ima doha conference...draft qatar vat law 3 may 2017: draft vat implementation regulations...

TRANSCRIPT

IMA Doha ConferenceGCC VAT Update

15 September 2019

01 Section

Current Status of

GCC VAT

Page 3 GCC Value Added Tax

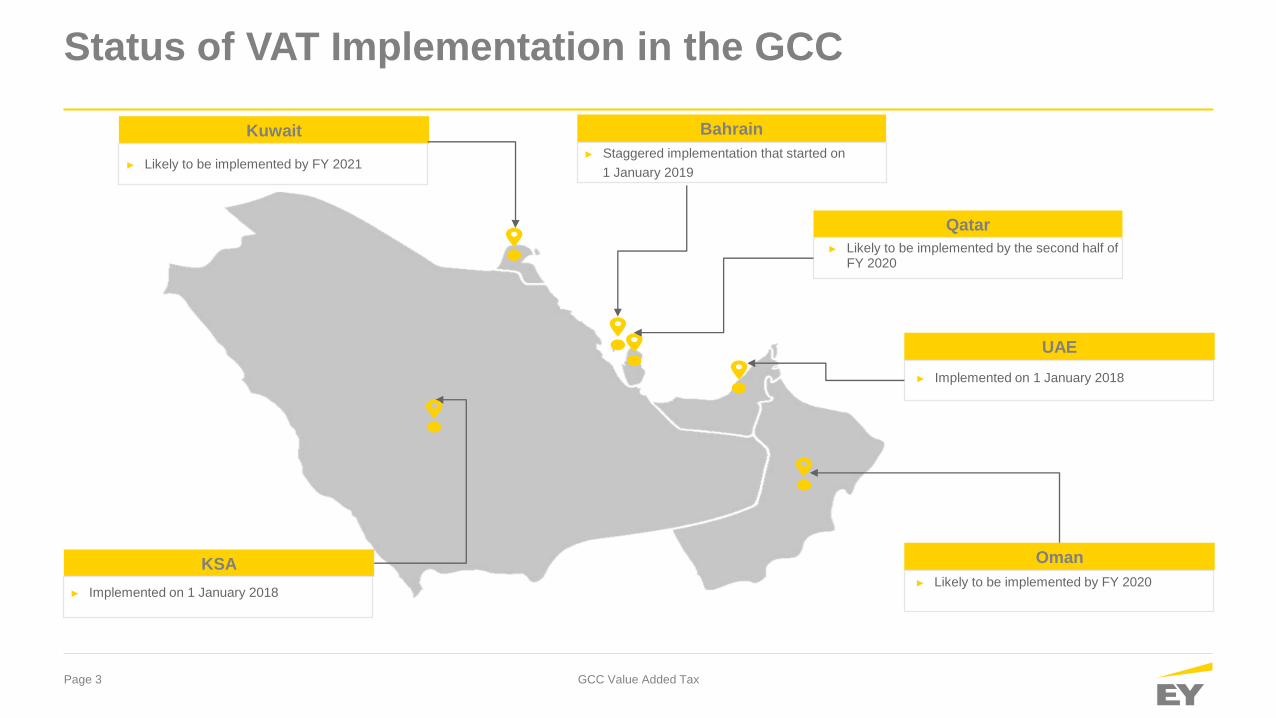

Status of VAT Implementation in the GCC

Kuwait

► Likely to be implemented by FY 2021

KSA

► Implemented on 1 January 2018

Bahrain

► Staggered implementation that started on

1 January 2019

Qatar

► Likely to be implemented by the second half of FY 2020

UAE

► Implemented on 1 January 2018

Oman

► Likely to be implemented by FY 2020

Page 4 GCC Value Added Tax

Developments in the Qatar VAT Legislation

► 3 May 2017: Council of Ministers approval of the GCC VAT Framework Agreement.GCC VAT

Framework

► 3 May 2017: Draft VAT law circulated among a few government-affiliated companies

for comment.Draft Qatar VAT

Law

► 3 May 2017: Draft VAT Implementation regulations circulated among a few

government –affiliated companies for comment.

