impact of exchange rate volatility on commodity trade between u.s. and china: is there a third...

TRANSCRIPT

Impact of exchange rate volatility on commodity tradebetween U.S. and China: is there a third country effect

Mohsen Bahmani-Oskooee & Jia Xu

Published online: 6 April 2010# Springer Science+Business Media, LLC 2010

Abstract Impact of exchange rate uncertainty on trade flows still continues to dominatethe literature. Most previous research has used aggregate trade data between one countryand the rest of the world or between two countries at a bilateral level. A recent study,however, considered the trade between the U.S. and China at the commodity level, butexcluded the “third-country” effect in its analysis. In this paper, we consider thecommodity trade between the U.S. and China one more time and investigate whethervolatility of the real U.S. dollar-Canadian dollar has any implication on the trade flowsbetween the U.S. and China. The answer happens to be in the affirmative, though a moresignificant third-country effect is found in the short run as compared to the long run.

Keywords Exchange Rate Volatility . China . The U.S. . Canada . Industry Data

JEL Classification F31

1 Introduction

Since the late 1970s when China adopted some liberalization measures to boost hertrade and some elements of free-market economy to improve her standard of living,

J Econ Finan (2012) 36:555–586DOI 10.1007/s12197-010-9126-y

Mohsen Bahmani-Oskooee is Patricia and Harvey Wilmeth Professor of economics and director of theCenter for Research on International Economics at the University of Wisconsin-Milwaukee. Jia Xu is adoctoral student in the department of economics at the University of Wisconsin-Milwaukee.

Valuable comments of an anonymous referee as well as those of the editor are greatly appreciated withoutimplicating them.

M. Bahmani-Oskooee (*) : J. XuThe Center for Research on International Economics, The University of Wisconsin-Milwaukee,Milwaukee, WI 53201, USAe-mail: [email protected]

M. Bahmani-Oskooee : J. XuThe Department of Economics, The University of Wisconsin-Milwaukee, Milwaukee, WI 53201, USA

it has become one of the major trading partners of the U.S. In 1978, the U.S. exportsto China were in the magnitude of almost 816 million dollars, exceeding her importsfrom China in tune of 356 million dollars. However, in 2006, the last year for whichdata were available, that trend has shifted in favor of China. In that year, the U.S.exported about 51 billion dollars while she imported 306 billion dollars. During thesame period, the yuan has fluctuated against the U.S. dollar from 1.684 yuan perdollar to 7.973 yuan per dollar.1

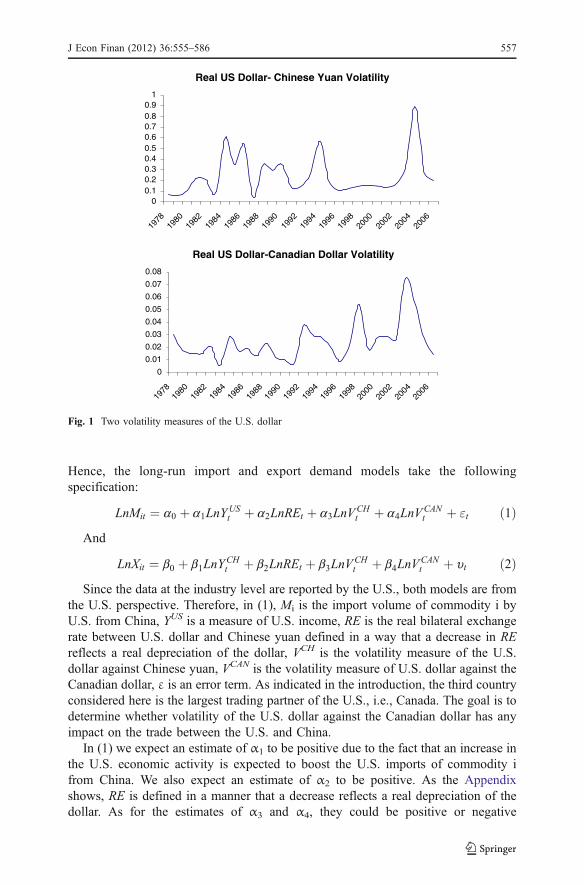

A glance through the monthly obervations of the yuan-dollar real exchange rateindicate some degree of volatility, as reflected in Fig. 1. In addition to the realdepreciation of the yuan against the U.S. dollar which could influence China’sexports to and imports from the U.S., the volatility of the yuan-dollar exchange ratecould also affect the trade flows between the two countries. Could part of theincreased trade between the U.S. and China be also due to exchange rate volatilitybetween the U.S. dollar and the Canadian dollar? As reflected in Fig. 1, thisvolatility has also been erratic during the period of 1978–2006 and could giveincentive to traders in the U.S. to shift their imports or exports from Canada toChina. This third country effect was originally recognized by Cushman (1983, 1986)who investigated the impact of exchange rate uncertainty on bilateral trade flows ofseveral industrial countries. Concentrating on the floating exchange rate period andthe U.S.-Canadian trade, Cushman (1986) found a significantly positive effect ofexchange rate uncertainty on U.S. exports to Canada. However, this significantlypositive effect disappeared when the third-country effect was included in theanalysis. Thus, it appears that excluding the third-country effect could haveimplications on the results.

In a recent article, Bahmani-Oskooee and Hegerty (2007) investigated the impact ofvolatility of the yuan-dollar rate on commodity trade between the U.S. and China. Outof 88 industries considered, they showed that imports and exports of 38 indistrues wereaffected significantly in the short run. In the long run, however, while 36 of China’sexporting industries were significantly affected, only 33 of her importing industrieswere affected. Following Cushman’s (1986) analysis, we wonder if including the third-country effect in Bahmani-Oskooee and Wang’s (2007) models will change theirfinding in one direction or another.2 To this end, we introduce the models and themethodology in Section 2. Section 3 reports the results and Section 4 concludes.

2 The models and methods

To investigate the imact of exchange rate volatility on trade flows, every studyexpresses the volume of imports and exports as a function of a scale variable andrelative prices in addition to a measure of exchange rate volatility. Since our goal isto include a third-country effect, we add the volatility measure of the real U.S.dollar-Canadian dollar to Bahmani-Oskooee and Wang’s (2007) specifications.

1 For more on China’s reform policies see Zhang (1999).2 A review article by Bahmani-Oskooee and Hegerty (2007) shows that as a matter of fact, most studieshave ignored the third-country effect in the literature.

556 J Econ Finan (2012) 36:555–586

Hence, the long-run import and export demand models take the followingspecification:

LnMit ¼ a0 þ a1LnYUSt þ a2LnREt þ a3LnV

CHt þ a4LnV

CANt þ "t ð1Þ

And

LnXit ¼ b0 þ b1LnYCHt þ b2LnREt þ b3LnV

CHt þ b4LnV

CANt þ ut ð2Þ

Since the data at the industry level are reported by the U.S., both models are fromthe U.S. perspective. Therefore, in (1), Mi is the import volume of commodity i byU.S. from China, YUS is a measure of U.S. income, RE is the real bilateral exchangerate between U.S. dollar and Chinese yuan defined in a way that a decrease in REreflects a real depreciation of the dollar, VCH is the volatility measure of the U.S.dollar against Chinese yuan, VCAN is the volatility measure of U.S. dollar against theCanadian dollar, ε is an error term. As indicated in the introduction, the third countryconsidered here is the largest trading partner of the U.S., i.e., Canada. The goal is todetermine whether volatility of the U.S. dollar against the Canadian dollar has anyimpact on the trade between the U.S. and China.

In (1) we expect an estimate of α1 to be positive due to the fact that an increase inthe U.S. economic activity is expected to boost the U.S. imports of commodity ifrom China. We also expect an estimate of α2 to be positive. As the Appendixshows, RE is defined in a manner that a decrease reflects a real depreciation of thedollar. As for the estimates of α3 and α4, they could be positive or negative

Real US Dollar- Chinese Yuan Volatility

00.10.20.30.40.50.60.70.80.9

1

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Real US Dollar-Canadian Dollar Volatility

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Fig. 1 Two volatility measures of the U.S. dollar

J Econ Finan (2012) 36:555–586 557

depending on the risk-taking position of traders. An increase in volatility of the U.Sdollar-yuan rate could introduce uncertainty about the future prices and profitshurting trade today. On the other hand, the same volatility could induce traders totrade more in order to avoid loss of profit and income in the future. The same couldapply to volatility of the U.S. dollar-Canadian dollar. Increased volatility couldintroduce more uncertainty which in turn, could intice U.S. traders to divert tradefrom Canada to China. Alternatively, increased U.S. dollar-Canadian dollar volatilitycould provide opportunities for traders to capitalize on the situation and divert tradefrom China to Canada.

Shifting to the export demand model (2), Xi denotes the U.S. export of commodityi to China which is expected to depend positively on Chinese income (YCH) andnegatively on the real exchange rate, RE. Therefore, we expect estimates β1 and β2

to be positive and negative respectively. Following the same argument as above, theestimates of β3 and β4 could be negative and positive.

