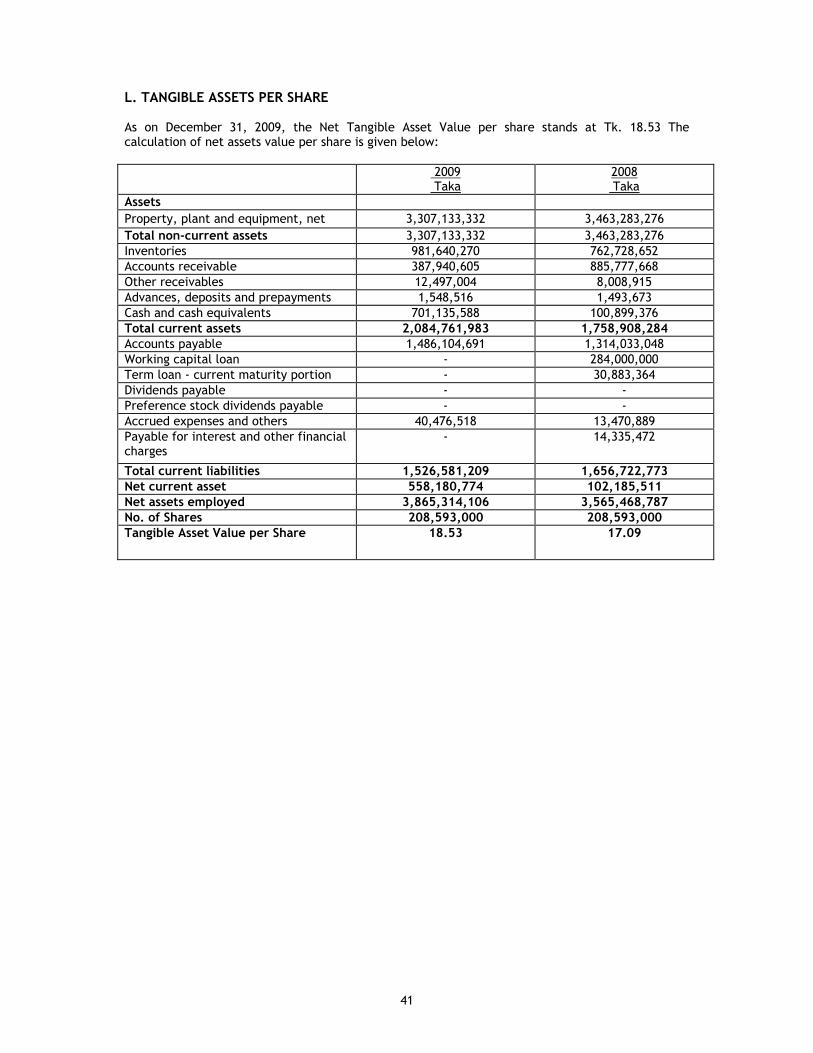

C.1 Net Asset Value 3,865,314,106

C.2 Number of Shares 208,593,000

C.3 Net Asset Value Per Share (NAVPS) (C.1/C.2) 18.53

D. Market Value Of similar share under Power industry:

Company Name Face Value (BDT)

Six Month Avg. Price (BDT)

Dhaka Electricity Supply Company Ltd

10* 166.08*

Summit Power Limited 10* 129.46*

Average 147.77 * In equivalent face value These companies’ stock prices are greater than their issue prices and face value. The strongest reasons are the earning potential of the companies. Most of the companies are operating in their full capacity and they are consistent in their operating performance and market dominance.

Qualitative factors: Rationales for fixing indicative price of KPCL

A) CRISL has assigned “AA” (pronounced as double A ) rating in the Long Term and “ST-1” rating in the Short Term to Khulna Power Company Ltd. based on financials and other relevant quantitative and qualitative information. The above ratings have been done on the basis of its good fundamentals such as sound equity based capital structure, sound debt repayment background, high quality plant, satisfactory profitability, government guarantee against power purchase, insignificant market risk on demand, government supportive policies for power sector etc. Entities rated in this category are adjudged to be of high quality, offer higher safety and have high credit quality. This level of rating indicates a corporate entity with sound credit profile and without significant problems. Risk factors are modest and may vary slightly from time to time because of economic conditions. The short term rating indicates highest certainly of timely payment. Short-term liquidity including internal fund generation is very strong and access to alternative sources of fund is outstanding. Safety is almost risk free like Government short-term obligations.

B) Bangladesh Power Development Board (BPDB), off-taker of KPCL, acknowledges KPCL as the best available and the most reliable power plant for its excellent track record in operation. It has been successfully supplying reliable power to the national grid since 1998 without any interruption for a single day. KPCL plant has also been recognized by the third party inspectors, surveyors and specialists as the best maintained fuel oil operated power plant. The plant availability has always been near to 100%.

4

C) KPCL never compromises with the quality of operation, maintenance, safety of plant and personnel and in that consideration, engaged Wartsila, Finland, a world renowned equipment manufacture (also the manufacturer of KPCL plant), for the operation and maintenance of KPCL plant. KPCL plant operation has been certified by Bureau Veritas (BV) on :

• Quality Management System (QMS) with ISO 9001 – 2008 • Environmental Management System (EMS) with ISO 14001 – 2007 • Occupational Health and Safety Administration System (OHSAS) 18001 – 2007

D) KPCL plant engines are having the dual fired capability i.e it can be converted into natural gas whenever gas will be available at the south-eastern region. Conversion into natural gas will enable the company to earn more revenue as compared to running on furnace oil, since the gas tariff structure as fixed by BPDB is more attractive than furnace oil based tariff structure.

E) The strategic location of the KPCL plant at the south-eastern region is an added advantage for KPCL. There are only few power plants in that region and as such KPCL is required to meet major portion of the demand of that region. Therefore, the utilization of the entire capacity of KPCL plant through out the year is almost certain.

F) The useful life of KPCL plant is 30 years. Therefore, no further capital investment will be required for the existing plant to carry out another extended term.

G) BPDB is the only buyer of KPCL and thus the revenues are 100% realizable. Unlike DESCO or DESA, KPCL has no system loss or no bad or doubtful debt.

H) In the context of Bangladesh economy, the demand for power or the demand of power sector is thriving and insatiable. At present, the demand and supply gap is 1,700 MW. In consideration of current generation capacity, also together with the future planning for generation of additional capacity, Bangladesh will not be able to meet the increasing demand for power. As a result, the power sector will continue to rule as top most demanding and dominating sector in the economy and no other sectors enjoys such a high demand profile. Therefore, KPCL’s revenue earnings and its further growth and future potential is highly certain beyond any doubt.

I) The proposed expansion of KPCL plant will enhance the KPCL earnings almost three times higher than the existing one. There will be no further fixed operating expenditure except the variables for the additional unit as the same will be run by the same management and production team. No further land will be required and the engines are likely to be more efficient for improved technology over the years.

