impact of shale gas, tight oil and oil sands on european refining

TRANSCRIPT

1 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

OMV Refining & Marketing

Impact of shale gas, tight oil and oil sands on European refining and petrochemical Industry Brussels, Sep.20th, 2013

2 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Legal Disclaimer This presentation is prepared in order to outline our expression of interest. Nothing in this presentation shall be construed to create any legally binding obligations on any of the parties. Neither party shall be obligated to execute any agreement or otherwise enter into, complete or affect any transaction in relation to this presentation.

All figures and information in this presentation are strictly confidential, they are by no means binding and thus indicative only.

© 2013 OMV Aktiengesellschaft, all rights reserved, no reproduction without our explicit consent.

3 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

4 Refineries in Austria, Germany, and Romania with total capacity ~22 mn t/a Germany: Burghausen (3.5 mn t ), Bayernoil (4.5 mn t, JV, on sale)

Austria: Schwechat (9.6 mn t)

Romania: Petrobrazi (4.2 mn t)

20% market share in the Danube region High product quality and environmental standards Strong retail brand and high-quality, innovative

non-oil business (VIVA) Active in 13 countries with around 4,400 filling

stations in 2012 (incl. Petrol Ofisi) Total ~ 3,300 employees

OMV Refining & Marketing as European Company is Supplying over 200 mn People with Energy

OMV filling station network

4 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Unconventional oil and gas has the potential to change the refining and petrochemical

industry globally.