In line with Bahmani-Oskooee and Wang’s (2007) approach, we also try todistinguish the short-run effects of all right-hand side variables in (1) and (2) fromtheir long-run effects on the trade flows by specifying these models in error-correction modeling formats. Like them, we follow Pesaran et al.’s (2001) boundstesting approach as in (3) and (4) below:

ΔLnMit ¼ c0 þXn1

k¼1

c1k ΔLnMit�k þXn2

k¼0

c2k ΔLnYUSt�k þ

Xn3

k¼0

c3k ΔLnREt�k þXn4

k¼0

c4k ΔLnVCHt�k

þXn5

k¼0

c5k ΔLnVCANt�k þd0LnMit�1 þ d1LnY

USt�1 þ d2LnREt�1 þ d3LnV

CHt�1 þ d4LnV

CANt�1 þ mt

ð3Þ

And

ΔLnXit ¼ d0 þXn1

k¼1

d1k ΔLnXit�k þXn2

k¼0

d2k ΔLnYCHt�k þ

Xn3

k¼0

d3k ΔLnREt�k þXn4

k¼0

d4k ΔLnVCHt�k

þXn5

k¼0

ΔLnVCANt�k þl0LnXit�1 þ l1LnY

CHt�1 þ l2LnREt�1 þ l3LnV

CHt�1 þ l4LnV

CANt�1 þ xt

ð4ÞThe advantage of the bounds testing approach is that there is no need for pre-unit

root testing and variables could be a combination of stationary and non-stationaryvariables. Pesaran et al. (2001) account for stationary and non-stationarity when theyapply the F test for joint significance of the lagged level variables in each model as asign of cointegration. An upper bound new critical value is tabulated by Pesaran etal. (2001) by assuming all variables to be non-stationary. Similarly, when all thevariables are assumed to be stationary, they tabulate a lower bound critical value. Toestablish cointegration, the calculated F statistic must be greater than the upperbound critical value. Another advantage of specifications (3) and (4) are that theyprovide the short-run and the long-run effects in one estimation step. For example,concentrating on the effects of VCH on imports while the short-run effects areinferred by the estimates of c4k’s in model (3), its long-run effects are judged by the

558 J Econ Finan (2012) 36:555–586

estimate of δ3 normalized on δ0. The same interpretation applies for other variablesin both models (3) and (4).3

3 The results

Error-correction models (3) and (4) are estimated for 101 industries that tradebetween the U.S. and China, using annual data over the period 1978–2006. Theupdated data is longer than the period considered by Bahmani-Oskooee and Wang(2007) by 2 years and includes 13 additional industries for which the revised data setis complete. Like Bahmani-Oskooee and Wang (2007) and many others, we imposea maximum of four lags on each first differenced variable and use Akaike’sInformation Criterion (AIC) to select the optimum number of lags in each model. Wethen report selected results for each industry from each optimum model. Consideringmodel (3) first, the results are reported in Tables 1, 2 and 3.

Table 1 includes only the short-run coefficient estimates. However, due to volumeof results we only report the short-run coefficient estimates of two exchange-ratevolatility measures. From these results we gather that the real U.S. dollar-Chineseyuan volatility (VCH) carries at least one lagged significant coefficient at the 10%level in 87 out of 101 industries, implying that the U.S. imports (or Chinese exports)of most industries are affected by their own exchange rate uncertainty. The real U.S.dollar-Canadian dollar volatility measure (VCAN) carries at least one significantcoefficient in 88 of 101 industries, implying that indeed, the third country effect is inforce and has implication on the U.S. imports from China. What remains to be seenis whether these significant short-run effects are transitory or if they last into the longrun. To answer this question, we shift to Table 2.

Table 2 reports the long-run coefficient estimates for all variables. As can be seen,the VCH variable carries a significant coefficient, at least at the 10% level, in only 44industries. Furthermore while the estimated coefficient is negative in 20 cases, it ispositive in the remaining 24 industries. However, the VCAN measure of volatilitycarries a significant coefficient only in 27 cases. More precisely, in 16 industriescoded 011, 221, 276, 514, 551, 553, 554, 613, 656, 665, 698, 711, 812, 842, 861,861, and 896 the long-run effect is positive impying that volatility of the U.S. dollaragainst the Canadian dollar induces U.S. importers to import more from China. Onthe other hand in 11 industries coded 025, 112, 261, 533, 553, 653, 841, 864, 893,894, and 895 the effect is negative. In sum, it appears that while the third countrymeasure of exchange rate volatility has short-run effects on the majority of the U.S.importing industries from China, the short-run effects last into the long run in only25% of the industries which all together do have almost 25% of the market share.4

Majority of the affected industries happen to be small as measured by their marketshare. The only large industries that are affected by third-country effect is 841

4 Note that the market share of each industry is reported inside the parenthesis next to the name of eachindustry in Tbale 2. For example, 0.494 as market share of industry 031 means that this industry hasalmost 0.5% (not 5%) market share. These shares are defined as the ratio of each industry’s imports as apercent of total U.S. imports from China.

3 For other applications of this approach see Siddiki (2000), Boyd et al. (2001), Bahmani-Oskooee et al. (2005),Halicioglu (2007), Tang (2007), Mohammadi et al. (2008), and Bahmani-Oskooee and Bolhasani (2008).

J Econ Finan (2012) 36:555–586 559

Tab

le1

Short-run

coefficientestim

ates

oftheU.S.Im

portDem

andfrom

model

3(absolutevalueof

t-ratio

sinside

parentheses)

Industry

Short-Run

Coefficient

Estim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

011-Meat,fresh,

chilled

orfrozen

−0.73(5.66)

––

0.16(0.88)

−0.87(4.42)

−0.76(4.58)

025-

Eggs

−0.20(3.80)

0.39(5.48)

0.34(5.55)

−0.07(0.98)

0.41(4.81)

0.20(3.02)

031-

Fish,fresh&

simplypreserved

0.08(1.32)

––

0.20(2.65)

––

032-

Fish,in

airtight

containers,nes

&f

−0.37(5.53)

−0.50(6.68)

−0.31(3.74)

0.44(4.65)

−0.81(4.80)

−0.24(2.33)

047-Meal&

flourof

cereals,except

whea

0.52(2.67)

0.96(4.66)

−0.89(3.76)

−2.20(5.32)

−0.89(3.02)

048-Cerealpreps&

prepsof

flourof

fr−0

.01(0.31)

0.10(4.52)

–−0

.07(1.99)

––

051–Fruit,

fresh,

andnuts-excl.oil

0.04(0.88)

−0.12(2.78)

–0.09(1.85)

0.30(6.22)

–

052-Dried

fruitincludingartificially

0.62(6.06)

−1.16(4.53)

−0.44(3.51)

−0.20(1.82)

0.31(2.62)

–

053-

Fruit,preservedandfruitpreparati

−0.06(1.26)

−0.32(5.40)

−0.21(4.56)

0.13(2.20)

0.08(1.32)

–

054-Vegetables,roots&

tubers,fresho

0.22(2.90)

−0.17(1.96)

−0.17(2.13)

−0.16(1.79)

0.41(3.16)

0.24(2.45)

055-Vegetables,roots&

tubers

pres

or0.06(1.79)

−0.19(3.49)

−0.18(4.23)

0.08(1.47)

−0.25(4.81)

−0.13(2.82)

061-Sugar

andhoney

0.04(0.41)

––

−0.00(0.03)

––

062-Sugar

confy,

sugarpreps.ex

chocol

0.05(1.61)

−0.03(0.75)

−0.11(3.13)

0.09(2.16)

0.14(3.20)

0.18(4.82)

071-Coffee

0.40(0.83)

2.63(3.33)

2.51(3.84)

−2.12(3.98)

−0.93(1.87)

–

073-Chocolate

&otherfood

preptnscont

−0.01(0.06)

−0.60(3.74)

–0.41(2.13)

1.23(5.01)

0.65(3.58)

074-Tea

andmate

0.15(4.31)

−0.29(5.20)

−0.14(3.07)

0.03(0.70)

0.21(3.89)

0.07(1.55)

075-Spices

0.19(6.37)

−0.17(2.76)

−0.38(7.06)

0.11(2.99)

−0.15(3.58)

–

099-

Foodpreparations,nes

−0.10(4.28)

0.02(0.49)

0.09(2.90)

−0.09(2.63)

0.17(5.84)

–

111-Non-alcoholic

beverages,nes

0.19(2.44)

0.25(3.36)

–−0

.17(1.89)

−0.20(1.82)

−0.27(3.18)

112-Alcoholic

beverages

0.05(2.47)

−0.01(0.51)

0.18(7.41)

−0.10(3.26)

0.34(6.45)

0.06(1.61)

121-Tobacco,unmanufactured

−0.21(0.90)

––

−0.08(0.28)

1.08(3.21)

1.45(4.94)

122-Tobacco

manufactures

−0.37(1.53)

−0.38(1.64)

–1.60(5.57)

1.31(3.50)

1.18(4.26)

212-Fur

skins,undressed

0.10(0.34)

−1.06(4.27)

–0.53(1.55)

––

560 J Econ Finan (2012) 36:555–586

Industry

Short-Run

Coefficient

Estim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

221-Oil-seeds,oilnutsandoilkernels

0.86(10.08)

−1.51(11.12)

−0.80(8.49)

0.29(2.55)

––

261-Silk

0.26(5.25)

−0.61(9.27)

0.48(5.64)

−13.29(5.13)

2.69(1.18)

5.06(2.05)

262-

Woolandotheranim

alhair

−0.28(3.35)

––

−0.03(0.34)

––

265-Vegetable

fibres,exceptcotto

nand

0.34(1.28)

−0.17(0.56)

−0.93(3.82)

−0.21(0.53)

−1.03(3.66)

–

276–

Other

crudeminerals

−0.06(1.82)

−−

0.12(2.41)

−0.36(6.53)

−0.22(4.86)

283-

Ores&

concentrates

ofnon-ferrous

0.24(5.12)

−0.10(1.63)

−0.26(4.38)

0.10(1.46)

−0.65(6.67)

−0.48(6.59)

291-Crude

anim

almaterials,nes

0.01(0.42)

−0.00(0.11)

−0.10(2.97)

0.12(3.22)

−0.12(3.41)

–

292-Crude

vegetablematerials,nes

−0.09(1.91)

−0.10(2.00)

–0.09(1.60)

0.34(4.37)

0.19(3.45)

332-

Petroleum

products

−0.16(2.67)

−0.18(2.71)

−0.22(3.27)

0.33(4.39)

––

422-Other

fixedvegetableoils

−0.03(0.27)

−0.56(4.03)

−0.37(3.14)

0.15(1.24)

0.46(3.16)

0.60(4.86)

512-Organic

chem

icals

0.04(1.75)

––

0.00(0.15)

−.7476E-3(0.04)

0.06(2.35)

513-Inorg.chem

icals-elem

s.,oxides,halog

0.03(0.75)

––

0.05(0.94)

−0.27(5.91)

−0.10(2.16)

514-Other

inorganicchem

icals

−0.07(1.63)

––

−0.02(0.25)

−0.39(5.19)

−0.32(5.75)

533-Pigments,paints,varnishes&

relat

0.43(3.69)

0.48(4.71)

0.20(1.99)

−1.02(4.89)

0.88(4.14)

0.39(2.90)

541-Medicinal

&pharmaceutical

products

−0.04(1.27)

––

−0.03(0.71)

0.14(3.46)