Draft VAT

Regulations

► No time lines as yet announced for approval of the final VAT regulations. The draft

regulations, at this point, is with the Council of Ministers for review.

Final VAT

Regulations

Introduction of

VAT

► It was announced that VAT will not be implemented in 2019. Based on discussions

with the Tax Authority, we expect that the VAT implementation date will be 1 July 2020.

Policy

discussions

► On-going discussions between the MoF and the large O&G companies and financial

sector players in Qatar to determine the VAT treatment for these sectors.

02 Section

Overview of VAT

Page 6 GCC Value Added Tax

What is VAT?

Direct vs. indirect tax:

► Direct tax — imposed and collected from the person who earns the income:

► Paid directly to the government by the taxpayer — usually through “pay as you earn”

► Tax liability cannot be passed onto someone else

► Indirect tax — collected from someone other than the person responsible for the tax:

► The supplier can pass on the burden of an indirect tax to the final consumer

► Should be neutral for the business supplier (unless consumptions stops there)

► VAT is not an income tax:

► VAT is a tax levied on the supply of goods and services made by a “taxable person” in the course of furtherance of

a business

► A comprehensive levy on the supply of goods and services

► Transaction based tax borne by the end consumer

► Paid in successive stages, i.e., for each transaction in the manufacturing and

distribution process

► Invoice based tax credit mechanism with audit trail for authorities

VAT

Page 7 GCC Value Added Tax

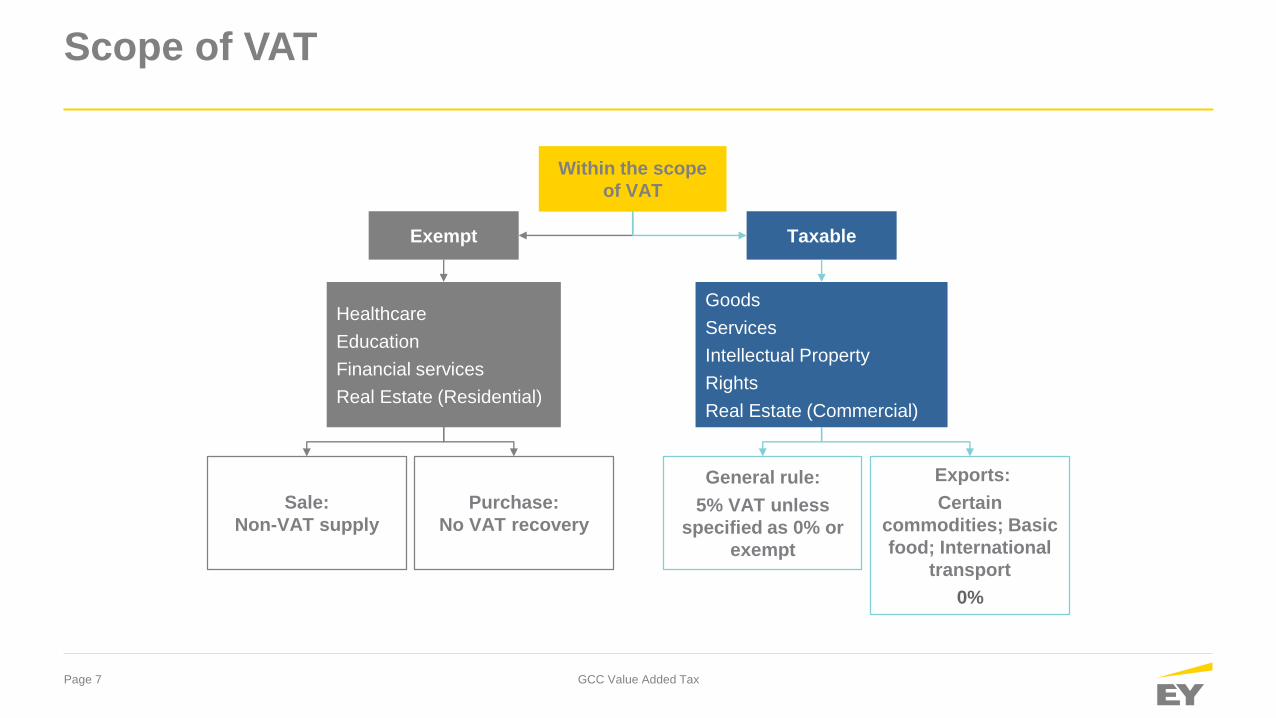

Scope of VAT

Within the scope

of VAT

General rule:

5% VAT unless

specified as 0% or

exempt

Exports:

Certain

commodities; Basic

food; International

transport

0%

Healthcare

Education

Financial services

Real Estate (Residential)

Goods

Services

Intellectual Property

Rights

Real Estate (Commercial)

Exempt Taxable

Sale:

Non-VAT supply

Purchase:

No VAT recovery

Page 8 GCC Value Added Tax

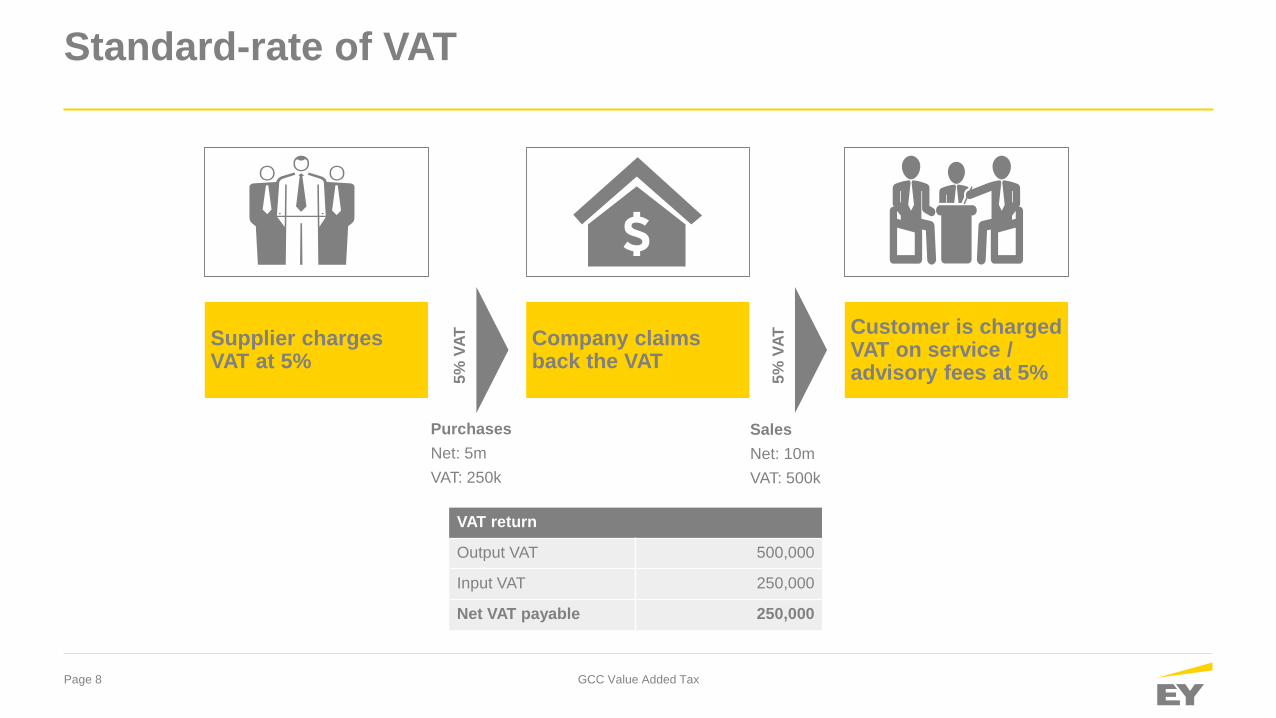

Standard-rate of VAT

Purchases

Net: 5m

VAT: 250k

Sales

Net: 10m

VAT: 500k

VAT return

Output VAT 500,000

Input VAT 250,000

Net VAT payable 250,000

Supplier charges VAT at 5%

Company claims back the VAT

Customer is charged VAT on service / advisory fees at 5%5

% V

AT

5%

VA

T

Page 9 GCC Value Added Tax

Zero-rate of VAT

Purchases

Net: 5m

VAT: 250k

Sales

Net: 10m

VAT: –

VAT return

Output VAT –

Input VAT 250,000

Net VAT refundable 250,000

Supplier charges VAT at 5%

Company claims back the VAT

Services or credit are exported and customer is charged 0% VAT 5

% V

AT

0%

VA

T

Page 10 GCC Value Added Tax

VAT Exemption

Purchases

Net: 5m

VAT: 250k

Sales

Net: 10m

VAT: –

Supplier charges VAT at 5%

Company cannot claim back the VAT

Customer does not pay VAT on the Murabaha profit spread payments5

% V

AT

VA

T e

xe

mp

t

The 250k of VAT incurred is not recoverable and becomes an absolute cost.