5 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

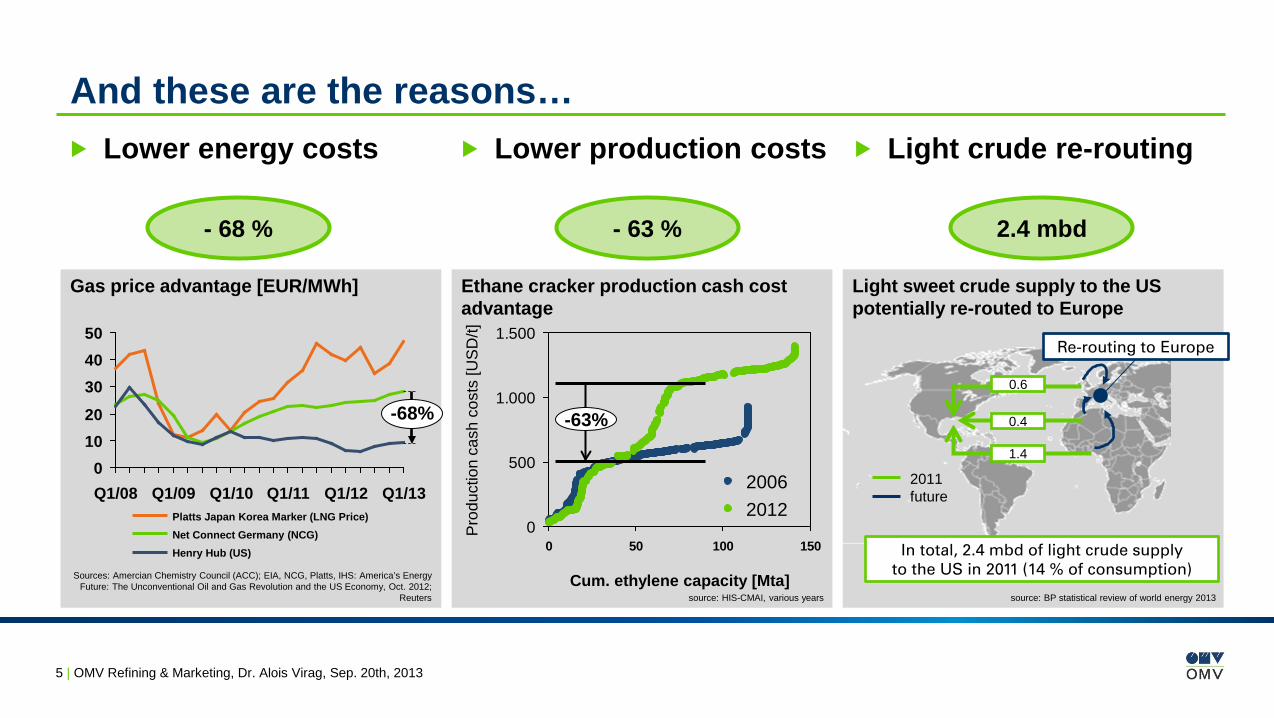

Light sweet crude supply to the US potentially re-routed to Europe

And these are the reasons… Lower energy costs

Gas price advantage [EUR/MWh]

source: BP statistical review of world energy 2013

Sources: Amercian Chemistry Council (ACC); EIA, NCG, Platts, IHS: America’s Energy Future: The Unconventional Oil and Gas Revolution and the US Economy, Oct. 2012;

Reuters

Ethane cracker production cash cost advantage

0

500

1.000

1.500

0 50 100 150

Pro

duct

ion

cash

cos

ts [U

SD

/t]

Cum. ethylene capacity [Mta] source: HIS-CMAI, various years

Lower production costs

Light crude re-routing

2006 2012

-63%

In total, 2.4 mbd of light crude supply to the US in 2011 (14 % of consumption)

0.6

0.4

1.4

- 68 % - 63 % 2.4 mbd

01020

304050

Q1/13 Q1/12 Q1/11 Q1/10 Q1/09 Q1/08

-68%

Net Connect Germany (NCG)

Henry Hub (US)

Platts Japan Korea Marker (LNG Price)

