impact analysis of options for implementing article …...final report impact analysis of options...

TRANSCRIPT

Final Report

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive)

02 August 2013

Submitted to:

Wojciech Winkler

European Commission

DG Climate Action

B-1049 Brussels

BELGIUM

Submitted by:

ICF International

3rd Floor

Kean House

6 Kean Street

London WC2B 4AS

U.K.

Final Report

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive)

02 August 2013

Submitted to:

Wojciech Winkler

European Commission

DG Climate Action

B-1049 Brussels

BELGIUM

Submitted by:

ICF International

3rd Floor

Kean House

6 Kean Street

London WC2B 4AS

U.K.

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 i

Table of Contents

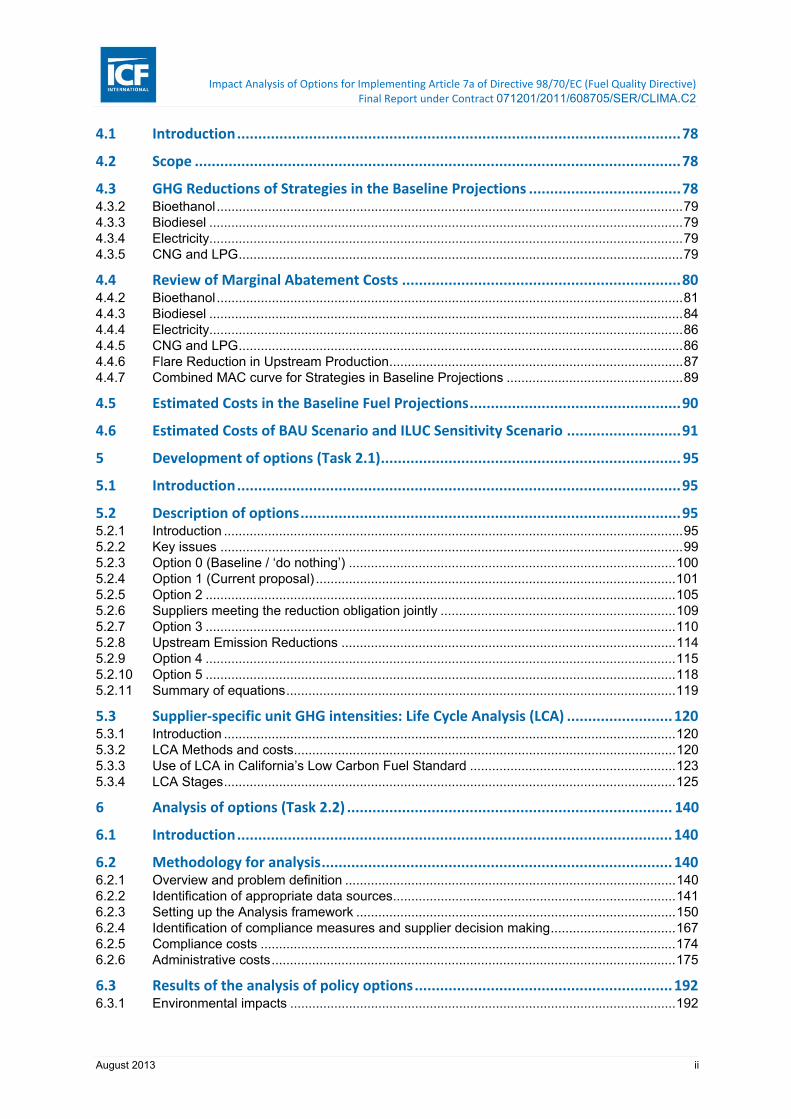

Table of tables ................................................................................................................ iv

Table of figures ................................................................................................................. viii

1 Introduction ........................................................................................................... 1

1.1 Objectives of Project .............................................................................................. 1

1.2 This Report ............................................................................................................. 1

2 Develop Fuel Projections under Baseline Reporting (Task 1.1) ............................... 2

2.1 Introduction ........................................................................................................... 2

2.2 Literature review ................................................................................................... 2

2.3 Preliminary Assessment ......................................................................................... 3

2.4 In‐Depth Assessment ........................................................................................... 11 2.4.1 The EU Transport GHG: Routes to 2050 – Illustrative Scenarios Tool (SULTAN) ................ 11 2.4.2 The World Energy Outlook 2011 (WEO 2011) ....................................................................... 14 2.4.3 International Energy Outlook 2012 (IEO 2011) ...................................................................... 17 2.4.4 Wood Mackenzie Report ........................................................................................................ 18 2.4.5 WORLD Model ........................................................................................................................ 20 2.4.6 Overall Comments .................................................................................................................. 22

2.5 2020 Baseline Fuel Demand Projections ............................................................... 22 2.5.1 Assumptions for the 2020 Baseline Forecast Model .............................................................. 22 2.5.2 Meta-Analysis Forecast Begins with Data from IEA WEO 2011 ............................................ 24 2.5.3 Apportion Total Fuel Demand from IEA Midterm Report to the Road Transport Sector ........ 24 2.5.4 Scaled Projections to 2020 ..................................................................................................... 24 2.5.5 Incorporate Electricity and CNG Demand .............................................................................. 26 2.5.6 EC Supply of Biofuels ............................................................................................................. 28 2.5.7 2020 Baseline Demand Scenario Combination ...................................................................... 29

2.6 Feedstock and Product Projections ...................................................................... 29 2.6.1 Introduction to the WORLD Model .......................................................................................... 29 2.6.2 Key drivers of Product Trade in WORLD Model ..................................................................... 29 2.6.3 Summary of Premises for Model Run ..................................................................................... 31 2.6.4 Model Output and Results ...................................................................................................... 35 2.6.5 2020 Crude Trade ................................................................................................................... 37 2.6.6 Refinery Capacities and Utilisation ......................................................................................... 43 2.6.7 2020 Fuel Trade ..................................................................................................................... 55 2.6.8 Factors Contributing to European Diesel and Petrol Market .................................................. 56

3 Baseline GHG Emissions and GHG Intensity (Task 1.2) .......................................... 69

3.1 Introduction ......................................................................................................... 69

3.2 Scope ................................................................................................................... 69

3.3 Baseline GHG Emissions and GHG Intensity .......................................................... 69

3.4 Sensitivity Analysis including ILUC Emissions ....................................................... 74 3.4.1 Introduction to GHG Emissions from ILUC ............................................................................. 74 3.4.1 Scenario to Demonstrate Sensitivity ....................................................................................... 76

4 Costs of the Baseline (Task 1.3) ............................................................................ 78

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 ii

4.1 Introduction ......................................................................................................... 78

4.2 Scope ................................................................................................................... 78

4.3 GHG Reductions of Strategies in the Baseline Projections .................................... 78 4.3.2 Bioethanol ............................................................................................................................... 79 4.3.3 Biodiesel ................................................................................................................................. 79 4.3.4 Electricity................................................................................................................................. 79 4.3.5 CNG and LPG ......................................................................................................................... 79

4.4 Review of Marginal Abatement Costs .................................................................. 80 4.4.2 Bioethanol ............................................................................................................................... 81 4.4.3 Biodiesel ................................................................................................................................. 84 4.4.4 Electricity................................................................................................................................. 86 4.4.5 CNG and LPG ......................................................................................................................... 86 4.4.6 Flare Reduction in Upstream Production ................................................................................ 87 4.4.7 Combined MAC curve for Strategies in Baseline Projections ................................................ 89

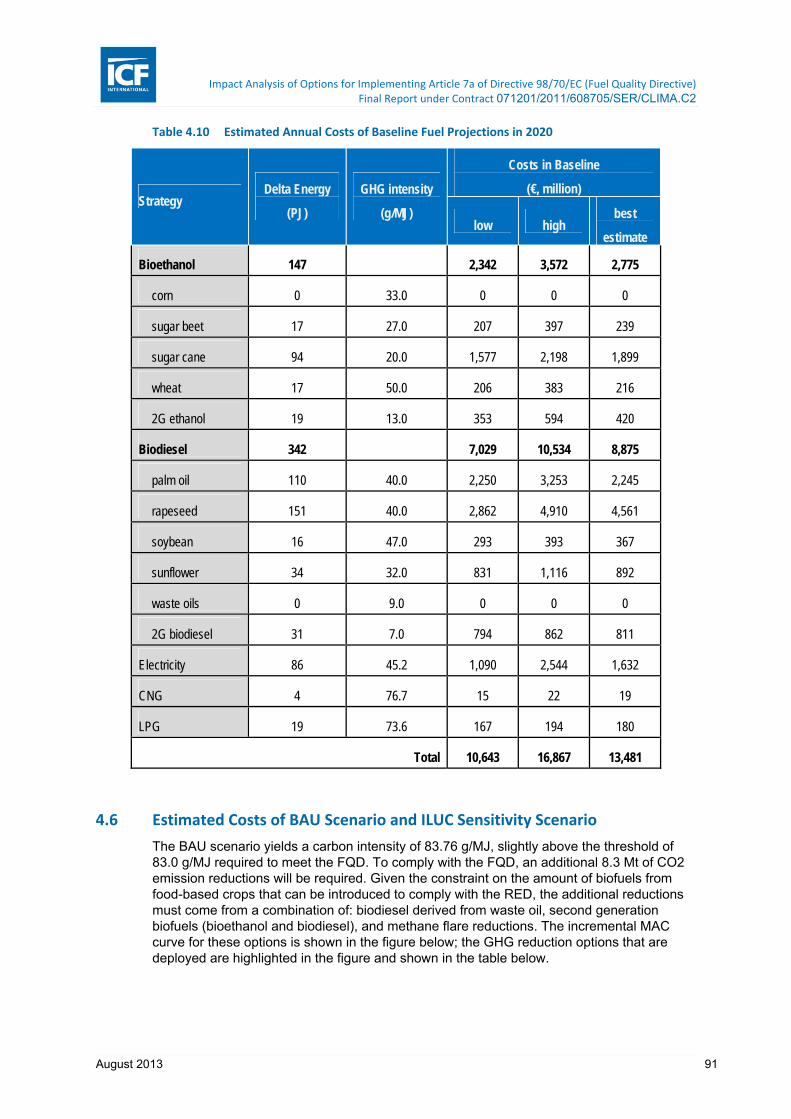

4.5 Estimated Costs in the Baseline Fuel Projections .................................................. 90

4.6 Estimated Costs of BAU Scenario and ILUC Sensitivity Scenario ........................... 91

5 Development of options (Task 2.1) ....................................................................... 95

5.1 Introduction ......................................................................................................... 95

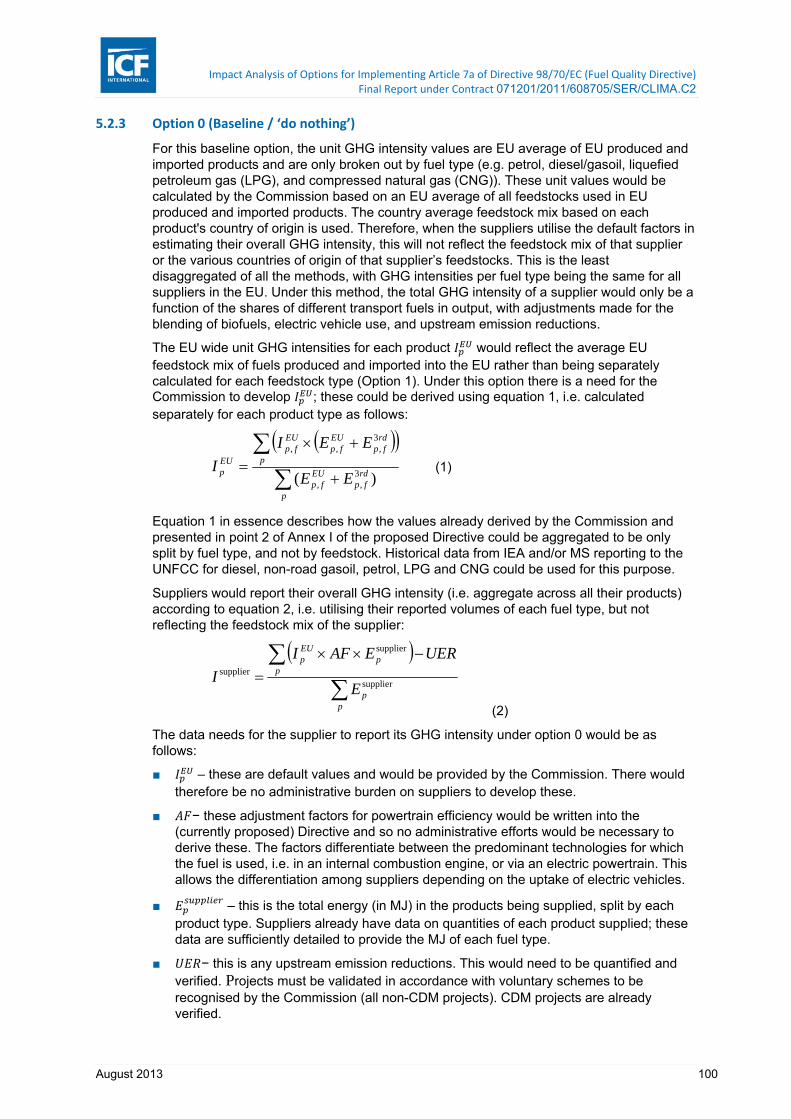

5.2 Description of options .......................................................................................... 95 5.2.1 Introduction ............................................................................................................................. 95 5.2.2 Key issues .............................................................................................................................. 99 5.2.3 Option 0 (Baseline / ‘do nothing’) ......................................................................................... 100 5.2.4 Option 1 (Current proposal) .................................................................................................. 101 5.2.5 Option 2 ................................................................................................................................ 105 5.2.6 Suppliers meeting the reduction obligation jointly ................................................................ 109 5.2.7 Option 3 ................................................................................................................................ 110 5.2.8 Upstream Emission Reductions ........................................................................................... 114 5.2.9 Option 4 ................................................................................................................................ 115 5.2.10 Option 5 ................................................................................................................................ 118 5.2.11 Summary of equations .......................................................................................................... 119

5.3 Supplier‐specific unit GHG intensities: Life Cycle Analysis (LCA) ......................... 120 5.3.1 Introduction ........................................................................................................................... 120 5.3.2 LCA Methods and costs ........................................................................................................ 120 5.3.3 Use of LCA in California’s Low Carbon Fuel Standard ........................................................ 123 5.3.4 LCA Stages ........................................................................................................................... 125

6 Analysis of options (Task 2.2) ............................................................................. 140

6.1 Introduction ....................................................................................................... 140

6.2 Methodology for analysis ................................................................................... 140 6.2.1 Overview and problem definition .......................................................................................... 140 6.2.2 Identification of appropriate data sources ............................................................................. 141 6.2.3 Setting up the Analysis framework ....................................................................................... 150 6.2.4 Identification of compliance measures and supplier decision making .................................. 167 6.2.5 Compliance costs ................................................................................................................. 174 6.2.6 Administrative costs .............................................................................................................. 175

6.3 Results of the analysis of policy options ............................................................. 192 6.3.1 Environmental impacts ......................................................................................................... 192

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 iii

6.3.2 Administrative impacts .......................................................................................................... 199