03 Section

VAT Impact and EY

Project Plan

Page 12 GCC Value Added Tax

VAT Impact Across the Organization

VAT implementation

challenges

Finance and administration

► Cash flow

► Transaction

► VAT refunds

► Process and

controls

► Input tax credits

► Tax payment and

accounting period

► Imported services

Information Technology

► System changes

► Data management

► System requirements

► Invoicing

► Archiving

► Auditability

► ERP or tax engines

Procurement

► Multiple transaction types

► Vendors registration

► Preferential treatment

Business

► Business structure

► Operating model

► Efficiency

► Reputation risk

► Large number of stakeholders

Sales and marketing

► Competitive pricing

► Long term contracts

► Demand impact

Compliance

► Group registration

► Compliance

► Tax authority audits

► Penalties and interest

► Quarterly VAT declarations

Human Resources

► Fringe benefits

► Communication

► Staff education and training

► Policy and procedures

Page 13 GCC Value Added Tax

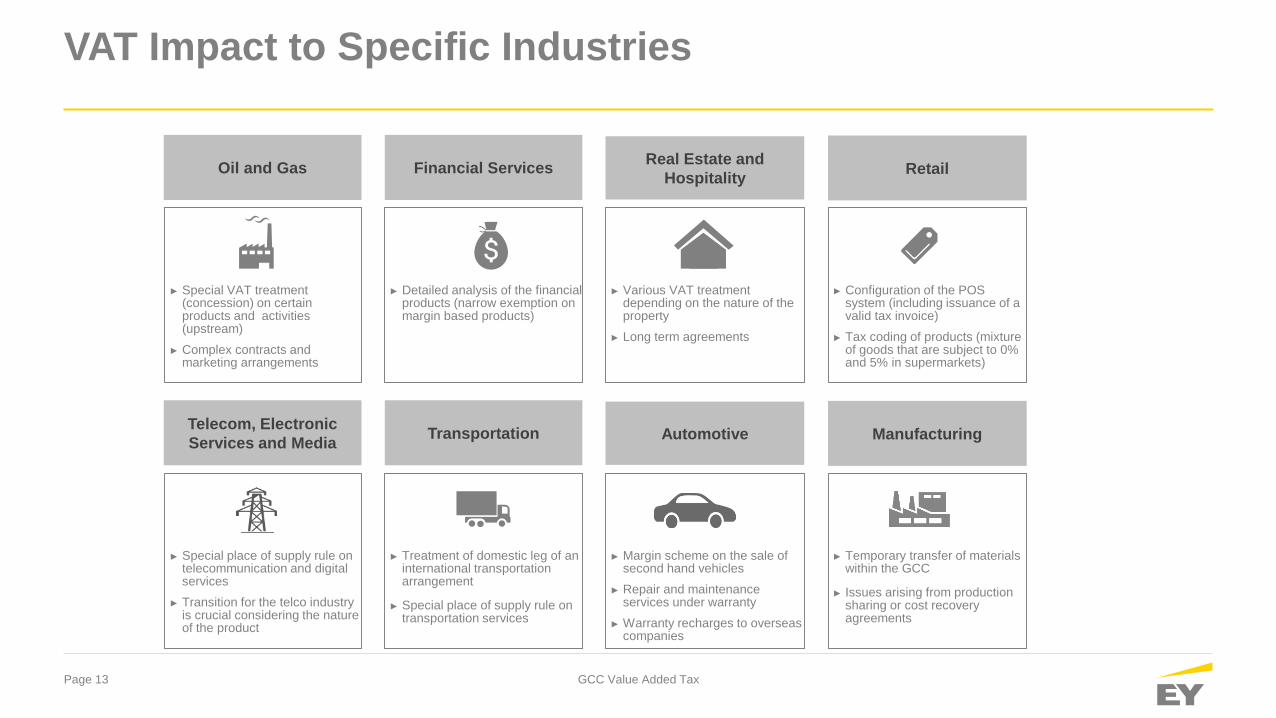

► Special place of supply rule on telecommunication and digital services

► Transition for the telco industry is crucial considering the nature of the product

► Treatment of domestic leg of an international transportation arrangement

► Special place of supply rule on transportation services

► Temporary transfer of materials within the GCC

► Issues arising from production sharing or cost recovery agreements

► Margin scheme on the sale of second hand vehicles

► Repair and maintenance services under warranty

► Warranty recharges to overseas companies

AutomotiveTelecom, Electronic

Services and MediaTransportation Manufacturing

VAT Impact to Specific Industries

► Special VAT treatment (concession) on certain products and activities (upstream)

► Complex contracts and marketing arrangements

► Detailed analysis of the financial products (narrow exemption on margin based products)

► Configuration of the POS system (including issuance of a valid tax invoice)

► Tax coding of products (mixture of goods that are subject to 0% and 5% in supermarkets)

► Various VAT treatment depending on the nature of the property

► Long term agreements

Real Estate and