Re-routing to Europe

2011 future

6 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

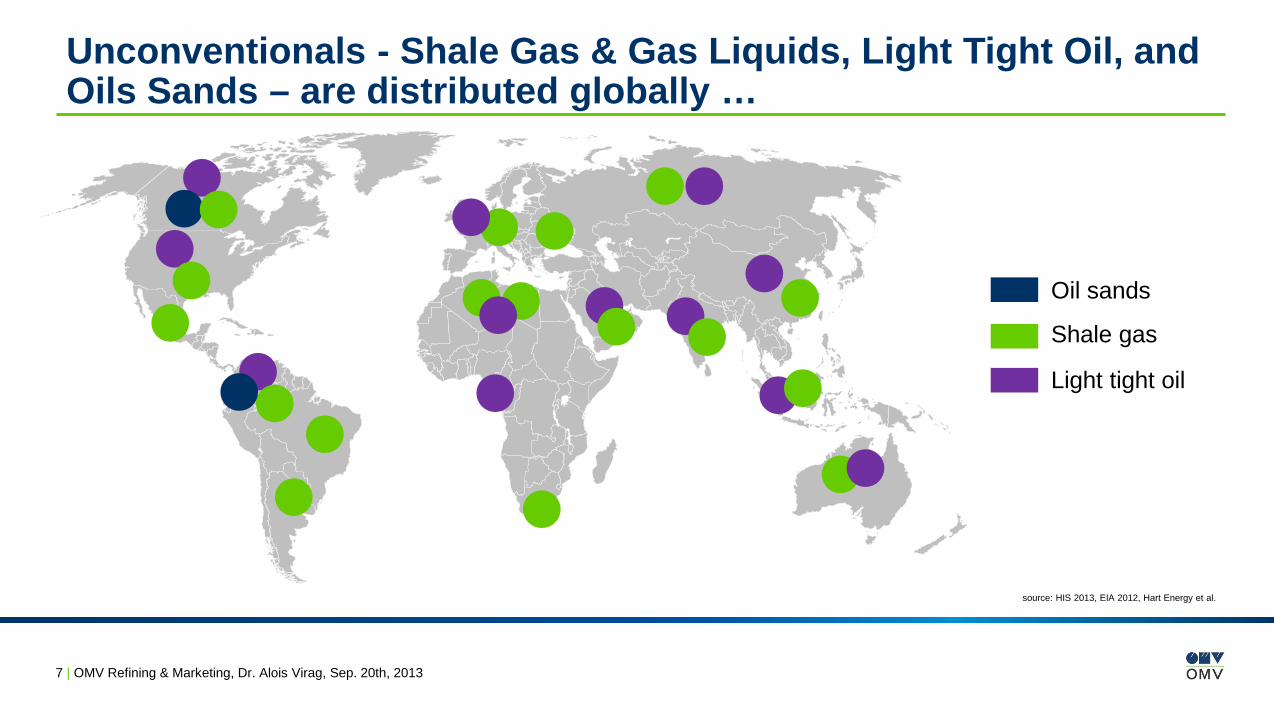

There are huge reserves of unconventionals - globally.

7 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Unconventionals - Shale Gas & Gas Liquids, Light Tight Oil, and Oils Sands – are distributed globally …

source: HIS 2013, EIA 2012, Hart Energy et al.

Oil sands

Shale gas

Light tight oil

8 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

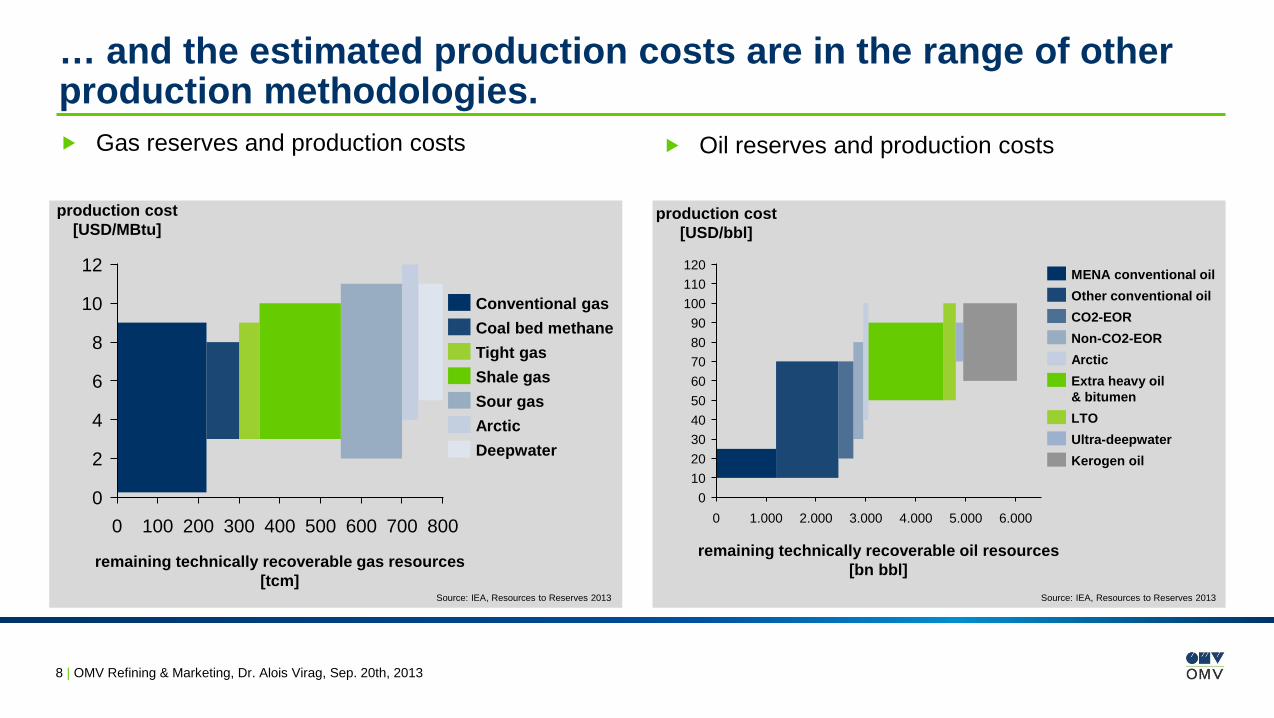

… and the estimated production costs are in the range of other production methodologies. Gas reserves and production costs