7 Characterisation of affected sectors (Task 3.1) ................................................... 203

7.1 Introduction to the EU refining industry ............................................................. 203

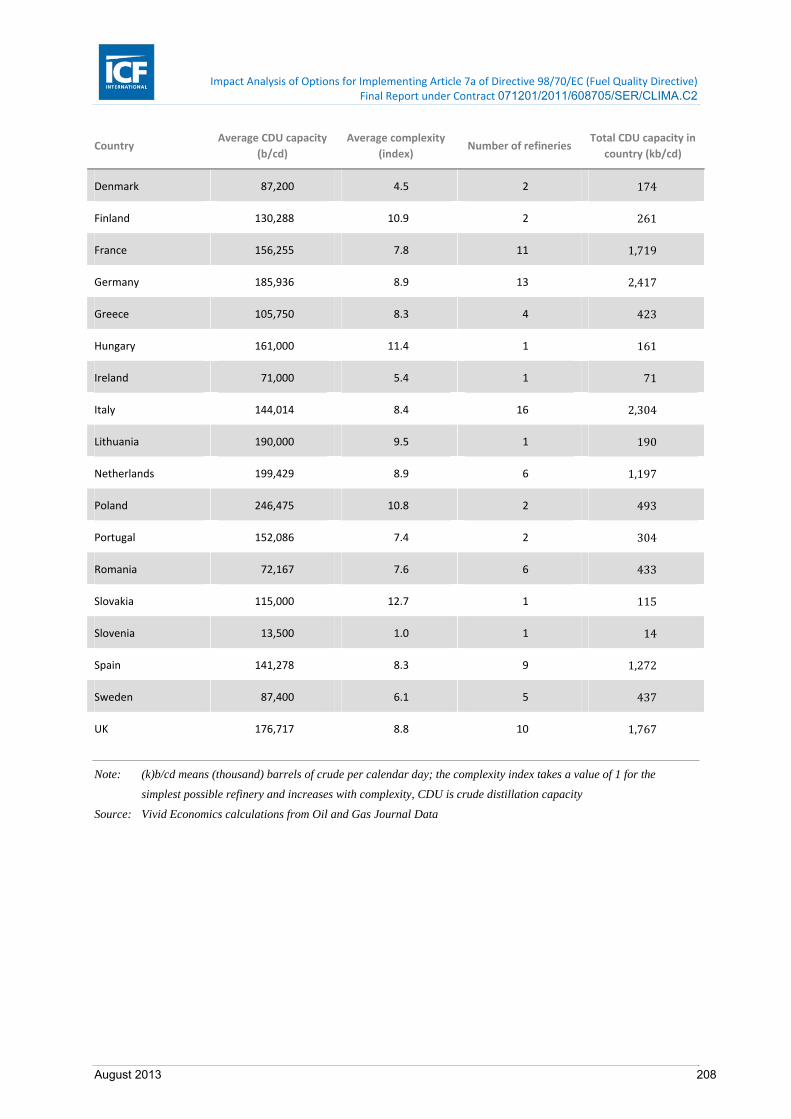

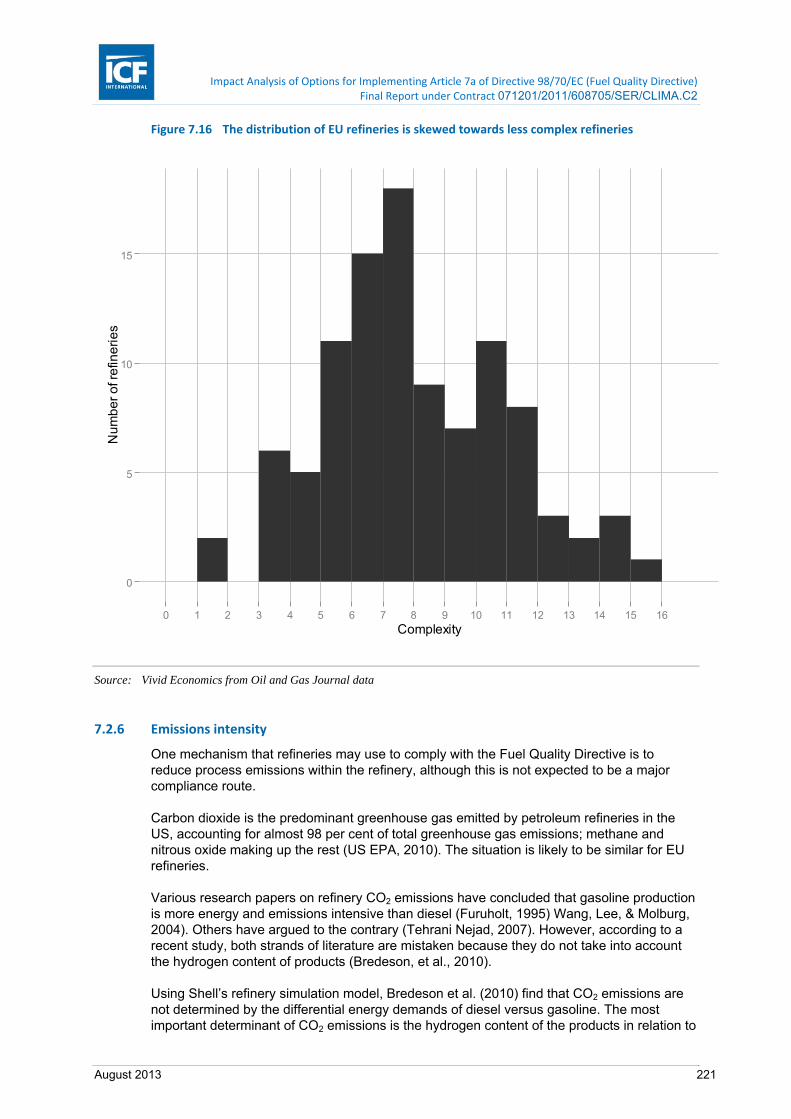

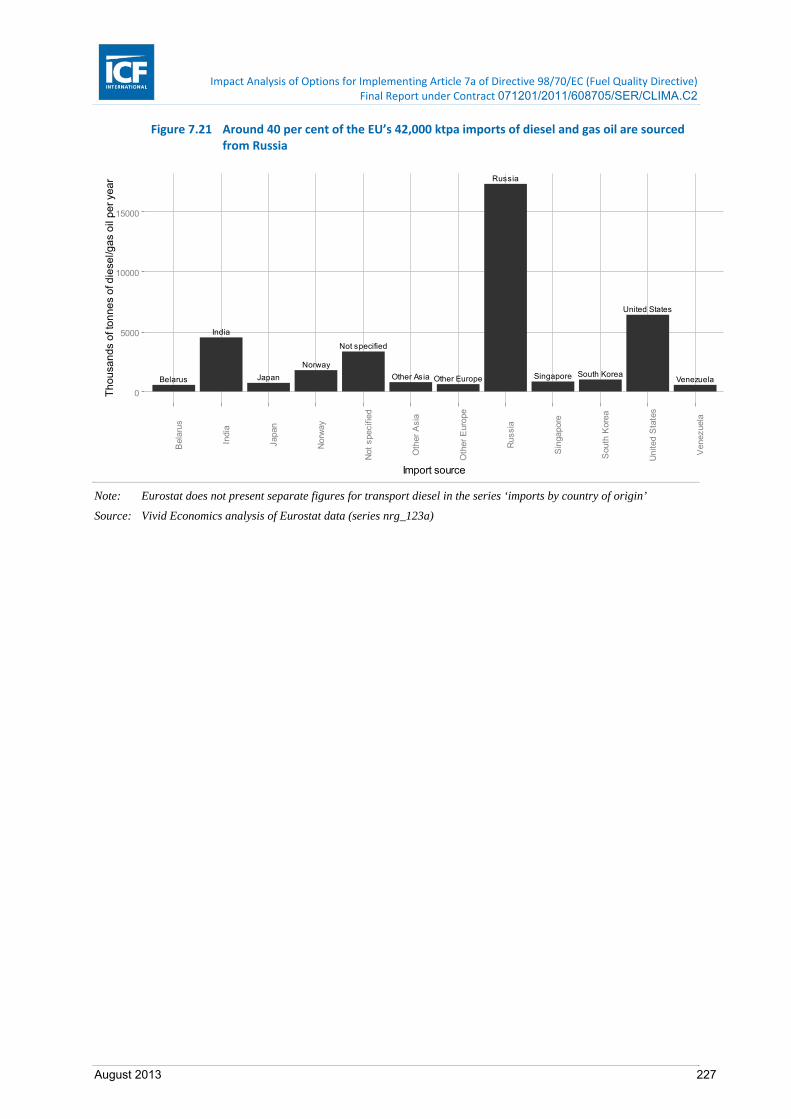

7.2 Structure of downstream industry ..................................................................... 205 7.2.1 Location and key statistics of the EU refining industry ......................................................... 205 7.2.2 Demand for refined products ................................................................................................ 211 7.2.3 Price elasticity of demand for refined product and refinery cost pass-through rates ........... 214 7.2.4 Profit margins in European refining ...................................................................................... 216 7.2.5 Complexity of EU refineries .................................................................................................. 219 7.2.6 Emissions intensity ............................................................................................................... 221 7.2.7 Trade in refined products ...................................................................................................... 224

8 Impacts of the Fuel Quality Directive on the EU road transport fuel market (Task 3.2) ........................................................................................................... 228

8.1 Introduction ....................................................................................................... 228

8.2 Main results ....................................................................................................... 229

8.3 Required emissions reduction in the EU transport fossil fuel market ................. 232

8.4 Analysis of options ............................................................................................. 233 8.4.1 Compliance cost curves ........................................................................................................ 233 8.4.2 EU transport fuel market effects ........................................................................................... 238 8.4.3 Crude market effects ............................................................................................................ 240 8.4.4 Product import market effects ............................................................................................... 240 8.4.5 Pump prices .......................................................................................................................... 241

Bibliography .................................................................................................................... 244

Appendix A – Further information on competitive impacts ............................................. 247

Appendix B ‐ Biofuel feedstock switching as an additional compliance method .............. 258

Appendix C – Pump Prices ............................................................................................... 261

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 iv

Table of tables

Table 2.1 Key characteristics for the projection ................................................................................. 2

Table 2.2 Preliminary Assessment of Reports to the European Commission .................................... 5

Table 2.3 Preliminary Assessment of Reports by Research and Government Agencies .................. 7

Table 2.4 Preliminary Assessment of Reports by Trade Organizations and Energy Companies ...... 9

Table 2.5 Summary of Rating for Important Reports and Studies After in-Depth Analysis .............. 11

Table 2.6 Detailed Assessment of the SULTAN Tool ...................................................................... 12

Table 2.7 Detailed Assessment of the WEO 2011 ........................................................................... 14

Table 2.8 Detailed assessment of International Energy Outlook. .................................................... 17

Table 2.9 Detailed Assessment of Wood Mackenzie Report. .......................................................... 19

Table 2.10 Detailed Assessment of WORLD Model .......................................................................... 21

Table 2.11 IEA 2009 Historical Fuel Consumption Data – Road Transport and Total ....................... 24

Table 2.12 Ratio of Specific Fuel Demand to Total Demand in 2017 Midterm .................................. 25

Table 2.13 2020 Scaled IEA Fuel Projections for EU-27 ................................................................... 25

Table 2.14 2020 Scaled IEA Fuel Projections for EU-27 Transport Sector ....................................... 25

Table 2.15 2020 On-Road Diesel and Off-Road Diesel Ratios from JEC Report .............................. 26

Table 2.16 2020 Scaled IEA Fuel Projections for EU-27 Transport Sector ....................................... 26

Table 2.17 2020 Fuel Projections for EU-27 Road Transport Sector ................................................. 27

Table 2.18 Petrol Demand in EU-27, 2006 – 2020 ............................................................................ 27

Table 2.19 Diesel Demand in EU-27, 2006 – 2020 ............................................................................ 28

Table 2.20 2020 EU-27 Road and NRMM Biofuel Supply Projections .............................................. 28

Table 2.21 Premise for WORLD Model 2020 Projections .................................................................. 32

Table 2.22 Summary of Crude Trade by Region of Origin in 2020 .................................................... 38

Table 2.23 Summary of Historical Crude Trade in 2010 .................................................................... 38

Table 2.24 Summary of Notional Crude Trade in 2020 ...................................................................... 41

Table 2.25 Announced European Refinery Closures ......................................................................... 43

Table 2.26 Summary of Refinery Projects Accounted for in the WORLD Model (‘Europe’ region) ... 44

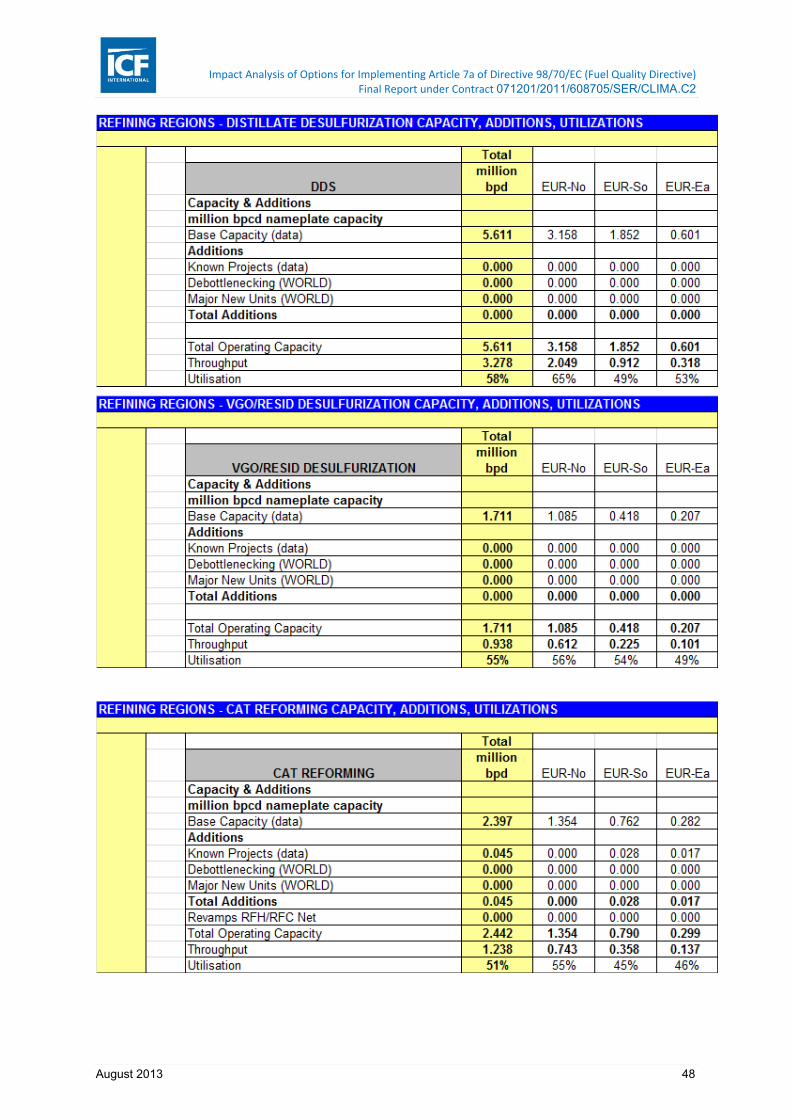

Table 2.27 European Refinery Process Unit Capacity Utilization in 2020 ......................................... 46

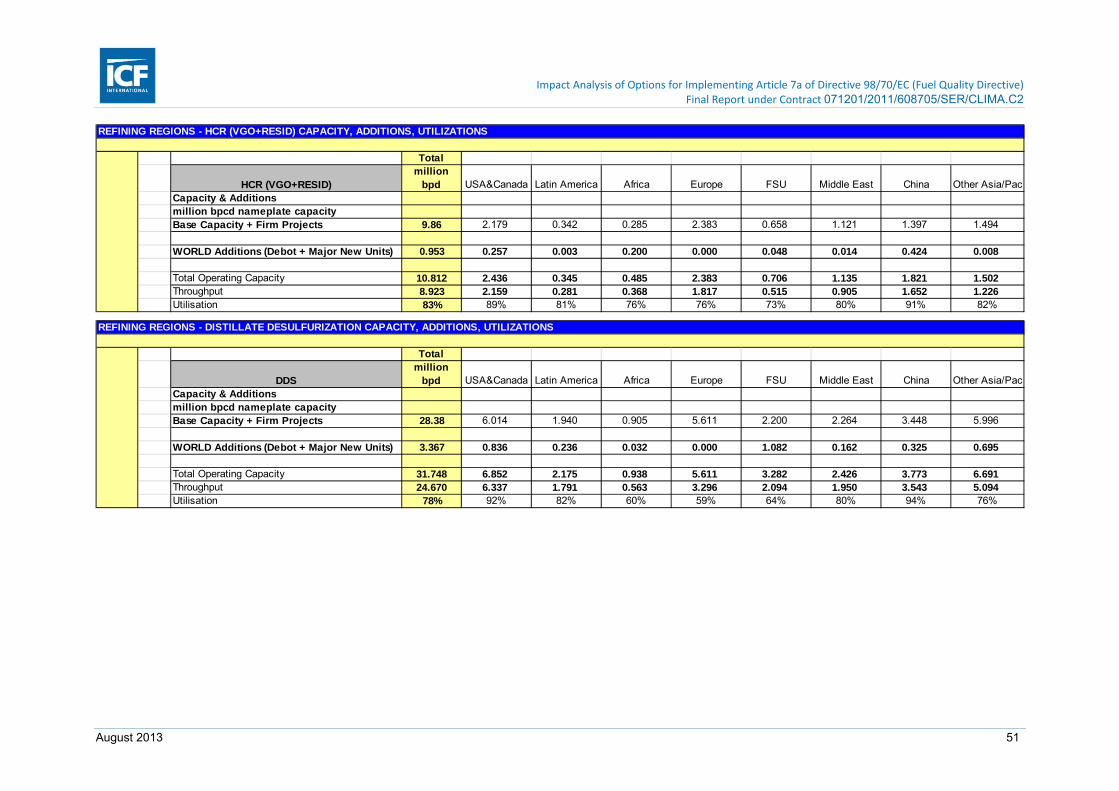

Table 2.28 Global Refinery Process Unit Capacity Utilization in 2020 ............................................... 49

