impact of immigration: disruptive or helpful? · unemployment rate near nairu 4 5 6 7 8 9 10 11 ......

TRANSCRIPT

DABE September Meeting

Denver, CO

September 21, 2016

Pia Orrenius, Ph.D.

Federal Reserve Bank of Dallas

Disclaimer: The views expressed herein are those of the presenter; they do not necessarily reflect the views of the

Federal Reserve Bank of Dallas or the Federal Reserve System.

Impact of Immigration:

Disruptive or Helpful?

Road map

Recent trends

Steady economic growth, tightening labor

markets, but slowing immigration

Forces of international migration

Push and pull factors

Economic and fiscal effects of immigration

Winners and losers

Short run versus long run

Implications for policy

ECONOMY’S GROWING

BUT IMMIGRATION IS

SLOWING

Recent Trends

U.S. employment well past its

pre-recession peak

126

128

130

132

134

136

138

140

142

144

146

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Millions, SA

138.4

144.6

SOURCE: Bureau of Labor Statistics.

7 years into expansion, U.S. GDP

plods along…

13

14

15

16

17

18

19

2003 2004 2005 2005 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Trillions 2015 Dollars,

SAAR

16.5

18.4

SOURCE: Bureau of Economic Analysis.

Hiring has accelerated;

unemployment rate near NAIRU

4

5

6

7

8

9

10

11

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Percent, SA

10.0

4.9

SOURCE: Bureau of Labor Statistics.

0

0.2

0.4

0.6

0.8

1

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Inflows as %

of working-age population

NOTE: Working age population is 16 to 64.

SOURCES: U.S. Department of State, Report of the Visa Office; U.S. Department of Homeland security, Yearbook of

Immigration Statistics; U.S. Customs and Border Protection; U.S. Census Bureau.

Legal permanent

residents (new arrivals)

Temporary worker visas

Apprehensions

(Southwest border)

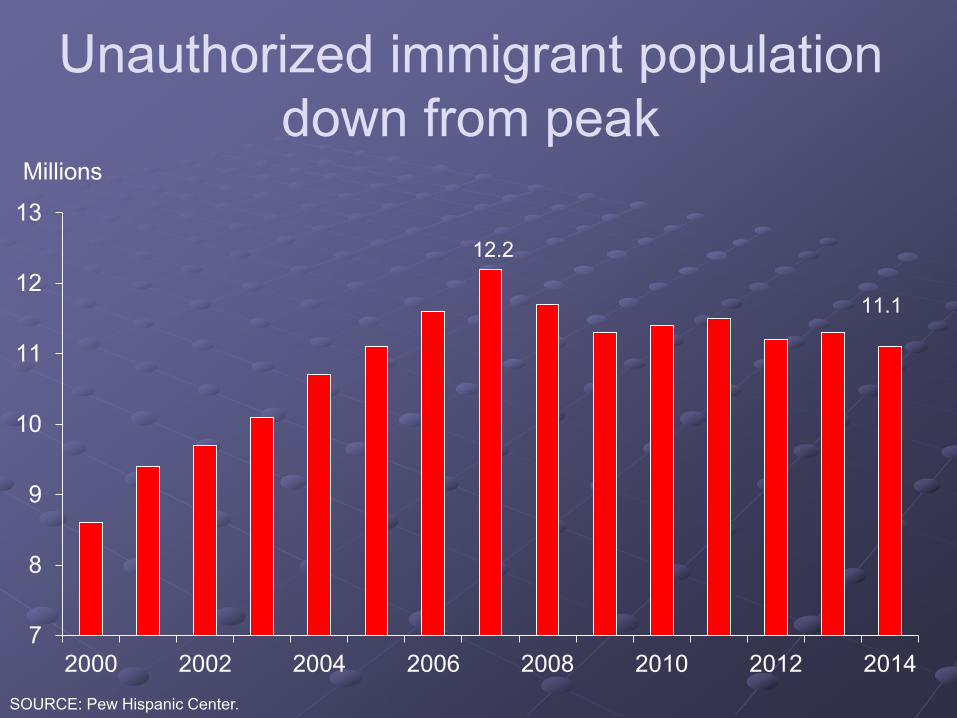

Despite steady growth, immigration

inflows are falling or flat

Unauthorized immigrant population

down from peak

SOURCE: Pew Hispanic Center.