Oil reserves and production costs

Source: IEA, Resources to Reserves 2013 Source: IEA, Resources to Reserves 2013

700 500 400 600

4

0 300

12

10

8

6

2

0 200 100 800

production cost [USD/MBtu]

remaining technically recoverable gas resources [tcm]

Deepwater Arctic Sour gas Shale gas Tight gas Coal bed methane Conventional gas

50

10

3.000

70

30

4.000 5.000

110

6.000

20

60

100

0 1.000

90

2.000

120

80

40

0

production cost [USD/bbl]

remaining technically recoverable oil resources [bn bbl]

Ultra-deepwater

Extra heavy oil & bitumen

Arctic Non-CO2-EOR CO2-EOR Other conventional oil MENA conventional oil

LTO

Kerogen oil

9 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Today, the main barriers are above ground: policy & public

opinion, land access, and product-to-processing site infrastructure.

10 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Current crude pipeline network is currently unable to handle the new situation ... Canadian oil sand and Bakken US shale oil cannot

be supplied to US refineries at the Gulf Coast.

… but major projects are commissioned soon and planed for the midterm future Starting with the Seaway Pipeline reversal 2012,

domestic light sweet crudes are entering the Gulf Coast region; an expansion is already planned

The Canadian heavy crude pipelines capacity starts to increase from 2015 onwards, but full capacity expected in 2017. Major projects like Keystone XL discussed controversially due to environmental issues.

Large volume flows of unconventional is currently limited by logistics – not only in North America

North American pipeline and expansion project

11 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

The most important above ground issues include: Policy / Public opinion Land access Business terms Supply Chain Midstream infrastructure Water availability and management Other regulatory

Current political boundary conditions in EU vary, but many of the countries are reluctant to shale gas production so far

Indication of political / public opinion on shale gas / fracking

sources : various

Poland

Ukraine

Spain

Denmark

France

Germany

Romania

United Kingdom

Lithuania

more negative more positive

12 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Advantaged feedstock affect petrochemical industry.

13 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

The cash costs for production of ethylene are affected by lower feedstock and lower energy costs, simultaneously Ethane based shale gas in the US shifts the global cost curve significantly.

Naphtha – Rest of the World Ethane- Middle East Ethane - North America

source: IHS WPC 2013

0

500

1.000

1.500

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

Pro

duct

ion

cash

cos

ts [U

SD

/t]

Cum. ethylene capacity [Mta]

2012: ~ 100 USD/bbl 2006: ~ 60 USD/bbl

margin

Ethylene price 2012

Demand 2012

14 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

There are on-purpose monomer production technologies available

which are already competitive.

15 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

The shift towards ethane crackers in North America resulted in a supply gap for propylene and other higher molecular petchem products affecting local prices.

Propane is the most available gas liquid.

Propane dehydration (PDH) is the most evolving technology in North America and North East Asia.

Propane Dehydration is the fastest emerging on-purpose technology

Propylene to ethylene Price Ratio

Share of propane dehydration capacity of total propylene capacity

source: IHS-CMAI, 2013

source: Nexant. 2ß12

0

10

20

2014 2013 2012 2011 2010 2009 2008 2007 2017 2016 2015

0,5

1,0

1,5

2010 2008 2012 2016 2006 2014

North East Asia North America

USA Western Europe

forecast

16 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Unconventionals have already affected global crude price

differentials.