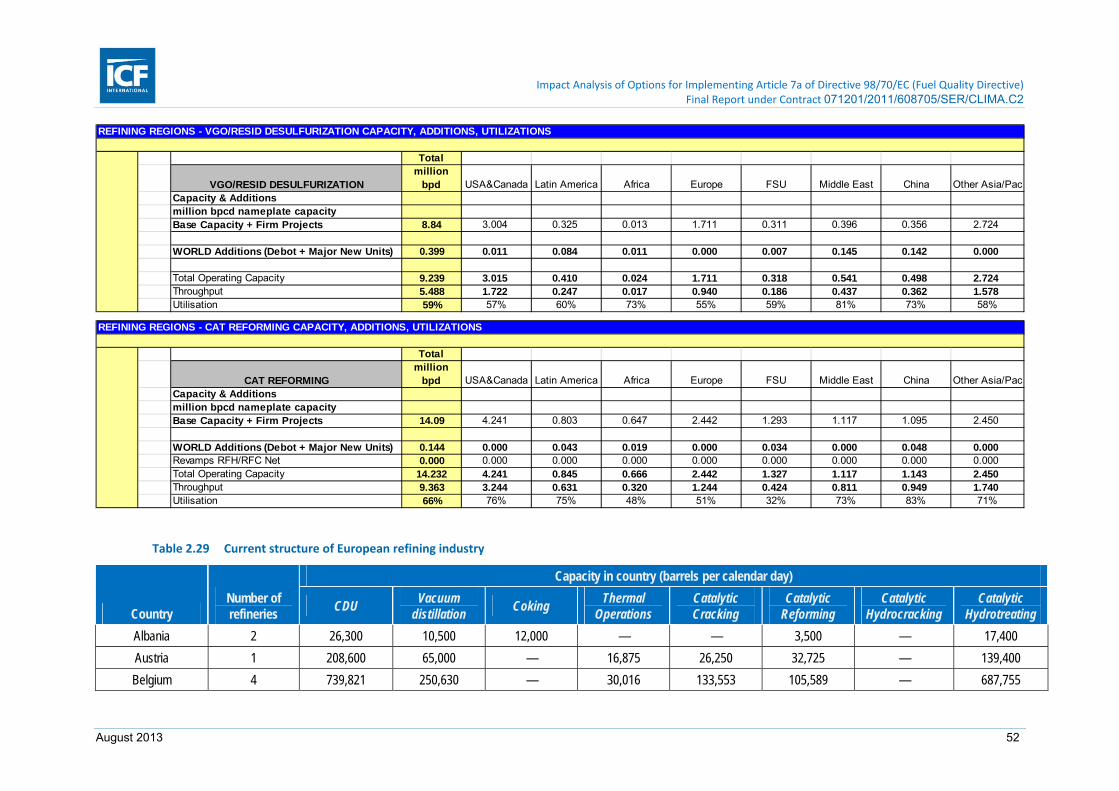

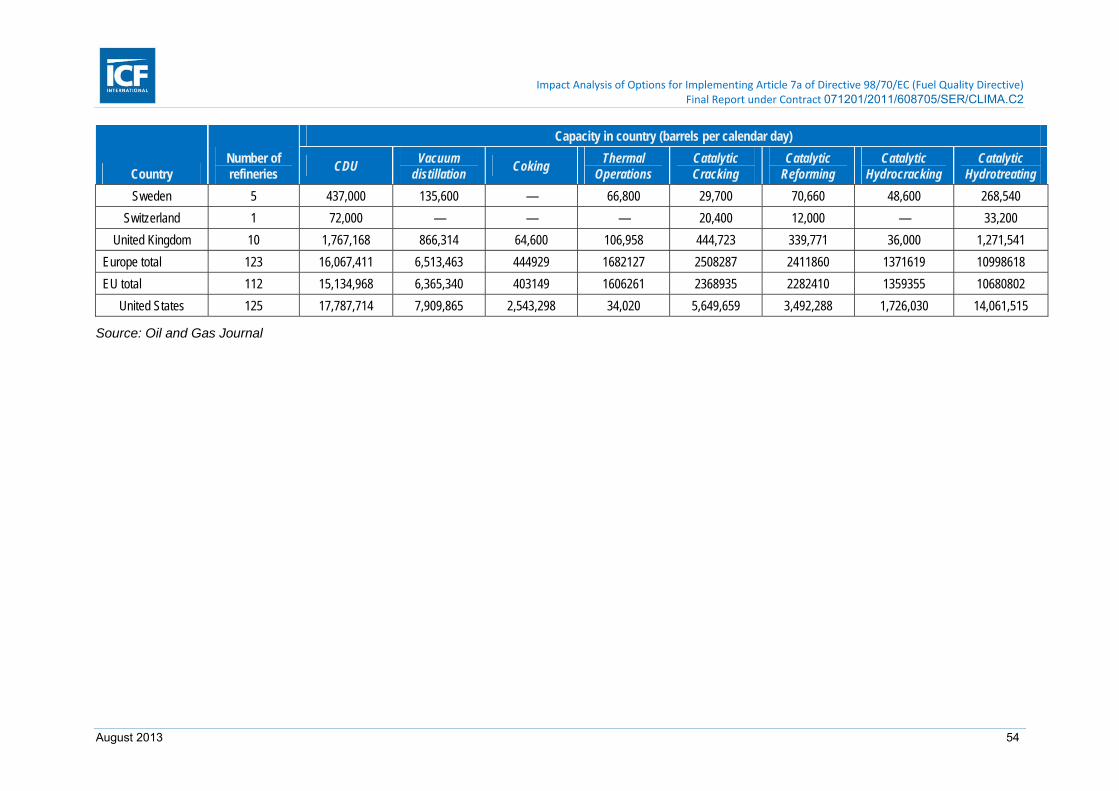

Table 2.29 Current structure of European refining industry ............................................................... 52

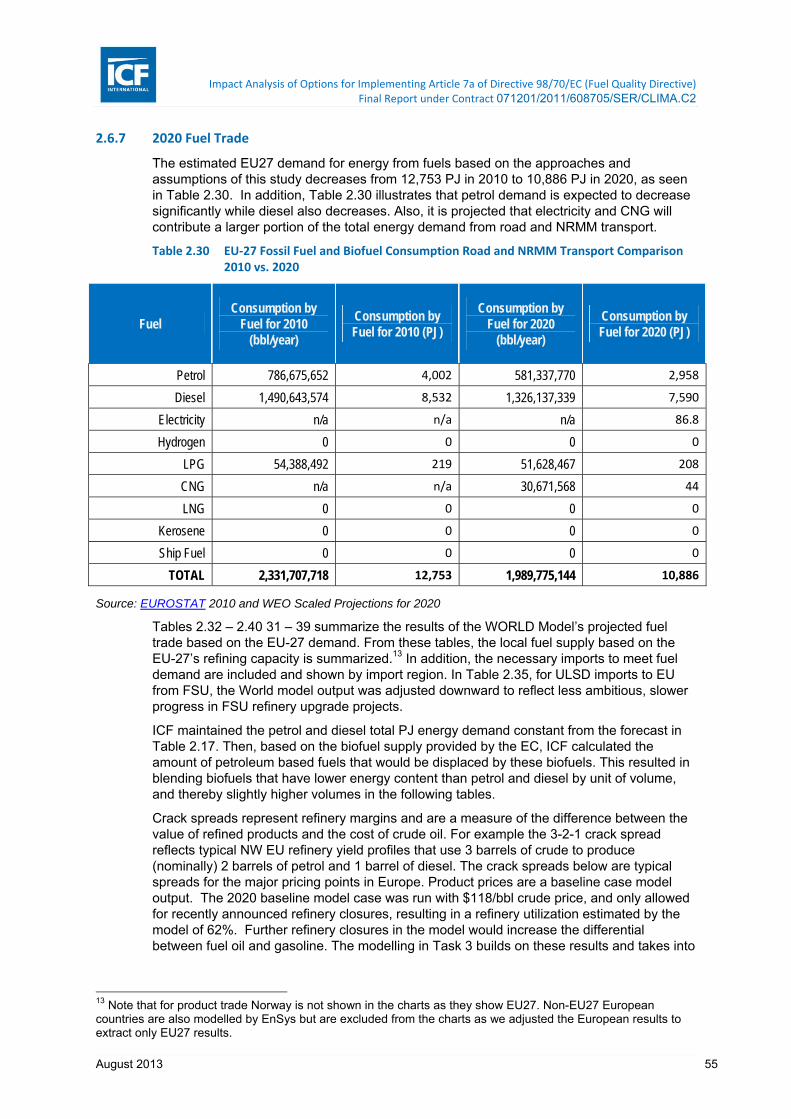

Table 2.30 EU-27 Fossil Fuel and Biofuel Consumption Road and NRMM Transport Comparison 2010 vs. 2020 ................................................................................................................... 55

Table 2.31 Crack Spreads in “Northern Europe” WORLD Model Region .......................................... 58

Table 2.32 Summary of Product Prices in 2020 WORLD Model Projection ...................................... 58

Table 2.33 2020 Petrol Trade (Fossil and Biofuel) ............................................................................. 60

Table 2.34 2020 Jet/Kerosene Trade ................................................................................................. 61

Table 2.35 Total ULSD Trade (Fossil and Biofuel) ............................................................................. 62

Table 2.36 2020 Total Distillate Trade (Fossil and Biofuel) ................................................................ 63

Table 2.37 2020 Total Residual Trade ............................................................................................... 64

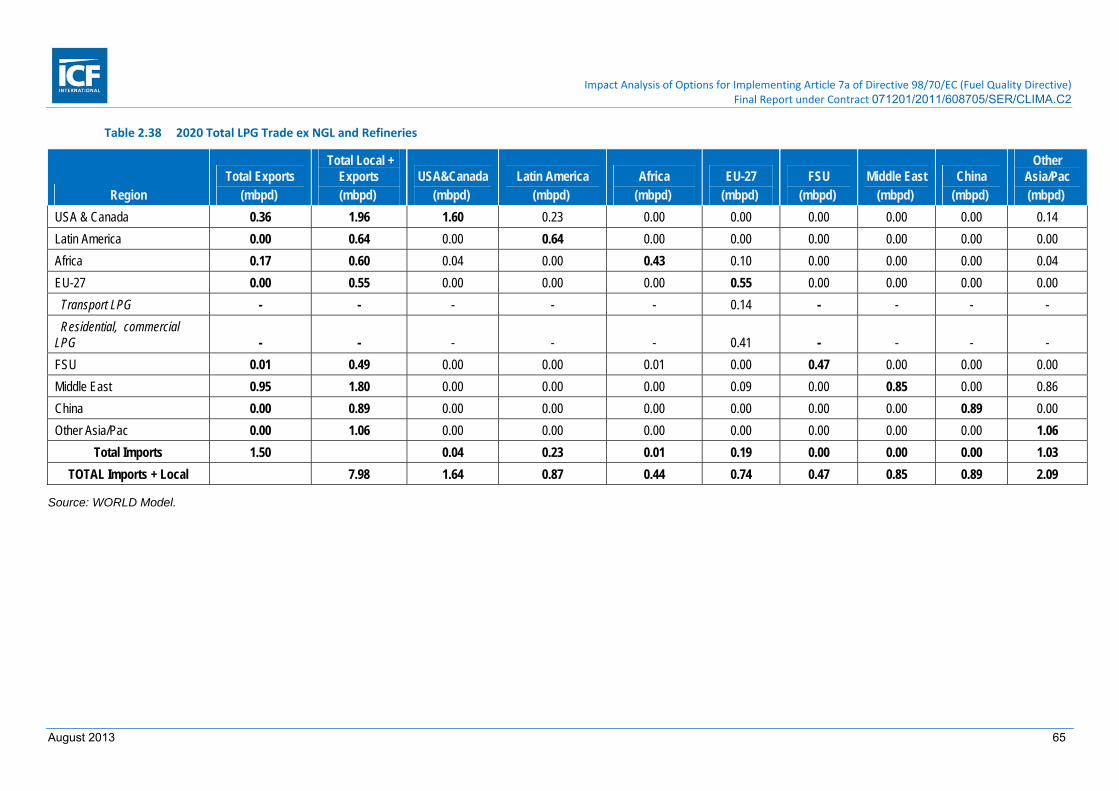

Table 2.38 2020 Total LPG Trade ex NGL and Refineries ................................................................ 65

Table 2.39 2020 Total Petrochemical Naphtha Trade (Fossil Fuel Only) .......................................... 66

Table 2.40 2020 Total GTL ULS Distillate Trade ............................................................................... 67

Table 2.41 2020 Total CTL ULS Distillate Liquids Trade ................................................................... 68

Table 3.1 Default GHG Intensity for Fossil Fuels 2010 .................................................................... 69

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 v

Table 3.2 GHG Intensity for Biofuels, ICF Study .............................................................................. 70

Table 3.3 GHG Intensity for Biofuels, FQD Annex V ........................................................................ 70

Table 3.4 Emissions intensity of displaced output ............................................................................ 72

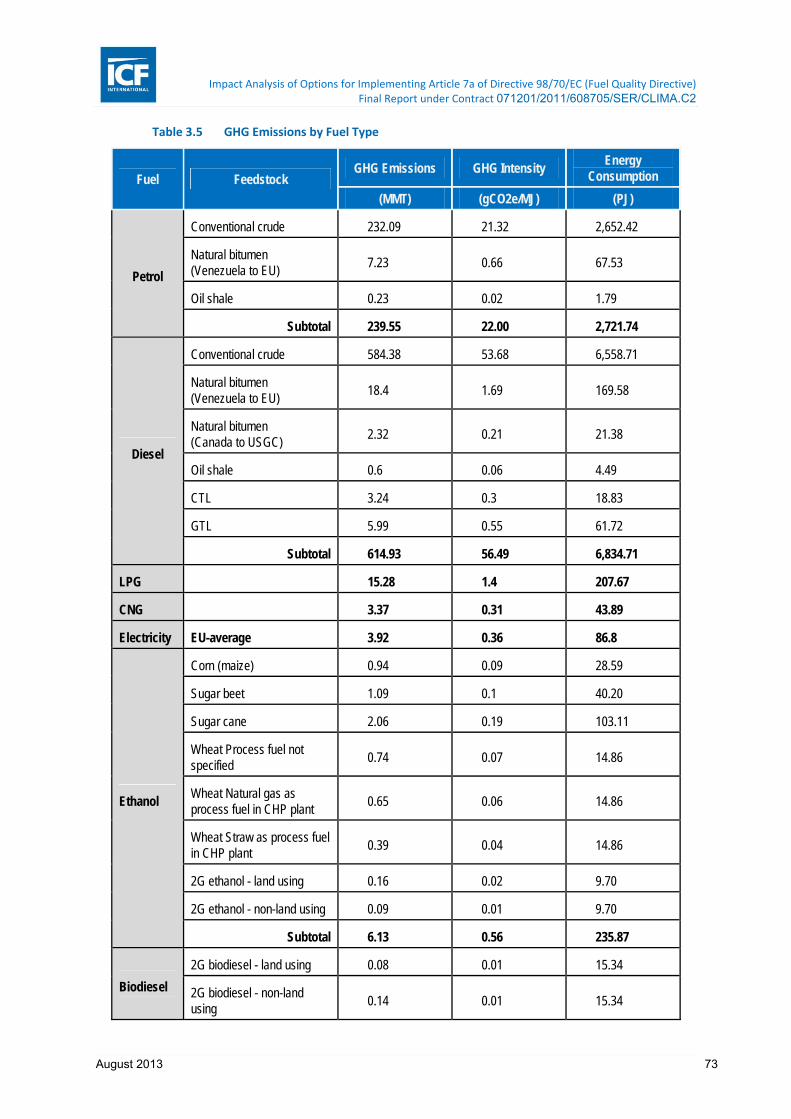

Table 3.5 GHG Emissions by Fuel Type .......................................................................................... 73

Table 3.6 Total Biofuel GHG Intensities Including ILUC .................................................................. 75

Table 3.7 GHG Intensity of Baseline Fuel Projections in 2020 ........................................................ 75

Table 3.8 GHG Emissions and Intensity for the ILUC Sensitivity Scenario ..................................... 77

Table 4.1 Change in Energy Demand for Transport Fuels, 2010-2020 ........................................... 79

Table 4.2 Range of MACs for Strategies in the Baseline Fuel Projections, 2020 ............................ 81

Table 4.3 Unit costs for selected bioethanol feedstocks .................................................................. 82

Table 4.4 Unit costs for selected biodiesel feedstocks ..................................................................... 84

Table 4.5 Marginal abatement costs of biofuels in the EU-27 .......................................................... 86

Table 4.6 2010 APG emission percentage of baseline .................................................................... 87

Table 4.7 Flared volumes and emissions for a sample of countries supplying crude to the EU ...... 88

Table 4.8 Marginal Abatement Costs of Methane Flare Reductions in Countries Supplying Crude to the EU in 2020 .................................................................................................................. 89

Table 4.9 Combined Marginal Abatement Cost Curve for Strategies in Baseline Projections ......... 90

Table 4.10 Estimated Annual Costs of Baseline Fuel Projections in 2020 ........................................ 91

Table 4.11 Incremental Marginal Abatement Cost Curve for FQD Compliance in BAU Scenario ..... 92

Table 4.12 Estimated Additional Cost of FQD Compliance for BAU in 2020 ..................................... 92

Table 4.13 Incremental Marginal Abatement Cost Curve for FQD Compliance in ILUC Sensitivity Scenario ............................................................................................................................ 93

Table 4.14 Estimated Annual Costs of ILUC Sensitivity Scenario in 2020 ........................................ 94

Table 5.1 Summary table of key characteristics of options (Note 1) ................................................ 97

Table 5.2 Summary of equations for deriving unit and total GHG intensities for each option ........ 119

Table 6.1 Data reported by certain Member States to the Commission on fuel suppliers (source: Personal Communication with European Commission, 2012) ....................................... 142

Table 6.2 Projected split of crudes across different Europe regions in 2020 (source: WORLD model this study) ....................................................................................................................... 144

Table 6.3 Analysis of data provided by 12 Member States of fuel producers (source: European Commission) ................................................................................................................... 152

Table 6.4 Analysis of data provided by 12 Member States of fuel traders (source: European Commission) ................................................................................................................... 152