7

8

9

10

11

12

13

2000 2002 2004 2006 2008 2010 2012 2014

Millions

12.2

11.1

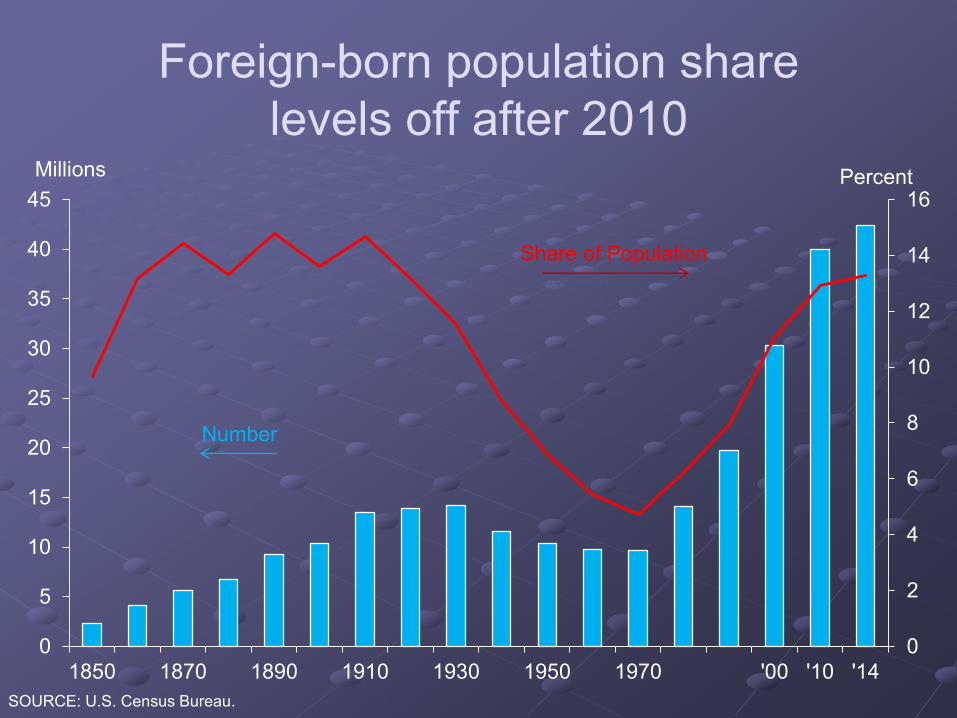

Foreign-born population

42.4 million in 2014

0

5

10

15

20

25

30

35

40

45

1850 1870 1890 1910 1930 1950 1970 '00 '10 '14

Millions

Share of

Population

Number

SOURCE: U.S. Census Bureau.

Foreign-born population share

levels off after 2010

0

2

4

6

8

10

12

14

16

0

5

10

15

20

25

30

35

40

45

1850 1870 1890 1910 1930 1950 1970 '00 '10 '14

Millions Percent

Share of

Population

Number

Share of Population

SOURCE: U.S. Census Bureau.