–

551-Essentialoils,perfum

eandflavour

0.00(0.07)

−0.09(3.20)

–0.04(0.90)

––

553-Perfumery,

cosm

etics,dentifrices,

0.07(2.04)

0.59(12.09)

0.35(8.53)

−0.25(7.06)

0.05(1.39)

0.07(2.05)

554-Soaps,cleansing

&polishing

prepara

0.19(5.82)

−0.71(8.04)

−0.34(6.99)

0.29(5.82)

−0.25(5.90)

−0.14(3.56)

571-

Explosivesandpyrotechnicproducts

−0.03(1.60)

−0.07(2.60)

−0.06(2.72)

0.05(2.07)

0.36(7.76)

0.22(6.40)

599-Chemical

materialsandproducts,nes

−0.25(10.74)

0.13(2.92)

0.17(6.20)

0.15(5.15)

−0.14(2.74)

−0.14(3.48)

611-Leather

0.61(2.14)

−1.28(2.77)

−0.56(1.78)

0.61(2.53)

––

612-Manuf.ofleatheror

ofartif.orrec

0.00(0.07)

––

0.13(1.47)

––

613-Fur

skins,tanned

ordressed,

inclu

−0.33(2.64)

––

0.39(2.36)

––

631-Veneers,plywoodboards

&otherwood

0.13(1.12)

−0.62(2.64)

−0.43(2.57)

0.39(1.98)

0.29(1.74)

–

632-Woodmanufactures,nes

−0.09(6.10)

−0.04(2.06)

0.04(2.09)

0.06(3.13)

0.13(7.76)

633-Corkmanufactures

0.11(1.66)

−0.26(3.16)

−0.25(3.13)

−0.07(0.84)

––

641-Paper

andpaperboard

0.04(0.36)

0.51(5.49)

0.00(0.03)

––

–

642-Articlesof

paper,pulp,paperboard

−0.03(0.95)

––

0.09(2.30)

––

J Econ Finan (2012) 36:555–586 561

Tab

le1

(con

tinued)

Industry

Short-Run

Coefficient

Estim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

651-Textileyarn

andthread

0.17(2.04)

−0.71(3.71)

−0.39(3.03)

0.38(2.76)

––

652-Cottonfabrics,woven

ex.narrow

ors

0.03(0.68)

––

−0.07(1.17)

0.33(4.27)

0.24(3.56)

653-Textfabricswoven

exnarrow

,spec,

−0.03(1.65)

−0.56(13.65)

−0.29(12.60)

0.25(8.64)

0.42(9.44)

0.29(8.58)

654-Tulle,lace,em

broidery,ribbons,t

−0.29(2.65)

––

−0.06(0.42)

––

655-Special

textile

fabricsandrelated

0.06(1.19)

−0.27(3.94)

−0.28(5.09)

−0.02(0.30)

−0.30(4.78)

−0.12(2.18)

656-Made-up

articles,wholly

orchiefly

0.1768(0.01)

−0.27(7.38)

−0.13(5.19)

0.22(7.09)

−0.10(3.97)

–

657-Floor

coverings,tapestries,etc.

0.06(4.05)

––

0.07(3.94)

––

661-Lim

e,cement&

fabr.bldg.mat.-ex

gla

−0.21(3.70)

−0.38(6.14)

–0.38(4.47)

0.14(1.73)

–

663-Mineral

manufactures,nes

0.45(3.85)

−0.68(3.17)

−0.81(5.39)

0.25(2.81)

0.29(2.23)

0.42(4.26)

664-Glass

0.03(0.68)

0.19(3.44)

–−0

.19(2.88)

−0.12(1.84)

−0.15(2.63)

665-Glassware

−0.18(5.31)

−0.11(3.34)

–0.10(2.72)

−0.26(3.94)

−0.10(1.75)

666-Pottery

−0.09(6.76)

−0.04(2.83)

–0.08(5.36)

0.01(0.64)

0.06(3.84)

667-Pearlsandprecious

andsemi-precio

0.56(11.78)

0.54(8.90)

0.16(4.36)

−0.67(10.80)

0.16(2.61)

0.18(4.26)

687-Tin

−0.31(3.51)

––

0.11(0.97)

––

689-Miscell.non-ferrousbase

metals

0.16(3.55)

−0.34(6.79)

−0.10(2.09)

0.18(3.63)

−0.27(4.03)

−0.28(4.77)

692-

Metal

containers

forstorageandtr

0.21(5.22)

0.24(4.64)

0.12(2.72)

−0.16(3.02)

−0.13(2.54)

−0.27(5.59)

694-Nails,screw

s,nuts,bolts,rivetsand

−0.05(0.93)

––

0.12(1.68)

−0.32(3.65)

−0.14(2.22)

695-Toolsforusein

thehand

orin

mac

−0.03(1.64)

−0.06(2.77)

−0.06(2.85)

0.06(2.47)

0.04(1.59)

0.07(2.82)

696-Cutlery

−0.06(1.68)

––

−0.02(0.35)

0.13(2.48)

0.20(3.78)

697-Household

equipm

entof

base

metals

−0.05(1.90)

––

−0.07(2.41)

−0.07(2.62)

−0.08(3.07)

698-Manufacturesof

metal,nes

−0.04(2.16)

−0.12(6.46)

–0.06(2.59)

––

711-Pow

ergeneratin

gmachinery,othert

0.07(2.66)

−0.28(5.61)

−0.07(2.20)

0.13(4.35)

––

714-Officemachines

0.03(0.27)

––

−0.36(1.75)

0.35(1.79)

0.64(3.93)

562 J Econ Finan (2012) 36:555–586

Tab

le1

(con

tinued)

Industry

Short-Run

Coefficient

Estim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

715-Metalworking

machinery

0.10(1.86)

−0.13(2.24)

–0.13(1.94)

0.16(2.34)

0.13(2.28)

717-Textileandleathermachinery

0.24(2.42)

−0.26(2.07)

−0.26(2.36)

0.45(3.47)

––

719-Machinery

andappliances-non

electr

−0.09(2.77)

0.03(0.91)

0.09(3.03)

−0.13(3.60)

−0.08(2.21)

−0.17(5.20)

722-Electricpower

machinery

andsw

itch

−0.11(0.90)

––

0.30(2.26)

––

724-

Telecom

munications

apparatus

0.07(1.09)

−0.18(2.34)

−0.27(3.74)

−0.09(0.96)

−0.26(3.13)

–

725-Dom

estic

electrical

equipm

ent

0.06(1.48)

−0.18(3.71)

−0.16(3.36)

0.08(1.54)

––

726-Elec.apparatusformedic.purp.,radi

−0.03(0.38)

0.27(2.48)

0.41(5.03)

0.11(1.07)

––

729-Other

electrical

machinery

andappa

−0.17(4.66)

−0.11(2.90)

–0.16(3.58)

––

812-Sanitary,plumbing,heatin

g&

lightin

−0.40(9.37)

−0.07(1.68)

–0.09(2.17)

−0.11(2.00)

–

821-Furniture

−0.09(4.62)

––

0.02(0.79)

0.13(4.58)

0.07(2.79)

831-Travelgoods,handbags

andsimilar

0.07(5.03)

−0.09(5.45)

−0.07(4.86)

−0.01(0.40)

0.08(4.13)

0.06(2.96)

841-Clothingexcept

furclothing

0.03(1.62)

−0.16(4.57)

−0.08(2.83)

0.05(1.80)

0.28(6.49)

0.23(6.70)

842-Fur

clothing

andarticlesof

artifi

0.01(0.14)

––

0.37(3.50)

−0.52(4.22)

−0.27(3.11)

851-Footwear

−0.02(1.35)

−0.05(3.12)

−0.04(2.69)

0.02(1.33)

––

861-Scientific,m

edical,optical,m

eas./co

−0.39(8.27)

––

0.25(4.34)

−0.39(6.03)

−0.21(3.85)

862-Photographicandcinematographic

su−0

.33(2.23)

––

0.90(4.16)

−1.59(5.80)

−0.73(3.64)

864-Watches

andclocks

−0.22(3.88)

0.47(3.96)

0.51(4.92)

−0.07(1.00)

0.32(4.03)

–

891-Musical

instruments,sound

recorders

−0.07(1.70)

––

0.09(1.81)

––

892-Printed

matter

−0.02(0.81)

––

−0.06(1.39)

––

893-Articlesof

artificialplastic

mate

−0.01(0.18)

0.27(4.77)

0.21(4.38)

−0.17(3.15)

0.10(2.17)

–

894-Peram

bulators,to

ys,gam

esandsporti

0.03(0.71)

0.07(2.04)

–−0

.09(2.04)

0.34(4.54)

0.16(3.14)

895-Officeandstationery

supplies,nes

0.23(3.39)

––

−0.11(1.52)

0.41(4.59)

0.40(5.29)

896-Works

ofart,collectorspieces

and

−0.37(5.77)

−0.50(7.96)

–0.67(7.04)

0.06(0.62)

0.19(2.37)

897-Jewellery

andgold/silv

er-smith

swa

−0.09(4.17)

0.07(2.14)

0.13(4.79)

−0.05(1.95)

––

899-Manufacturedarticles,nes

−0.03(2.05)

0.11(5.35)

–−0

.01(0.34)

−0.07(3.06)

–

941-Animals,nes-incl.zoo

anim

als,dogs

−0.30(1.97)

−0.34(2.49)

−0.52(3.40)

0.38(2.32)

−2.53(6.66)

−0.97(3.66)

951-Firearm

sof

war

andam

munition

ther

0.17(1.76)

−0.64(4.80)

−0.45(3.84)

−0.06(0.47)

0.77(3.99)

0.32(1.94)

J Econ Finan (2012) 36:555–586 563

Tab

le2

Long-runcoefficientestim

ates

ofim

portdemand(t-ratiosinside

parentheses)

Industry

(trade

share%)

Long-Run

Coefficient

Estim

ates

Constant

LnV

CH

LnV

CAN

LnY

US

LnR

E

011-Meat,fresh,

chilled

orfrozen

(0.004)

−7.88(0.90)

−1.01(3.30)

1.98(2.90)

4.27(2.33)

−0.85(0.83)

025-

Eggs(0.002)

−14.46(4.99)

−0.54(3.32)

−0.76(3.20)