17 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

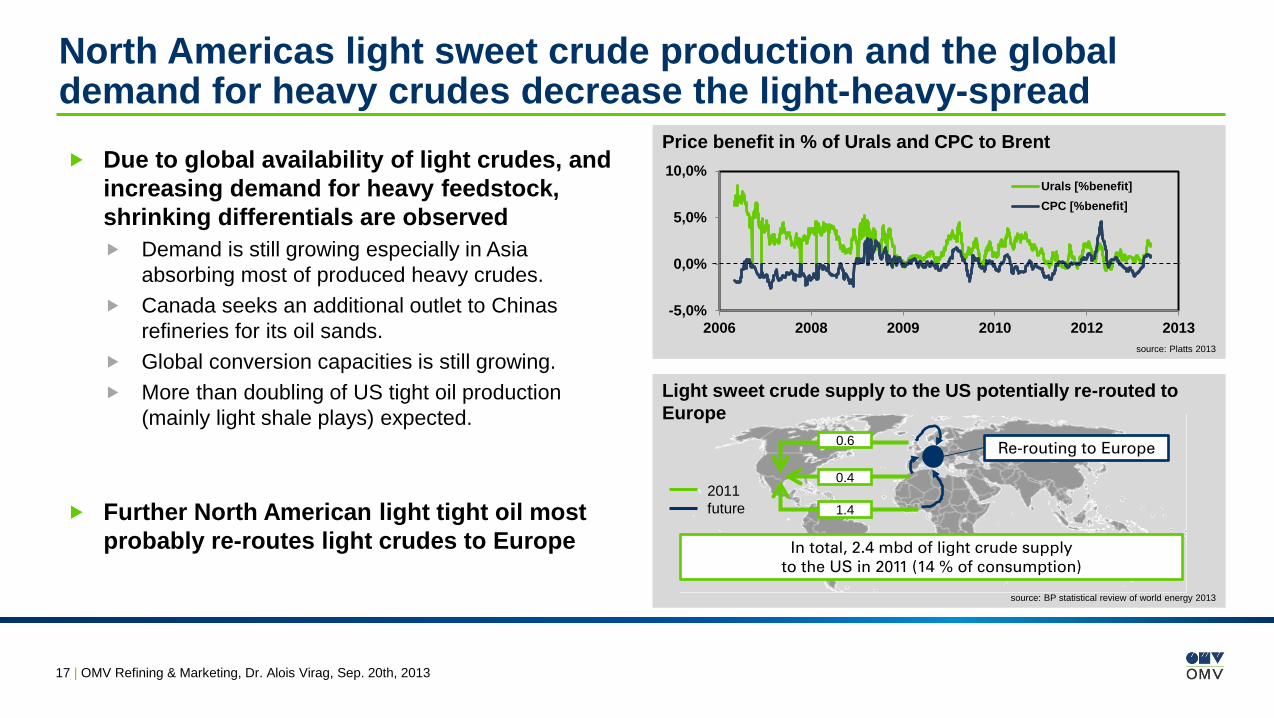

Due to global availability of light crudes, and increasing demand for heavy feedstock, shrinking differentials are observed Demand is still growing especially in Asia

absorbing most of produced heavy crudes. Canada seeks an additional outlet to Chinas

refineries for its oil sands. Global conversion capacities is still growing. More than doubling of US tight oil production

(mainly light shale plays) expected.

Further North American light tight oil most

probably re-routes light crudes to Europe

North Americas light sweet crude production and the global demand for heavy crudes decrease the light-heavy-spread

Price benefit in % of Urals and CPC to Brent

Light sweet crude supply to the US potentially re-routed to Europe

source: BP statistical review of world energy 2013

source: Platts 2013

In total, 2.4 mbd of light crude supply to the US in 2011 (14 % of consumption)

0.6

0.4

1.4

Re-routing to Europe

-5,0%

0,0%

5,0%

10,0%

2006 2008 2009 2010 2012 2013

Urals [%benefit]CPC [%benefit]

2011 future

18 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Domestic refining and petrochemical industry will play a

significant role in future, especially if vertical and horizontal

integration exists.