MIGRANTS GAIN

THE MOST FROM

MIGRATION

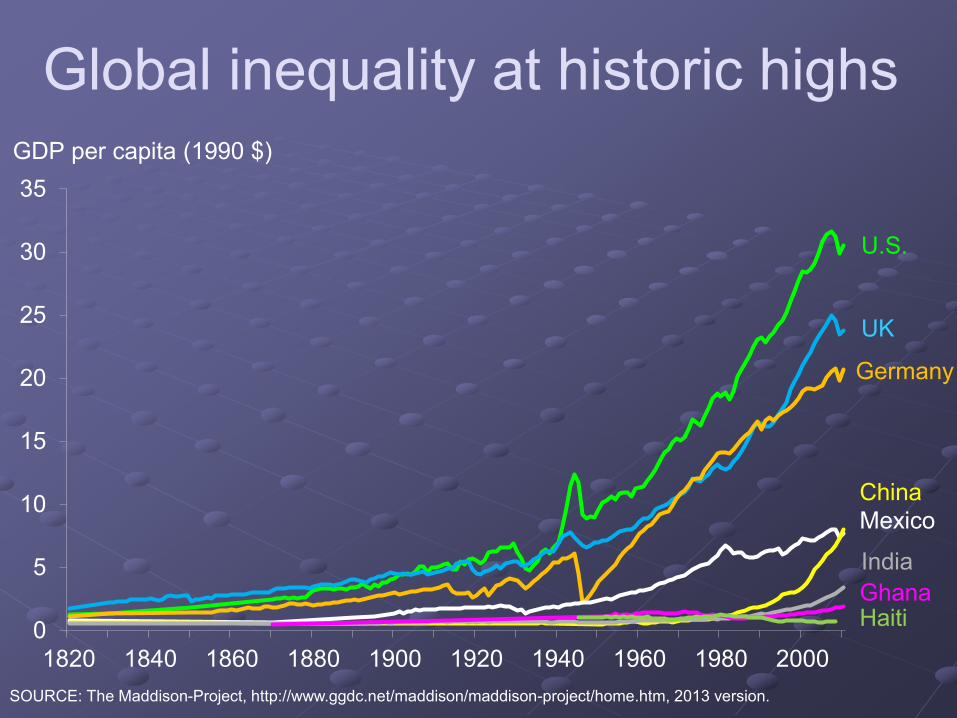

Forces of Migration: Push Factors

0

5

10

15

20

25

30

35

1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

GDP per capita (1990 $)

Global inequality at historic highs

U.S.

Germany

Mexico

China

India

GhanaHaiti

UK

SOURCE: The Maddison-Project, http://www.ggdc.net/maddison/maddison-project/home.htm, 2013 version.

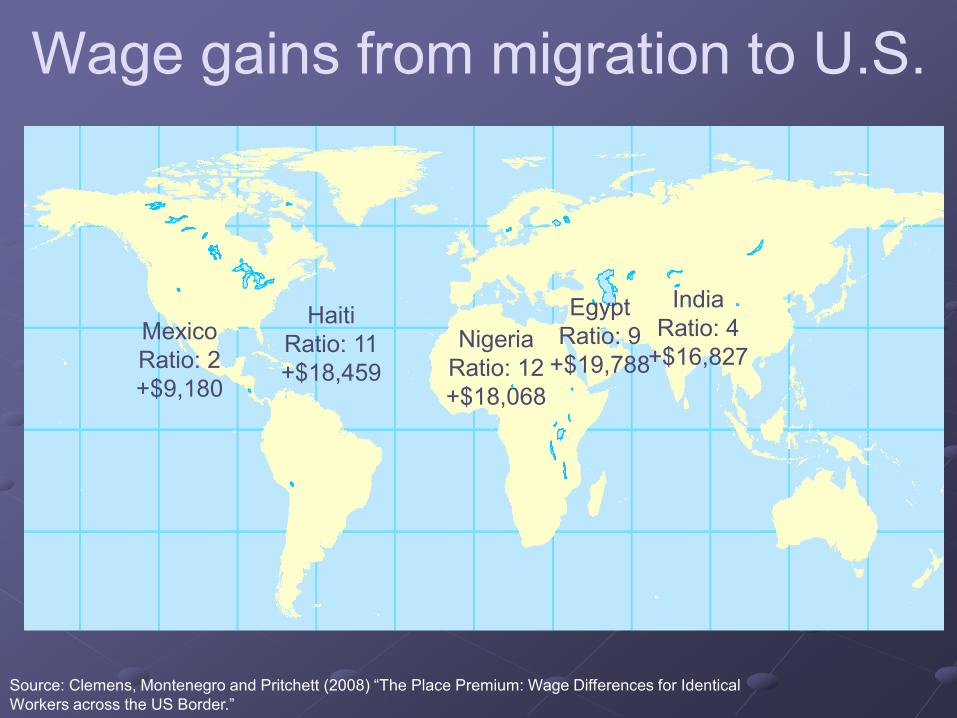

Wage gains from migration to U.S.

Nigeria

Ratio: 12

+$18,068

Haiti

Ratio: 11

+$18,459

Egypt

Ratio: 9

+$19,788

India

Ratio: 4

+$16,827Mexico

Ratio: 2

+$9,180

Source: Clemens, Montenegro and Pritchett (2008) “The Place Premium: Wage Differences for Identical

Workers across the US Border.”