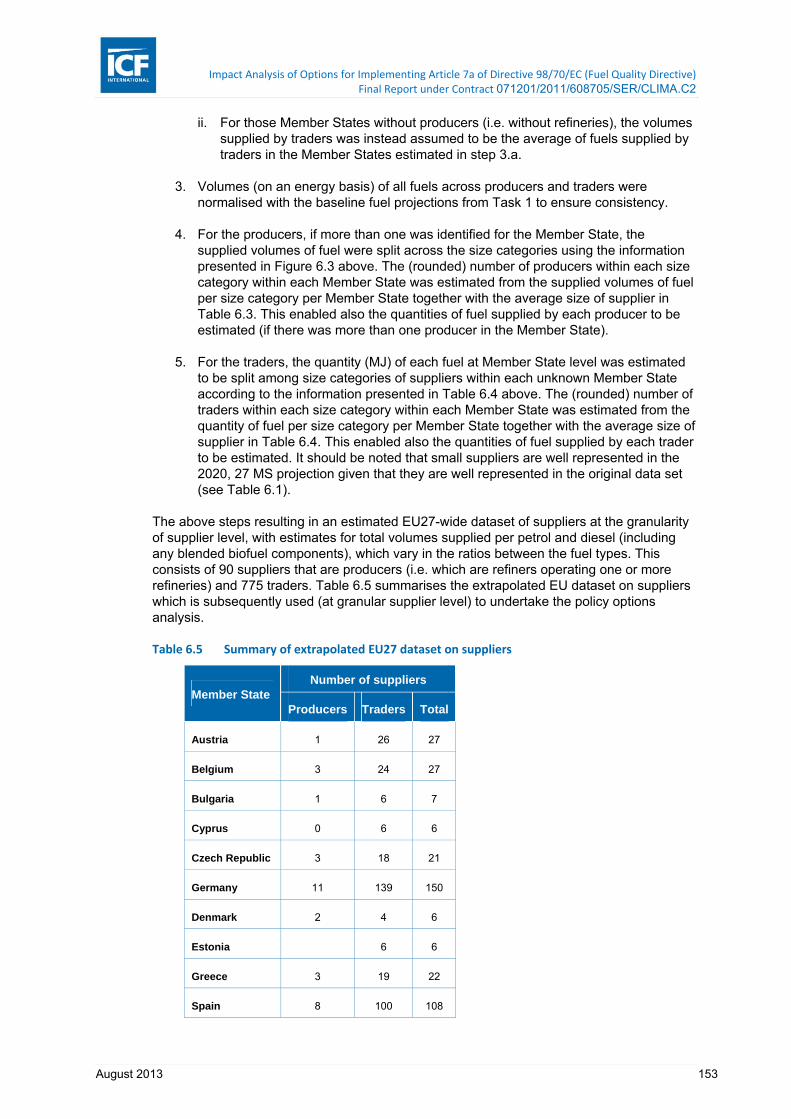

Table 6.5 Summary of extrapolated EU27 dataset on suppliers .................................................... 153

Table 6.6 Distribution of petrol, diesel (and their feedstock pathways) and LPG across the Member States .............................................................................................................................. 156

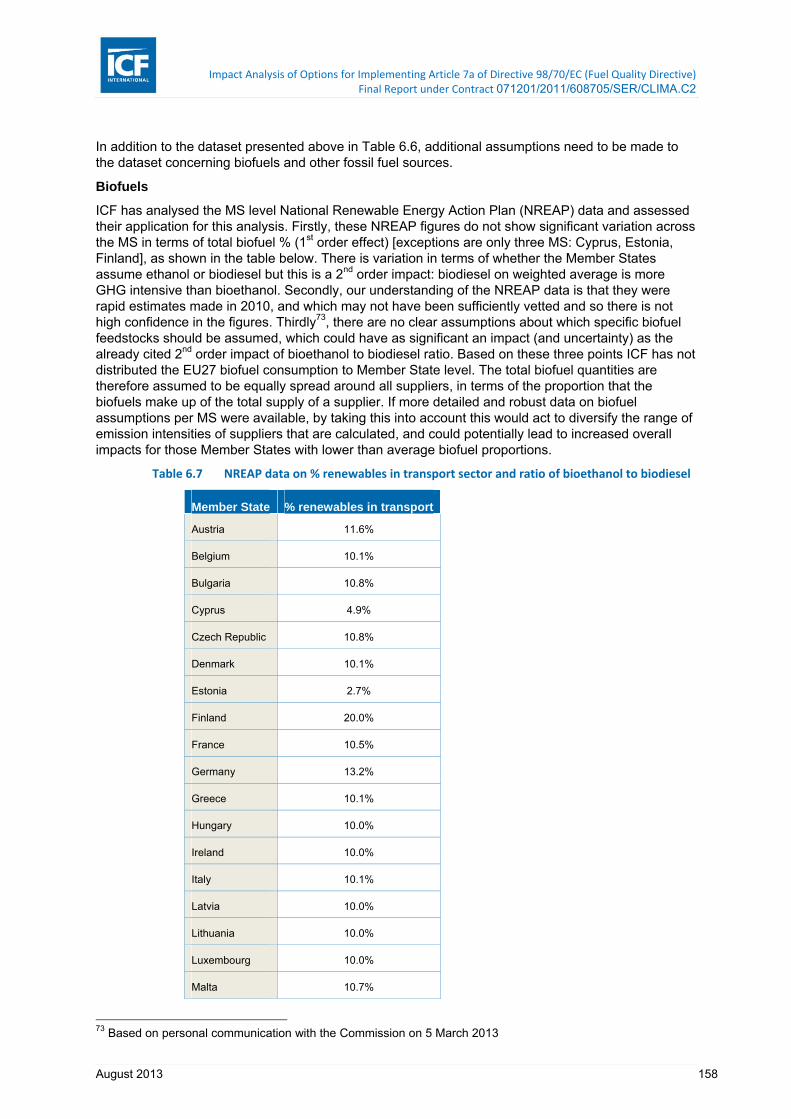

Table 6.7 NREAP data on % renewables in transport sector and ratio of bioethanol to biodiesel 158

Table 6.8 Development of upstream GHG intensities (gCO2e/MJ) for petrol and diesel derived from conventional crudes (source: based on JEC, 2011)....................................................... 160

Table 6.9 Assumed GHG intensities (gCO2e/MJ) for petrol and diesel derived from conventional crudes assumed to be used in the EU in 2020 (source: this study) ............................... 161

Table 6.10 Assumed GHG intensities (gCO2/MJ) for imported diesel derived from conventional crude under policy options 1 and 3 (opt in) .............................................................................. 163

Table 6.11 Assumed GHG intensities (gCO2/MJ) for petrol and diesel derived from unconventional crudes under policy options 1 and 3 (opt in and opt out) ............................................... 163

Table 6.12 Updates made to the default unit GHG intensities (gCO2e/MJ) of petrol and diesel derived from conventional crude .................................................................................... 164

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 vi

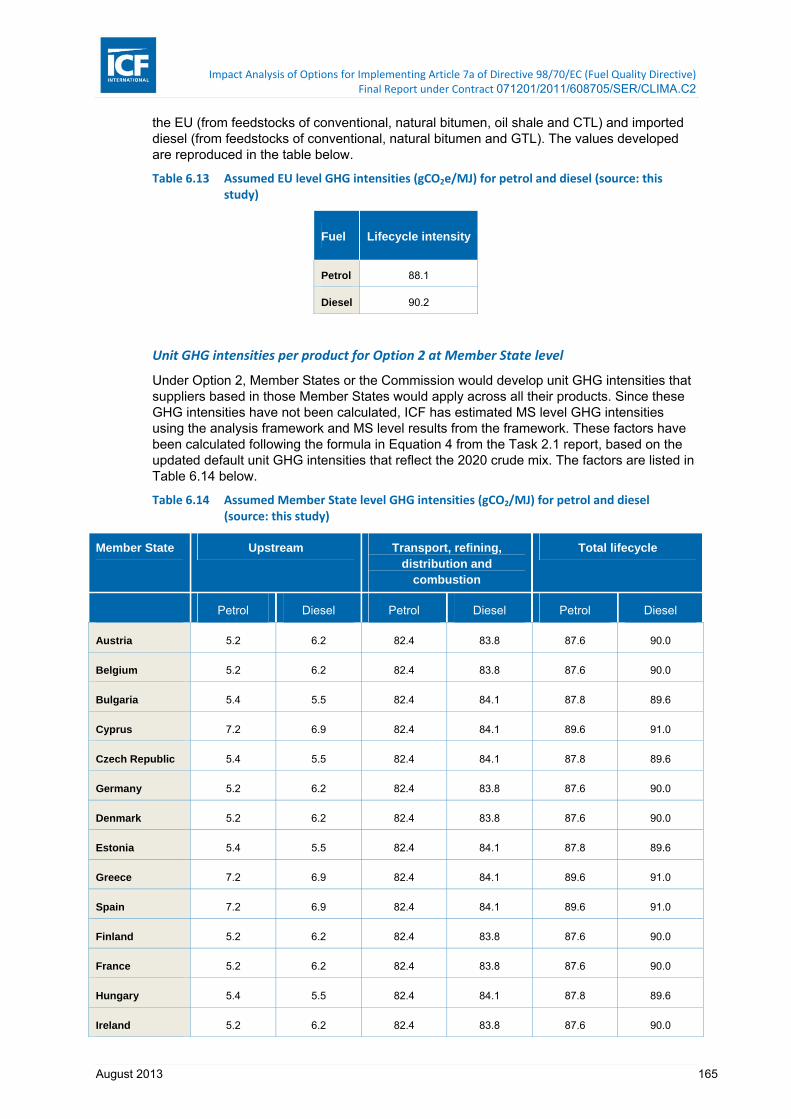

Table 6.13 Assumed EU level GHG intensities (gCO2e/MJ) for petrol and diesel (source: this study) ........................................................................................................................................ 165

Table 6.14 Assumed Member State level GHG intensities (gCO2/MJ) for petrol and diesel (source: this study) ....................................................................................................................... 165

Table 6.15 Abatement choices for suppliers .................................................................................... 168

Table 6.16 Additional biofuel blending options (non-ILUC) .............................................................. 173

Table 6.17 Additional biofuel blending options (ILUC) ..................................................................... 174

Table 6.18 MRV costs under Option 0 for suppliers ......................................................................... 181

Table 6.19 MRV costs under Option 0 for public authorities ............................................................ 182

Table 6.20 MRV costs under Option 1 for suppliers ......................................................................... 183

Table 6.21 MRV costs under Option 1 for public authorities ............................................................ 185

Table 6.22 MRV costs under Option 2 for suppliers ......................................................................... 186

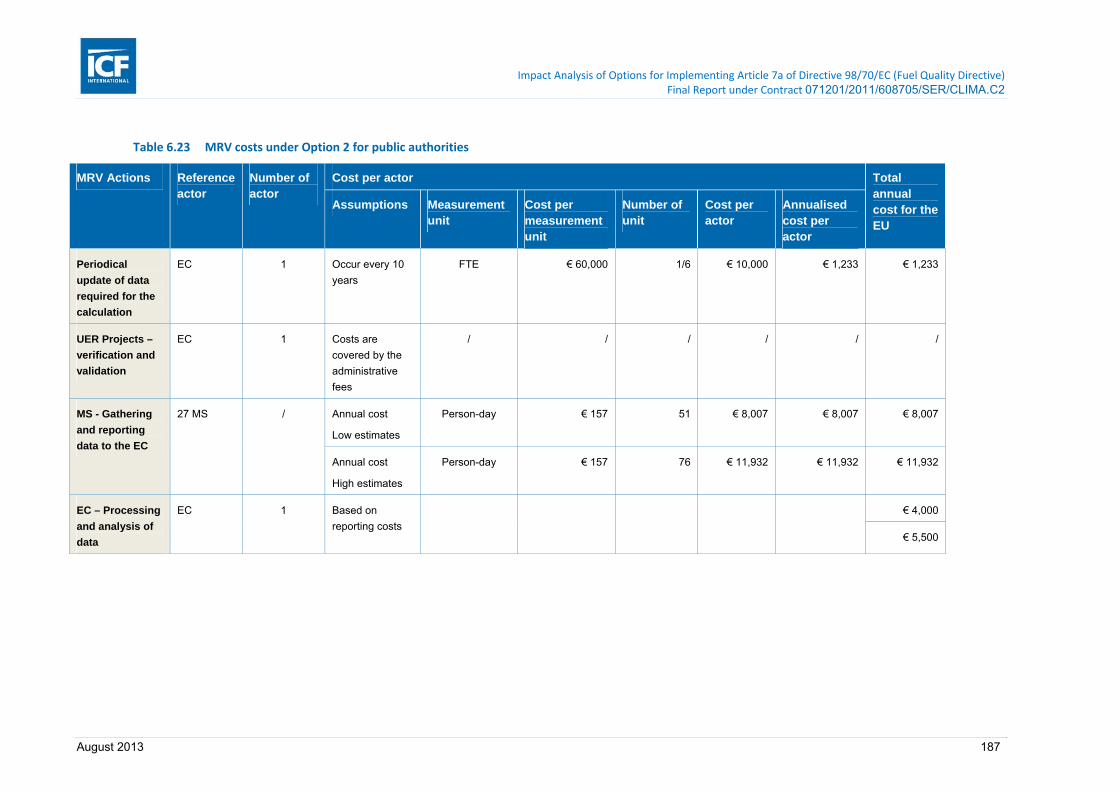

Table 6.23 MRV costs under Option 2 for public authorities ............................................................ 187

Table 6.24 MRV costs under Option 3 for suppliers (incurred by both opted in and opted out suppliers) ........................................................................................................................ 188

Table 6.25 Additional MRV costs under Option 3 for opted out suppliers ........................................ 189

Table 6.26 Additional MRV costs under Option 3 for opted in suppliers .......................................... 190

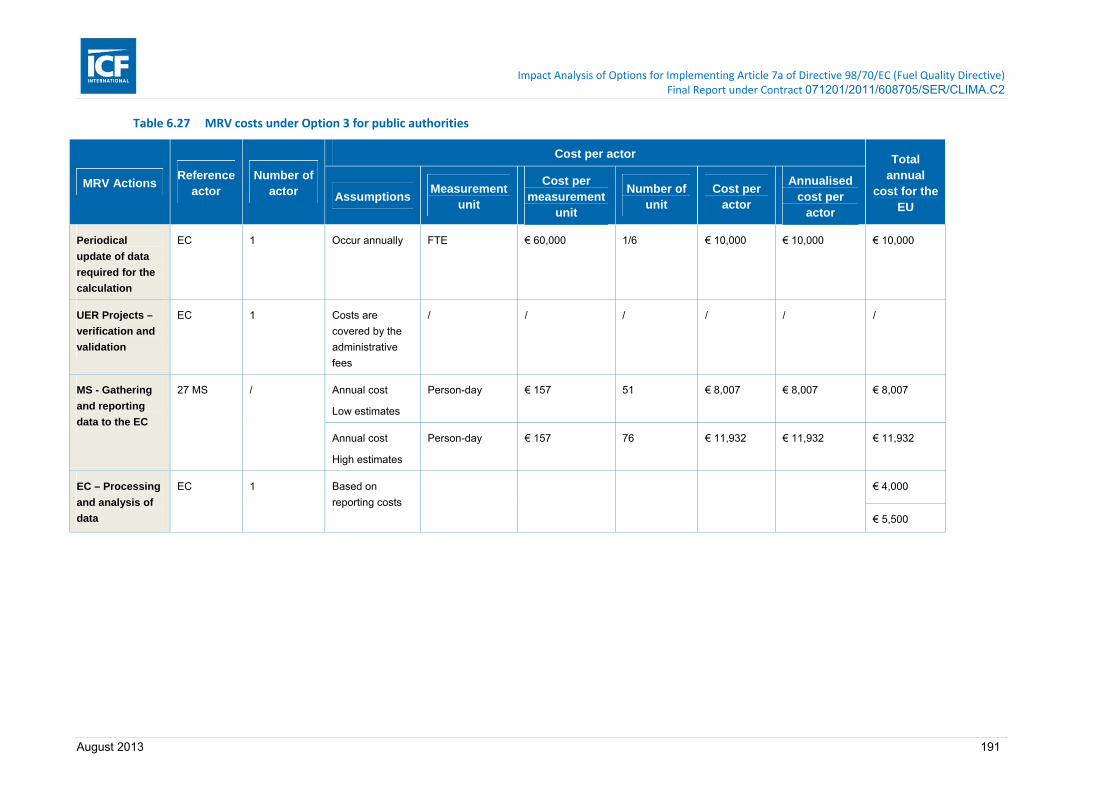

Table 6.27 MRV costs under Option 3 for public authorities ............................................................ 191

Table 6.28 Estimated emission reductions from the baseline to meet the target of 83.002 (Mt CO2e) ........................................................................................................................................ 192

Table 6.29 Opted in and opted out suppliers under Option 3 ........................................................... 194

Table 6.30 Summary results of the energy, GHG emissions and intensity of each policy option together with the absolute compliance costs to reach the target and the absolute administrative costs ........................................................................................................ 195

Table 6.31 Summary results of the energy, GHG emissions and intensity of each policy option together with the compliance costs to reach the target and the administrative costs, as compared to Option 0 ..................................................................................................... 196

Table 6.32 Emission reduction potential for crude and product switching for options 1 and 3 opt in ........................................................................................................................................ 198

Table 6.33 Total estimated administrative costs (€m / yr) per policy option under non-ILUC .......... 199

Table 6.34 Total estimated administrative costs (€m / yr) per policy option under ILUC sensitivity 200

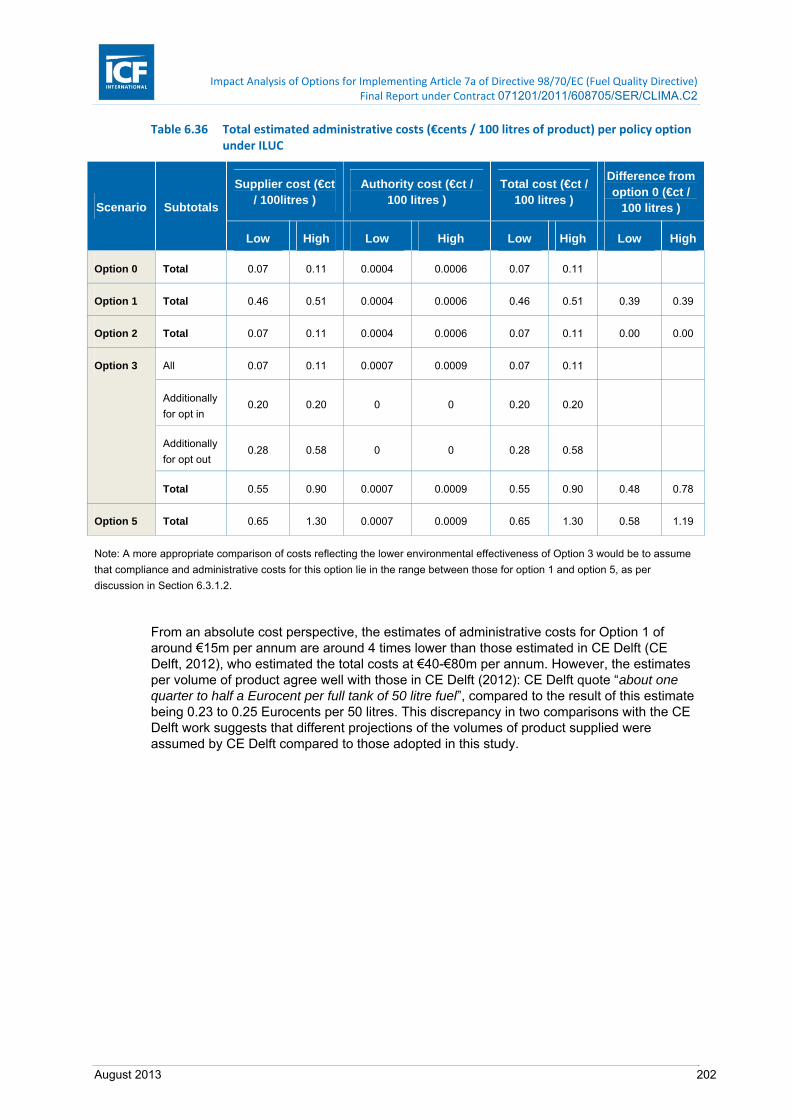

Table 6.35 Total estimated administrative costs (€cents / 100 litres of product) per policy option under non-ILUC .............................................................................................................. 201