2.64(4.20)

1.36(3.29)

031-

Fish,fresh&

simplypreserved(0.494)

−13.65(1.47)

0.24(0.90)

−0.32(0.67)

4.26(1.82)

0.90(0.57)

032-

Fish,in

airtight

containers,nes

&f(0.172)

58.96(0.89)

−1.79(0.91)

8.99(1.31)

−6.38(0.55)

3.85(0.77)

047-Meal&

flourof

cereals,except

whea(0.000)

52.66(0.85)

−3.11(0.73)

5.67(1.07)

−12.94(0.78)

10.98(0.81)

048-Cerealpreps&

prepsof

flourof

fr(0.026)

−15.28(4.51)

−0.27(0.80)

−0.21(0.86)

4.43(6.80)

0.10(0.15)

051–

Fruit,

fresh,

andnuts-excl.oil(0.027)

−15.86(4.56)

0.37(2.36)

−0.18(0.74)

5.30(6.49)

−1.48(2.63)

052-Dried

fruitincludingartificially

(0.013)

−16.83(3.96)

1.56(5.83)

0.01(0.03)

6.83(8.48)

−3.39(6.22)

053-

Fruit,preservedandfruitpreparati(0.196)

−27.11(11.65)

0.31(2.18)

0.13(0.73)

8.37(18.08)

−1.22(4.37)

054-Vegetables,roots&

tubers,fresho(0.059)

−25.86(2.26)

1.11(1.70)

−1.47(1.53)

6.34(2.56)

0.56(0.36)

055-Vegetables,roots&

tubers

pres

or(0.066)

9.51(1.80)

0.41(2.19)

0.78(1.59)

0.32(0.32)

−0.20(0.37)

061-Sugar

andhoney(0.012)

−0.15(0.06)

0.00(0.01)

0.07(0.42)

1.01(1.54)

0.63(1.23)

062-Sugar

confy,

sugarpreps.ex

chocol

(0.036)

−37.94(4.39)

−0.03(0.07)

−0.39(0.66)

10.59(5.16)

−2.45(1.96)

071-Coffee(0.001)

35.74(0.20)

−16.02(0.51)

0.60(0.07)

−15.81(0.29)

10.24(0.33)

073-Chocolate

&otherfood

preptnscont

(0.003)

−153.35(0.98)

4.69(1.10)

−4.99(0.67)

39.88(1.02)

−18.15(0.89)

074-Tea

andmate(0.017)

0.13(0.05)

0.65(4.53)

−0.29(1.48)

1.34(2.51)

−0.26(0.75)

075-Spices(0.018)

−8.34(4.32)

0.60(4.03)

0.25(1.60)

4.08(10.14)

−1.43(5.17)

099-

Foodpreparations,nes

(0.040)

−34.98(1.01)

−1.73(0.57)

−2.04(0.55)

6.52(1.76)

2.61(0.45)

1 11-Non-alcoholic

beverages,nes(0.004)

−36.86(5.12)

0.22(0.62)

−0.44(0.78)

9.66(6.50)

−2.54(2.58)

112-Alcoholic

beverages(0.005)

−31.09(1.93)

0.61(1.62)

−2.94(2.18)

5.97(1.94)

−0.73(0.39)

121-Tobacco,unmanufactured(0.002)

−28.89(1.25)

−1.24(1.61)

−2.64(1.34)

5.69(1.18)

−0.97(0.35)

122-Tobacco

manufactures(0.003)

−87.32(5.80)

−0.41(0.64)

−0.76(0.64)

23.73(7.46)

−9.89(5.10)

212-Fur

skins,undressed(0.000)

29.89(4.24)

1.30(2.16)

0.58(1.13)

−5.67(3.16)

−0.34(0.22)

564 J Econ Finan (2012) 36:555–586

Industry

(trade

share%)

Long-Run

Coefficient

Estim

ates

Constant

LnV

CH

LnV

CAN

LnY

US

LnR

E

221-Oil-seeds,oilnutsandoilkernels(0.011)

−11.03(4.18)

1.87(10.17)

0.43(2.34)

6.84(12.82)

−5.42(14.99)

261-Silk

(0.000)

26.96(15.27)

0.26(3.33)

−1.21(9.41)

−7.08(18.76)

1.62(7.55)

262-

Woolandotheranim

alhair(0.004)

2.40(0.95)

−0.56(3.58)

0.23(1.16)

0.68(1.14)

−0.77(1.82)

265-Vegetable

fibres,exceptcotto

nand(0.000)

−10.76(0.66)

0.90(1.08)

1.74(1.00)

7.79(2.55)

−8.19(4.10)

276–

Other

crudeminerals(0.125)

12.57(1.27)

−0.16(1.22)

1.31(1.89)

−0.23(0.12)

0.50(0.58)

283-

Ores&

concentrates

ofnon-ferrous(0.014)

143.99(0.43)

2.64(0.47)

13.94(0.41)

−24.85(0.41)

12.12(0.39)

291-Crude

anim

almaterials,nes

(0.095)

−5.09(1.20)

0.18(0.62)

0.46(1.21)

3.12(3.49)

−0.17(0.22)

292-Crude

vegetablematerials,nes

(0.077)

−8.42(0.74)

0.65(0.81)

−1.28(1.10)

3.05(1.24)

−0.41(0.28)

332-

Petroleum

products(0.102)

−27.60(5.21)

−0.02(0.04)

0.12(0.35)

11.49(10.24)

−9.07(11.27)

422-Other

fixedvegetableoils(0.003)

−19.02(2.16)

0.69(1.35)

−0.52(0.80)

5.98(2.94)

−2.80(2.12)

512-Organic

chem

icals(0.685)

−20.26(2.00)

0.81(0.84)

−0.47(0.43)

6.96(2.86)

−0.66(0.57)

513-Inorg.chem

icals-elem

s.,oxides,halog(0.156)

−8.30(1.56)

−0.10(0.66)

0.38(0.88)

3.54(3.28)

0.52(0.94)

514-Other

inorganicchem

icals(0.151)

−9.03(2.10)

−0.25(1.57)

0.61(1.70)

3.97(4.11)

0.01(0.01)

533-Pigments,paints,varnishes&

relat(0.046)

−45.86(6.77)

0.23(1.12)

−1.78(2.68)

9.22(6.45)

1.99(2.27)

541-Medicinal

&pharmaceutical

products(0.243)

−14.34(1.79)

−0.10(0.47)

−0.31(0.47)

4.65(2.86)

0.16(0.20)

551-Essentialoils,perfum

eandflavour(0.015)

2.58(2.16)

0.01(0.08)

0.16(1.76)

0.71(2.73)

0.19(1.02)

553-Perfumery,

cosm

etics,dentifrices,(0.132)

−36.86(11.03)

−1.08(3.84)

−0.74(2.74)

8.69(11.92)

0.66(1.54)

554-Soaps,cleansing

&polishing

prepara(0.047)

−22.92(14.02)

0.97(10.75)

0.69(5.04)

7.98(22.64)

−1.79(7.63)

571-

Explosivesandpyrotechnicproducts(0.089)

−47.81(0.41)

1.27(0.42)

−3.30(0.38)

12.77(0.48)

−5.88(0.39)

599-Chemical

materialsandproducts,nes

(0.193)

−27.52(4.88)

0.87(3.27)

−0.62(1.10)

8.99(7.50)

−4.15(4.42)

611-Leather

(0.016)

−3.49(0.75)

2.61(5.12)

0.40(1.09)

2.85(2.45)

0.16(0.16)

612-Manuf.ofleatheror

ofartif.orrec(0.151)

−22.27(3.75)

0.02(0.09)

−0.31(0.77)

4.88(3.58)

3.20(3.70)

613-Fur

skins,tanned

ordressed,

inclu(0.001)

−20.25(6.03)

−0.41(2.34)

0.46(2.16)

6.28(7.12)

−2.35(3.52)

631-Veneers,plywoodboards

&otherwood(0.382)

−52.72(3.92)

1.20(1.65)

0.58(0.51)

15.25(5.50)

−3.09(2.04)

632-Woodmanufactures,nes(0.535)

−25.93(6.98)

−0.33(1.45)

−0.26(1.00)

6.72(7.83)

1.27(2.20)

633-Corkmanufactures(0.007)

−49.24(2.52)

1.37(1.91)

−0.36(0.62)

14.50(3.00)

−6.15(2.82)

641-Paper

andpaperboard

(0.202)

−127.95(1.02)

0.03(0.01)

−3.01(0.61)

31.62(1.18)

−9.91(1.23)

642-Articlesof

paper,pulp,paperboard

(0.506)

−16.41(3.58)

−0.24(1.29)

0.31(1.38)

4.28(3.92)

3.20(5.15)

J Econ Finan (2012) 36:555–586 565

Tab

le2

(con

tinued)

Industry

(trade

share%)

Long-Run

Coefficient

Estim

ates

Constant

LnV

CH

LnV

CAN

LnY

US

LnR

E

651-Textileyarn

andthread

(0.079)

−0.90(0.10)

1.94(2.49)

1.53(1.51)

3.64(2.43)

−0.99(0.67)

652-Cottonfabrics,woven

ex.narrow

ors(0.084)

−6.52(0.46)

0.06(0.51)

−0.93(0.90)

2.63(0.86)

−0.65(0.36)

653-Textfabricswoven

exnarrow

,spec,(0.202)

−12.95(8.41)

0.84(5.86)

−0.35(2.65)

5.35(13.61)

−1.84(3.76)

654-Tulle,lace,em

broidery,ribbons,t(0.056)

−18.84(4.77)

−0.32(1.23)

−0.12(0.49)

3.10(3.19)

5.52(8.28)

655-Special

textile

fabricsandrelated(0.123)

−14.23(4.55)

0.48(3.05)

0.39(1.55)

5.59(8.88)

−1.16(2.92)

656-Made-up

articles,wholly

orchiefly(1.583)

−1.43(0.28)

0.60(4.33)

1.11(2.07)

4.07(8.59)

−0.93(1.35)

657-Floor

coverings,tapestries,etc.