Other factors in world mobility

Costs of moving at historic lows

Transportation

Information

Government-imposed barriers are

increasing

New sections of border fence

Source: Wayne Cornelius (2009) “Evaluating US Immigration Control Policy”

MIGRANTS READILY

FIND WORK

Forces of Migration: Pull Factors

Immigrants in the U.S. labor market

Immigrants are more likely than natives to

move to where the jobs are

Immigrants also

Complement native workers at high, low ends

of skill distribution

Fill jobs natives shun

Innovate/patent more than natives

Start businesses at a higher rate

AL

AK

AZ

AR

CA

CO

CT

DE

FL

GA

HI

ID

IL

IN

IA

KS

KY

LA

ME

MD

MA

MI

MN

MSMO

MT

NE

NV

NHNJ

NM

NY

NC

ND

OH

OK

OR

PA

RI

SC

SD

TN

TX

UT

VT

VA

WA

WV

WIWY

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

-0.15 -0.1 -0.05 0 0.05 0.1 0.15 0.2

In US, immigrants go where the jobs are

NOTE: Coordinates indicate deviation from median foreign born population growth (vertical axis) and from median state nonfarm

payroll growth (horizontal axis) from 1990 to 2014.

SOURCES: U.S. Census Bureau; 2014 American Community Survey; Bureau of Labor Statistics.

Fore

ign b

orn

popula

tion g

row

th

State employment growth

Sometimes they go to where others

are leaving from

NOTE: Population change by Hispanic ethnicity from 2000 to 2010.

SOURCE: U.S. Census Bureau, Census 2000, 2010

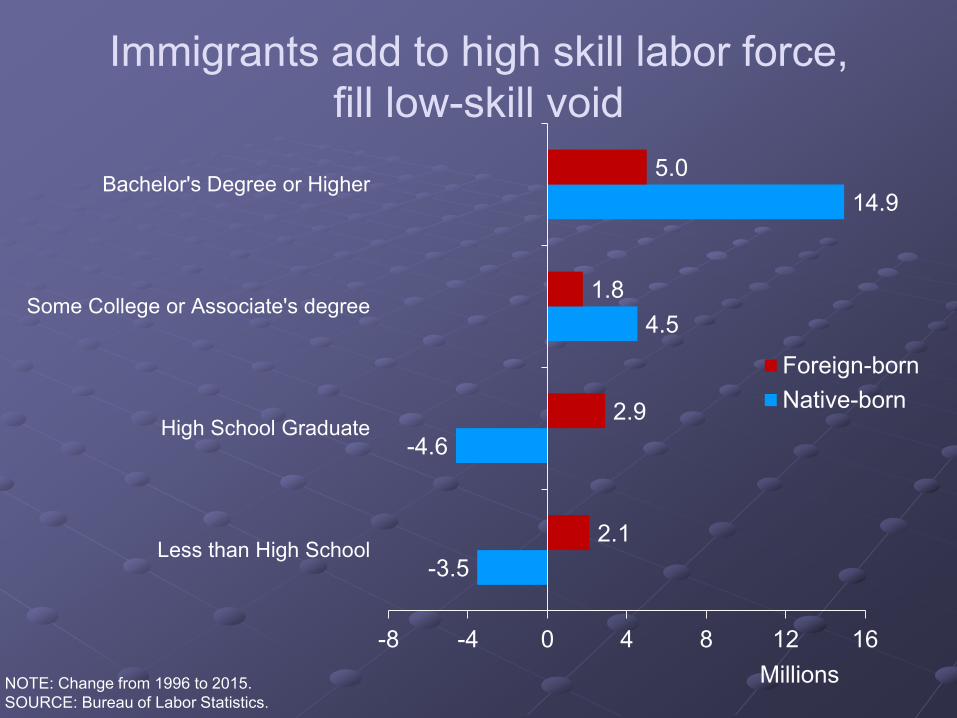

NOTE: Change from 1996 to 2015.

SOURCE: Bureau of Labor Statistics.