J) KPCL’s long eleven years of experience in running liquid fuel power plant and proven record of operation will help KPCL management to run the expansion unit more efficiently and diligently and to achieve more optimization and economy of operation which will contribute to the enhancement of KPCL’s earning.

Extension for another term of the project and Expansion of the capacity for additional 100 MW (+/- 10 MW): Rationale: i) The Article 2.3 of PPA has a clear provision that the project is renewable for a further period, subject to agreement in writing by the parties at the latest twelve months prior to the expiry. ii) The KPCL plant is most reliable and efficient plant in the BPDB grid, available for 365 days of the year and with its 19 generating units, it is the most flexible and capable to meet BPDB’s ever varying load demand. iii) For dwindling natural gas production in the country, the natural gas based power plants are in deep

crisis. Natural gas is being used in 85% of total generation and due to short supply, a few of the existing plants running on gas may face shut down in the near future. Taking the above into consideration, the Govt. has already adopted a policy to use liquid fuel for generation of electricity. Accordingly, the future power plants will be built based on liquid fuel operation. Therefore, the extension of the term of KPCL plant is the imperative for the BPDB to meet the shortage of power.

iv) KPCL plants runs on Furnace Oil, the least cost liquid fuel, shall be most viable commercially. v) The existing shortage in generation capacity of the country shall continue to exist much beyond the

year 2013, when the tenure of the current PPA expires. Even in the year 2013 many of the BPDB old plants shall retire and many will face shut down or capacity reduction owing to gas shortage

Therefore, the extension of current PPA with BPDB shall take place as a natural consequence. Currently maximum generation capacity of all public and private power plants together is about 4,300 MW but country’s peak demand is about 6,000 MW. There is a demand supply gap of 1,700 MW and it will be widen further as a result of the general increase of demand. Considering of the increasing demand of power and the

5

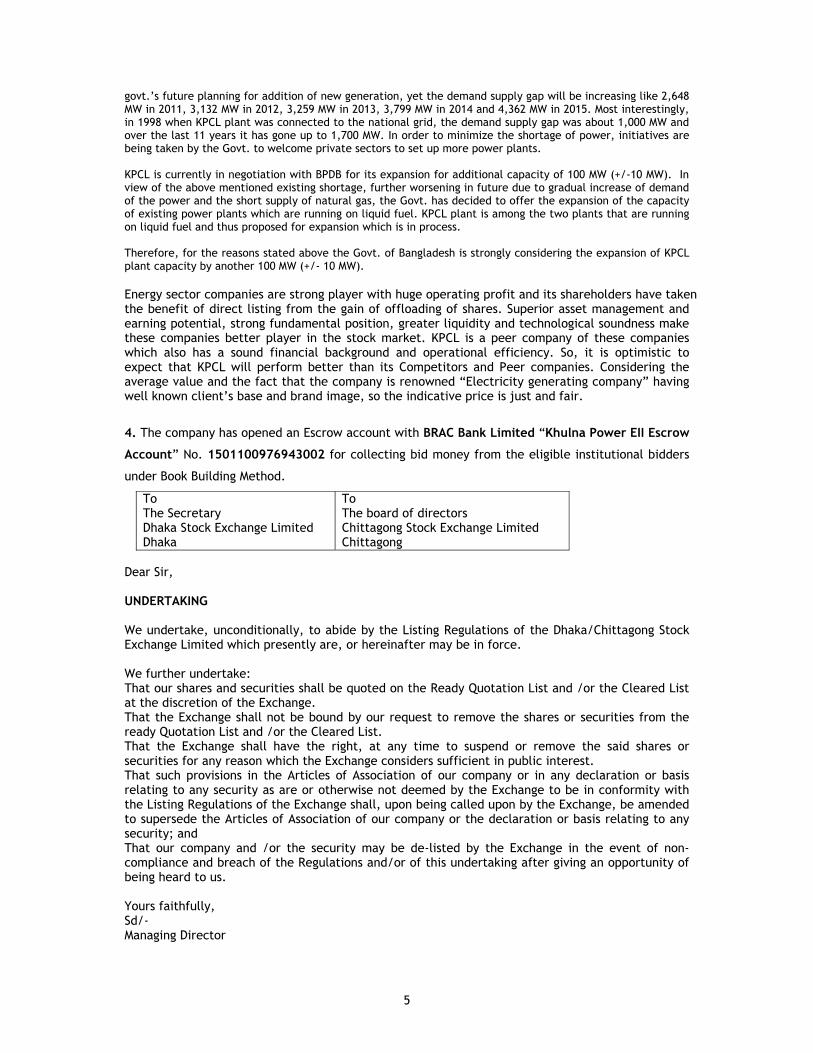

govt.’s future planning for addition of new generation, yet the demand supply gap will be increasing like 2,648 MW in 2011, 3,132 MW in 2012, 3,259 MW in 2013, 3,799 MW in 2014 and 4,362 MW in 2015. Most interestingly, in 1998 when KPCL plant was connected to the national grid, the demand supply gap was about 1,000 MW and over the last 11 years it has gone up to 1,700 MW. In order to minimize the shortage of power, initiatives are being taken by the Govt. to welcome private sectors to set up more power plants.

KPCL is currently in negotiation with BPDB for its expansion for additional capacity of 100 MW (+/-10 MW). In view of the above mentioned existing shortage, further worsening in future due to gradual increase of demand of the power and the short supply of natural gas, the Govt. has decided to offer the expansion of the capacity of existing power plants which are running on liquid fuel. KPCL plant is among the two plants that are running on liquid fuel and thus proposed for expansion which is in process. Therefore, for the reasons stated above the Govt. of Bangladesh is strongly considering the expansion of KPCL plant capacity by another 100 MW (+/- 10 MW). Energy sector companies are strong player with huge operating profit and its shareholders have taken the benefit of direct listing from the gain of offloading of shares. Superior asset management and earning potential, strong fundamental position, greater liquidity and technological soundness make these companies better player in the stock market. KPCL is a peer company of these companies which also has a sound financial background and operational efficiency. So, it is optimistic to expect that KPCL will perform better than its Competitors and Peer companies. Considering the average value and the fact that the company is renowned “Electricity generating company” having well known client’s base and brand image, so the indicative price is just and fair.

4. The company has opened an Escrow account with BRAC Bank Limited “Khulna Power EII Escrow

Account” No. 1501100976943002 for collecting bid money from the eligible institutional bidders

under Book Building Method.