(0.129)

−0.29(0.49)

0.10(3.33)

0.02(0.39)

1.71(12.72)

0.24(2.85)

661-Lim

e,cement&

fabr.bldg.mat.-ex

gla(0.433)

−19.71(1.91)

0.24(0.47)

1.12(1.54)

7.36(4.34)

−0.91(1.03)

663-Mineral

manufactures,nes(0.282)

−25.36(1.40)

−3.93(2.71)

1.06(0.91)

4.22(1.13)

6.40(2.75)

664-Glass

(0.233)

−29.58(5.68)

−0.39(1.81)

−0.28(0.69)

6.21(5.48)

3.71(5.45)

665-Glassware(0.190)

−12.53(1.96)

−0.57(1.60)

1.20(2.04)

4.59(3.44)

1.29(1.44)

666-Pottery

(0.416)

5.93(0.56)

−0.47(1.42)

0.46(0.72)

−0.36(0.16)

3.23(2.74)

667-Pearlsandprecious

andsemi-precio

(0.069)

74.76(0.72)

−1.58(0.92)

11.87(1.06)

−6.08(0.39)

−1.68(0.71)

687-Tin

(0.016)

6.86(2.48)

−0.28(2.38)

0.29(1.37)

−0.09(0.13)

−0.06(0.13)

689-Miscell.non-ferrou

sbase

metals(0.094)

86.04(0.54)

3.82(0.52)

8.09(0.58)

−16.87(0.48)

14.98(0.54)

692-

Metal

containers

forstorageandtr(0.041)

−30.87(2.95)

−0.57(1.04)

−0.50(0.55)

6.04(2.89)

3.48(1.74)

694-Nails,screw

s,nuts,bolts,rivetsand(0.429)

1.30(0.05)

−0.36(0.39)

4.33(0.91)

8.88(1.33)

−8.33(1.01)

695-Toolsforusein

thehand

orin

mac

(0.410)

−14.35(2.92)

−0.02(0.11)

0.04(0.12)

4.72(5.97)

0.90(1.16)

696-Cutlery

(0.289)

−25.52(2.21)

−0.42(1.16)

−0.88(0.96)

6.22(2.77)

1.32(1.14)

697-Household

equipm

entof

base

metals(1.261)

−23.94(4.83)

−0.58(2.70)

0.31(0.77)

6.54(5.89)

2.02(2.83)

698-Manufacturesof

metal,nes(1.563)

−13.39(2.38)

−0.03(0.24)

0.52(1.74)

4.84(5.81)

1.72(3.31)

711-Pow

ergeneratin

gmachinery,othert(0.230)

−24.04(27.08)

0.41(5.84)

0.11(2.18)

6.97(40.41)

0.28(1.38)

714-Officemachines(16.187)

−60.22(2.59)

−0.45(0.49)

−3.22(1.36)

12.19(2.48)

3.72(1.35)

566 J Econ Finan (2012) 36:555–586

()

Industry

(trade

share%)

Long-Run

Coefficient

Estim

ates

Constant

LnV

CH

LnV

CAN

LnY

US

LnR

E

715-Metalworking

machinery

(0.068)

1.18(0.06)

0.73(0.82)

0.34(0.29)

2.19(0.64)

−0.75(0.41)

717-Textileandleathermachinery

(0.076)

−3.43(0.15)

1.88(0.93)

0.49(0.41)

1.07(0.30)

5.32(2.18)

719-Machinery

andappliances-non

electr(3.114)

−25.75(9.38)

−0.23(1.94)

0.10(0.48)

7.20(13.95)

1.52(4.12)

722-Electricpower

machinery

andsw

itch(2.593)

−18.91(2.65)

−0.55(1.67)

0.41(1.16)

4.89(2.96)

4.11(4.11)

724-

Telecom

munications

apparatus(10.675)

10.42(0.31)

0.93(0.81)

1.28(0.73)

2.10(0.45)

−0.58(0.14)

725-Dom

estic

electrical

equipm

ent(2.442)

−15.76(2.23)

0.62(1.04)

0.25(0.65)

3.62(2.62)

5.27(4.26)

726-Elec.apparatusformedic.purp.,radi(0.074)

−41.65(10.40)

−0.70(2.28)

−0.14(0.49)

9.12(10.88)

2.44(4.13)

729-Other

electrical

machinery

andappa

(2.622)

−26.44(5.54)

−0.41(1.79)

0.42(1.43)

6.03(5.81)

4.86(7.09)

812-Sanitary,plumbing,heatin

g&

lightin

(1.685)

−17.82(2.95)

−1.51(5.03)

1.44(2.85)

4.37(3.36)

5.51(7.73)

821-Furniture

(5.752)

−145.67(0.07)

−20.17(0.05)

−22.14(0.05)

14.07(0.14)

14.11(0.05)

831-Travelgoods,handbags

andsimilar(1.846)

−4.18(1.56)

0.48(4.07)

−0.22(1.25)

3.01(6.70)

0.62(1.36)

841-Clothingexcept

furclothing

(7.768)

−10.20(2.58)

0.83(2.94)

−0.81(2.33)

4.91(4.68)

−0.92(1.02)

842-Fur

clothing

andarticlesof

artifi(0.045)

−1.13(0.20)

−0.00(0.01)

1.10(2.52)

2.20(2.08)

1.02(2.35)

851-Footwear(4.730)

−9.35(2.98)

−0.18(0.76)

0.11(0.73)

2.97(3.79)

3.62(6.73)

861-Scientific,m

edical,optical,m

eas./co(1.403)

5.74(0.43)

−1.45(3.57)

2.32(2.21)

−0.70(0.25)

7.04(5.38)

862-Photographicandcinematographic

su(0.027)

15.97(0.88)

−0.50(1.48)

4.52(3.24)

0.24(0.07)

2.42(1.48)

864-Watches

andclocks

(0.233)

−15.70(3.36)

−0.94(4.11)

−0.54(1.81)

2.17(2.30)

5.47(12.35)

891-Musical

instruments,sound

recorders(3.980)

−22.47(8.03)

−0.15(1.31)

0.18(1.42)

5.57(8.61)

4.22(10.26)

892-Printed

matter(0.527)

−36.47(16.15)

−0.48(3.12)

−0.10(0.77)

8.50(13.39)

2.63(4.77)

893-Articlesof

artificialplastic

mate(2.343)

−19.65(2.91)

−0.55(2.31)

−0.73(2.18)

3.94(3.47)

4.45(7.60)

894-Peram

bulators,to

ys,gam

esandsporti(7.493)

−20.35(5.37)

0.01(0.07)

−1.10(4.05)

4.45(5.93)

3.78(6.50)

895-Officeandstationery

supplies,nes(0.271)

−44.35(3.57)

0.99(1.60)

−3.71(2.48)

8.57(3.33)

1.32(0.78)

896-Works

ofart,collectorspieces

and(0.092)

1.58(0.22)

0.01(0.04)

1.21(2.00)

2.72(1.90)

−1.59(2.04)

897-Jewellery

andgold/silv

er-smith

swa(0.785)

−24.24(11.63)

−0.47(3.32)

0.04(0.30)

6.40(14.67)

1.95(6.41)

899-Manufacturedarticles,nes(1.099)

4.88(0.67)

−0.75(2.89)

0.36(1.24)

0.23(0.14)

2.31(3.84)

941-Animals,nes-incl.zoo

anim

als,dogs

(0.010)

102.91(0.78)

−1.96(0.67)

12.47(0.97)

−14.61(0.66)

5.71(0.84)

951-Firearm

sof

war

andam

munition

ther

(0.013)

−71.43(1.73)

3.61(1.86)

−4.72(1.48)

17.35(1.67)

−6.52(0.86)

J Econ Finan (2012) 36:555–586 567

Tab

le3

Diagnostic

statisticsfortheU.S.Im

portdemandmodel

(3)

Industry

Diagnostics

FECM

t−1

LM

RESE

TCUSU

MCUSU

MSQ

Adj.R2

011-Meat,fresh,

chilled

orfrozen

8.94

−0.95(7.87)

15.87

0.80

SS

0.87

025-

Eggs

7.27

−1.01(7.24)

0.24

3.27

SS

0.73

031-

Fish,fresh&

simplypreserved

1.39

−0.34(3.08)

0.50

0.34

SS

0.72

032-

Fish,in

airtight

containers,nes

&f

9.98

−0.26(8.28)

0.61

0.09

SS

0.84

047-Meal&

flourof

cereals,except

whea

4.10

−0.38(5.29)

3.77

0.67

SS

0.67

048-Cerealpreps&

prepsof

flou

rof

fr1.64

−0.26(3.25)

0.96

0.80

SS

0.59

051–Fruit,

fresh,

andnu

ts-excl.oil

8.08

−0.82(7.64)

2.76

0.06

SS

0.90

052-Dried

fruitincludingartificially

2.54

−1.20(4.47)

5.20

11.99

SS

0.81

053-

Fruit,preservedandfruitpreparati

4.14

−0.95(5.46)

0.03

0.05

SS

0.80

054-Vegetables,roots&

tubers,fresho

3.55

−0.46(5.06)

5.34

1.51

SU

0.49

055-Vegetables,roots&

tubers

pres

or5.60

−0.57(6.18)

0.02

0.14

SS

0.74

061-Sug

arandho

ney

11.12

−1.03(7.80)

3.59

5.59

SS

0.68

062-Sug

arconfy,

sugarpreps.ex

chocol

4.29

−0.34(5.67)

0.04

6.77

SS

0.85

071-Coffee

2.11

−0.25(4.07)

0.42

0.11

SS

0.75

073-Cho

colate

&otherfood

preptnscont

3.95

−0.20(5.26)

0.00

0.58

SS

0.80

074-Teaandmate

5.01

−0.79(5.84)

3.70

1.04

SS

0.70

075-Spices

5.55

−0.81(6.45)

10.00

0.01

SS

0.90

099-

Foodpreparations,nes

2.61

−0.08(4.34)

6.99

0.85

SS

0.74

111-Non-alcoholic

beverages,nes

3.31

−0.70(4.75)

1.30

0.66

SS

0.79

112-Alcoholic

beverages

4.78

−0.19(5.99)

1.53

0.48

SS

0.93

121-To

bacco,

unmanufactured

6.08

−0.64(6.31)

0.25

0.14

SS

0.71

122-To

baccomanufactures

17.35

−1.08(10.86)

