impacts on global coal trade under alternative coal transition scenarios€¦ · iea (2016b):...

TRANSCRIPT

COALMOD-World

Impacts on Global Coal Trade

under Alternative Coal Transition

Scenarios

WORK in PROGRESS – FINAL REPORT online in April 2018

Franziska Holz, Ivo Kafemann, Tim Scherwath (DIW Berlin),

Roman Mendelevitch (HU Berlin), Oliver Sartor (IDDRI), Thomas Spencer (TERI)

Strommarkttreffen "Kohleausstieg" 12. Januar 2018

The Coal Transitions Project 0

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 2

0 The Coal Transitions Project

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 3

Find updated information and publications on the website

www.coaltransitions.org

1 COALMOD-World Model A Representation of the Global Coal Value Chain

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 4

$/t

Q

Supply Demand Global Steam Coal

Market

Coal Infrastructure

1 COALMOD-World Model: A unique and established quantitative framework

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 5

Single-period trade model (2010)

Multi-period global model (2012)

Multi-period global model (2015)

Climate scenarios (2013)

Supply side policies (2016)

Assuming perfect competition:

Market power in the Atlantic (2012)

Export and produc-tion taxes (2015)

Other forms of market power:

The Global Steam Coal Market

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 6

Sou

rce

: IEA

(2

01

6b

)

Major producers in 2015 Major consumers in 2015

China (2,970 Mt) China (3,140 Mt)

United States (690 Mt) India (750 Mt)

India (590 Mt) United States (630 Mt)

Indonesia (450 Mt) World consumption 5,850 Mt

World production 5,835 Mt Seaborne Trade: 880 Mt (15%) Source: IEA (2017)

1

Overview of world steam coal market: supply, demand, trade

Coal Transitions Project: Climate Scenarios focusing on Coal Demand

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 7

Reference Scenario (NDC): • Coal consumption based on IEA Coal Information 2012 • Growth rates of coal demand derived from IEA (2016a) WEO 2016 New Policy Scenario + Partial equilibrium on regional level due to overarching consistent quantitative framework + Incorporating NDC policies in different countries/regions

2

450 ppm Scenario (2° C): • Coal consumption based on IEA Coal Information 2012 and growth rates derived from

WEO 2016 450 ppm scenario (consistent with the 2° C target) • Note that IEA (2016a) assumes strong use of CCS (430 GW CCS-power plants in 2040)

Enhanced Coal Transition Scenario (ECT): • Enhanced information on national transition scenarios from the project country teams • Based on NDC scenario, except with lower demand in China, India, USA, and South

Africa (after 2030)

Enhanced Coal Transition Scenario 2 (ECT 2): • As ECT, except for India (less ambitious with higher reference demand) and China (more

ambitious with lower reference demand)

Bottom -up

Top- Down

Enhanced Supply Side Scenario (ESS): • As ECT 2 and exogenously assuming realization of the Indian-owned Adani mine in

Queensland (Australia) with dedicated exports to India

2 COALMOD Results: Global Coal Consumption by Scenario

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 8

0

1000

2000

3000

4000

5000

6000

2010 2015 2020 2025 2030 2035 2040 2045 2050

Mt

ECT

Reference (NDC)

2°

- 32 %

Total consumption

2010-2050:

-10 %

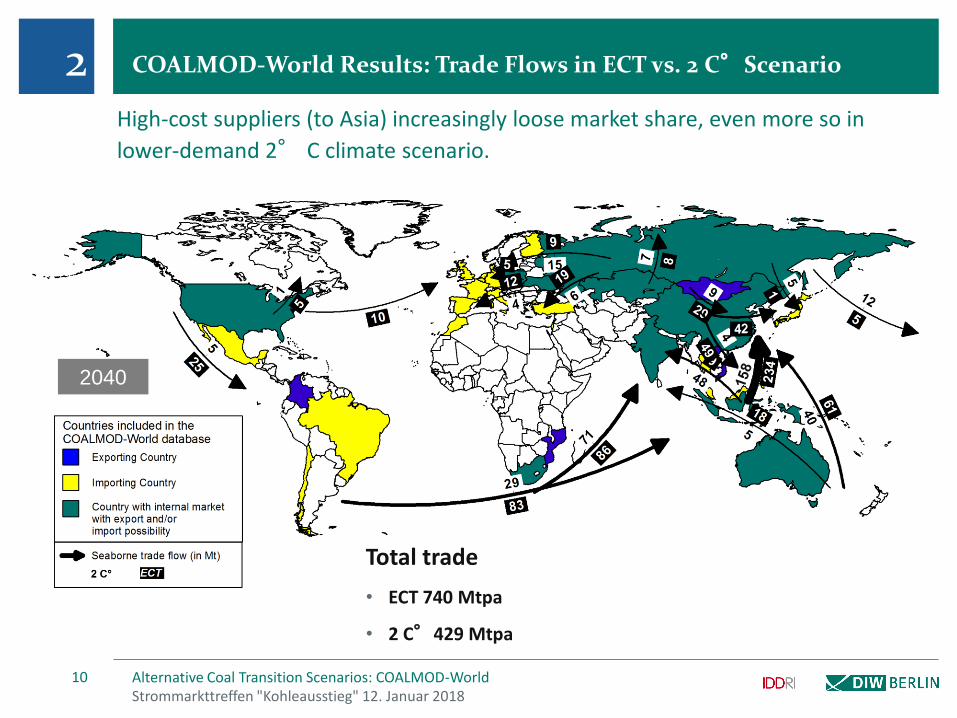

2 COALMOD-World Results: Trade Flows in ECT vs. 2 C°Scenario

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 9

Total trade

• ECT 795 Mtpa

• 2 C°632 Mtpa

Ongoing trend: the shift to Asia and especially India

2030

2 COALMOD-World Results: Trade Flows in ECT vs. 2 C°Scenario

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 10

Total trade

• ECT 740 Mtpa

• 2 C°429 Mtpa

High-cost suppliers (to Asia) increasingly loose market share, even more so in

lower-demand 2° C climate scenario.

2040

3 COALMOD-World Results: Investments in the Coal Value Chain

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 11

In climate-friendly scenarios, investments compensate for mine mortality and remove transport bottlenecks.

Even in a NDC world such as in the ECT scenario, investment needs can be considerably reduced compared to the reference case.

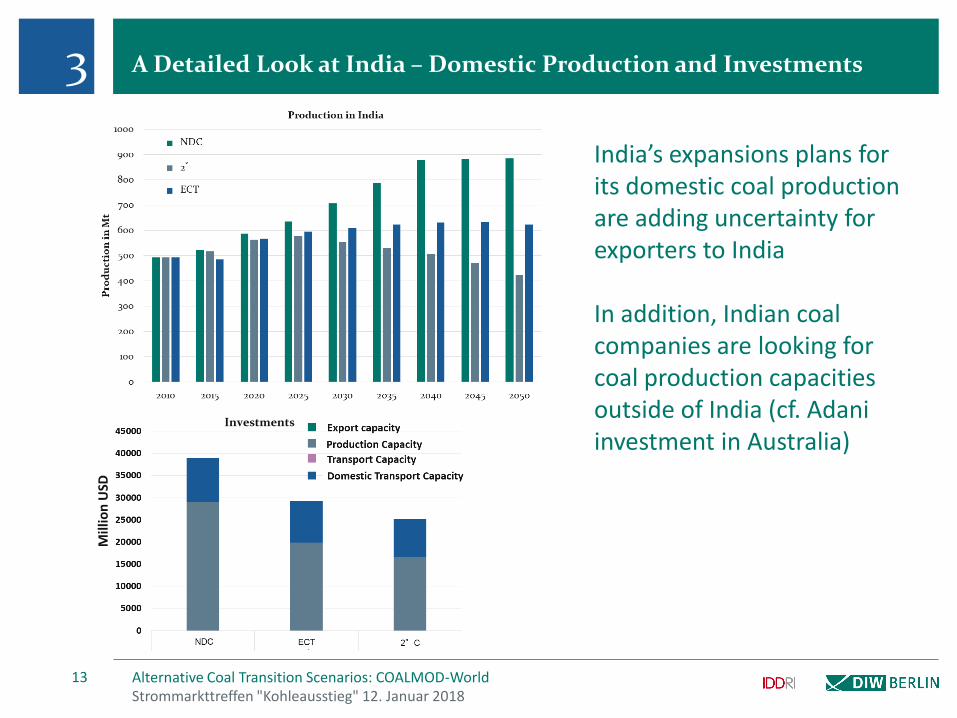

A Detailed Look at India

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 12

0

400

800

1200

2020 2025 2030 2035 2040 2045 2050

Consumption in India by scenario

NCD

mtp

a

2° C

ECT

33

3 A Detailed Look at India – Domestic Production and Investments

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 13

Investments

India’s expansions plans for its domestic coal production are adding uncertainty for exporters to India In addition, Indian coal companies are looking for coal production capacities outside of India (cf. Adani investment in Australia)