To The Secretary Dhaka Stock Exchange Limited Dhaka

To The board of directors Chittagong Stock Exchange Limited Chittagong

Dear Sir, UNDERTAKING We undertake, unconditionally, to abide by the Listing Regulations of the Dhaka/Chittagong Stock Exchange Limited which presently are, or hereinafter may be in force. We further undertake: That our shares and securities shall be quoted on the Ready Quotation List and /or the Cleared List at the discretion of the Exchange. That the Exchange shall not be bound by our request to remove the shares or securities from the ready Quotation List and /or the Cleared List. That the Exchange shall have the right, at any time to suspend or remove the said shares or securities for any reason which the Exchange considers sufficient in public interest. That such provisions in the Articles of Association of our company or in any declaration or basis relating to any security as are or otherwise not deemed by the Exchange to be in conformity with the Listing Regulations of the Exchange shall, upon being called upon by the Exchange, be amended to supersede the Articles of Association of our company or the declaration or basis relating to any security; and That our company and /or the security may be de-listed by the Exchange in the event of non-compliance and breach of the Regulations and/or of this undertaking after giving an opportunity of being heard to us. Yours faithfully, Sd/- Managing Director

6

B. RISK FACTORS AND MANAGEMENT PERCEPTION ABOUT RISK: As with all investments, investors should be aware that there are some risks associated with an investment in the Company. The investors should carefully consider the following risks in addition to the information contained in the prospectus for evaluating the offer and taking decision whether to invest in shares of the company.

a) Interest Rate Risk: Interest/financial charge are paid against any kind of borrowed fund/ preference shares. Instability in money market and increased requirement for fund may put pressure on interest rate structure. Rising of interest rate increases the cost of borrowed fund and consequently it may impact on the profitability. Management Perception: Currently, KPCL has working capital debt obligation from several banks and preference shares which are comprised with fixed financial charges. But the Company has solid revenue source and is highly profitable. The rate for the financial charges are fixed so, KPCL doesn’t have such risk.

b) Exchange Rate Risk: KPCL imports mostly fuel against payment of foreign currency. Unfavorable volatility or currency fluctuation may affect the profitability of the company. Management Perception: KPCL is fully aware of the risk related to currency fluctuation but practically doesn’t possess any foreign exchange risk as 99% of the Other Monthly Tariff (OMT)is convertible and fuel is being imported through L/C and the exchange rate Sonali Bank Ltd. is acceptable to BPDB under pass through payment process. Moreover, KPCL executes favorable and competitive foreign exchange rate from its bankers against its L/C payments.

c) Industry Risk: The supply of electricity and alternative energy is not adequate than the demand of it. For that reason organizations engaged in generating electricity can’t provide all required amount of electricity. Power companies mainly supply electricity to national power distributors to supply electricity. Management Perception: KPCL supplies electricity to BPDB in the south-western region of Bangladesh and it’s a dedicated power plant with a guaranteed payment from BPDB and GoB under the PPA. So, possibilities of entering new power companies wouldn’t create any industry risk for the company.

d) Market and technology related Risk: Technology is related to generation, transmission, distribution, quantity measuring and maintaining of required electricity generation. Management Perception: The Company is operated by the plant manufacturer, Wärtsilä, the leading power plant manufacturer and plant operator in the world. Wärtsilä is technologically advanced enough to keep KPCL plant out of such risk.

e) Potential or existing Government regulation: The business activities of KPCL is fully controlled by policies, rules and regulation framed by government, that is policies related to electricity price fixation, demand & supply and distribution is fully under the control of Government. So, government policies in this regard may impact business operation of KPCL.

7

Management Perception: The Power Purchase Agreement with BPDB safeguards KPCL from any changes in government regulation. The PPA agreement is valid for 15 years till 2013 and can be extended upon the consent of both parties. Moreover, in case of PPA termination, KPCL will get compensation under the agreement from BPDB or GoB. Additionally, the huge shortage of power in the country minimizes the chances of terminating the PPA agreement that mitigates related risks.

f) Potential changes in the global or national policies, natural calamities etc: The performance of the company may be affected due to unavoidable circumstances in Bangladesh, as such political turmoil, war, terrorism, political unrest in the country may adversely affect the economy in general. Moreover, natural disasters like Cyclone, Tide, and Earthquake may hamper normal performance of power generation. Management Perception: The risk due to changes in global or national policies is beyond control for any company. Yet the company is well prepared for adoption of policies and preventive measures as and when required to reduce the risk. The routine & proper maintenance of the distribution network undertaken by BPDB reduces major disruption due to natural calamities. But severe natural calamities, which sometimes are unpredictable and unforeseen, have the potential to disrupt normal operations of KPCL. But with prudent rehabilitation schemes and the very effective and quick repair and maintenance lessened the damages caused by such disasters. Political unrest leading to strikes, hortals etc. certainly plays negative impact in any business. But electricity service being considered a daily necessity & in consideration of its use by all irrespective of their political thoughts is always kept out of obstructions. Furthermore, all such above risks are covered under the insurance agreement with CODAN Marine (a subsidiary of RSA Group) to compensate the damages due to such uncertainties in extreme cases. Thus, the risk due to natural calamities & political unrest is minimized.

g) Operational Risk:

Risk associated with limited tenure of the present Power Purchase Agreement: The tenure of the present PPA between the Company and BPDB is limited to 15 (fifteen) years from the date of commercial operation i.e. till 13th October, 2013. Management Perception: On the backdrop of development need for the economy, power generation is one of the priority sectors of the government. With the existing deficit in power generation capacity, the government is expected to continue with the same policy level support for the sector. Dispute with any one operator may lead to adverse repercussions throughout the industry. As such, no major dispute with the government is envisaged. There is a provision in the PPA for enhancement of the project life. BPDB and KPCL have been considering to expand the capacity of the Berge Mounted Power Plant utilizing the area of its leasehold property, KPCL wants to install additional 7 generation units with the capacity of 15 MW each to generate total 100 MW. The strategy is to generate and produce more electricity by using fewer big engines with higher fuel efficiency.

Risk associated with single party exposure: The BPDB is the single buyer who purchases total electricity generated by the Company. The Company’s ability to service its both existing and future financial obligations rest on the BPDB’s ability to meet the tariff payments under the PPA. Management Perception: KPCL is out of the single party risk exposure as it is guaranteed by BPDB for the payment in case the plant runs lower than 50%. Moreover, L/C issued by BPDB for two months’ minimum guaranteed payment. Therefore, the Implementation Agreement signed by the Government through Ministry of Power, Energy and Mineral Resources is considered to be Government guarantee to protect the Company from single party risk exposure.

8

Risk associated with tariff of electricity: The BPDB is the single buyer who purchases total electricity generated by the Company. In these circumstances usually it is the buyer who may determine the tariff value of the electricity generated by the Company. Management Perception: In this case no risk is associated as BPDB and the Company have pre-determined and contracted the terms and condition regarding the tariff of electricity, expressed under two slabs – Other Monthly Tariff (OMT) and Fuel Tariff (FT) where OMT is based on delivered MWh and FT is pass through. Tariff for each year is adjusted and indexed from time to time in accordance with the PPA and the said Reference Tariff is used to calculate the Tariff in Effect for any Billing Month during the Term of the Agreement.

Risk associated with supply of raw materials: The main raw material for generating electricity is Heavy Fuel Oil (HFO). Any interruption of supplies of the fuel to the power plants will hamper the generation of electricity, the only product of the Company. Management Perception: Kuo Oil Pte Ltd. Singapore has been supplying Heavy Fuel Oil (HFO) to the Company through United Summit Coastal Oil Limited and the risk of price fluctuation in the global oil market is automatically done by the very FT structure which is based on fuel cost as a pass through item. Moreover, KPCL can source HFO from other sources if Kuo Oil is unable to supply.