1.64

1.13

SS

0.91

568 J Econ Finan (2012) 36:555–586

Tab

le3

(contin

ued)

Industry

Diagnostics

FECM

t−1

LM

RESE

TCUSU

MCUSU

MSQ

Adj.R2

212-Fur

skins,un

dressed

3.40

−0.98(4.53)

1.27

.8658E

-4S

S0.57

221-Oil-seeds,oilnutsandoilkernels

62.33

−1.67(20.89)

0.13

0.84

SS

0.97

261-Silk

20.40

−1.59(11.79)

3.67

0.70

SS

0.90

262-

Woo

landotheranim

alhair

5.23

−0.81(5.52)

1.03

0.30

SS

0.57

265-Vegetable

fibres,exceptcotto

nand

2.19

−0.64(3.73)

1.55

3.02

SU

0.79

276–Other

crudeminerals

7.28

−0.44(7.08)

3.19

0.30

SS

0.80

283-

Ores&

concentrates

ofno

n-ferrou

s5.61

−0.07(6.27)

1.81

0.06

SS

0.83

291-Crude

anim

almaterials,nes

2.48

−0.34(4.17)

2.37

1.41

SS

0.78

292-Crude

vegetablematerials,nes

3.96

−0.26(5.27)

2.89

1.26

SS

0.68

332-

Petroleum

prod

ucts

9.62

−0.68(8.50)

0.50

1.15

SS

0.88

422-Other

fixedvegetableoils

2.73

−0.82(4.43)

0.87

6.25

SS

0.76

512-Organic

chem

icals

2.03

−0.15(3.90)

11.26

5.99

SS

0.81

513-Inorg.chem

icals-elem

s.,oxides,halog

3.96

−0.69(5.20)

3.13

0.06

SS

0.80

514-Other

inorganicchem

icals

5.06

−0.72(6.05)

11.58

3.83

SS

0.81

533-Pigments,paints,varnishes&

relat

3.46

−1.46(5.37)

0.07

4.85

SS

0.77

541-Medicinal

&ph

armaceutical

products

1.04

−0.26(2.53)

9.80

3.11

SS

0.42

551-Essentialoils,perfum

eandflavou

r9.42

−1.18(7.03)

0.09

2.06

SS

0.71

553-Perfumery,

cosm

etics,dentifrices,

22.62

−0.60(13.73)

0.77

0.23

SS

0.97

554-Soaps,cleansing

&polishing

prepara

15.86

−1.23(10.70)

2.30

7.26

SS

0.88

571-

Exp

losivesandpy

rotechnicprod

ucts

5.78

−0.12(6.46)

1.57

0.03

SS

0.82

599-Chemical

materialsandprod

ucts,nes

6.33

0.52

(7.05)

5.40

0.81

SS

0.91

611-Leather

1.88

−1.01(3.38)

2.49

0.01

SS

0.35

612-Manuf.ofleatheror

ofartif.orrec

3.88

−0.43(5.02)

5.97

1.37

SS

0.60

613-Fur

skins,tanned

ordressed,

inclu

8.94

−0.70(6.88)

0.10

0.50

SS

0.62

631-Veneers,plywoodboards

&otherwood

1.31

−0.67(3.07)

6.74

4.46

SU

0.64

632-Woodmanufactures,nes

8.43

−0.25(7.95)

8.52

11.45

SS

0.90

633-Corkmanufactures

4.24

−0.27(5.25)

7.11

0.42

SS

0.46

J Econ Finan (2012) 36:555–586 569

Tab

le3

(contin

ued)

Industry

Diagnostics

FECM

t−1

LM

RESE

TCUSU

MCUSU

MSQ

Adj.R2

641-Paper

andpaperboard

2.71

−0.14(4.21)

0.94

7.52

SS

0.60

642-Articlesof

paper,pulp,paperboard

2.52

−0.37(4.10)

4.02

0.29

SS

0.78

651-Textile

yarn

andthread

3.46

−0.50(5.00)

4.10

6.26

SS

0.69

652-Cottonfabrics,woven

ex.narrow

ors

3.91

−0.57(5.12)

2.80

4.10

SS

0.75

653-Text

fabricswov

enex

narrow

,spec,

37.16

−0.93(17.60)

10.19

2.26

SS

0.96

654-Tulle,lace,em

broidery,ribbon

s,t

4.74

−0.82(5.64)

0.22

0.41

SS

0.69

655-Special

textile

fabricsandrelated

9.00

−1.02(8.21)

2.45

1.97

SS

0.89

656-Made-up

articles,wholly

orchiefly

8.70

−0.48(8.08)

6.87

0.03

SS

0.90

657-Floor

coverings,tapestries,etc.

28.14

−1.24(13.44)

0.12

0.5766

E-3

SS

0.90

661-Lim

e,cement&

fabr.bldg.mat.-ex

gla

3.96

−0.50(5.16)

5.64

10.46

SS

0.67

663-Mineral

manufactures,nes

1.79

0.36(3.75)

0.65

0.06

SS

0.75

664-Glass

5.24

−0.58(5.90)

1.19

4.66

SS

0.77

665-Glassware

4.26

−0.42(5.65)

1.18

1.89

SS

0.85

666-Pottery

5.60

−0.13(6.36)

13.13

0.10

SS

0.92

667-Pearlsandprecious

andsemi-precio

15.83

0.14(11.49)

4.70

0.11

SS

0.94

687-Tin

8.18

−0.77(6.84)

2.00

4.42

SS

0.67

689-Miscell.non-ferrousbase

metals

10.93

−0.08(9.06)

1.98

0.47

SS

0.92

692-

Metal

containers

forstorageandtr

5.77

−0.25(6.44)

7.37

0.72

SS

0.74

694-Nails,screw

s,nuts,bolts,rivetsand

4.74

−0.14(5.54)

1.21

0.54

SS

0.55

695-To

olsforusein

thehand

orin

mac

4.06

−0.34(5.41)

0.05

0.08

SS

0.95

696-Cutlery

3.43

−0.28(5.07)

12.01

1.07

SS

0.72

697-Hou

seho

ldequipm

entof

base

metals

8.75

−0.35(7.95)

11.69

6.43

SS

0.84

570 J Econ Finan (2012) 36:555–586

Indu

stry

Diagn

ostics

FECM

t−1

LM

RESE

TCUSU

MCUSU

MSQ

Adj.R2

698-Manufacturesof

metal,nes

5.29

−0.35(6.18

)12

.37

2.42

SS

0.89

711-Pow

ergeneratin

gmachinery,othert

23.33

−1.16(13

.17)

0.18

1.39

SS

0.95

714-Officemachines

3.88

−0.36(5.21

)7.05

14.60

SS

0.74

715-Metalworking

machinery

3.13

−0.26(4.85

)0.03

0.00

SS

0.79

717-Textile

andleathermachinery

3.50

−0.35(4.95

)0.21

3.82

SS

0.73

719-Machinery

andappliances-non

electr

58.13

−0.87(21

.37)

1.67

0.31

SS

0.98

722-Electricpo

wer

machinery

andsw

itch

4.79

−0.61(5.50

)0.64

0.55

SS

0.60

724-

Telecommun

ications

apparatus

6.27

−0.22(6.51

)3.50

6.71

SU

0.75

725-Dom

estic

electrical

equipm

ent

6.12

−0.23(6.19

)0.27

14.76

SS

0.90

726-Elec.apparatusformedic.purp.,radi

7.03

−0.83(6.92

)0.04

0.00

SS

0.88

729-Other

electrical

machinery

andappa

5.97

−0.39(6.35

)3.08

1.06

SS

0.84

812-Sanitary,plumbing,heatin

g&

lightin

10.17

−0.39(8.73

)5.90

2.74

SS

0.89

821-Furniture

2.60

−0.00(4.20

)10

.78

6.93

SS

0.78

831-Travelgoods,handbags

andsimilar

35.75

−0.40(16

.02)

0.98

2.94

SS

0.99

841-Clothingexcept

furclothing

12.13

−0.44(9.21

)0.93

6.82

SS

0.82

842-Fur

clothing

andarticlesof

artifi

4.59

−1.13(5.74

)3.44

2.18

SS

0.59

851-Footwear

13.97

−0.22(10

.04)

3.26

4.73

SS

0.96

861-Scientific,m

edical,optical,m

eas./co

10.15

−0.40(8.73

)0.64

14.51

SS

0.86

862-Photographicandcinematographic

su9.96

−0.72(8.33

)2.36

7.26

SS

0.81

864-Watches

andclocks

5.39

−0.86(6.36

)0.01

5.26

SS

0.82

891-Musical

instruments,sound

recorders

8.36

−0.61(7.41

)1.98

9.59

SS

0.81

892-Printed

matter

11.84

−0.45(8.86

)7.86

0.11

SS

0.87

893-Articlesof

artificialplastic

mate

5.56

−0.54(6.61

)0.86

10.15

SS

0.91

894-Peram

bulators,to

ys,gam

esandsporti

11.82

−0.66(9.24

)0.13

8.57

SS

0.93

895-Officeandstationery

supplies,nes

6.84

−0.25(6.87

)3.92

8.50

SS

0.71

896-Works

ofart,collectorspieces

and

5.09

−0.75(6.32

)0.64

5.56

SS

0.86

897-Jewellery

andgold/silv

er-smith

swa

19.14

−0.54(11.76)

3.92

0.68

SS

0.92

J Econ Finan (2012) 36:555–586 571

Tab

le3

(contin

ued)

Industry

Diagnostics

FECM

t−1

LM

RESE

TCUSU

MCUSU

MSQ

Adj.R2

899-Manufacturedarticles,nes

10.05

−0.30(8.17)

0.59

4.34

SS

0.79

941-Animals,nes-incl.zoo

anim

als,do

gs5.89

−0.31(6.65)

1.99

0.42

SS

0.84

951-Firearm

sof

war

andam

mun

ition

ther

3.96

−0.23(5.19)

3.42

2.10

SS

0.73

Atthe

10%

levelo

fsignificance

theupperboundcriticalv

alue

ofthebounds

testwhentherearefour

regressorsin

thelong-run

equatio

nis3.52.Itcom

esfrom

TableCI(iii)Case

III(Pesaran

etal.20

01,p.

300).

Num

bers

inside

parenthesesareabsolute

valueof

thet-ratio

s.