Table 6.36 Total estimated administrative costs (€cents / 100 litres of product) per policy option under ILUC ..................................................................................................................... 202

Table 7.1 European refinery closures out to 2020 follow projected road transport fossil fuel demand ........................................................................................................................................ 204

Table 7.2 Over fifty per cent of the EU’s refining capacity is in Germany, Italy, the UK and France ........................................................................................................................................ 207

Table 7.3 Estimates of elasticity of transport fuel demand with respect to income vary between 0.4 and 1.3 while most price elasticity estimates are between -0.8 and -0.22 ..................... 214

Table 7.4 Mad Dog, USA and Gullfaks, Norway are the oilfields with the lowest carbon intensity and highest API gravity in a sample of wellhead-to-refinery emissions calculations ..... 225

Table 8.1 Switching from full joint reporting to individual reporting results in slightly higher abatement targets under the non-ILUC scenario but no changes in the ILUC scenario, reduction in mtCO2e per annum ..................................................................................... 232

Table 8.2 UERs contribute approximately 75 per cent of all abatement with biofuels contributing almost all of the remainder ............................................................................................. 234

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 vii

Table 8.3 Market size for emissions abatement increases significantly under the ILUC scenario 238

Table 8.4 EU road transport fossil fuel demand decline does not vary significantly between options ........................................................................................................................................ 239

Table 8.5 Eastern European oil shale is no longer used at prices above €10/tCO2e and, in the ILUC scenario, Venezuelan natural bitumen exits the EU crude market as well .................... 240

Table 8.6 US diesel derived from unconventional crude is not imported in the EU under all options except option 3 non-ILUC ............................................................................................... 241

Table 8.7 Pump prices rise marginally as a consequence of the FQD .......................................... 241

Table 8.8 Assumptions and sources .............................................................................................. 243

Table A1.1 Biofuels production faces small direct impacts that are contingent on other policies .... 248

Table A1.2 Vehicle manufacturers could face small changes in demand if fuel prices increase ..... 249

Table A1.3 Public transport could experience a small increase in demand if fuel prices increase .. 249

Table A1.4 The competitiveness impacts on petrochemicals occur indirectly from the effects of policy on refineries .................................................................................................................... 250

Table A1.5 Refineries face the greatest direct effects to competitiveness and the nature of these effects depends on how the policy is implemented ........................................................ 250

Table A1.6 Traders also face direct effects but their competitiveness is largely unaffected ........... 251

Table A1.7 Process unit capacities can be converted into an overall complexity factor using a system of weights with a crude distillation unit having a weight of one while a lube unit has a weight of 60 .................................................................................................................... 252

Table A1.8 Final energy consumption of petrol has declined by 28% in the EU27 between 2001 and 2010 ................................................................................................................................ 253

Table A1.9 Final energy consumption of transport diesel has increased by 23% in the EU27 between 2001 and 2010 ................................................................................................................ 254

Table A1.10 Total crude oil imports have declined by 6 per cent in the EU-27 between 2001-10 ..... 255

Table A1.11 In 2010 the EU-27 consumed 32 per cent less motor gasoline than it produces and 14 per cent more transport diesel than it produced ............................................................. 256

Table A1.12 Approximately 90 per cent of the 2020 EU transport fuel market is based on fossil fuels and over approximately 80 per cent of these are refined in the EU ............................... 261

Table A1.13 Non-mineral transport fuels have an average GHG intensity far below the FQD target whereas EU mineral transport fuels are above the target .............................................. 261

Table A1.14 The market costs and compliance cost calculations make use the required additional abatement figure obtained as shown below ................................................................... 262

Table A1.15 Costs to the consumer are far larger than abatement market size and compliance costs ........................................................................................................................................ 265

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 viii

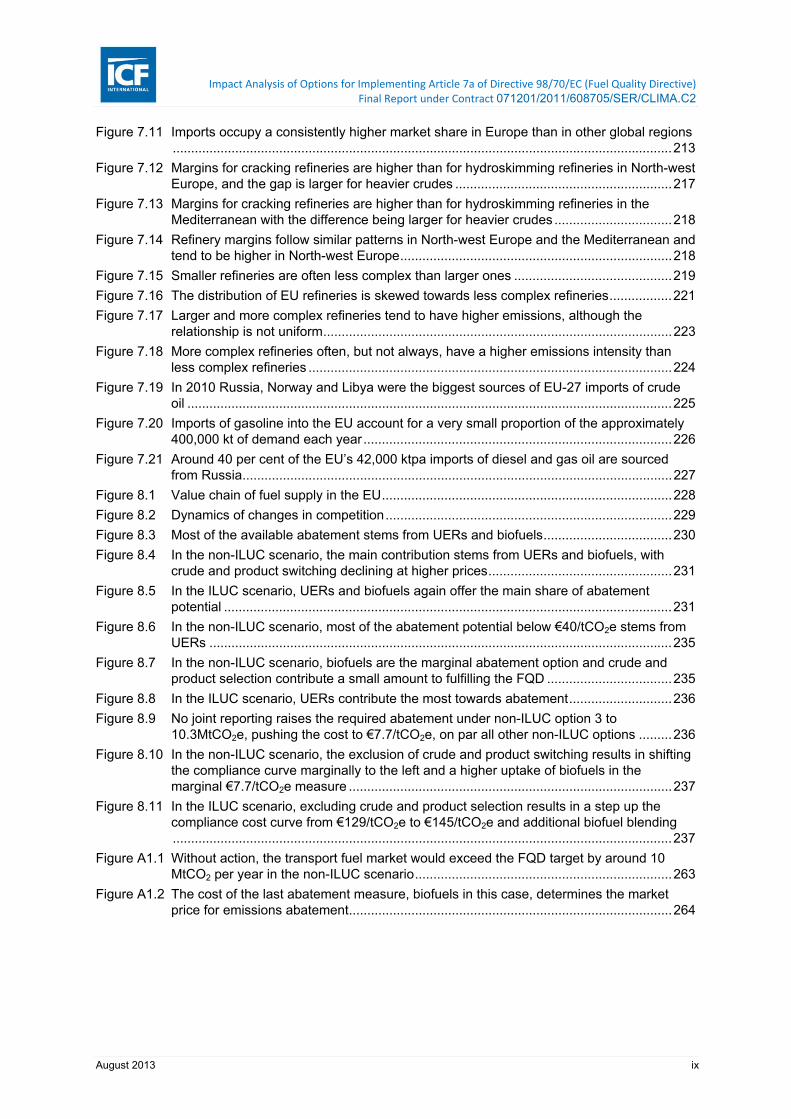

Table of figures

Figure 5.1 Weighted-average most likely oil sands emissions compared to weighted average conventional EU refinery feedstock. Source: Brandt (2011) .......................................... 116

Figure 5.2 Emissions as a function of cumulative normalized output, for oil sands projects and conventional oil imports to the EU. Source: Brandt (2011) ............................................ 116

Figure 5.3 GHG emissions intensity as a function of cumulative normalised EU crude use for crudes identified in the WORLD model for the baseline of Task 1 mapped to GHG intensity values from Jacobs (2012). Source: this work ............................................................... 117

Figure 6.1 Well to refinery upstream GHG emissions intensity from conventional crude oils to nominal EU refinery (gCO2/MJ crude) (Data source: (Brandt, 2011)) ........................... 148

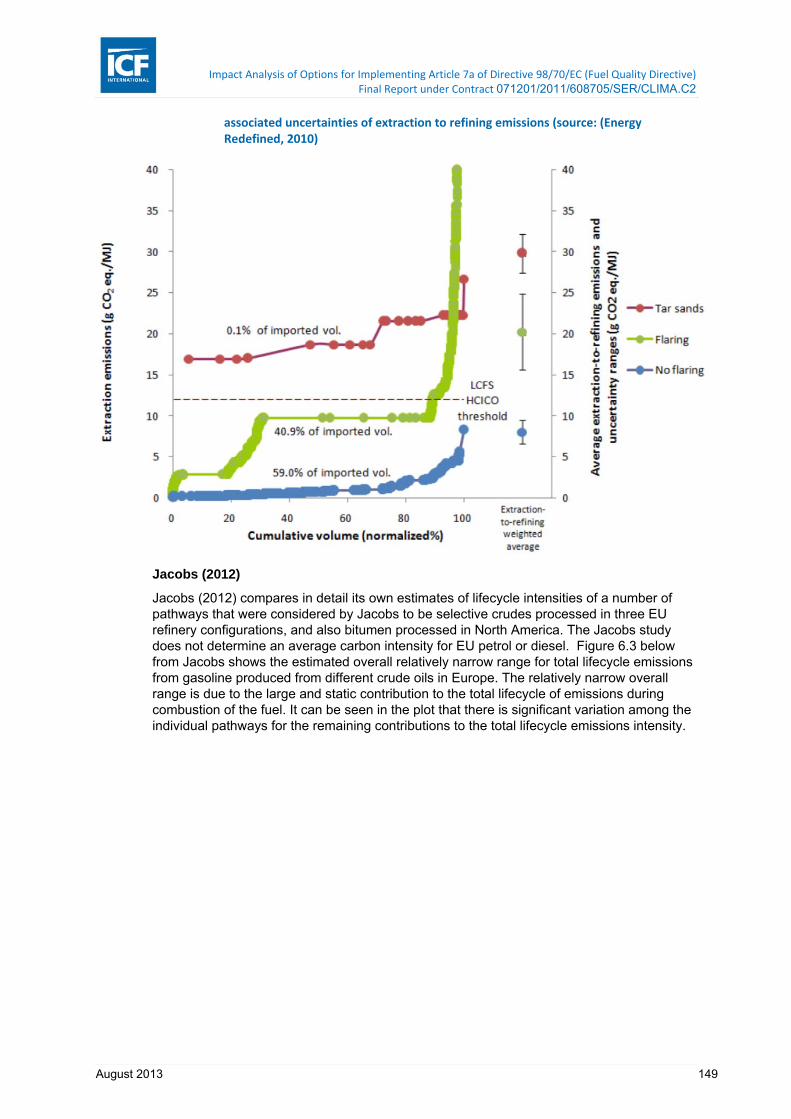

Figure 6.2 Upstream extraction GHG emissions for EU imported conventional crude oil (with and without flaring) and tar sands. Right-hand plot shows weighted averages and associated uncertainties of extraction to refining emissions (source: (Energy Redefined, 2010) .... 148

Figure 6.3 Lifecycle carbon Intensity of Producing Gasoline from Crude Oils to Europe (source: (Jacobs, 2012)) ............................................................................................................... 150

Figure 6.4 Histograms showing, for producers and traders separately, the breakdown by size of supplier (PJ/year total petrol and diesel) for 51 producers and 404 traders in the 12 Member States that responded to the 2010 questionnaire (data source: European Commission) ................................................................................................................... 151

Figure 6.5 Proportion of supply as petrol as a function of the normalised cumulative volume of total fuel supplied for 51 producers and 404 traders in the 12 Member States that responded to the 2010 questionnaire (data source: European Commission) .................................. 151

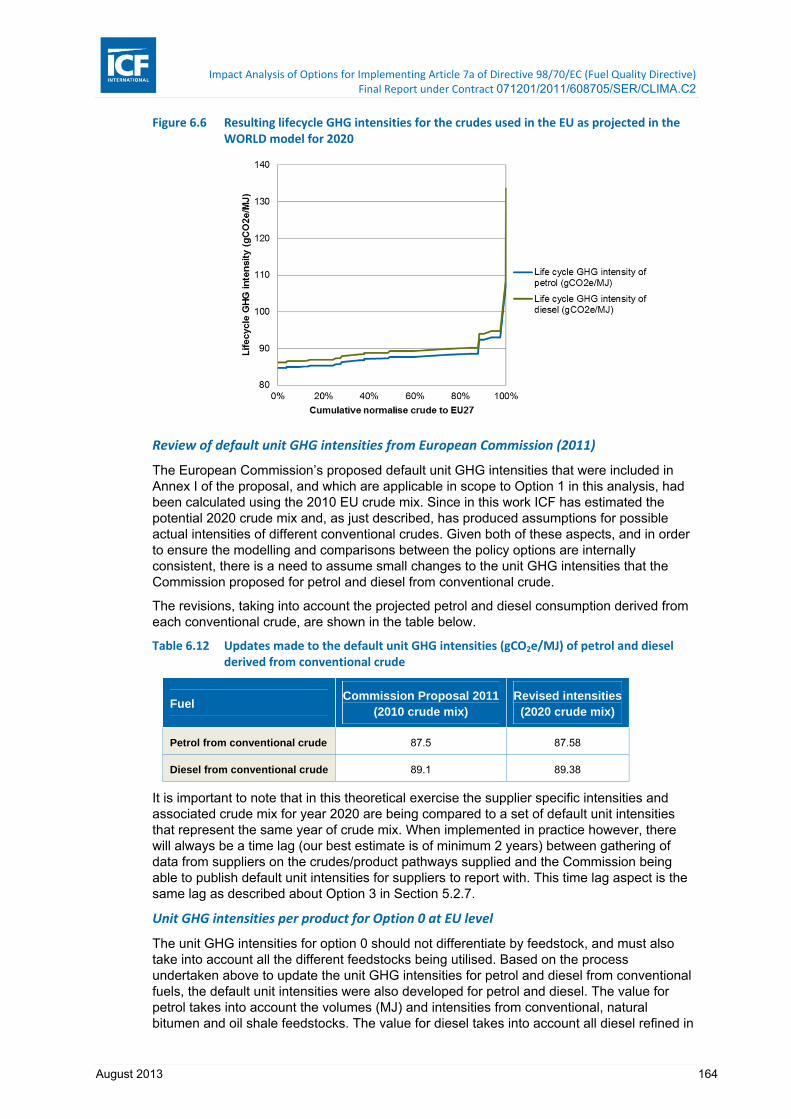

Figure 6.6 Resulting lifecycle GHG intensities for the crudes used in the EU as projected in the WORLD model for 2020 ................................................................................................. 164

Figure 6.7 Refining product yield from different feedstocks and refining operations (source: (Jacobs, 2012)) ............................................................................................................................. 171

Figure 6.8 Suppliers estimated total intensity (ordered lowest to highest) as a function of cumulative normalised total supply volumes under each policy option and compared to the target (source: this work) .......................................................................................................... 197

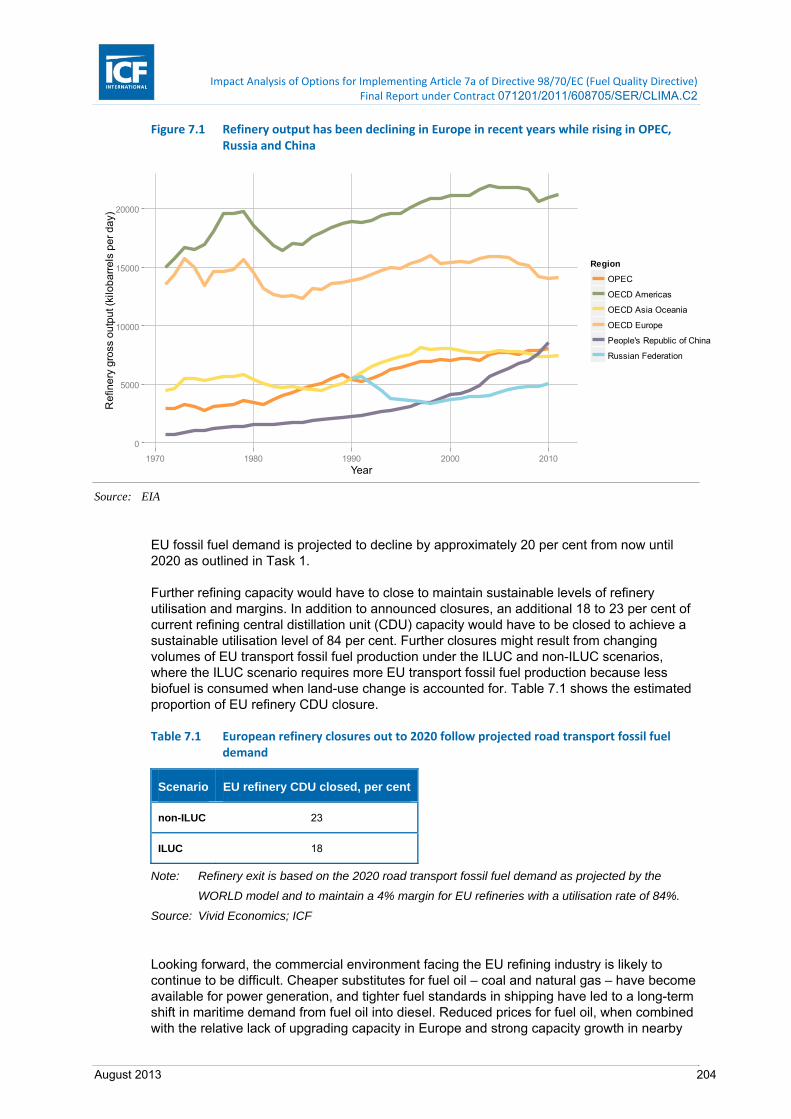

Figure 7.1 Refinery output has been declining in Europe in recent years while rising in OPEC, Russia and China ........................................................................................................... 204