Risk associated with supply of spare parts: The power plants are dependent on timely supply of spare parts for smooth operation purpose. Any disruption in supply flow of spares parts will put an adverse impact on power generation. Management Perception: Under the Operations & Maintenance Contract with Wartsila, the Company has signed a Spare Parts Support Agreement (SPSA). Wärtsilä also maintains sufficient spares parts inventory for smooth operation of KPCL plants. In addition, KPCL maintains safety spare parts stock of US$ 2 million.

Risk associated with payment: There is an impending risk in the case of delayed payment from BPDB. In case of any dispute with BPDB or failure to comply with certain rules and regulations, BPDB may stop making payments to KPCL resulting into non-payment to its lenders. Management Perception: KPCL is getting the payment regularly from BPDB. Sometimes, there are delays in payment but that is mainly due to administrative reasons. Till date, no payment has been defaulted. As per the PPA with BPDB, there is a penalty clause and BPDB needs to ensure minimum guaranteed payment supported by Letter of Credit. . Additionally, GoB through the Implementation Agreement provides sovereign guarantee with regard to payments, hence possibly mitigating risk of any non-payments.

Risk associated with systems failure and sabotage: System failure may take place resulting into damages for KPCL. Moreover, internal conflict among the workers and engineers may also disrupt operation. Management Perception: There is an agreement with the O & M Contractor and equipment supplier to provide maintenance and equipment support. Additionally, any equipment and mechanical support will be provided for in case the plant needs to be converted from a fuel based to a gas based plant. In addition, the company has prudent insurance coverage with CODAN Marine which covers all risks package including Machinery Breakdown, Business Interruption, Third Party Liability, Sabotage and Terrorism.

9

h) Force Majeure: Force Majeure events are circumstances in which a delay in the performance of any obligation under the PPA is beyond the reasonable control, and occurs without the faults or negligence, of the parties concerned. Management Perception: If the Company is affected by a Force Majeure event after commencement of commercial operation, the BPDB will only pay capacity components and energy components to the Company, to the extent that the unit is available. However, financial loss due to unavailability of the plant after a Force Majeure event will be mitigated by the Company’s insurance policy. If BPDB is affected by a Force Majeure event after commercial operation, it will pay the Company its debt servicing costs less insurance proceeds and / or any available capacity component and energy component received by the company during the Force Majeure period. In case of Political Force Majeure event or change in law, the BPDB will pay the Company, to the extent that the unit is available and the Government of Bangladesh will pay required amount to cover the capacity component up to 50%.

i) Risk associated with environmental pollution: KPCL plant operation may cause air and water pollution which may affect the ecological balance and living condition and health of the people around the plant. Management Perception: The Operations and Maintenance (O&M) contractor of KPCL plant, Wärtsilä Bangladesh Ltd, Khulna Plant (WBD-KP) is responsible for environmental management of the project. Plant operation is certified by Bureau Veritas (BV) on: • Quality Management System (QMS) with ISO 9001 - 2008 • Environmental Management System (EMS) with ISO 14001-2007 • Occupational Health and Safety Administration System (OHSAS) 18001 - 2007 The EMS Manual covers all the elements that are required to be monitored for compliance of ISO 14001 and local Department of Environmental Guidelines. Under the EMS, ambient air quality by passive sampling method continuously, basin water quality and sanitary discharge tested on monthly basis and ambient noise level is measured on monthly basis, and is monitored for compliance. Quarterly reports, compiling all the test and measurement results are submitted to Department of Environment (DOE). Exhaust gas emission is monitored by stack testing annually, and elaborate reports are submitted to DOE every year. For each and every fuel oil delivery and handling, containment boom is used to minimize the risk of accidental spillage and pollution. At regular intervals, independent auditors or Bureau Veritas carry out surveillance audit to assess the compliance with the EMS of ISO 14001-2007 but so far no non-conformity noted. Similarly, DOE officials inspect regularly and monitor environmental performance of the plant and till date no non-conformity reported. Overall, plant operation does not pose any hazard to the environment of the plant area and its surroundings.

j) Non-Operating history There is no history of non-operation in the case of KPCL. Management Perception: To overcome these uncertainties, the Company has its own extra Engine and fuel backup, efficient management and continuous monitoring systems, which reduce the non-operating risk.

k) Risk of “Operation and Maintenance Agreement” by “Wartsila” There is a risk of on non-continuation of “Operation and Maintenance Agreement” (“O&M Agreement) by “Wartsila” Management Perception: In case of discontinuation of the O&M agreement with Wartsila, KPCL shall take over the O&M under own management since Summit and United group have been operating & maintaining their own power plants over 300 MW capacity by themselves. Moreover, the existing personnel of the Wartsila can be retained too by KPCL if required.

10

C. DESCRIPTION OF THE BUSINESS: Information about the Company Background

In 1997 the Bangladesh Power Development Board (BPDB) was faced with the challenge to ease a critically short power supply in the South Western Zone of Bangladesh. The electrical demand had been consistently higher than available capacity, and generation costs in the area had been very high due to the low efficiency of existing equipment and the heavy use of expensive, low-availability fuel. In October 1997, BPDB signed a Power Purchase Agreement with Khulna Power Company Ltd. for a 110 MW floating base load power plant at Khulna, to help ease the electricity shortage. Description

Khulna Power Company Ltd. is a public limited company which was incorporated as a private limited company in Bangladesh on October 15, 1997. Its paid up capital is BDT 2085.93 million (US$ 44.10 million) It is the first independent 110MW barge-mounted power plant that commenced operation in October 1998 under a 15 year PPA from the government (expiry 2013). When established, KPCL shareholders were Coastal Power Company (later Coastal was merged with El Paso Corporation, USA) through its direct wholly-owned subsidiary El Paso Khulna Power ApS, Summit Industrial & Mercantile Corporation (Pvt.) Ltd. (Bangladesh), United Enterprises & Co Ltd. (Bangladesh) and Wärtsilä Development and Financial Services (Asia) Ltd. Now only local shareholders hold 100% ownership of the company. KPCL project was initially financed by the IFC and the sponsors’ equity with a debt-to-equity ratio of 54:46. The total initial project cost was USD 96.07 million The principal activity of KPCL is to own and operate barge mounted power plants in Khulna and supply electricity to the national grid of Bangladesh. The plant came into operation in October 1998. Nine engines generators are mounted on one barge and ten on the other. The barges, shipped as deck cargo on a submersible dry tow ship, are moored in a closed basin. Each barge is approximately 91 meters long and 24 meters wide. These two barge-mounted plants were connected to the national grid. The plant consumes about 600 MT of Heavy Fuel Oil daily to generate 110 MW power by the 19 generators on the two barges located in Khalishpur, Khulna. The project was the first IPP implemented under the then new Government of Bangladesh guidelines for private power projects. As Bangladesh has enjoyed steady growth in recent years, the infrastructure to supply electricity to the economy has not kept pace with this growth. Reliability of electricity supply, which has been a growing problem over the years, has now reached crisis proportions. Peak demand is about 5500-6000 MW, whereas available generation is about 4200-4500 MW. The demand supply imbalance has now become a major bottleneck to economic growth. The Khulna power project is a fast-track response to the power shortage. KPCL plant was designed to alleviate the severe power shortages in the Khulna and adjacent areas, identified as industrial growth Centres by the Government of Bangladesh, while improving the overall reliability of the country's power supply. The facility displaced the generating capacity of the older, less efficient, and high-cost plants in the region. The plant conformed to all applicable environmental standards. The plant has already changed the economy of the adjacent region directly and positively. It has provided employment to over 110 people from the surrounding areas and many of the jobs are technical and managerial in nature. Significant numbers of jobs have been created at the fuel terminal, barges, restaurants, transportation services, and other ancillary businesses created to serve the needs of the plant. New industrial and commercial establishments have been opened to take advantage of the stable and reliable power, and existing establishments do not require back-up generators. In addition, the plant has contributed significant funds toward social causes in the region.