Immigrants add to high skill labor force,

fill low-skill void

-3.5

-4.6

4.5

14.9

2.1

2.9

1.8

5.0

-8 -4 0 4 8 12 16

Less than High School

High School Graduate

Some College or Associate's degree

Bachelor's Degree or Higher

Foreign-born

Native-born

Millions

Immigrant workers overrepresented at

extremes of the education distribution

0

10

20

30

40

50

60

Less thanhigh schoolgraduate

High schoolgraduate,

some college

Bachelor'sdegree

Master'sdegree

Professionaldegree

Doctoraldegree

Percent

Foreign born share of

labor force

NOTE: Percent of foreign workers age 25 and over in the U.S. labor force by education.

SOURCE: 2014 American Community Survey

Foreign students drive the rise

in PhDs awarded since 2000

SOURCE: National Science Foundation.

0

10

20

30

40

50

60

1966 1972 1978 1984 1990 1996 2002 2008 2014

Thousands of PhDs

Total

Citizen or perm resident

Temporary resident

STEM, health care occupations rely on

high-skilled foreign workers

NOTE: Percent of workers age 25 and over, with bachelor's degree or higher who are foreign born for selected occupations.

SOURCE: 2014 American Community Survey.

0 10 20 30 40 50

Lawyers/Judges

Veterinarians

Actors, directors, producers

Chief executives and public administrators

Sales Related

Economists, market researchers, survey…

Financial managers

Managers and administrators

Accountants and auditors

Architects

Biological scientists

Biological technicians

Registered nurses

Pharmacists

Mechanical engineers

High school and college instructors

Dentists

Chemical engineers

Computer systems analysts and…

Mathematicians

Physicians

Chemists

Computer software developers

Medical scientists

Foreign-born as a

percentage of college

graduate labor force

16.7

IMMIGRATION

CREATES WINNERS

AND LOSERS

Economic Impact of Immigration

Economic impact of immigration

Labor force grows, GDP rises

Immigrants account for nearly one-half labor

force growth since 1996

Some of the GDP increase accrues to natives;

the “Immigration surplus”

But the immigration surplus is not shared

equally

Wages fall; Return to capital, land rises

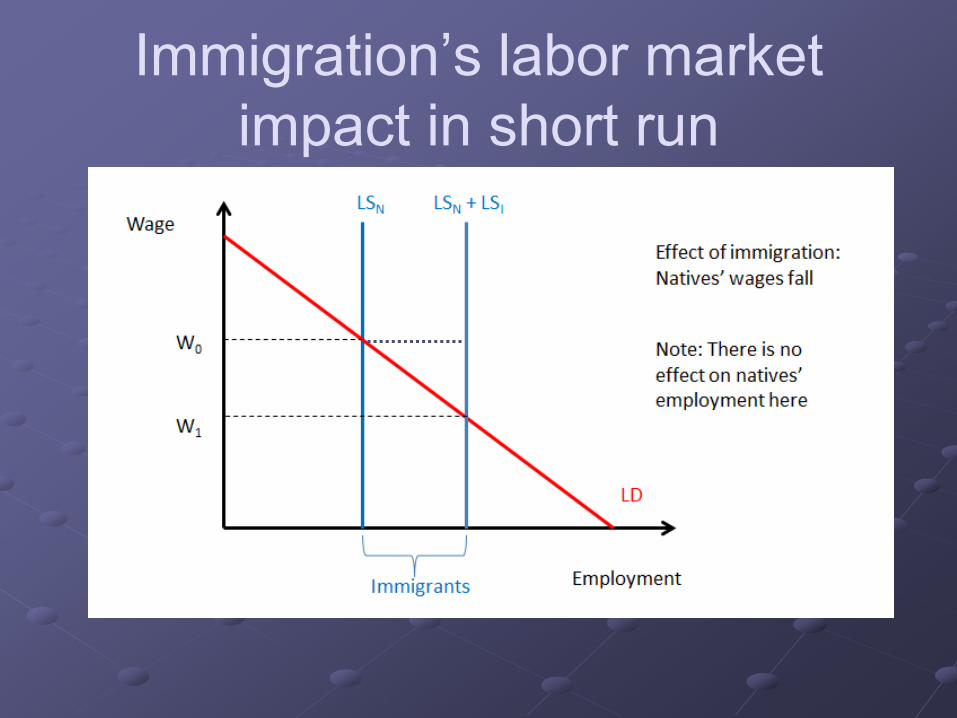

Immigration’s labor market

impact in short run

Immigration’s labor market

impact in long run

Simulated wage impact of 1990-2010

immigrant influx on the preexisting workforce

HS

dropouts

HS

graduates

Some

college

College

graduates

Post-

college

All

workers

Percent supply

shift25.9 8.4 6.1 10.9 15.0 10.6

Percent wage effects

Short run -6.2 -2.7 -2.3 -3.2 -4.1 -3.2

Long run -3.1 0.4 0.9 -0.1 -0.9 0.0

SOURCE: Immigration Economics, George Borjas, table 5.2, page 114.