Figure 7.2 The bulk of global refining capacity is found in North America and the Asia-Pacific, though European countries also contribute a substantial share .................................... 205

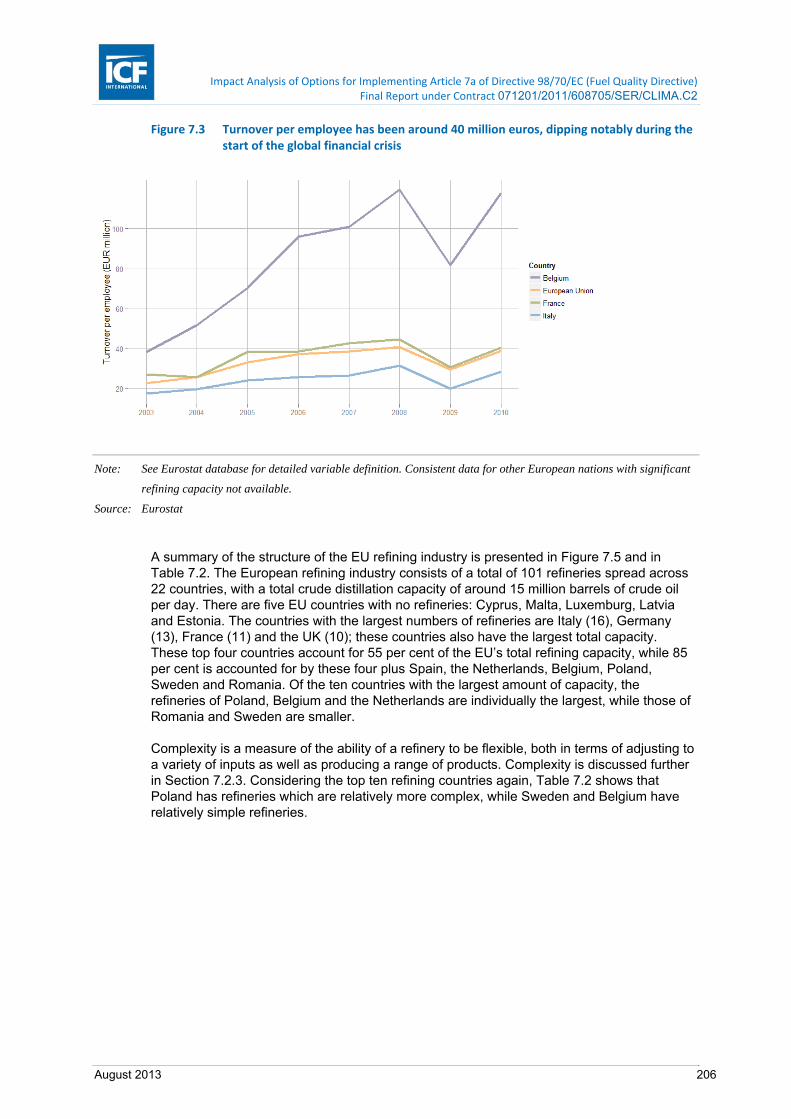

Figure 7.3 Turnover per employee has been around 40 million euros, dipping notably during the start of the global financial crisis ..................................................................................... 206

Figure 7.4 Labour productivity in the coke and refined petroleum sector under €200,000 in 2010, down by approximately one-third since 2005 ................................................................. 207

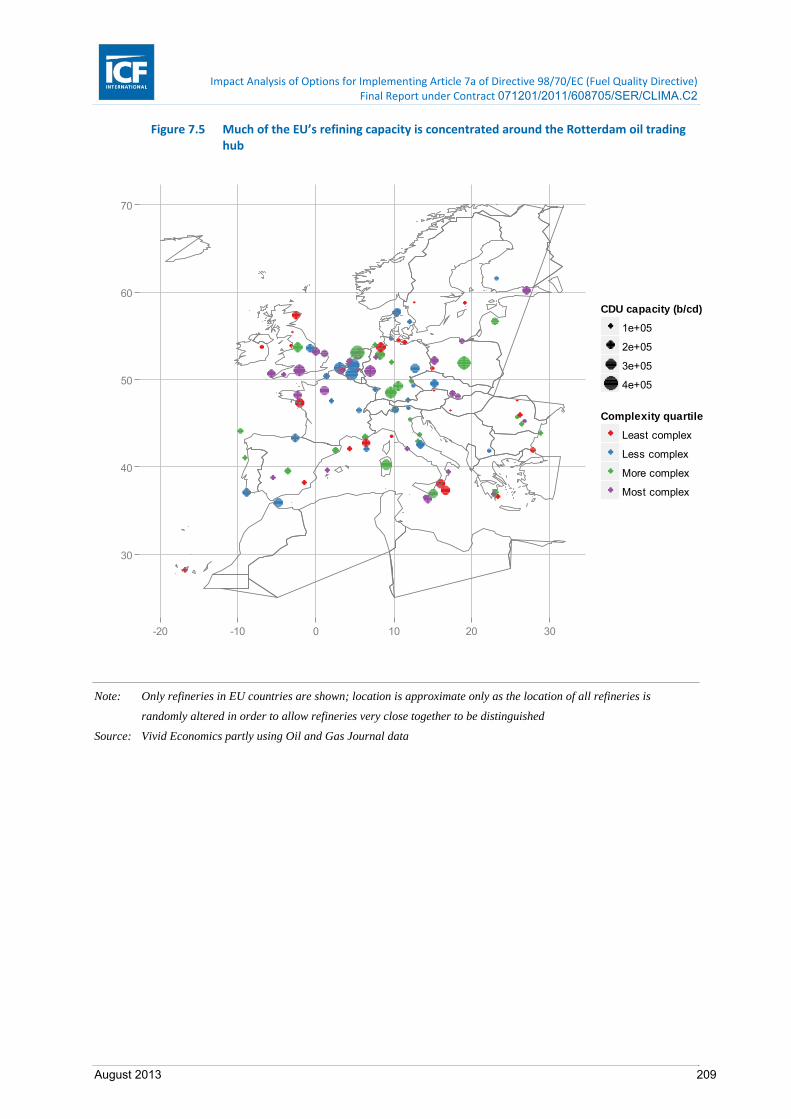

Figure 7.5 Much of the EU’s refining capacity is concentrated around the Rotterdam oil trading hub ........................................................................................................................................ 209

Figure 7.6 Around half of the EU’s refineries have a crude distillation capacity of between 50 and 150 thousand barrels per calendar day .......................................................................... 210

Figure 7.7 Independent owners account for around 40 per cent of the total number of refineries in the EU ............................................................................................................................. 211

Figure 7.8 The six oil majors account for a greater share of refining capacity than their share of the number of refineries in the EU ........................................................................................ 211

Figure 7.9 Fuel demand has risen sharply outside Europe, the US and Japan over the last decade ........................................................................................................................................ 212

Figure 7.10 Distillate fuel oil has seen growth in demand in Europe, while fuel oil and, recently, gasoline, have seen reductions in demand .................................................................... 212

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 ix

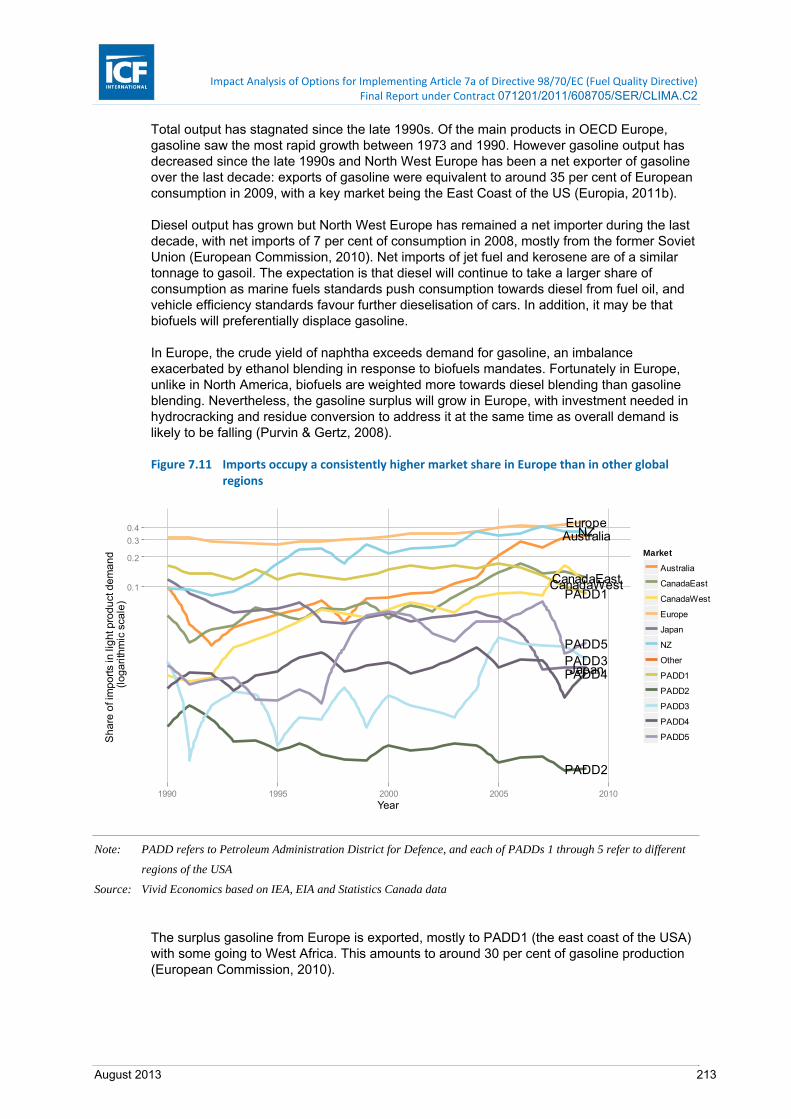

Figure 7.11 Imports occupy a consistently higher market share in Europe than in other global regions ........................................................................................................................................ 213

Figure 7.12 Margins for cracking refineries are higher than for hydroskimming refineries in North-west Europe, and the gap is larger for heavier crudes ........................................................... 217

Figure 7.13 Margins for cracking refineries are higher than for hydroskimming refineries in the Mediterranean with the difference being larger for heavier crudes ................................ 218

Figure 7.14 Refinery margins follow similar patterns in North-west Europe and the Mediterranean and tend to be higher in North-west Europe .......................................................................... 218

Figure 7.15 Smaller refineries are often less complex than larger ones ........................................... 219 Figure 7.16 The distribution of EU refineries is skewed towards less complex refineries ................. 221 Figure 7.17 Larger and more complex refineries tend to have higher emissions, although the

relationship is not uniform ............................................................................................... 223 Figure 7.18 More complex refineries often, but not always, have a higher emissions intensity than

less complex refineries ................................................................................................... 224 Figure 7.19 In 2010 Russia, Norway and Libya were the biggest sources of EU-27 imports of crude

oil .................................................................................................................................... 225 Figure 7.20 Imports of gasoline into the EU account for a very small proportion of the approximately

400,000 kt of demand each year .................................................................................... 226 Figure 7.21 Around 40 per cent of the EU’s 42,000 ktpa imports of diesel and gas oil are sourced

from Russia ..................................................................................................................... 227 Figure 8.1 Value chain of fuel supply in the EU ............................................................................... 228 Figure 8.2 Dynamics of changes in competition .............................................................................. 229 Figure 8.3 Most of the available abatement stems from UERs and biofuels ................................... 230 Figure 8.4 In the non-ILUC scenario, the main contribution stems from UERs and biofuels, with

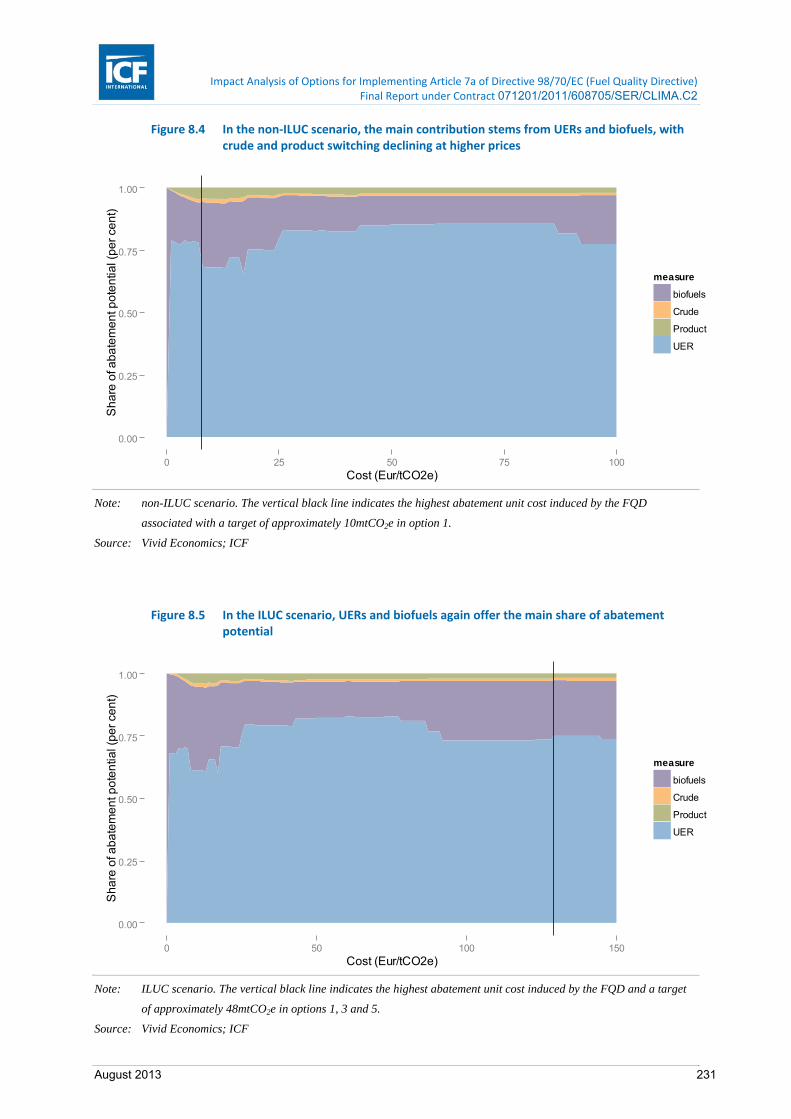

crude and product switching declining at higher prices .................................................. 231 Figure 8.5 In the ILUC scenario, UERs and biofuels again offer the main share of abatement

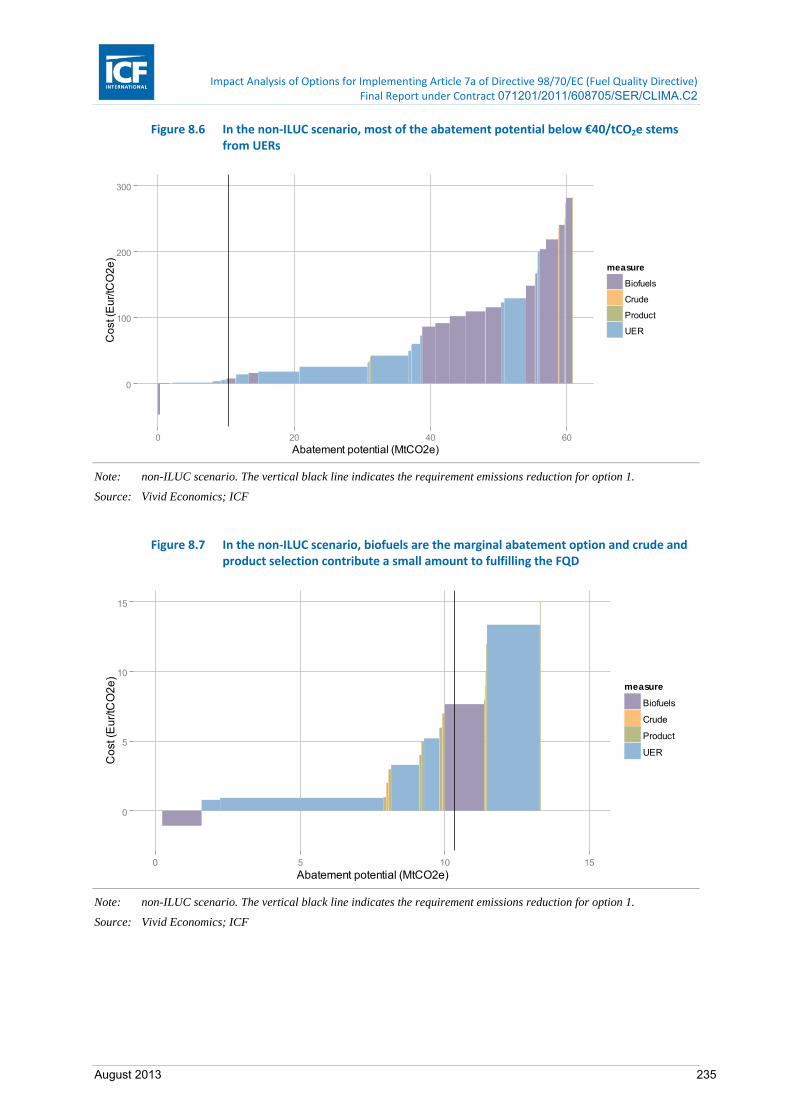

potential .......................................................................................................................... 231 Figure 8.6 In the non-ILUC scenario, most of the abatement potential below €40/tCO2e stems from