11

The plant is managed by the O&M operator – Wärtsilä, a globally recognized power plant manufacturer and operator. A team of skilled technical people are engaged in the operations of the plant. The operational process has been developed by an expert team. For any technical assistance, the equipment suppliers extend their support, this is backed by other consultants support as and when needed. Management team is professional and has a successful track record and possesses requisite expertise to run the operations. KPCL financials is audited by Rahman Rahman Huq, a member of KPMG. The company has shown stable performance with steady sales as in any typical utility companies. The company has received power a tariff of BDT 8.06/kWh during the January – December 2009 period, whereas it received a tariff of BDT 10.51/kWh during the January – December 2008 period. The differences between the period was due to tariff slabs variation of cost of fuel and foreign currency rate. This is an environmental review category B project. Environmental and social issues associated with the project include: site selection and land use, site contamination from past activities, air emissions and noise from construction and plant operation, liquid effluents, liquid and solid waste disposal, oil transportation safety and spill potential, social impacts, fire prevention and emergency response, employee health and safety programs, and impact management and monitoring. KPCL has prepared an environmental assessment for the project to address these issues and demonstrate that the proposed project will comply with applicable governmental and World Bank requirements. The proposed site for the project was identified by BPDB in their RFP for the project. The project is located on an uninhabited, vacant property owned by PADMA, the state oil company. No resettlement of residents or economic displacement was required. Expansion plan

During establishment of the company, the project concept envisaged expansion. KPCL is now discussing the next expansion plan of the company with BPDB which the management wants to finalize within one year. The experience gathered by the management during the implementation of initial 110 MW project will be applied for formulating new strategy in tariff determination and operation of the future projects. Accordingly management took the strategy of negotiating with BPDB for the revised Power Purchase Agreement (PPA) and other project documents for easy operation, maintenance and better return of the expansion project. Accordingly the BPDB and KPCL have been considering the agreements to expand the capacity of its Berge Mounted Power Plant to land based power plant. With the area of its leasehold property, KPCL wants to install additional 110 MW capacities with power generating engines. The strategy is to generate and produce more electricity by using fewer engines. The expansion plan will be for 22 years effective from Commercial Operation Date.

12

Ownership The ownership structure of KPCL is as follows:

Summit Industrial and Mercantile Corporation (Pvt.) Ltd. 49.9832% United Enterprises & Co. Ltd. 49.9832% Others 0.0336%

Company At A Glance

Company Name : Khulna Power Company Ltd. (KPCL)

Registered Address : Summit Centre (5th Floor), 18 Karwan Bazar, Dhaka-1215

Plant Address : Goalpara, Khalishpur, Khulna

Paid Up Capital : Tk. 2,085,930,000.00 (Ordinary Shares)

Tk. 1,100,000,000.00 (Preference Shares)

Sponsors : Summit Industrial and Mercantile Corporation (Pvt.) Ltd.

United Enterprises & Co. Ltd.

Unique Client : Bangladesh Power Development Board

EPC Contractor : Wärtsilä NSD OY, Finland

Number of Employees : KPCL has 10 and plant has 113 engaged by Wärtsilä O&M operator

Total electric output : 110 MW

Electrical efficiency : 43.5 %

Engine type : 19 x Wärtsilä 18V32LN

Year of Starting Operation : 13th October 1998

Annual General Meeting held in last 5 years:

Year Date of AGM held Declared dividend

2004 (7th) 3 May 2005 7% Cash

2005(8th) 11 September 2006 Nil

2006(9th) 24 July 2007 Nil

2007(10th) 21 June 2008 57.53% Cash

2008(11th) 23 June 2009 10% Cash

13

(1) Principal Product or Service of the Company: KPCL is engaged in business of generation of electricity and sells the same in bulk to BPDB through its national transmission grid and BPDB distributes the energy in the south-western region of Bangladesh. (2) The relative contribution to sales and income of each product or service that accounts for more than 10% of the company’s total revenues: Electricity is the only product of KPCL. So, contribution of more than 10% by any other product to the total revenue of the company doesn’t arise. (3) Name of associates, the subsidiary/related holding company and their core areas of business: Khulna Power Company Ltd. (KPCL) has no associates, the subsidiary/related holding company however there are common directorship in the following related companies: Sponsors KPCL is now fully owned by the local entrepreneur group, namely – Summit Industrial and Mercantile Corporation (Pvt.) Ltd. and United Enterprises & Co. Ltd. However, the Khulna Power Project was originally developed by a consortium led by Wärtsilä Corporation (“Wärtsilä”) with which BPDB signed a Power Purchase Agreement (“PPA”). Wärtsilä is a leading manufacturer of medium speed diesel engines and had successfully developed similar power projects at several locations worldwide. Coastal Power Company, a wholly owned subsidiary of The Coastal Corporation (“Coastal”), joined the consortium in August 1998. Thereafter, Coastal and El Paso Energy Corporation merged in January 2001 to form El Paso Corporation (“El Paso”). El Paso is one of the world’s largest and most diversified natural gas exploration and pipeline companies with an enterprise value in excess of $50 billion. As the major equity holder in KPCL with 73.9% interest, El Paso was responsible for the management of the Plant up to April, 2008. The local Shareholders are Summit Industrial and Mercantile Corporation (Pvt.) Ltd. (“Summit”) and United Enterprises & Co. Ltd. (“United”). Summit is an investment group with significant holdings in liquid fuel storage terminals. It is also an investor in six Rural Electrification Board (“BPDB”) small power projects, gas pipeline construction on a build-transfer basis, liquid fuel shipping, and real estate construction. United has ownership in Bangladesh’s largest private liquid product bulk storage terminal, real estates, and one of the largest Hospitals and a private University. It has implemented several BPDB small power projects, and has worked very closely with Summit. Summit and United have contributed a combined 20% of the Project’s equity. The sponsors have invested total equity capital of US$ 44 million, with 73.9% ownership by El Paso Energy; 10% by Summit Industrial and Mercantile Corporation (Pvt.) Ltd.; 10% by United Enterprises & Co. Ltd.; and 6.1% by Wärtsilä. But changes were made in the Ownership Structure as El Paso Corporation, as part of its global repositioning strategy, offered its stake of 73.9% in KPCL for sale. Reportedly CDC Globeleq has principally agreed to purchase El Paso's interests in Asia on a portfolio basis (Bangladesh, Indonesia, Pakistan, Philippines). However, for sale of shares in the company per terms of the shareholders' agreement allows existing shareholders first right of refusal and therefore local shareholders – Summit Industrial & Mercantile Corporation (Pvt.) Ltd. and United Enterprises & Co. Ltd. have expressed interest to purchase El Paso's 73.9% stake in KPCL, at the offered price of CDC Globeleq. Consequently, Summit and United jointly acquired El Paso shareholding and later Wärtsilä’s share was also acquired by Summit and United.