LM

=Lagrangemultip

liertestof

residual

serial

correlation.

Itisdistributedas

χ2(1).The

criticalvalueis3.84.

RESET=Ram

sey’stestforfunctio

nform

.Itisdistributedas

χ2(1).The

criticalvalueis3.84.

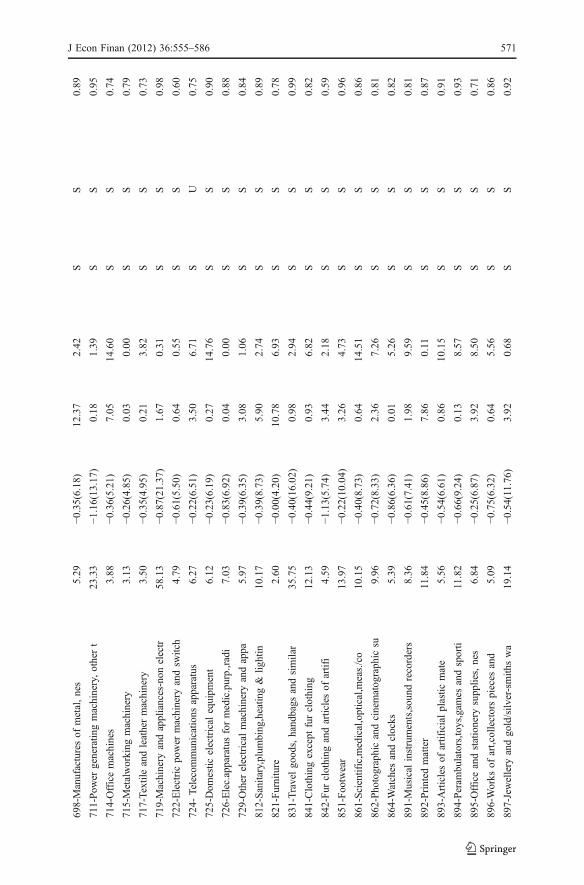

572 J Econ Finan (2012) 36:555–586

(clothing except fur clothing) and 894 (Perambulators, toys, games,…), each littleover 7% market share. Furthermore, introducing the third country effect does notseem to change the results of Bahmani-Oskooee and Wang (2007) when theyexcluded the third-country effect from their model.5

In order for the long-run results and our analysis to be meaningful, we mustestablish cointegration among the variables. To this end, we move to Table 3 whichnot only reports the results of the F test, but also additional diagnostic statistics foreach optimum model. The F test results clearly reveal that at the 10% level ofsignificance, the calculated statistic is greater than its critical value of 3.52 in 79industries supporint cointegration and validating our long-run analysis. Furthermore,following Pesaran et al. (2001) the long-run coefficient estimates from Table 2 areused to form an error-correction term, say, ECM. Then in each model, the linearcombination of the lagged level variables is replaced by ECMt−1 and the model isestimated one more time by impositing the optimum number of lags. A significantlynegative coefficient obtained for ECMt−1 in every industry reflects the fact that theshort-run adjustment is toward long-run equilibrium.6 For each model, we alsoreport the Lagrange Multiplier (LM) statistic for serial correlation and Ramsey’sRESET statistic for functional misspecification. Both are distributed as χ2 with onedegree of freedom. As can be seen, in 70% of the models both statistics are less thantheir critical value of 3.84, indicationg auto-correlation free residuals in the majorityof the correctly specified models. Correct specification of each model is furthersupported by the size of adjusted R2 in almost all the models.7 Finally, once the well-known CUSUM and CUSUMSQ tests are applied to the residuals of each optimummodel, Table 3 reveals that all short-run as well as long-run coefficient estimates arestable as reflected by “S” for stable coefficients and “U” for unstable models.

We now shift to estimates of error-correction model (4) for each of the U.S.exporting industries. Here, countinous data over the period 1978–2006 were onlyavailable for 75 industries which all together have 77% of the market share.8 Onceagain model (4) is estimated using the same procedure as model (3) and the resultsfrom each optimum model are reported in Tables 4, 5 and 6.

Consider first the short-run coefficient estimates of the two volatility measuresreported in Table 4. At the 10% level of significance, the volatility of the real U.S.dollar-yuan exchange rate has significant impact on the U.S. exports to China of 66industries. At the same significance level the third-country effect is present in almostthe same number of industries (63 of the 75 industries). Unlike Cushman (1986) who

5 From the long-run coefficient estimates we also conclude that the U.S. income carries its expectedpositive sign in majority of the models, impying that economic growth in the U.S. is major determinant ofU.S. imports from China. The real U.S. dollar-Chinese yuan rate also carries a significant coefficient in 51cases. Furtheremore, the coefficient is expectedly positive in 31 industries and negative in 20 industries.6 Note that there are three industries coded 599, 663, and 667 in which ECMt−1 carries a positivecoefficient, implying adjustment away from equilibrium. Business cycles and shocks to exchange rate thatiduces severe volatility could cause trade flows of these industries not to adjust.7 Note that in 20 out of 29 models that are misspecified (due to significant RESET statistic), the third-country effect is insignificant, leaving our long-run analysis almost unchanged.8 Once again for each industry, its market share is defined as that industry’s export as a % of total U.S.exports to China. These shares are reported inside the parenthesis next to the name of each industry inTable 5. Sum of all these shares add up to 77.25, implying that about 23% of the U.S. exports to China areby other industries for which data were not available.

J Econ Finan (2012) 36:555–586 573

Tab

le4

Short-run

coefficientestim

ates

ofexportdemand(t-ratiosinside

parentheses)

Industry

Short-run

coefficientestim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

001-Liveanim

als

−0.34(1.76)

−1.20(4.34)

−0.48(2.35)

0.82(3.33)

−0.58(2.23)

–

041-Wheat

-includingspelt-andmesli

1.22(3.99)

1.19(3.45)

–−0

.11(0.31)

−2.41(6.46)

−2.00(7.72)

051–Fruit,

fresh,

andnuts-excl.oil

−0.13(0.66)

––

1.05(5.05)

––

211-Hides

&skins,-exc.fur

skins-

undre

0.17(1.25)

0.85(6.33)

–−0

.42(2.83)

−0.56(3.96)

−0.46(3.50)

231-Crude

rubber-incl.synthetic

&recla

0.30(4.67)

––

−0.24(3.15)

−0.21(2.79)

–

251-Pulp&

waste

paper

−0.36(6.84)

−0.25(4.11)

−0.27(4.80)

0.25(3.63)

−0.97(6.90)

−0.36(4.02)

263-Cotton

1.14(2.11)

1.58(2.89)

–−0

.34(0.48)

−4.86(4.90)

−2.09(2.57)

266-Synthetic

andregenerated-artificia

0.19(2.61)

––

0.07(0.64)

−0.64(5.73)

−0.40(4.11)

291-Crude

anim

almaterials,nes

−0.19(3.37)

−0.69(7.39)

−0.39(4.68)

0.16(2.61)

−0.01(0.09)

0.13(2.22)

292-Crude

vegetablematerials,nes

0.11(1.10)

−0.16(1.65)

−0.64(5.75)

−0.27(2.26)

––

332-

Petroleum

products

0.21(1.28)

−1.56(9.35)

−1.16(8.38)

−0.27(1.29)

1.41(6.79)

0.79(4.89)

512-Organic

chem

icals

0.37(5.02)

−0.24(1.78)

−0.44(4.56)

0.03(0.36)

−0.18(2.19)

–

513-Inorg.chem

icals-elem

s.,oxides,halog

0.91(5.59)

−1.39(5.23)

−1.26(6.13)

−0.41(2.79)

––

514-Other

inorganicchem

icals

0.08(1.29)

−0.77(5.91)

−0.73(6.84)

0.20(1.97)

−0.65(6.95)

–

515-Radioactiv

eandassociated

material

0.09(0.63)

––

0.18(0.97)

––

531-Synth.organic

dyestuffs,naturalin

0.49(3.52)

––

−0.04(0.25)

––

533-Pigments,paints,varnishes&

relat

0.44(4.82)

0.49(3.88)

0.18(1.89)

−0.24(2.13)

––

541-Medicinal

&pharmaceutical

products

−0.32(5.30)

−0.47(4.26)

−0.16(2.16)

0.45(5.36)

––

551-Essentialoils,perfum

eandflavour

0.31(1.40)

––

−0.08(0.29)

––

554-Soaps,cleansing

&polishing

prepara

0.36(3.15)

––

0.11(0.70)

––

581-

Plastic

materials,regenerd.cellu

los

0.24(2.91)

−0.79(4.81)

−0.42(3.67)

0.45(3.54)

−0.57(4.90)

−0.30(3.09)

599-Chemical

materialsandproducts,nes

0.04(3.23)

−0.17(11.85)

−0.03(2.27)

0.18(11.55)

−0.39(14.21)

−0.17(9.35)

611-Leather

−0.07(1.35)

−0.50(5.57)

−0.36(4.87)

0.40(6.08)

––

574 J Econ Finan (2012) 36:555–586

Industry

Short-run

coefficientestim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

629-Articlesof

rubber,nes

0.48(6.02)

––

−0.09(0.90)

−0.42(3.86)

−0.32(3.12)

641-Paper

andpaperboard

−0.17(4.95)

−0.17(4.96)

−0.18(5.92)

0.27(6.51)

−0.19(4.13)

0.08(2.42)

642-Articlesof

paper,pulp,paperboard

−0.29(2.43)

––

−0.10(0.84)

0.22(1.80)

0.42(3.85)

651-Textileyarn

andthread

0.42(3.06)

−0.47(2.82)

–0.37(2.27)

––

652-Cottonfabrics,woven

ex.narrow

ors

0.37(2.50)

––

0.63(3.26)

−0.38(2.24)

–

653-Textfabricswoven

exnarrow

,spec,

−0.00(0.03)

−1.90(9.10)

−1.25(8.28)

0.80(4.36)

−1.35(7.07)

−0.64(4.53)

654-Tulle,lace,em

broidery,ribbons,t

0.10(0.11)

−0.25(2.25)

−0.56(5.51)

0.27(2.42)

−0.27(2.24)

–

655-Special

textile

fabricsandrelated

0.25(1.32)

––

−0.08(0.33)