UERs .............................................................................................................................. 235 Figure 8.7 In the non-ILUC scenario, biofuels are the marginal abatement option and crude and

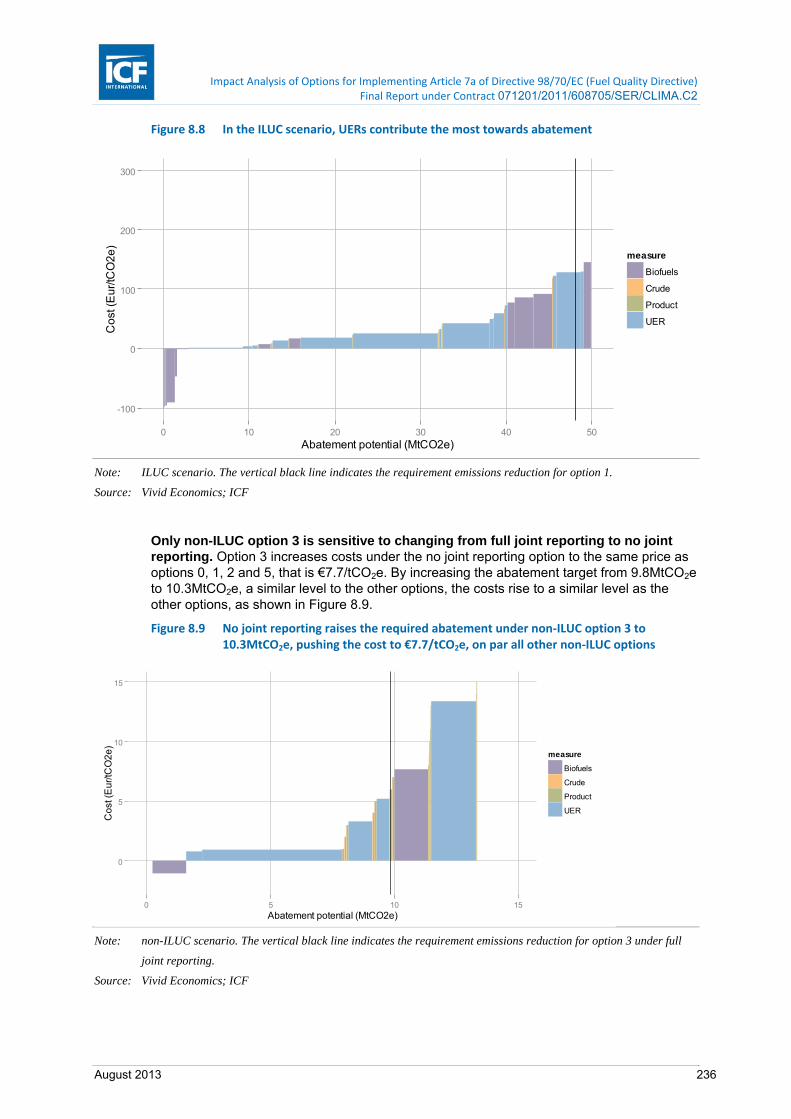

product selection contribute a small amount to fulfilling the FQD .................................. 235 Figure 8.8 In the ILUC scenario, UERs contribute the most towards abatement ............................ 236 Figure 8.9 No joint reporting raises the required abatement under non-ILUC option 3 to

10.3MtCO2e, pushing the cost to €7.7/tCO2e, on par all other non-ILUC options ......... 236 Figure 8.10 In the non-ILUC scenario, the exclusion of crude and product switching results in shifting

the compliance curve marginally to the left and a higher uptake of biofuels in the marginal €7.7/tCO2e measure ........................................................................................ 237

Figure 8.11 In the ILUC scenario, excluding crude and product selection results in a step up the compliance cost curve from €129/tCO2e to €145/tCO2e and additional biofuel blending ........................................................................................................................................ 237

Figure A1.1 Without action, the transport fuel market would exceed the FQD target by around 10 MtCO2 per year in the non-ILUC scenario ...................................................................... 263

Figure A1.2 The cost of the last abatement measure, biofuels in this case, determines the market price for emissions abatement ........................................................................................ 264

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 1

1 Introduction

1.1 Objectives of Project

The Fuel Quality Directive (FQD)1 as amended by Directive 2009/30/EC requires fossil fuel suppliers to achieve a 6% reduction in greenhouse gas (GHG) intensity of road transport2 fuels.

Although the method for calculating GHG emissions for biofuels is included in the Directive, the method for calculating the fossil fuel GHG intensity was left for comitology and is the subject of the proposed Article 7a implementing measure. The Commission proposed to the Fuel Quality Committee of Member State experts, in October 2011, an implementing measure which was discussed and voted on. The Committee vote in February 2012 resulted in a “no opinion”. Consequently the Commission has to submit a proposal to the Council to adopt the required methodology. The proposal is to be accompanied by an impact assessment.

This study will underpin the analysis of the regulatory options and associated economic and GHG impacts for the implementation of the Article 7a method for calculating GHG emissions from fossil fuels for road vehicles. Considering the use of default and/or actual values of lifecycle GHG intensities as well as varying degrees of disaggregation, different methodologies for the estimation of lifecycle GHG emissions from fossil fuels are to be assessed.

The overall effort is to be divided into 3 overarching tasks, each of which consists of a set of subtasks:

■ Task 1: Development of a baseline

■ Task 2: Cost benefit analysis of options

■ Task 3: Competitiveness analysis

1.2 This Report

This is the Final Report of the study which presents the findings of each of the tasks in the following sections:

■ Section 2: Development of fuel projections under baseline reporting (Task 1.1)

■ Section 3: Baseline GHG emissions and GHG intensity (Task 1.2)

■ Section 4: Costs of the baseline (Task 1.3)

■ Section 5: Development and screening of options (Task 2.1)

■ Section 6: Analysis of options (Task 2.2)

■ Section 7: Characterisation of affected sectors (Task 3.1)

■ Section 8: Impacts on the EU road transport fuel market (Task 3.2)

This report has been developed by ICF and Vivid Economics, with support from EnSys on fuel and feedstock modelling. The work has involved close co-operation with DG CLIMA throughout the study and has included industry stakeholder workshops in December 2012 and April 2013.

1 Directive 98/70/EC 2 Road vehicles, non-road mobile machinery (NRMM, including inland waterway vessels) and agricultural or forestry tractor or recreational craft.

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 2

2 Develop Fuel Projections under Baseline Reporting (Task 1.1)

2.1 Introduction

This task is to develop a baseline of EU fuel projections to 2020 for road vehicles3. This baseline will effectively serve as the foundation for subsequent tasks involving the estimation of impacts on lifecycle GHG emissions and costs associated with various reporting methodologies. The baseline should represent the specific default GHG intensities and biofuel feedstock quantities provided by the Commission. Additionally, this task is to identify crude feedstocks to the EU and crude imports and exports.

The fuel projection must be adequately disaggregated to allow an accurate assessment of the regulatory options the EC is considering. Table 2.1 describes what a complete fuel projection should ideally include.

Table 2.1 Key characteristics for the projection

Scope and Level of Disaggregation

Fuel consuming sectors Road vehicles and non-road mobile machinery (NRMM i.e. agricultural and forestry tractors, and inland waterway vessels and recreational crafts when not out at sea).

Geography EU 27

Year(s) of forecast 2020

Refinery data The amount and type of crude refined by groups of refineries

Feedstock type For fossil fuels, the source of feedstock (i.e. conventional crude, natural bitumen, oil shale). For biofuels, the grain used (i.e. rapeseed, wheat, sugar beet, corn, etc.)

Fuel type The consumption of the different fuels (petrol, diesel, LPG, CNG, non-road gasoil, biofuels). In addition, the forecasts for the amount of fuels must take into account the penetration of electric vehicles into the fleet.

Trade of fuel The fuel projection must differentiate between crude/fuels that are produced in the EU27 and crude/fuels that imported.

Regulatory Considerations

EU policies The projections must include the impact of the Renewable Energy Directive (RED)4 and the CO2 limits of emissions from cars and vans

2.2 Literature review

To develop a robust baseline of fuel projections for the road vehicle and NRMM sector, the ICF team began with a literature review. The purpose was to assess the suitability and quality of existing projections in accordance with the goals and objectives of this task.

For this effort the following 15 documents / models were reviewed.

■ EU Transport GHG: Routes to 2050 (‘SULTAN’ Tool)

■ Impact of the use of biofuels on oil refining and fuels specifications, Wood Mackenzie

■ Transvisions, Report on Transport Scenarios with a 20 and 40 Year Horizon - Developing a set of long-term scenarios (2030 - 2050) for transport and mobility in Europe, European Commission DG TREN (2009)

■ Assessing the Land Use Change Consequences of European Biofuel Policies, IFPRI

3 Also included will be non-road mobile machinery, agricultural and forest tractors, and recreational craft when not at sea. 4 The Renewable Energy Directive (Directive 2009/28/EC) requires Member States to ensure that 10% of the energy used in transport is from renewable sources from 2020.

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 3

■ NREAP -- Renewable Energy Projections as Published in the National Renewable Energy Action Plans of the European Member States, EEA.

■ The World Energy Outlook 2012, International Energy Agency (IEA)

■ Europia White Paper on Fueling EU Transport, A contribution from the EU refining industry to the debate on the future of transport, European Petroleum Industry Association (2011) (Europia, 2011b)

■ EU-27 Annual Biofuels Report USDA/GAIN

■ Global Energy Outlook, Platts Insight

■ International Energy Outlook, EIA/DOE (USA)

■ Eurogas, The European Gas Industry: Long Term Outlook for Gas Demand and Supply

■ Shell: Energy Scenarios to 2050 (Scramble and Blueprint)

■ Exxon: Outlook for Energy—A View to 2040

■ OPEC: World Oil Outlook

■ WORLD model, EnSys

Each document / model was evaluated according to determined criteria as described in the next section.

From the literature review and biofuel GHG intensities and feedstocks provided by the EC, ICF determined a representative fuel demand scenario for biofuels and petroleum based fuels. The fuel demand had to be in compliance with the relevant policies while also taking into account uptake of electric vehicles, biofuel feedstocks, and petroleum fuel feedstocks. Using this demand scenario and a proprietary model from ICF’s subcontractor, EnSys, an assessment of the crude trade impacts on the European Refining sector was developed.

2.3 Preliminary Assessment

A robust EU fuel projection to 2020 is required to forecast baseline GHG emissions against which the regulatory options to estimate lifecycle GHG emissions will be evaluated. There are numerous studies independently conducted by organizations that project the supply and demand for fuel in the transportation sector. A preliminary assessment rated the studies / models by the following criteria:

a. Scope of data: The projections must consider the fuel demand and/or supply in the road transportation sector for the EU 27 by fuel type and feedstock type.

b. Disaggregation of data: The data for the projections must be broken out by fuel type and feedstock type.

c. Timescale: The projections must have forecasted values to 2020.

d. Policies considered: The projections must consider the RED, FQD and the regulation of CO2 emissions from cars and vans.

e. Data accessibility: The data must be publicly accessible, available through the EC or available to purchase within the data budget for this study.

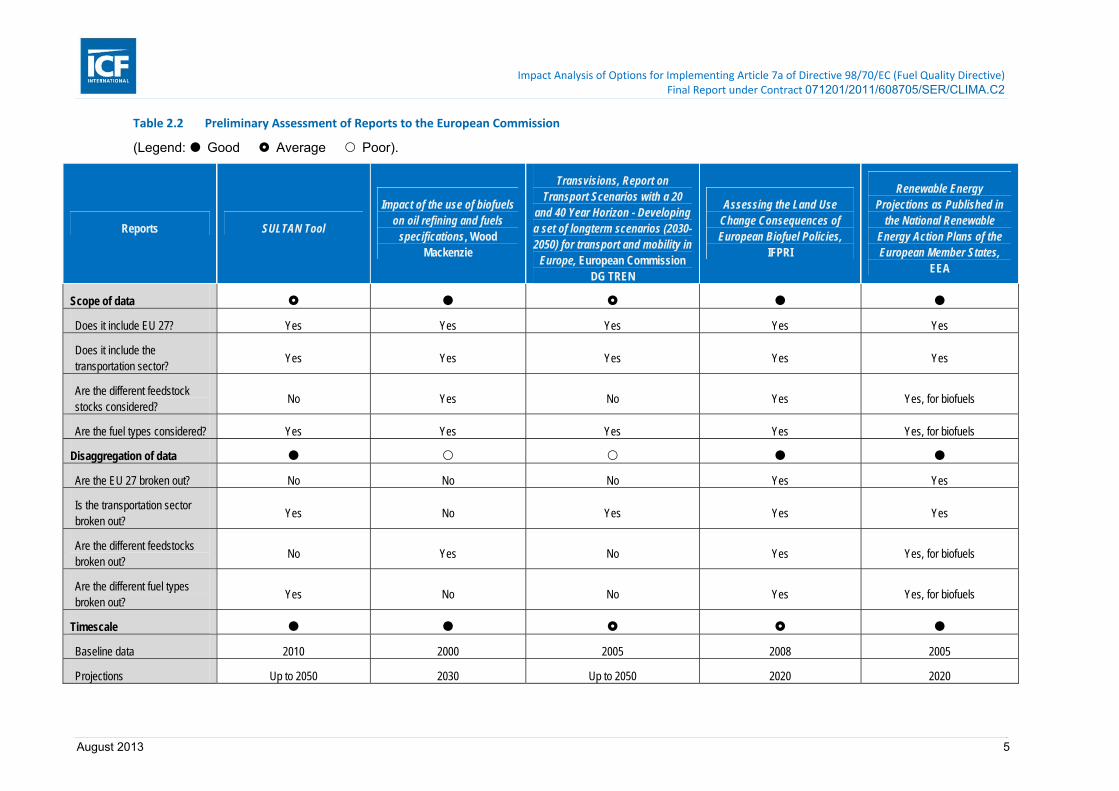

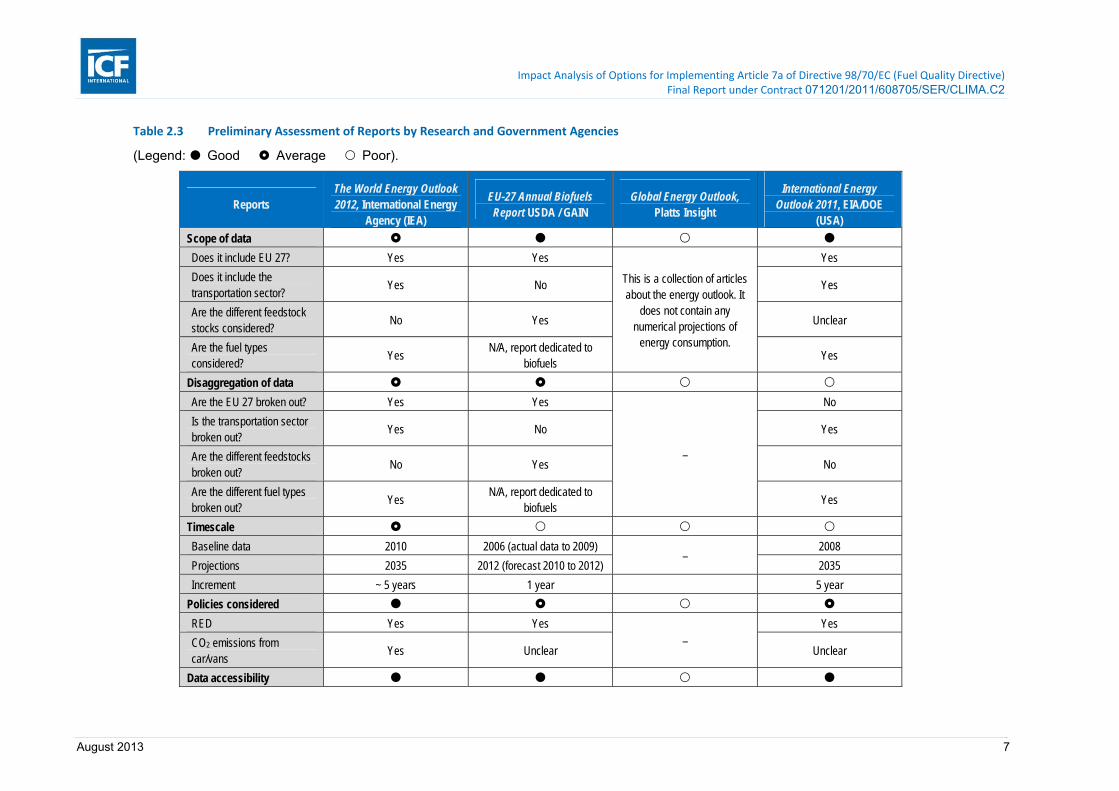

Table 2.2, 2.3 and 2.4 summarize the preliminary assessment of each reviewed literature. The result of the review was that five studies were selected as reasonably viable fuel projections for inclusion in the next step of this task of in-depth analysis. The five studies / models selected are:

■ the International Energy Outlook 2011 by the Energy Information Administration,

■ The World Energy Outlook by the International Energy Agency,

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 4

■ the SULTAN tool5,

■ the WORLD model by EnSys.