14

Background of Past Shareholders EL PASO El Paso, North America’s leading provider of natural gas services was a 73.9% shareholder in KPCL. The company has core businesses in production, gathering, processing, and transmission of natural gas, as well as liquefied natural gas transport and receiving, petroleum logistics, power generation, and merchant energy services. It is rich in assets and is fully integrated across in natural gas value chain and is committed to developing new supplies and technologies to deliver energy to communities around the world. El Paso Energy International pursues a low risk, power-oriented investment strategy, as a project developer. This strategy has helped the company build diversified project portfolios supported by fixed return contracts in countries around the world. These portfolios present significant opportunities to build robust businesses in selected markets where the right combination of economic, regulatory and industry conditions exist. By focusing on regional business growth, El Paso can export the broader skill set of the entire company to produce significant growth. WÄRTSILÄ Wärtsilä Corporation is the leading global ship power and power plant supplier. Wärtsilä enhances the business of its customers by providing them with complete lifecycle power solutions. It is a major provider of solutions for decentralized power generation and of supporting services. Most of its IPP deliveries were directed to Asia, North America and all other continents. Wärtsilä plans to contribute to solving the global needs of sea transportation and power generation by developing equipment and services that convert fuels into power efficiently at the lowest possible environmental impact. It has its own worldwide service network in 80 countries. Wärtsilä takes complete care of customers’ ship machinery and related equipment at every lifecycle stage. It plans to expand the business by providing innovative, reliable and valuable service, such as non-O&M service in key ports, scheduled and condition-based maintenance, as well as operations and maintenance contracts.

15

Background of Present Shareholders

Summit Industrial & Mercantile Corporation (PVT.) Limited – SUMMIT GROUP Summit Group is one of the reputed local conglomerates of the country having interests in power, EPC contracting, tank terminal, shipping, properties, petroleum, inland container depot, trading and so on. The group sponsored the first independent 110 MW barge-mounted power plant KPCL in 1998, three 11 MW power plants for BPDB, the country's first and biggest private sector inland container depot in Chittagong. They have also pioneered locally the first granite and marble cutting, polishing and finishing plant. The group is recognized as a major infrastructure-industry company of Bangladesh employing over 1,000 people. Brief overview on Summit Group sister concerns are given in the following: Summit Industrial & Mercantile Corporation (Pvt.) Limited

Summit Industrial & Mercantile Corporation (Pvt.) Limited (SIMCL) is a holding company established in 1985 sponsoring fourteen different companies, ranging from shipping to power. SIMCL is one of the largest companies in Bangladesh with a significant interest in infrastructural development. Out of fourteen different companies, two of its holdings, Summit Power Limited (DSE: SUMITPOWER) and Summit Alliance Port limited (DSE: SAPORTL) are publicly listed. Of these publicly listed companies Summit Power Limited (SPL) accounts for supplying a total of 215 MWs of electricity in Bangladesh. It has power plants located in various parts of Bangladesh mainly in the suburban industrial areas where there is the greatest need for electricity. SPL has grown over 600 % in the past 10 years resulting in increased efficiency and economies of scale.

Brief history of the growth and development of SIMCL

• SIMCL was incorporated as a private limited company in Bangladesh on 7th December 1985.

• In 1988, the company in addition to the import business started the export of Molasses from Bangladesh.

• The year 1989 marked SIMCL's first foray into infrastructure development with the establishment of Summit United Tanks Terminal (SUTT), which established SIMCL as the first owner in Bangladesh of a liquid storage tank terminal.

• In 1991 SIMCL bought Van Omaren Tanks Terminal becoming the largest private terminal owner and operator in Bangladesh. Subsequently the two terminals were sold off.

• In 1992, the SIMCL started to export Urea fertilizer becoming the largest fertilizer exporter in Bangladesh. That same year SIMCL purchased BTT, the oldest liquid Tanks Terminal depot in Chittagong Port area, renaming it to SUTTL. After the purchase the storage capacity of SUTT expanded from 17200 MT to 65100 MT. SUTT further increased after the acquisition of VOTTL, a private sector tank terminal, in Chittagong port.

• In 1997 the company took another leap in infrastructure development by establishing the first private sector electricity generation plant of 114 MW, which operated on furnace oil. Khulna Power Company (KPCL) continues to flourish till date and is planning on expanding and also going public.

16

• The year 1999 marked one of the highest rates of growth in the company’s history through the formation of various companies in partnership with other major companies and conglomerates both domestic and international. In 1999 SIMCL partnered the United Group and Wartsila USA to form KPCL, the country’s first 110 MW Barge Mounted power Generation plant. That year also led to the formation of USPCL, an LPG plant in Mongla, in association with the United Group. Finally, the year was rounded to a close, in terms of energy development through the formation of USCOL, an energy oil company, in conjunction with EL Paso USA and the United Group. The year 1999 also earmarks the establishment and development of USSL, a shipping company, created with joint partnership between Summit and United Group. In its year of conception it bought two Ocean going tanker vessels and became the first ISO 9002 certified shipping company in Bangladesh. Summit continued its extraordinary growth through the formation of Summit Pipeco Limited in partnership with the Alliance Group. Summit Pipeco teamed up with Daquing a company based out of China to execute the EPC of 54 Km Ashuganj- Hobiganj gas pipe line construction work in Bangladesh

• In 2000 summit power limited (SPL) was established to set up ‘distributed power’ in Bangladesh. Presently SPL has seven power plants providing electricity to 600,000 homes, generating 215 MWs of electricity with natural gas as its fuel.

• In 2004, the company formed SAPL to expand its capacity and operations in the container terminal field. SAPL is also traded and publicly listed in the Dhaka Stock Exchange and Chittagong Stock Exchange. OCL and SAPL together deals with 15% of the country’s import cargo and 30% of the export cargos. The two companies are both located in Chittagong port and helps facilitate port services, they over 50 acres of freehold land and operates a streamlined modern container handling and empty storage facility with a capacity of 4000 tones.