HospitalityOil and Gas Financial Services Retail

Page 14 GCC Value Added Tax

VAT Readiness Project Plan

Post-implementation

assistance

VAT implementation

support

Solution design and

implementationVAT issues identification

Phase I Phase II Phase III Phase IV

► Key steps to ensure VAT

readiness

► Contract reviews

► Staff readiness

► Process reviews

► VAT process design or review

► VAT compliance requirements

► IT systems implementation

► Tax coding and transactional

analysis

► Communication strategy

► VAT returns review

► Ongoing compliance and

advisory

VAT ready

► Review of IT test result

► Advice on drafting VAT manual

► Conduct VAT training sessions

Discussion

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory

services. The insights and quality services we deliver help build trust

and confidence in the capital markets and in economies the world

over. We develop outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play a critical role

in building a better working world for our people, for our clients and

for our communities

EY refers to the global organization, and may refer to one or more, of

the member firms of Ernst & Young Global Limited, each of which is

a separate legal entity. Ernst & Young Global Limited, a UK company

limited by guarantee, does not provide services to clients. For more

information about our organization, please visit ey.com.

The MENA practice of EY has been operating in the region since

1923. For more than 90 years, we have grown to more than 6,000

people united across 20 offices and 15 countries, sharing the same

values and an unwavering commitment to quality. As an

organization, we continue to develop outstanding leaders who deliver

exceptional services to our clients and who contribute to our

communities. We are proud of our accomplishments over the years,

reaffirming our position as the largest and most established

professional services organization in the region.

© 2019 EYGM Limited.

All Rights Reserved.

ED None

This material has been prepared for general informational purposes only and is not intended

to be relied upon as accounting, tax, or other professional advice. Please refer to your

advisors for specific advice.

ey.com/mena