Simulated long-run wage impact of 1990-

2010 immigrant influx, allowing for within-

group complementarities

Percent wage

effects

HS

dropouts

HS

graduates

Some

college

College

graduates

Post-

college

All

workers

Native-born -1.7 0.9 1.2 0.5 -0.1 0.6

Foreign-born -5.3 -3.4 -2.7 -4.9 -5.3 -4.4

All workers -3.1 0.4 0.9 -0.1 -0.9 0.0

SOURCE: Immigration Economics, George Borjas, table 5.4, page 120.

Two remaining questions

How long is the long run?

How long will it take capital to adjust?

What about other costs of immigration?

Fiscal impact: what you contribute in taxes

minus what you consume in publicly provided

goods and services

Low-skilled immigrants have a negative fiscal

impact

Fiscal impact negative at state and local level,

positive at federal level

WHO SHOULD

COME?

Implications for Policy

Summary & policy implications

Net economic benefits to immigration

So we should have immigration

But immigration appears to be slowing

Need better immigration policy

Some natives lose from immigration in short

run

Get to the long run faster by speeding

adjustment; making immigration predictable

Summary & policy implications -2-

Migrants are the biggest winners

Policy doesn’t need to confer additional

benefits

Low-skilled immigration has negative fiscal

impact

Transfer funds from federal to state & local

Admit more high-skilled immigrants

Consider temporary worker program

Bottom line

Immigration is disruptive AND helpful

Low-skilled: H-2B visa applications

outstrip number availableThousands

Applications

Available visas

SOURCE: Office of Foreign Labor Certification, Annual Reports for various years.

0

50

100

150

200

250

300

350

400

2000 2002 2004 2006 2008 2010 2012 2014

Naturalized citizens

Legal permanent residents

Temporary legal residents

Unauthorized immigrants

Unauthorized population almost as large

as permanent resident population

SOURCE: Pew Research Center estimates for 2012 based on augmented American Community Survey data from IPUMS.

High-Skilled: Not enough temporary visas,

H-1B cap reached before year-end since 2004

0

50

100

150

200

250

300

350

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Number of days until cap reached

SOURCE: U.S. Citizenship and Immigration Services.

In the U.S., green cards go to

family, not work-based immigrants

NOTE: Averages for years 2010-2014.

SOURCE: U.S. Department of Homeland Security, Yearbook of Immigration Statistics.