––

656-Made-up

articles,wholly

orchiefly

−0.06(0.52)

0.38(2.77)

0.46(3.62)

0.49(3.27)

0.62(3.06)

0.45(2.71)

661-Lim

e,cement&

fabr.bldg.mat.-ex

gla

−0.80(3.30)

––

0.40(1.21)

––

662-Clayandrefractory

constructio

nma

1.85(5.75)

0.42(2.33)

–−1

.31(5.04)

2.14(5.36)

0.88(3.41)

663-Mineral

manufactures,nes

0.33(6.28)

−0.16(1.97)

−0.32(5.07)

−0.25(3.37)

−0.12(1.63)

–

673-Iron

andsteelbars,rods,angles,sha

−0.13(1.12)

0.49(3.49)

1.06(8.34)

−0.22(1.66)

0.77(5.13)

1.21(9.07)

674-Universals,plates

andsheetsof

iro

0.82(2.28)

−2.46(3.91)

−1.57(3.68)

0.78(2.30)

−1.61(3.31)

−0.56(1.46)

678-Tubes,pipes

andfittingsof

iron

or1.16(11.19)

0.01(0.10)

−0.47(4.60)

−0.63(5.57)

0.22(1.76)

–

682-Copper

0.71(2.89)

1.33(4.32)

0.73(2.25)

−0.29(0.96)

−0.85(2.93)

–

684-Aluminium

−0.75(2.67)

2.68(6.19)

1.28(3.94)

−2.02(7.68)

1.27(3.75)

–

689-Miscell.non-ferrousbase

metals

−0.65(4.21)

−3.86(7.92)

−1.91(6.32)

1.45(5.65)

−0.92(5.21)

–

691-Finishedstructural

partsandstruc

0.16(0.78)

––

−0.07(0.28)

0.10(0.40)

−0.54(2.25)

692-

Metal

containers

forstorageandtr

−0.20(1.77)

––

0.23(1.49)

––

694-Nails,screw

s,nuts,bolts,rivetsand

0.31(2.41)

−0.57(3.60)

−0.32(2.41)

−0.14(1.17)

––

695-Toolsforusein

thehand

orin

mac

0.12(1.49)

––

−0.41(4.39)

−0.08(0.89)

−0.23(2.65)

698-Manufacturesof

metal,nes

0.07(0.96)

––

−0.25(2.70)

––

711-Pow

ergeneratin

gmachinery,othert

−0.26(2.70)

−0.42(4.16)

–−0

.13(1.38)

0.36(3.21)

0.17(1.66)

712-Agriculturalmachinery

andim

plem

en0.23(1.67)

––

0.10(0.52)

––

714-Officemachines

−0.13(1.69)

––

0.21(2.19)

––

715-Metalworking

machinery

0.22(4.98)

−0.91(12.24)

−0.39(7.10)

−0.09(1.56)

0.25(4.32)

–

717-Textileandleathermachinery

0.35(3.23)

−0.59(4.08)

−0.21(2.31)

−0.33(2.89)

0.59(3.10)

0.45(3.04)

718-Machinesforspecialindustries

0.22(4.46)

––

−0.20(3.06)

0.22(3.66)

–

J Econ Finan (2012) 36:555–586 575

Tab

le4

(con

tinued)

Industry

Short-run

coefficientestim

ates

ΔLnV

CH

tΔLnV

CH

t�1

ΔLnV

CH

t�2

ΔLnV

CAN

tΔLnV

CAN

t�1

ΔLnV

CAN

t�2

719-Machinery

andappliances-non

electr

0.14(3.73)

−0.39(5.75)

−0.18(4.34)

0.13(2.78)

––

722-Electricpower

machinery

andsw

itch

0.03(0.53)

0.14(2.30)

0.19(3.69)

−0.10(1.60)

0.52(4.77)

0.13(1.79)

723-Equipmentfordistributin

gelectric

−0.08(0.98)

0.28(3.11)

0.18(2.07)

−0.22(2.19)

0.39(2.65)

0.22(1.84)

724-

Telecom

munications

apparatus

−0.14(2.08)

––

0.07(0.78)

––

725-Dom

estic

electrical

equipm

ent

0.26(3.45)

0.46(4.33)

0.27(2.71)

−0.27(2.86)

––

726-Elec.apparatusformedic.purp.,radi

0.15(2.90)

––

−0.17(2.27)

0.35(3.87)

0.18(2.64)

729-Other

electrical

machinery

andappa

−0.09(2.49)

0.22(4.59)

0.31(8.47)

−0.11(2.65)

0.29(5.68)

0.06(1.46)

732-Roadmotor

vehicles

0.31(3.58)

––

−0.32(2.51)

0.82(4.61)

0.44(3.24)

733-Roadvehicles

otherthan

motor

vehi

−0.05(0.48)

−0.39(4.13)

–0.26(2.44)

––

734-Aircraft

−0.31(4.14)

––

−0.31(3.10)

1.06(8.81)

0.43(4.36)

735-Ships

andboats

−0.27(0.93)

––

0.88(2.50)

−2.29(4.69)

−1.78(5.05)

812-Sanitary,plumbing,heatin

g&

lightin

−0.38(4.33)

0.47(4.44)

0.64(6.83)

0.37(3.84)

−0.42(4.07)

−0.30(3.46)

861-Scientific,m

edical,optical,m

eas./co

0.23(8.64)

−0.04(1.13)

−0.14(4.72)

−0.27(8.28)

0.39(5.64)

0.10(2.48)

862-Photographicandcinematographic

su−0

.32(4.15)

––

0.12(1.03)

0.49(4.72)

0.37(3.64)

863-Developed

cinematographic

film

0.36(1.61)

−1.74(7.29)

−1.32(6.02)

0.07(0.32)

1.52(5.25)

–

864-Watches

andclocks

0.45(1.99)

1.08(3.09)

0.67(2.44)

−0.92(3.72)

––

891-Musical

instruments,sound

recorders

−0.03(0.49)

0.43(5.89)

0.28(4.79)

−0.17(2.46)

−0.24(3.01)

−0.29(4.50)

892-Printed

matter

−0.42(6.58)

−0.47(6.36)

−0.18(2.89)

0.39(5.41)

0.32(4.53)

0.28(3.87)

893-Articlesof

artificialplastic

mate

0.22(4.87)

0.35(6.00)

–−0

.29(4.88)

––

894-Peram

bulators,to

ys,gam

esandsporti

0.18(2.00)

0.71(6.72)

0.44(5.40)

−0.03(0.29)

––

895-Officeandstationery

supplies,nes

−0.30(2.14)

−0.06(0.40)

−0.34(2.46)

0.42(2.72)

−0.68(3.64)

−0.52(3.64)

897-Jewellery

andgold/silv

er-smith

swa

0.41(1.57)

––

0.20(0.57)

––

899-Manufacturedarticles,nes

0.10(1.04)

−0.59(5.71)

−0.55(5.93)

−0.24(2.15)

––

576 J Econ Finan (2012) 36:555–586

found inclusion of the third-country effect eliminated significance impact of the U.S.dollar-Canadian dollar volatility on the U.S. exports to Canada, we find that not onlythe third-country effect, i.e., the volatility of the real U.S. dollar-Canadian dollar hasiimplication on U.S. exports to China, so does the volatility of the U.S. dollar-Chinese yuan.

From the long-run coefficient estimates reported in Table 5, it is clear the theshort-run effects of VCH last into the long run in 39 industries and in most of theindustries, the estimated coefficient is positive, results similar to those of Bahmani-Oskooee and Wang (2007). Once again, these long-run significant effects do notdisappear by including the third-country effect, VCAN, in Bahmani-Oskooee andWang’s specification. Indeed, VCAN carries a significant coefficient in 26 industries.Furthermore, in industries coded 001, 266, 514, 541, 581, 599, 611, 641, 653, 661,674, 689, 719, 735, and 895 the estimated effect is positive, implying that increasedrisk due to the volatility of the U.S. dollar-Canadian dollar increases U.S. exports toChina in these 16 industries. This increased risk, however, reduces U.S. exports toChina in 11 industries coded 533, 662, 673, 684, 718, 722, 726, 734, 861, and 893.All in all, while volatility of the U.S. dollar-Canadian dollar has short-run effects onthe U.S. exports to China in the majority of the industries, the short-run effectstranslate into the long run in one-third of the industries, a unique finding absent fromthe literature. Once again, most of the affected industries are small. Turning to thelong-run effects of Chinese income on the U.S. exports we gather that it carries itssignificantly positive coefficient in the majority of the industries, implying thateconomic growth in China stimulates their imports of American made goods. Thiseffect is negative in four industries coded 001, 041, 652, and 735, implying that asChina’s economy grows they produce more goods that are a close substitute to thesefour industries helping to reduce their imports (or U.S. exports).9 The real exchangerate itself carries a significant coefficient in 36 industries and the estimatedcoefficient is expectedly negative in 13 industries and unexpectedly positive in 23.

Finally, we report all diagnostic statistics in Table 6. To validate the above long-run analysis, we see that cointegration is supported either by a significant F statisticor a significantly negative ECMt−1.

10 The LM test shows lack of autocorrelationamong the residuals of most of the models and the RESET statistic indicatescorrectly specified models in most cases. The estimated short-run and long-runcoefficients are stable as reflected by CUSUM and CUSUMSQ tests and almostevery error-correction model enjoys a nice size of adjusted R2 or goodness of fit.11

4 Summary and conclusion

The impact of exchange rate uncertainty on the trade flows still continues todominate international finance literature. The most recent review article reveals thatmajority of the studies in the literature have looked at the issue without considering

9 For more on this effect see Bahmani-Oskooee (1986).10 Note that there are three exporting industries coded 251, 654, and 812 in which ECMt−1 carries apositive coefficient, implying that in these three models adjustment is not toward long-run equilibrium.11 It is possible that finding for certain industries might be sensitive to the choice of third country. Futureresearch should explore this point.

J Econ Finan (2012) 36:555–586 577

Tab

le5

Long-runcoefficientestim

ates

ofexportdemand(t-ratiosinside

parentheses)

Industry

(trade

share%)

Long-runcoefficientestim

ates

Constant

LnV

CH

LnV

CAN

LnY

CH

LnR

E

001-Liveanim