Mill

ion

USD

3 Investments in Key Exporting Countries to India

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 14

Risk of asset stranding may arise quickly M

illio

n U

SD

Indonesia Indonesia Indonesia South Africa South Africa

3 Diversification of Trade Flows: Varying Exposure to Demand Changes

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 15

Mtp

a M

tpa

0

50

100

Mtpa Mtpa Mtpa

2030 2030 2030

001 002 003

Exports by South Africa in 2030

ZAF - IND

NDC 2° C ECT

0

50

100

Mtpa Mtpa Mtpa

2030 2030 2030

001 002 003

Exports by Australia in 2030

AUS - TWN

AUS - THA

AUS - PHL

AUS - CHN

NDC 2° C ECT

Summarizing COALMOD Results: Reference vs. 2°C Scenario

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 16

0

1000

2000

3000

4000

5000

Refe

rence (

ND

C)

2°

C

Mt

0

1000

2000

3000

4000

5000

2010 2015 2020 2025 2030 2035 2040 2045 2050

India imports

China imports

International seaborne trade (except China & India imports) Domestic supply (except China & India) India domestic supply

China domestic supply

4 Shift to Asia – in particular India – in all scenarios. China remains the largest coal consumer in all scenarios

Summarizing COALMOD Results: Reference vs. ECT Scenario

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 17

0

1000

2000

3000

4000

5000

0

1000

2000

3000

4000

5000

2010 2015 2020 2025 2030 2035 2040 2045 2050

India imports

China imports

International seaborne trade (except China & India imports) Domestic supply (except China & India) India domestic supply

China domestic supply

Mt

Refe

rence (

ND

C)

EC

T

4 International coordination of coal transition required, but importantly on national policies that tackle coal consumption at the domestic levels (in China, India, …)

4 Conclusions

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 18

• Global coal market modeling shows that there is a broad

range of possible futures that are NDC-compatible

• Additional policies are needed to close the gap between

NDC/ECT and 2°scenarios

• Governments need to take into account that stakeholders

might oppose – even low-ambitious – climate policies

because of the fear of losing market shares and foregoing

revenues from reserves and capacities (asset stranding)

• In particular in South Africa, but also Australia, …

• Overcapacity from high investments and rising concentration

on market Pressure on prices and revenues Transition

policies should address this “revenue gap”

Insights from a Global Coal Model

Thank you very much for

your attention!

Franziska Holz (DIW Berlin)

References

Strommarkttreffen "Kohleausstieg" 12. Januar 2018 Alternative Coal Transition Scenarios: COALMOD-World 20

Haftendorn, Holz, Kemfert, and Hirschhausen (2013): Global Steam Coal Markets until 2030 – Perspectives on Production, Trade, and Consumption under Increasing Carbon Constraints. In: R. Fouquet (Ed.) “Handbook on Energy and Climate Change”, 103-122, Edward Elgar Publ.

Haftendorn, Kemfert, and Holz (2012): What about Coal? Interactions between Climate Policies and the Global Steam Coal Market until 2030. Energy Policy 48, 274-283.

Haftendorn (2012): Evidence of Market Power in the Atlantic Steam Coal Market Using Oligopoly Models with a Competitive Fringe. DIW Discussion Paper 1185.

Haftendorn, Holz, and Hirschhausen (2012): The End of Cheap Coal? A Techno-economic Analysis Until 2030 using the COALMOD-World Model. FUEL 102, 305-325.

Haftendorn and Holz (2010): Modeling and Analysis of the International Steam Coal Trade. The Energy Journal 31 (4), 201-225.

IEA (2012): Coal Information 2012. Coal information. OECD/Paris.

IEA (2016a): World Energy Outlook 2016. OECD/Paris.

IEA (2016b): Medium-Term Coal Market Report 2016. OECD/Paris.

IEA (2017): Coal Information 2017. Coal information. OECD/Paris.

Holz, Haftendorn, Mendelevitch, and Hirschhausen (2015): COALMOD-World: A Model to Assess International Coal Markets Through 2030. In: M.C. Thurber and R.K. Morse (Eds.) “Asia and the Global Coal Market”, Cambridge Univ. Press.

Mendelevitch (2016): Testing Supply-Side Climate Policies for the Global Steam Coal Market – Can They Curb Coal Consumption?, DIW DP 1604.

Mendelevitch, Holz, Hirschhausen, and Haftendorn (2016): A Model of the International Steam Coal Market (COALMOD-World), DIW Data Doc 85.

Richter, Jotzo, and Mendelevitch (2015): Market Power Rents and Climate Change Mitigation: A Rationale for Coal Taxes?, DIW DP 1471.