Family65%

Employment14%

Refugees and asylees

14%

Diversity5%

Others2%

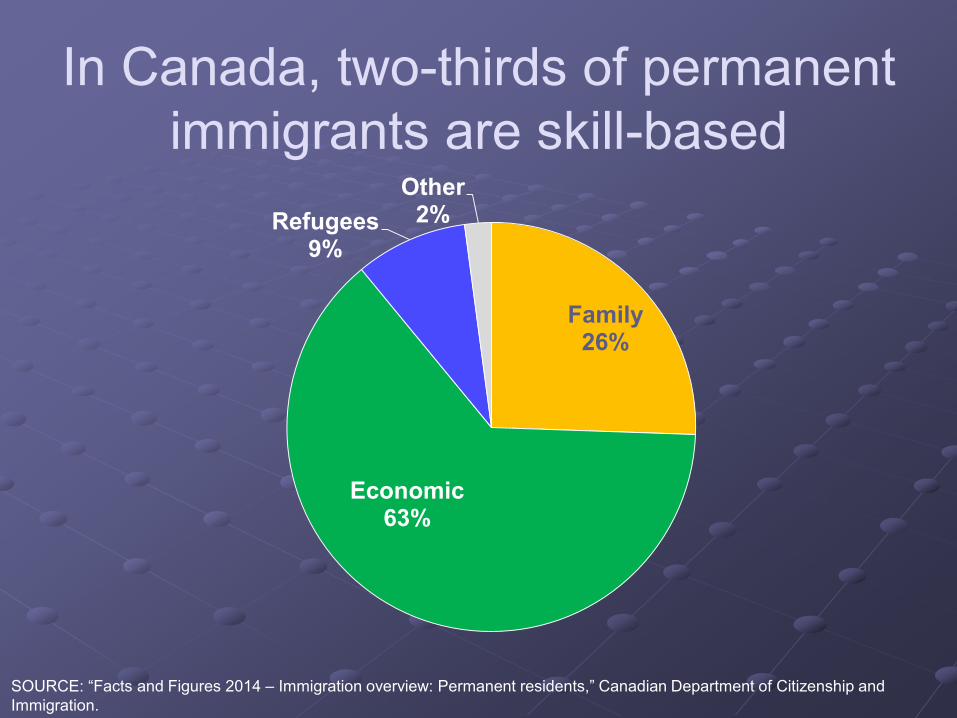

In Canada, two-thirds of permanent

immigrants are skill-based

Family26%

Economic63%

Refugees9%

Other2%

SOURCE: “Facts and Figures 2014 – Immigration overview: Permanent residents,” Canadian Department of Citizenship and

Immigration.

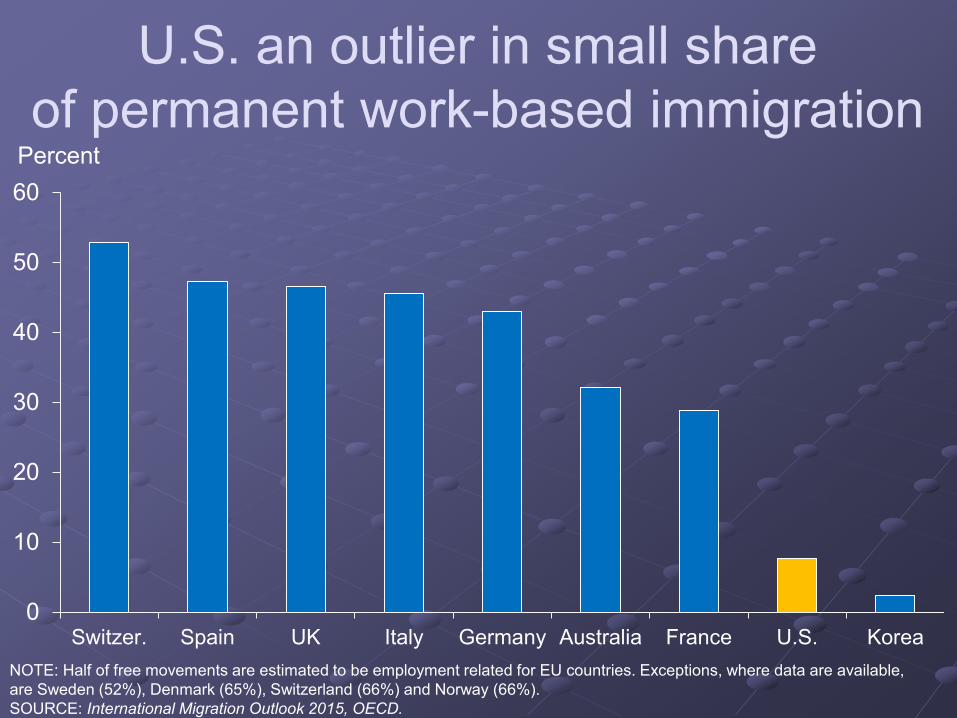

0

10

20

30

40

50

60

Switzer. Spain UK Italy Germany Australia France U.S. Korea

U.S. an outlier in small share

of permanent work-based immigration

NOTE: Half of free movements are estimated to be employment related for EU countries. Exceptions, where data are available,

are Sweden (52%), Denmark (65%), Switzerland (66%) and Norway (66%).

SOURCE: International Migration Outlook 2015, OECD.

Percent

Problems with current U.S. policy

Priority is family, not work or skills

No alternative for unauthorized

immigration

Work-based visa quotas insufficient, fixed;

temporary inconsistent with permanent

Skilled workers face long queues if want to

stay permanently

Country quotas penalize populous nations

Visa allocation nonsensical: first come,

first served or a lottery