■ Impact of the use of biofuels on oil refining and fuels specifications, by Wood Mackenzie

In addition, aspects of three other studies have been identified as being useful to contribute to the development of a more complete fuel projection, although they were not reviewed in-depth. These three studies are:

■ Assessing the Land Use Change Consequences of European Biofuel Policies by International Food Policy Research Institute (IFPRI), and

■ Renewable Energy Projections as Published in the National Renewable Energy Action Plans of the European Member States by EEA.

Ten of the fifteen reports were not considered for in-depth analysis because they did not meet sufficient criteria of the preliminary assessment (e.g. projections were not to 2020, projections were not disaggregated to EU level, projections were not disaggregated by fuel type, or projections were not disaggregated by sector including the road transport sector).

5 Also known as The EU Transport GHG: Routes to 2050.

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 5

Table 2.2 Preliminary Assessment of Reports to the European Commission

(Legend: Good Average Poor).

Reports SULTAN Tool

Impact of the use of biofuels on oil refining and fuels

specifications, Wood Mackenzie

Transvisions, Report on Transport Scenarios with a 20

and 40 Year Horizon - Developing a set of longterm scenarios (2030-2050) for transport and mobility in

Europe, European Commission DG TREN

Assessing the Land Use Change Consequences of European Biofuel Policies,

IFPRI

Renewable Energy Projections as Published in

the National Renewable Energy Action Plans of the European Member States,

EEA

Scope of data

Does it include EU 27? Yes Yes Yes Yes Yes

Does it include the transportation sector?

Yes Yes Yes Yes Yes

Are the different feedstock stocks considered?

No Yes No Yes Yes, for biofuels

Are the fuel types considered? Yes Yes Yes Yes Yes, for biofuels

Disaggregation of data

Are the EU 27 broken out? No No No Yes Yes

Is the transportation sector broken out?

Yes No Yes Yes Yes

Are the different feedstocks broken out?

No Yes No Yes Yes, for biofuels

Are the different fuel types broken out?

Yes No No Yes Yes, for biofuels

Timescale

Baseline data 2010 2000 2005 2008 2005

Projections Up to 2050 2030 Up to 2050 2020 2020

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 6

Reports SULTAN Tool

Impact of the use of biofuels on oil refining and fuels

specifications, Wood Mackenzie

Transvisions, Report on Transport Scenarios with a 20

and 40 Year Horizon - Developing a set of longterm scenarios (2030-2050) for transport and mobility in

Europe, European Commission DG TREN

Assessing the Land Use Change Consequences of European Biofuel Policies,

IFPRI

Renewable Energy Projections as Published in

the National Renewable Energy Action Plans of the European Member States,

EEA

Increment 5 year 1 year 5 year 12 years (only shows data for

2008 and 2012) 1 year

Policies considered

RED Yes Yes Yes Yes Yes

CO2 emissions from car/vans Yes Yes Yes No Yes

Data accessibility

Public Yes Yes No Yes Yes

Available for purchase N/A N/A No N/A N/A

Available through EC N/A N/A Yes Yes N/A

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 7

Table 2.3 Preliminary Assessment of Reports by Research and Government Agencies

(Legend: Good Average Poor).

Reports The World Energy Outlook 2012, International Energy

Agency (IEA)

EU-27 Annual Biofuels Report USDA / GAIN

Global Energy Outlook, Platts Insight

International Energy Outlook 2011, EIA/DOE

(USA)

Scope of data

Does it include EU 27? Yes Yes

This is a collection of articles about the energy outlook. It

does not contain any numerical projections of

energy consumption.

Yes

Does it include the transportation sector?

Yes No Yes

Are the different feedstock stocks considered?

No Yes Unclear

Are the fuel types considered?

Yes N/A, report dedicated to

biofuels Yes

Disaggregation of data

Are the EU 27 broken out? Yes Yes

–

No

Is the transportation sector broken out?

Yes No Yes

Are the different feedstocks broken out?

No Yes No

Are the different fuel types broken out?

Yes N/A, report dedicated to

biofuels Yes

Timescale

Baseline data 2010 2006 (actual data to 2009) –

2008

Projections 2035 2012 (forecast 2010 to 2012) 2035

Increment ~ 5 years 1 year 5 year

Policies considered

RED Yes Yes

–

Yes

CO2 emissions from car/vans

Yes Unclear Unclear

Data accessibility

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 8

Reports The World Energy Outlook 2012, International Energy

Agency (IEA)

EU-27 Annual Biofuels Report USDA / GAIN

Global Energy Outlook, Platts Insight

International Energy Outlook 2011, EIA/DOE

(USA)

Public Yes Yes

–

Yes

Available for purchase N/A N/A N/A

Available through EC Yes N/A N/A

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 9

Table 2.4 Preliminary Assessment of Reports by Trade Organizations and Energy Companies

(Legend: Good Average Poor).

Reports WORLD Model, EnSys

Europia White Paper on Fuelling EU Transport, A contribution from the EU refining Industry to the debate on the

future of transport, European Petroleum Industry Association

Long Term Outlook for Gas Demand and Supply, Eurogas,

The European Gas Industry

Energy Scenarios to 2050 (Scramble and Blueprint),

Shell

Outlook for Energy: A View to 2040, ExxonMobil

World Oil Outlook, OPEC

Scope of data

Does it include EU 27? Yes Yes Yes Yes Yes Yes

Does it include the transportation sector?

Yes Yes Yes Yes Yes Yes

Are the different feedstock stocks considered?

No Yes No No No No

Are the fuel types considered?

Yes Yes No No Yes Yes

Disaggregation of data

Are the EU 27 broken out? No Yes No No No No

Is the transportation sector broken out?

No Yes Yes Yes Yes Yes

Are the different feedstocks broken out?

No Yes No No No No

Are the different fuel types broken out?

Yes Yes No No No Yes

Timescale

Baseline data 2020 None particularly specified 2005 2000 1990 2010

Projections 2020 Up to 2015, 2020, 2030, 2035 2030 2050 2040 2035

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 10

Reports WORLD Model, EnSys

Europia White Paper on Fuelling EU Transport, A contribution from the EU refining Industry to the debate on the

future of transport, European Petroleum Industry Association

Long Term Outlook for Gas Demand and Supply, Eurogas,

The European Gas Industry

Energy Scenarios to 2050 (Scramble and Blueprint),

Shell

Outlook for Energy: A View to 2040, ExxonMobil

World Oil Outlook, OPEC

Increment N/A 1,5, 15 years 5 years 10 years 10-15 years 5 years

Policies considered

RED Yes Yes Yes No Unclear Yes

CO2 emissions from car/vans

Yes Yes No No Unclear Unclear

Data accessibility

Public No Yes Yes Yes Yes Yes

Available for purchase Yes N/A N/A N/A N/A N/A

Available through EC No N/A N/A N/A N/A N/A

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 11

2.4 In‐Depth Assessment

Subsequent to the preliminary assessment, an in-depth assessment was performed for the five selected studies / models which are listed in Table 2.5. The assessment criteria are as follows:

Transparency: The multitude of assumptions that go into the model must be readily accessible.

Data quality: The data sources used by the projections must be reliable, peer-reviewed, and accepted by the scientific / technical community.

Technical consideration: The assumptions used in the projections or in each scenario must be technically feasible and achievable.

Modelling domain: The model must target the EU 27 or EU 27 data must be extractable from projections that are on a regional or global scale. In addition, projections must be for the transport sector from 2010 to 2020 with feedstock and fuel type segregated. Finally, the projections should consider the penetration of electric vehicles into the vehicle fleet.

Modelling inputs: The report or data must clearly outline the key endogenous and exogenous variables that went into the model.

Regulatory considerations: Fuel projections developed must reflect the effect of the RED has on fuel demand and must include a justified estimate for the penetration of electric vehicles. Also, the limits on CO2 emissions from cars and vans must be accounted.

Table 2.5 tabulates the rating given to the five studies. The subsequent sections provide further details of the evaluation of each study.

Table 2.5 Summary of Rating for Important Reports and Studies After in‐Depth Analysis

(Legend: Good Average Poor).

Reports WORLD Model,

EnSys SULTAN Tool

The World Energy Outlook 2012, International

Energy Agency (IEA)

International Energy

Outlook 2011, EIA/DOE

(USA)

Impact of the use of biofuels on oil

refining and fuels specifications, Wood

Mackenzie

Modelling domain

Data quality

Transparency

Modelling inputs

Technical considerations

Regulatory considerations

2.4.1 The EU Transport GHG: Routes to 2050 – Illustrative Scenarios Tool (SULTAN)

The SULTAN (Sustainable Transport) Illustrative Scenarios Tool was developed for the European Commission’s Environment Directorate-General as part of the “EU Transport GHG: Routes to 2050” project. The tool was intended to serve as a “high-level calculator” and not an in-depth model of fossil fuels market supply and demand. It is a “high-level” tool in the sense that the outputs from this tool are for entire sectors instead of individual suppliers, facilities, etc. The model provides indicative estimates of the possible impacts of policy on the transport sector within the EU. The primary focus was on energy use, GHG emissions, costs, energy security, NOx emissions, and PM emissions. The tool allows for relatively quick scoping of a wide range of policy options.

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 12

The SULTAN tool is Microsoft Excel based, allowing for the public to make use of the tool and run scenarios in a familiar format. The tool is freely distributed allowing the public to develop alternative scenarios to model or re-create the results presented to the European Commission.

Table 2.6 Detailed Assessment of the SULTAN Tool

Model Domain

Level of Disaggregation

Are the EU 27 broken out? Yes

Is the data broken out for each member state?

No

Is the data broken out by individual refineries or refinery type?

No

Are the different feedstocks broken out?

Yes.

Are the different fuel types broken out? Yes

Are the different modes of transportation broken out?

Yes

Is the penetration of electric vehicles considered?

Yes

Timescale

Range Ranges from 2010 to 2050

Increments 5 year increments

Year of actual data on which projections are based

2010 baseline

Other

Data Quality

Is EUROSTAT used? No

What other sources are used? PRIMES-TREMOVE Tremove v3.3.2

Do the GHG intensity values for biofuels match EC values in Annex 5 of

the RED for 2010? Yes, uses values provided by the EC

Do the GHG intensity values for fossil fuels match Annex 1 of the amended

directive?

Unclear if these are the same values as those that can be found in the annex of the Fuel Quality Directive.

Transparency

Publicly available tool and supporting databases. Tabular results for each modelling scenario, including the baseline.

Exact equations used/calculation methodology is unclear.

Modelling Inputs

GDP Yes (Source: PRIMES-TREMOVE)

Population Yes (Source: PRIMES-TREMOVE)

Other Exogenous No projections regarding trade impacts and crude oil feedstock variations.

Other Endogenous Passenger-km (Source: PRIMES-TREMOVE) Tonne-km (Source: PRIMES-TREMOVE)

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 13

Model Domain

Technical Considerations

Model Simplifications

Depending on demand of energy and supply of biofuels, corrective actions might have to be taken to still reach the target emissions. It was assumed that it was possible to achieve these targets through improvements in efficiency, shifting modes of transportation, and strengthening regulation.

Base scenario (BAU-a) assumes no unconventional oil is used for production of petrol and diesel in Europe.

Others Assumptions

Reduction Scenario (R1) designed to achieve the 60% GHG reduction target (on 1990 levels) for transport excluding maritime shipping by 2050. Conventional fuel prices used for Scenario R1 were provided by the EC.

Fuel prices for the Baseline scenario (BAU-a) were higher than those used for the regulatory scenarios.

2050 targets were assumed to be achieved through predominantly technical measured, plus additional measures consistent with other White Paper Goals (e.g. internalizing of external costs, additional shift of road freight transport to rail/IWW).

Scenario R2 modelled sensitivity in Scenario R1 by assuming biofuel GHG savings would be lower.

Scenario R3 modelled sensitivity in Scenario R1 by assuming biofuel and electricity GHG savings would be lower.

Scenario R4 modelled sensitivity of Scenario R1 assuming there would be lower demand for fuels.

Scenario R5 modelled sensitivity of Scenario R1 assuming there would be higher demand for fuels.

All scenarios were carried out on a lifecycle basis (denoted by the “-a” after the scenario name) as well as a direct emissions basis (denoted by the “-b” after the scenario name).

Percent reductions of lifecycle GHG on 2010 on basis of low biofuel savings for each given transport type except aviation and rail.

Assumed biofuel GHG savings rising from 55% in 2010 to 85% in 2050.

Regulatory Considerations

Is the RED/FQD included? Yes

Are the CO2 limits for cars/vans considered?

Yes

Others policies considered? Yes

From the review of the SULTAN tool, as summarized in the table above, it was evident that the tool was user-friendly and transparent. It was also evident that the outputs of the model were in line with the relevant policies outlined by the EC in Task 1.1. The tool exhibited great adaptability as well as consideration for numerous scenarios in combination with current regulatory practices. However, the model did not provide projections of crude trade balance and feedstock mix.

SULTAN does provide forecasts of EU27 demand for the five relevant fossil fuels (petrol, diesel, non-road gasoil, LPG, CNG). However it is not a petroleum market model, and does not take into account crude supply, oil refineries or trade. SULTAN appears to make broad assumptions in that specific energy consumption is not attributed to the specific petroleum fuel in diesel, petrol, kerosene and ship marine fuel. For example, SULTAN’s forecast for EU27 kerosene and ship marine fuel is inconsistent with both historical data and other forecasts such as IEA. Although kerosene and ship marine fuel are not within the scope of the fuels covered by the FQD Article 7a GHG intensity reduction target, their supply and

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 14

demand affect the petroleum market and trade and refinery utilization. SULTAN’s forecast for petrol and diesel also appears questionable. The SULTAN petrol and diesel forecast was analysed against historical Eurostat data and also the IEA forecast, and is significantly different than the IEA forecast. Therefore the SULTAN forecast appears to have made errors in determining which fuels will supply the energy demand on the liquid fuels market and does not represent the liquid fuels product market balance, and therefore will not be relied upon in this study.

2.4.2 The World Energy Outlook 2011 (WEO 2011)

The World Energy Outlook 2011 (WEO 2011) is published annually by the International Energy Agency (IEA) and provides energy market analysis and projections. These projections are used by the public and private sectors as a framework on which to base policy-making, planning, investment decisions, and to identify what actions are needed to promote sustainable energy in the future. The WEO 2011 gives the latest energy demand and supply projections for various future scenarios—broken down by country, energy resource, and sector. It also gives focus to such topical energy sector issues as the scale of fossil fuel subsidies and support for renewable energy and their impact on energy, economic, and environmental trends.

The WEO 2011 projections are based on the outputs from the World Energy Model (WEM). The model is a large-scale mathematical construct designed to replicate how energy markets function and is the principal tool used to generate detailed sector-by-sector and region-by region projections for various scenarios. The model consists of six main modules: 1) final energy demand (with sub-models covering residential, services, agriculture, industry, transport and non-energy use); 2) power generation and heat; 3) refinery/petrochemicals and other transformation; 4) fossil-fuel supply; 5) CO2 emissions; and 6) investment. Huge quantities of historical data on economic and energy variables are used as inputs to the WEM. Much of the data is obtained from the IEA’s own databases of energy and economic statistics (http://www.iea.org/statistics). Additional data from a wide range of external sources is also used. These sources are indicated in the relevant sections of the WEM – Methodology and Assumptions document. The WEM is frequently reviewed and updated to ensure its completeness and relevance.

In Table 2.7 below, a detailed characterisation is given to illustrate the WEO 2011 as a possible source of 2020 fuel projections, based on the criteria outlined in this study.

Table 2.7 Detailed Assessment of the WEO 2011

Model Domain

Level of Disaggregation

Are the EU 27 broken out? Yes

Is the data broken out for each member state?

No

Is the data broken out by individual refineries or refinery type?

No

Are the different feedstocks broken out?

No

Are the different fuel types broken out? Yes Very limited (broken out into mainly petrol and biofuels [ethanol and biodiesel]) All fuels are grouped into “oil”

Are the different modes of transportation broken out?

Yes Data/projections limited to passenger light duty vehicles (PLDVs)—including

conventional, electric, and plug-in hybrids. In general, PLDVs comprise passenger cars, sports utility vehicles, and pick-up trucks.

Is the penetration of electric vehicles Yes

Impact Analysis of Options for Implementing Article 7a of Directive 98/70/EC (Fuel Quality Directive) Final Report under Contract 071201/2011/608705/SER/CLIMA.C2

August 2013 15

Model Domain

considered?

Timescale

Range Ranges from 2010 to 2035

Increments 5 year increments; no consistent increments of 1 year (for more comprehensive estimates)

Year of actual data on which projections are based

Year 2010 baseline (most available complete annual data; 2011 estimates not available until late 2012)

Other Not based on most current complete data (WEO 2012 with 2011 data not published yet; scheduled for Nov 2012)

Data Quality

Is EUROSTAT used? No

What other sources are used? World Energy Model (WEM), IEA data and analysis, U.S. Federal Highway Association database, China Automotive Review statistics database, WardsAuto, National Bureau of Statistics of China, German Federal Institute for Geosciences and Natural Resources, U.S. Geological Survey, Oil and Gas Journal

Do the GHG intensity values for biofuels match EC values in Annex 5 of

the RED for 2010?

No GHG intensity values not given for biofuels in WEO 2011. Provides carbon

intensities measured as “emissions per dollar of gross domestic product” (as opposed to “per MJ” of energy)

Do the GHG intensity values for fossil fuels match Annex 1 of the amended

directive?

No GHG intensity values not given for fossil fuels in WEO 2011

Transparency

Publicly available document Provides supporting documentation of methodology and assumptions for the WEM Provides descriptions and methodologies for: transport sector demand module,