19 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

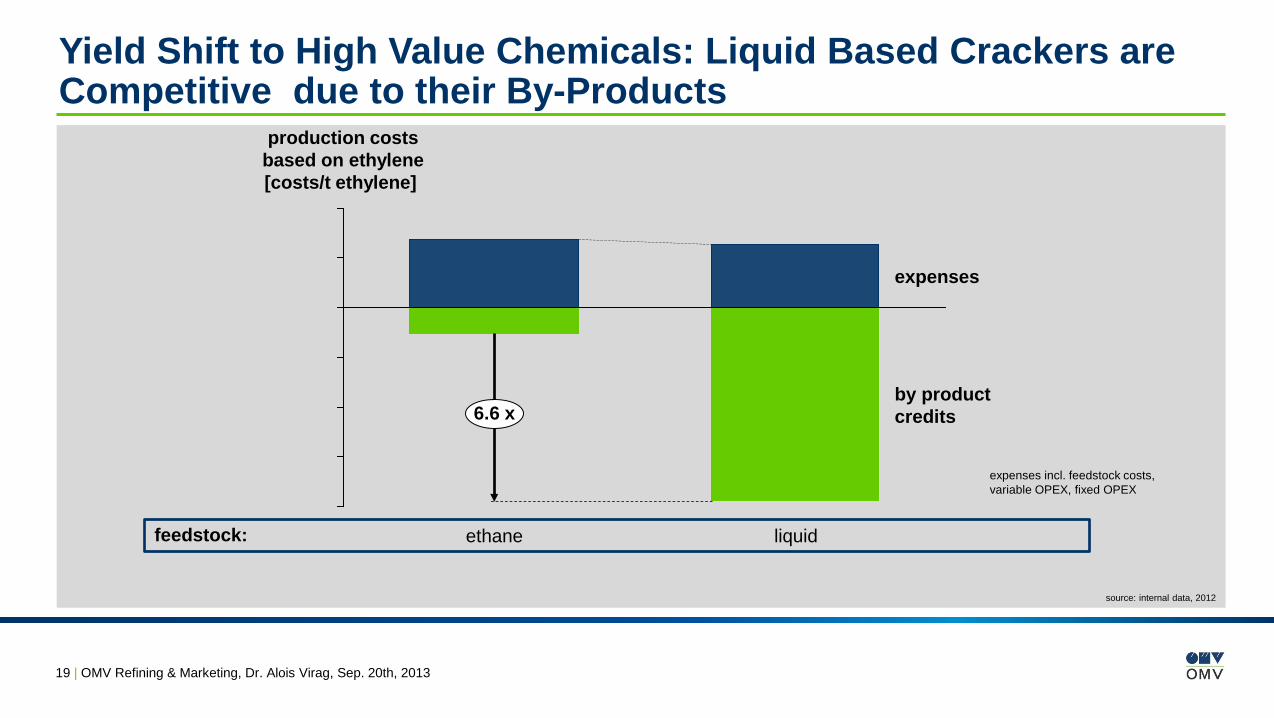

Yield Shift to High Value Chemicals: Liquid Based Crackers are Competitive due to their By-Products

source: internal data, 2012

production costs based on ethylene [costs/t ethylene]

6.6 x by product credits

expenses

liquid ethane feedstock:

expenses incl. feedstock costs, variable OPEX, fixed OPEX

20 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

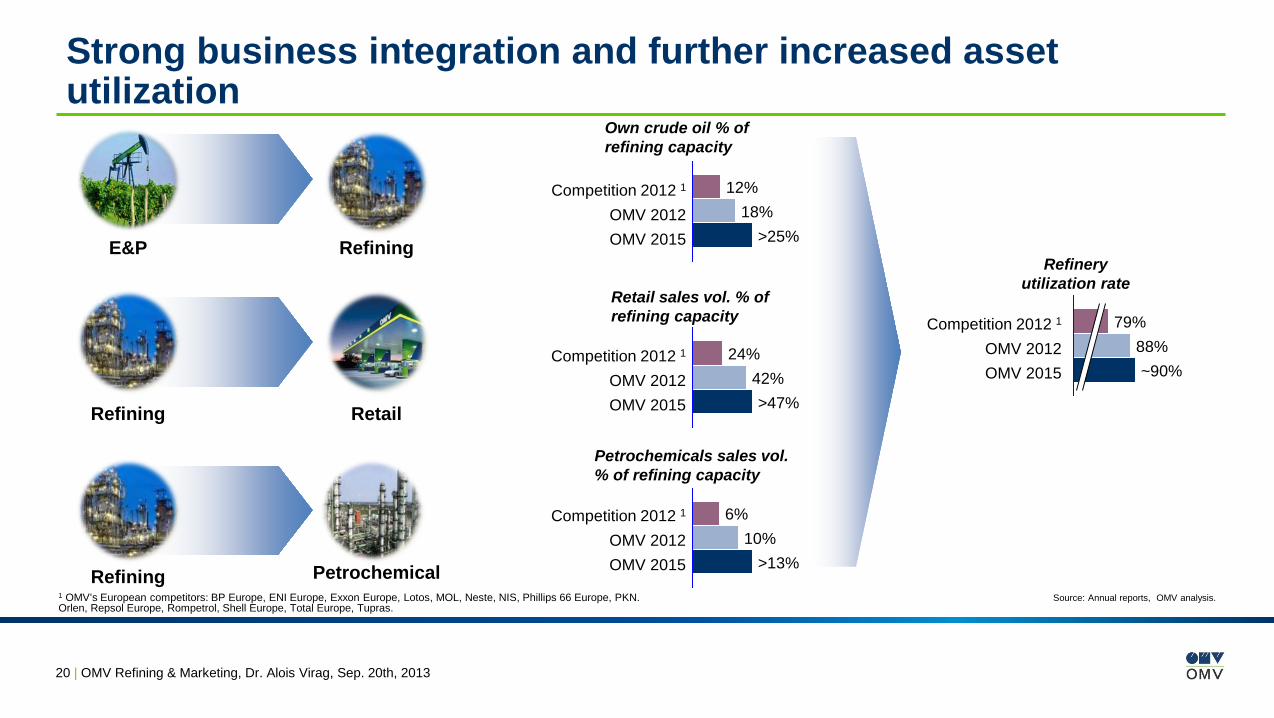

Strong business integration and further increased asset utilization

Source: Annual reports, OMV analysis.

Competition 2012 1 OMV 2012 OMV 2015

Competition 2012 1 OMV 2012 OMV 2015

1 OMV’s European competitors: BP Europe, ENI Europe, Exxon Europe, Lotos, MOL, Neste, NIS, Phillips 66 Europe, PKN. Orlen, Repsol Europe, Rompetrol, Shell Europe, Total Europe, Tupras.

E&P Refining

Retail

Petrochemical

Refining

Petrochemicals sales vol. % of refining capacity

Retail sales vol. % of refining capacity

Own crude oil % of refining capacity

Refining

Refinery utilization rate

>25% 18%

12%

>47% 42%

24%

>13%

6% 10%

79%

~90% 88%

Competition 2012 1 OMV 2012 OMV 2015

Competition 2012 1 OMV 2012 OMV 2015

21 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013

Starting in North America, global unconventional oil and gas reserves have the potential to change our business.

Low energy prices and low feedstock prices stimulate refining and petrochemical business incl. upcoming new technology to balance the limited supply of higher hydrocarbon petrochemical feedstock.

Increasing domestic availability of light sweet crude pressurises the heavy-light differential.

Integration into upstream, downstream, and in petrochemicals as well as cost performance leadership deliver the basis for a vital oil and gas business in Europe

OMV as highly integrated oil and gas player

is prepared to play a significant role in the future.

Summary

22 | OMV Refining & Marketing, Dr. Alois Virag, Sep. 20th, 2013