• In 2006, the Summit acquired a Dhaka Stock Exchange membership (Membership # 146) in the name of Cosmopolitan Traders (Pvt.) Limited a sister company of SIMCL and substantial share of the following companies:

i) National Housing Finance & Investments Limited. ii) IPDC of Bangladesh Ltd. iii) Bangladesh Commerce Bank Limited

• In 2009, the company set up SCL (Summit Communications Limited) to break into the telecommunication sector to provide much needed revitalization to the Bangladesh’s telecommunications. Improvement in the telecommunications sector is a move towards ingratiating Bangladesh into the larger global community. This project is yet another inference to the revolutionary nature of SIMCL investment portfolio.

SIMCL’s financial position at the end of the accounting year as of 31st December 2009 was in a sound and stable position having a total of Taka 593.70 crores in total assets with a net worth of Taka 560.32 crores. The total turnover for the year was Taka 198 crores with a net profit of Taka178.29 crores after tax.

Ocean Containers Ltd. Ocean Containers Limited (OCL) is a pioneer in the inland container depot and freight stations and is the largest privately owned land container port in Bangladesh. It is located at Patenga Industrial Area of Chittagong on the international airport road, which is only 6 km from the country’s largest seaport, Chittagong Port. OCL owns 15 acres of custom bonded free hold land. Currently, OCL can stuff and de-stuff 50,000 containers annually. It also has an empty storage facility for 6,000 TEUs. OCL is a custom bonded warehouse. With the logistic support of its surface transport subsidiary in Ocean Transport

17

Company, it can deliver containers anywhere in Bangladesh. The company currently operates a fleet of 24 prime movers with 40 feet trailers. Government customs officers and OCL are working round the clock to keep our commitment. Our fully computerized system allows us to keep track of all containers. OCL is an ISO 9001: 2000 Quality Management Certified Company. It is the first company in Bangladesh to have the ISO certification for Inland Container Depot (ICD) and container freight station (CFS) operators. OCL clienteles include Maersk-Sealand, Yang Ming Line, Happag-Lloyd, Kuhene & Nagel, Danzas, Zim Line etc. OCL is in discussion with APL-NOL to have long term contract for consolidating their export bound cargoes from Bangladesh. OCL already has similar arrangement with Maersk-Sealand. OCL currently caters to the 30% of the garment’s export bound cargoes. By the year 2004 OCL aims to consolidate 50% export bound cargoes of Bangladesh. Summit Power Limited Summit Power Limited (SPL), a concern of Summit Group is the first Bangladeshi Independent Power Producer (IPP) in Bangladesh and until now the only local company in private electricity generation and supply business providing power to national grid. SPL was incorporated in Bangladesh on March 30, 1997 as a Private Limited Company. On June 7, 2004 the Company was converted to Public Limited Company under the Companies Act 1994. SPL’s shares are quoted on both DSE and CSE. SPL is the first company signing PPA with BPDB to build small size power project in private sector with the objective of providing electricity to PBS through national Grid. SPL has so far successfully established seven power plants and is supplying total 215 MW of electricity to the national grid. SPL’s power plants comprises as follows: i) Ashulia plant - 44.75 MW ii) Chandina plant - 24.50 MW iii) Madhabdi plant- 35.30 MW iv) Rupganj plant - 33 .00 MW v) Jangalia plant- 33.00 MW vi) Maona plant - 33.00 MW vii) Ullapara plant - 11.00 MW Considering the immense opportunities, the company is striving to establish more power plants around the country. The company is also planning to explore energy markets in Sri Lanka and Vietnam. Cosmopolitan Traders (Pvt.) Ltd (CTL) Cosmopolitan Traders (Pvt.) Ltd (CTL) is a holding company involved in port related businesses such as container depot, liquid storage terminal, gas terminal, shipping and other businesses. Summit Shipping Ltd. (SSL) Summit Shipping Limited (SSL), a private limited company was incorporated in 2nd June 1998 to operate in transportation of liquid products. Cosmopolitan Traders (Pvt.) Ltd., a sister concern of Summit Group, is the major shareholder of the shipping company. Subsequent to its incorporation, SSL executed a 15-year ‘Transportation Agreement’ with United Summit Coastal Oil Limited (USCOL). Presently SSL operates two tankers with a load capacity of 1,800 MT and 1,200 MT respectively. Expansion plans of the company include procurement of ocean going tankers for transportation of furnace oil, edible oil and LPG from international market to Bangladesh. SSL has also implemented ISO 9002 Quality Management System (QMS) in 2001. This was the first ISO 9002 certified shipping company in Bangladesh.

18

United Summit Coastal Oil Ltd. (USCOL) United Summit Coastal Oil Ltd. (USCOL), a joint venture between Summit, United and El Paso International, USA, is the first private sector energy oil management company of Bangladesh. This company was formed with the goal of managing the furnace oil requirements of the country’s emerging private sector power generation companies. Leveraging on the expertise of a major integrated oil company El Paso International USA, USCOL actively participates in sourcing, trading and supplying energy oil in Bangladesh. The principal client of USCOL is Khulna Power Company Ltd., which requires furnace oil to fire its generators. USCOL also actively markets its expertise to other barge mounted power plants operational in Bangladesh, to other power producers who require oil-based fuel for power generation. Summit Alliance Port Ltd. Located on both sides of the Beach road which is 7 km away from the multipurpose berths of the Chittagong port, Summit Alliance Port is currently spread over an area of 17 acres. The port has a 40,000 sft warehouse capable of handling CFS stuffing upto 1,000 TEUs monthly and ICD with handling capacity of about 4,500 TEUs for storage of empty containers at any time. SUMCYNET SUMCYNET is an innovative Web Design and Software Development company. The company is composed of team of talented, experienced professionals, inspired by life, to generate the best quality work. The excellence of work supported by the company is reflected in the client's satisfaction. With extended experience and comprehensive knowledge, Sumcynet believes to have a full understanding of its client's requirements and how to attend to them in the best way possible within their specific time frame. The customers are presented with top of the range, user-friendly, striking and interactive updated website. The focus is to make sure that the client’s business is SEEN! The web designs/pages are 100% originals and are designed to the highest standards. The company ensures that clients receive personalized care round the clock. Everything at Sumcynet Web Design is done in-house. The company strives to create professional website for businesses at affordable price. UNITED ENTERPRISES & CO. LTD – UNITED GROUP OF BANGLADESH United Group has grown into one of the leading business houses in Bangladesh since its inception in 1978. United Group focuses in providing value added services and fostering business including provision of total solutions to an increasingly developing economy of Bangladesh. United Group’s fundamental strength is its commitment and enthusiasm to provide an excellent service for customers. Since the beginning of the last decade the objectives of the group has been to participate and take up investment opportunities in selected key infrastructure sectors and enables it to meet the challenges of the new century. From its inception the group’s focus has been to invest in key infrastructure areas. The key sectors where the group is currently engaged are power generation, civil & hydro engineering, real estate developments, land port services on a build, own and operate basis, international university, multi specialty hospital, shared banking ATM network, textile mills, polymer industries, heavy construction equipments division, passenger lift & escalators, turnkey solutions etc. The key sector in which it is engaged includes:

Manufacturing Energy& Power generation Broadcasting and communications Port & Maritime transportation Textile mills Real Estate and Constriction Healthcare and Hospital Education

19

United Enterprises & Company Limited United Enterprises & Co. Ltd. was established in mid-July 1978. The company expanded its areas of business covering power generation, sub-stations, broadcasting and telecommunications, maritime transportation and freights and the turnkey solutions and system management. United Enterprises participated in various nation-building tasks of the GOB. NOVO Healthcare & Pharma Ltd. NOVO Healthcare & Pharma Ltd. started its journey in 2004 and has since gone on to become one of the most trusted brands by doctors across the various fields of medical practice. Keeping in line with the norm at United Group, NOVO is also a pioneering company among the other key players in the field of pharmaceutics. With its cutting edge technology, NOVO has been successfully manufacturing bulk drugs (RTF Pellets) since its inception. As a matter of fact, it is the first company in Bangladesh which has been approved by the Drugs Authority (DA) for producing such bulk pellets. Through rigorous research and development and thorough dedication, they are currently manufacturing very specialized pellets of PPIs, Hematinics, etc. As a matter of fact, a significant quantity of this is presently being used by a large number of local pharmaceutical companies on a daily basis. This alone is a testament to how the company has heralded a new era in the Bangladesh Pharmaceutical sector with its ever-evolving portfolio of powerful and precision-tuned pharmaceutical products that help people to live healthier lives. NOVO's concern for quality is reflected in every aspect of its products – from raw materials to packaging materials. Utilizing quality ingredients in our manufacturing processes, fully equipped quality control laboratories and state of the art production plants, the firm has been organized with modern sophisticated technology that is continuously upgraded and standardized to meet the highest level of international standards. In fact we are one of the few companies in Bangladesh who have received the World Health Organization (WHO) certification for Current Good Manufacturing Practices from the Drug Directorate. In the analytical and the micro biological laboratories; young, energetic and skilled professionals are working with a great sense of responsibility to ensure quality of all the products that leave through the factory gates. Along with various commonly acceptable dosage forms like tablets, capsules, liquid, cream & ointment (LCO) as well as Powder for Suspension (PFS), a wide range of life saving antibiotics and other pharmaceutics are predominant in NOVO's product line. United Hospital Ltd United Hospital Ltd was born out of a vision to provide a complete and one-stop healthcare solution to the people of Bangladesh. Opening its doors in August 2006 and situated besides the picturesque Gulshan Lake, this hospital is one of the largest private sector healthcare facilities in Bangladesh. With a capacity to house over 450 patients and established across a total covered area of over 400,000 sft, the hospital has 11 state of the art operation theatres to cater to the needs of our varied patient base. Departments of cardiology, gynaecology, orthopaedic and paediatrics of United Hospital are staffed by the most esteemed doctors in their respective fields. As an example, a glimpse at our cardiology department would reveal that till date we have conducted over 2300 open heart surgeries and over 8300 angiograms and angioplasty operations. That’s over 12 heart related surgeries per day alone since our inception. With its technology and expertise, and with the support of very friendly staff, United Hospital strives each day to be the number one healthcare provider, not only within Bangladesh but within the Asia-Pacific region. Malancha Holdings Ltd In January 2007 Malancha Holdings Ltd. was born out of the necessity for uninterrupted, quality power supply to the industries housed within the Export Processing Zones (EPZ) of Bangladesh. Currently operating a 35 megawatt unit in Dhaka EPZ and a 44 megawatt unit in Chittagong EPZ, this company allows its clients to concentrate only on their core business rather than worrying

20

about their energy requirements. The total project cost of the plants stand at Tk. 3750 million and is powered by the latest Wartsila gas engines with the ability to produce 8.73 megawatts of electricity each. High voltage 33/11 KV substations comprising of two 16/25 MVA, 11/33 KV power transformers along with required length of 11 KV distribution lines have been built by MHL under each of the two project sites. Thus MHL has constructed multidisciplinary infrastructures like power generation, high voltage transmissions and distribution and high/low pressure gas pipelines for the project. In effect, this makes us the only true independent power generation and distribution company in all senses of the term. It is a model that we plan to replicate across all the EPZs of the country. On top of this unique achievement, MHL has been regularly providing its surplus energy to the Rural Electrification Board (REB) of Bangladesh, thus lighting up thousands of homes across the nation. We can only hope that one day our approach to power generation will make our country a shining beacon within the Asian region. Comilla Spinning Mills Ltd. In a country where the textiles industry is one of the major contributors to the GDP and indeed one of the largest earners of foreign exchange, Comilla Spinning Mills Ltd. has managed to make its mark as a maker of high quality cotton, polyester and mixed yarns. Established in 1996, the factory is nestled in the heart of Burichong, Comilla, spread over 13 acres of land, with 1100 full-time dedicated workers managing and operating the plant around the clock. With 18,000 spindles initially, it was projected to go under a progressive expansion program and methodical development through scientific research, design and creative plan of operation. As it stands now, the plant has almost 50,000 functioning spindles being complimented by other high-end European machineries producing roughly 14 tons of yarn a day. A fun fact – that is almost enough high quality yarn to cover over a 1000 kilometres a day. However, we have no plans of stopping now. In the near future, we hope to increase this capacity to almost 70,000 spindles. United International University Proper education solidifies the backbone of a nation – the youth who are destined to lead the country into the future. In 2003, United Group ventured into this noble professional sector by uniting together some of the finest academic minds in the nation under the banner of United International University. With an excellent library, well equipped laboratories, proper classrooms and student recreational facilities, it is an ideal place to excel in learning. It was surprising that even after a decade of operations; similar educational institutions were yet to achieve the same. UIU believes that only by providing the right environment could the desired results it achieved. Having such a campus was thus an absolute necessity. Even now the faculty is engaged in designing new disciplines that are relevant for the Bangladesh economic context. They would of course include Accounting, Textile Engineering, Pharmacology and Nursing departments, to name a few. With plans of opening a new major campus to ever-growing student base and faculty, steadily but surely it plans on becoming the largest private university in the country within the next few years. Neptune Land Development Ltd. Neptune Land Development Ltd. began its commercial operation as a premium real estate company in 2003 with United City being its flagship project. Imagine a scenic landscape where all the beauty that nature has to provide resides in perfect harmony with the excellence of Man’s creativity in the field of architecture. Imagine wide open fields echoing with children’s laughter, a lake beside which to sit and while an evening away, and the absolute tranquility of suburbia. It will be the most beautiful setting within one of the largest metropolitan cities in the world. Located a stone’s throw distance away from the US Embassy in Baridhara, it can simply be described as a piece of heaven in Dhaka, where families can start their lives anew, secure in their knowledge that they reside in one of the finest of localities in the capital. With over 300 acres currently under development in United City and 650 plots already handed over to a most excellent clientele, the main goal of NLDL is to become the premier and most trusted

21